Challenges and Trends of Financial Technology (Fintech): A Systematic Literature Review

1

Faculty of Computer Science, Universitas Indonesia, Depok 16424, Indonesia

2

Faculty of Engineering and Computer Science, Universitas Teknokrat Indonesia, Lampung 35142, Indonesia

*

Author to whom correspondence should be addressed.

Information 2020, 11(12), 590; https://0-doi-org.brum.beds.ac.uk/10.3390/info11120590

Submission received: 16 October 2020

/

Revised: 17 December 2020

/

Accepted: 17 December 2020

/

Published: 21 December 2020

(This article belongs to the Special Issue Digitalized Economy, Society and Information Management)

Abstract

:Digital transformation creates challenges in all industries and business sectors. The development of digital transformation has also clearly triggered the emergence of fintech (financial technology) initiatives, which are recognized as some of the most important innovations in the financial industry. These initiatives are developing rapidly, driven in part by the sharing economy, regulations, and information technology. However, research in the field of fintech remains in its infancy. Fintech offers several services, such as funding, payment (including electronic wallets), e-aggregators, e-trading, and e-insurance, and cryptocurrencies such as Bitcoin. This provides an opportunity to more closely examine fintech’s research challenges and trends. This study aims to (1) determine the state of the art of financial technology research; (2) identify gaps in the financial technology research field; and (3) identify challenges and trends for future research potential. The novel proposal in this study includes theoretical contributions regarding financial technology. Using the systematic literature review approach of Kitchenham, in addition to thematic analysis, meta-analysis and observation to validate the quality of literature and analysis, the results of this study provide a theoretical basis fintech research from an information systems perspective, including the formulation of fintech technology concepts and their development.

1. Introduction

Fintech is a new financial industry that applies technology to improve financial activities [1]. Moreover, according to Leong and Sung (2018), fintech can also be considered as “any innovative ideas that improve financial service processes by proposing technology solutions according to different business situations” [2]. Advances in e-finance and mobile technology for financial companies, which drove the innovation of fintech, emerged after the global financial crisis in 2008. This development was characterized by integration in e-finance innovation, Internet technology, social networking services, social media, artificial intelligence, and big analytic data [3]. This challenges many traditional financial institutions, such as banks, to develop their business models in a more practical direction [4]. In addition, start-ups saw this as an opportunity to enter the financial services industry [5].

Two types of start-ups are relevant to this research, e-commerce and financial technology (fintech). Fintech is one of the most important innovations in the financial services industry and is driven by economic sharing, regulation, policy, and information technology [3]. Like that of banks, the business model of fintech also focuses on payment and loan services. In addition, it includes personal financial consulting services, crowdfunding, virtual currencies, and security (e.g., cyber security) [6].

Zavolokina et al. examined how fintech is perceived. The term “fintech” can be interpreted as the application of information technology in the fields of finance, financial innovation, and digital innovation, in addition to start-ups (the financial service industry outside of banks) [7]. There are six fintech business models: insurance services, crowdfunding, payment, lending, wealth management, and capital markets [3]. Clearly, the greater the level of development of financial technology services, the greater the challenges for businesses. Online loan services have caused controversy in communities, including moral hazard, loan defaults, and information asymmetry [8]. The case of money laundering via Bitcoin [8] has also been widely discussed. For this reason, it is important for regulators to formulate how this innovation should be addressed in the rules. Regulators encourage innovation in the financial sector and apply the principles of consumer protection and risk management to obtain safe and appropriate financial services [4].

The history of technological innovation in the financial sector began with the emergence of checks as a means of payment (1945). Subsequently, the Bank of America produced the first credit card (1958), and ATMs appeared to help process financial transactions in 1967, followed by the issuance of a debit card as a transaction tool. In the 1990s, supported by the advancement of the Internet, Internet banking was launched. In the 2000s, fintech developments of mobile payments and crowdfunding were introduced. This shows that fintech is a fast-growing industry, and it is thus necessary to review previous research to capture the evolution of financial services [9].

To increase the understanding of academics, industry players, and regulators about the extent to which the fintech industry is developing, it is necessary to conduct a literature review. This study aims to: (1) determine state of the art of financial technology; (2) identify gaps in the financial technology research; and (3) identify challenges and trends for future research potential. A systematic literature review is used to accomplish these objectives [10].

The need remains to discuss the initial problems raised by the development of fintech, such as moral hazard, loan defaults, and information asymmetry. Kitchenham’s systematic literature review (SLR) method is required for the metadata process. From the journal work process and library extraction, analysis and grouping can be undertaken. Research related to using the SLR method was conducted by Suryono et al. to find the state of the art of peer-to-peer (P2P) lending [8]. The results of this analysis were validated by experts. Finally, this research provides an overview of the challenges, problems, and trends in the fintech sector.

2. Methodology

In developing the initial issue to investigate, we began by conducting an SLR. Related to the SLR is the concept of a literature study, which is widely adopted for research in the field of information systems and is useful for determining the state of the art of a research topic.

2.1. Research Question

The research question in this article is:

- RQ1. “What are the challenges and trends of fintech research?”

Regarding RQ1, we tried to identify the need for a literature review. After identifying articles that discuss fintech, we obtained fintech articles published in early 2014. Therefore, the search for publications was limited to the period 2014 to 2019. In general, the term fintech was undefined at this time. Several articles mention digital financial innovations, in addition to electronic financial payments. For this reason, we attempted to review these innovations in the financial services sector.

2.2. Search Process

First, we determined the journal database portals or scientific publications to be used. The quality of the articles used as references is influenced by the selected journal databases. The databases used in this study included SCOPUS, ACM, ScienceDirect, and IEEE Xplore. Second, we formulated a protocol review to formulate research questions by classifying keywords according to the population, intervention, comparison, outcomes, and context (PICOC) strategy. Then, we identified populations such as "fintech and financial technology" in the context of "trends, problems, adoption, innovation and challenges". We released the intervention section to obtain information on various fintech focuses, such as types of fintech payments, funding, and investment. The keywords used for searching literature reviews were as follows: (fintech OR “financial technology” AND (trends OR problems OR adoptions OR innovations OR challenges)).

2.3. Implementation

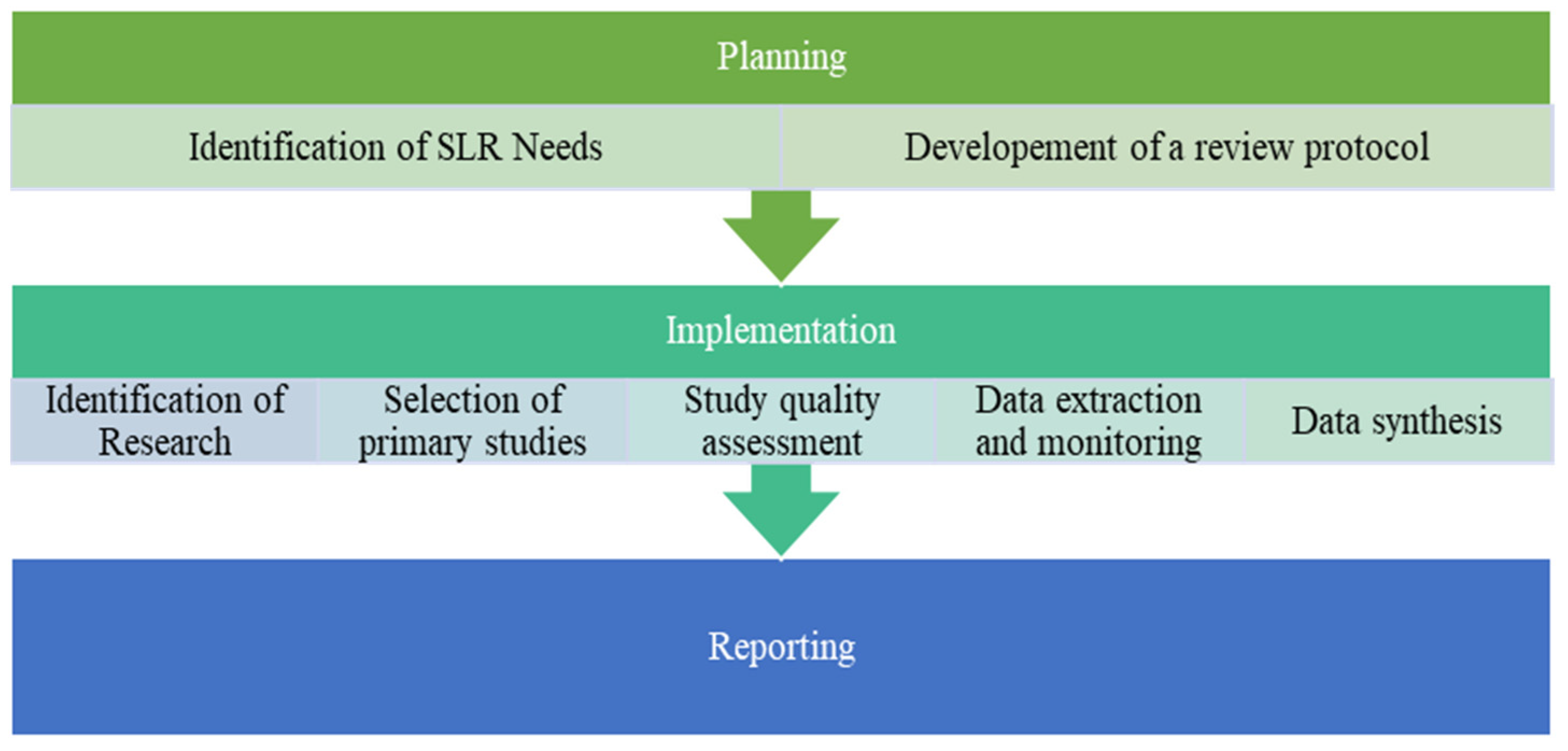

To minimize the subjectivity of article selection, inclusion and exclusion criteria were determined, such as choosing journal articles and papers in English and excluding other languages such as Mandarin and Spanish. Then, articles were selected that matched the research question and duplicate articles were removed. This research used Mendeley’s software to organize articles. The methodology is shown in Figure 1.

After the final documents were obtained, data extraction and data synthesis were carried out. Figure 2 shows the document selection process, starting from the title and abstract selection, then the full text selection, which was synthesized using thematic analysis and meta-analysis.

3. Results

This section discusses the results of the analysis and synthesis of literature on fintech. The discussion includes history and terminology, thematic analysis of methodology, and content analysis of fintech’s business processes.

3.1. Background and Terminology

Fintech is a relatively modern concept. The biggest innovation in the financial industry was the creation of the ATM [11]. Previously, since 1838, financial transactions were carried out using telegraphs. The banking industry has developed information technology to improve its processes [12].

The development of the Internet in the United States and Europe marked technological advancements in various sectors. In the early 1990s, analog technology was transformed into digital technology for the financial services industry. Information communication technology (ICT) investment is relevant to the financial services industry. More recently, in 2009, Satoshi Nakamoto introduced a digital currency called Bitcoin. Bitcoin is a new currency or form of electronic money [13,14].

In their systematic literature review, Zavolokina et al. stated that fintech was not only the application of information technology in finance. Some literature argues that fintech can also be interpreted as start-ups, services, technologies, companies, digitalization, industry, new generations, chance, products, and threats [7]. The term fintech (sometimes Fin-tech or FinTech) is a new term that refers to modern relationships and, in particular, technologies related to the Internet (for example, cloud computing, mobile Internet) and business activities in the financial services industry (for example, lending money and banking transactions). Due to automatic processing and the availability of ICT, fintech represents a disruption to the financial sector [15]. Fintech has a variety of business models that consider security, speed, and innovation in the financial services sector [16]. The term fintech is also defined as a financial service and solution based on technological advancements [17]. A simple definition of fintech is an industry consisting of organizations that use sophisticated financial technology to trigger fast financial services without long procedures [18]. Fintech includes start-ups, the use of ICT for financial services, and start-up industry collaboration with traditional financial services.

3.2. Thematic Analysis of the Articles Selected

In this section, the results of the thematic analysis are explained. We summarize the areas of fintech that are discussed, per year, the general topics and business models of fintech, the main methodologies used in each study, and classification by country.

3.2.1. Publication Per Year

We selected articles from the past five years (2014–2019). From a comparison of the articles published each year, research on the topic of fintech (in general) was the most widely discussed (41 articles). Furthermore, research on the topic of payments began in 2014 with a total of 23 articles. In addition, research on the topic of P2P loans began to appear in 2017 with a total of 20 articles. In 2018, there were 54 articles on fintech. This included topics such as payments, risk management and investment, market aggregators, crowdfunding, P2P lending, and blockchain technology. This can be seen in Table 1.

3.2.2. Classification of Articles by Fintech Business Model

This section explains the theme of fintech’s views in terms of general issues, such as adoption, problems, trends, challenges, and innovations. This grouping is seen from the titles, keywords, and article texts. See Table 2.

3.2.3. Classification of Articles by (Main) Methodology

The collection of articles was also analyzed regarding the main methodologies they applied. It was found that the majority of articles (33) applied an empirical methodology, including using archival and survey data. Furthermore, qualitative methodologies, such as case study research and observations of certain phenomena, were used in 27 articles. In addition, adoption model research was used to build a conceptual model in a total of 18 articles. Experimental research was used in 12 articles. Literature review studies from various fields of fintech were conducted in eight articles. In addition, theoretical, scientific, and simulative research was also found. Table 3 classifies the articles by methodology.

3.2.4. Classification of Articles by Publications

Six journal articles were published in Electronic Commerce Research and Applications, three articles in Electronic Markets, three articles in European Business Organization Law Review, three articles in Investment Management and Financial Innovations, three articles in the Journal of Economics and Business, two articles in the Computer Law and Security Review, two articles in Industrial Management and Data Systems, two articles in the International Journal of Engineering and Technology (UAE), and two articles in the Journal of Retailing and Consumer Services. Seven proceeding articles were obtained from the ACM International Conference Proceeding Series, three articles from Procedia Computer Science, and four articles from the IOP Conference Series. The grouping of papers based on publications can be seen in Table 4.

3.2.5. Classification of Articles by Locations

Articles were grouped by location according to author location and case study location. The purpose of this grouping is to see trends and topics of interest in a location. We divided the locations based on continents, i.e., Asia, Europe, America, Africa, and Australia, in addition to Global (no specific area). From the data we obtained, the Asian Continent was ranked first in fintech research. This comprised the research of several countries, such as China, which produced 20 studies; Indonesia, which produced 19 studies; and Korea, which produced nine studies; in addition to several other countries, such as Taiwan, Malaysia, India, Japan, Singapore, Thailand, and Brunei Darussalam. Furthermore, the European continent occupied second position with representatives from Germany, with 10 studies; England, with eight studies; and several other countries, such as France, Switzerland, Russia, Finland, and the Netherlands. Furthermore, the American continent occupied third position with representatives from the USA producing 12 studies, Spain producing four studies, and other countries, such as Brazil and Canada. Finally, the continent of Australia produced a total of 10 studies.

The case studies from each study cannot be specifically identified. A total of 37 studies involved case studies. However, the largest number of case studies was produced by the Asian area, with 49 studies, including Indonesia, which was the most researched country with a total of 19 studies, and China with 17 studies. In addition to these two countries, countries including Malaysia, Taiwan, Japan, Korea, Thailand, and Singapore produced studies. Furthermore, the European area, which does not specify which country, produced 10 case studies in England, France, and Ukraine. Furthermore, the American area used the US as a case study with a total of 10 studies, and several regions such as Brazil and Canada. Finally, the continent of Africa undertakes little research on fintech, with Kenya producing one study.

3.3. Meta-analysis of the Articles Selected

We conducted a meta-analysis to further explore any issues relating to the fintech topic. Using NVIVO software, we performed selective coding, adapting it to the needs of the research question. As discussed in the methodology section of this review, this article explores the research challenges and trends of the topic of fintech. Table 5 describes the challenges, and Table 6 describes the research trends.

4. Discussions and Recommendations

4.1. Discussions

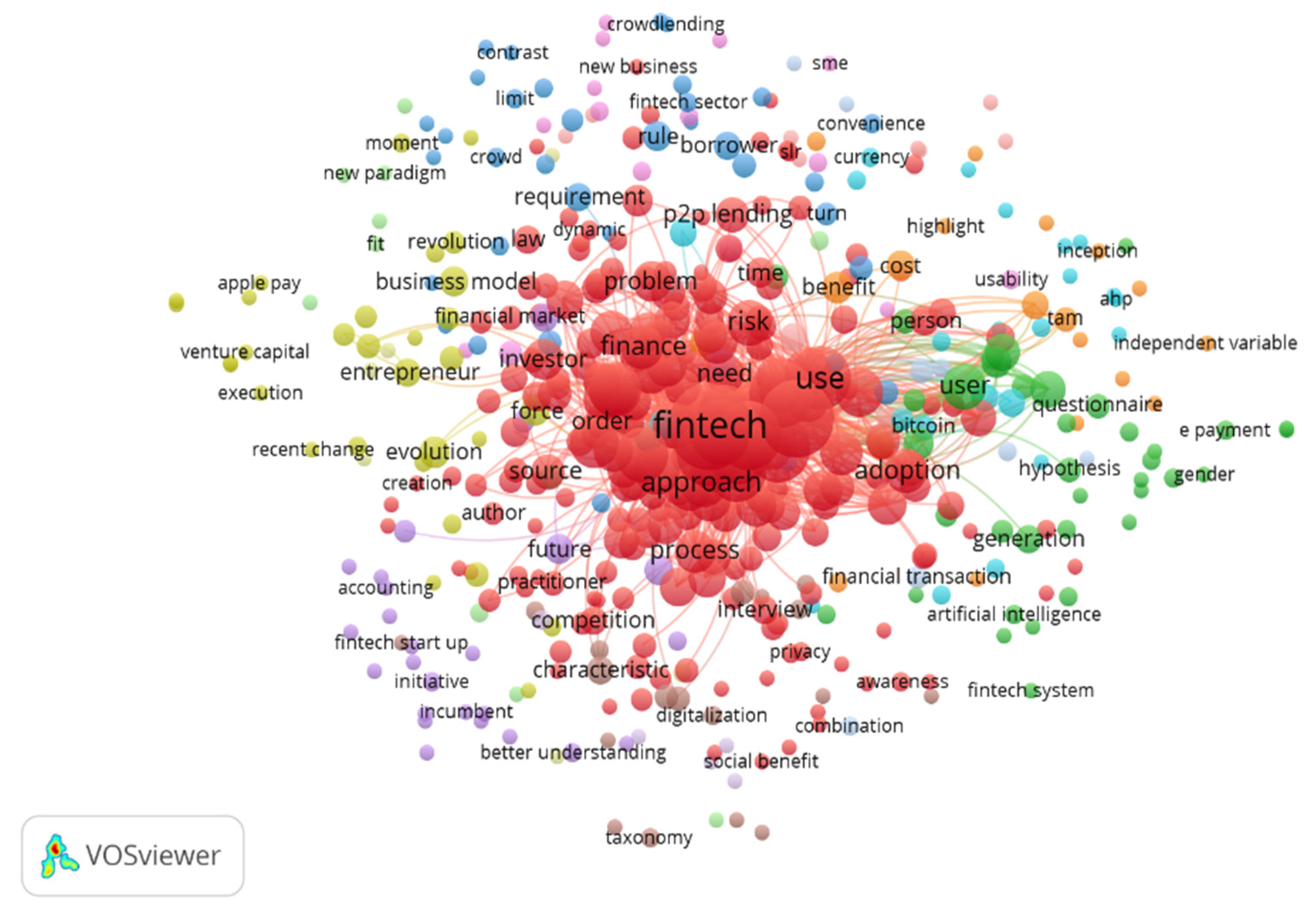

We performed a keyword mapping of all the articles. Using the VOS Viewer application, we found keywords that often appear, such as fintech, use, approach, process, finance, risk, need, problem, adoption, and investor. See Figure 3.

4.1.1. Research on Fintech (In General)

Fintech research generally begins with the evaluation of fintech (including machines and financial instruments) and the social and ethical consequences of the use of robots [47]. In addition, fintech is considered to modulate financial technology because it can provide added value to financial services [21]. Due to the evolution of technology and its application in the design and delivery of financial products, the monitoring, management, and control of financial services must pursue compliance and reporting for implementation in achieving effective objectives in the financial sector [31]. A large amount of research addresses the adoption of fintech in terms of technology and user perceptions [19,20,21,22,23,24,25,26]. The historical view of fintech, ecosystems, business models, and types of fintech investments was found to be a preliminary topic of study [3,15,18]. An important issue in developing fintech is data privacy and data security, hence, studies have been undertaken that propose methods to approach data-based processes, such as strong authentication functions [39]. For this reason, mechanisms for using innovative financial technology need to be refined, and rules relating to the experiences of various countries need to be integrated. Several countries appoint financial service authorities to build regulatory sandboxes as a process of assisting fintech start-ups [52,105]. This is a limited, safe trial space for testing financial technology operators and their products, services, technology, and/or business models. [4,50].

4.1.2. Research on Payment, Clearing, and Settlement

At present, innovations in the fintech sector have had an impact on other fintech business models, such as the payment model. Several innovations have emerged in the form of electronic wallets, electronic money, and payment gateways [64,119]. This has happened because there is a high level of heterogeneity among payment schemes in terms of payment processing, transaction settlement methods, and e-commerce developers who apply numerous payment methods [54,67]. Because of the many payment methods available, adoption research also dominates this topic [53,54,55,56,57,58,59,60,61,62]. The mobile payment system currently operates in a complex and multidimensional network with the same shared infrastructure, and competes to produce and deliver value to customers [73]. Furthermore, studies have been conducted that explain biometrics regarding individual security issues, benefits received, and trust in electronic payments in the context of e-commerce [68]. In addition, due to the use of numerous virtual currencies for online transactions, it is feared that these could endanger the financial system because regulators have difficulty in the supervisory process [116].

4.1.3. Research on Risk Management and Investment

Smartphones are pervasive. At present, many financial planning applications are available on smartphones [80]. Users can determine financial plans based on personal data [79]. This trend started from the discussions of insurance companies [78,85,86], who developed an integrated, knowledge-based model for AI (artificial intelligence), the robo-advisor [76,81,82,83,84], to evaluate equity portfolios and study negative and positive reactions to portfolio risk management [77]. In addition, research on the adoption of mutual fund services has also been discussed [75].

4.1.4. Research on Market Aggregators

Market aggregators are portals that collect various information on financial service options for users. Based on this information, users can compare the best financial products, including credit cards, insurance, or investments. Research has proposed a new model that aims to produce a more accurate and effective reputation score from aggregation methods based on normal distribution [87].

4.1.5. Research on Financing (Crowdfunding and P2P Lending)

Fintech research in the field of financing is divided into crowdfunding and P2P lending research. Despite having different goals, P2P lending and crowdfunding both represent financial marketplaces. This type of platforms is able to bring together those who need funds with those who provide funds as capital or investments [90]. Crowdfunding can be divided into two types, reward-based and equity-based [95,96]. Reward-based crowdfunding entails an individual who contributes to a project or business in the hope of receiving non-financial rewards, such as goods or services, at a later stage [88]. By comparison, equity-based crowdfunding works more like conventional investments in the form of shares [88,89,93]. A crowdfunding campaign is a matter of convincing the audience, especially potential donors, of the ideas and business models offered. However, due to the higher level of individual investor participation in funding new ventures, asymmetric information is generated [92]. Thus, the challenge for future research is to reduce information asymmetry and protect the market by building investor confidence [91]. P2P lending is a financial service that brings lenders and borrowers together on one platform [120]. Suryono et al. examined issues such as information asymmetry, which can make it difficult for investors to make P2P investments, and the determination of the score borrowers need to utilize big data. In addition, moral hazard is also an issue in the development of the P2P lending industry that influences investment decisions. For this reason, regulations and policies continue to be discussed to determine the feasibility of the P2P loan platforms [8]. Therefore, research related to the adoption of P2P loans is still growing [97,98,99]. Studies on government policies continue to be carried out to provide regulations that can be accepted by all stakeholders [4].

4.1.6. Research on Cryptocurrency and Blockchain

A cryptocurrency is any digital currency that is secured by encryption. Examples of some popular cryptocurrencies are Bitcoin, Ethereum, Litecoin, Ripple, Dash, Peercoin, and Dogecoin [116]. “Secure by encryption” means that on the blockchain there is an encryption technique in use. In addition, the blockchain is not limited by the government because this technology is centralized among its users [46]. However, blockchain has vulnerabilities and loopholes that lead to exploits such as operation without regulatory rules [54]. Blockchain technology has four advantages: (1) it is freely accessed by users who agree to join the database; (2) the system gives each user a copy of millions of transactions with visible updates; (3) with complex algorithms, blockchain can be updated for each ledger; and (4) it utilizes network technology [41].

4.2. Recommendations

We have seen that the development of articles about fintech has attracted the attention of researchers. From the results of our meta-analysis, we found many themes that consist of numerous keywords. Thus, we define three main challenges and means to overcome them.

The first is collaboration. The challenge for the future is the development of a practical and systematic framework for fintech [33,34,75]. Several research trends are trying to establish sustainable adoption models, identifying factors that influence a person to use fintech services [53]. However, it is still unclear how consumers will continue to use these services. Moreover, the identification of these factors is not the only way to look at adoption rates. Public knowledge about financial literacy and support from stakeholders can support the running of the Fintech industry. This is an important role in the collaboration of all stakeholders [108]. Fintech should no longer be considered a disruptive business. Good relationships are required between fellow financial service industries, such as banks [113], and good relationships between fintech and regulators significantly affect the continuation of fintech practices [109]. Fintech should be able to aid transition of the economy. The government must see the fintech sector as helping with this transition, for example, by providing permission to use electronic money and digital wallets and their implementation as a payment method. These methods clearly make it easier for people to pay in cash via their smartphones. Previously, fintech was the enemy of banking, but now banks can collaborate, and the government is not only a regulator but a player to create a better digital payment ecosystem.

The second is supervision. Loans are one of the many financial service models influenced by fintech, in addition to payments, wealth management, and digital insurance [101]. Although the idea of P2P lending is not new, it is a product of fintech that is developing in countries such as the USA, China, and Indonesia [4]. The hope is that this business model can help SMEs and individuals to obtain loan capital [43]. However, many illegal fintech loans have emerged due to fintech practices that rely on user trust [30]. The approaches taken to fintech regulation vary widely. For example, the US has taken a reactive approach by relying on its rules and regulations, whereas China is taking a proactive step in developing a specific regulatory structure [4]. Product-focused regulatory oversight sometimes does not lead to rapid technological advances. There is an impression that regulations and policies are slow and incompatible with digital transformation.

For this reason, regulators should adopt a “regulatory sandbox” approach. The sandbox allows regulators to work alongside industry players to develop this industry [52]. Fintech operators should be officially registered and members of government-recognized fintech associations. The regulator should implement a direct inspection mechanism by checking the website and application channels. In addition, the government is also advised to have a complaint forum for illegal fintech. A more interesting suggestion is to explore public opinion using social media commentary data, highlight fintech product reviews, and analyze user complaints using text analysis, such as sentiment analysis and opinion mining [119].

The third is protection. New technology trends in the development of fintech cannot be separated from the use of Big Data, artificial intelligence, and machine learning [117]. The effect of using data is complicated and extensive, motivating this industry to pay close attention to its security [54,103]. Security in this context applies not only to technology, but also to data [17]. Fintech must protect consumers from issues regarding data leaks and data access restrictions, including personal data protection. Thus, the existence of strict rules regarding personal data protection is needed [44]. Consumers must also be aware of digital literacy. Digital literacy demands smart technology users [28]. Furthermore, the fintech industry must maintain the quality of fintech software, taking advantage of technology integration to avoid fraud [102].

5. Conclusions

Based on an SLR, 1002 articles were obtained from the ACM, IEEE, SCOPUS, and ScienceDirect databases. The articles were selected by title and abstract. Then, 111 final articles were reviewed using thematic analysis and an annotated bibliography. From the literature review results, fintech research was divided into several business processes: research on payments, risk management and investment, financing (crowdfunding and P2P lending), market aggregators, and cryptocurrency and blockchain technology. The most common research theme was around the adoption of fintech itself.

The meta-analysis results show that the challenges of fintech research begin with determining the fintech framework [33,34,75], including business models and models that are appropriate to the culture of each country [56]. These conditions clearly affect the regulations and policies made by the government [4,15,38,44,50]. This industry requires broad principles in which these rules must be adapted to technological advances [44]. For this reason, several countries have applied the regulatory sandbox concept (incubation for fintech start-ups) [52,103]. Fintech requires a large amount of personal data [103], so monitoring the platform is also beneficial for consumer protection [74]. On this basis, the level of data security and infrastructure must be continuously developed [41,43,102,117]. Currently, fintech is also required to collaborate with traditional financial institutions such as banks [31,35]. This addresses the problem that fintech is a disruptive technology [38]. Banks need fintech as a strategic partner because fintech is considered to be faster in following digital transformation [108].

Then, the research trend continues by developing a conceptual model for fintech adoption [53,75,76]. Various variables, such as perceptions that build attitudes, intention to use, government support, user innovation, brand image, trust, and technology risk, continue to be developed [20,22,25,26,56]. Furthermore, the development of the fintech business model and ecosystem is a widely discussed research topic [3,5,7,15,16,18]. This exploration is supported by the evolution of mobile phones and the Internet [9,19]. Start-ups are starting to receive special attention as development teams’ expertise continues to improve [34,41,60]. Several technologies, such as the robo-advisor [47,76], artificial intelligence [82], big data [78], and a combination of decision support algorithms, are of interest among fintech researchers [80,83,107]. Finally, many opportunities remain that can be obtained from fintech research, including policy, security, monitoring, and even other technological developments.

This research contributes to improving the education about digital finance, in which experiences from fintech practices are an important point of the expansion of digital finance. Practically speaking, the selection of articles, journal databases, and proceedings can provide a reference for research in the field of fintech to obtain quality literature. Other researchers can also see the development of research on fintech topics from year to year. The article classification can help future researchers to review references according to their research needs.

Future studies can use this literature review as an initial foundation to understand fintech. In the field of computer science, future work can address AI, including algorithms, methods, and techniques for fintech systems. For example, payments can develop payment gateways or other easy payment methods and use biometrics as security for transactions [64,65,67]. In P2P lending research, the profile matching method can be used to connect lenders and borrowers [8,104]. Big data techniques can present financial service information, including the development of robo-advisors [76,84]. Further research can also be conducted on blockchain technology and cryptocurrency [118].

In the field of information systems, research can discuss technology adoption, including combining user acceptance models with other behavioral models [19,20,21,22,23,24,25,26]. Collaboration on the fintech business model with other industries is also possible (particularly for funding) [109]. It is also feasible to measure the maturity of the technology used and provide technical and non-technical recommendations [121], use social media data to analyze public opinion on the development of fintech [122,123], and review policies to create regulations that are acceptable to stakeholders and in accordance with the fintech system [121]. It is also an important to include fintech in education [124] to prepare the potential workforce for the market [12].

Author Contributions

Methodology, R.R.S.; Supervision, I.B. and B.P.; Writing—original draft, R.R.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Doctoral Research Grant from the Ministry of Research and Technology /National Research and Innovation Agency of the Republic of Indonesia, contract number NKB-387/UN2.RST/HKP.05.00/2020

Conflicts of Interest

The authors declare no conflict of interest.

References

- Schueffel, P. Taming the beast: A scientific definition of fintech. J. Innov. Manag. 2017, 4, 32–54. [Google Scholar] [CrossRef]

- Leong, K. FinTech (Financial Technology): What is it and how to use technologies to create business value in fintech way? Int. J. Innov. Manag. Technol. 2018, 9, 74–78. [Google Scholar] [CrossRef]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Davis, K.; Maddock, R.; Foo, M. Catching up with Indonesia’s fintech industry. Law Financ. Mark. Rev. 2017, 11, 33–40. [Google Scholar] [CrossRef]

- Gimpel, H.; Rau, D.; Röglinger, M. Understanding FinTech start-ups—A taxonomy of consumer-oriented service offerings. Electron. Mark. 2018, 28, 245–264. [Google Scholar] [CrossRef] [Green Version]

- Stern, C.; Makinen, M.; Qian, Z. FinTechs in China—With a special focus on peer to peer lending. J. Chin. Econ. Foreign Trade Stud. 2017, 10, 215–228. [Google Scholar] [CrossRef] [Green Version]

- Zavolokina, L.; Dolata, M.; Schwabe, G. FinTech—What’s in a name? In Proceedings of the Thirty Seventh International Conference on Information Systems, Dublin, Ireland, 11–14 December 2016; pp. 469–490. [Google Scholar]

- Suryono, R.R.; Purwandari, B.; Budi, I. Peer to peer (P2P) lending problems and potential solutions: A systematic literature review. Procedia Comput. Sci. 2019, 161, 204–214. [Google Scholar] [CrossRef]

- Ashta, A.; Biot-Paquerot, G. FinTech evolution: Strategic value management issues in a fast changing industry. Strateg. Chang. 2018, 27, 301–311. [Google Scholar] [CrossRef]

- Kitchenham, B.; Brereton, P. A systematic review of systematic review process research in software engineering. Inf. Softw. Technol. 2013, 55, 2049–2075. [Google Scholar] [CrossRef]

- Panurach, P. Money in electronic commerce: Digital cash, electronic fund transfer, and eCash. Commun. ACM 1996, 39, 45–50. [Google Scholar] [CrossRef]

- Nicoletti, B. Financial Services and Fintech. In The Future of FinTech; Palgrave Macmillan: London, UK, 2017. [Google Scholar] [CrossRef]

- Chang, T.-C.; Chen, Y.-L. Fintech puzzle: The case of bitcoin. In Proceedings of the PICMET 2018 Portland International Conference on Management of Engineering and Technology: Managing Technological Entrepreneurship: The Engine for Economic Growth, Taichung, Taiwan, 19–23 August 2018. [Google Scholar]

- Eyal, I. Blockchain technology: Transforming libertarian cryptocurrency dreams to finance and banking realities. Computer 2017, 50, 38–49. [Google Scholar] [CrossRef]

- Gomber, P.; Koch, J.A.; Siering, M. Digital finance and FinTech: Current research and future research directions. J. Bus. Econ. 2017, 87, 537–580. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Gai, K.; Qiu, M.; Sun, X. A survey on FinTech. J. Netw. Comput. Appl. 2018, 103, 262–273. [Google Scholar] [CrossRef]

- Puschmann, T. Fintech. Bus. Inf. Syst. Eng. 2017, 59, 69–76. [Google Scholar] [CrossRef]

- Mathur, N.; Karre, S.A.; Mohan, S.L.; Reddy, Y.R. Analysis of fintech mobile app usability for geriatric users in India. In Proceedings of the ACM International Conference on Human-Computer Interaction and User Experience in Indonesia, Yogyakarta, Indonesia, 23–29 March 2018; pp. 1–11. [Google Scholar]

- Fernando, E.; Surjandy; Meyliana; Touriano, D. Development and validation of instruments adoption fintech services in Indonesia (perspective of trust and risk). In Proceedings of the 3rd International Conference on Sustainable Information Engineering and Technology, Malang, Indonesia, 10–12 November 2018; pp. 283–287. [Google Scholar] [CrossRef]

- Nomakuchi, T. A case study on fintech in Japan based on keystone strategy. In Proceedings of the PICMET 2018 Portland International Conference on Management of Engineering and Technology: Managing Technological Entrepreneurship: The Engine for Economic Growth, Honolulu, HI, USA, 19–23 August 2018. [Google Scholar]

- Ryu, H.S. What makes users willing or hesitant to use Fintech? The moderating effect of user type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Iman, N. Assessing the dynamics of fintech in Indonesia. Invest. Manag. Financ. Innov. 2018, 15, 296–303. [Google Scholar] [CrossRef] [Green Version]

- Stewart, H.; Jürjens, J. Data security and consumer trust in FinTech innovation in Germany. Inf. Comput. Secur. 2018, 26, 109–128. [Google Scholar] [CrossRef]

- Huei, C.T.; Cheng, L.S.; Seong, L.C.; Khin, A.A.; Leh Bin, R.L. Preliminary study on consumer attitude towards fintech products and services in Malaysia. Int. J. Eng. Technol. 2018, 7, 166–169. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry 2019, 11, 340. [Google Scholar] [CrossRef] [Green Version]

- Wang, Q.; Gu, L.; Xue, M.; Xu, L.; Niu, W.; Dou, L.; He, L.; Xie, T. FACTS: Automated black-box testing of fintech systems. In Proceedings of the 2018 26th ACM Joint Meeting on European Software Engineering Conference and Symposium on the Foundations of Software Engineering, Lake Buena Vista, FL, USA, 4–9 November 2018; pp. 839–844. [Google Scholar]

- Hatammimi, J.; Krisnawati, A. Financial literacy for entrepreneur in the industry 4.0 era: A conceptual framework in Indonesia. In Proceedings of the ACM International Conference on Information Management and Engineering, Salford, UK, 22–24 September 2018; pp. 183–187. [Google Scholar]

- Jin, T.; Wang, Q. FinExpert: Domain-specific test generation for fintech systems. In Proceedings of the 2019 27th ACM Joint Meeting on European Software Engineering Conference and Symposium on the Foundations of Software Engineering, Tallinn, Estonia, 26–30 August 2019; pp. 853–862. [Google Scholar]

- Pantielieieva, N.; Krynytsia, S.; Khutorna, M.; Potapenko, L. FinTech, transformation of financial intermediation and financial stability. In Proceedings of the 2018 International Scientific-Practical Conference on Problems of Infocommunications Science and Technology, Kharkiv, Ukraine, 9–12 October 2018; pp. 553–559. [Google Scholar]

- Mehrotra, A. Financial inclusion through fintech—A case of lost focus. In Proceedings of the 2019 International Conference on Automation, Computational and Technology Management (ICACTM), London, UK, 24–26 April 2019; pp. 103–107. [Google Scholar]

- Shim, Y.; Shin, D.H. Analyzing China’s fintech industry from the perspective of actor-network theory. Telecommun. Policy 2016, 40, 168–181. [Google Scholar] [CrossRef]

- Eickhoff, M.; Muntermann, J.; Weinrich, T. What Do Fintechs Actually Do? A Taxonomy of Fintech Business Models. In Proceedings of the ICIS 2017: Transforming Society with Digital Innovation, Seoul, Korea, 10–12 December 2017; Volume 22. [Google Scholar]

- Basole, R.C.; Patel, S.S. Transformation through unbundling: Visualizing the global FinTech ecosystem. Serv. Sci. 2018, 10, 379–396. [Google Scholar] [CrossRef]

- Riyanto, A.; Primiana, I.; Yunizar; Azis, Y. Disruptive technology: The phenomenon of FinTech towards conventional banking in Indonesia. Mater. Sci. Eng. 2018, 407. [Google Scholar] [CrossRef]

- Haddad, C.; Hornuf, L. The emergence of the global fintech market: Economic and technological determinants. Small Bus. Econ. 2019, 53, 81–105. [Google Scholar] [CrossRef] [Green Version]

- Anagnostopoulos, I. Fintech and regtech: Impact on regulators and banks. J. Econ. Bus. 2018, 100, 7–25. [Google Scholar] [CrossRef]

- Hung, J.L.; Luo, B. FinTech in Taiwan: A case study of a Bank’s strategic planning for an investment in a FinTech company. Financ. Innov. 2016, 2. [Google Scholar] [CrossRef] [Green Version]

- Kim, K.; Hong, S. The data processing approach for preserving personal data in fintech-driven paradigm. Int. J. Secur. Appl. 2016, 10, 341–350. [Google Scholar] [CrossRef]

- Okamura, T.; Teranishi, I. Enhancing FinTech security with secure multi-party computation technology. NEC Tech. J. 2017, 11, 46–50. [Google Scholar]

- Dimbean-Creta, O. Fintech—Already new fashion in finance, but what about the future? Qual. Access Success 2017, 18, 25–29. [Google Scholar]

- Muthukannan, P.; Tan, F.T.C.; Tan, B.; Leong, C. The Concentric Development of the Financial Technology (Fintech) Ecosystem in Indonesia. In Proceedings of the ICIS 2017: Transforming Society with Digital, Seoul, Korea, 10–12 December 2017. [Google Scholar]

- Sybirianska, Y.; Dyba, M.; Britchenko, I.; Ivashchenko, A.; Vasylyshen, Y.; Polishchuk, Y. Fintech platforms in sme’s financing: Eu experience and ways of their application in Ukraine. Invest. Manag. Financ. Innov. 2018, 15, 83–96. [Google Scholar] [CrossRef] [Green Version]

- Abubakar, L.; Handayani, T. Financial technology: Legal challenges for Indonesia financial sector. In Proceedings of the IOP Conference Series: Earth and Environmental Science, Makassar, Indonesia, 25–26 October 2018; Volume 175. [Google Scholar]

- Xiang, D.; Zhang, Y.; Worthington, A.C. Determinants of the use of fintech finance among Chinese small and medium-sized enterprises. In Proceedings of the TEMS-ISIE 2018 1st Annual International Symposium on Innovation and Entrepreneurship of the IEEE Technology and Engineering Management Society, Beijing, China, 30 March–1 April 2018; pp. 1–10. [Google Scholar]

- Milian, E.Z.; Spinola, M.D.M.; Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Coeckelbergh, M. The invisible robots of global finance: Making visible machines, people and places. SIGCAS Comput. Soc. 2015, 45, 287–289. [Google Scholar] [CrossRef]

- Soloviev, V. Fintech ecosystem in Russia. In Proceedings of the 2018 11th International Conference on Management of Large-Scale System Development, Moscow, Russia, 1–3 October 2018; pp. 1–5. [Google Scholar]

- Drasch, B.J.; Schweizer, A.; Urbach, N. Integrating the ‘Troublemakers’: A taxonomy for cooperation between banks and fintechs. J. Econ. Bus. 2018, 100, 26–42. [Google Scholar] [CrossRef] [Green Version]

- Tsai, C.H.; Peng, K.J. The FinTech revolution and financial regulation: The case of online supply-chain financing. Asian J. Law Soc. 2017, 4, 109–132. [Google Scholar] [CrossRef]

- Wonglimpiyarat, J. FinTech banking industry: A systemic approach. Foresight 2017, 19, 590–603. [Google Scholar] [CrossRef]

- Azarenkova, G.; Shkodina, I.; Samorodov, B.; Babenko, M.; Onishchenko, I. The influence of financial technologies on the global financial system stability. Invest. Manag. Financ. Innov. 2018, 15, 229–238. [Google Scholar] [CrossRef]

- Chang, Y.; Wong, S.F.; Lee, H.; Jeong, S.P. What motivates Chinese consumers to adopt FinTech services: A regulatory focus theory. In Proceedings of the 18th Annual International Conference on Electronic Commerce: E-Commerce in Smart Connected World, Suwon, Korea, 17–19 August 2016; pp. 1–3. [Google Scholar] [CrossRef]

- Bello, G.; Perez, A.J. Adapting financial technology standards to blockchain platforms. In Proceedings of the 2019 ACM Southeast Conference, Columbus State University, Kennesaw, GA, USA, 18–20 April 2019; pp. 109–116. [Google Scholar]

- Nabila, M.; Purwandari, B.; Nazief, B.A.A.; Chalid, D.A.; Wibowo, S.S.; Solichah, I. Financial technology acceptance factors of electronic wallet and digital cash in Indonesia. In Proceedings of the 2018 International Conference on Information Technology Systems and Innovation, Padang, Indonesia, 22–26 October 2018; pp. 284–289. [Google Scholar] [CrossRef]

- Chandra, Y.U.; Kristin, D.M.; Suhartono, J.; Sutarto, F.S.; Sung, M. Analysis of determinant factors of user acceptance of mobile payment system in Indonesia. In Proceedings of the 2018 International Conference on Information Management and Technology, Jakarta, Indonesia, 3–5 September 2018; pp. 454–459. [Google Scholar]

- Wiradinata, T. Mobile payment services adoption: The role of perceived technology risk. In Proceedings of the 2018 International Conference on Orange Technologies, Nusa Dua, Indonesia, 23–26 October 2018. [Google Scholar]

- Ting, H.; Yacob, Y.; Liew, L.; Lau, W.M. Intention to use mobile payment system: A case of developing market by ethnicity. Procedia Soc. Behav. Sci. 2016, 224, 368–375. [Google Scholar] [CrossRef] [Green Version]

- Riskinanto, A.; Kelana, B.; Hilmawan, D.R. The moderation effect of age on adopting E-payment technology. Procedia Comput. Sci. 2017, 124, 536–543. [Google Scholar] [CrossRef]

- De Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2018, 146, 931–944. [Google Scholar] [CrossRef]

- Kalinic, Z.; Marinkovic, V.; Molinillo, S.; Liébana-Cabanillas, F. A multi-analytical approach to peer-to-peer mobile payment acceptance prediction. J. Retail. Consum. Serv. 2019, 49, 143–153. [Google Scholar] [CrossRef]

- Kelana, B.; Riskinanto, A.; Hilamawan, D.R. The acceptance of E-payment among Indonesian millennials. In Proceedings of the 2017 International Conference on Sustainable Information Engineering and Technology, Malang, Indonesia, 24–25 November 2017; pp. 348–352. [Google Scholar] [CrossRef]

- Armey, L.E.; Lipow, J.; Webb, N.J. The impact of electronic financial payments on crime. Inf. Econ. Policy 2014, 29, 46–57. [Google Scholar] [CrossRef] [Green Version]

- Dahlberg, T.; Guo, J.; Ondrus, J. A critical review of mobile payment research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Lin, C.Y.; Su, F.P.; Lai, K.K.; Shih, H.C.; Liu, C.C. Research and development portfolio for the payment FinTech company—The perspectives of patent statistics. In Proceedings of the 2nd International Conference on E-Society, E-Education and E-Technology, Taichung, Taiwan, 13–15 August 2018; pp. 98–102. [Google Scholar]

- Omarini, A.E. Fintech and the future of the payment landscape: The mobile wallet ecosystem—A challenge for retail banks? Int. J. Financ. Res. 2018, 9, 97–116. [Google Scholar] [CrossRef]

- Moon, W.Y.; Kim, S.D. A payment mediation platform for heterogeneous fintech schemes. In Proceedings of the 2016 IEEE Advanced Information Management, Communicates, Electronic and Automation Control Conference, Xi’an, China, 3–5 October 2016; pp. 511–516. [Google Scholar]

- Ogbanufe, O.; Kim, D.J. Comparing fingerprint-based biometrics authentication versus traditional authentication methods for e-payment. Decis. Support Syst. 2018, 106, 1–14. [Google Scholar] [CrossRef]

- Kang, J. Mobile payment in Fintech environment: Trends, security challenges, and services. Hum. Cent. Comput. Inf. Sci. 2018, 8, 32. [Google Scholar] [CrossRef] [Green Version]

- Lai, W.C. Measured near field communication antenna for Fintech innovation. In Proceedings of the 2018 7th International Symposium on Next-Generation Electronics, Taipei, Taiwan, 7–9 May 2018; pp. 1–3. [Google Scholar]

- Liu, J.; Kauffman, R.J.; Ma, D. Competition, cooperation, and regulation: Understanding the evolution of the mobile payments technology ecosystem. Electron. Commer. Res. Appl. 2015, 14, 372–391. [Google Scholar] [CrossRef]

- Heredia Salazar, R. Apple pay & digital wallets in Mexico and the United States: Illusion or financial revolution? Mex. Law Rev. 2017, 1, 29. [Google Scholar] [CrossRef]

- Iman, N. Is mobile payment still relevant in the fintech era? Electron. Commer. Res. Appl. 2018, 30, 72–82. [Google Scholar] [CrossRef]

- Chiu, I.H.Y. A new era in fintech payment innovations? A perspective from the institutions and regulation of payment systems. Law Innov. Technol. 2017, 9, 190–234. [Google Scholar] [CrossRef]

- Abdullah, E.M.E.; Rahman, A.A.; Rahim, R.A. Adoption of financial technology (Fintech) in mutual fund/unit trust investment among Malaysians: Unified theory of acceptance and use of technology (UTAUT). Int. J. Eng. Technol. 2018, 7, 110–118. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló, L.V.; Flavián, C. Artificial intelligence in FinTech: Understanding robo-advisors adoption among customers. Ind. Manag. Data Syst. 2019, 119, 1411–1430. [Google Scholar] [CrossRef]

- Alexeev, V.; Urga, G.; Yao, W. Asymmetric jump beta estimation with implications for portfolio risk management. Int. Rev. Econ. Financ. 2019, 62, 20–40. [Google Scholar] [CrossRef]

- Liu, Y.; Peng, J.; Yu, Z. Big data platform architecture under the background of financial technology—In the insurance industry as an example example. In Proceedings of the ACM International Conference 2018 on Big Data Engineering and Technology, Chengdu, China, 25–27 August 2018; pp. 31–35. [Google Scholar]

- Kumari, A.; Kumar Sharma, A. Infrastructure financing and development: A bibliometric review. Int. J. Crit. Infrastruct. Prot. 2017, 16, 49–65. [Google Scholar] [CrossRef]

- Lee, R.S.T. COSMOS trader—Chaotic neuro-oscillatory multiagent financial prediction and trading system. J. Financ. Data Sci. 2019, 5, 61–82. [Google Scholar] [CrossRef]

- Faloon, M.; Scherer, B. Individualization of robo-advice. J. Wealth Manag. 2017, 20, 30–36. [Google Scholar] [CrossRef] [Green Version]

- Day, M.-Y.; Lin, J.-T.; Chen, Y.-C. Artificial intelligence for conversational robo-advisor. In Proceedings of the 2018 IEEE/ACM International Conference on Advances in Social Networks Analysis and Mining (ASONAM), Barcelona, Spain, 28–31 August 2018; pp. 1057–1064. [Google Scholar]

- Serrano, W. Fintech model: The random neural network with genetic algorithm. Procedia Comput. Sci. 2018, 126, 537–546. [Google Scholar] [CrossRef]

- Jung, D.; Dorner, V.; Weinhardt, C.; Pusmaz, H. Designing a robo-advisor for risk-averse, low-budget consumers. Electron. Mark. 2018, 28, 367–380. [Google Scholar] [CrossRef]

- Stoeckli, E.; Dremel, C.; Uebernickel, F. Exploring characteristics and transformational capabilities of InsurTech innovations to understand insurance value creation in a digital world. Electron. Mark. 2018, 28, 287–305. [Google Scholar] [CrossRef] [Green Version]

- Marafie, Z.; Lin, K.J.; Zhai, Y.; Li, J. Proactive fintech: Using intelligent IoT to deliver positive insurtech feedback. In Proceedings of the 2018 20th IEEE International Conference on Business Informatics, Vienna, Austria, 11–14 July 2018; pp. 72–81. [Google Scholar] [CrossRef]

- Liu, Y.; Chitawa, U.S.; Guo, G.; Wang, X.; Tan, Z.; Wang, S. A reputation model for aggregating ratings based on beta distribution function. In Proceedings of the ACM International Conference on Crowd Science and Engineering, Beijing, China, 6–9 July 2017; pp. 77–81. [Google Scholar]

- Ferreira, F.; Pereira, L. Success factors in a reward and equity based crowdfunding campaign. In Proceedings of the 2018 IEEE International Conference on Engineering, Technology and Innovation, Stuttgart, Germany, 17–20 June 2018; pp. 1–8. [Google Scholar] [CrossRef] [Green Version]

- Huang, T.; Zhao, Y. Revolution of securities law in the Internet Age: A review on equity crowd-funding. Comput. Law Secur. Rev. 2017, 33, 802–810. [Google Scholar] [CrossRef]

- Maier, E. Supply and demand on crowdlending platforms: Connecting small and medium-sized enterprise borrowers and consumer investors. J. Retail. Consum. Serv. 2016, 33, 143–153. [Google Scholar] [CrossRef]

- Zetzsche, D.; Preiner, C. Cross-border crowdfunding: Towards a single crowdlending and crowdinvesting market for Europe. Eur. Bus. Organ. Law Rev. 2018, 19, 217–251. [Google Scholar] [CrossRef]

- Barbi, M.; Mattioli, S. Human capital, investor trust, and equity crowdfunding. Res. Int. Bus. Financ. 2019, 49, 1–12. [Google Scholar] [CrossRef]

- Mamonov, S.; Malaga, R. Success factors in Title III equity crowdfunding in the United States. Electron. Commer. Res. Appl. 2018, 27, 65–73. [Google Scholar] [CrossRef] [Green Version]

- Anshari, M.; Almunawar, M.N.; Masri, M.; Hamdan, M. Digital marketplace and FinTech to support agriculture sustainability. Energy Procedia 2019, 156, 234–238. [Google Scholar] [CrossRef]

- Wonglimpiyarat, J. Challenges and dynamics of FinTech crowd funding: An innovation system approach. J. High Technol. Manag. Res. 2018, 29, 98–108. [Google Scholar] [CrossRef]

- Wang, W.; Mahmood, A.; Sismeiro, C.; Vulkan, N. The evolution of equity crowdfunding: Insights from co-investments of angels and the crowd. Res. Policy 2019, 48, 103727. [Google Scholar] [CrossRef]

- Lee, S. Evaluation of mobile application in user’s perspective: Case of P2P lending apps in FinTech industry. KSII Trans. Internet Inf. Syst. 2017, 11, 1105–1115. [Google Scholar] [CrossRef]

- Contreras Pinochet, L.H.; Diogo, G.T.; Lopes, E.L.; Herrero, E.; Bueno, R.L.P. Propensity of contracting loans services from FinTech’s in Brazil. Int. J. Bank Mark. 2019, 37, 1190–1214. [Google Scholar] [CrossRef]

- Rosavina, M.; Rahadi, R.A.; Kitri, M.L.; Nuraeni, S.; Mayangsari, L. P2P lending adoption by SMEs in Indonesia. Qual. Res. Financ. Mark. 2019, 11, 260–279. [Google Scholar] [CrossRef]

- Fang, X.; Wang, B.; Liu, L.; Song, Y. Heterogeneous traders, the leverage effect and volatility of the Chinese P2P market. J. Manag. Sci. Eng. 2018, 3, 39–57. [Google Scholar] [CrossRef]

- Leong, C.; Tan, B.; Xiao, X.; Tan, F.T.C.; Sun, Y. Nurturing a FinTech ecosystem: The case of a youth microloan startup in China. Int. J. Inf. Manag. 2017, 37, 92–97. [Google Scholar] [CrossRef]

- Wang, H.; Wang, Z.; Zhang, B.; Zhou, J. Information collection for fraud detection in P2P financial market. In Proceedings of the MATEC Web of Conferences 189, Beijing, China, 25–27 May 2018; p. 06006. [Google Scholar]

- Anugerah, D.P.; Indriani, M. Data Protection in financial technology services: Indonesian legal perspective. In Proceedings of the IOP Conference Series: Earth and Environmental Science, Makassar, Indonesia, 25–26 October 2017. [Google Scholar]

- Yunus, U. A comparison peer to peer lending platforms in Singapore and Indonesia. In Journal of Physics: Conference Series; IOP Publishing: Medan, Indonesia, 2019; Volume 1235, p. 012008. [Google Scholar]

- Buchak, G.; Matvos, G.; Piskorski, T.; Seru, A. Fintech, regulatory arbitrage, and the rise of shadow banks. J. Financ. Econ. 2018, 130, 453–483. [Google Scholar] [CrossRef]

- Tao, Q.; Dong, Y.; Lin, Z. Who can get money? Evidence from the Chinese peer-to-peer lending platform. Inf. Syst. Front. 2017, 19, 425–441. [Google Scholar] [CrossRef] [Green Version]

- Hsueh, S.C.; Kuo, C.H. Effective matching for P2P lending by mining strong association rules. In Proceedings of the 3rd International Conference on Industrial and Business Engineering, Sapporo, Japan, 17–19 August 2017; pp. 30–33. [Google Scholar]

- Fermay, A.H.; Santosa, B.; Kertopati, A.Y.; Eprianto, I.M. The development of collaborative model between fintech and bank in Indonesia. In Proceedings of the 2nd International Conference on E-commerce, E-Business and E-Government, Hong Kong, 13–15 June 2018; pp. 1–6. [Google Scholar] [CrossRef]

- Suryono, R.R.; Marlina, E.; Purwaningsih, M.; Sensuse, D.I.; Sutoyo, M.A.H. Challenges in P2P lending development: Collaboration with tourism commerce. In Proceedings of the 2019 International Conference on Computer Science, Information Technology, and Electrical Engineering, ICOMITEE 2019, Jember, Indonesia, 16–17 October 2019; pp. 129–133. [Google Scholar]

- Yu, T.; Shen, W. Funds sharing regulation in the context of the sharing economy: Understanding the logic of China’s P2P lending regulation. Comput. Law Secur. Rev. 2019, 35, 42–58. [Google Scholar] [CrossRef]

- Jagtiani, J.; Lemieux, C. Do fintech lenders penetrate areas that are underserved by traditional banks? J. Econ. Bus. 2018, 100, 43–54. [Google Scholar] [CrossRef] [Green Version]

- Anresnani, D.S.; Widodo, E.; Syairuddin, B. modelling integration of system dinamics and game theory for of financial technology peer to peer lending industry. In Proceedings of the International Mechanical and Industrial Engineering Conference, Malang, Indonesia, 30–31 August 2018; p. 07006. [Google Scholar]

- Huang, R.H. Online P2P lending and regulatory responses in China: Opportunities and challenges. Eur. Bus. Organ. Law Rev. 2018, 19, 63–92. [Google Scholar] [CrossRef]

- Nugraha, A.P.; Rolando; Puspasari, M.A.; Syaifullah, D.H. Usability Evaluation for User Interface Redesign of Financial Technology Application. In Proceedings of the 1st International Conference on Industrial and Manufacturing Engineering, Medan City North Sumatera, Indonesia, 16 October 2018. [Google Scholar] [CrossRef]

- Jonker, N. What drives the adoption of crypto-payments by online retailers? Electron. Commer. Res. Appl. 2019, 35, 100848. [Google Scholar] [CrossRef]

- Todorof, M. FinTech on the dark web: The rise of cryptos. In Era Forum; Springer: Berlin/Heidelberg, Germany, 2019; Volume 20. [Google Scholar] [CrossRef]

- Brownsword, R. Regulatory fitness: Fintech, funny money, and smart contracts. Eur. Bus. Organ. Law Rev. 2019, 20, 5–27. [Google Scholar] [CrossRef] [Green Version]

- Du, W.D.; Pan, S.L.; Leidner, D.E.; Ying, W. Affordances, experimentation and actualization of FinTech: A blockchain implementation study. J. Strateg. Inf. Syst. 2019, 28, 50–65. [Google Scholar] [CrossRef]

- Niu, B.; Ren, J.; Zhao, A.; Li, X. Lender trust on the P2P lending: Analysis based on sentiment analysis of comment text. Sustainability 2020, 12, 3293. [Google Scholar] [CrossRef] [Green Version]

- Fang, Z.; Zhang, J.; Zhiyuan, F. Study on P2P E-finance platform system: A case in China. In Proceedings of the 11th IEEE International Conference on E-Business Engineering, Guangzhou, China, 5–7 November 2014; pp. 331–337. [Google Scholar]

- Wang, J.G.; Xu, H.; Ma, J. Financing the Underfinanced: Online Lending in China; Springer: Berlin/Heidelberg, Germany, 2015; ISBN 9783662465257. [Google Scholar]

- Pohan, N.W.A.; Budi, I.; Suryono, R.R. Borrower sentiment on P2P lending in Indonesia based on Google Playstore reviews. In Proceedings of the Sriwijaya International Conference on Information Technology and Its Applications (SICONIAN 2019), Palembang, Indonesia, 16 November 2019; pp. 17–23. [Google Scholar]

- Suryono, R.R.; Budi, I. P2P Lending sentiment analysis in Indonesian online news. In Proceedings of the Sriwijaya International Conference on Information Technology and Its Applications (SICONIAN 2019), Palembang, Indonesia, 16 November 2019; pp. 39–44. [Google Scholar]

- Kursh, S.R.; Gold, N.A. Adding FinTech and blockchain to your curriculum. Bus. Educ. Innov. J. Contents 2016, 8, 6–12. [Google Scholar]

Figure 1.

Systematic literature review (SLR) methodology.

Figure 2.

The selection process for final papers.

Figure 3.

Result of content analysis using VOS Viewer.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Literature review results.

| Year | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | Total |

|---|---|---|---|---|---|---|---|

| Research on fintech (in general) | - | 1 | 4 | 7 | 23 | 6 | 41 |

| Research on payment, clearing, and settlement | 1 | 2 | 2 | 4 | 11 | 3 | 23 |

| Research on risk management and investment | - | - | - | 2 | 7 | 3 | 12 |

| Research on market aggregator | - | - | - | 1 | - | - | 1 |

| Research on crowdfunding | - | - | 1 | 1 | 4 | 3 | 9 |

| Research on P2P Lending | - | - | - | 5 | 8 | 7 | 20 |

| Research on cryptocurrency and blockchain | - | - | - | - | 1 | 4 | 5 |

| Total | 1 | 3 | 7 | 20 | 54 | 26 | 111 |

Table 2.

Classification of articles by fintech business model.

| Topic | Adoption | Problems | Trends | Challenges | Innovation |

|---|---|---|---|---|---|

| Research on Fintech (in general) | [19,20,21,22,23,24,25,26] | [27] | [5,7,17,28,29,30,31,32,33,34,35,36] | [3,15,37,38,39,40,41,42,43,44,45,46] | [16,18,47,48,49,50,51,52] |

| Research on Payment, Clearing, and Settlement | [53,54,55,56,57,58,59,60,61,62] | [63] | [64,65,66] | [67,68,69] | [9,70,71,72,73,74] |

| Research on Risk Management and Investment | [75,76] | [77] | [78,79,80,81] | - | [82,83,84,85,86] |

| Research on Market Aggregator | - | [87] | - | - | - |

| Research on Crowdfunding | - | - | [88,89,90,91] | [92,93,94] | [95,96] |

| Research on Peer-to-peer lending (P2P Lending) | [97,98,99] | [8,100,101,102,103,104] | [105,106] | [4,107,108,109,110,111,112,113,114] | - |

| Research on Cryptocurrency and Blockchain | [115] | [116] | [117] | - | [13,118] |

Table 3.

Classification of articles by (main) methodology.

| Methodology (Main) | Total |

|---|---|

| Empirical | |

| -- articles using archival data | 13 |

| -- articles using survey data | 20 |

| Qualitative (case study/interviews/qual. analysis) | 27 |

| Experimental | 12 |

| Conceptual model | 18 |

| Simulative | 3 |

| Theoretical | 5 |

| Design science | 5 |

| Literature review | 8 |

| Total Articles | 111 |

Table 4.

Classification of articles by publication.

| Journal and Proceedings Name | Total |

|---|---|

| Electronic Commerce Research and Applications | 6 |

| Electronic Markets | 3 |

| European Business Organization Law Review | 3 |

| Investment Management and Financial Innovations | 3 |

| Computer Law and Security Review | 2 |

| Industrial Management and Data Systems | 2 |

| International Journal of Engineering and Technology UAE | 2 |

| Journal of Retailing and Consumer Services | 2 |

| ACM International Conference Proceeding Series | 7 |

| Procedia Computer Science | 3 |

| IOP Conference Series: Earth and Environmental Science | 2 |

| IOP Conference Series: Materials Science and Engineering | 2 |

| Others | 74 |

Table 5.

Research challenges.

| Challenges | Issues |

|---|---|

| Framework and Model | 1. Developing a practical and systematic framework for fintech [33,34,75] 2. The model of the fintech p2p lending system needs to be detailed [52,112] 3. Development of culturally appropriate models [56] 4. Design new service configurations [5] 5. Fintech is changing the role of IT, consumer behavior, ecosystems, and regulations [18] 6. The challenges and dynamics of the FinTech crowdfunding platform [51] |

| Regulation and Policy | 7. Fintech need for comprehensive regulation [4,15,38,44,50] 8. Development of international prudential standards [52] 9. Required regulatory reform regarding the information technology [44] 10. Revised licensing regime for financial companies [52] 11. Public policy requires a stable and efficient public infrastructure and trust in the payment system [74] 12. There must be clear rules in the agreement, including penalties, dispute resolution, and settlement mechanisms in the event of a business closure [4] 13. There are market standardization and transparency in the era of big data [100] 14. Fintech entrepreneurs should monitor upcoming changes in the regulatory environment [36] 15. Public policy against the financial revolution [72] 16. The online loan platform has registration requirements [113] 17. Securities law on the development of equity crowdfunding funding [89] 18. Fintech focus on changing the role of the state in encouraging national industrial growth [32] |

| Regulator | 19. Institutional support for new financial technologies [52] 20. Creating a regulatory sandbox for fintech start-ups [52,103] 21. Regulators must secure and respect the conditions of the moral community [117] |

| Financial Ethics | 22. Financial ethics must be following principles [47] |

| Financial Literacy | 23. Financial literacy should be technology-based oriented as well [28] 24. Lack of knowledge of success factors of equity crowdfunding open to non-accredited investors [93] |

| Supervisory | 25. Supervisory aspects by the financial services authorities are urgently [44] 26. Supervision of the problematic p2p lending platform [8] |

| Personal data protection | 27. The protection of misuse of personal data [17,44] 28. The use of big data and new technologies raises significant data protection issues [103] 29. Blockchain solves data protection issues regarding data integrity [54] 30. Privacy protection on InsurTech [86] |

| Customer Protection | 31. Trust in the payment system can fulfill consumer protection [74] 32. Utilization of electronic signatures for agreements [4] 33. Customer management [3] |

| Portfolio risk management | 34. The risk exposure of individual stocks with portfolios [77] |

| Collaboration | 35. Banks need to consider fintech and strategic partnerships [31,35,37,49,51,66] 36. Incubator model [108] 37. The channeling model can provide benefits for both fintech and banks [108] 38. Collaboration between online lending firms and banks [113] 39. Bank strategic planning for investment in fintech companies [38] 40. Offers strategic capabilities for a company to occupy a market niche in the financial sector [101] 41. Fintech collaboration with other industries [109] 42. Cross-Border Crowdfunding [91] |

| Security | 43. Broad access to electronic financial transactions should enhance personal protection [63] 44. Data security standards for blockchain platform payment applications [54] 45. Authentication and access control mechanisms [17] 46. Secure data storage and processing [17] 47. Developing a trust-based financial system, including comprehensive and measurable security mechanisms [39] 48. Data security and consumer trust [24] |

| Infrastructure | 49. Sources of infrastructure financing [79] 50. Role of infrastructure [79] 51. Factors affecting infrastructure construction projects [79] |

| Payment Systems | 52. Developing payment systems on mobile phones with biometric fingerprints or voice payments [60,68] 53. The right framework or guidelines for a mobile/digital wallet [72] 54. Requires standard definitions of mobile payments (including mobile banking, mobile money, mobile wallets, mobile commerce, mobile pos, and mobile finance) [73] 55. Fintech mobile payment services in the future will develop into a more secure service [69] |

| Blockchain | 56. The blockchain concept (including blockchain structures and payment transactions on the blockchain) [46,52,54,118] 57. Blockchain is a future technology [9,41] |

| Bitcoin | 58. Price conversion between bitcoin and the physical currency or other virtual currencies [13] 59. Explore ideas about coins that have major crypto features [116] |

| Technology | 60. Rapid developments in artificial intelligence (ai), machine learning, and blockchain [117] 61. Development of an optimization algorithm model and asset allocation to predict trends [82] 62. Develop integrated knowledge-based and generative models for the ai conversational robot advisor [82] 63. Need to ensure the quality of the software system at fintech [29] 64. Technology integration [3] 65. Alternative credit scoring based on non-traditional data [101] 66. Open Application Programming Interfaces (APIs) [43] 67. Digital identification and biometrics [43] 68. The design of big data-based lending markets [106] 69. Information collection for fraud detection [102] |

| Robo-Advisor | 70. Banks and other companies in the financial industry must design Robo-advisors [76] 71. AI for conversational Robo-advisor [82] 72. Designing a Robo-advisor for risk-averse [84] |

| Digital Insurances | 73. Concerning the business function of digital insurances [15] 74. Using Smart IoT to Provide Positive InsurTech Feedback [86] 75. Understand insurance value creation in a digital world [85] |

Table 6.

Research Trends.

| Trends | Issues |

|---|---|

| Business Model and Ecosystem | 1. Fintech has a variety of business models [3,5,7,15,16,18,23,33,42,43,46,48,50,78] 2. The fintech business model can be adopted by existing financial organizations [36] 3. Fintech is changing the business and economic landscape [23,45] 4. Analyzed the function and structure of FinTech [21] 5. Transformation of financial intermediation and financial stability [30] 6. P2P lending business model [8,104] |

| Adoption | 7. The process of consumer self-regulation and behavioral intentions affects fintech adoption [53] 8. Adoption in mutual fund [75] 9. The attitude of consumers towards Robo-advisors influences adoption [76] 10. The adoption of mobile payments/fintech [20,22,26,25,56,57,58,59,62,97] 11. The adoption of fintech loans (P2P lending) [97,98,99] 12. Perceived usefulness of P2Pm-pay influences their decision to adopt [61] 13. Evaluating the usability of fintech [114] |

| Payment | 14. Bitcoin is a popular financial asset [13] 15. Multi-perspective framework for mobile payment ecosystems [64] 16. comparing mobile payment systems for SMS (short message service), NFC (near field communication), and QR (quick response) [60] 17. The most severe barrier for crypto-acceptance is a lack of consumer demand [105] 18. Development Portfolio for the Payment FinTech Company [65] 19. Evolution of the mobile payments technology ecosystem [71] 20. Developing payment transaction mediation among heterogeneous FinTech payment schemes [67] 21. Fintech acceptance factors of e-wallet and digital cash [55] 22. Ecosystem concepts as applied to the new payment landscape [66] |

| Financing | 23. Fintech is an alternative solution for small micro-businesses to obtain the funding through p2p lending model [44] 24. The company chooses a high level of profit margin [37] 25. The borrower decides a low level of debt time [37] 26. The lender chooses a high level of ROI [37] 27. Fintech is used to finance agriculture [94] 28. P2P platforms pose a considerable risk for market investors [100] 29. The advent of equity crowdfunding has had a fundamental impact on securities law and its legislative philosophy [89] 30. P2P lending consumer lending activity has penetrated areas that traditional banks may be underserved [111] 31. Success factors in equity crowdfunding [93,96] 32. Understanding P2P lending regulation [110] |

| Evolution of the mobile phone | 33. Mobile devices with increased storage media and data transfer capabilities [9] 34. Proposes a framework called UMETRIX for evaluating the usability of mobile applications [19] |

| Companies | 35. Early-stage companies will be at risk and do not understand market conditions [92] |

| Investor | 36. A higher level of participation of individual investors in the funding of new ventures [92] 37. Market consolidation trends through acquisitions and mergers between investors, start-ups, and financial shareholders [34] 38. Shareholders, including "big" banks, will continue to play a central role in the fintech ecosystem [34] 39. The rise of shadow banks [105] 40. Robo-advisors provide risky portfolios to individual investors based on an investment algorithm [81] 41. There are similarities in investor motivation in equity and crowdfunding rewards [88] 42. Connecting SME borrowers and consumer investors [90] |

| Start-up | 43. Focused on improving the consumer experience [34] 44. Focuses on integrating services across various fintech categories [34] |

| Technology | 45. The invisible robots of global finance [47] 46. Near Field Communication (NFC) antenna for fintech innovation [70] 47. New technological applications have emerged for electronic payments, electronic deposits, personal and consumer loans, insurance, various trade transactions driven by e-commerce [41] 48. Apply a priori algorithm to P2P lending [107] 49. Intelligent agent-based hedge and trading system design and development [80] 50. A reputation model for aggregating Ratings [87] 51. Big data platform architectural technology innovation combined with insurance [78] 52. NEC for Secure Multi-Party Computation (SMPC) technology [40] 53. The Random Neural Network with Genetic Algorithm [83] 54. FinTech Systems Automated Black Box Testing [27] |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Suryono, R.R.; Budi, I.; Purwandari, B. Challenges and Trends of Financial Technology (Fintech): A Systematic Literature Review. Information 2020, 11, 590. https://0-doi-org.brum.beds.ac.uk/10.3390/info11120590

AMA Style

Suryono RR, Budi I, Purwandari B. Challenges and Trends of Financial Technology (Fintech): A Systematic Literature Review. Information. 2020; 11(12):590. https://0-doi-org.brum.beds.ac.uk/10.3390/info11120590

Chicago/Turabian StyleSuryono, Ryan Randy, Indra Budi, and Betty Purwandari. 2020. "Challenges and Trends of Financial Technology (Fintech): A Systematic Literature Review" Information 11, no. 12: 590. https://0-doi-org.brum.beds.ac.uk/10.3390/info11120590

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.