An Artificial Neural Network Approach to Predicting Most Applicable Post-Contract Cost Controlling Techniques in Construction Projects

Abstract

:1. Introduction

2. Literature Review

2.1. Post-Contract Cost Control and the Decision-Making Process

2.2. Post-Contract Cost Control Techniques in Construction

2.3. Artificial Neural Network in Construction Management Research

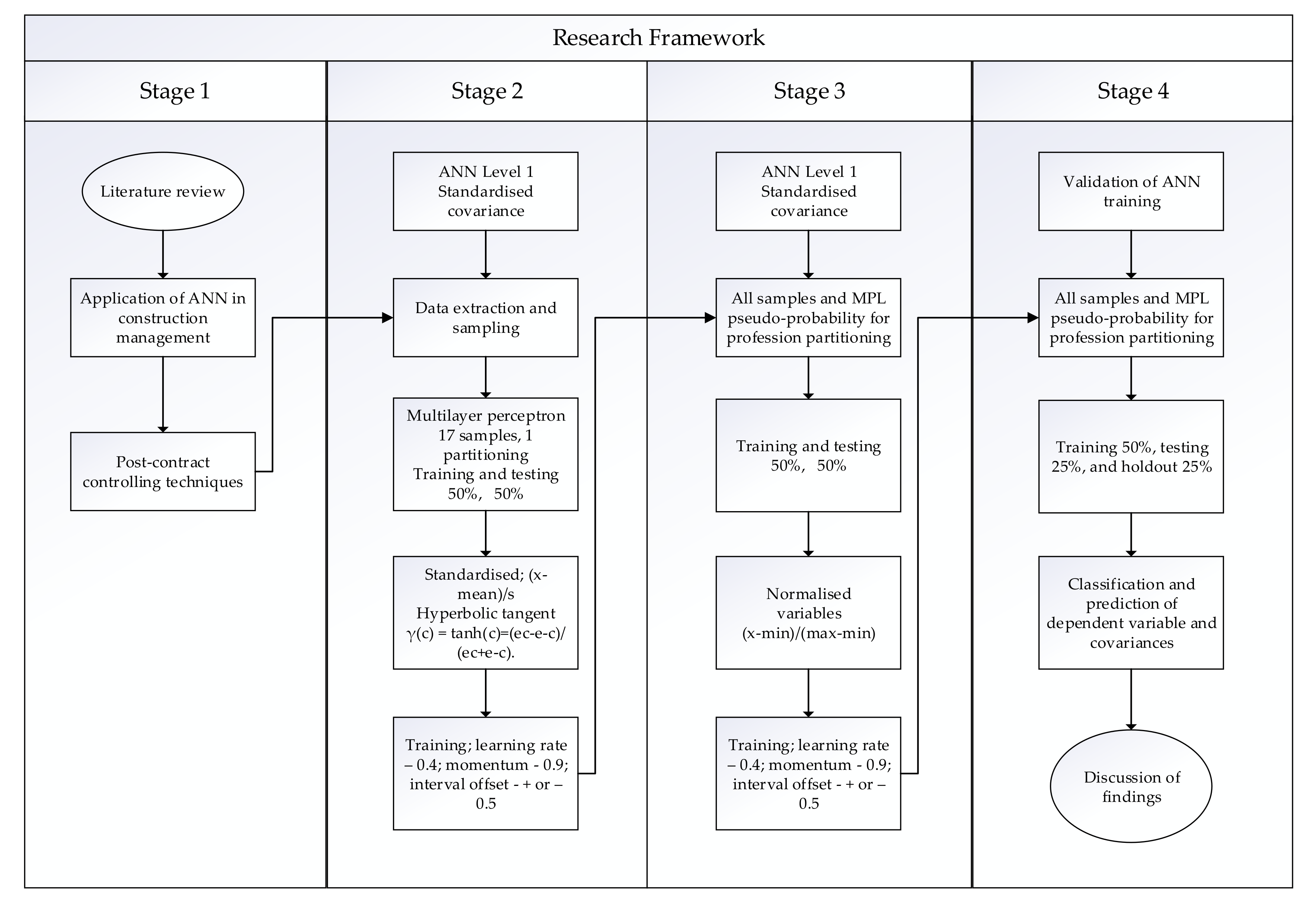

3. Research Methodology

Artificial Neural Network: Multilayer Perceptron (MPL)

4. Presentation and Discussion of Findings

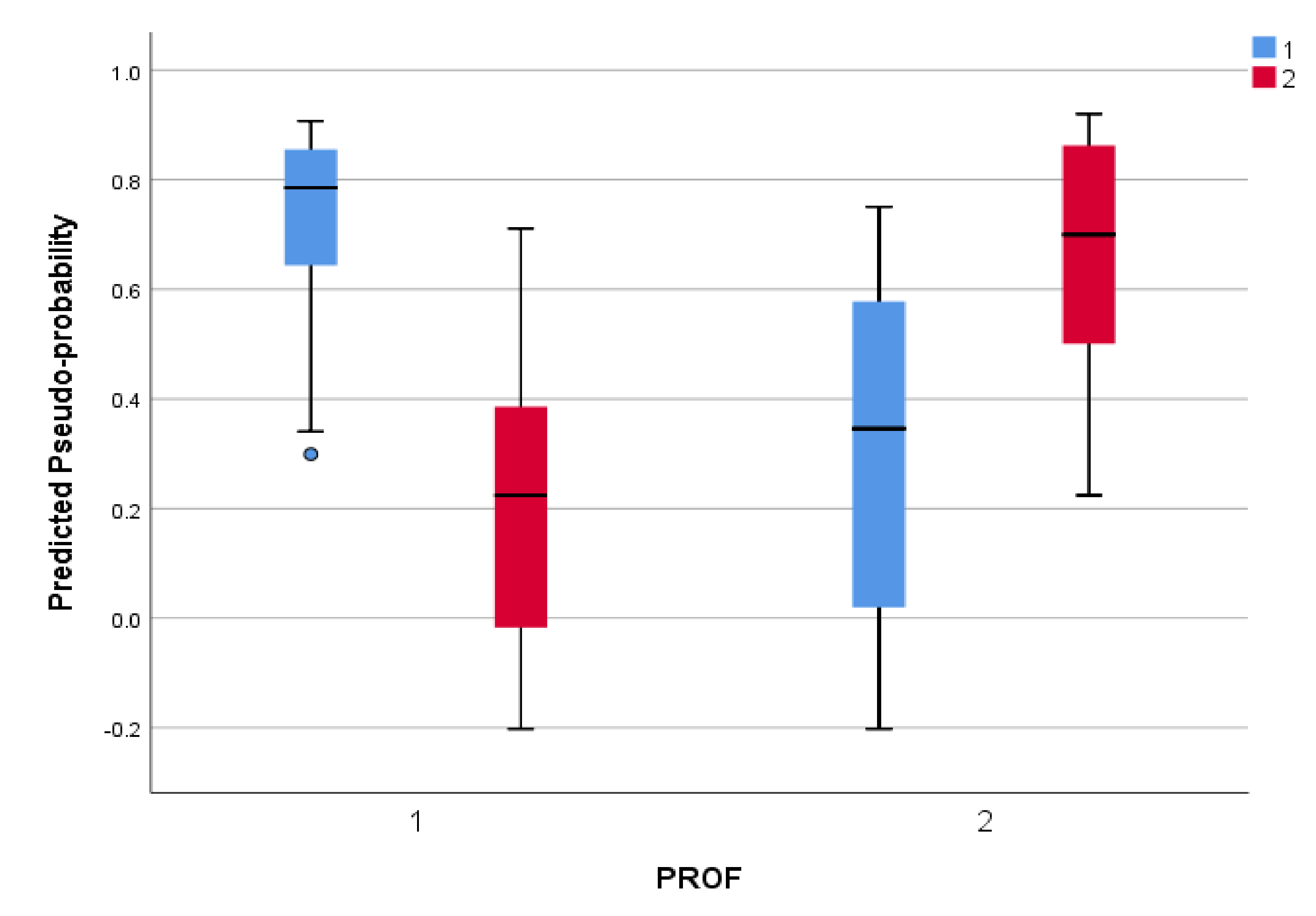

4.1. Predicted Pseudo-Probability of the Professionals

4.2. Importance of the Independent Variables

4.3. Validation Using Holdout Samples

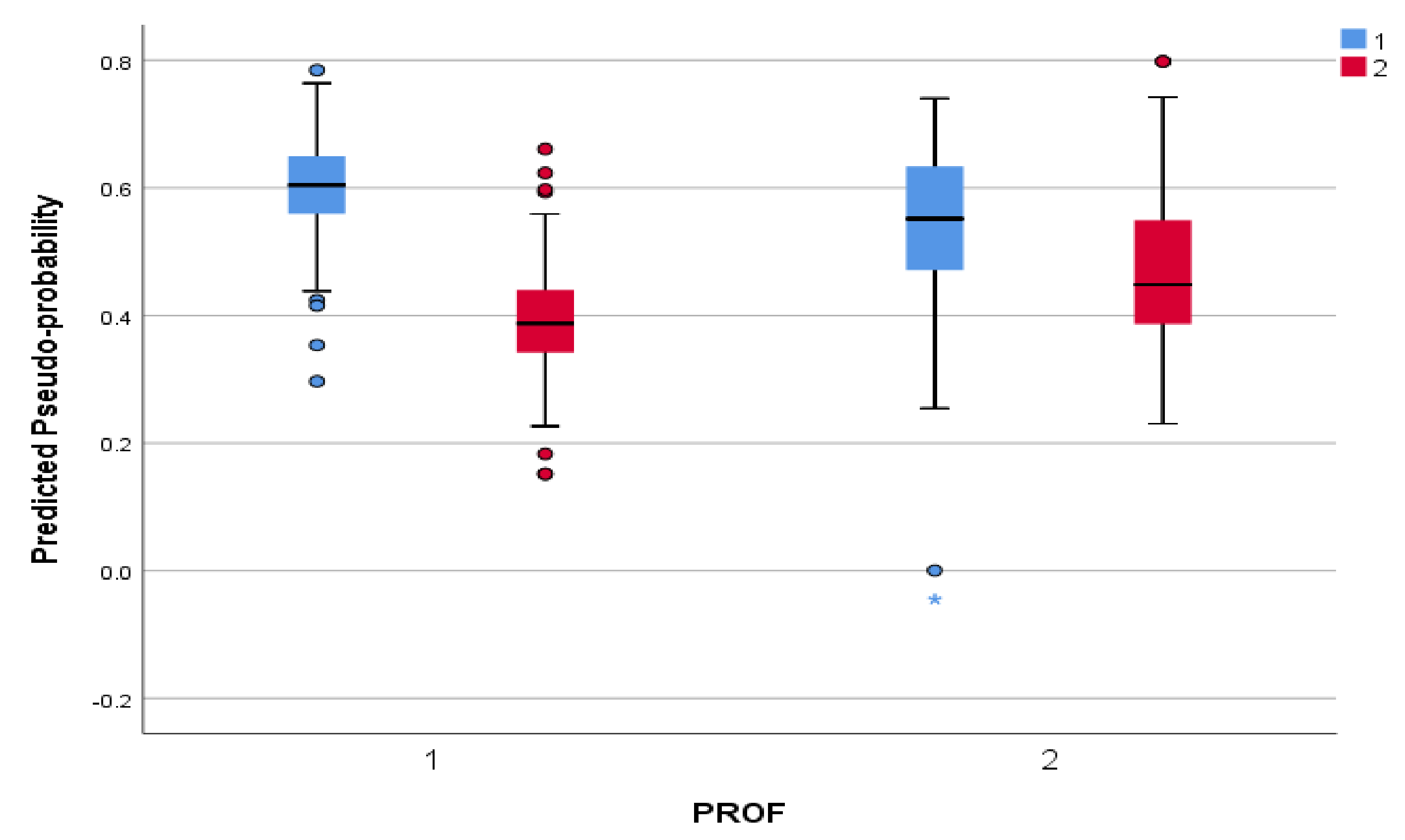

4.4. Validated Predicted Pseudo-Probability of the Professionals

4.5. Importance of the Validated Normalised Independent Variables

4.6. Reliability of Models Using Root Square Mean Error (RMSE)

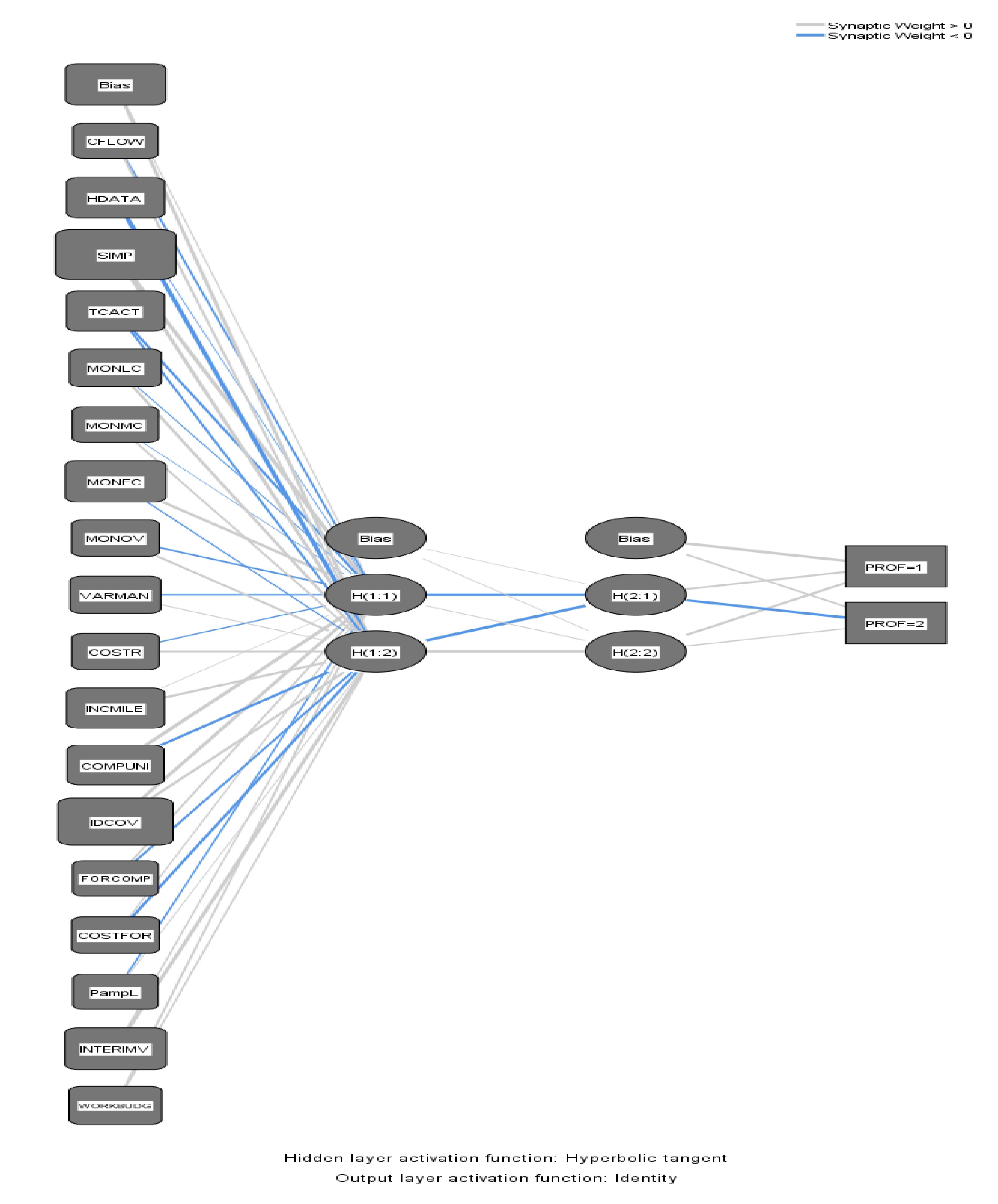

4.7. Network Model

5. The Implications of Results

5.1. Levels 1 and 2

5.2. Validation: Towards the End and after Construction

6. Limitations of this Study

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Jugdev, K.; Müller, R. A retrospective look at our evolving understanding of project success. Proj. Manag. J. 2005, 36, 19–31. [Google Scholar] [CrossRef]

- Munns, A.K.; Bjeirmi, B.F. The role of project management in achieving project success. Int. J. Proj. Manag. 1996, 14, 81–87. [Google Scholar] [CrossRef]

- Radujković, M.; Sjekavica, M. Project management success factors. Procedia Eng. 2017, 196, 607–615. [Google Scholar] [CrossRef]

- Khodeir, L.M.; El Ghandour, A. Examining the role of value management in controlling cost overrun [application on residential construction projects in Egypt]. Ain Shams Eng. J. 2019, 10, 471–479. [Google Scholar] [CrossRef]

- Petheram, C.; McMahon, T. Dams, dam costs and damnable cost overruns. J. Hydrol. X 2019, 3, 100026. [Google Scholar] [CrossRef]

- Pinheiro Catalão, F.; Cruz, C.O.; Sarmento, J.M. Exogenous determinants of cost deviations and overruns in local infrastructure projects. Constr. Manag. Econ. 2019, 37, 697–711. [Google Scholar] [CrossRef]

- Love, P.E.; Sing, M.C.; Ika, L.A.; Newton, S. The cost performance of transportation projects: The fallacy of the Planning Fallacy account. Transp. Res. Part A Policy Pract. 2019, 122, 1–20. [Google Scholar] [CrossRef]

- Pilger, J.D.; Machado, Ê.L.; de Assis Lawisch-Rodriguez, A.; Zappe, A.L.; Rodriguez-Lopez, D.A. Environmental impacts and cost overrun derived from adjustments of a road construction project setting. J. Clean. Prod. 2020, 2020, 120731. [Google Scholar] [CrossRef]

- Cunningham, T. Cost Control during The Construction Phase of the Building Project: The Consultant Quantity Surveyor’s Perspective; Dublin Institute of Technology: Dublin, Ireland, 2017. [Google Scholar]

- Potts, K.; Ankrah, N. Construction Cost Management: Learning from Case Studies; Routledge: London, UK, 2014. [Google Scholar]

- Omotayo, T.; Kulatunga, U. A continuous improvement framework using IDEF0 for post-contract cost control. J. Constr. Project Manag. Innov. 2017, 7, 1807–1823. [Google Scholar]

- Monyane, G.; Emuze, F.; Awuzie, B.; Crafford, G. Evaluating a Collaborative Cost Management Framework with Lean Construction Experts. In Proceedings of the The 10th International Conference on Engineering, Project, and Production Management, Berlin, Germany, 2–4 September 2019; Springer: Singapore, 2020. [Google Scholar]

- Ahsan, K.; Ho, M.; Khan, S. Recruiting project managers: A comparative analysis of competencies and recruitment signals from job advertisements. Project Manag. J. 2013, 44, 36–54. [Google Scholar] [CrossRef]

- Ashworth, A.; Perera, S. Cost Studies of Buildings; Routledge: London, UK, 2015. [Google Scholar]

- Olawale, Y.A.; Sun, M. Cost and time control of construction projects: Inhibiting factors and mitigating measures in practice. Constr. Manag. Econ. 2010, 28, 509–526. [Google Scholar] [CrossRef]

- Cartlidge, D. Construction Project Manager’s Pocket Book; Routledge: London, UK, 2015. [Google Scholar]

- Oyeyipo, O.; Odusami, K.T.; Ojelabi, R.A.; Afolabi, A.O. Factors affecting contractors’ bidding decisions for construction projects in Nigeria. J. Constr. Dev. Ctries. 2016, 21, 21–35. [Google Scholar] [CrossRef]

- Igwe, U.S.; Mohamed, S.F.; Azwarie, M.B.M.D.; Paulson Eberechukwu, N. Recent Developments in Construction Post Contract Cost Control Systems. J. Comput. Theor. Nanosci. 2020, 17, 1236–1241. [Google Scholar] [CrossRef]

- Abobakr, A. Necessity of Cost Control Process (Pre & Post Contract Stage) in Construction Projects: Cost Control in Pre & Post Contract. MSc Thesis, University of Applied Sciences, Berlin, Germany, 2018. [Google Scholar]

- Sanni, A.; Durodola, O. Assessment of contractors’ cost control practices in Metropolitan Lagos. In Proceedings of the Procs 4th West Africa built Environment Research (WABER) Conference, Abuja, Nigeria, 24–26 July 2012. [Google Scholar]

- Mac-Barango, D. Cost Control Systems and Good Governance: Tools for Effective Project Delivery. Int. J. Econ. Financ. Manag. 2017, 2, 29–44. [Google Scholar]

- Omotayo, T.; Kulatunga, U. Re-Thinking Post-Contract Cost Controlling Techniques in the Nigerian Construction Industry. In Proceedings of the 5th World Construction Symposium: Greening Environment, Eco Innovations and Entrepreneurship, Colombo, Sri Lanka, 29–31 July 2016. [Google Scholar]

- Kern, A.; Soares, A.; Formoso, C. Introducing target costing in cost planning and control: A case study in a Brazilian construction firm. In Proceedings of the CIB W107 Construction in Developing Countries International Symposium-“ Construction in Developing Economies: New issues and Challenges”, Santiago, Brazil, 18–20 January 2006. [Google Scholar]

- Fedorova, N.V.; Shaforost, D.A.; Bundikova, V.R.; Denisova, I.A. Some aspects of functional modeling in the IDEF0 standard as the initial stage of TPPs design. AIP Conf. Proc 2019, 2188, 050010. [Google Scholar]

- Presley, A.; Liles, D.H. The use of IDEF0 for the design and specification of methodologies. In Proceedings of the 4th Industrial Engineering Research Conference, Nashville, TN, USA, 24–25 May 1995. [Google Scholar]

- Oladapo, M. A framework for cost management of low-cost housing. In Proceedings of the International Conference on Spatial Information for Sustainable Development, Nairobi, Kenya, 2–5 October 2001. [Google Scholar]

- Akintoye, A.S.; Ajewole, O.; Olomolaiye, P.O. Construction cost information management in Nigeria. Constr. Manag. Econ. 1992, 10, 107–116. [Google Scholar] [CrossRef]

- Corbett, P.; Rowley, P. The use of BCIS elemental cost data by quantity surveyors as part of cost planning techniques: The practitioners’ perspective. In Proceedings of the 15th Annual ARCOM Conference, Liverpool John Moores University, Liverpool, UK, 15–17 September 1999. [Google Scholar]

- Robson, A.; Boyd, D.; Thurairajah, N. Studying ‘cost as information’ to account for construction improvements. Constr. Manag. Econ. 2016, 34, 418–431. [Google Scholar] [CrossRef]

- Sanni, A.; Hashim, M. Assessing the challenges of cost control practices in Nigerian construction industry. Interdiscip. J. Contemp. Res. Bus. 2013, 4, 366–374. [Google Scholar]

- Aliverdi, R.; Naeni, L.M.; Salehipour, A. Monitoring project duration and cost in a construction project by applying statistical quality control charts. Int. J. Project Manag. 2013, 31, 411–423. [Google Scholar] [CrossRef]

- Kubba, S. Handbook of Green Building Design and Construction: LEED, BREEAM, and Green Globes; Butterworth-Heinemann: Oxford, UK, 2012. [Google Scholar]

- Al-Jibouri, S.H. Monitoring systems and their effectiveness for project cost control in construction. Int. J. Project Manag. 2003, 21, 145–154. [Google Scholar] [CrossRef] [Green Version]

- Al-Hazim, N.; Salem, Z.A.; Ahmad, H. Delay and cost overrun in infrastructure projects in Jordan. Procedia Eng. 2017, 182, 18–24. [Google Scholar] [CrossRef]

- Bolhassani, B.; Hovorka, S.D.; Hosseini, S.A.; Young, M.H.; Anderson, J.S.; Yang, C. Model-based assessment of the site-specific cost of monitoring. Energy Procedia 2017, 114, 5316–5319. [Google Scholar] [CrossRef]

- Moser, R.; Narayanamurthy, G.; Kusaba, K.; Kaiser, G. Performance of low-cost country sourcing projects–Conceptual model & empirical analysis. Int. J. Prod. Econ. 2018, 204, 30–43. [Google Scholar]

- Jeong, H.; Sun, A.Y.; Zhang, X. Cost-optimal design of pressure-based monitoring networks for carbon sequestration projects, with consideration of geological uncertainty. Int. J. Greenh. Gas Control 2018, 71, 278–292. [Google Scholar] [CrossRef]

- Martens, A.; Vanhoucke, M. The impact of applying effort to reduce activity variability on the project time and cost performance. Eur. J. Oper. Res. 2019, 277, 442–453. [Google Scholar] [CrossRef] [Green Version]

- Odeck, J.; Kjerkreit, A. The accuracy of benefit-cost analyses (BCAs) in transportation: An ex-post evaluation of road projects. Transp. Res. Part A Policy Pract. 2019, 120, 277–294. [Google Scholar] [CrossRef]

- Oliveira, R. Monitoring and Control of Schedule and Cost Performance in Facade Conservation. Procedia Struct. Integr. 2019, 22, 151–159. [Google Scholar] [CrossRef]

- Cavalieri, M.; Cristaudo, R.; Guccio, C. On the magnitude of cost overruns throughout the project life-cycle: An assessment for the Italian transport infrastructure projects. Transp. Policy 2019, 79, 21–36. [Google Scholar] [CrossRef]

- Çelik, T.; Arayici, Y.; Budayan, C. Assessing the social cost of housing projects on the built environment: Analysis and monetization of the adverse impacts incurred on the neighbouring communities. Environ. Impact Assess. Rev. 2019, 77, 1–10. [Google Scholar] [CrossRef]

- Peñaloza, G.A.; Saurin, T.A.; Formoso, C.T. Monitoring complexity and resilience in construction projects: The contribution of safety performance measurement systems. Appl. Ergon. 2020, 82, 102978. [Google Scholar] [CrossRef]

- Construction Industry Institute. Control for Construction; Construction Industry Institute: Texas, TX, USA, 1987. [Google Scholar]

- Czernigowska, A. Earned value method as a tool for project control. Bud. Archit. 2008, 3, 15–32. [Google Scholar]

- Verma, A.; Pathak, K.; Dixit, R. Earned value analysis of construction project at Rashtriya Sanskrit Sansthan, Bhopal. Int. J. Innov. Res. Sci. Eng. Technol. 2014, 3, 11350–11355. [Google Scholar]

- Puvanasvaran, A.; Kerk, S.; Ismail, A. A case study of kaizen implemention in SMI. In Proceedings of the National Conference in Mechanical Engineering Research and Postgraduate Studies, UMP Pekan, Pahang, Malaysia, 3–4 December 2010. [Google Scholar]

- Okoye, P.V.C.; Egbunike, F.C.; Meduoye, O.M. Product cost management via the kaizen costing system: Perception of Accountants. J. Mgmt. Sustain. 2013, 3, 114. [Google Scholar]

- Sanchez, F.; Steria, S.; Bonjour, E.; Micaelli, J.P.; Monticolo, D. An approach based on bayesian network for improving project management maturity: An application to reduce cost overrun risks in engineering projects. Comput. Ind. 2020, 119, 1066–3615. [Google Scholar] [CrossRef]

- Sarbayev, M.; Yang, M.; Wang, H. Risk assessment of process systems by mapping fault tree into artificial neural network. J. Loss Prev. Process Ind. 2019, 60, 203–212. [Google Scholar] [CrossRef]

- Zainuddin, N.H.; Lola, M.S.; Djauhari, M.A.; Yusof, F.; Ramlee, M.N.A.; Deraman, A.; Ibrahim, Y.; Abdullah, M.T. Improvement of time forecasting models using a novel hybridization of bootstrap and double bootstrap artificial neural networks. Appl. Soft Comput. 2019, 84, 1568–4946. [Google Scholar] [CrossRef]

- Bewes, J.; Low, A.; Morphett, A.; Pate, F.D.; Henneberg, M. Artificial intelligence for sex determination of skeletal remains: Application of a deep learning artificial neural network to human skulls. J. Forensic Legal Med. 2019, 62, 40–43. [Google Scholar] [CrossRef]

- Ok, S.C.; Sinha, S.K. Construction equipment productivity estimation using artificial neural network model. Constr. Manag. Econ. 2006, 24, 1029–1044. [Google Scholar] [CrossRef]

- Attalla, M.; Hegazy, T. Predicting cost deviation in reconstruction projects: Artificial neural networks versus regression. J. Constr. Eng. Manag. 2003, 129, 405–411. [Google Scholar] [CrossRef]

- Ogunlana, S.O.; Sdhabhon, B. Application of artificial neural network to forecast construction duration of buildings at the predesign stage. Eng. Constr. Archit. Manag. 1999, 6, 133–144. [Google Scholar]

- Bhosale, A.; Konnur, B. Use of Artificial Neural Network in Construction Management. Int. J. Innov. Eng. Sci. 2019, 4, 73–76. [Google Scholar]

- Waziri, B.S.; Bala, K.; Bustani, S.A. Artificial neural networks in construction engineering and management. Int. J. Arch. Eng. Constr. 2017, 6, 50–60. [Google Scholar] [CrossRef]

- StackExchange. What is the difference between estimation and prediction? 2011. Available online: https://stats.stackexchange.com/questions/17773/what-is-the-difference-between-estimation-and-prediction (accessed on 20 January 2020).

- Goh, Y.M.; Chua, D. Neural network analysis of construction safety management systems: A case study in Singapore. Constr. Manag. Econ. 2013, 31, 460–470. [Google Scholar] [CrossRef]

- Sodikov, J. Cost estimation of highway projects in developing countries: Artificial neural network approach. J. East. Asia Soc. Transp. Stud. 2005, 6, 1036–1047. [Google Scholar]

- Jha, K.N.; Chockalingam, C. Prediction of schedule performance of Indian construction projects using an artificial neural network. Constr. Manag. Econ. 2011, 29, 901–911. [Google Scholar] [CrossRef]

- Wilmot, C.G.; Mei, B. Neural network modeling of highway construction costs. J. Constr. Eng. Manag. 2005, 131, 765–771. [Google Scholar] [CrossRef]

- Lam, K.C.; Ng, S.T.; Tiesong, H.; Skitmore, M.; Cheung, S.O. Decision support system for contractor pre-qualification—artificial neural network model. Eng. Constr. Archit. Manag. 2000, 7, 251–266. [Google Scholar]

- Shan, M.; Le, Y.; Yiu, K.T.; Chan, A.P.; Hu, Y.; Zhou, Y. Assessing collusion risks in managing construction projects using artificial neural network. Technol. Econ. Dev. Econ. 2018, 24, 2003–2025. [Google Scholar] [CrossRef]

- Li, H.; Love, P.E. Combining rule-based expert systems and artificial neural networks for mark-up estimation. Constr. Manag. Econ. 1999, 17, 169–176. [Google Scholar] [CrossRef]

- Mirahadi, F.; Zayed, T. Simulation-based construction productivity forecast using neural-network-driven fuzzy reasoning. Autom. Constr. 2016, 65, 102–115. [Google Scholar] [CrossRef]

- Shan, M.; Le, Y.; Yiu, K.T.; Chan, A.P.; Hu, Y.; Zhou, Y. Application of artificial neural network (s) in predicting formwork labour productivity. Adv. Civil Eng. 2019, 2019, 1–11. [Google Scholar]

- Arafa, M.; Alqedra, M. Early stage cost estimation of buildings construction projects using artificial neural networks. Early Stage Cost Estim. Build. Constr. Proj. Using Artif. Neural Netw. 2011, 4, 63–75. [Google Scholar] [CrossRef] [Green Version]

- Owens, L.K. Introduction to survey research design. SRL Fall 2002 Seminar Series, 1 January 2002. [Google Scholar]

- Roman, N.D.; Bre, F.; Fachinotti, V.D.; Lamberts, R. Application and characterization of metamodels based on artificial neural networks for building performance simulation: A systematic review. Energy Build. 2020, 2020, 109972. [Google Scholar] [CrossRef]

- International Business Machine (IBM). IBM Neural Networks 19; SPPS: Sussex, UK, 2010. [Google Scholar]

- Yu, Y.; Qu, Y. Multi-component spectral detection based on neural network in water quality inspection. Optik 2020, 2020, 164915. [Google Scholar] [CrossRef]

- Iyer, R.; Menon, V.; Buice, M.; Koch, C.; Mihalas, S. The influence of synaptic weight distribution on neuronal population dynamics. PLoS Comput. Biol. 2013, 9, e1003248. [Google Scholar] [CrossRef] [Green Version]

- Kharin, V.V.; Zwiers, F.W. On the ROC score of probability forecasts. J. Clim. 2003, 16, 4145–4150. [Google Scholar] [CrossRef]

- Fawcett, T. An introduction to ROC analysis. Pattern Recognit. Lett. 2006, 27, 861–874. [Google Scholar] [CrossRef]

- AgriMetSoft. RMSE (Root Mean Square Error). 2019. Available online: https://agrimetsoft.com/calculators/Root%20Mean%20Square%20Error (accessed on 4 June 2020).

- Nykamp, D. An introduction to networks. 2020. Available online: https://mathinsight.org/network_introduction (accessed on 4 January 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| CODE | Post-Contract Cost Controlling Techniques | Sources |

|---|---|---|

| CFLOW | Cash flow | [14,20,30] |

| WORKBUD | Working budget | [14,20,30] |

| TCACT | Taking corrective action | [14,20] |

| MONOV | Monitoring overheads | [14,20,30,31,32] |

| MONLC | Monitoring labour cost | [14,20,30,33] |

| MONMC | Monitoring material cost | [14,20,34,35,36] |

| MONEC | Monitoring equipment cost | [14,20,37,38] |

| VARMAN | Managing variations | [14,15,20,39,40] |

| FORCOM | Forecasting at completion | [41,42] |

| COMPUNI | Compounding unit | [14,15] |

| INTERIMV | Interim valuations | [14,43] |

| INCMIL | Incremental milestone | [36,37,44] |

| SIMP | Site meeting and post-project reviews | [45,46] |

| IDCOV | Identifying indicators of cost overruns | [14,15,20] |

| PampL | Summarising profit and loss | [14,20,43] |

| HDATA | Historical data | [47,48] |

| COSTR | Cost ratio | [20,49] |

| COSTFOR | Cost forecasting | [20,39,40] |

| Summary | Level 1 | Level 2 |

|---|---|---|

| Input Layer | ||

| Valid number of Samples | 135 | 135 |

| Number of Units | 17 | 18 |

| Rescaling Method for Covariates | Standardized | Normalized |

| Hidden Layer | ||

| Number of Hidden Layers (1) | √ | √ |

| Number of Units in Hidden (6) Layer 1 | √ | √ |

| Activation Function (Hyperbolic tangent) | √ | √ |

| Output Layer | ||

| Dependent Variable (1) | √ | √ |

| Number of Units (2) | √ | √ |

| Activation Function (hyperbolic tangent) | √ | √ |

| Error Function (Sum of Squares) | 16.706 | 29.829 |

| Training time (sec) | 2 | 3 |

| Predictor | Predicted | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Hidden Layer 1 | Output Layer | ||||||||

| H(1:1) | H(1:2) | H(1:3) | H(1:4) | H(1:5) | H(1:6) | QS | CPM | ||

| Input Layer | (Bias) | 0.217 | 0.290 | 0.346 | −0.143 | 0.535 | 0.025 | ||

| CFLOW | −0.303 | 0.107 | 0.487 | 0.057 | −0.243 | 0.370 | |||

| HDATA | 0.030 | −0.661 | −0.083 | 0.196 | −0.558 | −0.461 | |||

| SIMP | 0.062 | 0.514 | −0.243 | 0.331 | −0.001 | −0.187 | |||

| TCACT | 0.019 | 0.520 | −0.435 | −0.102 | 0.144 | −0.562 | |||

| MONLC | 0.034 | 0.202 | −0.395 | −0.115 | 0.197 | −0.007 | |||

| MONMC | −0.095 | −0.100 | −0.377 | −0.481 | −0.504 | 0.486 | |||

| MONEC | 0.201 | −0.882 | 0.183 | −0.045 | −0.521 | −0.212 | |||

| MONOV | −0.541 | 0.479 | −0.805 | −0.505 | −0.616 | 0.232 | |||

| VARMAN | 0.653 | −0.441 | −0.072 | 0.592 | 0.191 | −0.245 | |||

| COSTR | −0.365 | 0.277 | 0.432 | 0.932 | −0.554 | 0.078 | |||

| INCMILE | −0.806 | 0.405 | −0.124 | 0.501 | −0.568 | −0.113 | |||

| COMPUNI | −0.115 | 0.431 | 0.098 | 0.185 | 0.456 | 0.277 | |||

| IDCOV | −0.152 | −0.071 | −0.577 | −0.840 | 0.391 | 0.596 | |||

| FORCOMP | 0.099 | −0.353 | −0.690 | −0.051 | −0.335 | −0.061 | |||

| COSTFOR | −0.338 | 0.381 | −0.348 | −0.239 | −0.014 | 0.793 | |||

| INTERIMV | 0.706 | −0.094 | −0.613 | 0.192 | 0.616 | 0.172 | |||

| WORKBUD | 0.601 | 0.166 | −0.934 | −0.162 | 0.665 | 0.569 | |||

| Hidden Layer 1 | (Bias) | 0.503 | 0.740 | ||||||

| H(1:1) | 1.063 | −1.063 | |||||||

| H(1:2) | 0.565 | −0.617 | |||||||

| H(1:3) | 0.594 | −0.536 | |||||||

| H(1:4) | −0.463 | 0.485 | |||||||

| H(1:5) | −1.046 | 1.069 | |||||||

| H(1:6) | 0.421 | −0.421 | |||||||

| Predictor | Predicted | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Hidden Layer 1 | Output Layer | ||||||||

| H(1:1) | H(1:2) | H(1:3) | H(1:4) | H(1:5) | H(1:6) | QS | CPM | ||

| Input Layer | (Bias) | 0.058 | −0.064 | 0.266 | 0.452 | 0.350 | 0.184 | ||

| CFLOW | 0.254 | 0.053 | 0.562 | 0.349 | 0.376 | 0.303 | |||

| HDATA | 0.527 | −0.144 | −0.158 | −0.372 | −0.261 | 0.195 | |||

| SIMP | 0.196 | 0.253 | −0.062 | 0.138 | 0.023 | 0.434 | |||

| TCACT | 0.072 | 0.376 | −0.500 | 0.030 | −0.382 | 0.456 | |||

| MONLC | 0.341 | 0.564 | 0.151 | 0.078 | 0.077 | −0.044 | |||

| MONMC | −0.297 | 0.523 | 0.283 | 0.224 | −0.322 | 0.606 | |||

| MONEC | −0.405 | −0.090 | 0.566 | −0.339 | −0.402 | 0.667 | |||

| MONOV | −0.130 | 0.136 | −0.098 | 0.196 | 0.326 | −0.201 | |||

| VARMAN | −0.272 | −0.100 | −0.340 | −0.322 | −0.247 | 0.030 | |||

| COSTR | −0.146 | −0.342 | −0.059 | 0.334 | 0.107 | −0.099 | |||

| INCMILE | −0.278 | 0.338 | 0.529 | −0.627 | −0.388 | 0.275 | |||

| COMPUNI | 0.617 | −0.223 | −0.076 | −0.034 | 0.058 | −0.413 | |||

| IDCOV | 0.381 | −0.352 | −0.189 | 0.233 | 0.074 | 0.294 | |||

| FORCOMP | 0.018 | −0.104 | 0.117 | −0.098 | 0.126 | 0.275 | |||

| COSTFOR | −0.349 | 0.140 | 0.656 | 0.114 | 0.335 | 0.159 | |||

| INTERIMV | 0.160 | 0.445 | 0.546 | 0.017 | 0.132 | −0.185 | |||

| WORKBUD | 0.627 | 0.574 | −0.225 | 0.322 | −0.107 | 0.056 | |||

| PampL | 0.215 | −0.567 | 0.285 | −0.444 | −0.235 | −0.069 | |||

| Hidden Layer 1 | (Bias) | 0.555 | 0.030 | ||||||

| H(1:1) | −0.494 | 0.367 | |||||||

| H(1:2) | 0.163 | −0.294 | |||||||

| H(1:3) | 0.259 | −0.198 | |||||||

| H(1:4) | 0.527 | −0.388 | |||||||

| H(1:5) | 0.295 | −0.229 | |||||||

| H(1:6) | 0.034 | 0.638 | |||||||

| Sample | Observed | QS | CPM | Percent Correct |

|---|---|---|---|---|

| Level 1 | ||||

| Training | QS | 70 | 7 | 90.90% |

| CPM | 19 | 39 | 67.20% | |

| Overall Percent | 65.90% | 34.10% | 80.70% | |

| Level 2 | ||||

| Training | QS | 68 | 9 | 88.30% |

| CPM | 38 | 20 | 34.50% | |

| Overall Percent | 78.50% | 21.50% | 65.20% |

| Level 1 | Level 2 | ||||||

|---|---|---|---|---|---|---|---|

| Variables | Importance | Standardised Importance | Rank | Variables | Importance | Normalised Importance | Rank |

| MONMC | 0.087 | 100.00% | 1 | HDATA | 0.126 | 100.00% | 1 |

| MONOV | 0.086 | 98.40% | 2 | PampL | 0.113 | 89.80% | 2 |

| MONEC | 0.076 | 87.60% | 3 | COSTFOR | 0.089 | 70.10% | 3 |

| INCMILE | 0.071 | 82.00% | 4 | INCMILE | 0.079 | 62.80% | 4 |

| VARMAN | 0.069 | 79.40% | 5 | CFLOW | 0.079 | 62.20% | 5 |

| COSTR | 0.064 | 73.10% | 6 | MONOV | 0.073 | 57.80% | 6 |

| COMPUNI | 0.063 | 72.50% | 7 | VARMAN | 0.061 | 48.50% | 7 |

| WORKBUD | 0.062 | 71.40% | 8 | MONEC | 0.06 | 47.40% | 8 |

| CFLOW | 0.062 | 71.30% | 9 | COSTR | 0.055 | 43.90% | 9 |

| IDCOV | 0.061 | 70.50% | 10 | COMPUNI | 0.053 | 42.10% | 10 |

| INTERIMV | 0.05 | 57.70% | 11 | MONMC | 0.047 | 36.90% | 11 |

| HDATA | 0.05 | 56.80% | 12 | INTERIMV | 0.038 | 30.30% | 12 |

| FORCOMP | 0.049 | 56.00% | 13 | TCACT | 0.035 | 27.70% | 13 |

| COSTFOR | 0.047 | 54.50% | 14 | MONLC | 0.026 | 20.90% | 14 |

| TCACT | 0.039 | 44.50% | 15 | WORKBUD | 0.02 | 16.20% | 15 |

| MONLC | 0.032 | 36.50% | 16 | IDCOV | 0.02 | 15.70% | 16 |

| SIMP | 0.03 | 34.80% | 17 | SIMP | 0.014 | 11.30% | 17 |

| FORCOMP | 0.011 | 8.70% | 18 |

| Activity | Parameters | Values |

|---|---|---|

| Training | Sum of Squares Error | 4.331 |

| Percent Incorrect Predictions | 7.90% | |

| Stopping Rule Used | 1 consecutive step(s) with no decrease in error | |

| Training Time | 00:00.02 | |

| Testing | Sum of Squares Error | 5.283 |

| Percent Incorrect Predictions | 17.10% | |

| Holdout | Percent Incorrect Predictions | 10.70% |

| Predictor | Predicted | ||||||

|---|---|---|---|---|---|---|---|

| Hidden Layer 1 | Hidden Layer 2 | Output Layer | |||||

| H(1:1) | H(1:2) | H(2:1) | H(2:2) | QS | CPM | ||

| Input Layer | (Bias) | 0.046 | 0.322 | ||||

| CFLOW | −0.138 | 0.181 | |||||

| HDATA | −0.012 | −0.474 | |||||

| SIMP | 0.452 | 0.360 | |||||

| TCACT | −0.234 | −0.174 | |||||

| MONLC | −0.038 | 0.306 | |||||

| MONMC | −0.005 | 0.150 | |||||

| MONEC | 0.422 | −0.110 | |||||

| MONOV | −0.210 | 0.299 | |||||

| VARMAN | −0.261 | 0.086 | |||||

| COSTR | −0.135 | 0.274 | |||||

| INCMILE | 0.017 | 0.398 | |||||

| COMPUNI | 0.499 | −0.359 | |||||

| IDCOV | 0.398 | 0.313 | |||||

| FORCOMP | 0.148 | −0.201 | |||||

| COSTFOR | 0.100 | −0.286 | |||||

| PampL | −0.118 | 0.032 | |||||

| INTERIMV | 0.117 | 0.364 | |||||

| WORKBUD | 0.139 | 0.132 | |||||

| Hidden Layer 1 | (Bias) | 0.018 | 0.033 | ||||

| H(1:1) | −0.461 | 0.083 | |||||

| H(1:2) | −0.505 | 0.424 | |||||

| Hidden Layer 2 | (Bias) | 0.575 | 0.222 | ||||

| H(2:1) | 0.318 | −0.474 | |||||

| H(2:2) | 0.324 | 0.137 | |||||

| Sample | Observed | Predicted | ||

|---|---|---|---|---|

| QS | CPM | Percent Correct | ||

| Training | QS | 11 | 26 | 29.7% |

| CPM | 8 | 19 | 70.4% | |

| Overall Percent | 29.7% | 70.3% | 46.9% | |

| Testing | QS | 6 | 14 | 30.0% |

| CPM | 5 | 15 | 75.0% | |

| Overall Percent | 27.5% | 72.5% | 52.5% | |

| Holdout | QC | 6 | 14 | 30.0% |

| CPM | 2 | 9 | 81.8% | |

| Overall Percent | 25.8% | 74.2% | 48.4% | |

| Variable | Importance | Normalised Percentage | Rank |

|---|---|---|---|

| SIMP | 0.152 | 100.00% | 1 |

| IDCOV | 0.131 | 86.20% | 2 |

| INTERIMV | 0.08 | 52.60% | 3 |

| MONEC | 0.077 | 50.90% | 4 |

| HDATA | 0.068 | 44.60% | 5 |

| TCACT | 0.067 | 44.00% | 6 |

| INCMILE | 0.067 | 44.20% | 7 |

| COMPUNI | 0.062 | 41.00% | 8 |

| WORKBUDG | 0.047 | 30.90% | 9 |

| MONLC | 0.043 | 28.60% | 10 |

| VARMAN | 0.039 | 25.70% | 11 |

| MONOV | 0.029 | 18.80% | 12 |

| COSTFOR | 0.029 | 18.80% | 13 |

| COSTR | 0.027 | 17.80% | 14 |

| MONMC | 0.023 | 15.00% | 15 |

| FORCOMP | 0.02 | 13.30% | 16 |

| PampL | 0.019 | 12.30% | 17 |

| CFLOW | 0.018 | 12.10% | 18 |

| Level | N | R SQUARE | RMSE |

|---|---|---|---|

| 1 | 135 | 0.308 | 0.048 |

| 2 | 135 | 0.725 | 0.073 |

| Validation | 135 | 0.726 | 0.073 |

| Network | Number of Nodes | Number of Non-Zero Edges | Sparsity |

|---|---|---|---|

| QS | 18 | 153/144 | 0.000 |

| CPM | 18 | 153/144 | 0.000 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Omotayo, T.; Bankole, A.; Olubunmi Olanipekun, A. An Artificial Neural Network Approach to Predicting Most Applicable Post-Contract Cost Controlling Techniques in Construction Projects. Appl. Sci. 2020, 10, 5171. https://0-doi-org.brum.beds.ac.uk/10.3390/app10155171

Omotayo T, Bankole A, Olubunmi Olanipekun A. An Artificial Neural Network Approach to Predicting Most Applicable Post-Contract Cost Controlling Techniques in Construction Projects. Applied Sciences. 2020; 10(15):5171. https://0-doi-org.brum.beds.ac.uk/10.3390/app10155171

Chicago/Turabian StyleOmotayo, Temitope, Awuzie Bankole, and Ayokunle Olubunmi Olanipekun. 2020. "An Artificial Neural Network Approach to Predicting Most Applicable Post-Contract Cost Controlling Techniques in Construction Projects" Applied Sciences 10, no. 15: 5171. https://0-doi-org.brum.beds.ac.uk/10.3390/app10155171