Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach

1

Department of Economic Analysis & ICEI, Complutense University of Madrid, 28223 Madrid, Spain

2

School of Economics, National University of Costa Rica, Heredia 86-3000, Costa Rica

3

Faculty of Economics and Business, Complutense University of Madrid, 28223 Madrid, Spain

*

Author to whom correspondence should be addressed.

Sustainability 2020, 12(2), 737; https://0-doi-org.brum.beds.ac.uk/10.3390/su12020737

Submission received: 12 December 2019

/

Revised: 10 January 2020

/

Accepted: 13 January 2020

/

Published: 20 January 2020

(This article belongs to the Special Issue Sustainability as a Multi-criteria Concept: New Developments and Applications)

Abstract

:We propose addressing an organization’s adoption of an environmental certification as a multicriteria problem considering environmental sustainability as well as economic and strategic aspects. Our methodological approach uses the Analytical Hierarchy Process (AHP), which we use in an empirical application to analyze the adoption decision of several Costa Rican firms and institutions. Firstly, we select a set of economic, strategic, and environmental criteria that seem relevant for the organization’s direction. We select these criteria according to our literature review and a series of face-to-face interviews with scholars and companies’ managers. As an environmental certification, we focus on Carbon Neutral (CN), which is a domestic certification aimed at reducing or offsetting carbon emissions. For the sake of comparison, we also consider ISO 14001, which is a well-known international standard aimed at compliance with environmental norms. We conduct the AHP analysis using the answers given by 24 companies and institutions, which in aggregate terms, give CN a higher score than ISO 14001. This result is mainly due to the fact that CN ranks above ISO 14001 when attending to environmental sustainability, although ISO 14001 tends to be preferred in economic and strategic terms.

1. Introduction

The 2030 Agenda for Sustainable Development [1] established 17 Sustainable Development Goals (SDGs) as a roadmap to guarantee a more sustainable future and overcome some of the most urgent challenges of mankind. These challenges include social and economic problems such as poverty and inequality and environmental threats such as global warming and climate change [2]. By shifting from conventional, polluting patterns to cleaner and more sustainable ones, companies can play a crucial role to achieve the SDGs, especially some of them such as providing affordable and clean energy (SDG 7), decent work and economic growth (SDG 8), ensuring sustainable consumption and production patterns (SDG 12) and fighting climate change and its impacts (SDG 13); see e.g., [3,4,5].

This change in companies’ policies can involve adopting some voluntary environmental certification (VEC) or program (VEP). VECs and VEPs are non-mandatory approaches by which companies commit to improve their environmental standards in accordance with the specific requirements of each certification or program [6]. According to the OECD, these voluntary approaches “provide pragmatic responses to new policy problems, namely the need for more flexible ways to achieve sustainability, and the need to consider the rising concerns about industrial competitiveness and the increasing administrative burden” [7]. Moreover, it can be argued that VECs and VEPs are win-win approaches for companies and for society, because they improve the environmental performance of firms, while yielding them some economic and strategic benefits such as improving their competitiveness [8,9,10].

There is a wide variety of VECs and VEPs available for companies. Choosing one or some of them can be a complex task for business managers, since this decision will typically involve multiple criteria, including strategic, economic, environmental, or even ethical ones. The Analytical Hierarchy Process (AHP) can be a helpful tool to assist managers in taking certification decisions. AHP was developed by Saaty [11] and has become one of the most used methods, both in the public and the private sector, for making decisions that involve multiple criteria.

In business, AHP is typically used in contexts of uncertainty that require evaluating different alternatives based on qualitative and quantitative criteria. For example, Chin et al. [12] used AHP to rank success factors and develop strategies to implement an Environmental Management System (EMS) in Hong Kong manufacturing companies, as well as to decide whether to implement ISO 14001. Also in Hong Kong, Pun and Hui [13] investigated the companies’ criteria, sub-criteria and benefits of implementing ISO 14001. Mathiyazhagan et al. [14] used AHP in combination with experts’ opinions to rank the pressures to adopt Green Supply Chain Management in the Indian mining and mineral industry. In the same country and sector, Shen et al. [15] evaluated the relative importance of social, economic, and environmental criteria of green supply chain management. Cuadrado et al. [16] ranked the main factors involved in the construction of an industrial building in Europe. Ho et al. [17] used AHP to determine the importance of the barriers faced by electrical and electronics manufacturing companies in Malaysia when implementing material efficiency strategies. Thanki et al. [18] evaluated the influence of lean and green paradigms on the overall performance of small and medium enterprises. Malik et al. [19] applied AHP to evaluate the environmental performance of healthcare suppliers in the United Arab Emirates. Wang et al. [20] calculated the effect of the technical measures implemented in the tobacco industry for energy conservation and emissions reduction. Karaman and Akman [21] applied AHP to identify key criteria and sub-criteria of a Corporate Social Responsibility program in the airline industry.

In this study, we use AHP to evaluate the preferences of firms when choosing between different VECs and, ultimately, the propensity of the same firms to choose a specific VEC. We apply our proposal to the selection of an environmental certification in a group of Costa Rican firms and public institutions. Costa Rica is considered an international leader in terms of environmental sustainability, especially in forest conservation and the reduction of the Greenhouse Gas (GHG) footprint [22]. Different public and private environmental approaches contributed to improve the environmental quality and green image of Costa Rican companies and the country itself [23,24,25,26,27,28].

The Carbon Neutrality Program is a recent public initiative looking for a cleaner economy in Costa Rica. After measuring their carbon emissions and reducing or offsetting them, participating organizations can obtain a Carbon Neutral (CN) certification [29,30,31]. We are interested in finding out the managers′ preferences and criteria that determine their decision to take part in this program. For the sake of comparison, we consider an alternative certification, namely ISO 14001, which is a well-known international standard.

The first methodological aim of our study is to establish a relevant set of criteria that firms and institutions consider when choosing an environmental certification. To do so, we perform three preliminary steps, which include an exhaustive bibliographic review, a series of in-depth face-to-face interviews with 11 managers of certified companies and a discussion with two scholars, experts in the field. As a result, we come up with a selection of criteria that we group in two blocks: environmental sustainability and economic-strategic factors.

Then, we use the AHP methodology with a double purpose: first, to measure the weights given by Costa Rican firms and institutions to the relevant criteria. Second, we evaluate how firms perceive the CN certification versus ISO 14001 in terms of those criteria. We apply AHP by conducting an e-mail survey that was successfully completed by 22 company managers and two managers of public institutions.

The remainder of the paper has the following structure: The following section provides a background of the certifications and the relevant criteria to evaluate them according to the previous literature. Section 3 presents the methodological steps that we followed in our research. Section 4 shows our results and provides some discussion. Finally, Section 5 concludes the paper.

2. Background

In this section, we review the main aspects of the two certifications under study, CN and ISO 14001, and the main criteria identified in the literature regarding firms’ selection of environmental certifications.

The CN Program was introduced in Costa Rica in 2012 as a policy instrument in accordance with the government strategy to have a zero-carbon economy in 2050 [22,26,32]. The program began with the participation of two companies and currently involves around 84 organizations [29]. This program requires participants first to create GHG emissions inventories, and second, to build strategies to cut down, capture or offset those emissions. An auditing agency must verify both the inventories and the veracity of the reduction and offset strategies. All this information is corroborated by the Climate Change Department of the Costa Rican Government, which gives to the companies the “Carbon Neutral Declaration or Certification” [30,31].

ISO 14001 is an international environmental standard for companies that want to implement or improve an EMS. The number of worldwide ISO 14001 certified firms increased by 134% between 2007 and 2017. In the case of Costa Rica, 119 organizations were certified in 2017, showing a 18% growth in 10 years [33]. The aim of ISO 14001 is to help organizations improve their environmental performance in different dimensions. These include creating and putting into operation an EMS, with objectives, policies, and assignment of responsibilities within the firm to comply with them, generating some corrective and preventive actions in order to reduce the polluting emissions of the company and complying with national environmental laws [34].

We conducted a literature review about the criteria related to environmental aspects that companies consider when adopting different VECs and VEPs (not only those under consideration in our study). We grouped these criteria in two blocks: first, those related to environmental sustainability and, second, those associated with economic and strategic aspects.

Regarding environmental sustainability, there are two broad elements that are explicitly or implicitly present in most of the previous studies, namely the reduction in the use of materials and energy [13,14,15,16,18,19,21,35,36,37,38,39] and the reduction in the company′s emissions [13,15,16,18,19,20,21,35,36,37,38,39].

Regarding economic and strategic aspects, the most frequently reported ones include improving the green image of the firm [6,14,40,41,42,43,44,45,46,47,48,49,50], increasing market shares or prices [6,14,42,49,50,51,52,53,54,55,56], saving production costs or increasing productivity [41,42,43,44,45,49,51,55,57,58,59,60], improving the company’s relationship with stakeholders [6,42,51,57,59,61], adapting to mandatory regulations [6,45] and imitating the strategy of competitors [45,51]. In addition, managers also consider the costs related to the certification [12,45,46,48,51,62,63,64,65].

3. Materials and Methods

3.1. In-Depth Face-To-Face Interviews with Firms’ Managers and Scholar Experts

To complement the conclusions obtained in our literature review and get a more detailed vision of firms’ motivations to adopt VECs and VEPs, we conducted several in-depth face-to-face interviews with two groups of experts. Firstly, we interviewed 11 managers in charge of the environmental certification process in some Costa Rican companies (see Appendix A, Table A1). The interviews were not structured, i.e., we allowed for feedback comments during the interviews. This approach provided us some first-hand knowledge about the companies′ reasons to adopt VECs.

Secondly, as a further validation, we also consulted two academic experts of the Faculty of Economic and Business Sciences at the Complutense University of Madrid, namely Gregorio Martín-de-Castro and Javier Amores-Salvadó. The aim of this discussion was to come up with a set of criteria that was representative enough of the relevant criteria, but not extremely large and detailed to make it manageable and easy to be handled by our survey respondents.

3.2. Questionnaire and AHP Application

Table 1 displays the set of criteria that we selected based on the literature review, the interviews to the managers and the academic experts’ advice. We used these criteria to elaborate the questionnaire four our AHP application.

We have a double purpose: first, to evaluate the perception of a group of Costa Rican firms and public institutions with respect to the selected criteria and, second, to measure the propensity of those organizations to adopt a specific environmental certification according to this set of criteria. Among all the available certifications, this study focusses on CN for its relevance for the sake of pursuing sustainability in Costa Rica. As an alternative, we take ISO 14001, which as an important and well-established certification oriented to the EMS of the company.

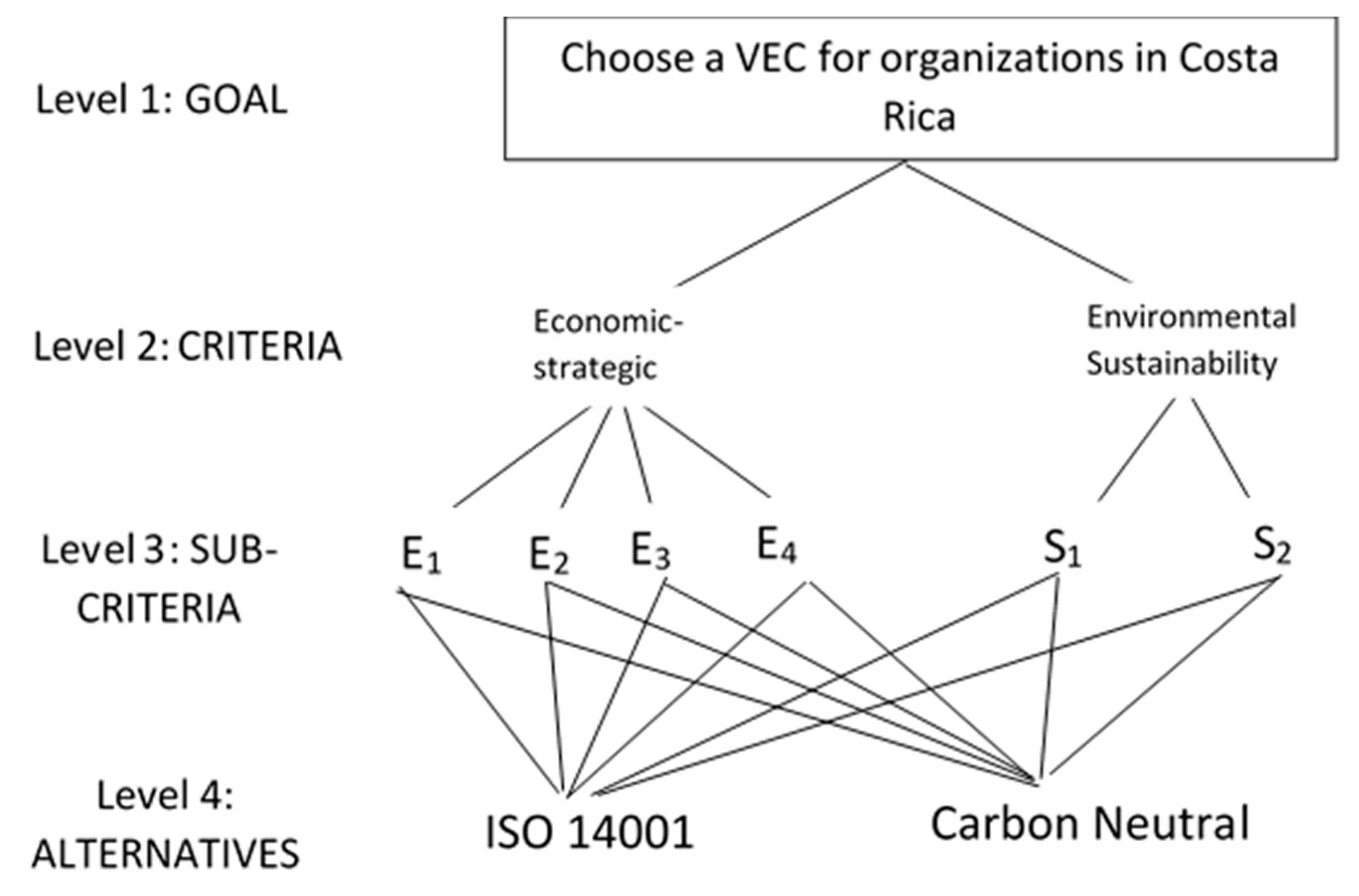

We conducted a four-level-AHP exercise as shown in Figure 1. The first level (“Goal”) is the organization’s objective to choose an environmental certification. The second level refers to the general-purpose criteria (or simply “Criteria”) that we consider relevant for the decision. According to our classification, these are the economic-strategic aspects, on the one hand, and environmental sustainability, on the one hand. The third level (“Sub-criteria”) disaggregates the general-purpose criteria into more specific aspects. We refer to the latter as “sub-criteria” to differentiate them form the aggregate “criteria” on the second level. The lower level (“Alternatives”) refers to the environment certifications that the respondents will evaluate in terms of the criteria and sub-criteria.

To conduct the exercise, we identified a group of companies holding the CN certification, the ISO 14001 certification, or both. For the sake of completeness, we also included some companies that did not hold any of them. Apart from companies, we also addressed some public institutions to check if the latter had somewhat different perceptions and preferences than the former. We identified the CN companies and institutions from the Climate Change Department [29] and the ISO 14001 organizations from the Institute of Technical Standards of Costa Rica [66]. In the case of non-certified companies, we searched the emails’ contacts on their webpages.

In 24 May 2019, we invited 171 companies and 12 certified public institutions to complete the questionnaire on the Google’s survey platform. In the group of companies, 58 of them did not have the CN or ISO 14001 certification, 62 were CN but not ISO 14001 certified, 33 were 14001 but not CN certified and 18 had both certifications. With respect to public institutions, six of them were CN certified, 2 were ISO 14001 certified and four did not have any of both certifications.

In October 2019, 22 companies ‘managers had completed the questionnaire correctly; four of them were CN certified, four ISO 14001 certified, seven had both certifications and seven had neither. In addition, two respondents were from public institutions (a university and a governmental department), both of which were CN but not ISO 14001 certified. Appendix A Table A2 lists the organizations’ features and the positions of the respondents.

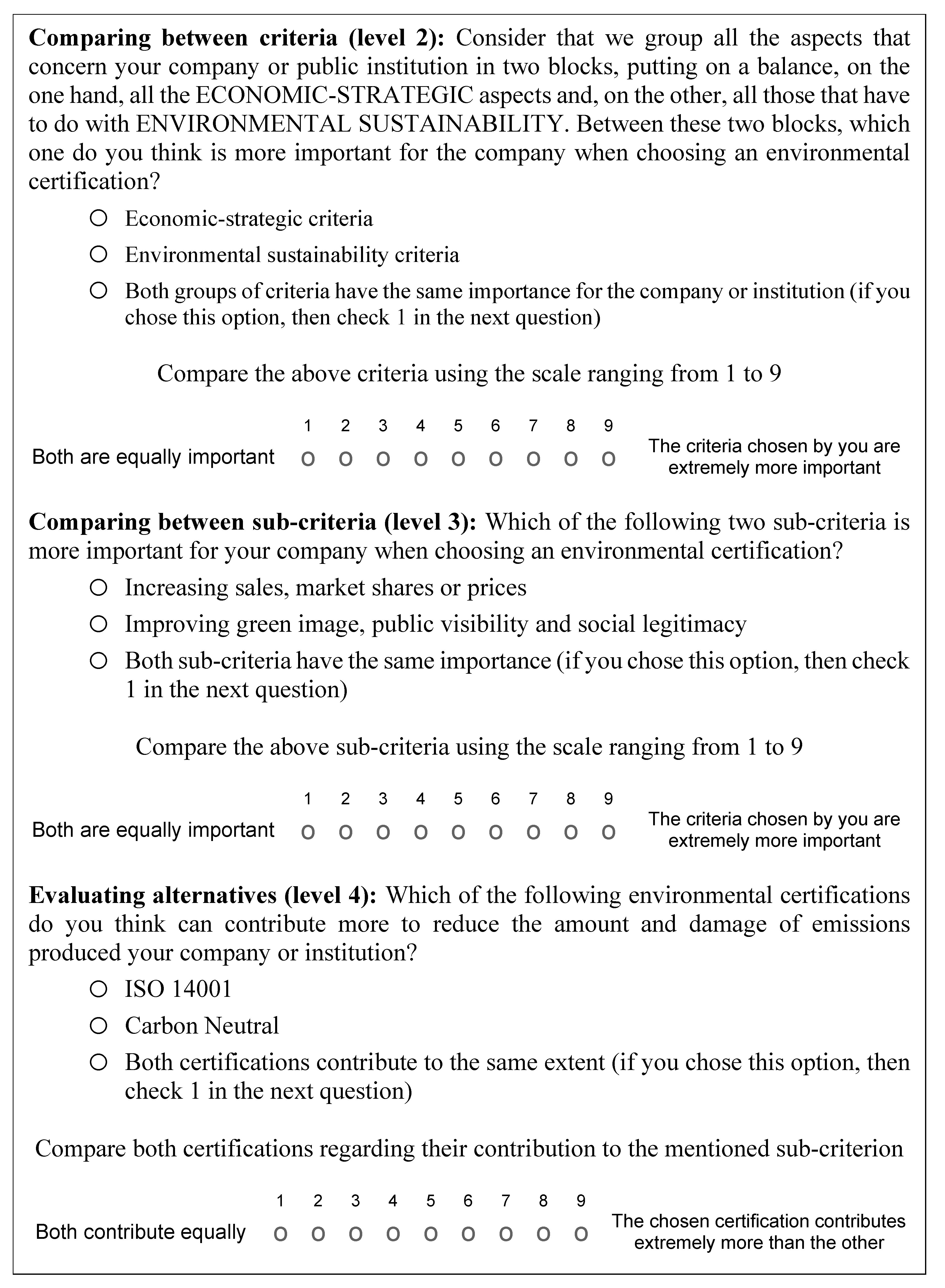

Following standard AHP methodology, the questionnaire sets pairwise comparisons of elements (criteria, sub-criteria, or alternatives) belonging to the same level with respect to their contribution to the immediate superior level. It is based on Satty’s [11,67] scale, which allows us to convert the qualitative judgments into numerical values (see Table 2).

At the beginning of the questionnaire, we explained the structure of the questions and the Saaty scale. Then, we asked the respondents for their pairwise judgments within each level of the study, i.e., about the importance level of criteria (with respect to the goal of selecting a VEC), sub-criteria (with respect to each of the general criteria) and the relative merit of the alternatives, CN and ISO 14001 (with respect to each of the sub-criteria). Figure 2 shows three examples of the questions presented to the managers for levels 2, 3, and 4. The rest of questions had the same structure.

The individual responses give rise to the individual Satty’s comparison matrices. Then, we use the geometric mean to combine the individual matrices and obtain the consensus pairwise comparison matrices [67,68,69]. These combined matrices are the ones that we use to compute the consensus priority weights for each level of the study, first for the whole group of respondents, and then to different subgroups (see Section 4.1 and Section 4.2 below). Before computing the priority weights, we computed the consistency ratios (CR) of each of the relevant consensus comparison matrices. The consistency ratio is defined as , where CI is the consistency index of each matrix and RI is the consistency index of a random matrix of the same size. See Saaty [11,67] for details about the calculation of the consistency indexes (CI) and the average consistency values (RI) of randomly generated matrices. The consistency ratios of all the consensus comparison matrices that we use in the study (for the whole group and the subgroups) are well below 0.10, which is the threshold value recommended by Saaty [11,12,19,67].

We calculated the priority weights for the criteria, sub-criteria and alternatives using a variant of the traditional eigenvector method. For each level, we multiply the associated comparison matrix iteratively by itself. In each iteration, we add up the elements of each row of the matrix and normalize the resulting vector yielding an approximation to the first eigenvector of the initial matrix [70]. The process stops when the approximate eigenvector obtained in one iteration does not change significantly (up to four decimal places) from the previous iteration. The result is taken as the vector of relative importance or priority weights; see e.g., [71,72].

We denote the criteria eigenvector (level 2) as VC. It indicates the weights or relative importance of economic-strategic and environmental sustainability criteria. In level 3, we have two eigenvectors: One for the economic-strategic sub-criteria, denoted as VEC, and one for the environmental sustainability sub-criteria, denoted as VSC. By combining levels 2 and 3 we can obtain the eigenvectors representing the global contributions of each sub-criterion to the goal of the study. Thus, the global eigenvector associated with the economic-strategic sub-criteria (VGEC) is obtained as follows: , where is the weight given to the economic-strategic criterion in level 2, i.e., the first element of VC. Similarly, the global eigenvector of all the sustainability sub-criteria (VGSC) is obtained as follows: , where is the weight given to the environmental sustainability criterion (the second element of VC).

At level 4, we have six two-components eigenvectors, VAi (i = 1, …, 6), each of one indicates the weight or relative score of the alternatives in terms of a given sub-criterion. Specifically, we get four eigenvectors related to the economic-strategic sub-criteria that can be grouped as and 2 eigenvectors related to the environmental sustainability sub-criteria, . We can order the alternatives according only to the economic-strategic criteria by computing or only to the environmental sustainability criteria by computing . Finally, the globally preferred alternative can be determined by computing the global weight vector as follows: .

4. Results and Discussion

4.1. Overall Results

As a first approximation, we take the results arising from the combined answers of all 24 respondents, as shown in Table 3. At level 2, the participants considered, on average, that the economic-strategic criterion is more important (with a relative weight of 0.6) than environmental sustainability (0.4) when adopting a VEC.

Regarding level 3, it is illustrative to compare the different sub-criteria related to economic and strategic aspects among themselves and do the same with the two sub-criteria related to environmental sustainability. Regarding economic-strategic aspects, saving production costs or increasing productivity (sub-criterion E3) and improving green image, public visibility and social legitimacy of the company or the public institution (E1) turn out to be the most important ones. Similar conclusions were found in previous studies about companies’ motivations to adopt environmental certifications in Europe [41,43,44,45,47,58,61], North America [43,48,51], and Latin-America [40,46].

On the environmental side, the respondents consider that sub-criterion S1, related to materials and energy use reductions during the production and distribution processes is slightly more important than S2, which refers to reducing the amount and damage of emissions generated by the company (relative weights 0.52 vs. 0.48). The same or similar motivations were identified in previous studies applied to European [16,21,35,36], Asian [13,14,15,17,18,19,21,38], and American [36,37] companies.

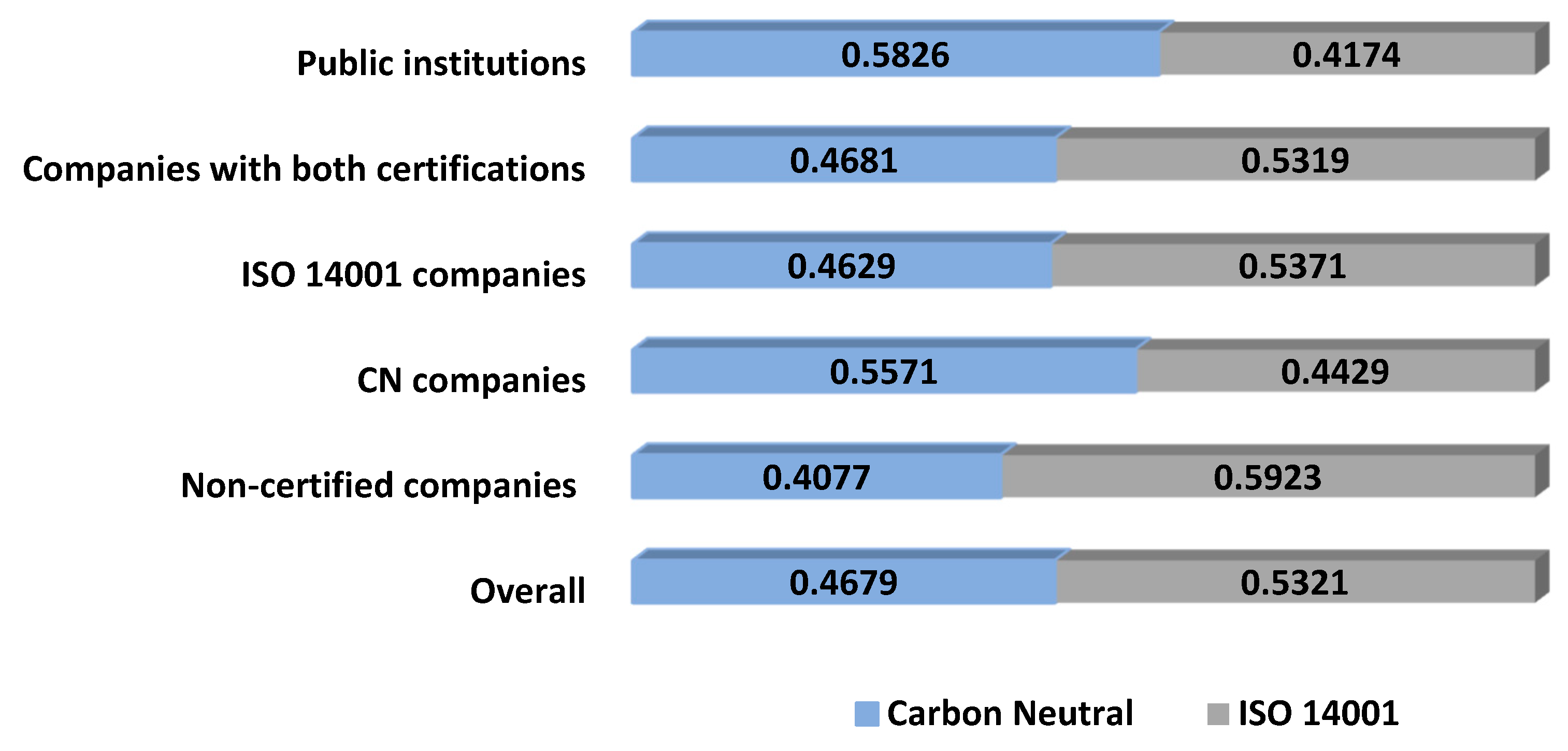

When comparing the alternatives (certifications) according to each sub-criterion at level 4, we observe that CN is preferred under sub-criteria E1, E4, S1 and S2, but ISO 14001 is preferred under E2 and E3. Thus, as is typically the case in any multicriteria decision problem, our decision problem involves some degree of conflict in the sense that by adopting a specific certification, it is unlikely to get the best possible result in all the (sub) criteria at the same time.

In Table 4 we show the results of evaluating the alternatives, first, in terms of the economic-strategic criterion (and, implicitly, the associated sub-criteria), second, in terms of the environmental sustainability criterion (and sub-criteria) and, finally, combining both. It turns out that ISO 14001 is preferred to CN when considering only the economic-strategic criterion (0.53 vs. 0.47). On the contrary, CN is preferred to ISO 14001 in terms of the environmental sustainability aspects (0.62 vs. 0.38). When considering both criteria (and all the corresponding sub-criteria), CN turns out to be preferred to ISO 14001 (0.53 vs. 0.47).

A general reflection about these results has to do with the current relevance of environmental criteria in the organizations’ decision-making process. In our case, considering environmental sustainability makes organizations, in aggregate terms, more prone to adopt CN rather than ISO 14001, although the latter is the preferred option when considering only economic and strategic aspects. This is the case even though the respondents place a larger weight on the economic-strategic criterion. The reason for this is that the respondents perceive CN as clearly preferred to ISO 14001 in environmental terms while the advantage of ISO 14001 over CN in economic-strategic terms is not so pronounced. This conclusion is in line with previous studies in the literature reporting that ethical and environmental concerns beyond purely economic motivations are becoming increasingly relevant in corporate decision-making; see e.g., [42,44,50,58,61,63,73].

4.2. Differences Across Groups

In this section, we split the group of respondents in five mutually exclusive sub-groups to explore how different they are in terms of their perceptions and preferences as regards criteria, sub-criteria, and alternatives. The groups are the following:

- (i)

- Non-certified firms: Companies that are not CN nor ISO 14001 certified (n = 7),

- (ii)

- CN firms: Companies that are CN but not ISO 14001 certified (n = 4),

- (iii)

- ISO 14001 firms: Companies that are ISO 14001 but not CN certified (n = 4),

- (iv)

- Companies that are CN and ISO 14001 certified (n = 7),

- (v)

- Public institutions (n = 2), which include a university and a governmental department. Both are CN but not ISO 14001 certified.

4.2.1. Relative Importance of the Criteria and Sub-Criteria

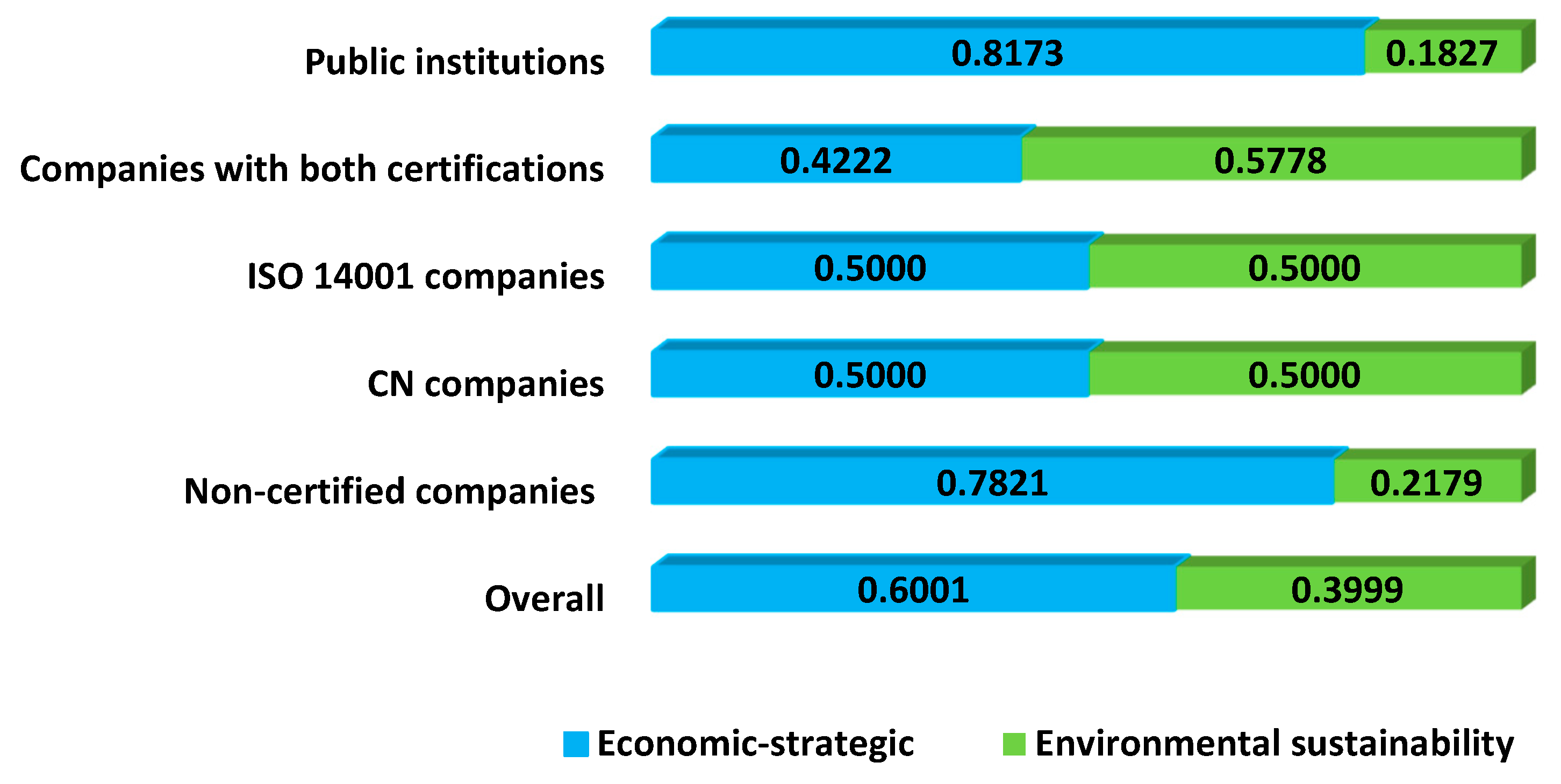

Figure 3 illustrates the average weights given by the different groups to the general criteria (level 2). Notice that there are no differences between the weights given by “CN” and “ISO 14001” firms, both of which declare to consider both criteria equally important.

The only group that gave larger importance to environmental sustainability (0.58) than to the economic-strategic criterion (0.42) is the one of firms that hold both certifications. This contrasts with firms without any of the certifications, which consider the economic-strategic criterion, by far, the most important one. We can interpret this difference as the former group being more concerned with sustainability, which is consistent with their decision to adopt more than one certification. As noted above, it was reported that ethical and environmental concerns are becoming more and more relevant for practical decisions in companies. In our respondents, this feature is particularly visible in the groups of certified companies, while the group of non-certified ones seem to be more concerned about more traditional, economic, and strategic factors. Inevitably, such priorities are institution-specific. Probably, if the answers were from other entities such as the Ministry of Tourism or Environment, the answers would be different, but those institutions were not among our respondents.

It is not so intuitive that the respondents belonging to public institutions constitute the group that give more importance to economic-strategic issues and less to environmental sustainability. One possible explanation for this fact is the existence of important legal and administrative barriers and rigidities in the management process of those institutions. Each of the consulted public entities has a delineated annual budget under which it must meet strategically defined and evaluated objectives [74]. Thus, they may consider environmental sustainability a complement rather than their central target, as they have other defined priorities, which are probably more directly linked to economic and strategic aspects.

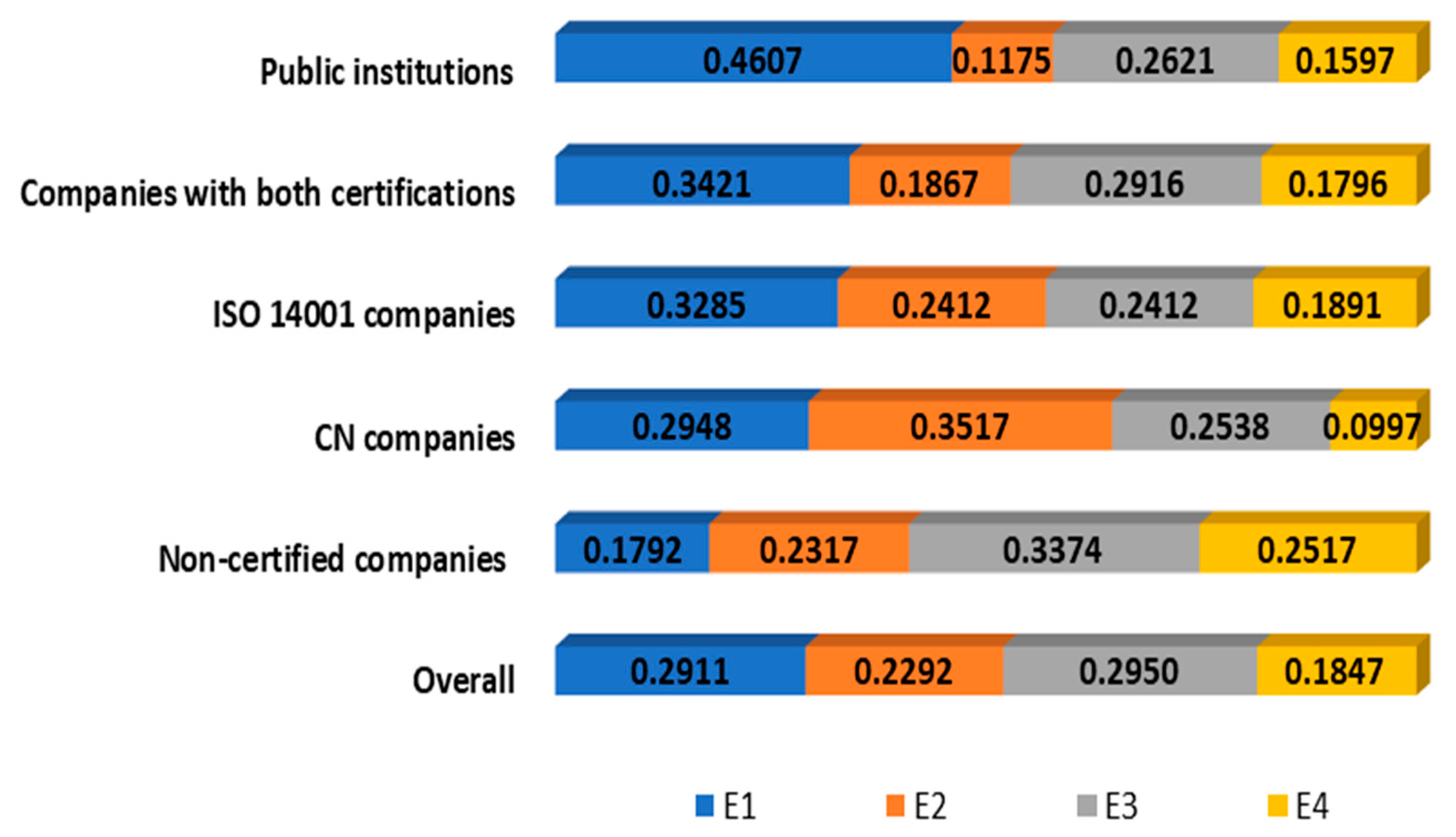

Moving to level 3, Figure 4 shows the weights given by different groups to the economic-strategic sub-criteria. This comparison reveals that “public institutions” is clearly the group that gives larger importance to sub-criterion E1 (improving the green image, public visibility, and social legitimacy of the organization), with nearly half of the total weight within the economic-strategic sub-criteria. It is also the most important one for companies holding the ISO 14001 certification (either alone or jointly with CN), although the difference with other sub-criteria is not so pronounced.

It is also revealing that “non-certified companies” is the group that gives greater importance to sub-criteria E3 (saving production costs or increasing productivity) and E4 (the cost of certification and investment in clean technologies). These results seem consistent with their decision of not adopting any of the alternatives, which we can naturally understand as the result of a traditional and purely economic cost-benefit analysis.

Once again, CN and ISO 14001 companies are not very different regarding their assessment of economic and strategic criteria, although it is noticeable that the CN group seems particularly concerned about “increasing sales, market shares or prices” (E2) and, on the other hand, they attach the smallest importance to the sub-criterion associated with costs (E4).

Regarding the sub-criteria related to environmental sustainability (see Figure 5), those companies holding the CN certification (either alone or together with ISO 14001) are the only ones that give more importance to “reduction in the amount and damage of emissions (gas, solid and water)” (S2) than to saving materials and energy use (S1). This is an expected result, since the CN certification requires the reduction and/or compensation of the GHG footprint of participating organizations [30]. We can argue that CN companies are more concerned about the current environmental threat of climate change [23], which is more directly linked to polluting emissions than to saving materials and energy. It may be surprising to some extent that the same result does not hold for the public institutions, which are also CN certified. The explanation can be like the one given in level 2 regarding the rigidity of institutional targets and budgets.

4.2.2. Choosing a Certification

At level 4, the two proposed certifications are evaluated in terms of the criteria and sub-criteria. Firstly, consider that the decision is made attending only at the economic-strategic criteria and sub-criteria. The results are shown in Figure 6. Consistent with their current behavior, CN companies and institutions consider that CN is preferable to ISO 14001 in economic-strategic terms. The rest of groups consider the opposite, although the differences in this respect are not very large.

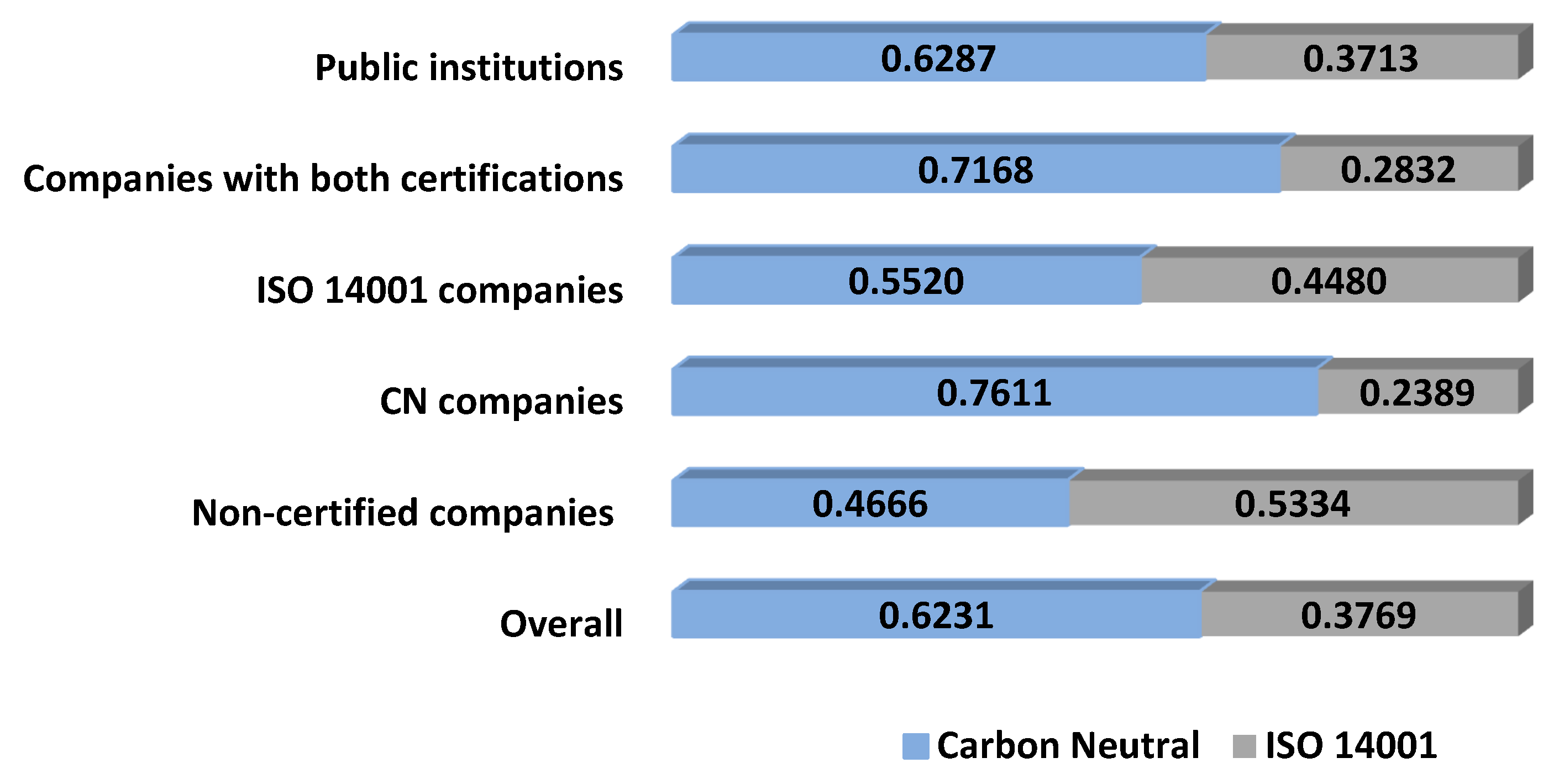

The situation is much clearer when we focus only on environmental sustainability (see Figure 7). All the groups consider that CN is clearly preferable to ISO 14001 except for the group of non-certified firms, which slightly consider the opposite. CN certification receives higher scores by all the sub-groups regarding S2 (amount and damage of emissions), which is consistent with the nature of the CN program as it aims at reducing or offsetting the GHG footprint (see the evaluation of the alternatives according to each sub-criterion on Appendix A Table A3). Other expected associated benefits of this program include generating income to pay environmental services to farm owners who maintain forests or arboreal plantations. In addition to capturing carbon emissions, forests generate other environmental services such as biodiversity protection, watershed protection and scenic beauty [28].

As expected, the relative valuation of the CN certification in environmental terms is particularly notable for those institutions and companies that are CN certified (either alone or together with ISO 14001).

Finally, by using the global weights of all the criteria and sub-criteria, we can determine the most preferred option, as shown in Figure 8. Except for the group of companies without any certification, CN always receives higher global scores than ISO 14001. As expected, CN is particularly well considered among those institutions and companies that already adopted it, which we can interpret as a proof of consistency between their reported preferences and their observed behavior. It is remarkable; anyway that even those companies that adopted only ISO 14001 also attach a marginally higher score to CN than ISO 14001 (roughly, 0.51 vs. 0.49). Although this is not a strong result, the fact that these firms do not give a higher score to the certification that they adopted is already a surprise.

This counterintuitive result merits some explanation. One partial reason is that on average, “ISO 14001” companies considered that CN certification was clearly preferable to ISO 14001 as regards sub-criterion S2, “amount and damage of emissions” (0.74 vs. 0.26), which has a reflection in the final score. Moreover, two of the companies in the ISO 14001 group obtained this certification more than 18 years ago, when climate change and carbon emissions were not considered to be important as they are today, and the CN program did not even exist. Our findings suggest that their certification decision would not be necessarily the same if they had to decide right now for the first time.

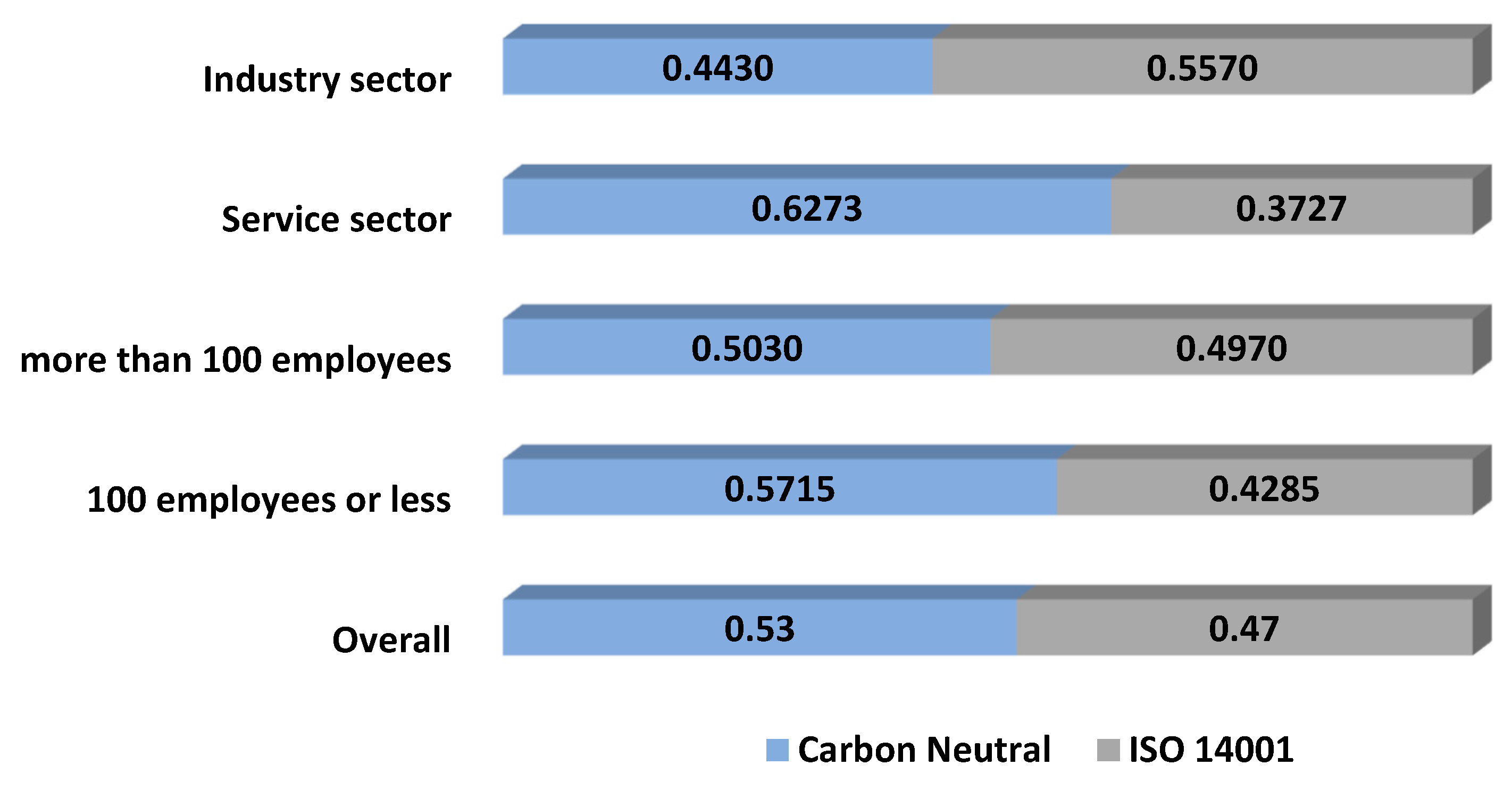

As a future extension of this analysis, it would be interesting to perform a more detailed analysis of how different firms’ characteristics influence their preferences and propensity to adopt each certification. A statistically significant test would require a larger sample and is beyond the scope of this paper but, to have a glimpse, in Appendix A Figure A1 we show a preliminary approach by splitting our group of respondents, in two different ways: By size (large vs. small and medium, where “large” means more than 100 employees) and by sector (industry vs. services). The distinction in terms of size does not seem very relevant in qualitative terms in the sense that both groups of firms (large and small-medium) give a larger aggregate score to CN than ISO 14001 but, in quantitative terms, small and medium firms tend to have a more pronounced preference towards CN, while for larger companies there is almost a tie between both certifications. On the other hand, the activity sector seems to matter in qualitative terms since the service sector (where we included the relevant companies and the two public institutions in our sample) turns out to prefer CN while manufacturing companies give a higher score to ISO 14001 than to CN. Given the limited number of respondents and the possible interactions among different effects, these results should be taken with care, but they provide us with useful hints for future developments.

5. Conclusions

Both environmental sustainability and economic-strategic aspects appear to be important for Costa Rican organizations (firms and public institutions) when adopting an environmental certification. The group of firms and institutions that participated in our AHP study reported that on average, they consider the economic-strategic criterion more important than environmental sustainability. When considering both criteria with their corresponding weights, the CN certification is preferred, on average, to ISO14001. We can consider this result as a reflection of the increasing concern about climate change and the impulse given by the Costa Rican Government to the CN Program.

By splitting the respondents into groups, we find that the environmental sustainability criterion is the most important one only for firms that hold both CN and ISO 14001 certifications, which is consistent with their observed behavior.

In economic and strategic terms, ISO 14001 is considered superior to CN, except by those companies and institutions that are CN (and not ISO 14001) certified. On the other hand, the CN certification received, on average, a much higher score in terms of environmental sustainability by all groups of certified organizations and institutions (CN or ISO 14001). This clear preference under the environmental component makes CN be the preferred almost unanimously across different subgroup of respondents.

One central conclusion is that presently, environmental sustainability is becoming more and more relevant in managers′ decisions. Considering this criterion apart from purely economic and strategic ones can lead them to implement deeper environmental improvements, such as carbon neutrality.

Although AHP is a decision methodology designed to rank alternatives and ultimately choosing among them, it is important to underline that the two certifications that we considered are not mutually exclusive. On the contrary, they could be complementary in improving the environmental performance of organizations.

Author Contributions

Conceptualization, F.J.A. and J.A.V.-S.; Formal analysis, F.J.A. and J.A.V.-S.; Investigation, F.J.A. and J.A.V.-S.; Methodology, F.J.A. and J.A.V.-S.; Supervision, F.J.A.; Writing—original draft, J.A.V.-S.; Writing—review & editing, F.J.A. All authors have read and agreed to the published version of the manuscript.

Funding

Francisco J. André acknowledges support from the Spanish Ministry of Economy, Industry and Competitiveness and Development Fund, ERDF (grant ECO2015-70349-P), the European Commission (project SOE1/P1/F0173), and Complutense University of Madrid and Banco Santander (grant PR26/16-15B-4). J. A. Valenciano acknowledges support from the Scholarship Department of the National University of Costa Rica, (grant JB-C-1106-2016).

Acknowledgments

The authors would like to thank Gregorio Martín-de-Castro and Javier Amores-Salvadó for their valuable contribution in the determination of the relevant criteria. In addition, the authors would like to thank three anonymous referees and all the managers and executives of the companies that participated in the different stages of this research.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Managers interviewed face-to-face in Costa Rica about companies’ reasons to get environmental certifications.

Table A1.

Managers interviewed face-to-face in Costa Rica about companies’ reasons to get environmental certifications.

| Number of Interviewees * | Position | Activity | Environmental Certifications | Interview Day |

|---|---|---|---|---|

| 1 | MM | Industrial | CN, ISO 14001, EBF | 09/09/2016 |

| 2 | MM, EM | Financial | CN, ISO 14001 | 22/09/2016 |

| 2 | CSRC, EM | Car Sales | CN, ISO 14001 | 13/09/2016 |

| 1 | CSRC | Car Sales | CN, ISO 14001 | 16/08/2017 |

| 1 | MM | Industrial | ISO 14001 | 11/08/2017 |

| 1 | MM | Internal Audit | ISO 14001, EBF, OHAS 18000 | 17/08/2017 |

| 1 | MM | Financial | CN, ISO 14001 | 18/08/2017 |

| 1 | GM | Agricultural | Fairtrade, Eco-LOGICA, USDA organic | 22/08/2017 |

| 1 | GM | Travel agency | CST, CN, EBF | 23/08/2017 |

Notes: GM-General Manager, MM—Management Manager, EM—Environmental Manager, CSRC—Corporate Social Responsibility Coordinator, CST—The Costa Rican Certification for Sustainable Tourism; CN-Carbon Neutral, EBF—Ecological Blue Flag. * The name of the interviewees and companies are omitted for the sake of anonymity.

Table A2.

Position of the questionnaire respondents and companies’ features.

| Respondent Position | Activity | Size | Certifications | |

|---|---|---|---|---|

| CN | ISO 14001 | |||

| EM | Construction and building rental | L | Yes | Yes |

| EA | Energy | L | Yes | Yes |

| MM | Information and communication | L | Yes | Yes |

| MM | Pharmaceutical industry | L | Yes | Yes |

| EM | Finance | L | Yes | Yes |

| MM | Industrial | M | Yes | Yes |

| CSRC | Car Sales | L | Yes | Yes |

| MM | Education * | L | Yes | No |

| CSRC | Pension Fund Administration | L | Yes | No |

| Sub MM | Machinery sales | M | Yes | No |

| EM | Food Industry | M | Yes | No |

| HRM | Tourism Agency | M | Yes | No |

| EM | Government Department * | L | Yes | No |

| MM | Technology | L | No | Yes |

| EA | Food Industry | M | No | Yes |

| MMa | Industry | L | No | Yes |

| MM | Industry | M | No | Yes |

| GM | Food Industry | L | No | No |

| MMa | Consulting services | S | No | No |

| N.A. | Manufacture | M | No | No |

| MM | Commercialization | S | No | No |

| MM | Food Industry | M | No | No |

| GM | Food Industry | M | No | No |

| MM | Industry | L | No | No |

Legend. Position: EA—Working into the environmental area, GM—General Manager, HRM—Human Resources Manager, MMa—Market Manager, MM—Management Manager, EM—Environmental Manager, CSRC—Corporate Social Responsibility Coordinator. Size: S-Small (fewer than five employees), M-Medium (between 6 and 100 employees), L-Large (more than 100 employees). * Public Institutions.

Table A3.

Deciding an alternative based on different individual criteria.

| Groups | Overall | Non-Certified Firms | CN Firms | ISO 14001 Firms | Firms with both Certifications | Public Institutions | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sub Criteria | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 | CN | ISO 14001 |

| E1 | 0.5522 | 0.4478 | 0.5397 | 0.4603 | 0.6271 | 0.3729 | 0.5319 | 0.4681 | 0.4442 | 0.5558 | 0.8093 | 0.1907 |

| E2 | 0.3509 | 0.6491 | 0.3290 | 0.6710 | 0.5432 | 0.4568 | 0.4633 | 0.5367 | 0.2643 | 0.7357 | 0.2052 | 0.7948 |

| E3 | 0.4151 | 0.5849 | 0.2901 | 0.7099 | 0.5114 | 0.4886 | 0.3660 | 0.6340 | 0.5895 | 0.4105 | 0.2240 | 0.7760 |

| E4 | 0.5645 | 0.4355 | 0.5439 | 0.4561 | 0.5157 | 0.4843 | 0.4663 | 0.5337 | 0.5285 | 0.4715 | 0.7948 | 0.2052 |

| S1 | 0.5137 | 0.4863 | 0.4091 | 0.5909 | 0.7180 | 0.2820 | 0.3660 | 0.6340 | 0.5832 | 0.4168 | 0.5000 | 0.5000 |

| S2 | 0.7419 | 0.2581 | 0.6392 | 0.3608 | 0.7876 | 0.2124 | 0.7380 | 0.2620 | 0.7893 | 0.2107 | 0.7948 | 0.2052 |

Figure A1.

Deciding an alternative based on environmental sustainability and economic-strategic criteria. According to sector and size of the organizations.

Figure A1.

Deciding an alternative based on environmental sustainability and economic-strategic criteria. According to sector and size of the organizations.

References

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development. 2019. Available online: https://sustainabledevelopment.un.org/post2015/transformingourworld (accessed on 31 December 2019).

- Edenhofer, O. (Ed.) Climate Change 2014: Mitigation of Climate Change; Intergovernmental Panel on Climate; Change Contribution of Working Group III; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014; Available online: http://danida.vnu.edu.vn/cpis/files/IPCC/wg3/pdf/ipcc_wg3_ar5_frontmatter.pdf (accessed on 29 December 2019).

- Marseglia, G.; Medaglia, C.M.; Petrozzi, A.; Nicolini, A.; Cotana, F.; Sormani, F. Experimental tests and modeling on a combined heat and power biomass plant. Energies 2019, 12, 2615. [Google Scholar] [CrossRef] [Green Version]

- Manni, M.; Valentina, C.; Nicolini, A.; Marseglia, G.; Alessandro, P. Towards Zero Energy Stadiums: The Case Study of the Dacia Arena in Udine, Italy. Energies 2018, 11, 2396. [Google Scholar] [CrossRef] [Green Version]

- Shayegh, S.; Sanchez, D.L.; Caldeira, K. Evaluating relative benefits of different types of R&D for clean energy technologies. Energy Policy 2017, 107, 532–538. [Google Scholar] [CrossRef]

- Khanna, M. Non-mandatory approaches to environmental protection. J. Econ. Surv. 2001, 15, 291–324. [Google Scholar] [CrossRef]

- OECD. Voluntary Approaches for Environmental Policy: An Assessment, 1st ed.; Organisation for Economic Cooperation and Development Publishing: Paris, France, 2000. [Google Scholar]

- André, F.J. Strategic Behavior and the Porter Hypothesis. In The WSPC Reference on Natural Resource and Environmental Policy in the Era of Global Change; Dinar, A., Espinola-Arredondo, A., Munoz-Garcia, F., Eds.; World Scientific: Hackensack, NJ, USA, 2016; Volume 1, pp. 231–262. [Google Scholar]

- Ibanez, M.; Blackman, A. Is eco-certification a win–win for developing country agriculture? Organic coffee certification in Colombia. World Dev. 2016, 82, 14–27. [Google Scholar] [CrossRef]

- Porter, M.E.; Van der Linde, C.V.D. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. Available online: www.jstor.org/stable/2138392 (accessed on 11 November 2019). [CrossRef]

- Saaty, T.L. The Analytic Hierarchy Process: Planning Priority Setting and Resource Allocation; McGraw-Hill: New York, NY, USA, 1980. [Google Scholar]

- Chin, K.; Chiu, S.; Tummala, V.M.R. An evaluation of success factors using the AHP to implement ISO 14001-based EMS. Int. J. Qual. Reliab. Manag. 1999, 16, 341–362. [Google Scholar] [CrossRef]

- Pun, K.F.; Hui, I.K. An analytical hierarchy process assessment of the ISO 14001 environmental management system. Integr. Manuf. Syst. 2001, 12, 333–345. [Google Scholar] [CrossRef]

- Mathiyazhagan, M.; Diabat, A.; Al-Refaie, A.; Xu, L. Application of analytical hierarchy process to evaluate pressures to implement green supply chain management. J. Clean. Prod. 2015, 107, 229–236. [Google Scholar] [CrossRef]

- Shen, L.; Muduli, K.; Barve, A. Developing a sustainable development framework in the context of mining industries: AHP approach. Resour. Policy 2015, 46, 15–26. [Google Scholar] [CrossRef]

- Cuadrado, J.; Zubizarreta, M.; Rojí, E.; García, H.; Larrauri, M. Sustainability-related decision making in industrial buildings: An AHP analysis. Math. Probl. Eng. 2015, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Ho, F.H.; Abdul-Rashid, S.H.; Raja Ghazilla, R.A. Analytic hierarchy process-based analysis to determine the barriers to implementing a material efficiency strategy: Electrical and electronics’ companies in the Malaysian context. Sustainability 2016, 8, 1035. [Google Scholar] [CrossRef] [Green Version]

- Thanki, S.; Govindan, K.; Thakkar, J. An investigation on lean-green implementation practices in Indian SMEs using analytical hierarchy process (AHP) approach. J. Clean. Prod. 2016, 135, 284–298. [Google Scholar] [CrossRef]

- Malik, M.M.; Abdallah, S.; Hussain, M. Assessing supplier environmental performance: Applying Analytical Hierarchical Process in the United Arab Emirates health care chain. Renew. Sustain. Energy Rev. 2016, 55, 1313–1321. [Google Scholar] [CrossRef]

- Wang, Q.; Han, R.; Huang, Q.; Hao, J.; Lv, N.; Li, T.; Tang, B. Research on energy conservation and emissions reduction based on AHP-fuzzy synthetic evaluation model: A case study of tobacco enterprises. J. Clean. Prod. 2018, 201, 88–97. [Google Scholar] [CrossRef]

- Karaman, A.S.; Akman, E. Taking-off corporate social responsibility programs: An AHP application in airline industry. J. Air Transp. Manag. 2018, 68, 187–197. [Google Scholar] [CrossRef]

- United Nations Environment Programme. Costa Rica Named ‘UN Champion of the Earth’ for Pioneering Role in Fighting Climate Change. 2019. Available online: https://www.unenvironment.org/news-and-stories/press-release/costa-rica-named-un-champion-earth-pioneering-role-fighting-climate (accessed on 14 November 2019).

- Birkenberg, A.; Birner, R. The world’s first carbon neutral coffee: Lessons on certification and innovation from a pioneer case in Costa Rica. J. Clean. Prod. 2018, 189, 485–501. [Google Scholar] [CrossRef]

- Blackman, A.; Naranjo, M.A.; Robalino, J.; Alpízar, F.; Rivera, J. Does tourism eco-certification pay? Costa Rica’s Blue Flag Program. World Dev. 2014, 58, 41–52. [Google Scholar] [CrossRef]

- Blum, N. Environmental education in Costa Rica: Building a framework for sustainable. Int. J. Educ. Dev. 2008, 28, 348–358. [Google Scholar] [CrossRef] [Green Version]

- Flagg, J.A. Carbon Neutral by 2021: The past and present of Costa Rica’s unusual political tradition. Sustainability 2018, 10, 296. [Google Scholar] [CrossRef] [Green Version]

- Rivera, J. Assessing a voluntary environmental initiative in the developing world: The Costa Rican Certification for Sustainable Tourism. Policy Sci. 2002, 35, 333–360. [Google Scholar] [CrossRef]

- Sánchez-Azofeifa, G.A.; Pfaff, A.; Robalino, J.A.; Boomhower, J.P. Costa Rica’s Payment for Environmental Services Program: Intention, implementation, and impact. Conserv. Biol. 2007, 21, 1165–1173. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ministerio de Ambiente y Energía. Dirección de Cambio Climático [Climate Change Department]. Costa Rica: Ministerio de Amiente y Energía. 2018. Available online: https://cambioclimatico.go.cr/recursos/empresas-ppcn/ (accessed on 14 August 2019).

- Dirección de Cambio Climático. Guía Para Diseñar un Manual que Permita a las PYMES Realizar Declaraciones de Carbono Neutralidad Bajo la Norma INTE 12.01.06. [Guide to Design a Manual that Allows SMEs to Make Carbon Emissions Declarations Under the INTE 12.01.06 Standard]. Costa Rica. 2014. Available online: http://www.digeca.go.cr/sites/default/files/documentos/manualcarbononeutral-web.pdf (accessed on 28 October 2019).

- Musmanni, S. Implementación de la estrategia de Carbono-Neutralidad como modelo de desarrollo bajo en emisiones en Costa Rica [Implementation of the Carbon-Neutrality strategy as a low-emission development model in Costa Rica]. Ambientico 2014, 247, 4–9. Available online: http://www.ambientico.una.ac.cr/pdfs/ambientico/247.pdf (accessed on 12 August 2018).

- Valenciano-Salazar, J.A. Reducción de gases de efecto invernadero: Algunos desafíos para Costa Rica [Greenhouse gas reduction: Some challenges for Costa Rica]. Ambientico 2016, 258, 76–81. Available online: http://www.ambientico.una.ac.cr/pdfs/art/ambientico/258-76-81.pdf (accessed on 2 January 2020).

- International Organization for Standardization. ISO Survey of Certifications to Management System Standards. 2019. Available online: https://isotc.iso.org/livelink/livelink?func=ll&objId=20719433&objAction=browse&viewType=1 (accessed on 2 April 2019).

- International Organization for Standardization. Introduction to ISO 14001:2015. Geneva, Switzerland. 2015. Available online: https://www.iso.org/files/live/sites/isoorg/files/archive/pdf/en/introduction_to_iso_14001.pdf (accessed on 9 August 2019).

- Abdul Rashid, S. An Investigation into the Material Efficiency Practices of UK Manufacturers. Ph.D. Thesis, Cranfield University, Cranfield, UK, October 2009. Available online: http://hdl.handle.net/1826/4477 (accessed on 28 October 2019).

- Verschoor, A.H.; Reijnders, L. Toxics reduction in ten large companies, why and how. J. Clean. Prod. 2000, 8, 69–78. [Google Scholar] [CrossRef]

- Doczy, R.; AbdelRazig, Y. Green buildings case study analysis using AHP and MAUT. J. Arch. Eng. 2017, 23. [Google Scholar] [CrossRef]

- Eltayeb, T.K.; Zailani, S.; Ramayah, T. Green supply chain initiatives among certified companies in Malaysia and environmental sustainability: Investigating the outcomes. Resour. Conserv. Recycl. 2011, 55, 495–506. [Google Scholar] [CrossRef]

- Govindan, K.; Rajendran, S.; Sarkis, J.; Murugesan, P. Multi criteria decision making approaches for green supplier evaluation and selection: A literature review. J. Clean. Prod. 2015, 98, 66–83. [Google Scholar] [CrossRef]

- Faggi, A.M.; Zuleta, G.A.; Homberg, M. Motivations for implementing voluntary environmental actions in Argentine forest companies. Land Use Policy 2014, 41, 541–549. [Google Scholar] [CrossRef]

- Hillary, R. Environmental management systems and the smaller enterprise. J. Clean. Prod. 2004, 12, 561–569. [Google Scholar] [CrossRef]

- Mariotti, F.; Kadasah, N.; Abdulghaffar, N. Motivations and barriers affecting the implementation of ISO 14001 in Saudi Arabia: An empirical investigation. Total Qual. Manag. Bus. Excell. 2014, 25, 1352–1364. [Google Scholar] [CrossRef]

- Morrow, D.; Rondinelli, D. Adopting corporate environmental management systems: Motivations and results of ISO 14001 and EMAS certification. Eur. Manag. J. 2002, 20, 159–171. [Google Scholar] [CrossRef]

- Okereke, C. An exploration of motivations, drivers and barriers to carbon management: The UK FTSE 100. Eur. Manag. J. 2007, 25, 475–486. [Google Scholar] [CrossRef]

- Ormazabal, M.; Sarriegi, J.M. Environmental management evolution: Empirical evidence from Spain and Italy. Bus. Strateg. Environ. 2014, 23, 73–88. [Google Scholar] [CrossRef]

- Pérez-Ramírez, M.; Phillips, B.; Lluch-Belda, D.; Lluch-Cota, S. Perspectives for implementing fisheries certification in developing countries. Mar. Policy 2012, 36, 297–302. [Google Scholar] [CrossRef] [Green Version]

- Schylander, E.; Martinuzzi, A. ISO 14001–experiences, effects and future challenges: A national study in Austria. Bus. Strateg. Environ. 2007, 16, 133–147. [Google Scholar] [CrossRef]

- Yiridoe, E.K.; Clark, J.S.; Marett, G.E.; Gordon, R.; Duinker, P. ISO 14001 EMS standard registration decisions among Canadian organizations. Agribusiness 2003, 19, 439–457. [Google Scholar] [CrossRef]

- Zeng, S.X.; Tam, C.M.; Tam, V.; Deng, Z.M. Towards implementation of ISO 14001 environmental management systems in selected industries in China. J. Clean. Prod. 2005, 13, 645–656. [Google Scholar] [CrossRef]

- Zeppel, H.; Beaumont, N. Assessing motivations for carbon offsetting by environmentally certified tourism enterprises. Anatolia 2013, 24, 297–318. [Google Scholar] [CrossRef]

- Bansal, P.; Bogner, W.C. Deciding on ISO 14001: Economics, institutions, and context. Long Range Plan. 2002, 35, 269–290. [Google Scholar] [CrossRef]

- Barham, B.L.; Callenes, M.; Gitter, J.; Lewis, J.; Weber, J. Fair Trade/Organic coffee, rural livelihoods, and the “agrarian question”: Southern Mexican coffee families in transition. World Dev. 2011, 39, 134–145. [Google Scholar] [CrossRef]

- Lyngbæk, A.E.; Muschler, R.G.; Sinclair, F.L. Productivity and profitability of multistrata organic versus conventional coffee farms in Costa Rica. Agrofor. Syst. 2001, 53, 205–213. [Google Scholar] [CrossRef]

- Méndez, V.E.; Bacon, C.M.; Olson, M.; Petchers, S.; Herrador, D.; Carranza, C.; Trujillo, L.; Guadarrama-Zugasti, C.; Cordón, A.; Mendoza, A. Effects of Fair Trade and organic certifications on small-scale coffee farmer households in Central America and Mexico. Renew. Agric. Food Syst. 2010, 25, 236–251. [Google Scholar] [CrossRef] [Green Version]

- Pan, J.-N. A comparative study on motivation for and experience with ISO 9000 and ISO 14000 certification among Far Eastern countries. Ind. Manag. Data Syst. 2003, 103, 564–578. [Google Scholar] [CrossRef] [Green Version]

- Weber, J.G. How much more do growers receive for Fair Trade-organic coffee? Food Policy 2011, 36, 678–685. [Google Scholar] [CrossRef]

- Fryxell, G.E.; Szeto, A. The influence of motivations for seeking ISO 14001 certification: An empirical study of ISO 14001 certified facilities in Hong Kong. J. Environ. Manag. 2002, 65, 223–238. [Google Scholar] [CrossRef] [Green Version]

- González-Benito, J.; Gonzáles-Benito, O. An analysis of the relationship between environmental motivations and ISO14001 certification. Br. J. Manag. 2005, 16, 133–148. [Google Scholar] [CrossRef]

- Lim, S.; Prakash, A. Voluntary regulations and innovation: The case of ISO 14001. Public Adm. Rev. 2014, 74, 233–244. [Google Scholar] [CrossRef]

- Quazi, H.A.; Khoo, Y.K.; Tan, C.M.; Wong, P.S. Motivation for ISO 14000 certification: Development of a predictive model. Omega 2001, 29, 525–542. [Google Scholar] [CrossRef]

- Poksinska, B.; Dahlgaard, J.J.; Eklund, J.A.E. Implementing ISO 14000 in Sweden: Motives, benefits and comparisons with ISO 9000. Int. J. Qual. Reliab. Manag. 2003, 20, 585–606. [Google Scholar] [CrossRef]

- Babakri, K.; Bennett, R.; Franchetti, M. Critical factors for implementing ISO 14001 standard in United States industrial companies. J. Clean. Prod. 2003, 11, 749–752. [Google Scholar] [CrossRef]

- Santos, G.; Rebelo, M.; Lopes, N.; Alves, M.R.; Silva, R. Implementing and certifying ISO 14001 in Portugal: Motives, difficulties and benefits after ISO 9001 certification. Total Qual. Manag. Bus. Excell. 2016, 27, 1211–1223. [Google Scholar] [CrossRef]

- Snider, A.; Gutiérrez, I.; Sibelet, N.; Faure, G. Small farmer cooperatives and voluntary coffee certifications:Rewarding progressive farmers of engendering widespread change in Costa Rica. Food Policy 2017, 69, 231–242. [Google Scholar] [CrossRef]

- Tellman, B.; Gray, L.C.; Bacon, C.M. Not fair enough: Historic and institutional barriers to Fair Trade coffee in El Salvador. J. Lat. Am. Geogr. 2011, 10, 107–127. [Google Scholar] [CrossRef]

- INTECO. Instituto de Normas Técnicas de Costa Rica [Institute of Technical Standards of Costa Rica]. 2019. Available online: https://www.inteco.org/ (accessed on 11 October 2019).

- Saaty, T. Decision Making for Leaders: The Analytical Hierarchy Process for Decisions in a Complex World, 3rd ed.; RWS Publications: Pittsburg, PA, USA, 2012. [Google Scholar]

- Aczél, J.; Alsina, C. On synthesis of judgements. Socio Econ. Plan. Sci. 1986, 20, 333–339. [Google Scholar] [CrossRef]

- Xu, Z. On consistency of the weighted geometric mean complex judgement matrix in AHP. Eur. J. Oper. Res. 2000, 126, 683–687. [Google Scholar] [CrossRef]

- Perron, O. Zur Theorie der Matrices. Math. Ann. 1907, 64, 248–263. [Google Scholar] [CrossRef]

- Aznar Bellver, J.; Caballer Mellado, V. An application of the analytic hierarchy process method in farmland appraisal. Span. J. Agric. Res. 2005, 3, 17–24. Available online: http://revistas.inia.es/index.php/sjar/article/view/120/117 (accessed on 14 November 2019). [CrossRef]

- Vázquez-Burgos, J.L.; Carbajal-Hernández, J.J.; Sánchez-Fernández, L.P.; Moreno-Armendáriz, M.A.; Tello-Ballinas, J.A.; Hernández-Bautista, I. An Analytical Hierarchy Process to manage water quality in white fish (Chirostoma estor estor) intensive culture. Comput. Electron. Agric. 2019, 167, 105071. [Google Scholar] [CrossRef]

- Cater, J.; Collins, L.A.; Beal, B.D. Ethics, faith, and profit: Exploring the motives of the U.S. Fair Trade social entrepreneurs. J. Bus. Ethics 2017, 146, 185–201. [Google Scholar] [CrossRef]

- Muñoz, A. El Presupuesto Nacional en Costa Rica [The National Budget in Costa Rica]. Ministerio de Hacienda de Costa Rica, Cooperación Alemana, FOCEVAL. Available online: https://www.hacienda.go.cr/docs/5228c0e0637a1_Folleto_Presupuesto_Nacional.pdf (accessed on 11 December 2019).

Figure 1.

Analytic hierarchy structure of the study.

Figure 2.

Three examples of questions used in the questionnaire to compare criteria (level 2), sub-criteria (level 3) and alternatives (level 4).

Figure 2.

Three examples of questions used in the questionnaire to compare criteria (level 2), sub-criteria (level 3) and alternatives (level 4).

Figure 3.

Weights’ vector of criteria by respondents’ subgroup.

Figure 4.

Weights’ vector of economic-strategic criteria by respondents’ subgroup. Note. For public institutions, we present sub-criterion E2 as “the possible improvements in the quality of the services offered and the increase in user satisfaction”.

Figure 4.

Weights’ vector of economic-strategic criteria by respondents’ subgroup. Note. For public institutions, we present sub-criterion E2 as “the possible improvements in the quality of the services offered and the increase in user satisfaction”.

Figure 5.

Weights’ vector of environmental sustainability criteria by respondents’ subgroup.

Figure 6.

Deciding an alternative based on the economic-strategic criterion.

Figure 7.

Deciding an alternative based on environmental sustainability criteria.

Figure 8.

Deciding an alternative based on environmental sustainability and economic-strategic criteria.

Figure 8.

Deciding an alternative based on environmental sustainability and economic-strategic criteria.

Table 1.

Criteria included in the AHP questionnaire.

| Economic-Strategic (E) | Environmental Sustainability (S) |

|---|---|

| Improving green image, public visibility and social legitimacy of the company (E1). Increasing sales, market shares or prices (E2) * Saving production costs or increasing productivity (E3). Cost of the certification and investment in clean technologies (E4). | Materials and energy use reductions during the production and distribution (S1). Reduction in the amount and damage of emissions (gas, solid and water) generated by the company (S2). |

| Note: * Since public institutions do not have a profit motive, we reformulate sub-criterion E2 for them as “the possible improvements in the quality of the services offered and the increase in user satisfaction.” | |

Table 2.

Saaty’s scale of preference between two elements.

| Numerical Values | Definition | Explanation |

|---|---|---|

| 1 | Equal | Two elements contribute equally to the objective |

| 3 | Moderate | Experience and judgment slightly favor one aspect over another |

| 5 | Strongly | Experience and judgment strongly or essentially favor one aspect over another |

| 7 | Very strongly | An aspect is strongly favored over another and its dominance demonstrated in practice |

| 9 | Extremely | The evidence favoring one aspect over another is of the highest degree possible for affirmation |

| 2, 4, 6, 8 | Intermediate values | Used to represent a compromise between preferences listed above |

Source: Saaty [11].

Table 3.

Priority weights by level (criteria, sub-criteria, and alternatives). All respondents (n = 24).

Table 3.

Priority weights by level (criteria, sub-criteria, and alternatives). All respondents (n = 24).

| Criteria | Vc | Sub-Criteria | VEC and VSC | VGEC and VGSC | Comparing Alternatives (VAi) | |

|---|---|---|---|---|---|---|

| ISO 14001 | CN | |||||

| Economics-strategic (Ei) | we 0.6001 | E1 | 0.2911 | 0.1747 | 0.4478 | 0.5522 |

| E2 | 0.2292 | 0.1376 | 0.6491 | 0.3501 | ||

| E3 | 0.2950 | 0.1770 | 0.5849 | 0.4151 | ||

| E4 | 0.1847 | 0.1108 | 0.4355 | 0.5645 | ||

| Environmental sustainability (Si) | ws 0.3999 | S1 | 0.5207 | 0.2082 | 0.4863 | 0.5137 |

| S2 | 0.4793 | 0.1917 | 0.2581 | 0.7419 | ||

Note: The question regarding the comparison of alternatives in terms of sub-criterion E4 was answered by 23 respondents.

Table 4.

Choosing an alternative according to the criteria. All respondents (n = 24).

| Alternatives | According to Each Criterion | According to Global Weights | |||

|---|---|---|---|---|---|

| WAE | WAS | VGEC × VAE | VGSC × VAS | WGA | |

| CN | 0.4679 | 0.6231 | 0.2808 | 0.2492 | 0.5300 |

| ISO 14001 | 0.5321 | 0.3769 | 0.3193 | 0.1507 | 0.4700 |

| Total | 1 | 1 | 0.6001 | 0.3999 | 1 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

André, F.J.; Valenciano-Salazar, J.A. Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach. Sustainability 2020, 12, 737. https://0-doi-org.brum.beds.ac.uk/10.3390/su12020737

AMA Style

André FJ, Valenciano-Salazar JA. Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach. Sustainability. 2020; 12(2):737. https://0-doi-org.brum.beds.ac.uk/10.3390/su12020737

Chicago/Turabian StyleAndré, Francisco J., and Jorge A. Valenciano-Salazar. 2020. "Becoming Carbon Neutral in Costa Rica to Be More Sustainable: An AHP Approach" Sustainability 12, no. 2: 737. https://0-doi-org.brum.beds.ac.uk/10.3390/su12020737

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.