Adoption and Implementation of Sustainable Development Goals (SDGs) in China—Agenda 2030

, and

, and

Abstract

:1. Introduction

2. Theoretical Background, Research Questions and Literature Review

2.1. Theoretical Background and Research Questions

2.2. Literature Review: Sustainable Development Goals (SDGs) Reporting

2.3. Sustainable Development Goals (SDGs) Agenda 2030

3. Materials and Methods

3.1. Sample and Data Collection

3.2. Research Method

4. Results

5. Conclusions, Policy Implications, and Future Research

Author Contributions

Funding

Conflicts of Interest

References

- Tao, M.; Chen, L.; Su, L.; Tao, J. Satellite observation of regional haze pollution over the North China Plain. J. Geophys. Res. Space Phys. 2012, 117, 117. [Google Scholar] [CrossRef]

- Vo, X.V. Do foreign investors improve stock price informativeness in emerging equity markets? Evidence from Vietnam. Res. Int. Bus. Finance 2017, 42, 986–991. [Google Scholar] [CrossRef]

- Li, L.; Xia, X.; Chen, B.; Sun, L. Public participation in achieving sustainable development goals in China: Evidence from the practice of air pollution control. J. Clean. Prod. 2018, 201, 499–506. [Google Scholar] [CrossRef]

- Vo, X.V. Trading of foreign investors and stock returns in an emerging market-Evidence from Vietnam. Int. Rev. Financ. Anal. 2017, 52, 88–93. [Google Scholar] [CrossRef]

- Allen, F.; Qian, J.; Qian, M. Law, finance, and economic growth in China. J. Financ. Econ. 2005, 77, 57–116. [Google Scholar] [CrossRef] [Green Version]

- Ye, J.; Fues, T. A Strong Voice for Global Sustainable Development: How China can Play a Leading Role in the Post-2015 Agenda. RePEc 2014, 2, 11–22. [Google Scholar]

- Rosati, F.; Faria, L.G. Addressing the SDGs in sustainability reports: The relationship with institutional factors. J. Clean. Prod. 2019, 215, 1312–1326. [Google Scholar] [CrossRef]

- Scott, L.; McGill, A. From Promise to Reality: Does Business Really Care about the SDGs; PriceWaterhouseCoopers: London, UK, 2018. [Google Scholar]

- Courtis, J.K. Expanding the future financial corporate reporting package. Account. Forum 2000, 24, 248–263. [Google Scholar] [CrossRef]

- Griggs, D.; Nilsson, M.; Stevance, A.; McCollum, D. A Guide to SDG Interactions: From Science to Implementation; International Council for Science: Paris, France, 2017. [Google Scholar]

- Deegan, C. Introduction: The legitimising effect of social and environmental disclosures—A theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Campbell, D.; Craven, B.; Shrives, P. Voluntary social reporting in three FTSE sectors: A comment on perception and legitimacy. Account. Audit. Account. J. 2003, 16, 558–581. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Vo, X.V. Bank lending behavior in emerging markets. Financ. Res. Lett. 2018, 27, 129–134. [Google Scholar] [CrossRef]

- Oliver, C. Determinants of interorganizational relationships: Integration and future directions. Acad. Manag. Rev. 1990, 15, 241–265. [Google Scholar] [CrossRef]

- Ntim, C.G.; Soobaroyen, T. Corporate Governance and Performance in Socially Responsible Corporations: New Empirical Insights from a Neo-Institutional Framework. Corp. Gov. Int. Rev. 2013, 21, 468–494. [Google Scholar] [CrossRef]

- Kolk, A.; Perego, P. Determinants of the adoption of sustainability assurance statements: An international investigation. Bus. Strat. Environ. 2008, 19, 182–198. [Google Scholar] [CrossRef] [Green Version]

- Kuhn, B. Sustainable Development Discourses in China. J. Sustain. Dev. 2016, 9, 158. [Google Scholar] [CrossRef]

- Wang, B.; Lyv, M.; Xing, J.; Zhou, Q.; Ding, M.; Shen, Y. Climate Change in the Chinese Mind: Survey Report 2017; China Center for Climate Change Communication: Beijing, China, 2017. [Google Scholar]

- Cohen, M. A systematic review of urban sustainability assessment literature. Sustainability 2017, 9, 2048. [Google Scholar] [CrossRef] [Green Version]

- Borys, T. Zrównoważony rozwój–jak rozpoznać ład zintegrowany. Probl. Ekorozw. 2011, 6, 75–81. [Google Scholar]

- Vasconcellos Oliveira, R. Back to the Future: The potential of intergenerational justice for the achievement of the sustainable development goals. Sustainability 2018, 10, 427. [Google Scholar] [CrossRef] [Green Version]

- UN. UN Documents: Gathering a Body of Global Agreements; UN: New York, NY, USA, 2016. [Google Scholar]

- UN. Agenda 21: Programme of Action for Sustainable Development Rio Declaration on Enviroment and Development Statement of Forest Principles the Final Text. In Proceedings of the Agreements Negotiated by Governments at the United Nations Conference on Environment and Development (UNCED), Rio de Janeiro, Brazil, 3–14 June 1992. [Google Scholar]

- Division, U.N.S. Millennium Development Goals Indicators: The Official United Nations Site for the MDG Indicators; UNSD: New York, NY, USA, 2008. [Google Scholar]

- Smith, R.J. A social worker’s report from the United Nations Conference on Sustainable Development (Rio+ 20). Soc. Work 2013, 58, 369–372. [Google Scholar] [CrossRef] [Green Version]

- Assembly, G. United Nations: Transforming Our World: The 2030 Agenda for Sustainable Development; UN: New York, NY, USA, 2015. [Google Scholar]

- Raszkowski, A. The strategy of local development as a component of creative human capital development process. Pr. Nauk. Uniw. Ekon. We Wrocławiu 2015, 394, 135–143. [Google Scholar] [CrossRef]

- Judson, G. Engaging Imagination in Environmental Education: Practical Strategies for Teachers; University of British Columbia Press: Vancouver, BC, Canada, 2017. [Google Scholar]

- Caputo, F.; Veltri, S.; Venturelli, A. A Conceptual Model of Forces Driving the Introduction of a Sustainability Report in SMEs: Evidence from a Case Study. Int. Bus. Res. 2017, 10, 39. [Google Scholar] [CrossRef] [Green Version]

- Baumgartner, R.J.; Korhonen, J. Strategic thinking for sustainable development. Sustain. Dev. 2010, 18, 71–75. [Google Scholar] [CrossRef]

- Röller, L.-H.; Waverman, L. Telecommunications Infrastructure and Economic Development: A Simultaneous Approach. Am. Econ. Rev. 2001, 91, 909–923. [Google Scholar] [CrossRef] [Green Version]

- Yigitcanlar, T.; Dur, F. Developing a Sustainability Assessment Model: The Sustainable Infrastructure, Land-Use, Environment and Transport Model. Sustainability 2010, 2, 321–340. [Google Scholar] [CrossRef] [Green Version]

- Bulkeley, H.; Betsill, M. Rethinking Sustainable Cities: Multilevel Governance and the ’Urban’ Politics of Climate Change. Environ. Politi. 2005, 14, 42–63. [Google Scholar] [CrossRef]

- Plum, A.; Kaljee, L. Achieving Sustainable, Community-Based Health in Detroit Through Adaptation of the UNSDGs. Ann. Glob. Health 2017, 82, 981–990. [Google Scholar] [CrossRef]

- Sharifi, A.; Yamagata, Y. On the suitability of assessment tools for guiding communities towards disaster resilience. Int. J. Disaster Risk Reduct. 2016, 18, 115–124. [Google Scholar] [CrossRef] [Green Version]

- Mariño, R.; Banga, R.S. UN Sustainable Development Goals (SDGs): A time to act. J. Oral Res. 2016, 5, 5–6. [Google Scholar] [CrossRef] [Green Version]

- Northrop, E.; Hana, B.; Sylvia, L.; Mathilde, B.; Ranping, S. Examining the Alignment between the Intended Nationally Determined Contributions and Sustainable Development Goals; World Resources Institute: Washington, DC, USA, 2016. [Google Scholar]

- Ali, S.; Huda, M. Constructive Consumption: Bridging Livelihoods and Conservation in Democratic Societies. In CSR, Sustainability and Leadership; Gabriel, E., Ralph, B., Eds.; Routledge: Abington, UK, 2016. [Google Scholar]

- Kosgey, H.S. Green Energy Strategies And United Nations Sustainable Development Goal Onaffordable Clean Energy At Kenya Electricity Generating Company Limited. IJRISS 2017, 3, 1. [Google Scholar]

- UN. Sustainable Development Goals. Available online: https://sustainabledevelopment.un.org/ (accessed on 25 September 2017).

- Gnanapragasam, A.; Cole, C.; Singh, J.; Cooper, T. Consumer Perspectives on Longevity and Reliability: A National Study of Purchasing Factors Across Eighteen Product Categories. Procedia CIRP 2018, 69, 910–915. [Google Scholar] [CrossRef]

- Knox, J.H. Linking human rights and climate change at the United Nations. Harv. Environ. Law Rev. 2009, 33, 477. [Google Scholar]

- Griggs, D.; Stafford-Smith, M.; Gaffney, O.; Rockström, J.; Öhman, M.C.; Shyamsundar, P.; Steffen, W.; Glaser, G.; Kanie, N.; Noble, I. Sustainable development goals for people and planet. Nature 2013, 495, 305–307. [Google Scholar] [CrossRef] [PubMed]

- Information, UNDoP. The Millennium Development Goals Report 2005; United Nations Publications: New York, NY, USA, 2005. [Google Scholar]

- Travis, P.; Bennett, S.; Haines, A.; Pang, T.; Bhutta, Z.; A Hyder, A.; Pielemeier, N.R.; Mills, A.; Evans, T. Overcoming health-systems constraints to achieve the Millennium Development Goals. Lancet 2004, 364, 900–906. [Google Scholar] [CrossRef]

- Lusk, E.J. Cognitive aspects of annual reports: Field independence/dependence. J. Account. Res. 1973, 11, 191–202. [Google Scholar] [CrossRef]

- Healy, P.M.; Palepu, K.G. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. J. Account. Econ. 2001, 31, 405–440. [Google Scholar] [CrossRef]

- Campopiano, G.; De Massis, A. Corporate Social Responsibility Reporting: A Content Analysis in Family and Non-family Firms. J. Bus. Ethic. 2014, 129, 511–534. [Google Scholar] [CrossRef]

- Krippendorff, K. Content Analysis: An Introduction to Its Methodology; Sage publications: New York, NY, USA, 2018. [Google Scholar]

- Tagesson, T.; Blank, V.; Broberg, P.; Collin, S.-O.Y. What explains the extent and content of social and environmental disclosures on corporate websites: A study of social and environmental reporting in Swedish listed corporations. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 352–364. [Google Scholar] [CrossRef]

- Lee, K.-H.; Barker, M.; Mouasher, A. Is it even espoused? An exploratory study of commitment to sustainability as evidenced in vision, mission, and graduate attribute statements in Australian universities. J. Clean. Prod. 2013, 48, 20–28. [Google Scholar] [CrossRef]

- Ford, L. Sustainable development goals: All you need to know. Guardian 2015, 19, 13–31. [Google Scholar]

- Allen, C.; Metternicht, G.; Wiedmann, T. Initial progress in implementing the Sustainable Development Goals (SDGs): A review of evidence from countries. Sustain. Sci. 2018, 13, 1453–1467. [Google Scholar] [CrossRef]

- Citizenship, C. Advancing the Sustainable Development Goals: Business Action and Millennials’ Views; Corporate Citizenship: London, UK, 2016. [Google Scholar]

- Hajer, M.; Nilsson, M.; Raworth, K.; Bakker, P.; Berkhout, F.; De Boer, Y.; Rockström, J.; Ludwig, K.; Kok, M. Beyond Cockpit-ism: Four Insights to Enhance the Transformative Potential of the Sustainable Development Goals. Sustainability 2015, 7, 1651–1660. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

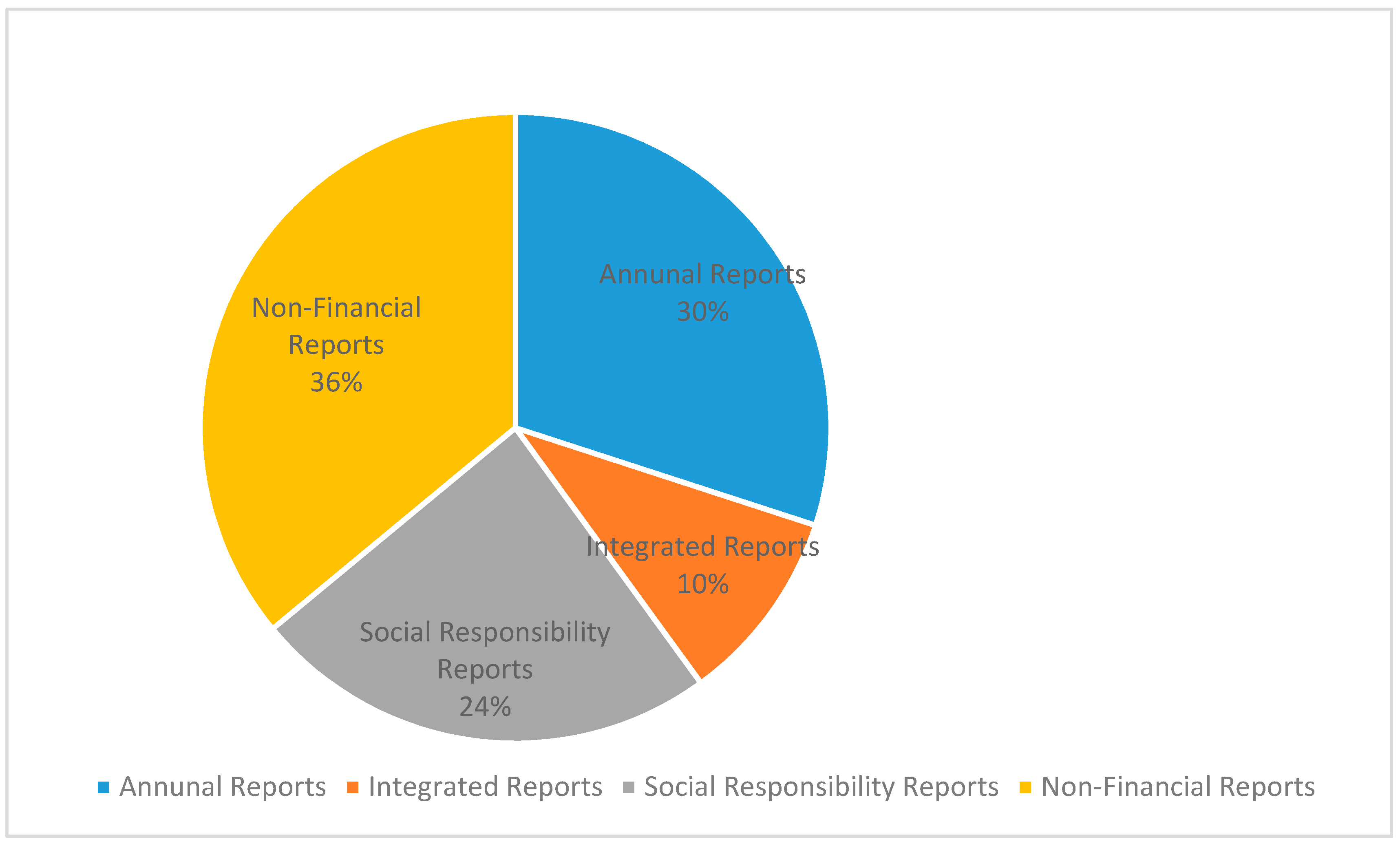

| Reports | Coding | 2016 | 2017 | 2018 | Number | Percentage (%) |

|---|---|---|---|---|---|---|

| Annual Reports | AR | 7 | 10 | 13 | 30 | 30 |

| Integrated Reports | IR | 3 | 4 | 6 | 10 | 10 |

| Social Responsibility Reports | SRR | 6 | 8 | 10 | 24 | 24 |

| Non-Financial Statements | NFS | 10 | 11 | 15 | 36 | 36 |

| Total | 100 | 100% |

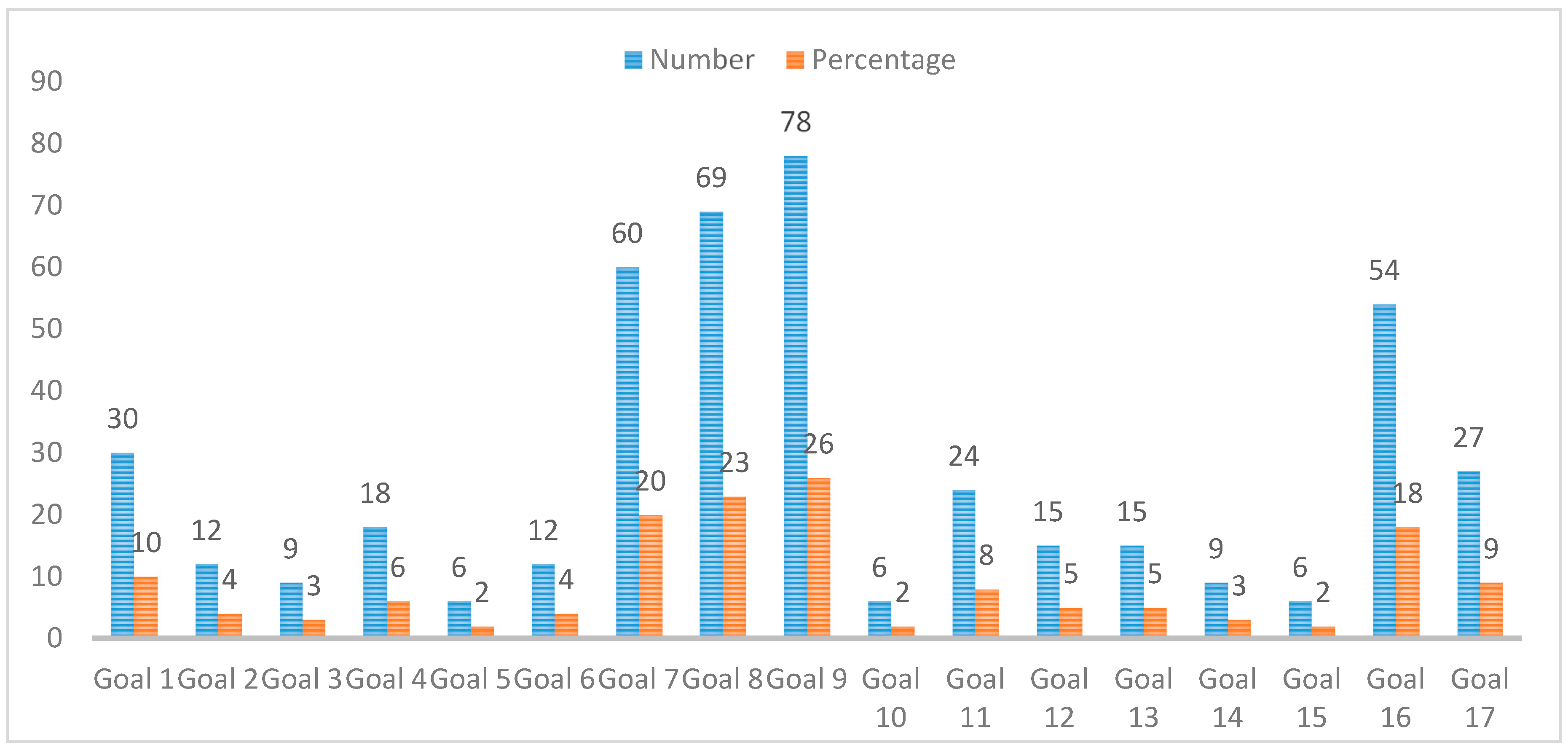

| SDGs | Number | % | Unit of Analysis | Reports for Analysis |

|---|---|---|---|---|

| G 1. No Poverty | 30 | 10 | Thematic | Annual Reports Integrated Reports Social Responsibility Reports Non-Financial Reports |

| G 2. Zero Hunger | 12 | 4 | ||

| G 3. Good health and wellbeing | 9 | 3 | ||

| G 4. Quality Education | 18 | 6 | ||

| G 5. Gender Equality | 6 | 2 | ||

| G 6. Clean water and sanitation | 12 | 4 | ||

| G 7. Affordable and clean energy | 60 | 20 | ||

| G 8. Decent work and economic growth | 69 | 23 | ||

| G 9. Industry, innovation, and infrastructure | 78 | 26 | ||

| G 10. Reduced inequalities | 6 | 2 | ||

| G 11. Sustainable cities and communities | 24 | 8 | ||

| G 12. Responsible production and consumption | 15 | 5 | ||

| G 13. Climate action | 15 | 5 | ||

| G 14. Life below water | 9 | 3 | ||

| G 15. Life on land | 6 | 2 | ||

| G 16. Peace, justice, and strong institutions | 54 | 18 | ||

| G 17. Partnership for goals | 27 | 9 | ||

| Total | 300 | 100 |

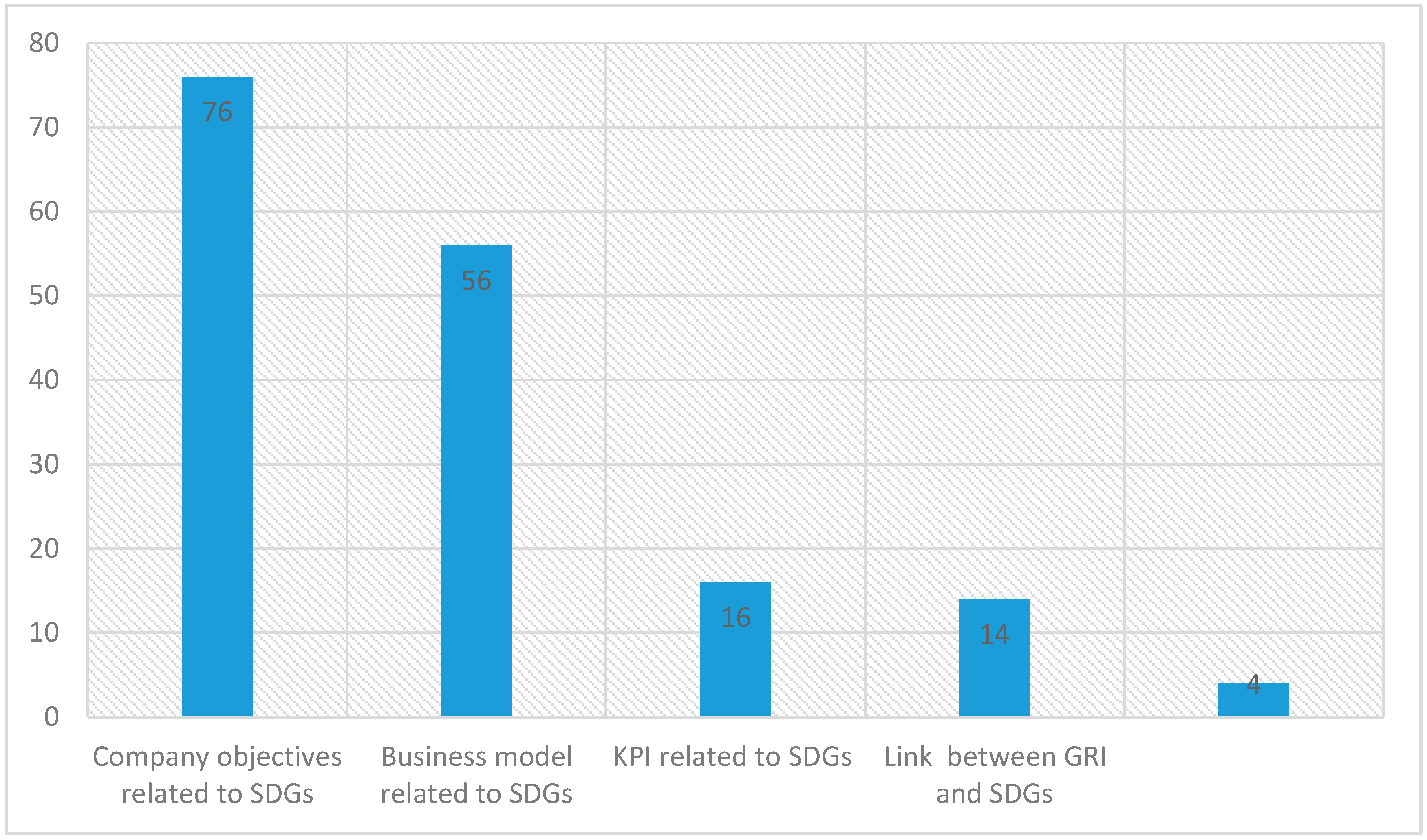

| Reports | Percentage (%) |

|---|---|

| Specific documents in reports related to SDGs | 74 |

| Company objectives related to SDGs | 56 |

| Business model related to SDGs | 16 |

| KPI related to SDGs | 14 |

| Link between GRI and SDGs | 4 |

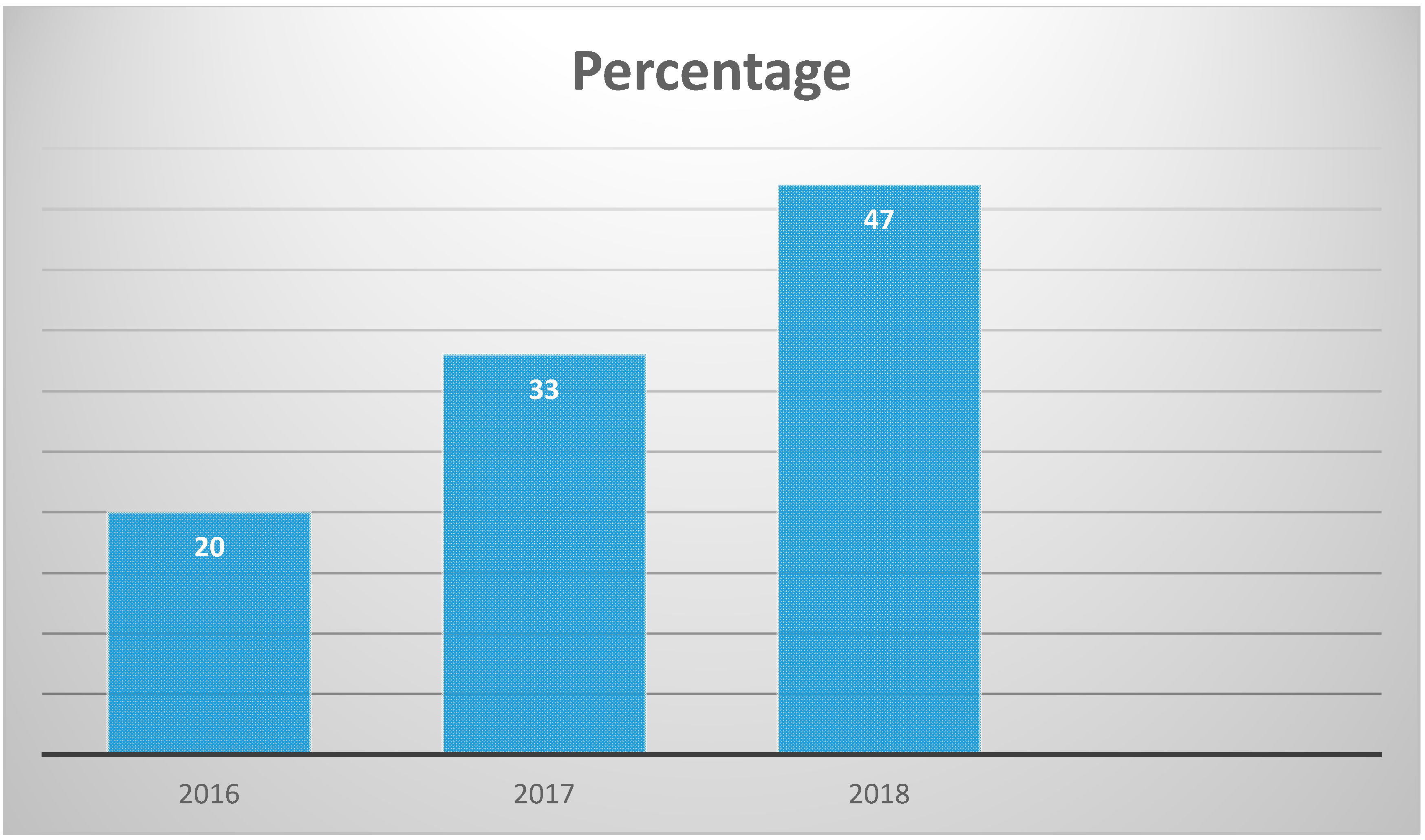

| Year | Total Number of SDGs | Percentage (%) |

|---|---|---|

| 2016 | 60 | 20 |

| 2017 | 100 | 33 |

| 2018 | 140 | 47 |

| Total | 300 | 100% |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, S.; Sial, M.S.; Tran, D.K.; Badulescu, A.; Thu, P.A.; Sehleanu, M. Adoption and Implementation of Sustainable Development Goals (SDGs) in China—Agenda 2030. Sustainability 2020, 12, 6288. https://0-doi-org.brum.beds.ac.uk/10.3390/su12156288

Yu S, Sial MS, Tran DK, Badulescu A, Thu PA, Sehleanu M. Adoption and Implementation of Sustainable Development Goals (SDGs) in China—Agenda 2030. Sustainability. 2020; 12(15):6288. https://0-doi-org.brum.beds.ac.uk/10.3390/su12156288

Chicago/Turabian StyleYu, Siming, Muhammad Safdar Sial, Dang Khoa Tran, Alina Badulescu, Phung Anh Thu, and Mariana Sehleanu. 2020. "Adoption and Implementation of Sustainable Development Goals (SDGs) in China—Agenda 2030" Sustainability 12, no. 15: 6288. https://0-doi-org.brum.beds.ac.uk/10.3390/su12156288