Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation

Department of Economics, University of Thessaly, 38333 Volos, Greece

J. Risk Financial Manag. 2021, 14(1), 41; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010041

Submission received: 5 January 2021

/

Accepted: 14 January 2021

/

Published: 18 January 2021

(This article belongs to the Special Issue International Trade Theory and Policy)

Abstract

:This paper conducts a review on theoretical and empirical findings on the increasingly popular measure of trade policy uncertainty (TPU) in economics and finance. Moreover, an empirical investigation takes place in order to find the impact that TPU exerts on Bitcoin market values by employing a spectrum of Generalized Autoregressive Conditional Heteroskedasticity (GARCH) specifications. Existing studies support that trade policy uncertainty leads to lower-quality and more expensive products and weak participation in international trade. Moreover, it contributes to lower democratic sentiment, hesitant internal migration and lesser socio-economic mobility and higher fluctuations in profitable assets. Moreover, our econometric findings reveal that TPU positively affects Bitcoin prices while crude oil values negatively influence this major cryptocurrency. Thereby, higher trade policy uncertainty is found to increase demand and favorite investments into risky assets in order to ameliorate the risk-return trade-off in investors’ portfolios. This study provides a compass for investing during turmoil due to trade wars and tariffs.

1. Introduction

One of the major tiers of economic and financial growth throughout the centuries has been international trade. Trade agreements between counterparties enable the exchange of products that each part can acquire at lower prices than if needed to produce them. This benefits economic development and leads to wealth increases. Thereby, uncertainty as regards trade conditions includes a lot of noise in international markets and prevents the creation of a favorable environment for developing irreversible and large-scale investments. Fears about uncertainty concerning future trade policies may block the participation of firms into foreign markets. This would impede the optimal allocation of resources at a worldwide level and impose the burden of high sunk costs to financially healthy and potentially sustainable investment projects.

A debate about whether tariffs, quotas or subsidies would be most appropriate to protect an infant industry has been at the heart of discussions about trade policy uncertainty (Bhagwati and Ramaswami 1963). Discussion about whether free trade is a better policy than no trade for price-taker countries and whether this leads to higher welfare has generated high-quality academic work and an ongoing exchange of opinions among economists (Samuelson 1939, 1962; Myint 1954; Burstein and Cravino 2015; Edmond et al. 2015). Production across importing and exporting competing goods is considered to be tightly connected with economic development (Krueger 1980, 1997) and income distribution (Edwards 1997). These issues are pertinent to the development policy debate.

Trade wars can result in inflation—especially, manufactured goods can render much more expensive—this boosts prices in domestic economies. A voluminous bulk of academic research has focused interest on tariffs and quotas and their effects as the most popular forms of trade protectionism. Dasgupta and Stiglitz (1977) supported that the optimum fixed tariff is preferable in order to maximize consumer’s surplus in relation to the optimum fixed quota in a competitive world with no uncertainty. Moreover, Findlay and Wellisz (1982) argue that welfare losses do not increase monotonically with tariff levels. They also support that free trade constitutes the first-best social optimum in the absence of national monopoly power over the terms of trade. Kimbrough (1985) argues that adjustment costs in a monetary union are lower under a tariff than under a quota. It is supported that trade liberalization combined with favorable monetary policy leads to beneficial results for the economy. Furthermore, Rodriguez and Rodrik (2000) analyzed the linkage between trade barriers and economic growth and cast doubt on the view that they are strongly and negatively connected.

Notably, the hot topic of free trade agreements (FTAs) is connected to trade policy uncertainty and has spurred increasing interest. Feenstra (1992) analyzed that US protectionism has burdened foreign countries with substantial costs. Free trade agreements have led to greater discrimination and losses for the countries excluded, and this urges the latter to participate in alternative FTAs. Moreover, according to Grossman and Helpman (1993), conditions that favorited the viability of a potential free trade agreement between regions also increased the probability that this agreement would result in lower aggregate social welfare. Krugman (1991) found that free trade areas are quite harmful for countries outside them as trading blocs pursue more aggressive trade policies. He supports that trade war leaves each side worse off while Levy (1997) argued that bilateral free trade agreements could never increase political support for multilateral free trade. Baier and Bergstrand (2004) argue that potential welfare gains deriving from a free trade agreement between a pair of countries are higher when these two regions are close in distance, have similar economies and possibilities in exploiting economies of scale. Moreover, benefits from FTA increase when there is a great difference in capital-labor endowment ratios because of gains in comparative advantages. The concept of FTAs is tightly connected to liberalization of trade and trade negotiations. Ben-David (1993) explained that liberalization of trade could contribute to income convergence among members of the European Economic Community. Additionally, Foellmi and Oechslin (2010) document that less-developed countries suffer widening of income disparities caused by free trade. This is because liberalization leads to a surge in top-income shares. Moreover, Ossa (2014) estimated that the possible government welfare gains from future multilateral trade negotiations would be small (0.5% on average).

The advantages and disadvantages of trade wars that generate trade policy uncertainty have also been at the core of serious economic debate. Lindé and Pescatori (2019) argue that trade wars can lead to permanently lower income and trade volumes. Li et al. (2018) provide evidence that China would be significantly hurt by the China–US trade war, but the damages would not be detrimental. Such wars would hurt most countries regarding GDP and manufacturing employment but would prove beneficial as concerns their welfare and trade. Moreover, Li et al. (2020) revealed that mainly Asian economies would be benefited in terms of welfare when US–China trade wars occurred.

A large portion of the empirical literature on trade policy uncertainty is based on the embryonic but rapidly popular measure of Trade Policy Uncertainty constructed by Caldara et al. (2020). The trade policy uncertainty (TPU) index hinges on automated text searches of the electronic archives of seven newspapers: Boston Globe, Chicago Tribune, Guardian, Los Angeles Times, New York Times, Wall Street Journal and Washington Post. The calculation of this index takes place by counting the monthly frequency of articles discussing trade policy uncertainty for each newspaper.1

This paper adds to trade literature in a three-fold manner. Firstly, the understanding of trade policy uncertainty and its consequences is ameliorated and a bird’s-eye view of this phenomenon on the macro economy, institutions, socio-economic matters such as migration and financial markets is laid out. Secondly, it provides an integrated survey of the high-quality academic research on trade policy uncertainty before and after the creation of the highly innovative Caldara et al. (2020) index. Moreover, empirical estimations by traditional as well as innovative ARCH and GARCH specifications take place in order to evaluate the impact of trade policy uncertainty and crude oil on the market values of the highly risky Bitcoin asset. Thereby, the strenuous task of casting light on every aspect of trade policy effects is undertaken.

The remainder of this study is structured as follows. Section 2 furnishes an analysis of the theoretical and empirical academic literature concerning trade policy uncertainty. The analysis is conducted as regards a range of recipients of trade policy uncertainty impacts. Moreover, Section 3 provides the data and methodologies employed for the purposes of econometric estimations. Section 4 displays the empirical outcomes and analyzes the economic implications of findings related to portfolio construction and welfare maximization. Finally, Section 5 concludes and suggests avenues for further research. It should be noted that Table A1 displays the basic characteristics of studies investigating trade policy uncertainty and Figure A1, Figure A2 and Figure A3 in the Appendix A capture the level of diffusion of these studies to interested readers.

2. Studies about Trade Policy Uncertainty

Academic work on trade policy uncertainty has been based on high-quality academic papers that have provided a thorough and in-depth analysis of how uncertainty about free trade affects the macro economy, institutions, socio-economic phenomena and financial markets. It should be underlined that the benchmark separating latest academic work from more modern research has been the highly innovative measure of trade policy uncertainty by Caldara et al. (2020) that measures newspaper-based information about trade conditions. The TPU index has been constructed regarding three major economies: US, China and Japan.

To be more precise, Caldara et al. (2020) constructed three measures of trade policy uncertainty in the US economy. The first one is a firm-level measure while the second is based on newspaper coverage of news related to trade policy uncertainty. The third measure is derived from the estimation of a stochastic volatility model for US import tariffs. Findings based on firm-level and aggregate macroeconomic data support that higher TPU results in lower US business investment by 1% while vector autoregressive (VAR) results reveal even greater reduction. The two-country general equilibrium model employed indicates that higher tariffs and uncertainty about future tariffs impede investments as non-exporters accumulate more capital than exporters.

Moreover, Steinberg (2020) provided a comment on Caldara et al. (2020) and argues that the US input–output accounts matter for the nexus between TPU and US economic activity. Moreover, by employing a simple model of price-setting under nominal rigidities the modeling assumptions of the empirical outcomes in Caldara et al. (2020) are tested. According to Steinberg (2020), industry-level measures of trade exposure are not perfect measures. Moreover, it is argued that the mechanisms underlying firms’ concerns about TPU do not indispensably mean that the mechanisms have similar economic impacts. Some critical issues arise concerning whether tariff shocks are unilateral or whether domestic import tariffs have no direct impacts on domestic marginal cost. Furthermore, the issue of whether sticky prices indeed mitigate rather than amplify the expected macroeconomic contraction emerges.

2.1. Linkages between Trade Policy Uncertainty and the Macro Economy

A number of influential studies have investigated the linkage between trade policy uncertainty and the overall economy in a macroeconomic level. In order to acquire the findings by these related papers by the aforementioned strand of the literature, we dwell on four specific academic studies that examined impacts on exports, consumption and welfare in economies. The papers of Handley (2014); Feng et al. (2017); Steinberg (2019) and Imbruno (2019) made use of dynamic models or panel methodologies in order to trace effects on the real economy.

Handley (2014) employed a dynamic, heterogeneous firms’ model and considers trade policy uncertainty that delays the entry of exporters into new markets and renders them less sensitive to tariff reductions. It is argued that reducing trade uncertainty with multilateral commitments at the World Trade Organization (WTO) leads to higher entry into markets. Additionally, it is supported that reliability about the severity of punishments for deviations is crucial for preserving product entry in Australia. Estimations indicate that without the WTO binding commitments in 1996 the growth of Australian exporter-product varieties would have been lower by 7%. Moreover, if no tariffs and bindings existed in Australia more than 50% of predicted product growth would rely on uncertainty.

In a similar mentality, Steinberg (2019) made use of a dynamic general equilibrium model with heterogeneous firms, endogenous export participation and stochastic trade costs in order to measure the effect of trade policy uncertainty on UK trade after the Brexit. Input–output data since 2011 was adopted and soft as well as hard Brexit scenarios were considered. Calibration was employed for estimations and a number of sensitivity analyses take place. It was predicted that the Brexit effect on the UK economy would be substantial, especially in the long-run. Trade flows with the European Union would decrease by 8.2%–44.8% and consumption would fall by 0.5%–1.3%. Moreover, UK households would face welfare losses of about 7000–19,000 GBP. Nevertheless, the macroeconomic impacts are not predicted to be large. It should be noted that Brexit-induced uncertainty is small in comparison with other macroeconomic uncertainties. Namely, the total consumption-welfare equivalent welfare cost of Brexit ranges from 0.4% to 1.2% but less than 25% of this impact is attributed to Brexit uncertainty.

In a somewhat similar vein, Feng et al. (2017) developed a model of heterogeneous firms that incorporates trade policy uncertainty. A firm–product level dataset about Chinese exports to the US and the European Union around China’s WTO accession was adopted. Findings document that the reduction in trade policy uncertainty led to firms entering and exiting export activity within fine product-level markets. To be more precise, firms with higher quality products at lower prices entered the market while firms with the opposite characteristics left the market. Thereby, Chinese tariff policy uncertainty decreases were determinants of aggregate reallocation of Chinese exports and encouraged participation by exporters with higher-quality and lower-price products.

By a different perspective, Imbruno (2019) uses Chinese import data at the country/product/firm level and panel regressions so as to detect how Chinese imports react to tariff binding due to China’s accession to the WTO. Evidence is provided that lower TPU allows access to a larger spectrum of foreign goods that are also characterized by higher quality. Tariff binding is found to prove beneficial for China in terms of imports as Chinese producers and trade intermediaries start importing and this results in potential gains for consumers. It is also emphasized that foreign firms that are located in China present more intense market seeking in China rather than seeking for resources when trade policy uncertainty becomes lower because of tariff binding.

2.2. The Nexus between Trade Policy Uncertainty and Institutions

Apart from studies focusing on the macro economy, an embryonic strand of literature about trade policy uncertainty has emerged that investigates impacts on institutions, such as democracy. Up to the present, only the study of Tian et al. (2020) has appeared. Nevertheless, this constitutes a highly promising topic and could spur a proliferating bulk of relevant research.

More specifically, Tian et al. (2020) look into how income variations driven by trade uncertainty influence democratic transitions during the 1960–2013 period by using a large sample of countries. The Polity2score (Marshall et al. 2015) is employed as a measure of democracy and trade uncertainty is estimated in a gravity model framework. Moreover, ordinary least squares (OLS) and generalized method of moments (GMM) procedures are adopted for estimations. Outcomes provide evidence that higher income leads to transition to democracy and this is more evident in developing regions rather than advanced countries. It is argued that significantly higher levels of democracy are traced when GDP growth increases by 1%. These findings are robust to using different measures of GDP and uncertainty.

2.3. Trade Policy Uncertainty and Migration

The nexus of socio-economic phenomena with uncertainty regarding economic conditions constitutes another highly promising strand of literature. This is the reason why the adoption of sophisticated indices measuring economic, monetary, geopolitical or trade conditions have given a significant boost to relevant empirical estimations. The connection between trade policy and migration was studied in the paper of Facchini et al. (2019) and provides a compass for the development of a significantly larger avenue for research connecting trade policy uncertainty and socio-economic phenomena.

Thereby, Facchini et al. (2019) investigated the level by which trade policy uncertainty concerning Chinese exporters in the US has influenced internal worker migration in China. The difference-in-difference specification employed in order to capture variation among prefectures provides evidence that higher migration emerged due to lower trade uncertainty. More specifically, empirical outcomes reveal higher migration by 24%. The migrants most responsive to this effect of trade policy uncertainty are “non-hukou”, skilled and in their prime working age. Moreover, it is argued that “native” unskilled workers in these prefectures were occupied for more working hours and that internal migrants found a job in the places they migrated to during lower trade policy uncertainty periods.

2.4. The Connection between Trade Policy Uncertainty and Financial Markets

A highly growing strand of literature about trade policy uncertainty consists of academic work investigating the impacts of uncertainty οn trade in traditional or modern financial markets. Crowley et al. (2018); Gozgor et al. (2019); He et al. (2020) and Karabulut et al. (2020) examine the impacts of TPU on financial markets in general, cryptocurrencies and commodities, respectively. These could put the basis for generating a series of influential papers that would cast light on how financial markets respond to tariffs, quotas and other generators of trade uncertainty.

More specifically, Crowley et al. (2018) examine how higher trade policy uncertainty influences entry or exit decisions of Chinese firms regarding export markets. By being based on the model of Handley and Limao (2015) three distinct cases of entry are investigated. Findings indicate that high levels of trade policy uncertainty urge Chinese firms to exit established foreign markets and render them more hesitant towards entering new foreign markets. The imposition of antidumping duties in a market is considered as a measure of rising trade policy uncertainty. Analysis is based on the “tariff echoing” phenomenon (a firm that did not face tariff hikes is less likely to enter a new market when its neighboring firms did face one). It is revealed that the potential of tariffs in the future has a minor effect on Chinese entry into foreign markets. Furthermore, He et al. (2020) examine how international trade policy uncertainty influences stock markets. The time-varying VAR (TVP-SV-VAR) methodology is adopted. Evidence indicates that TPU has heterogeneous impacts on the US and Chinese equity markets. To be more precise, trade conflicts between these countries generate positive effects on the US stock market whereas exert negative impacts on the Chinese stock market.

As concerns the study of Gozgor et al. (2019), they explore the nexus between Bitcoin returns and the TPU index in the US by employing the wavelet power spectrum (WPS), the wavelet coherency (WTC) and the cross-wavelet (XWT) methodologies. The period examined spans from July 2010 until August 2018. Econometric results provide evidence of the existence of significant regime alterations in Bitcoin returns as well as the TPU index during the first couple and the last couple of years investigated. More specifically, a negative causal linkage is found from TPU towards Bitcoin during these periods. Thereby, evidence reveals that trade policy uncertainty is very influential concerning this major cryptocurrency when regime changes take place.

When it comes to Karabulut et al. (2020), they investigate the connection between commodity prices and US trade uncertainty spanning the period from January 1996 to September 2019. The continuous wavelet transform (CWT), WTC and WPS methodologies are employed for estimations. Moreover, frequency-based Granger causality and conventional vector autoregression techniques are used. It is revealed that strong noises are detected concerning world trade uncertainty between 2009–2010 and 2015–2016 as well as for the commodity price index (CPI) between 2008–2009 and 2015–2016 and between 2008–2009 and 2017–2018. Positively correlated and significant co-motional predictions emerge. Outcomes from wavelet estimations indicate that these co-movements are linked with important political and economic events in a worldwide level.

In an overall perspective, these four strands of literature reveal that trade policy is influential on a large range of economic and financial aspects. Evidence indicates that Australia has significantly benefited in terms of exporter-product varieties and GDP from tariffs and bindings that lowered trade policy uncertainty. On the other hand, it is revealed that the United Kingdom has not been largely affected by TPU in the advent of shocks such as the Brexit. As regards China, it is shown that lower trade policy uncertainty has brought about significant benefits related to as it has favorited high-quality imports in low prices, the reallocation of exports, and has allowed potential wealth benefits for Chinese producers, intermediaries and consumers.

Lower uncertainty as regards trade in a worldwide level is also found to be beneficial for the development of democratic institutions by a modest extent. This effect takes place through achieving levels of higher output due to beneficial trading conditions. It is noteworthy that better conditions for trade lead to social and spatial mobility that result in higher employment for migrants in different Chinese prefectures. Emphasis should be put in that the most productive workers prove to be receivers of large positive impacts by reductions in trade uncertainty in China.

Apart from that, lower levels of trade uncertainty are drivers of stronger incentives concerning Chinese firms to remain in established foreign markets and become entrants in new foreign markets. Moreover, it is supported that higher trade policy uncertainty leads to higher volatility in the market values of Bitcoin. Similar findings come to the surface regarding commodity prices.

All in all, it can be argued that high trade policy uncertainty is at the root of a number of malfunctions in the real economy and the financial sector in a global context. Worse reallocation of resources, lower-quality and expensive products, weak incentives for participation in international trade, erosion of democratic sentiment, inability of internal migration and impediment to socio-economic mobility, higher fluctuations in profitable assets would be brought about by deterioration in trade conditions. Overall, effects of uncertainty as regards trade activities are found to be modest and cover a wide spectrum of social, economic and financial domains.

3. Data and Methodology

Apart from conducting a survey on the theoretical and empirical papers that investigate the nexus between trade policy uncertainty and the macro economy as well as financial assets, this study undertakes the strenuous task of employing a number of GARCH specifications in order to investigate how TPU and crude oil market values affect Bitcoin prices. The period examined starts from 4 March 2012 (when data about Bitcoin trades was available for the first time and sizeable trading volume of Bitcoin appeared). Data covers until late July 2019 (the latest date when data about TPU was available). Thereby, we investigate whether TPU and crude oil exert impacts on returns and volatility of the most important cryptocurrency during its existence. Data about the highly innovative index of trade policy uncertainty in the US has been extracted from www.policyuncertainty.com/trade_uncertainty.html. Furthermore, weekly data about Bitcoin closing prices is used based on the series downloaded from the coinmarketcap.com database and weekly market values of the West Texas Intermediate (WTI) oil have been extracted by Datastream. Data are transformed into logarithms and become stationary in order to conduct estimations.

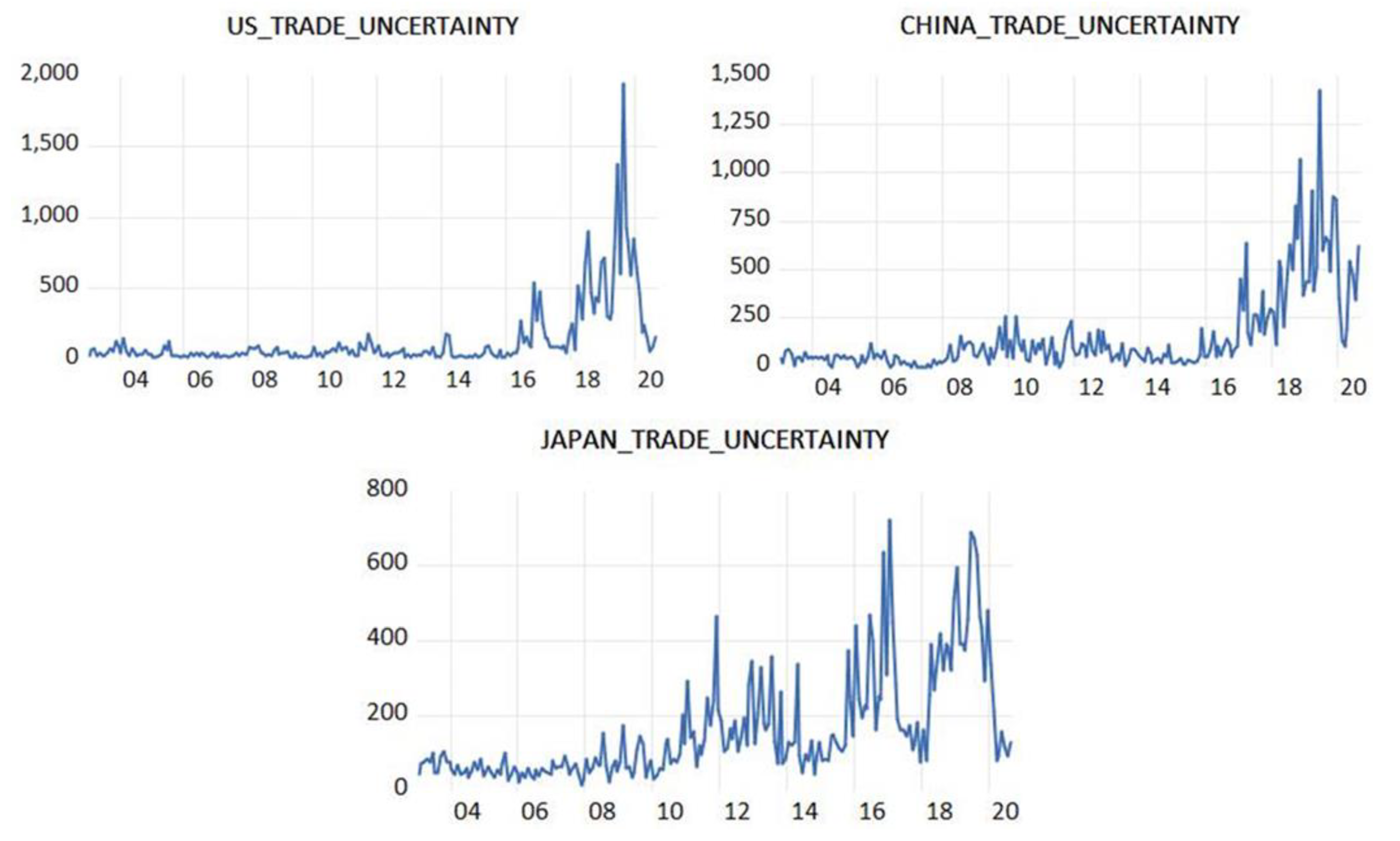

Figure 1 displays the values of the TPU index concerning the US, China and Japan, respectively. It can be observed that Japan exhibits large fluctuations in trade policy uncertainty throughout the entire last decade while the US and China present high trade uncertainty only since 2016 (the launch of Trump’s administration in the US).

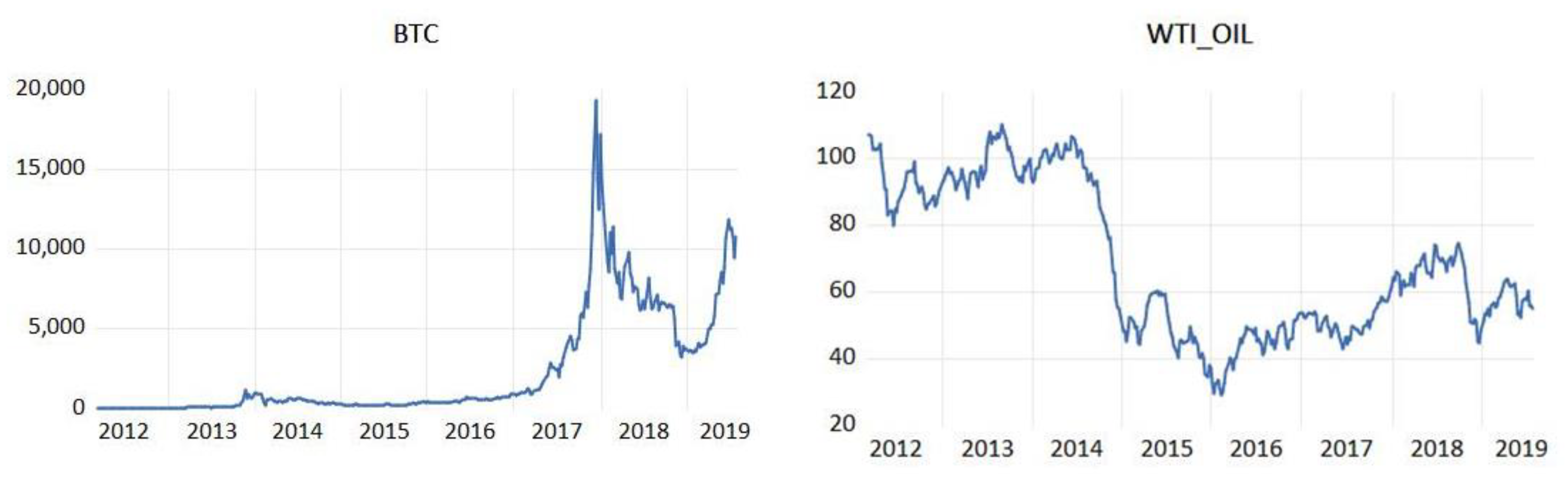

Figure 2 demonstrates the market values of Bitcoin and WTI oil. It can be seen that Bitcoin enjoyed a skyrocketing increase of its prices during the 2017 bull market. On the other hand, oil prices plummeted during 2014 because oil’s market value was too high during the early 21st century and demand from emerging countries was also high before 2014. Moreover, the appreciation of the US dollar during 2013 paved the way for this abrupt fall in oil prices.

We proceed to analyze the impacts that uncertainty in trade policy in the US and oil prices (that constitute a major determinant of economic growth) exert on the values of the most innovative form of liquidity and investment up to the present, which is Bitcoin. For the purposes of our estimations, we employ a battery of alternative ARCH and GARCH specifications. More specifically, ARCH, GARCH, threshold ARCH, Glosten-Jagannathan-Runkle (GJR) form of threshold ARCH, simple asymmetric ARCH, power ARCH, non-linear ARCH, non-linear GARCH, non-linear ARCH with one shift, non-linear GARCH with one shift, asymmetric power ARCH and asymmetric power GARCH specifications are adopted.

The Dickey–Fuller and Phillips–Perron tests are used in order to test for the existence of autocorrelation. The ARCH and GARCH methodologies and their specifications are appropriate for estimating fluctuations in volatility over time and suit well in order to examine highly risky financial assets such as Bitcoin. It should also be noted that the Akaike information criterion (AIC) (Akaike 1974) and information Bayesian criterion (SBC/BIC) (Schwarz 1978) criteria are employed in order to detect which specification is more suitable for this examination.

The ARCH (Engle 1982) and GARCH (Bollerslev 1986) models are introduced and support that the variance of the current error is a function of the volatility of the error conditions of previous time periods. The residual effect left unexplained by other models stands for the error conditions in these models.

The ARCH model can be represented by:

and the GARCH specification is given by:

Other specifications employed are given by Equations (3)–(8).

Non-linear GARCH:

Asymmetric Power GARCH:

Simple asymmetric ARCH based on Capie et al. (2005) and power ARCH based on Ding et al. (1993) are also adopted as alternative forms of non-linear ARCH and asymmetric power ARCH, respectively.

In order to select which of the aforementioned specifications is appropriate for estimating Bitcoin’s impacts received from TPU and crude oil, the AIC has been applied:

Moreover, the SBC/BIC has been adopted:

Lowest values in both criteria represent the best fit model for the estimations undertaken.

4. Econometric Results

A number of significant econometric results are brought about by employing a range of GARCH specifications in order to detect the nexus between Bitcoin market values and trade policy uncertainty as well as crude oil. The following Table 1a–c provides GARCH estimations about this linkage by adopting 12 different specifications. It should be noted that some alternative models could not be applied for the purposes of estimations of the specific relation between variables. Moreover, the AIC and SBC/BIC criteria have been employed in order to detect which methodology is more appropriate in this study.

From the tables, it can be seen that according to the AIC criterion the most suitable methodology is the application of the simple asymmetric ARCH model as this presents the lowest AIC value (985.013). Nevertheless, the SBC/BIC criterion indicates that the optimal model is the GARCH because the lowest BIC value (1006.054) is estimated for this among all methodologies used. These findings provide evidence that, indeed, GARCH-type specifications are needed in order to capture the special volatility characteristics of the variables under scrutiny. Based on the AIC criterion, Bitcoin exhibits asymmetric form volatility when examining its linkage with trade policy uncertainty. This can be attributed to the highly volatile character of this major cryptocurrency as well as the highly unexpected incidents (trade wars, tariffs) that generate trade policy uncertainty.

It should be emphasized that in almost all the estimations undertaken (except for the asymmetric power GARCH methodology) evidence is provided that trade policy uncertainty positively influences Bitcoin prices in a statistically significant manner. Furthermore, it is revealed that crude oil market values are negative determinants of Bitcoin prices also in a statistically trustworthy manner according to all methodologies (with the exception of the asymmetric power GARCH). Notably, in the majority of estimations, the impact of trade policy uncertainty on Bitcoin market value ranges from 0.2478 to 0.5596, while the asymmetric power GARCH results present a higher coefficient (0.7517) and GARCH results display that such uncertainty is very highly influential (2.2595). As concerns findings about crude oil impacts, the coefficient estimated ranges from −1.1499 to −0.1059, with the exception of the asymmetric power GARCH estimation (0.7271). Thereby, it can be seen in an overall perspective that trade policy uncertainty exerts positive effects in a medium extent towards Bitcoin market values. Moreover, econometric outcomes suggest that oil prices have strong impacts on Bitcoin values in a negative direction.

The economic implications of these findings are extremely important for policymakers and investors. Bitcoin enjoys a proliferating rhythm of popularity concerning investors’ preferences and since its bull market in a skyrocketing pace during 2017 has been among the most widely used financial assets in the effort of portfolio managers to improve their risk-return trade-off. Generally, Bitcoin is considered to be a risky asset due to its bubble characteristics (for more details see: Kyriazis et al. 2020). Nevertheless, there is academic work supporting that it can be categorized somewhere between the US dollar and gold as concerns safe haven characteristics (Dyhrberg 2016; Baur et al. 2018). Notably, recent studies have shown that as the Bitcoin market matures, this renders more similar to conventional assets and its speculatory character fades out (for more details see: Kyriazis 2019).

The modest and positive nexus between trade policy uncertainty and Bitcoin prices indicates that trade wars, higher tariffs and other events that hurt free trade led to the growth of speculative incentives among investors. That is, when conventional ways of wealth generating (trade) fail speculative forms of investments constitute a modestly connected alternative solution. Therefore, during financial turmoil that trade uncertainty is to blame, profit-seeking economic agents should include Bitcoin in their portfolios as this would highly likely lead to increases in their investment profits. Special emphasis should also be put in that lower oil prices negatively affect Bitcoin market values. When demand for oil is low, this means that economic activity is not vivid and investment plans are not as promising as would be desired if the economy was flourishing. Differently said, lower oil prices are significant indicators of crises, such as the COVID-19 pandemic (Sharif et al. 2020). Following a similar reasoning as above, it is easily discernible that low economic activity (as revealed by low oil prices) would lead to lower income for the majority of people and would highly likely increase their incentives to invest in risky and innovative financial assets in order not to suffer losses. Thereby, Bitcoin would enjoy higher demand and consequently higher market values. This is because a large number of investors would prefer to replace conventional assets with Bitcoin in order to safeguard a respectable level of profits and not suffer a much higher level of riskiness than with conventional assets that usually are bearish during crises.

For the reasons analyzed above, the innovative measure of trade policy uncertainty can offer fruitful indications to investors about how to re-arrange the synthesis of their portfolios when economic and trade conditions are not favorable for traditional investments. This would provide a roadmap for policymakers and economic agents in a worldwide level and significantly improve the perception of investors about the influence of adverse trade effects on financial markets and the macro economy.

5. Conclusions and Avenues for Further Research

This study constitutes an integrated survey on the impacts of trade policy uncertainty on a range on aspects of the economy and the financial sector. More specifically, the focus of our research is made on the macro economy, institutions, socio-economic mobility in the form of migration opportunities and financial markets. Although the bulk of relevant research is still not large, it reflects in a crystal-clear manner the potential for generating a highly proliferating body of academic work based on a range of remarkably interesting trade-related strands of literature in economics and finance.

Findings based on the thirteen primary studies under scrutiny provide evidence that high levels of trade policy uncertainty are responsible for a lot of failures in the real economy and the financial sector. Outcomes about the impacts of trade policy uncertainty on different facets of the economy reveal that if TPU decreases many benefits are brought about regarding major economies such as the US, China, Japan, Australia and the United Kingdom. It should be noted that the impacts on imports, exports and income in China appear to be modest and concern a large portion of the TPU academic literature. It is supported that China’s accession in the WTO has enabled easier entry into international markets and prevented exit from established markets. Moreover, it has incentivized Chinese producers and trade intermediaries and has boosted imports of high-quality and low-price products so increased potential benefits for consumers. Moreover, it is argued that lower trade uncertainty promotes higher migration by 24%. The migrants most perceptive of this impact are “non-hukou”, skilled and in their prime working age. Moreover, US–China trade conflicts cause positive impacts on the US stock market while the opposite happens regarding China.

Tariffs and bindings are connected with product growth in Australia. Furthermore, it is supported that compliance with the WTO agreements is essential for preserving imports and not suffer lower exporter-product varieties. Moreover, commodity prices in the US are substantially influenced from turbulent US trade conditions. Such co-movements are also enhanced by important political and economic events in a global level.

Furthermore, TPU makes an important giver of impacts towards Bitcoin when regime changes take place. This happens, especially, during the first and the last couple of Bitcoin’s trading. Another highly promising finding is that trade policy uncertainty is a positive determinant of commodity prices as significant co-motional predictions are brought to the surface. Notably, TPU also influences the strength of democratic institutions in a country as it found to strengthen democracy in a range of countries. This cast light on recently unknown aspects of political economics and offers the foundations for a highly promising new strand of literature.

Almost all the estimations conducted (except for the asymmetric power GARCH methodology) reveal that trade policy uncertainty positively influences and that crude oil market values negative impact Bitcoin prices also in a statistically significant manner. In the majority of estimations, the effect of TPU on Bitcoin market value mostly ranges from 0.2478 to 0.5596. By analyzing oil impacts, the coefficient estimated mostly takes values from −1.1499 to −0.1059. Therefore, trade policy uncertainty is found to exert positive and modest impacts towards Bitcoin prices whereas oil prices strongly and negatively influence Bitcoin values. The AIC and BIC criteria indicate that simple asymmetric ARCH and ARCH are the most appropriate specifications for estimations, respectively.

In an overall perspective, evidence reveals that high trade policy uncertainty urges towards non-optimal allocation of resources, imports of lower-quality and expensive products, less willingness to participation in international trade and a weakening of democratic sentiment. Moreover, instability in trade conditions impedes internal migration and constitutes an obstacle to socio-economic mobility. Apart from that, higher TPU is linked to higher levels of volatility in risky assets. Generally, trade policy uncertainty is a giver of impacts in a modest level but covers a wide variety of economic and financial domains. As concerns the empirical estimations undertaken in this study, it is documented that TPU strengthens speculator incentives among investors as traditional investment assets are not profitable. The inclusion of Bitcoin in portfolios would help investors preserve a satisfactory trade-off level of risk-return. Moreover, oil prices display negative nexus with Bitcoin market values due to weak economic activity during uncertain periods.

There is a threefold contribution of this study. Firstly, it helps understanding trade policy uncertainty and its impacts and provides a bird’s-eye view of its nexus with the macro economy, institutions, socio-economic matters like migration, as well as financial markets (stocks, cryptocurrencies and commodities). Secondly, it constitutes an integrated survey of advanced theoretical and empirical research on trade policy uncertainty not only after but also before the breakthrough by the Caldara et al. (2020) index took place. Furthermore, econometric outcomes by a large spectrum of ARCH and GARCH specifications provide insights on how trade policy uncertainty and crude oil influence prices of highly speculative assets, such as Bitcoin. Thereby, the strenuous task of casting light on every aspect of trade policy effects is undertaken.

This integrated survey could provide a compass for taking safer investment decisions during periods of uncertainty in trade policies and provide a beneficial boost to literature about the highly promising strand of TPU effects in economics and finance. Avenues for further research related to trade policy uncertainty could include examination of a larger range of studies and estimation of the nexus with alternative macroeconomic variables traditional or sophisticated financial products. It would be extremely interesting to investigate deeper into the TPU linkage with social mobility and demographic or labor characteristics as well as to examine effects on other than democratic regimes. The creation of TPU indices concerning European countries or less advanced regions would significantly help towards the development of this remarkably promising domain of economics and finance.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data sharing not applicable.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Basic characteristics of studies investigating trade policy uncertainty.

| Authors | Journal | Variables | Data Source | Period | Country | Methodology | Findings |

|---|---|---|---|---|---|---|---|

| Caldara et al. (2020) | JME | Three measures of US Trade Policy Uncertainty Tariff rates Firm-level and aggregate macroeconomic data | 11 newspapers (Boston Globe, Chicago Tribune, Guardian, Los Angeles Times, New York Times, Wall Street Journal, Washington Post) Compustat | 1960–2018 | USA | Open-economy New Keynesian DSGE model with a discrete choice of entering and exiting the export market Calibration Regressions Vector Autoregressions (VAR) | Higher TPU results in lower US business investment by 1% while VAR outcomes present even greater reduction |

| Crowley et al. (2018) | JIE | Chinese trade transactions Tariffs Macroeconomic data on real GDP and exchange rates | Chinese Customs Database (CCD) by China’s General Administration of Customs Global Antidumping Database (GAD) by Chad Bown and maintained by the World Bank World Bank’s Development Indicators database USDA Economic Research Service | 2000–2009 | China 33 countries (20 largest export destinations and countries with antidumping duties against China) | Model based on Handley and Limao (2015) Panel regressions | High trade policy uncertainty urges Chinese firms to exit established foreign markets and become more hesitant towards entering new foreign markets. |

| Facchini et al. (2019) | JIE | US Trade Policy Uncertainty Internal migration Exports (firm-level data) Industry skill-intensity data Tariffs Pervasiveness of barriers to investment in China US Multi Fiber Agreement (MFA) quota Availability of production subsidies to Chinese firms | China’s Population Census China Custom Data (CCD) (also called “China Import and Export data”) from World Integrated Trading Solution (WITS) database 2004 China’s Annual Survey of Industrial Firms (CASIF) (also known as “Chinese Industrial Enterprises Database”) | 2000–2005 | USA China | Panel estimations | Higher migrationin China by 24% due to lower TPU. The migrants most responsive are “non-hukou”, skilled and in their prime working age |

| Feng et al. (2017) | JIE | Firm-product level dataset Fixed export costs (measured as fixed assets of exporting firms or as the intermediary share of exports) Tariffs New entrant and exiter margins | China’s manufacturing survey data | 2000–2006 | China connected to USA and European Union | Heterogeneous firm model based on Handley and Limao (2015) Panel regressions | Lower Chinese tariff policy uncertainty determined aggregate reallocation of Chinese exports and encouraged participation by exporters with higher-quality and lower-price products |

| Gozgor et al. (2019) | FRL | Bitcoin price index USA Trade Policy Uncertainty (TPI) | www.coindesk.com www.policyuncertainty.com | July 2010–August 2018 | USA | Wavelet Power Spectrum (WPS) methodology by Torrence and Compo (1998) Cross Wavelet Transform (CWT) method by Grinsted et al. (2004) Wavelet Coherency (WTC) method by Grinsted et al. (2004) VAR-based frequency domain Granger causality by Breitung and Candelon (2006) | USA TPU positively and significantly affects Bitcoin returns but exert a negative impact on these returns during extreme events (regime change) |

| Handley (2014) | JIE | Tariffs Bindings for Australia’s Uruguay Round Commitments Import data | UNCTAD TRAINS database via the World Integrated Trade Solution (WITS) WTO’s consolidated tariff schedules (CTS) by the Tariff Analysis On-line database Australian Bureau of Statistics | 1993–2001 | Australia | Dynamic heterogeneous firms model | Growth of exporter-product varieties would have been 7% lower if no binding commitments took place by the WTO after 1996 If no tariffs and bindings existed, over 50% of predicted product growth would be linked with uncertainty WTO commitments could lead to lower uncertainty and higher product entry |

| He et al. (2020) | FRL | S&P500 Shanghai Composite Index | - | January 2000–April 2019 | USA China | TVP-SV-VAR by Nakajima (2011) | US–China trade conflicts generate positive effects on the US stock market whereas negative impacts on the Chinese stock market |

| Imbruno (2019) | JCE | Imports at the country/product/firm level Applied tariffs Bound tariffs Non-tariff trade barriers | Chinese Customs Trade Statistics (CCTS) World Bank’s World Integrated Trade Solution (WITS) database WTO’s Consolidated Tariff Schedules (CTS) database China’s Protocol of the WTO accession | 2000–2006 | China | Panel regression with dummies Linear probability model | Lower Chinese TPU leads to multinationals relocating the downstreame stages of global value chains in China more than the upstream stages. So they are market-seeking rather than resource-seeking in China. |

| Karabulut et al. (2020) | EAP | World Trade Uncertainty Index by Ahir et al. (2018) US Commodity Price Index (CPI) | IMF database | January 1996–September 2019 | USA | VAR based on Breitung and Candelon (2006) Granger causality by Granger (1969) Continuous Wavelet Transform (CWT), Wavelet Coherency (WC), Wavelet Power Spectrum (WPS) based on Ramsey (1999) | Strong noises concerning world trade uncertainty between 2009–2010 and 2015–2016 as well as for CPI between 2008–2009 and 2015–2016 and between 2008–2009 and 2017–2018. Co-movements linked with important political and economic events |

| Steinberg (2019) | JIE | Macroeconomic variables Prices | World Input Output Database (Timmer et al. 2015) EFIGE dataset (Altomonte and Aquilante 2012) World Bank Exporter Dynamics Database (Fernandes et al. 2016) | Since 2011 | UK European Union Rest of the world | Dynamic General Equilibrium Model with heterogeneous firms, endogenous export participation and stochastic trade costs Regime construction Calibration | The total consumption-equivalent welfare cost due to Brexit is between 0.4% and 1.2% but uncertainty is repsonsible for less than 25% of this cost |

| Steinberg (2020) | JME | Firm-level TPU dataset of Caldara et al. (2020) linked to the US input–output accounts Trade exposure (export exposure, imported input exposure) | US Bureau of Economic Analysis Compustat | 1960–2018 | USA | DSGE model with sticky prices and sunk exporting costs Simple model of price- setting under nominal rigidities | A number of issues arise concerning Caldara et al. (2020) |

| Tian et al. (2020) | EM | 3-year and 5-year uncertainty measures based on Jurado et al. (2015) Polity2score (democracy) | Data from Glick and Rose (2016) Data from Marshall et al. (2015) | 1960–2013 | 194 countries | Ordinary Least Squares (OLS) Generalized Method of Moments (GMM) by Blundell and Bond (1998) | Higher income leads to democratic transitions but mainly in developing countries |

Notes: EAP, EM, FRL, JCE, JIE and JME stand for Economic Analysis and Policy, Economic Modelling, Finance Research Letters, Journal of Comparative Economics, Journal of International Economics and Journal of Monetary Economics.

Figure A1.

Google Scholar citations and Plum-X citations (as of 7 September 2020).

Figure A2.

Plum-X captures (as of 7 September 2020).

Figure A3.

Tweets per paper (as of 7 September 2020).

References

- Ahir, Hites, Nicholas Bloom, and Davide Furceri. 2018. The World Uncertainty Index. Available online: http://0-dx-doi-org.brum.beds.ac.uk/10.2139/ssrn.3275033 (accessed on 10 September 2020).

- Akaike, Hirotugu. 1974. A new look at the statistical model identification. IEEE Transactions on Automatic Control 19: 716–23. [Google Scholar] [CrossRef]

- Altomonte, Carlo, and Tommaso Aquilante. 2012. The EU-EFIGE/Bruegel-Unicredit Dataset (No. 2012/13). Bruegel Working Paper. Brussels: Bruegel, Available online: https://www.bruegel.org/2012/10/the-eu-efigebruegel-unicredit-dataset/ (accessed on 10 September 2020).

- Baier, Scott L., and Jeffrey H. Bergstrand. 2004. Economic determinants of free trade agreements. Journal of international Economics 64: 29–63. [Google Scholar] [CrossRef] [Green Version]

- Baur, Dirk G., Thomas Dimpfl, and Konstantin Kuck. 2018. Bitcoin, gold and the US dollar—A replication and extension. Finance Research Letters 25: 103–10. [Google Scholar] [CrossRef]

- Ben-David, Dan. 1993. Equalizing exchange: Trade liberalization and income convergence. The Quarterly Journal of Economics 108: 653–79. [Google Scholar] [CrossRef]

- Bhagwati, Jagdish, and Vangal K. Ramaswami. 1963. Domestic distortions, tariffs and the theory of optimum subsidy. Journal of Political Economy 71: 44–50. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef] [Green Version]

- Bollerslev, Tim. 1986. Glossary to ARCH (GARCH). In Volatility and Time Series Econometrics Essays in Honor of Robert Engle. MarkWatson, Tim Bollerslev and Jerey. Oxford: University Press. [Google Scholar]

- Breitung, Jörg, and Bertrand Candelon. 2006. Testing for short-and long-run causality: A frequency-domain approach. Journal of Econometrics 132: 363–78. [Google Scholar] [CrossRef]

- Burstein, Ariel, and Javier Cravino. 2015. Measured aggregate gains from international trade. American Economic Journal: Macroeconomics 7: 181–218. [Google Scholar] [CrossRef] [Green Version]

- Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo. 2020. The economic effects of trade policy uncertainty. Journal of Monetary Economics 109: 38–59. [Google Scholar] [CrossRef]

- Capie, Forrest, Terence C. Mills, and Geoffrey Wood. 2005. Gold as a hedge against the dollar. Journal of International Financial Markets, Institutions and Money 15: 343–52. [Google Scholar] [CrossRef]

- Crowley, Meredith, Ning Meng, and Huasheng Song. 2018. Tariff scares: Trade policy uncertainty and foreign market entry by Chinese firms. Journal of International Economics 114: 96–115. [Google Scholar] [CrossRef] [Green Version]

- Dasgupta, Partha, and Joseph Stiglitz. 1977. Tariffs vs. quotas as revenue raising devices under uncertainty. The American Economic Review 67: 975–81. [Google Scholar]

- Ding, Zhuanxin, Clive W. J. Granger, and Robert F. Engle. 1993. A long memory property of stock market returns and a new model. Journal of Empirical Financ 1: 83–106. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016. Bitcoin, gold and the dollar—A GARCH volatility analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef] [Green Version]

- Edmond, Chris, Virgiliu Midrigan, and Daniel Yi Xu. 2015. Competition, markups, and the gains from international trade. American Economic Review 105: 3183–221. [Google Scholar] [CrossRef] [Green Version]

- Edwards, Sebastian. 1997. Trade policy, growth, and income distribution. The American Economic Review 87: 205–10. [Google Scholar]

- Engle Robert, F. 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the Econometric Society 50: 987–1007. [Google Scholar] [CrossRef]

- Facchini, Giovanni, Maggie Y. Liu, Anna Maria Mayda, and Minghai Zhou. 2019. China’s “Great Migration”: The impact of the reduction in trade policy uncertainty. Journal of International Economics 120: 126–44. [Google Scholar] [CrossRef]

- Feenstra, Robert C. 1992. How costly is protectionism? Journal of Economic Perspectives 6: 159–78. [Google Scholar] [CrossRef] [Green Version]

- Feng, Ling, Zhiyuan Li, and Deborah L. Swenson. 2017. Trade policy uncertainty and exports: Evidence from China’s WTO accession. Journal of International Economics 106: 20–36. [Google Scholar] [CrossRef] [Green Version]

- Fernandes, Ana M., Caroline Freund, and Martha Denisse Pierola. 2016. Exporter Behavior, Country Size and Stage of Development: Evidence from the Exporter Dynamics Database. Washington, DC: The World Bank. [Google Scholar]

- Findlay, Ronald, and Stanislaw Wellisz. 1982. Endogenous tariffs, the political economy of trade restrictions, and welfare. In Import Competition and Response. Chicago: University of Chicago Press, pp. 223–44. [Google Scholar]

- Foellmi, Reto, and Manuel Oechslin. 2010. Market imperfections, wealth inequality, and the distribution of trade gains. Journal of International Economics 81: 15–25. [Google Scholar] [CrossRef] [Green Version]

- Glick, Reuven, and Andrew K. Rose. 2016. Currency unions and trade: A post-EMU reassessment. European Economic Review 87: 78–91. [Google Scholar] [CrossRef]

- Glosten, Lawrence R., Ravi Jagannathan, and David E. Runkle. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance 48: 1779–801. [Google Scholar]

- Gozgor, Giray, Aviral Kumar Tiwari, Ender Demir, and Sagi Akron. 2019. The relationship between Bitcoin returns and trade policy uncertainty. Finance Research Letters 29: 75–82. [Google Scholar] [CrossRef]

- Granger, Clive W. J. 1969. Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society 37: 424–38. [Google Scholar] [CrossRef]

- Grinsted, Aslak, John C. Moore, and Svetlana Jevrejeva. 2004. Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Processes in Geophysics 11: 561–66. [Google Scholar] [CrossRef]

- Grossman, Gene M., and Elhanan Helpman. 1993. The Politics of free Trade Agreements (No. w4597). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Handley, Kyle. 2014. Exporting under trade policy uncertainty: Theory and evidence. Journal of International Economics 94: 50–66. [Google Scholar] [CrossRef] [Green Version]

- Handley, Kyle, and Nuno Limao. 2015. Trade and investment under policy uncertainty: Theory and firm evidence. American Economic Journal: Economic Policy 7: 189–222. [Google Scholar] [CrossRef] [Green Version]

- He, Feng, Brian Lucey, and Ziwei Wang. 2020. Trade Policy Uncertainty and its Impact on the Stock Market-evidence from China-US trade conflict. Finance Research Letters. [Google Scholar] [CrossRef]

- Higgins, Matthew L., and Anil K. Bera. 1992. A class of nonlinear ARCH models. International Economic Review 33: 137–58. [Google Scholar] [CrossRef]

- Imbruno, Michele. 2019. Importing under trade policy uncertainty: Evidence from China. Journal of Comparative Economics 47: 806–26. [Google Scholar] [CrossRef]

- Jurado, Kyle, Sydney C. Ludvigson, and Serena Ng. 2015. Measuring uncertainty. American Economic Review 105: 1177–216. [Google Scholar] [CrossRef]

- Karabulut, Gokhan, Mehmet Huseyin Bilgin, and Asli Cansin Doker. 2020. The relationship between commodity prices and world trade uncertainty. Economic Analysis and Policy. [Google Scholar] [CrossRef]

- Kimbrough, Kent P. 1985. Tariffs, quotas and welfare in a monetary economy. Journal of International Economics 19: 257–77. [Google Scholar] [CrossRef]

- Krueger, Anne O. 1980. Trade Policy as an Input to Development (No. w0466). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Krueger, Anne O. 1997. Trade Policy and Economic Development: How We Learn (No. w5896). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Krugman, Paul. 1991. The move toward free trade zones. Economic Review 76: 5. [Google Scholar]

- Kyriazis, Nikolaos A. 2019. A survey on efficiency and profitable trading opportunities in cryptocurrency markets. Journal of Risk and Financial Management 12: 67. [Google Scholar] [CrossRef] [Green Version]

- Kyriazis, Nikolaos, Stephanos Papadamou, and Shaen Corbet. 2020. A Systematic Review of the Bubble Dynamics of Cryptocurrency Prices. Research in International Business and Finance 54: 101254. [Google Scholar] [CrossRef]

- Levy, Philip I. 1997. A political-economic analysis of free-trade agreements. The American Economic Review 87: 506–19. [Google Scholar]

- Li, Chunding, Chuantian He, and Chuangwei Lin. 2018. Economic impacts of the possible China–US trade war. Emerging Markets Finance and Trade 54: 1557–77. [Google Scholar] [CrossRef]

- Li, Minghao, Edward J. Balistreri, and Wendong Zhang. 2020. The US–China trade war: Tariff data and general equilibrium analysis. Journal of Asian Economics 69: 101216. [Google Scholar] [CrossRef]

- Lindé, Jesper, and Andrea Pescatori. 2019. The macroeconomic effects of trade tariffs: Revisiting the lerner symmetry result. Journal of International Money and Finance 95: 52–69. [Google Scholar] [CrossRef] [Green Version]

- Marshall, Monty G., G. Ted Robert, and Keith Jaggers. 2015. Polity IV Project: Political Regime Characteristics and Transitions, 1800–2015. Available online: http://www.systemicpeace.org/inscr/p4manualv2016.pdf (accessed on 10 September 2020).

- Myint, Hla. 1954. The gains from international trade and the backward countries. The Review of Economic Studies 22: 129–42. [Google Scholar] [CrossRef]

- Nakajima, Jouchi. 2011. Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Monetary and Economic Studies 29: 107–42. [Google Scholar]

- Ossa, Ralph. 2014. Trade wars and trade talks with data. American Economic Review 104: 4104–46. [Google Scholar] [CrossRef] [Green Version]

- Ramsey, James B. 1999. The Contribution of Wavelets to the Analysis of Economic and Financial Data. Philosophical Transactions: Mathematical, Physical and Engineering Sciences 357: 2593–606. [Google Scholar] [CrossRef]

- Rodriguez, Francisco, and Dani Rodrik. 2000. Trade policy and economic growth: A skeptic’s guide to the cross-national evidence. NBER Macroeconomics Annual 15: 261–325. [Google Scholar] [CrossRef]

- Samuelson, Paul A. 1939. The gains from international trade. The Canadian Journal of Economics and Political Science/Revue Canadienne d’Economique Et De Science Politique 5: 195–205. [Google Scholar] [CrossRef]

- Samuelson, Paul Anthony. 1962. The gains from international trade once again. The Economic Journal 72: 820–29. [Google Scholar] [CrossRef]

- Schwarz, Gideon. 1978. Estimating the dimension of a model. The Annals of Statistics 6: 461–64. [Google Scholar] [CrossRef]

- Sharif, Arshian, Chaker Aloui, and Larisa Yarovaya. 2020. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis 70: 101496. [Google Scholar] [CrossRef]

- Steinberg, Joseph B. 2019. Brexit and the macroeconomic impact of trade policy uncertainty. Journal of International Economics 117: 175–95. [Google Scholar] [CrossRef] [Green Version]

- Steinberg, Joseph B. 2020. Comment on: “The economic effects of Trade Policy Uncertainty” by Dario Caldara, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo. Journal of Monetary Economics 109: 60–64. [Google Scholar] [CrossRef]

- Tian, Jilin, Nicholas Sim, Wenshou Yan, and Yanyun Li. 2020. Trade uncertainty, income, and democracy. Economic Modelling. [Google Scholar] [CrossRef]

- Timmer, Marcel P., Erik Dietzenbacher, Bart Los, Robert Stehrer, and Gaaitzen J. De Vries. 2015. An illustrated user guide to the world input–output database: The case of global automotive production. Review of International Economics 23: 575–605. [Google Scholar] [CrossRef]

- Torrence, Christopher, and Gilbert P. Compo. 1998. A practical guide to wavelet analysis. Bulletin of the American Meteorological Society 79: 61–78. [Google Scholar] [CrossRef] [Green Version]

- Zakoian, Jean-Michel. 1994. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18: 931–55. [Google Scholar] [CrossRef]

| 1 |

Figure 1.

Trade policy uncertainty in the US, China and Japan.

Figure 2.

Bitcoin and WTI oil market values.

Table 1.

Econometric outcomes based on (a) ARCH, GARCH, threshold ARCH, and GJR-form of threshold ARCH specifications; (b) simple asymmetric ARCH, power ARCH, non-linear ARCH and non-linear GARCH specifications; (c) non-linear ARCH with one shift, non-linear GARCH with one shift, asymmetric power ARCH and asymmetric power GARCH specifications.

Table 1.

Econometric outcomes based on (a) ARCH, GARCH, threshold ARCH, and GJR-form of threshold ARCH specifications; (b) simple asymmetric ARCH, power ARCH, non-linear ARCH and non-linear GARCH specifications; (c) non-linear ARCH with one shift, non-linear GARCH with one shift, asymmetric power ARCH and asymmetric power GARCH specifications.

| (a) | |||||

| ARCH | GARCH | Threshold ARCH | GJR-Form of Threshold ARCH | ||

| Mean equation | TPU | 2.2595 (0.000) *** | 0.3661 (0.000) *** | 0.4434 (0.000) *** | 0.259 (0.000) *** |

| Oil | −0.1069 (0.000) *** | −0.6985 (0.000) *** | −0.3336 (0.000) *** | −0.1059 (0.000) *** | |

| constant | 5.513 (0.000)*** | 7.2684 (0.000)*** | 5.578 (0.000)*** | 5.5132 (0.000) *** | |

| Variance equation | Arch | 1.0375 (0.000) *** | 0.9683 (0.000) *** | 0.9585 (0.005) *** | |

| Abarch | 0.9272 (0.000) *** | ||||

| Atarch | 0.0452 (0.843) | ||||

| Tarch | 0.1435 (0.746) | ||||

| Garch | 0.0988 (0.224) | ||||

| Constant | 0.01 (0.000) *** | 0.0082 (0.145) | 0.0761 (0.001) *** | 0.0099 (0.000) *** | |

| AIC | 986.262 | 1034.152 | 1014.299 | 987.516 | |

| BIC | 1006.054 | 1057.903 | 1038.05 | 1011.267 | |

| (b) | |||||

| Simple Asymmetric ARCH | Power ARCH | Non-linear ARCH | Non-linear GARCH | ||

| Mean equation | TPU | 0.2478 (0.000) *** | 0.5553 (0.000) *** | 0.5477 (0.000) *** | 0.501 (0.000) *** |

| Oil | −0.0702 (0.018) ** | −1.134 (0.000) *** | −1.1087 (0.000) *** | −1.1499 (0.000) *** | |

| constant | 5.42 (0.000) *** | 8.0777 (0.000) *** | 8.0137 (0.000) *** | 8.3442 (0.000) *** | |

| Variance equation | Arch | 1.036 (0.000) *** | |||

| Saarch | 0.0663 (0.147) | ||||

| Parch | 0.9905 (0.002) *** | ||||

| Narch | 0.9793 (0.000) *** | 0.7593 (0.001) *** | |||

| Narch_k | −0.0391 (0.356) | −0.0619 (0.084) * | |||

| Garch | 0.2157 (0.001) *** | ||||

| Constant | 0.0096 (0.000) *** | 0.0341 (0.601) | 0.0253 (0.000) *** | 0.0129 (0.000) *** | |

| Power | 1.7719 (0.122) | ||||

| AIC | 985.013 | 1033.445 | 1032.704 | 1028.214 | |

| BIC | 1008.764 | 1057.196 | 1056.455 | 1055.923 | |

| (c) | |||||

| Non-linear ARCH with one shift | Non-linear GARCH with one shift | Asymmetric Power ARCH | Asymmetric Power GARCH | ||

| Mean equation | TPU | 0.5476 (0.000) *** | 0.501 (0.000) *** | 0.5596 (0.000) *** | 0.7517 (0.000) *** |

| Oil | −1.1087 (0.000) *** | −1.1499 (0.000) *** | −1.1351 (0.000) *** | 0.7271 (0.000) *** | |

| constant | 8.0137 (0.000) *** | 8.3442 (0.000) *** | 8.0702 (0.000) *** | 0.4941 (0.199) | |

| Narch | 0.9793 (0.000) *** | 0.7593 (0.001) *** | |||

| Narch_k | −0.0391 (0.356) | −0.0619 (0.084) * | |||

| Aparch | 0.9505 (0.002) *** | 1.0525 (0.001) *** | |||

| Aparch_e | 0.0569 (0.702) | 0.0368 (0.725) | |||

| Garch | 0.2157 (0.001) *** | −0.0286 (0.737) | |||

| Constant | 0.0253 (0.000) *** | 0.0129 (0.000) *** | 0.0453 (0.532) | 0.0472 (0.423) | |

| Power | 1.5837 (0.1) | 2.5123 (0.014) ** | |||

| AIC | 1032.704 | 1028.214 | 1035.267 | 1022.707 | |

| BIC | 1056.455 | 1055.923 | 1062.976 | 1054.374 | |

Note: *, **, *** stand for 90%, 95%, and 99% levels of statistical significance, respectively.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kyriazis, N.A. Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation. J. Risk Financial Manag. 2021, 14, 41. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010041

AMA Style

Kyriazis NA. Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation. Journal of Risk and Financial Management. 2021; 14(1):41. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010041

Chicago/Turabian StyleKyriazis, Nikolaos A. 2021. "Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation" Journal of Risk and Financial Management 14, no. 1: 41. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010041