Consumer Stock Ownership Plans (CSOPs)—The Prototype Business Model for Renewable Energy Communities

Comparative Law, East European Business Law and European Legal Policy at the Faculty of Business Administration and Economics, Europa Universität Viadrina, Große Scharrnstraße 59, D-15230 Frankfurt, Germany

Energies 2020, 13(1), 118; https://0-doi-org.brum.beds.ac.uk/10.3390/en13010118

Submission received: 31 October 2019

/

Revised: 10 December 2019

/

Accepted: 13 December 2019

/

Published: 25 December 2019

(This article belongs to the Special Issue New Pathways for Community Energy and Storage)

Abstract

:The 2018 recast of the Renewable Energy Directive (RED II) defines “renewable energy communities” (RECs), introducing a new governance model and the possibility of energy sharing for them. It has to be transposed into national law by all European Union Member States until June 2021. This article introduces consumer stock ownership plans (CSOPs) as the prototype business model for RECs. Based on the analysis of a dataset of 67 best-practice cases of consumer (co-) ownership from 18 countries it demonstrates the importance of flexibility of business models to include heterogeneous co-investors for meeting the requirements of the RED II and that of RE clusters. It is shown that CSOPs—designed to facilitate scalable investments in utilities—facilitate co-investments by municipalities, SMEs, plant engineers or energy suppliers. A low-threshold financing method, they enable individuals, in particular low-income households, to invest in renewable projects. Employing one bank loan instead of many micro loans, CSOPs reduce transaction costs and enable consumers to acquire productive capital, providing them with an additional source of income. Stressing the importance of a holistic approach including the governance and the technical side for the acceptance of RECs on the energy markets recommendations for the transposition are formulated.

1. Introduction

A consumer stock ownership plan (CSOP) is a financing technique that employs an intermediary corporate vehicle and facilitates the involvement of individual investors through a trusteeship. It is a type of investment transaction that may use external financing, thereby achieving the benefit of financial leverage. The CSOP was applied for the first time in 1958 with spectacular success in the U.S. by its innovator, Louis O. Kelso, a business and financial lawyer turning 4,580 farmers into (co-)owners of the new fertilizer manufacturer Valley Nitrogen Producers, Inc. This involved an investment of USD 120 million which today inflation adjusted would equal around EUR 915 million. It is related to Kelso’s best-known financial innovation, the employee stock ownership plan (ESOP), that enabled millions of American workers to become (co-)owners of their employer companies. Both plans repay the acquisition loan not from wages or savings but from the future earnings of the shares acquired. Today the ESOP is an integral part of American corporate finance with around 6,660 ESOPs and a little under 3,000 ESOP-like plans in the USA, about 14.2 million participating employees holding around USD 1.4 trillion in assets as of 2016 [1]. Applied to the energy context as CSOP can buy into an existing or invest in a new renewable energy (RE) plant. Designed to facilitate scalable investments in utilities, it is open to co-investments by municipalities, plant engineers, energy suppliers or other strategic partners. Moreover, as a low-threshold financing method, it enables individuals to invest in RE projects [2]. The renewable energy consumer stock ownership plan (RE-CSOP) as an alternative financing source for sustainable investments is of particular importance for municipalities that are charged with fulfilling energy efficiency (EE) and climate policy goals but have limited budgets and often lack the funding to make these investments. An objective of this contractual model is, above all, to facilitate single-source financing (i.e., employing one bank loan instead of many micro loans), thus reducing transaction costs. At the same time, individual liability of consumers is avoided, while participating consumers are able to acquire capital ownership, providing them with an additional source of income. Other important issues are easy tradability of shares, deferred taxation for consumer-shareholders and pooling of voting rights.

Especially, low-income households who usually do not dispose of savings necessary for conventional investment schemes are enabled to repay their share of the acquisition loan from the future earnings of the investment: A fiduciary entity that is set up by the local community and managed by an independent director is authorized to take on a bank loan to acquire shares in the RE plant on behalf of the consumers. The shares are allocated among the consumer-beneficiaries in proportion to their respective energy purchases. Monies saved by self-consumption and increased EE as well as revenues from the sale of the excess energy production are used to repay the acquisition loan. After amortisation of this debt, profits are distributed to the consumer-beneficiaries.

In 2018 the European Union has introduced a legal framework for renewable energy communities (RECs) that will have to prove its success in the years to come. A crucial element for the acceptance of RECs by the energy markets will be the underlying business model. This article introduces RE-CSOPs as the prototype business model for RECs. In the limited time since the entering into force of the new rules only very few articles, for the most part policy papers of the different interest groups, have been published. Therefore, the focus lies on the conceptual side of this business model omitting a review of the literature.

1.1. Prosumership in the 2018/19 EU Clean Energy Package

Consumer (co-)ownership in RE is one essential cornerstone of the overall success of energy transition. Marshall McLuhan and Barrington Nevitt as early as 1972 suggested in their book Take Today [3] that technological progress would transform the consumer into a producer of electricity. When consumers acquire ownership in RE, they can become prosumers (Alvin Toffler probably first introduced the artificial word stemming from the Latin in his book The Third Wave [4]), generating a part of the energy they consume, thus reducing their overall expenditure for energy, while at the same time having a second source of income from the sale of excess production. The European Union agreed on a corresponding legal framework as part of a recast of the Renewable Energy Directive (RED II) [5], which entered into force in December 2018:

- Consumers, as prosumers, will have the right to consume, store or sell RE generated on their premises, (1) individually (Art. 21 RED II), that is, households and non-energy small and medium sized enterprises (SMEs); and collectively, for example, in tenant electricity projects, or (2) as part of RECs (Art. 22 RED II) organised as independent legal entities.

- Transposing the RED II into national law, Member States—amongst others—have until June 2021 to adopt an “enabling framework” for prosumership and, in particular, for RECs. The Directive defines citizen’s rights and duties and links prosumership to such different topics as increasing acceptance, fostering local development, fighting energy poverty, and incentivising demand-flexibility.

The RED II is part of the “Clean Energy for all Europeans Package” of the European Union, a package of measures that the European Commission presented on 30 November 2016 to keep the EU competitive as the energy transition changes global energy markets; this legislative initiative has four main goals, that is, energy efficiency, global leadership in RE, a fair deal for consumers and a redesign of the internal electricity market. The RED II rules are embedded in those of the 2019 Internal Electricity Market Directive (IEMD) [6] and Regulation (IEMR) [7]. The transposition of these comprehensive rules—in particular those on energy communities—requires developing, implementing and rolling out business models that broaden the capital participation of consumers in all Member States [8].

RED II introduced RECs as a new Europe-wide governance model for RE projects and defined them in Art. 2 as a legal entity:

- “which, according to applicable national law, is based on open and voluntary participation, is autonomous, and is effectively controlled by shareholders or members that are located in the proximity of the renewable energy projects owned and developed by that community;

- whose shareholders or members are natural persons, local authorities, including municipalities, or SMEs;

- whose primary purpose is to provide environmental, economic or social community benefits for its members/the local areas where it operates rather than financial profits.”

Complying with the prerequisites for RECs, a corresponding business model needs to have the capability of involving heterogeneous co-investors, that is, local citizens, municipalities, SMEs but possibly also commercial investors in RE projects. Other than bringing together the interests of local citizens and their municipalities, this is an important prerequisite for preferential conditions under the “enabling framework” for RECs, as defined in Art. 22 RED II. This approach facilitates the involvement of municipalities who need to respect the typical prerequisites of municipal law for participation in RE projects, i.e., public purpose, capacities for the investment, subsidiarity, appropriate representation as pacemakers of the energy transition. (Optional) minority stakes for commercial investors is itself nothing new, as citizens’ energy models in the wind sector often include professional partners as members of limited partnerships [9]. Depending on the type of project and the underlying technology, it may be useful to include them as operation and maintenance of infrastructure in RE projects can be very complex; this concerns, for example, not only wind energy and bioenergy, but also energy cluster projects aiming at sector coupling that may involve electricity sharing, storage, e-mobility, cogeneration, and the like [10,11].

1.2. Research Questions and Approach

Conventional business models for consumer ownership may not always allow for the combination of different types of co-investors. With regard to cooperatives [12], for example, the one-member one-vote principle is often an obstacle to partnering with SMEs and commercial investors, since these parties will prefer voting rights proportional to their shareholding. Furthermore, municipal co-investments are hindered by the necessity of representation on management and supervisory bodies, as cooperative law does not acknowledge a right of delegation similar to legislation applicable to joint stock companies. Cooperative projects often set up special purpose vehicles (usually a privately held corporation with limited liability) to avoid this problem [13]. The RE-CSOP involves such a standard special purpose vehicle, but with a defined governance structure allowing for the direct involvement of municipalities and strategic partners while safeguarding the interests of the local partners. Unlike cooperatives, where all management and board positions are reserved for members and representation by third parties is not permitted [14], a CSOP may hire external management. Thus, it avoids obstacles related to the principle of self-governance and ensures the representation of municipalities on the board. At the same time members of an energy cooperative can participate in a RE-CSOP, together with strategic partners, when expanding an existing RE plant together with strategic partners.

With regard to the RED II requirements for RECs and the necessary contractual arrangements, this article seeks to answer the following questions:

- To what extent does the governance model for energy communities stipulated by the Clean Energy Package actually meet the needs of practice?

- Can the RE-CSOP and similar business models provide attractive conditions respecting both the RED II prerequisites for RECs as well as the individual needs of different types of co-investors?

As the novelty legislation is not broadly known yet, Section 2 on theory first lays out the new legal framework for energy communities with a focus on the governance model for RECs and their importance for RE clusters. Reflecting on available empirical evidence, Section 3 draws on the experience of already existing best practice energy communities in the field of RE, assessing how many involve heterogeneous partners, and in those that do, their relationship to each other with regard to ownership structure and governance. To identify these patterns, the analysis [15] of a dataset of 67 best practice cases from 18 countries covering Europe, North and South America and Asia [16] is referred to asking: (a) Whether they are open to different actors (i.e., the heterogeneity of members or shareholders); and (b) if so, what their governance and ownership structure was. In the light of these empirical findings, Section 4 presents the RE-CSOP putting forward a proposal for future practice using a modular approach: (a) Three levels for co-investments are identified; and (b) the RE-CSOP is adapted to each of these levels describing how it reflects the needs of the different co-investors. Section 5 then discuss specific aspects of this business model, namely, how to convey individual consumers’ shareholding, the financing of the investment, and its taxation. Section 6 concludes and formulates policy recommendations with a view to the pending transposition of the RED II. The glossary provides definitions.

2. Theory

Energy communities are mentioned and defined in both the RED II and the IEMD. While the recast of the renewables directive focuses on the promotion of RE and thus speaks of “renewable energy communities” (RECs), the directive on the internal electricity market of the European Union as the more general legal act addresses “citizen energy communities” (CECs) [17]. This raises the question of the relationship between these two types of energy communities and, more generally, the relationship between these two legal acts. Furthermore, the Clean Energy Package introduces a new Europe-wide governance model for RECs and CECs to foster environmental, economic or social community benefits. These benefits are of particular importance for the development of the energy systems of tomorrow, that is, RE clusters that further support the deployment of renewable energy sources (RES) and provide stability of the grid and energy supply in energy markets increasingly characterised by volatility of production [15]. Flexibility [18], bi-directionality, interconnectivity [19] and complementarity [20] are prerequisites to these RE clusters that; however, require an active involvement of all actors involved, including consumers.

2.1. Relation of Electricity Market Directive/Regulation and Renewable Energy Directive

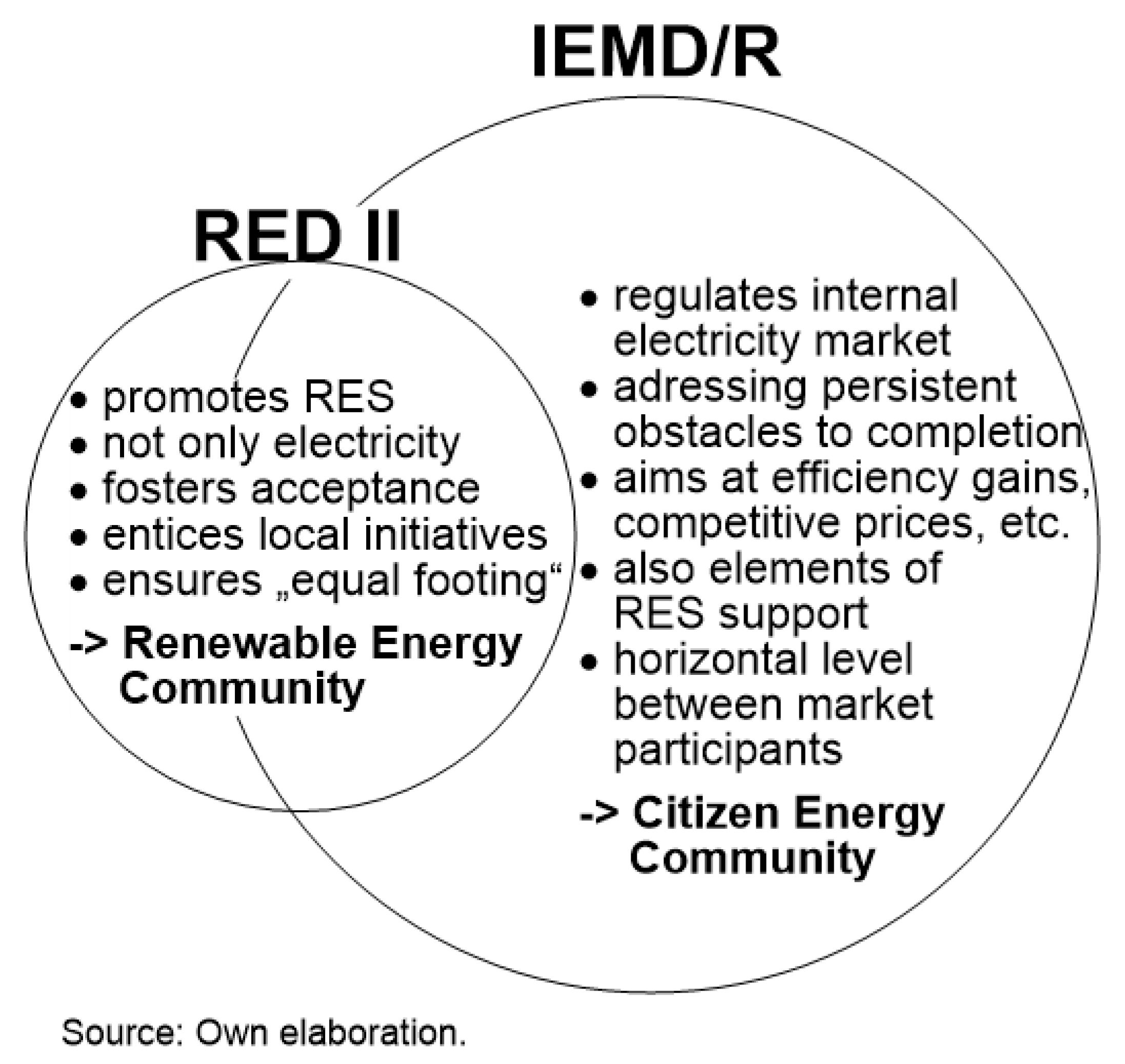

While the purpose of IEMD/R is the completion of the internal market in electricity that has progressively been implemented since 1999, that of RED II on the other hand is to specifically support the deployment of RES for energy production, including electricity, and to foster acceptance for renewables among the Europeans. Both directives expressly see the consumer “at the heart of the energy markets”, defining him or her—individually or jointly—respectively as “active consumer” (IEMD) and “renewable self-consumer” (RED II). With regard to energy communities, the IEMD mainly concerns the horizontal level, that is, their rights and obligations towards public authorities, other electricity enterprises and consumers. This design is also reflected in recital 2 IEMR on the aim of the internal market in electricity “to deliver a real choice for all consumers in the Union, both citizens and businesses, new business opportunities and more cross-border trade, so as to achieve efficiency gains, competitive prices and higher standards of service, and to contribute to security of supply and sustainability”. Amongst other issues the IEMD provides energy communities with a level playing field vis-a-vis other market participants (see Art. 65 IEMD). RED II, on the other hand, additionally ensures that RECs can compete for support “on an equal footing with other market participants” and calls on the Member States to “take into account specificities of renewable energy communities when designing support schemes” (Art. 22 para 7 RED II).

While the framework under IEMD is primarily a “regulatory framework” (see Art. 16 para. 1, sentence 1), that of RED II has the explicit aim “to promote and facilitate the development of RECs” (see Art. 22 para. 4, sentence 1), including preferential conditions or incentives. However, the above distinction is not always sharp since the IEMR/D also contain elements that support the deployment of RES. Recital 3a IEMR stipulates as an explicit aim “to ensure the functioning of the internal energy market while integrating requirements related to the development of renewable forms of energy and environmental policy, in particular specific rules for certain renewable power generating facilities, concerning balancing responsibility, dispatch and redispatch as well as a threshold for CO2 emissions of new generation capacity where it is subject to a capacity mechanism”. As enshrined in Art. 11, for example, the IEMR defines the principle of priority dispatch for RE plants with an installed electricity capacity of less than 400 kW (for RE plants commissioned after 1 January 2026 less than 200 kW) and for “demonstration projects for innovative technologies”. RE-plants that concluded contracts before the entering into force of the IEMR continue to benefit from priority dispatch. Furthermore, with regard to RECs Art 7 para. 3 IEMR stipulates that “Nominated electricity market operators shall provide products for trading in day-ahead and intraday markets which are sufficiently small in size, with minimum bid sizes of 500 Kilowatt or less, to allow for the effective participation of demand-side response, energy storage and small-scale renewables including directly by customers”. Figure 1 illustrates the relation of the RED II and the IEMD/R.

In sum, generally speaking, RECs are a specific form of CECs that benefit from an “enabling framework” promoting and facilitate their development. However, they have their own area of operations not falling under the IEMD/R as far as other types of energy (i.e., not electricity) are concerned. In this regard, the possibility of benefitting from conventional small-scale back-up generation is an important element for REC’s micro-grid solutions, be it on- or off-grid. Most importantly, unlike CECs they benefit from the preferential conditions of the “enabling framework”.

2.2. The New Governance Model and its Importance for RE Clusters

With regard to energy communities, of course, European energy law does not rule out other private law citizens’ or consumer-oriented initiatives facilitated by and implemented with the participation of the public administration in the Member States [17]. However, such initiatives would benefit neither from the possibility of electricity/energy sharing nor from the preferential conditions and incentives foreseen in the “enabling framework” to promote and facilitate the development of RECs under the RED II. Therefore, the new Europe-wide governance model for energy communities is a determining factor for the choice of business models applied [21]. Both types of energy communities focus more on environmental, economic or social community benefits than on profits and both limit the effective control of the community to their beneficiaries; however, whereas RECs do this by tying control to the criteria of locality and geographic proximity, CECs limit it by the size of the shareholders and their commercial activity, excluding those for which energy constitutes the primary area of activity. An overview is provided in Table 1.

With regard to RE, the two crucial consequences of this governance model for the CSOP—as well as for any other business model—are that a REC according to Art. 22 RED II:

- Must be autonomous and independent of other RES project partners. “Autonomy” in this context should be understood as a 33% ceiling for ownership stakes of individual shareholders or members; recital 71 RED II stipulates that “REC should be capable of remaining autonomous from individual members and other traditional market actors that participate in the community as members or shareholders, or who cooperate through other means such as investment”.

- In addition, “is effectively controlled by shareholders or members that are located in the proximity of the renewable energy projects owned and developed by that community” result in a ceiling for the strategic investor’s participation of 49% (see the requirements of the definition of Art. 2 of the RED II in Section 1.1 above) or at least binding contractual arrangements that confer decisive influence on the composition, voting or decisions. Art. 2 pt. (56) IEMD defines “control” as “rights, contracts or other means which, either separately or in combination and having regard to the considerations of fact or law involved, confer the possibility of exercising decisive influence on an undertaking, in particular by: (a) ownership or the right to use all or part of the assets of an undertaking; (b) rights or contracts which confer decisive influence on the composition, voting or decisions of the organs of an undertaking”.

These new rules for the lawful control over and administration of (local) energy generation, supply and management concern also the fair distribution of responsibilities and benefits and are the governance side of the technical solutions for the Energy Transition. Energy communities; thus, are the mirror image of energy clusters; the former concern the governance, the latter the technological side of the (renewable) energy systems of the future, entailing flexibility, bi-directionality and interconnectivity options between prosumers and producers of energy and the market [15]. Most importantly they allow energy sharing of a portfolio of RES, that can enhance complementarity, lower energy costs for prosumers [10] and, through (co-)ownership in RES, increase social acceptance of the architecture and logic of a RE future [22].

3. Empirical Evidence: Material, Methods and Results

To cast a light on available empirical information on the structure of renewable energy communities the results of an analysis [15] of a dataset of 67 best-practice examples of consumer (co-)ownership reported in the Palgrave Macmillan publication “Energy Transition: Financing Consumer Co-Ownership in Renewables” [16] are briefly summarised in this section. The notion of (co-)ownership is used not in the technical sense of joint ownership but to indicate that there may be other owners next to the consumers amongst the shareholders such as municipalities or conventional investors. The cases are from 18 countries covering Europe, North and South America and Asia, that is, CZ, DK, FR, DE, IT, NL, PL, ENG, SCT, ES, CH, CAL, CAD, BR, CL, IND, PAK, JAP; these countries were analysed following a consistent pattern including the energy mix, policies supporting consumer (co-)ownership, energy poverty, the regulatory framework, best practice, financing conditions, obstacles and perspectives to enable a like-to-like comparison. In light of the potential for replication of the regulatory framework beyond Europe, and to confirm the existence of projects that fit the criteria elsewhere, the extra-European cases present in the dataset were included in the analysis. The definition of consumer (co-)ownership as “participation schemes that (a) confer ownership rights in RE projects (b) to consumers (c) in a local or regional area” [23] (pp. 7–8) is followed in this article.

As mentioned, eligible members for RECs are natural persons, SMEs and local authorities, while CECs are, in principle, open to all entities. Both the IEMD and the RED II; thus, support heterogeneity of members, which follows from the purpose and guiding principle for both types of energy communities “to provide environmental, economic or social community benefits for its shareholders or members or for the local areas where it operates, rather than financial profits”. However, with a view to the legislative process it remained unclear whether these guiding principles and in particular the emphasis on local and diverse co-investors originated from political desiderata or practical experience of already operating energy communities. Similar doubts arose with regard to the RED II prerequisites that to qualify as a REC, (a) the effective control should be held by members based in the proximity of the RE installations, and (b) its autonomy from single shareholders is to be upheld by the principle that no single shareholder owns a controlling stake. The IEMD contains a comparable but fairly milder restriction in precluding entities engaged in large-scale commercial activity and for which energy constitutes the primary activity as well as medium and large-sized enterprises from the shareholders effectively controlling the CEC.

The resulting limitations for enterprises which are either not local, too large or dominant in the energy sector with regard to control and size of their shareholding in energy communities may hamper their participation in RECs; together with those stemming from the business models prevalent to date risk to render RECs unattractive for these potential co-investors [21]. While good legislative intentions can lead to over-complex regulations that may actually hinder project implementation, a lot depends on how existing best practice deals with such problems [15]. Amongst other issues Lowitzsch, Hoicka and van Tulder investigated the diversity of co-investors and the prevalent governance structures, testing the dataset for the two following criteria: (a) Heterogeneity of members and (b) governance and ownership. The results of the analyses for these two criteria can be summarised as follows:

- They show that in the evaluation of the 67 cases, 37 had co-investors as envisioned by the RED II for the future RECs. Although these numbers seem low they are nevertheless unsurprising as energy communities operating exclusively in RE are a recent phenomenon not yet widely implemented.

- What is more surprising is, that only 9 projects already meet RE cluster requirements while merely 22 have RE cluster potential. Many projects are of small size and do not or only to a limited extend involve flexibility, bi-directionality, interconnectivity and complementarity; but this is a condition to become fully fledged RECs that will also be able to benefit from energy sharing [15].

- Only in 20 of the 37 cases this involved genuinely heterogeneous co-investors although not all of them comply with the governance structure required by the RED II. Some projects are solely owned by one shareholder; other projects, although showing heterogeneous co-investors are dominated by commercial actors not based in the proximity of the RE installations; in yet other projects a large energy firm has a majority ownership stake violating the autonomy criterion.

- Of the remaining 17 cases that only formally comply with the heterogeneity criterion of the RED II some cases were either cooperatives exclusively with citizens as members or municipal projects without other co-investors.

- Furthermore, geographic and cultural diversity of RE projects even within a given country lead to complexities that do not permit “one size fits all” solutions. While identities and interests are often deeply rooted in geographies and cultures, organizational and contractual arrangements are a more flexible factor that can be adapted to the former two [24].

Against the background of these empirical findings the question which business model is best suited for the RECs of the future becomes even more important. Only a sufficiently flexible business model like the RE-CSOP will be able to fulfil the necessary functions of RE clusters and allow truly heterogeneous partnerships for investment.

4. Presentation of the Renewable Energy Consumer Stock Ownership Plan

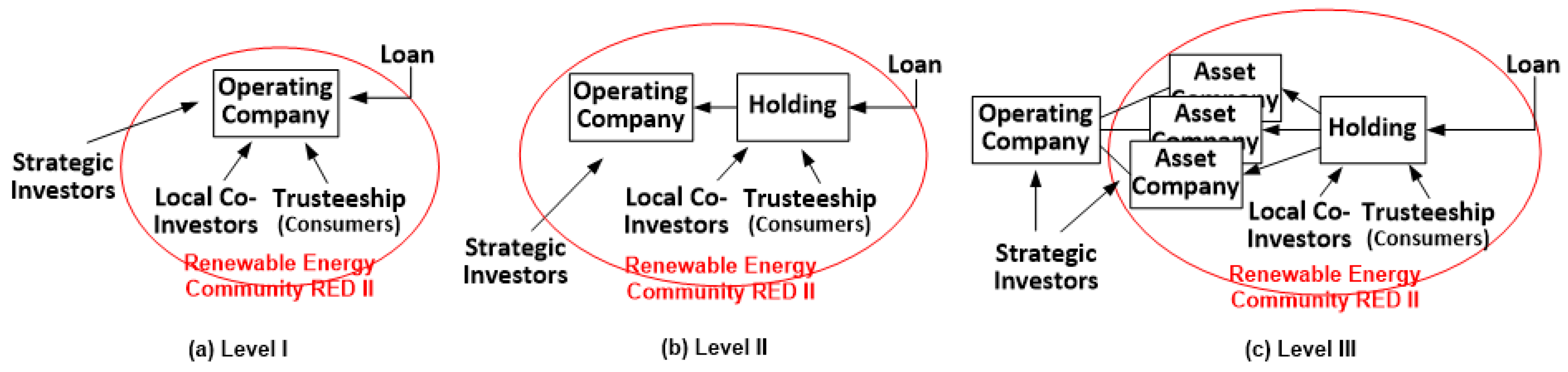

The modular approach of the RE-CSOP (see Figure 2) and the structure for each level of co-investment as described in this section is conceived under the assumption of complying with the new RED II governance model in order to benefit from the preferential conditions or incentives foreseen “enabling framework” to facilitate setting up RECs. Therefore, Figure 3, Figure 4 and Figure 5 emphasise the role of the controlling members of RECs. As a rule, prosumers (households and non-energy small and medium sized enterprises) will hold between 33% and 51% of the shares in the corporation operating the RE-facility (Operating Company) and, together with the municipality, will have a majority interest. However, the CSOP conveys individual shareholding of the participating consumers through a trusteeship. Regarding the exercise of consumer’s voting rights, the model offers flexibility: The fiduciary arrangements stipulate which matters are to be decided by the trustee or the managing director of the fiduciary entity (e.g., day-to-day business) and which will be voted on by CSOP-members (e.g., strategic decisions). It is; thus, the consumers themselves that determine the extent of their involvement, thus facilitating a process of apprenticeship. Finally, as the CSOP business model uses the borrowing power of a corporation, it enables the participation of vulnerable consumers that are underrepresented so far.

4.1. The Modular CSOP Approach

In practice, CSOP financing is based on a modular approach, starting with a “base model” and extending to higher levels, depending on the type of different co-investors involved, their investment horizons, needs and aims (see Figure 2a–c).

Level I: The base model is composed of two closely held corporations with limited liability, the fiduciary entity (Trusteeship) and the CSOP operating company (Operating Company). The fiduciary entity can also be a limited partnership or a RE-cooperative already in place which; however, this would have implications for the taxation of individual consumer (co-)owners and their corporate rights. This structure corresponds to a situation where a strategic co-investor has a local long-term interest (e.g., acceptance of a wind project) and does not mind burdening the Operating Company with a capital acquisition loan for consumers; all shareholders are proportionally liable for the debt.

Level II: A more complex structure results when the strategic investor, for example, has a short-term interest and will not engage in the project if his shareholding would be burdened with the acquisition loan that facilitates the consumer shareholding; in this situation the Operating Company stands next to a Holding (again a closely held corporation with limited liability) with only the latter being liable for the acquisition loan. Of course, the Operating Company will still provide security for the loan pledging part of the assets of the RE installation.

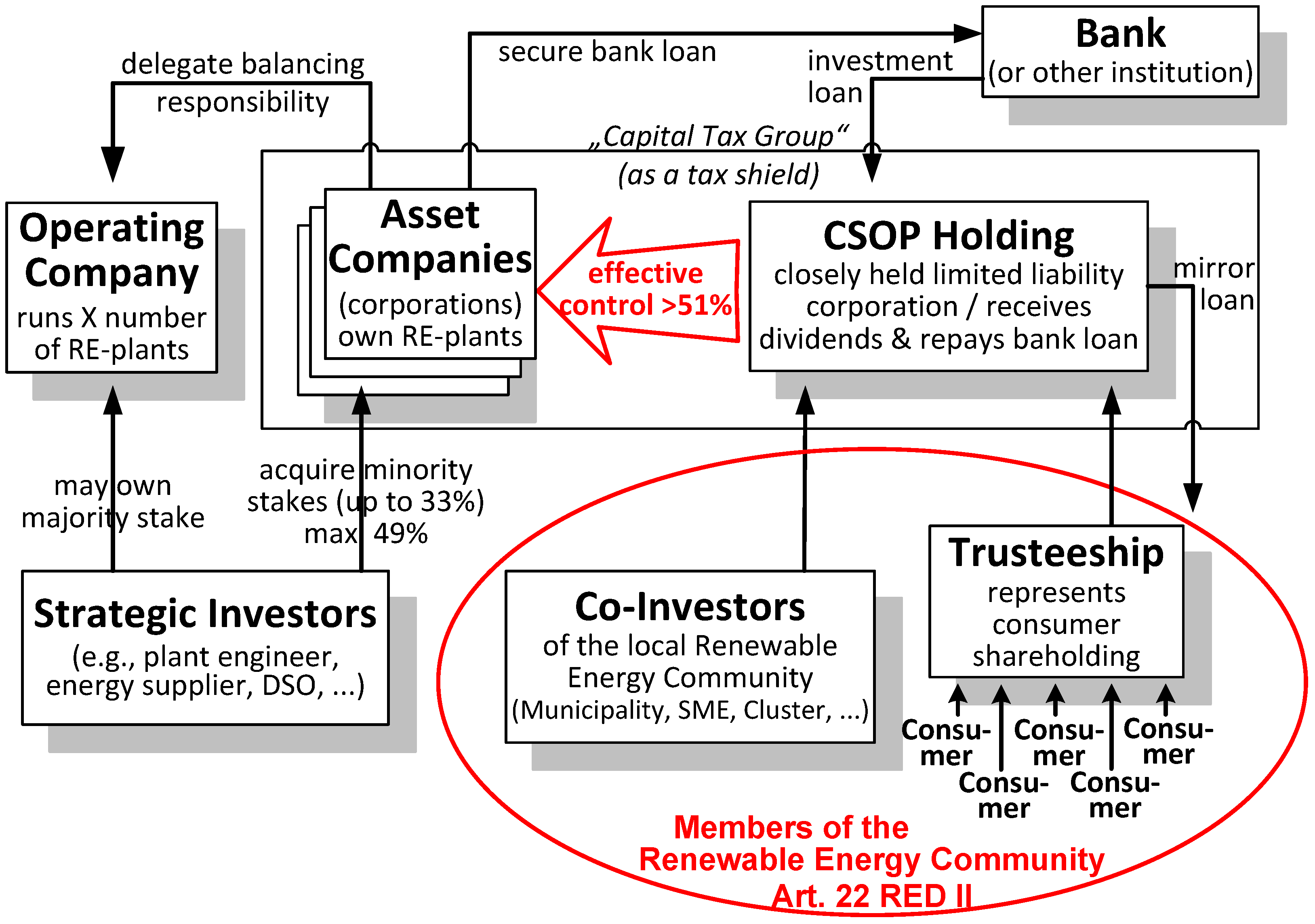

Level III: When upscaling and pooling more than one CSOP investment, the structure is still more complex: The Operating Company runs X number of RE projects, while separate Asset Companies own the RE installations of various RE-CSOPs. Strategic investors with differing short- or long-term interest (such as management, capital investment, electricity storage, aggregation and demand response) or a distribution system operator of a micro grid, for example, can invest at different levels accordingly.

To sum up, compatibility with conventional investments together with the potential of scalability, gives the RE-CSOP the advantage of avoiding concerns of market fragmentation [23]. Sub-scale investments can be eschewed, local projects pooled and partnerships with municipalities set up, thus advancing to economies of scale while retaining the benefits of individual consumer participation. Other than qualifying as a RECs and thus benefitting from the RED II “enabling framework” the RE-CSOP at the same time provides a business model flexible enough to allow for the cooperation with professional energy companies (see in particular Level III).

Against this background, RE-CSOPs can be an important “bridge technology” in financing citizen energy projects while extending the advantages of RE-cooperatives where projects involve heterogeneous co-investors, or where the cooperative model is not feasible for other reasons [12]. This is especially the case in Eastern Europe where citizen energy projects are still rare and where the cooperative model is associated with the socialist past. Furthermore, the flexible governance structure of CSOPs offers the advantage of combining RE projects with active citizen participation, both in financial returns and in decision-making, while also allowing for the participation of commercial investors. Especially in RE clusters that target sector coupling and may involve electricity sharing, storage, e-mobility, cogeneration, etc., including professional operators will become increasingly important as the operation and maintenance of the infrastructure of RE projects becomes more complex [15]. Here the RE-CSOP provides a standard governance model that safeguards the interests of local partners vis-à-vis their co-investors.

4.2. Level I—Key Elements of the Base Model (Leveraged or not)

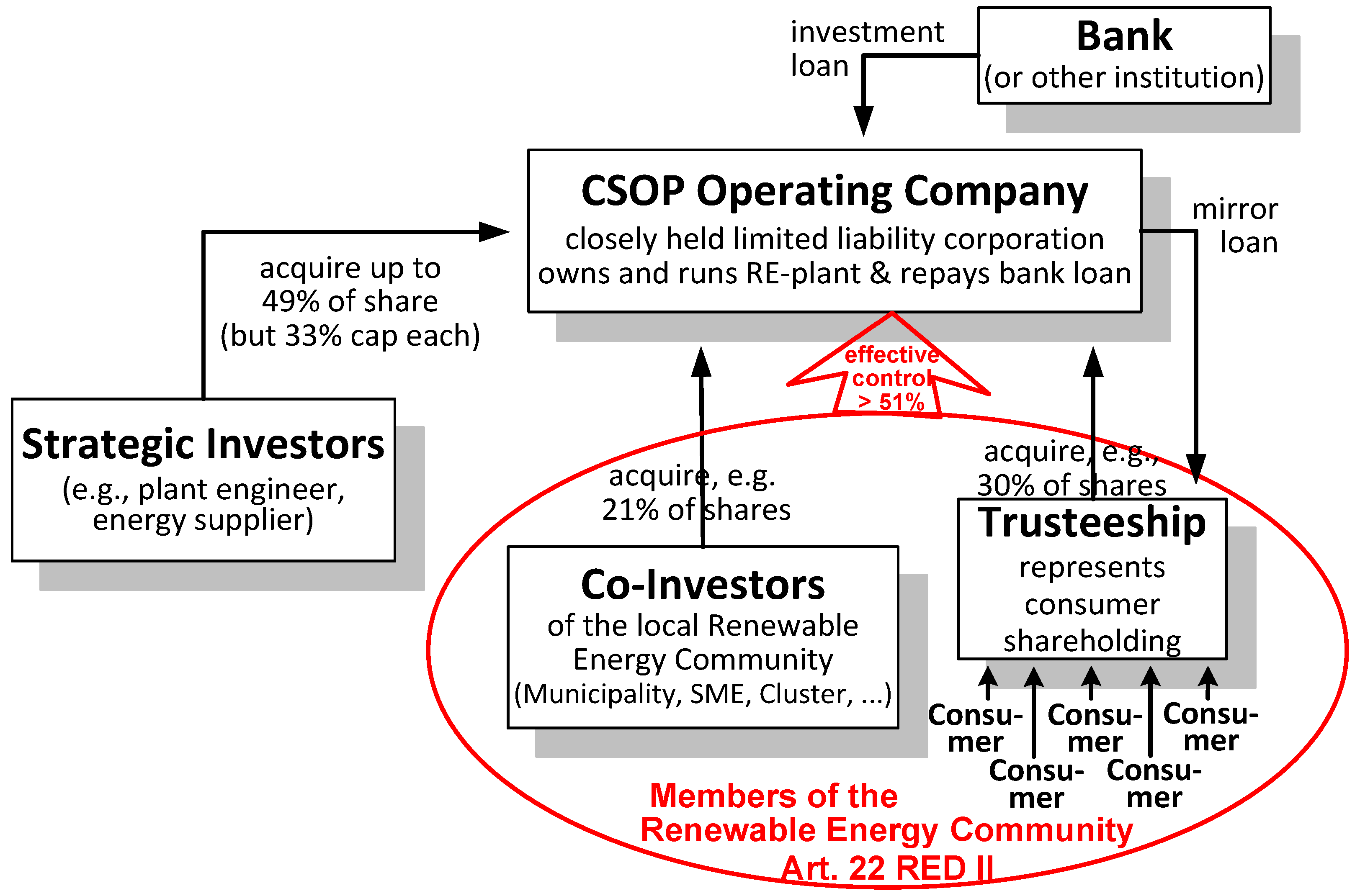

The first element of the RE-CSOP structure is the RE installation that is operated and managed by the Operating Company. The Operating Company is set up as a closely held limited liability corporation which is the best solution with regard to the functionality of the whole structure as well as with regard to the optimisation of taxation (for example, under Polish law a “spółka z ograniczoną odpowiedzialnością”, under Italian law a “societá a responsabilita limitata”, under Czech law a “společnost s ručením omezeným” and under U.S. American law a “closely held corporation”).

Variant A—A new Operating Company is set up as a special purpose vehicle specifically for the new consumer co-investment: The consumers involved become (co-)owners of the RE installation by themselves or in partnership with other local public partners (e.g., a municipality, entity of local self-administration, public law corporation or a municipal enterprise) and possibly with local private investors such as SMEs.

Variant B—An existing Operating Company is running and managing an existing RE installation: It is taken over partly or entirely by another legal subject assuming control on behalf of the consumers and the other co-investors of the local RE community pursuant Art. 22 RED II.

As the ultimate goal of creating the overall structure is to grant corporate rights to the consumers, it is necessary to answer the question, how will they be included in this plan? This concerns in particular what kind of legal, corporate and property ties will connect the consumers of the RE installation with the Operational Company (independently of the contractual relationship for the supply of energy, of course). On the one hand, consumers could be direct shareholders of the Operating Company, but from a functional perspective this is not a desirable solution. Another component of the RE-CSOP; therefore, is a fiduciary entity. It is this fiduciary entity that on behalf of the consumer-shareholders, together with the other local shareholders, effectively controls the Operating Company (running the RE plant). The legal form of the intermediary entity administering the CSOP shares in the CSOP model for continental Europe, is derived from the Anglo-American Common Law of trusts [25]. In the absence of genuine trust legislation, this requires a two-tier structure (i.e., a closely held corporation with limited liability as fiduciary entity (Trusteeship) that holds consumer’s shares in a closely held corporation with limited liability that operates the RE plant (Operating Company)). Figure 3 gives an overview of the financing structure and the key elements of the base model (Level I).

As mentioned earlier, a RE-CSOP can use a bank loan to leverage the acquisition of shares in a RE project for consumers that have neither savings nor access to capital credit. National company and tax law permitting, using corporate credit to guarantee the loan that funds the acquisition of consumer shares by the CSOP, reduces the financing costs. If the Trusteeship borrows money to buy shares, the Operating Company repays the loan through periodic contributions (however, financing costs will not be tax-deductible) and dividends paid on the shares the fiduciary entity holds in trust for the consumer-shareholders. As the loan is retired, paid-up shares are allocated to individual consumer accounts, usually on the basis of relative energy consumption.

In a variation of the above described loan structure, the lender often prefers to make the loan directly to the Operating Company, followed by a second “mirror loan” from the Operating Company to the Trusteeship. The tax results will be better than in the case of a direct loan to the fiduciary entity. The interest repayments—national company and tax law permitting—will be a deductible expense from taxable corporate income as financing costs of the RE-investment. However, the Operating Company has to make annual contributions to the Trusteeship in amounts sufficient to amortise the internal loan from the Operating Company to the Trusteeship. The amounts paid by the fiduciary entity to the Operating Company to amortise the internal loan will as a rule constitute tax-free loan repayments and will be used by the Operating Company in turn to amortise the external loan. The “mirror loan” structure provides the lender with a stronger security interest in the assets pledged as collateral for the loan [26]. The lender will be in a better position to defend against claims of fraudulent conveyance in the case of default if collateral is taken directly from the borrower rather than from a guarantor of the loan. This should also lower the financing cost for the leveraged transaction significantly.

However, to use this structure the other shareholders of the Operating Company that do not directly benefit from the leveraged transaction must agree to assume the risk associated with financing the acquisition of shares by the Trusteeship with a bank loan. This may be acceptable if these shareholders are all members of the REC and share a genuine interest in involving the consumers. However, in situations where either the interests of the members of the REC are too heterogeneous or where external co-investors are involved, such co-investors may object to the mirror loan structure. In these situations, it may be necessary to set up a Holding Company, as described in the next section.

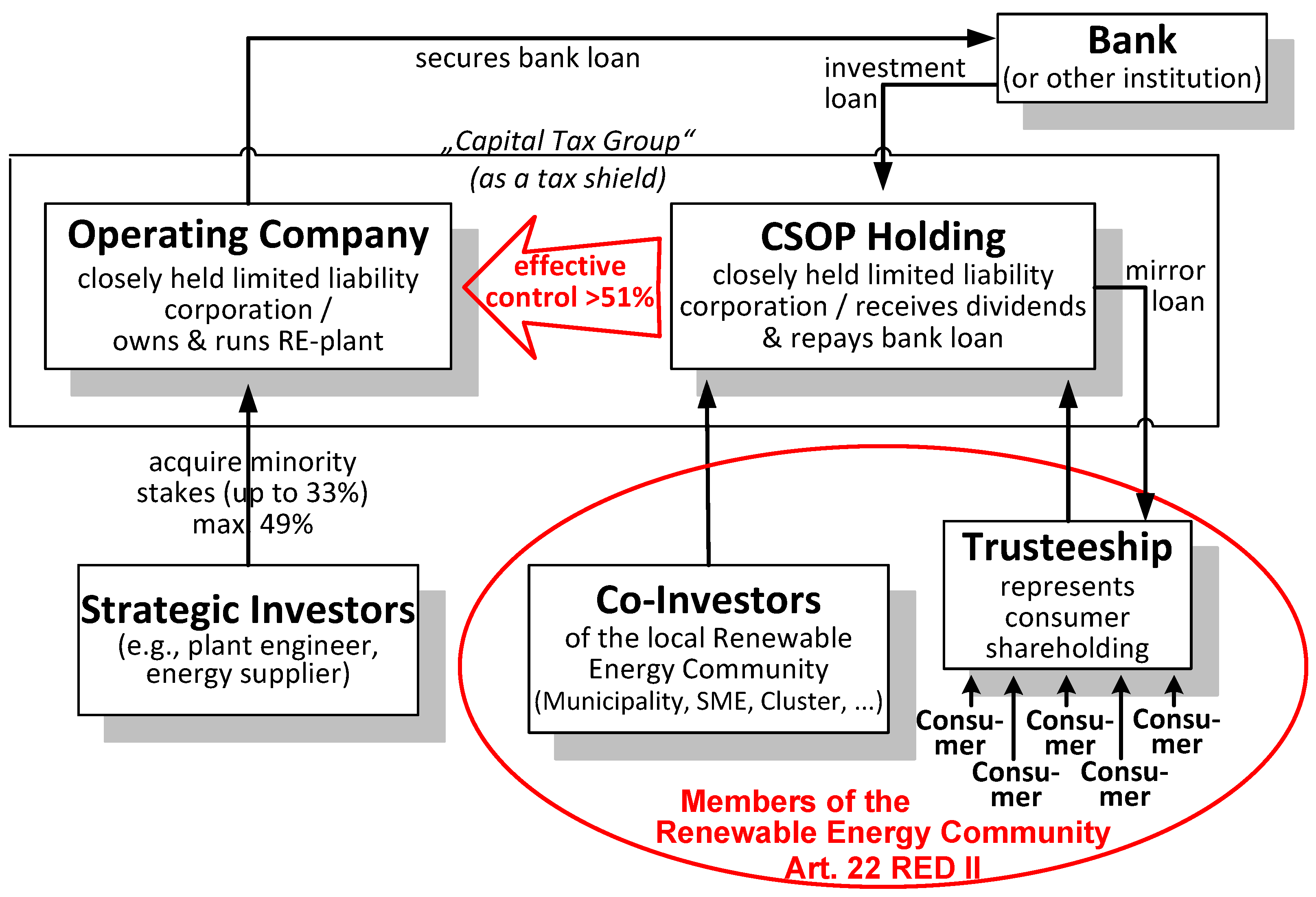

4.3. Level II—Leveraged RE-CSOP with External Strategic Investor

The following alternative structure of the RE-CSOP model employs a Holding Company which obtains external financing both for the consumers and for the other members of the local REC (i.e., taking on a loan or credit and then investing it in the Operating Company (Variant A); or acquiring the shares from the current owner(s) (Variant B)). The justification for this structure is the diversity of interests of the potential co-investors.

The Holding Company is again a closely held corporation with limited liability which, at the same time, may facilitate the functioning of the entire structure from the viewpoint of tax optimization. The investment or acquisition is financed from external sources, with the loan/credit being repaid from the future profits of the RE installation run by the Operating Company (with such profits coming from the sale of electricity to consumers or to the grid and from the difference in price of the energy provided to the prosumers). National tax law permitting, the Operating Company and the Holding Company may establish a capital tax group (see 5.2. below). In the case of such a structure, profits, losses and, what is most important here, costs, are calculated for tax purposes jointly for the combined tax group. As a result, in practice, financing costs (especially interest) can be deducted from the tax base of the Operating Company. Such a solution has many advantages, including the following:

- Consumers are still not direct shareholders in the dominating Holding Company (in the case of a Holding Company whose direct shareholders would be supplied by the dependent Operating Company, problems relating company law institutions could arise, such as actions to exclude a shareholder, the increase and decrease of share capital, organization of shareholders’ meetings, change of statutes, etc.).

- The division of the shareholding between the members of the REC (i.e., municipality, SMEs, and other local co-investors on the one hand, and the consumers represented by the fiduciary entity (Trusteeship) on the other hand) is flexible and reflects the respective contributions and roles, as long as they together have effective control of the operating company by keeping at least 51% of its shares.

- External strategic investors can buy into the project without being burdened by the leveraged transaction that enables consumers without significant savings to participate.

Thus, at Level II there are three entities in this structure—an Operating Company running the RE installation, a CSOP Holding (dominating company) and a Trusteeship, being the sole shareholder or the co-owner of the Holding, and thus indirectly controlling the Operating Company. Figure 4 shows the advanced scheme of the RE-CSOP model of Level II.

In summary, this solution offers two opportunities for co-investments at Level II:

(1) Leveraged investments financed by an investment loan taken on by the Holding Company. The target groups for this type of co-investment are, above all, local co-investors belonging to the REC pursuant to Art. 22 RED II as, for example, a municipality, a small or medium enterprise, members of a RE cluster, etc. They all have in common that their investment horizon is long- to mid-term and that, as a rule, they will have difficulties in obtaining financing individually, or, at least will incur higher financing cost [27], than when benefitting from the borrowing power of the Holding that pledges its shares in the Operating Company to secure the repayment of the investment loan.

(2) Non-leveraged investments financed by a strategic investor in the Operating Company. The target group for this type of co-investment is, generally speaking, external strategic investors that either do not qualify as members of a REC pursuant to Art. 22 RED II and/or have different motivations for their engagement in the project. They typically will have a short- or mid-term investment horizon with preferences for liquidity and a clear exit strategy. Examples are, on the one hand, shareholders engaged in large scale commercial activity for which energy constitutes a primary area of activity (e.g., an energy supplier), or, on the other hand, an external investor with a specific temporary investment interest, as, for example, a plant engineer that seeks acceptance for RE project [28].

4.4. Level III—Upscaling and Pooling RE-CSOP Investments

When RECs reach more complexity both with regard to the technical aspects of energy generation, use or transfer and with regard to the variety of heterogeneous co-investors involved, a need for upscaling and pooling of several RE-CSOP projects will arise. This is, in particular, the case with RE clusters emerging in the Energy Transition [15]. The needs that these RECs will depend on a number of factors that can be grouped into two categories:

- The variety of renewable sources (wind, PV, biomass, etc. and their complementarity) or other energy sources (fossils as back-up but also those not easily to divest from);

- The specific combination of different energy sources where energy production is not the primary aim of economic activity (e.g., cogeneration, waste, biomass, etc.).

- Management and governance requirements [29]:

- More than one RE-CSOP project organised in various asset companies with majority ownership stakes of the members of the REC but managed by one operating company in which a professional energy company may have a majority interest;

- The operating company is run by a third party with expertise in installation and operation, including metering and maintenance, but such third party remains subject to the RECs instructions.

In all the different combinations of scenarios resulting from the factors enumerated above, it will be important to have the possibility to separate the ownership of production assets from their management as illustrated in Figure 5 for Level III.

This is of particular importance, as it will also allow the involvement of strategic investors with majority interest in the Operating Company, which in this case may also be an already existing daughter of a professional energy company; such a strategic partner [29] can be delegated by the REC to provide a variety of services, such as balancing responsibilities, coordination and settlement between REC participants or the implementation of a virtual power plant. Consequently, Art. 21 para 5 RED II foresees that Member States allow the possibility that prosumer’s installations are owned by a third party but remain under the direction of self-consumers as Art 16 IEMD permits that Member States allow CECs to own, establish, purchase or lease distribution networks and to manage them or delegate management to third parties. The fact that RECs will bundle functions ranging from generation to distribution and sale is de facto an exception from the unbundling rules for energy markets implemented over the last decades, and again may make them attractive to strategic investors with regard to aggregation, demand flexibility, etc.

5. Discussion of the Key Elements of the RE-CSOP as Applied at Levels I–III

5.1. Indirect Consumer-Shareholding in the Capital of the Operating Company (or Holding)

(Co-)ownership resulting from consumer investment leads in practice to a situation where consumers have influence on the management of the company. From the point of view of co-investors—internal or external—such influence is problematic in terms of predictability and steering of the dynamics in decision-making processes [9]. First, it is highly undesirable that a co-investor would have to interact constantly with all consumer-shareholders, which easily can be hundreds in large CSOPs. Second, with regard to the question of how participating consumers vote their shares, it is undesirable that every consumer takes individual decisions without coordination with the others making it difficult for the remaining shareholders to understand and forecast their voting behaviour and interests. At the same time avoiding fragmentation of their ownership stake ensures that consumers voice has an appropriate weight vis-à-vis that of their co-investors [30]. Therefore, it is desirable that consumer-shareholders take a common position after an informed decision-making process.

5.1.1. Conveying Individual Share Ownership through a Trusteeship

Against this background, the CSOP model conveys individual shareholding of the participating consumers through a Trusteeship, which also—if desired—enables a cautious and gradual transfer of involvement in management decisions; the responsibility for day-to-day decisions of business operations stays with skilled management [31]. The vehicle of a fiduciary entity is a tool for professionalization of decision-making processes on the part of consumers, which at the same time ensures that consumers vote their shares together (en block) after an internal consultation advised by an expert. The fiduciary entity typically takes the form of a closely held corporation with limited liability (however, it could also be, for example, a limited partnership) administered by a managing director [25]. The fiduciary entity has only one shareholder (i.e., its founder; usually the initiator of the RE-project), shown in the list of shareholders at the registry court, with its sole purpose to represent the shareholding of the consumer-shareholders in the operating company. The establishment of the trust follows the conclusion of fiduciary contracts between the trustors and the managing director representing the Trusteeship. From a tax point of view the fiduciary entity is transparent as it is the consumer-shareholders who are the economic owners of the shares.

Instead of direct shareholding in the operating company the RE-CSOP, thus, involves a fiduciary entity that conveys the capital participation of the consumer-shareholders. A (fiduciary, fully fledged) Trusteeship of a shareholding occurs when a shareholder (here the fiduciary entity = trustee) owns the shareholding for the account of one or more other entities (here individual consumer-shareholders = trustors) in the sense that she is entitled to the rights arising from the shareholding only in accordance with a fiduciary contract concluded with the trustors [32]. Unlike in the case of an “authorisation trust” or the “power of attorney trust” in this case the separation of the trustee’s external legal competence from his internal fiduciary duty is purely accomplished. The trustee (fiduciary entity) has a dual role: in relation to the other shareholders (e.g., municipality, strategic investor) she is the holder of the shareholder rights and in relation to the settlors she is entitled and obliged to exercise these rights for the account of the settlors (i.e., the participating consumers). The settlors can be described as holders of shareholder rights merely in the economic sense of the term. The trustee is in every respect carrier of the membership (i.e., shareholder) and, consequently, it is the fiduciary entity that is shown in the list of shareholders of the operating company (here a closely held corporation with limited liability).

5.1.2. Core Issues to be Considered for all RE-CSOP Models (Levels I–III)

In the context of enabling consumers to purchase shares, three key aspects need to be considered: (a) Securing the transferability of shares; (b) minimizing the cost of changes of ownership within the consumer-shareholders; and (c) granting corporate rights to the consumers.

Transferability of shares—The rules for changes of ownership among the consumer-shareholders represented by the managing director of the fiduciary entity are enshrined in statutes of the Trusteeship (and will be mirrored in the individual Investment Agreements that the consumer-shareholders conclude with the fiduciary entity):

- Exit of a consumer-shareholder with simultaneous transfer of the capital participation to a new CSOP participant only requiring a change of the party of the fiduciary contract (Investment Agreement).

- Exit of a consumer-shareholder with sale of the capital participation to the Operating Company which holds the share(s) until a new CSOP participant buys into the RE-CSOP. The Operating Company “warehouses” the shares, while at the same time creating a market place of these shares between the CSOP participants; this requires a definition of the legitimate motives to exit and of the period to announce this leave, as well as that of the instalment period for the cashing-out to avoid haemorrhaging of liquidity for CSOP.

- Exclusion of “bad leavers” (e.g., where consumer-shareholders obstruct decision-making within the fiduciary entity (Trusteeship), violate the supply contract substantially, etc). Here a cancellation of shares may occur with a subsequent transfer of monies from the Trusteeship.

- Exit following the death of a consumer-shareholder, which requires rules concerning the transfer by inheritance.

Minimizing the cost of changes amongst the consumer-shareholder—Pooling consumers’ ownership rights in a fiduciary entity reduces transaction cost of share transfers between participating individuals (e.g., when CSOP participants move away from the region and transfer their share to new residents). At the same time facilitating consumer (co-)ownership through a fiduciary entity also ensures easy tradability of the shares. “Brokering” consumer shareholding in the Operating Company by the Trusteeship is sufficient to render consumer shares fungible and only requires a fiduciary contract (here Investment Agreement) between the consumers and the Trusteeship: It is the fiduciary entity represented by its managing director that—entering into the Investment Agreement with the consumer-trustors—now holds the shares of the Operating Company on behalf of the consumers. When consumer-shareholders change, the buyer or heir simply steps into the Investment Agreement in lieu of the former trustor. Changes of shareholders need not be registered—as would be the case for direct shareholding in the Operating Company—and the amount of participation held by the Trusteeship can fluctuate making administration easy. The basic mechanism is a fiduciary contract as is used in other investment settings. This structure is a standard solution in Germany tested many times by so-called public companies (“Publikumsgesellschaften“ [33]) in real estate investments, who face a similar problem: A very large number of investors is intended to participate in the equity of a company where every change in ownership, whether it be due to death, sale of shares, or seizure has to be signed into the commercial register following the relevant formal procedures. Whether or not the transfer of capital participation from one consumer to another requires notarisation depends on the type of trusteed entity and national company law. For example, in Germany this would be the case for a closely held corporation with limited liability but not for a limited partnership, which in the latter case would have the advantage of lowering the transaction costs of transfers of capital participation from one consumer-shareholder to another. In contrast, the transfer of shares of an Italian closely held corporation with limited liability, following a 2019 reform of company law, does not require notarisation any longer. Depending on national tax and company law the advantages and disadvantages of the different legal design options, therefore, must be weighed against each other.

Granting corporate rights to consumer-shareholders—The statues of the trusteed entity, which as a rule will be a closely held corporation with limited liability, will include a catalogue of decision that can be taken only after a vote among the consumer-shareholders. This leads to a two-tier structure for the decision-making process with regard to representation and control and especially voting rights distinguishing between:

- Decisions concerning the day-to-day business of the Operating Company (or respectively of the CSOP Holding) that the Trusteeship represented by its managing director is authorized to take on behalf of the consumer-shareholders as trustors.

- Decisions of strategic importance (e.g., change of range of activity or business purpose, change of management, and those decisions involving financial commitments above a specific threshold; for example, EUR 50,000 requiring a vote of all trustors).

In this way, as mentioned above, the Trusteeship is also a tool for professionalization of the decision-making processes in the Operating Company while at the same time ensuring that:

- They have the possibility for an internal consultation advised by an expert (the managing director of the Trusteeship should have appropriate qualifications or access to expertise).

- They vote their shares together (in a block proportional to the Trusteeship’s share in the Operating Company’s or CSOP Holding’s capital).

5.2. Financing the Consumer-Investment in the Operating Company

The CSOP is a type of leveraged investment (or buyout) transaction that uses external financing (debt), thereby achieving the benefit of financial leverage [9]. The cost of raising capital, as well as the repayment method, and, above all, the repayment period of the entire debt is all of key importance for the success and efficiency of this type of transaction. This section presents several legal and economic ways to shorten the debt repayment period or reduce the cost of financing and thus increase the effectiveness of financing RE-CSOP transactions.

The basic variable to be analysed is the debt repayment period. This is the period during which the CSOP Holding repays the debt using funds from the profits of the RE installation (the Operating Company). On the Holding or the Operating Company’s balance sheet, liabilities from loans taken will gradually decrease in favour of equity. After the repayment period, the debt liabilities will be paid off, which means that external lenders no longer have any claims against the acquirer. In a simplified manner, it can be said that in such a situation the CSOP Holding (and indirectly the consumers) becomes the "full" economic owner of the RE installation (the Operating Company).

The repayment period is influenced by several factors. Determinants can be divided into two groups. The first group are economic factors of a more external nature, one being the size of the debt incurred, measured as the relation between equity and liabilities—the larger the percentage of the CSOP Holding’s or Operating Company’s assets financed from external funds, the longer the debt repayment period. Another factor is the profitability of the RE installation, that is, of the Operating Company measured by the return on equity ratio (ROE)—the higher the profit generated by the RE installation, the faster the repayment period. The second group of factors affecting the repayment period are legal and economic factors used in a specific transaction. This category includes, among others: (a) funds contributed by consumers; (b) tax optimization; or (c) a preferential loan granted by a public partner.

Contributions by the consumers—The application of CSOP financing in the context of Local Energy Communities according to Art. 22 RED II brings benefits to all parties, especially to the consumers. Therefore, it is justified that consumers make determined financial contributions to the RE-CSOP, which will help to increase its economic efficiency. However, against the background of the principle of proportional participation of CSOP participants depending on consumption (and not on financial strength), a limit is the average income of citizens and their access to savings. The amount of consumer contributions and their importance for the overall project depends on the size of the projected RE installation and the number of consumers supplied, the average purchasing power parity and, above all, the part of the income allocated for contributions. From experience in the U.S., it seems right to limit individual consumer contributions to a maximum of 10% of their respective earnings to avoid risk concentration [31].

Furthermore, it has to be taken into account that there may be changes after the initial allocation of shares to the individuals proportional to the households’ respective energy purchases. In order not to incentivise increased energy use by a strict coupling of the acquisition of shares to consumption, a correcting factor should reward increased EE measured by a decrease in consumption per household member. Rewarding consumer-shareholders for reducing their consumption is also justified by the accelerated amortisation of the bank loan, as this will result in an earlier point in time that dividends are paid out.

Capital Tax Group—An important solution may be the creation of a tax capital group [34], which includes the Operating Company (running the RE installation) and the Holding Company. In this way, financing costs (interest) can be deducted from the tax base, which translates into a higher net profit of the entire capital group and enables the use of the so-called tax shield effect. Repayment of debt using a capital tax group can be made using:

- Fixed capital and interest instalments—in certain periods additional financial resources will be generated that can be allocated to reserves to ensure timely repayment in the event of an economic downturn or the payment of funds to consumers due to resignation from the plan;

- Or variable capital and interest instalments—allocation of a fixed percentage of the net profit for this purpose in each period.

Thus, the setting up of a capital tax group is desirable and—provided that it is permissible under the relevant national taxation legislation—should be considered during the creation of CSOP structures. However, restrictions with regard to the effective control of the two entities may occur. For example, under Polish tax law creating a capital tax group requires that the Holding Company has a 75% majority interest, thus lowering the ceiling for strategic investors’ share to 25%.

Preferential conditions, subsidies or loans—Some of the solutions aimed at shortening the debt repayment period and thus improving the efficiency of the entire undertaking, are preferential conditions for land use, public subsidies or, if available, preferential loans from a public partner who owns part of the infrastructure where the investments take place [35]. In the case of a municipality, these may be buildings on which RE installations are constructed. Thus, a part of the funds for RE investments could come from one of the REC’s partners according to Art. 22 RED II. This solution facilitates obtaining external financing and reducing the costs of the entire project. In addition, the public partner earns a higher interest rate than is earned on the funds invested in the capital market. Under this method, there are two options for debt repayment:

- Deferment of the repayment to the public partner until the loan is repaid in relation to the bank: The public partner agrees to subordinate its loan repayment to the investment loan, and agrees to postpone of its repayment period until other creditors, in particular those of the co-financing bank, have been repaid.

- Parallel repayment of the bank and the public partner.

5.3. Taxation of the RE-CSOP and its Consumer-Shareholders

Deferred taxation for consumer-shareholders—Under continental European tax law, the Trusteeship is treated as “transparent” [32] (i.e., the shares of the Operating Company are deemed to be owned by the consumer-shareholders) as beneficial owners (or economic owners) of the Operating Company. However, the standard Investment Agreement of the RE-CSOP (fiduciary contract) stipulates that a consumer-shareholder cannot dispose of his or her share(s) held in trust until fully paid for and until the CSOP participant decides to leave the plan. In this way, deferred taxation of the appreciation of their investment is guaranteed as taxation does not occur until the shares are eligible to be distributed from the Trusteeship and the consumers are actually able to economically dispose thereof. The parallel structure of the Operating Company and the Trusteeship (pooling the shares of the consumer-shareholders) ensures that only dividends paid out are taxed at the level of the consumer-shareholders.

Tax treatment of profits at the level of the Operating Company—In the form of a privately held corporation with limited liability, the Operating Company is, tax-wise, not transparent and with regard to profits incurred at the level of the Operating Company shelters the consumer-shareholders [36]:

- When leveraged, the transaction is financed, if possible, by loans from state development banks with low interest rates under programs specifically promoting RE.

- As a rule, the Operating Company—due to the financing cost of the leveraged transaction—will make losses or, in the best case, very small profits during the first years.

- In the case that the CSOP invests in a new RE plant pro rata profits/losses are allocated directly to the Operating Company; when it invests in an existing incorporated utility, they are allocated indirectly through dividend payments/depreciation of shares. In both cases taxation of profits occurs only once at the level of the Operating Company.

Tax treatment of the financing cost—Usually, the project vehicle will be set up and capitalized as a new Operating Company since buying into an existing utility will be the exception for RE projects. When leveraging the CSOP investment, it is important that the bank loan be taken directly at the level of the Operating Company that is operating the project (e.g., a wind turbine (mirror loan, see above 4.2.)) and that it is the Operating Company that repays the loan from its profits. Only after the bank loan is repaid will profits be paid out to plan participants. Building and running the newly installed facility, profits/losses accrue directly with the Operating Company. Therefore, both deduction of interest payments, as well as depreciation and carry forward of losses, lower the tax burden, increase liquidity and thus accelerate principal payments [36].

The treatment of interest payments is less advantageous in the event of a leveraged investment in an existing incorporated utility. Interest payments incur for the Operating Company rather than at the level of the utility where they would lower the tax burden and thus generate additional liquidity to repay principal. Usually, during the first years the Operating Company will incur losses or, if at all, very small profits as the deductible financing cost, that is the interest on the bank loan, is offset by any taxable income. Of course, the Operating Company must generate enough income to cover the cost of financing servicing both interest and principal of the bank loan. Although, as a rule, double taxation is avoided and the Operating Company in the form of a privately held corporation with limited liability shields the consumer-shareholders taxwise, the benefits are limited under this scenario. Nevertheless, acceleration of principal payments as under the first scenario could be achieved by a debt-push-down through a merger of the Operating Company with the RE utility as target.

6. Conclusions and Policy Recommendations

With regard to energy communities, European energy law does not rule out other private law citizens’ or consumer-oriented initiatives than RECs which may be supported by and implemented with the participation of municipalities in the Member States [17] (p. 30). Such projects, while not complying with the RED II / IEMD governance model, would, of course, not benefit from the privilege of energy sharing of IEMD, and in particular the preferential conditions and incentives foreseen in the “enabling framework” under RED II. However, such initiatives could be led and controlled by professional actors on the energy markets who in RECs would be constraint to remain external investors or minority shareholders. The question whether such professional actors will accept the new governance model and decide to join RECs will depend on two factors:

- The attractiveness and coherence of the RED II “enabling framework”;

- The flexibility of the underlying business model allowing for an adequate division of responsibilities and benefits between the different co-investors according to their expertise and contributions.

The legislative instrument to advance RECs by tying the benefits of the “enabling framework” to the compliance with the governance model can be described as an opt-in mechanism [37] aiming at creating peer-pressure: With a rising number of RECs operating successfully in European municipalities, this new business model will also become increasingly attractive to the incumbents; at the same time the underlying governance model, with its emphasis on the prosumer and the active consumer, will become more acceptable. However, the number of RECs set up in turn will depend on their ability to involve heterogenous co-investors which, as the empirical evidence discussed in Section 3 shows, is key to the success of RE clusters. Here trusteed investment models and in particular the RE-CSOP, introduced in Section 4 as a flexible low-threshold financing method, can play an important role as a bridge technology. The capability to align the interests of municipal, individual and commercial investors, while mitigating the frictions stemming from inherent limitations of conventional approaches make the RE-CSOP the prototype business model for RECs, as has been argued in Section 5.

6.1. Recognising the Challenges of RE Clusters in the Energy Systems of Tomorrow

Against this background, a holistic approach is key to the success of RECs. This has to include not only the governance but also the technical side. The best legislative intentions may lead to over-complexity in one field, while having unintended consequences in another, if not thought through consistently in an interdisciplinary approach. Notwithstanding, the RED II and, to a lesser extent, the IEMD focus on governance issues without providing details on the incentives that make a cooperation let alone partnership of RECs with professional energy companies in RE clusters [15] economically attractive. Therefore, four issues require specific attention:

- With decreasing cost of energy storage and increasing demand for local flexibility, community energy storage systems will become increasingly important for the energy transition as such and, consequently, for RECs. The challenge of integrating community storage in the energy system that presently is still largely centralized demands for socio-technical innovation [38].

- Apart from concerns that the new European regulatory framework does not sufficiently encourage, or in places even inadvertently discourages, complementarity between RES [15], the RED II does not adequately answer the question how energy sharing between local partners within RECs and with the possible involvement of professional energy companies can be facilitated.

- The question of operating and managing electricity networks and especially grid ownership of energy communities both RECs and CECs remains a thorny issue since regulators and the incumbent DSOs are inclined to opposition [29]. Although optional for Member States, it should be supported for RE clusters depending on their complexity and incentivised in a targeted way, in particular during the pioneering period to foster RE deployment.

- Inclusion of low-income households and vulnerable consumers is an important cornerstone in the fight against energy poverty and a postulate of energy justice [39] taken up both in RED II and IEMD. However, although prosumership reduces households’ overall expenditure for energy and provides a second source of income through the sale of excess production [40], we observed a lack of concrete proposals in view to facilitate their participation.

Again, a lot will depend on the underlying business models and their capacity to provide flexible solutions that meet the different needs of the diverse actors. To test and demonstrate their potential RE-CSOPs are currently being implemented in the Horizon 2020 project SCORE, which runs from 2018 to 2021 in three pilot regions and in cities across Europe following these pilot projects [41,42]. During implementation, SCORE puts an emphasis on vulnerable groups affected by fuel poverty as a rule excluded from RE investments.

6.2. Spelling Out the “Enabling Framework” for RECs

The provisions on energy communities of the RED II and the IEMD remain relatively open to interpretation and leave the national lawmakers with room to manoeuvre. The transposition into national law until June 2021 is an opportunity to fine-tune and adapt the RED II rules to the needs of RE clusters and to formulate appropriate incentives supporting the underlying business models, like the RE-CSOP. In particular, during this period, the challenge is to overcome obstacles stemming from a lack of compatibility both with the existing regulatory frameworks and the national idiosyncrasies in order not to discourage national legislators. Without going into detail, four general aspects are key to successful transposition:

- Elasticity with regard to the eligibility requirements of proximity of shareholders is important in order not to unintentionally hinder the realisation of more complex RECs, namely fully fledged RE clusters. This is particularly important in view of their impact on complementarity of RES in urban settings [15].

- Where it is expected to delegate the balancing responsibility to professional partners or to pool it for more than one REC, the incentive system of the “enabling framework” should take into account the increased costs of pioneering RE clusters in the still largely centralized present energy systems.

- Energy sharing in RECs is highly sensitive to national regulation, especially when using the public grid, as value creation depends on the ability of its members to sell electricity to each other or make use of offsetting mechanisms of the electricity meters [28]. Network fees should be reduced in proportion to the actual distances in order to maintain the benefits of prosumership in RECs.

- To this end, a real-world testing environment, operated for a limited period of time, also dubbed “regulatory sandboxes” [43], should allow for the testing of incentives for RECs. This would allow to better tailor the “enabling framework” to the most suited business models, proving to meet, in particular, the challenges of RE clusters. Identified best practise could then be supported in a more targeted manner.

Funding

The SCORE project that this research is based on has received funding for a coordination and support action from the European Union’s Horizon 2020 research and innovation programme under grant agreement No 784960.

Acknowledgments

The author is indebted to the Kelso Institute for the study of economic systems to have facilitated fruitful exchange of ideas with experts in the field at the 2019 Procida Symposium. The experience from implementing the Horizon 2020 project “SCORE” had a valuable impact on the reflections in this article and publishing it open access was possible thanks to its funding.

Conflicts of Interest

The author declares no conflict of interest.

Glossary

| Autonomy of a REC | Recital 71 RED II stipulates the capability “of remaining autonomous from individual members and other traditional market actors that participate in the community as members or shareholders, or who cooperate through other means such as investment”. |

| Capital Tax Group | Corporate structure that permits to calculate profits, losses and, what is most important here, costs, for tax purposes jointly for the combined tax group. |

| Clean Energy for All Europeans Package of the European Union | A package of measures that the European Commission presented on 30 November 2016 to keep the EU competitive as the energy transition changes global energy markets; this legislative initiative has four main goals, that is, energy efficiency, global leadership in RE, a fair deal for consumers and a redesign of the internal electricity market. |

| Citizen Energy Communities (CECs) | Defined in Art. 2 (11) of the IEMD as a legal entity that “(a) is based on voluntary and open participation and is effectively controlled by members or shareholders that are natural persons, local authorities, including municipalities, or small enterprises; (b) has for its primary purpose to provide environmental, economic or social community benefits to its members or shareholders or to the local areas where it operates rather than to generate financial profits; and (c) may engage in generation, including from renewable sources, distribution, supply, consumption, aggregation, energy storage, energy efficiency services or charging services for electric vehicles or provide other energy services to its members or shareholders“. |

| Consumer Stock Ownership Plan (CSOP) | A financing technique that employs an intermediary corporate vehicle, facilitates the involvement of individual investors through a trusteeship and may use external financing, thereby achieving the benefit of financial leverage. |

| Demonstration Projects for Innovative Technologies | Defined in Art. 2 para. 2 (x) of the IEMR as “a project demonstrating a technology as a first of its kind in the Union and representing a significant innovation that goes well beyond the state of the art”. |

| Effective control of RECs and CECs | Defined in Art. 2 pt. (56) IEMD as “rights, contracts or other means which, either separately or in combination and having regard to the considerations of fact or law involved, confer the possibility of exercising decisive influence on an undertaking, in particular by (a) ownership or the right to use all or part of the assets of an undertaking; (b) rights or contracts which confer decisive influence on the composition, voting or decisions of the organs of an undertaking”. |

| Electricity/Energy Sharing (incl. (virtual) net-metering) | Recital (46) IEMD stipulates: “Electricity sharing enables members or shareholders to be supplied with electricity from the generation installations within the community without being in direct physical proximity to the generating installation and without being behind a single metering point”. In the context of RECs, this is extended in Recital (71) and Art. 21 para. 6 to energy sharing. |

| Employee Stock Ownership Plan (ESOP) | An ESOP can use leverage and enables workers to acquire shares of their employer corporations, repaying the acquisition loan not from their wages but from the future earnings of their shares in the company. |

| Enabling Framework | Art. 22 para. 4 RED II foresees an enabling framework “to promote and facilitate the development of RECs”; furthermore, Art. 21 para. 6. foresees an enabling framework “to promote and facilitate the development of renewables self-consumption“. |

| Fiduciary Trusteeship | A fiduciary, fully fledged Trusteeship of a shareholding occurs when a shareholder (here the fiduciary entity = trustee) owns the shareholding for the account of one or more other entities (here individual consumer-shareholders = trustors) in the sense that she is entitled to the rights arising from the shareholding only in accordance with a fiduciary contract concluded with the trustors. |