A Non-Market Valuation Approach to Environmental Cost-Benefit Analysis for Sanitary Landfill Project Appraisal

Abstract

:1. Introduction

1.1. Background of the Study

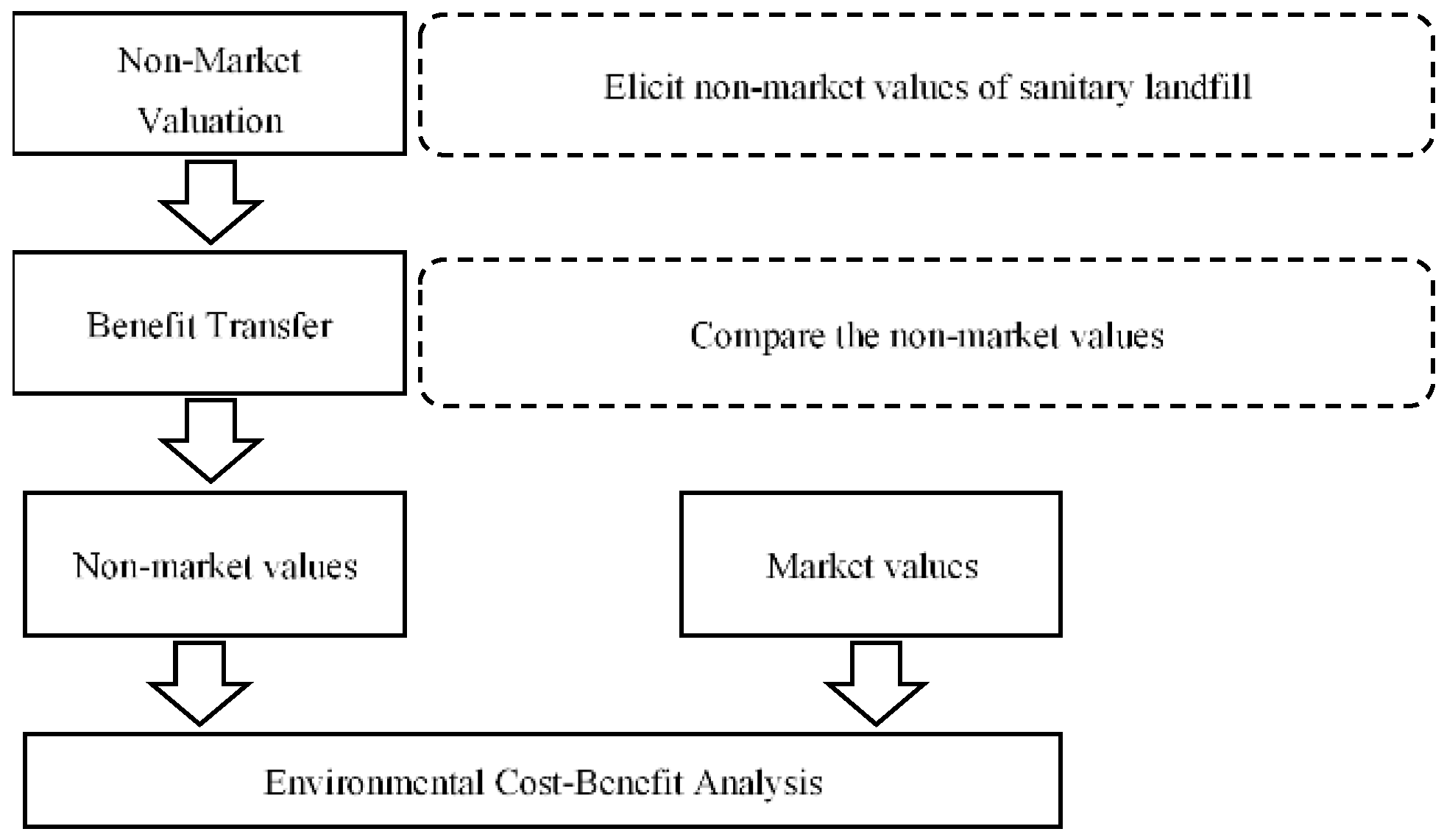

1.2. Conceptual Framework of Environmental Cost-Benefit Analysis

2. Materials and Methods

2.1. Non-Market Valuation by Choice Modeling

2.2. Benefit Transfer

2.3. Environmental Cost-Benefit Analysis

3. Results

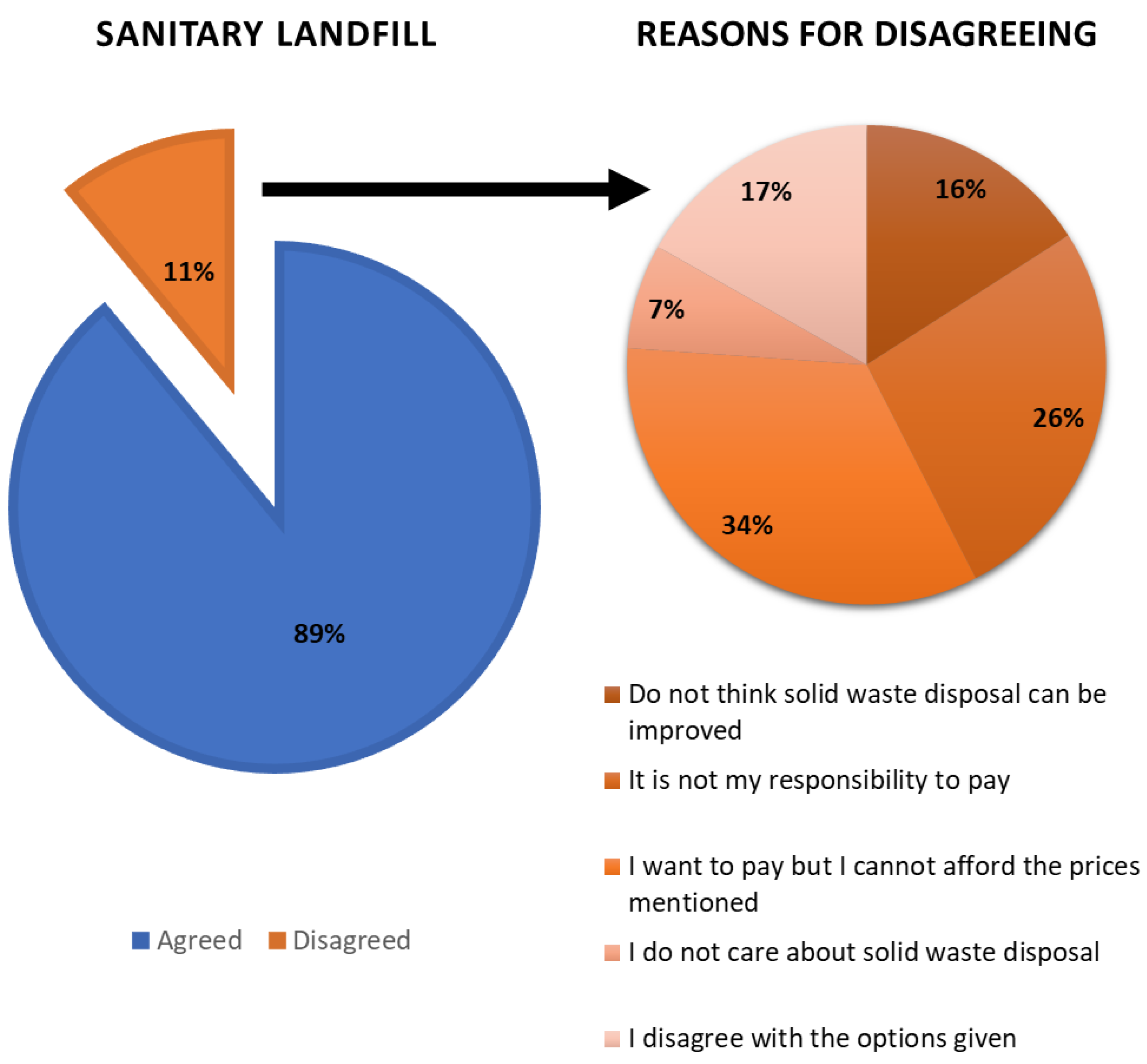

3.1. Environmental Values of a Sanitary Landfill

3.2. Transferability of the Environmental Values of the Sanitary Landfill

3.3. Environmental Cost-Benefit Analysis for the Sanitary Landfill

3.3.1. Identified Costs and Benefits

3.3.2. Estimation of Net Present Values

4. Discussions

4.1. Environmental Values from Non-Market Valuation

4.2. Transferable Environmental Values

4.3. Environmental Cost-Benefit Analysis

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Matheson, T. Disposal Is Not Free: Fiscal Instruments to Internalize the Environmental Costs of Solid Waste; International Monetary Fund Working Paper; IMF: Washington, DC, USA, 2019. [Google Scholar]

- Idowu, I.A.; Atherton, W.; Hashim, K.; Kot, P.; Alkhaddar, R.; Alo, B.I.; Shaw, A. An analysis of the status of landfill classification systems in developing countries: Sub Saharan Africa landfill experiences. Waste Manag. 2019, 87, 761–771. [Google Scholar] [CrossRef]

- Tchobanoglous, G.; Theisen, H.; Vigil, S.A. Integrated Solid Waste Management: Engineering Principles and Management Issues; McGraw Hill Int.: New York, NY, USA, 1993; pp. 7–21. [Google Scholar]

- Kamaruddin, M.A.; Yusoff, M.S.; Rui, L.M. An overview of municipal solid waste management and landfill leachate treatment: Malaysia and Asian perspectives. Environ. Sci. Pollut. Res. 2007, 24, 26988–27020. [Google Scholar] [CrossRef]

- Aziale, L.K.; Asafo-Adjei, E. logistic challenges in urban waste management in Ghana (a case of tema metropolitan assembly). Eur. J. Bus. Manag. 2013, 5, 116–128. [Google Scholar]

- Korhonen, J.; Honkasalo, A.; Seppälä, J. Circular economy: The concept and its limitations. Ecol. Econ. 2018, 143, 37–46. [Google Scholar] [CrossRef]

- Hogland, M.; Āriņa, D.; Kriipsalu, M.; Jani, Y.; Kaczala, F.; de Sá Salomão, A.L.; Hogland, W. Remarks on four novel landfill mining case studies in Estonia and Sweden. J. Mater. Cycles Waste Manag. 2017, 20, 1355–1363. [Google Scholar] [CrossRef]

- Laner, D.; Esguerra, J.L.; Krook, J.; Horttanainen, M.; Kriipsalu, M.; Rosendal, R.M.; Stanisavljević, N. Systematic assessment of critical factors for the economic performance of landfill mining in Europe: What drives the economy of landfill mining? Waste Manag. 2019, 95, 674–686. [Google Scholar] [CrossRef] [PubMed]

- Devadoss, P.S.; Agamuthu, P.; Mehran, S.B.; Santha, C.; Fauziah, S.H. Implications of municipal solid waste management on greenhouse gas emissions in Malaysia and the way forward. Waste Manag. 2021, 119, 135–144. [Google Scholar] [CrossRef] [PubMed]

- Paes, L.A.; Bezerra, B.S.; Deus, R.M.; Jugend, D.; Gomes Battistelle, R.A. Organic solid waste management in a circular economy perspective—A systematic review and SWOT analysis. J. Clean. Prod. 2019, 239, 118086. [Google Scholar] [CrossRef]

- Gutberlet, J. Informal and cooperative recycling as a poverty eradication strategy. Geogr. Compass. 2012, 6, 19–34. [Google Scholar] [CrossRef]

- Sohoo, I.; Ritzkowski, M.; Kuchta, K.; Cinar, S. Environmental Sustainability Enhancement of Waste Disposal Sites in Developing Countries through Controlling Greenhouse Gas Emissions. Sustainability 2021, 13, 151. [Google Scholar] [CrossRef]

- Sasao, T. An estimation of the social costs of landfill siting using a choice experiment. Waste Manag. 2004, 24, 753–762. [Google Scholar] [CrossRef] [Green Version]

- Guikema, S.D. An estimation of the social costs of landfill siting using a choice experiment. Waste Manag. 2005, 25, 331–333. [Google Scholar] [CrossRef]

- Damigos, D.; Kaliampakos, D.; Menegaki, M. How much are people willing to pay for efficient waste management schemes? A benefit transfer application. Waste Manag. Res. 2016, 34, 1–11. [Google Scholar] [CrossRef]

- Martins, A.M.; Cró, S. Impact of tourism on solid waste generation and management cost in madeira island for the period 1996–2018. Sustainability 2021, 13, 5238. [Google Scholar] [CrossRef]

- Ko, S.; Kim, W.; Shin, S.; Shin, J. The economic value of sustainable recycling and waste management policies: The case of a waste management crisis in South Korea. Waste Manag. 2020, 104, 220–227. [Google Scholar] [CrossRef] [PubMed]

- Gebreeyosus, M.A.; Berhanu, W. Households’ preferences for improved solid waste management options in Aksum city, North Ethiopia: An application of choice modelling. Cogent Environ. Sci. 2019, 5. [Google Scholar] [CrossRef]

- Woretaw, E.; Woubishet, D.; Asmare, W. Households’ preferences and willingness to pay for improved solid waste management interventions using choice experiment approach: Debre Tabor Town, Northwest Ethiopia. J. Econ. Sustain. Dev. 2017, 8, 16–32. [Google Scholar]

- Dobraja, K.; Barisa, A.; Rosa, M. Cost-benefit analysis of integrated approach of waste and energy management. Energy Procedia 2015, 95, 104–111. [Google Scholar] [CrossRef] [Green Version]

- Zhou, C.; Gong, Z.; Hu, J.; Cao, A.; Liang, H. A cost-benefit analysis of landfill mining and material recycling in china. Waste Manag. 2015, 35, 191–198. [Google Scholar] [CrossRef] [PubMed]

- Mutavchi, V. Solid Waste Management Based on Cost-Benefit Analysis Using the WAMED Model. Ph.D. Thesis, Linnaeus University, Växjö, Sweden, 2012. [Google Scholar]

- Begum, R.A.; Siwar, C.; Pereira, J.J.; Jaafar, A.H. A benefit–cost analysis on the economic feasibility of construction waste minimization: The case of Malaysia. Resour. Conserv. Recycl. 2006, 48, 86–98. [Google Scholar] [CrossRef]

- Yedla, S.; Parikh, J.K. Economic evaluation of a landfill system with gas recovery for municipal solid waste management: A case study. Int. J. Environ. Pollut. 2001, 15, 433. [Google Scholar] [CrossRef]

- Jeanty, P.W.; Haab, T.; Hitzhusen, F. Willingness to pay for biodiesel in diesel engines: A stochastic double bounded contingent valuation survey. In Proceedings of the American Agricultural Economics Association Annual Meeting, Portland, OR, USA, 29 July–1 August 2007. [Google Scholar]

- Hasan-Basri, B.; Abd Karim, M.Z. Can benefits in recreational parks in Malaysia be transferred? A choice experiment (ce) technique. Int. J. Tour. Res. 2014, 18, 19–26. [Google Scholar] [CrossRef]

- Hanley, N.; Wright, R.E.; Alvarez-Farizo, B. Estimating the economic value of improvements in river ecology using choice experiments: An application to the water framework directive. J. Environ. Manag. 2006, 78, 183–193. [Google Scholar] [CrossRef]

- Morrison, M.; Bennett, J. Valuing New South Wales rivers for use in benefit transfer. Aust. J. Agric. Resour. Econ. 2004, 48, 591–611. [Google Scholar] [CrossRef] [Green Version]

- Johnston, R.J.; Duke, J.M. Willingness to Pay and Policy Process Attributes. Am. J. Agric. Econ. 2007, 89, 1098–1115. [Google Scholar] [CrossRef]

- Morrison, M.; Bennett, J.; Blamey, R.; Louviere, J. Choice Modeling and tests of benefit transfer. Am. J. Agric. Econ. 2002, 84, 161–170. [Google Scholar] [CrossRef]

- Carolus, J.F.; Hanley, N.; Olsen, S.B.; Pedersen, S.M. A bottom-up approach to environmental cost-benefit analysis. Ecol. Econ. 2018, 152, 282–295. [Google Scholar] [CrossRef] [Green Version]

- Atkinson, G.; Groom, B.; Hanley, N.; Mourato, S. environmental valuation and benefit-cost analysis in U.K. policy. J. Benefit-Cost Anal. 2018, 9, 97–119. [Google Scholar] [CrossRef] [Green Version]

- Pellizzoni, L. Uncertainty and participatory democracy. Environ. Values 2003, 12, 195–224. [Google Scholar] [CrossRef]

- Perni, A.; Martínez-Paz, J.M. A participatory approach for selecting cost-effective measures in the WFD context: The Mar Menor (SE Spain). Sci. Total Environ. 2013, 458, 303–311. [Google Scholar] [CrossRef]

- Wright, S.A.L.; Fritsch, O. Operationalising active involvement in the EU Water Framework Directive: Why, when and how? Ecol. Econ. 2011, 70, 2268–2274. [Google Scholar] [CrossRef]

- Fischer, A.R.H.; Wentholt, M.T.A.; Rowe, G.; Frewer, L.J. Expert involvement in policy development: A systematic review of current practice. Sci. Public Policy 2013, 41, 332–343. [Google Scholar] [CrossRef] [Green Version]

- Manski, C.H. The Structure of Random Utility Models. Theory Decis. 1977, 8, 229–254. [Google Scholar] [CrossRef]

- Krinsky, I.; Robb, A.L. On approximating the statistical properties of elasticities. Rev. Econ. Stat. 1986, 68, 715. [Google Scholar] [CrossRef] [Green Version]

- Foster, V.; Mourato, S. Valuing the multiple impacts of pesticide use in the UK: A contingent ranking approach. J. Agric. Econ. 2008, 51, 1–21. [Google Scholar] [CrossRef]

- Pek, C.-K.; Jamal, O. A choice experiment analysis for solid waste disposal option: A case study in Malaysia. J. Environ. Manag. 2011, 92, 2993–3001. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Jamal, O. Economic valuation of household preference for solid waste management in Malaysia: A choice modeling approach. Int. J. Manag. Studies 2007, 14, 189–212. [Google Scholar]

- KBMC. News of MPKB. Available online: http://www.mpkbbri.gov.my/ms/mpk/pusat-media/akhbar/kerja-tiga-syif-bersih-bandar-kota-bharu (accessed on 26 April 2018).

- Chong, T.L.; Matsufuji, Y.; Hassan, M.N. Implementation of the semi-aerobic landfill system (Fukuoka method) in developing countries: A Malaysia cost analysis. Waste Manag. 2005, 25, 702–711. [Google Scholar] [CrossRef] [PubMed]

- Nadzri, Y. The way forward: Solid waste management in Malaysia. In Proceedings of the 10th Annual Waste Management Conference and Exhibition, Kuala Lumpur, Malaysia, 19 July 2013. [Google Scholar]

- Zhuang, J.; Liang, Z.; Lin, T.; De-Guzman, F. Theory and Practice in the Choice of Social Discount Rate in Cost Benefit Analysis: A Survey; Economics and Research Department; ERD Working Paper No. 94; Asian Development Bank: Metro Manila, Philippines, 20 May 2007. [Google Scholar]

- Ahmed, S.A.; Ali, S.M. People as partners: Facilitating people’s participation in public–private partnerships for solid waste management. Habitat Int. 2006, 30, 781–796. [Google Scholar] [CrossRef]

- Guerrero, L.A.; Maas, G.; Hogland, W. Solid waste management challenges for cities in developing countries. Waste Manag. 2013, 33, 220–232. [Google Scholar] [CrossRef]

- Lu, H.; Sidortsov, R. Sorting out a problem: A co-production approach to household waste management in Shanghai, China. Waste Manag. 2019, 95, 271–277. [Google Scholar] [CrossRef]

- Moh, Y.C.; Abd Manaf, L. Overview of household solid waste recycling policy status and challenges in Malaysia. Resour. Conserv. Recycl. 2014, 82, 50–61. [Google Scholar] [CrossRef]

- Choon, S.-W.; Tan, S.-H.; Chong, L.L. The perception of households about solid waste management issues in Malaysia. Environ. Dev. Sustain. 2016, 19, 1685–1700. [Google Scholar] [CrossRef]

- Kubanza, N.; Simatele, M.D. Sustainable solid waste management in developing countries: A study of institutional strengthening for solid waste management in Johannesburg, South Africa. J. Environ. Plan. Manag. 2019, 63, 175–188. [Google Scholar] [CrossRef]

- Kahn, J.R.; Vásquez, W.F.; de Rezende, C.E. Choice modeling of system-wide or large scale environmental change in a developing country context: Lessons from the Paraíba do Sul River. Sci. Total Environ. 2017, 598, 488–496. [Google Scholar] [CrossRef]

- Diaz, L.F. Waste management in developing countries and the circular economy. Waste Manag. Res. 2017, 35, 1–2. [Google Scholar] [CrossRef] [PubMed]

- Haas, W.; Krausmann, F.; Wiedenhofer, D.; Heinz, M. How circular is the global economy?: An assessment of material flows, waste production, and recycling in the European Union and the world in 2005. J. Ind. Ecol. 2015, 19, 765–777. [Google Scholar] [CrossRef]

- Rathore, P.; Sarmah, S.P. Economic, environmental and social optimization of solid waste management in the context of circular economy. Comput. Ind. Eng. 2020, 145, 106510. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Methods | Previous Related Studies | Scope |

|---|---|---|

| Non-Market Valuation | Ko et al. (2020) | Solid waste management |

| Gabreeyosus and Berhanu (2019) | Solid waste management | |

| Czajkowski et al. (2014) | Recycling | |

| Li et al. (2014) | Waste to energy incinerator | |

| Khee and Jamal (2011) | Solid waste disposal | |

| Ku et al. (2009) | Solid waste management | |

| Jamal (2007) | Solid waste management | |

| Jin et al. (2005) | Solid waste management | |

| Sasao (2004) | Solid waste management | |

| Cost-Benefit Analysis | Begum et al. (2006) | Solid waste disposal |

| Dobraja et al. (2015) | Waste to energy incinerator | |

| Zhou et al. (2014) | Landfill mining | |

| Mutavchi (2012) | Solid waste management | |

| Kumar et al. (2004) | Landfill | |

| Yedla and Parikh (2001) | Landfill | |

| Chong et al. (2005) | Sanitary landfill | |

| Liu, Zhang and Wang (2020) | Recycling project |

| Attribute | Definition | Levels |

|---|---|---|

| Leachate | Discharge of toxic liquid formed from degraded waste and rainwater | 1: Untreated discharge (Status Quo) |

| 2: Half-treated discharge | ||

| 3: Fully treated discharge | ||

| Bad odor | Presence of bad odor due to disposed waste in the landfill | 1: Strong (Status Quo) |

| 2: Distinct | ||

| 3: Weak | ||

| 4: No odor | ||

| Disease vector | Breeding of vectors (e.g., rats, mosquitoes, flies) in the landfill | 1: Uncontrolled (Status Quo) |

| 2: Controlled | ||

| View | Aesthetic surrounding of the landfill | 1: Unpleasant (Status Quo) |

| 2: Pleasant | ||

| Additional fee | Additional fee for sanitary landfill incorporated into annual assessment payment | 1: No payment (Status Quo) |

| 2: RM3 per month | ||

| 3: RM5 per month | ||

| 4: RM7 per month |

| Variables | Multinomial Logit | Nested Logit | ||

|---|---|---|---|---|

| Kota Bharu | Bachok | Kota Bharu | Bachok | |

| Leachate discharge | 0.313 *** (0.042) | 0.675 *** (0.091) | 0.342 *** (0.044)) | 0.675 *** (0.092) |

| Bad odor | 0.267 *** (0.036) | 0.421 *** (0.076) | 0.320 *** (0.040) | 0.421 *** (0.076) |

| Disease vector | 1.382 *** (0.081) | 1.963 *** (0.204) | 1.593 *** (0.096) | 1.972 *** (0.205) |

| View | 0.464 *** (0.073) | 0.661 *** (0.149) | 0.555 *** (0.080) | 0.661 *** (0.150) |

| Additional solid waste management fee | −0.109 *** (0.014) | −0.184 *** (0.029) | −0.120 *** (0.015) | −0.185 *** (0.029) |

| Inclusive value parameters | ||||

| Improvement | 0.368 *** (0.110) | 1.195 (1.942) | ||

| No improvement (fixed parameters) | 1 | 1 | ||

| Summary Statistics | ||||

| Log likelihood | −1502.589 | −268.232 | −1403.218 | −283.919 |

| Pseudo-R2 | 0.13 | 0.33 | 0.43 | 0.64 |

| Iterations completed | 6 | 31 | 26 | 11 |

| Observations | 1872 | 572 | 1872 | 572 |

| Attribute | Multinomial Logit Model | Nested Logit Model | ||

|---|---|---|---|---|

| Kota Bharu | Bachok | Kota Bharu | Bachok | |

| Leachate discharge | 2.87 | 3.66 | 2.87 | 3.65 |

| Bad odor | 2.44 | 2.29 | 2.68 | 2.28 |

| Disease vector | 12.63 | 10.66 | 13.33 | 10.67 |

| View | 4.24 | 3.59 | 4.64 | 3.58 |

| Attribute | Extended Multinomial Logit Model | Nested LogitModel | ||

|---|---|---|---|---|

| Kota Bharu | Bachok | Kota Bharu | Bachok | |

| Leachate discharge | 2.87 *** (2.34, 3.40) | 3.66 *** (3.54, 3.78) | 2.87 *** (2.85, 2.89) | 3.65 *** (3.64, 3.65) |

| Bad odor | 2.44 *** (2.00, 2.87) | 2.29 *** (2.21, 2.37) | 2.68 (−1.74, 7.09) | 2.28 (0.13, 4.43) |

| Disease vector | 12.63 *** (10.92, 14.35) | 10.66 *** (10.37,10.96) | 13.33 (11.37,15.29) | 10.67 *** (10.32, 11.02) |

| View | 4.24 *** (3.36, 5.11) | 3.59 *** (3.44, 3.74) | 4.64 (1.50, 7.78) | 3.58 (−10.47,17.63) |

| Crude Dumping Landfill (Status Quo) | Sanitary Landfill | ||

|---|---|---|---|

| Year | Year | ||

| Costs | Costs | ||

| Land cost | 0 | Capital cost | 0 |

| Operation cost | 1 to 25 | Operation cost | 1 to 24 |

| Machine rental | 1 to 25 | Closure cost | 25 |

| Benefits | Benefits | ||

| Revenues from solid waste disposal fee | 0 to 25 | Revenues from solid waste disposal fee | 0 to 25 |

| Additional payment for solid waste disposal fee | 0 to 25 | ||

| Discount Rate | ||

|---|---|---|

| 5% | 10% | |

| Crude dumping landfill | ||

| Net Present Value | −16,604,762 | −10,089,451 |

| Benefit-Cost Ratio | 0.82 | 0.83 |

| Sanitary landfill | ||

| Net Present Value | 50,264,040 | 32,618,078 |

| Benefit-Cost Ratio | 1.50 | 1.50 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nik Ab Rahim, N.N.R.; Othman, J.; Hanim Mohd Salleh, N.; Chamhuri, N. A Non-Market Valuation Approach to Environmental Cost-Benefit Analysis for Sanitary Landfill Project Appraisal. Sustainability 2021, 13, 7718. https://0-doi-org.brum.beds.ac.uk/10.3390/su13147718

Nik Ab Rahim NNR, Othman J, Hanim Mohd Salleh N, Chamhuri N. A Non-Market Valuation Approach to Environmental Cost-Benefit Analysis for Sanitary Landfill Project Appraisal. Sustainability. 2021; 13(14):7718. https://0-doi-org.brum.beds.ac.uk/10.3390/su13147718

Chicago/Turabian StyleNik Ab Rahim, Nik Nor Rahimah, Jamal Othman, Norlida Hanim Mohd Salleh, and Norshamliza Chamhuri. 2021. "A Non-Market Valuation Approach to Environmental Cost-Benefit Analysis for Sanitary Landfill Project Appraisal" Sustainability 13, no. 14: 7718. https://0-doi-org.brum.beds.ac.uk/10.3390/su13147718