Slow Steaming as Part of SECA Compliance Strategies among RoRo and RoPax Shipping Companies

1

Department of Business Administration, University of Gothenburg, 405 30 Gothenburg, Sweden

2

SSPA Sweden AB, 412 58 Gothenburg, Sweden

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(5), 1435; https://0-doi-org.brum.beds.ac.uk/10.3390/su11051435

Submission received: 29 December 2018

/

Revised: 27 February 2019

/

Accepted: 2 March 2019

/

Published: 8 March 2019

(This article belongs to the Special Issue Sustainable Short Sea Shipping)

Abstract

:Many geographically peripheral member states of the EU are critically dependent on short sea Roll-on/Roll-off (RoRo) and mixed freight–passenger (RoPax) shipping services for intra-European trade. The implementation of the Sulfur Emission Control Area (SECA) regulation was expected to raise the operating cost for RoRo and RoPax shipping, and slow steaming was proposed as an immediate solution to save the increased cost. Previous research has investigated the issue of slow steaming and SECA using a quantitative approach. However, the reaction of the RoRo and RoPax shipping firms toward slow steaming as a mitigating factor in the face of expected additional SECA compliance costs using qualitative methodology has not been explored yet. In addition, the knowledge regarding the impact of slow steaming on the competitiveness of short sea RoRo and RoPax with respect to service quality is limited. This article has addressed these issues through the analysis of multiple cases focusing on RoRo and RoPax firms operating in the North and Baltic Seas. Overall, our findings suggest that the 0.1% SECA regulation of 2015 requiring the use of higher-priced MGO has not caused slow steaming in the RoRo and RoPax segments to a large extent. The increased bunker prices are partially transferred to the customers via increased Bunker Adjustment Factor and partly borne by the shipowners. We have found that out of 11 case firms in our study only one RoRo and one RoPax firm have reduced vessel speeds to compensate for the additional SECA compliance costs. We conclude that for RoPax and RoRo segment bunker prices, rigorous competition and, most important, different service quality requirements have significantly restricted the potential implementation of slow steaming.

1. Introduction

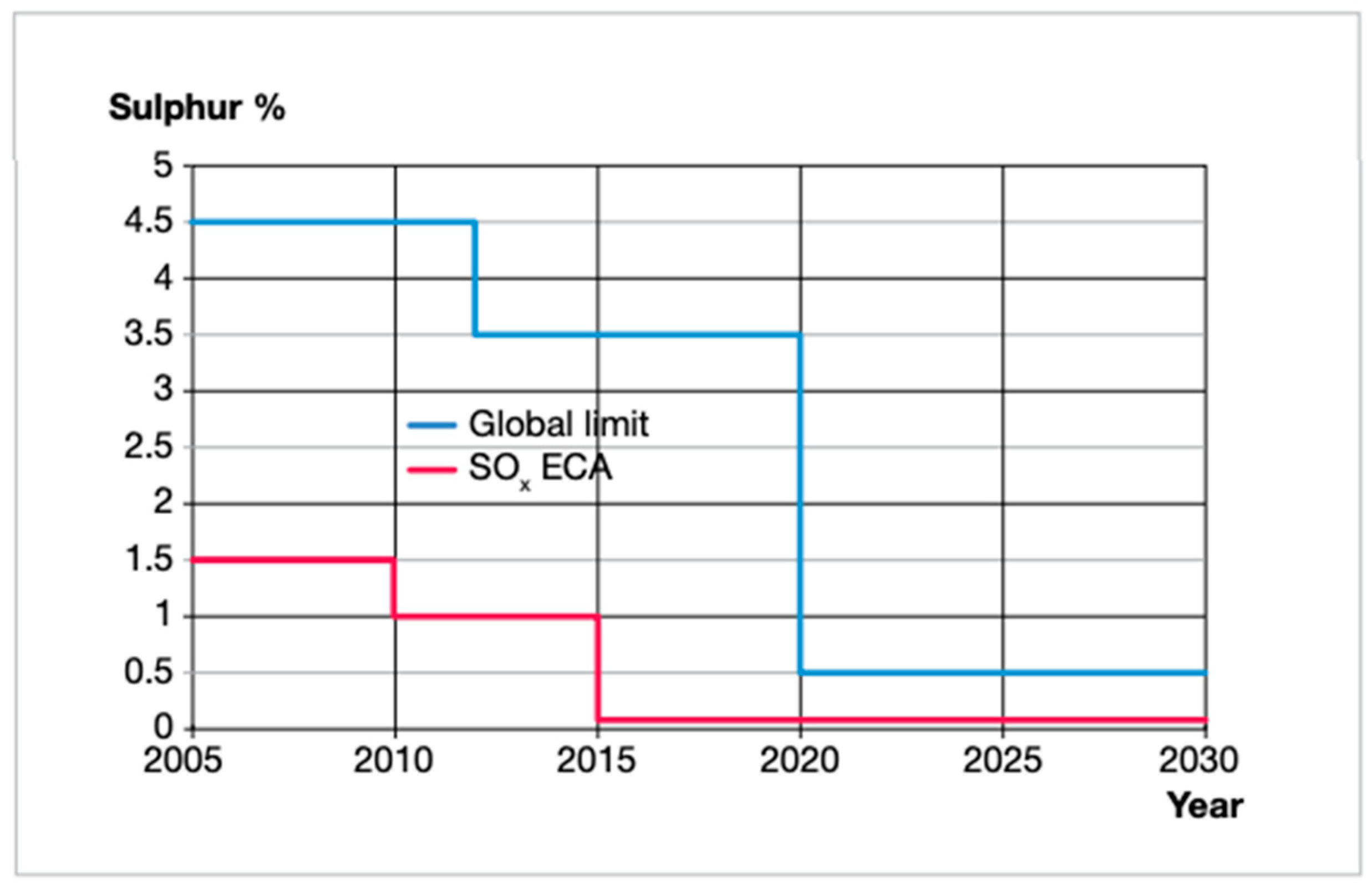

Over the past several decades, emissions of noxious gases from maritime transport have considerably amplified, although the role of shipping for world trade continues to be strong [1]. To mitigate rising shipping emissions, in particular sulfur oxides (SOx), the International Maritime Organization (IMO)—under Annex VI to the International Convention for the Prevention of Pollution from Ships (MARPOL Convention)—introduced limits on the maximum sulfur content allowed in the fuel used by ships [2]. Currently this regulation is implemented in specific zones called sulfur emission control areas (SECAs), where the stringent sulfur limits are applied progressively. All ships sailing in SECAs, which include the Baltic Sea, the North Sea, the English Channel, the North American east and west coasts, and the US Caribbean area, are now subject to this regulation. Under the sulfur regulation from 1 January 2015, the level of allowed sulfur content in the fuel of ships was reduced to 0.1 percent. Furthermore, the regulation stipulates that from 2020, the global limit of allowed sulfur content will be 0.5% for ships sailing outside the SECAs [3]. The progression of sulfur limits within and outside the SECAs is presented in Figure 1:

In total, nearly 14,000 ships are active in the SECAs each year. From this total, about 2200 ships operate 100% in the area, while 2700 ships spend more than 50% of their time in the region [5,6]. Before and after the implementation of the 0.1% sulfur limit in SECAs, multiple research studies were conducted providing a techno-economic analysis of the two major compliance alternatives, namely scrubbers and low sulfur marine gas oil (MGO) available to shipowners. In this respect, Zis, et al. [7] found that the scrubber installation reduces the ship operating cost; however, the lower bunker prices delay the payback period of a scrubber investment. In addition, the findings of Jiang, et al. [8] and Lindstad, et al. [9] indicate that a scrubber is a better compliance option when the price spread between heavy fuel oil (HFO) and MGO is high (more than 231 Euros per ton), when the remaining lifespan of a vessel is more than 4 years, and when the vessel operates on a long-distance route with high fuel consumption.

On the other hand, it was forecast [10] that, due to the uncertain future of fuel prices as well as technological and regulatory uncertainty, a majority of shipping companies would switch to distillates such as marine gas oil (MGO) to conform to the sulfur regulation. A report by BPO [11] revealed that at the beginning of 2016 there were only 83 ships with scrubber installations and that this number was expected to exceed 200 by 2017. However, this represents a minority share of the 2200 ships sailing in the SECAs and corroborates the feeling that the majority of shipowners preferred low-sulfur fuel as a compliance solution.

The compliance with the sulfur regulation was predicted to negatively affect the competitiveness of short sea shipping (SSS), in particular the Roll-on/Roll-off pure freight (RoRo) and mixed freight–passenger (RoPax) sectors operating in the North and Baltic Seas, by substantially increasing their operating costs [12]. In this context, a reduction in sailing speed—also termed ‘slow steaming’—as an energy efficiency measure is deemed an immediately feasible approach for reducing operating costs and cutting the shipping carbon footprints on the environment [13]. Due to the cubic relationship between speed and fuel consumption, which is even higher than a cubic as asserted by Psaraftis and Kontovas [14], particularly for ships that sail at a comparatively faster speed—such as containerships, RoRo, and RoPax—a nominal speed reduction leads to a substantial saving in total fuel consumption. In the existing literature, different speed optimization models and the cost-saving potential of slow steaming for the European RoRo segment in the context of SECA regulations have been identified [15] as low-impact fixes.

Admittedly, slow steaming is somewhat complicated for tank and bulk shipping, and still more complicated for deep-sea liner shipping. However, it is truly complex for RoRo and RoPax shipping, as the RoRo and RoPax segments face fierce competition not only from the neighboring shipping routes but also from land transport modes. Any speed reduction could affect the competitiveness of SSS in the form of service quality (SQ). Earlier research has approached the issue of slow steaming from multiple angles. In this context, using the route-specific data for 2014 and 2015 for RoRo and RoPax services, Zis and Psaraftis [16] quantitatively assessed the potential of slow steaming as an operational measure that could be deployed by shipowners to lower the operating costs in SECAs. Along the same line, Santos and Guedes Soares [17] developed a methodology to determine the optimum ship speed considering the RoRo ship operations in SECAs.

We have noticed that the existing research has explored the potential of slow steaming in the SECAs primarily deploying the quantitative methods. However, there is insufficient knowledge related to the actual reaction of RoRo and RoPax shipping companies pertaining to slow steaming in the aftermath of the 0.1 percent sulfur regulation of 2015. In addition, the knowledge is limited regarding the impact of slow steaming on the competitiveness of short sea RoRo and RoPax with respect to service quality.

Thus, the purpose of this article is to qualitatively investigate the feasibility of slow steaming for the RoRo and RoPax sectors in the context of SECA regulations. More specifically, we seek to identify the reaction of RoRo and RoPax firms toward slow steaming in the wake of the North Sea and Baltic Sea sulfur regulations, and to investigate how slow steaming affects competitiveness in these sectors. This is done through an in-depth analysis of multiple cases focusing on RoRo and RoPax firms. The data for this study is derived from the existing literature as well as from several interviews of the management of RoRo and RoPax firms operating vessels in the North and Baltic Seas emission control areas.

The article is structured as follows. A brief literature review focusing on SECA, slow steaming and competitiveness is presented in Section 2. Section 3 addresses the methodology, while Section 4 presents the findings of our analysis. Section 5 discusses the results and concludes the research implications.

2. Literature Review

2.1. SECA Regulation and Its Implications

Sea transport growth has caused a commensurate upsurge in anthropogenic aquatic and air contamination, and in order to mitigate the escalating airborne emissions from vessels, various regulations are being imposed at the global and regional levels. One of the instrumental regulations in this context is the creation of SECAs, which are a part of Annex VI of IMO’s MARPOL protocol and came into force in May 2005. Under Annex VI, limits on maximum sulfur content in fuel used by the ships operating in the designated ECAs were incrementally reduced [12], as shown above in Figure 1.

In the wake of SECA regulations, a number of researchers have attempted to investigate the impact of SECA on the affected shipping sector, from technical, operational, environmental and economic perspectives [18,19,20]. To comply with the 0.1 percent sulfur regulation, shipping companies were faced with a number of possible solutions. They could switch from traditional heavy fuel oil (HFO) to distillate fuel (marine gas oil or ultra-low sulfur fuel) having a maximum sulfur content of 0.1%. Another option was to install after-treatment technologies (e.g., scrubbers) on board, or convert the vessels to use alternative fuels such as liquid natural gas (LNG), methanol or biofuels [21,22]. While all these alternatives would allow shipowners to operate within SECA waters, they were characterized by very different financial consequences. In addition to the required extensive additional capital costs for retrofitting the vessels, immature technology and price uncertainty regarding the latter two approaches (i.e., scrubbers and LNG) made these solutions unattractive for a number of shipping companies [23,24]. Distillates did not require capital investments, but their higher price could rapidly become a heavy burden for ship operators [7].

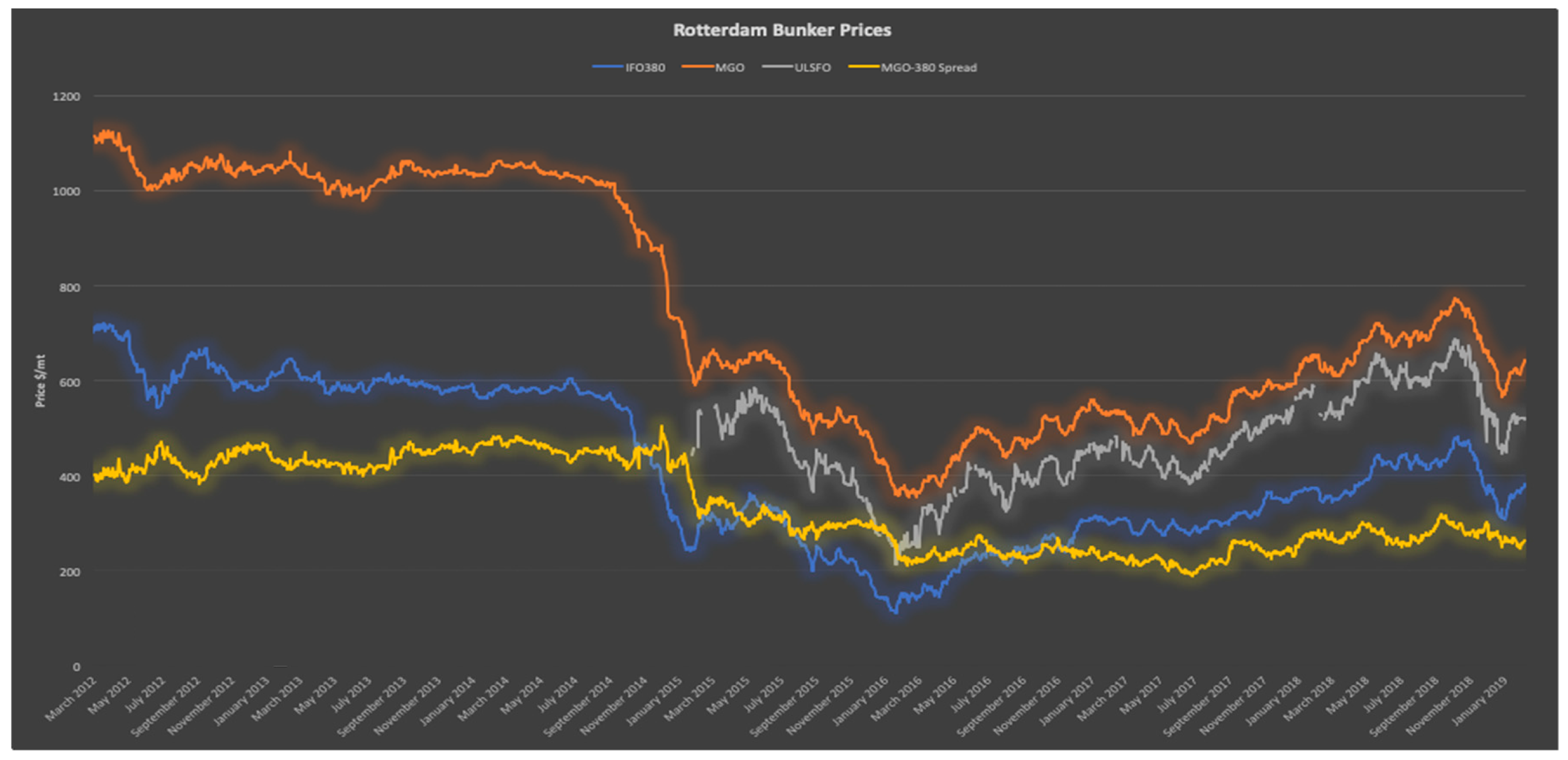

Fuel costs represent the largest share in the total operating cost of a vessel, and a fuel switch to MGO was likely to increase the freight rates on certain routes and eventually lead to the so-called modal backshift from sea transport to road transport [12,25]. This modal shift to road would not only put the local industry and many ship and port operators out of business but could also challenge the EU policy to improve the environment, as road transport causes severe congestion and more emissions [26]. Figure 2 depicts the price fluctuations in dollars per metric ton for MGO, HFO (IFO380), ultra-low sulfur fuel oil (ULSFO), and the price difference between MGO and IFO380 before and after the implementation of 0.1 percent sulfur limits of 2015.

It can be seen in the figure that when the 0.1 percent sulfur regulation came into force in January 2015 the price of MGO dropped significantly compared to 2014. Thus, in 2015, because of a crash in bunker prices, the predictions regarding the modal backshift and negative repercussions of SECA for the shipping industry did not become reality [28]. However, again from 2016 bunker prices have shown a rising trend, which might reverse the situation and in particular the RoRo sector might lose cargo to competitive land-based transport modes as asserted by Zis and Psaraftis [12] and, therefore, additional operational measures such as slow steaming may be required to survive in the market [16].

2.2. Slow Steaming

It was anticipated that as a consequence of SECA regulations, ship operators may reduce the sailing speed to compensate for the extensive cost caused by SECA compliance, as noted by Zis and Psaraftis [16]. In order to analyze the impact of slow steaming on the carrier’s and the shipper’s costs, Mallidis, et al. [29] developed continuous-time analytical models. Further, Wen, et al. [30] presented a speed optimization algorithm that can be applied by shipowners to optimize the vessel’s fuel consumption. Studies by Johnson and Styhre [31] and Zis and Psaraftis [16] suggested that reduced waiting time in port could support slow steaming and mitigate the additional cost effects of SECA for dry bulk shipping in the North and Baltic Seas. Using AIS data, Adland, et al. [13] found that the strict sulfur regulation of 2015 did not affect the speed patterns of the vessels crossing the North Sea ECA. Furthermore, they claimed that vessel speed is not generally determined by fuel prices or freight rates but is rather dependent on factors such as route characteristics, vessel type, weather, market segment and conditions and the nature of the commercial contract between a shipper and a ship operator.

The role of energy efficiency is immensely crucial for the short sea RoRo/RoPax sector as it faces fierce competition from the alternative transport modes of road and rail. Greater energy efficiency not only results in cost savings, but it also brings about a reduction in the emissions per unit of transport work. Due to the non-linear correlation between speed and fuel consumption as embodied in the propeller law [4], even a marginal speed reduction from full or normal steaming speed will result in a substantial reduction in fuel consumption. As with most energy efficiency measures, slow steaming is potentially associated with a negative abatement cost, that is, measures that reduce emissions will at the same time also reduce costs [32].

The positive role of slow steaming in gaining energy efficiency and supporting environmental sustainability is evident, but it may have negative corollaries for the shippers and shipping companies by affecting the entire supply chain. Slow steaming may increase the transit time and pipeline inventory costs for shippers due to delayed cargo delivery [33]. Shipping companies may need additional tonnage to maintain the schedule frequency which will result in extra costs and emissions [34]. Businesses with lean, just-in-time supply chains may be required to have additional safety stocks because of increased shipping time. In particular, shippers with perishable and short life-cycle goods are likely to be affected more [29].

In contrast to tank and dry bulk ships that transport low-value cargo for a single or a few shippers, the RoPax vessels will find the issue of speed to be even more complex. In bulk and tanker shipping, the transport cost is high compared to the value of the goods, and fuel costs constitute a major burden for the shipowners. On the other hand, RoPax bunker costs are less significant compared to time-dependent costs due to expensive vessels and large crews. Resembling deep-sea liner shipping, the value of cargo transported by RoRo shipping is also higher than that of tramp shipping, and thus the RoRo shippers are less price sensitive but are more conscious about the time-related service quality attributes such as reliability, speed, port turnaround time, transit time, convenient scheduling, and frequency [35,36]. RoRo/RoPax shipping in general operates like liner shipping on a regular schedule, at an advertised price, with predetermined routes and destination ports. A change in price, schedule, frequency and speed of the vessels can enhance or deteriorate the service quality of the shipping companies [37].

In the RoPax sector, the variety in demand is also as wide as it gets in the transport industry. Travelers with cars who want to cross the water to continue driving are mixed with passengers who want to eat, shop, or just entertain themselves on board. Time-critical cargoes like vegetables, components scheduled for assembly, and e-commerce deliveries are loaded on lorries on board and mixed with less demanding goods loaded in unaccompanied semi-trailers or containers. Revenues obviously stem from the transport service, but there is also a time-dependent element in terms of sales on board.

Hence, scheduling is a big compromise between different time requirements and the compromise differs depending on routes, time of day and season. Most customers want a high speed, but on some routes a slow speed is a value added for passengers who want to eat and for lorry and bus drivers who want to use the crossing as a rest period and thus, on some routes longer sailing times result in an increase in revenue from on-board spending, as stated by Zis and Psaraftis [16]. To further complicate the issue, a lower speed might force the shipping line to deploy more or larger ships, choose a shorter crossing route or skew the timetable between days. Competition with land modes and a fixed connection are also liable to be affected and a modal backshift from sea to road, in particular for cargoes of very high value, can also be a likely outcome of slow steaming [16]. If the speed changes significantly, the vessel might have to be reconfigured to get the right combination of shops, restaurants, bars, seating areas and cabins. In addition, operating far from the design speed is likely to necessitate modification of the hull, a change of propellers and possibly also adjustments to the engines [38].

2.3. Competitiveness

RoRo and RoPax vessels on some routes compete wing-to-wing with the alternative transport modes of road and rail. Reducing the speed beyond a certain level may put sea services in an unfavorable competitive position by negatively affecting their service quality. Mancera [39] defines service quality as the shipper’s perceived quality of a transport process based on its performance, and sees SQ as comprising five main attributes, namely speed, reliability, lead time, freight rates, and cargo loss and damage.

Service quality is one of the most substantial components of competitiveness [40] and both Paixão Casaca and Marlow [36] and Yang, et al. [41] have verified that high service quality improves the competitiveness of shipping firms. High-quality services assist to differentiate a shipping firm from its competitors [42]. Among other factors, time is one of the key components of service quality, and time-related factors such as schedule reliability, sailing frequency, and speed are valued highly by cargo owners when selecting shipping services [43]. High performance in these time-related factors can considerably reduce the shippers’ inventory, production, and logistical costs [37]. The positive effect of service quality on the competitiveness of shipping firms is empirically proved [42]. High performance in SQ improves customer satisfaction [44], and satisfied customers usually continue purchasing and even recommending the services to others [45]. Consequently, this may enhance a firm’s competitiveness in terms of higher revenues or retained customers [46].

Some other studies suggest that employing larger vessels with more cargo on board on a single voyage and increasing port efficiency may counteract the side effects of slow steaming to some extent [47]. Similarly, ship operators pursuing a slow steaming strategy may gain competitive advantage over their rivals and attract more customers through service differentiation based on different transit times, reduced freight rates, and speed [42,48,49]. The methodology used in this article is presented in the next section.

3. Method

This study is exploratory in nature. Therefore, based on Yin [50], a multiple case study methodology has been applied. Yin [50] suggests that a case study investigates a contemporary phenomenon within the real-life situation, in particular when the relation between the phenomenon and context is complex. This observation is applicable to our research, as we explore the contemporary phenomenon of slow steaming in the context of SECA regulations and their impact on the competitiveness of shipping companies. Slow steaming is a complex topic and depends on multiple factors; therefore, a qualitative approach is more appropriate to explore this topic in-depth. Through interviews, it is possible to ask follow-up questions and to draw more information from the interviewees. This eventually helps to enrich the data and uncover the important topics and concepts that may be missed in quantitative research [50].

Around 387 RoRo and RoPax ships were affected by the sulfur regulation in the North and Baltic Seas SECA [11]. The case studies in this research comprise a sample of eleven case firms, that operate a total of 154 RoRo and RoPax ships in SECAs and represent about 40% of the RoRo and RoPax ships that are affected by the sulfur regulation. The main reasons for selecting the RoRo and RoPax segments for this study are that they play a pivotal role in intra-European freight transport and they operate fully within the SECA. In addition, these segments consume large amounts of fuel, were expected to be highly affected by SECA regulations, and have not been the focus of scientific studies. The service type, size, and other significant information about case firms and the respondents are summarized in Table 1.

After a comprehensive literature review focusing on short sea RoRo/RoPax shipping, slow steaming, SECA compliance strategies, and customer requirements regarding the service quality of RoRo/RoPax shipping, 25 RoRo and RoPax companies operating in the North and Baltic Seas were approached for interviews. In the end, 11 managers from such firms participated in semi-structured face-to-face or telephone interviews. Eisenhardt [51] suggests that when the objective of the research is explorative, this sample size sufficiently provides a clear picture of the context. All the interviews were audio-taped and transcribed. Follow-up interviews were conducted in January 2019 to collect the updated information regarding slow steaming in the context of increased bunker prices in 2018. The research questions (Appendix A) were provided to the interviewees beforehand, and they were reassured about the confidentiality of their identity and information. Company names are represented in the remainder of this article simply by capital letters.

NVivo software (QSR International, Melbourne, Australia) was used to organize and analyze the interview text. In NVivo, the interview text was categorized into themes and concepts (Appendix B), which helped to identify the relevant and important concepts and strengthened our findings. It was an iterative process, where we moved back and forth between the collected data, analysis, and interpretation. The findings of this case study are presented in the next section.

4. Results

In this section, the results obtained through the analysis of case companies are presented.

4.1. SECA Compliance and Slow Steaming

In the pre-SECA phase, when managers were planning for SECA compliance, case firms reported that they commenced preparing prior to the 0.1% sulfur limit deadline of 1 January 2015. Various feasibility analyses were conducted for each SECA compliance option—MGO, scrubbers and LNG—and these analyses were based on individual vessel characteristics, operating routes, and the short- and long-term costs of each option. In addition, firms in both clusters outlined that they developed mechanisms for the Bunker Adjustment Factor (BAF) and that data regarding the extra freight rates were transferred to freight customers through information sessions. In general, customers understood the situation and accepted the extra costs caused by SECA. The actual compliance strategy of each case company and its reactions regarding slow steaming and increased BAF in the aftermath of the 0.1% SECA regulation are presented in Table 2.

With respect to actual SECA compliance solutions, most of the RoRo and RoPax case firms followed a mixed strategy (Table 2). They switched to MGO and ultra-low sulfur fuel (e.g., RMD 80) for smaller and older vessels that were operating on comparatively short-distance routes and selected scrubbers or LNG for bigger, newer and high-fuel-consuming vessels operating on long-distance routes. Furthermore, the case of firm RoRo E was remarkably different, as it used MGO on its entire fleet and instead of choosing technological solutions to save on costs, firm E opted for operational changes that constituted schedule and route adjustments and slow steaming on some routes. In the same vein, RoPax I switched to MGO and reduced the vessel speed as an energy efficiency measure on its route between Baltic ports. On the other hand, the case of RoPax F, in contrast, is relatively different. For certain routes, RoPax F switched to MGO and converted one of its vessels to methanol.

Overall, it appears slow steaming as a SECA cost-reduction approach has not been part of the plan among the majority of the case companies. Out of 11 case firms, only two firms—RoRo E and RoPax I—as part of their pre-SECA plans, in addition to switching to MGO, also made some route changes and reduced the vessel speed on some routes, each increasing their total crossing times from 32 to 36 h and from 4 to 4.5 h, respectively.

It is found that neither the reduced bunker prices in 2015 nor the increased bunker prices in 2018 have affected the speed patterns in most of the RoRo and RoPax case firms. As the interviewee from RoRo E stressed:

There are a lot of other parameters besides oil price that we have to consider before making any change in our speed, and the biggest factors are competition, contract, and market situation.

In RoRo and RoPax segments, the additional bunker cost driven by SECA compliance is borne by both the customers and the shipowners. All the case firms have transferred these additional costs to their customers through an increased BAF. The interviewee from RoRo A mentioned:

Yes, we have partially increased BAF. Basically, all contracts are governed by a bunker adjustment formula. This doesn’t mean that bunker costs are irrelevant, but we cannot transfer all the extra bunker cost to our customers. If we are not efficient enough, we will then lose all contracts upon renewal due to the cost base being too high. But inside a contract the risk is limited for the shipping company.

Moreover, for the new ships in the pipeline, the case companies intend to comply with SECA by burning comparatively cheaper and environmentally friendly fuels, such as LNG, or by using batteries. LNG would not favor slow steaming, while the use of battery power might be more favorable for slow steaming.

4.2. Slow Steaming in the RoRo and RoPax Cases

Regarding the feasibility of slow steaming in the existing market situation, significant divergences are noticed between the RoRo and RoPax case firms. The RoRo case firms picture slow steaming as a popular choice to save bunker costs, at least under the existing market conditions, and currently almost all of them have reduced their speed by 4 to 10 knots, except for RoRo B that has set a reduction of only 1–2 knots seasonally. However, it must be noted that this slow steaming is not driven by the 0.1 percent sulfur regulation; rather it is based on the market conditions and customer demand, and was in existence even during 2015 when the bunker prices were low. It was found that RoRo case firms have benefited considerably by steaming at a slower speed, as, for instance, was revealed by the interviewee from RoRo C:

Of course, on a route between Western Norway and UK using slow steaming we are saving cost and we save more by having two slow vessels rather than just one fast vessel.

One of the reasons behind slow steaming in RoRo was also the economic downturn of 2008. As the interviewee from RoRo A mentioned:

This is something we started quite early in 2008 or 2009 because of the financial crisis. We were forced to do that and the main purpose behind this was financial savings.

The interviewees from nearly every RoPax case firm favored slow steaming as an energy efficiency and cost-saving measure. For example, the interviewee from RoPax H mentioned that:

We are tweaking here and there. We are looking for minutes, 15 minutes or so, and there is a lot of money in there. In RoPax, we don’t talk about hours, but we talk about minutes.

However, in contrast to the RoRo segment, it was revealed that there is a very little potential for slow steaming in the RoPax sector. It was found that RoPax case firms have instituted some route-specific slow steaming in the range of 1–2 knots slower, and this varies seasonally. To meet market requirements, RoPax firms F, J, and K operate high-speed ferries on some routes with speeds in the range of 27–35 knots. For some routes, in the summer season, when passenger demand is high and extra time needs to be spent in port for loading and offloading, it is not usually possible to slow steam. The interviewee from RoPax H stated:

It is possible that we can change the itinerary in summer and winter times, but that’s not good because the market wants to have the same schedule for arrival and departure times throughout the year.

Technical reconfigurations and shorter routes might be needed to implement slow steaming. To facilitate slow steaming, all RoRo case firms, except RoRo B, have made some technical reconfigurations to their vessels by optimizing the pitch and rotation speed of the propellers. Moreover, case firms RoRo B, D, and E sometimes choose a shorter course for steaming slow. The interviewee from RoRo B stated:

We also sometimes adjust our routes to adjust the speed and it depends on fuel prices as well. So there is interplay between route, speed, and fuel price.

However, RoPax case firms did not make any reconfigurations in either their cabins or engine rooms, nor did they change the sailing route as they have introduced only a minor speed reduction.

4.3. Slow Steaming and Service Quality

In addition, all interviewees strikingly emphasized that vessel speed is highly dependent on their customers’ lead time requirements, inventory costs, bunker prices, and competitors’ operating speed. As the interviewees from RoRo A mentioned:

We have to consider our customers’ requirements that were set in the contract. So, to meet customer demand, we may even have to speed up although it might pollute the environment. As long as our competitors will go fast, we will also go fast. Otherwise, we will be out of business.

Similarly, the interviewee from RoRo B emphasized:

We cannot play at least with lead time, as our customers give us lead time. For instance, if our customer wants their cars transported from Zeebrugge to Malmo, let’s say in three days, we have to transport them in three days.

This is verified in the case of RoRo D, who in order to meet the customers’ demand, made some adjustments in their routes, accelerated the sailing frequency, and raised the speed from 12 knots to 14 knots.

Vessel speed in the RoPax sector also critically depends on offered transit time, vessel type, departure and arrival time, distance between origin–destination ports, and the competitive environment. The interviewee from RoPax H explained the situation in this way:

Compared to RoRo service, the RoPax segment is different in a way as we have passengers on board who are usually in a hurry. Cruise ships may do slow steaming, but for ferry transport it’s not possible as it has a proper timetable and not many people want to arrive at midnight and leave before 6 in the morning. Passengers need to shop on board, relax and eat as well, so we have to adjust the time accordingly. In this segment, we compete on time. For a shorter distance, forget slow steaming. However, for a longer distance, it’s different. For instance, a ship from Stavanger (Norway) to France can go a little slower.

The speed and schedule sometimes vary en route and on a customer segment basis. As the interviewee from RoPax F stressed:

If there is a heavy freight route, then the drivers need time. Then, of course, it’s better to spend 9 hours at sea instead of 2 hours, and if the route is very passenger heavy, they don’t want to spend too much time at sea.

However, the departure times are not based only on the drivers’ time; as the RoPax case firms mentioned, they do not know where the truck is coming from and hence do not know if the drivers require a longer resting time on board the vessel. Scheduling, pricing and crossing timing is complex in the RoPax segment, and compared to RoRo, RoPax serves a wide variety of customers. Thus, it may not be possible to slow steam beyond a certain limit. As the interviewee from RoPax H stressed:

We have many markets on each ship. For instance, one of our ships has 13 different categories of passengers: cruise passengers, conference guests, truck drivers and so on. These 13 different passenger categories have different requirements when deciding whether they are sailing with us or not. Some customer segments can be affected if we sail slower, so at the moment the market is not favorable for steaming slower.

Moreover, RoPax case firms have a fiercer competitive environment than RoRo, as depending on the route, RoPax competes with low-cost airlines, domestic ferry companies, trucking (cheaper double-driver effect), tunnels, bridges, landside conference centers, cargo ships or RoRo, and all other sources of entertainment. On some routes, vessel speed also depends on other ferry competitors’ speed, as stated above. Some case firms indicated that currently they are at the optimum level; but if a new competitor shows up, then they will adjust it accordingly. The interviewee from RoPax H expressed the competitive situation as below:

Although the slower you go, the more energy you save for a container cargo, the competition is extremely high. For example, the Helsinki–Tallinn route in the Baltic Sea is one market where more than three companies are now operating more than ten ships—and even a helicopter line is operating sometimes—and their competitive advantage is if they go faster. If one goes 15 minutes faster, then another does the same. They go 27 knots and they lie still for 2 hours as they need to come back again at 27 knots. So, this is what markets want instead of sailing at 22 knots, lying still for 1 hour, and then going 22 knots back. That’s how a bad market mechanism works in a free open market, because time is money in this market.

In addition, RoPax case firms were extremely concerned about the cheaper and double drivers from low-cost countries employed by trucking companies, as they are undermining the competitive position of the shipping industry, and therefore, it further reduces the possibilities of gaining energy efficiency through slow steaming. Similarly, the interviewee from RoPax F mentioned:

If oil prices increase again, then slow steaming may come into play. But then there are some road taxation and other elements to consider in that situation.

Therefore, it can be inferred from the above interview excerpts that the matter of speed reduction is highly sensitive for both RoRo and RoPax segments, as both segments need to comply strictly with the offered lead time while maintaining the service frequency. In the current market settings, too much gambling with speed may negatively affect the service quality of both shipping segments and eventually may reduce the competitiveness of this sector.

RoRo and RoPax case firms pointed out that demand for their services is highly elastic in terms of service quality (e.g., lead time, convenience of departure and arrival) and price on certain routes, and this is because the customers have multiple alternatives to travel and transport their cargo. The interviewee from RoPax I said:

Our leisure passengers are extremely price sensitive, and any increase or decrease in the price can affect the demand as they have various alternatives available.

…and RoPax H pointed out:

We tried to reduce the speed and increase time to 3 hours from 2.5 on our route to country S, but customers didn’t like it and then we reversed it back again.

Thus, service quality requirements, service price and route competition are some of the vital factors deciding the speed of RoRo and RoPax vessels.

4.4. Slow Steaming through Port Efficiency

The study found that there is some potential to improve port efficiency while reducing the speed at sea. All RoRo case firms expressed the view that improved port efficiency could enhance the feasibility of slow steaming. In particular, RoRo C and D are focusing on making slow steaming a favorable move by improving port productivity. As the interviewee from RoRo C emphasized:

In our fleet we have turned vessels earlier. This means we have reduced the loading and discharging time at port to get extra time at sea and reduce the speed. Port efficiency is important not only for slow steaming but also to maintain the schedule in bad weather as reliability is important for our customers.

Similarly, RoPax case firms agreed that to allow more time at sea at a lower speed they try to optimize the port operations as much as possible, and this also depends on the season. As the interviewee from RoPax K mentioned:

We have tried to optimize port operations so we could spend more time at sea at a lower speed. We have also shortened our turnaround time on a route between Western Norway and Northern Denmark. Instead of 2 hours, we now stay 1 hour in port and have spare time at sea to slow steam.

A follow-up question related to the above statement was asked by the interviewer:

Well, but don’t you think that staying only 1 hour at the port limits your catchment area?

The interviewee from RoPax K responded:

No, no. It’s not like that. Passengers and freight forwarders know the timetable so they reach on time and they go at that time every day. Of course, you have a catchment area, but the market is like this.

Although slow steaming through improved port efficiency is feasible, there are still some limits. RoRo operators cannot depart immediately after arrival as they have to complement their schedule with cargo arrivals at the terminals, and RoPax operators need to follow their posted departure time. In addition, slow steaming by reducing port turnaround time leads to a reduced catchment area for the customers and, thus, RoPax and RoRo companies may lose some business. So they always need to weigh the savings they make by steaming slow against the business they may lose in the form of reduced sales caused by short turnaround times.

4.5. Slow Steaming through Service Differentiation

Due to high competition and expensive cargo, service differentiation through slow and express services in the RoRo cases cannot be attained to any large extent in the existing market mechanism. As the interviewees from RoRo A and B stated, respectively:

I think it’s not about speed; it’s more about precision. If we follow this policy, then there will be a competitor who will do the same, so it’s not possible for us.

Well, our customers who usually ship highly expensive cargo are not talking about such things, and it also depends on their customers as well. So there is no room for much speed reduction and our timing depends on our contract with customers.

This is evident by the fact that in 2010 RoRo E pursued a differentiation strategy by introducing the slowest RoRo service in the Baltic Sea. However, intensive competition from rival RoRo companies and an alternative rail service operating on the same route compelled RoRo E to close its operations on this route.

On the other hand, service differentiation and slow steaming may be feasible for at least some RoPax customer segments on certain routes. This differentiation can be illustrated in the case of RoPax H and RoPax K. RoPax H operates a cruise ferry on a route and the transit time is 3 h 15 min with a return ticket price for one person of EUR 56. Meanwhile, on the same route, RoPax K offers an express service only in the summer season that takes just 2 h 15 min and is even cheaper, with a return ticket price for one person of EUR 35.

So unlike deep-sea shipping where shipping firms compete mainly with other shipping firms serving the same route, the offer of reduced speed and price as a service differentiation strategy may not be feasible in the RoRo segment, which is also competing with land modes. For a RoPax firm, however, it may be realistic depending on the route and customer demand.

4.6. Slow Steaming through Increased Vessel Size

Finally, our study found that transporting more cargo onboard the larger vessels is not feasible for the RoRo and RoPax shipping segments, as they still would have to follow the lead time and frequency requirements of their customers. In addition, there might not be sufficient port infrastructure to cater for the larger vessels. Different opinions are noticed on this issue as the interviewee from RoRo D suggested:

I think for paper-shipping companies, it is possible as the customer can live with a little longer lead time.

RoPax G in this respect stressed that:

We are increasing vessel capacity and unit size in our new vessels, but there will be no change in speed requirements.

The interviewee from RoPax K commented on this by saying:

When you get larger vessels, you also reduce the frequency and that may not be a good idea. In deep-sea shipping, with low competition from alternative modes, it can work where you have crossing times in weeks from China to the EU. Then you can have bigger vessels and reduce the frequency. But in SSS, you also need frequency; otherwise, you will lose the load.

The majority of RoRo and RoPax case companies rejected the idea of supporting slow steaming by building larger vessels, as it might affect their customers’ logistical arrangements and lead to a modal shift to road transport. The results presented here are discussed in the context of the existing literature in the section below.

5. Discussion and Conclusions

In this article, we have addressed the feasibility of slow steaming to mitigate the anticipated SECA compliance costs from the perspective of RoRo and RoPax shipping firms. In addition, the impact of slow steaming on the competitiveness of short sea RoRo and RoPax segments with respect to service quality is explored. Multiple case studies focusing primarily on 11 short sea RoRo and RoPax firms with operations in the North and Baltic Seas were conducted.

Overall, our findings suggest that the 0.1% SECA regulation of 2015 requiring the use of higher-priced MGO has not caused slow steaming in the RoRo and RoPax segments to any great extent. The increased bunker prices are partially transferred to the customers via increased BAF and partly borne by the shipowners. Thus, our findings are consistent with those of Adland, et al. [13], who in their empirical study found no evidence of slow steaming in the wake of North Sea SECA regulations and asserted that vessel speed is not generally determined by fuel prices or freight rates but is rather dependent on factors such as route characteristics, vessel type, weather, market segment and conditions, and the nature of the commercial contract between the shipper and the ship operator.

Furthermore, time-related attributes of service quality, such as total transit or lead time, frequency, reliability, and convenient departure and arrival times, are found to be considerably more significant for the customers of RoRo and RoPax case firms. In this way, we agree with previous research studies by Meixell and Norbis [35], Bergantino and Bolis [52], and Pantouvakis [53], who claim that for ferry and RoRo transport customers service quality—in regard to schedule convenience, frequency, reliability, and transit time—is even more important than the price of the ticket or the freight rate. For the RoRo and RoPax case firms, the elasticity of demand in terms of price and service quality is significant, as verified by Notteboom [10]. Therefore, in the present market setting, the potential of slow steaming is not high, as it may increase the lead time or affect the frequency, reliability, and departure and arrival times of the services. The slow steaming strategy that neglects the customers’ convenience is likely to diminish the service quality of RoRo and RoPax firms, leading to a poor competitive position in the market.

Furthermore, the idea of slow steaming by using larger vessels with more cargo on board, which may be effective when applied in deep-sea shipping [47], is not practical for short sea RoRo and RoPax shipping. As officials of the case firms interviewed for our article stressed, in short sea shipping frequency is highly critical for the customers, and to maintain sailing frequency firms will need to employ more vessels which is not possible currently.

Similarly, our findings strongly support earlier studies by Johnson and Styhre [31] and Zis and Psaraftis [16] which suggest that due to high port efficiency and low turnaround port time, slow steaming can be employed without affecting the total transit time for the customers. The examples of case firms RoRo C and D and RoPax K, presented in the findings section, justify this phenomenon.

Finally, service differentiation through slow and express services as proposed by Lindstad, et al. [49] may be feasible also for the short sea RoPax segment but only on certain routes. This has been demonstrated by the example of case firms RoPax H and RoPax K who compete on the basis of transit time by operating a slow cruise ferry and a fast-express ferry, respectively. Conversely, due to high inventory costs and competition from alternative transport modes for RoRo cargo, this differentiation may not be favorable in the RoRo segment. Previously, a Swedish RoRo shipping firm tried this concept as described by [54], but this service was discontinued in 2013 due to low market demand and fierce competition by direct rail service started between Germany and Sweden [55].

The quest to cut bunker costs and airborne emissions through slow steaming may result in negative ramifications for short sea RoRo/RoPax shipping and its customers by affecting entire supply chains. The case studies reveal that in the current market situation RoRo case firms are already steaming at slow speed and they may increase the speed based on the customers’ demand.

We believe that the potential of slow steaming for the RoPax and RoRo segments are impeded by a number of factors, including bunker prices, rigorous competition in terms of cost and time within RoPax shipping lines and routes as well as with land modes, and most important different service quality-related attributes. It is evident from the interviewees from the case firms that slow steaming across a certain limit in the RoPax segment may either lead to a loss of business volumes or otherwise will require more vessels to maintain the frequency. However, the present market situation does not favor additional tonnage in the sector as it appears that the market has found its equilibrium. Finally, the slow steaming strategy that works against the customers’ convenience may deteriorate the service quality of RoRo and RoPax services, which ultimately may lead the sector into an unfavorable competitive position in the market. In the next section, the limitations and suggestions for future research are presented.

Limitations and Future Research

Even though some valuable insights have been generated, this article is not without its limitations. The experienced interviewees from the case firms provided their expert opinions on the subject that could fairly represent the viewpoint of the entire RoRo and RoPax sector, yet a larger sample size would perhaps have supported the findings better. Secondly, it would be valuable to conduct surveys involving more firms from different sectors and countries. Finally, findings regarding the service quality requirements of customers are based on the opinions of interviewees from RoRo and RoPax case firms and a survey with actual customers of these services might have added more balance to the results. All these limitations form the basis for future research.

Author Contributions

All authors planned the study, prepared and participated in interviews. Z.R. provided literature reviews, conducted several interviews, and drafted the manuscript. J.W. reviewed, edited, and supervised the manuscript. C.F. reviewed and edited the manuscript and conducted several interviews. Z.R. improved the manuscript by responding to the review comments. All authors read and approved the final manuscript.

Funding

The research was funded by the Swedish Maritime Administration and the Logistics and Transport Foundation LTS.

Acknowledgments

The authors thank the interviewees and Joakim Kalantari for conducting some of the interviews.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

Appendix A. Interview Questions

SECA

- How did you prepare before the introduction of the stringent sulfur limits of 0.1% implemented from January 1, 2015?

- What option have you chosen to conform to the SECA—e.g., LNG, MGO, methanol, scrubbers, or a combination of different alternatives?

- Did you test any low-sulfur fuels before the introduction of the 0.1% limit? What experiences/lessons arose as a result?

- How has the ensuing situation been different compared with the assessments you did before the introduction of the SECA 2015 0.1% sulfur limits?

- Do you think that other RoRo/RoPax operators that chose other strategies (scrubbers, for example) implemented their strategies, or did they put them on hold due to the decreased bunker prices?

- If the oil price increases again, do you feel that you are better prepared than your competitors who retrofitted with scrubbers or LNG?

Slow Steaming

- Have you worked with any slow steaming in your RoRo (or RoPax) segment? How has it been differently customized based on vessel type, route, season, etc.?

- Have there been any discussions in your company to compensate for the additional SECA costs through slow steaming?

- Has the transition to low-sulfur fuels affected the slow steaming profile of the ships?

- Have you considered changing the route, such as searching for the shortest crossing to allow a lower speed?

- Do your vessels need to be reconfigured (cabins/seats, restaurants, car tire heights/ramps, etc.) to adapt to a different sailing speed and transit time? Do they need to be rebuilt (bulb adapted for a different speed, slow steaming kits, etc.)?

- Would it be possible for some lines to differentiate their services by increasing vessel speed and get a higher price or reduce the speed and get a lower price?

- Do you think increased port efficiency can encourage slow steaming?

- For the RoRo and RoPax segments, is it feasible to transport more cargo on bigger vessels in a single journey and slow steam?

Service Quality Requirements

- Which customer segments do your various lines serve? Is there a dominant segment that sets the conditions for service design, schedule, quality, price segmentation, etc.?

- What is your "value proposition"?

- What are your customers’ service quality requirements?

- Do you have an idea of the elasticity of the customer demand curve in terms of transit time, frequency, price, departure and arrival timing?

Future Plans

- What plans/strategies/scenarios do you see ahead regarding slow steaming in the RoRo (or RoPax) segment?

- Are there any other important issues related to this topic?

Appendix B

{kind=link}

{kind=link}

Table A1.

Code tree developed based on the in-depth analysis of interview transcripts.

| Concepts Emerged |

|---|

| 1. SECA regulation |

| 1.1. Pre-SECA preparation |

| 1.1.1. Low sulfur fuel tests |

| 1.1.2. Commercial approach |

| 1.2. Post SECA situation |

| 1.2.1. Evolution of new fuels |

| 1.2.2. Bunker price decline |

| 1.3. Firms’ SECA compliance solution and slow steaming |

| 1.3.1. Scrubbers |

| 1.3.2. MGO |

| 1.3.3. LNG |

| 1.3.4. Hybrid or ultra-low sulfur fuel |

| 1.3.5. Methanol |

| 1.3.6. Mix |

| 2. Service quality requirements |

| 2.1. Service frequency |

| 2.2. Schedule flexibility |

| 2.3. Price |

| 2.4. Lead time |

| 2.5. Inventory costs |

| 2.6. Departure and arrival time convenience |

| 2.7. Elasticity of demand for services |

| 2.7.1. Price |

| 2.7.2. Lead time |

| 2.8. Customer segment that set quality requirements |

| 2.8.1.Truck drivers or freight forwarders |

| 2.8.2.Cargo owners |

| 2.8.3.Car drivers and passengers |

| 2.9.Core values of the firms |

| 3. Slow Steaming |

| 3.1. Existing slow steaming pattern |

| 3.2. Slow steaming and vessel configurations |

| 3.3. Slow steaming and shorter routes |

| 3.4. Future potential for slow steaming |

| 3.4.1. Slow steaming through port efficiency |

| 3.4.2. Slow steaming through larger vessels |

| 3.4.3. Slow steaming and service differentiation |

| 3.4.4. Levy or CO2 taxes |

| 3.4.5. Future bunker price |

| 3.4.6. Competitors’ speed |

| 3.4.7. Competition and market mechanism |

References

- Buhaug, O.; Corbett, J.J.; Eyring, V.; Endresen, O.; Faber, J.; Hanayama, S.; Lee, D.S.; Lee, D.; Lindstad, H.; Markowska, A.Z.; et al. Prevention of Air Pollution From Ships—Second IMO GHG Study; International Maritime Organization: London, UK, 2009. [Google Scholar]

- IMO. Revised MARPOL Annex VI: Regulations for the Prevention of Air Pollution From Ships and NOx Technical Code; IMO Marine Environmental Protection Committee (MEPC): London, UK, 2008. [Google Scholar]

- Smith, T.W.P.; Jalkanen, J.P.; Anderson, B.A.; Corbett, J.J.; Faber, J.; Hanayama, S.; O’Keeffe, E.; Parker, S.; Johansson, L.; Aldous, L.; et al. Third IMO GHG Study; International Maritime Organization (IMO): London, UK, 2014; Available online: http://www.imo.org/en/OurWork/Environment/PollutionPrevention/AirPollution/Documents/Third%20Greenhouse%20Gas%20Study/GHG3%20Executive%20Summary%20and%20Report.pdf (accessed on 7 January 2019).

- Man Diesel and Turbo. Basic Principles of Ship Propulsion. Available online: https://marine.man-es.com/docs/librariesprovider6/propeller-aftship/5510-0004-04_18-1021-basic-principles-of-ship-propulsion_web.pdf?sfvrsn=c01858a2_2 (accessed on 11 January 2019).

- Bergqvist, R.; Turesson, M.; Weddmark, A. Sulphur emission control areas and transport strategies -the case of Sweden and the forest industry. Eur. Transp. Res. Rev. 2015, 7, 10. [Google Scholar] [CrossRef]

- ESN. Way Forward SECA Report by European Shortsea Network. Available online: http://www.shortsea.info/openatrium-6.x-1.4/sites/default/files/esn-seca-report-2013_0.pdf (accessed on 5 January 2019).

- Zis, T.; Angeloudis, P.; Bell, M.G.H.; Psaraftis, H.N. Payback Period for Emissions Abatement Alternatives: Role of Regulation and Fuel Prices. Transp. Res. Rec. J. Transp. Res. Board 2016, 2549, 37–44. [Google Scholar] [Green Version]

- Jiang, L.; Kronbak, J.; Christensen, L.P. The costs and benefits of sulphur reduction measures: Sulphur scrubbers versus marine gas oil. Transp. Res. Part D Transp. Environ. 2014, 28, 19–27. [Google Scholar] [CrossRef]

- Lindstad, H.E.; Rehn, C.F.; Eskeland, G.S. Sulphur abatement globally in maritime shipping. Transp. Res. Part D Transp. Environ. 2017, 57, 303–313. [Google Scholar] [Green Version]

- Notteboom, T. The impact of low sulphur fuel requirements in shipping on the competitiveness of roro shipping in Northern Europe. WMU J. Marit. Aff. 2011, 10, 63–95. [Google Scholar] [CrossRef]

- BPO. The Baltic Sea as a Model Region for Green Ports and Maritime Transport. Available online: http://www.bpoports.com/BPC/Helsinki/BPO_report_internet-final.pdf (accessed on 17 January 2019).

- Zis, T.; Psaraftis, H.N. The implications of the new sulphur limits on the European Ro-Ro sector. Transp. Res. Part D Transp. Environ. 2017, 52, 185–201. [Google Scholar] [CrossRef]

- Adland, R.; Fonnes, G.; Jia, H.; Lampe, O.D.; Strandenes, S.P. The impact of regional environmental regulations on empirical vessel speeds. Transp. Res. Part D Transp. Environ. 2017, 53, 37–49. [Google Scholar] [CrossRef] [Green Version]

- Psaraftis, H.N.; Kontovas, C.A. Speed models for energy-efficient maritime transportation: A taxonomy and survey. Transp. Res. Part C Emerg. Technol. 2013, 26, 331–351. [Google Scholar] [CrossRef]

- Fagerholt, K.; Gausel, N.T.; Rakke, J.G.; Psaraftis, H.N. Maritime routing and speed optimization with emission control areas. Transp. Res. Part C Emerg. Technol. 2015, 52, 57–73. [Google Scholar] [CrossRef] [Green Version]

- Zis, T.; Psaraftis, H.N. Operational measures to mitigate and reverse the potential modal shifts due to environmental legislation. Marit. Policy Manag. 2018, 46, 117–132. [Google Scholar] [CrossRef]

- Santos, T.A.; Guedes Soares, C. Methodology for ro-ro ship and fleet sizing with application to short sea shipping. Marit. Policy Manag. 2017, 44, 859–881. [Google Scholar] [CrossRef]

- Svindland, M. The environmental effects of emission control area regulations on short sea shipping in Northern Europe: The case of container feeder vessels. Transp. Res. Part D Transp. Environ. 2018, 61, 423–430. [Google Scholar] [CrossRef]

- Chen, L.; Yip, T.L.; Mou, J. Provision of Emission Control Area and the impact on shipping route choice and ship emissions. Transp. Res. Part D Transp. Environ. 2018, 58, 280–291. [Google Scholar] [CrossRef]

- Chang, Y.-T.; Park, H.; Lee, S.; Kim, E. Have Emission Control Areas (ECAs) harmed port efficiency in Europe? Transp. Res. Part D Transp. Environ. 2018, 58, 39–53. [Google Scholar] [CrossRef]

- Halff, A.; Younes, L.; Boersma, T. The likely implications of the new IMO standards on the shipping industry. Energy Policy 2019, 126, 277–286. [Google Scholar] [CrossRef]

- Lindstad, H.E.; Eskeland, G.S. Environmental regulations in shipping: Policies leaning towards globalization of scrubbers deserve scrutiny. Transp. Res. Part D Transp. Environ. 2016, 47, 67–76. [Google Scholar] [CrossRef] [Green Version]

- Gu, Y.; Wallace, S.W. Scrubber: A potentially overestimated compliance method for the Emission Control Areas. Transp. Res. Part D Transp. Environ. 2017, 55, 51–66. [Google Scholar] [CrossRef]

- Abadie, L.M.; Goicoechea, N.; Galarraga, I. Adapting the shipping sector to stricter emissions regulations: Fuel switching or installing a scrubber? Transp. Res. Part D Transp. Environ. 2017, 57, 237–250. [Google Scholar] [CrossRef]

- Sys, C.; Vanelslander, T.; Adriaenssens, M.; Van Rillaer, I. International emission regulation in sea transport: Economic feasibility and impact. Transp. Res. Part D Transp. Environ. 2016, 45, 139–151. [Google Scholar] [CrossRef]

- Holmgren, J.; Nikopoulou, Z.; Ramstedt, L.; Woxenius, J. Modelling modal choice effects of regulation on low-sulphur marine fuels in Northern Europe. Transp. Res. Part D Transp. Environ. 2014, 28, 62–73. [Google Scholar] [CrossRef]

- Ship and Bunker, Bunker Prices in Rotterdam. Available online: https://shipandbunker.com/prices/emea/nwe/nl-rtm-rotterdam (accessed on 7 February 2019).

- Hilmola, O.-P. The Sulphur Cap in Maritime Supply Chains-Environmental Regulations in European Logistics; Springer Nature AG: Cham, Switzerland, 2019. [Google Scholar]

- Mallidis, I.; Iakovou, E.; Dekker, R.; Vlachos, D. The impact of slow steaming on the carriers’ and shippers’ costs: The case of a global logistics network. Transp. Res. Part E Logist. Transp. Rev. 2018, 111, 18–39. [Google Scholar] [CrossRef] [Green Version]

- Wen, M.; Pacino, D.; Kontovas, C.A.; Psaraftis, H.N. A multiple ship routing and speed optimization problem under time, cost and environmental objectives. Transp. Res. Part D Transp. Environ. 2017, 52, 303–321. [Google Scholar] [CrossRef]

- Johnson, H.; Styhre, L. Increased energy efficiency in short sea shipping through decreased time in port. Transp. Res. Part A Policy Pract. 2015, 71, 167–178. [Google Scholar] [CrossRef] [Green Version]

- Maloni, M.; Paul, J.A.; Gligor, D.M. Slow steaming impacts on ocean carriers and shippers. Maritime Economics & Logistics 2013, 15, 151–171. [Google Scholar] [Green Version]

- Psaraftis, H.N.; Kontovas, C.A. Balancing the economic and environmental performance of maritime transportation. Transp. Res. Part D Transp. Environ. 2010, 15, 458–462. [Google Scholar] [CrossRef]

- Lee, C.-Y.; Lee, H.L.; Zhang, J. The impact of slow ocean steaming on delivery reliability and fuel consumption. Transp. Res. Part E Logist. Transp. Rev. 2015, 76, 176–190. [Google Scholar] [CrossRef]

- Meixell, M.J.; Norbis, M. A review of the transportation mode choice and carrier selection literature. The International Journal of Logistics Management 2008, 19, 183–211. [Google Scholar] [CrossRef]

- Paixão Casaca, A.C.; Marlow, P.B. The competitiveness of short sea shipping in multimodal logistics supply chains: Service attributes. Marit. Policy Manag. 2005, 32, 363–382. [Google Scholar] [CrossRef]

- Yuen, K.F.; Thai, V.V. Service quality and customer satisfaction in liner shipping. Int. J. Qual. Serv. Sci. 2015, 7, 170–183. [Google Scholar] [CrossRef]

- Armstrong, V.N. Vessel optimisation for low carbon shipping. Ocean Eng. 2013, 73, 195–207. [Google Scholar] [CrossRef]

- Mancera, A. Measuring Service Quality in Freight Transport Networks. Ph.D. Thesis, ETH Zurich, Zurich, Switzerland, 2017. [Google Scholar]

- Sharma, S. Different strokes: Regulatory styles and environmental strategy in the North-American oil and gas industry. Bus. Strategy Environ. 2001, 10, 344–364. [Google Scholar] [CrossRef]

- Yang, C.S.; Lu, C.S.; Haider, J.J.; Marlow, P.B. The effect of green supply chain management on green performance and firm competitiveness in the context of container shipping in Taiwan. Transp. Res. Part E Logist. Transp. Rev. 2013, 55, 55–73. [Google Scholar] [CrossRef]

- Yuen, K.F.; Thai, V.V. Corporate social responsibility and service quality provision in shipping firms: Financial synergies or trade-offs? Marit. Policy Manag. 2016, 44, 1–16. [Google Scholar] [CrossRef]

- Notteboom, T.E. The Time Factor in Liner Shipping Services. Marit. Econ. Logist. 2006, 8, 19–39. [Google Scholar] [CrossRef]

- Liang, X.; Zhang, S. Investigation of customer satisfaction in student food service. Int. J. Qual. Serv. Sci. 2009, 1, 113–124. [Google Scholar] [CrossRef]

- Senić, V.; Marinković, V. Examining the Effect of Different Components of Customer Value on Attitudinal Loyalty and Behavioral Intentions. Int. J. Qual. Serv. Sci. 2014, 6, 134–142. [Google Scholar] [CrossRef]

- Lam, S.-Y.; Lee, V.-H.; Ooi, K.-B.; Lin, B. The relationship between TQM, learning orientation and market performance in service organisations: An empirical analysis. Total Qual. Manag. Bus. Excell. 2011, 22, 1277–1297. [Google Scholar] [CrossRef]

- International Maritime Organisation (IMO). Prevention of air Pollution from Ships. Second IMO GHG Study 2009 Update of the 2000 IMO GHG Study—Final Report Covering Phase 1 and Phase 2; International Maritime Organization: London, UK, 2009. [Google Scholar]

- Yuen, K.F.; Thai, V.V.; Wong, Y.D. Corporate social responsibility and classical competitive strategies of maritime transport firms: A contingency-fit perspective. Transp. Res. Part A Policy Pract. 2017, 98, 1–13. [Google Scholar] [CrossRef]

- Lindstad, H.; Asbjørnslett, B.E.; Strømman, A.H. Opportunities for increased profit and reduced cost and emissions by service differentiation within container liner shipping. Marit. Policy Manag. 2016, 43, 280–294. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research: Design and Methods, 6th ed.; SAGE Publications Inc.: Thousand Oaks, CA, USA, 2018. [Google Scholar]

- Eisenhardt, K.M. Building Theories from Case Study Research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Bergantino, A.S.; Bolis, S. Monetary values of transport service attributes: Land versus maritime ro-ro transport. An application using adaptive stated preferences. Marit. Policy Manag. 2008, 35, 159–174. [Google Scholar] [CrossRef]

- Pantouvakis, A.M. Who pays the ferryman? An analysis of the ferry passenger’s selection dilemma. Marit. Policy Manag. 2007, 34, 591–612. [Google Scholar] [CrossRef]

- Woxenius, J. Flexibility vs. specialisation in European Short Sea Shipping. Transport 2012, 27, 250–262. [Google Scholar] [CrossRef]

- Baltic Transport Journal. SOL Closes the Helsingborg-Travemünde Ro-Ro Line. 2013. Available online: http://baltictransportjournal.com/germany/sol-closes-the-helsingborg travem%EF%BF%BD%C2%BCnde-ro-ro-line,826.html (accessed on 15 June 2018).

Figure 1.

Fuel sulfur limits and implementation dates within and outside SECAs. Source: MAN [4].

Figure 1.

Fuel sulfur limits and implementation dates within and outside SECAs. Source: MAN [4].

Figure 2.

Fluctuations in bunker prices before and after enforcement of 0.1% sulfur regulation. Source: Ship and Bunker [27].

Figure 2.

Fluctuations in bunker prices before and after enforcement of 0.1% sulfur regulation. Source: Ship and Bunker [27].

Table 1.

Summary of case companies.

| Case Company Profile | Respondents | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Name | Vessel Types | Fleet Size | Main Service Region | Annual Cargo and Passenger Transport | Main Customers | Head-Quarters | Function | Position | Secondary Data |

| Case RoRo | |||||||||

| A | Pure car truck carrier (PCTC) | 21 | All European seas | 1.7 million car equivalent units | New cars, commercial vehicles, semi-trailers, high & heavy cargo | Norway | Head of sales and marketing, business generation and performance | Senior | Company website, annual reports, internal newsletters |

| B | Pure car truck carrier (PCTC) | 10 | North Sea and Baltic Sea | 0.8 million units | New cars, commercial vehicles, trailers high & heavy cargo | Germany | Manager, quality & technology | Senior | Company website, annual reports, internal newsletters |

| C | RoRo | 10 | North Sea | - | RoRo, trailers, high and heavy | Norway | Director, shipping division | Senior | Company website, annual reports, internal newsletters |

| D | RoRo | 5, including 3 RoRo | North Sea and Baltic Sea | - | Project cargo, paper products, rolling units | Sweden | Head, marine transportation | Senior | Company website, annual reports, internal newsletters |

| E | RoRo LoLo | 11, including 8 RoRo vessels | North, Baltic, Mediterranean Seas | - | Project cargo, paper products, military transport | Sweden | Managing director | Senior | Company website, annual reports, internal newsletters |

| Case RoPax | |||||||||

| F | RoPax RoRo | 37, including 31 RoPax and 6 RoRo | North Sea, English Channel, Baltic Sea | 7 million passengers, 1.5 million cars, 2 million freight units | Passengers, RoRo cargo, new cars and project cargo | Sweden | Freight commercial manager Scandinavia | Senior | Company website, annual reports, internal newsletters |

| G | RoPax RoRo | 50 | North Sea, English Channel, Baltic Sea | 6 million passengers, 31 million lane-meters of freight | New cars, passengers, trailers | Denmark | Director, environment and sustainability | Senior | Company website, annual reports, internal newsletters |

| H | RoPax | 6 | North Sea | 4 million passengers, 0.9 million cars, 0.71 million freight units | Passengers, cars, trailers | Norway | Vice president, marine | Senior | Company website, annual reports, internal newsletters |

| I | RoPax | 1 | Baltic Sea | - | Passengers, trailers | Finland | Chief operating officer | Senior | Company website, annual reports, internal newsletters |

| J | RoPax | 4 | Baltic Sea | 1.6 million passengers, 0.48 million cars, 0.73 million lane-meters of cargo | Passengers, trailers | Sweden | CEO | Senior | Company website, annual reports, internal newsletters |

| K | RoPax | 4 | North Sea | 1.1 million passengers, 0.34 million cars, 50,000 trailers | Passengers, freight | Norway | Managing and technical director | Senior | Company website, annual reports |

Table 2.

SECA compliance measures and SECA-driven slow steaming. Source: Interviews.

| Company Name | SECA Compliance Measures | SECA-Driven Slow Steaming | SECA-Driven Increased BAF |

|---|---|---|---|

| RoRo | |||

| A | MGO and LNG for new vessels | No | ✓ |

| B | MGO and scrubbers | No | ✓ |

| C | MGO and ultra-low sulfur fuel | No | ✓ |

| D | Ultra-low sulfur fuel (RMD 80) | No | ✓ |

| E | MGO | Yes—Reduced speed from 16.5 knots to 14.5 knots between Finland and Germany | ✓ |

| RoPax | |||

| F | MGO, scrubbers, and methanol | No | ✓ |

| G | Scrubbers, ultra-low sulfur fuel and MGO | No | ✓ |

| H | Scrubbers and MGO | No | ✓ |

| I | MGO | Yes—reduced speed from 19.5 knots to 17.5 knots on a route between Finland and Sweden | ✓ |

| J | LNG and MGO | No | ✓ |

| K | LNG and MGO | No | ✓ |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Raza, Z.; Woxenius, J.; Finnsgård, C. Slow Steaming as Part of SECA Compliance Strategies among RoRo and RoPax Shipping Companies. Sustainability 2019, 11, 1435. https://0-doi-org.brum.beds.ac.uk/10.3390/su11051435

AMA Style

Raza Z, Woxenius J, Finnsgård C. Slow Steaming as Part of SECA Compliance Strategies among RoRo and RoPax Shipping Companies. Sustainability. 2019; 11(5):1435. https://0-doi-org.brum.beds.ac.uk/10.3390/su11051435

Chicago/Turabian StyleRaza, Zeeshan, Johan Woxenius, and Christian Finnsgård. 2019. "Slow Steaming as Part of SECA Compliance Strategies among RoRo and RoPax Shipping Companies" Sustainability 11, no. 5: 1435. https://0-doi-org.brum.beds.ac.uk/10.3390/su11051435

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.