The Effect of Product Knowledge, Perceived Benefits, and Perceptions of Risk on Indonesian Student Decisions to Use E-Wallets for Warunk Upnormal

Abstract

:1. Introduction

2. Literature Review

2.1. Technology Acceptance Model (TAM)

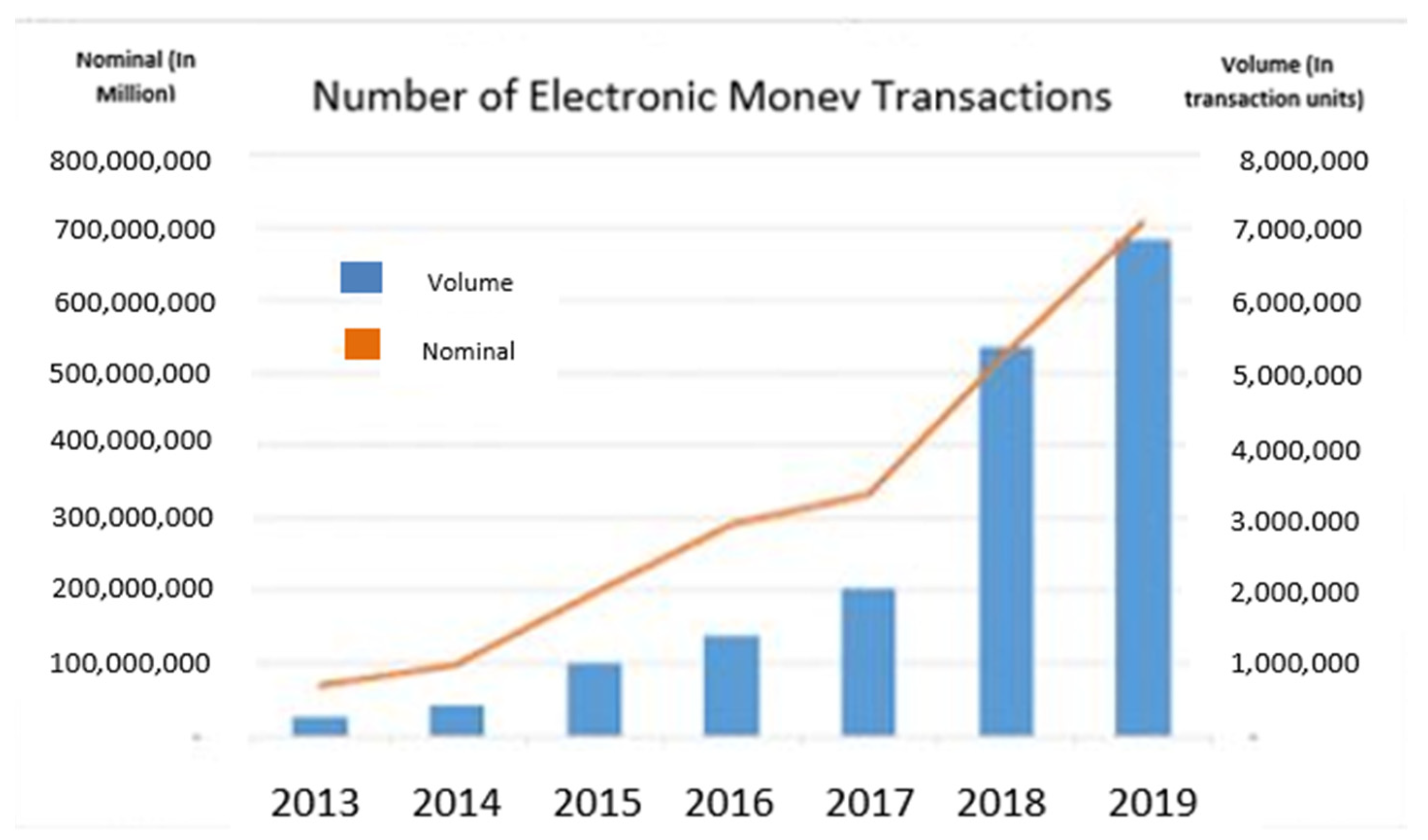

2.2. Mobile Payment

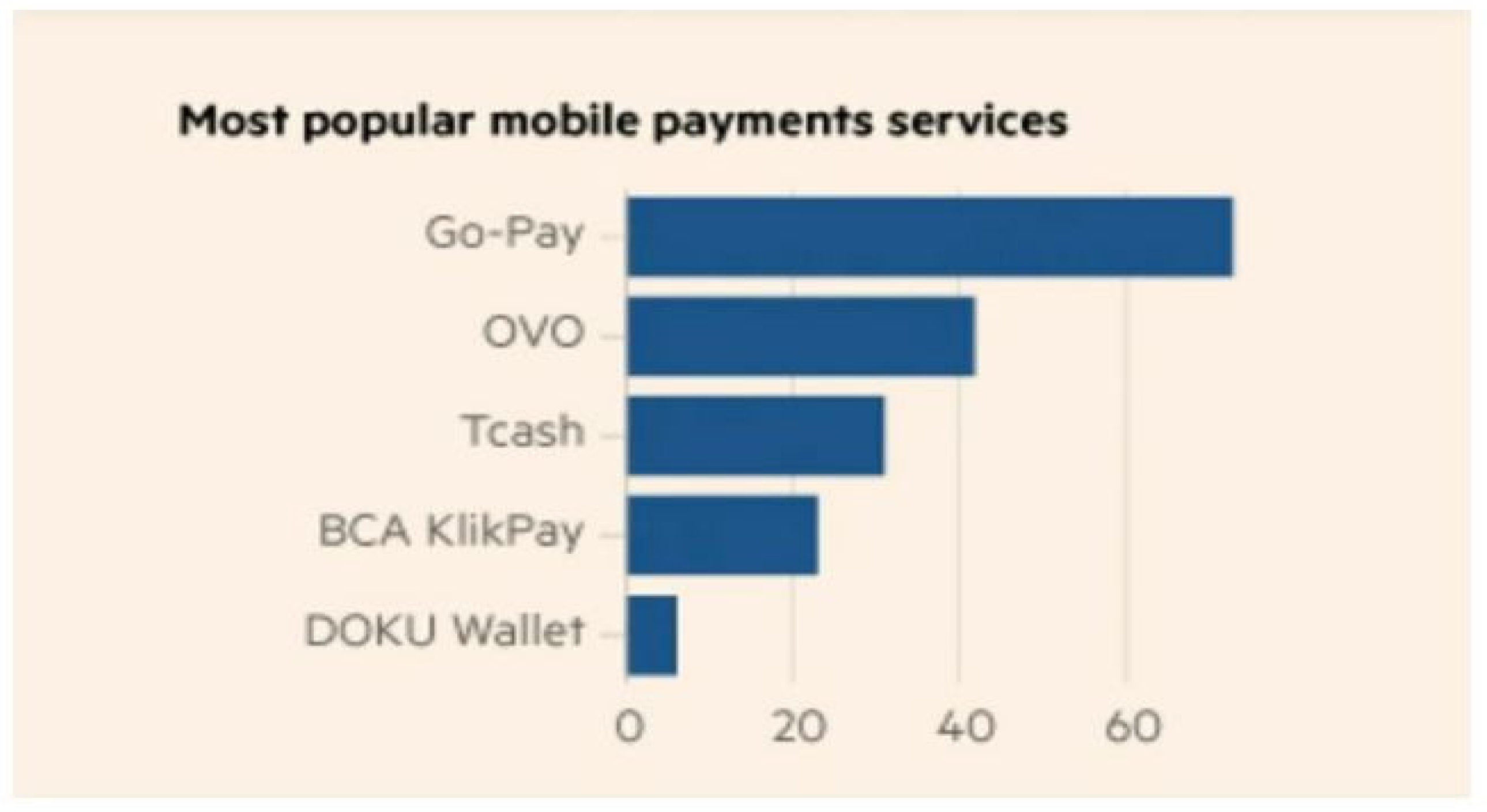

2.3. Go-Pay

2.4. Product Knowledge

2.5. Perceived Benefits

2.6. Perceived Risk

2.7. Usage Decision

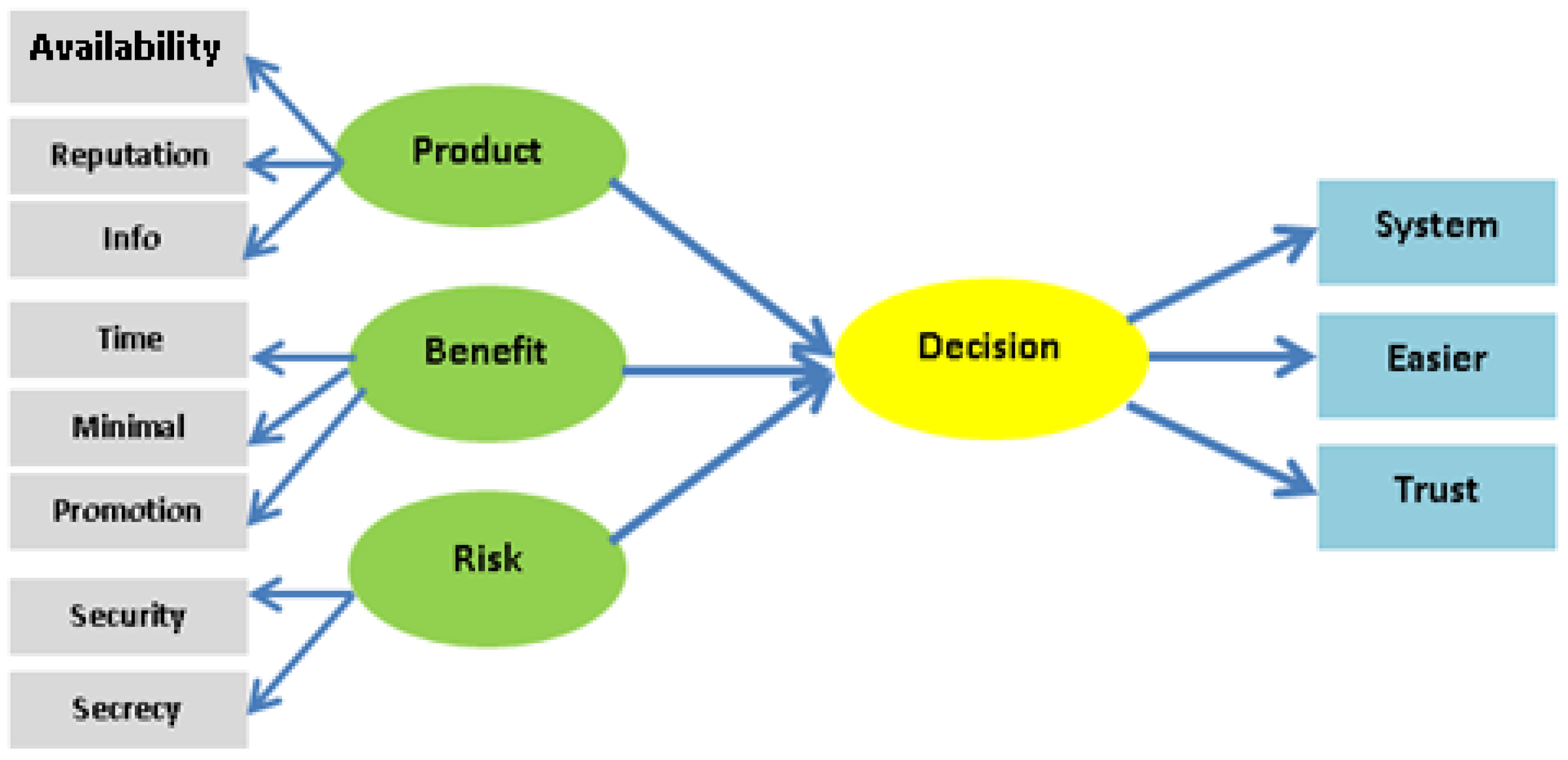

Research Paradigm

- (1)

- X1 = Product knowledge influences usage decisions,

- (2)

- X2 = Perception of benefits affects the decision to use,

- (3)

- X3 = Risk perception affects the decision to use.

3. Materials and Methods

3.1. Data Collection

3.2. Sampling Technique

3.3. Data Processing

4. Results and Discussion

4.1. Respondent Profile

4.2. Structural Equation Model

For Structural Equation

5. Discussion

5.1. The Effect of Product Knowledge on Usage Decisions

5.2. The Influence of Perceived Benefits on Use Decisions

5.3. The Influence of Risk Perception on Use Decisions

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Han, A.S. Chinese fintech companies and their “going out” strategies. J. Internet Digit. Econ. 2021, 1, 47–63. [Google Scholar] [CrossRef]

- Hussain, S.; Song, X.; Niu, B. Consumers’ Motivational Involvement in eWOM for Information Adoption: The Mediating Role of Organizational Motives. Front. Psychol. 2020, 10, 3055. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Priyono, A. Analysis of the influence of trust and risk in the acceptance of Go-Pay electronic wallet technology. J. Bus. Strategy 2017, 21, 88–106. [Google Scholar] [CrossRef] [Green Version]

- Jumanto. 3 Benefits of Go Pay for Gojek Drivers (Go Ride and Go Car). 2018. Available online: http://www.jumanto.com/2017/11/benefit-go-pay-bagi-driver-gojek.html (accessed on 17 December 2018).

- Ferdiana, A.M.K. Understanding Fintech through Go–Pay. Int. J. Innov. Sci. Res. Technol. 2019, 4, 257–260. [Google Scholar]

- Sembiring Carolina, F.; Tambunan, J. Analysis of consumer satisfaction toward go-pay fin-tech service at faculty of economics and business stundents at Christian University of Indonesia. Fundam. Manag. J. 2019, 4, 62–81. [Google Scholar]

- FT Confidential Research. Top 5 Mobile Payment di Indonesia 2018. Available online: https://selular.id/2019/01/top-5-mobile-payment-di-indonesia-2018/ (accessed on 6 March 2022).

- Juniwati. Influence of Perceived Usefulness, Ease of Use, Risk on Attitude and Intention to Shop Online. Eur. J. Bus. Manag. 2014, 6, 218–229. [Google Scholar]

- Zhang, X.; Yu, X. The Impact of Perceived Risk on Consumers’ Cross-Platform Buying Behavior. Front. Psychol. 2020, 11, 592246. [Google Scholar] [CrossRef]

- Kamalul Ariffin, S.; Mohan, T.; Goh, Y.-N. Influence of consumers’ perceived risk on consumers’ online purchase intention. J. Res. Interact. Mark. 2018, 12, 309–327. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Hamed, T. A review of technology acceptance and adoption models and theories. Procedia Manuf. 2018, 22, 960–967. [Google Scholar]

- Muntianah, S.T.; Astuti, E.S.; Azizah, D.F. The Influence of Behavioral Interests on the Actual Use of Information Technology with the Technology Acceptance Model (TAM) Approach. Profit Univ. Brawijaya Malang 2012, 6, 88–113. [Google Scholar]

- Liu, G.S.; Thai, P.T. A Study of Factors Affecting the Intention to Use Mobile Payment Services in Vietnam. Econ. World 2015, 4, 10–12. [Google Scholar] [CrossRef]

- Yang, M.; Mamun, A.; Mohiuddin, M.; Nawi, N.; Zainol, N. Cashless Transactions: A Study on Intention and Adoption of e-Wallets. Sustainability 2021, 13, 831. [Google Scholar] [CrossRef]

- Tedja, R.T.; Tjong, Y.; Deniswara, K. Factors Affecting the Behavioral Intention of E-Wallet Use during COVID-19 Pandemic in DKI Jakarta. In Proceedings of the 2021 International Conference on Information Management and Technology (ICIMTech), Jakarta, Indonesia, 14 September 2021. [Google Scholar] [CrossRef]

- Malik, A.N.A.; Annuar, S.N.S. The Effect of Perceived Usefulness, Perceived Ease of Use, Reward, and Perceived Risk toward E-Wallet Usage Intention. In Eurasian Business and Economics Perspectives; Springer: Berlin/Heidelberg, Germany, 2021; pp. 115–130. [Google Scholar]

- Ahn, J.; Park, H.S. The reward for organ donation: Is it effective or not as a promotion strategy? Int. J. Nonprofit Volunt. Sect. Mark. 2016, 21, 118–129. [Google Scholar] [CrossRef]

- Davies, R.; Harty, C. Measurement and exploration of individual beliefs about the consequences of building information modelling use. Constr. Manag. Econ. 2013, 31, 1110–1127. [Google Scholar] [CrossRef]

- Kim, Y.J.; Han, J. Why smartphone advertising attracts customers: A model of web advertising, flow, and personalization. Comput. Hum. Behav. 2014, 33, 256–269. [Google Scholar] [CrossRef]

- Grover, P.; Kar, A.K. User engagement for mobile payment service providers—Introducing the social media engagement model. J. Retail. Consum. Serv. 2020, 53, 101718. [Google Scholar] [CrossRef]

- Aji, H.M.; Berakon, I.; Husin, M. COVID-19 and e-wallet usage intention: A multigroup analysis between Indonesia and Malaysia. Cogent Bus. Manag. 2020, 7, 1804181. [Google Scholar] [CrossRef]

- Renny Guritno, S.; Siringoringo, H. Perceived Usefulness, Ease of Use, and Attitude towards Online Shopping Usefulness Towards Online Airlines Ticket Purchase. Procedia Soc. Behav. Sci. 2013, 81, 212–216. [Google Scholar] [CrossRef] [Green Version]

- Yang, Y.; Liu, Y.; Li, H.; Yu, B. Understanding perceived risks in mobile payment acceptance. Ind. Manag. Data Syst. 2015, 115, 253–269. [Google Scholar] [CrossRef]

- Abdullah, A. An Overview of Mobile Payments, Fintech, and Digital Wallet in Saudi Arabia; IEEE: Piscataway Township, NJ, USA, 2020. [Google Scholar]

- Leong, L.-Y.; Hew, T.-S.; Ooi, K.-B.; Wei, J. Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. Int. J. Inf. Manag. 2020, 51, 102047. [Google Scholar] [CrossRef]

- Chawla, D.; Joshi, H. Importance-performance map analysis to enhance the performance of attitude towards mobile wallet adoption among Indian consumer segments. Int. Manag. Inst. New Delhi India 2021, 73, 946–966. [Google Scholar] [CrossRef]

- Hong, Z.; Yi, L. Research on the Influence of Perceived Risk in Consumer Online Purchasing Decisions. Int. Conf. Appl. Phys. Ind. Eng. 2012, 24 Pt B, 1304–1310. [Google Scholar]

- Nurcahyo, R.; Putra, P.A. Critical factors in indonesia’s e-commerce collaboration. J. Theor. Appl. Electron. Commer. Res. Access 2021, 16, 135. [Google Scholar] [CrossRef]

- Susanti, N.; Padmakusumah, R.R.; Rahmayanti, R.; Achmad Drajat Aji Sujai, R. Relationship marketing as a key success factor of co-operative enterprise business performance. J. Adv. Res. Dyn. Control. Syst. 2019, 11, 922–932. [Google Scholar]

- Joshi, D.C. Consumer attitude and intention to adopt mobile wallet in India—An empirical study. Int. J. Bank Mark. Emerald Publ. Ltd. 2018. [Google Scholar] [CrossRef]

- Romadloniyah, A.L.; Prayitno, D.H. Pengaruh Persepsi Kemudahan Penggunaan, Persepsi Daya Guna, Persepsi Kepercayaan, Dan Persepsi Manfaat Terhadap Minat Nasabah Dalam Menggunaan E-Money Pada Bank Bri Lamongan. J. Akunt. 2018, 3, 699. [Google Scholar] [CrossRef]

- Haryani, D.S. Pengaruh Persepsi Risiko Terhadap Keputusan Pembelian Online di Tanjungpinang. Dimensi 2019, 8. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Parastiti, D.E.; Mukhlis, I.; Haryono, A. Analysis of Electronic Money Use in Students of the Faculty of Economics, State University of Malang. J. Econ. Dev. Stud. 2015, 7, 75–82. [Google Scholar]

- Wardhani, D.K. Analisis faktor-faktor yang mempengaruhi persepsi pengguna gojek terhadap gopay (In-App Payment di Gojek). In Skripsi; Jurusan Akuntansi Fakultas Ekonomi, Universitas Gajah Mada: Yogyakarta, Indonesia, 2016. [Google Scholar]

- Tham, K.W.; Dastane, O.; Johari, Z.; Ismail, N.B. Perceived Risk Factors Affecting Consumers’ Online Shopping Behaviour. J. Asian Financ. Econ. Bus. 2019, 6, 249–260. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Construct | Loading Factor | Rho_A | AVE | Cronbach’s Alpha | Composite Reliability |

|---|---|---|---|---|---|

| Product Knowledge | 0.665 | 0.829 | 0.726 | 0.813 | 0.888 |

| Perceived Benefits | 0.889 | 1 | 1 | 1 | 1 |

| Perceptions of Risk | 0.856 | 0.731 | 0.775 | 0.713 | 0.775 |

| No | Description | Frequency | Percentage (%) |

|---|---|---|---|

| 1 | Gender | ||

| Man | 34 | 34 | |

| Woman | 66 | 66 | |

| 2 | Age | ||

| 15–25 years | 41 | 41 | |

| 26–35 years | 42 | 42 | |

| 36–45 years | 17 | 17 | |

| 3 | Education Level | ||

| Junior High School | 5 | 5 | |

| Senior High School | 10 | 10 | |

| College | 20 | 20 | |

| Academy | 5 | 5 | |

| Bachelor | 33 | 33 | |

| Magister | 20 | 20 | |

| Doctoral | 7 | 7 | |

| 4 | Duration of Using E-Wallets | ||

| >1 year | 79 | 79 | |

| <1 year | 21 | 21 | |

| 5 | Reason of Use | ||

| Easy to Use | 23 | 23 | |

| Benefit Offer | 53 | 53 | |

| Low Risk | 24 | 24 | |

| Overall Model Fit Test Size | Benchmark Value for Model Fit | Model Fit to Data | |

|---|---|---|---|

| Probability of X2 count | 0.12 | ≥0.05 | Yes |

| RMSEA | 0.055 | ≤0.08 | Yes |

| NFI | 0.97 | ≥0.90 | Yes |

| NNFI | 0.99 | ≥0.90 | Yes |

| CFI | 0.99 | ≥0.90 | Yes |

| IFI | 0.99 | ≥0.90 | Yes |

| RFI | 0.95 | ≥0.90 | Yes |

| RMR | 0.026 | ≤0.05 | Yes |

| SRMR | 0.045 | ≤0.05 | Yes |

| GFI | 0.92 | ≥0.90 | Yes |

| AGFI | 0.86 | 0.8 ≤ AGFI < 0.90 | Yes (Marginal Fit) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Foster, B.; Hurriyati, R.; Johansyah, M.D. The Effect of Product Knowledge, Perceived Benefits, and Perceptions of Risk on Indonesian Student Decisions to Use E-Wallets for Warunk Upnormal. Sustainability 2022, 14, 6475. https://0-doi-org.brum.beds.ac.uk/10.3390/su14116475

Foster B, Hurriyati R, Johansyah MD. The Effect of Product Knowledge, Perceived Benefits, and Perceptions of Risk on Indonesian Student Decisions to Use E-Wallets for Warunk Upnormal. Sustainability. 2022; 14(11):6475. https://0-doi-org.brum.beds.ac.uk/10.3390/su14116475

Chicago/Turabian StyleFoster, Bob, Ratih Hurriyati, and Muhamad Deni Johansyah. 2022. "The Effect of Product Knowledge, Perceived Benefits, and Perceptions of Risk on Indonesian Student Decisions to Use E-Wallets for Warunk Upnormal" Sustainability 14, no. 11: 6475. https://0-doi-org.brum.beds.ac.uk/10.3390/su14116475