A New Approach to Examine Non-Linear and Mediated Growth and Convergence Outcomes of Cohesion Policy

,

,

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Model

3.2. Data

3.3. Estimation Strategy

4. Estimation Results and Discussion

4.1. Fixed Effects Estimations

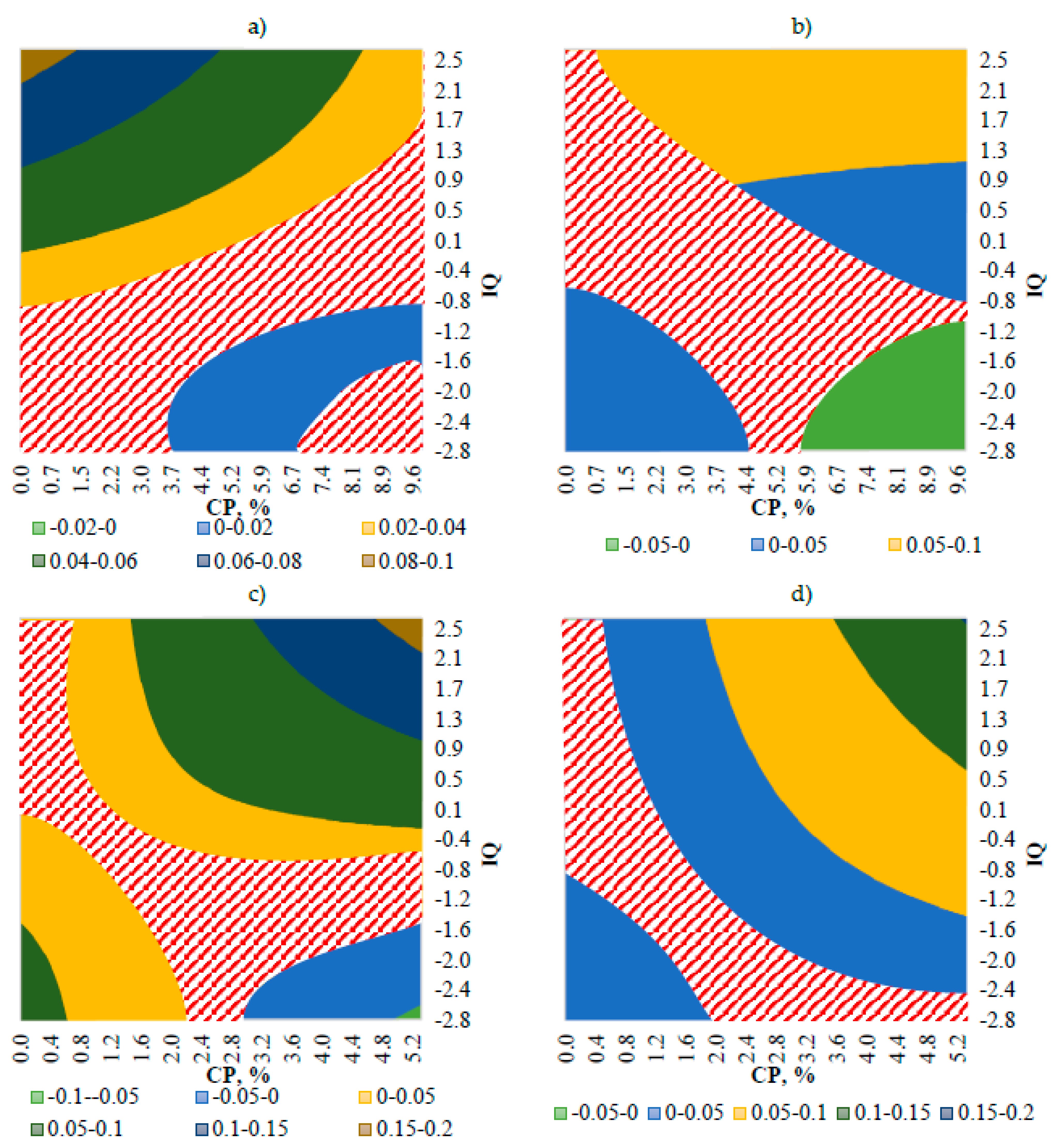

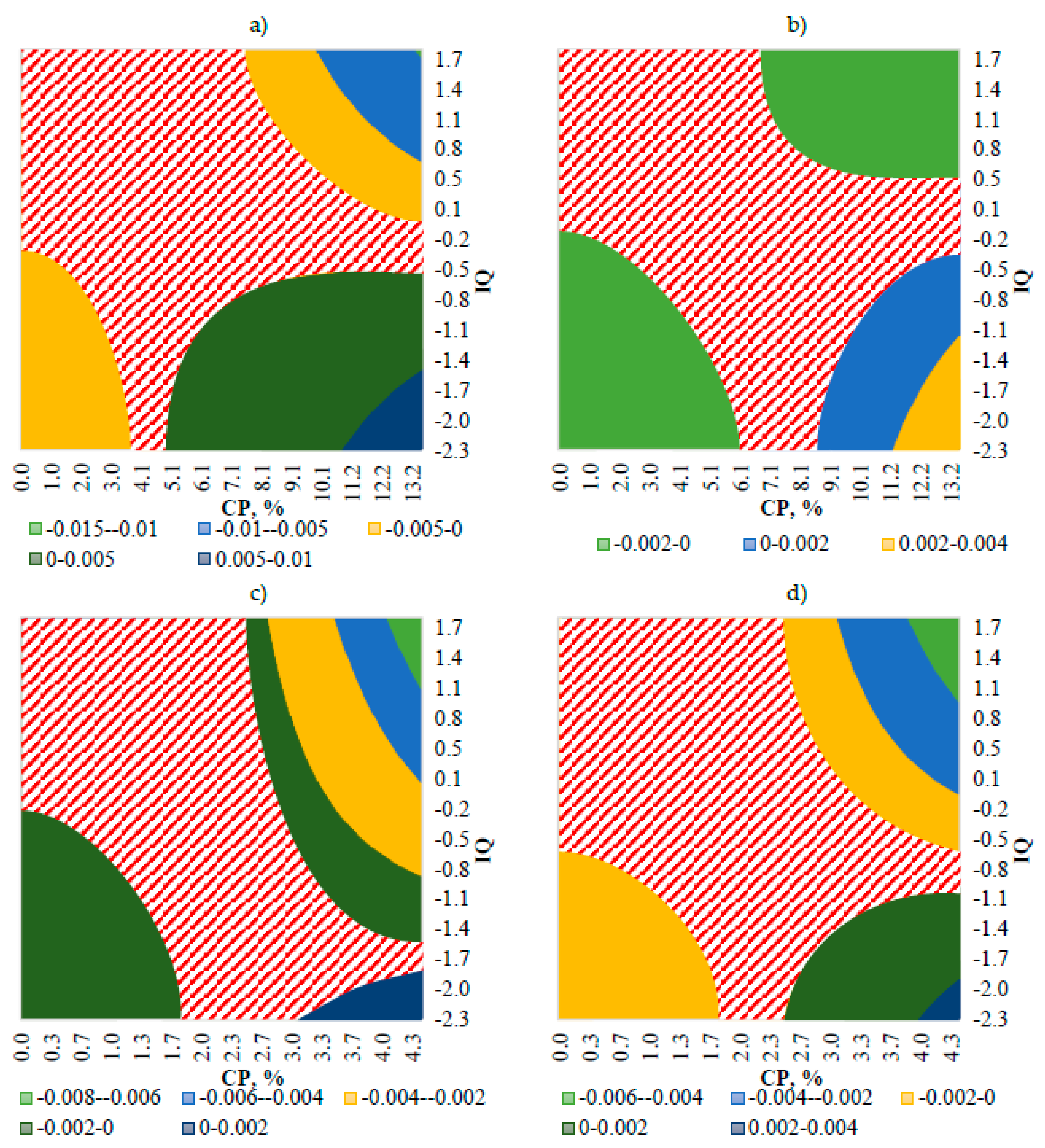

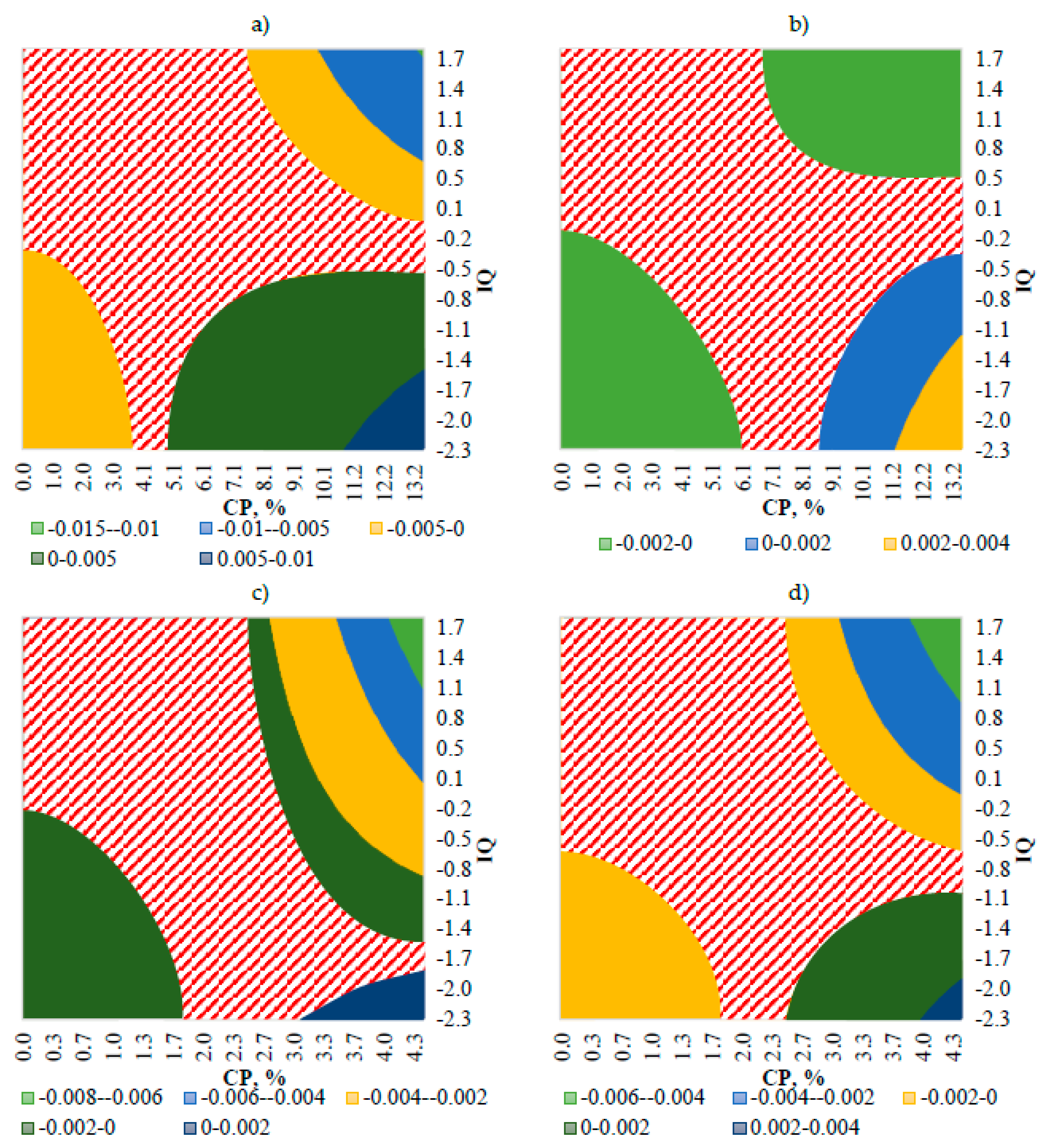

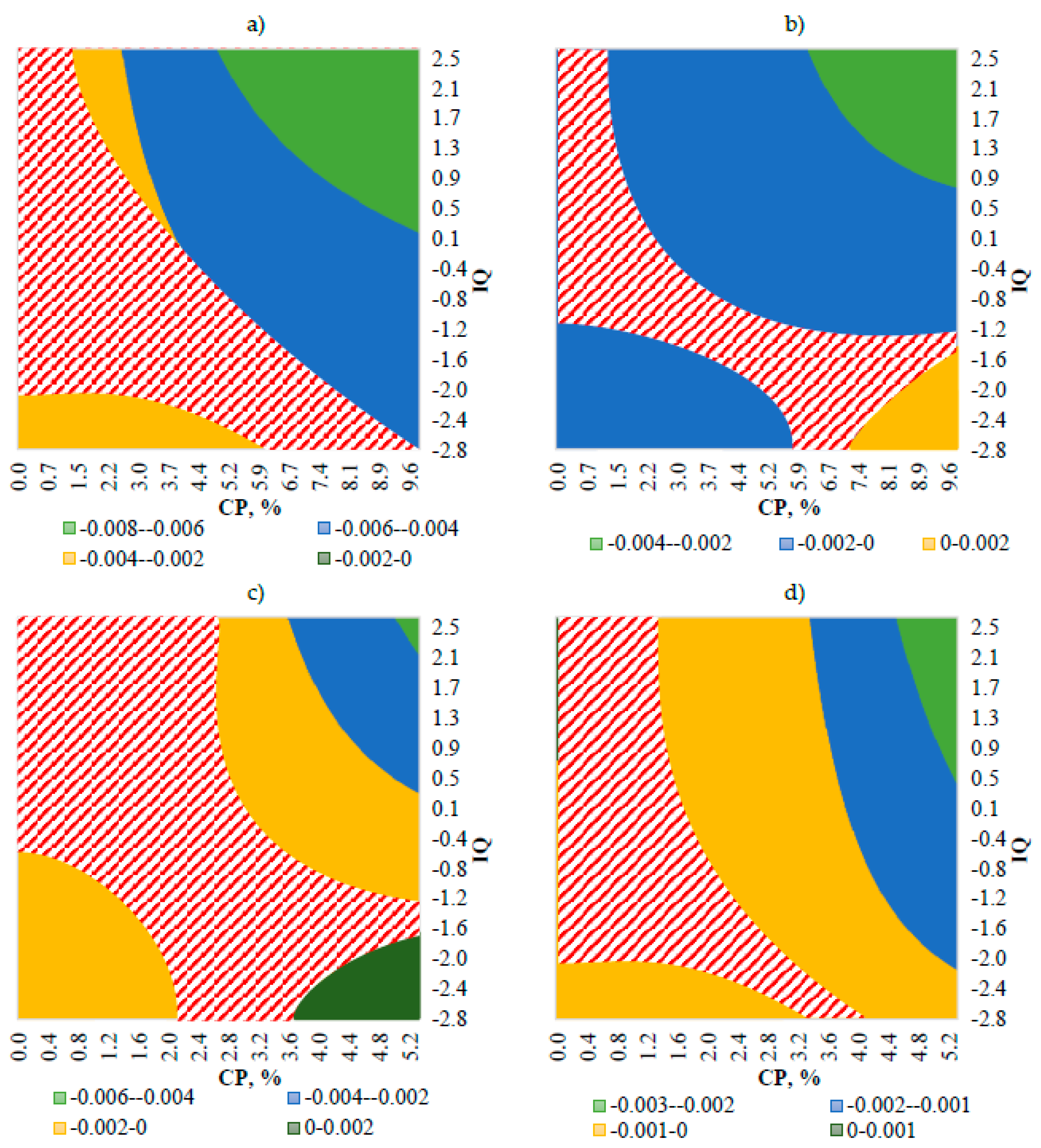

4.2. Non-Linear Effects of CP on Growth Moderated by Institutional Quality

4.3. Non-Linear Convergence Outcomes of CP Moderated by the Institutional Quality

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix B

| 1 | Countries that joined the EU after 2006, i.e., Romania, Bulgaria and Croatia, are not included. |

| 2 | All right-hand side variables in the Equation (2) are lagged twice; thus, we fail to capture effects that manifest with the longer lag. |

| 3 | An alternative input approach to measure innovation activity uses investment in R&D activities. |

| 4 | Cross-sectional independence is tested, using Pesaran’s CD test. |

| 5 | Assuming other factors are equal and IQ = 0. |

| 6 | and are statistically insignificant. |

| 7 | We are measuring here the effect of the intensity of the CP commitment, i.e., CP commitments at a regional level to the regional GDP ratio, equal to 1 percent. |

| 8 | What we saw when analyzing the interaction . |

| 9 | Assuming that there is no moderating effect of institutions on CP represented by . |

| 10 | Estimations are made assuming that the intensity of the CP commitments and the level of institutional quality are all equal to zero. |

| 11 | Assuming that only a linear effect exists. |

| 12 | Assuming that the institutional environment has no effect. |

References

- Arbolino, Roberta, and Raffaele Boffardi. 2017. The Impact of Institutional Quality and Efficient Cohesion Investments on Economic Growth Evidence from Italian Regions. Sustainability 9: 1432. [Google Scholar] [CrossRef] [Green Version]

- Arbolino, Roberta, Paolo Di Caro, and Ugo Marani. 2020. Did the governance of EU funds help Italian regional labour markets during the Great Recession? Journal Common Market Studies 58: 235–55. [Google Scholar] [CrossRef]

- Bähr, Cornelius. 2008. How does Sub-National Autonomy Affect the Effectiveness of Structural Funds? Kyklos 61: 3–18. [Google Scholar] [CrossRef]

- Barca, F. 2009. An Agenda for a Reformed Cohesion Policy: A Place-based Approach to Meeting European Union Challenges and Expectations. Available online: http://www.europarl.europa.eu/meetdocs/2009_2014/documents/regi/dv/barca_report_/barca_report_en.pdf (accessed on 27 September 2019).

- Becker, Sascha O., Peter H. Egger, and Maximilian Von Ehrlich. 2012. Too Much of a Good Thing? On the Growth Effects of the EU’s Regional Policy. European Economic Review 56: 648–68. [Google Scholar] [CrossRef] [Green Version]

- Becker, Sascha O., Peter H. Egger, and Maximilian Von Ehrlich. 2013. Absorptive capacity and the growth and investment effects of regional transfers: A regression discontinuity design with heterogeneous treatment effects. American Economic Journal 5: 29–77. [Google Scholar] [CrossRef] [Green Version]

- Becker, Sascha O., Peter H. Egger, and Maximilian Von Ehrlich. 2015. Regional Policy (Chapter 17). In Handbook of the Economics of European Integration. Edited by H. Badinger and V. Nitsch. London: Routledge. [Google Scholar]

- Becker, Sascha O., Peter H. Egger, and Maximilian Von Ehrlich. 2018. Effects of EU Regional Policy: 1989–2013. Regional Science and Urban Economics 69: 143–52. [Google Scholar] [CrossRef]

- Beugelsdijk, Maaike, and Sylvester C. W. Eijffinger. 2005. The effectiveness of structural policy in the European Union: An empirical analysis for the EU–15 in 1995–2001. Journal of Common Market Studies 43: 37–51. [Google Scholar] [CrossRef] [Green Version]

- Bourdin, Sebastien. 2019. Does the Cohesion Policy Have the Same Influence on Growth Everywhere? A Geographically Weighted Regression Approach in Central and Eastern Europe. Economic Geography 95: 256–87. [Google Scholar] [CrossRef]

- Brambor, Thomas, William Roberts Clark, and Matt Golder. 2006. Understanding Interaction Models: Improving Empirical Analyses. Political Analysis 14: 63–82. [Google Scholar] [CrossRef] [Green Version]

- Butkus, Mindaugas, Alma Mačiulytė-Šniukienė, and Kristina Matuzevičiūtė. 2020a. The role of institutions in shaping geography of development disparities across European Union. Geografický Časopis 72: 25–47. [Google Scholar] [CrossRef]

- Butkus, Mindaugas, Diana Cibulskienė, Alma Mačiulytė-Šniukienė, and Kristina Matuzevičiutė. 2020b. Non-linear and Lagging Convergence Effects of the EU’s Regional Support at NUTS3 Level. Journal of Urban and Regional Analysis 12: 35–52. [Google Scholar] [CrossRef]

- Butkus, Mindaugas, Diana Cibulskienė, Alma Mačiulytė-Šniukienė, and Kristina Matuzevičiutė. 2020c. Mediating Effects of Cohesion Policy and Institutional Quality on Convergence between EU Regions: An Examination Based on a Conditional Β-convergence Model with a 3-Way Multiplicative Term. Sustainability 12: 3025. [Google Scholar] [CrossRef] [Green Version]

- Butkus, Mindaugas, Diana Cibulskienė, Alma Mačiulytė-Šniukienė, and Kristina Matuzevičiutė. 2020d. Does Financial Support from ERDF and CF Contribute to Convergence in the EU? Empirical Evidence at NUTS3 Level. Prague Economic Papers 29: 315–29. [Google Scholar] [CrossRef]

- Casula, Mattia. 2020. Under which conditions is Cohesion Policy effective: Proposing an Hirschmanian approach to EU structural funds. Regional and Federal Studies, 1–27. [Google Scholar] [CrossRef]

- Cerqua, Augusto, and Guido Pellegrini. 2018. Are we spending too much to grow? The case of Structural Funds. Journal of Regional Science 58: 535–63. [Google Scholar] [CrossRef]

- Charron, Nicholas. 2016. Explaining the allocation of regional Structural Funds: The conditional effect of governance and self-rule. European Union Politics 17: 1–22. [Google Scholar] [CrossRef]

- Charron, Nicholas, Victor Lapuente, and Bo Rothstein, eds. 2010. Measuring the Quality of Government and Subnational Variation. Report for the European Commission Directorate–General Regional Policy, Directorate Regional Policy. Gothenburg: Quality of Quality of Government and Returns of Investment: Cohesion Expenditure in European Regions 1289 Government Institute, Department of Political Science, University of Gothenburg, Available online: http://ec.europa.eu/regional_policy/sources/docgener/studies/pdf/2010_government_1.pdf (accessed on 27 June 2019).

- Charron, Nicholas, Lewis Dijkstra, and Victor Lapuente. 2014. Regional governance matters: Quality of government within European Union member states. Regional Studies 48: 68–90. [Google Scholar] [CrossRef]

- Ciffolilli, Andrea, Stefano Condello, Marco Pompili, and Roman Roemish. 2015. Geography of Expenditure. Final Report. Work Package 13. Ex post evaluation of Cohesion Policy Programmes 2007–2013, Focusing on the European Regional Development Fund (ERDF) and the Cohesion Fund (CF). Available online: https://ec.europa.eu/regional_policy/sources/docgener/evaluation/pdf/expost2013/wp13_final_report_en.pdf (accessed on 27 June 2019).

- Crescenzi, Riccardo, and Mara Giua. 2014. The EU Cohesion Policy in Context: Regional Growth and the Influence of Agricultural and Rural Development Policies. LSE’ Europe in Question. Discussion Paper Series Paper, 85. Available online: http://aei.pitt.edu/93663/ (accessed on 26 April 2020).

- Crescenzi, Riccardo, and Mara Giua. 2020. One or many Cohesion Policies of the European Union? On the differential economic impacts of Cohesion Policy across member states. Regional Studies 54: 10–20. [Google Scholar] [CrossRef] [Green Version]

- Dall’erba, Sandy, Rachel Guillain, and Julie Le Gallo. 2009. Impact of structural funds on regional growth: How to reconsider a 9-year-old black box. Région et Développement 30: 77–100. [Google Scholar]

- Del Bo, Chiara, Massimo Florio, Emanuela Sirtori, and Silvia Vignetti. 2011. Additionality and Regional Development: Are EU Structural Funds Complements or Substitutes of National Public Finance? CSIL Working Paper N. 01/2011. Milan: CSIL. [Google Scholar]

- Dellmuth, Lisa Maria, Dominik Schraff, and Michael F. Stoffel. 2017. Distributive Politics, Electoral Institutions and European Structural and Investment Funding: Evidence from Italy and France. Journal of Common Market Studies 55: 275–93. [Google Scholar] [CrossRef] [Green Version]

- Di Cataldo, Marco. 2017. The impact of EU Objective 1 funds on regional development: Evidence from the UK and the prospect of Brexit. Journal of Regional Science 57: 814–39. [Google Scholar] [CrossRef]

- Di Cataldo, Marco, and Vassilis Monastiriotis. 2018. An Assessment of EU Cohesion Policy in the UK Regions: Direct Effects and the Dividend of Targeting. LEQS Paper 135. Available online: https://ssrn.com/abstract=3198691 (accessed on 17 June 2019).

- Di Cataldo, Marco, and Vassilis Monastiriotis. 2020. Regional needs, regional targeting and regional growth: An assessment of EU Cohesion Policy in UK regions. Regional Studies 54: 35–47. [Google Scholar] [CrossRef] [Green Version]

- Eberle, Jonathan, and Thomas Brenner. 2016. More Bucks, More Growth, More Justice? The Effects of Regional Structural Funds on Regional Economic Growth and Convergence in Germany. Working Papers on Innovation and Space, 01.16. Marburg: Philipps University Marburg, Department of Geography, Available online: http://hdl.handle.net/10419/147971 (accessed on 17 June 2019).

- Ederveen, Sjef, Henri L.F. De Groot, and Richard Nahuis. 2006. Fertile soil for structural funds? A panel data analysis of the conditional effectiveness of European cohesion policy. Kyklos 59: 17–42. [Google Scholar] [CrossRef]

- Esposti, Roberto, and Stefania Bussoletti. 2008. Impact of objective 1 funds on regional growth convergence in the European Union: A panel–data approach. Regional Studies 42: 159–73. [Google Scholar] [CrossRef]

- European Commission. 2016. Measuring the impact of Structural and Cohesion Funds Using Regression Discontinuity Design in EU27 in the period 1994–2011, Ex Post Evaluation of Cohesion Policy Programmes 2007–2013, focusing on the European Regional Development Fund (ERDF) and the Cohesion Fund (CF). Final Technical Report, Work Package 14c—Tasks 2 and 3. Available online: https://ec.europa.eu/regional_policy/sources/docgener/evaluation/pdf/expost2013/wp14c_task1_final_report_en.pdf (accessed on 1 June 2019).

- European Commission. 2019. European Structural and Investment Funds. Available online: https://cohesiondata.ec.europa.eu/overview (accessed on 26 April 2020).

- Florio, Massimo, and Luigi Moretti. 2014. The Effect of Business Support on Employment in Manufacturing: Evidence from the European Union Structural Funds in Germany, Italy and Spain. European Planning Studies 22: 1802–23. [Google Scholar] [CrossRef]

- Fratesi, Ugo, and Giovanni Perucca. 2014. Territorial Capital and the Effectiveness of Cohesion Policies: An Assessment for CEE Regions, GRINCOH. Working Paper Series, 8.05. Available online: http://www.grincoh.eu/media/serie_8__cohesion_and_its_dimensions/grincoh_wp8.05_fratesi_perucca.pdf (accessed on 1 June 2019).

- Gagliardi, Luisa, and Marco Percoco. 2017. The impact of European Cohesion Policy in urban and rural regions. Regional Studies 51: 857–68. [Google Scholar] [CrossRef]

- Ganau, Roberto, and Andrés Rodríguez-Pose. 2019. Do high-quality local institutions shape labour productivity in Western European manufacturing firms? Papers in Regional Science 98: 1633–66. [Google Scholar] [CrossRef]

- Gorzelak, Grzegorz. 2016. Cohesion Policy and regional development. In 33EU Cohesion Policy—Reassessing Performance and Direction. Edited by J. Bachtler, P. Berkowitz, S. Hardy and T. Muravska. London: Routledge. [Google Scholar] [CrossRef]

- Host, Alen, Vinko Zaninović, and Krešimir Parat. 2017. Cohesion Policy Instruments and Economic Growth: Do Institutions Matter? Ekonomiska Misao I Praksa 2: 541–59. [Google Scholar]

- Kyriacou, Andreas P., and Oriol Roca-Sagalés. 2012. The Impact of EU Structural Funds on Regional Disparities within Member States. Environment and Planning C: Politics and Space 30: 267–81. [Google Scholar] [CrossRef] [Green Version]

- Leona, S. Aiken, and Stephen G. West. 1991. Multiple Regression: Testing and Interpreting Interactions. London: Sage. [Google Scholar]

- Lippman, S. S., and John J. McCall. 2015. Three Principal–Agent Models with Asymmetric Information. In International Encyclopedia of the Social & Behavioral Sciences, 2nd ed. Edited by J. D. Wright. Oxford: Elsevier Ltd. [Google Scholar]

- Marzinotto, Benedicta. 2012. The Growth Effects of EU Cohesion Policy: A Meta–Analysis. Bruegel Working Paper No. 2012/14. Available online: https://www.econstor.eu/bitstream/10419/78011/1/728570688.pdf (accessed on 10 June 2020).

- Maynou, Laia, Marc Saez, Andreas Kyriacou, and Jordi Bacaria. 2016. The Impact of Structural and Cohesion Funds on Eurozone Convergence, 1990–2010. Regional Studies 50: 1127–39. [Google Scholar] [CrossRef]

- Olson, Mancur. 1965. The Logic of Collective Action: Public Goods and the Theory of Groups. Cambridge and London: Harvard University Press. [Google Scholar]

- Pellegrini, Guido, and Augusto Cerqua. 2016. Measuring the impact of intensity of treatment using RDD and covariates: The case of Structural Funds. Paper presented at 57th RSA Annual Conference, Milano, Italy, October 20–22. [Google Scholar]

- Pellegrini, Guido, Federica Busillo, Teo Muccigrosso, Ornella Tarola, and Flavia Terribile. 2013. Measuring the Impact of the European Regional Policy on Economic Growth: A Regression Discontinuity Design Approach. Papers in Regional Science 92: 217–33. [Google Scholar] [CrossRef]

- Piętak, Łukasz. 2018. Did Structural Funds Affect Economic Growth and Convergence across Regions? Spanish Case in the Years 1989–2016. INE PAN Working Paper Series, No. 44. Available online: http://inepan.pl/wp–content/uploads/2016/07/working–papers–44–Hiszpania–Pietak.pdf (accessed on 10 June 2020).

- Pinho, Carlos, Celeste Varum, and Micaela Antunes. 2015a. Structural Funds and European Regional Growth: Comparison of Effects among Different Programming Periods. European Planning Studies 23: 1302–26. [Google Scholar] [CrossRef] [Green Version]

- Pinho, Carlos, Celeste Varum, and Micaela Antunes. 2015b. Under What Conditions Do Structural Funds Play a Significant Role in European Regional Economic Growth? Some Evidence from Recent Panel Data. Journal of Economic Issues 49: 749–71. [Google Scholar] [CrossRef] [Green Version]

- Pontarollo, Nicola. 2017. Does Cohesion Policy affect regional growth? New evidence from a semi-parametric approach. In EU Cohesion Policy. Edited by J. Bachtler, P. Berkowitz, S. Hardy and T. Muravska. London and New York: Routledge, pp. 93–108. [Google Scholar]

- Rodríguez-Pose, Andrés, and Ugo Fratesi. 2004. Between Development and Social Policies: The Impact of European Structural Funds in Objective 1 Regions. Regional Studies 38: 97–113. [Google Scholar] [CrossRef]

- Rodríguez-Pose, Andrés, and Katja Novak. 2013. Learning processes and economic returns in European Cohesion Policy. Investigaciones Regionales 25: 7–26. [Google Scholar]

- Rodríguez-Pose, Andrés, and Enrique Garcilazo. 2015. Quality of Government and the Returns of Investment: Examining the Impact of Cohesion Expenditure in European Regions. Regional Studies 49: 1274–90. [Google Scholar] [CrossRef]

- Rodríguez-Pose, Andrés, and Tobias Ketterer. 2019. Institutional change and the development of lagging regions in Europe. Regional Studies 54: 974–86. [Google Scholar] [CrossRef] [Green Version]

- SWECO. 2008. Final Report—ERDF and CF Regional Expenditure Contract No. 2007.CE.16.0.AT.036. Available online: https://ec.europa.eu/regional_policy/sources/docgener/evaluation/pdf/expost2006/expenditure_final.pdf (accessed on 17 July 2020).

- Szitásiová, Valeria, Monika Martišková, and Miroslav Šipikal. 2014. Substitution Effect of Public Support Programs at Local Level. Transylvanian Review of Administrative Sciences 10: 167–82. [Google Scholar]

- Wostner, Peter, and Sonja Šlander. 2009. The Effectiveness of EU Cohesion Policy Revisited: Are eu Funds Really Additional? European Policy Research Paper 69: 1–26. Available online: https://strathprints.strath.ac.uk/70313/1/EPRP_69.pdf (accessed on 17 July 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Source and Transformations | |

|---|---|---|

| Growth, i.e., and the initial development level, i.e., | Per capita GDP | Data were collected from the Eurostat GDP indicators (reg_eco10gdp) subsection for the GDP at current market prices by NUTS3 regions (nama_10r_3gdp). To correct the changes of price levels over time, we applied the price index (implicit deflator PD10_EUR). To calculate per capita GDP, we used the average annual population to calculate regional GDP data by NUTS3 regions (nama_10r_3popgdp). |

| GVA per employee | Data were collected from the Eurostat branch and household accounts (reg_eco10brch) subsection for GVA at basic prices by NUTS3 regions (nama_10r_3gva). To correct the changes of price levels over time, we applied the price index (implicit deflator PD10_EUR). To calculate GVA per worker, we used employment by NUTS3 regions (nama_10r_3empers). | |

| Cohesion policy (CP), i.e., CP commitments to GDP ratio | For the 2000–2006 programming period, we used the SWECO (2008) database, which contains the Cohesion Fund, ERDF Objective 1, ERDF Objective 2, URBAN and INTERREG IIIA commitments data at NUTS2 & 3 disaggregation levels. For the 2007–2013 programming period, we used Ciffolilli et al.’s (2015) database, which contains the ERDF and CF programmes’ commitments data at NUTS2 & 3 levels. | |

| Institutional quality (IQ), i.e., European Quality of Government Index (EQI) | The Quality of Government Institute provides EQI data for 2010 (Charron et al. 2010) and 2013, i.e., for two years over the whole period covered by the analysis. Following Rodríguez-Pose and Garcilazo (2015) and Charron et al. (2014), we interpolated values for the remaining years. To do that, we combined the EQI data at NUTS2 disaggregation with the World Bank’s World Governance Indicators at the national level available for the EU Member States. As previous contributions, for the interpolation, we used the following assumptions: (i) the variation of institutional quality over time at NUTS2 disaggregation within the country is relatively stable, and (ii) variation over time at the national level is captured by the World Bank’s World Governance Indicators. Charron et al. (2014) provide details on how this indicator is calculated. We use EQI estimates at NUTS2 disaggregation as a proxy for institution quality across all NUTS3 regions within NUTS2 regions. Since the strategy to use estimates at a NUTS2 level for NUTS3 regions creates clusters, we controlled them by estimating cluster robust standard errors. | |

| Average annual population (POP), thousand persons. | Data were collected from Eurostat. The average annual population to calculate regional GDP data by NUTS3 regions was found (nama_10r_3popgdp). | |

| Investment to GDP ratio (IGDP), %. | Data were collected from Eurostat and calculated as the ratio between gross fixed capital formation by NUTS2 regions (nama_10r_2gfcf) and gross domestic product at current market prices by NUTS2 regions (nama_10r_2gdp). | |

| Investment per worker (IWRK), Euro. | Data were collected from Eurostat, and the IWRK was calculated as the ratio between gross fixed capital formation by NUTS2 regions (nama_10r_2gfcf) and employment by NUTS3 regions (nama_10r_3empers). | |

| Primary educations (PEDUC), %. | Data were collected from Eurostat. Data were retrieved from the population aged 25–64, and according to educational attainment level, sex, and NUTS2 regions (edat_lfse_04). Primary education was calculated as the proportion of the 25–64 year-old population with less than primary, or primary and lower secondary education (levels 0–2). Tertiary education was calculated as the proportion of the 25–64 year-old population with tertiary education (levels 5–8). | |

| Tertiary education (TEDUC), %. | ||

| Employment in High–technology sectors (HTEC), percentage of total employment. | Data were collected from Eurostat. Data were retrieved from employment in technology and knowledge-intensive sectors according to NUTS2 regions and sex (1994–2008, NACE Rev. 1.1) (htec_emp_reg) and from employment in technology and knowledge-intensive sectors according to NUTS2 regions and sex (from 2008 onwards, NACE Rev. 2) (htec_emp_reg2). | |

| Innovation (INOV), the number of patents per million inhabitants. | Data were collected from Eurostat. Data were retrieved from patent applications to the EPO by priority year according to NUTS3 regions (pat_ep_rtot). | |

| Motorways (MINFR), kilometres of motorways per thousand square kilometres. | Data were collected from Eurostat. Data were retrieved from the road, rail and navigable inland waterways networks according to NUTS2 regions (tran_r_net). | |

| Railway lines (RINFR), kilometres of total railway lines per thousand square kilometres. | ||

| Population density (PDENS), the number of inhabitants per square kilometre. | Data were collected from Eurostat. Data were retrieved from population density according to the NUTS3 region (demo_r_d3dens). | |

| Employment density (EDENS), employed per square kilometre. | Data were collected from Eurostat and calculated as the ratio between total employment by NUTS3 regions (nama_10r_3empers) and area by NUTS3 region (reg_area3). | |

| Population structure (PSTR), %. | Data were collected from Eurostat. Data were retrieved from the population on 1 January according to the broad age group, sex and NUTS3 region (demo_r_pjanaggr3), and calculated as the proportion of 15–64 year-old to a total number of inhabitants in the region. | |

| Employment in the agriculture sector (AEMPL), %. | Data were collected from Eurostat. Data were retrieved from employment by NUTS3 regions (nama_10r_3empers). Employment in the agriculture sector was calculated as the proportion of workers employed in the agriculture, forestry and fishing industries (A in NACE activities). Employment in the services sector was calculated as the proportion of workers employed in the services sector (G–U in NACE activities). | |

| Employment in the services sector (SEMPL), %. | ||

| Agriculture gross value added (AGVA), %. | Data were collected from Eurostat. Data were retrieved from the gross value added at basic prices by NUTS3 regions (nama_10r_3gva). Agriculture gross value added was calculated as the proportion of GVA created in the agriculture, forestry and fishing industries (A in NACE activities). Services gross value added was calculated as the proportion of GVA created in the services sector (G–U in NACE activities). | |

| Services gross value added (SGVA), %. | ||

| Spatial interdependence (SI), %. | Data were collected from Eurostat and calculated as the ratio between regional and national per capita GDP. | |

| Variable | Parameter | 2000–2006 Programming Period | 2007–2013 Programming Period | ||||||

|---|---|---|---|---|---|---|---|---|---|

| NUTS3 Disaggregation Level | NUTS2 Disaggregation Level | NUTS3 Disaggregation Level | NUTS2 Disaggregation Level | ||||||

| Outcome Variable—per Capita GDP growth | Outcome Variable—GVA per Worker growth | Outcome variable—per Capita GDP growth | Outcome Variable—GVA per Worker growth | Outcome Variable—per Capita GDP growth | Outcome Variable—GVA per Worker growth | Outcome Variable—per Capita GDP growth | Outcome Variable—GVA per Worker growth | ||

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | ||

| Intercept | 0.0113 *** | 0.0197 *** | 0.0115 *** | 0.0152 *** | −0.0136 *** | −0.0154 *** | −0.0051 *** | −0.0060 *** | |

| (0.0014) | (0.0014) | (0.0032) | (0.0037) | (0.0013) | (0.0016) | (0.0037) | (0.0041) | ||

| −0.0100 *** | −0.0173 *** | −0.0101 *** | −0.0131 *** | −0.0143 *** | −0.0060 *** | −0.0145 *** | −0.0050 *** | ||

| (0.0011) | (0.0013) | (0.0032) | (0.0034) | (0.0014) | (0.0003) | (0.0015) | (0.0004) | ||

| 0.0100 ** | 0.0051 ** | 0.0257 ** | 0.0216 ** | 0.0105 *** | 0.0084 *** | 0.0168 ** | 0.0159 *** | ||

| (0.0048) | (0.0022) | (0.0119) | (0.0108) | (0.0026) | (0.0027) | (0.0076) | (0.0043) | ||

| −0.0111 ** | −0.0039 ** | −0.0237 *** | −0.0149 *** | −0.0062 *** | −0.0041 *** | −0.0105 ** | −0.0076 ** | ||

| (0.0057) | (0.0016) | (0.0079) | (0.0056) | (0.0007) | (0.0007) | (0.0046) | (0.0037) | ||

| 0.0504 ** | 0.0466 ** | 0.0427 *** | 0.0452 *** | 0.0663 *** | 0.0642 *** | 0.0498 ** | 0.0540 ** | ||

| (0.0205) | (0.0227) | (0.0121) | (0.0141) | (0.0135) | (0.0184) | (0.0186) | (0.0197) | ||

| −0.0014 ** | −0.0013 ** | −0.0028 ** | −0.0029 ** | −0.0019 ** | −0.0018 ** | −0.0017 ** | −0.0014 ** | ||

| (0.0006) | (0.0005) | (0.0014) | (0.0015) | (0.0008) | (0.0007) | (0.0008) | (0.0007) | ||

| 0.0110 ** | 0.0123 *** | 0.0101 *** | 0.0129 *** | 0.0084 *** | 0.0148 ** | 0.0095 ** | 0.0143 * | ||

| (0.0045) | (0.0037) | (0.0032) | (0.0012) | (0.0022) | (0.0063) | (0.0042) | (0.0076) | ||

| −0.0068 *** | −0.0064 *** | −0.0051 *** | −0.0054 *** | −0.0072 ** | −0.0066 ** | −0.0056 ** | −0.0054 *** | ||

| (0.0014) | (0.0017) | (0.0018) | (0.0015) | (0.0030) | (0.0023) | (0.0025) | (0.0012) | ||

| −0.0130 *** | −0.0146 ** | −0.0110 *** | −0.0155 ** | −0.0112 *** | −0.0128 ** | −0.0166 ** | −0.0123 ** | ||

| (0.0040) | (0.0042) | (0.0034) | (0.0059) | (0.0037) | (0.0052) | (0.0081) | (0.0068) | ||

| 0.0006 ** | 0.0005 ** | 0.0012 ** | 0.0015 *** | 0.0005 ** | 0.0004 ** | 0.0004 ** | 0.0003 ** | ||

| (0.0003) | (0.0002) | (0.0006) | (0.0005) | (0.0002) | (0.0002) | (0.0002) | (0.0001) | ||

| 0.0046 *** | 0.0020 ** | 0.0172 ** | 0.0065 *** | 0.0042 *** | 0.0018 ** | 0.0049 *** | 0.0021 ** | ||

| (0.0014) | (0.0009) | (0.0086) | (0.0017) | (0.0013) | (0.0009) | (0.0013) | (0.0012) | ||

| −0.0003 ** | −0.0002 ** | −0.0002 ** | −0.0002 *** | −0.0004 ** | −0.0002 ** | −0.0001 * | −0.0002 * | ||

| (0.0002) | (0.0001) | (0.0001) | (0.0000) | (0.0002) | (0.0001) | (0.0001) | (0.0001) | ||

| −0.0148 | −0.0067 | −0.0161 | −0.0049 | ||||||

| (0.0188) | (0.0082) | (0.0110) | (0.0039) | ||||||

| 0.0012 *** | 0.0015 *** | ||||||||

| (0.0004) | (0.0004) | ||||||||

| 0.1823 *** | 0.2027 *** | ||||||||

| (0.0162) | (0.0140) | ||||||||

| −0.0009 ** | −0.0006 ** | −0.0007 * | −0.0007 ** | ||||||

| (0.0004) | (0.0003) | (0.0004) | (0.0003) | ||||||

| 0.0013 | 0.0019 | 0.0017 * | 0.0014 ** | ||||||

| (0.0054) | (0.0046) | (0.0011) | (0.0006) | ||||||

| 0.0028 * | 0.0027 ** | ||||||||

| (0.0019) | (0.0013) | ||||||||

| 0.2219 | 0.1795 | 0.3900 | 0.3681 | ||||||

| (0.6491) | (0.6265) | (0.6155) | (0.8060) | ||||||

| 0.0030 ** | 0.0029 ** | 0.0031 ** | 0.0028 ** | ||||||

| (0.0011) | (0.0010) | (0.0012) | (0.0014) | ||||||

| 0.0103 ** | 0.0121 ** | 0.0118 *** | 0.0137 *** | ||||||

| (0.0048) | (0.0059) | (0.0035) | (0.0042) | ||||||

| 0.0578 | 0.0273 | 0.0789 * | 0.0777 * | ||||||

| (0.0513) | (0.0874) | (0.0399) | (0.0450) | ||||||

| 0.0484 | 0.0314 | 0.0691 | 0.0622 * | ||||||

| (0.0450) | (0.0683) | (0.0395) | (0.0396) | ||||||

| 0.0006 | 0.0015 | 0.0009 | 0.0007 | ||||||

| (0.0008) | (0.0018) | (0.0007) | (0.0008) | ||||||

| −0.0014 *** | −0.0014 *** | −0.0012 *** | −0.0018 *** | ||||||

| (0.0002) | (0.0002) | (0.0002) | (0.0002) | ||||||

| 0.0013 *** | 0.0015 *** | 0.0015 *** | 0.0016 *** | ||||||

| (0.0001) | (0.0001) | (0.0001) | (0.0001) | ||||||

| −0.0018 *** | −0.0012 *** | −0.0015 *** | −0.0016 *** | ||||||

| (0.0002) | (0.0002) | (0.0002) | (0.0002) | ||||||

| 0.0014 *** | 0.0014 *** | 0.0012 *** | 0.0013 | ||||||

| (0.0001) | (0.0002) | (0.0001) | (0.0001) | ||||||

| SI | 0.0735 * | 0.0834 * | 0.0839 * | 0.0761 * | 0.0522 * | 0.0434 * | 0.0661 * | 0.0747 * | |

| (0.0416) | (0.0421) | (0.0446) | (0.0463) | (0.0413) | (0.0338) | (0.0519) | (0.0509) | ||

| Number of regions | 1248 | 1247 | 257 | 256 | 1326 | 1326 | 270 | 270 | |

| Observations | 5429 | 5125 | 1208 | 1160 | 6458 | 6153 | 1350 | 1326 | |

| Avg. obs. per region | 4.35 | 4.11 | 4.70 | 4.53 | 4.87 | 4.64 | 5.00 | 4.91 | |

| Within R-squared | 0.6785 | 0.5984 | 0.6114 | 0.5613 | 0.6131 | 0.5663 | 0.6226 | 0.5135 | |

| Pesaran’s CD test (1) | [0.2413] | [0.2591] | [0.2970] | [0.2451] | [0.2194] | [0.2239] | [0.1660] | [0.2176] | |

| Woodridge test (2) | [0.1560] | [0.1376] | [0.1406] | [0.1291] | [0.1410] | [0.1302] | [0.1432] | [0.1181] | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Butkus, M.; Maciulyte-Sniukiene, A.; Macaitiene, R.; Matuzeviciute, K. A New Approach to Examine Non-Linear and Mediated Growth and Convergence Outcomes of Cohesion Policy. Economies 2021, 9, 103. https://0-doi-org.brum.beds.ac.uk/10.3390/economies9030103

Butkus M, Maciulyte-Sniukiene A, Macaitiene R, Matuzeviciute K. A New Approach to Examine Non-Linear and Mediated Growth and Convergence Outcomes of Cohesion Policy. Economies. 2021; 9(3):103. https://0-doi-org.brum.beds.ac.uk/10.3390/economies9030103

Chicago/Turabian StyleButkus, Mindaugas, Alma Maciulyte-Sniukiene, Renata Macaitiene, and Kristina Matuzeviciute. 2021. "A New Approach to Examine Non-Linear and Mediated Growth and Convergence Outcomes of Cohesion Policy" Economies 9, no. 3: 103. https://0-doi-org.brum.beds.ac.uk/10.3390/economies9030103