Moderating Effects of Founders’ Role on the Influence of Internationalization on IPO Performance of Listed Companies in Thailand

Abstract

:1. Introduction

2. Literature Review

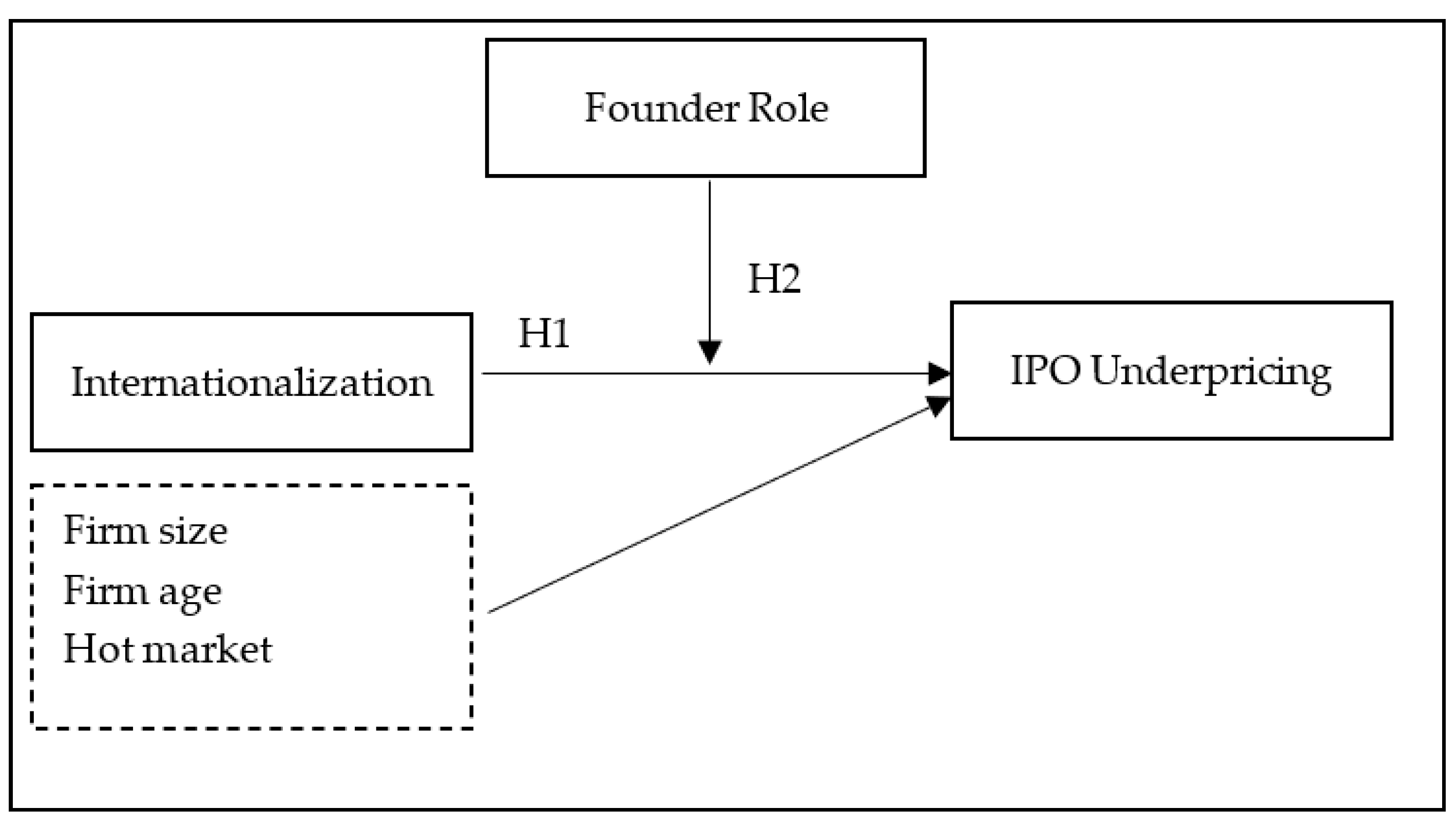

2.1. Internationalization and Underpricing

2.2. Moderating Effect of the Founders’ Role

3. Methodology

3.1. Sample and Data

3.2. Variable and Measurement

3.2.1. Underpricing

- UPi,t = the underpricing at the time of IPO for stock “i”

- Pi,0 = the IPO offer price of the stock “i”

- Pi,1 = the first-day closing price of the stock “i”

- Rmi,t = the market return of the corresponding stock exchange at the time of IPO “t” for stock “i”.

- MIi,0 = the closing price of the corresponding stock exchange index where stock “i” was listed at the offering day of the company

- MIi,t = the closing price of the corresponding stock exchange index where stock “i” was listed at the end of the first-day trading

3.2.2. Internationalization

3.2.3. Founders’ Role

3.2.4. Control Variables

3.3. Regression Model and Research Framework

4. Results

4.1. Descriptive Statistics and Correlation Matrix

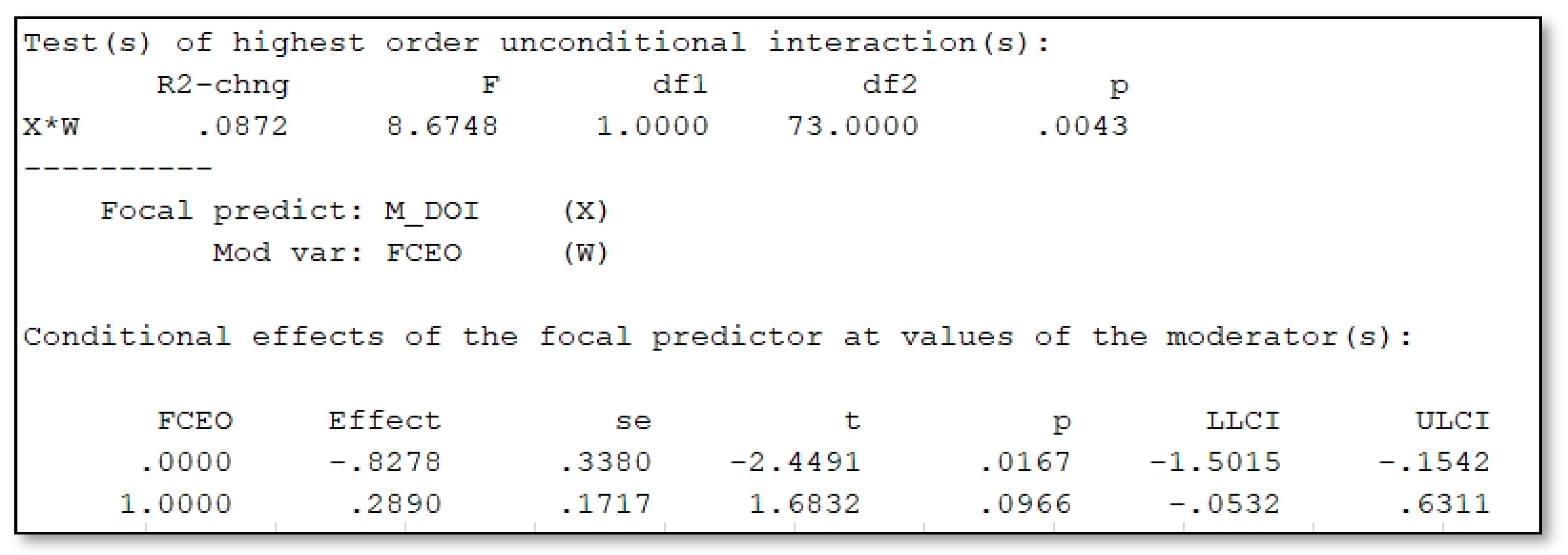

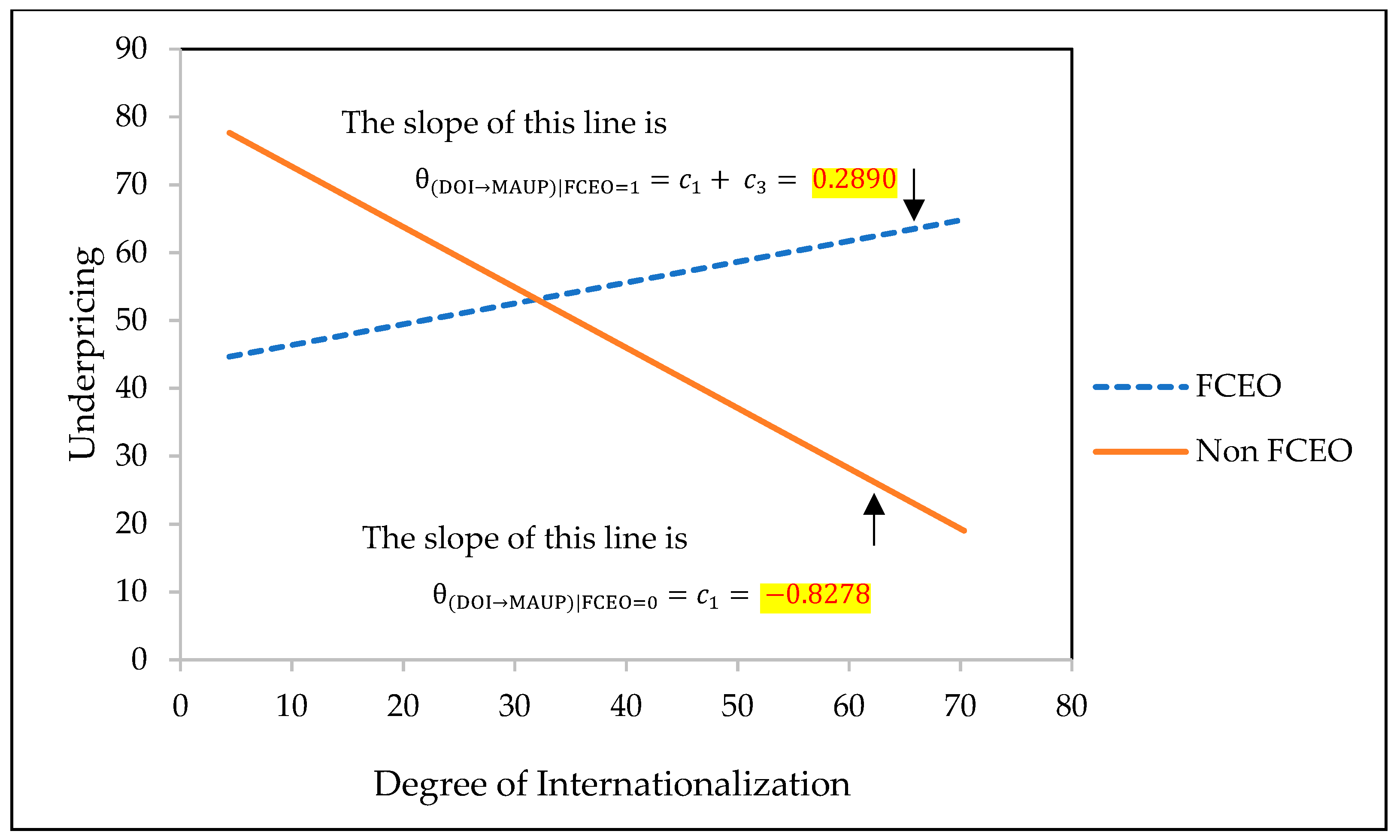

4.2. Regression Analysis Results

5. Discussion and Conclusions

6. Limitations and Recommendations for Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | Based on data available on Jay Ritter’s website: https://site.warrington.ufl.edu/ritter/ipo data/ [accessed 1 April 2018]. |

References

- Aiken, Leona S., Stephen G. West, and Raymond R. Reno. 1991. Multiple Regression: Testing and Interpreting Interactions. Sage: United States of America. [Google Scholar]

- Al-Shammari, Hussam A., W. Ross O’Brien, and Yousuf Hamed AlBusaidi. 2013. Firm internationalization and IPO firm performance: The moderating effects of firm ownership structure. International Journal of Commerce and Management 23: 242–61. [Google Scholar] [CrossRef]

- Arthurs, Jonathan D., Robert E. Hoskisson, Lowell W. Busenitz, and Richard A. Johnson. 2008. Managerial agents watching other agents: Multiple agency conflicts regarding underpricing in IPO firms. Academy of Management Journal 51: 277–94. [Google Scholar] [CrossRef]

- Baker, Malcolm, and Paul A. Gompers. 2003. The determinants of board structure at the initial public offering. The Journal of Law and Economics 46: 569–98. [Google Scholar] [CrossRef]

- Brau, James C., and Stanley E. Fawcett. 2006. Initial public offerings: An analysis of theory and practice. The Journal of Finance 61: 399–436. [Google Scholar] [CrossRef]

- Brealey, Richard, Hayne E. Leland, and David H. Pyle. 1977. Informational asymmetries, financial structure, and financial intermediation. The Journal of Finance 32: 371–87. [Google Scholar] [CrossRef]

- Capar, Nejat, and Masaaki Kotabe. 2003. The relationship between international diversification and performance in service firms. Journal of International Business Studies 34: 345–55. [Google Scholar] [CrossRef]

- Carter, Richard, and Steven Manaster. 1990. Initial public offerings and underwriter reputation. The Journal of Finance 45: 1045–67. [Google Scholar] [CrossRef]

- Certo, S. Trevis. 2003. Influencing initial public offering investors with prestige: Signaling with board structures. Academy of Management Review 28: 432–46. [Google Scholar] [CrossRef] [Green Version]

- Certo, S. Trevis, Catherine M. Daily, and Dan R. Dalton. 2001a. Signaling firm value through board structure: An investigation of initial public offerings. Entrepreneurship Theory and Practice 26: 33–50. [Google Scholar] [CrossRef]

- Certo, S. Trevis, Jeffrey G. Covin, Catherine M. Daily, and Dan R. Dalton. 2001b. Wealth and the effects of founder management among IPO-stage new ventures. Strategic Management Journal 22: 641–58. [Google Scholar] [CrossRef]

- Certo, S. Trevis, Catherine M. Daily, Albert A. Cannella Jr., and Dan R. Dalton. 2003. Giving money to get money: How CEO stock options and CEO equity enhance IPO valuations. Academy of Management Journal 46: 643–53. [Google Scholar]

- Certo, S. Trevis, Tim R. Holcomb, and R. Michael Holmes Jr. 2009. IPO research in management and entrepreneurship: Moving the agenda forward. Journal of Management 35: 1340–78. [Google Scholar] [CrossRef]

- Chemmanur, Thomas J. 1993. The pricing of initial public offerings: A dynamic model with information production. The Journal of Finance 48: 285–304. [Google Scholar] [CrossRef]

- Cheung, Yan-leung, Yunhao Dai, Zhiwei Ouyang, and Weiqiang Tan. 2018. Who leaves money on the table? The role of founder identity in Hong Kong. Applied Economics 50: 774–88. [Google Scholar] [CrossRef]

- Contractor, Farok J., Sumit K. Kundu, and Chin-Chun Hsu. 2003. A three-stage theory of international expansion: The link between multinationality and performance in the service sector. Journal of International Business Studies 34: 5–18. [Google Scholar] [CrossRef]

- Daily, Catherine M., and Dan R. Dalton. 1992. Financial performance of founder-managed versus professionally managed small corporations. Journal of Small Business Management 30: 25–34. [Google Scholar]

- Daily, Catherine M., S. Trevis Certo, Dan R. Dalton, and Rungpen Roengpitya. 2003. IPO Underpricing: A Meta–Analysis and Research Synthesis. Entrepreneurship Theory and Practice 27: 271–95. [Google Scholar]

- Gao, Ning, and Bharat A. Jain. 2011. Founder CEO management and the long-run investment performance of IPO firms. Journal of Banking & Finance 35: 1669–82. [Google Scholar]

- Gounopoulos, Dimitrios, and Hang Pham. 2017. Specialist CEOs and IPO survival. Journal of Corporate Finance 48: 217–43. [Google Scholar] [CrossRef] [Green Version]

- Hayes, Andrew F. 2012. PROCESS: A Versatile Computational tool for Observed Variable Mediation, Moderation, and Conditional Process Modeling. Lawrence: University of Kansas. [Google Scholar]

- Heeley, Michael B., Sharon F. Matusik, and Neelam Jain. 2007. Innovation, appropriability, and the underpricing of initial public offerings. Academy of Management Journal 50: 209–25. [Google Scholar] [CrossRef]

- Hsieh, Tsun-Jui, Yu-Ju Chen, and Hsueh-Chang Tsai. 2017. Business Group Internationalization, Family Control and IPO Underpricing. Managemant Review 36: 117–36. [Google Scholar]

- Hsu, Chin-Chun, and Arun Pereira. 2008. Internationalization and performance: The moderating effects of organizational learning. Omega 36: 188–205. [Google Scholar] [CrossRef]

- Hymer, Stephen Herbert. 1976. International Operations of National Firms. Cambridge: MIT Press. [Google Scholar]

- Jenkins, David G., and Pedro F. Quintana-Ascencio. 2020. A solution to minimum sample size for regressions. PLoS ONE 15: e0229345. [Google Scholar] [CrossRef] [Green Version]

- Komenkul, Kulabutr, and Dhanawat Siriwattanakul. 2016. How the unremunerated reserve requirement by the Bank of Thailand affects IPO underpricing and the long-run performance of IPOs. Journal of Financial Regulation and Compliance 24: 317–42. [Google Scholar] [CrossRef]

- Kongkaew, Tharitsaya, Supa Tongkong, and Sungworn Ngudgratoke. 2020. Factors Influencing Initial Returns of New Listed Companies: Evidence from Thailand. In 4th ICBTT2020. Kota Bharu: Global Academic Excellence(M) SDN BHD (125757-U), pp. 37–46. [Google Scholar]

- Kotlar, Josip, Andrea Signori, Alfredo De Massis, and Silvio Vismara. 2018. Financial wealth, socioemotional wealth, and IPO underpricing in family firms: A two-stage gamble model. Academy of Management Journal 61: 1073–99. [Google Scholar] [CrossRef] [Green Version]

- Lieberman, Mary G., and John D. Morris. 2014. The precise effect of multicollinearity on classification prediction. Multiple Linear Regression Viewpoints 40: 5–10. [Google Scholar]

- Lin, Wen-Ting, Yunshi Liu, and Kuei-Yang Cheng. 2011. The internationalization and performance of a firm: Moderating effect of a firm’s behavior. Journal of international Management 17: 83–95. [Google Scholar] [CrossRef]

- LiPuma, Joseph A. 2012. Internationalization and the IPO performance of new ventures. Journal of Business Research 65: 914–21. [Google Scholar] [CrossRef]

- Ljungqvist, Alexander. 2007. IPO underpricing. Handbook of Corporate Finance: Empirical Corporate Finance 1: 375–422. [Google Scholar]

- Loughran, Tim, and Jay R. Ritter. 2002. Why don’t issuers get upset about leaving money on the table in IPOs? The Review of Financial Studies 15: 413–44. [Google Scholar] [CrossRef]

- Loughran, Tim, and Jay R. Ritter. 2004. Why has IPO underpricing changed over time? Financial management, 5–37. [Google Scholar]

- Lowry, Michelle, Roni Michaely, and Ekaterina Volkova. 2017. Initial public offerings: A synthesis of the literature and directions for future research. Foundations and Trends® in Finance 11: 154–320. [Google Scholar] [CrossRef] [Green Version]

- McDougall, Patricia Phillips, and Benjamin M. Oviatt. 1996. New venture internationalization, strategic change, and performance: A follow-up study. Journal of Business Venturing 11: 23–40. [Google Scholar] [CrossRef]

- Mehmood, Waqas, Rasidah Mohd Rashid, and Ahmad Hakimi Tajuddin. 2020. A Review of IPO Underpricing: Evidences from Developed, Developing and Emerging Markets. Journal of Contemporary Issues Thought 11: 1–20. [Google Scholar]

- Mudambi, Ram, Susan M. Mudambi, Arif Khurshed, and Marc Goergen. 2012. Multinationality and the performance of IPOs. Applied Financial Economics 22: 763–76. [Google Scholar] [CrossRef]

- Nelson, Teresa. 2003. The persistence of founder influence: Management, ownership, and performance effects at initial public offering. Strategic Management Journal 24: 707–24. [Google Scholar] [CrossRef]

- Ozdemir, Ozgur, and Arun Upneja. 2016. The role of internationalization on the IPO performance of service firms: Examination of initial returns, long-run returns, and survivability. International Business Review 25: 997–1009. [Google Scholar] [CrossRef]

- Pangarkar, Nitin. 2008. Internationalization and performance of small-and medium-sized enterprises. Journal of World Business 43: 475–85. [Google Scholar] [CrossRef]

- Peng, Xuan, Yibo Jia, and Kam C. Chan. 2021. The impact of internationalization on IPO underpricing: A result of agency costs reduction, a certification effect, or a diversification benefit? Finance Research Letters, 102059. [Google Scholar] [CrossRef]

- Pour, Eilnaz Kashefi. 2015. IPO survival and CEOs’ decision-making power: The evidence of China. Research in International Business and Finance 33: 247–67. [Google Scholar] [CrossRef]

- Ritter, Jay R. 1984. The “hot issue” market of 1980. Journal of Business, 215–40. [Google Scholar] [CrossRef]

- Ritter, Jay R. 1987. The costs of going public. Journal of Financial Economics 19: 269–81. [Google Scholar] [CrossRef] [Green Version]

- Ritter, Jay R. 1998. Initial public offerings, Warren Gorham & Lamont handbook of modern finance. Contemporary Finance Digest 2: 5–30. [Google Scholar]

- Rock, Kevin. 1986. Why New Issues Are Underpriced. Journal of Financial Economics 15: 187. [Google Scholar] [CrossRef]

- Rugman, Alan M. 1979. International Diversification and the Multinational Enterprise. Lexington: Lexington Books/Fortress Academic. [Google Scholar]

- Stanton, Phillip, and Patricia Stanton. 2011. The concept of internationalization and its relevance to small and medium service enterprises (SMSEs). The Business Review, Cambridge 17: 28–34. [Google Scholar]

- Stoughton, Neal M., and Josef Zechner. 1998. IPO-mechanisms, monitoring and ownership structure. Journal of Financial Economics 49: 45–77. [Google Scholar] [CrossRef]

- Sullivan, Daniel. 1994. Measuring the Degree of Internationalization of a Firm. Journal of International Business Studies 25: 325–42. [Google Scholar] [CrossRef]

- Vernon, Raymond. 1971. Sovereignty at bay: The multinational spread of US enterprises. The International Executive 13: 1–3. [Google Scholar] [CrossRef]

- Welch, Ivo. 1989. Seasoned offerings, imitation costs, and the underpricing of initial public offerings. The Journal of Finance 44: 421–49. [Google Scholar] [CrossRef]

- Xiao, Simon Shufeng, Insik Jeong, Jon Jungbien Moon, Chris Changwha Chung, and Jaiho Chung. 2013. Internationalization and performance of firms in China: Moderating effects of governance structure and the degree of centralized control. Journal of International Management 19: 118–37. [Google Scholar] [CrossRef]

- Zahra, Shaker A., R. Duane Ireland, and Michael A. Hitt. 2000. International expansion by new venture firms: International diversity, mode of market entry, technological learning, and performance. Academy of Management Journal 43: 925–50. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Study | Country | Period | Sample | Independent Variable | Moderator Variable(s) | IPO Performance Measure | Theory | |

|---|---|---|---|---|---|---|---|---|

| Signaling | Agency | |||||||

| Effect of internationalization on IPO performance | ||||||||

| LiPuma (2012) | US | 1997–2003 | 184 | FSTS | ST-Pre-money (−) | ↑/↓ | ||

| Ozdemir and Upneja (2016) | US | 1980–2009 | 1822 | International/Domestic (dichotomous) | ST-UP (−) LT-CAR (+), BAH (+) | ↓ ↑ ↑ | ||

| Peng et al. (2021) | China | 2003–2016 | 891 | FSTS | ST-UP | ↓ | ||

| Effect of governance on IPO performance | ||||||||

| Certo et al. (2001a) | US | 1990–1998 | 748 | Outside directors Board reputation | ST-UP (+) ST-UP (−) | ↓ ↓ | ||

| Gao and Jain (2011) | US | 1997–2000 | 1963 | Founder CEO | High/Low technology | LT- BAH (+) | ↑ | ↑ |

| Effect of internationalization (proxy is FSTS) and governance on IPO performance | ||||||||

| Al-Shammari et al. (2013) | US | 1997, 1998, 2001 and 2002 | 1084 | FSTS | Block holder CEO ownership | ST-UP (+/−) ST-UP (+) | ↑ ↑ | ↑ ↑ |

| Hsieh et al. (2017) | Taiwan | 2001–2010 | 109 | FSTS | Family/Non-controlled business groups | ST-UP (+/+) | ↑ | |

| Business group owner ship | ST-UP (−/−) | ↓ | ||||||

| Year | N | Mean (%) | Standard Deviation | Maximum | Minimum | Market Returns (%) |

|---|---|---|---|---|---|---|

| 2013 | 28 | 57.55 | 68.64 | 200.00 | −29.33 | −7.73 |

| 2014 | 36 | 83.26 | 71.20 | 200.00 | −25.47 | 21.69 |

| 2015 | 33 | 51.66 | 59.49 | 200.00 | −12.84 | −13.16 |

| 2016 | 23 | 57.95 | 48.57 | 200.00 | 7.00 | 22.13 |

| 2017 | 38 | 27.45 | 32.60 | 151.09 | −10.26 | 12.16 |

| 2018 | 18 | 11.15 | 26.98 | 71.58 | −21.33 | −12.07 |

| 2019 | 28 | 2.47 | 17.07 | 47.06 | −30.07 | 0.89 |

| 2020 | 16 | 53.46 | 71.31 | 200.00 | −3.68 | −15.63 |

| Total | 220 | 44.61 | 58.60 | 200.00 | −30.07 | 1.03 |

| Variables | Abbreviations | Definitions |

|---|---|---|

| Dependent variable Underpricing | MAUP | The market adjusted underpricing |

| Independent variable - Degree of internationalization | DOI | The percentage of foreign sales of total sales |

| Moderator variable - Founders’ role | FCEO | Code 1 for a founder CEO, 0 for a non-founder CEO |

| Control Variables - Firm size | FSIZE | The company total asset in the year of IPO |

| - Firm age | AGE | The difference between firm’s founding year and its IPO year |

| - Hot market | HOT | Code 1 if the IPO was issued in 2014, Code 0 if the IPO was issued in other years |

| Issue Year | Number | Average of MAUP (%) | Offer Size (Million Baht) | Money Left on the Table (Million Baht) |

|---|---|---|---|---|

| 2013 | 12 | 62.12 | 14,549.78 | 3173.27 |

| 2014 | 18 | 79.89 | 22,455.70 | 8288.40 |

| 2015 | 15 | 57.74 | 11,047.57 | 5420.23 |

| 2016 | 11 | 50.75 | 26,426.95 | 8014.37 |

| 2017 | 15 | 41.75 | 35,331.16 | 10,167.98 |

| 2018 | 3 | 11.96 | 14,374.93 | 1081.10 |

| 2019 | 4 | 13.92 | 3324.00 | 720.86 |

| 2020 | 2 | 53.92 | 16,238.92 | 12,037.57 |

| Total | 80 | 55.31 | 143,749.01 | 48,903.77 |

| Industries | Overall Number | Average of MAUP (%) | Average of DOI (%) |

|---|---|---|---|

| Panel A: Overall sample | |||

| Agribusiness & Food | 15 | 31.98 | 33.05 |

| Consumer Products | 7 | 77.75 | 61.13 |

| Industrials | 13 | 62.22 | 31.50 |

| Property & Construction | 11 | 50.22 | 49.02 |

| Resources | 10 | 34.11 | 14.38 |

| Services | 19 | 72.91 | 45.44 |

| Technology | 5 | 62.62 | 21.78 |

| Total | 80 | 53.49 | 37.36 |

| Panel B: Founder CEO | |||

| Agribusiness & Food | 13 | 32.20 | 37.51 |

| Consumer Products | 7 | 44.63 | 61.13 |

| Industrials | 10 | 59.50 | 33.16 |

| Property & Construction | 8 | 50.24 | 43.89 |

| Resources | 4 | 5.13 | 7.76 |

| Services | 15 | 58.56 | 46.80 |

| Technology | 4 | 26.74 | 21.33 |

| Total | 61 | 49.24 | 39.62 |

| Panel C: Non-Founder CEO | |||

| Agribusiness & Food | 2 | 14.35 | 4.05 |

| Consumer Products | - | - | - |

| Industrials | 3 | 68.80 | 25.97 |

| Property & Construction | 3 | 56.62 | 62.69 |

| Resources | 6 | 48.61 | 18.79 |

| Services | 4 | 81.81 | 40.35 |

| Technology | 1 | 37.13 | 23.59 |

| Total | 19 | 55.84 | 30.09 |

| Variables | Frequency | Mean | SD | FSIZE | AGE | HOT | DOI | FCEO | UP |

|---|---|---|---|---|---|---|---|---|---|

| HOT | 18 | ||||||||

| FCEO | 61 | ||||||||

| FSIZE | 4248.93 | 10,031.55 | 1.000 | ||||||

| AGE | 19.60 | 12.00 | 0.154 | 1.000 | |||||

| DOI | 37.36 | 32.96 | −0.148 | −0.001 | −0.011 | 1.000 | |||

| MAUP | 55.31 | 54.09 | −0.224 ** | −0.286 *** | 0.285 ** | 0.059 | −0.006 | 1.000 |

| Model 1 | Model 2 | Model 3 | Model 4 | |

|---|---|---|---|---|

| Control Variables | ||||

| FSIZE | −0.0009 | −0.0009 | −0.0009 | −0.0009 * |

| (−1.5894) | (−1.5087) | (−1.4964) | (−1.7532) | |

| AGE | −1.0598 ** | −1.0633 ** | −1.0648 | −0.8965 ** |

| (−2.2252) | (−2.2193) | (2.1935) | (−2.1168) | |

| HOT | 31.8945 ** | 31.9989 ** | 31.9880 ** | 22.9312 ** |

| (2.3651) | (2.3587) | (2.3411) | (1.9899) | |

| Main effects | ||||

| DOI | 0.0618 | 0.0612 | −0.8278 ** | |

| (0.3557) | (0.3476) | (−2.4491) | ||

| FCEO | 0.3705 | 7.6433 | ||

| (0.0275) | (0.6428) | |||

| Interaction | ||||

| DOI × FCEO | 1.1168 *** | |||

| (2.9453) | ||||

| Intercept | 72.7454 | 70.3520 | 70.1199 | 61.9295 |

| R square | 0.1757 | 0.1771 | 0.1792 | 0.2664 |

| Adjusted R Square | 0.1432 | 0.1332 | 0.1215 | 0.1999 |

| R Square change | 0.1757 | 0.0014 | 0.0000 | 0.0872 |

| VIF | 1.01–1.03 | 1.02–1.05 | 1.02–1.05 | 1.04–5.06 |

| F | 5.3998 *** | 4.0350 *** | 3.1851 *** | 4.4192 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kongkaew, T.; Tongkong, S.; Ngudgratoke, S. Moderating Effects of Founders’ Role on the Influence of Internationalization on IPO Performance of Listed Companies in Thailand. Int. J. Financial Stud. 2021, 9, 37. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs9030037

Kongkaew T, Tongkong S, Ngudgratoke S. Moderating Effects of Founders’ Role on the Influence of Internationalization on IPO Performance of Listed Companies in Thailand. International Journal of Financial Studies. 2021; 9(3):37. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs9030037

Chicago/Turabian StyleKongkaew, Tharitsaya, Supa Tongkong, and Sungworn Ngudgratoke. 2021. "Moderating Effects of Founders’ Role on the Influence of Internationalization on IPO Performance of Listed Companies in Thailand" International Journal of Financial Studies 9, no. 3: 37. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs9030037