Assessing the Economic Viability of an Animal Byproduct Rendering Plant: Case Study of a Slaughterhouse in Greece

Abstract

:

1. Introduction

2. Materials and Methods

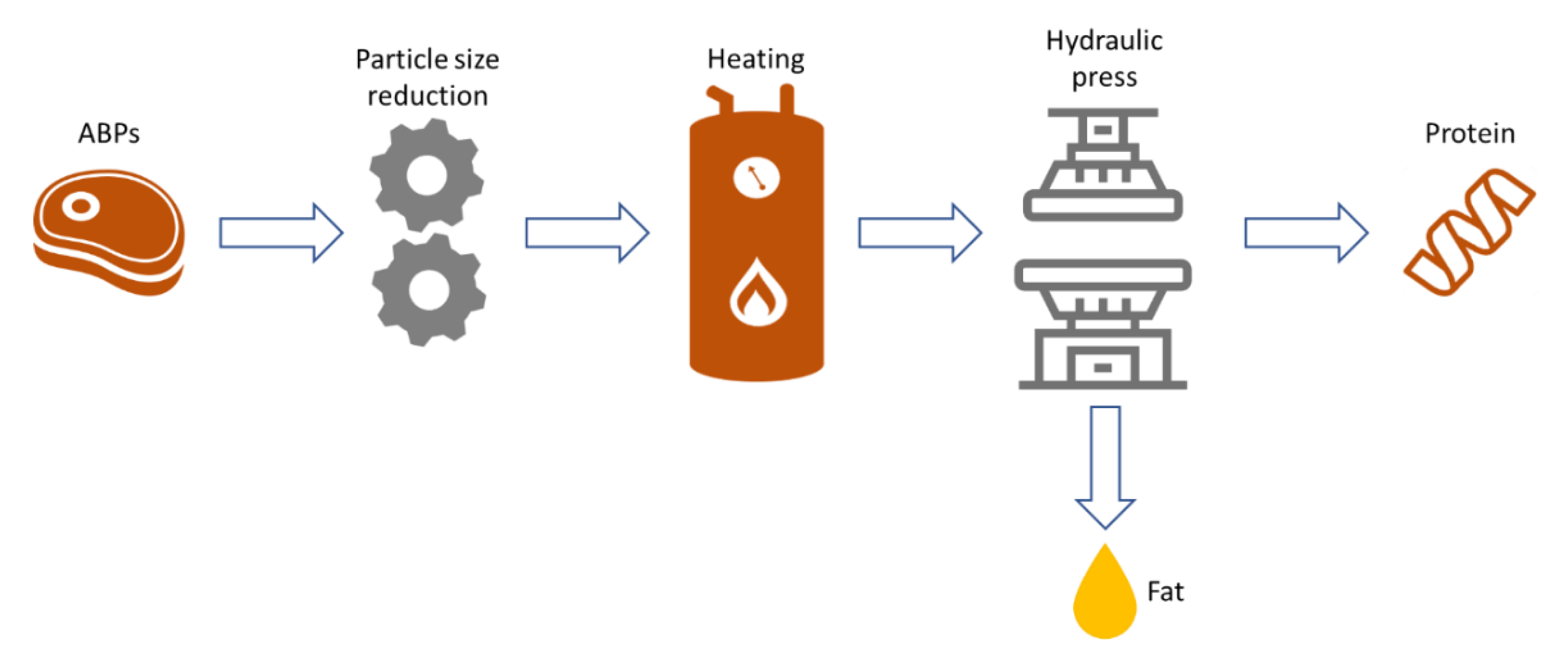

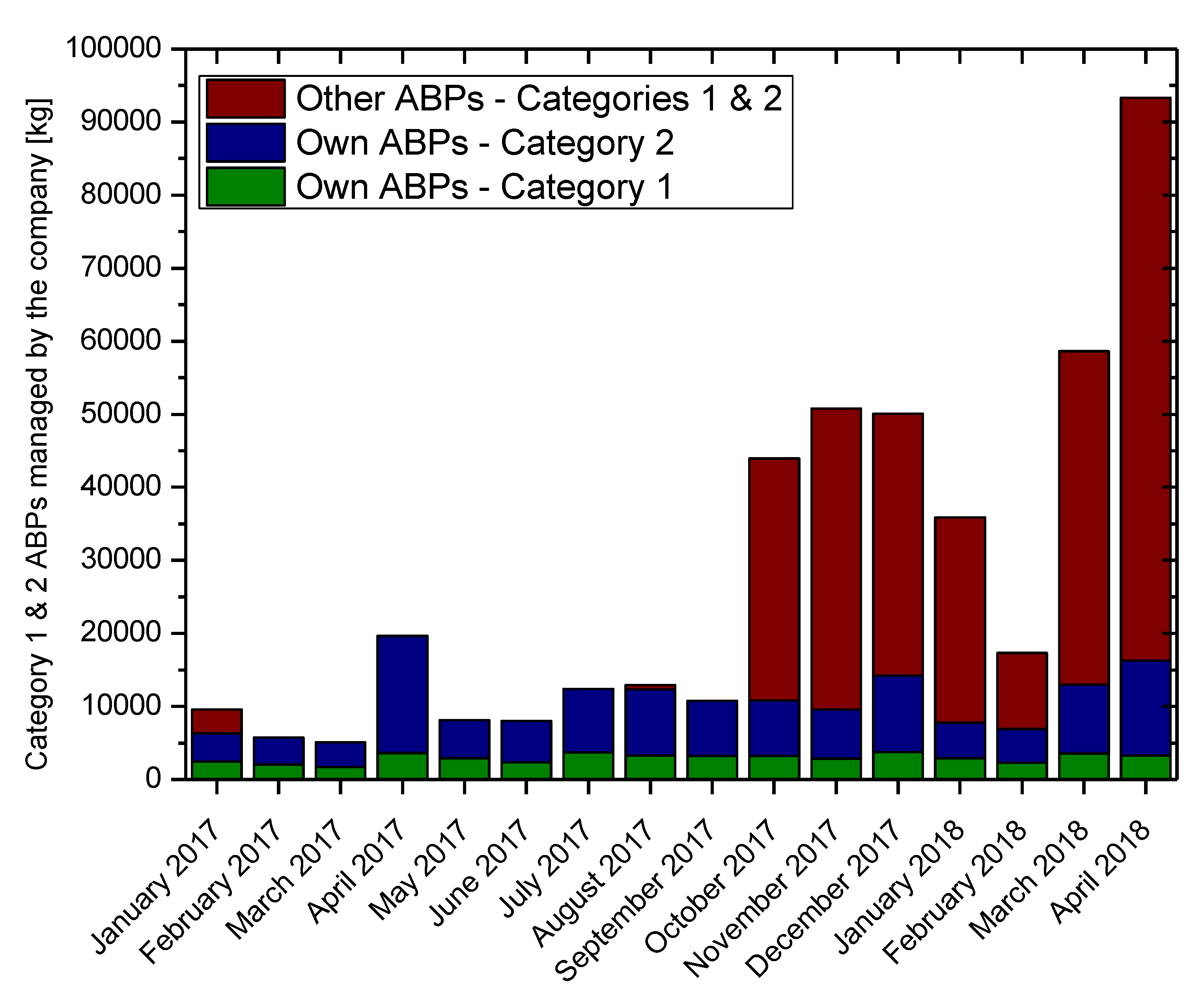

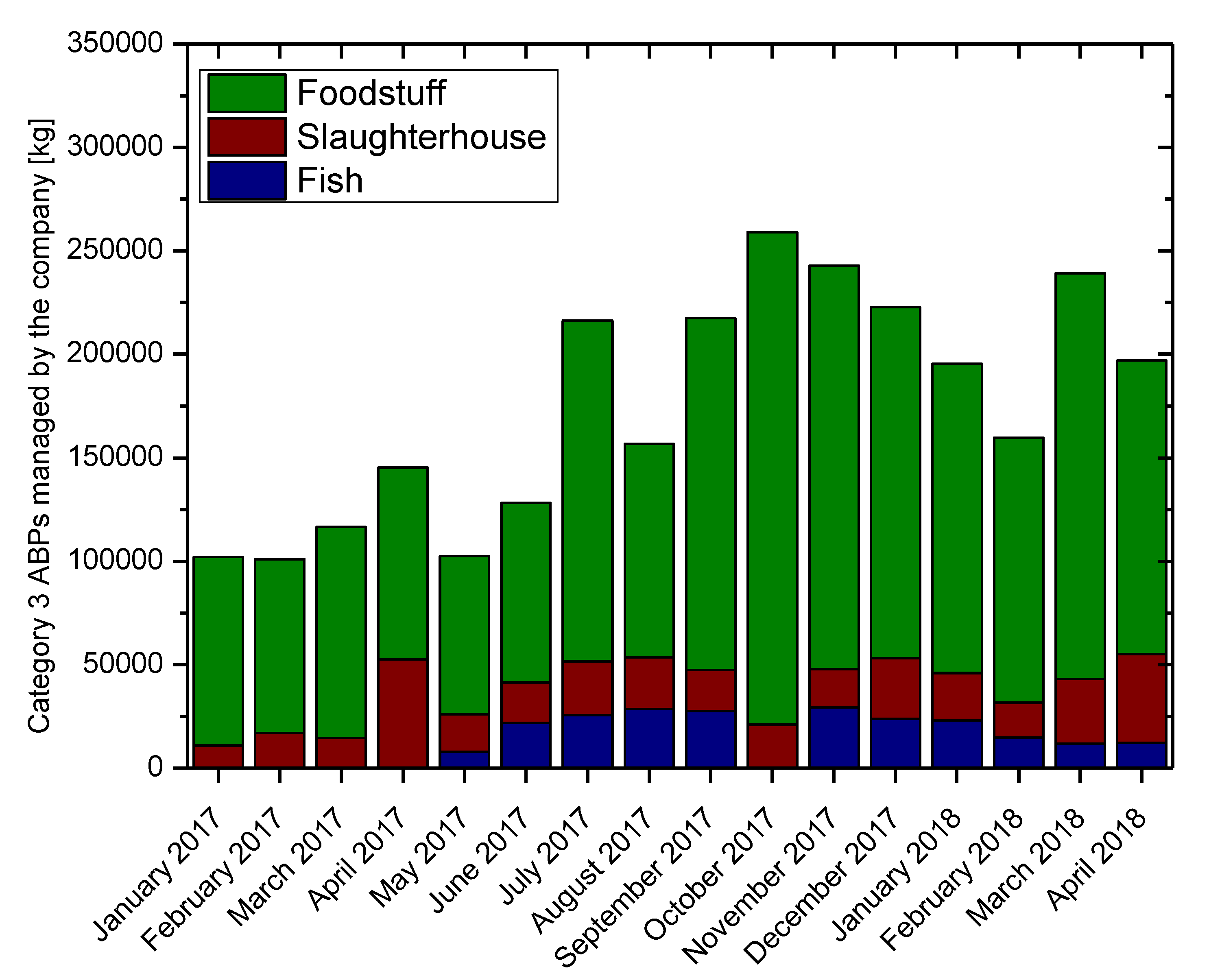

2.1. Description of Current Operation

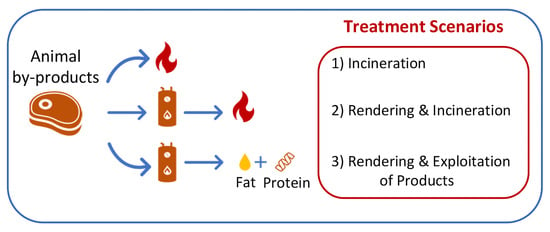

2.2. Assessment of Operating Scenarios

3. Results

3.1. Scenario 1—Incineration of ABPs

3.1.1. Calculation of Total Cost of Scenario 1

3.1.2. Calculation of Net Profit of Scenario 1

3.2. Scenario 2—Rendering of ABPs and Incineration of the Resulting Materials

3.2.1. Calculation of Total Cost of Scenario 2

3.2.2. Calculation of Net Profit of Scenario 2

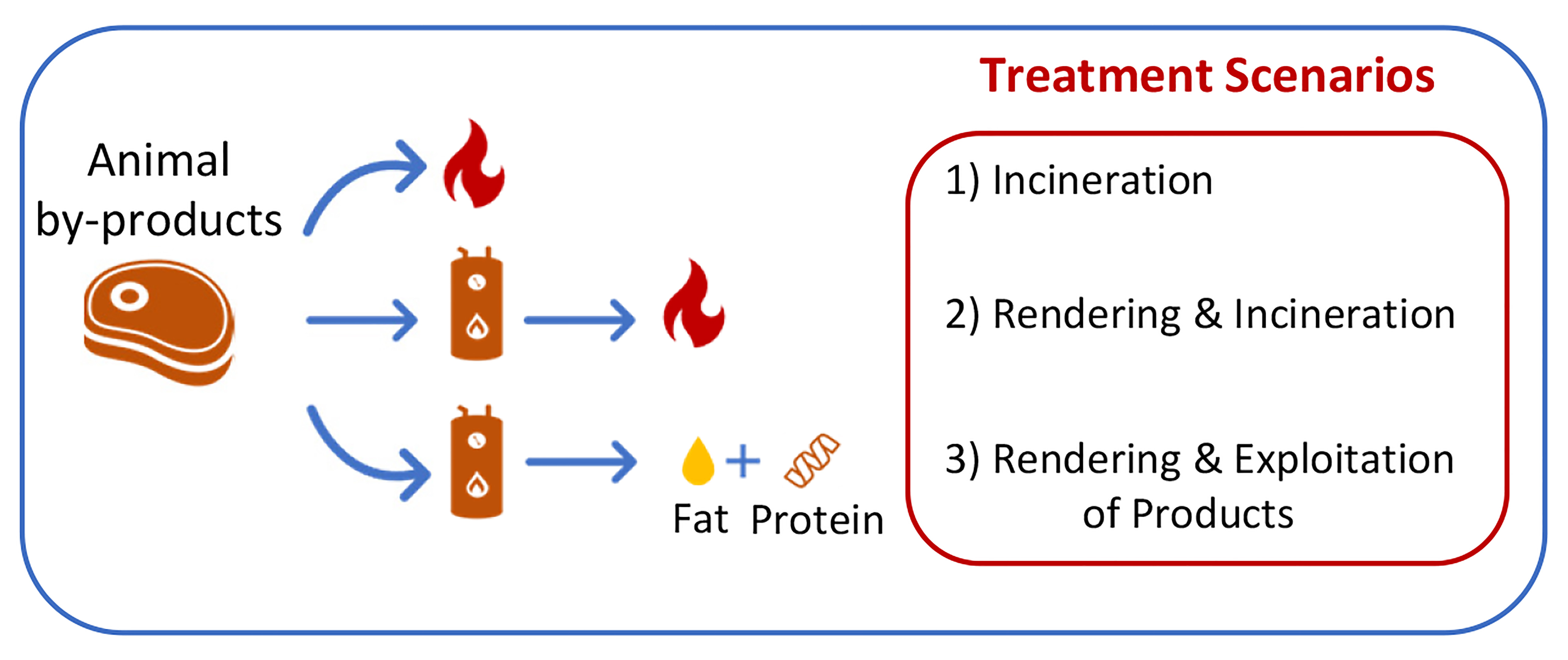

3.3. Scenario 3—Rendering of ABPs and Exploitation of Products

3.3.1. Calculation of Total Cost of Scenario 3

3.3.2. Calculation of Net Profit of Scenario 3

3.4. Comparing the Three Scenarios

4. Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Aguado, S.; Alvarez, R.; Domingo, R. Model of efficient and sustainable improvements in a lean production system through processes of environmental innovation. J. Clean. Prod. 2013, 47, 141–148. [Google Scholar] [CrossRef]

- Musmarra, D.; Zafeirakou, A.; Manakou, V.; Emmanouil, C. Efficient and sustainable environmental management as a means of addressing current pollution issues. Environ. Sci. Pollut. Res. 2019, 26, 14703–14705. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- European Union Directive 2008/98/EC of the European Parliament and of the Council of 19 November 2008 on waste and repealing certain Directives”. Off. J. Eur. Union 2008, 51, 3–30.

- Girotto, F.; Cossu, C.A. Animal waste and waste animal by-products generated along the livestock breeding and meat food chain. Waste Manag. 2017, 70, 1. [Google Scholar] [CrossRef]

- Marti, D.L.; Johnson, R.J.; Mathews, K.H. Where’s the (Not) meat? Byproducts from beef and pork production. In There’s The Beef: Select Research on Global Beef Production and Trade; Nova Science Publishers, Inc.: Washington, DC, USA, 2012; pp. 55–81. ISBN 9781619429437. [Google Scholar]

- European Commission Commission decision of 21 October 2009 laying down health rules as regards animal by-products and derived products not intended for human consumption and repealing Regulation No. 1774/2002 (Animal by-products Regulation), 1069/2009/EC. Off. J. 2009, 50, 1–33.

- Jędrejek, D.; Levic, J.; Wallace, J.; Oleszek, W. characteristics, European regulatory framework, and potential impacts on human and animal health and the environment. J. Anim. Feed Sci. 2016, 25, 189–202. [Google Scholar] [CrossRef]

- Bellarby, J.; Tirado, R.; Leip, A.; Weiss, F.; Lesschen, J.P.; Smith, P. Livestock greenhouse gas emissions and mitigation potential in Europe. Glob. Chang. Biol. 2013, 19, 3–18. [Google Scholar] [CrossRef]

- Sakadevan, K.; Nguyen, M.-L. Livestock production and its impact on nutrient pollution and greenhouse gas emissions. Adv. Agron. 2017, 141, 147–184. [Google Scholar] [CrossRef]

- Gerber, P.J.; Steinfeld, H.; Henderson, B.; Mottet, A.; Opio, C.; Dijkman, J.; Falcucci, A.; Tempio, G. Tackling Climate Change through Livestock: A Global Assessment of Emissions and Mitigation Opportunities; Food and Agriculture Organization of the United Nations (FAO): Rome, Italy, 2013; ISBN 925107920X. [Google Scholar]

- European Commission Commission regulation 999/2001/EC of 22 May 2001 laying down rules for the prevention, control and eradication of certain transmissible spongiform encephalopathies. Off. J. Eur. Commun. 2001, 147, 1–40.

- Alao, B.; Falowo, A.; Chulayo, A.; Muchenje, V. The potential of animal by-products in food systems: Production, prospects and challenges. Sustainability 2017, 9, 1089. [Google Scholar] [CrossRef] [Green Version]

- Toldrá, F.; Mora, L.; Reig, M. New insights into meat by-product utilization. Meat Sci. 2016, 120, 54–59. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Becker, G. Animal rendering: Economics and policy. In Proceedings of the Congressional Research Service report for Library of Congress; Congressional Research Service: Washington, DC, USA, 2004. [Google Scholar]

- Gooding, C.H.; Meeker, D.L. Comparison of 3 alternatives for large-scale processing of animal carcasses and meat by-products. Prof. Anim. Sci. 2016, 32, 259–270. [Google Scholar] [CrossRef] [Green Version]

- Woodgate, S.; Van Der Veen, J. The role of fat processing and rendering in the European Union animal production industry. Biotechnol. Agron. Société Environ. 2004, 8, 283–294. [Google Scholar]

- European Commission Commission Regulation (EU) No 142/2011 of 25 February 2011 implementing Regulation (EC) No 1069/2009 of the European Parliament and of the Council laying down health rules as regards animal by-products and derived products not intended for human consumpti. Off. J. Eur. Commun. 2011, 50, 1–254.

- Baladincz, P.; Hancsók, J. Fuel from waste animal fats. Chem. Eng. J. 2015, 282, 152–160. [Google Scholar] [CrossRef]

- European Parliament and Council Directive 2009/28/EC of the European Parliament and of the Council of 23 April 2009 on the promotion of the use of energy from renewable sources and amending and subsequently repealing Directives 2001/77/EC and 2003/30/EC. Off. J. Eur. Union 2009, 140, 16–62.

- Meeker, D.L. Essential Rendering; National Renderers Association: Arlington, TX, USA, 2006; ISBN 0965466035. [Google Scholar]

- Anderson, D. Rendering Operations. In Essential Rendering All about the Animal By-Products Industry; Meeker, D.L., Ed.; National Renderers Association: Arlington, TX, USA, 2006; pp. 31–52. ISBN 0-9654660-3-5. [Google Scholar]

- Bisplinghoff, F.D. A History of North American Rendering. In Essential Rendering: All about the Animal By-Products Industry; Meeker, D.L., Ed.; National Renderers Association: Arlington, TX, USA, 2006; p. 302. ISBN 9780965466035. [Google Scholar]

- Barrena, R.; Artola, A.; Vázquez, F.; Sánchez, A. The use of composting for the treatment of animal by-products: Experiments at lab scale. J. Hazard. Mater. 2009, 161, 380–386. [Google Scholar] [CrossRef] [Green Version]

- Zhang, H.; Matsuto, T. Comparison of mass balance, energy consumption and cost of composting facilities for different types of organic waste. Waste Manag. 2011, 31, 416–422. [Google Scholar] [CrossRef]

- Moukazis, I.; Pellera, F.-M.; Gidarakos, E. Slaughterhouse by-products treatment using anaerobic digestion. Waste Manag. 2018, 71, 652–662. [Google Scholar] [CrossRef]

- Salehiyoun, A.R.; Francesco Di, M.; Sharifi, M.; Noroozi, O.; Zilouei, H.; Aghbashlo, M. Anaerobic Co-Digestion of Sewage Sludge and Animal by-Product BT—Recent Trends in Waste Water Treatment and Water Resource Management; Ghosh, S.K., Saha, P.D., Francesco Di, M., Eds.; Springer: Singapore, 2020; pp. 1–10. ISBN 978-981-15-0706-9. [Google Scholar]

- Morales-Polo, C.; Del Mar Cledera-Castro, M.; Hueso-Kortekaas, K.; Revuelta-Aramburu, M. Anaerobic digestion in wastewater reactors of separated organic fractions from wholesale markets waste. Compositional and batch characterization. Energy and environmental feasibility. Sci. Total Environ. 2020, 726, 138567. [Google Scholar] [CrossRef]

- Vasco-Correa, J.; Khanal, S.; Manandhar, A.; Shah, A. Anaerobic digestion for bioenergy production: Global status, environmental and techno-economic implications, and government policies. Bioresour. Technol. 2018, 247, 1015–1026. [Google Scholar] [CrossRef] [PubMed]

- Kim, S.; Lee, Y.; Andrew Lin, K.-Y.; Hong, E.; Kwon, E.E.; Lee, J. The valorization of food waste via pyrolysis. J. Clean. Prod. 2020, 259, 120816. [Google Scholar] [CrossRef]

- Leon, M.; Garcia, A.N.; Marcilla, A.; Martinez-Castellanos, I.; Navarro, R.; Catala, L. Thermochemical conversion of animal by-products and rendering products. Waste Manag. 2018, 73, 447–463. [Google Scholar] [CrossRef] [PubMed]

- Irshad, A.; Sharma, B.D. Abattoir by-product utilization for sustainable meat industry: A review. J. Anim. Prod. Adv. 2015, 5, 681–696. [Google Scholar] [CrossRef] [Green Version]

- Jurgilevich, A.; Birge, T.; Kentala-Lehtonen, J.; Korhonen-Kurki, K.; Pietikäinen, J.; Saikku, L.; Schösler, H. Transition towards circular economy in the food system. Sustainability 2016, 8, 69. [Google Scholar] [CrossRef] [Green Version]

- Ajila, C.M.; Brar, S.K.; Verma, M.; Tyagi, R.D.; Godbout, S.; Valéro, J.R. Bio-processing of agro-byproducts to animal feed. Crit. Rev. Biotechnol. 2012, 32, 382–400. [Google Scholar] [CrossRef]

- Nelson, R.G.; Schrock, M.D. Energetic and economic feasibility associated with the production, processing, and conversion of beef tallow to a substitute diesel fuel. Biomass Bioenergy 2006, 30, 584–591. [Google Scholar] [CrossRef]

- Banković-Ilić, I.B.; Stojković, I.J.; Stamenković, O.S.; Veljkovic, V.B.; Hung, Y.-T. Waste animal fats as feedstocks for biodiesel production. Renew. Sustain. Energy Rev. 2014, 32, 238–254. [Google Scholar] [CrossRef] [Green Version]

- Shahzad, K.; Narodoslawsky, M.; Sagir, M.; Ali, N.; Ali, S.; Rashid, M.I.; Ismail, I.M.I.; Koller, M. Techno-economic feasibility of waste biorefinery: Using slaughtering waste streams as starting material for biopolyester production. Waste Manag. 2017, 67, 73–85. [Google Scholar] [CrossRef]

- Bottero, M.; Comino, E.; Riggio, V. Application of the Analytic Hierarchy Process and the Analytic Network Process for the assessment of different wastewater treatment systems. Environ. Model. Softw. 2011, 26, 1211–1224. [Google Scholar] [CrossRef]

- Samah, M.A.A.; Manaf, L.A.; Zuki, N.I.M. Application of AHP model for evaluation of solid waste treatment technology. Int. J. Eng. Techsci 2010, 1, 35–40. [Google Scholar]

- Chen, T.; Jin, Y.; Qiu, X.; Chen, X. A hybrid fuzzy evaluation method for safety assessment of food-waste feed based on entropy and the analytic hierarchy process methods. Expert Syst. Appl. 2014, 41, 7328–7337. [Google Scholar] [CrossRef]

- Valta, K.; Damala, P.; Orli, E.; Papadaskalopoulou, C.; Moustakas, K.; Malamis, D.; Loizidou, M. Valorisation opportunities related to wastewater and animal by-products exploitation by the greek slaughtering industry: Current status and future potentials. Waste Biomass Valorization 2015, 6, 927–945. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Category | Risk | Material |

|---|---|---|

| 1 | High risk |

|

| ||

| ||

| ||

| ||

| ||

| ||

| 2 | Medium risk |

|

| ||

| ||

| ||

| 3 | Low risk |

|

| ||

| ||

| ||

| ||

| ||

| ||

|

| Cost Category | Cost Coefficients | |||

|---|---|---|---|---|

| Units | Scenario 1 | Scenario 2 | Scenario 3 | |

| Natural gas (A) | KWh/ton ABP | 1136 | 1114 | 725 |

| Electricity (B) | KWh/ton ABP | 6.087 | 30.517 | 34.884 |

| Incinerator maintenance (1/C) | y/ton ABP | 4.35 × 10−4 | 1.49 × 10−4 | - |

| Rendering maintenance (1/D) | y/ton ABP | - | 4 × 10−4 | 4 × 10−4 |

| Ash disposal (E) | kg Ash/ton ABP | 30 | 10.26 | - |

| Labor (F) | h/ton ABP | 0.87 | 1.498 | 1.8 |

| Environmental (G) | h/ton ABP | 0.87 | 0.298 | - |

| Scenario 1 | Scenario 2 | Scenario 3 | ||||

|---|---|---|---|---|---|---|

| Cost (€/ton ABP) | (%) | Cost (€/ton ABP) | (%) | Cost (€/ton ABP) | (%) | |

| Natural gas | 56.80 | 76.7 | 55.72 | 77.2 | 37.62 | 72.6 |

| Electricity | 1.22 | 1.6 | 6.10 | 8.5 | 6.98 | 13.5 |

| Ash disposal | 12.60 | 17 | 4.31 | 6 | - | - |

| Labor | 3.48 | 4.7 | 6.00 | 8.3 | 7.20 | 13.9 |

| Total | 74.10 | 100 | 72.13 | 100 | 51.80 | 100 |

| Composting | Anaerobic Digestion | Scenario 1 Incineration | Scenario 2 Rendering and Incineration | Scenario 3 Rendering | |

|---|---|---|---|---|---|

| Energy consumption (MJ/ton ABP) | 250 [15] | 600 [15] | 4111 | 4118 | 2736 |

| Cost (€/ton ABP) | 30 [24] | 63 [28] | 74.1 | 72.13 | 51.8 |

| Profit (€/ton ABP) | 30 [15] | 68 [15] | 0 | 0 | 270 [15] |

| Net profit (€/ton ABP) | 0 | 5 | −74.1 | −72.13 | 218.2 |

| Retention time (d) | 50 [37] | 40 [37] | <1 | <1 | <1 |

| Normalized | |||||

| Environmental score | 1.00 | 0.91 | 0.00 | 0.00 | 0.36 |

| Economic score | 0.25 | 0.27 | 0.00 | 0.01 | 1.00 |

| Technological score | 0.00 | 0.20 | 1.00 | 1.00 | 1.00 |

| AHP score (%) | 53.9 | 54.9 | 10.1 | 10.3 | 72.4 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zagklis, D.; Konstantinidou, E.; Zafiri, C.; Kornaros, M. Assessing the Economic Viability of an Animal Byproduct Rendering Plant: Case Study of a Slaughterhouse in Greece. Sustainability 2020, 12, 5870. https://0-doi-org.brum.beds.ac.uk/10.3390/su12145870

Zagklis D, Konstantinidou E, Zafiri C, Kornaros M. Assessing the Economic Viability of an Animal Byproduct Rendering Plant: Case Study of a Slaughterhouse in Greece. Sustainability. 2020; 12(14):5870. https://0-doi-org.brum.beds.ac.uk/10.3390/su12145870

Chicago/Turabian StyleZagklis, Dimitris, Eva Konstantinidou, Constantina Zafiri, and Michael Kornaros. 2020. "Assessing the Economic Viability of an Animal Byproduct Rendering Plant: Case Study of a Slaughterhouse in Greece" Sustainability 12, no. 14: 5870. https://0-doi-org.brum.beds.ac.uk/10.3390/su12145870