Higher Academic Qualifications, Professional Training and Operating Performance of Audit Firms

1

Department of Accounting, National Yunlin University of Science and Technology, Yunlin 64002, Taiwan

2

Department of Accounting and Information Systems, Chang Jung Christian University, Tainan 71101, Taiwan

*

Author to whom correspondence should be addressed.

Sustainability 2020, 12(3), 1254; https://0-doi-org.brum.beds.ac.uk/10.3390/su12031254

Submission received: 10 January 2020

/

Revised: 6 February 2020

/

Accepted: 7 February 2020

/

Published: 10 February 2020

Abstract

:This study examines the association between professional training, higher academic qualifications (educational levels) and operating performance of audit firms in Taiwan. We particularly focus on the curvilinear effects of higher academic qualifications on operating performance. We group the total sample into three categories: national, regional and local audit firms. Based on the theoretical framework in industrial economics, we establish a cross-sectional multiple regression equation to test our hypotheses. Both higher academic qualifications and professional training are positively related to the operating performance of audit firms. Professional training moderates the relation between higher academic qualifications and operating performance. Higher academic qualifications exhibit a curvilinear effect on operating performance with a reverse U-shaped relation for the national audit firms and a U-shaped relation for both regional and local audit firms. Due to data unavailability, some factors affecting the audit quality and operating performance are not included in our analysis, such as auditor teamwork, internal control system, operating policies and auditing procedures of audit firms. The findings that higher academic qualifications are positively associated with the operating performance of audit firms justify the educational policy of establishing institutes or graduate schools in accounting over the past two decades. Furthermore, audit firms skillfully exploit employees with higher academic qualifications to improve their operating performance. We are the first to document the moderating effects of professional training and the curvilinear association between higher academic qualifications and operating performance, contributing knowledge to related literature.

1. Introduction

Education of higher degree talents is relevant to a nation’s power and materially affects the political, economic, and cultural development of a country. Recently, the global village has tended to intensify drastic cross-border competition in business, trade, and politics, thus justifying the significance of higher academic qualifications/educational levels and attracting the attention of the government in highly developed countries on this issue. For example, the United Kingdom issued a white paper in 1987 to enhance the implementation of higher education. Its 1988 Education Reform Act transformed the polytechnics and other higher education colleges into independent institutions. The 1992 Further and Higher Education Act approved the reorganization of many polytechnics as universities. The United Kingdom conducted a major reorganization and convergence in the pattern of higher education institutions [1,2,3].

Similar development occurred in Taiwan and many other countries. Beginning in the 21st century, Taiwanese Ministry of Education has loosened the higher education policy, resulting in the reorganization of many junior colleges as an academy or technology university. The sharp increases in the number of university lead to substantial growth in the number of graduates with higher educational levels. Taking the higher education of accounting as an example, to date, 37 universities establish departments of accounting to grant bachelor’s degree. Among which, 26 universities set institute or graduate school in accounting to deliver master or doctoral degree. Under the landscape of educational policy, Taiwanese audit firms recruit more auditors with higher educational levels. The Taiwanese Financial Supervisory Commission indicates that the ratio of auditors with bachelor’s degrees rose from 49.3% in 1992 to 66.8% in 2015. The ratio of auditors with master’s degree or above was 7.6% in 1992 and climbed to 20.4% in 2015. The growth rates of auditors with bachelor’s degree are 35.5% but that of auditors with master’s degree or above are as high as 168.4%.

Audit firms are a professional organization and an expertise and human capital-intensive industry. To fulfil their auditing jobs, auditors are required to have academic educational levels, professional training and work experience [4]. Auditors typically include assistants and practicing certified public accountants (CPAs), the owners of an audit firm. When more and more universities grant master’s degrees or above, the following question is raised: Do auditors with higher academic qualifications matter in the industry? This question is a critical and influential one raised by academics, practitioners, and regulators. To the best of our knowledge, few studies focused on the effects of higher academic qualifications of auditors. This situation motivates us to investigate the usefulness of higher academic qualifications in the Taiwanese auditing industry, the first purpose of this study.

Human resource management researches note that training is a process that enables employees to obtain and develop expertise, skills and attitudes to enhance work performance and maintain organizational competitiveness [5,6]. Training sets out from the operational needs of a company to advance the professional capabilities of employees, such as knowledge, skill, and behavior [7]. To promote audit quality, the Taiwanese Certified Public Accountant Act requires the continuing professional training for auditors. Regulations governing pre-professional training and continuing professional education are enacted as well. These regulations on the professional training of auditors are similar around the world. A total-training-hour requirement is applied in the United States, the United Kingdom, Canada, Australia, New Zealand, Singapore, France, and Taiwan.

Knowledge of a professional organization is mostly found in human capital which is fostered by the experience and skills obtained from academic education and training [8,9]. Human capital is a key factor in gaining competitive advantage and a critical element in determining operating results. Examining the relation between professional training and operating performance of audit firms is our second purpose.

Auditors gain knowledge through formal academic education, which is an articulable knowledge. Audit firms cultivate employees’ expertise, skills, and behaviors through professional training. Academic educational level is an indicator of employees’ theoretical knowledge. Professional training puts theoretical knowledge into practice and combines theory and practice together. Therefore, professional training fills the gap left by academic education. As the third purpose of this study, we further examine the moderating effects of professional training on higher academic qualifications of auditors.

Prior researches employ a linear relationship to examine the association between human capital and operating performance of audit firms [10,11,12]. When more auditors with a master’s degree or above are hired, audit firms assume higher human capital cost, thus resulting in lower operating profits. Human capital cost accounts for the majority of operating cost of an audit firm. A trade-off exists between the higher human capital from auditors with a higher education level and the higher operating cost. Instead of a linear relation, this study claims that the association between higher academic qualifications and operating performance is curvilinear. Few studies addressed the curvilinear relationship in the professional organization. To fill the knowledge gap, we finally purport to examine the curvilinear effects of higher academic qualifications on operating performance of audit firms.

To investigate the relation between professional training, higher academic qualifications, and operating performance of audit firms, we take empirical data from the 1992–2015 Survey Report of Audit Firms in Taiwan. In terms of the market segmentation and based on previous studies [13,14,15,16], this study categorizes audit firms into three groups, national, regional, and local ones. Empirical results are as follows. First, both higher academic qualifications and professional training positively associate with the operating performance of audit firms. Second, professional training positively moderates the relation between higher academic qualifications and operating performance. Third, higher academic qualifications exhibit a curvilinear effect on operating performance of audit firms. Specifically, national firms present a reverse U-shaped relation, and regional and local firms a U-shaped relation. To the best of knowledge, this study is the first using master’s degree or above as the measurement of higher academic qualifications to investigate its effects on operating performance. With the results, this study contributes to and fills the gap in the related literature. Firstly, our finding that professional training positively moderates the relation between higher academic qualifications and operating performance not only enriches human resource management knowledge but also justifies the worldwide requirement of auditors’ professional training. Moreover, we are the first to address and corroborate the curvilinear association between higher academic qualifications and operating performance of a professional organization. The findings demonstrate different shapes of the curvilinear relation for audit firms in different market segments. For the auditing industry, academic qualifications and professional training of auditors are operationally similar around the world. Specifically, international large audit firms, the Big 4, establish uniform training programs and SOPs for their member firms worldwide. Small audit firms have similar internal and external training curriculums [14]. Accordingly, the managerial implications of our findings apply to the practitioners in auditing industries in the world.

2. Hypotheses Development

2.1. Higher Academic Qualifications

Auditors worldwide are required to meet a minimum academic qualification to adapt to the changing business environment. For example, the American Institute of Certified Public Accountants (AICPA) set up a membership requirement in 1988, the 150-h rule, which states that all new members of AICPA must have completed 150 semester hours of college education. Similar requirements are stated in the Taiwanese CPA examination rule. To take the examination, examinees are required to have a bachelor’s degree in accounting or business and to complete at least 20 credits of courses in accounting and auditing. Assistants are required to have an associate bachelor’s degree or above and to complete at least 10 credits of courses in accounting, auditing, tax, and computer science.

Professionals gain explicit (articulable) knowledge through formal academic education and tacit knowledge through professional training and work experience. To render services, professionals are usually required to have extensive academic education, which provides a high level of explicit knowledge in the field of specialty. However, to the extent, the quality of the academic education varies [17]. Students from top universities or those with higher academic degree, such as a master’s or PhD, are perceived to have great explicit knowledge. Noticeable external institutions rank or appraise students by their universities and degrees. Those who received education from top universities or obtained a higher academic degree are assumed to have great knowledge and high intellectual potential to learn and accumulate tacit knowledge, such as skills and expertise.

Human resource of a typical audit firm is embodied in the auditors’ expertise and experience. Auditors with high technical competencies have increased ability to detect errors and provide great assurance to readers that financial statements do not contain material errors, an indicator of quality services [18,19,20]. They differentiate themselves from others not only in retaining existing clients but also in attracting new ones. By summarizing an AICPA task force report on the quality of government unit audits, prior studies find that academic education of auditors is an important factor affecting the audit quality [21]. Based on the effects of the 150-h rule, prior researches report a positive association between higher education level of auditors and the audit quality [22]. Therefore, skilful auditors render high-quality services to clients, thus resulting in a good reputation and improved operating performance [16].

Based on human resource management theory, auditors with a master’s degree or above are assumed to have extensive knowledge of accounting, auditing, management, and information system, and thus superior integration, analysis and judgment competencies. Accordingly, this study expects a higher contribution to the operating performance of audit firms from higher education level auditors and forms the following hypothesis.

Hypothesis 1.

A positive association exists between higher academic qualifications and operating performance of audit firms.

2.2. Professional Training

In theory, an organization invests in employees’ professional training to increase their efficiency and performance, thus improving the productivity of the organization [23,24]. Professional training and academic education are critical ingredients in the formation of human capital. Human capital and physical capital are substitutable, and their productivity and capacity improve through investment [25]. Specifically, productivity of human capital can be elevated through academic education and professional training, and that of physical capital can be enhanced through plant expansion and addition of new equipment. According to the resource-based view of firms, resources that are valuable, unique and difficult to imitate can provide a basis for firms’ competitive advantage [26,27,28]. As a professional organization, audit firms utilize human capital as an important input factor to gain competitive advantage and as a critical element to improve operating performance. Therefore, auditors are required to be equipped with professional training, work experience, and academic education in accounting and auditing [4].

Professional training plays an important role in upgrading audit quality. The UK Financial Reporting Council [29] indicates that professional training given to audit personnel drives audit quality. Article 13 of the Taiwanese Certified Public Accountant Act stipulates that practicing CPAs who serve public (private) companies are required to obtain 100 (50) professional training hours in every three-year period and a minimum of 24 (12) hours in each year. Assistants are also required to obtain a minimum requirement of professional training hours each year. Auditors’ professional training is a worldwide compulsory requirement in such countries as United States, United Kingdom, Canada, France, New Zealand, and Australia. For example, in some US states, auditors are required to obtain 120 professional training hours in every three-year period and a minimum of 20 h in each year [30].

Previous research states that professional training is positively associated with human resource outcomes and organizational performance. However, the findings of relation between professional training and financial results are mixed and far from conclusive [31,32].

In the line of research on continuing professional education in audit firms, a low level of technical professional training is associated with a deficient practice [33] and substandard professional performance related to competency [34]. A high level of professional training is associated with increased knowledge, a necessary component of competence demand [35] and improved service quality [36,37,38]. When auditors receive more formal instructions through either academic education or professional training courses, they have better audit performance than those who do not [39]. Further, the association between the internal and external professional trainings of assistants and the financial performance of proprietorship audit firms is positive [14]. Technical efficiencies are improved in audit firms with high expenditures in professional training [40]. Audit firms providing professional training are superior in financial performance to those with no professional training [12].

On the basis of accounting research, we expect a positive relation between professional training and operating performance. We establish the following hypothesis to substantiate the findings in the accounting literature:

Hypothesis 2.

A positive association exists between professional training and operating performance of audit firms.

2.3. Moderating Effects of Professional Training

Professional training is a supporting system that enhances human capital, especially firm-specific human capital. When training leads to improvement in job performance, organizational outcomes or results, such as productivity or profitability, are enhanced. Therefore, professional training can be considered a critical element in the first phase of attaining competitive advantage for an organization.

After completing advanced education, professionals begin their careers as assistant staffs and continue to learn to gain significant tacit knowledge or work experience [41]. By entering audit firms, auditors gain practical knowledge through pre-professional training and continuing professional training. Professional training promotes the learning effects of auditors and expedites their accumulation of expertise and skills. Continuing professional training of auditors is an important area affecting audit quality [21]. The UK Financial Reporting Council [29] identifies professional training as a driver of audit quality.

In sum, as professional training improves the manpower of audit firms and strengthens audit quality, their operating performance is improved. This study expects that professional training improves the relation between higher academic qualifications and operating performance and hypothesises:

Hypothesis 3.

Professional training positively moderates the association between higher academic qualifications of auditors and operating performance of audit firms.

2.4. Curvilinear Effects of Academic Qualifications

Audit firms hiring employees with higher education levels and much experience saliently improves operating performance [42,43]. Previous studies report a linear relationship between education levels of auditors and operating performance of audit firms [12,14,40]. However, employing auditors with higher academic qualifications increases the operating cost of audit firms. In Taiwanese auditing industry, auditors with a master’s degree or above are compensated higher salaries than those without.

When more auditors with a master’s degree or above are hired, audit firms assume higher human capital cost and result in lower operating profits. A trade-off exists between the higher human capital and the higher operating cost. Initial investments in higher human capital may not produce enough benefits to offset the costs. Continuing investments begin to reap great benefits and produce both economies and synergies to result in improved performance. Accordingly, this study expects a curvilinear, either U-shaped or reverse U-shaped, effect of higher academic qualifications on the performance of audit firms. The effects of higher academic qualifications on performance are initially negative (positive) but becomes positive (negative) because of the hiring of additional auditors with higher academic qualifications.

Previous studies confirm the existence of market segmentation in the auditing industry [13,44]. Market segmentation originates from the incomplete competition market theory, which assumes that consumers in a market are heterogeneous and possess different preferences. To market their products, firms seek consumers with homogeneous preferences and group them into a smaller unit [45]. Thus, market segmentation refers to a group of consumers possessing a set of common attributes, such as demographic factors, geography, buyer’s industry and size of the purchasing firm, within a broader market [46]. Through market segmentation, firms determine their target market and precisely adjust their products and marketing activities to meet consumers’ needs [47].

In practice, larger companies are complicated in organizational structure and assume higher internal agency cost [48]. They hire large audit firms to audit their financial statements to alleviate the agency cost [49]. Public companies are larger in size and more revenues compared to private companies. Under the regulation and laws, audit firms which render services to public companies are larger in size and hire more assistants. Based on prior studies [13,14,15,16], this study categorizes audit firms into three groups in terms of size, including national, regional, and local ones.

National firms are large-scaled in either numbers of employees or revenues and own abundant physical and human resources. This study expects that their operating performance increases at a diminishing rate as the employees with a master’s degree or above increase. In econometrics, the curvilinear relation between higher academic qualifications and performance is reverse U-shaped, a concave pattern. Local firms are a proprietorship organization and render audit and non-audit services to the small-sized enterprises. We expect their operating performance is proportional to the employees with a master’s degree or above at an increasing rate. The curvilinear relation of local audit firms is U-shaped, a convex pattern. Compared to the size of national and local firms, regional firms are medium-scaled ones. They are not legally allowed to provide auditing services to public companies. Their main clients are the small and medium-sized enterprises. We thus argue their curvilinear relation pattern falls between that of national and local firms. Specifically, their operating performance increases at a nearly fixed rate as the employees with a master’s degree or above increase. The curvilinear relation of regional firms is either reverse U-shaped or U-shaped, a concave or convex pattern. We advance the following three hypotheses accordingly.

Hypothesis 4a.

The curvilinear relation between higher academic qualifications and operating performance of national audit firms is reverse U-shaped, a concave pattern.

Hypothesis 4b.

The curvilinear relation between higher academic qualifications and operating performance of regional audit firms is either reverse U-shaped or U-shaped, a concave or convex pattern.

Hypothesis 4c.

The curvilinear relation between higher academic qualifications and operating performance of local audit firms is U-shaped, a convex pattern.

3. Methodology

3.1. Data and Sample Classification

Empirical data of this study are taken from the 1992–2015 Survey Report of Audit Firms in Taiwan published by the Financial Supervisory Commission (FSC), Executive Yuan. The FSC administers the survey pursuant to the Statistics Act and requires audit firms surveyed to fill out the questionnaire correctly before the due time. The Survey Report reveals an annual response rate of over eighty percent. As a pooled cross-sectional empirical data, this study conducts the Durbin–Watson test and obtains DW statistics between 1.33 and 2.19, which implies low correlation between residual terms. Next, as the sample period spans over 24 years, all monetary variables are deflated by the yearly Consumer Price Index to account for inflation and the year effects are controlled accordingly.

In terms of market segmentation, we group the total sample into three categories: National, regional, and local audit firms. National firms refer to partnership audit firms that audit financial statements of public companies, regional firms are partnership firms that do not offer this service and local firms represent proprietorship audit firms. We use total number of employees and total revenues to measure the size of an audit firm. Both measures indicate that national firms are statistically and significantly greater than regional firms, and regional firms greater than local firms. After excluding the outliers, we have 11,979 firm-year observations, including 1072 national, 3280 regional, and 7627 local audit firms.

3.2. Regression Models and Variable Definitions

In industrial economics, the structure–conduct–performance (S–C–P) theoretical framework states that market structures affect the conducts of firms and further affect firm performance [50,51]. Based on the S–C–P framework and prior studies on audit firms [11,12,14], this study establishes the following cross-sectional regression equation to test our hypotheses.

where:

PFM = β0 + β1 EDU + β2 TRAIN + β3 EDU × TRAIN + β4 EDU2 + β5 SCALE + β6 AGE + β7 EXP + β8 YEAR + ε

| PFM | = | Operating performance; |

| EDU | = | Higher academic qualifications; |

| TRAIN | = | Professional training; |

| SCALE | = | Size of audit firms; |

| AGE | = | Ages of audit firms; |

| EXP | = | Work experience of auditors; |

| YEAR | = | Year effects; and |

| ε | = | Error term. |

In testing HYPOTHESES 1 to 3, this study expects that β1, β2, and β3 to be positive. In testing HYPOTHESIS 4, β4 is predicted to be either positive or negative.

3.3. Dependent Variable and Research Variables

Following Collins-Dodd et al. [11], this study defines dependent variable, operating performance (PFM), as production contribution per employees or product of employees, namely, revenues per employees. In economics, the operating performance (PFM) is a ratio of output to input. Prior researches utilize an average educational level to estimate academic qualification [42,43,52]. Instead, this study defines the higher academic qualifications (EDU) as the percentage of auditors with a master’s degree or above. Following prior studies (for example, [12]), this study defines another research variable, professional training (TRAIN), as natural logarithm of total training expenses in an audit firm. The total training expenses include pre-professional training and continuing professional training expenditures. The third research variable of this study is the interaction term of professional training and higher academic qualifications (EDU × TRAIN).

Previous researches indicate that audit quality significantly affects operating performance of audit firms. They identify key determinants or drivers of audit quality, including academic qualifications [22,53], professional training [21,29] and work experience of auditors [29,54]. Our regression model takes the audit quality into account. Hence, it is an audit quality control model and also a model of performance determinant of audit firms.

3.4. Control Variables

In addition to the variables of interest, this study includes some other factors affecting operating performance of audit firms in the regression equation as control variables. Theoretically, audit firms can enjoy economy of scale when their size expands [55]. This study includes audit firm size (SCALE), defined as natural logarithm of total income of an audit firm, and expects it to be positively related to performance [11,14]. In an audit firm, human capital and customer base increase over time and contribute to revenues. Based on prior studies, this study includes age of audit firms (AGE) to control its effects on operating performance [10,14,43,56].

In auditing industry, auditors enter their careers and serve as assistants in audit firms after their acquiring the academic qualifications in accounting. In a typical audit firm, mean years of work experience for partners, managers, seniors or in-charge auditors, and assistants are over 10 years, 5–10 years, 2–5 years, and 0–2 years, respectively [57]. Previous researches find a positive association between work experience and job performance [58]. Also, work experience of auditors constitutes a human capital factor that affects audit quality [29,54]. In the line of literature on auditing, prior studies indicate a positive relation between work experience and performance of audit firms [10,14]. Based on prior studies [10,11,14,43], this study includes work experience of auditors (EXP) to control its effects on operating performance.

Pooled cross-sectional data of 24 years are used in this study and span over two centuries. Local economy or environmental factors affect financial performance of audit firms [59]. To control both yearly and economy effects, this study includes the Taiwan Stock Exchange Capitalization Weighted Stock Index as the year effect indicator (YEAR).

4. Results

4.1. Descriptive Statistics

Table 1 lists the descriptive statistics for three categories of audit firms. When Panels A, B, and C are compared, mean operating performance of national audit firms, $961,121, is higher than that of regional firms, $758,269, and that of local firms, $668,955. Mean higher academic qualifications (EDU) of 0.082 denotes that auditors with master’s degree or above account for 8.2% of total employees in the national audit firms. The means for regional and local firms are 0.104 and 0.118, respectively. On average, professional training (TRAIN) of national firms is 11.555, indicating that the untransformed training expenses equal $362,666. Regional and local firms have mean professional training (TRAIN) of 10.288 and 9.529, lower than that of national firms.

For control variables, mean size (SCALE) of national audit firms is 17.589, higher than that of regional firms, 16.121, and that of local firms, 14.844. The average ages (AGE) of national audit firms are 17.009. Average ages (AGE) of regional and local firms are 13.917 and 12.048, younger than that of national firms. Mean work experience of auditors (EXP), 33.450, indicates that the average auditor ages in national firms are about 33. The average ages of auditors in regional and local firms are about 36 and 39, older than that of national firms.

4.2. Regression Results

This study displays empirical results in Table 2. We estimate the standardized regression coefficients and conduct some econometric tests to correct for heteroscedasticity of variable coefficient and multi-collinearity among independent variables.

4.3. National Audit Firms

As can be seen in the National column of Table 2, the research variable of higher academic qualifications (EDU) appears in three terms, EDU, EDU × TRAIN, and EDU2. In econometrics, both interaction and quadratic terms should be taken into account in determining the relation between higher academic qualifications and performance. Thus, this study takes a first-order differentiation over higher academic qualifications (EDU) in National column with the value of 2.0482 (0.243 + 0.160 × 11.555 − 2 × 0.266 × 0.082). Also, the research variable of professional training (TRAIN) appears in two terms. Similar econometric treatment applies to professional training (TRAIN) and this study obtains value of 0.1461 (0.133 + 0.160 × 0.082). Consistent with expectations, this indicates that higher academic qualifications and professional training positively associate with operating performance of national audit firms, lending supports to HYPOTHESIS 1 and HYPOTHESIS 2, respectively.

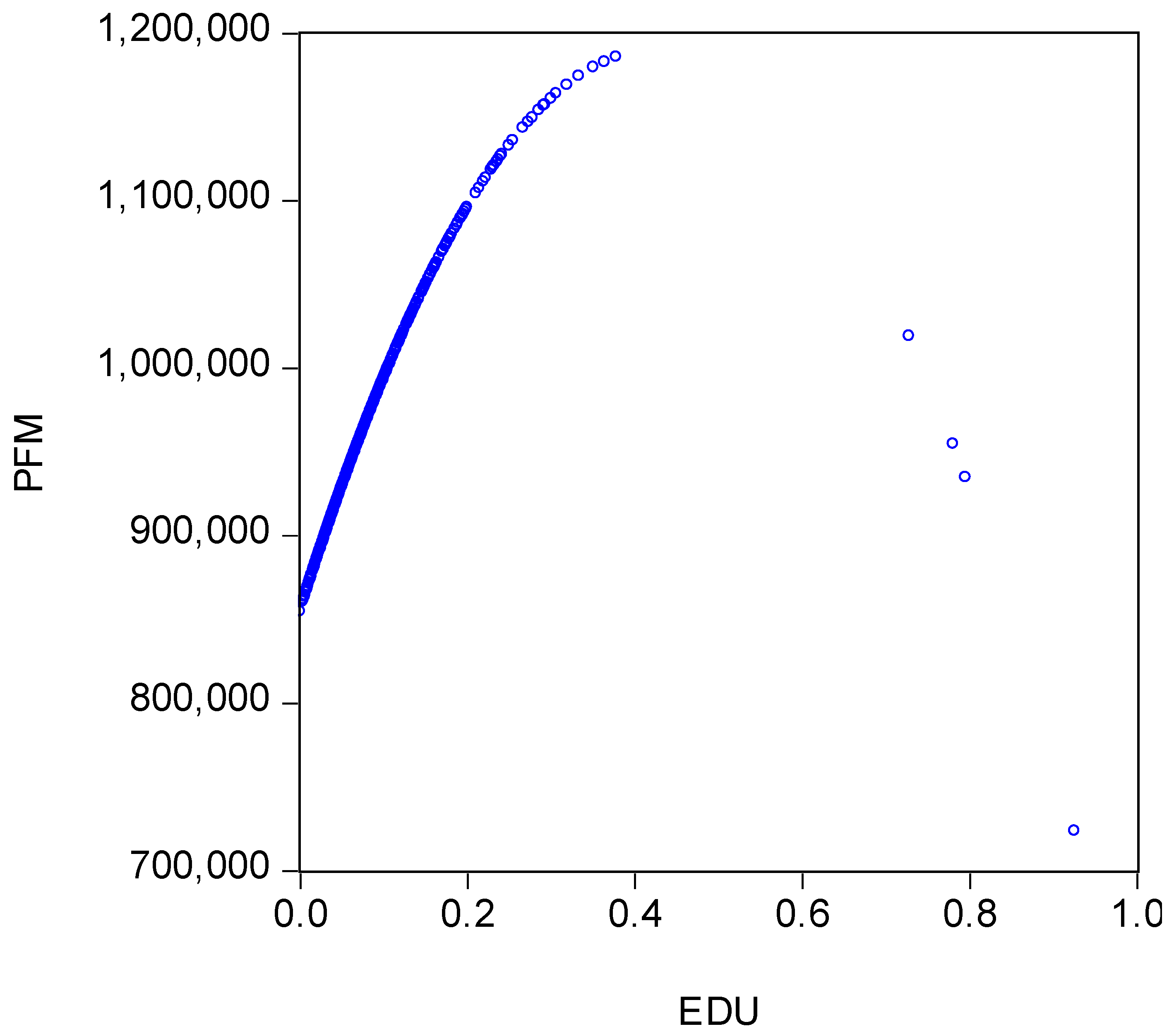

Next, the coefficients on interaction term between higher academic qualifications and professional training (EDU × TRAIN) are positive but insignificantly. Inconsistent with the sign and direction of coefficients, HYPOTHESIS 3 is not supported. Finally, the quadratic term of higher academic qualifications (EDU2) negatively associate with performance (t = −5.766, p < 0.01). In econometrics, curvilinear relation between higher academic qualifications and performance is determined by taking a second order differentiation over higher academic qualifications (EDU). The resulting positive (negative) value stands for a U-shaped (reverse U-shaped) curvilinear relation. The second derivative value for national audit firms is −0.532 (−0.266 × 2). As shown in Figure 1, the curvilinear relation is reverse U-shaped, a concave pattern. When national audit firms hire more employees with a master’s degree or above, their operating performance increases at a diminishing rate before the turning point of EDU, 40%. After the turning point, operating performance of national audit firms decreases sharply. This indicates that their operating performance (PFM) increases at a diminishing rate as the employees with a master’s degree or above (EDU) increase. HYPOTHESIS 4a is supported.

4.4. Regional Audit Firms

In the Regional column of Table 2, both the research variable of higher academic qualifications (EDU) and professional training (TRAIN) appears in three and two terms, respectively. This study applies similar econometric treatments as for national firms to the regional firms. The results indicate that higher academic qualifications and professional training positively associate with operating performance of regional audit firms, lending supports to HYPOTHESIS 1 and HYPOTHESIS 2.

Next, the coefficients on interaction term between higher academic qualifications and professional training (EDU × TRAIN) are significantly positive (t = 5.937, p < 0.01). Consistent with the sign and direction of coefficients, HYPOTHESIS 3 is supported. Finally, the quadratic term of higher academic qualifications (EDU2) positively associate with performance (t = 2.218, p < 0.01). After taking a second order differentiation over higher academic qualifications (EDU), this study obtains a value of 0.134 (0.067 × 2). As can be seen in Figure 2, operating performance of regional firms (PFM) increases at a nearly fixed rate as the employees with a master’s degree or above (EDU) increase. The curvilinear relation of regional firms is a U-shaped and convex pattern, lending a support to HYPOTHESIS 4b.

4.5. Local Audit Firms

In the Local column of Table 2, both the research variable of higher academic qualifications (EDU) and professional training (TRAIN) appears in three and two terms, respectively. After applying similar econometric treatments as before, this study obtains that higher academic qualifications and professional training positively associate with operating performance of local audit firms, lending supports to HYPOTHESIS 1 and HYPOTHESIS 2.

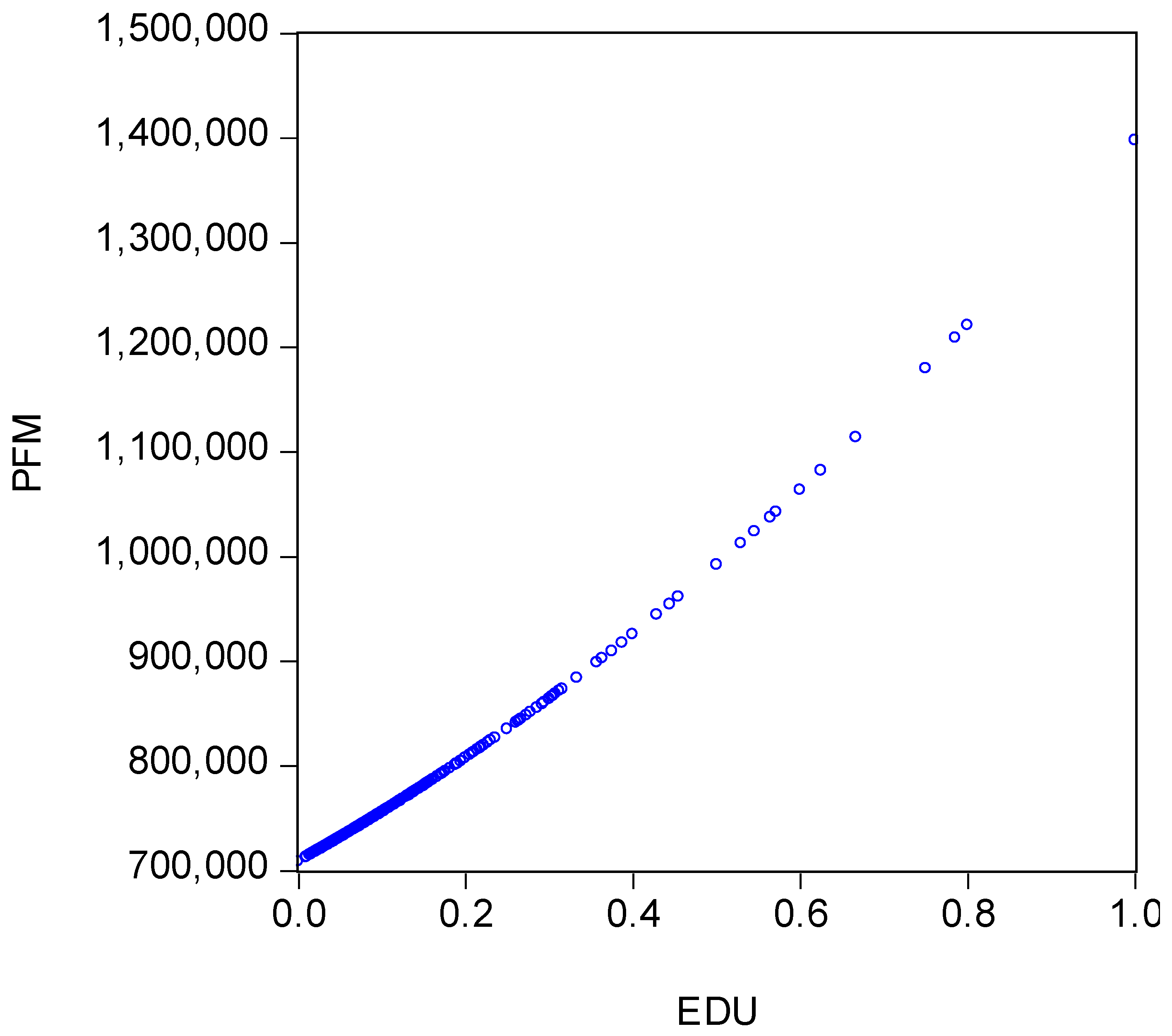

Next, the coefficients on interaction term between higher academic qualifications and professional training (EDU × TRAIN) are significantly positive (t = 12.131, p < 0.01). Consistent with the sign and direction of coefficients, HYPOTHESIS 3 is supported. Finally, the quadratic term of higher academic qualifications (EDU2) positively associate with performance (t = 11.961, p < 0.01). After taking a second order differentiation over higher academic qualifications (EDU), this study obtains a value of 0.560 (0.280 × 2). As shown in Figure 3, the curvilinear relation of local audit firms is U-shaped, a convex pattern. This reveals that their operating performance is proportional to the employees with a master’s degree or above at an increasing rate. HYPOTHESIS 4c receives support.

5. Conclusions

5.1. Discussions

Some prior studies, including Pennings et al. [42], Bröcheler et al. [43], and Chen and Chen [52], display a positive relation between average educational levels and financial performance of audit firms. These studies estimate the average educational levels using the average years of academic education of auditors. However, Fasci and Valdez [10] and Collins-Dodd et al. [11] report an insignificant association between average educational levels of auditors and operating performance of proprietorship audit firms. Fasci and Valdez [10] define educational levels of auditors as the amount of education beyond baccalaureate. Collins-Dodd et al. [11] categorize the educational levels of employees into secondary, postsecondary, college or technical school and university. Then, they set dummy variables to measure the educational levels of auditors. In contrast, Fasci and Valdez [10] measure educational levels by number of employees, which is an absolute value that does not take the size of audit firms into account. In the classification of educational levels, Collins-Dodd et al. [11] put the master’s and bachelor’s degrees in the same category, thus weakening the robustness of the results.

The mixed results between academic educational levels of auditors and operating performance come from the confounding effects of educational level measurement. To clearly define higher educational levels, this study exclusively estimates the master’s degree or above. With the improvement of variable definitions, this study assesses the relation between higher educational levels and operating performance with less measurement error, resulting in definite and bright findings of higher academic qualifications.

5.2. Implications for Theory

Our empirical results indicate a positive relation between professional training and operating performance of audit firms, consistent with previous researches [12,14,56]. Next, this study extends the literature on professional training and educational levels to incorporate their interaction terms. The results obtained show a positive association between interaction terms and performance. This represents that professional training moderates the effects of higher educational levels and improves their relation to the performance of audit firms, adding knowledge to the human resources management theory.

The empirical results in the previous sections display that higher educational levels are positively associated with the operating performance of audit firms. This findings justify the educational policy of establishing institutes or graduate schools in the department of accounting over the past two decades in Taiwan. Being a professional organization, audit firms that hire employees with a higher educational level benefit their operating performance. With results, this study substantiates theoretically that higher academic qualifications matter, an incremental contribution in knowledge to the theory.

5.3. Implications for Human Resources Management Practice

In fulfillment of their social role, audit firms provide traditional audit services and non-audit services which are typically referred to as management advisory services (MASs). The MASs offered by a typical audit firm includes, but not limited to, information technology (IT), electrical commerce advisory services, personal financial planning, integrated tax planning, mergers and acquisitions (M&A), business valuation, pension funds actuarial advisory services, and budgeting and forecasting services [60]. Traditional audit services include audits of financial statements and income tax returns. These businesses are required by various governmental agencies in Taiwan, resulting in a law-protected and statutory traditional practice. Some accounting educators and practitioners regard them as services which clients need but do not necessarily want [61]. Since 1988, the passing rate of the Certified Public Accountant (CPA) uniform examination was raised by Taiwanese authorities, leading to substantial increases in the number of qualified CPAs and in market competition. Further, the authorities abolished the long-standing audit fee standards to ensure fair audit market competition in 1998. Cancellation of audit fee standards adversely impacts the traditional audit service market. In 2004, the tax authorities established a tax agent system which legalized the provision of tax services, corporate registration and accounting services by tax agents to small and medium-sized entities (SMEs). As regional and local audit firms provide the same practices as tax agents to the SMEs for years, both of them are negatively impacted by the tax agent legalization due to the competitive advantages the tax agents possess for a relatively lower service fees and easy service access by the clients.

Responding to the external environment effectively to gain competitive forces [62], audit firms provide services to the same clients for years and are familiar with their clients’ daily operation and financial condition. With the long-term partnership and close client relations, audit firms gain a more favorable position in providing MASs than an ordinary professional consulting firm. Joint provisions of audit services and MASs theoretically create synergy and knowledge spillover effects for audit firms [63,64].

In rendering MASs to meet clients’ demand for specific services, auditors devote more involvements and communications and gain more flexible service provisions in format, timing, and place. Because MASs are a tailor-made and innovative practice, they generally bring higher profits, higher growth potential and industry expansion rather than predatory competition [65]. Auditors have shifted their human resources from traditional, low-margin revenue product areas of auditing and accounting into relatively new, high-margin revenue product areas of MASs in the beginning of 1990s [66]. The dataset of this study indicates that the mean ratios of MASs of national, regional and local firms are 0.2104, 0.2995, and 0.3631 during the sample period. The MASs ratios were 0.1791, 0.2364, and 0.2867 in 1992 and rose to 0.3016, 0.3685, and 0.4261 in 2015. The growth of MASs documents the business structure of audit firms after the 1990s.

Because MASs require a diverse product line, customization, and service innovations, audit firms take differing business strategies by their auditors’ distinctive competencies, including academic background, professional experience, and customer network. This study claims that audit firms hire more auditors with a master’s degree or above to respond to the competitive MASs market after the 1990s. Those higher-education-level auditors have enhanced organizing and coordinating capabilities to contribute greatly to the operating performance of audit firms. Our empirical results document that higher academic qualifications contribute positively to operating performance of audit firms after the 1990s. Audit firms skillfully exploit employees with higher educational levels to expand their business to the MASs and improve operating performance for the sample period, 1992 to 2015.

5.4. Limitations and Future Studies

After the 2001 Enron event, the Public Company Accounting Oversight Board (PCAOB) in the United States established auditing and quality control standards for audits of public companies. Moreover, it performs quality control inspections in audit firms rendering these services. PCAOB focuses on the assessment of professional competency of auditors, assignment of responsibility and continuing professional training programs. Following prior studies, this study uses academic qualifications [22,53], professional training [21,29], and work experience [29,54] to control audit quality. However, as limitation of this study, we are not able to control teamwork, which is an important driver of audit quality, because of data unavailability. In addition, PCAOB is concerned about the internal control system, operating policies and auditing procedures of audit firms. This study is again limited by the data unavailability of these factors that influence the operating performance of audit firms.

This study empirically finds a negative association between higher academic qualifications and age of audit firms. Future studies may take the life cycle of an organization into account when examining national, regional, and local audit firms to acquire more effective practical implications.

Author Contributions

Y.-S.C. proposed the idea and finished the original and final draft of this paper. Y.-F.Y. collected data, established the model, completed the empirical tests and analyzed the results. C.-C.Y. improved the model and gave significant suggestions to the implications of the results. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- DES. Higher Education: A New Framework (1541); HMSO: London, UK, 1991; ISBN 978-0101154123. [Google Scholar]

- DfEE. Education and Training Statistics for the United Kingdom; Stationery Office Books: London, UK, 1999; ISBN 978-0112710752. [Google Scholar]

- HESA. Students in Higher Education Institutions, 1999/2000; HESA: Cheltenham, UK, 2001. [Google Scholar]

- Boynton, W.C.; Johnson, R.N.; Kell, W.G. Modern Auditing, 7th ed.; John Wiley & Sons Inc.: New York, NY, USA, 2001; ISBN 0471345938. [Google Scholar]

- Salas, E.; Cannon-Bowers, J.A. The Science of Training: A Decade of Progress. Annu. Rev. Psychol. 2001, 52, 471–499. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Psacharopoulos, G. Returns to Education: A Further International Update and Implications. J. Hum. Resour. 1985, 20, 583–604. [Google Scholar] [CrossRef]

- Noe, R.A. Employee Training and Development; McGraw Hill: New York, NY, USA, 1999. [Google Scholar]

- Lepak, D.P.; Snell, S.A. The Human Resource Architecture: Toward A theory of Human Capital Allocation and Development. Acad. Manag. Rev. 1999, 24, 31–48. [Google Scholar] [CrossRef]

- Schultz, T.W. Investment in Human Capital. Am. Econ. Rev. 1961, 51, 1–17. [Google Scholar]

- Fasci, M.A.; Valdez, J. A Performance Contrast of Male- and Female-Owned Local Accounting Practices. J. Local Bus. Manag. 1998, 36, 1. [Google Scholar]

- Collins-Dodd, C.; Gordon, I.M.; Smart, C. Further Evidence on the Role of Gender in Financial Performance. J. Local Bus. Manag. 2004, 42, 395–417. [Google Scholar] [CrossRef]

- Yang, Y.F.; Chen, Y.S.; Yang, L.W. Gender Gap, Training, and Financial Performance: Evidence from Public Accounting Industry. Int. J. Hum. Resour. Manag. 2013, 24, 3697–3718. [Google Scholar] [CrossRef]

- Ghosh, A.; Lustgarten, S. Pricing of Initial Audit Engagements by National and Local Audit Firms. Contemp. Account. Res. 2006, 23, 333–368. [Google Scholar] [CrossRef]

- Chen, Y.S.; Chang, B.G.; Lee, C.C. The Association between Continuing Professional Education and Financial Performance of Public Accounting Firms. Int. J. Hum. Resour. Manag. 2008, 19, 1720–1737. [Google Scholar] [CrossRef]

- Chen, Y.S.; Huang, I.C. Product Innovations and Performance of Audit Firms in Taiwan: Consideration of Life Cycles and Market Segments. Asia-Pac. J. Manag. Res. Innov. 2012, 8, 365–387. [Google Scholar] [CrossRef]

- Yang, Y.F.; Chen, Y.S. Quality Moderates Market Competition: Evidence of Taiwanese Service Industry. Int. J. Qual. Reliab. Manag. 2016, 33, 1332–1345. [Google Scholar] [CrossRef]

- Hitt, M.A.; Berman, L.; Shimizu, K.; Kochhar, R. Direct and Moderating Effects of Human Capital on Strategy and Performance in Professional Service Firms: A Resource-Based Perspective. Acad. Manag. J. 2001, 44, 13–28. [Google Scholar] [CrossRef] [Green Version]

- Becker, C.L.; DeFond, M.L.; Jiambalvo, J.; Subramanyam, K.R. The Effect of Audit Quality on Earnings Management. Contemp. Account. Res. 1998, 15, 1–24. [Google Scholar] [CrossRef]

- Chen, S.; Sun, S.Y.J.; Wu, D. Client Importance, Institutional Improvements, and Audit Quality in China: An Office and Individual Auditor Level Analysis. Account. Rev. 2010, 85, 127–158. [Google Scholar] [CrossRef]

- Liu, J.; Wang, Y.; Wu, L. The Effect of Guanxi on Audit Quality in China. J. Bus. Ethics 2011, 103, 621–638. [Google Scholar] [CrossRef]

- Meinhardt, J.; Moraglio, J.F.; Steinberg, H.I. Governmental Audits: An Action Plan for Excellence. J. Account. 1987, 164, 86–91. [Google Scholar]

- Lee, C.W.; Liu, C.W.; Wang, T.C. The 150-Hour Rule. J. Account. Econ. 1999, 27, 203–228. [Google Scholar] [CrossRef]

- Nielsen, K.; Randall, R.; Christensen, K.B. Does Training Managers Enhance the Effects of Implementing Team-Working? A Longitudinal, Mixed Methods Field Study. Hum. Relat. 2010, 63, 1719–1741. [Google Scholar] [CrossRef] [Green Version]

- Sahinidis, A.G.; Bouris, J. Employee Perceived Training Effectiveness Relationship to Employee Attitudes. J. Eur. Ind. Train. 2008, 32, 63–76. [Google Scholar] [CrossRef] [Green Version]

- Becker, G.S. Human Capital; Columbia University Press: New York, NY, USA, 1964; ISBN 0-226-04119-0. [Google Scholar]

- Grant, R.M. The Resource-Based Theory of Competitive Advantage: Implication for Strategy Formulation. Calif. Manag. Rev. 1991, 33, 114–135. [Google Scholar] [CrossRef] [Green Version]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Amit, R.; Schoemaker, P.J.H. Strategic Assets and Organizational Rent. Strateg. Manag. J. 1993, 14, 33–46. [Google Scholar] [CrossRef]

- Financial Reporting Council (FRC). Discussion Paper: Promoting Audit Quality. 2006. Available online: http://www.frcpublications.com (accessed on 8 February 2002).

- Louwers, T.J.; Ramsay, R.J.; Sinason, D.H.; Strawser, J.R. Auditing and Assurance Services; McGraw Hill: New York, NY, USA, 2005; ISBN 9780071113007. [Google Scholar]

- Tharenou, P.; Saks, A.M.; Moore, C. A Review and Critique of Research on Training and Organizational-Level Outcomes. Hum. Resour. Manag. Rev. 2007, 17, 251–273. [Google Scholar] [CrossRef]

- Alhejji, H.; Garavan, T.; Carbery, R.; O’Brien, F.; McGuire, D. Diversity Training Programme Outcomes: A Systematic Review. Hum. Resour. Dev. Q. 2015, 22, 95–149. [Google Scholar] [CrossRef]

- Wallace, W.A.; Campbell, R.L. State Boards of Accountancy: Quality Review and Positive Enforcement Programs. Res. Account. Regul. 1988, 2, 123–154. [Google Scholar]

- Thomas, C.W.; Davis, C.E.; Seaman, S.L. Quality Review, Continuing Professional Education, Experience and Substandard Performance: An Empirical Study. Account. Horiz. 1998, 12, 340–362. [Google Scholar]

- Grotelueschen, A.D. The Effectiveness of Mandatory Continuing Education for Licensed Accountants in Public Practice in the State of New York; Special Report by the Mandatory Continuing Education Study Committee, New York State Board for Public Accountancy, Department of Education; Academic Press: Albany, NY, USA, 1990. [Google Scholar]

- Lee, G.J. Firm Size and the Effectiveness of Training for Customer Service. Int. J. Hum. Resour. Manag. 2012, 23, 2597–2613. [Google Scholar] [CrossRef]

- Liao, T.S.; Rice, J.; Martin, N. The Role of the Market in Transforming Training and Knowledge to Superior Performance: Evidence from the Australian Manufacturing Sector. Int. J. Hum. Resour. Manag. 2011, 22, 376–394. [Google Scholar] [CrossRef]

- Sun, P.C.; Hsu, W.J.; Wang, K.C. Enhancing the Commitment to Service Quality through Developmental and Rewarding Systems: CSQ Consistency as A Moderator. Int. J. Hum. Resour. Manag. 2012, 23, 1462–1480. [Google Scholar] [CrossRef]

- Bonner, S.E.; Pennington, N. Cognitive Processes and Knowledge as Determinants of Auditor Expertise. J. Account. Lit. 1991, 10, 1–50. [Google Scholar]

- Lin, C.L.; Chen, Y.S. Human Capital and Operating Performance. Chiao Da Manag. Rev. 2009, 29, 83–130. [Google Scholar] [CrossRef]

- Pisano, G.P. Knowledge, Integration and the Locus of Learning: An Empirical Analysis of Process Development. Strateg. Manag. J. 1994, 15, 85–100. [Google Scholar] [CrossRef]

- Pennings, J.M.; Lee, K.; Witteloostuijn, A.V. Human Capital, Social Capital, and Firm Dissolution. Acad. Manag. J. 1998, 41, 425–440. [Google Scholar] [CrossRef]

- Bröcheler, V.; Maijoor, S.; Witteloostuijn, A.V. Auditor Human Capital and Audit Firm Survival: The Dutch Audit Industry in 1930–1992. Account. Organ. Soc. 2004, 29, 627–646. [Google Scholar] [CrossRef]

- DeFond, M.; Francis, J.T.; Wong, J. Auditor Industry Specialization and Market Segmentation: Evidence from Hong Kong. Audit. A J. Pract. Theory 2000, 19, 49–66. [Google Scholar] [CrossRef]

- Kotler, P. Marketing Management, 11th ed.; Prentice Hall: Englewood Cliffs, NJ, USA, 2003. [Google Scholar]

- Besanko, D.; Dranove, D.; Shanley, M. Economics of Strategy, 2nd ed.; John Wiley and Sons: New York, NY, USA, 2000; ISBN 978-0471212133. [Google Scholar]

- Wendell, R.S. Product Differentiation and Market Segmentation as Alternative Marketing Strategy. J. Mark. 1956, 21, 3–8. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Francis, J.R.; Maydew, E.L.; Sparks, C.H. The Role of Big 6 auditors in the Credible Reporting of Accruals. Audit. A J. Pract. Theory 1999, 18, 17–34. [Google Scholar] [CrossRef]

- Cowling, K.; Waterson, M. Price-cost Margins and Market Structure. Economica 1976, 43, 267–274. [Google Scholar] [CrossRef] [Green Version]

- Ballas, A.; Fafaliou, I. Market Shares and Concentration in the EU Auditing Industry: The Effects of Andersen’s Demise. Int. Atl. Econ. Soc. 2008, 14, 485–497. [Google Scholar] [CrossRef]

- Chen, Y.S.; Chen, C.Y. Audit Firms’ Alliance with Consulting Firms for Management Advisory Services and Operating Performance. J. Account. Rev. 2014, 59, 73–105. (In Chinese) [Google Scholar]

- Liu, C. Legal Liability, Human Capital Investment, and Audit Quality. Ph.D. Thesis, University of National Taiwan University, Taipei, Taiwan, 1997. [Google Scholar]

- Aldhizer, G.R.; Miller, J.R.; Moraglio, J.E. Common Attributes of Quality Audits. J. Account. 1995, 1, 61–71. [Google Scholar]

- Watts, R.; Zimmerman, J. Positive Accounting Theory; Prentice-Hall: Englewood Cliffs, NJ, USA, 1986; ISBN 978-0136861898. [Google Scholar]

- Chen, Y.S.; Goan, K.T.; Chen, S.P. Training and Audit Firms Financial Performance: Consideration of Strategy and Market Segment. J. Hum. Resour. Manag. 2011, 11, 23–46. (In Chinese) [Google Scholar]

- Elder, R.J.; Beasley, M.S.; Arens, A.A. Auditing and Assurance Services: An Integrated Approach, 12th ed.; Pearson Education: Upper Saddle River, NJ, USA, 2008; ISBN 978-0136128274. [Google Scholar]

- Schmidt, F.L.; Hunter, J.E.; Outerbridge, A.M. Impact of Job Experience and Ability on Job Knowledge, Work Sample Performance, and Supervisory Ratings of Job Performance. J. Appl. Psychol. 1986, 71, 432–439. [Google Scholar] [CrossRef]

- Reynolds, J.K.; Francis, J.R. Does Size Matter? The Influence of Large Clients on Office-Level Auditor Reporting Decision. J. Account. Econ. 2000, 30, 375–400. [Google Scholar] [CrossRef]

- Arens, A.A.; Elder, R.J.; Mark, B. Auditing and Assurance Services: An Integrated Approach; Prentice Hall: Englewood Cliffs, NJ, USA, 2012; ISBN 978-0136084730. [Google Scholar]

- Istvan, D.F. The Future of the Accounting Profession: Will Your Firm Survive until 1990? Pract. Account. 1984, 17, 71–74. [Google Scholar]

- Porter, M.E. The Competitive Advantage of Nations; The Free Press: New York, NY, USA, 1990; ISBN 9780029253618. [Google Scholar]

- Beck, P.J.; Frecka, T.J.; Solomon, I. A Model of the Market for MAS and Audit Services: Knowledge Spillovers and Auditor-Auditee Bonding. J. Account. Lit. 1988, 7, 50–64. [Google Scholar]

- Simunic, D.A. Auditing, Consulting, and Auditor Independence. J. Account. Res. 1984, 22, 679–702. [Google Scholar] [CrossRef]

- Rescho, J.A. Public Accounting Firm Strategy and Innovativeness: A Study of the Adoption of Product, Technical, and Administrative Innovations Using a Trategic Typology. Ph.D. Thesis, University of Mississippi, Oxford, MS, USA, 1987. [Google Scholar]

- Banker, R.D.; Chang, H.; Natarajan, R. Productivity Change, Technical Progress, and Relative Efficiency Change in the Public Accounting Industry. Manag. Sci. 2005, 51, 291–304. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Curvilinear relation between higher educational levels and operating performance of national audit firms.

Figure 1.

Curvilinear relation between higher educational levels and operating performance of national audit firms.

Figure 2.

Curvilinear relation between higher educational levels and operating performance of regional audit firms.

Figure 2.

Curvilinear relation between higher educational levels and operating performance of regional audit firms.

Figure 3.

Curvilinear relation between higher educational levels and operating performance of local audit firms.

Figure 3.

Curvilinear relation between higher educational levels and operating performance of local audit firms.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Descriptive statistics.

| PFM | EDU | TRAIN | SIZE | AGE | EXP | YEAR | |

|---|---|---|---|---|---|---|---|

| Panel A: National audit firms (n = 1072) | |||||||

| Mean | 961,121 | 0.082 | 11.555 | 17.589 | 17.009 | 33.450 | 6856.109 |

| Stand. Dev. | 299,956 | 0.075 | 1.374 | 0.890 | 9.653 | 2.880 | 1376.023 |

| Mini. | 171,981 | 0.000 | 6.832 | 13.391 | 1.000 | 26.857 | 4214.780 |

| Maxi. | 2,373,405 | 0.926 | 17.422 | 22.737 | 47.000 | 49.722 | 8992.010 |

| Median | 948,861 | 0.066 | 11.435 | 17.555 | 16.000 | 33.074 | 7024.060 |

| Panel B: egional audit firms (n = 3280) | |||||||

| Mean | 758,269 | 0.104 | 10.288 | 16.121 | 13.917 | 35.840 | 7102.014 |

| Stand. Dev. | 350,246 | 0.134 | 1.484 | 0.952 | 9.564 | 4.988 | 1336.482 |

| Mini. | 312 | 0.000 | 1.872 | 7.530 | 1.000 | 26.250 | 4214.780 |

| Maxi. | 7,685,010 | 1.000 | 14.999 | 19.339 | 59.000 | 62.000 | 8992.010 |

| Median | 711,682 | 0.071 | 10.313 | 16.187 | 12.000 | 35.000 | 7426.690 |

| Panel C: Local audit firms (n = 7627) | |||||||

| Mean | 668,955 | 0.118 | 9.529 | 14.844 | 12.048 | 39.025 | 7165.881 |

| Stand. Dev. | 466,931 | 2.573 | 1.479 | 1.055 | 8.831 | 7.506 | 1349.620 |

| Mini. | 27 | 0.000 | 1.037 | 4.018 | 1.000 | 25.000 | 4214.780 |

| Maxi. | 9,000,000 | 1.000 | 15.574 | 17.398 | 56.000 | 70.000 | 8992.010 |

| Median | 598,668 | 0.000 | 9.649 | 15.016 | 10.000 | 37.500 | 7481.340 |

Note: PFM: Operating performance; EDU: Higher academic qualifications; TRAIN: Professional training; SCALE: Size of audit firms; AGE: Ages of audit firms; EXP: Work experience of auditors; YEAR: Year effect indicators.

Table 2.

Regression results of the effects of higher academic qualifications and professional training on operating performance of audit firms.

Table 2.

Regression results of the effects of higher academic qualifications and professional training on operating performance of audit firms.

| PFM = β0 + β1 EDU + β2 TRAIN + β3 EDU × TRAIN + β4 EDU2 + β5 SCALE + β6 AGE + β7 EXP + β8 YEAR + ε | |||

| Independent Variables (Predicted Sign) | National | Regional | Local |

| Std. Coeff. (t-Value) | Std. Coeff. (t-Value) | Std. Coeff. (t-Value) | |

| EDU (+) | 0.243 (1.281) | −0.456 *** (−4.181) | −0.796 *** (−12.173) |

| TRAIN (+) | 0.133 *** (3.176) | 0.048 ** (2.455) | 0.034 *** (3.065) |

| EDU × TRAIN (+) | 0.160 (0.831) | 0.588 ** (5.937) | 0.732 *** (12.131) |

| EDU2 (?) | −0.266 *** (−5.766) | 0.067 ** (2.218) | 0.280 *** (11.961) |

| SCALE (+) | 0.358 *** (10.422) | 0.557 *** (30.502) | 0.609 *** (53.359) |

| AGE (?) | 0.073 ** (2.471) | −0.087 *** (−5.107) | −0.137 *** (−12.428) |

| EXP (+) | 0.132 *** (4.659) | 0.224 *** (13.242) | 0.256 *** (22.636) |

| YEAR (?) | −0.095 *** (−3.429) | 0.020 (1.320) | 0.019 * (1.938) |

| Adjusted R2 | 0.277 | 0.333 | 0.346 |

| F-statistic | 52.185 *** | 206.021 *** | 505.489 *** |

| Number of observations | 1072 | 3280 | 7627 |

Notes: 1. *, **, *** denote significance at the 10%, 5%, and 1% level for two-tailed test; 2. All VIFs are less than 6.410 in all regression models; 3. Variables are defined in Table 1.

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Chen, Y.-S.; Yang, C.-C.; Yang, Y.-F. Higher Academic Qualifications, Professional Training and Operating Performance of Audit Firms. Sustainability 2020, 12, 1254. https://0-doi-org.brum.beds.ac.uk/10.3390/su12031254

AMA Style

Chen Y-S, Yang C-C, Yang Y-F. Higher Academic Qualifications, Professional Training and Operating Performance of Audit Firms. Sustainability. 2020; 12(3):1254. https://0-doi-org.brum.beds.ac.uk/10.3390/su12031254

Chicago/Turabian StyleChen, Yahn-Shir, Chung-Cheng Yang, and Yi-Fang Yang. 2020. "Higher Academic Qualifications, Professional Training and Operating Performance of Audit Firms" Sustainability 12, no. 3: 1254. https://0-doi-org.brum.beds.ac.uk/10.3390/su12031254

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.