1. Introduction

Liquidity is one of the fundamental characteristics, which can describe a stock market. This notion is vastly discussed in the scientific literature, especially in terms of liquidity measurements (

Chang et al. 2018;

Xu et al. 2022), liquidity patterns (

Angerer et al. 2018;

Weigerding and Hanke 2018) or information efficiency determined by market liquidity (

Miloș et al. 2021). In the simplest terms, liquidity is understood as the time needed to exchange an asset for money (

Ranaldo 2001). The provision of liquidity through the viability of an order-driven market lies in the profitability of liquidity trading (

Biais et al. 1995;

Ranaldo 2001). The advancement of information technology allowed for real-time transactions and thus ensured greater liquidity. Consequently, it increased the market efficiency as investors were able to monitor stock prices on an ongoing basis, as well as make decisions as soon as they obtained new information (

Amihud and Mendelson 1987).

The digitization of trading in securities has increased the availability of data, and thus made it possible to detect certain relationships more accurately when trading (

Jin et al. 2019). One of the most important market features is the analysis of trading time in intraday financial studies (

Ranaldo 2001). The availability of intraday data allows for the exploration of the market microstructure (

Kholisoh and Hermawati 2011).

Anghel et al. (

2020) emphasized the value of studies concerning the understanding of intraday patterns in the developing markets. The Warsaw Stock Exchange (WSE) represents a stock market that is developing in terms of its participants, volume and available financial instruments (

Włosik 2017;

Kubiczek 2020). Furthermore, WSE is the biggest and one of the most emerging stock markets in Central and Eastern Europe (

Glavina 2015;

Będowska-Sójka and Kilber 2019;

Tuszkiewicz 2022). It is also a stock market of particular importance in the region (

Buszko et al. 2021). However, there is no study to date that would examine the issue of intraday patterns on the WSE and include potential COVID-19 impact (for another study concerning intraday patterns on WSE see

Będowska-Sójka 2013). This article partially fills this research gap by investigating intraday patterns in transactions in terms of their number, value (turnover) and time difference, as well as the price changes between transactions during the session on the main market of the WSE. Moreover, this study is of distinct value, due to an indication of the intraday pattern formation during the beginning of the COVID-19 pandemic. Moreover, the situation that occurred in the WSE during the first phase of the pandemic was of particular interest, because of the emergence of a vast number of companies from the gaming sector (

Tuszkiewicz 2022). Those enterprises, which were indexed on the WSE, recorded remarkable profits, which translated as a significant impact on the whole market (

Kubiczek and Derej 2021).

The paper aims to verify the existence of intraday liquidity patterns on the Warsaw Stock Exchange. Hence, the following research questions were raised: did the intraday liquidity patterns show a pattern of distribution? If so, how was the distribution formed? What could be the reason for this? How did the pandemic outbreak impact the intraday patterns?

The structure of this paper is as follows.

Section 2 presents the literature review on the multidimensional aspects of the stock markets’ liquidity, with particular emphasis on the intraday patterns and impact of COVID-19. In this section, the characteristics of the Warsaw Stock Exchange is also presented.

Section 3 includes a description of the methodology used in the research, i.e., the justification for the selection of the analysis period, measures and statistical tests used.

Section 4 introduces the research results. The article ends with the Discussion and Conclusion, which are developed in

Section 5 and

Section 6, respectively.

3. Methodology

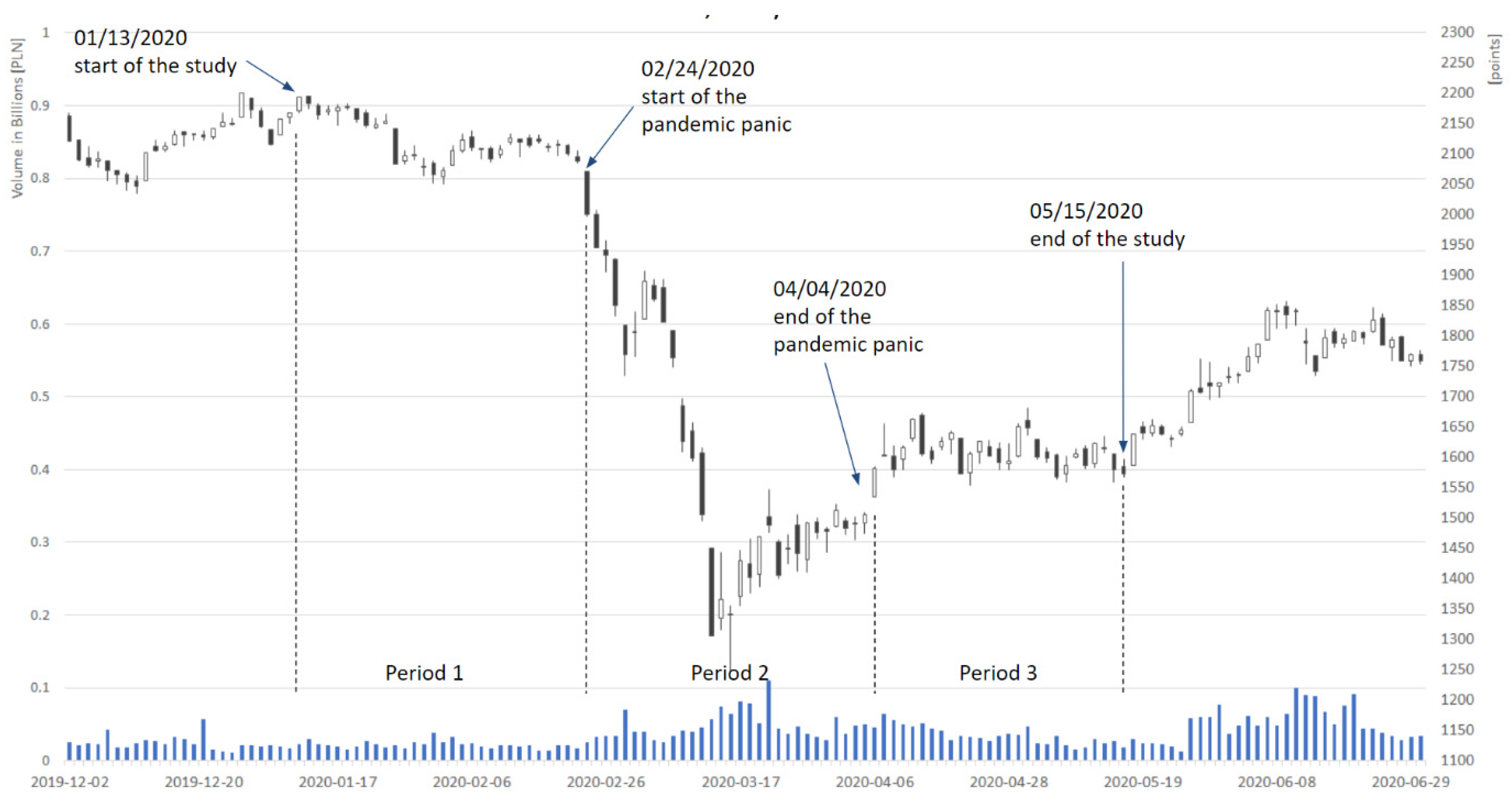

The analysis covers the period from 13 January 2020 to 15 May 2020. The choice of such an analysis period is due to the fact that although the first case of the coronavirus was recorded in China at the end of 2019, the outbreak of COVID-19 was still not acknowledged as a pandemic by the World Health

Organization (

2020) on 11 March 2020. Furthermore, these dates indicate the timeframes for the downturn caused by the COVID-19 pandemic in Poland (

Figure 1). On 24 February 2020, the decline in the WIG20 index amounted to 4.2%, which was 5.9 times the change from the average of the 250 sessions preceding that day. A strong downward trend started. It lasted until the session on 6 April 2020, when the WIG20 index increased by 4.9%, compared to the previous day, breaking the previous local maximum. Thus, the period of increased volatility and declines lasted for 6 weeks (see

Figure 1).

While the World Health Organization announced the COVID-19 pandemic on 11 March 2020, it is noted that investors began reacting fairly earlier, so the bear market was taken as a reference point. In order to maintain the comparability of the analyzed periods, an analogous period of 6 weeks was set, both before and after the first significant drops in the Warsaw Stock Exchange. The analyzed periods consist of the following intervals:

From 13 January 2020 to 21 February 2020 (Period 1);

From 24 February 2020 to 4 April 2020 (Period 2);

From 6 April 2020 to 15 May 2020 (Period 3).

The WSE is considered as an effective market because it is sufficiently liquid (

Stereńczak 2018). The subject of the present study is the transactions of the companies listed on the main market of the Warsaw Stock Exchange. Due to the non-market nature of block trades, they were excluded from the study. From among 424 companies noted on the WSE, companies in the single-price auction system, as well as IPOs and companies withdrawn from trading sometime within the study period, were excluded. As a result, 386 companies being in the continuous trading system throughout the whole study period were selected for the analyses.

The following data was collected and, at the very beginning, aggregated into minute data and weekly periods:

The number of transactions made;

The sum of the transaction volume;

Total turnover;

The sum of differences between transactions in seconds;

The sum of the percentage changes caused by transactions.

As a result, 18-week observations (for the above-mentioned periods) were obtained. Then, the values of the above data for the minute intervals in Periods 1, 2 and 3 were summed up. The following indices were also calculated for the minute data and individual periods:

The average time interval between transactions in seconds;

The average percentage change between transactions;

The average transaction value.

The last step was to eliminate the non-significant unit changes and additionally aggregate the data into five-minute intervals, in order to better illustrate the trends prevailing during the session.

On the basis of such a preliminary analysis (including

Figure 2,

Figure 3,

Figure 4 and

Figure 5), first conclusions were drawn, and then the number of transactions was statistically verified. The session time was divided into the first 5 min (F5, 9:00–9:05), the last 5 min (L5, 16:45–16:50) and the remaining session duration (CL, 9:05–16:45). To relativize CL, the values ere averaged based on the use of 5 min intervals (92 intervals).

For statistical verification, non-parametric tests for the paired samples were used, and the session time was taken as an influencing factor. The choice of this group of tests resulted from the lack of assumption of normal distribution and the insufficient number of observations (aggregated data in daily intervals). First, it was checked whether the analyzed values in the session time intervals were dissimilar; therefore, the hypothesis (Friedman’s rank test (

Friedman 1937)) verified that there was no difference between the analyzed values in the three considered session time intervals. If differences were found, a pairwise verification (Wilcoxon test (

Wilcoxon 1945)) was performed on the hypothesis that there was no divergence between the analyzed values in each pair of session time intervals. A Monte Carlo approach (10,000 replicates) was performed simultaneously. The results were interpreted for the three significance levels: 0.1, 0.05 and 0.01.

4. Results

Based on the analysis of the minute ranges, it can be observed that between 09:00:00 and 09:00:59, most of the transactions were made during the continuous trading phase (CT). The number of transactions in this period exceeds the average number of transactions in the entire continuous trading phase by 1055%, 1086% and 1191% for Periods 1, 2 and 3, respectively.

The value of the turnover made in the first minute of trading is higher than the average by 483.9% in Period 1, 764.35% in Period 2 and by 869.6% in Period 3.

Table 1 provides data on the share of the first minute and the first five minutes, in terms of the volume of trading throughout the CT phase. Moreover, the value of the turnover in the post-time phase and its share in the turnover during the entire session in the individual periods are presented.

The first minute accounted for 1.24% of the total turnover in the continuous trading phase in Period 1, while with each subsequent period this share grew up to 2.06%. On the other hand, the situation with overtime in trading throughout the session is noteworthy. In each subsequent period, this share decreased and the nominal value of turnover in Period 3 also fell in relation to Period 1.

The relation of transactions in individual session hours is slightly different.

Table 2 presents the share of transactions made in the first minute and in the first five minutes of the session in the number of transactions during the continuous trading phase. The number of transactions during the trading-at-last phase was also compared to the total number of transactions.

The number of transactions in the first minute accounted for 2.46% of the total number of transactions in the continuous trading phase in Period 1, and as much as 2.75% in Period 3. The dominance of overtime in this ranking is no longer visible, and the trend is decreasing. The difference between Periods 1, 2 and 3 equals to 1 pp. The next step in the study was the analysis of the changes in the average transaction value in individual periods, as shown in

Table 3.

An increasing average trade value can be observed in the first minute of the session, and a decreasing average in the extra time, especially between Periods 2 and 3. It is worth noting that there is a significant decrease in the average transaction value throughout the session between Periods 1 and 2.

Data from 5 min periods were used to present the course of the entire session. However, attention was focused on the continuous trading phase while ignoring the trading-at-last period. As indicated in

Table 1,

Table 2 and

Table 3, the trading-at-last period is a significant phase of the session in terms of the number of trades and their value. However, it is characterized by the fact that all trades are made at a predetermined price resulting from the pre-close market rebalancing phase, resulting in the percentage change between transactions always being equal to 0. Simultaneously, the time distance between the transactions is close to zero for most transactions, as the vast majority of them result from orders placed in the pre-close market balancing phase and is settled at 5:00 p.m., at the closing price.

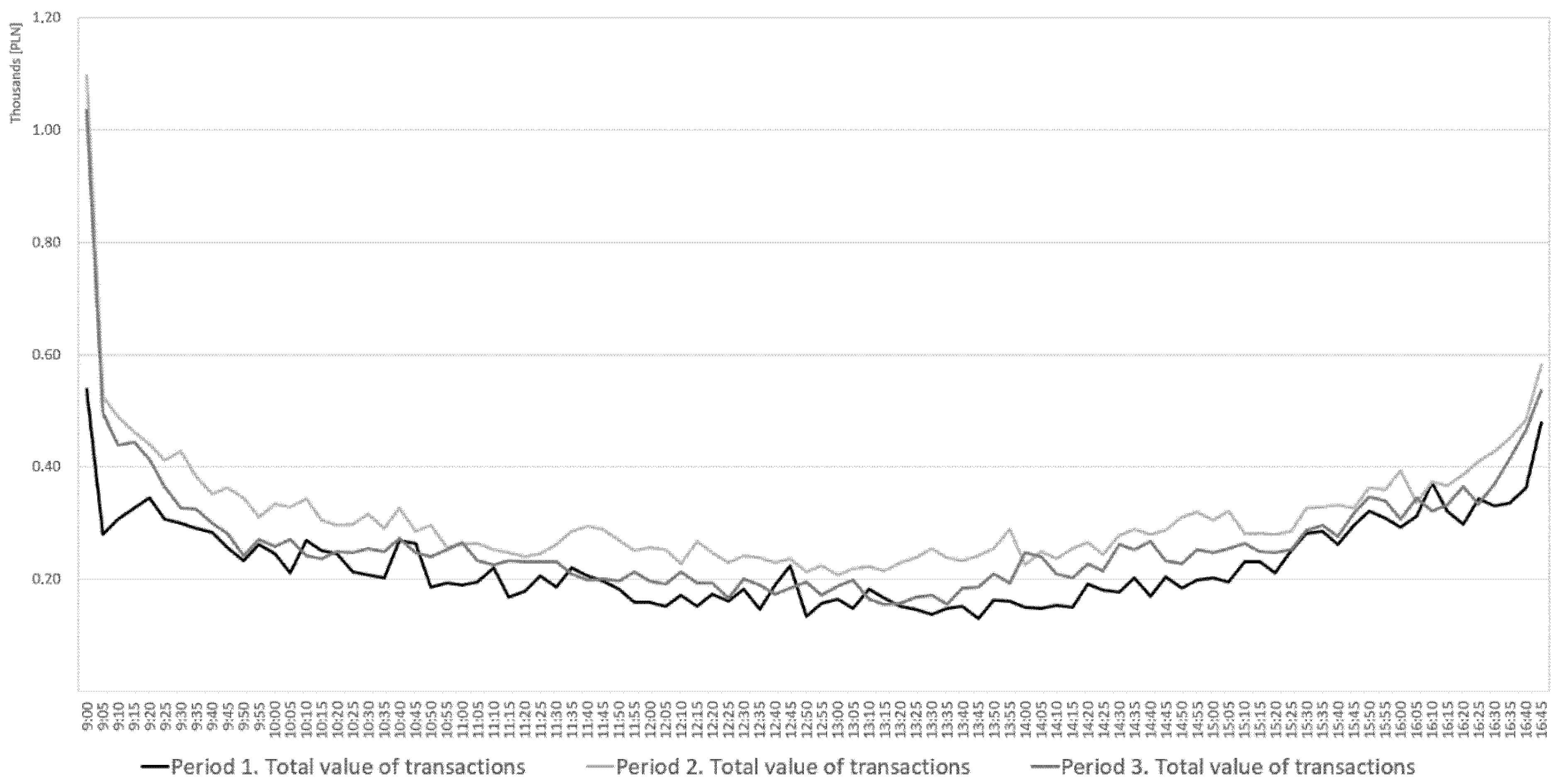

Figure 2 shows the transaction distribution of the trading value in the successive 5 min windows for Periods 1, 2 and 3.

Figure 2 confirms that a U-shaped distribution of the trading value exists during the session, regardless of the chosen period. In the crisis period (Period 2) and after the crisis (Period 3), the initial phase of the session (the first 20 min) was characterized by a much higher value of share turnover than in the pre-crisis period.

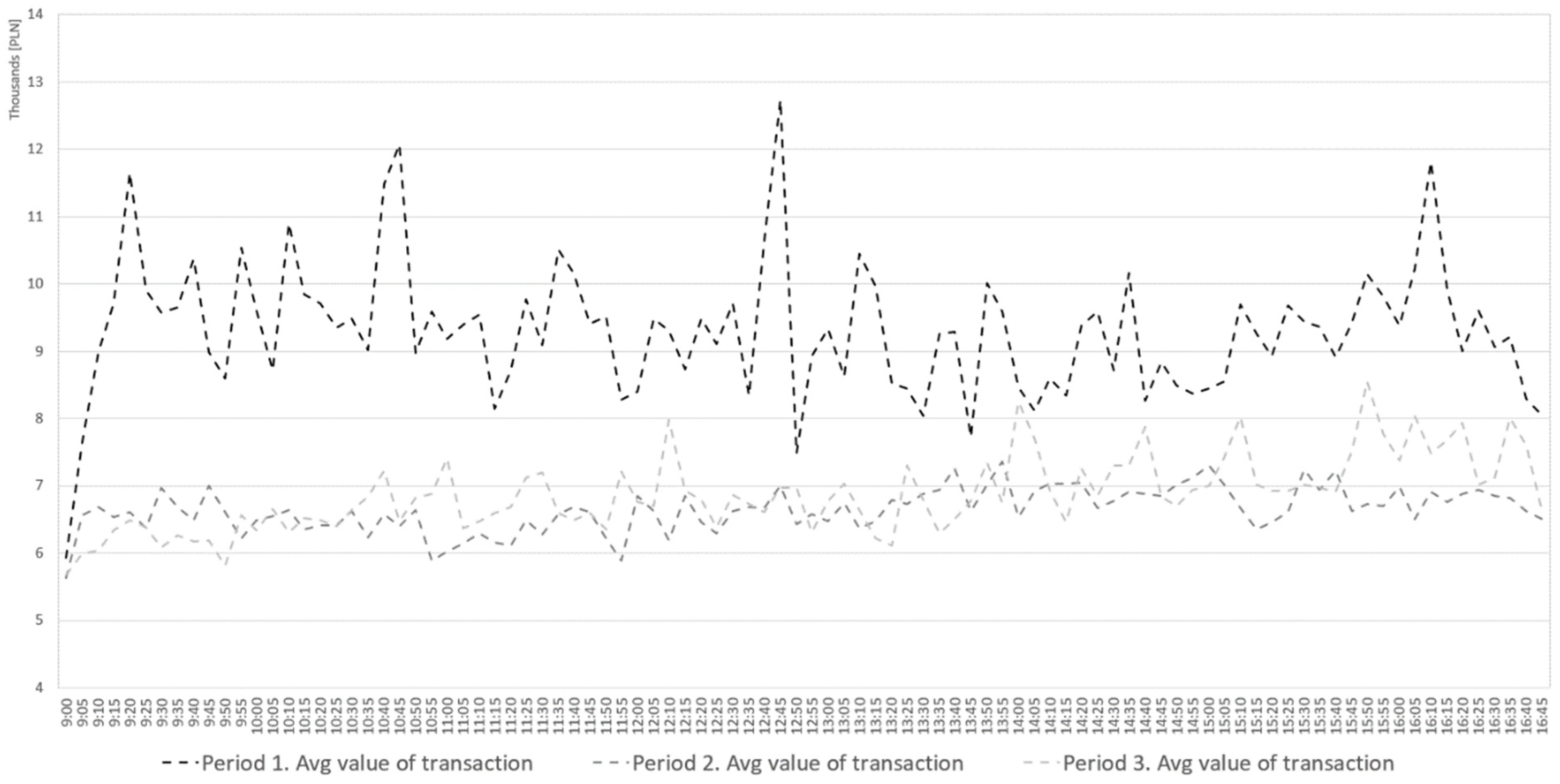

Figure 3 presents the average transaction value in the successive 5 min windows for Periods 1, 2 and 3.

The average transaction value in the initial phase of the session is similar in each analyzed period, while the following minutes and hours leave no doubt that the average transaction value in Period 1 is much higher than in Periods 2 and 3. It is worth noting how equal the average values of the trades are in Periods 2 and 3.

It suggests that in Period 2, which is crucial in this paper, some deviation occurs in the investor’s behavior. If compared with the average time between subsequent transactions, which is clearly higher in Period 1 and the lowest in Period 2, it can be concluded that the activity of investors with less capital increased in Period 2. In

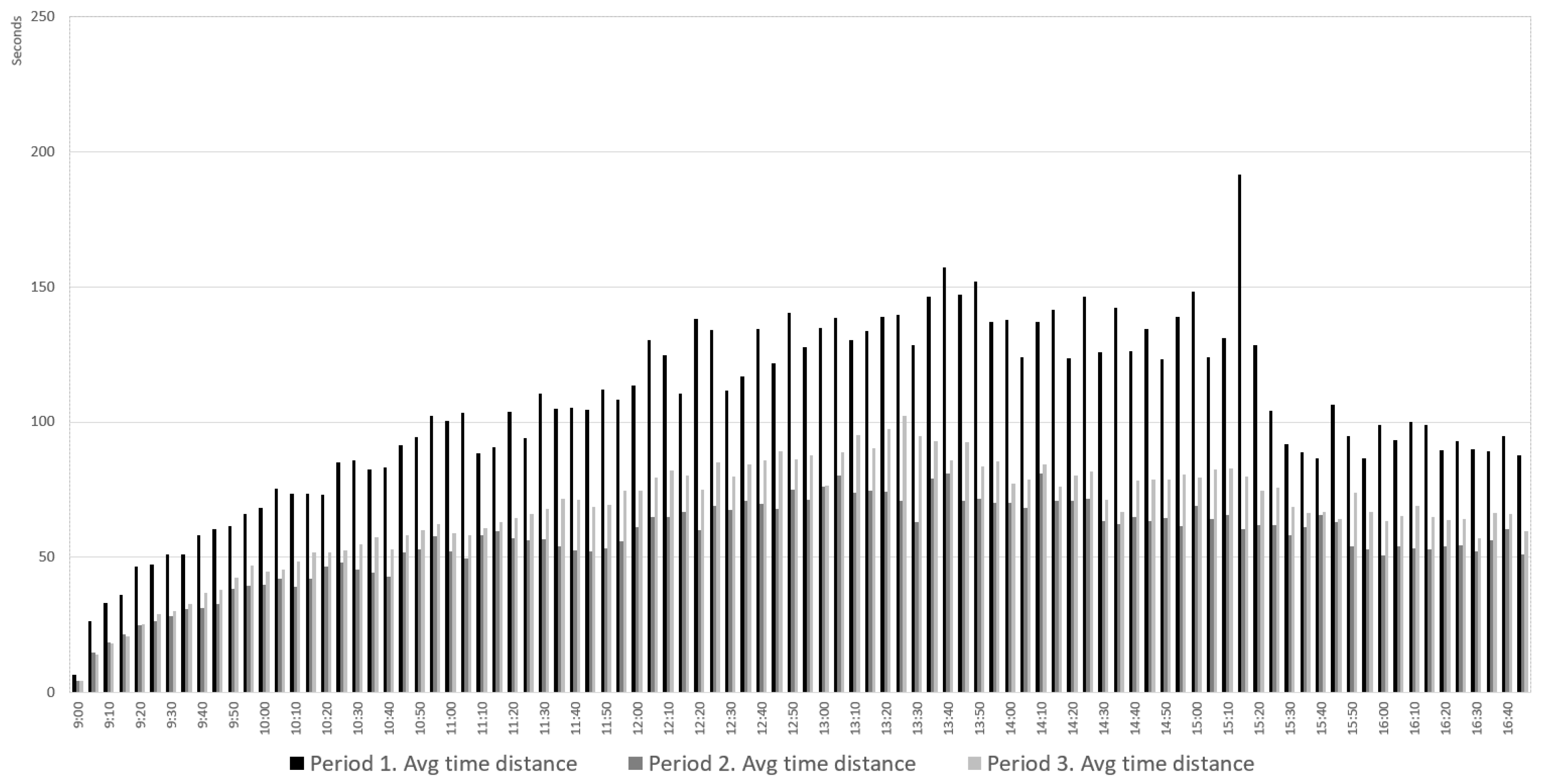

Figure 4, it can be seen that, in addition to the drop in average time distance in Period 2, Period 1 is distinguished by a significant decrease in the time interval between transactions from 3:30 p.m.

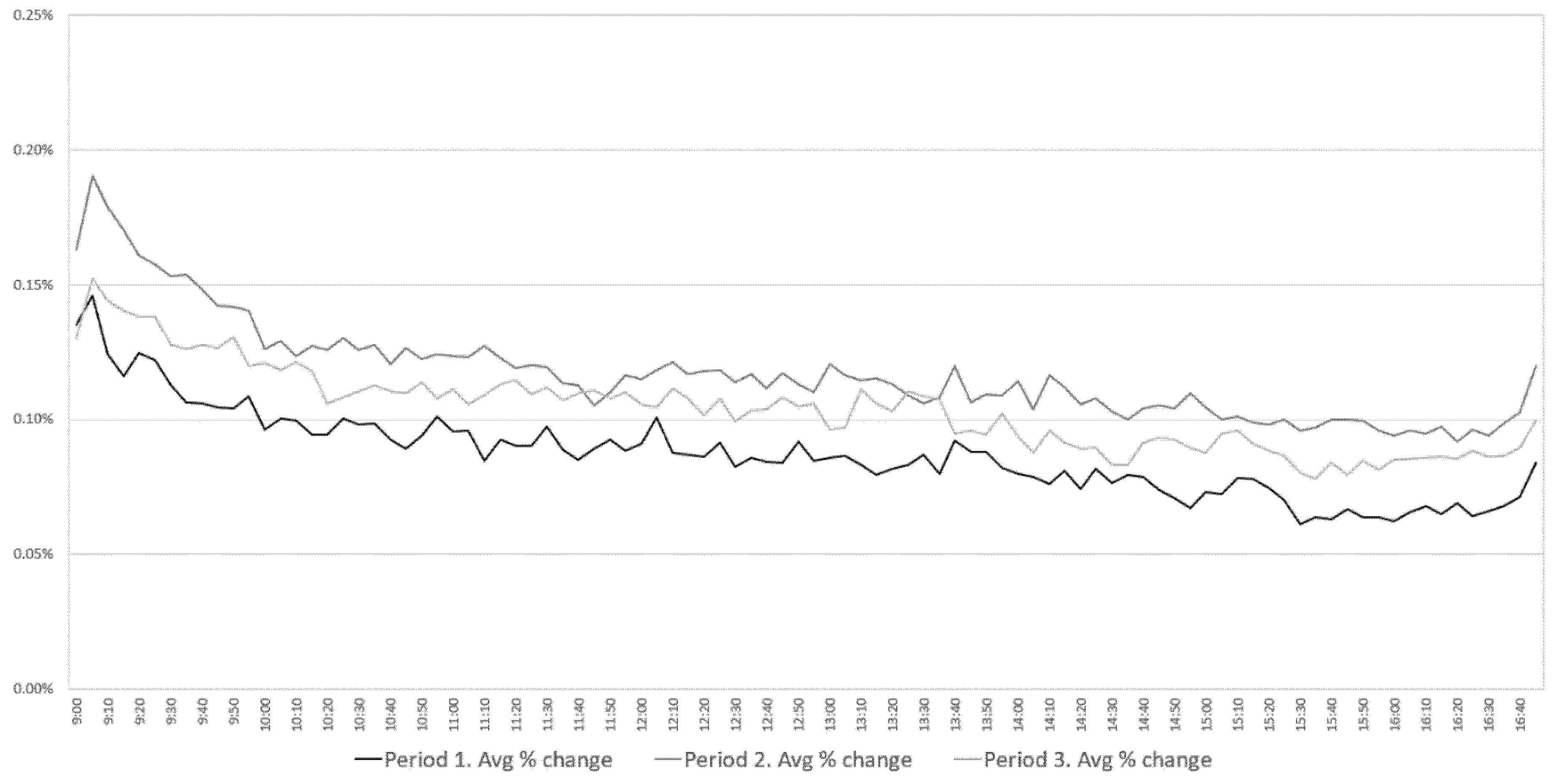

The average percentage distance between transactions shown in

Figure 4 increased in Period 2 by 36%, and remained higher in Period 3 than in Period 1 by 20.5%. This means that the realized spread between transactions increased during the COVID-19 crisis and remained higher after it was over. Its smallest value appears at 3:30 p.m. and this is related to the pattern observable in the time distance between the transactions ratio. Moreover, in the case of the distance between transactions, the minimum amount is observed at the same hour in each of the analyzed periods. It is worth noting that during the pandemic, the fact that the lowest distances between trades occurred by hours, the start of the session on stocks in the United States did not change.

Furthermore, the highest level of percent distance between transactions was observed at 9:05 a.m. Therefore, it can be assumed that after the first transactions are settled directly after the opening of the session, investors agreed to bear the higher cost of a transaction, if one was carried out.

The results show that the most active period during a session is its beginning. Then, the trades have the highest average value, time distance is the shortest and high volatility is observed. An explanation of this phenomenon can be found in the investors’ discounting of the information published between the closing of one session and the opening of another.

This behavior was observed throughout each period considered in this study. However, there are differences in behavior between periods in the later hours of the session. The significant decrease in the time distance between transactions observed in Period 1 at 3:30 p.m. was reduced in subsequent periods to insignificant in Periods 2 and 3. The overall liquidity in Period 2 was the highest, while in Period 3 it was higher than in Period 1.

Statistical Verification

The graphical representation of the formation of the liquidity patterns in the U-shape can be confirmed, assuming that at the beginning and at the end of the session the number of transactions is, on average, higher than it is during the remaining session time. The average number of transactions is presented in

Table 4.

The average number of transactions in the analyzed moments of the session in all of them is the highest in the first 5 min of the session (F5), then in the last 5 min of the session (L5) and the lowest in the remaining moments (CL). The Friedman’s rank test was used to verify the value of the number in a particular moment of the session. The results are presented in

Table 5.

At the significance level of 0.01, it should be argued that the number of transactions varies in at least one session period. It is worth noting that this is a conclusion for all the analyzed periods. The Wilcoxon test was used to verify between the two individual sessions, the results of which are presented in

Table 6.

When analyzing the liquidity patterns throughout the whole period, it should be stated that all pairwise differences in the number of transactions are significant at the level of 0.01, which confirms the presence of the U-shape of liquidity patterns. In Period 1 and Period 2, assuming a significance level of 0.05, the existence of a U-shaped relationship is also confirmed. However, in Period 3 a significance level of 0.1 should be adopted to confirm the occurrence of a U-shape in the liquidity patterns based on the average number of transactions. This indicates that there is a strong difference between F5 and CL and F5, however the difference between CL and F5 is decreasing and therefore the U shape is less visible but still exists.

5. Discussion

Knowing the distribution of liquidity during the session allows a trader to optimize their investment decisions. The best time to trade with high volume is in the first minutes of a session, followed by the hours 15:30 to 16:50. The period of the lowest liquidity is between 1.30 p.m. and 1.50 p.m. The hypothesis about the U-shape intraday pattern of liquidity, put forward by the conducted preliminary analysis, was confirmed by statistical verification based on the number of transactions in the first 5 min, the last 5 min and the remaining duration of the session. It is worth noting that these liquidity patterns were confirmed in all three analyzed periods.

Furthermore, regarding to observations made by

Madhavan (

1992), this study confirms that spreads, measured by the percentage changes between transactions, decrease during the day.

Madhavan (

1992) defines this phenomenon as the increasing reduction in the information asymmetry between dealers and traders. The results of the study are similar to those of the research of the depth and spread at the Stock Exchange of Hong Kong (

Ahn and Cheung 1999). Our findings prove that, regardless of the way the spread is interpreted (the difference between the best bid and asking prices or the difference in price between consecutive transactions), the liquidity patterns are analogous.

The decrease in the average interval between transactions around 3:30 p.m. in Period 1 is extremely unusual, as there are no regular cyclical events in Poland or Europe that could directly affect the liquidity of the WSE. Moreover, the detection of such behavior is a novelty because, in the results of a similar study on intraday patterns of the stock liquidity,

Będowska-Sójka (

2013) did not observe it. However, the explanation for this behavior can be found in the impact of stock exchanges in the United States, because this is when the session opens. An analogical decrease was also observed in Periods 2 and 3, but to a much lesser extent.

Another observation is the increase in the average percentage change between transactions in Periods 2 and 3 as compared to Period 1. This, in turn, can be associated with a decrease in liquidity on the stock exchange with the simultaneous improvement of all other parameters, i.e., transaction speed as well as their size and total number. This could be explained by the increased overall volatility in the market, especially since a decrease in the percentage change in Period 3 relative to Period 2 can be observed with a simultaneous increase in the intervals between transactions.

The findings of the study concerning the liquidity behavior of shares are similar to

Olbryś and Mursztyn (

2017) research, in which they analyzed the period of the previous financial crisis of 2007–2009. Therefore, it can be assumed that the behavior of retail investors trading on the Warsaw Stock Exchange during the crisis is similar, regardless of its duration and circumstances.

In-depth research could also confirm the observed increase in the percentage difference between transactions in Periods 2 and 3 in relation to Period 1. Thus, it could be determined whether it is characteristic of the stock market crash, as

Amihud et al. (

1990) claimed. Authors suggests that the key reason for the crash in 1987 was a lack of liquidity caused inter alia by the trading mechanism (

Amihud et al. 1990). Nevertheless, authors also highlighted that a few days before the biggest price decline, a lower liquidity level was observed.

6. Conclusions

The aim of this study was to verify if intraday liquidity patterns existed on the Warsaw Stock Exchange before, during and after the panic caused by the COVID-19 pandemic. The findings confirmed the existence of a U-shaped intraday distribution of transaction numbers, emphasizing the importance of the first and last minutes of the trading session. The COVID-19 pandemic dominated the WSE transactions—the average percentage change between transactions increased during the pandemic.

The value of the study is its universal character due to the use of simple liquidity measures. The conclusions of the research presented in the study concern the WSE, which is an order-driven exchange and, to a large extent, fill the identified research gap. It should be emphasized that this gap still exists as there is no extensive research of similar markets around the world. One of the reasons for this state of affairs is different models of the stock exchange, e.g., quote-driven, represented by American stock markets.

6.1. Practical Implications

The article provides knowledge on the frequency of transactions, and their volume allows for better planning, especially for large institutional investors. It should be noted that liquidity intraday patterns are identical even in periods of strong market turmoil, and thus it confirms their relevance and applicability in practice. In addition, as investors are aware of liquidity patterns, they reduce the cost of trades as they trade with a tighter spread (i.e., the difference between the ask and bid).

6.2. Limitations

The limitation of the study was its relatively short period of analysis. The adoption of such a short period in the analysis was caused by the fact that the financed markets’ crisis caused by COVID-19 was exceedingly short. This makes it puzzling to generalize the conclusions about the durability of the demonstrated distribution tendency.

6.3. Further Study

Further research may focus on examining the liquidity in specific sectors (stock indices) over the same period. Moreover, researchers can conduct similar studies by modifying the time intervals. It would also be worth considering the liquidity of other exchanges applying the methodology used in this study, adjusting it to the specificity of the analyzed market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}