1. Introduction

Economic policy uncertainty (EPU) is termed an independent nature of risk associated with the financial system of countries due to the undefined pathways of fiscal, monetary, and other regulatory policies (

Baker et al. 2016). Security-specific risk is often easier to diversify than systematic risks, such as EPU. Financial integration and global trade wars among countries have increased economic policy uncertainty (

Al-Thaqeb and Algharabali 2019;

Wang et al. 2019a). Moreover, the current COVID-19 crisis continues to raise economic policy uncertainty in the United States, and appears to be a more catastrophic event than the global financial crisis and European debt crisis (

Baker et al. 2020). Interestingly, the COVID-19 crisis damaged the financial market far more than any other pandemic in the past, including the Spanish flu. Higher economic policy uncertainty curbs the flow of investment (

Bernanke 1983;

Kido 2016), and investors (regardless of type; institutional or individual) always look to eliminate the risk associated with their investment. Therefore, the current financial and economic crisis due to COVID-19 remains a heated topic among scholars and policymakers around the world (

Abdelrhim et al. 2020).

Previously, researchers have investigated the hedging ability of financial assets such as cryptocurrency commodities and international stocks against inflation, EPU (

Cheng and Yen 2019;

Yen and Cheng 2020), global EPU (

Al Mamun et al. 2020;

Shaikh 2020;

Su et al. 2020), and VIX (

Bouri et al. 2017a;

Kalyvas et al. 2020;

Wang et al. 2019b). Very few studies have examined green bonds, such as the correlation patterns of green bonds and conventional bonds (

Nguyen et al. 2020), green bonds and black bonds (

Broadstock and Cheng 2019), pricing spillover from green bonds and financial markets (

Reboredo 2018;

Saeed et al. 2020a,

2020b), and the yield spread of US green and conventional municipal bonds and the impact of green bonds market liquidity on the green bonds yield (

Karpf and Mandel 2018). However, the investigation of the hedging and safe haven properties of green bonds against economic policy uncertainty has been previously ignored, as the emerging green bonds market requires further econometric investigation and more empirical evidence. Moreover, the linkage of environmentally friendly securities and macroeconomic variables can serve as a novel line of inquiry (

Broadstock and Cheng 2019). Due to the worldwide impact, the literature on the risk management strand has started to grow quickly. The correlation between financial and non-financial firms has experienced a surge, and increased the optimal hedge ratio to a higher hedging cost during the COVID-19 (

Akhtaruzzaman et al. 2021a). During the COVID-19 period, the oil industry received higher benefits while the financial industry and oil consumers reacted negatively during oil price shocks (

Akhtaruzzaman et al. 2020). Interestingly, (

Akhtaruzzaman et al. 2021b) investigated the safe haven properties of gold in multiple phases during the COVID-19; they found a mixture of risk mitigation patterns, as gold proved a safe haven during the first phase and lost in the second phase.

Previous literature is limited to discussing the risk management role of gold (

Akhtaruzzaman et al. 2021b;

Paule-Vianez et al. 2020;

Qin et al. 2020;

Wu et al. 2019), cryptocurrencies (

Baur and Hoang 2020;

Dwita Mariana et al. 2020;

Haq and Aftab, forthcoming;

Paule-Vianez et al. 2020;

Qin et al. 2020;

Wu et al. 2019) against economic policy uncertainty. Therefore, this research has two main purposes. The primary purpose of this paper is to explore sustainable risk management avenues (green bonds, clean energy stocks, and rare earth elements) against the economic policy uncertainty of the USA, China, and the United Kingdom. Moreover, the secondary purpose is to investigate the diversification properties between green bonds, clean energy stocks, and rare earth elements. This research is conducted to answer the question of how green bonds, clean energy stocks, and rare earth elements are correlated with economic policy uncertainty and each other over time.

Green bonds offer potential pathways for risk management and diversification as they fulfill both needs for investors, such as environmental protection and financial resources (

Huynh et al. 2020). Green bonds can improve the overall performance of the environment and provide returns to investors (

Flammer 2019;

Maltais and Nykvist 2020). Recently, stock exchanges have introduced specific green bonds segments; moreover, since its inception in 2007, the green bonds market has been growing in size and significance for institutions and individual investors (

Febi et al. 2018;

Reboredo and Ugolini 2020;

Tang and Zhang 2020). Therefore, this may help green bonds become a sustainable and well-established investment instrument (

Maltais and Nykvist 2020). Green bonds are better performing financial instruments than conventional bonds (

Kanamura 2020), and their correlation is sensitive to changes in economic policy uncertainty (

Broadstock and Cheng 2019).

Rare earth elements (REEs) have become attractive due to their progressive mining, production, and recycling activities in recent years. REEs were discovered in 1788 and, until the 1950s, the worldwide production of RREs and their utilization rate was less than 5 thousand metric tons (

Zhou et al. 2017), even if the REEs were scarcely used in our everyday lives (

Klinger and Svensson 2015). According to

Zhou et al. (

2017), the worldwide consumption rate for REEs has increased rapidly as rare earth elements (REEs) have certain electromagnetic and conductive properties, and these properties are salient features in a broad range of applications, i.e., wind turbines, photovoltaic cells, aircraft engines, mobile phones, electric vehicle batteries, LEDs, drill bits for oil, natural gas mining, and many others. Based on these properties, in the 21st century, the usage of rare earth elements escalated due to the transformation of traditional industries into the manufacturing of highly technological products (

Li et al. 2019;

Wang et al. 2015).

This paper contributes to the related literature in at least three ways. First, it is the first attempt to capture the dynamic conditional co-movements between green bonds and economic policy uncertainty. Overall, green bonds show negative correlation patterns with EPUs. Second, this study tests the hedging role of green bonds against the economic policy uncertainty of China, the UK, and the USA, and the diversification properties of green bonds against clean energy stocks and global rare earth elements. Third, despite the hedging and diversification role of green bonds, this study also uncovers the safe haven role of green bonds under the shadow of COVID-19. This work adds a novel addition to the safe haven literature, as it is the first to consider the safe haven role of green bonds, clean energy stocks, and rare earth elements against the economic policy uncertainty of China, the UK, and the USA, which adds to a recent study by (

Bouri et al. 2021). Additionally, these findings provide support in the shadow of modern portfolio or portfolio diversification theory

1. Hedging and diversification properties support the portfolio theory and offer some new insight and avenues regarding risk mitigation in green finance.

The empirical results demonstrate dynamic conditional correlations among US green bonds, US clean energy stocks, global rare earth elements, and EPUs (USA, China, and UK). Firstly, green bonds demonstrated a positive correlation with US EPU, however a negative correlation with China EPU and UK EPU indexes in full sample estimation, implying that they play a hedging role against the economic policy uncertainty of China and the UK, but not the USA. This is due to the fact that the volatility of green bonds may prone to economic policy uncertainty of the USA, therefore green bonds were not proven as a hedge. Moreover, clean energy stocks proved a strong hedge against the economic policy risk, however a weak hedge against China EPU. Thirdly, the index of global rare earth elements proved a strong hedge against the economic policy uncertainty of China and the UK. However, a positive association between US-EPU and global rare earth elements implies that US EPU may prone to the volatility of global rare earth elements due to the monopolistic control of China over rare earth elements. Therefore, it removes the hedging ability of global rare earth elements against US EPU. A positive, but not perfectly positive correlation between green bonds, clean energy stocks, and rare earth elements suggests that these can be used as diversifiers with one another. The financial assets also demonstrated similar correlation patterns during the COVID-19 pandemic. Moreover, green bonds and clean energy stocks were confirmed as a strong safe haven against the US and UK economic policy uncertainty, however not against China EPU. Afterward, rare earth elements proved a strong safe haven against all EPU indexes. These findings suggest a road map to the fund managers for policy risk mitigation. Additionally, the results guide policymakers, regulators, and all market participants to develop strategies to cope with independent economic policy risk in the USA, China, and the UK.

The remainder of the paper is organized as follows.

Section 2 describes the data description and methods.

Section 3 presents the analysis and results.

Section 4 conducts a robustness check during COVID-19.

Section 5 debates the discussion, while

Section 6 concludes the paper.

3. Empirical Results

The analysis part is divided into two samples: full sample estimation and COVID-19 analysis.

Table 1 illustrates the descriptive statistics for each index based on daily values. The descriptive statistics are based on the daily logarithm values of all indices. Values in bold indicate significant coefficients at the 5% level. The mean and standard deviation coefficients for EPU reflect the stability of economic policy uncertainty in China; however, economic policy uncertainty is more volatile in the cases of the USA and UK. Countries with high EPU are more volatile, such as the US and UK. Green bonds are less volatile than clean energy stocks and global rare earth elements. This may be due to the sustainability and environmentally friendly perspective attached to green bonds. Moreover, green bonds are often considered long-term investments; thus, investors often buy and hold securities.

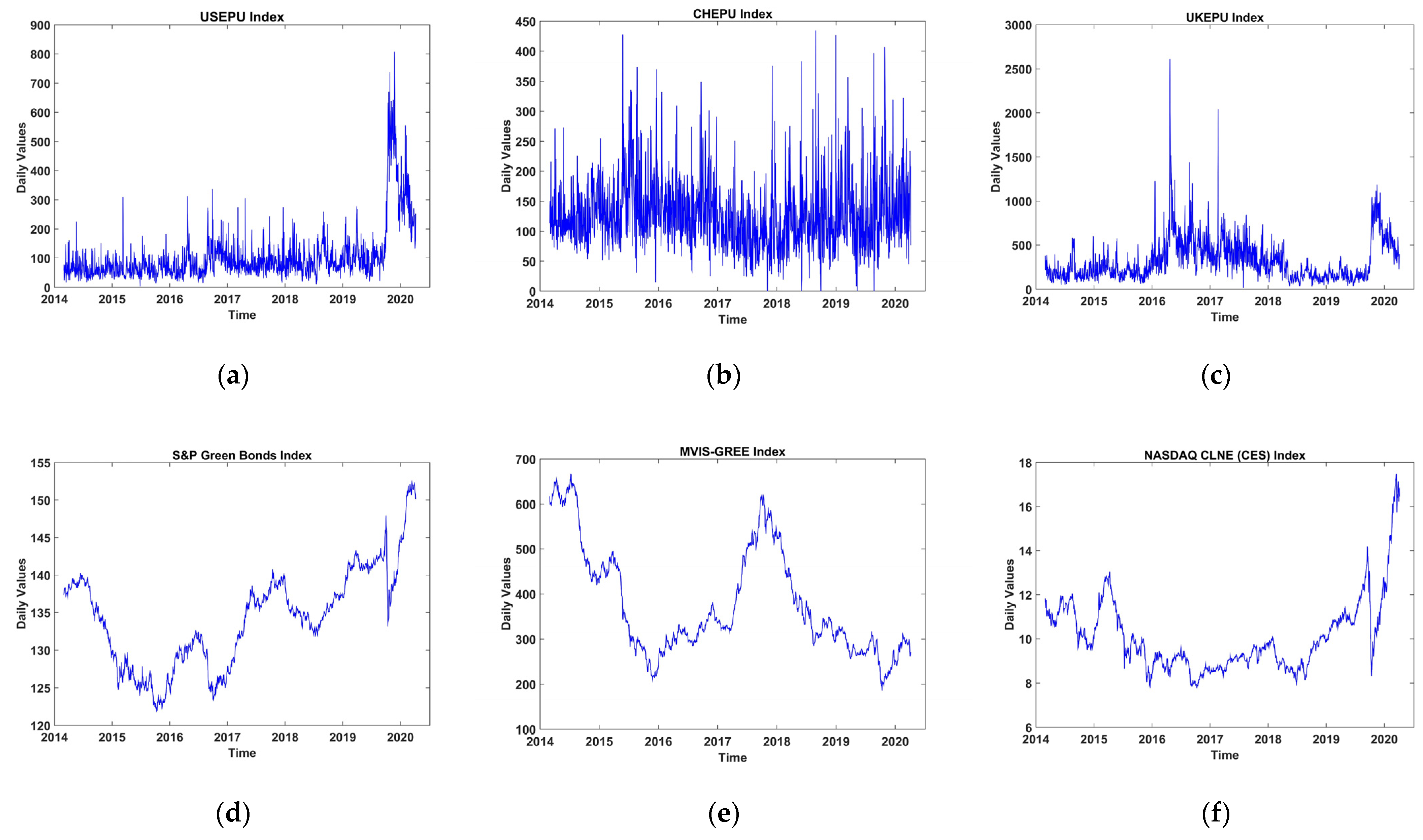

Figure 1 demonstrated an increase in economic policy uncertainty of the USA and UK during the COVID-19, whereas this is not true in case of China EPU. Moreover, green bonds index and global rare earth element index showed a surge. All coefficients and

p-values for the Jarque–Bera test confirmed that all series are non-normally distributed, thus violating normality.

The presence of serial correlation in financial time series is one of the critical issues. Serial correlation reflects the correlation of a time series with itself over multiple lagged periods; moreover, a serially correlated time series may not be a random walk.

Table 2 illustrates the outputs for the Portmanteau (Q) test for serial correlation up to the 40th order. Bold values in parentheses depict the

p-values at the 5% level. The Q statistic and

p-values supported the alternative hypothesis and rejected the null hypothesis of no serial correlation in EPUs, clean energy stocks, green bonds, and global rare earth elements. Thus, current estimates lead to choosing the DCC-MGARCH model to capture time-varying volatility in a time series, as the authors find GARCH (1,1) to be the best suitable model based on the Akaike information criterion.

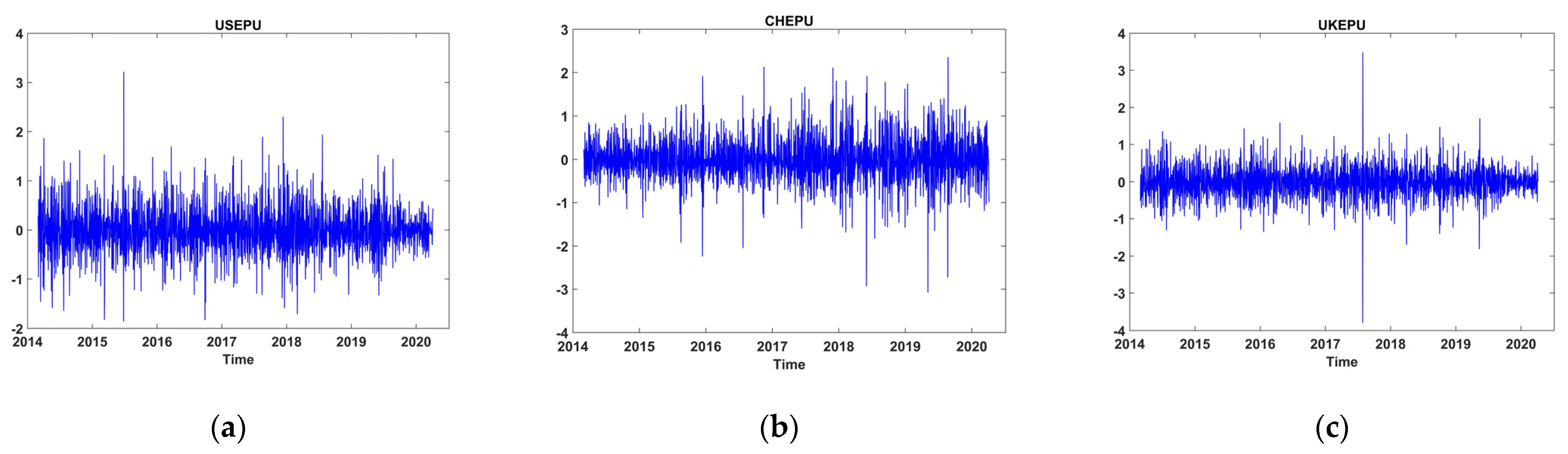

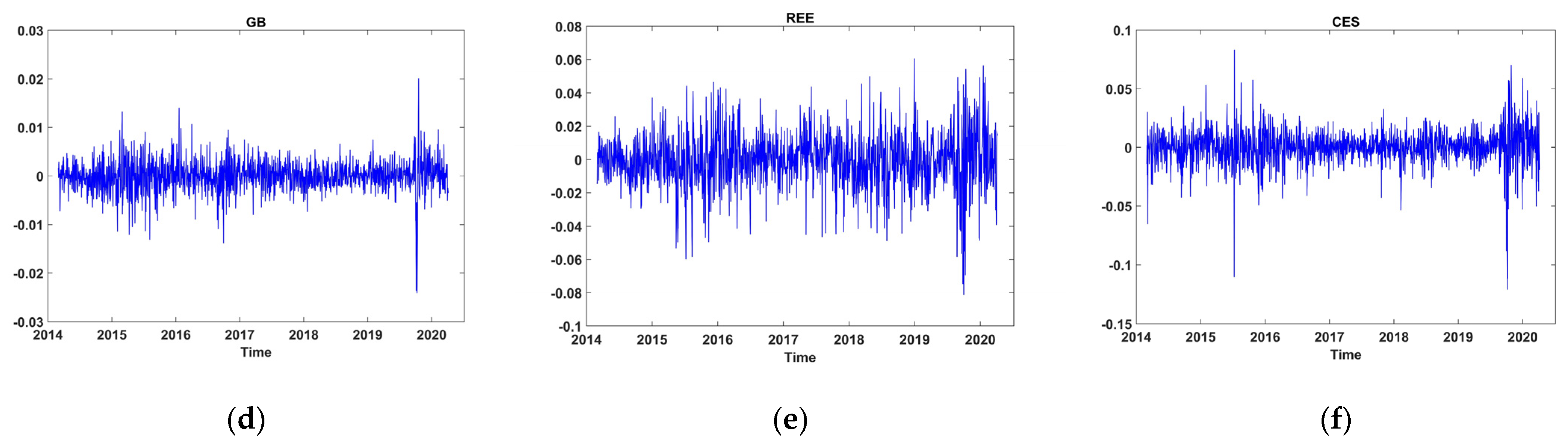

Results of Phillips Perron test for unit root are illustrated in

Table 3. Results confirmed that the null hypothesis is rejected for all indexes at a high-level significance. Therefore, all variables are stationary at the first difference and fulfilling a pre-estimation assumption for DCC-GARCH estimation. *** indicates significance at 5%. All variables are stationary, as can be viewed in

Figure 2.

However, the authors estimated unconditional correlation before DCC-MGARCH estimation, as shown by the results in

Table 4. The authors also tested the null hypothesis that the unconditional correlation is equal to zero. The results for unconditional correlations reported in

Table 4 confirm the evidence for a negative and not perfect positive correlation based on the

p-values and

t-test statistics. Thus, a predominant positive correlation sign suggests that clean energy stocks, green bonds, and rare earth elements are avenues for diversification, and that green bonds, rare earth elements, and clean energy stocks are strong hedges against the economic policy uncertainty of the USA. Moreover, green bonds and clean energy stocks proved to be strong hedges against UKEPU and CHEPU indexes, respectively. In contrast, the negative correlation of green bonds, clean energy stocks, and rare earth elements against EPUs suggests that green bonds’ hedging ability is not limited to the USA only. These findings are consistent with our proposal that hedging ability prevails in green bonds, clean energy stocks, and rare earth elements against EPU. Correlation values in bold denote unconditional correlation coefficients at

at a 5% statistical significance level.

Authors estimated the DCC-GARCH model quasi-maximum likelihood technique due to non-normality in the time series. The quasi-maximum likelihood function ignores non-normality and generates standard errors by maximizing the likelihood. This technique assumes that residuals are conditionally normal, but originally draw from other conditional distributions. After consideration of several log-likelihood value evaluations, the authors consider GARCH (1,1) as the data are better fitted in DCC (1,1) with each conditional variance in GARCH (1,1) in the current lag periods for all series.

Table 5 and

Table 6 illustrate the GARCH (1,1) results for the full sample and during COVID-19, respectively, to estimate conditional volatility since 2014 and during the novel coronavirus to uncover the diversification properties among green bonds, clean energy stocks, and rare earth elements with more hedge and safe haven efficiency against EPUs. The sum of

and

is near 1; thus, all GARCH processes are highly persistent.

Likewise, the DCC parameters are consistent and statistically significant, as the chi-square coefficient and probability values are significant in

Table 5 and

Table 6. This suggests that the null hypothesis, which assumes a constant correlation over time, is rejected.

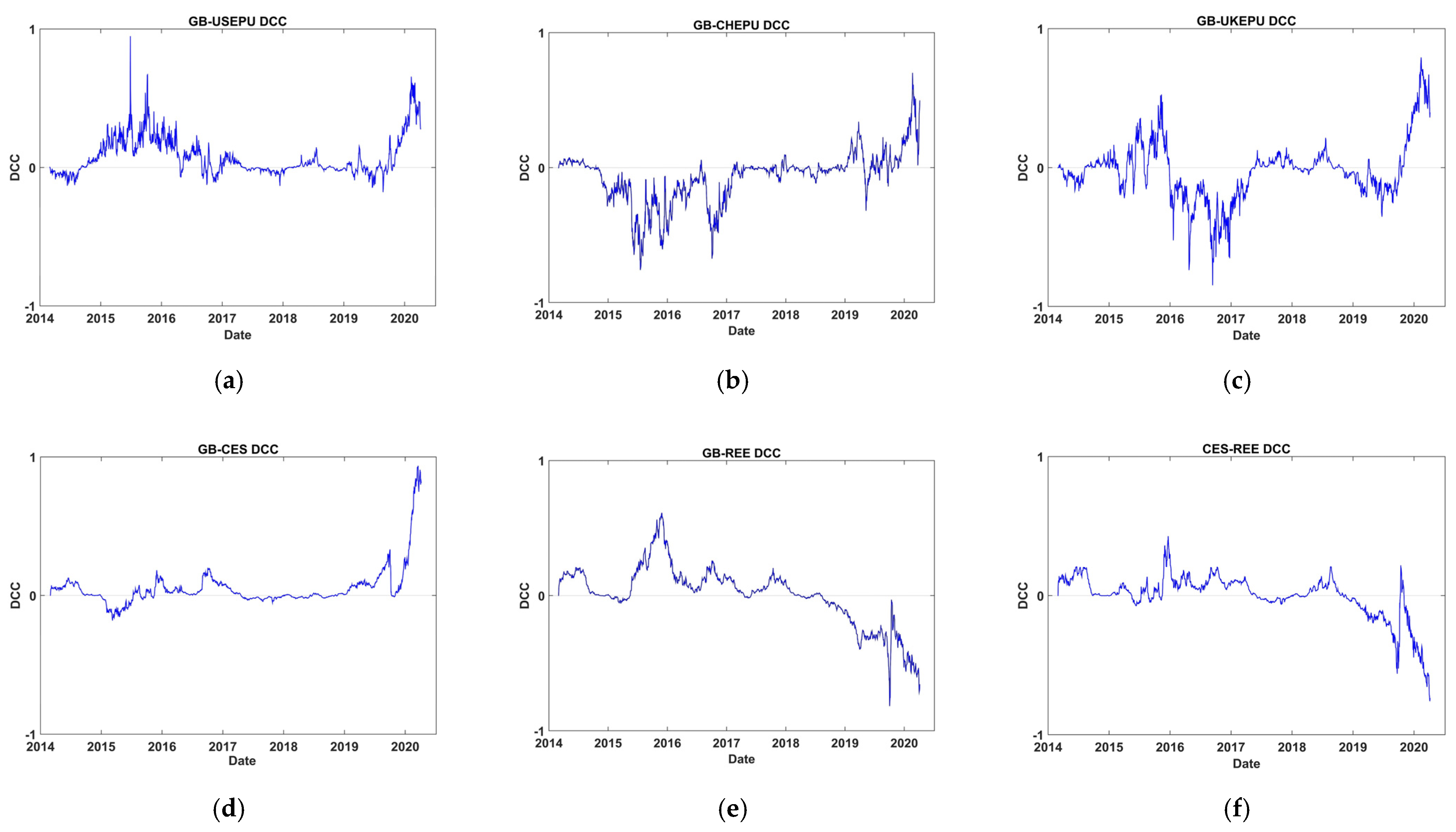

The second step estimation covers dynamic conditional correlations;

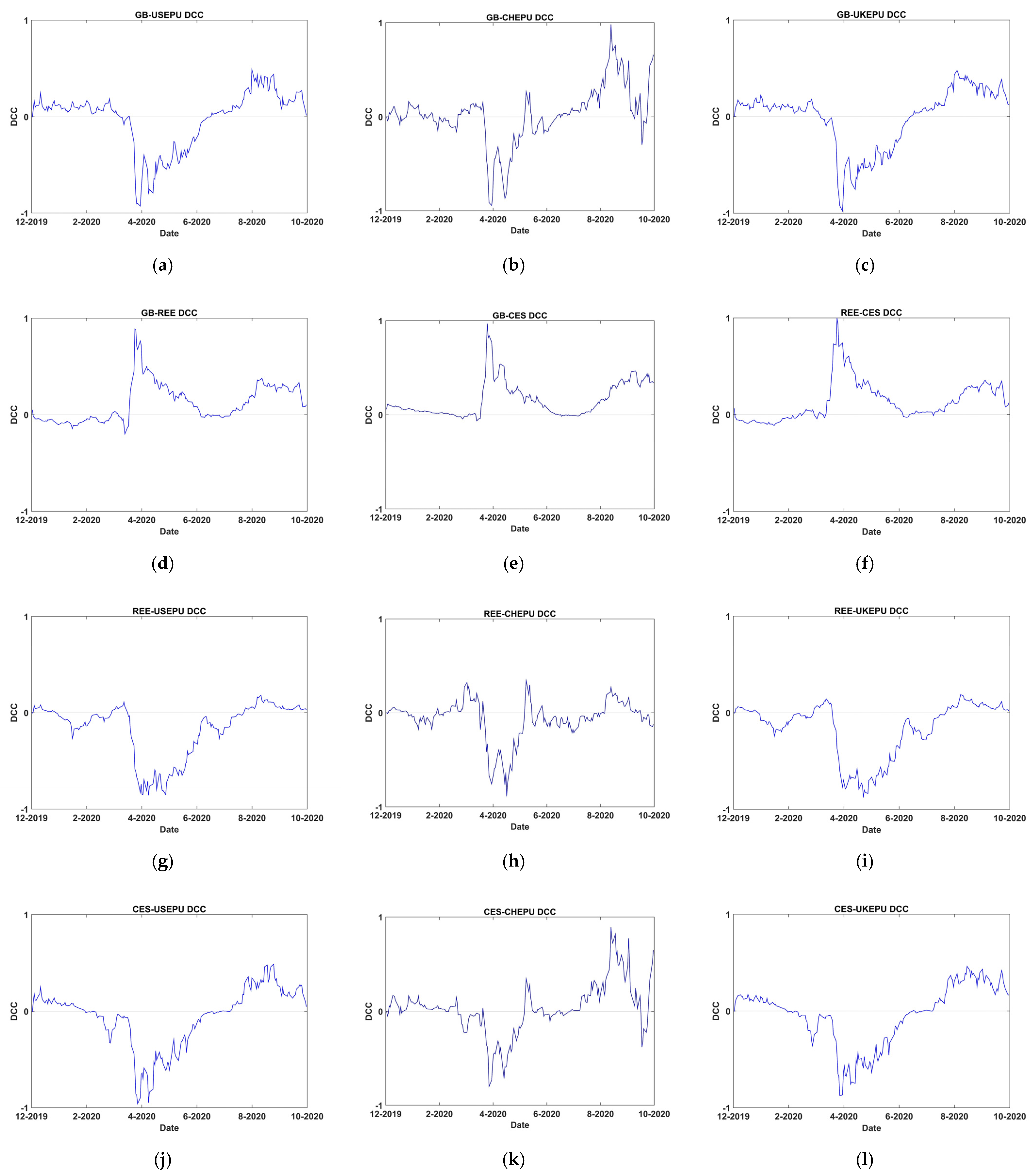

Figure 3 reports the dynamic conditional correlations between green bonds and EPUs, and DCCs among green bonds, clean energy stocks, and rare earth elements. In the full sample, outcomes confirm the conditional correlation between green bonds volatility and EPU’s dominantly negative in the case of the UK and China; however, green bonds volatility and USEPU demonstrated a positive correlation with few negative high magnitude correlation trends.

Afterwards, mixed volatility correlation patterns for green bonds with rare earth elements and clean energy stocks were observed; however, in 2020, the correlation demonstrated an unconventional pattern. Rare earth elements and clean energy stocks are dominantly positively correlated over time.

4. Robustness Check: During COVID-19

Moving towards the COVID-19 pandemic, the authors estimated a separate analysis to verify the robustness of findings in full sample estimation.

Table 6 illustrates DCC M-GARCH results for sub-sample during the COVID-19, and it shows the persistence of all GARCH processes as, for all cases of any two return series, the sum of

and

is close to “1”, thus fulfilling the GARCH assumption. Moreover,

Table 7 reports that DCC parameters for correlation are also consistent in all cases.

Figure 4 illustrates the time-varying conditional correlation among green bonds, rare earth elements, and clean energy stocks against EPUs during the novel coronavirus. Interestingly, dynamic conditional correlation outcomes validate that the negative association of green bonds, clean energy stocks, and rare earth elements is more prominent with the economic policy uncertainty of the USA, China, and the UK during the COVID-19 episode. However, alternative positive trends are spotted. In contrast, all other indices, such as green bonds, clean energy stocks, and rare earth elements, are positively correlated with each other during the sanitary crisis. This positive (though not perfectly positive) association infers that these securities may be considered as diversifiers against each other.

Table 7 demonstrates the DCC parameters that are statistically significant and consistent with

Figure 4. The authors report a median spline graph to smooth reoccurring variations as a

Figure 4. The horizontal line in the graph demonstrates the zero correlation on the

y-axis, and bold values in

Table 7 denote the dynamic conditional correlation coefficient between all indices. All values in parentheses are the

p-values at a 5% significance level. “A” refers to full sample estimation for hedging and diversification and “B” refers to the COVID-19 period. In overview, diversification, hedging, and safe haven properties for green bonds, clean energy stocks, and rare earth elements are alive during the COVID-19 period, during which previous studies have indicated evidence of strong linkages across major stock indices (

Abuzayed et al. 2021).

5. Discussion

Economic policy uncertainty is deteriorating. Global financial integration and trade wars among nations are sources of higher EPU. Undoubtedly, the outbreak of COVID-19 has also led to devastating effects on foreign exchange markets (

Aslam et al. 2020a), volatility of financial markets (

Aslam et al. 2020b), and economic policy uncertainty (

Baker et al. 2020). Thus, investors urgently need to find potential avenues that may protect their investments from loss during a catastrophic event (such as COVID-19). Interestingly, countries have heterogeneous national economic policy uncertainty patterns based on their regulatory framework and monetary and fiscal policies (

Haq and Aftab, forthcoming). Therefore, every country-specific economic policy uncertainty requires diverse solutions to hedge.

To the best of our knowledge, this study is the first to consider economic policy uncertainty and green bonds time-varying associations. This study revealed that green bonds are a strong hedge against clean energy stocks, rare earth elements, China-EPU and UK-EPU. However, they serve as a weak hedge against the economic policy uncertainty of the USA, and rare earth elements act more as a diversifier against clean energy stocks. This suggests that green bonds can serve as a good financial instrument to hedge economic policy risk in the USA and even better in other countries, such as China and the United Kingdom. Thus, the emergence of green bonds is a potential avenue to hedge and mitigate risk in financial and economic systems (

Broadstock and Cheng 2019).

Green bonds are a promising financial asset-class, and their economic significance is not restricted to the setting of the US. However, the hedging abilities are going beyond the borders, proving green bonds as an encouraging risk management tool worldwide. These findings have significance for international investors who have an investment in financial markets of China and the UK, as adding green bonds to a portfolio can shield certain investments from the economic policy shocks in these countries during normal economic conditions. Additionally, there exists a positive volatility linkage between global rare earth elements and clean energy stocks. This is due to the dependency of clean energy production on rare earth elements; these findings are well-aligned with (

De Koning et al. 2018). In addition, this is also due to the monopolistic control China holds over rare earth elements (

Marscheider-Weidemann et al. 2013), and the US imports rare earth elements for clean energy production from China. This is the main reason that the volatility of US clean energy stocks is positively correlated with global rare earth elements. Moreover, rising tensions between the United States and China have sparked concerns. The Chinese government and National Development and Reform Commission (NDRC) took this seriously against the US by blocking its REE supply (

Schmid 2019;

Global Times 2019) which will ultimately affect the US’s clean energy industry. In current crucial times, the US green bonds demonstrated a positive volatility correlation with both clean energy stocks and rare earth elements during the period of this study. Therefore, US investors have ample risk management opportunities in the shape of having US green bonds, as green bonds are proven diversifiers against the volatility of clean energy stocks and global rare earth elements in normal market conditions.

The COVID-19 pandemic unveiled some interesting correlation patterns and implications for investors. Interestingly, clean energy stocks and rare earth elements are strong safe havens against economic policy uncertainty, as the correlation signs are predominantly negative during catastrophic events such as COVID-19. However, green bonds stood as strong safe havens against US EPU and UK EPU; thus, green bonds as a safe haven faded during COVID-19 in the case of the China EPU. This may be as US EPU influences the performance and movements of green bonds (

Broadstock and Cheng 2019). These findings imply that green bonds are more of a hedge than a safe haven. Moreover, the abilities of safe havens are more pronounced in clean energy stocks and rare earth elements against EPUs’ economic policy uncertainty. Clean energy stocks, rare earth elements, and green bonds are not a hedge or a safe haven, but act as diversifiers against each other as these financial assets share homogeneous characteristics. Likewise, this observation may be due to the limited connectedness between the green bonds market and general stock markets, as clean energy stocks and green bonds belong to two different asset classes (

Ferrer et al. 2021).

Policy Implications

This research provides useful implications for several sustainable economists and economic actors in terms of hedging, portfolio management, and sustainability policy. The restrictive exports policy of China and ban over REE exports to the USA damaging clean energy production and other dependent industries, i.e., high technology firms. Thus, American authorities should keep promoting US green bonds, as they can hedge the volatility of global rare earth elements and the US clean energy stocks for clean energy investors. Moreover, it can protect US REE investors from the volatility spillover effect from China’s rare earth metals (due to its dominance over rare earth resources) and win the trade war. The description of the nature and usage of green bonds should be standardized internationally to improve their wider acceptance worldwide. Moreover, monitoring the development and formalization of green bonds can be an effective area of action for any sustainable economist. The emerging US green bonds hedging properties beyond the borders suggest that Chinese and UK authorities should ease the restrictions and allow investors to invest in the US green bonds market. At the same time, these findings provide a useful roadmap for international policymakers and fund managers having investments in the USA, China, and the UK. Overall, it infers that US clean energy stocks are vulnerable to the global rare earth elements.

In terms of sustainability policy, it is time to move the attention toward green finance and sustainable investment, i.e., green bonds to raise funds. Therefore, the attractiveness of green bonds are twofold; they are not solely a risk mitigation and hedging tool, but also are issued to generate money to mitigate climate change and environmental projects, improve energy efficacy, and accelerate decarbonization in the economy.

6. Conclusions

Despite the growing interest in green investment avenues such as green bonds, the current finance and economics literature still lacks empirical evidence for their risk management abilities as a hedge, safe haven, and diversifier against clean energy stocks, rare earth elements in general, and economic policy uncertainty in particular. Thus, this study focuses on the hedging and safe haven abilities of green bonds, clean energy stocks, and global rare earth elements. Additionally, it explored diversification properties between green bonds, clean energy stocks, and global rare earth elements in the full sample and during the COVID-19 episode. Thus, this study focuses on four ideas: (i) the hedge and safe haven properties of green bonds against economic policy uncertainty during COVID-19; (ii) hedging and the safe haven properties of clean energy stocks; (iii) hedging and safe haven role of rare earth elements against economic policy uncertainty during COVID-19; and (iv) the diversification properties among green bonds, clean energy stocks, and rare earth elements, using five-day daily values for each index within a dynamic conditional correlation model (

Engle 2002).

Firstly, the results for the full sample estimation reveal that green bonds are potential avenues for risk mitigation. The authors find that the DCCs between green bonds and China EPU and UK EPU indices are negative in the full sample estimation, indicating that green bonds were a strong hedge against China and UK EPU. However, the DCC between US EPU and green bonds indices was positive in the full sample, indicating that green bonds were not a hedge (strong or weak) against US EPU. This implies that the volatility of green bonds may prone to economic policy uncertainty, therefore green bonds lost their hedging role. On the other hand, the DCCs between green bonds, US EPU, and UK EPU are negative during COVID-19, indicating green bonds were a strong safe haven against US EPU and UK EPU during COVID-19. However, there was not a statically significant correlation between green bonds and China EPU, indicating that green bonds lost their safe haven ability during COVID-19.

Secondly, clean energy stocks serve as an effective strong hedge against the US EPU and UK EPU in full sample estimation. As the DCCs between clean energy stocks, US EPU, and UK EPU were negative in the full sample. However, DCC was negative insignificant in the case of China EPU, thus clean energy stocks were not a hedge against China EPU. Particularly during COVID-19, the DCC’s patterns remained the same as the full sample estimation, thus clean energy stocks were a safe haven against US EPU and UK EPU, but not against China EPU.

Thirdly, the DCCs between global rare earth elements, China EPU, and UK EPU indices are negative in full sample estimation, indicating that global rare earth elements were a strong hedge against the economic policy uncertainty indices of China and the UK. However, insignificant DCC between US EPU and global rare earth elements indicated no presence of hedging role against US EPU. This may be due to the monopolistic control of China over rare earth elements production. During COVID-19, the DCCs between global rare earth elements and all EPUs (USA, China, and UK) were negative, indicating that global rare earth elements were a strong safe haven against the economic policy uncertainty of the USA, China, and the UK.

Fourthly, the results of DCCs between green bonds, clean energy stocks, and global rare earth elements are mainly positive (though not perfectly positive) in the full sample estimation, indicating that these securities can be used as diversifiers collectively with each other. In particular, the positive DCCs (not perfectly positive) remained similar to the full sample, thus these assets are diversifiers if used in a single portfolio. These results can guide policymakers and fund managers to form suitable policies and strategies considering COVID-19.

Finally, future studies should explore the real-life importance of green bonds in terms of sustainability in the USA and around the globe. Further research is expected on how US EPU and China EPU are related to their country-specific rare earth elements. It will be interesting to capture the impact of trade wars between the USA and China on rare earth elements, especially as China has monopolistic control over rare earth production worldwide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}