1. Introduction

The European electricity market is on a straight road towards a liberalized and integrated European market: full integration of the day-ahead European market has already been implemented [

1] while clear roadmaps are defined for the integration of the intra-day [

2] and balancing markets [

3]. The main goals of this process are: (i) maximizing social welfare; (ii) optimally integrating renewable energy sources; (iii) maximizing cross-border trade opportunities; (iv) providing competitive energy prices [

4]. To identify the optimal market clearing solution for these markets, complex optimization algorithms are used, e.g., [

5,

6] for the day-ahead market or [

7] for the intra-day market.

This work focuses on the first level of the European energy market, i.e., in the day-ahead market which is a zonal market: the European transmission network is divided into several bidding zones that integrate, in a simplified manner, the relevant transmission constraints in the day-ahead market clearing algorithm, limiting the possibility of significant incompatibilities between generation schedules resulting from the market and the real-time system security, which, if present, could lead to gaming opportunities for the market participants. Thus, the bidding zones are areas of the transmission network within which the market actors can exchange energy unconstrainted by the transmission network, while the energy transferred between these areas is limited to the available capacity evaluated using methodologies specified by the CACM.

Therefore, within European energy markets the transmission grid is represented through bidding zones connected by equivalent interconnectors where the energy flow is limited by the available transmission capacity. In these circumstances, the market clearing solution is strongly influenced by the congestion of these interconnectors [

5,

6,

7] leading to the conclusion that the bidding zone review process is an important activity where network operation security, market efficiency and the bidding zone’s stability and robustness requirements must be properly balanced. While the security criteria could be inclined to point towards more granular bidding zone configurations, market efficiency and or stability/robustness requirements could favor configurations characterized by a reduced number of geographically large bidding zones.

Consequently, CACM established a monitoring procedure to continuously verify the ability of the bidding zone configuration presently used by the market to meet the above-mentioned goals: the European Network of Transmission System Operators for Electricity (Entso-E) publishes a technical document every three years reporting the congestions registered in the investigated period and their related costs to the transmission grid [

8], while the Agency for the Cooperation of Energy Regulators (ACER) publishes a Market Monitoring Report [

9], where market efficiency issues are evaluated.

If these monitoring activities find potential issues, a bidding zone configuration review process is activated. On the other hand, the process could also be initiated by transmission system operators (TSOs) or national regulators if it is thought that improvements are possible within the geographic area of their competence. Last, but not the least, it should be mentioned that the CEP regulation requires the initiation of a bidding zones configuration review process at European level right after its approval (the process is currently ongoing).

One of the key components of a bidding zone configuration review process is the definition of alternative configurations and their evaluation against the current one. For this purpose, two approaches can be adopted: (i) expert-based, that exploits the transmission network operation knowledge of the TSO, its experience, as well as on some statistical information built on actual data and/or future scenarios evaluation, and (ii), model-based, that uses specially designed mathematical models to support the TSO. In general, the model-based approaches consist of the following steps: (i) determining, by employing a complete model of the transmission network, electric grid-specific indicators related to optimal electricity market clearing and (ii) passing them as inputs to specially tailored clustering algorithms that identify the bidding zones as consistent areas of the electric grid where the specified indicators present similar values. Clearly, since a bidding zone configuration must be stable over time and over a realistic range of network operating conditions, the clustering algorithms must process a significant number of network operating conditions cases so that the identified bidding zone configuration reflects consistent over time network indicator patterns. The focus of the current work is on the first step.

Work reported in [

10,

11,

12,

13] performs a critical literature review regarding the model-based indicators, the mathematical models used to determine them and the clustering algorithms used to determine the zonal structure of transmission networks for electricity markets. A few important conclusions can be derived. In general, the most used indicators are the locational marginal price (LMP), which is defined as the marginal energy price of a bus of the electric network according to the solution of a nodal market clearing algorithm, and the power transmission distribution factor (PTDF) which is defined as the sensitivity of the variation in the power flow through a branch of the network to variations in the nodal injected power at a considered bus. To calculate these indicators, nodal market models where the electric grid is represented in detail are used. This is a very important aspect as precise identification of network congestions can only be performed on a complete model of the transmission network. Here, in general, the literature review identifies the use of DC power flow (DC PF) models to represent the grid, and the adoption of only the N security criterion, i.e., network elements outages are not explicitly considered when network indicators are calculated for the identification of alternative bidding zone configurations. The DC PF model is an approximation that neglects voltage and reactive power from the network model and, in general, this approximation is considered reasonable for HV transmission networks. However, adopting only the N security criterion is a critical aspect as, often, the unexpected outage of network elements leads to congestion of the electric branches in the grid. In practice, the N-1 security criterion, preventive or corrective, involving one network element outage (branch, generator) is adopted. Indeed, the regulators and/or the TSOs require that the electricity market is solved such that the N-1 security criterion is satisfied by the market clearing solution. For example, at European level the day-ahead and intra-day electricity market uses two approaches to manage the intra-zone flows, both specified by the CACM and both considering the N-1 security criterion: (i) the available transfer capacity (ATC) approach where the net transfer capacities on the equivalent interconnectors between two neighboring bidding zones need to include the effect of the outage of a critical network element (see Article 21 of Commission Regulation (EU) 2015/1222 of 24 July 2015) or (ii) the flow-based approach where the flows related to the set of critical branch–critical outages of main intra-zone interconnectors is explicitly considered in the market clearing algorithm through approximated linear equations for central western European countries [

14].

However, in the forementioned literature review, checked for updates by the authors, a few papers indirectly consider the N-1 security criterion, while most of them do not, when it comes to the calculation of network indicators. Breuer et al. [

15] models the optimization problem that calculates the LMPs with only the N security criterion, therefore only limiting the branch currents to their corresponding thermal limits. The N-1 security criterion is considered only through an economic evaluation of the corrective actions needed to mitigate the congestions in case of outages. However, the paper does not consider the length of the short-term thermal limit violation in case of outages: the violation could be so high that the congested line is tripped before corrective actions can be determined and applied. As a consequence, the network could go into cascading trips that would lead to blackouts. Bjorndal et al. [

16] limit in N security operating conditions the total flow over sets of critical lines with the goal to prevent the overloading of one of these lines in case of outage of another. But the calculation of the sets power flow limits is very network specific and relies heavily on the TSO experience. Hence, it may not be generally applicable, especially if network expansion scenarios are to be considered, and it tends to be more of an expert-based approach rather than a model-based approach. Finally, another approach is to apply the N security criterion but reduce the limits of branch power flows by a percentage of the thermal limit hoping that a tighter N security limit would guarantee the satisfaction of N-1 security criterion [

17,

18,

19] Thus, Breuer et al. [

17] set the branch flow limit to 70% of the thermal limit, Burstedde [

18] to 80% and Felling et al. [

19] to 85%. However, there is no clear theoretical support for these values as it is not proven any of them could completely satisfy the N-1 security criteria.

Even though the N-1 security criteria has not yet been included in the mathematic models that calculates network indicators for identification of alternative bidding zone configurations, it has however been considered in the literature when solving various security constraint optimal power flow problems (SCOPF). The major difficulty of the SCOPF is its high dimensionality, especially for large systems: solving the problem directly for a large power system by imposing simultaneously all N-1 constraints, would lead to prohibitive memory and CPU time requirements. Moreover, as in real life applications most contingencies do not constrain the optimum, including them all into the SCOPF problem increases the complexity of the computations by shrinking the feasible region, and can lead to algorithmic/numerical problems. This is especially true under stressed operating conditions, i.e., when the SCOPF is most useful. Besides adopting various contingency filtering techniques [

20], which are generally used in all works since the seminal work of Monticelli et al. [

21], Benders decomposition (BD) [

22] has been widely used to solve various SCOPF problems. Just to name a few noteworthy contributions, Monticelli et al. [

21] focused on the optimal scheduling of the post-contingency corrective actions and use the DC PF to model the network, Yamin et al. [

23] propose a linearized power flow model that include both congestion mitigation and voltage security in electricity market model, while Capitanescu et al. [

20] solve a typical AC SCOPF also using BD. The BD approach decomposes the original SCOPF problem into a master and several slave problems that interact iteratively. It is very attractive approach as it can keep the size of the decomposed problems tractable as well as for potential use with parallel computations. On the other hand, BD solutions can still preserve a certain degree of infeasibility [

23] and (theoretically) BD requires the convexity of the feasible region which cannot be guaranteed in AC SCOPF models [

20]. Other approaches, like [

24,

25,

26] formulate SCOPF models that include all network equations for the normal operating conditions and for all considered contingencies. Even for a small set of carefully filtered contingencies such an approach would generate a large size optimization model, possibly non-tractable, in case of large, realistic, transmission networks. In fact, the mentioned papers test only very small power systems. Finally, Lin et al. [

27] use a standard OPF model consisting of only the constraints written for the normal operating conditions, while the N-1 operating conditions are indirectly present in the optimization model through iterative update of the normal operating conditions bounds. The approach could be promising but it does not consider the corrective actions and relies on postulating, without proof, the “coherence of steady-state with post-contingency” forgetting that some control resources (like synchronous generators) may change their behavior discreetly between steady-state and post-contingency (like generators go from PV to PQ) making the stated coherence hard to believe.

In this paper an optimization problem in the form of optimal power flow (OPF) is proposed for the computation of network indicators for identification of alternative bidding zone configurations. The optimization problem is characterized by a proper representation of the critical aspects related to the actual electric grid operation, such as the explicit N-1 security criterion, with the integration of exceptional contingencies [

28], like the double circuits line trips, and with the integration of both preventive and curative remedial actions to guarantee the security. The integration consists in formulating an optimization problem that includes, in compact form, all contingency-related constraints without using decomposition techniques and by avoiding the formulation of all technical and operational constraints for each contingency within the model using proper sensitivities. Thus, a compact and robust optimization problem results that can be applied on large-scale test systems. In fact, the proposed optimization problem is evaluated using an actual model and operating conditions of the Italian transmission system and its advantages are shown.

It should be mentioned that the work presented here is an extension of [

29] where the basic algorithm is presented and it is shown that, for the Italian transmission system, the LMP patterns calculated by the algorithm (and, therefore, the corresponding congestions that determined them) for various snapshots of the 2018 Italian network data, present a correlation with the 2018 Italian market bidding zones configuration and that other known situation (like Italian NORD, or Sicily area inner congestions) can be detected. Therefore, the proposed approach can provide clustering algorithms with realistic data. Instead, the current work further develops the model by maturing (i) the identification procedure of critical contingencies, (ii) the solution for the management of the double line trips and (iii) the calculation of network indicators, including the PTDFs. However, the main contribution of the paper consists in extending the numerical analysis of the results: the entire range of considered snapshots (cases) and simulation scenarios (including comparison with the commonly encountered approach in literature when it comes to the calculation of network indicators for bidding zone configuration) is analyzed and the advantages of proposed approach are emphasized. Additionally, considerations about PTDFs as network indicators are also included. Moreover, a small network case was analyzed to prove the correctness of the proposed approach and the numerical performance of the proposed approach are shown.

Therefore, the goal of the current work is to develop a model for the calculation of network indicators to be used in a model-based definition of bidding zone configuration (first step of the process). The outputs of this work can be taken over by other works where the indicators here-calculated are processed by especially tailored clustering algorithms to identify alternative bidding zone configurations. For example, by paper [

30] that considers only the LMPs, and by paper [

31] which also considers the PTDFs.

2. Proposed Optimization Model

2.1. Optimization Problem Definition

A model-based methodology for alternative bidding zone configurations must be designed using computational models that include, among others: (i) a complete representation of the transmission network that considers explicitly all relevant security standards (contingency analysis, operational limits, etc.) and (ii) a detailed representation of the market rules (production costs, market bids, etc.). This requires the adoption of an advanced market model in which the electric grid is accurately represented: an optimal power flow (OPF) problem that integrates network security and market rules related constraints.

2.2. Objective Function and N Security Constraints

The generating units real power outputs are modeled using market bids defined according to the rules of the Italian day-ahead market [

32] which allows the definition of up to three price–quantity pairs representing the economic bids for each production or consumption unit. Here, the proposed optimization problem is solved using historical data and thus the market clearing point is already available. Thus, for simplification, the demand is fixed to the quantity given by actual conditions. However, the model can be easily extended to consider variable demand using the same type of equations employed for the supply side and correctly considering the sign of the demand power. The goal of the optimization problem is the maximization the social welfare that, considering the demand is fixed, can be defined as the minimization of the total costs of generation acceptance:

where

is the set of generating units;

is the set of supply bids;

are the offered energy prices;

are the accepted supply quantities for each

m step of supply bid pertaining to

kth generating unit. Variables

are positive and upper bounded by the submitted quantities. The generators real power output is:

Looking at Equation (2), it should be mentioned that the continuity of the generated power is guaranteed by the convexity requirements of the bids specified by the market rules [

32] which paired with the minimization of (1) ensure the sequential acceptance, according to economic merit order, of the offered quantities.

The constraints of the optimization model are given by equations that model the transmission network operation constraints. The normal operating conditions are given by the DC PF model:

where

is the vector of real power injections into network buses calculated as the difference between the nodal generation and demand;

is the bus admittance matrix of the DC PF method;

is the bus to phase-shifting transformers (PST) admittance matrix;

is the unknowns vector of the bus voltage angles (excluding the slack bus angle that is fixed to zero) and

is the unknowns vector of PSTs angles. At this point, it should be noted that in order to distinguish between vector and scalar quantities, bold notation is used for the former.

The real power flows in the branches of the electric grid,

, are:

where

and

are the branch-to-nodes and branch-to-PSTs admittance matrices, respectively.

According to the N security criterion, these flows are limited in upwards and downwards directions by the maximum flow limits corresponding to the thermal limits of the network’s branches:

where

is the vector containing the maximum power flow allowed through the network’s branches, in general coinciding with the long-term thermal limit of the branch.

The generator’s and PST’s capability constraints are:

where

is the vector containing the real power produced by all the generators in the grid, i.e., the vector containing

,

;

and

are the vectors of lower and upper bounds for generator’s real powers production, respectively;

and

are the vectors of lower and upper bounds of the PST angles, respectively.

2.3. The N-1 Security–Preventive Criterion Constraints

The N-1 preventive security criterion assumes that following a network element outage (branch or generator) there is not enough time available to calculate and apply corrective actions that would solve potential resulting congestions; therefore, in these operating conditions the normal network operating constraints have to be satisfied.

2.3.1. Network Branch Outage

The impact of branch

b outage on the real power flowing in branch

a is evaluated using the Linear Outage Distribution Factors, i.e.,

, described by Enns et al. in [

33]. Thus, the resulting N-1 preventive security constraints are given by:

Equation (8) is defined for all (

a,

b) pairs that are critical for the considered network. In Equation (8),

and

are unknown vectors of branches real power flows, i.e., elements of

, defined according to the considered set of (

a,

b) pairs: the

nth element of

and the

nth element of

represent the

nth (

a,

b) pair. Parameter vector

contains the maximum power flow limits of the critical branches

a, while

is a vector of user-defined coefficients to properly scale vector

. If the preventive security criterion is adopted, then all elements of

vector are equal to 1; if the corrective security criterion is adopted, then the elements of

vector can be greater than 1 to allow temporary overload before corrective actions are applied, where the short-term thermal limits allow it, as will be explained in

Section 2.4.

2.3.2. Generator Outage

The generation real power profile automatically changes at the outage of the

kth generator due to the primary frequency regulation actions. Thus, for the

mth generator participating in primary frequency regulation the variation of its real power output at the outage of the

kth generator is:

where

is the regulating energy associated to primary frequency regulation of the

th generator. It is calculated as:

where

is the maximum real power limit of

mth generator (

mth element of parameter vector

) in MW;

is the statism of

mth generator in p.u. while

is the nominal frequency of the network in Hz.

Considering all generators, the real power change due to primary frequency regulation at the outage of

kth generator is quantified by vector

that includes all the

elements, except for the slack generator which, according to the DC PF model, automatically adjusts its power variation. Finally, these power changes need not to violate generating units’ capability constraints:

The power flow in each branch considering the generation real power output following the outage of

kth generator is determined by introducing the next constraints:

where

is a vector of user-defined coefficients to scale

(same logic as with the previously defined

), while

represents the variation of the power flow at branch

a, linking node

i to

j, due to the outage of the

kth generator:

where

are the

ith and

jth rows of the inverse of

.

Equation (11) represents the capability limits of the remaining generators following the outage of the kth generator. Equation (12) limits the branch power flows following the outage of the kth generator to the defined limits. To limit the dimensions of the optimization problem, Equations (10) and (11) are considered only for the (a, k) pairs that are critical to the network, i.e., for the kth generators of which outages could congest branches a. Thus, the size of (11a) is equal to the number of outage generators, the size of (11b) and (12) is equal to the number of critical (a, k) pairs.

2.4. The N-1 Security-Corrective Criterion Constraints

According to the N-1 security-corrective criterion, in case of single line/generator outage, a current violation is allowed if it is within appropriate limits (typically 120% of the permanent thermal limit) and it is possible to identify and apply remedial actions (generation re-dispatch) within a short time (about 30 min) to mitigate the violation.

Figure 1 illustrates these operating conditions by showing the time evolution of the value of the current in a generic branch of the network considering the outage of another network element. As can be seen, satisfying the N-1 corrective security criterion involves three stages of time:

- (i)

first, before the outage (N operating conditions), the maximum current limit for the considered generic branch is not reached—the network satisfies the N security criterion;

- (ii)

an outage occurs and the current in the considered generic branch increases as a consequence but without violating the relaxed current limit (the short-term thermal limit)—the network satisfies a relaxed/equivalent N-1 preventive security criterion. The value of the current is contained enough to allow the operation of the considered generic branch for a short period of time, time necessary to determine the optimal corrective actions necessary to solve the congestion;

- (iii)

the corrective actions are applied and the current in the considered generic line is again bellow its maximum—the congestion has been solved and the network now satisfies the N-1 corrective security criterion.

The three stages shown in

Figure 1 need to be represented through adequate constraints in the considered optimization problem. The first stage is already modeled by constraints (5)–(7) which assure network security in N operating conditions. The second stage operating constraints is guaranteed by constraints (8)–(13) through a proper setting of the

and

parameters, i.e., to values that represent the short-term thermal limit of the branches. Therefore, only the calculation of the corrective actions and their effect (stage three) need to be mathematically formulated.

2.4.1. Network Branch Outage

The change in the power flow in branch

a introduced by the application of corrective actions in case of outage of branch

b,

, can be determined using sensitivities obtained from the DC PF model. Thus:

where

is the vector of

variables for all the considered

pairs;

is a sensitivity matrix expressing the variation of the flow in branch

a at the variation of the generators real power profile, while

is the vector of corrective redispatch actions of the generating units. Here, matrix

is obtained like the linear coefficients of Equation (13) with the difference that

are now the

ith and

jth rows of the inverse of

, i.e., the bus admittance matrix obtained considering the outage of branch

a.

Thus, the branch flows after the branch

a outage and application of corrective actions, are constrained by:

where

is a user-defined vector of coefficients introduced in analogy with the other scaling coefficients, e.g.,

, to scale

; if no particular requirements are in place, then all elements of

are 1, in agreement with what was explained previously. In Equation (15) the equivalent preventive and corrective steps of the N-1 security-corrective criterion (second and third stages in

Figure 1) are in superposition: this is allowed by the linearity of the DC PF model. The corrective actions need to comply with the generator’s capabilities:

where

and

are vectors quantifying the ramp-up and -down generator limits, respectively.

2.4.2. Generator Outage

As with the case of branch outage, the case of generator outage is also necessary to model the corrective actions and their impact on the branches’ power flow. The variation of the power flow in branch

a at the application of the corrective actions following the outage of generator

k,

, is quantified using the same approach as in (14):

where

is the vector of

variables for all the considered

pairs;

is a sensitivity matrix that expresses the variation of the flow in branch

a at the variation of the generators real power profile, while

is the vector of corrective redispatch actions of the generating units. Matrix

is obtained as the linear coefficients of Equation (12) and, since the network topology does not vary when generator outages occur, then it remains invariant no matter the outage.

Thus, the branch flow constraints following the outage of generator

k and the application of the corrective actions, for all the considered

pairs, are given by the following equation:

where

is a user-defined vector of coefficients introduced in analogy with the other scaling coefficients, e.g.,

, to scale

; if no particular requirements are in place, then all elements of

are 1, in agreement with what was explained in previous section. In Equation (17), similarly to Equation (14), the equivalent preventive and corrective steps of the N-1 security-corrective criterion are in superposition. The corrective actions need to be also constrained by the generators’ capabilities:

2.5. Constraints on Critical Sections

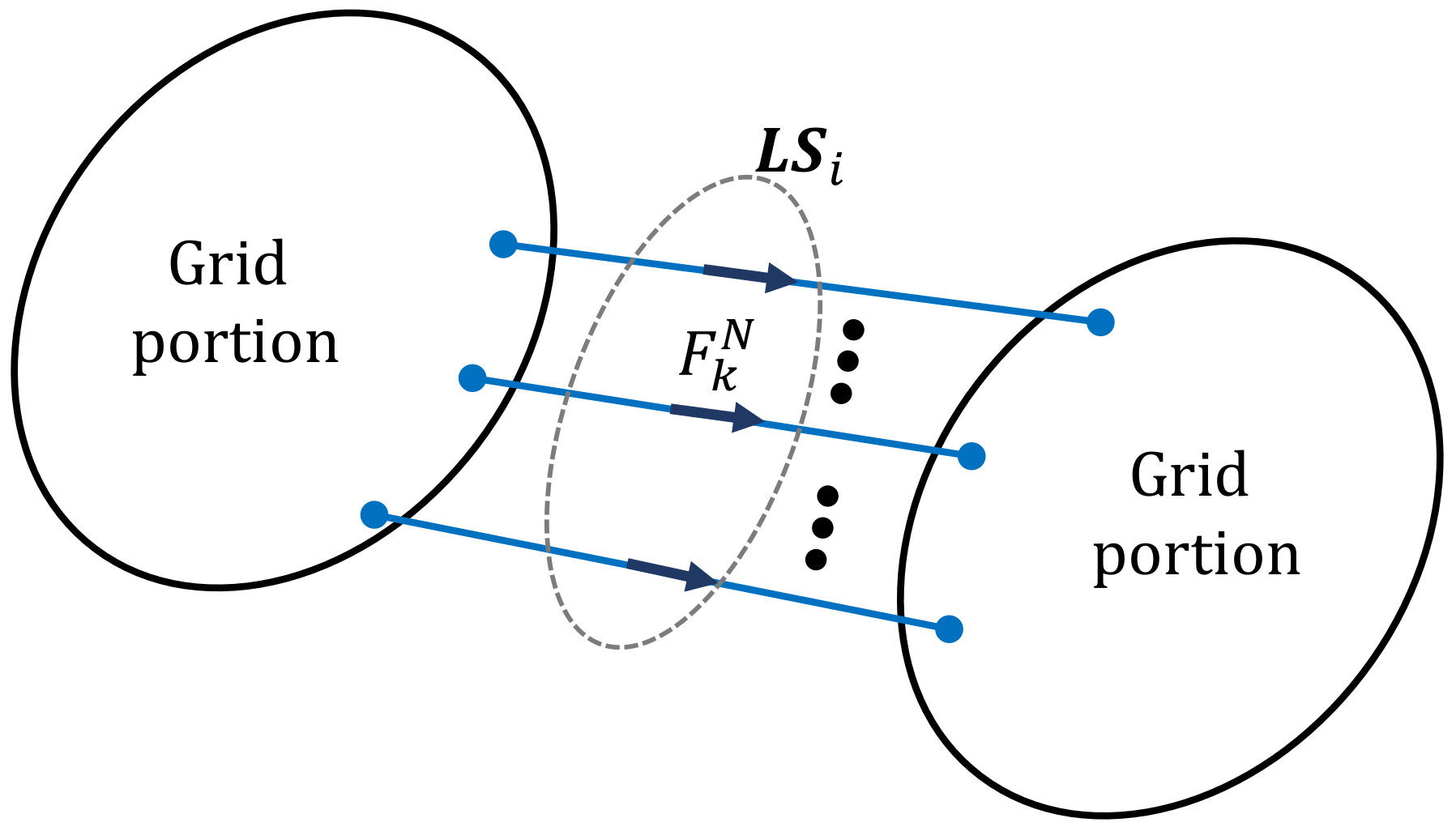

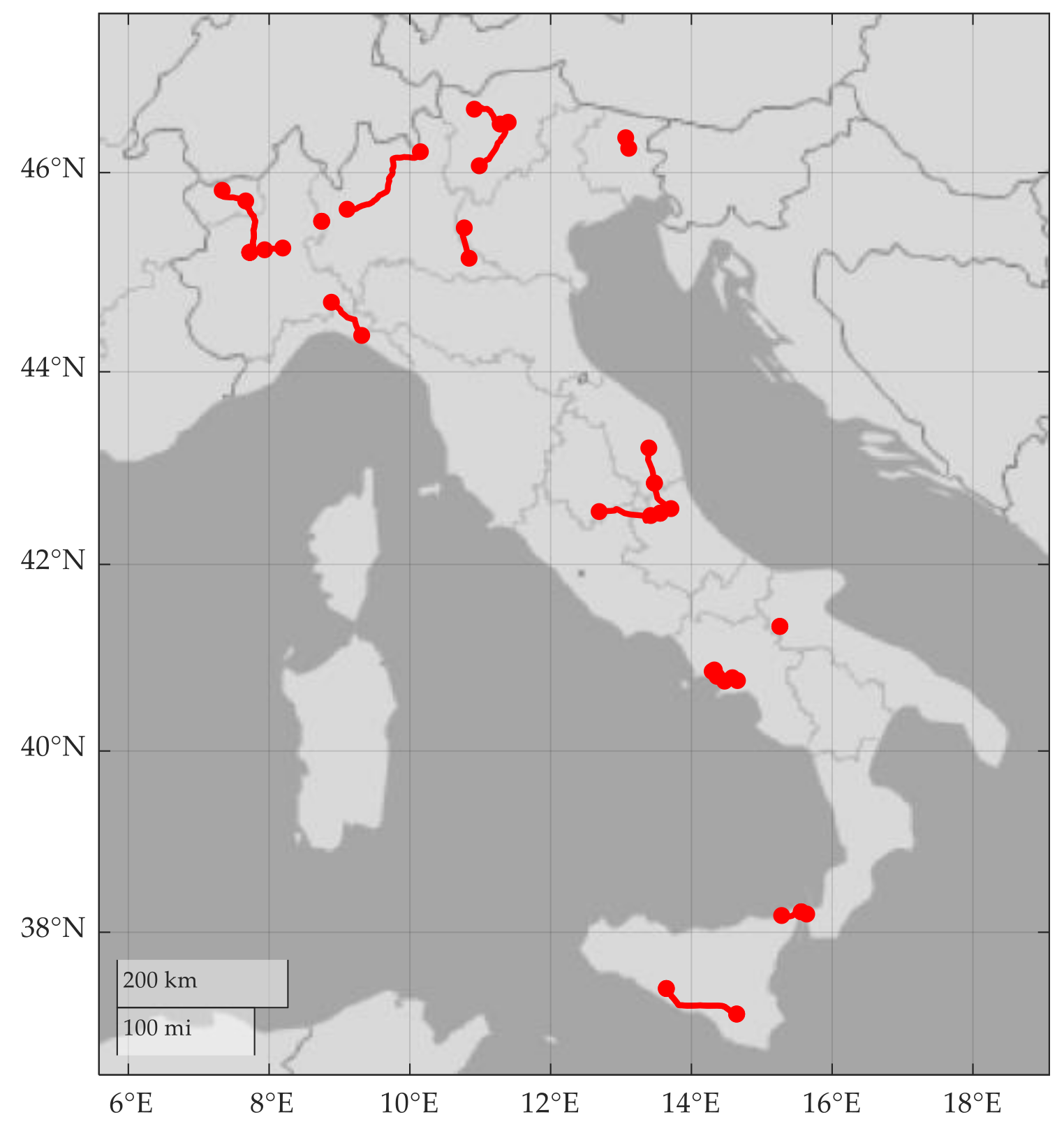

In actual network operation it is possible that some portions of the grid are weakly meshed or there is a scarcity of control resources available and, as consequence, high power (current) flows through some sections of the grid introducing high voltage drops that are difficult to manage. For these cases, the DC PF model is not able to directly assess the potential voltage problems: maximum flow constraints on some network interfaces (set of network branches connecting various portions of the electric grid) are introduced:

where

is the set of branches included in the critical section

i (see

Figure 2);

is the set of critical sections, with

;

and

are the maximum and minimum power flow limits on the critical section

i, respectively; they can be obtained from off-line network studies.

2.6. Definition of the Critical Branches–Critical Outages Sets

The defined DC OPF problem is characterized by a high sparsity index as it relies on a complete approach, unlike the compact models: the equations that guarantee the power balance of the system represent the entire set of power flow equations. Compared to compact models, this defined model uses a much larger number of variables and equations, but, at the same time, due to its sparsity can easily be solved by linear, large-scale, optimization solvers. However, this does not mean that it is not important to contain, as much as possible, the size of the optimization problem (the number of variables and number of constraints): the smaller it becomes, the faster it is solved. A key role in the proposed optimization problem is played by the equations modelling the security criteria: without any intervention there should be (i) as many equation sets as there are branches in the network for N security conditions and, (ii) as many (a, b) and (a, k) pairs as the network topology and number of generators allows for N-1 security conditions. This, for a real network, would result in an extremely large number of variables and constraints, impossible to be dealt with even by the best performing optimization solvers. Therefore, it is necessary to minimize the set of branches constrained in N security conditions and for the (a, b) and (a, k) pairs to be constrained in N-1 security conditions. The following iterative procedure consisting in the sequential update of the set and finding the solution to the DC OPF problem, is adopted:

- Step 0

consider an initial generation real power production profile and set the iteration counter to iter = 1; consider the set of critical branches in N security conditions, i.e., the set used to formulate constraints (5), null; consider the set of critical (a, b) and (a, k) pairs, i.e., the sets used to formulate the constraints of the DC OPF model, null;

- Step 1

calculate sensitivities and the constant coefficient terms of Equation (11) for all the (a, b) and (a, k) pairs. Since the DC PF model is sparse and linear this calculation is very fast;

- Step 2

compute the DC PF solution using the generation real power production profile at iteration iter in N operating conditions;

- Step 3

Update the set of critical branches in N security conditions by adding the new branches for which:

while keeping the already present branches in the set.

In Equation (21) is a user-defined parameter; for this paper, its value has been set to 0.7, a value that allows a reduced number of iterations without losing any critical branches from inclusion in the set.

- Step 4

Update the set of critical (

a,

b) pairs by adding the new branches for which:

with

and

being user-defined parameters.

Basically, a pair (a, b) should be included in the optimization problem if the outage of b brings the power flow in branch a above a critical threshold quantified by parameter in Equation (22a), with being lower than 1. However, this can be too constrained for low values of where there is the risk of including branches with low values of initial power flow that see small variations in their power flow due to outage of b, therefore are not actually critical. Alternatively, it can be too relaxed for high values of where there is the risk to omit branches that see a large variation in their power flow due to outage of b but don’t violate the high values of , therefore branches that are actually critical. To mitigate these flaws condition (22b) is also introduced: if the threshold given by is reached then it means that outage of b has significant impact on power flow in branch a. After extensive preliminary studies, it was found that three pairs of (, ) values are sufficient to detect all critical (a, b) pairs: (, ) = {(0.2, 0.7), (0.1, 0.9), (0.01, 0.99)}. If an (a, b) pair satisfies (22) for at least one (, ) pair of values, then it should be included in the optimization problem. Clearly, the last pair value, i.e., (0.01, 0.99) is the most conservative and it should detect, by itself, all critical (a, b) pairs or, in other words, all congested branches a following the outage of branches b. However, the optimal solution changes with the update of the (a, b) set and there is the risk of performing too many iterations due to previously not detected (a, b) pairs. To mitigate this, the set of (a, b) pairs is broadened by also adopting softer values for (, ) values.

As in the previous step, the already present (a, b) pairs are maintained in the set;

- Step 5

Update the set of critical (

a,

k) pairs by adding the new branches for which:

Basically, a pair (a, k) is included in the optimization problem if the outage of k has significant impact on a, (23a) and if it brings the power flow in a into a critical region, (23b). As in the previous step, the already present (a, k) pairs are maintained in the set;

- Step 6

If the sets of critical branches in N security conditions and the sets of critical (a, b) and (a, k) pairs at iteration iter are the same as in the previous iteration, iter-1, then STOP.

- Step 7

find the DC OPF solution; update the iteration index iter = iter + 1 and go to Step 2.

2.7. Calculation of Network Indicators

Starting from the results of the OPF, the electric grid indicators related to optimal electricity market clearing can be calculated and employed by clustering algorithms to propose alternative bidding zones configurations. Taking into account [

10,

11], two different indicators are considered: the locational marginal prices (LMPs) and the power transfer distribution factors (PTDFs).

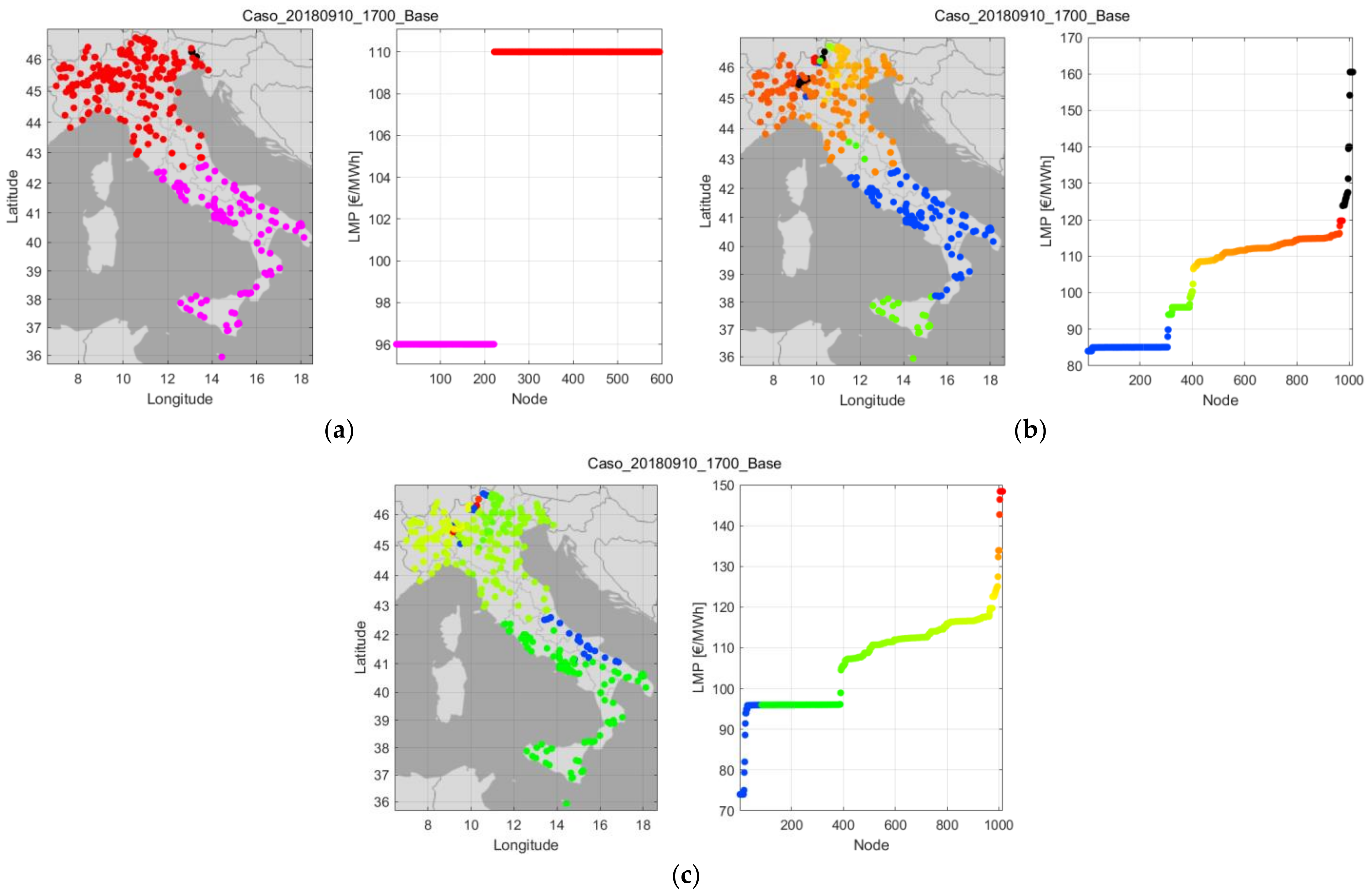

The LMPs are the nodal marginal electricity prices and are calculated, in general, using the Lagrange multipliers of the constraints of the OPF problem. In this paper, the LMPs are computed starting from the solution provided by the proposed DC OPF model where the security criteria are modelled explicitly. In this way, the LMPs reflect the adopted hypotheses and therefore reflect both the technical requirements of power system operation and the energy market efficiency requirements and its rules. In particular, they are equal to the Lagrangian multipliers of the power flow equations in normal operating conditions (3): these constraints quantify the nodal power balance and, therefore, the Lagrangian multipliers of these constraints quantify the variation of the objective function (total cost of generation) at a change of a parameter in these equations (e.g., nodal demand variation), therefore they represent the nodal marginal price of energy according to the market clearing solution. Moreover, Equation (3) determines the vectors of independent variables , which, in turn, determine the power flows through the branches . The latter variables are subject also to the N-1 security criteria constraints of the model and, therefore, the LMPs values are implicitly influenced by the security related constraints when they are activated.

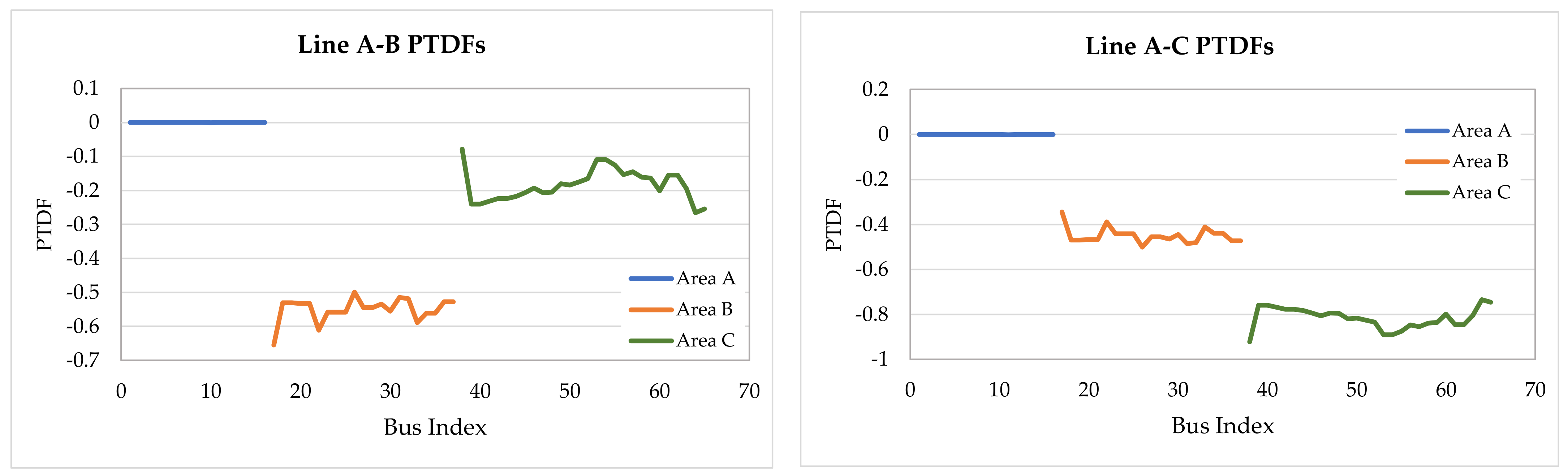

In general, the PTDFs are defined as the sensitivity of the power flow variation in a branch of the network at the variation of a bus power injection [

10]. To calculate the PTDF of a generic branch

k connecting bus

i to bus

j one needs to first consider the expressions of the power flows in the branch. For the DC PF model, only the real power flow in the branch,

, can be calculated as:

where

is the reactance of branch

k.

According to the DC PF model (3) and in the absence of the PST angles, the vector of voltage angles

can be expressed as:

where

is the inverse of

.

Now, (26) includes the nodal power injections in vector

. Therefore, the variation of the flow in branch

k at the variation of the nodal power injection at bus

p, i.e., the PTDF of branch

k at the variation of the nodal power at bus

p, can be calculated as:

where

and

are the

ip and

jp elements of matrix

, respectively.

Looking at (27) it is now clear why the PST angles have been neglected from the beginning: if considered, according to (3) the same results of (27) would have been obtained since the flow of (26) would have resulted in a linear combination between nodal power injections and the PST angles and therefore, the derivative would have resulted null for the PST angles terms, in any case.

It is interesting to note that (27) is invariant with respect to the network operating conditions (the values of

,

,

) but it depends strictly on the network topology and parameters. In these conditions the PTDFs do not depend on the results of the proposed optimization problem therefore, they could be calculated for the entire grid. However, the solution of the proposed optimization problem is very important because besides providing the LMPs, it also provides the set of congested lines (i.e., the set of branches for which the flow bounds are activated either in N or N-1 security conditions): the PTDFs of the identified congested branches can therefore be extracted and used as network indicators to provide the clustering algorithms with important topological data. In details, for a given congested branch, the buses with similar PTDFs are the buses that can influence similarly the power flow in the congested branch and therefore, if topologically coherent, could form a bidding zone, or constitute part of a bigger one. Paper [

31] explains in detail how the PTDFs can be used for the definition of bidding zones.

2.8. Strategies to Enforce the Robustness of the Optimization Problem

In general, if the DC OPF problem is infeasible and a solution cannot be found, then the iterative procedure defined in the previous subsection halts without the satisfaction of the stopping criterion. Various numerical tests have shown this situation to occur when a branch outage leaves a portion of the grid in radial configuration characterized only by demand buses, as shown in

Figure 3. In this situation, the demand may require more power than the limits of the radially connected branches allow and, since the demand is not controllable by the optimization, the DC OPF model will diverge due to the impossibility of satisfying constraints (8). This situation is a consequence of a simplified network model adopted that does not represent the 150 kV grid (it includes the 380/220 kV grid) which, in case of occurrence of the considered outage would be able to supply the demand, and/or of the DC PF model simplifying hypothesis, in particular the fact that the nodal voltage magnitude is considered equal to 1 p.u.; if the AC PF model were adopted, a lower nodal voltage profile would determine lower currents and, hence, the possibility to satisfy the branch current constraints.

To mitigate this situation, a pair of fictitious generators are considered at specific buses in the grid: one that can produce between −1000 MW and 0 MW and offered at a very low and negative price, and another that can produce between 0 MW and +1000 MW and offered at a very high positive price. These prices have been set at −3000 €/MWh, and +3000 €/MWh (the cap limit of the Italian market bids [

32]), respectively. Moreover, these generators are dispatched only to provide corrective actions and therefore, for them,

,

is dispatchable and penalized by the fictious prices in the objective function. Thus, since they have very high prices, they are characterized by the lowest dispatch priority among all generators and, thus, they will be accepted only if necessary, i.e., to satisfy the N-1 security constraints.

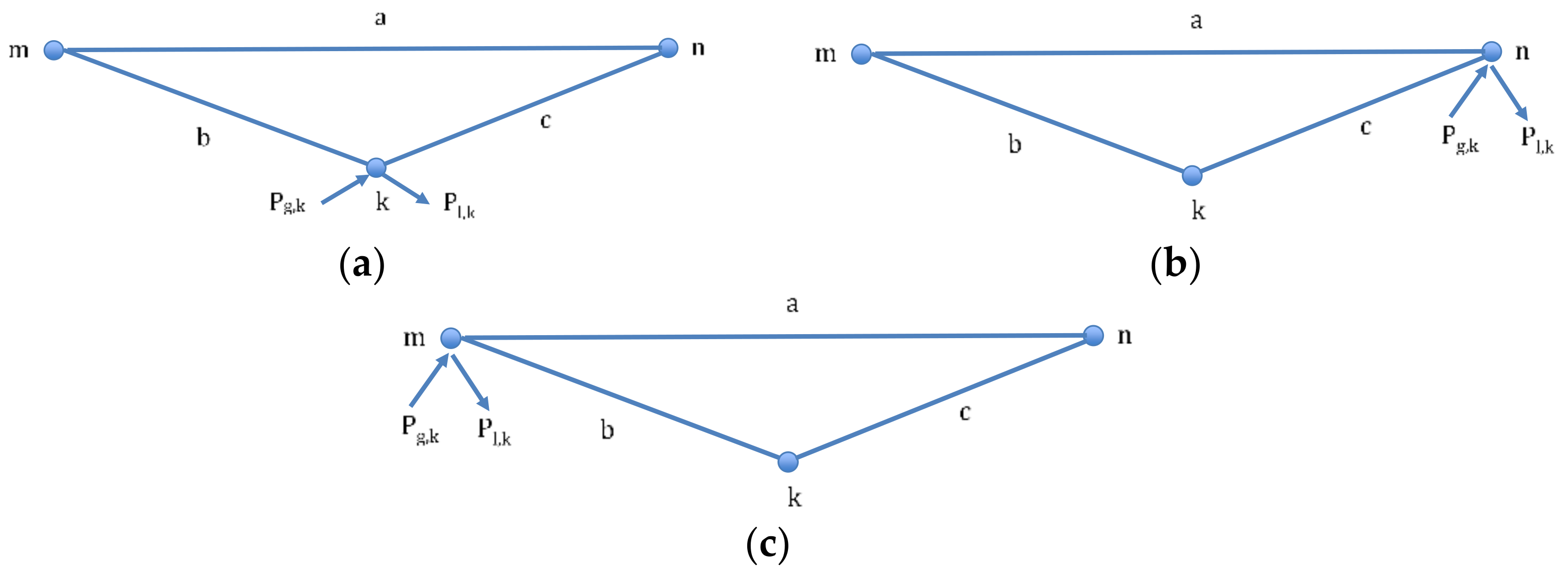

2.9. Modelling of Multiple Line Outages

Some network operating conditions involve the simultaneous loss of two or more transmission branches. This is the case of electric lines that share, partially or fully, the same sustaining pillars: an outage due to damage at a sustaining pillar will outage all the involved electric lines. In general, there are no more than two electric lines involved, therefore this case is going to be further considered. In the case the share of sustaining pillars is full then the two lines are perfectly connected in parallel: the double outage is immediately implemented by modifying the network model and replacing the double lines with a single connection consisting of the parallel of the two.

In case of partial share of sustaining pillars, the situation is more complex because one of the ends of the two lines is not the same. These situations are illustrated in

Figure 4 where the double outage is made of either outage (

a,

b) or (

a,

c). This situation is managed by adapting the network model and moving the electrical demand and generation production present at bus

k into buses

n or

m depending on whether the double outage regards branches (

a,

b) or branches (

a,

c), as illustrated in

Figure 4a,b, respectively. For both cases, this allows to consider the equivalent branch made of the parallel of

a with the series of

b +

c and then simulate the double outage as the outage of the equivalent branch. It should be noted that this approach is able to model the effects of the double line trip only for the part of the grid outside ring (

a,

b,

c). However, the approximation is found reasonable since the actual double line trip leaves bus

k radially connected to the external grid and the nodal power of bus k is, in general, contained.

4. Concluding Remarks

This paper proposes an optimization model that integrates both electricity market and transmission grid security aspects. The model is formulated as a DC OPF problem and the optimal solution provided is used to compute indicators (LMPs and PTDFs) adopted in clustering algorithms to define alternative bidding zone configurations to be considered in a bidding zone review process for European electricity markets.

Unlike similar approaches in the literature, the proposed model can manage explicitly the N and the N-1 security criteria (corrective and preventive) where the transmission lines and the generating units are included in the contingency set. The proposed model has been tested on a wide set of scenarios representing relevant Italian HV transmission network operating conditions. Through the results reported, this work investigated the ability of different modelling approaches to reflect the impact of the N-1 security constraints on network congestions. Thus, the full model results (N1cor scenario) were compared against (i) the traditional approach in the literature where the N-1 security criteria are not represented explicitly but modeled by reducing the N security limits of the branches (N70 scenario) and against (ii) applying only the N-1 preventive security criterion (N1prev scenario).

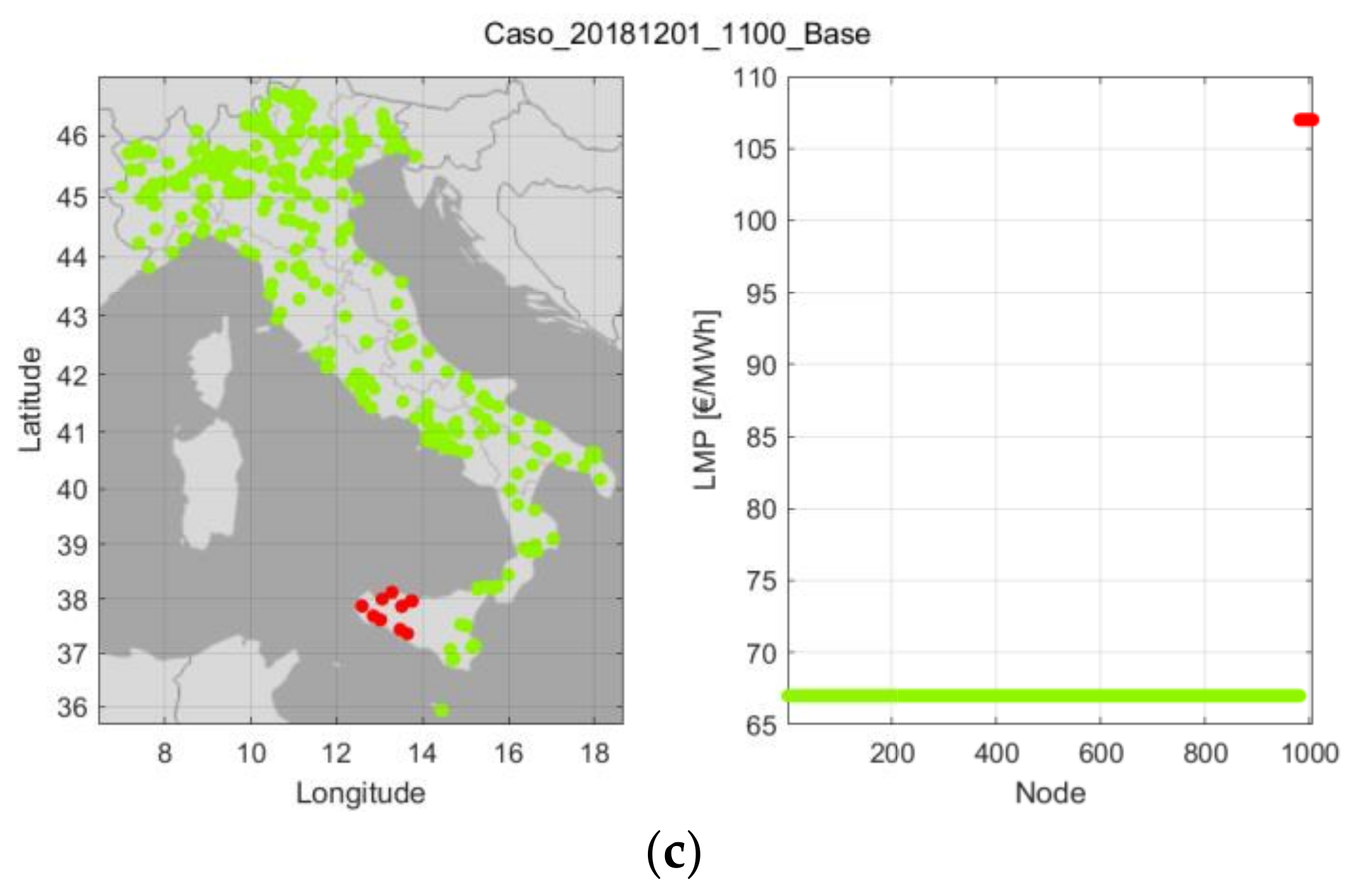

The N1cor scenario proved to offer many advantages. It identified the relevant existing congestions confirming the current bidding zone configuration used in the actual Italian day-ahead market, but also reflected well the expected issues incurred when some grid elements are put out of service (confirming the ability of the algorithm to produce reliable LMP profiles). Moreover, it also provided the best exploitation of the available transmission capacity and it provided good LMP profiles that should, in general, not force the clustering algorithms into identifying many micro bidding zones or identify, with difficulty, large bidding zones.

The N1prev scenario results showed that the relevant congestions can still be identified but this time, due to tighter limits applied in N-1 operating conditions and neglect of corrective actions, the congestions had a more limiting effect: (i) the LMPs are in general higher and characterized by increased spread, which can lead to bidding zone configurations favoring high market prices; (ii) the LMP profiles are less uniform and more localized and (iii) the available transmission capacity is less efficiently explored.

Finally, the approach generally proposed in the literature, here the N70 scenario, showed disadvantages. First, it proved not able to guarantee the N-1 security constraints for all the considered outages: in most of the scenarios, critical branches that cannot satisfy the N-1 corrective security criterion have been detected; in other words there are outages that cannot be mitigated by corrective actions since the short-term limit is violated before applying them. This could be mitigated through an iterative update of the N security limits but this would involve solving, at each iteration and outside the main problem, many sub-problems to identify potential corrective actions without considering them directly inside the main problem, but through an update of the main problem’s variable bounds. This would lead to the formulation of a problem that tries to do the same as the proposed approach but in a much more complex and indirect manner. From another point of view, the N-1 corrective security criterion violation in the N70 scenario could be acceptable if the probability of outage is introduced in the optimization model; but the N70 scenario, with respect to the proposed model, cannot explicitly manage the outages and the critical congestions. On the other hand, the N70 scenario proved, on one hand, not able to identify all significant congestions identified by the proposed model while, on the other hand, prone to increased LMP granularity, similar to the N1prev scenario. Last, but not the least, it provided the worst exploitation of the available transmission capacity.

Clearly, the proposed model in its complete version, i.e., considering the N-1 corrective security criteria, is the more reliable and realistic out of the analyzed scenarios. Moreover, it represents a significant step forward in the development of nodal market algorithms able to provide reliable network indicators. Since the process of model-based bidding zones configuration involves two steps and this work develops only the first, the network indicators calculated can be processed by second step clustering algorithms.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}