The Impact of ESG Management on Investment Decision: Institutional Investors’ Perceptions of Country-Specific ESG Criteria

Abstract

:1. Introduction

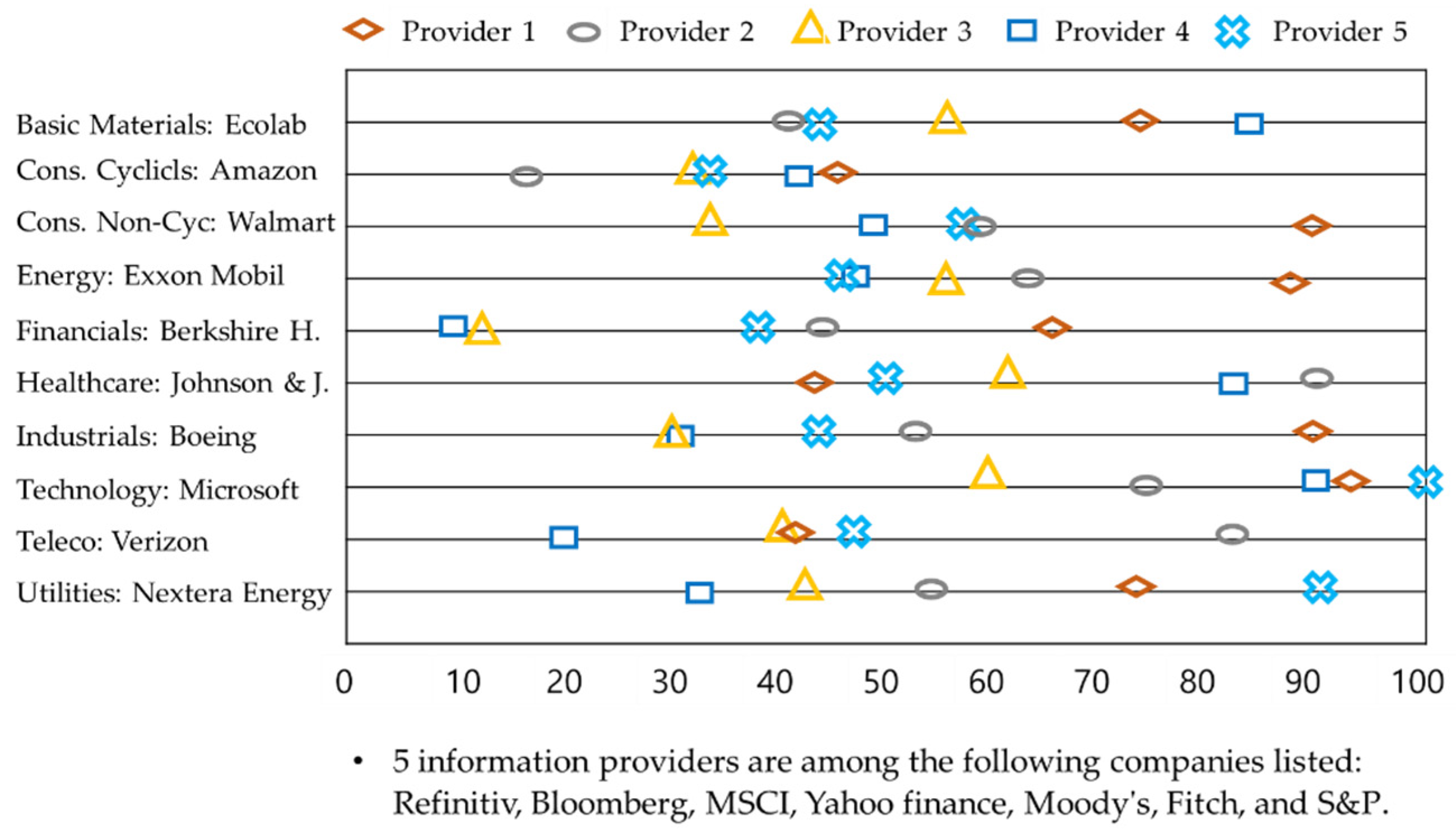

2. Literature Review

3. Research Methodology and Materials

3.1. Decision Framework: Application of the AHP Method

- Step 1: Identify ESG factors used by the existing literature and major ESG information providers, and point out limitations and problems of existing models. This has already been investigated in this literature review section, but it will be further explored in Section 3.2.

- Step 2: Analyze the factors and construct a hierarchy of decision-making factors.

- Step 3: Prepare questionnaires for pairwise comparisons, distribute them to experts, and collect responses.

- Step 4: Check for consistency.

- Step 5: Prioritize and evaluate it.

3.2. Derivation of Components

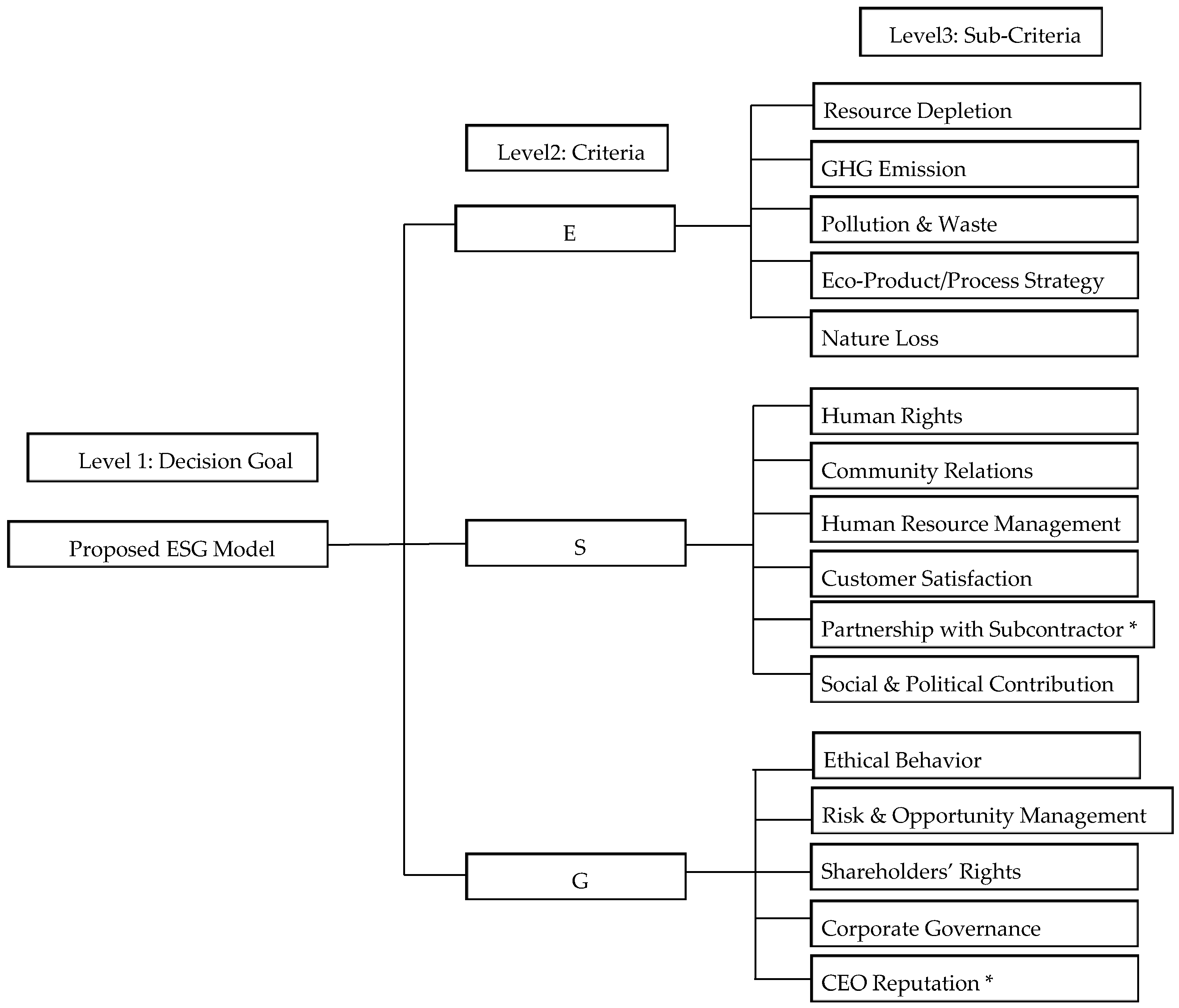

4. Composition of Hierarchical Structure

4.1. Developing the Assessment Criteria

4.2. Respondent Selection and Survey

- Period of service: at least 15 years of investment experience as an institutional investor

- Institutions at work: various types of financial institutions such as asset management companies, pension funds, insurers, securities firms, and banks

- Main business: Invest in various types of asset classes, including bond investment, equity investment, and alternative investment.

- As presented in Table 3, the experts in the sample are well distributed by institution and major businesses. The frequency of type by institution is less than 25%.

- The respondents in the sample are institutional investors and experts with an average of 20 years of experience in the investment field.

- Most (74%) of the respondents in the sample have past experience considering ESG factors as one of their investment decisions.

5. Results

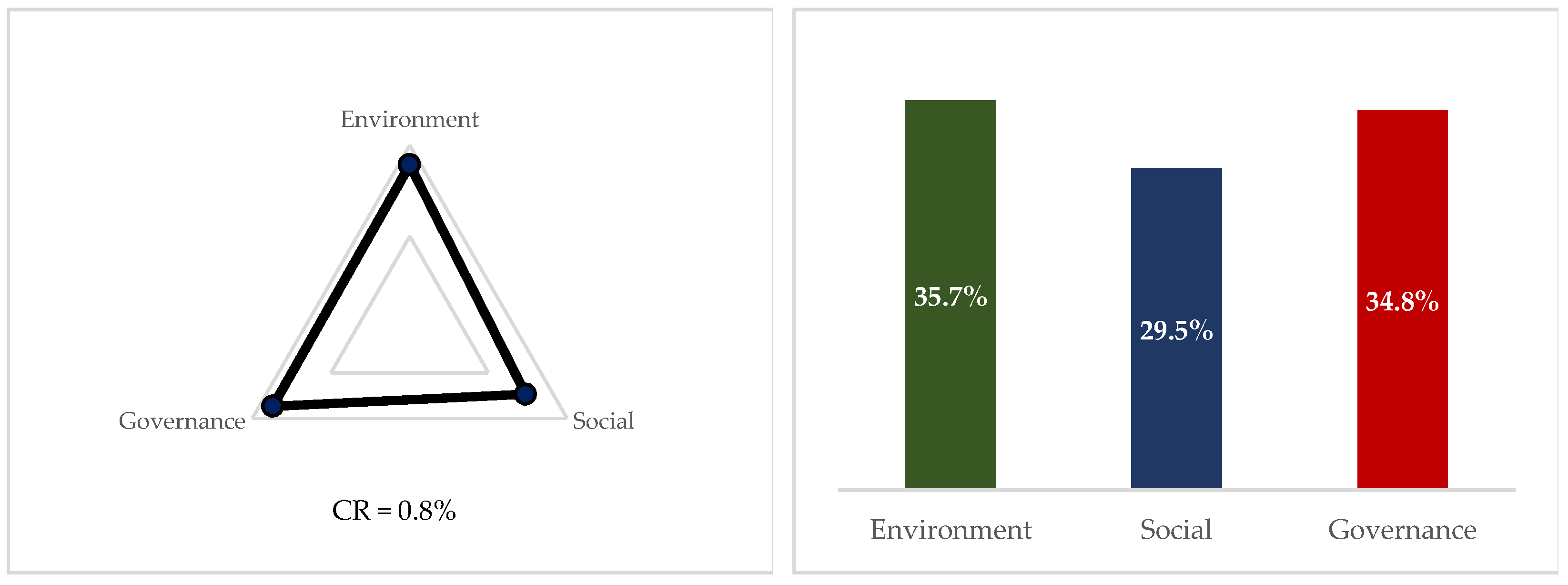

5.1. Weights of the Factors and Attributes

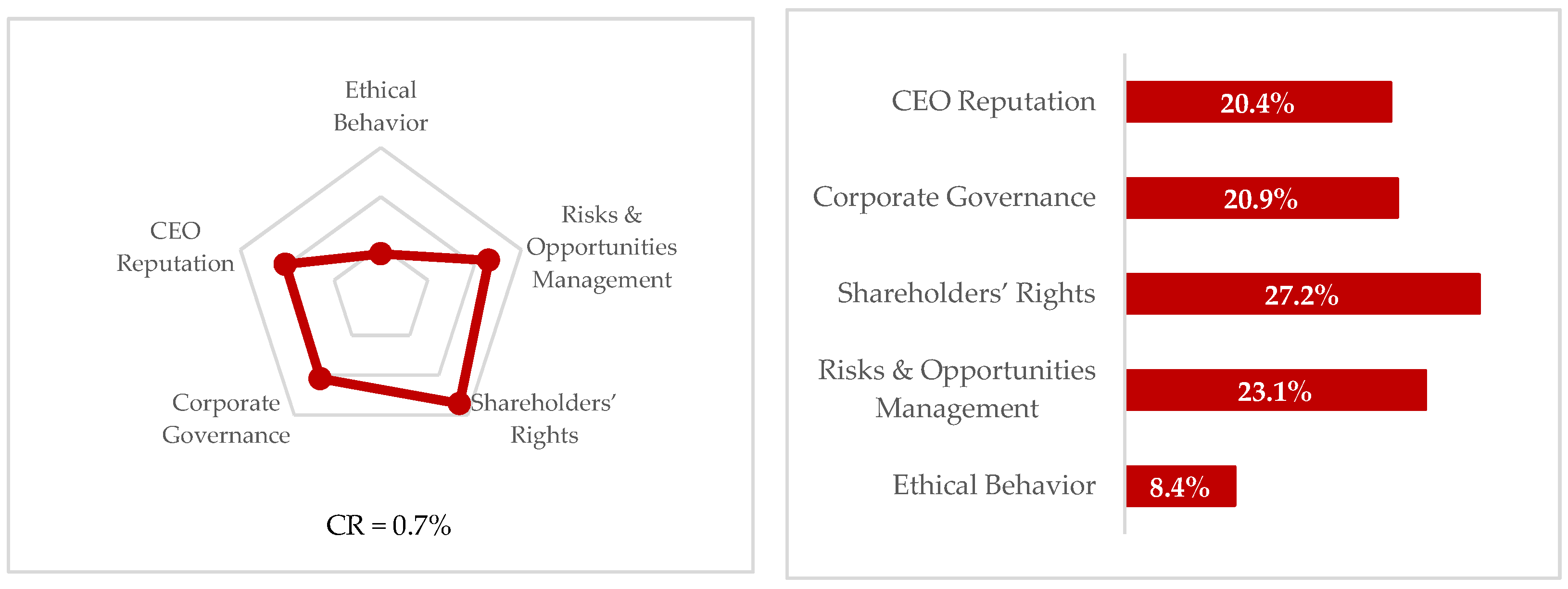

5.1.1. Local Weights for Main Criteria (Level 2)

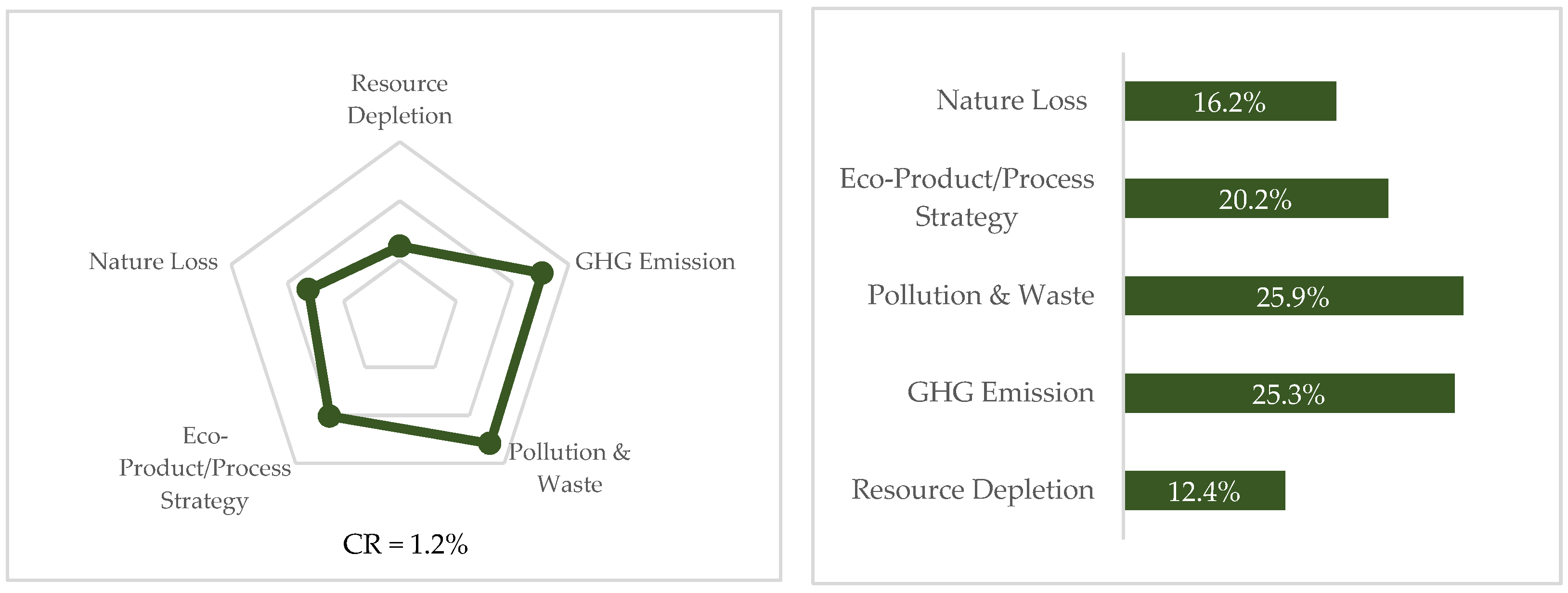

5.1.2. Local Weights for Sub-Criteria

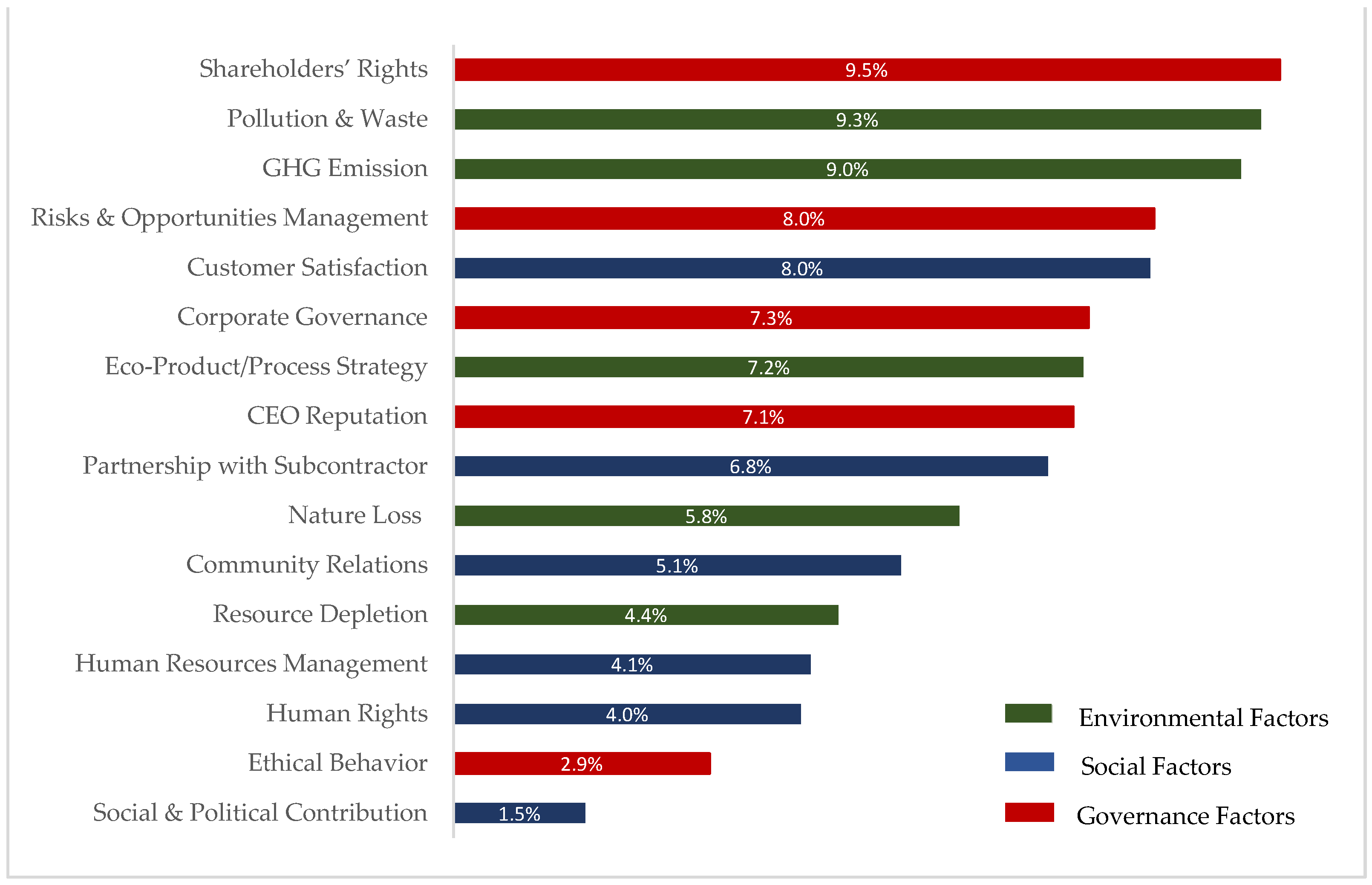

5.1.3. Global Weights for Sub-Criteria

5.2. Weights of the Factors and Attributes Divided by Five Groups (by Investment Institution) and by Three Groups (by Main Business)

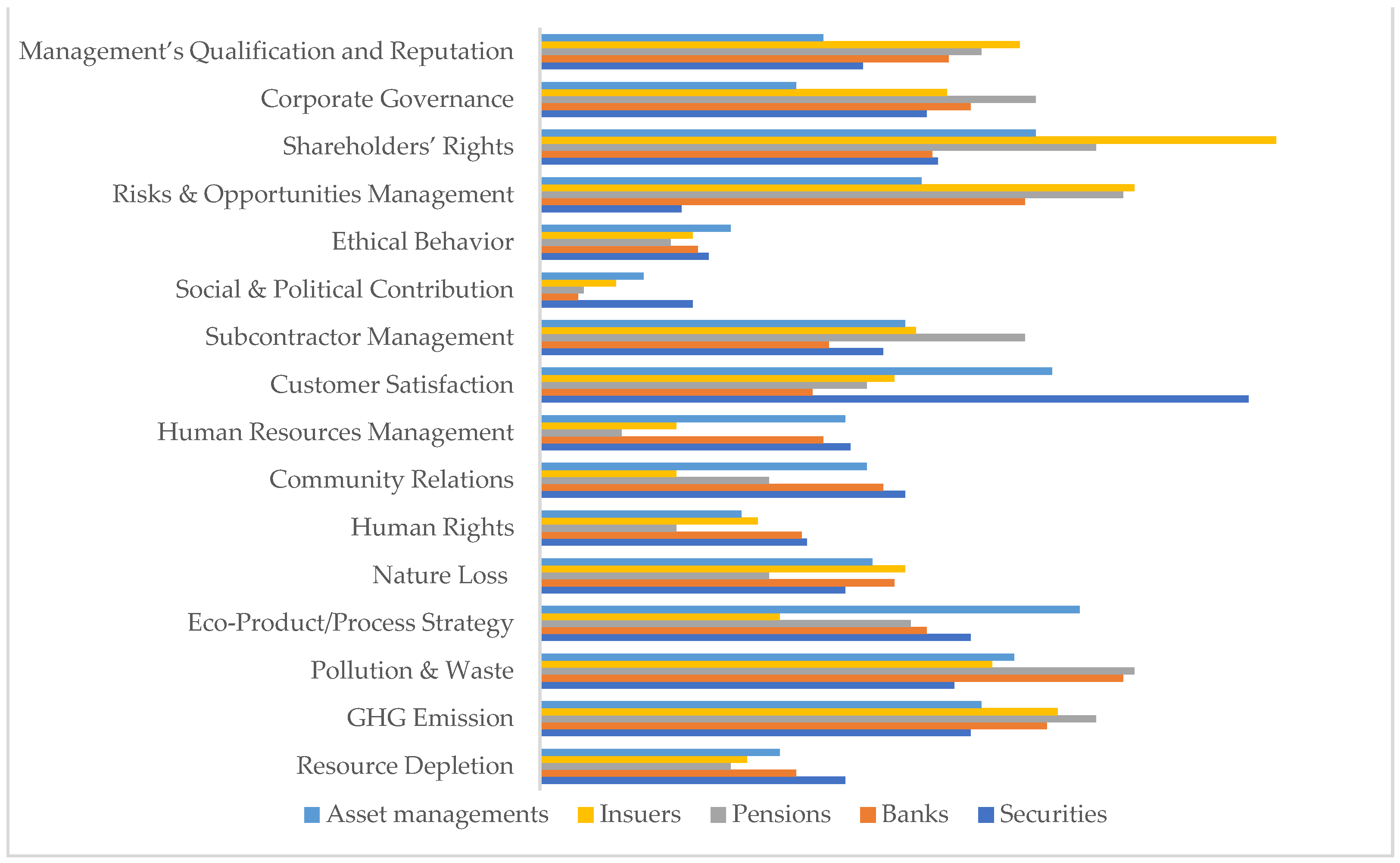

5.2.1. Global Weights of the Factors and Attributes Divided by Five Groups (by Investment Institution)

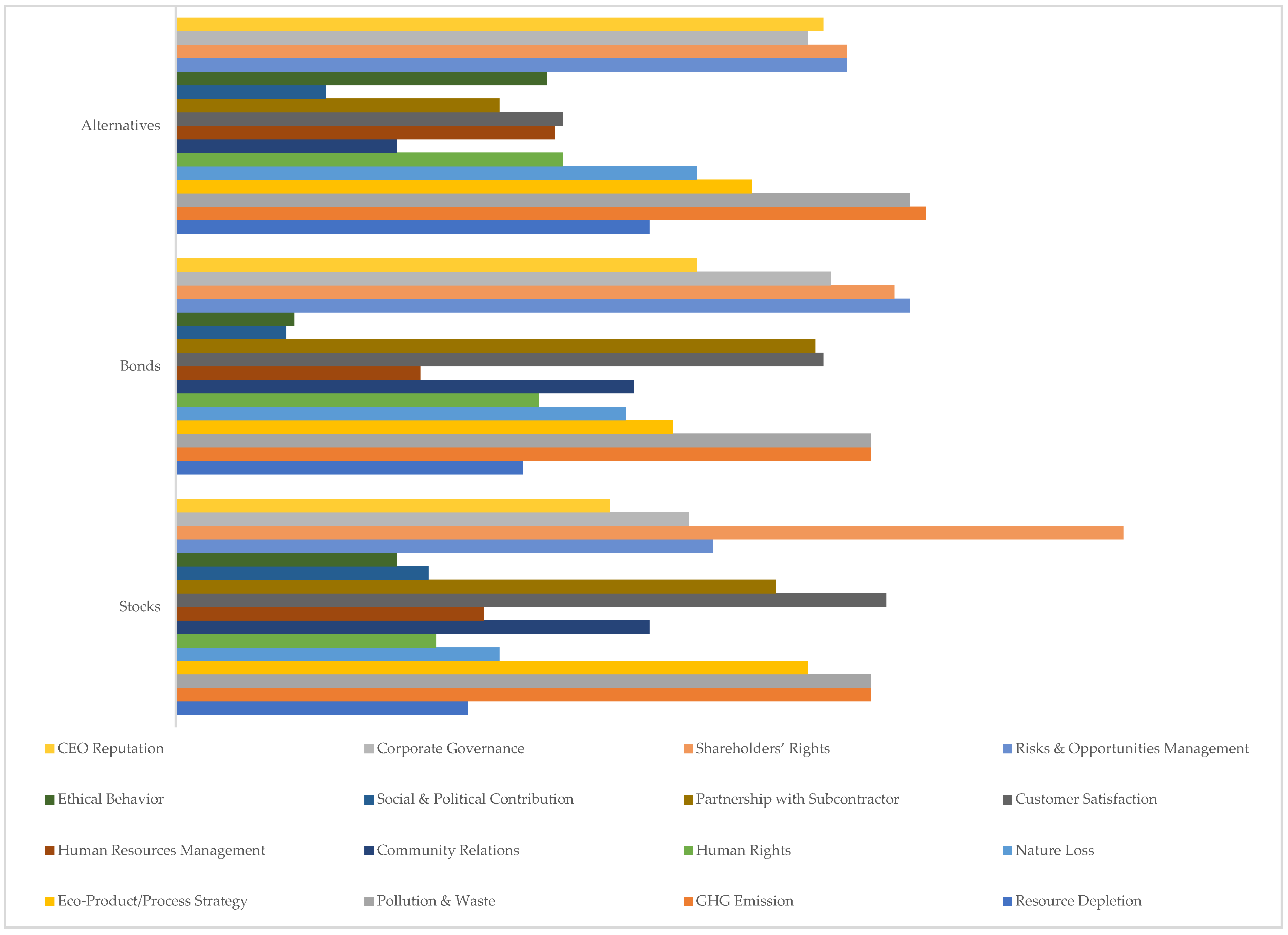

5.2.2. Global Weights of the Factors and Attributes Divided by Three Groups (by Main Business)

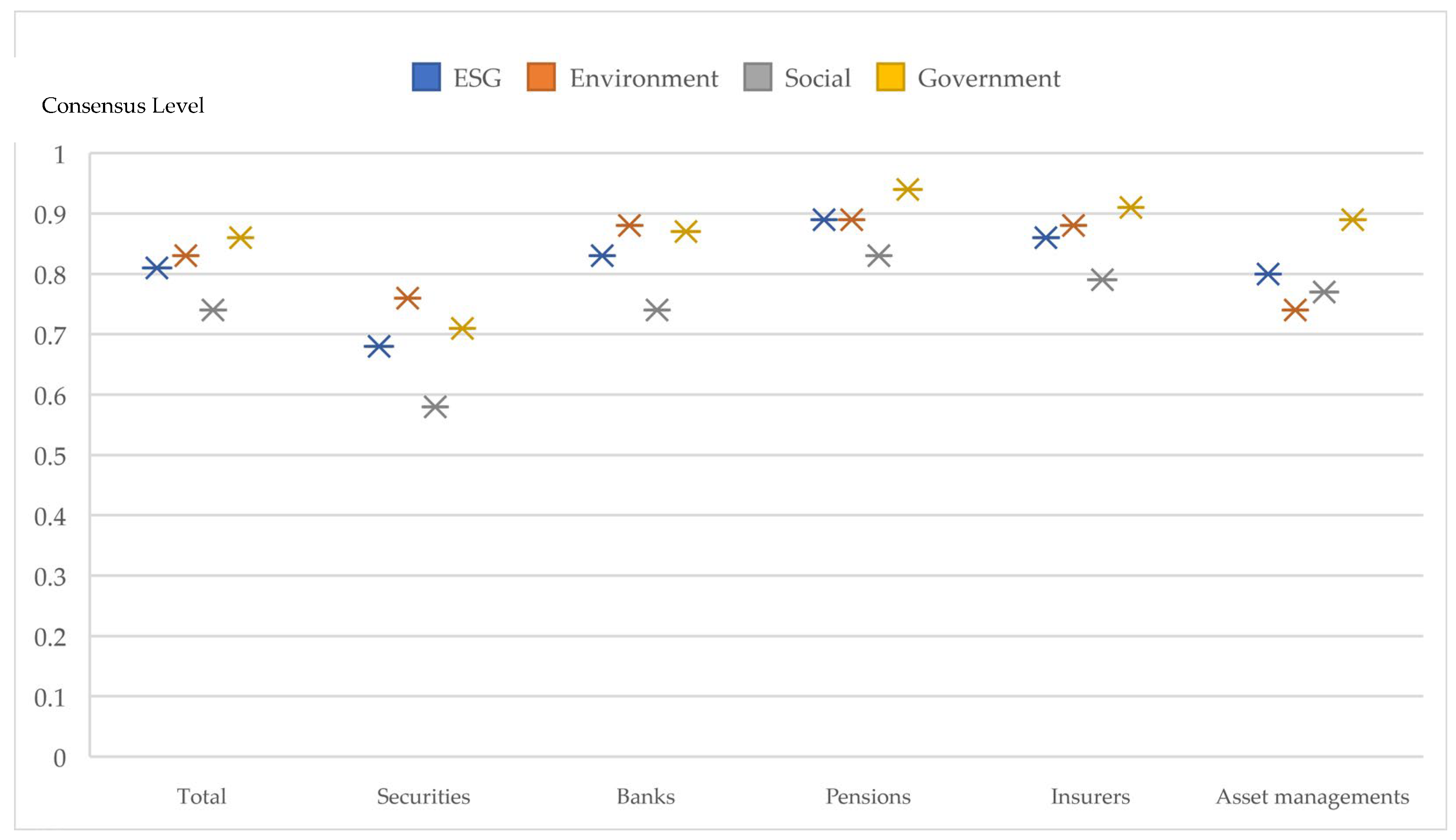

5.3. Consensus Level

5.4. Other Discussion Points

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Survey Qestionarie

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 1 | What field are you currently working in? |

| ① Asset management ② Pension fund ③ Insurance ④ Securities ⑤ Bank ⑥ Other ( ) | |

| 2 | In which area of your investment business are you currently working? |

| ① Stocks ② Bonds ③ Alternative investment ④ Management ⑤ Others ( ) | |

| 3 | How many years have you worked in the entire investment field? |

| ① 15 years or less ② 15–25 years ③ 25 years or more | |

| 4 | To what extent do you have an understanding and interest in ESG? |

| ① Very large ② Large ③ Average ④ Small ⑤ Not at all | |

| 5 | Have you ever considered ESG as an investment decision factor when making an investment decision? |

| ① Yes ② No | |

| 6 | To what extent do you see the impact of ESG on the future investment environment? |

| ① Expected to be very large ② Moderate ③ Not expected to be significant | |

| 7 | Countries around the world are preparing laws and regulations to have companies’ disclosure regarding ESG practices. In this regard, do you think it is necessary to have a separate Korean ESG (K-ESG) framework reflecting Korean business/economic and social characteristics? |

| ① Very necessary ② Necessary ③ Not necessary | |

| 8 | The South Korean government is planning to introduce various regulations and ESG disclosure systems, such as making ESG-related disclosures mandatory for all KOSPI-listed companies from 2030. How do you feel about the timeline of the current Korean ESG (K-ESG) introduction? |

| ① Appropriate ② Moderate ③ Too fast | |

| 9 | Do you evaluate the consistency of the government’s policies related to business management? |

| ① Consistent ② Moderate ③ Very inconsistent |

| Measurement Item | Evaluation Scale | Measurement Item |

|---|---|---|

| A | 5 4 3 2 1 2 3 4 5 | B |

| Extremely Important Equal Extremely Important |

| Criteria | Description | Measurement |

|---|---|---|

| Environmental Factors | Measure the company’s environmental reporting and environmental risks, and pursue innovation opportunities for sustainable growth | Composition of subcategories: resource consumption, greenhouse gas emission, pollution and waste emission, eco-friendly products and production process strategy, nature loss |

| Social Factors | Understand the impact of corporate activities on stakeholders, and pursue social values as a member of the local community | Subcategory composition: human rights protection, community relations, human resource management, customer satisfaction, partnership with subcontractor, social and political contribution |

| Environmental Factors | Corporate management aligns the interests of shareholders, management, and workers, and pursues sustainable growth strategies | Subcategory composition: ethical behavior, risks and opportunities management, shareholders’ rights, corporate governance, CEO reputation |

| Measurement Item | Evaluation Scale | Measurement Item |

|---|---|---|

| Environmental Factors | 5 4 3 2 1 2 3 4 5 | Social Factors |

| Social Factors | 5 4 3 2 1 2 3 4 5 | Governance Factors |

| Environmental Factors | 5 4 3 2 1 2 3 4 5 | Governance Factors |

| Criteria | Sub-Criteria | Descriptions | Measurements |

|---|---|---|---|

| E | Resource Depletion | Managing the amount of energy and other consumable resources | Energy/water consumption |

| GHG (Greenhouse Gas) Emission | Managing and reducing the level of GHG emissions to meet the target for the Paris Agreement | GHG emission and climate risk targets and assessments, product carbon footprint | |

| Pollution and Waste | Managing the level of pollution and waste | Waste disposal, water/air/land pollution, single use plastic | |

| Eco-Product/Process Strategy | Strategic efforts to reduce the corporate’s environmental impacts, i.e., produce more using less resource | R&D expenditure | |

| Nature Loss | Levels of potential damage to the nature and efforts for ecological protection | Land use and ecological sensitivity, biodiversity |

| Measurement Item | Evaluation Scale | Measurement Item |

|---|---|---|

| Resource Depletion | 5 4 3 2 1 2 3 4 5 | GHG (Greenhouse Gas) Emission |

| Resource Depletion | 5 4 3 2 1 2 3 4 5 | Pollution and Waste |

| Resource Depletion | 5 4 3 2 1 2 3 4 5 | Eco-Product/Process Strategy |

| Resource Depletion | 5 4 3 2 1 2 3 4 5 | Nature Loss |

| GHG (Greenhouse Gas) Emission | 5 4 3 2 1 2 3 4 5 | Pollution and Waste |

| GHG (Greenhouse Gas) Emission | 5 4 3 2 1 2 3 4 5 | Eco-Product/Process Strategy |

| GHG (Greenhouse Gas) Emission | 5 4 3 2 1 2 3 4 5 | Nature Loss |

| Pollution and Waste | 5 4 3 2 1 2 3 4 5 | Eco-Product/Process Strategy |

| Pollution and Waste | 5 4 3 2 1 2 3 4 5 | Nature Loss |

| Eco-Product/Process Strategy | 5 4 3 2 1 2 3 4 5 | Nature Loss |

| Criteria | Sub-Criteria | Description | Measurement |

|---|---|---|---|

| S | Human Rights | Respecting and securing human rights in the business practices | Discrimination, harassment, diversity ratio, freedom of association, child/forced/compulsory labor |

| Community Relations | Efforts to build solid reputation and relationship with local communities | Local investment, community investment | |

| Human Resources Management | Ensuring the dignity, equality, health, and benefits of employees | Talent attraction and retention Providing health, safety and training opportunities | |

| Customer Satisfaction | Provide products and services that satisfy customers | Privacy, data security, product safety and quality, financial product safety | |

| Partnership with Subcontractor | Promoting satisfaction, trust, and inclusive growth with subcontractor(s) | Contract satisfaction, trusting relationship | |

| Social and Political Contribution | As a responsible citizen, making effort to build greater overall value to the society | Contributions, philanthropy, infrastructure investment, employment, total tax paid |

| Measurement Item | Evaluation Scale | Measurement Item |

|---|---|---|

| Human Rights | 5 4 3 2 1 2 3 4 5 | Community Relations |

| Human Rights | 5 4 3 2 1 2 3 4 5 | Customer Satisfaction |

| Human Rights | 5 4 3 2 1 2 3 4 5 | Human Resources Management |

| Human Rights | 5 4 3 2 1 2 3 4 5 | Partnership with Subcontractor |

| Human Rights | 5 4 3 2 1 2 3 4 5 | Social and Political Contribution |

| Community Relations | 5 4 3 2 1 2 3 4 5 | Customer Satisfaction |

| Community Relations | 5 4 3 2 1 2 3 4 5 | Human Resources Management |

| Community Relations | 5 4 3 2 1 2 3 4 5 | Partnership with Subcontractor |

| Community Relations | 5 4 3 2 1 2 3 4 5 | Social and Political Contribution |

| Customer Satisfaction | 5 4 3 2 1 2 3 4 5 | Human Resources Management |

| Customer Satisfaction | 5 4 3 2 1 2 3 4 5 | Partnership with Subcontractor |

| Customer Satisfaction | 5 4 3 2 1 2 3 4 5 | Social and Political Contribution |

| Human Resources Management | 5 4 3 2 1 2 3 4 5 | Partnership with Subcontractor |

| Human Resources Management | 5 4 3 2 1 2 3 4 5 | Social and Political Contribution |

| Partnership with Subcontractor | 5 4 3 2 1 2 3 4 5 | Social and Political Contribution |

| Criteria | Sub-Criteria | Description | Measurement |

|---|---|---|---|

| G | Ethical Behavior | Monitoring and management to comply with applicable laws and regulations | Anti-competitive practices, anti-corruption and bribery policy |

| Risks and Opportunities Management | Identification and management of strategic risks and opportunities regarding long-term value creation | Systemic risk management, critical incident risk management, business model resilience | |

| Shareholders’ Rights | Upholding shareholders’ concerns and voices in company strategy and management | Investment return, voting rights, information disclosure | |

| Corporate Governance | Structure of management system that reflects the direction and controlment of the company. | Gender ratio, experiences of the board members | |

| CEO Reputation | Impact of CEO and top management personality and qualifications have on the corporate image and value | CEO image, management controversy |

| Measurement Item | Evaluation Scale | Measurement Item |

|---|---|---|

| Ethical Behavior | 5 4 3 2 1 2 3 4 5 | Risks and Opportunities Management |

| Ethical Behavior | 5 4 3 2 1 2 3 4 5 | Shareholders’ Rights |

| Ethical Behavior | 5 4 3 2 1 2 3 4 5 | Corporate Governance |

| Ethical Behavior | 5 4 3 2 1 2 3 4 5 | CEO Reputation |

| Risks and Opportunities Management | 5 4 3 2 1 2 3 4 5 | Shareholders’ Rights |

| Risks and Opportunities Management | 5 4 3 2 1 2 3 4 5 | Corporate Governance |

| Risks and Opportunities Management | 5 4 3 2 1 2 3 4 5 | CEO Reputation |

| Shareholders’ Rights | 5 4 3 2 1 2 3 4 5 | Corporate Governance |

| Shareholders’ Rights | 5 4 3 2 1 2 3 4 5 | CEO Reputation |

| Corporate Governance | 5 4 3 2 1 2 3 4 5 | CEO Reputation |

References

- Agarwal, Upasna A., Sumita Datta, Stacy Blake-Beard, and Shivganesh Bhargava. 2012. Linking LMX, Innovative work behaviour and turnover intentions: The mediating role of work engagement. Career Development International 17: 208–30. [Google Scholar] [CrossRef]

- Aghion, Philippe, Sergei Guriev, and Kangchul Jo. 2021. Chaebols and firm dynamics in Korea. London: Centre for Economic Policy Research, Available online: https://cepr.org/active/publications/discussion_papers/dp.php?dpno=13825 (accessed on 22 July 2021).

- Allouche, Jose, and Patrice Laroche. 2005. A meta-analytical examination of the link between corporate social and financial performance. Revue de Gestion des Resources Humaines 57: 18–41. [Google Scholar]

- Amel-Zadeh, Amir, and George Serafeim. 2018. Why and how investors use ESG information: Evidence from a global survey. Financial Anlysts Journal 74: 87–103. [Google Scholar] [CrossRef] [Green Version]

- Becchetti, Leonardo, Rocco Cicretti, Ambrogio Dalo, and Stefano Herzel. 2015. Socially responsible and conventional investment funds: Performance comparison and the global financial crisis. Applied Economics 47: 2541–62. [Google Scholar] [CrossRef]

- Bender, Jennifer, Todd Bridges, Chen He, Anna Lester, and Xioaole Sun. 2018. A Blueprint for Integrating ESG into Equity Portfolios. The Journal of Investment Management 16. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3080381 (accessed on 24 July 2021).

- Beyond Coal. 2018. Available online: http://beyondcoal.kr/en/ (accessed on 4 July 2021).

- Bhushan, Navneet, and Kanwal Raj. 2004. Strategic Decision Making: Applying the Analytical Hierarchy Process. London: Springer, pp. 11–21. [Google Scholar]

- Boffo, R., and R. Patalano. 2020. ESG Investing: Practices, Progress and Challenges. Paris: OECD, Available online: https://www.oecd.org/finance/ESG-Investing-Practices-Progress-Challenges.pdf (accessed on 24 June 2021).

- Boukattaya, Sonia, and Abdelwahed Omri. 2021. Impact of board gender diversity on corporate social responsibility and irresponsibility: Empirical evidence from France. Sustainability 13: 4712. [Google Scholar] [CrossRef]

- Broadstock, David C., Kalok Chan, Louis T. W. Cheng, and Xiaowei Wang. 2021. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance Research Letters 38: 101716. [Google Scholar] [CrossRef]

- Brulhart, Franck, Sandrine Gherra, and Bertrand V. Quelin. 2019. Do stakeholder orientation and environmental proactivity impact firm profitability? Journal of Business Ethics 158: 25–46. [Google Scholar] [CrossRef]

- CFA Institute. 2018. ESG Integration in the Americas: Markets, Practices, and Data. Available online: https://www.cfainstitute.org/-/media/documents/survey/esg-integration-in-the-americas.ashx (accessed on 27 August 2021).

- Chen, Chien-Ming, and Magali Delmas. 2011. Measuring Corporate Social Performance: An efficiency perspective. Production and Operations Management 20: 789–804. [Google Scholar] [CrossRef]

- Choi, Mi Hwa. 2015. The effect of corporate social responsibility on the tax aggressiveness and cost of capital. Accounting Information Review 33: 161–93. [Google Scholar]

- Choi, Mi Hwa. 2018. The performance factors of CSR, investment efficiency and firm value. Journal of Finance and Accounting Information 18: 45–66. [Google Scholar] [CrossRef]

- Cornett, Marcia Milon, Otgontsetseg Erhemjamts, and Hassan Tehranian. 2016. Greed or good deeds: An examination of the relation between corporate social responsibility and the financial performance of U.S. commercial banks around the financial crisis. Journal of Banking & Finance 70: 137–59. [Google Scholar]

- De Franco, Carmine. 2020. ESG controversies and their impact on performance. The Journal of Investing 29: 33–45. [Google Scholar] [CrossRef]

- Eccles, Robert G., and George Serafeim. 2013. The Performance Frontier: Innovating for a Sustainable Strategy. Available online: https://www.hbs.edu/faculty/Pages/item.aspx?num=44737 (accessed on 24 July 2021).

- Escrig-Olmedo, Elena, María Á. Fernández-Izquierdo, Idoya Ferrero-Ferrero, Juana María Rivera-Lirio, and María Jejús Muñoz-Torres. 2019. Rating the raters: Evaluating how ESG rating agencies integrate sustainability principles. Sustainability 11: 915. [Google Scholar] [CrossRef] [Green Version]

- Felice, Fabio D., Antonella Petrillo, and Claudio Autorino. 2015. Development of a framework for sustainable outsourcing: Analytic Balanced Scorecard Method (A-BSC). Sustainability 7: 8399–419. [Google Scholar] [CrossRef] [Green Version]

- Francis, Jennifer, Allen H. Huang, Shivaram Rajgopal, and Amy Y. Zang. 2008. CEO reputation and earning quality. Contemporary Accounting Research 25: 109–47. [Google Scholar] [CrossRef]

- Freeman, R. E. 1984. Strategic Management: A Stakeholder Approach. New York: Cambridge University Press. [Google Scholar]

- Friede, Gunnar, Timo Busch, and Alexander Bassen. 2015. ESG and financial performance: Aggregated evidence for more than 2000 empirical studies. Journal of Sustainable Finance & Investment 5: 210–33. [Google Scholar]

- Gallego-Alvarez, Isabel, and Lilane Christina Segura. 2015. Greenhouse gas emissions variation and corporate performance in international companies. International Journal of Global Warming 8: 555–82. [Google Scholar] [CrossRef]

- Gandhi, Sumeet, Sachin Kumar Mangla, Pradip Kumar, and Dinesh Kumar. 2015. Valuating factors in implementation of successful green supply chain management using DEMATEL: A case study. International Strategic Management Review 3: 96–106. [Google Scholar] [CrossRef] [Green Version]

- Garefalakis, Alexandros, and Augustinos Dimitras. 2020. Looking back and forging ahead: The weighing of ESG factors. Annals of Operations Research 294: 151–89. [Google Scholar] [CrossRef]

- Ghassim, Babak, and Marcel Boger. 2019. Linking stakeholder engagement to profitability through sustainability-oriented innovation: A quantitative study of the minerals industry. Journal of Cleaner Production 224: 905–19. [Google Scholar] [CrossRef]

- Goepel, Klaus D. 2013. Implementing the Analytic Hierarchy Process as a standard method for multi-criteria decision making in corporate enterprises—A new AHP Excel template with multiple inputs. Paper presented at International Symposium on the Analytic Hierarchy Process, Kuala Lumpur, Malaysia, June 23–26. [Google Scholar]

- Hart, Stuart L., and Gautam Ahuja. 1996. Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Business Strategy and the Environment 5: 30–37. [Google Scholar] [CrossRef]

- Hazelton, J., and S. Perkiss. 2018. How Useful are CSR Reports for Investors? In Research Handbook of Finance and Sustainability, 1st ed. Edited by Boubaker Sabri, Cumming Douglas and Duc Khuong Nguyen. Cheltenham: Edward Elgar Publishing, Inc., pp. 93–109. [Google Scholar]

- Ho, William, and Xin Ma. 2018. The state-of-the-art integrations and applications of the Analytic Hierarchy Process. European Journal of Operational Research 267: 399–414. [Google Scholar] [CrossRef]

- Hoepner, Andreas G. F., Ioannis Oikonomou, Zacharias Sautner, Laura T. Starks, and Xiao Y. Zhou. 2019. ESG Shareholder Engagement and Downside Risk (Unpublished Working Paper). Available online: https://www.researchgate.net/profile/Xiaoyan-Zhou-7/publication/318002428_ESG_Shareholder_Engagement_and_Downside_Risk/links/5e6769ce299bf1744f6f12f6/ESG-Shareholder-Engagement-and-Downside-Risk.pdf (accessed on 20 June 2021).

- Ilhan, Emirhan, Zacharias Sautner, and Grigory Vilkov. 2021. Carbon tail risk. The Review of Financial Studies 34: 1540–71. [Google Scholar] [CrossRef]

- Jang, Jae Young, and Erdal Atukeren. 2019. Sustainable local currency debt: An analysis of foreigners’ Korea treasury bonds investments using a LA-VARX model. Sustainability 11: 3603. [Google Scholar] [CrossRef] [Green Version]

- Jang, Jae Young, and Min Jae Park. 2019. A study on global investors’ criteria for investment in the local currency bond markets using AHP Methods: The case of the Republic of Korea. Risks 7: 101. [Google Scholar] [CrossRef] [Green Version]

- Jo, Hoje, and Haejung Na. 2012. Does CSR reduce firm risk? Evidence from controversial industry sector. Journal of Business Ethics 110: 441–56. [Google Scholar] [CrossRef]

- Jost, Lou. 2006. Entropy and diversity. OIKOS 113: 363–75. [Google Scholar] [CrossRef]

- KCGS. 2012. CGS Report. Available online: http://www.cgs.or.kr/CGSDownload/eBook/REP/R002021002.pdf (accessed on 16 June 2021).

- Khan, Mozaffar, George Serafeim, and Aaron Yoon. 2017. Corporate sustainability: First evidence on materiality. The Accounting Review 91: 1697–724. [Google Scholar] [CrossRef] [Green Version]

- Kil, Sung-Ho, Dong Kun Lee, Jun-Hyun Kim, Ming-Han Li, and Galen Newman. 2016. Utilizing the Analytic Hierarchy Process to establish weighted values for evaluating the stability of slope revegetation based on hydroseeding applications in South Korea. Sustainability 8: 58. [Google Scholar] [CrossRef] [Green Version]

- Kim, Dae Young, and Sangho Byun. 2016. Influence of corporation-CEO reputation gap on purchase intention, growth prospect, investment attraction, and corporate preference. Asia-Pacific Journal of Business Venturing and Entrepreneurship 11: 131–14. [Google Scholar]

- Kim, Se Jik. 2016. The fall of growth and structural reform in Korea. Seoul Journal of Economics 55: 3–27. [Google Scholar]

- Kim, Sun-Hwa, and Yong-Ki Jung. 2012. The monitoring power of foreign ownership on corporate social responsibility: Evidence from Korea. Korean Accounting Review 37: 1–62. [Google Scholar]

- Kim, Sun-Hwa, and Yong-Ki Jung. 2018. The effects of CSR activities on management risk and information asymmetry, and the differentiated recognition of debtholders: A comparison between large and small-medium companies. Study on Accounting, Taxation & Auditing 60: 237–74. [Google Scholar]

- Kim, Tae Wan, and Jin Woo Kim. 2018. Differentiative market response of management performance based on the corporate social responsibility activity. Tax Accounting Research 55: 95–114. [Google Scholar]

- Kim, Woo Cheol, and Ji Won Park. 2017. Examining structural relationships between work engagement, organizational procedural justice, knowledge sharing, and innovative work behavior for sustainable organizations. Sustainability 9: 205. [Google Scholar] [CrossRef] [Green Version]

- Lee, Daren, Robert Faff, and Saphira Rekker. 2013. Do high and low-ranked sustainability stocks perform differently? International Journal of Accounting and Information Management 21: 116–32. [Google Scholar] [CrossRef]

- Lee, Yun Sang. 2018. A study on the relationship between corporate social responsibility detailed index and tax avoidance. Tax Accounting Research 57: 55–73. [Google Scholar]

- Matos, Pedro Verga, Victor Barros, and Joaquim Miranda Sarmento. 2020. Does ESG affect stability of dividend policies in Europe? Sustainability 12: 8840. [Google Scholar]

- Menguc, Bulent, and Lucie K. Oanne. 2005. Challenges of the “green imperative”: A natural resource-based approach to the environmental orientation-business performance relationship. Journal of Business Research 58: 430–38. [Google Scholar] [CrossRef]

- Ministry of Economy and Finance. 2021. Korea Treasury Bonds 2020. Available online: https://www.moef.go.kr/com/synap/synapView.do?atchFileId=ATCH_000000000017001&fileSn=3 (accessed on 25 August 2021).

- Moody’s. 2021. ESG Issuer Profile and Credit Impact Scores Expanded across More Enterprise, Government Sectors. Available online: https://www.moodys.com/credit-ratings/korea-government-of-credit-rating-440230 (accessed on 25 August 2021).

- MSCI. 2020. MSCI ESG Ratings Methodology. Available online: https://www.msci.com/documents/1296102/21901542/MSCI+ESG+Ratings+Methodology+-+Exec+Summary+Nov+2020.pdf (accessed on 10 June 2021).

- Nagy, Zoltan, Linda-Eling Lee, and Guido Giese. 2020. ESG Ratings: How the Weighing Scheme Affected Performance. Available online: https://www.msci.com/www/blog-posts/esg-ratings-how-the-weighting/01944696204 (accessed on 24 July 2021).

- Nam, Vu Hoang, Minh Mgoc Nguyen, Duong Anh Nguyen, and Hiep Ngoc Luu. 2020. The impact of corruption on the performance of newly established enterprises: Empirical evidence from a transition economy. Borsa Istanbul Review 20: 383–95. [Google Scholar] [CrossRef]

- National Pension Service. 2021. 2021 ESG Plus Forum: ‘Korean-style ESG Investing (23 May 2021). Available online: http://www.koreatimes.co.kr/www/biz/2021/06/175_309245.html (accessed on 25 June 2021).

- Noland, Marcus, Tyler Moran, and Barbara R. Kotzchwar. 2016. Is gender diversity profitable? Peterson Institute for International Economics Working Paper. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2729348 (accessed on 12 June 2021).

- OECD. 2020. OECD Business and Finance Outlook 2020: Sustainable and Resilient Finance. Available online: https://0-www-oecd--ilibrary-org.brum.beds.ac.uk/sites/eb61fd29-en/1/3/1/index.html?itemId=/content/publication/eb61fd29-en&_csp_=648f628b9c3583d125efc89498a6a043&itemIGO=oecd&itemContentType=book#section-d1e1088 (accessed on 1 June 2021).

- Park, Kwang-Hun, and Ju-Seong Lee. 2017. The effect of corporate philanthropy on accounting transparency: Focusing on accrual quality and real activities earnings management. Review of Accounting and Policy Studies 22: 49–80. [Google Scholar]

- Park, Kwong O. 2020. How CSV and CSR affect organizational performance: A productive behavior perspective. International Journal of Environmental Research and Public Health 17: 2556. [Google Scholar] [CrossRef] [Green Version]

- Park, Mi Young. 2017. The effects of corporate governance on corporate social responsibility in China. Korean Computers and Accounting Review 15: 77–99. [Google Scholar]

- Pineiro-Chousa, Juan, Marcos Vizcaíno-González, María Ángeles López-Cabarcos, and Noelia Romero-Castro. 2017. Managing reputational risk through environmental management and reporting: An options theory approach. Sustainability 9: 376. [Google Scholar] [CrossRef] [Green Version]

- Porter, Michael, Serafeim George, and Kramer Mark. 2019. Where ESG Fails. Institutional Investor. Available online: https://www.institutionalinvestor.com/article/b1hm5ghqtxj9s7/Where-ESG-Fails (accessed on 10 June 2021).

- Refinitiv. 2021. ESG Scores Methodology. Available online: https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/refinitiv-esg-scores-methodology.pdf (accessed on 10 June 2021).

- Rehman, Hania, Muhammad Ramzo, Muhammad Zia Ul Haq, Jinsoo Hwang, and Kyoung-Bae Kim. 2021. Risk Management in Corporate Governance Framework. Sustainability 13: 5015. [Google Scholar] [CrossRef]

- S&P Global. 2021. CSA Companion 2021: Corporate Sustainability Assessment. Available online: https://portal.csa.spglobal.com/survey/documents/CSA_Companion.pdf (accessed on 10 June 2021).

- Saaty, Thomas L. 2003. Decision-making with the AHP: Why is the principal eigenvector necessary. European Journal of Operational Research 145: 85–91. [Google Scholar] [CrossRef]

- Saaty, Thomas L., Paul C. Rogers, and Ricardo Pell. 1980. Portfolio selection through hierarchies. Journal of Portfolio Management 6: 16–21. [Google Scholar] [CrossRef]

- SASB. 2020. SASB Materiality Map. Available online: https://materiality.sasb.org/ (accessed on 21 June 2021).

- Sherwood, Matthew W., and Julia Pollard. 2017. The risk-adjusted return potential of integrating ESG strategies into emerging market equities. Journal of Sustainable Finance & Investment 8: 26–44. [Google Scholar]

- Son, Young Hoa. 2012. Prohibit abuse of dominant market position. Inha Law Review 15: 783–818. [Google Scholar]

- Song, Chanhoo, and Seung Hun Han. 2017. Stock market reaction to corporate crime: Evidence from South Korea. Journal of Business Ethics 143: 323–51. [Google Scholar] [CrossRef]

- SustainAbility. 2020. Rate the Raters 2020: Investor Survey and Interview Results. Available online: https://www.sustainability.com/thinking/rate-the-raters-2020/ (accessed on 19 June 2021).

- Swanson, Diane L. 1999. Toward an integrative theory of business and society: A research strategy for corporate social performance. Academy of Management Review 24: 506–21. [Google Scholar] [CrossRef]

- Thakur, Bhanu Pratap Singh, M. Kannadhasan, Parikshit Charan, and C. P. Gupta. 2019. Corruption and firm value: Evidence from emerging market economies. Emerging Markets Finance and Trade 4: 1182–97. [Google Scholar] [CrossRef]

- UNPRI. 2021. PRI Update Q1 2021. Available online: https://www.unpri.org/download?ac=12423 (accessed on 4 July 2021).

- Van Duuren, Emiel, Auke Plantinga, and Bert Scholtens. 2016. ESG integration and the investment management process: Fundamental investment reinvented. Journal of Business Ethics 138: 525–33. [Google Scholar] [CrossRef] [Green Version]

- Weber Shandwick. 2018. The CEO Reputation Premium: Gaining Advantage in the Engagement Era. Available online: https://www.webershandwick.com/wp-content/uploads/2018/04/ceo-reputation-premium-infographic.pdf (accessed on 5 July 2021).

- Welling, John. 2020. Is South Korea Crowding Your Emerging Markets Allocation? Available online: https://www.indexologyblog.com/2020/11/23/is-south-korea-crowding-your-emerging-markets-allocation/ (accessed on 24 July 2021).

- Woo, Min-Chul, and Myoung-Ae Kim. 2015. Trading pattern of institutional investors in Korean stock markets: Analysis by institution type. Journal of Industrial Economics and Business 28: 1109–34. [Google Scholar]

- World Economic Forum. 2020. Measuring Stakeholder Capitalism Towards Common Metrics and Consistent Reporting of Sustainable Value Creation. Available online: https://www.weforum.org/reports/measuring-stakeholder-capitalism-towards-common-metrics-and-consistent-reporting-of-sustainable-value-creation (accessed on 10 June 2021).

- Yang, Hyung Mo, and Tae Hwa Yoon. 2015. A study on investors’ evaluation of corporate social responsibility—Using a verification model for value relevance of accounting information. Accounting Information Review 33: 25–52. [Google Scholar]

- Yu, Seungwon. 2013. CEO’s political independence, board chair separation, executive’s expertise, and performance in state-owned enterprises. KDI Economy Policy 35: 1–39. [Google Scholar]

- Zerfass, Ansgar, Joachim Schwalbach, Gunter Bentele, and Muschda Sherzada. 2014. Corporate communications from the top and from the center: Comparing experiences and expectations of CEOs and communicators. International Journal of Strategic Communication 8: 61–78. [Google Scholar] [CrossRef] [Green Version]

| Stakeholder Capitalism Matric | SASB | Refinitiv | MSCI | S&P Global | |

|---|---|---|---|---|---|

| E | - Freshwater availability - Climate change - Air pollution - Nature loss - Innovation of better products and services | - Energy management - Water management - GHG emissions - Climate change - Waste and hazardous materials - Product design and lifecycle management - Ecological damage - Material sourcing | - Resource use - Emission - Innovative environmental strategy - Controversies on environmental issues | - Natural resources depletion - Climate change - Pollution and waste - Environmental strategy | - Operational eco-efficiency - Climate strategy - Environmental reporting - Environmental policy and management system |

| S | - Dignity and equality - Health and well-being - Skills for the future - Employment and wealth generation - Community and social support | - Human rights and community relations - Human capital - Product quality, safety selling practices, and product labeling - Customer privacy - Data security - Customer welfare - Access and affordability | - Human rights - Community - Workforce - Product responsibility - Controversies on social issues | - Product, human capital - Social opportunities - Satisfaction of customer, employee, supplier, and other stakeholders | - Human rights - Corporate citizenship and philanthropy - Labor practice indicator - Talent attraction and retention - Customer relationship management - Information security and system availability - Policy influence - Social reporting |

| G | - Ethical behavior - Governing purpose - Risk and opportunity oversight - Stakeholder engagement - Quality of governance body | - Business ethics - Business model resilience - Management of the legal and regulatory environment - Supply chain management - Risk (critical incident and systemic) management | - Management structure and compensation - ESG strategy and reporting - Shareholder rights - Controversies on governance issues | - Corporate behavior - Corporate governance | - Codes of business conduct - Tax strategy - Supply chain management - Risk and crisis management - Corporate governance - Materiality |

| Criteria | Sub-Criteria | Description | Measurement |

|---|---|---|---|

| E | Resource Depletion | Managing the amount of energy and other consumable resources | Energy/water consumption |

| GHG (Greenhouse Gas) Emission | Managing and reducing the level of GHG emissions to meet the target for the Paris Agreement | GHG emission and climate risk targets and assessments, product carbon footprint | |

| Pollution and Waste | Managing the level of pollution and waste | Waste disposal, water/air/land pollution, single-use plastic | |

| Eco-Product/Process Strategy | Strategic efforts to reduce the corporate’s environmental impacts, i.e., produce more using less resource | R&D expenditure | |

| Nature Loss | Levels of potential damage to the nature and efforts for ecological protection | Land use and ecological sensitivity, biodiversity | |

| S | Human Rights | Respecting and securing human rights in the business practices | Discrimination, harassment, diversity ratio, freedom of association, child/forced/compulsory labor |

| Community Relations | Efforts to build solid reputation and relationship with local communities | Local investment, community investment | |

| Human Resources Management | Ensuring the dignity, equality, health, and benefits of employees | Talent attraction and retention Providing health, safety and training opportunities | |

| Customer Satisfaction | Provide products and services that satisfy customers | Privacy, data security, product safety and quality, financial product safety | |

| Partnership with Subcontractor | Promoting satisfaction, trust, and inclusive growth with subcontractor(s) | Contract satisfaction, trusting relationship | |

| Social and Political Contribution | As a responsible citizen, making effort to build greater overall value to the society | Contributions, philanthropy, infrastructure investment, employment, total tax paid | |

| G | Ethical Behavior | Monitoring and management to comply with applicable laws and regulations | Anti-competitive practices, anti-corruption and bribery policy |

| Risks and Opportunities Management | Identification and management of strategic risks and opportunities regarding long-term value creation | Systemic risk management, critical incident risk management, business model resilience | |

| Shareholders’ Rights | Upholding shareholders’ concerns and voices in company strategy and management | Investment return, voting rights, information disclosure | |

| Corporate Governance | Structure of management system that reflects the direction and controlment of the company. | Gender ratio, experiences of the board members | |

| CEO Reputation | Impact of CEO and top management personality and qualifications have on the corporate image and value | CEO image, management controversy |

| Type of Institution | Frequency | % | Main Business | Frequency | % | Service Period | Frequency | % |

|---|---|---|---|---|---|---|---|---|

| Asset Management | 11 | 20 | Bonds | 26 | 48 | 15–25 years | 48 | 89 |

| Pension Fund | 13 | 24 | Stocks | 12 | 22 | Over 25 years | 6 | 11 |

| Insurance Company | 10 | 19 | Alternatives | 16 | 30 | |||

| Securities Company | 13 | 24 | ||||||

| Bank | 7 | 13 | ||||||

| Total | 54 | 100 | Total | 54 | 100 | Total | 54 | 100 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Park, S.R.; Jang, J.Y. The Impact of ESG Management on Investment Decision: Institutional Investors’ Perceptions of Country-Specific ESG Criteria. Int. J. Financial Stud. 2021, 9, 48. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs9030048

Park SR, Jang JY. The Impact of ESG Management on Investment Decision: Institutional Investors’ Perceptions of Country-Specific ESG Criteria. International Journal of Financial Studies. 2021; 9(3):48. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs9030048

Chicago/Turabian StylePark, So Ra, and Jae Young Jang. 2021. "The Impact of ESG Management on Investment Decision: Institutional Investors’ Perceptions of Country-Specific ESG Criteria" International Journal of Financial Studies 9, no. 3: 48. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs9030048