1. Introduction

Sustainability is not a new concept. In 1713, the monograph

Sylvicultura oeconomica was published [

1]. In his monograph, Hanns Carl von Carlowitz considered how to make sustainable use of wood “

steady and sustained use of timber” [

2]. In 2015, the General Assembly of the United Nations (UN) accepted a new set of 17 Sustainable Development Goals and 169 targets for people, the planet and prosperity. The document came into effect on 1 January 2016 and will be the strategic map for the decisions makers in the public and private sector until 2030 [

3]. Nowadays, sustainability is a crucial theoretical framework in the scope of environmental economics [

4]. Social and financial exclusion, increasing income disparities, an inefficient redistribution system, and negative economic externalities (such as: noise, pollution, smog) are typical challenges faced by national and local governments. At this point, the special role of sustainable development in dealing with a wider and socially harmful phenomenon, namely negative externalities, needs to be emphasized.

When assessing the role of the financial sector in the economy, it can be stated that this sector plays a key role in the implementation of the sustainable development goals [

5]. Effectively operating financial markets ensure efficient capital transfer in economy, reducing financial risk and ensuring stable financing of the real economy [

6]. The traditional paradigm on which the financial sector is based relies on multiplying profits. This context is well reflected in the assumptions of the efficient market hypothesis, which does not take into account the aspects of sustainable development. The financial sphere evolving towards sustainable finance allows for the inclusion of social and environmental aspects into the general theory of finance, correlating with the pillars of sustainable development [

7]. Sustainable finance needs to provide an alternative to the conventional finance paradigm and should be redirected towards ensuring wellbeing and welfare in the global economy. In a nutshell, the paradigm of conventional finance turns out to be inadequate and incoherent with the changes taking place in the economy, in particular related to the growing threat of social and environmental risk [

8,

9]. Sustainable development is a very specific economic category, which requires an effective funding mechanism that should take into account a three-dimensional (economic, social, environmental) sustainability perspective [

5,

7].

The literature reveals that the relation between finance and sustainable development is a relatively novel area. Earlier theoretical models were based on selected aspects of sustainable finance. The models failed to search for the relation between finance and negative externalities from the perspective of sustainable development. This study provides an original approach to sustainable finance and negative externalities, especially as it presents a systematic review of definitions in the scope of sustainable finance, explains the link between sustainable finance and three pillars of sustainable development and describes negative externalities in this context.

The paper aims to verify the hypothesis assuming that there is a strong interaction between sustainable finance and negative externalities which need to be managed. The study aims to draw attention to the significant gap in the current research related to the issues of financing sustainable development. The concept of sustainable development, viewed as an economic category, requires considerable attention, with questions remaining unanswered. While most empirical studies have focused on the effects of economic growth and economic and financial development on negative externalities, especially in the context of environmental quality [

10,

11], this study extends the research and refers to the impact of financial development, not only on the environmental but also social effects of economic growth and development. The study contributes to existing research, covers the gap in existing literature, and provides a complex theoretical framework for defining and understanding the problem of sustainable finance and its role in the contemporary economy from the perspective of achieving sustainable development goals (Agenda 2030) and mitigating negative externalities. In particular, the paper assumes that sustainable finance significantly undermines negative externalities and that it is possible to assign particular types of sustainable finance to the negative externalities that they affect. In this approach, environmental finance mitigates environmental degradation, in particular green finance affects green gas emission, carbon finance supports decarbonisation processes, microfinance reduces the effects of social exclusion and, finally, development and responsible finance affect both environmental and social performance. Green finance is a part of sustainable finance referring exclusively to the environmental pillar of sustainable development; while sustainable finance is a three-dimensional perspective and is coherent with all three pillars of sustainable development: economic, social and environmental. The authors assume that the more instruments of sustainable finance are included in the financial system; the system is more sustainable and responsive to negative externalities and as result supports the achievement of sustainable development goals. In the public financial system, one can distinguish such instruments as: environmental taxes, sustainable public debt and deficit (sustainable fiscal policy) or public expenditures that support the financing of sustainable development. In the market (commercial) financial system, there are such instruments as sustainable financial products, and among this group: green financial products influencing environmental quality and microfinance supporting social inclusion.

In the selected countries, financial systems differ and are more or less sustainable with regard to the number of sustainable financial instruments incorporated in the public and private financial systems. Usually, developed countries have a developed financial market and sustainable financial systems; by contrast, developing economies base on conventional (one-dimensional) financial systems and are modernizing their financial systems towards the three-dimensional, sustainable financial systems. Thus, in developing countries sustainable finance usually is more important. However, the opposite effect is observed for developed financial markets (for example Luxemburg, the United Kingdom) because of financialisation, which is the reason for the distressed relation between sustainable finance and negative externalities. The main goal of the study is to explain the link between sustainable finance and three pillars of sustainable development and to describe negative externalities in this context.

The article, contributes to the existing research by analyzing the sustainability of financial systems of European Union (EU) countries belonging to the Organization for Economic Cooperation and Development (OECD) and their impact on economic, environmental and social development. The authors argue that developed countries are more financially sustainable and as a result they represent a higher level of sustainable development indicated by sustainable developments goals indicators included in Agenda 2030. The paper aims to contribute to the body of knowledge of finance theory, especially providing a new general theory of sustainable finance. The study contributes to finance in the following ways:

providing original, systematic knowledge about the sustainable finance paradigm and sustainable finance typology;

explaining the link between sustainable finance and other pillars of sustainable development: economic, social and environmental, in view of negative externalities,

diagnosing and explaining differences among EU countries in the scope of traditional pillars of sustainable development: economic, social and environmental development and the new proposal of the authors, which implies taking into account among them also the sustainable finance pillar;

emphasizing the role of sustainable finance in mitigating negative externalities.

The results seem to indicate that there is a strong link between sustainable finance and negative externalities which affects economic, social and environmental development. The relationship between financial development and economic, social and environmental development depends on the country group (developed or developing ones). The extensive analysis shows that:

in the case of Scandinavian countries economic growth does not affect the natural environment negatively; such dependencies are no longer so obvious in the case of other EU countries belonging to the OECD;

well developed countries in Western Europe, i.e., Belgium, Germany, Luxembourg, the Netherlands and the United Kingdom, achieved high ranking positions in the economic, social and very often also financial development but much worse results in the case of environmental development;

the countries located in Southern and Eastern Europe, including, Greece, Hungary, Portugal, and Poland most often reported worse results in terms of economic and social development than in the environmental scope;

similar results are observed, for the country groups with similar geographical location. The geographical proximity of these countries has a significant impact on the positions they achieve in the rankings;

the countries with the highest level of financial development (Sweden, Denmark) are also the country group with the highest level of economic, social and environmental development;

the countries with the lowest level of environmental development are the countries with the highest level of the greenhouse gas emissions (Germany, the United Kingdom, France, Italy, the Netherlands, Poland, Spain);

the countries with the highest ranking positions in financial development are the countries with: a well-developed sustainable financial system with strong elements such as: the system of environmental taxes (Denmark, the Netherlands, Latvia); a high level of gross domestic expenditure on research and development (R&D), percentage of GDP (Denmark, Sweden and the Netherlands), a sustainable public debt (Denmark, Sweden) or an efficient redistribution system (Finland, Sweden, Denmark);

it is possible to observe a positive relationship between the countries with the highest green growth indicators and the countries with highest financial development.

The paper is organized as follows: an introduction has been presented in

Section 1.

Section 2 discusses the literature review.

Section 3 presents the data, the variable description and methodological framework.

Section 4 provides the empirical results and

Section 5. offers conclusion.

4. Research Results and Discussion

Table 5,

Table 6,

Table 7 and

Table 8 present the results of classification separately for each analyzed scope: economic, social, environmental and financial ones in 2007, 2013 and 2016.

In accordance with the adopted assumptions, the countries achieving lower ratings of the relative taxonomic measure of development occupy higher positions in the created rankings. In all rankings, the following countries were in top positions:

- (a)

in the area of economic development: Denmark, Sweden, and the Netherlands or Germany;

- (b)

in the area of social development most frequently: Sweden, Finland and the Netherlands (in 2007) or Denmark (in: 2013 and 2016);

- (c)

in the area of environmental development: Denmark, Sweden Austria (in 2007) and Latvia (in: 2013 and 2016);

- (d)

in the area of financial development: Denmark, Sweden and the Netherlands.

It is clear that in the case of Scandinavian countries one can speak of permanent separation of economic growth from its negative impact on the natural environment. Such dependencies are no longer so obvious in the case of other EU countries belonging to the OECD. Therefore, attention need to be paid to the most economically developed countries in Western Europe, i.e., Belgium, Germany, Luxembourg, the Netherlands and the United Kingdom, whose high rankings in the case of economic, social and very often also financial results correspond to much worse results in the case of environmental development. Such relations have already been observed in the earlier works of the authors [

116,

128,

138]. They clearly show that simultaneous development in all areas at the same level is difficult to achieve in practice. This is also confirmed most often by worse results in terms of economic and social development and much better in the case of the environmental area in the case of countries located in Southern and Eastern Europe, including: Greece, Hungary, Portugal, and Poland. These are economically less developed countries, at the same time causing less pressure on the natural environment.

This also draws attention to the lack of changes in the classification results in the last rankings positions in case of the financial scope. In all rankings, the last three places were occupied by: Poland, Belgium and Luxembourg. Particularly surprising is the appearance of a country like Luxembourg in this group, which is indicated as one of the financial centers in Europe.

The similarity of the results achieved is also visible, depending on the geographical location of the EU countries belonging to the OECD included in analysis. The similar results of Scandinavian countries or countries located in Eastern and Southern Europe are confirmed. The geographical proximity of these countries has a significant impact on the positions they achieve in the rankings.

The results of the classification of EU countries belonging to the OECD in the analyzed period are basically similar to each other, which is also confirmed by the Kendall τ correlation coefficients assigned to the rank of countries in subsequent years (

Table 5,

Table 6,

Table 7,

Table 8,

Table 9 and

Table 10).

In 2007, only in the case of economic and social areas, the average dependence between the classification results was identified. The result of this kind should not come as a surprise. They also repeat in the case of rankings from subsequent years. As a rule, economic development causes similar changes in social development. The obtained results confirm the previously observed lack of dependence between ranking positions in the economic and environmental areas. The relationship between these areas basically does not occur.

The previous considerations present the results of classification of EU countries belonging to the OECD separately due to economic, social, environmental and financial aspects. In order to assess the situation of the analyzed country group, from the economic, environmental, social and financial point of view, a multi-criteria taxonomy was applied. This method allows to analyse the obtained results as the one data set. On the basis of 64 features describing development in the economic (13 features), social (28 features), environmental (8 features) and financial (15 features) areas, 7 typological groups were obtained in 2007 and 2013 and 8 groups in 2016 (

Table 11).

The largest group is the first one, in which, depending on the analyzed year, consist of 11–13 EU countries, while the eight of them did not change their positions in the subsequent years. Noteworthy is Belgium, which in 2013 created a one-piece cluster, and in the remaining years was included in the first group. A similar situation applies to the United Kingdom-in 2002 it created one-element cluster, and in the remaining years belonged to the first group. Finland and Italy also moved between the first and the second group. Out of the 23 surveyed countries, only eight in all the examined years were included in the same, first typological group. They were the four countries of Western and Northern Europe (Austria, Denmark, the Netherlands, Sweden), three located in the east of Europe (the Czech Republic, Hungary, and Slovakia), and one from the south of Europe (Slovenia).

It is worth taking a closer look at which features had the greatest impact on the allocation of the analyzed countries to the designated typological groups. In the subject literature [

107] it is pointed out that very often the division of objects into groups is affected by a limited number of indicators whose level clearly differentiates the examined objects. In order to determine which indicators had the greatest impact on the classification results, a measure (11) was calculated according to the following formula:

where:

Vj—the coefficient of variation calculated for the

j-th diagnostic feature;

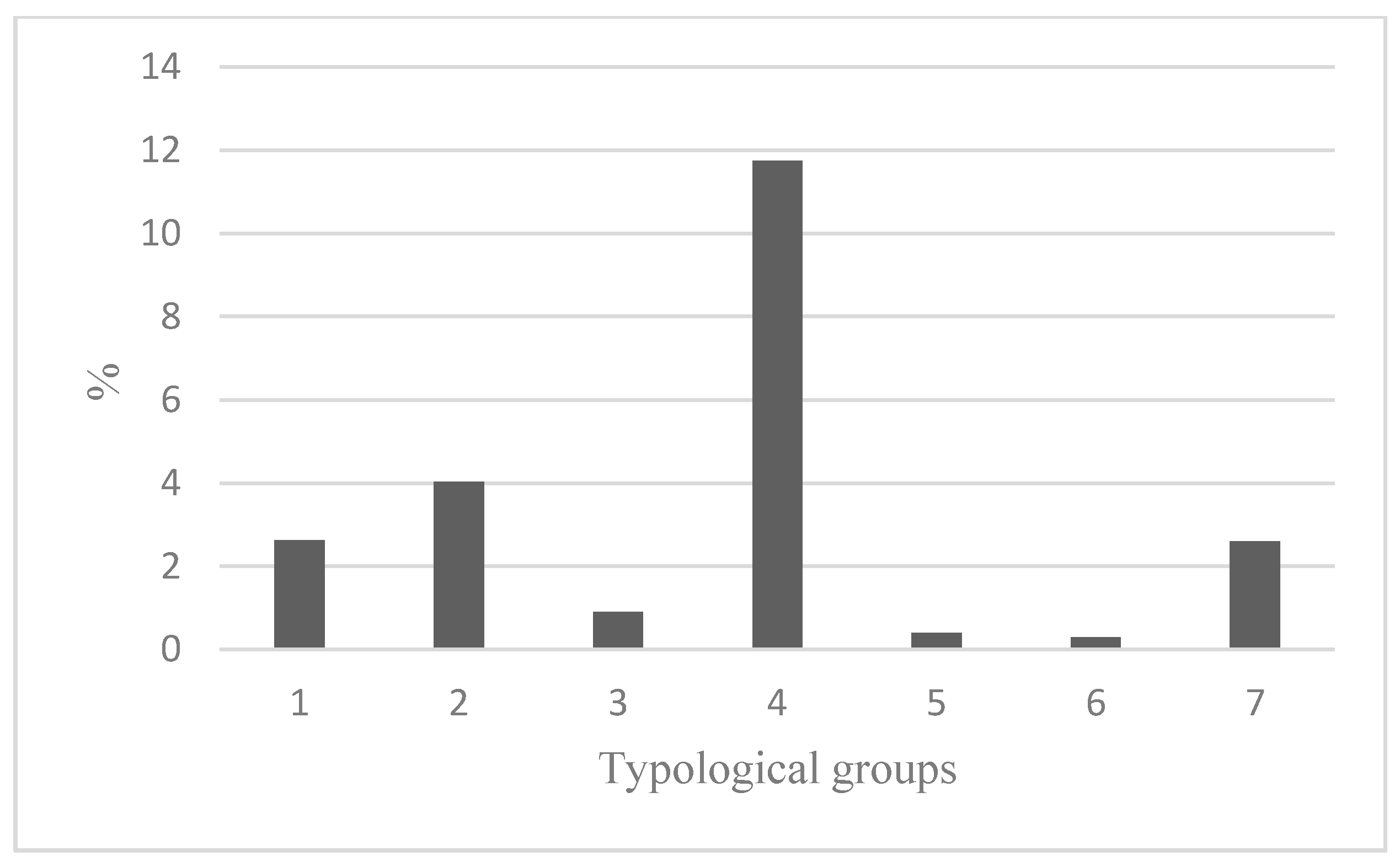

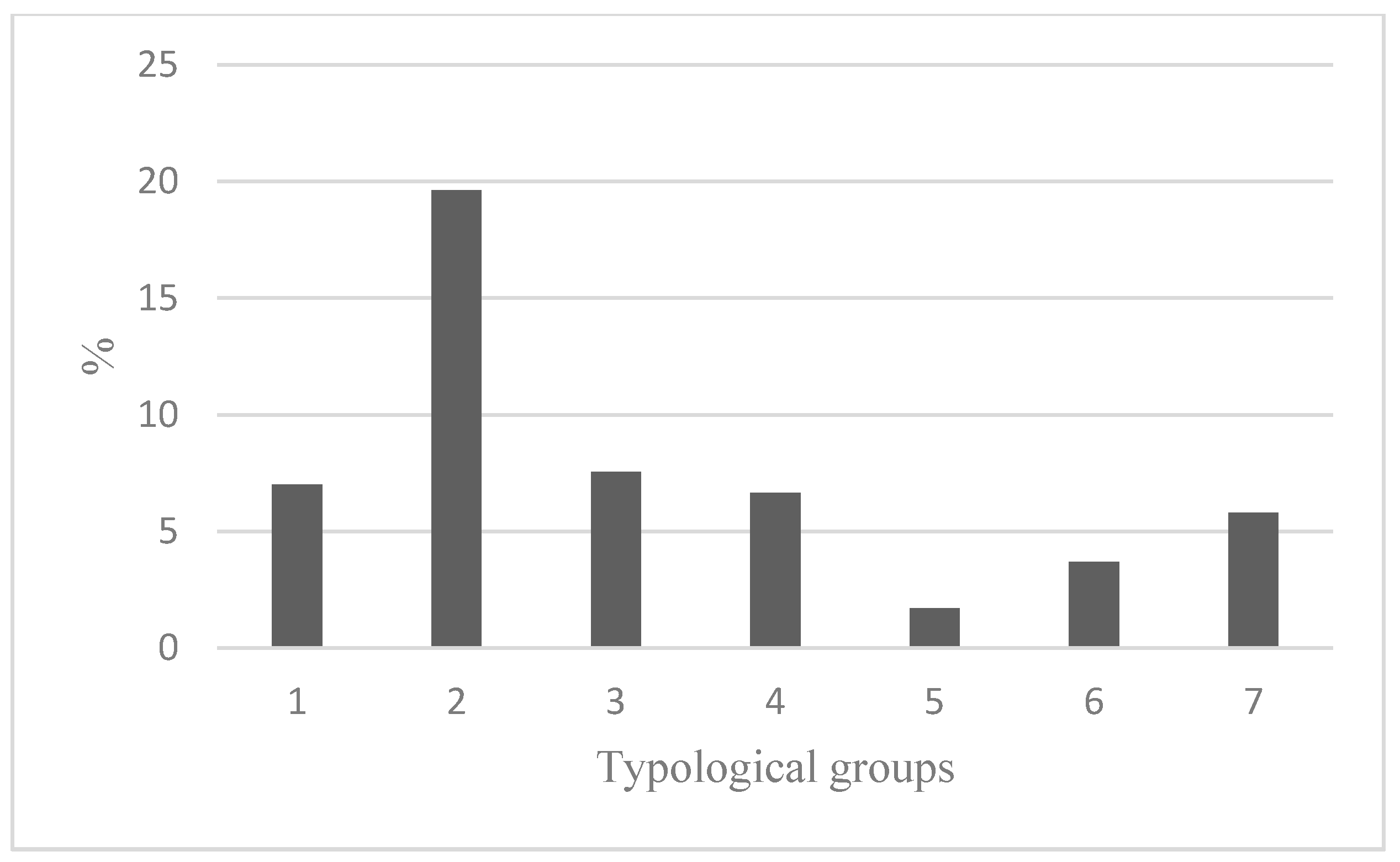

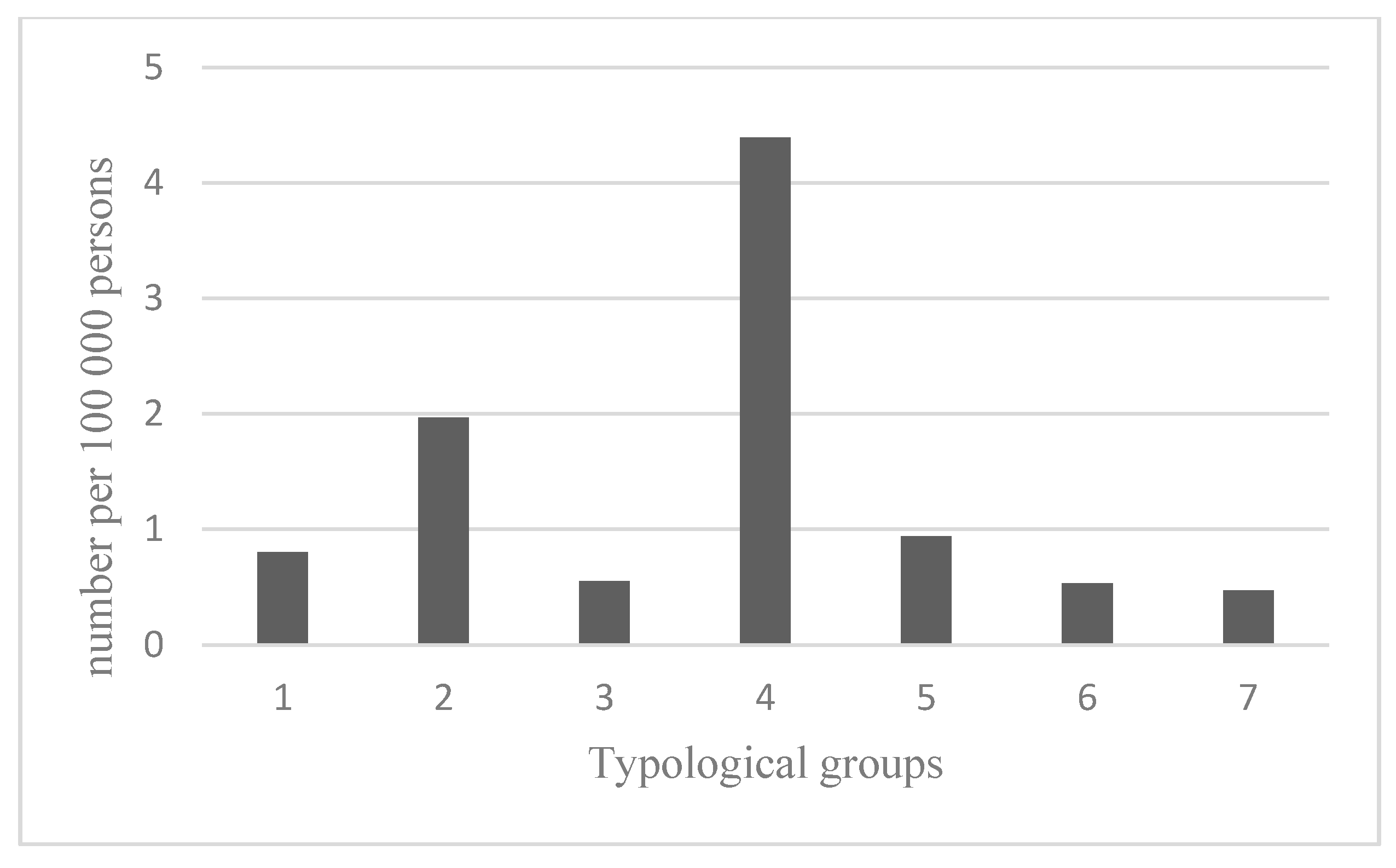

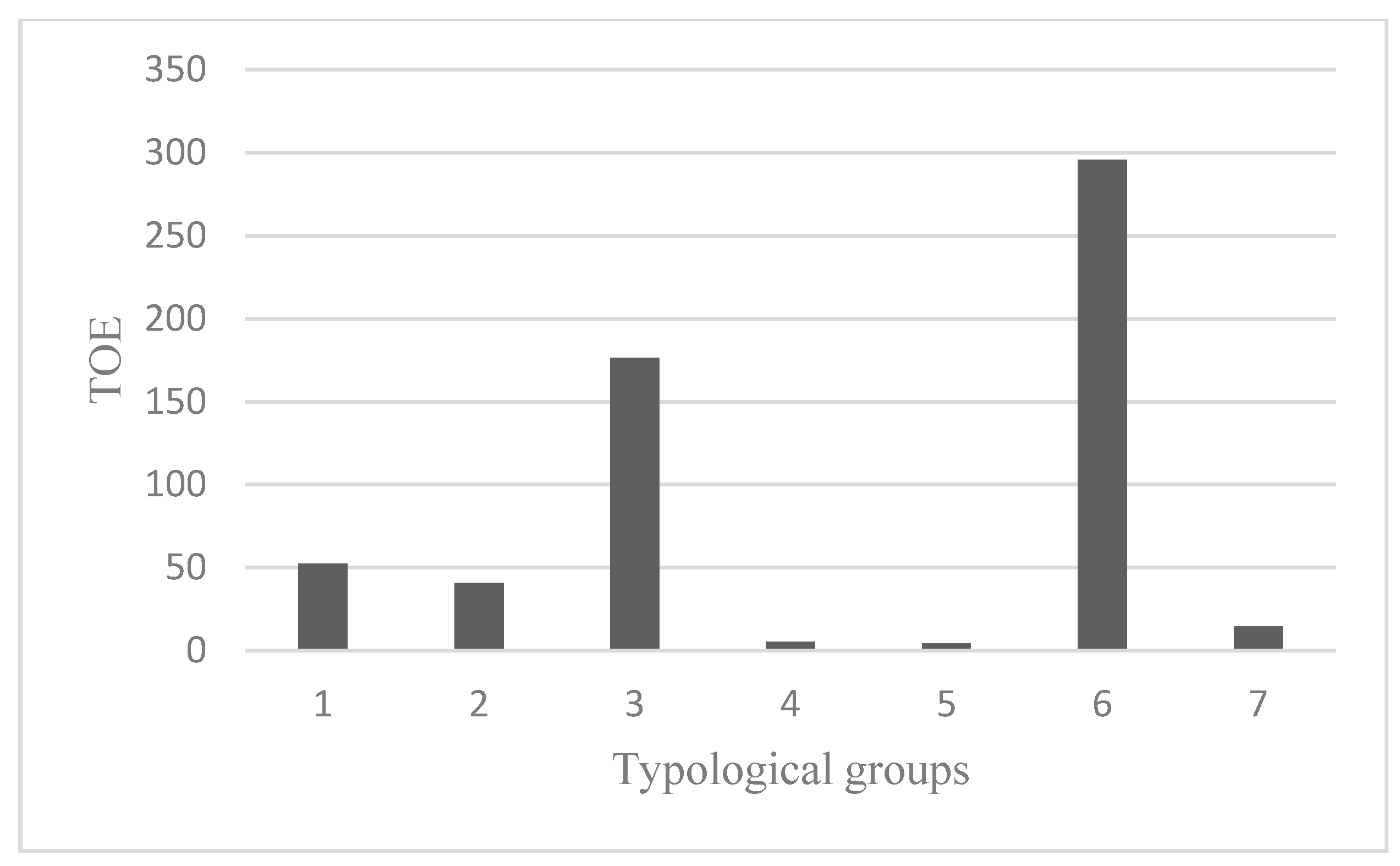

This measure could be interpreted as weights defining the relative importance of individual indicators. It turned out that in the study of the level of sustainable development of OECD countries in Europe, the following four indicators are the most important in all examined years:

X3.10-self-reported unmet need of medical care by a detailed reason, % of population aged 16 and over, too expensive or too far to travel or waiting list,

X3.15 - population unable to keep home adequately warm, % of population,

X3.22 - death rate due to homicide, number per 100,000 persons,

X2.2 - primary energy consumption equivalent (TOE). The share of each of them in the overall volatility of all ratios exceeded 3%, while the share of almost 70% of the ratios did not exceed 2%. In order to show the differences in the level of the aforementioned features, average values in groups were calculated in particular groups and are presented in

Figure 1,

Figure 2,

Figure 3 and

Figure 4.

According to

Figure 1,

Figure 2,

Figure 3 and

Figure 4, the results for the individual, analyzed groups are significantly different. A detailed analysis of the average level of diagnostic features in individual groups may be the basis for explaining why, for example, in the first group there were countries that would seem to have a different socio-economic situation, e.g., Austria and Greece. Their presence in the same group was caused mainly by the low level of such features as: death rate due to homicide, number par 100,000 persons, primary energy consumption, Million tonnes of oil equivalent (TOE), Income from natural resources, percent of GDP, Agricultural factor income per annual work unit (AWU), chain linked volumes, and the low level of features: GDP, general government expenditure on social protection, % of GDP.

In the second group in 2016, there were three countries characterized by a very high (except Poland) level of the population unable to keep home adequately warm by population status, % of population, total and severely materially deprived people,%, and the lowest in comparison with other groups, the average levels of such traits as: self-perceived health, very good or good, % of population, final energy consumption in households per capita, kg of oil equivalent. France and Spain have created a two-element cluster due to the similar values of the majority of diagnostic characteristics accepted for the study, although significant differences are noted in some of the features. This applies to the following indicators: total involuntary temporary employment by sex, % of employees aged 20 to 73, housing cost overburden rate by poverty status, % of population (twice the rate for Spain), adult participation in learning by sex, % of population aged 25 to 70 (twice the rate for France), population unable to keep home adequately warm by poverty status, % of population, Total (twice the rate for Spain).

Another two-element group is Estonia and Latvia, countries for which the average levels of indicators adopted for the study significantly diverge from other groups. This applies to 18 features with the highest average values and thirteen with the lowest values.

The separation of Luxembourg was related to the fact that the majority of diagnostic features, which had the greatest discriminatory significance, were significantly different from the average level for the countries studied. In the case of some of the characteristics for Luxembourg, the lowest values were recorded among OECD countries, for example, such features as: population unable to keep home adequately warm by poverty status, % of population, primary energy consumption, Million tonnes of oil equivalent (TOE), Government support to agricultural research and development, euro per inhabitant. Other indicators for this country were the highest, such as real GDP per capita, chain linked volumes (2010), euro per capita, people killed in accidents at work, number per 100,000 employees, ammonia emissions from agriculture (source: EEA), kilograms per hectare, % of gross national income (GNI). According research carried out by Guijarro and Poyatos (2018) Luxemburg is one of the best performing countries regarding the sustainable development [

139].

In a similar way the other one-element clusters may be analyzed. Germany ranked in the sixth group in the case of 13 diagnostic features differed in plus from the other groups, and in the case of six features in minus. In the case of Ireland, such discrepancies concerned 16 indicators with the lowest values and five with the highest values.

When summarizing the research results, the attention is drawn to the dominant position of Scandinavian countries as leading countries in the field of sustainability. This finding is also reported by Bluszcz et al. (2016), Bujanowicz-Haraś et al. Filip et al. (2014) [

140,

141,

142]. These countries are an example of countries implementing postulates of sustainable development, which is reflected in every pillar of sustainable development: economic, social and environmental. Interestingly, these are not the countries with a large financial market (inter alia capitalization, financial assets to GDP) in comparison with the biggest European financial centers (London, Luxemburg, Frankfurt, Amsterdam, Paris, Brussels, Dublin, Geneva). This fits in with the conclusions of Goldsmith’s research [

143] which indicated that economic policy should focus less on the dilemma if within a given country a market-oriented or a bank-oriented system dominates, and focus more on the legal system and relevant legal regulations as well as on specifying reform directions in the result of which actions will be initiated to stimulate the development and effective functioning of capital markets as well as banks. The financial system in Scandinavian countries is characterized by a high level of sustainability due to the adopted solutions and instruments effectively financing the goals of sustainable development. Scandinavian countries are countries characterized by the low level of income inequality, low level of deficit and public debt, they are part of balanced debt management, a developed system of green taxes and support for companies and households in access to preferential financing of modern environmentally friendly solutions. Our finding is in line with research results presented by Lin and Li (2011) [

123], Scrimgeour et al. (2005) [

144], and Fisher (2008) [

145] that assume that sustainable public finance (especially environmental taxation) mitigate the impact of negative externalities (air pollution). At the same time, Scandinavian countries allocate significant public funds to finance pro-environmental solutions. Due to the fact that the financial (market and public) system is based on instruments supporting social and environmental development, it is a highly sustainable and effective financing system for sustainable development goals. Apergis et al. (2013) and Lee and Min (2015) declare research results that are coherent with our study [

124,

125]. On the other hand, leading financial centers (London, Frankfurt etc.) are located in countries with the highest greenhouse gas emissions, which results in a reverse relationship between financial development and environmental development in these countries. In addition, the great financial centers of Europe focus their activity on investment banking or financial engineering, which are more profitable and burdened with lower risk than financing the real sphere. Therefore, it can be concluded that the level of sustainability of the financial system is determined by the state policy which is responsible for legal regulations and the framework of the financial system [

24,

146,

147].

Referring to external effects, the financial system should aim at sustainability, here as: (i) it is constantly exposed to market failures (which is associated with the first group externalities: externalities induced by market failures); (ii) state intervention includes to be aimed to fix on sustainable public policy (with sustainable public instruments as green taxes, CO2 limitation, low level of deficit and public debt, the legal system, et al.) and sustainable public finance (financial instruments, fiscal policy, management financial risk, et al.); (iii) development should be expected to push market toward internalizing externalities (sustainable private finance, as: effective functioning of capital markets as well as banks, et al.).

5. Conclusions

The research explains the link between sustainable finance and the three pillars of sustainable development and describes negative externalities from this point of view. The hypothesis assuming that there is an interaction between sustainable finance and negative externalities has been verified positively. In order to diagnose and explain the differences between EU countries in the traditional pillars of sustainable development: economic, social and environmental development and the authors’ new proposal, which implies including a sustainable financial pillar among them, the multi-criteria taxonomy was used. This method was applied to create typological groups within which the average values of the accepted diagnostic features were determined. On the basis of 62 statistical features characterizing development in the economic (12), social (28), environmental (7) and financial (15) scope, 7 groups of countries were obtained in 2007 and 2013 and 8 groups in 2016. A detailed analysis of the average level of diagnostic features in individual groups has become the basis for clarifying which indicators implicate the division of countries into specific groups. When analyzing

Figure 1,

Figure 2 and

Figure 3, it should be noted that they include mainly indicators that can be classified as negative externalities.

The originality of the research consists in including in the analysis of the financial sphere variables representing sustainable finance and extending the classical approach based on economic variables in the assessment of financial development with variables representing the environmental and social aspect in finance. At the same time, the variables for researching the financial sphere were selected in such a way as to correspond with the public and commercial financial system. Such an approach is justified due to the relationships that occur between finances and negative externalities, which we tried to prove in the analyses. The authors would like to emphasize that in the literature there are not yet described any concepts for studying the links between the social, economic, environmental and financial development of the world’s countries. The grounds of this kind of research are established. Therefore, there are not enough comprehensive databases in this area. It is the main problem in the analyses related to these areas but this direction of the research seems to be inevitable. Research of this kind is a natural consequence of the development of knowledge and needs of countries in the world in the field of sustainable development.

The results of the study presented in the paper can be divided into two parts. The first one is devoted to the construction of the ranking of EU countries belonging to the OECD in each analysed area: social, economic, environmental and financial. In the second one, the results of correlations between considered areas and explanations of the main reasons influenced on the ranks of these countries are presented. The authors made efforts to explain which indicators had the most influence on the countries positions and its division into typological groups. Out of the 23 analyzed countries, only eight in all the examined years were included in the same, first typological group. The group included four countries of Western and Northern Europe (Austria, Denmark, the Netherlands, and Sweden), three located in the East of Europe (the Czech Republic, Hungary, Slovakia) and only one from the south of Europe (Slovenia). Countries ranked first in the rankings: Denmark, Sweden, and the Netherlands were characterized by sustainable development in all four researched areas.

As a result of the conducted analyses, it was shown that geographical location weighs on results. Similar results were obtained by Scandinavian countries or countries located in Eastern and Southern Europe. Most often, worse results in terms of economic and social development were observed, and much better in the case of the environmental area in the case of countries located in Southern and Eastern Europe, including Greece, Hungary, Portugal, and Poland. Countries that are less developed economically exert less pressure on the natural environment. An interesting observation resulted in the financial sphere where the effect of financialization on the countries’ places in the rankings was observed. The development of financial markets due to advanced financial engineering did not harmonize with economic and social development (e.g., Luxembourg). Nevertheless, in the analyzed period, research has shown that in most of the countries surveyed, the pressure is increasing and the natural environment also in the financial sector. It should be noted that the obtained results are the effect of the indicators used to show the current level of development of EU countries belonging to OECD in the areas of social, economic, environmental and financial development. The ordering of countries is not constant and this classification may be different if the final set of diagnostic indicators change.

Generally, research shows a preliminary tendency to include the financial area into the analysis of the impact of sustainable development on the public and market financial system. In the future, this trend, which has been demonstrated in the countries of Denmark, Sweden, and the Netherlands, can have a strong occurrence in other countries. Externalities affect resource allocation because the market fails to fully price the external effects generated by some economic activities. The existence of externalities will thus lead to a sub-optimal allocation. Too many resources are used in processes conferring uncompensated social costs, suboptimal allocation of financial resources within the financial system, may cause financial crises, undermine the economy. The important role of finance in eliminating the effects of negative externalities is noticeable, especially in the social and environmental dimension. As a result of the research, a strong positive relationship was found between economic development and social development, economic development and environmental development as well as the sphere of sustainable finances and economic, social and environmental development.

Although our research has shown that there are financial systems (Scandinavian countries) characterized by a high level of sustainable development thanks to the adopted solutions and instruments that effectively finance the goals of sustainable development, the other countries in the global perspective should strive to implement adequate instruments for financing the objectives sustainable development. Globally, after the financial crisis countries should strive to create policies that favor sustainability, and in particular to achieve a low level of income disparities, low deficit and public debt as part of sustainable debt management, a developed green tax system, green investment and business support and households in access to preferential financing for a modern, environmentally friendly solution. In global terms, a common policy is needed that will help smoothly eliminate the effects of negative externalities. There is a significant and important role of the finance and financial systems. Thanks to financial instruments, the possibility of elimination or mitigation the effects of negative externalities is noticeable, especially in the social and environmental dimension. In global terms, the period of economic development favors the impact of environmental development through the financial system (a series of innovative instruments) as well as social and environmental development.

It is worth addressing actual policy recommendations and challenges referring to sustainability and finance. Our paper fills the significant gap in the current research related to the issues of financing sustainable development and negative externalities. The challenges include: balancing sustainable development dimensions which are typically focused on the long term with the typically short-term profit focus of conventional finance. The difference is crucial for efficiency of financing for sustainable development as there is a need to identify and evaluate negative externalities [

9]. A few suggestions can be made to include the sustainable development perspective into finance: (1) internalization of externalities in the calculation of an investment (i.e., in a company’s present value); (2) assigning a long-term horizon to investments, also as a necessity for maintaining the prospect of safeguarding financial capital for the future; (3) progressive substitution of financial ratios with sustainability ratios; (4) a changing perspective on the connotation of financial profits [

9]. On the other hand, there are many limitations that prevent effective use of finances to provide sustainability, referring especially to designing sustainable financial systems [

111]. There are three scopes that need to be improved discussing in the literature review: (a) measurement (better indicators and tools for assessing the sustainable development goals (SDGs); (b) policy reforms to create benefits for financing and investing in sustainable development; and (c) improving communications among stakeholders in order to better match supply and demand for the sustainable financing of SDGs [

148].

The authors see the need for further in-depth studies of the analyzed phenomenon, especially in the context of the impact of individual financial sector instruments on sustainability. The next step of these analyses could be devoted to the more explanatory analyses which could describe the causality of the obtained rankings and division into typological groups. This kind of analysis can be found in these papers: Li et al. (2019), Ferrero-Ferrero et al. (2016) and Crifo et al. (2015) [

149,

150,

151]. In order to assess the situation in the future of the analyzed country group, from the economic, environmental, social and financial point of view, it is necessary to develop a uniform approach and uniform data in order to be able to assess the sustainability of the financial system. The authors encountered a number of difficulties in the selection of data characterizing the country group, from the economic, social and financial point of view. While the data is available for economic, environmental, and social aspects, the data for the financial pillar is still being discussed in many countries and by many researchers. For EU countries belonging to OECD, there are no uniform data and indicators in the long-term (e.g., 10 years). They change in the long-term and, for example, the EU recommends new indicators every few years, just as the authorities of individual countries do. Other researchers also show data problems and the need to verify them in the future [

149,

152]. This situation has forced us (despite the fact that different research discuss different indicators) to choose the most universal indicators and data. Our proposal is universal for the countries indicated, as comparisons can be made on that basis, and the data in the analyzed period did not change. Therefore, a future interesting research would be to consider a wider time window in order to observe and identify the indicators and effects of negative externalities [

153]. We accept our measurement proposal for the financial scope as a benchmark for testing other studies. This will provide the basis for determining whether there will be any positive changes in the elimination of negative externalities in the future. Our concept should be verified in the next empirical review based on data in the future. It will allow you to conclude about factors affecting the stability of the financial system and the relationship between the economic and financial point of view. The economy and the sustainability financial system needs the actually data about effects of negative externalities. In our future study we also would like to extend research carried out by Zorlu (2018), especially the problem of incorporating ESG risks to global monitoring of financial stability and stress tests [

154]. Incorporating ESG factors by financial institutions’ decision making process is not a new concept. The United Nations Environmental Programme Financial Initiative has required its implementation since 1992 [

155], and in many documents it is still there as a recommendation and as a challenge for financial markets [

156].

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}