The Interconnection between Decent Workplace and Firm Financial Performance through the Mediation of Environmental Sustainability: Lessons from an Emerging Economy

,

,  , , ,

, , ,

Abstract

:1. Introduction

2. Literature Review

2.1. Workplace Sustainability

2.2. Theoretical Framework and Hypotheses Development

2.2.1. Workplace and Environmental Sustainability

2.2.2. Environmental Sustainability and Financial Performance

2.2.3. Workplace Sustainability and Financial Performance

2.2.4. Workplace, Environmental Sustainability, and Financial Performance

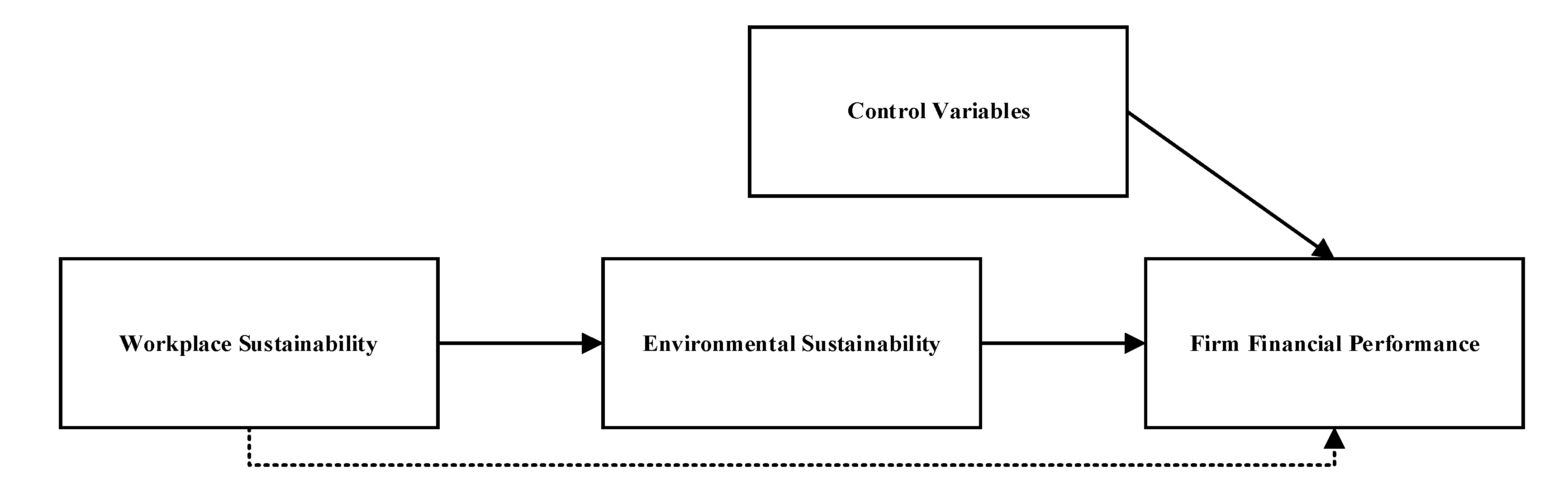

2.2.5. Conceptual Framework

3. Research Methods

3.1. Population and Sample

3.2. Statistical Techniques

- γ = Dependent Variable(s)

- it = i Representing for Firm and t Representing Year

- α1, α2 = Constants of 1st and 2nd stage, respectively

- β1𝑖𝑡 = Endogenous Independent Variable(s)

- γ1χit, γ2χit = Control Variables in 1st and 2nd stage, respectively

- δt = Year Dummies

- ηi = Industry Dummies

- θΖit = Instrumental Variable

- ε1it, ε2it = Error Terms of 1st and 2nd stage, respectively

4. Results and Discussion

5. Conclusions, Limitation and Future Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Workplace Sustainability | Environmental Sustainability |

|---|---|

| Decent Labor Practices | Environmental Management System (EMS) and Certifications |

| Minimum Wages for employees | Material Used and Produced |

| Workplace Ethical Values | Material Recycled |

| Employment Opportunities | Energy Consumption and Reduction |

| Occupational Health and Safety | Water Consumption |

| Training and Development | Biodiversity |

| Diversity and Equal Opportunities | Emissions including Greenhouse Gases (GHG) |

| Supplier’s Labor Assessment | Effluents and Waste Reductions |

| Protection of Human Rights | Product Environmental Impacts |

| Collective Bargaining Power | Transportation Impacts |

| Prevent Child and Compulsory Labor | Suppliers’ Environmental Impacts |

| Employees Satisfaction Survey | Environmental Related Awards |

| Shelters for Employees and their Family | |

| Anti-Corruption | |

| Sports and Work–life Balance | |

| Workplace Related Awards |

References

- Islam, M.A.; Hunt, A.; Jantan, A.H.; Hashim, H.; Chong, C.W. Exploring challenges and solutions in applying green human resource management practices for the sustainable workplace in the ready-made garment industry in Bangladesh. Bus. Strateg. Dev. 2019, 3. [Google Scholar] [CrossRef]

- Rehman, H.U.; Zahid, M.; Asif, M.; Ullah, Z. Sustainability Key Performance Indicators in Islamic Banking Industries of Malaysia and Pakistan: A Scale Based Evidence. J. Islam. Bus. Manag. 2020, 10, 65–79. [Google Scholar]

- Sustainable Development Goals (SDGs). Available online: https://sdgs.un.org/goals (accessed on 28 March 2021).

- WCED—World Commision on Environment and Development. Our Common Future; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- G4 Global Reporting Initiative Guidelines: Reporting Principles and Standard Disclosures. Available online: https://respect.international/g4-sustainability-reporting-guidelines-reporting-principles-and-standard-disclosures/ (accessed on 17 April 2021).

- Jan, A.; Mata, M.N.; Albinsson, P.A.; Martins, J.M.; Hassan, R.B.; Mata, P.N. Alignment of islamic banking sustainability indicators with sustainable development goals: Policy recommendations for addressing the covid-19 pandemic. Sustainability 2021, 13, 2607. [Google Scholar] [CrossRef]

- Neely, A.; Gregory, M.; Platts, K. Performance measurement system design: A literature review and research agenda. Int. J. Oper. Prod. Manag. 2005, 25, 1228–1263. [Google Scholar] [CrossRef]

- Zahid, M.; Rahman, H.U.; Muneer, S.; Butt, B.Z.; Isah-Chikaji, A.; Memon, M.A. Nexus Between Government Initiatives, Integrated Strategies, Internal Factors and Corporate Sustainability Practices in Malaysia. J. Clean. Prod. 2019, 241, 118329. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Laksmana, I.; Yang, Y. Board diversity and corporate investment oversight. J. Bus. Res. 2018, 90, 40–47. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef] [Green Version]

- Ehnert, I.; Parsa, S.; Roper, I.; Wagner, M.; Muller-Camen, M. Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world’s largest companies. Int. J. Hum. Resour. Manag. 2016, 27, 88–108. [Google Scholar] [CrossRef]

- Ehnert, I.; Harry, W.; Brewster, C.J. Sustainability and Human Resource Management; Springer: Berlin/Heidelberg, Germany, 2014; pp. 339–357. [Google Scholar] [CrossRef]

- Ehnert, I. Sustainability and human resource management: Reasoning and applications on corporate websites. Eur. J. Int. Manag. 2009, 3, 419. [Google Scholar] [CrossRef]

- Tang, G.; Chen, Y.; Jiang, Y.; Paillé, P.; Jia, J. Green human resource management practices: Scale development and validity. Asia Pac. J. Hum. Resour. 2018, 56, 31–55. [Google Scholar] [CrossRef]

- Shah, M. Green human resource management: Development of a valid measurement scale. Bus. Strateg. Environ. 2019, 28, 771–785. [Google Scholar] [CrossRef]

- Roscoe, S.; Subramanian, N.; Jabbour, C.J.C.; Chong, T. Green human resource manageacment and the enablers of green aorganisational culture: Enhancing a firm’s environmental performance for sustainable development. Bus. Strateg. Environ. 2019, 28, 737–749. [Google Scholar] [CrossRef]

- Yong, J.Y.; Yusliza, M.; Ramayah, T.; Chiappetta Jabbour, C.J.; Sehnem, S.; Mani, V. Pathways towards sustainability in manufacturing organizations: Empirical evidence on the role of green human resource management. Bus. Strateg. Environ. 2019, 29, 212–228. [Google Scholar] [CrossRef]

- Zahid, M.; Rehman, H.U.; Mirza, M.Z.; Memon, M.A. Workplace Sustainability in Emerging Economies: A Comprehensive Evidence from Malaysia. City Univ. Res. J. 2019, 9, 498–512. [Google Scholar]

- Mirza, M.Z.; Isha, A.S.N.; Memon, M.A.; Azeem, S.; Zahid, M. Psychosocial safety climate, safety compliance and safety participation: The mediating role of psychological distress. J. Manag. Organ. 2019, 1–16. [Google Scholar] [CrossRef]

- Soytas, M.A.; Denizel, M.; Usar, D.D. Addressing endogeneity in the causal relationship between sustainability and financial performance. Int. J. Prod. Econ. 2019, 210, 56–71. [Google Scholar] [CrossRef]

- Zahid, M.; Rahman, H.U.; Khan, M.; Ali, W.; Shad, F. Addressing endogeneity by proposing novel instrumental variables in the nexus of sustainability reporting and firm financial performance: A step-by-step procedure for non- experts. Bus. Strateg. Environ. 2020, 29, 3086–3103. [Google Scholar] [CrossRef]

- GRI—Global Reporting Initiative. G4 Global Reporting Initiative Guidelines: Reporting Principles and Standard Disclosures; Global Reporting Initiative: Boston, MA, USA, 2013; Available online: https://respect.international/g4-sustainability-reporting-guidelines-implementation-manual/ (accessed on 28 March 2021).

- Freeman, R.E. Strategic Management Stakeholder Approach; Cambridge University Press: Cambridge, UK, 1984; Volume 3, pp. 38–48. [Google Scholar] [CrossRef]

- GRI—Global Reporting Initiative. Sustainability Reporting Guideline; Global Reporting Initiative: Boston, MA, USA, 2002; pp. 1–104. [Google Scholar]

- Drew, E.N. Personnel Selection, Safety Performance, and Job Performance: Are Safe Workers Better Workers? Ph.D. Thesis, Florida International University, Miami, FL, USA, 2014; pp. 1–137. [Google Scholar]

- Chan, C.K.-C.; Hui, E.S.-I. The Dynamics and Dilemma of Workplace Trade Union Reform in China: The Case of the Honda Workers’ Strike. J. Ind. Relations 2012, 54, 653–668. [Google Scholar] [CrossRef]

- Round, J.; Williams, C.C.; Rodgers, P. Corruption in the post-Soviet workplace: The experiences of recent graduates in contemporary Ukraine. Work. Employ. Soc. 2008, 22, 149–166. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Devinney, T.M.; Auger, P.; Eckhardt, G.; Birtchnell, T. The Other CSR: Consumer Social Responsibility. Stanf. Soc. Innov. Rev. 2006. [Google Scholar] [CrossRef]

- Delai, I.; Takahashi, S. Sustainability measurement system: A reference model proposal. Soc. Responsib. J. 2011, 7, 438–471. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Vallance, S.; Perkins, H.C.; Dixon, J.E. What is social sustainability? A clarification of concepts. Geoforum 2011, 42, 342–348. [Google Scholar] [CrossRef]

- Ehnert, I. Sustainable Human Resource Management; Springer: Berlin/Heidelberg, Germany, 2009. [Google Scholar]

- Kramar, R. Beyond strategic human resource management: Is sustainable human resource management the next approach? Int. J. Hum. Resour. Manag. 2014, 25, 1069–1089. [Google Scholar] [CrossRef]

- Wagner, M. “Green” Human Resource Benefits: Do they Matter as Determinants of Environmental Management System Implementation? J. Bus. Ethics 2013, 114, 443–456. [Google Scholar] [CrossRef]

- Rayner, J.; Morgan, D. An empirical study of ‘green’ workplace behaviours: Ability, motivation and opportunity. Asia Pac. J. Hum. Resour. 2017, 56. [Google Scholar] [CrossRef]

- Jamal, T.; Zahid, M.; Martins, J.M.; Mata, M.N.; Rahman, H.U.; Mata, P.N. Perceived Green Human Resource Management Practices and Corporate Sustainability: Multigroup Analysis and Major Industries Perspectives. Sustainability 2021, 13, 3045. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Dixon-Fowler, H.R.; Slater, D.J.; Johnson, J.L.; Ellstrand, A.E.; Romi, A.M. Beyond “Does it Pay to be Green?” A Meta-Analysis of Moderators of the CEP-CFP Relationship. J. Bus. Ethics 2013, 112, 353–366. [Google Scholar] [CrossRef] [Green Version]

- Mahoney, L.; Roberts, R.W. Corporate social performance, financial performance and institutional ownership in Canadian firms. Account. Forum 2007, 31, 233–253. [Google Scholar] [CrossRef]

- Wagner, M. How to reconcile environmental and economic performance to improve corporate sustainability: Corporate environmental strategies in the European paper industry. J. Environ. Manag. 2005, 76, 105–118. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Saleh, M.; Zulkifli, N.; Muhamad, R. Looking for evidence of the relationship between corporate social responsibility and corporate financial performance in an emerging market. Asia Pac. J. Bus. Adm. 2011, 3, 165–190. [Google Scholar] [CrossRef] [Green Version]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Molloy, L.; Erekson, H.; Gorman, R. Exploring the relationship between environmental and financial performance. In Proceedings of the Workshop on Capital Markets and Environmental Performance; US Environmental Protection Agency: Laguna Beach, CA, USA; pp. 1–55.

- Allouche, J.; Laroche, P. A meta-analytical investigation of the relationship between corporate social and financial performance. Rev. Gest. Ressour. Hum. 2005, 57, 18–41. [Google Scholar]

- Wagner, M.; Schaltegger, S.; Wehrmeyer, W. A Review of Empirical Studies Concerning the Relationship Between Environmental and Economic Performance: What Does the Evidence Tell Us? Centre for Sustainability Management: Lüneburg, Germany, 2001; Volume 2001. [Google Scholar]

- Mishra, S.; Suar, D. Does Corporate Social Responsibility Influence Firm Performance of Indian Companies? J. Bus. Ethics 2010, 95. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- O’Riordan, L.; Fairbrass, J. Corporate Social Responsibility (CSR): Models and Theories in Stakeholder Dialogue. J. Bus. Ethics 2008, 83, 745–758. [Google Scholar] [CrossRef]

- Finch, N. The motivations for adopting sustainability disclosure. Management 2005, 22. [Google Scholar] [CrossRef]

- Tomsic, N.; Bojnec, S.; Simcic, B. Corporate sustainability and economic performance in small and medium sized enterprises. J. Clean. Prod. 2015, 108, 603–612. [Google Scholar] [CrossRef]

- Renwick, D.W.S.; Redman, T.; Maguire, S. Green Human Resource Management: A Review and Research Agenda*. Int. J. Manag. Rev. 2013, 15, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Economic Planning Unit. Eleventh Malaysian Plan Executive Summary. Rancangan Malaysia Kesebelas (Eleventh Malaysia Plan): 2016–2020. 2016. Available online: http://apps-cfm.ump.edu.my/others/glory/doc/RMK11/BI/11MP Summary BI.pdf (accessed on 19 May 2020).

- Bursa Malaysia. Corporate Social Responsibility (CSR) Framework for Malaysian Public Listed Companies. 2006. Available online: https://www.scribd.com/document/76636360/Csr-Writeup (accessed on 23 June 2019).

- Zahid, M.; Rehman, H.U.; Khan, M.A. ESG in Focus: The Malaysian Evidence. City Univ. Res. J. 2018, 9, 72–84. [Google Scholar]

- Anas, A.; Abdul Rashid, H.M.; Annuar, H.A. The effect of award on CSR disclosures in annual reports of Malaysian PLCs. Soc. Responsib. J. 2015, 11, 831–852. [Google Scholar] [CrossRef]

- Lee, S.; Singal, M.; Kang, K.H. The corporate social responsibility-financial performance link in the U.S. restaurant industry: Do economic conditions matter? Int. J. Hosp. Manag. 2013, 32, 2–10. [Google Scholar] [CrossRef]

- Zahid, M.; Rehman, H.U.; Ali, W.; Khan, M.; Alharthi, M.; Qureshi, M.I.; Jan, A. Boardroom gender diversity: Implications for corporate sustainability disclosures in Malaysia. J. Clean. Prod. 2019, 244, 8683. [Google Scholar] [CrossRef]

- Gao, J.; Bansal, P. Instrumental and Integrative Logics in Business Sustainability. J. Bus. Ethics 2013, 112, 241–255. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting: Evidence from Four Countries. Harv. Bus. Sch. Res. Work. Pap. 2017, 1–34. Available online: http://ssrn.com/abstract=1799589 (accessed on 17 April 2021).

- Dissanayake, D.; Tilt, C.; Xydias-Lobo, M. Sustainability reporting by publicly listed companies in Sri Lanka. J. Clean. Prod. 2016, 129, 169–182. [Google Scholar] [CrossRef]

- Kansal, M.; Joshi, M.; Batra, G.S. Determinants of corporate social responsibility disclosures: Evidence from India. Adv. Account. 2014, 30, 217–229. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Introductory Econometrics; South-Western Cengage Learning: Mason, OH, USA, 2013; Volume 120–121. [Google Scholar]

- Whittington, J.L.; Galpin, T.J. The engagement factor: Building a high-commitment organization in a low-commitment world. J. Bus. Strategy 2010, 31, 14–24. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. Embedded Versus Peripheral Corporate Social Responsibility: Psychological Foundations. Ind. Organ. Psychol. 2013, 6, 314–332. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Zutshi, A.; Ahmad, N. An integrated management systems approach to corporate sustainability. Eur. Bus. Rev. 2011, 23, 353–367. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 6th ed.; Pearson Prentice Hall Upper Saddle River: Hoboken, NJ, USA, 2006. [Google Scholar]

- Baron, R.; Kenny, D. The moderator-mediator variable distinction in social psychological research. J. Pers. Soc. Psychol. 1986, 51, 1173. [Google Scholar] [CrossRef] [PubMed]

- Preacher, K.J.; Hayes, A.F. SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behav. Res. Methods Instrum. Comput. 2004, 36, 717–731. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Preacher, K.J.; Rucker, D.D.; Hayes, A.F. Addressing Moderated Mediation Hypotheses: Theory, Methods, and Prescriptions. Multivar. Behav. Res. 2007, 42, 185–227. [Google Scholar] [CrossRef] [PubMed]

| No. | Sectors | No. of Sample Companies | Percent |

|---|---|---|---|

| 1. | Consumer | 30 | 10 |

| 2. | Trading | 51 | 17 |

| 3. | Industrial | 48 | 16 |

| 4. | Plantation | 24 | 8 |

| 5. | Hotels | 6 | 2 |

| 6. | Real estate | 15 | 5 |

| 7. | Infrastructure | 9 | 3 |

| 8. | Properties | 30 | 10 |

| 9. | Technology | 33 | 11 |

| 10. | Finance | 9 | 3 |

| 11. | Construction | 42 | 14 |

| 12. | Mining | 3 | 1 |

| Total | 300 | 100 |

| Min | Max | Mean | S.D | Skewness | Kurtosis | |||

|---|---|---|---|---|---|---|---|---|

| Stat | S.E | Stat | S.E | |||||

| Return on equity | –1.113 | 0.89 | 0.090 | 16.549 | 0.000 | 0.083 | –0.098 | 0.165 |

| Workplace sustainability | 1 | 17 | 5.83 | 2.645 | 1.234 | 0.083 | 2.222 | 0.165 |

| Environmental sustainability | 2 | 12 | 4.43 | 2.865 | 0.492 | 0.083 | –0.425 | 0.165 |

| Firm size | 4.440 | 9.53 | 5.569 | 0.755 | 0.029 | 0.083 | –0.272 | 0.165 |

| Firm age | 1 | 43 | 15.99 | 8.036 | 0.134 | 0.083 | –0.661 | 0.165 |

| Firm leverage | 0.00 | 67.87 | 1.37 | 0.216 | –0.029 | 0.083 | –0.155 | 0.165 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Return on equity (1) | 1 | |||||

| Workplace sustainability (2) | 0.187 ** | 1 | ||||

| Environmental sustainability (3) | 0.084 * | 0.630** | 1 | |||

| Firm size (4) | 0.153 ** | 0.300 ** | 0.231 ** | 1 | ||

| Firm age (5) | –0.083 * | 0.166 ** | 0.147 ** | 0.189 ** | 1 | |

| Firm leverage (6) | –0.015 | 0.085 * | 0.034 | 0.234 ** | 0.005 | 1 |

| (OLS) | (2SLS) | (OLS) | (2SLS) | (OLS) | (2SLS) | |

|---|---|---|---|---|---|---|

| Environmental | Environmental | ROE | ROE | ROE | ROE | |

| Workplace sustainability | 0.632 *** | 0.839 *** | 0.871 *** | 1.267 ** | ||

| (0.030) | (0.075) | (0.204) | (0.541) | |||

| Environmental sustainability | 0.427 ** | 2.028 *** | ||||

| (0.194) | (0.648) | |||||

| Firm size | 0.047 *** | 0.033 *** | 0.231 *** | 0.117 | 0.212 ** | 0.155 |

| (0.012) | (0.013) | (0.083) | (0.112) | (0.090) | (0.096) | |

| Firm age | 0.009 | 0.005 | –0.248 *** | –0.348 *** | –0.257 *** | –0.371 *** |

| (0.010) | (0.010) | (0.070) | (0.076) | (0.068) | (0.072) | |

| Firm leverage | 0.000 | –0.000 | –0.005 ** | –0.005 * | –0.005 * | –0.005 * |

| (0.000) | (0.000) | (0.002) | (0.003) | (0.003) | (0.003) | |

| Lag of DV | –0.009 | –0.010 | 0.335 *** | –0.018 | 0.327 *** | 0.685 *** |

| (0.025) | (0.026) | (0.031) | (0.190) | (0.058) | (0.116) | |

| Constant | –1.479 | –2.493 * | –13.431 ** | 2.351 | –15.314 ** | –4.950 |

| (0.941) | (1.446) | (6.479) | (11.734) | (6.021) | (12.419) | |

| Obs. | 877 | 877 | 877 | 877 | 877 | 877 |

| R-squared | 0.457 | 0.427 | 0.202 | 0.025 | 0.214 | 0.161 |

| Durbin (score) chi2(1) | 9.754 | 7.678 | 1.415 | |||

| p–value | 0.065 | 0.064 | 0.234 | |||

| Wu-Hausman F | 9.639 | 7.570 | 1.385 | |||

| p–value | 0.075 | 0.061 | 0.239 | |||

| Years Dummy | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry Dummy | Yes | Yes | Yes | Yes | Yes | Yes |

| Mediation Model | ||||

|---|---|---|---|---|

| Independent Variable | Mediating Variable | Dependent var. | Indirect Effect (t–Value)/ Confidence Interval | Mediation |

| Workplace Sustainability | Environmental Sustainability | Financial Performance (ROE) | 3.97 | Yes |

| [0.121–0.328] | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zahid, M.; Martins, J.M.; Rahman, H.U.; Mata, M.N.; Shah, S.A.; Mata, P.N. The Interconnection between Decent Workplace and Firm Financial Performance through the Mediation of Environmental Sustainability: Lessons from an Emerging Economy. Sustainability 2021, 13, 4570. https://0-doi-org.brum.beds.ac.uk/10.3390/su13084570

Zahid M, Martins JM, Rahman HU, Mata MN, Shah SA, Mata PN. The Interconnection between Decent Workplace and Firm Financial Performance through the Mediation of Environmental Sustainability: Lessons from an Emerging Economy. Sustainability. 2021; 13(8):4570. https://0-doi-org.brum.beds.ac.uk/10.3390/su13084570

Chicago/Turabian StyleZahid, Muhammad, José Moleiro Martins, Haseeb Ur Rahman, Mário Nuno Mata, Syed Asim Shah, and Pedro Neves Mata. 2021. "The Interconnection between Decent Workplace and Firm Financial Performance through the Mediation of Environmental Sustainability: Lessons from an Emerging Economy" Sustainability 13, no. 8: 4570. https://0-doi-org.brum.beds.ac.uk/10.3390/su13084570