1. Introduction

In January 2015, the South Korean government launched the Emissions Trading Scheme (ETS), a key policy to achieve its goal of cutting greenhouse gases 30% below the business-as-usual (BAU) level by 2020. One notable feature in the South Korean ETS is that indirect emissions from electricity and heat consumption as well as direct emissions are regulated by the authorities while the EU Emissions Trading System (EU-ETS) and the California ETS cover only direct emissions. Here, “direct emissions” refers to the emissions from onsite combustion or processes while “indirect emissions” relates to the consumption of power and heat generated and supplied by a utility.

Covering both direct and indirect emissions is not a unique feature to the South Korean ETS. ETS schemes implemented by some other neighboring countries also share this feature. For example, the ETS of the Tokyo Metropolitan Area and other municipalities regulates indirect emissions caused by electricity consumption. China’s pilot ETSs running in five cities and two provinces regulate both direct and indirect emissions from consuming outsourced power or heat [

1,

2].

There are pros and cons as to whether it is desirable to include indirect emissions within the coverage of ETSs. Those who oppose including indirect emissions are concerned that covering indirect emissions could jeopardize the environmental integrity and price stability of the emissions trading market [

3]. Including indirect emissions generates double counting of power sector emissions, which could be neither efficient nor equitable. For instance, power companies may enjoy windfall profits if their direct emissions become less than the grandfathered permits due to the drop in power demand caused by end users’ efforts such as energy conservation or energy efficiency activities. This provides power companies with incentives to free-ride and distorts efficient allocation. Furthermore, covering indirect emissions may impede the price stability of the emissions trading market because it could amplify excess supply or excess demand. For example, with a sluggish economy, electricity consumption tends to fall, which in turn generates the surplus of permits in both non-power sectors and power sectors under grandfathering allocation schemes. The amplified excess supply in an ETS can exacerbate the price reduction. In case of the economic boom, similar reasoning can be applied.

On the other hand, including indirect emissions can serve as a second-best option when electricity markets are heavily regulated and electricity prices are not determined purely by supply and demand in the market as in South Korea [

4]. As is well known, the market intervention of the government, such as price control, may prevent the carbon price from being passed through completely in retail prices. For instance, as of June 2016 the electricity retail prices of South Korea have not changed at all since November 2013, although the ETS started in January 2015 [

5]. Such intervention results in failing to provide consumers with sufficient incentives to reduce electricity consumption, in which an ETS may not achieve the expected socially efficient allocation. Arguably, the best way to fix this inefficiency may be to deregulate power sectors so as to let prices be guided purely by market forces. However, deregulation takes a long time to be realized and may fall in the mire of political impasse, and thus including indirect emissions can provide a partial incentive for covered sectors to enhance their electricity consumption efficiency. In this regard, the South Korean and Chinese governments have finally chosen to include indirect emissions within the coverage of their ETSs.

The main reason many economists are in favor of the ETS is that they believe it helps achieve greenhouse gas reduction goals cost-effectively. Such cost-effectiveness can be achieved only when several conditions are satisfied. There are numerous factors that distort a cost-effective allocation and thereby raise the effectiveness of the ETS in question. According to [

6,

7], allocative efficiency is guaranteed when the following factors do not exist in the allowance market: (1) transaction cost; (2) market power; (3) other regulations; and (4) uncertainty. When some of these factors are pervasive, allocative efficiency will be achieved only if the initial allocation happens to be efficient. This is possible only when a regulatory authority knows the true abatement costs of participating firms, which is not only nearly impossible but also against the original intent of ETSs. Minimizing the effect of each factor is equally important for the successful implementation of an ETS, and deserves separate in-depth study.

This study focuses on market power since there is concern over the market power in the South Korean emissions trading market. In the South Korean ETS, large shares of allowances are allocated to a handful of firms such as power, steel, and cement companies. The emissions of the top 10 major emitters account for 60% of the total emissions of companies covered by the ETS. The absence of market power is a critical condition for the success of an ETS because, as general lessons from economics teach, market power is likely to cause a market failure. In this sense, it is imperative to devise a policy to lessen the likelihood of market power in the allowance market.

There are, however, a few studies showing that market power in an ETS may not be a serious concern in the case of zero-cost pass-through. In particular, [

8] convincingly argues that a dominant firm’s market power is substantially mitigated by a commitment problem when the firm becomes a net buyer. Still, it also finds that if the dominant firm becomes a net seller, it exercises market power no differently than a large supplier of a conventional exhaustible resource. Because the possibility that the dominant firm becomes a net seller cannot be excluded

ex ante, especially when an ETS is in its nascent stage, market power remains one of the main concerns even in the zero-cost pass-through.

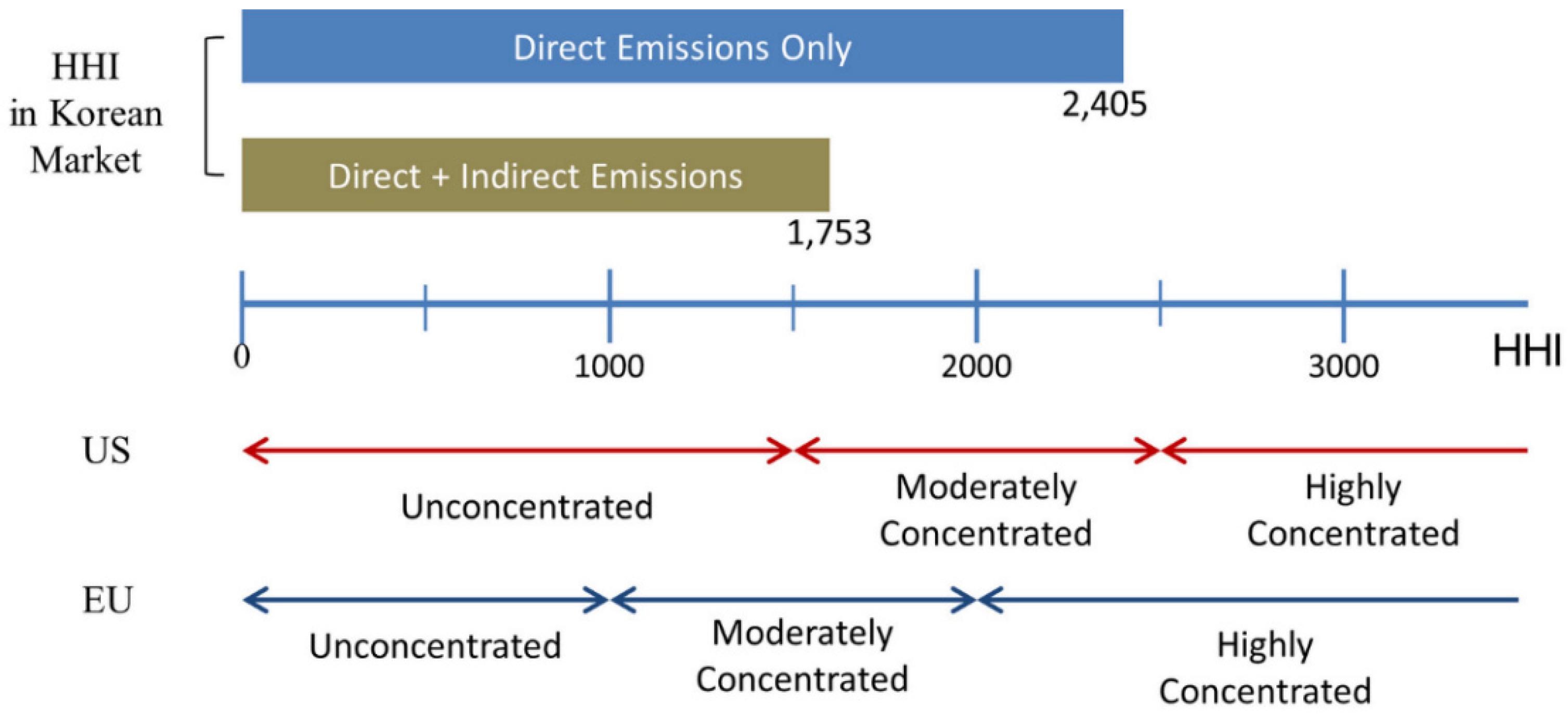

This study shows that covering both direct and indirect emissions has the additional advantage of mitigating market power in the emissions trading market, besides the aforementioned effect of managing the final consumers’ electricity demand. The direct-to-indirect emissions ratios of most heavy emitters, such as power, steel, and cement companies, are much higher than the overall average of the covered entities in the South Korean ETS. Thus, the inclusion of indirect emissions can contribute to the lessening market concentration, thereby mitigating market power by lowering the shares of allowances allocated to heavy emitters. This study, using the case of South Korea, shows that market power can be mitigated substantially by including indirect emissions. Following the literature, the Herfindahl-Hirschman Index (HHI), the most widely used measure in both theory and empirics, is used to quantify market power. In addition, other market concentration measures are considered to confirm that the conclusion is robust to the choice of measures.

The rest of this paper is organized as follows.

Section 2 examines how market power causes inefficiency of ETSs and outlines the HHI.

Section 3 verifies that including indirect emissions can mitigate market power in the Korean ETS using the HHI index.

Section 4 considers three other concentration measures and checks the robustness of the result.

Section 5 concludes the paper.

2. Market Power in an ETS

2.1. Market Power and Allocative Inefficiency

Theoretically, an ETS results in the allocative efficiency of the market equilibrium. This result depends on several conditions, one of which is that the allowance market is competitive. If this condition is violated so that there is market power in the allowance market, allocative efficiency is no longer ensured because firms can take advantage of their market power to pursue the excess profit.

The first study on the theory of market power in emissions markets is examined by [

9]. Motivated by the emissions market in Los Angeles, he studies the case in which there is a single dominant firm and many small fringe firms. His result shows that the initial degree of misallocation determines the type of market power of the dominant firm, regardless of its position as a dominant seller or buyer, and the firm enjoys excessive gains by manipulating the inelastic parts of competitors’ demand curves. The author of [

6] classifies market power exercised in the allowance market into two types. One type aims to maximize revenue or minimize abatement cost by manipulating the allowance prices. This type focuses on the allowance market itself. The other type exercises its market power in the allowance market in order to take competitive advantage in the product market in which it originally competes. This type is known as exclusionary price manipulation because market power in the allowance market is used as leverage to influence competition in the product market. This type of market power is in line with the strategy of “raising rival’s cost” in the sense that a firm attempts to be more dominant by increasing other firms’ costs, thereby deriving more profit on the product market [

10,

11].

As far as the South Korean ETS is concerned, the second type of market power is unlikely to arise because various industries including power, steel, electronic equipment, and cars, would be covered by the ETS. Note that the second type of market power would arise when most firms competing in the same product market also participate in the allowance market. If firms covered by an ETS are diverse, as is the case in South Korea, it is likely that exclusionary price manipulation would not occur. However, the first type of market power could arise in the South Korean ETS. Because small numbers of firms have large numbers of allowances, strategic price-setting behavior by these firms has been warned of in the debate over the introduction of the ETS.

When a dominant firm exercises its market power in the allowance market, the final allocation is not necessarily equal to the socially optimal outcome. If a dominant firm is allocated more than needed and becomes a monopoly in the allowance market, it cuts emissions less than the socially optimal level while other small firms should reduce emissions more. This would raise allowance prices in the market and the dominant firm would benefit from the price rise. The opposite scenario is also possible. In addition, in the presence of market power a final allocation depends on an initial allocation. The property that a final allocation is independent of an initial allocation is one of the most desirable characteristics of an ETS. This helps us to deal with equity concerns separately from efficiency. This property allows us to focus on equity concerns because a socially efficient allocation can be achieved for any initial allocation. As [

6,

7] point out, however, the final allocation varies according to an initial allowance allocation in the presence of market power. This market power creates inter-linkages between distributional and efficiency issues, which puts an extra burden on regulators to address the efficiency issues in the market. Since distributional issues are inter-linked with efficiency issues in the presence of market power, regulators have a larger burden in addressing efficiency issues as well as distributional issues simultaneously. In this regard, mitigating market power in an ETS is a necessary condition for a successful ETS.

2.2. Evaluating the Concerns of Market Power in an ETS

Market power is defined as the ability to control market price. The price-cost margin typically is used to identify the presence of market power in a market. In practice, however, when evaluating the concerns of market power, an index of market concentration represented as a functional form of market shares is usually used because it is difficult to find true marginal costs in many cases. Of course, the value of a market concentration index is not the only measurement to evaluate the concern of market power. Other factors, such as the number of market participants, the degree of product variety and the ease of coordinated interaction among firms, should be considered together. Nonetheless, the value of the market concentration index ought to be one very useful element in evaluating the concerns of market power. Most anti-trust authorities have used an index of market concentration as a screening device when assessing the level of constraints to market competition. This can be also applied to assessing the concerns of market power in an ETS. Several studies, including [

12,

13,

14], suggest that the initial shares of allocation to the covered firms can evaluate the possibility of market power in the allowance market.

The most well-known concentration measure among several measures based on market shares is the HHI. The index is defined as

where

n is the number of firms in the market and (

s1,

s2, …,

sn) are the market shares. One of the attractive features of the HHI is that it has foundations in oligopoly theory. It can be shown that the HHI is associated with a weighted average of firms’ price-cost margins from the Cournot solution [

15].

The HHI is used widely as a measure of concentration in the literature on industrial organization and serves as a reference for the assessment of concentration indexes [

16]. In the context of the EU-ETS, [

13] calculate the HHI for each of the top 10 companies in the EU-ETS and conclude that no firm has market power in the emissions market. [

14] also reach the same result. While a degree of concentration exists at the firm level, an analysis based on the HHI verifies that it does not present any threat to market power.

Following the literature, this study uses the HHI to assess the market concentration in the Korean ETS. Thereafter, other concentration measures are considered as well.

2.3. Criteria Based on the Herfindahl-Hirschman Index

The HHI is widely used as an indicator examining the concentration of a market in many regulation-related bodies. It is one of the most common assessment measures for the likely competitive effects from horizontal mergers. The anti-trust authorities consider both the absolute level of the HHI and the change of the HHI after a merger to evaluate the likely competitive concerns in a merger.

In the United States, the HHI serves a major role in the execution process of anti-trust laws. The Antitrust Division of the Justice Department and the Federal Trade Commission issued guidelines based on the HHI concerning their policy toward mergers [

17]. According to the guidelines, there are three categories of market concentration: unconcentrated (HHI < 1500), moderately concentrated (1500 < HHI < 2500), and highly concentrated (HHI > 2500). If the value of the HHI after the merger falls into the unconcentrated market category, no negative effects are considered to limit market competition. In addition, a small change of the HHI, that below 100, is considered unlikely to have competitive concerns regardless of the absolute level of the HHI. If the HHI value falls into the moderately or highly concentrated market category and the change of the HHI is more than 100, there is the possibility of significant competitive concerns.

The EU also sets concentration thresholds of the HHI, although somewhat differently, and these have the practical effect of determining safe harbors. The guideline of the European Commission (EC) states that the EC is unlikely to recognize horizontal competition concerns in a market with a post-merger HHI of less than 1000 [

18]. In addition, the guidelines are unlikely to recognize competition concerns in a merger with a post-merger HHI value of between 1000 and 2000 and a change in the HHI of less than 250, or a merger with a post-merger HHI of more than 2000 and a change in the HHI below 150. The guidelines of South Korea are very similar to those of the EC. The difference is that the HHI thresholds in South Korea are 1200 and 2500 while those in the EU are 1000 and 2000, respectively.

It should be noted here that the purpose of the criteria is not to judge the existence of market power. Rather, the criteria are used mainly to provide a safe harbor rule judging what is likely to be anti-competitive. They also provide a standard for screening what is likely to raise potential competitive concerns. Once possible competitive concerns are raised from the criteria, they should be reviewed more closely in conjunction with some other factors.

5. Conclusions

Some ETSs cover both direct and indirect emissions while others cover only direct emissions. The main argument favoring the inclusion of indirect emissions is that it can be a second-best option when the retail prices of electricity cannot properly adjust to reflect the cost of carbon due to the government’s intervention in the power industry. This study presents an additional argument in support of the inclusion of indirect emissions: it can help to mitigate market power concerns. The HHI, the major concentration measure, in the South Korean ETS substantially decreases in the case of covering both direct and indirect emissions. A similar level of the moderation of market concentration is also observed using different concentration measures. Such an effect of including indirect emissions carries over into other ETSs that do not have as many players as the EU-ETS or the California ETS, and thus is exposed to the risk of market power.

The findings in this study have important policy implications because one of the main concerns of policymakers is that some firms may well enjoy market power owing to their share of emissions. In economies with regulated electricity prices, covering indirect emissions may not only open another channel for cost pass-through but may also lower market power concerns. Given that many national and regional governments are currently considering launching ETSs to cut greenhouse gas emissions, this finding is worth considering in the initial stage of the ETS design.

However, it should not be ignored that including indirect emissions will incur costs due to double counting. Since this paper mainly focuses on its positive effect of mitigating market power, the costs associated with double counting are beyond the scope of this paper. To conclude whether it is desirable to include indirect emissions, more research is needed to reach a fuller understanding involving all benefits and costs.

{kind=link}