The Social Dimensions of Corporate Sustainability: An Integrative Framework Including COVID-19 Insights

1

College of Management, Research Institute of Business Analytics and Supply Chain Management, Shenzhen University, Shenzhen 518060, China

2

Donahue Graduate School of Business, Duquesne University, 820 Rockwell Hall, 600 Forbes Avenue, Pittsburg, PA 15282, USA

3

Applied Social Sciences Department, Community University of Chapeco Region, Chapecó 89809-900, Brazil

*

Authors to whom correspondence should be addressed.

Sustainability 2020, 12(20), 8747; https://0-doi-org.brum.beds.ac.uk/10.3390/su12208747

Submission received: 1 October 2020

/

Revised: 7 October 2020

/

Accepted: 16 October 2020

/

Published: 21 October 2020

(This article belongs to the Section Sustainable Management)

Abstract

:Corporate sustainability is considered a fundamental paradigm and solution in creating a prosperous future for organizations. However, social sustainability issues and pandemic problems from COVID-19 have affected corporations and interrupted plans for sustainable development. To date, corporate sustainability frameworks have taken a relatively narrow view of this paradigm. This study highlights serious challenges to corporate sustainability while providing a framework in an attempt to enable more sustainable business practices. To fill the gap in the literature, we have developed a framework to organize and prioritize important sustainability indicators. The first phase of the study involves the classification of 45 sub-criteria of corporate sustainability under nine main categories by using a literature review and novel Fuzzy Delphi method. The resulting categories are Corporate Governance, Product Responsibility, Transparency and Communication, Economic, Environmental, Social, Natural Environment and Climate Vulnerability, Energy Consumption along with Energy Saving, and includes Pandemic COVID-19 as a new aspect of social sustainability. Next, we applied the Fuzzy Analytical Hierarchical Process (FAHP) to help determine the weights and prioritizing the criteria and sub-criteria. The results revealed that the Pandemic, along with the Natural Environment and Climate Vulnerability, ranked higher among the main criteria category. Whereas, emergency response planning, social distances, modification of working hours, and just-in-time delivery are the most influencing sub-attributes among the 45 sub-barriers of different categories. Contributions of this study include new insights regarding corporate sustainability criteria and subcriteria, application of novel methods, and integrated framework for dimensions of corporate sustainability. This study is among the first of its kind to consider the COVID-19 pandemic as an essential category and social sustainability attribute of corporate sustainable business practices. Outcomes of this study can help assist scholars, corporations, and decision-makers in understanding sustainable development initiatives while simultaneously improving social sustainability practices.

1. Introduction

Sustainable development is the potential to fulfill today’s needs without undermining a future generation’s ability to satisfy their needs [1]. Sustainability has become a significant alternative to business as usual, which appears to focus primarily on short-term productivity with little or no social and environmental impacts considered over the long term [2]. Despite this, the business environment is changing rapidly, guided by social, economic, and ecological developments [3,4]. For these and other aligned reasons, companies have become increasingly interested in corporate sustainability; see, for example, Christ et al. [5] and Manrique and Martí-Ballester [6]. While managers have noticed that the integration of sustainability is an opportunity, they rarely consider it in tactical management decisions [7]. The consideration of sustainability in corporate strategy and processes has become one promising way of dealing with a changing business landscape and increasing pressure for social sustainability performance. Since decisions relating to sustainability are made at a strategic level, there has also been an increasing scientific interest in the field of strategic management in connection with the inclusion of sustainability in the strategy, vision, change management, and culture of a company [8].

Due to the variety of different sustainability initiatives, there is an ongoing opportunity for researchers to quantify what ongoing and emerging practices look like [9]. Yet, there has been so much published by researchers that it can be an overwhelming amount of information to sort through. Add to this, the idea that stakeholders are continually seeking more information beyond financial performance by wanting to see the ecological and social policies of a company [10], and the importance of understanding corporate sustainability, continue to grow. Corporate sustainability reporting can be a primary motivation for organizations to communicate with stakeholders about sustainability initiatives. This gets difficult due to the terminology and growing categories of these diverse efforts. For example, firms have been reporting the use of different terminologies, e.g., corporate social responsibility (CSR), sustainable development (SD), economic and non-economic reporting, and referring to the main pillars of sustainability which are social, environmental, and economic (SEE), and triple bottom line (TBL). The evolution of such reporting is fascinating. Tschopp and Huefner [11] found that the companies were focusing on environmental management compliance reporting during the 1970s and 1980s, and they also observed a weak relation between sustainability reporting and organization performance. Later, in the 1990s, sustainability reporting on occupational health and safety (OHS) was observed, and a paradigm shift to reporting on societal-based activities, accompanied by institutionalization.

Considering that each participant in society has its unique responsibility to engage sustainable development at a global scale, corporate sustainability reflects the organizations’ part to global challenges of sustainable development [12], including depletion of natural resources and social sustainability. There are several challenges regarding corporate sustainability, such as the need for considering both external and internal stakeholders in corporate decisions [13]; to resolve discrepancies, contradictions, and synergies among the three pillars of TBL sustainability [14]; to promote an approach to corporate sustainability based in moral-values [15]; to foster corporate social responsibility across the business life-cycle thinking [16]. Add to this, the several contributions available in the literature from different epistemological fields connected with environmental, economic, and social performance, and it seems evident that there is an absence of coordination among them. Diouf et al. [17] emphasized the growing significance of sustainability reporting and the use of international regulations, targets for reducing carbon emissions, and international standards and guidelines. Arribas et al. [18] investigated that the inclusion of irresponsible companies in the Dow Jones Sustainability Index (DJSI) from S&P Dow Jones Indices, and Social Accountability (SA8000) from Social Accountability International—SAI (2008) is a fact.

Those who manage business decisions face multiple criteria for achieving the best practices while trying to achieve multiple goals. Decisions regarding sustainable business practices have multi-level characteristics as TBL dimensions can be broken down into hierarchical variables [19]. One primary objective of this study is to help researchers and practitioners identify essential corporate sustainability criteria. Therefore, Multi-Criteria Decision Analysis (MCDA) is recommended for simultaneously addressing decisions with multiple objectives and multiple criteria. Multi-criteria decision theory helps to orchestrate the various awareness of practices involving sustainability [20] and to help when making decisions regarding dynamic topics. Multi-stakeholder, multi-objective, and multi-level frameworks have been developed and utilized in the literature to assess corporate sustainability results but, so far, the initiatives have not provided a consistent, single measure capturing the TBL’s complexities and integrating the MCDA. Therefore, the second objective of this study is to provide a methodology to help organize and understand this dynamic context for sustainable business practices.

Add to this dynamic context, a global pandemic and things can get interesting. Due to the pandemic COVID-19 outbreak, the modern world is suffering a global economic crisis with well over 9 million cases, and over 501,000 fatalities as of September 2020 affecting more than 200 countries [21]. Many businesses have shut down, and the rate of unemployment has increased. According to the World Health Organization, COVID-19 has become an unparalleled global crisis and is challenging organizations, which ultimately can have a negative effect on corporate sustainability and business practices [22]. Until now, corporations have not had to plan for a pandemic. Moreover, corporate sustainability has been marginalized due to organizations, governments, and society struggling to survive in times of a pandemic. Researchers have stated that the COVID-19 pandemic is opening new challenges for corporate sustainability, mainly because supply chains and their manufacturers are facing the pandemic’s negative effects, such as market downturn, SMEs bankruptcy, employees’ resignations, revenue loss, to name a few. Therefore, we see the post-COVID-19 era as an opportunity by which organizations can rethink their sustainable business practices concerning a shift in their manufacturing, supply chain, and sustainability strategies. Here we find the third objective for this study to extend our understanding of corporate sustainability by also exploring the more recent impacts of the pandemic.

Researchers, policymakers, and decision-makers are now more concerned about how to make corporations more sustainable. This study is an attempt to help decision-makers and researchers by developing a framework for corporations regarding social sustainability dimensions that include COVID-19 as a new attribute of sustainable business practices. Many aspects of corporate sustainability can be measured to calculate the company’s sustainability efficiency. In this study of corporate sustainability, we assess this paradigm using (i) Governance; (ii) Product Responsibility; (iii) Transparency and Communication; (iv) Economic; (v) Environmental; (vi) Social; (vii) Natural Environment and Climate Vulnerability (viii) Energy Consumption and Saving, and a new criterion, (ix) Pandemic COVID-19. These nine aspects are further divided into forty-five sub-criteria. In doing so, one contribution of this study is the addition of values for these major criteria and sub-criteria as we attempt to fill a gap in the corporate sustainability literature. As a partial response to the recent and growing call for understanding the pandemic COVID-19 effects on businesses, the authors conducted this research aiming to contribute to the growing literature on the topic by developing a multidimensional framework for corporate sustainability. Further, this study prioritizes the main and sub-attributes of an emerging sustainability model by being among the first to use MCDA techniques.

To help start us down a path to understanding this dynamic context for corporate sustainability, fundamental factors can be identified from the literature and further classified as a foundation for understanding corporate sustainability. In this study, we draw from the literature to develop lists of main and sub-attributes essential for developing corporate sustainability business practices. Building on our objectives for this study, our primary research questions include, but are not limited, to what are the most influenceable metrics for corporate sustainability? And how can they be evaluated and ranked in a way that provide value to practitioners and scholars? After reviewing the literature, conceptual models, our research framework, and applying a Fuzzy Delphi method, we assess nine sustainability criteria and forty-five sub-criteria. We review our methods for employing the Fuzzy Analytical Hierarchical Process (FAHP) for calculations of weights for both the sub-criteria using a matrix of pairwise comparisons. Results are then discussed, and the last section provides main conclusions, contributions to the field, and avenues for aspects of corporate sustainability, social sustainability, and sustainable development for future researches.

2. Literature Review

The definitions of sustainability have many interpretations, such as environmental protection, ecosystem resources, economic concerns, social acceptance, licensing and externalities, and many other perspectives. The recent literature shows that sustainable development is going beyond “green” to a more comprehensive, systematic, methodological, and integrated understanding of sustainability. Researchers and decision-makers are aware of the need for systematic sustainability assessments to evaluate complex systems to replace traditional and unsustainable business practices. Such assessments ultimately concentrate on historical strategies for sustainability, demonstrating the need to improve corporate sustainability programs over time, along with allocating resources that reduce sustainability risks. Further, organizations need to combine efficiency and market performance initiatives to develop strategic corporate sustainability opportunities [23].

Asif at el. [24], conceptualized the integration of economic, social, and environmental bottom lines dimension by using a triple bottom line. This view of a corporation means that the efficiency and sustainability aspects of the integrated structure are matched together. Several models have been proposed to develop corporate sustainability in efforts to make it accessible, practical, and quantifiable. The wide range of sustainability frameworks is because of the variety of definitions of sustainable development, i.e. ecological sustainability, environmental efficiency, corporate citizenship, and TBL. In prior studies, one dimension of corporate sustainability is evaluated to define, measure, and sometimes test constructs and relationships. For instance, environmental sustainability frameworks concentrate on environmental issues by providing metrics for mitigating pollution, climate vulnerability, environmental degradation, land use, and loss of biodiversity [25]. Social sustainability models focus on societal and ethical facets of corporate sustainability, such as infrastructure, community welfare, human rights, health, equity, and education [26]. Further, economic sustainability involves the economic structure of organizations and concentrates on businesses seeking to optimize the company’s resources through social and environmental strategies [27]. Some studies proposed the two-dimensional sustainability frameworks in which two or more dimensions of corporate sustainability (such as environmental and social dimensions evaluated by providing sustainability indices and MCDA approaches). The fundamental model of corporate sustainability is shown in Figure 1.

Concerns regarding the social and environmental effects of sustainability must be weighted, but economic viability should not be threatened. The company’s financial performance can be affected and impacts its risk of survival if it fails to give due attention to its economic performance [28]. Longoni and Cagliano [29] argued that managing and balancing TBL performance is paramount. The authors acknowledge the difficulties of doing this while also trying to understand any negative tradeoffs between the three sustainability dimensions.

The International Organization of Standardization (ISO) and the Global Reporting Initiative (GRI) systems assist companies in integrating sustainable development and TBL performance. GRI measures and reports the “material” performance of companies and its business activities and its effectiveness in multiple dimensions, i.e., three folds result to the public, most of the time through sustainability reports [30]. Several sustainability indices have been developed to highlight sustainability activities so that investors can consider the sustainable performance of enterprises. By analyzing the sustainability practices by each corporation, the sustainability indices act as a knowledge intermediary of companies with their different players (including business specialists, shareholders, and financial intermediaries). Specialized data accessed by neutral parties are seen by these intermediaries as objective. Conventional definitions of sustainability suggest that the businesses are supposed to be listed only if they are more socially and environmentally responsible than their competitors within these stock indexes. Sustainability stock indexes can, therefore, be treated as suitable sustainability performance indicators. Weber [31] suggests sustainability guidance that describes the most relevant performance metrics and issues in six banking industries. They showed specific important issues are shared by many industries, particularly social sustainability aspects, whereas others are unique in a sector.

Several researchers have used MCDA methods to measure the company’s sustainability performance. A list of different MCDA approaches used to develop a sustainability framework is shown in Table 1.

Previously, before the COVID-19 pandemic, organizations, governments, and society were dealing with and focusing on environmental issues. It is believed that, after the COVID-19 pandemic, business transitions will increase in order to achieve a more sustainable corporate sustainability. This transition will allow organizations to develop flexible manufacturing systems, prioritizing environmental, economic, and social sustainability. Regarding decision support systems for resilient production, there are various options available, such as those proposed by Tan et al. [52] and the prediction model for supply chains of Ivanov et al. [53]. Thus, companies and supply chains need to be resilient to tackle tough times, such as what occurs during the current pandemic.

As expected, the economic crisis that followed the COVID-19 epidemic affected several businesses, from manufacturers to service providers due to the social distancing and lockdowns [54]. Thus, the businesses in which customers interact with each other were immediately stopped [55,56]. To avoid bankruptcy, these businesses moved to palliative solutions aiming for their survival, mainly migrating the businesses to digital platforms [57].

The epidemic effects on delivery delays are affecting supply chains, causing bullwhip effects, and unbalancing organizations’ performances in almost all industries. Thus, companies are focusing on essential items for manufacturing and maintaining supply activities regarding the unexpected disruptions. At the same time, these organizations are planning how to restart the businesses close to the ‘new normal’, as society is returning to (a semi) normality.

The main justification for considering the COVID-19 pandemic effects in corporate sustainability, within this study, is that its consequences will be felt for decades [58]. Thus, as a long-lasting event, it is assumed that the COVID-19 pandemic will affect organizations regarding their sustainability actions in the future.

We considered various decision attributes and indicators for the development of a multidimensional sustainability framework. These attributes can assist in the construction of an effective corporate sustainability model while also providing insights into sustainable business practices. This study develops a decision criterion for sustainable development based on the literature and then checked the criteria validity provided by key expert’s contributions. The main sustainability criteria in our development of a sustainability framework include Corporate Governance, Product Responsibility, Transparency and Communication, Economics, Social, Environmental, Natural Environmental and Climate Change, Energy Saving and Consumption, and what we believe to be used for the first time, the COVID-19 pandemic criteria. As per the best of the authors’ knowledge, pandemic impacts have not been used before in sustainability models to date, the consideration of COVID-19 pandemic effects will help to fulfill a gap in the literature.

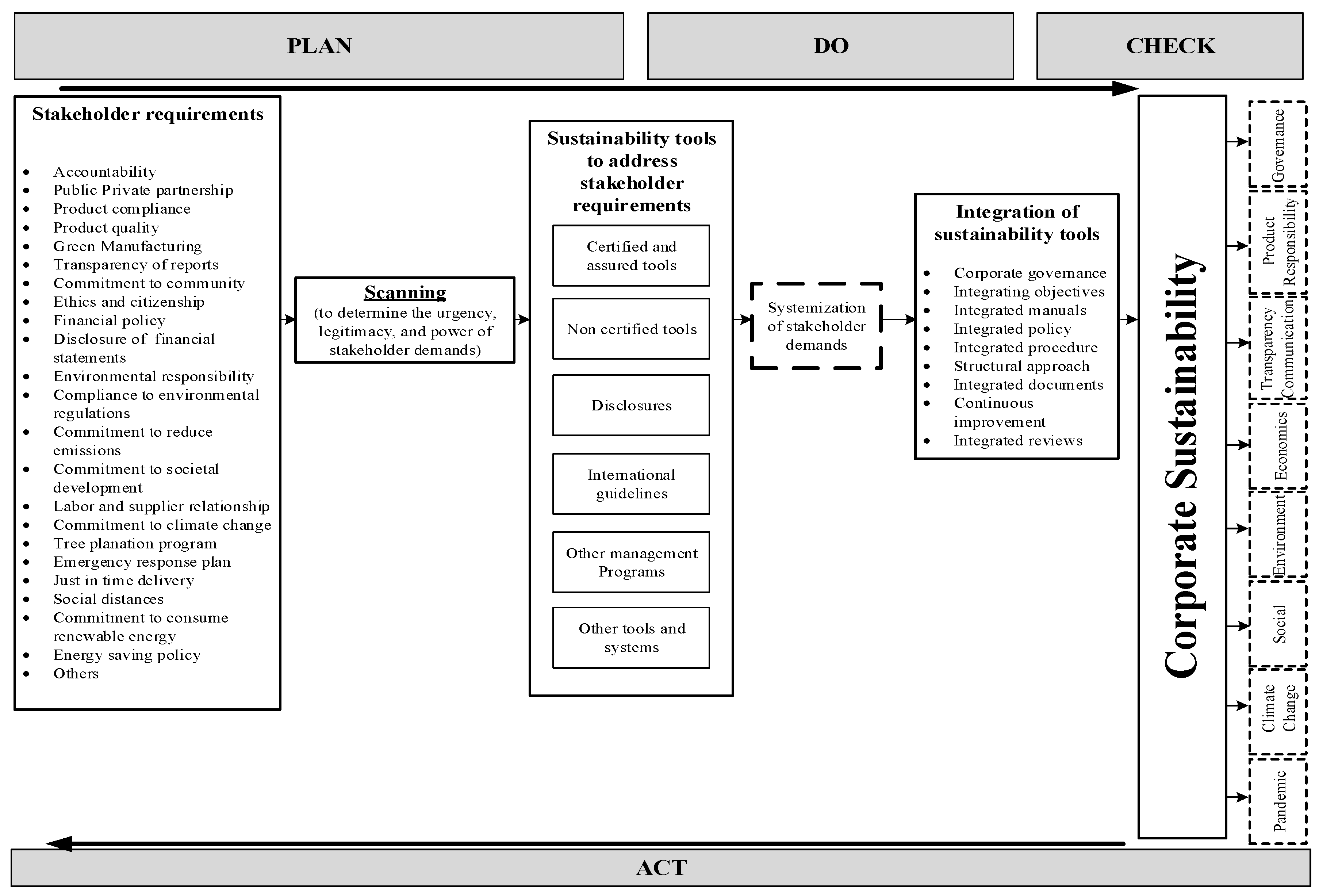

Each of these sustainability criteria has a total of forty-five sub-criteria. These criteria were identified after reviewing and summarizing the literature. The results of which criteria and sub-criteria are shown in Table 2. Next, we attempt to extend the corporate sustainability model based on the ‘Plan, Do, Check, and Act’ (PDCA) approach, as presented in Figure 2.

3. Research Framework

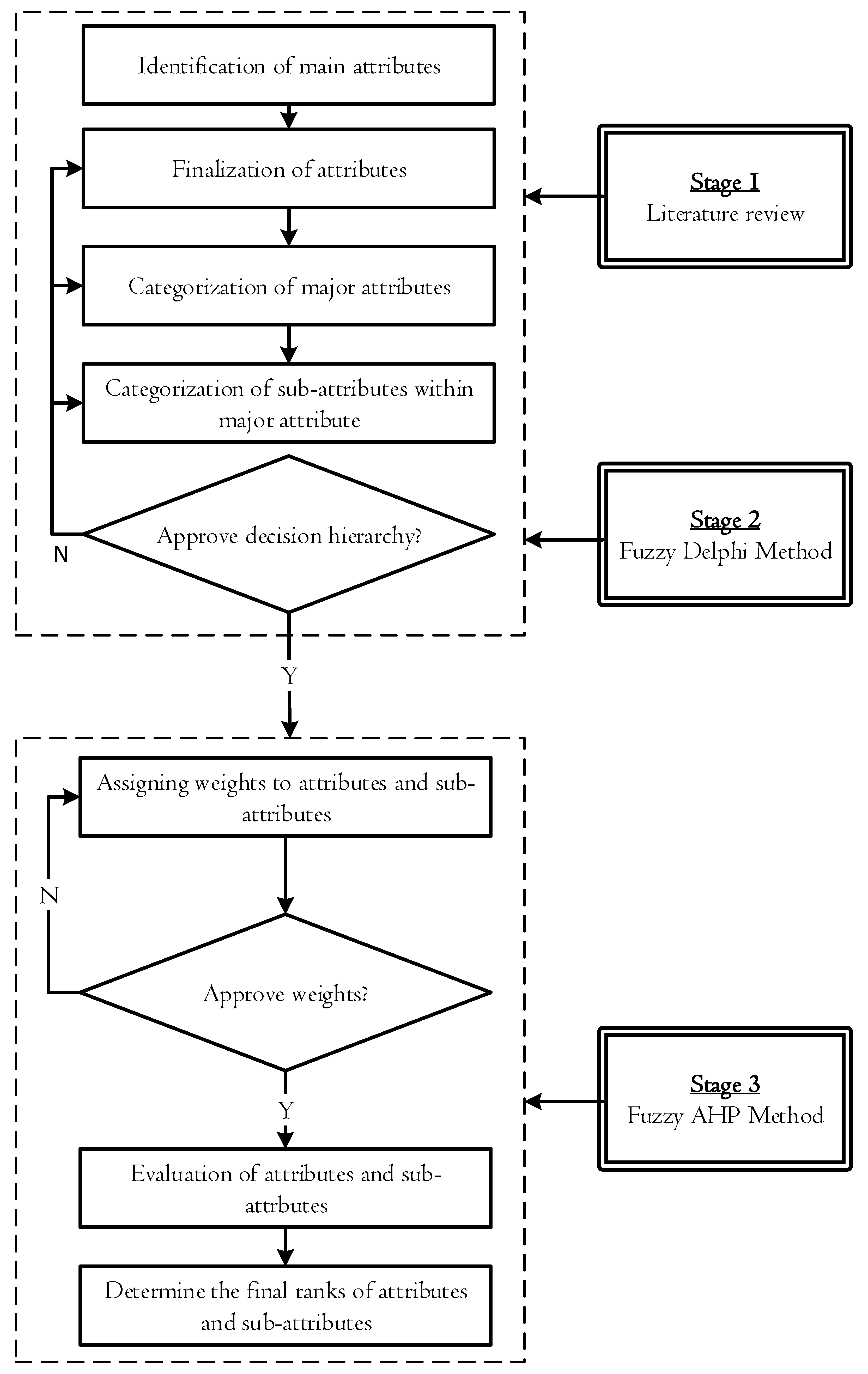

We have used the Fuzzy Delphi, and FAHP approaches to finalize and prioritize the most important criteria and select sustainability options for the development of corporate sustainability. The framework operationalized in this study is shown in Figure 3. Fuzzy Delphi proposed by Hsu et al. [88] has been adopted in this study to finalize corporate sustainability criteria. The advantage of Fuzzy Delphi over the conventional Delphi method is that the latter is a lengthy process of obtaining a consensus on experts’ opinions. The expert’s opinion in the conventional Delphi method often suffers from low convergence, which ultimately complicates consensus-building. The experts are therefore consulted repeatedly to reform their feedback so that a possible consensus can be reached. On the other hand, Fuzzy Delphi can obtain experts’ consensus through only one round of investigation [89]. The Fuzzy Delphi uses membership functions to characterize the experts’ feedback. In this way, experts are not consulted twice to alter their opinions, which also saves useful information from being lost as all the experts’ opinions are taken while computing the membership degrees.

Regarding the development of the fuzzy membership degrees, most of the previous studies used a Triangular Fuzzy Number (TFN), Gaussian fuzzy number, and trapezoidal fuzzy number [88]. This study employs TFNs, to construct the membership degree function. To find the converging point of the decision group, TFNs were solved using the geometric mean following previous studies such as [90,91]. In taking this approach, a FAHP methodology was used for computing the weights of the main and sub-attributes of corporate sustainability, supported by decision-makers, using a pairwise comparison matrix. To carry out the analysis, eight academic and industrial experts were involved whose detail is provided in Appendix A (see Table A1).

Fuzzy Analytical Hierarchy Process

The Analytical Hierarchy Process (AHP) is a well-known and adaptable Multi-Criteria Decision Analysis (MCDA) approach to solve complex problems used across a variety of fields of research. The logic of AHP is based on a ratio scale to quantify the different sets of alternatives priorities provided by decision-makers [92]. This approach evaluates the consistency and importance of the decision-makers’ instinctive opinions to provide an optimal solution for complex problems. Researchers have integrated the AHP approach with other methods, such as grey system theory, data analysis envelopment, fuzzy system theory, and even linear programming [93].

Although AHP methods have shown satisfactory results and can be used to evaluate decision-makers’ opinions, this technique has some deficiencies in terms of human behavior and thinking approach. Hence, the traditional method has some limitations, such as (i) handling with the inconsistent and unbalanced expert opinion scale, (ii) unable to handle the uncertain and ambiguous relationship with expert’s judgment numbers, (iii) imprecise results, and (iv) decision-makers’ subjective opinion preferences.

Due to these limitations, AHP has evolved into FAHP, as a widely used and more accurate approach over conventional methods to solve uncertain and complex problems involving a decision-maker’s judgment. FAHP is the combination of traditional AHP and Fuzzy set theory, where the membership of each element is represented by a function. Further, each element of the membership function is divided into the membership’s degree with a value between 0 and 1, which implies that any membership’s element has a value of “1”. Conversely, any element has no membership with a “0” value. Those elements which lie between “0 and 1” have a partial or incomplete degree of membership [94]. To effectively handle the uncertainties during the logistic estimation process, there is a need to convert the linguistic term of membership function into ‘fuzzy numbers’, meanwhile, in FAHP, linguistic values are shown as a TFN.

To develop corporate sustainability for the purposes of this study, FAHP was applied to estimate weights of criteria and sub-criteria in the six following steps:

- Step I.

- Designing the problem structure using a hierarchical approach

- Step II.

- Constructing of pairwise comparison matrix and developing the scale of the relative importance

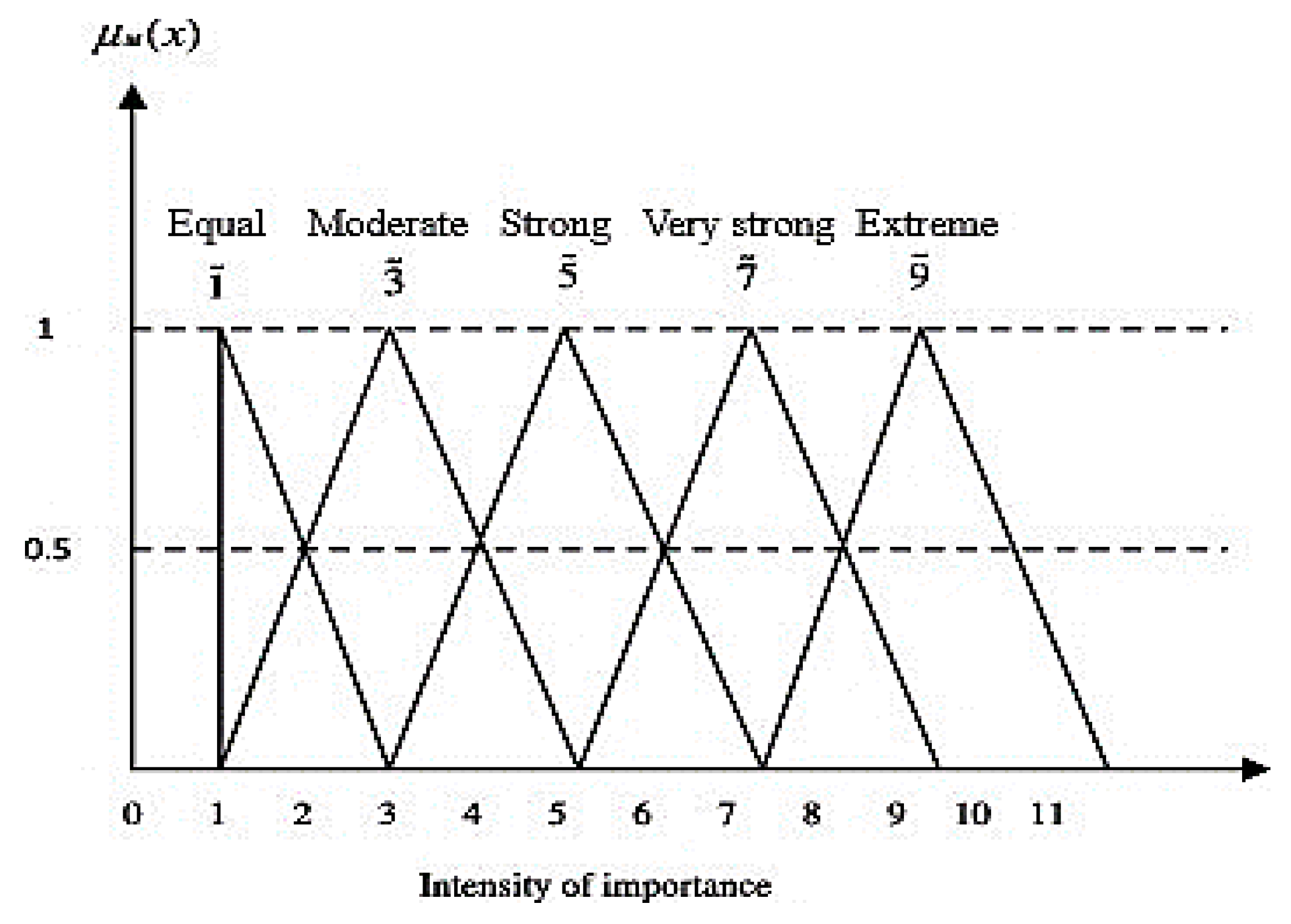

After designing the problem structure in a hierarchical way, the next step is to define the scale of relative importance in order to construct a pairwise comparison matrix. Table 3 presents the TFN, which are from 1 to 9, and are used to improve the accuracy of the traditional model. We employed five TFNs relative to correspondence number for expert qualitative assessment in order to capture the vagueness and remove uncertainties. The fuzzy membership for attributes and sub-attributes is shown in Figure 4.

- Step III.

- Constructing a fuzzy-based matrix for comparison purposes

Experts used the TFNs to elaborate pairwise comparisons of corporate sustainability main and sub-attributes. The fuzzy comparison matrix X was drawn from the expert’s opinions by using the arithmetic mean function for pairwise comparison, as presented in Equation (1).

where , if , and or if . To calculates the scores for a pair, a reverse comparison was applied in the matrix for giving a reciprocal score.

Supposing that if indicates the value of a matrix which is allocated to the combination of components and , then .

- Step IV.

- Developing the crisp comparison matrix

To make the expert and decision-makers judgments more confident, the α-cut method can be used through the ranking of fuzzy numbers, in which it provides an interval of values based on fuzzy numbers. Figure 5 presented the α-cut method on TFN for this instance, if will yield .

Based on the fuzzy comparison matrix, while the optimism index is considered on a fixed value of and consider to the degree of satisfaction in order to obtain α-cut comparison matrix, then:

The value of index optimism is provided by experts based on the satisfaction degree in the preference matrix. Then, the higher the degree of optimism influenced, the larger the value of . Lee et al. [96] introduced the optimism index denoted by ‘’ which is linear convex as given in the below equation.

Inserting the value of in Equation (3) at this step, the comparison of the α-cut fuzzy matrix is converted into crisp comparison matrix as follows.

- Step V.

- Consistency check

The last step explains the consistency of each matrix by using a consistency ratio (CR), and an overall consistency of hierarchy is calculated as well. Meanwhile, the conversion of crisp comparison matrix present by letter into a consistent fuzzy comparison matrix .

The calculation formula of the largest Eigenvalue is presented in Equation (5).

In this equation, represents the principle Eigenvector of the matrix in the above equation.

Equation (5) involves the CR calculation formula through expert pairwise.

where presents the index of consistency, whereas the random index is indicated by , and is the size of the matrix, as presented in Table 4.

The acceptability of CR of any matrix when its value records less than 0.10. Otherwise, the expert’s judgment procedure needs to be revised in the matrix for pairwise comparisons.

- Step VI.

- Computing attributes weights

The final step describes the calculations of the weights by normalizing the criteria of all the rows and columns of the crisp comparison matrix.

4. Results and Discussion

This research used multiple methods to develop a corporate sustainability framework that assists policymakers, government, decision-makers, and managers, to effectively develop sustainability and make better decisions in implementing sustainable business practices. This study is the first of its kind to develop a multidimensional corporate sustainability model based on important sustainability indicators that include pandemic information due to the COVID-19 outbreak. Further, this study identifies and assesses valuable sustainability options retrieved from literature and experts’ knowledge to provide the most suitable sustainability practices for making corporate sustainability resilient. Our investigation is a roadmap for organizations and policymakers in the contemporary world aiming to determine further applications based on our findings, which provides a more rational solution for the development of corporate sustainability.

4.1. Fuzzy Analytical Hierarchy Process Results

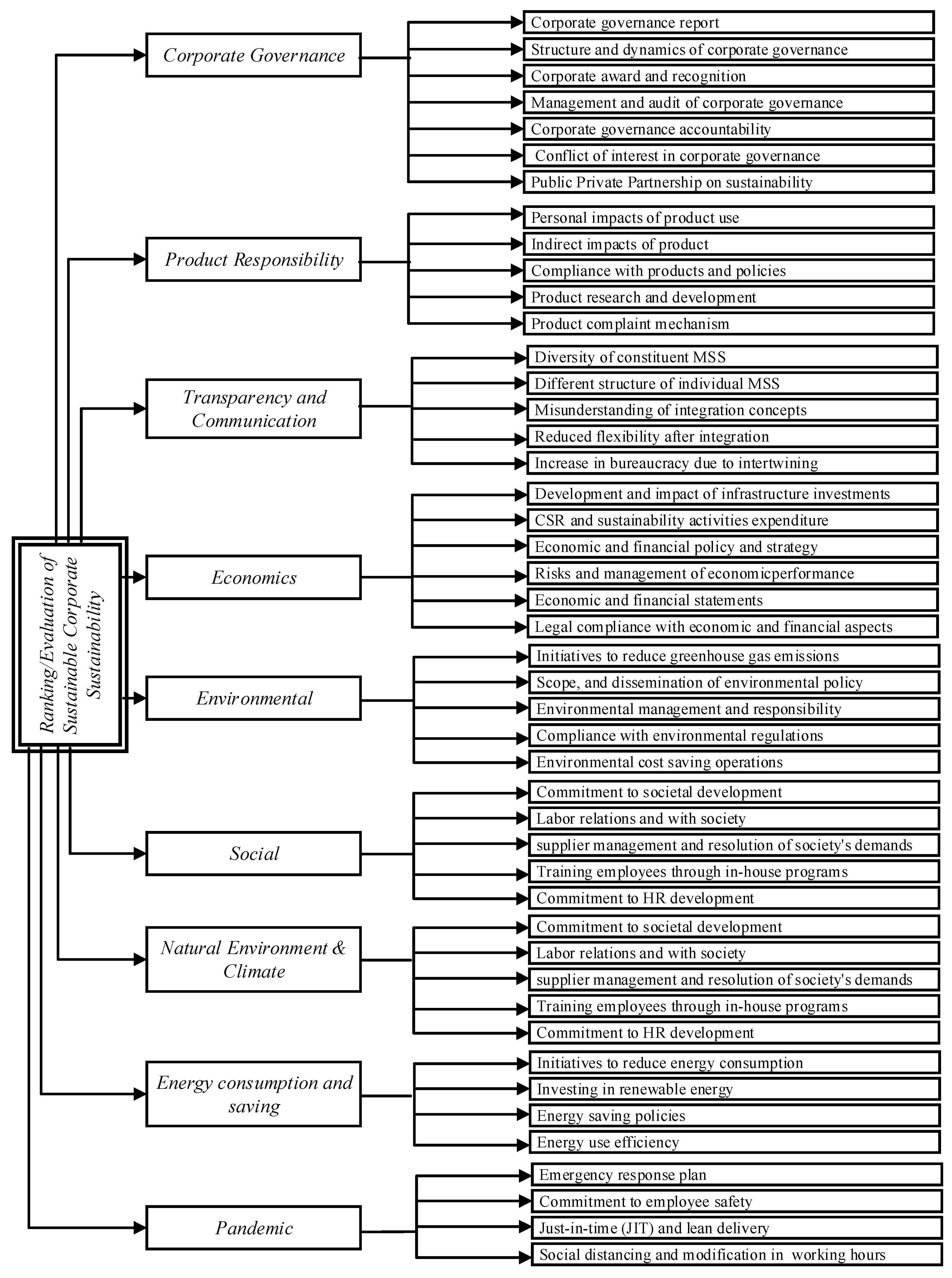

Our analysis started by using the FAHP method based on a pairwise comparison matrix. This matrix was built for determining individual expert scores through a geometric mean approach. The group-based decision-making approach was adopted for calculations of sustainability attributes and sub-attributes weights. Supported by experts and analyzing the related literature review, we can classify nine main sustainability attributes, i.e., Corporate Governance, Environment, Social, Economic, Product Responsibility, Natural Environment and Climate, Energy Consumption and Saving, Transparency and Communication, and COVID-19 pandemic. The first phase of the FAHP method comprises the calculation of the nine most important criteria’s weights and, at the second stage, we determined the 45 sub-attributes weights in total. Figure 6 presents the hierarchal structure of corporate sustainability with the main attributes and sub-attributes.

4.2. Prioritizing Main Attributes

The FAHP computed the weight of each sustainability attribute in a hierarchical structure. The main attributes are presented in Table 5 and reveal that the COVID-19 pandemic is the most important criteria by obtaining the highest weight of 0.4129. The importance of criteria were as follows: Economic (0.3754), Corporate Governance (0.2532), Natural Environment and Climate (0.2195), Environmental (ENV), Energy Consumption and Saving (0.1775), Transparency and Communication (0.1210), Social (0.0542), and Product Responsibility (0.0492) criteria, respectively. The details of each main sustainability indicator’s weights are presented in Table 5. The rapid spreading of the pandemic involving COVID-19 is the most influential barrier disrupting corporate sustainability. The pandemic has affected overall business performances. Economic sustainability and governance was the second most important indicator in our analysis. Due to the COVID-19 pandemic’s effects, it brings new challenges for corporations to affect their ability to operationalize sustainability. In addition to new compliance and regulatory parameters, it appears to be a mandatory part of corporate sustainability in the organization. Therefore, corporations need to develop a corporate sustainability system in order to cope with these new issues and enable more sustainable business practices.

According to the calculation of the main sustainability attributes’ weights, the Pandemic attribute came first in the main corporate sustainability criteria. To this end, organizations should develop an emergency response plan to tackle any emergency, which may become a hurdle in the effective implementation of corporate sustainability. Hence, organizations should develop a sustainable structure that can prevent the organization from crises. Moreover, organizations should also implement suitable and long-lasting sustainability practices that assure optimal progress toward sustainability and provide benefits while utilizing scarce resources. Further, it was observed that the delivery time of goods supplies has been drastically disrupted due to the COVID-19 outbreak. Therefore, organizations need to develop a sustainable delivery system like just-in-time (JIT), which provides a more resilient solution during any emergency faced by the organization. Economic sustainability, governance, and natural environment and climate took their position after the pandemic attribute. Whereas product responsibility came last and observed the least essential attributes by obtaining the lowest weight (0.0492). The 45 sub-attributes of the study were evaluated through with the help of expert’s opinion, according to the pairwise comparisons matrix.

4.3. The Prioritizing of Sub-Attributes

The ranking of sub-attributes of corporate sustainability is presented in Figure 7, Figure 8, Figure 9, Figure 10, Figure 11, Figure 12, Figure 13, Figure 14 and Figure 15.

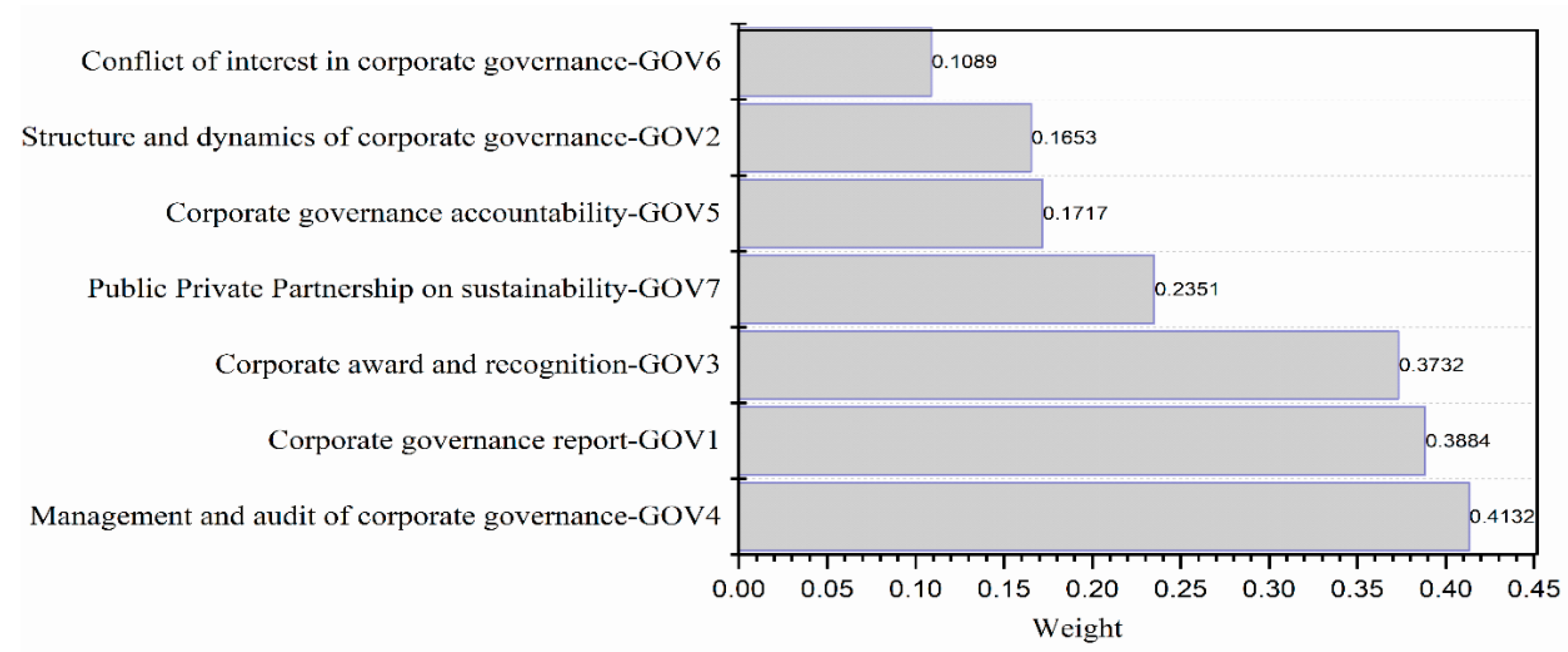

Governance sub-attributes: We identified the sub-attributes ranking (GOV) as following: GOV4>GOV1>GOV3>GOV7>GOV5>GOV2>GOV6. Management and audit of corporate governance (GOV4) obtained the highest score (0.4132) and is considered the main influencing sub-attribute of its category. The outcome proved that face validity is an accurate justification as audit expertise, then skilled personnel are credited for corporate sustainability actions. In the same way, the businesses must address governance and strengthening it since governance is responsible for guiding companies towards sustainability. Another high score observed with sub-criteria in this category is the corporate governance report (GOV1), with a weight of 0.3884. Corporate award and recognition (GOV3) showed a score of 0.3732, standing at the top-three most important sub-criteria of this category (as seen in Figure 7). Investors are evaluating both economic and financial returns on investments (ROI), but the valuation of investees’ reputation is increasing. Then, reputation is positively influenced by corporate sustainability governance at high standards (Gottschalk, 2011). Public Private Partnership on sustainability (GOV7) received a score of 0.2351, putting this sub-attribute at the fourth position of most important sub-attributes. Moreover, corporate governance accountability (GOV5) showed a score of 0.1717, being the fifth most important sub-attribute in this category. The structure and dynamics of corporate governance (GOV2) and conduct and conflict of interest in corporate governance (GOV6) are the least influencing sub-criteria, obtaining the weights of 0.1653 and 0.1089, respectively. The decision for a given company for engaging corporate sustainability governance depends on the achievements of the corporate goals. In this way, [97] underlined that a company’s sustainability is influenced by the stakeholder’s sustainability. Additionally, relations with stakeholders must be considered key for decision-making processes which, in turn, support the establishment of corporate strategies.

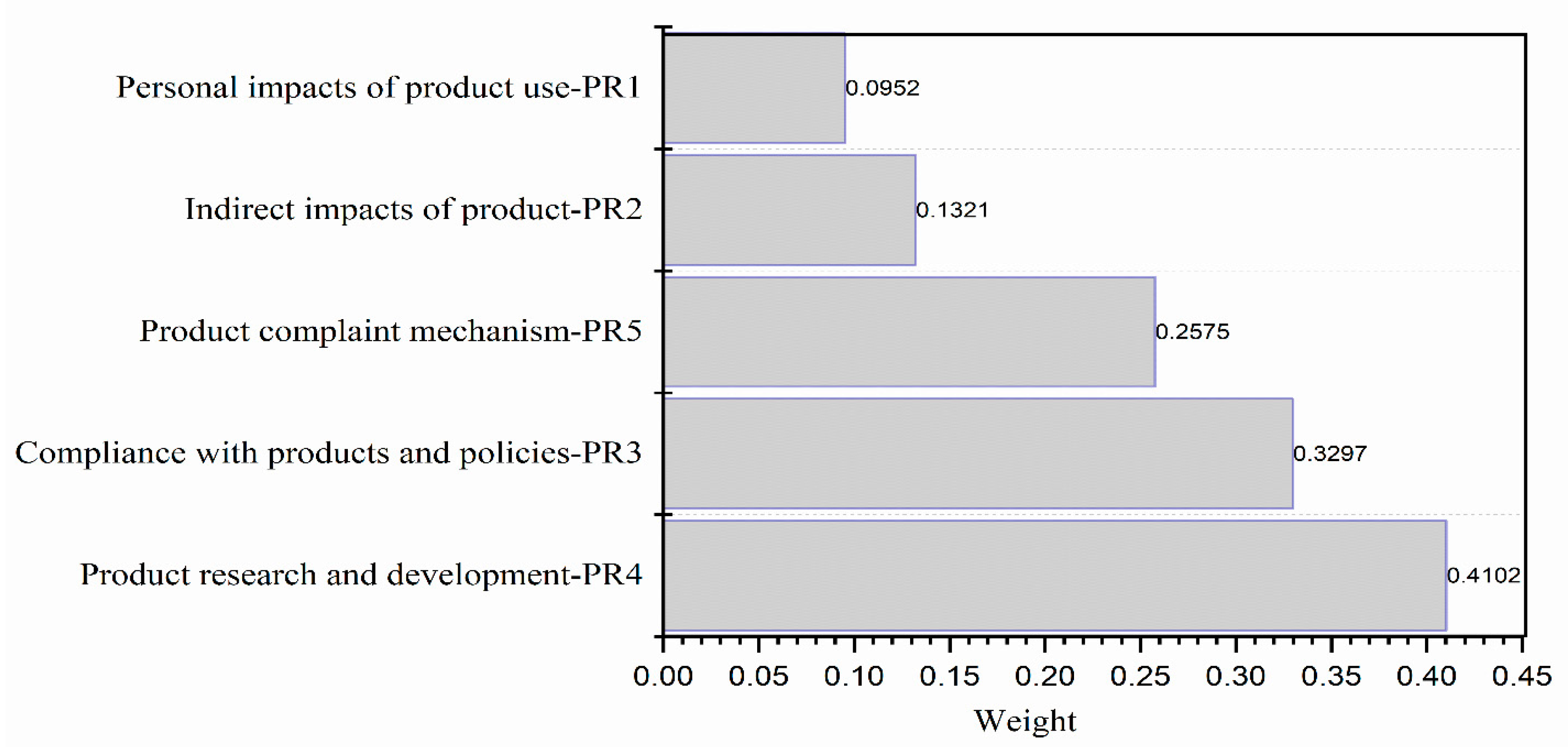

Product Responsibility: Under the Product responsibility (PR) category, we obtained the following sub-criteria ranking: PR4>PR3>PR5>PR2>PR1, as presented in Figure 8. Product research and development (PR4) is seen as a challenge in supporting the development of corporate sustainability infrastructure, with a score of 0.4102. The next sub-criteria that received the highest score is the compliance with products and policies (PR3) category, with a weight of 0.3297. Product complaint mechanism (PR5) received a score of 0.1737, being the third most important sub-criteria. Following this, indirect impacts of the product (PR2) reached the fourth position (within Product Responsibility category) with a weight of 0.1321. The fifth most important sub-attribute came from the personal impacts of product use (PR1) with a weight of 0.0952. Then, the first phases of product-innovation processes, as well as decision-making processes, must address a sustainability perspective in order to introduce a sustainability paradigm into the business’s practices. Additionally, organizations must incorporate a long-term perspective when considering sustainability as a strategic asset for businesses [98].

Transparency and Communication: As shown in Figure 9, the ranking of sub-attribute within Transparency and Communication is TC4>TC3>TC1>TC2>TC5, with a consistency ratio of 0.0107. Transparency of general reports (TC4) reached the first position in the Transparency and Communication category, showing a score of 0.4321. Moreover, strategic perspectives after transparency of general reports (TC3) is in the second position, reaching a score of 0.3487. Following, commitments to the community (TC1) and alignment of commitments (TC2) are ranked at the third and fourth positions, obtaining a score of 0.2175 and 0.1564, respectively. Finally, ethics and citizenship (TC5) are considered the least influencing sub-criteria with a score of 0.1324. Thus, sustainability supports knowledge creation and sharing, which, in turn, eases communication within organizations. To make a proactive sustainability strategy realistic, Kim and Ji [99] suggested that corporations aiming for a proactive sustainability strategy must consider the communication of a shared vision within an organization and among the company’s stakeholders. When companies communicate their visions related to sustainability, they improve their reputation which increases stakeholders’ interests in such organizations. Moreover, Dyllick and Muff [100] stated that corporate sustainability mission and vision statements should be adopted to convey corporate commitment throughout the corporation. Then, top managers have to consider sustainability goals in the company’s core values in order to align the company’s motivations, strategic goals, and responsibilities related to customers, employees, and society, as well as stakeholders. Companies need to address sustainability due it inspires commitments through proactive sustainability strategies.

Economics: The outcomes showed the sub-attribute ranking: ECO4>ECO2>ECO6>ECO5>ECO1>ECO3, as seen in Figure 10. Firstly, risks and the management of economic and financial performance (ECO4) has a weight of 0.4932, whereas CSR and sustainability activities expenditure (ECO2) are ranked in the second position with a score of 0.4321. Economic difficulties are explained due to the financial resources required for sustainability development. Results showed that sustainability is directly related to costs (such as costs with audit, training, certification) and indirectly related to operational and social resources, skilled personnel, preventive actions, and regulations adherence. The legal compliance with economic and financial aspects (ECO6) and economic and financial statements (ECO5) is considered at the third and fourth positions within the sub-criteria category of economics with a score of 0.2383 and 0.1894, respectively. Lastly, the development and impact of infrastructure investments (ECO1) and economic and financial policy and strategy (ECO3) with a weight of 0.1765 and 0.1634, respectively. Sustainability actions are the basic elements for putting the economic dimension into practice, and these actions consider profitability, financial stability and liquidity, and financial benefits [101]. Therefore, the CSR spending, the management of innovation and technology, knowledge management, collaborations, organizational processes management, and elaboration of sustainability reports are some of the relevant actions towards corporate sustainability [102].

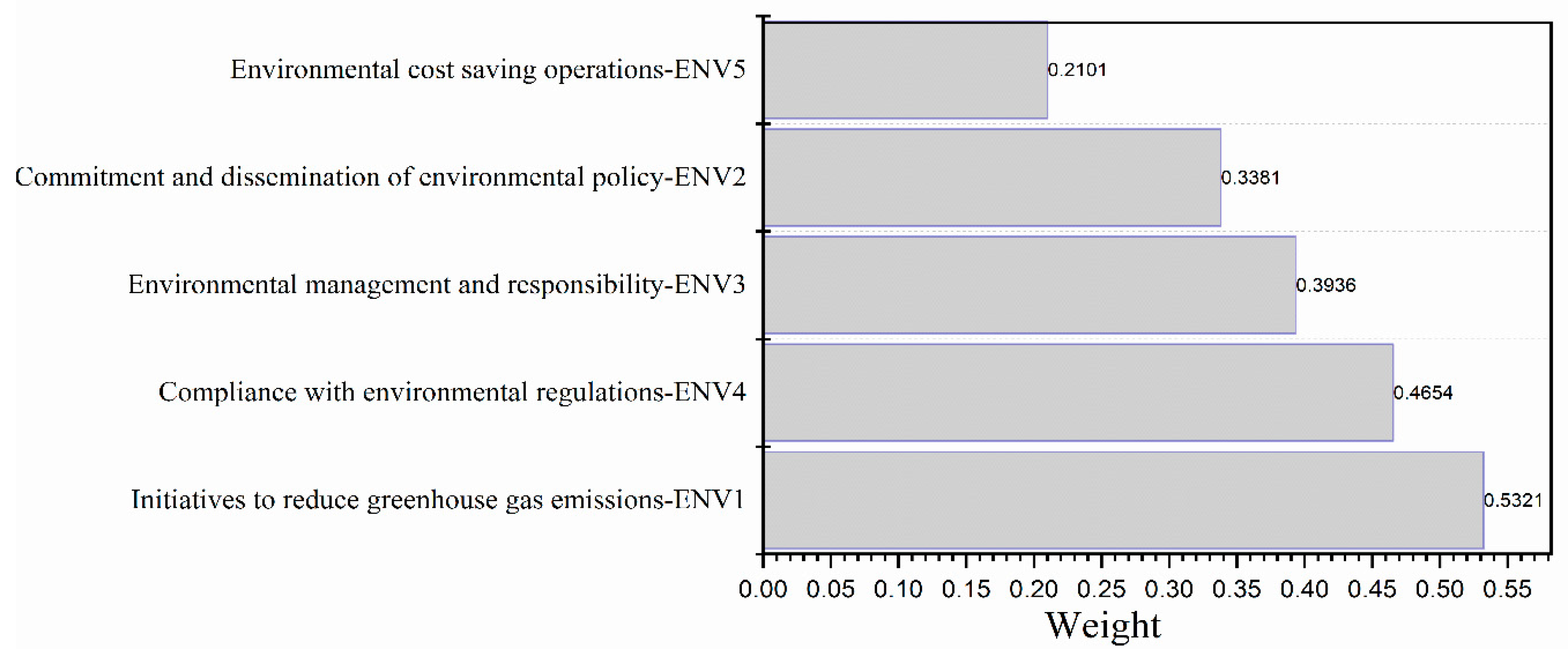

Environment: Results showed the ranking within the Environmental dimension of corporate sustainability are as follows: ENV1>ENV4>ENV3>ENV2>ENV5, as shown in Figure 11. The highest weight, 0.5321, obtained of sub-criteria within the environment category is initiatives to reduce greenhouse gas emissions (ENV1). Compliance with environmental regulations (ENV4) reported the second sub-criteria in the row with a weight of 0.4654. Whereas, environmental management and responsibility (ENV3) sub-barrier and commitment, scope, and dissemination of environmental policy (ENV2) are ranked at third and fourth positions, within the environmental sustainability category, presenting a score of 0.3936 and 0.3381, respectively. Finally, environmental cost-saving operations (ENV5) come fifth in the row with a weight of 0.2101. Government regulations have been the primary drivers of a part of corporate sustainability. Literature showed that environmental sustainability provides cost reductions for the businesses, and these reductions are related to the use of energy, raw materials, and water, as well as reducing waste generation. Environmental sustainability improves the company’s reputation for stakeholders and into the market which, in turn, eases acquiring new customers prone to environmental issues. The incorporation of EMS by companies leads to CO2 emission reductions as well as a reduction in pollution [103,104].

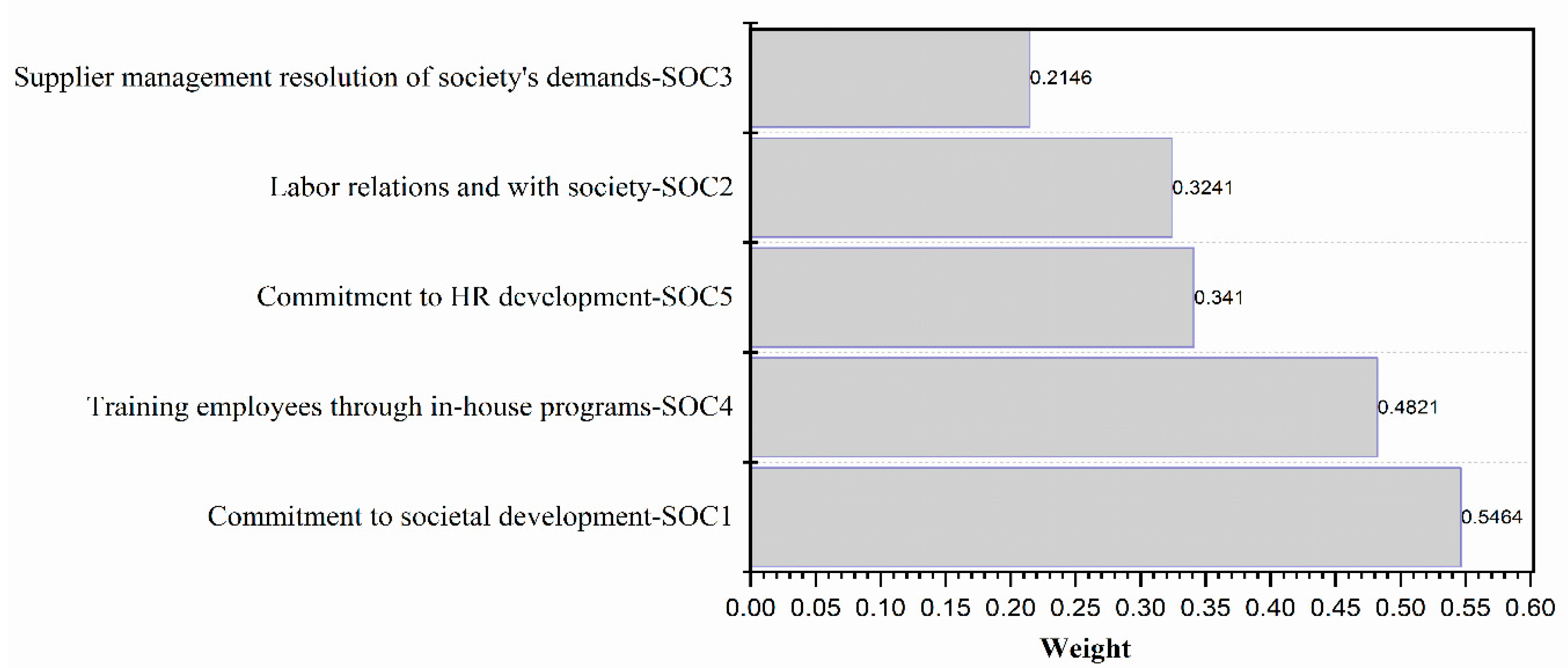

Social: Figure 12 shows the outcomes, ranking the sub-criteria as follows: SOC1>SOC4>SOC5>SOC2>SOC3. The highest sub-attribute of social criteria is the commitment to societal development (SOC1) with a weight of 0.5464. Training employees through in-house programs (SOC4) is ranked at the second position, presenting a score of 0.4821. Companies must train their personnel to work in an integrated way. Additionally, companies must use integration between auditing services and administration support for building stronger relationships with stakeholders. These relations promote efficiency, may save resources, and provide assertiveness amongst personnel.

Whereas commitment to HR development (SOC5) is ranked as the third most important sub-criterium, showing a score of 0.3410. Human resources (HR) have a crucial role in the implementation of sustainability by companies [105]. The companies aiming the implementation of sustainability must address the commitment from top managers, supportive actions towards training, personnel empowerment, and teamwork in areas such as Quality Management. Labor relations and with society (SOC2) as well as diversity and equity, supplier management, and resolution of society’s demands (SOC3) are ranked into the fourth and fifth positions, presenting scores of 0.3241 and 0.2146, respectively. Here, we see a strong relationship with suppliers, which emphasizes the need for developing an integrative decision support program for managing the supply chain, taking into account the stakeholders that strategically improve the company’s production processes and balance the supplier sustainability system.

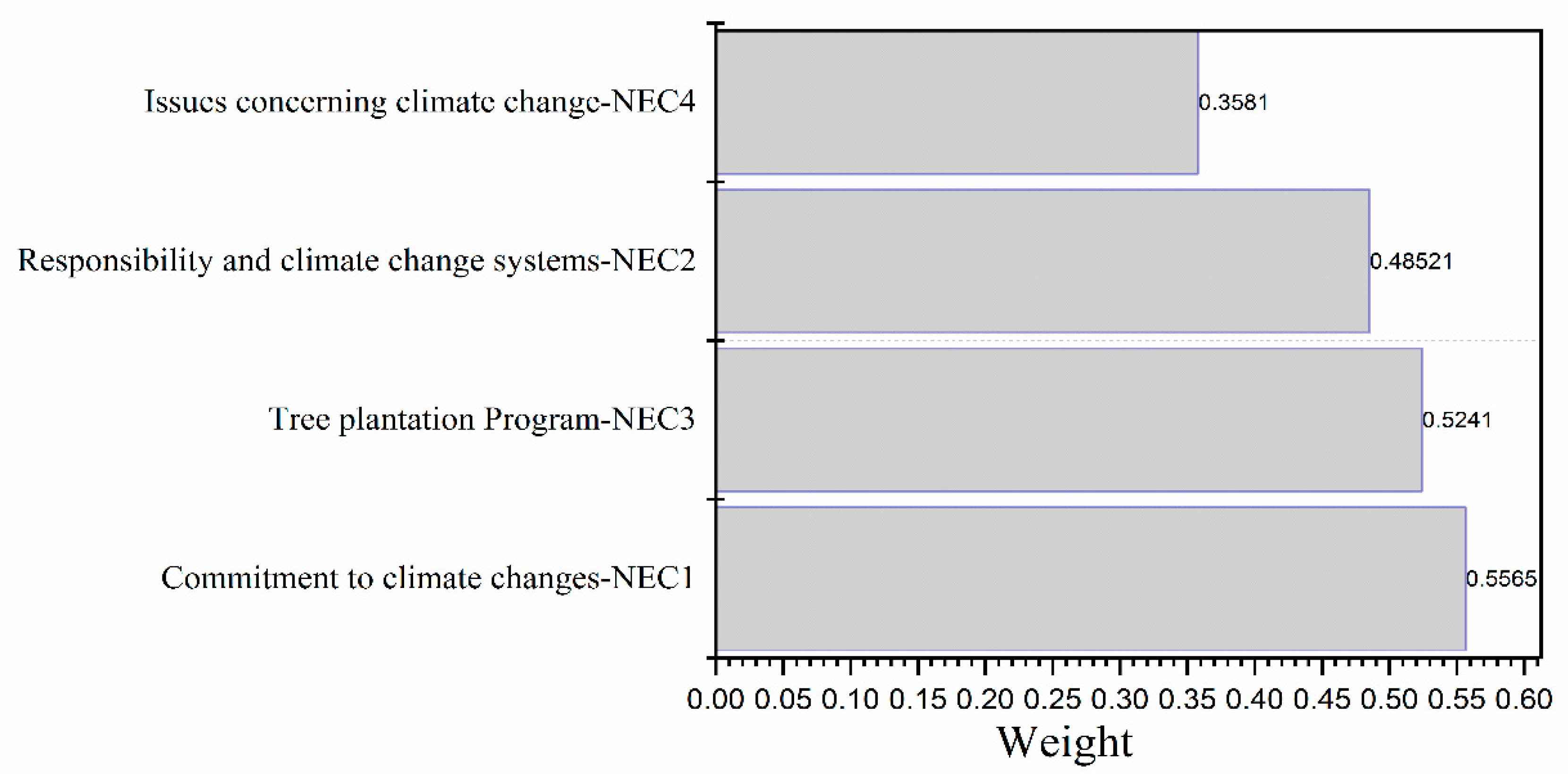

Natural Environment and Climate: under the natural environment and climate change category, results showed in Figure 13 allowed the identification of the following ranking: NEC1>NEC3>NEC2>NEC4. Commitment to climate change (NEC1) is presented as the highest score within 0.5565. Commitment to handle climate vulnerability is a relevant topic to be addressed by corporate sustainability, stimulating employees in creating new opportunities for improving and monitoring effective systems. Moreover, climate change is usually considered an important threat in society and nature, more critical than biodiversity loss. Regarding the company’s sustainability performance, the tree planting program (NEC3) is located in the second position with a 0.5241 score. The responsibility and climate change systems (NEC2) and Issues concerning climate change (NEC4) come in at the third and fourth positions within the category with scores of 0.48521 and 0.3581, respectively. A responsibility attributed to businesses regarding environmental crisis mitigation is crucial, due to these organizations possessing greater experience than any other group in society when dealing with such kind of problems. The organization should develop an environment towards a climate-friendly perspective, since climate changes are affecting societies and will affect, as a consequence, companies’ revenues. In this scenario, tougher legislation and binding treaties are needed [106].

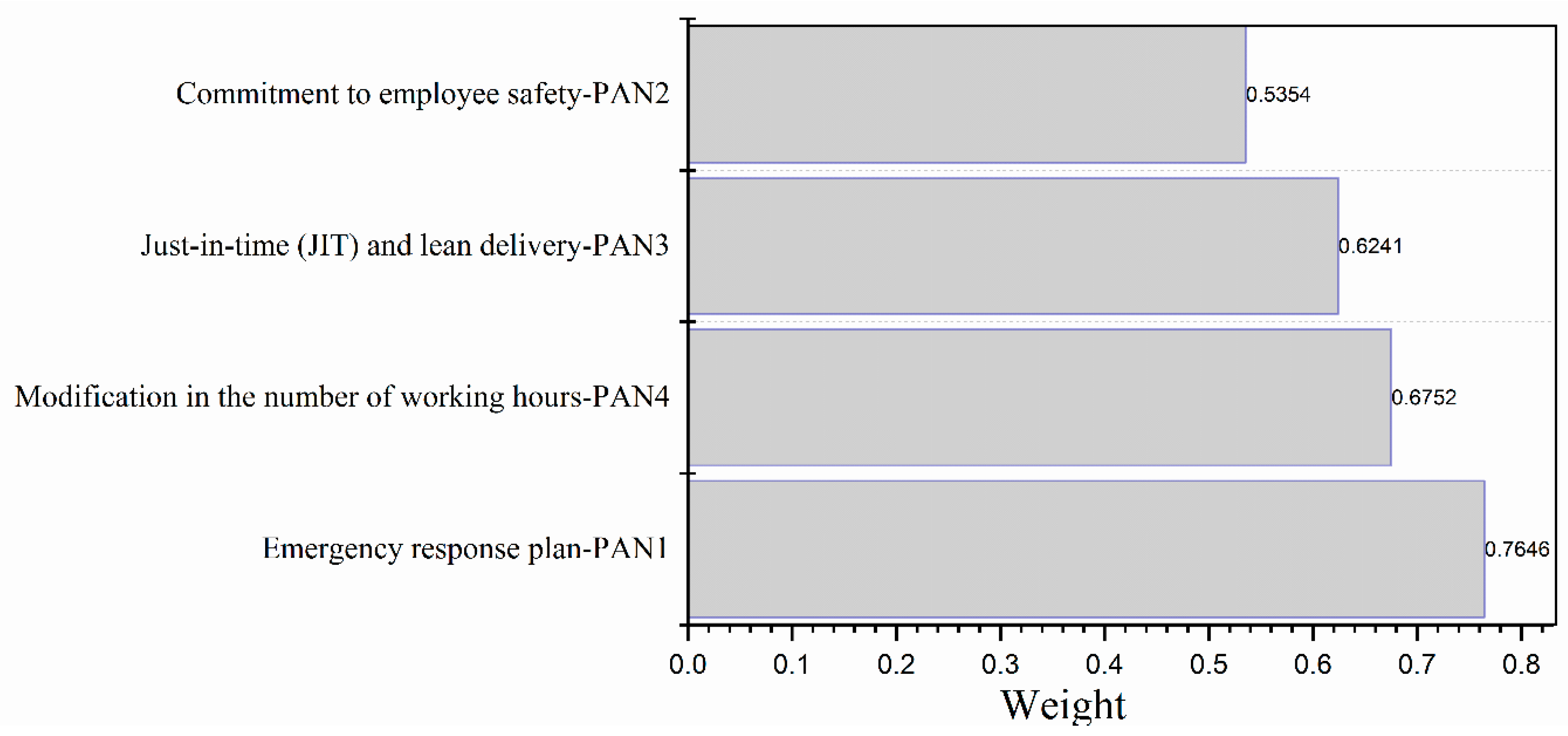

Pandemic: Under the Pandemic (PAN) category, results in Figure 14 show the sub-attributes in the following order of importance: PAN1>PAN4>PAN2>PAN3. An emergency response plan (PAN1) obtained the highest weight 0.7646. Due to the COVID-19 pandemic outbreak, whose major consequences are expected to be revealed in the long-term, results provided a deeper analysis of business risks, which can help organizations to plan accordingly. The organizations should incorporate an emergency plan in order to respond to the pandemic (PAN1), which is considered a community-led initiative based on different scenarios for testing the resilience and the plans addressing the several impacts of the crisis.

Following this, the highest sub-criteria identified is the modification in the number of working hours and social distancing (PAN4) with a weight of 0.6752. Environmental dimensions are the focus of companies and, for this research, organizations are taking several actions to fight the coronavirus outbreak, especially with social distancing and the modification in employee working hours. Organizations should also dedicate focus on their supply chains and on social innovations issues that may result from this pandemic. Results also showed that the JIT as well as lean delivery (PAN2) obtained 0.6241 weight and are in the third position within this category. The pandemic caused by the coronavirus emphasized vulnerabilities related to the overreliance of JIT and lean delivery systems. Additionally, there is a concern about whether JIT systems can contribute to the overall efficiency of resources and waste, in order to transform them into environmentally sound [85].

The growing smarter logistics systems are witnessed by organizations, specifically the consideration of Internet-of-Things (IoT) technologies applications, and reverse logistics for secondary materials and waste products. Some possible applications of IoT and reverse logistics are addressed. In the first example, monitoring where electronics and appliances and their components are may ease their retrieval and allocation at local levels. As a second example, companies may benefit by using intermediary storage/depots instead of using extensive transportation of processed goods, also favoring reverse logistics. The fourth sub-criteria under the COVID-19 pandemic category, commitment to employee safety (PAN3), has a weight of 0.5354.

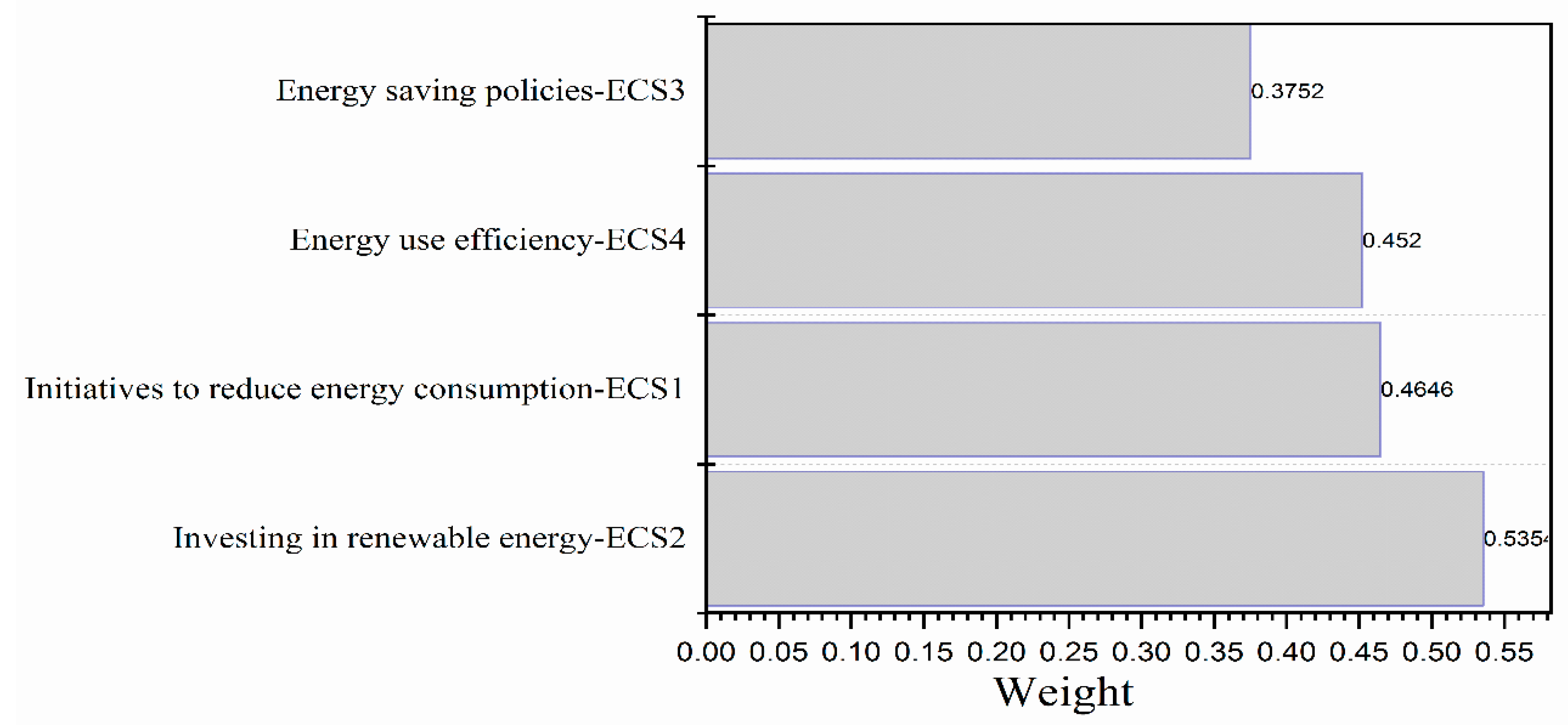

Energy Consumption and Caving: Figure 15 presents the ranking of sub-criteria related to Energy Consumption and Caving to develop corporate sustainability as follows: ECS2>ECS1>ECS4>ECS3, with consistency ratio 0.0140. Investing in renewable energy (ECS2) holds the first position within the Energy Consumption and Saving category with the highest score (0.5354). Moreover, initiatives to reduce energy consumption (ECS1) is located at the second position with a score of 0.4646. The third and fourth sub-criteria within the energy consumption and saving category are energy use efficiency (ECS4) and energy saving policies (ECS3), which received weights of 0.4520 and 0.3752, respectively. Investments in renewable energy projects lead to greater engagement by the local community related to renewable energy development. Thus, renewable energy projects can empower the community and enrich their social capital. In addition, an expected outcome is an increase in energy efficiency within a community and reducing energy costs. Organizations can improve sustainability by reducing material waste, energy consumption, and carbon emissions.

4.4. Final Ranking of Sub-Criteria Analyses

After determining the weights of sustainability sub-attributes, it involved multiplying the sub-barrier of global weights by the weight of each respective category, as shown in Table 6. It is noticed that the overall ranking of sub-criteria for the development of corporate sustainability is based on final weights. The criteria of sub-attributes for the development of corporate sustainability is as follows:

PAN1>PAN4>PAN3>NEC1>SOC1>PAN2>ECS2>ENV1>NEC3>ECO4>NEC2>SOC4>ENV4>ECS1>ECS4>TC4>ECO2>GOV4>PR4>ENV3>GOV1>ECS3>GOV3>NEC4>TC3>SOC5>ENV2>PR3>SOC2>PR5>GOV7>TC1>SOC3>ENV5>ECO5>ECO1>GOV5>GOV2>ECO3>TC2>TC5>PR2>GOV6>PR1

For the sustainable development of corporate sustainability, an emergency response plan is the attribute that showed the highest score, 0.7646, followed by modification in the number of working hours and social distances 0.6752. JIT and lean delivery, and commitment to climate changes are ranked at third and fourth positions of the most important sub-attributes, obtaining scores of 0.6241 and 0.5565, respectively. Finally, in the following three positions, influencing sub-attributes in the development of corporate sustainability are indirect impacts of product (0.1321), conflict of interest in corporate governance (0.1089), and personal impacts of product use (0.0952), respectively.

5. Conclusions

This study’s goal is to propose a corporate sustainability framework that is more resilient than prior models and, to rank relevant criteria to the degree that could help develop a corporate sustainability model. This study is grounded in previous studies and showed the interconnected relations of sustainability and the relevance of considering stakeholders [107]. In meeting the objectives of this study we have multiple contributions to the field of sustainable business practices; (1) to help researchers and practitioners identify essential corporate sustainability criteria as part of a new integrated framework; (2) provide a methodology to help organize and understand a dynamic context for sustainable business practices; (3) extend our understanding of social sustainability be also exploring and finding new insights regarding the COVID-19 pandemic.

We were able to identify several sustainability attributes from literature, which allowed for an analysis of prior studies and the identification of sustainability attributes, which is also supported by experts’ assessments. As a result, 45 sustainability sub-criteria were developed and ranked according to the main nine categories of Corporate Governance, Transparency and Communication, Product Responsibility, Environment, Social, Economics, Natural Environment and Climate Change, Energy Consumption and Saving and, for the very first time, we have included Pandemic as an important criterion in the development of corporate sustainability model. These criteria help to develop a new integrative framework of social sustainability. Additional contributions of this study include the application of a Fuzzy Delphi and FAHP methodology, and the computation of nine main criteria and 45 sub-criteria. These criteria provide a more dynamic assessment of the interrelated social dimensions that have in the past been looked at individually and as environmental impacts of firms. Due to the COVID-19 pandemic, new insights include the Pandemic, along with Economic and Corporate Governance are top-ranked criteria to focus on improving corporate sustainability practices. Whereas, emergency response plan, social distance and modification in the number of working hours, commitment to climate changes, and JIT and lean delivery emerged in the top-ranked sub-criteria.

The outcomes of our work lead us to call for more action from decision-makers and policymakers as sustainability provides an integration opportunity with dynamic social benefits. Moreover, scholars also can consider relevant criteria from literature, and building on this research when combining insights from experts and develop a new, more integrated, corporate sustainability model. The research in this study also contributes to developing theory with contemporary approaches for decision-making analysis to show corporate sustainability theory can and should include more social sustainability practices. When doing so, we hope the efforts of both researchers and practitioners will be able to find more dynamic relationships between practices, firm performance, and resiliency to overcome future pandemics. Our results also provide insights to scholars wanting to further develop theories considering Multiple Management Standards (MMSs), the Stakeholder Theory [108], Integrated Management [109], Integrated Management Systems (IMS), and possibilities for a new theory such as a social sustainability-based view (SBV) of the firm.

The methods used in this study support decision-making in a powerful and relatively simple way. This useful perspective addresses decision-makers and researchers dealing with resource allocation or project prioritization. These methods may be applied toward further replications by future studies. The methods described in this study help in measuring strategic goals as a set of scored criteria for determining project selection. Multi-criterion decision-making methodologies have proven to be useful in the application for manufacturing sectors. We can foresee the need for more work with these types of firms using the application of MCDA in complex interdisciplinary and social sustainability problems. We recommend future studies include developing FAHP techniques in combination with other analysis opportunities in an integrated system, supply chains, cities, and even entire countries aiming to tackle grand challenges, for example, the United Nations’ Sustainable Development Goals (SDGs).

Finally, this research is the first of its kind considering the development of an integrated social sustainability model with social sustainability criteria that include the pandemic and COVID-19. Outcomes of this study can help organizations to consider the most suitable programs and systems for advancing corporate sustainability while also considering stakeholders and social sustainability. As managerial implications, we see sustainable development enabling companies to integrate audits, engage personnel, and optimizing companies’ processes and resource allocation. Social sustainability is dynamic, not easily understood, and can be disruptive if not taken into account as part of corporate social sustainability at every level of the firm.

This study presents some limitations. We address the limitation related to the developed models based on experts’ assessments. By choosing this approach, it is assumed that bias will always occur in the process. Future applications of this approach may include a diversified set of experts and managers from companies that may be more impacted by systems implementations. Another limitation is concerning data availability. Managers involved in an MCDA process may have limited access to data concerning all criteria or even the entire multinational company as a consequence of a lack of integrated information. Moreover, these issues can be solved by careful consideration of practitioners involved in the decision-making process when realizing that inputs are qualitative, in nature, and the time needed for options assessments. Then, the criteria and outcomes should be revisited when assessing corporate sustainability performance over time.

Author Contributions

conceptualization, M.I.; methodology, M.I.; software, M.I.; validation, M.I., Q.Z., R.S and M.F.; formal analysis, M.I.; investigation, M.I, Q.Z., R.S. and M.F; resources, M.I. and Q.Z.; data curation, M.I.; writing—original draft preparation, M.I.; writing—review and editing, M.I.,Q.Z.,R.S. and M.F; visualization, M.I.; supervision, Q.Z. and R.S.; project administration, Q.Z. and R.S; funding acquisition, Q.Z. All authors have read and agreed to the published version of the manuscript.

Funding

“This research was funded by, National Natural Science Foundation of China, Grant/Award Number: 71572115; Major Program of Social Science Foundation of Guangdong, Grant/Award Number: 2016WZDXM005; 2020 Guangdong 13th-Five-Year-Plan Philosophical and Social Science Fund (#GD20CGL28); and Natural Science Foundation of SZU, Grant/Award Number: 836”.

Acknowledgments

The authors thank the anonymous reviewers and Editor for their valuable contributions that improved this manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

List of experts.

| No. | Designation | Qualification | Age | Organization |

|---|---|---|---|---|

| 1 | Director | PhD | 43 | Ministry of climate change |

| 2 | Professor | PhD | 50 | Nanjing University |

| 3 | Deputy Director | PhD | 56 | SGS Group, Shenzhen |

| 4 | Manager Quality control | Graduation | 37 | Walmart, Beijing |

| 5 | Health & Safety Manager | Graduation | 38 | Honda, Guangzhou |

| 6 | Director Shipping | Graduation | 47 | YTS auto spare parts Guangzhou |

| 7 | Associate Professor | PhD | 42 | Zhejiang University |

| 8 | Executive director | Graduation | 53 | Ministry of Energy & Power |

References

- Brundtland World Commission on Environment and Development. Report of the World Commission on Environment and Development: Our Common Future; United Nations: Geneva, Switzerland, 1987; Chapters 2 and 4. [Google Scholar]

- Ikram, M.; Sroufe, R.; Rehman, E.; Shah, P.S.Z.A.; Mahmoudi, A. Do Quality, Environmental, and Social (QES) Certifications Improve International Trade? A Comparative Grey Relation Analysis of Developing vs. Developed Countries. Phys. A Stat. Mech. its Appl. 2020, 545, 123486. [Google Scholar] [CrossRef]

- International Organization for Standardization. The ISO Survey of Management System Standard Certifications—2018; ISO: Geneva, Switzerland, 2018. [Google Scholar]

- Global Reporting Initiative. Consolidated Set of GRI Sustainability Reporting Standards; GRI: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Christ, K.L.; Burritt, R.L.; Varsei, M. Coopetition as a Potential Strategy for Corporate Sustainability. Bus. Strat. Environ. 2017, 26, 1029–1040. [Google Scholar] [CrossRef]

- Manrique, S.; Marti-Ballester, C. Analyzing the Effect of Corporate Environmental Performance on Corporate Financial Performance in Developed and Developing Countries. Sustainability 2017, 9, 1957. [Google Scholar] [CrossRef] [Green Version]

- Gonzalez-Perez, M.A.; Leonard, L. The Global Compact: Corporate Sustainability in the Post 2015 World. In Advances in Sustainability and Environmental Justice; 2015; Volume 17, pp. 1–19. [Google Scholar]

- Engert, S.; Rauter, R.; Baumgartner, R.J. Exploring the integration of corporate sustainability into strategic management: A literature review. J. Clean. Prod. 2016, 112, 2833–2850. [Google Scholar] [CrossRef]

- Bezerra, M.C.D.C.; Gohr, C.F.; Morioka, S.N. Organizational capabilities towards corporate sustainability benefits: A systematic literature review and an integrative framework proposal. J. Clean. Prod. 2020, 247, 119114. [Google Scholar] [CrossRef]

- Herremans, I.M.; Nazari, J.A.; Mahmoudian, F. Stakeholder Relationships, Engagement, and Sustainability Reporting. J. Bus. Ethics 2016, 138, 417–435. [Google Scholar] [CrossRef]

- Tschopp, D.; Huefner, R.J. Comparing the Evolution of CSR Reporting to that of Financial Reporting. J. Bus. Ethics 2015, 127, 565–577. [Google Scholar] [CrossRef]

- Ikram, M.; Zhou, P.; Shah, S.; Liu, G. Do environmental management systems help improve corporate sustainable development? Evidence from manufacturing companies in Pakistan. J. Clean. Prod. 2019, 226, 628–641. [Google Scholar] [CrossRef]

- Qi, G.; Zeng, S.; Yin, H.; Lin, H. ISO and OHSAS certifications. Manag. Decis. 2013, 51, 1983–2005. [Google Scholar] [CrossRef]

- Elkington, J. Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environ. Qual. Manag. 1998, 8, 37–51. [Google Scholar] [CrossRef]

- Bolis, I.; Morioka, S.N.; Sznelwar, L.I. When sustainable development risks losing its meaning. Delimiting the concept with a comprehensive literature review and a conceptual model. J. Clean. Prod. 2014, 83, 7–20. [Google Scholar] [CrossRef]

- Carroll, A.B. A Three-Dimensional Conceptual Model of Corporate Performance. Acad. Manag. Rev. 1979, 4, 497. [Google Scholar] [CrossRef] [Green Version]

- Diouf, D.; Boiral, O. The quality of sustainability reports and impression management. Accounting Audit. Account. J. 2017, 30, 643–667. [Google Scholar] [CrossRef]

- Arribas, I.; Espinós-Vañó, M.D.; García, F.; Morales-Bañuelos, P.B. The Inclusion of Socially Irresponsible Companies in Sustainable Stock Indices. Sustainability 2019, 11, 2047. [Google Scholar] [CrossRef] [Green Version]

- Varyash, I.; Mikhaylov, A.; Moiseev, N.; Aleshin, K. Triple bottom line and corporate social responsibility performance indicators for Russian companies. Entrep. Sustain. Issues 2020, 8, 313–329. [Google Scholar] [CrossRef]

- Munda, G. Social multi-criteria evaluation for urban sustainability policies. Land Use Policy 2006, 23, 86–94. [Google Scholar] [CrossRef]

- Worldometers. Worldometerse. 2020. Available online: https://www.worldometers.info/coronavirus (accessed on 23 June 2020).

- Hakovirta, M.; Denuwara, N. How COVID-19 Redefines the Concept of Sustainability. Sustainability 2020, 12, 3727. [Google Scholar] [CrossRef]

- Maletic, M.; Maletic, D.; Dahlgaard, J.; Dahlgaard-Park, S.M.; Gomišcek, B. Do corporate sustainability practices enhance organizational economic performance? Int. J. Qual. Serv. Sci. 2015, 7, 184–200. [Google Scholar] [CrossRef] [Green Version]

- Asif, M.; Searcy, C.; Zutshi, A.; Fisscher, O.A. An integrated management systems approach to corporate social responsibility. J. Clean. Prod. 2013, 56, 7–17. [Google Scholar] [CrossRef]

- Ikram, M.; Zhang, Q.; Sroufe, R.; Shah, P.S.Z.A. Towards a sustainable environment: The nexus between ISO 14001, renewable energy consumption, access to electricity, agriculture and CO2 emissions in SAARC countries. Sustain. Prod. Consum. 2020, 22, 218–230. [Google Scholar] [CrossRef]

- Amrutha, V.; Geetha, S. A systematic review on green human resource management: Implications for social sustainability. J. Clean. Prod. 2020, 247, 119131. [Google Scholar] [CrossRef]

- Landrum, N.E.; Ohsowski, B. Identifying Worldviews on Corporate Sustainability: A Content Analysis of Corporate Sustainability Reports. Bus. Strateg. Environ. 2017, 27, 128–151. [Google Scholar] [CrossRef] [Green Version]

- Landrum, N.E. Stages of Corporate Sustainability: Integrating the Strong Sustainability Worldview. Organ. Environ. 2018, 31, 287–313. [Google Scholar] [CrossRef]

- Longoni, A.; Cagliano, R. Sustainable Innovativeness and the Triple Bottom Line: The Role of Organizational Time Perspective. J. Bus. Ethics 2018, 151, 1097–1120. [Google Scholar] [CrossRef] [Green Version]

- Stacchezzini, R.; Melloni, G.; Lai, A. Sustainability management and reporting: The role of integrated reporting for communicating corporate sustainability management. J. Clean. Prod. 2016, 136, 102–110. [Google Scholar] [CrossRef]

- Weber, O. Corporate sustainability and financial performance of Chinese banks. Sustain. Accounting Manag. Policy J. 2017, 8, 358–385. [Google Scholar] [CrossRef] [Green Version]

- Karaman, A.S.; Akman, E. Taking-off corporate social responsibility programs: An AHP application in airline industry. J. Air Transp. Manag. 2018, 68, 187–197. [Google Scholar] [CrossRef]

- Handfield, R.; Walton, S.V.; Sroufe, R.; Melnyk, S.A. Applying environmental criteria to supplier assessment: A study in the application of the Analytical Hierarchy Process. Eur. J. Oper. Res. 2002, 141, 70–87. [Google Scholar] [CrossRef]

- Boggia, A.; Massei, G.; Pace, E.; Rocchi, L.; Paolotti, L.; Attard, M. Spatial multicriteria analysis for sustainability assessment: A new model for decision making. Land Use Policy 2018, 71, 281–292. [Google Scholar] [CrossRef] [Green Version]

- Tyagi, M.; Kumar, P.; Kumar, D. Assessment of CSR based supply chain performance system using an integrated fuzzy AHP-TOPSIS approach. Int. J. Logist. Res. Appl. 2018, 21, 378–406. [Google Scholar] [CrossRef]

- Phochanikorn, P.; Tan, C. An Integrated Multi-Criteria Decision-Making Model Based on Prospect Theory for Green Supplier Selection under Uncertain Environment: A Case Study of the Thailand Palm Oil Products Industry. Sustainability 2019, 11, 1872. [Google Scholar] [CrossRef] [Green Version]

- Bai, C.; Kusi-Sarpong, S.; Ahmadi, H.B.; Sarkis, J. Social sustainable supplier evaluation and selection: A group decision-support approach. Int. J. Prod. Res. 2019, 57, 7046–7067. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Chou, W.-C.; Hsu, W. The sustainability balanced scorecard as a framework for selecting socially responsible investment: An effective MCDM model. J. Oper. Res. Soc. 2009, 60, 1396–1410. [Google Scholar] [CrossRef]

- Kusi-Sarpong, S.; Gupta, H.; Sarkis, J. A supply chain sustainability innovation framework and evaluation methodology. Int. J. Prod. Res. 2019, 57, 1990–2008. [Google Scholar] [CrossRef] [Green Version]

- Liao, P.-C.; Xue, J.; Liu, B.; Fang, D. Selection of the approach for producing a weighting scheme for the CSR evaluation framework. KSCE J. Civ. Eng. 2015, 19, 1549–1559. [Google Scholar] [CrossRef]

- Esteves, A. Evaluating community investments in the mining sector using multi-criteria decision analysis to integrate SIA with business planning. Environ. Impact Assess. Rev. 2008, 28, 338–348. [Google Scholar] [CrossRef]

- Raut, R.D.; Cheikhrouhou, N.; Kharat, M. Sustainability in The Banking Industry: A Strategic Multi-Criterion Analysis. Bus. Strateg. Environ. 2017, 26, 550–568. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M. Ángeles; Rivera-Lirio, J.M. Measuring Corporate Environmental Performance: A Methodology for Sustainable Development. Bus. Strateg. Environ. 2017, 26, 142–162. [Google Scholar] [CrossRef]

- Wibowo, S.; Deng, H. Multi-criteria group decision making for evaluating the performance of e-waste recycling programs under uncertainty. Waste Manag. 2015, 40, 127–135. [Google Scholar] [CrossRef]

- Raut, R.; Narkhede, B.E.; Gardas, B.B.; Luong, H.T. An ISM approach for the barrier analysis in implementing sustainable practices. Benchmarking Int. J. 2018, 25, 1245–1271. [Google Scholar] [CrossRef]

- Petrillo, A.; De Felice, F.; Garcia-Melon, M.; Gladish, B.P. Investing in socially responsible mutual funds: Proposal of non-financial ranking in Italian market. Res. Int. Bus. Finance 2016, 37, 541–555. [Google Scholar] [CrossRef]

- Jindal, A.; Sangwan, K.S. A fuzzy-based decision support framework for product recovery process selection in reverse logistics. Int. J. Serv. Oper. Manag. 2016, 25, 413. [Google Scholar] [CrossRef]

- Željko, S.; Pamučar, D.; Puška, A.; Chatterjee, P. Sustainable supplier selection in healthcare industries using a new MCDM method: Measurement of alternatives and ranking according to Compromise solution (MARCOS). Comput. Ind. Eng. 2020, 140, 106231. [Google Scholar] [CrossRef]

- Yang, J.-J.; Chuang, Y.-C.; Lo, H.-W.; Lee, T.-I. A Two-Stage MCDM Model for Exploring the Influential Relationships of Sustainable Sports Tourism Criteria in Taichung City. Int. J. Environ. Res. Public Health 2020, 17, 2319. [Google Scholar] [CrossRef] [Green Version]

- Kumar, A.; Ramesh, A. An MCDM framework for assessment of social sustainability indicators of the freight transport industry under uncertainty. A multi-company perspective. J. Enterp. Inf. Manag 2020. [Google Scholar] [CrossRef]

- Ikram, M.; Zhang, Q.; Sroufe, R. Developing integrated management systems using an AHP-Fuzzy VIKOR approach. Bus. Strateg. Environ. 2020, 29, 2265–2283. [Google Scholar] [CrossRef]

- Tan, W.J.; Cai, W.; Zhang, A.N. Structural-aware simulation analysis of supply chain resilience. Int. J. Prod. Res. 2020, 58, 5175–5195. [Google Scholar] [CrossRef]

- Ivanov, D.; Dolgui, A. Viability of intertwined supply networks: Extending the supply chain resilience angles towards survivability. A position paper motivated by COVID-19 outbreak. Int. J. Prod. Res. 2020, 58, 2904–2915. [Google Scholar] [CrossRef] [Green Version]

- Gössling, S.; Scott, D.; Hall, C.M. Pandemics, tourism and global change: A rapid assessment of COVID-19. J. Sustain. Tour. 2020, 1–20. [Google Scholar] [CrossRef]

- Fernandes, N. Economic Effects of Coronavirus Outbreak (COVID-19) on the World Economy. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Hartmann, N.N.; Lussier, B. Managing the sales force through the unexpected exogenous COVID-19 crisis. Ind. Mark. Manag. 2020, 88, 101–111. [Google Scholar] [CrossRef]

- Gustafson, E.J.; Kern, C.C.; Miranda, B.R.; Sturtevant, B.R.; Bronson, D.R.; Kabrick, J.M. Climate adaptive silviculture strategies: How do they impact growth, yield, diversity and value in forested landscapes? For. Ecol. Manag. 2020, 470–471, 118208. [Google Scholar] [CrossRef]

- UN. Shared Responsibility, Global Solidarity: Responding to the Socio-Economic Impacts of COVID-19. UN Secretary General, New York. 2020. Available online: https://www.un.org/sites/un2.un.org/files/sg_report_socio-economic_impact_of_covid19.pdf (accessed on 24 August 2020).

- Correa-García, J.A.; García-Benau, M.A.; García-Meca, E. Corporate governance and its implications for sustainability reporting quality in Latin American business groups. J. Clean. Prod. 2020, 260, 121142. [Google Scholar] [CrossRef]

- Lau, C.; Lu, Y.; Liang, Q. Corporate Social Responsibility in China: A Corporate Governance Approach. J. Bus. Ethics 2016, 136, 73–87. [Google Scholar] [CrossRef]

- Alzyoud, S.A.; Bani-Hani, K. Social Responsibility in Higher Education Institutions: Application case from the Middle East. Eur. Sci. J. 2015, 11, 122–129. Available online: http://eujournal.org/index.php/esj/article/view/5259 (accessed on 11 July 2020).

- Miko, N.U.; Kamardin, H. Impact of Audit Committee and Audit Quality on Preventing Earnings Management in the Pre- and Post- Nigerian Corporate Governance Code 2011. Procedia Soc. Behav. Sci. 2015, 172, 651–657. [Google Scholar] [CrossRef] [Green Version]

- Chen, J.; Cumming, D.; Hou, W.; Lee, E. CEO Accountability for Corporate Fraud: Evidence from the Split Share Structure Reform in China. J. Bus. Ethics 2016, 138, 787–806. [Google Scholar] [CrossRef] [Green Version]

- Luan, C.-J.; Chen, Y.-Y.; Huang, H.-Y.; Wang, K.-S. CEO succession decision in family businesses—A corporate governance perspective. Asia Pac. Manag. Rev. 2018, 23, 130–136. [Google Scholar] [CrossRef]

- Sudarto, S.; Takahashi, K.; Morikawa, K.; Nagasawa, K. The impact of capacity planning on product lifecycle for performance on sustainability dimensions in Reverse Logistics Social Responsibility. J. Clean. Prod. 2016, 133, 28–42. [Google Scholar] [CrossRef] [Green Version]

- Faccio, M.; Persona, A.; Sgarbossa, F.; Zanin, G. Sustainable SC through the complete reprocessing of end-of-life products by manufacturers: A traditional versus social responsibility company perspective. Eur. J. Oper. Res. 2014, 233, 359–373. [Google Scholar] [CrossRef]

- Doyle, E.; McGovern, D.; McCarthy, S.; Perez-Alaniz, M. Compliance-innovation: A quality-based route to sustainability. J. Clean. Prod. 2019, 210, 266–275. [Google Scholar] [CrossRef]

- Bilodeau, L.; Podger, J.; Abd-El-Aziz, A. Advancing campus and community sustainability: Strategic alliances in action. Int. J. Sustain. High. Educ. 2014, 15, 157–168. [Google Scholar] [CrossRef]

- Higgins, C.; Tang, S.; Stubbs, W. On managing hypocrisy: The transparency of sustainability reports. J. Bus. Res. 2020, 114, 395–407. [Google Scholar] [CrossRef]

- Ikram, M.; Sroufe, R.; Mohsin, M.; Solangi, Y.A.; Shah, S.Z.A.; Shahzad, F. Does CSR influence firm performance? A longitudinal study of SME sectors of Pakistan. J. Glob. Responsib. 2019, 11, 27–53. [Google Scholar] [CrossRef]

- Alsayegh, M.F.; Rahman, R.A.; Homayoun, S. Corporate Economic, Environmental, and Social Sustainability Performance Transformation through ESG Disclosure. Sustainability 2020, 12, 3910. [Google Scholar] [CrossRef]

- Taylor, J.; Vithayathil, J.; Yim, D. Are corporate social responsibility (CSR) initiatives such as sustainable development and environmental policies value enhancing or window dressing? Corp. Soc. Responsib. Environ. Manag. 2018, 25, 971–980. [Google Scholar] [CrossRef]

- Giannakis, M.; Papadopoulos, T. Supply chain sustainability: A risk management approach. Int. J. Prod. Econ. 2016, 171, 455–470. [Google Scholar] [CrossRef]

- Yadava, R.N.; Sinha, B. Scoring Sustainability Reports Using GRI 2011 Guidelines for Assessing Environmental, Economic, and Social Dimensions of Leading Public and Private Indian Companies. J. Bus. Ethics 2016, 138, 549–558. [Google Scholar] [CrossRef]

- Rehman, E.; Ikram, M.; Feng, M.T.; Rehman, S. Sectoral-based CO2 emissions of Pakistan: A novel Grey Relation Analysis (GRA) approach. Environ. Sci. Pollut. Res. 2020, 27, 29118–29129. [Google Scholar] [CrossRef]

- Liu, X.; Ji, X.; Zhang, D.; Yang, J.; Wang, Y. How public environmental concern affects the sustainable development of Chinese cities: An empirical study using extended DEA models. J. Environ. Manag. 2019, 251, 109619. [Google Scholar] [CrossRef]

- Ayuso, S.; Navarrete-Báez, F.E. How Does Entrepreneurial and International Orientation Influence SMEs’ Commitment to Sustainable Development? Empirical Evidence from Spain and Mexico. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 80–94. [Google Scholar] [CrossRef]

- LeBaron, G.; Lister, J.; Dauvergne, P. Governing Global Supply Chain Sustainability through the Ethical Audit Regime. Globalization 2017, 14, 958–975. [Google Scholar] [CrossRef] [Green Version]

- Goh, C.Y.; Marimuthu, M. The Path towards Healthcare Sustainability: The Role of Organisational Commitment. Procedia Soc. Behav. Sci. 2016, 224, 587–592. [Google Scholar] [CrossRef] [Green Version]

- Balogun, A.-L.; Marks, D.; Sharma, R.; Shekhar, H.; Balmes, C.; Maheng, D.; Arshad, A.; Salehi, P. Assessing the Potentials of Digitalization as a Tool for Climate Change Adaptation and Sustainable Development in Urban Centres. Sustain. Cities Soc. 2020, 53, 101888. [Google Scholar] [CrossRef]

- Chow, J. Mangrove management for climate change adaptation and sustainable development in coastal zones. J. Sustain. For. 2018, 37, 139–156. [Google Scholar] [CrossRef]

- Cai, W.; Lai, K.-H.; Liu, C.; Wei, F.; Ma, M.; Jia, S.; Jiang, Z.; Lv, L. Promoting sustainability of manufacturing industry through the lean energy-saving and emission-reduction strategy. Sci. Total. Environ. 2019, 665, 23–32. [Google Scholar] [CrossRef] [PubMed]

- Strantzali, E.; Aravossis, K. Decision making in renewable energy investments: A review. Renew. Sustain. Energy Rev. 2016, 55, 885–898. [Google Scholar] [CrossRef]

- Hadian, S.; Madani, K. A system of systems approach to energy sustainability assessment: Are all renewables really green? Ecol. Indic. 2015, 52, 194–206. [Google Scholar] [CrossRef]

- Sarkis, J.; Cohen, M.J.; Dewick, P.; Schröder, P. A brave new world: Lessons from the COVID-19 pandemic for transitioning to sustainable supply and production. Resour. Conserv. Recycl. 2020, 159, 104894. [Google Scholar] [CrossRef]

- Cohen, M.J. Does the COVID-19 outbreak mark the onset of a sustainable consumption transition? Sustain. Sci. Pract. Policy 2020, 16, 1–3. [Google Scholar] [CrossRef]

- J. Temple. MIT Technology Review. 2020. Available online: https://www.technologyreview.com/2020/03/09/905415/%0Acoronavirus-emissions-climate-change (accessed on 9 March 2020).

- Hsu, Y.-L.; Lee, C.-H.; Kreng, V. The application of Fuzzy Delphi Method and Fuzzy AHP in lubricant regenerative technology selection. Expert Syst. Appl. 2010, 37, 419–425. [Google Scholar] [CrossRef]

- Kardaras, D.K.; Karakostas, B.; Mamakou, X.J. Content presentation personalisation and media adaptation in tourism web sites using Fuzzy Delphi Method and Fuzzy Cognitive Maps. Expert Syst. Appl. 2013, 40, 2331–2342. [Google Scholar] [CrossRef]

- Kuo, Y.-F.; Chen, P.-C. Constructing performance appraisal indicators for mobility of the service industries using Fuzzy Delphi Method. Expert Syst. Appl. 2008, 35, 1930–1939. [Google Scholar] [CrossRef]

- Ma, Z.; Shao, C.; Ma, S.; Ye, Z. Constructing road safety performance indicators using Fuzzy Delphi Method and Grey Delphi Method. Expert Syst. Appl. 2011, 38, 1509–1514. [Google Scholar] [CrossRef]

- Saaty, R. The analytic hierarchy process—What it is and how it is used. Math. Model. 1987, 9, 161–176. [Google Scholar] [CrossRef] [Green Version]

- Sipahi, S.; Timor, M. The analytic hierarchy process and analytic network process: An overview of applications. Manag. Decis. 2010, 48, 775–808. [Google Scholar] [CrossRef]

- Forman, E.H.; Gass, S.I. The Analytic Hierarchy Process—An Exposition. Oper. Res. 2001, 49, 469–486. [Google Scholar] [CrossRef]

- Shah, S.A.A.; Solangi, Y.; Ikram, M. Analysis of barriers to the adoption of cleaner energy technologies in Pakistan using Modified Delphi and Fuzzy Analytical Hierarchy Process. J. Clean. Prod. 2019, 235, 1037–1050. [Google Scholar] [CrossRef]

- Lee, M.; Pham, H.; Zhang, X. A methodology for priority setting with application to software development process. Eur. J. Oper. Res. 1999, 118, 375–389. [Google Scholar] [CrossRef]

- Amran, A.; Lee, S.P.; Devi, S.S. The Influence of Governance Structure and Strategic Corporate Social Responsibility Toward Sustainability Reporting Quality. Bus. Strateg. Environ. 2014, 23, 217–235. [Google Scholar] [CrossRef]

- Adams, R.J.; Jeanrenaud, S.; Bessant, J.; Denyer, D.; Overy, P. Sustainability-oriented Innovation: A Systematic Review. Int. J. Manag. Rev. 2016, 18, 180–205. [Google Scholar] [CrossRef]

- Kim, S.; Ji, Y. Chinese Consumers’ Expectations of Corporate Communication on CSR and Sustainability. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 570–588. [Google Scholar] [CrossRef]