1. Introduction

The COVID-19 pandemic, recognized by the WHO in March 2020, affected worldwide daily routines, from the way we interact and relate to others to the way we work or shop, influencing socioeconomic behavioral patterns [

1,

2,

3].

During the pandemic, consumption patterns changed [

1,

4,

5,

6], mainly due to the sanitary measures and imposed restrictions such as lockdowns, physical store closures, limited opening hours and stores’ reduced capacity and social distancing [

7,

8,

9]. At the same time, the payment market has changed, as cash payments were identified as a potential carrier of the virus. Due to that, the card payment acceptance infrastructure has been dynamically developing and consumers have been encouraged to use it [

10,

11].

Fear of contagion and restrictions imposed over a prolonged period have caused economic, social, and even psychological problems [

1,

3], having a significant impact in the context of sustainable consumption. Panic and social anxiety became the main reason for the change in consumption behavioral patterns [

11], which often translated into making ill-considered and hasty purchasing decisions. Since the pandemic outbreak, consumers’ reactions have evolved, from the impulsive buying of basic products [

1,

12] to avoiding shopping in physical stores [

12], causing fluctuations between the demand and supply sides.

It needs to be highlighted that the consumption patterns developed during the COVID-19 health crisis have been unusual and are unknown so far, according to retail experts [

13], and go far beyond the impulse buying of staple products [

12]. The health crisis has also increased consumers’ awareness and commitment to environmental issues, mindful consumption, and sustainability. For this reason, it is important to investigate the phenomenon of impulse buying in the new social situation of the COVID-19 pandemic.

The main purpose of this research is to investigate credit card usage as a trigger for fast fashion impulse buying [

14,

15,

16,

17] during the COVID-19 pandemic. For the purposes of the work, the following research questions were developed:

RQ1: Is there a relationship between the use of credit cards and impulsive buying behavior among consumers during the pandemic?

RQ2: What hedonic motivations are affecting impulsive buying behavior during the pandemic?

RQ3: Is there a relationship between the use of credit cards and hedonic motivations affecting impulsive buying behavior?

In the first part of the paper, the authors have conducted a literature review on cashless payments, motivations for impulse buying, and the impact of fashion consumption on sustainable development. The main part of the work is devoted to the presentation and quantitative analysis of results of an online survey of 300 regular fast fashion buyers in physical stores in 2020. In addition to the core of this investigation, hedonic motivations in fast fashion and their relationship with credit card use are analyzed, as well as the relationship between hedonic motivations and impulse buying in fast fashion [

18]. The work ends with a discussion and presentation of conclusions from the conducted research.

2. Literature Review

2.1. Contactless Payment and Credit Card Use

Today, consumers have at their disposal a myriad of technological solutions that enable cashless payments through physical credit cards or digital credit cards on smartphones or smartwatches [

19]. At the same time, a plethora of factors affect what payment method will be chosen by consumers to fulfil transactions [

20], among them the speed of transaction [

21] and perceived characteristics of the payment method in terms of, for example, ease of use or safety [

22].

A study performed in 2019 on payment behavior in the European area realized by European Central Bank [

23] shows that Spain is a country with generally substantial cash usage. About 83% of the number of transactions and 66% in terms of value were performed using cash. It should be noted, however, that during 2020 (during the COVID-19 pandemic), 50.2% of Spaniards adopted more cashless behavior [

10]. However, the increase in cashless payment use has not been uniform across all industries. For instance, the overall credit card use in both physical stores and online fast fashion stores during the restriction period in Spain fell by 27% [

24]. This may be related to the fact that many people lost their jobs or had a reduced income during the pandemic. Therefore, it can be assumed that consumption expenditure may have encountered budgetary constraints.

2.2. Impulse Buying

Impulsive buying is unplanned, thoughtless, spontaneous, and hedonically complex buying behavior [

25]. Impulsivity reveals the consumer’s willingness to make purchases unintentionally, unreflectively, immediately, and based on internal and/or external stimuli [

26,

27]. Among these stimuli, internal motivations classified into hedonic and utilitarian [

28] influence the purchase decision process [

29]. In addition, the relationship between fast fashion and consumers’ hedonic motivations to purchase the latest trends has a tremendous negative impact on sustainability, causing environmental damage [

30]. The issue of impulsive buying is the subject of research by many researchers around the world [

3,

25,

31,

32,

33,

34,

35]. As part of some research conducted by many researchers, it has been found so far that the most important factors influencing impulsive buying are credit card use [

3,

14,

16,

17,

36], gratification shopping [

3,

31,

37] and novelty-seeking shopping [

3,

30,

38,

39,

40]. Therefore, it can be assumed that some of those factors might also apply in the COVID-19 pandemic, leading to unsustainable decisions among consumers. Limited budgets, prolonged quarantines, and lockdowns could translate into the need for social or gratification impulsive shopping (need of social interaction), and usage of credit cards (relaxing budgetary constraints). Still, there are not many papers that directly address the situation related to the COVID-19 pandemic. Chauhan, Banerjee and Dagar [

3] have attempted to explain changes in behavior of conducting fashion purchases online. The lack of available research on changes in purchases at physical stores was one of the factors influencing the authors’ decision to undertake this research.

2.3. Hedonic Shopping Motivations

Hedonic motivations are internal factors that seek to satisfy needs for pleasure, enjoyment, searching for experiences, entertainment, excitement, and socialization during the shopping process [

31]. Additionally, some claim that hedonic motivations are positively related to impulsive buying behavior [

32].

Arnold and Reynolds [

37] proposed an inventory of six types of hedonic buying motivations:

- 1.

Gratification shopping relieves stress, improves mood, and provides emotional gratification [

41,

42].

- 2.

Idea or novelty shopping satisfies the need to keep up with fashion trends and triggers impulsive buying [

33,

38].

- 3.

Adventure-seeking shopping is related to the excitement and stimulation produced by the act of shopping and may be a trigger for impulsive buying [

39,

40,

43].

- 4.

Value shopping refers to getting more value at a lower price [

36] and relates positively to impulsive buying behavior [

26].

- 5.

Social shopping refers to motivations based on the need for social interactions and can trigger impulsive buying, according to several authors [

34,

35].

- 6.

Role shopping is motivated by the mere enjoyment of shopping for others.

2.4. Fashion Consumption and Sustainability

As behavioral economists point out, the act of shopping for fashion provides consumers with satisfaction and personal fulfilment [

44]; the latter is strongly rooted in hedonic motivations such as the search for emotional satisfaction, aesthetic criteria, amusement, symbolic meaning, sensory stimulation, socialization, or expression of social status [

39].

Therefore, shopping for fashion, or fast fashion in particular, is related to hedonic motivations and to the hedonic value and pleasure experienced when shopping [

45]. Clothing, footwear, and jewelry are products with high symbolic value, as they express and define shoppers’ identity, personality, appearance, and mood [

46].

Four aspects of sustainability relate to fashion industry: (i) sustainable production, (ii) green marketing, (iii) green information sharing, and (iv) green attitude and education. Our interest focus on the last one, inherent to customer behavior [

47,

48,

49,

50,

51].

Sustainability within the fast fashion sector was a challenge even before the COVID-19 pandemic [

52]. The idea of fast fashion and sustainability is quite paradoxical as the fast fashion accelerated business model relies on a globalized supply chain, low prices and speed in production and distribution, features that do not apply to sustainable practices and are contrary to the fast fashion business model itself. Consequently, fast fashion brands replenish stocks and introduce new trendy items on a weekly basis, making fashion consumers keep coming back [

53]. Some researchers point out that consumers feel concerned about sustainability and do believe that their behavior has a positive impact, but this knowledge does not influence their buying decision [

54]. This so called “intention-behavior gap” is particularly conspicuous in fast fashion and within consumer attitudes to sustainability.

2.5. Fast Fashion and Impulsive Buying Behavior

The fast fashion business model provides luxury fashion imitations at a low price and with a short shelf life [

55,

56]. The sense of urgency when purchasing fast fashion relies on recurrent consumption and impulse buying. As a consequence, fast fashion consumption enhances the consumer behavioral pattern of buying more but using items less frequently, which leads us to question its social and environmental impacts [

57]. Moreover, the behavioral pattern of fast fashion consumers has a detrimental impact on the environment, where the waste of outdated or unwanted outfits accounts for some 17 million tons, according to the figures from the Environmental Protection Agency. Therefore, fast fashion is one of the most polluting industries as it requires an important quantity of raw materials, generates water pollution and accounts for 10% of global CO2 emissions through both its “just-in-time” production model and its supply chain [

58].

The Spanish brand Zara is recognized as the fast fashion company par excellence, followed by two other brands, the Swedish brand H&M and the Dutch brand C&A [

59,

60,

61]. Retailers such as Zara and H&M can offer up to 24 collections per year, encouraging so called “throwaway fashion” and over-consumption [

62].

Fast fashion products, due to their high degree of symbolism, are considered as hedonic and can trigger impulsive buying behavior, as pointed out by several authors [

18,

45].

Internal variables involved in the impulsive buying of fast fashion include emotions produced by the mere act of shopping for fashion [

45], emotional gratification [

63], generation of positive mood states [

36], and fashion involvement [

64]. Therefore, interest in fashion trends is directly related to fast fashion impulsive buying behavior [

65].

2.6. Mediating Role of Credit Card Use in Impulsive Buying

Credit card availability and use are positively related to consumer spending and stimulate impulsive buying behavior [

66,

67,

68]. Several investigations point out that credit card use accelerates the decision-making process and increases consumer satisfaction [

69] in fast fashion impulsive buying [

16,

17]. Therefore, credit card use in fast fashion is a trigger for impulse buying behavior and has a detrimental impact on sustainability and on responsible consumption.

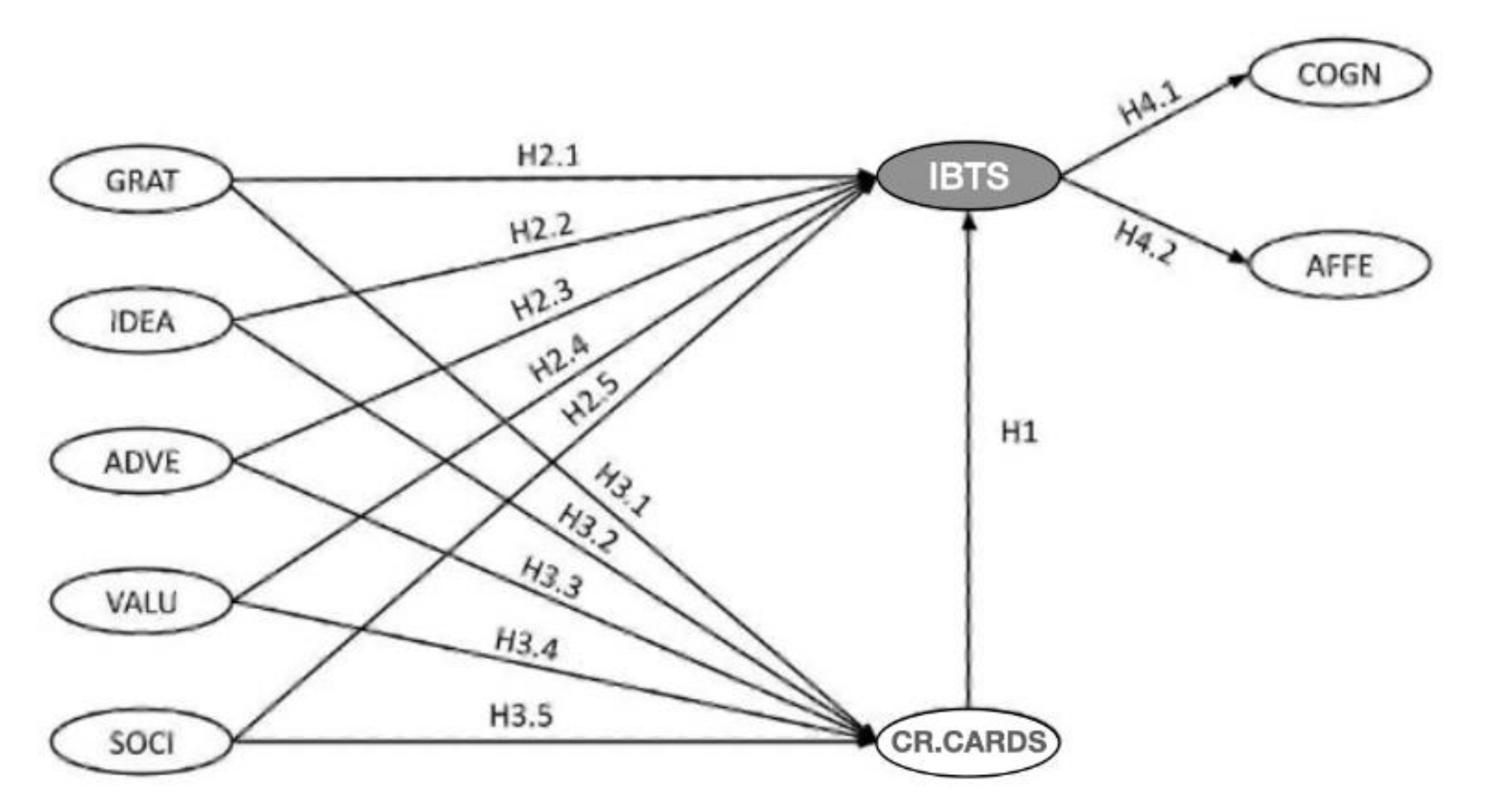

3. Research Hypothesis

This investigation seeks to determine the relationship between credit card use as a trigger for the impulsive buying of fast fashion products during the COVID-19 pandemic, as well as the relationship between credit card use and hedonic motivations (see

Section 2.3 for a description of the terms used within hypotheses). Based on the analyzed theory and according to the hypotheses formulated, the theoretical model is presented in

Figure 1.

From these relationships, the following hypotheses, presented in

Table 1, emerge.

4. Methodology

In this research, quantitative techniques have been used to analyze the relationship between the chosen variables of fast fashion impulsive buying in physical stores in Spain between the months of June and July 2021.

4.1. Sample and Data Collection

The data were collected through a self-administered online questionnaire using the Survey Monkey platform on a sample of regular fast fashion consumers who reported having shopped in physical fast fashion stores (Zara, H&M, C&A, Primark) between June 2020 and July 2021. The chosen period corresponds to the reopening of physical stores, unconstrained mobility across all Spanish provinces and the end of strict lockdown. The sample was made up of 300 participants, aged between 18 and 55 years old, living in the urban areas of Madrid and Barcelona and shopping in physical stores in one of the main fast fashion brands: Zara, H&M, Primark or C&A. A total of 289 valid responses were obtained.

4.2. Instruments

The self-administered questionnaire of four blocks of questions included sociodemographic variables, the impulse buying tendency scale (IBTS) [

70], the hedonic motivations scale [

37] and the credit card use scale [

71]. Sociodemographic variables included age, sex, marital status, level of education, as well as the payment methods used during purchase.

The IBTS [

70] was used to find the propensity of impulsive buying of fast fashion products in physical stores. The IBTS has been used and validated by, e.g., Dawson and Kim [

26] and Činjarević et al. [

72]; it measures affective (AFFE) (10 items) and cognitive (COGN) (10 items) components of impulsive buying tendency. A version adapted to impulsive buying in physical fast fashion stores was created through expert consensus (Delphi technique) and was subjected to be reviewed to determine its validity.

Hedonic shopping motivations [

37] were measured through a six-factor hedonic shopping motivations scale (gratification-seeking shopping motivations (GRAT), novelty-seeking (idea) shopping motivations (IDEA), value-seeking shopping motivations (VALU), adventure-seeking shopping motivations (ADVE), social shopping motivations (SOCI), and role shopping motivations). In this investigation, the role-shopping factor was removed after determining it was irrelevant. The hedonic motivations scale was used and validated by Nguyen et al. [

28] and Özen and Kodaz [

73].

The credit card use scale [

71] measures the level of payment responsibility, credit risk, and extravagance–prudence. The credit card use scale was used and validated by, e.g., Khare [

74]. For this research, 10 questions were selected to measure the credit card use among fast fashion shoppers in physical stores in Spain during the COVID-19 sanitary crisis (4 for risk measurement, 4 for extravagance–prudence, and 2 for card payment).

5. Results

The collected data were processed and analyzed using structural equation models (SEMs). Valid data from 289 consumers were collected according to the established criteria (

Table 2).

5.1. Validity and Reliability

Once the descriptive analyses were accomplished for all the measurement scales and considered valid, exploratory factor analysis was carried out. In particular, the suitability of the data for subsequent factor analysis was analyzed, as along with dimensionality and reliability.

It was found that in the sample, the determinant of the correlation matrices was minimal and close to 0, while in the anti-image correlation matrices, the elements that were not part of the diagonals were close to 0 or less than 0.3 and the values of the diagonals were close to 1 or greater than 0.8.

The Kaisser–Meyer–Olkin (KMO) test for the scales shows values greater than 0.5, and, in the case of Bartlett’s sphericity, the degree of significance was p < 0.001 (***).

Three psychometric properties of the scale dimensionality were evaluated: (i) number of extracted factors (must be 1), (ii) loading factor (must be greater than 0.5), and (iii) variance explained by each extracted factor (must exceed 60%).

The scale reliability showed Cronbach’s Alpha greater than 0.7, and the total item correlation was greater than 0.3.

5.2. Exploratory Factor Analysis of the Hedonic Motivations

The results of the validity and reliability tests of the Hedonic Motivations Scale are presented in

Table 3.

5.3. Exploratory Factor Analysis of Impulsive Buying Scale and Credit Card Use

The first evaluation of dimensionality and reliability for the Impulsive Buying Tendency Scale and Credit Card Use Scale did not meet the required parameters for the factor loadings of 10 items (from a total of 45 items), as well as for the variance and Cronbach’s Alpha for the Use of a Credit Card Scale and cognitive section of the Impulsive Buying Tendency Scale. To address these non-compliances, items were removed from those scales, and dimensionality and reliability analyses were repeated. After these analyses, the factorial loads, variances, and Cronbach’s Alpha met the necessary established parameters, maintaining their suitability.

It should be noted that the values of the variance obtained were 58.16%, 58.78%, and 57.21% for the COGN, AFFE, and CREDIT CARD scales, respectively. Although these values are slightly below the established limit of 60%, according to Hair et al. [

73] in the field of social sciences, such slightly lower values can be admitted. Therefore, these values validate the dimensionality analysis.

Once the second exploratory factor analysis has been carried out, it is confirmed that both scales are unidimensional and have sufficient reliability to continue with their subsequent confirmatory and structural analysis (

Table 4).

5.4. Confirmatory Factor Analysis of Measurement Models

Once the model was identified, the goodness of fit, reliability, convergence, and discriminant validity was analyzed.

A confirmatory factor analysis was carried out to demonstrate that the IBTS was a multidimensional variable. For this purpose, the correct identification of the measurement model was corroborated, verifying that the number of degrees of freedom was greater than zero. It was confirmed that the structure does not have contradictory estimates. The goodness of fit results are shown in

Table 5.

The reliability analysis and its convergent validity are shown in

Table 6.

The model’s discriminant validity analysis data are shown in

Table 7.

Confirmatory factor analysis results corroborate that the IBTS scale can be considered a multidimensional scale of the second order. The correct identification of the measurement model was verified along with the goodness of fit (

Table 8).

The GFI (absolute fit) parameter value of 0.877 does not reach the established limit of 0.9. However, according to Subhash [

75,

76], this parameter can be considered valid above 0.8. The parameters of AGFI (0.852) and NFI (0.884) do not reach 0.9. However, these parameters can also be considered valid above 0.8 [

76] or 0.85 in the case of AGFI [

77].

The convergent validity and reliability analysis are shown in

Table 9.

Although the estimate of the standardized load should be greater than 0.5, in the case of the item CC_4, it was 0.498. However, given the proximity of the value to the recommended minimum and the correct validation of the rest of the parameters analyzed for this scale, it can be considered acceptable and, therefore, maintained for the following phases. The data from the discriminant validity analysis of the model are shown in

Table 10.

According to the results of the variance test, it is observed that the square root of the AVE of each factor is always higher than the correlations of that factor with the rest of the factors.

5.5. Structural Equation Model

Once the model was identified, its goodness of fit was analyzed, as well as its nomological validity. The goodness-of-fit model was analyzed and found to be almost identical to the goodness of fit of the measurement model. Therefore, the modification indices do not justify the need to eliminate any additional item (

Table 11).

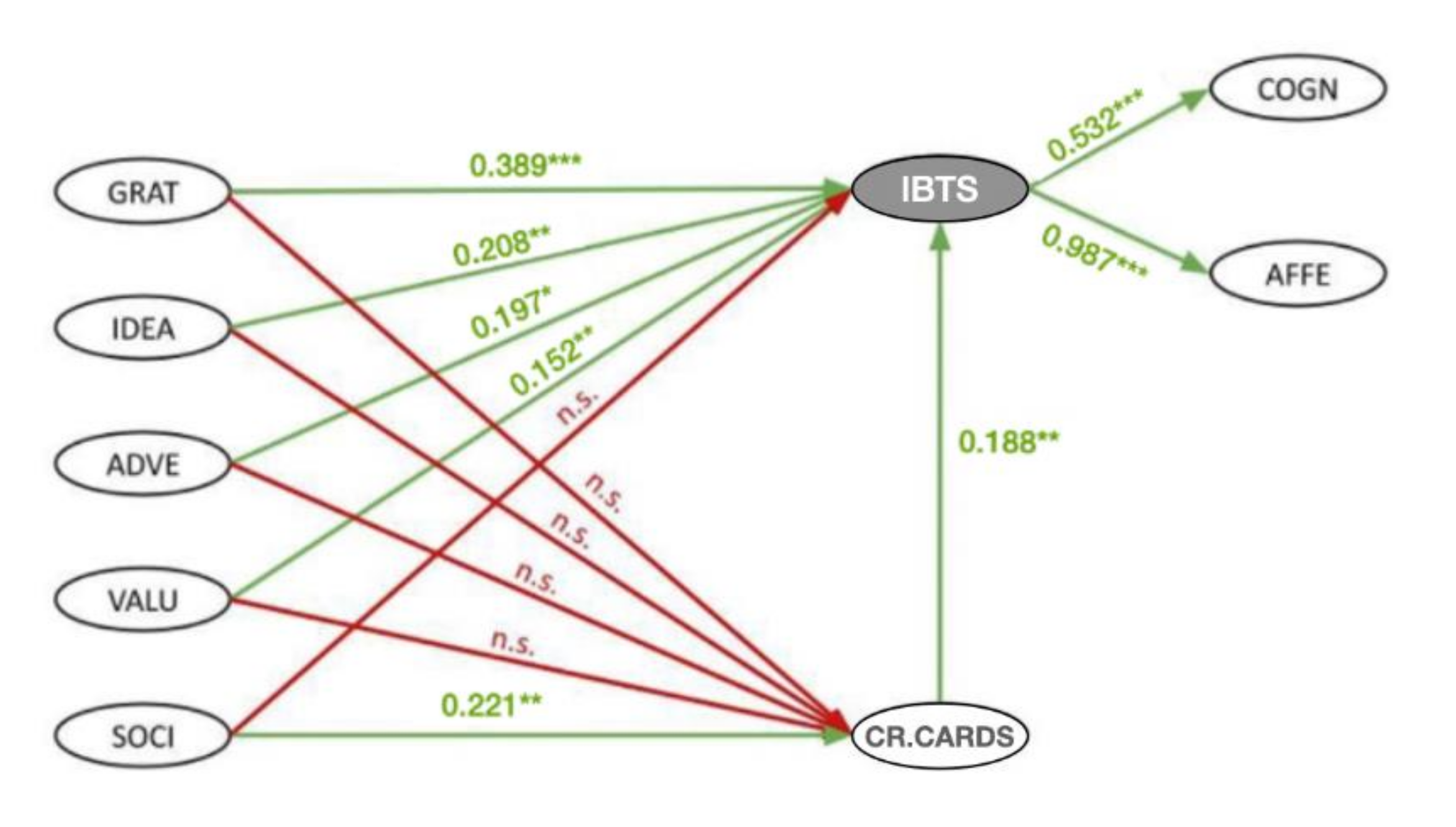

6. Results: Conceptual Summary

The scheme of the structural model is presented in

Figure 2. The factorial loads of the different causal or measurement relationships and the acceptance or not of their corresponding hypotheses are shown.

A summary with the details of each of the research hypotheses related to causal and measurement relationships is shown in

Table 12.

7. Discussion

This investigation aims to shed light on credit card use and its relationship with hedonic motivations and impulsive buying behavior in fast fashion physical stores in Spain during the COVID-19 era and its impact on responsible consumption of fast fashion mitigating environmental damages.

Answering research question RQ1, the findings of this study indicate that credit card use has a positive relationship with fast fashion impulsive buying (H1: 0.188), in line with previous findings on impulsive buying behavior and especially on fashion impulsive buying [

3,

14,

16,

17,

36]. Having a credit card, in the case of a reduced budget and rising prices as a result of COVID-19, gave consumers an apparent sense of financial security and satisfaction while shopping.

Contrary to the above, there is no statistically significant relationship between credit card use and hedonic motivations such as gratification shopping (H2.1), adventure-seeking shopping (H2.2), novelty-seeking shopping (H2.3), and value-seeking shopping (H2.4). This means that the use of a credit card is not directly related to most hedonic motivations. However, there is a positive relationship between social shopping motivations (H2.5: 0.221) and credit card use, possibly due to the strong need for social interactions and entertainment after a prolonged period of stay-at-home orders, curfews, quarantines, and social distancing. The data above can be clearly considered a response to research question RQ3. A sudden social and economic change in the form of a pandemic had a significant and negative impact on the mentality of society. After opening stores, consumers could unload their emotions through socialization and shopping with a tool that allows them to deceptively expand their wallets, resulting in unsustainable purchases.

Answering research question RQ2 regarding hedonic motivations as a trigger for fast fashion impulsive buying behavior, the results show that during COVID-19, gratification shopping motivations are the strongest (H3.1: 0.389); therefore, the need for mood enhancement or comfort during this time of distress is positively related to the impulsive buying of fast fashion products [

41,

42,

72]. Similar results on gratification shopping motivations have been presented in previous studies by many authors [

3,

31,

37]. This means that even during the COVID-19 pandemic, gratification seeking is an important trigger for fast fashion impulsive and reckless shopping.

Consumers who experienced idea or novelty-seeking motivations (H3.2: 0.208) show a very similar behavioral pattern in making impulsive purchases in physical fast fashion stores as gratification-seeking shoppers. These results are supported by previous findings on fashion interest and impulsive buying, where similar behavior was observed among consumers in Croatia [

78].

Entertainment or adventure-seeking shopping also shows a positive relationship with fast fashion impulsive buying behavior in physical stores during the COVID-19 era (H3.3: 0.197). These results are undoubtedly consistent with previous studies related to the search for stimulation and new sensations during the shopping trip to a store [

42,

79].

Similarly, there is a positive relationship between value-seeking motivations while shopping and fast fashion impulsive buying (H3.4: 0.152), which is consistent with similar findings on these types of motivations triggering impulsive buying. The authors of previous studies indicated that value-seeking is one of the key factors influencing impulsive buying [

72,

80]. During COVID-19, many consumers may buy things they do not necessarily need just because of a seemingly good price.

Contrary to the above, the relationship between motivations for social shopping and impulsive buying of fast fashion products during COVID-19 was not statistically significant. The reason could be explained by the fear of contagion.

As for H4.1. and H4.2., the results suggest that the analyzed measurement relationships show the suitability of the IBTS, with which the fast fashion impulse buying construct has been measured. It is important to note that the results of the measurement relationship of the affective subscale (0.987) are notably higher than those of the cognitive subscale.

8. Conclusions

Based on the results obtained, it can be concluded that the use of credit cards positively influences the impulsive buying behavior for fast fashion products in physical stores, even with the limitations and restrictions imposed to avoid contagion during the COVID-19 health crisis. Therefore, the findings show that credit card availability and credit card use could be important triggers for impulse buying for fast fashion, a fact that raises concerns about the environmental, social, and ethical breaches caused by the fast fashion industry.

Similarly, of the five hedonic motivations, only social shopping motivations are positively related to credit card use during the COVID-19 era, pointing out the need for social interactions during the lockdown and social distancing period. As many people lost their jobs or had a reduced income, credit cards eased and relaxed their budgets, enabling social participation and interactions in stores.

However, it should be noted that aside from the social factor and use of credit card connection, other factors such as gratification shopping, adventure-seeking shopping, idea-seeking shopping, and value-seeking shopping motivations are also positively related to impulse buying of fast fashion products in physical stores during COVID-19. At this point, it should be emphasized that in the new social situation, which is the pandemic, consumers ignore the environmental costs of their shopping habits, emphasizing the magnitude of the problem.

This research has had among its limitations the restrictions caused by the COVID-19 pandemic, which has not only affected the shopping conditions for purchasing fast fashion products but also the selection of convenient sampling among Spanish fast fashion consumers in the urban areas of Madrid and Barcelona. Therefore, replication of this research is proposed as a future line of research once the COVID-19 pandemic is over.

The authors emphasize the need to continue investigating the consumer behavior and the adoption of cashless technology at the point of sale and its impact on impulsive buying behavior without the limitations imposed by restrictions due to COVID-19. As impulse buying and hedonic motivations are a buying trigger for fast fashion products, there is a need for changes in the fast fashion business model towards focusing on sustainable practices. Hedonic motivations could positively influence green attitudes as some consumers identify themselves with green trends as an expression of their self-concept and image [

79,

80,

81,

82,

83]; nonetheless, there is still a gap between awareness of green attitudes and actual behavior. Future research should be conducted on a wider level globally, or at least at the interstate level. This would enable us to understand consumer attitudes towards sustainable fashion and delve deeper into how sustainability and sustainable practices influence customers’ decision-making processes. The authors recommend further research which could influence the development of activities that, with the proper recommendations of governments and other stakeholders, could reduce the phenomenon of impulsive buying. The main tasks, taking into account COVID-19 changes, could include: (a) proper education on the rationality of purchasing, (b) proper education of credits and loans, or (c) offering financial planning tools (PFM). With those implemented, it will be possible to achieve a positive impact on sustainable development in the fashion sector not only in Spain, but all over the world.

Author Contributions

Conceptualization, B.G. and J.L.d.O.; methodology, B.G. and M.P.; validation, B.G., M.P. and J.L.d.O.; formal analysis, B.G. and M.P.; investigation, B.G. and M.P.; resources, J.L.d.O. and M.P.; data curation, B.G. and M.P.; writing—original draft preparation, B.G. and M.P.; writing—review and editing, B.G. and M.P.; visualization, B.G.; supervision, M.P. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by the National Science Centre, Poland under Grant No. 2017/26/E/HS4/00858.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Xiao, H.; Zhang, Z.; Zhang, L. A diary study of impulsive buying during the COVID-19 pandemic. Curr. Psychol. 2020, 1–13. [Google Scholar] [CrossRef] [PubMed]

- Jo, H.; Shin, E.; Kim, H. Changes in consumer behaviour in the post-COVID-19 era in Seoul, South Korea. Sustainability 2021, 13, 136. [Google Scholar] [CrossRef]

- Chauhan, S.; Banerjee, R.; Dagar, V. Analysis of Impulse Buying Behaviour of Consumer During COVID-19: An Empirical Study. Millenn. Asia 2021, 09763996211041215. [Google Scholar] [CrossRef]

- Bounie, D.; Camara, Y.; Galbraith, J.W. Consumers’ Mobility, Expenditure and Online-Offline Substitution Response to Covid-19: Evidence from French Transaction Data; CIRANO: Montreal, QC, Canada, 2020. [Google Scholar]

- Christelis, D.; Georgarakos, D.; Jappelli, T.; Kenny, G. The Covid-19 Crisis and Consumption: Survey Evidence from Six EU Countries; ECB: Frankfurt am Main, Germany, 2020. [Google Scholar]

- Eger, L.; Komárková, L.; Egerová, D.; Mičík, M. The effect of COVID-19 on consumer shopping behaviour: Generational cohort perspective. J. Retail. Consum. Serv. 2021, 61, 102542. [Google Scholar] [CrossRef]

- Hale, T.; Angrist, N.; Goldszmidt, R.; Kira, B.; Petherick, A.; Phillips, T.; Webster, S.; Cameron-Blake, E.; Hallas, L.; Majumdar, S.; et al. A global panel database of pandemic policies (Oxford COVID-19 Government Response Tracker). Nat. Hum. Behav. 2021, 5, 529–538. [Google Scholar] [CrossRef]

- Bilińska-Reformat, K.; Dewalska-Opitek, A. ; E-commerce as the predominant business model of fast fashion retailers in the era of global COVID 19 pandemics. Proced. Comp. Sci. 2022, 192, 2479–2490. [Google Scholar] [CrossRef]

- Wisniewski, T.P.; Polasik, M.; Kotkowski, R.; Moro, A. Switching from Cash to Cashless Payments during the COVID-19 Pandemic and Beyond; NBP: Warsaw, Poland, 2021. [Google Scholar]

- Kotkowski, R.; Polasik, M. COVID-19 pandemic increases the divide between cash and cashless payment users in Europe. Econ. Lett. 2021, 209, 110139. [Google Scholar] [CrossRef]

- Kim, J. Impact of the perceived threat of COVID-19 on variety-seeking. Australas. Mark. J. 2020, 28, 108–116. [Google Scholar] [CrossRef]

- Naeem, M. Understanding the customer psychology of impulse buying during COVID-19 pandemic: Implications for retailers. Int. J. Retail Distrib. Manag. 2021, 49, 377–393. [Google Scholar] [CrossRef]

- Laato, S.; Islam, A.K.M.N.; Farooq, A.; Dhir, A. Unusual purchasing behavior during the early stages of the COVID-19 pandemic: The stimulus-organism-response approach. J. Retail. Consum. Serv. 2020, 57, 102224. [Google Scholar] [CrossRef]

- Ong, A.K.S.; Cleofas, M.A.; Prasetyo, Y.T.; Chuenyindee, T.; Young, M.N.; Diaz, J.F.T.; Nadlifatin, R.; Redi, A.A.N.P. Consumer Behavior in Clothing Industry and Its Relationship with Open Innovation Dynamics during the COVID-19 Pandemic. J. Open Innov. Technol. Mark. Complex. 2021, 7, 211. [Google Scholar] [CrossRef]

- Warwick, J.; Mansfield, P. Credit card consumers: College students’ knowledge and attitude. J. Consum. Mark. 2000, 17, 617–626. [Google Scholar] [CrossRef]

- Park, H.J.; Burns, L.D. Fashion orientation, credit card use, and compulsive buying. J. Consum. Mark. 2005, 22, 135–141. [Google Scholar] [CrossRef]

- Fogel, J.; Schneider, M. Credit card use: Disposable income and employment status. Young Consum. 2011, 12, 5–14. [Google Scholar] [CrossRef]

- Müller, A.; Mitchell, J.E.; De Zwaan, M. Compulsive buying. Am. J. Addict. 2015, 24, 132–137. [Google Scholar] [CrossRef]

- Bleyen, V.-A.; Van Hove, L.; Hartmann, M. Classifying Payment Instruments: A Matryoshka Approach. Commun. Strateg. 2010, 1, 73–94. [Google Scholar] [CrossRef] [Green Version]

- Świecka, B.; Terefenko, P.; Paprotny, D. Transaction factors’ influence on the choice of payment by Polish consumers. J. Retail. Consum. Serv. 2021, 58, 102264. [Google Scholar] [CrossRef]

- Polasik, M.; Górka, J.; Wilczewski, G.; Kunkowski, J.; Przenajkowska, K.; Tetkowska, N. Time Efficiency of Point-of-Sale Payment Methods: Empirical Results for Cash, Cards and Mobile Payments. In Proceedings of the 14th International Conference on Enterprise Information Systems (ICEIS), Wroclaw, Poland, 28 June–1 July 2012; Cordeiro, J., Maciaszek, L.A., Filipe, J., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; Volume 141, pp. 306–320. [Google Scholar]

- Koulayev, S.; Rysman, M.; Schuh, S.; Stavins, J. Explaining adoption and use of payment instruments by US consumers. RAND J. Econ. 2016, 47, 293–325. [Google Scholar] [CrossRef]

- European Central Bank. Study on the Payment Attitudes of Consumers in the Euro Area (SPACE); European Central Bank: Frankfurt am Main, Germany, 2020. [Google Scholar]

- Mastercard Según el Último Barómetro de Mastercard, el 67% de las Compras se han Realizado con Tarjeta en los Últimos Meses. 2020. Available online: https://www.mastercard.com/news/europe/es-es/noticias/notas-de-prensa/es-es/2020/julio/segun-el-ultimo-barometro-de-mastercard-el-67-de-las-compras-se-han-realizado/ (accessed on 22 February 2022).

- Badgaiyan, A.J.; Verma, A.; Dixit, S. Impulsive buying tendency: Measuring important relationships with a new perspective and an indigenous scale. IIMB Manag. Rev. 2016, 28, 186–199. [Google Scholar] [CrossRef] [Green Version]

- Dawson, S.; Kim, M. External and internal trigger cues of impulse buying online. Direct Mark. An Int. J. 2009, 3, 20–34. [Google Scholar] [CrossRef]

- Brici, N.; Hodkinson, C.; Sullivan-Mort, G. Conceptual differences between adolescent and adult impulse buyers. Young Consum. 2013, 14, 258–279. [Google Scholar] [CrossRef]

- Nguyen, T.T.M.; Nguyen, T.D.; Barrett, N.J. Hedonic shopping motivations, supermarket attributes, and shopper loyalty in transitional markets: Evidence from Vietnam. Asia Pac. J. Mark. Logist. 2007, 19, 227–239. [Google Scholar] [CrossRef] [Green Version]

- Jin, B.; Kim, J.O. A typology of Korean discount shoppers: Shopping motives, store attributes, and outcomes. Int. J. Serv. Ind. Manag. 2003, 14, 396–419. [Google Scholar] [CrossRef]

- Akram, U.; Hui, P.; Khan, M.; Yan, C.; Akram, Z. Factors Affecting Online Impulse Buying: Evidence from Chinese Social Commerce Environment. Sustainability 2018, 10, 352. [Google Scholar] [CrossRef] [Green Version]

- Mamuaya, N.C.I.; Pandowo, A. The effect of the situational factor, store atmosphere, and sales promotion on hedonic shopping motivation and its implication on supermarket consumer impulsive buying in Manado city. J. Bus. Retail. Manag. Res. 2018, 13. [Google Scholar] [CrossRef]

- Evangelin, M.R.; Sulthana, A.N.; Vasantha, S. The Effect of Hedonic Motivation towards Online Impulsive Buying with the Moderating Effect of Age. Qual. Access Success 2021, 22, 247–253. [Google Scholar] [CrossRef]

- Sharma, P.; Sivakumaran, B.; Marshall, R. Looking beyond impulse buying: A cross-cultural and multi-domain investigation of consumer impulsiveness. Eur. J. Mark. 2014, 48, 1159–1179. [Google Scholar] [CrossRef]

- Luo, X. How does shopping with others influence impulsive purchasing? J. Consum. Psychol. 2005, 15, 288–294. [Google Scholar] [CrossRef]

- Xi, H.; Hong, Z.; Jianshan, S.; Li, X.; Jiuchang, W.; Davison, R. Impulsive Purchase Behaviour in Social Commerce: The Role of Social Influence. In Proceedings of the Pacific Asia Conference on Information Systems, Chiayi, Taiwan, 27 June–1 July 2016; Association for Information Systems: Atlanta, GA, USA, 2016. [Google Scholar]

- Kang, J.; Park-Poaps, H. Hedonic and utilitarian shopping motivations of fashion leadership. J. Fash. Mark. Manag. 2010, 14, 312–328. [Google Scholar] [CrossRef]

- Arnold, M.J.; Reynolds, K.E. Hedonic shopping motivations. J. Retail 2003, 79, 77–95. [Google Scholar] [CrossRef]

- Bhattarai, G.; Subedi, B. Impact of COVID-19 on FDIs, Remittances and Foreign Aids: A Case Study of Nepal. Millenn. Asia 2021, 12, 145–161. [Google Scholar] [CrossRef]

- Verhagen, T.; Dolen, W. Van The influence of online store beliefs on consumer online impulse buying: A model and empirical application. Inf. Manag. 2011, 48, 320–327. [Google Scholar] [CrossRef]

- Iyer, G.R.; Blut, M.; Xiao, S.H.; Grewal, D. Impulse buying: A meta-analytic review. J. Acad. Mark. Sci. 2020, 48, 384–404. [Google Scholar] [CrossRef] [Green Version]

- Wang, X.; Ali, F.; Tauni, M.Z.; Zhang, Q.; Ahsan, T. Effects of hedonic shopping motivations and gender differences on compulsive online buyers. J. Mark. Theory Pract. 2021, 30, 120–135. [Google Scholar] [CrossRef]

- Gültekin, B.; Özer, L. The Influence of Hedonic Motives and Browsing on Impulse Buying. J. Econ. Behav. Stud. 2012, 4, 180–189. [Google Scholar] [CrossRef]

- Kalla, S.M.; Arora, A.P. Impulse buying: A literature review. Glob. Bus. Rev. 2011, 12, 145–157. [Google Scholar] [CrossRef]

- Lamb, C.W.; Hair, J.F.; Mcdaniel, C. Marketing, 11th ed.; Cengage Learning: Mason, OH, USA, 2011. [Google Scholar]

- Park, E.J.; Forney, J.C. Assessing and predicting apparel impulse buying. J. Glob. Fash. Mark. 2011, 2, 28–35. [Google Scholar] [CrossRef]

- Yu, C.; Bastin, M. Hedonic shopping value and impulse buying behavior in transitional economies: A symbiosis in the Mainland China marketplace. J. Brand Manag. 2010, 18, 105–114. [Google Scholar] [CrossRef]

- Yang, C.L.; Lin, S.P.; Chan, Y.-H.; Sheu, C. Mediated effect of environmental management on manufacturing competitiveness: An empirical study. Int. J. Prod. Econ. 2010, 123, 210–220. [Google Scholar] [CrossRef]

- Fraj, E.; Martinez, E. Environmental values and lifestyles as determining factors of ecological consumer behaviour: An empirical analysis. J. Consum. Mark. 2006, 23, 133–144. [Google Scholar] [CrossRef]

- Chan, T.Y.; Wong, C.W.Y. The consumption side of sustainable fashion supply chain: Understanding fashion consumer eco-fashion consumption decision. J. Fash. Mark. Manag. 2012, 16, 193–215. [Google Scholar] [CrossRef]

- Chiang, K.P.; Dholakia, R.R. Factors Driving Consumer Intention to Shop Online: An Empirical Investigation. J. Consum. Psychol. 2003, 13, 177–183. [Google Scholar] [CrossRef]

- Niinimäki, K. Eco-Clothing, Consumer Identity and Ideology Kirsi. Sustain. Dev. 2010, 18, 150–162. [Google Scholar] [CrossRef]

- Del Prete, M. Mindful Sustainable Consumption and Sustainability Chatbots in Fast Fashion Retailing During and after the COVID-19 Pandemic. J. Manag. Sustain. 2022, 12. [Google Scholar] [CrossRef]

- Joy, A.; Sherry, J.F.; Venkatesh, A.; Wang, J.; Chan, R. Fast Fashion, Sustainability, and the Ethical Appeal of Luxury Brands. Fash. Theory 2012, 16, 273–295. [Google Scholar] [CrossRef]

- Soyer, M.; Dittrich, K. Sustainable Consumer Behavior in Purchasing, Using and Disposing of Clothes. Sustainability 2021, 13, 8333. [Google Scholar] [CrossRef]

- Cachon, G.P.; Swinney, R. The value of fast fashion: Quick response, enhanced design, and strategic consumer behavior. Manag. Sci. 2011, 57, 778–795. [Google Scholar] [CrossRef] [Green Version]

- Caro, F.; Martínez-de-Albéniz, V. Fast Fashion: Business Model Overview and Research Opportunities. In Retail Supply Chain Management; Agrawal, N., Smith, S.A., Eds.; Springer: Boston, MA, USA, 2015; pp. 237–264. [Google Scholar]

- Niinimäki, K.; Peters, G.; Dahlbo, H.; Perry, P.; Rissanen, T.; Gwilt, A. The environmental price of fast fashion. Nat. Rev. Earth Environ. 2020, 1, 189–200. [Google Scholar] [CrossRef] [Green Version]

- Brewer, M.K. Slow Fashion in a Fast Fashion World: Promoting Sustainability and Responsibility. Laws 2019, 8, 24. [Google Scholar] [CrossRef] [Green Version]

- Ghemawat, P.; Nueno, J.L. ZARA: Fast Fashion; Harvard Business School: Boston, MA, USA, 2006; Volume 703497. [Google Scholar]

- Tokatli, N.; Kizilgün, Ö. From manufacturing garments for ready-to-wear to designing collections for fast fashion: Evidence from Turkey. Environ. Plan A Econ. Space 2009, 41, 146–162. [Google Scholar] [CrossRef]

- Shen, B. Sustainable Fashion Supply Chain: Lessons from H&M. Sustainability 2014, 6, 6236–6249. [Google Scholar] [CrossRef] [Green Version]

- Zhang, B.; Zhang, Y.; Zhou, P. Consumer Attitude towards Sustainability of Fast Fashion Products in the UK. Sustainability 2021, 13, 1646. [Google Scholar] [CrossRef]

- Lee, M.; Kim, Y.; Lee, H. Adventure versus gratification: Emotional shopping in online auctions. Eur. J. Mark. 2013, 47, 49–70. [Google Scholar] [CrossRef]

- Saran, R.; Roy, S.; Sethuraman, R. Personality and fashion consumption: A conceptual framework in the Indian context. J. Fash. Mark. Manag. 2016, 20, 157–176. [Google Scholar] [CrossRef]

- Eriksson, N.; Rosenbröijer, C.J.; Fagerstrøm, A. The relationship between young consumers’ decision-making styles and propensity to shop clothing online with a smartphone. Proced. Comput. Sci. 2017, 121, 519–524. [Google Scholar] [CrossRef]

- Thomas, M.; Desai, K.K.; Seenivasan, S. How credit card payments increase unhealthy food purchases: Visceral regulation of vices. J. Consum. Res. 2011, 38, 126–139. [Google Scholar] [CrossRef]

- Pradhan, D.; Israel, D.; Jena, A.K. Materialism and compulsive buying behaviour: The role of consumer credit card use and impulse buying. Asia Pac. J. Mark. Logist. 2018, 30, 1239–1258. [Google Scholar] [CrossRef]

- Banker, S.; Dunfield, D.; Huang, A.; Prelec, D. Neural mechanisms of credit card spending. Sci. Rep. 2021, 11, 4070. [Google Scholar] [CrossRef] [PubMed]

- Pirog, S.F.; Roberts, J.A. Personality and Credit Card Misuse among College Students: The Mediating Role of. J. Mark. Theory Pract. 2007, 15, 66–77. [Google Scholar] [CrossRef]

- Verplanken, B.; Herabadi, A. Individual differences in impulse buying tendency: Feeling and no thinking. Eur. J. Pers. 2001, 15, S71–S83. [Google Scholar] [CrossRef]

- Roberts, J.A.; Jones, E. Money attitudes, credit card use, and compulsive buying among American college students. J. Consum. Aff. 2001, 35, 213–240. [Google Scholar] [CrossRef]

- Činjarević, M.; Tatić, K.; Petrić, S. See it, like it, buy it! Hedonic shopping motivations and impulse buying. Econ. Rev. J. Econ. Bus. 2011, 9, 3–15. [Google Scholar]

- Özen, H.; Kodaz, N. Utilitarian or Hedonic? A Cross Cultural Study in Online Shopping. In Thriving in a New World Economy. Proceedings of the 2012 World Marketing Congress/Cultural Perspectives in Marketing Conference; Plangger, K., Ed.; Springer: Cham, Switzerland, 2016; pp. 234–239. [Google Scholar]

- Khare, A. Credit Card Use and Compulsive Buying Behavior. J. Glob. Mark. 2013, 26, 28–40. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis: Pearson New International Edition, 7th ed.; Pearson Education: Harlow, UK, 2013. [Google Scholar]

- Sharma, S. Applied Multivariate Techniques, 1st ed.; John Wiley and Sons: New York, NY, USA, 1996. [Google Scholar]

- Schermelleh-Engel, K.; Moosbrugger, H.; Müller, H. Evaluating the fit of structural equation models: Tests of significance and descriptive goodness-of-fit measures. Methods Psychol. Res. Online 2003, 8, 23–74. [Google Scholar]

- Anić, I.-D.; Mihić, M. Demographic profile and purchasing outcomes of fashion conscious consumers in Croatia. Ekon. Pregl. 2015, 66, 103–118. [Google Scholar]

- Park, E.J.; Kim, E.Y.; Forney, J.C. A structural model of fashion-oriented impulse buying behavior. J. Fash. Mark. Manag. 2006, 10, 433–446. [Google Scholar] [CrossRef]

- Kim, H.-S.; Hong, H. Fashion Leadership and Hedonic Shopping Motivations of Female Consumers. Cloth. Text. Res. J. 2011, 29, 314–330. [Google Scholar] [CrossRef]

- Tang, Y.; Chen, S.; Yuan, Z. The effects of hedonic, gain, and normative motives on sustainable consumption: Multiple mediating evidence from China. Sustain. Dev. 2020, 28, 741–750. [Google Scholar] [CrossRef]

- Shukla, P. Conspicuous consumption among middle age consumers: Psychological and brand antecedents. J. Prod. Brand Manag. 2008, 17, 25–36. [Google Scholar] [CrossRef]

- Islam, T.; Pitafi, A.H.; Arya, V.; Wang, Y.; Akhtar, N.; Mubarik, S.; Xiaobei, L. Panic buying in the COVID-19 pandemic: A multi-country examination. J. Retail. Consum. Serv. 2021, 59, 102357. [Google Scholar] [CrossRef]

| Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}