A Pattern New in Every Moment: The Temporal Clustering of Markets for Crude Oil, Refined Fuels, and Other Commodities

1

College of Law, Michigan State University, East Lansing, MI 48824, USA

2

Management Sciences, Shaheed Zulfikar Ali Bhutto Institute of Science and Technology (SZABIST), Islamabad 44000, Pakistan

*

Author to whom correspondence should be addressed.

Energies 2021, 14(19), 6099; https://0-doi-org.brum.beds.ac.uk/10.3390/en14196099

Submission received: 31 July 2021

/

Revised: 6 September 2021

/

Accepted: 15 September 2021

/

Published: 24 September 2021

(This article belongs to the Special Issue Emerging Trends in Energy Economics)

Abstract

:The identification of critical periods and business cycles contributes significantly to the analysis of financial markets and the macroeconomy. Financialization and cointegration place a premium on the accurate recognition of time-varying volatility in commodity markets, especially those for crude oil and refined fuels. This article seeks to identify critical periods in the trading of energy-related commodities as a step toward understanding the temporal dynamics of those markets. This article proposes a novel application of unsupervised machine learning. A suite of clustering methods, applied to conditional volatility forecasts by trading days and individual assets or asset classes, can identify critical periods in energy-related commodity markets. Unsupervised machine learning achieves this task without rules-based or subjective definitions of crises. Five clustering methods—affinity propagation, mean-shift, spectral, k-means, and hierarchical agglomerative clustering—can identify anomalous periods in commodities trading. These methods identified the financial crisis of 2008–2009 and the initial stages of the COVID-19 pandemic. Applied to four energy-related markets—Brent, West Texas intermediate, gasoil, and gasoline—the same methods identified additional periods connected to events such as the September 11 terrorist attacks and the 2003 Persian Gulf war. t-distributed stochastic neighbor embedding facilitates the visualization of trading regimes. Temporal clustering of conditional volatility forecasts reveals unusual financial properties that distinguish the trading of energy-related commodities during critical periods from trading during normal periods and from trade in other commodities in all periods. Whereas critical periods for all commodities appear to coincide with broader disruptions in demand for energy, critical periods unique to crude oil and refined fuels appear to arise from acute disruptions in supply. Extensions of these methods include the definition of bull and bear markets and the identification of recessions and recoveries in the real economy.

Keywords:

energy commodities; financial crises; Brent; WTI; gasoline; clustering; t-SNE; machine learning; COVID-19 pandemic

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

1. Introduction

1.1. The Motivation for this Research

Crises loom large in finance and macroeconomics. Defining transitions between bull and bear markets, or between recessions and expansions, helps identify distinctive financial or economic regimes. Commodity markets, especially those related to petroleum, undergo their own fluctuations. Indeed, abrupt and abnormal movements within these notoriously turbulent markets often signal trouble in other sectors of the broader economy. Oil price volatility, in particular, experiences structural shifts. The intense financialization of commodities, including crude oil and refined fuels, heightens the importance of identifying shifts and disruptions in volatility across time.

This article proposes a novel method for identifying critical moments in commodity markets, ranging from structural shifts to abrupt disruptions. It places special emphasis on markets for crude oil and refined fuels. Unsupervised machine learning can distinguish crises from normal conditions. It can identify anomalies within an economic time series and set those trading days apart for closer examination, as opposed to finding time time-varying effects through conventional analysis.

Recent work by the authors has demonstrated the use of clustering and manifold learning to arrange commodities into discrete markets for fuels, precious metals, base metals, and agricultural commodities by climate [1]. In an extension of that work, this article focuses more closely on the temporal domain of these markets. A suite of clustering can identify critical periods affecting all commodity markets, such as the 2008–2009 global financial crisis and the COVID-19 pandemic. These critical periods also affect markets specific to oil and refined fuels. Even closer examination reveals additional periods of special interest to energy-related markets. Most of those periods are shorter, acute supply disruptions through extreme weather or acts of war.

As between the clustering of commodities and trading days, temporal clustering poses the greater technical challenge and offers the greater practical reward. Discrete commodity markets number in the dozens. A comprehensive span of financial history can cover thousands of trading days. The configuration of commodities in metaphysical financial space need not observe a particular order. By contrast, cogent, temporally defined market regimes must represent contiguous or nearly contiguous blocs of trading days.

Certain branches of finance and macroeconomics seek to define cyclical peaks and troughs. Many conventional definitions of bull and bear markets or recessions and expansions within the broader economy, however, rely upon arbitrary benchmarks or even subjective judgment. If stock prices fall more than 20 percent from a recent peak, for instance, many analysts are prepared to declare the onset of a bear market. A 10 percent decline, by contrast, is labeled a “correction.”

Relative to these arbitrary, categorical distinctions, a mathematically informed treatment of conditional volatility forecasts may identify contiguous or nearly contiguous clusters of trading days. Although this article does not immediately pursue the possibility, the methods that it applies may ultimately enable new ways to identify distinctive regimes in financial markets or the broader economy. Though bull-and-bear market indicators and peak-and-trough definitions of the business cycle will undoubtedly persist, data-driven alternatives or complements may arise from unsupervised machine learning and related forms of artificial intelligence.

Unsupervised machine learning also obviates disputes over the definition of local maxima and minima across potentially expansive spans of financial history. These methods serve as an extended metaphor for one of the greatest challenges in machine learning and artificial intelligence: determining whether a model has been globally optimized, or whether an optimization algorithm has converged locally.

By the same token, reliance on unsupervised machine learning presents challenges unique to this set of methods. Unlike conventional regression-based methods or their equivalents within predictive applications of supervised machine learning, unsupervised methods such as clustering and manifold learning are not typically used to validate research hypotheses. They struggle to perform either of the traditional tasks in economics. Other methods outperform unsupervised machine learning in forecasting values and in enabling causal inference. What unsupervised machine learning does excel in doing, however, is revealing patterns within data itself, without reliance on labels, values, or research hypotheses formulated by human analysts.

Mindful of the potential of unsupervised machine learning, as well as its limits, this article targets questions that routinely arise in traditional research on commodities, broader financial markets, and the real economy. This article answers those questions in the narrower, more specific context of energy-related commodities. There is intense interest in comovement and connectedness among commodities trading, financial markets, and macroeconomic phenomena. These relationships are known to vary across time. At its most intriguing, time-varying conditional volatility supports hypotheses regarding cyclicality and structural shifts in many branches of economics.

This article asks whether raw data consisting of nothing more than logarithmic returns or conditional volatility forecasts can distinguish among ordinary trading days, acute crises that bend the arc of energy commodities trading sharply but only temporarily, and more enduring turning points that can credibly be described as turning points or structural shifts. If unsupervised learning succeeds in this task on a limited slice of the economic universe, then this article may support new approaches that can complement traditional peak-to-trough methods of defining cyclicality in financial markets and the broader business cycle.

1.2. A Section-by-Section Summary

Section 2 of this article reviews the literature on comovement and volatility spillovers in commodity markets, particularly those involving energy. Section 2 also reviews the literature on rules-based definitions of bull and bear markets and economic recessions. This extended review of the relevant economic literature provides complete background on volatility in crude oil and refined fuel markets. Section 2 ultimately explains why connections between commodities trading, financial markets, and the broader economy motivate efforts to describe cyclicality and other manifestations of variability in the volatility of energy-related markets over time.

Section 3 presents data sources and describes the unsupervised machine-learning methods underlying this article. Conditional volatility forecasts based on a GJR-GARCH(1, 1, 1) process for 22 commodity markets from 2000 through 2020 constitute the primary data source. The subarray containing volatility forecasts for four oil and fuel markets provides the central focus. Logarithmic returns, for all commodities and the energy-specific subset, constitute an additional source of data.

Section 4 aggregates results from five clustering methods—affinity propagation, mean-shift, spectral, k-means, and hierarchical agglomerative clustering—as applied to a comprehensive market basket of 22 commodities and to a more focused basket of four energy-related commodities: Brent, West Texas intermediate, gasoil, and gasoline. t-distributed stochastic neighbor embedding, or t-SNE, helps visualize all clustering results.

Meaningful temporal clusters for broader commodity markets delineate the global financial crisis and the COVID-19 pandemic. Focused clustering in energy-related markets identifies several additional critical periods for crude oil and refined fuel markets. Section 5 presents and distinguishes those two sets of results.

Section 6 discusses the implications of this article’s findings for managers, investors, and policymakers. Critical periods in energy-related markets demand a different approach to hedging and risk management, not merely for commodity investors, but also for investors using commodities to neutralize other sources of risk. The role of energy-related crises in macroeconomic policymaking also warrants careful consideration.

The identification of temporal regimes in commodity markets through clustering suggests the generalizability of unsupervised machine learning to other markets and to macroeconomic data. The second half of Section 6 describes these and other possible paths for future research.

2. Literature Review

The economic literature germane to this article spans four distinct subjects:

- Price volatility in oil and refined fuel markets;

- Comovement and volatility spillovers between these energy-related commodities and other commodity markets;

- Similar connections between energy-related commodity markets, other financial markets, and the real economy;

- Methods for identifying cyclicality and other time-varying effects in commodity markets, stock markets, and the real economy.

This section addresses each body of literature in turn. A review of the relevant literature on unsupervised machine learning is deferred until Section 3′s presentation of materials and methods.

2.1. Price Volatility in Crude Oil and Refined Fuels

2.1.1. Oil Price Volatility

Commodity markets figure prominently in developmental economics and international trade. Representing a quarter of global trade in goods, commodities provide the most important source of income for some of the world’s poorest countries [2,3]. Because advanced economies rely so heavily on petroleum-based fuels for transportation and many industrial processes, the wealth of developed nations also hinges on oil-based commodities [4].

The pervasive financialization of commodities raises the premium on proper understanding of the price and volatility dynamics in these markets [5]. This is particularly true of crude oil and fuels refined from it [6,7,8,9]. Producers and industrial customers have the greatest stake, since oil price volatility directly affects investments in oil inventories, production and transportation facilities, and physical capital based on oil consumption [10]. These sunk investments demonstrate why “costly reversibility” is a prime mover in the economics of market structure and industrial organization [11,12,13,14].

Because of their intrinsic volatility and their dependence on global supply chains, energy markets are especially sensitive to external shocks. The diverse factors affecting oil prices include sociopolitical disturbances, shifts in the global supply and demand, and technological and regulatory changes promoting demand for renewable energy [15]. Discrete events, “such as wars, the release of OPEC production quota decisions, oil stock fluctuations and extreme weather,” also affect oil prices [16] (p. 256).

Chronic or acute, these factors are never stable. Structural breaks punctuate the time-varying conditional heteroskedasticity of oil price volatility [17]. Although conventional tools for forecasting oil prices and volatility abound [18,19], models that ignore structural breaks and other sources of temporal variability in volatility “will have very low power” [17] (p. 555). This is yet another instance in which accurate forecasting relies upon the more realistic assumption that volatility does not remain constant [20].

2.1.2. Refined Fuels: Gasoline and Gasoil (Diesel)

Because gasoline and gasoil are refined petroleum products, their price and volatility dynamics depend heavily upon the economics of oil. These markets are nevertheless subject to forces befitting their proximity to retail consumers. Gasoline and gasoil are affected by time-varying consumer income [21] and the price elasticity of demand for petroleum-based fuels among other retail-level energy sources [22]. Demand for gasoline may be less elastic than typically assumed, especially in the short run [23].

Perhaps the most distinctive trait of the price behavior of refined fuels, particularly gasoline, is its asymmetry [24,25,26,27]. The “rockets and feathers” hypothesis posits that increases in crude oil prices are transmitted much more quickly to gasoline than decreases [28,29,30]. Data across the United States showed that retail gasoline prices increased 0.52 percent within the first week of an anticipated 1 percent increase in oil prices, but fell 0.24 percent within the first week of a 1 percent decrease [31].

Other sources describe asymmetry in gasoline pricing according to Edgeworth price cycles, characterized by sawtooth-shaped time series consisting of many price decreases punctuated by occasional upward jumps [32,33]. Straightforward measurements of gasoline demand have shown that elasticity decreases as volatility rises [34,35]. Both the “rockets and feathers” hypothesis and Edgeworth price cycles are consistent with this account of volatility.

Other sources contest the presence of asymmetry in the relationship between oil and refined fuel markets [36]. Asymmetry, if present for gasoline and gasoil in Europe, is fleeting and appears over very short time horizons [37]. Asymmetry appears in Spain and Italy, but not in Greece, the United Kingdom, or the United States [38]. Time-varying effects such as volatility clustering and structural breaks affect the degree of asymmetry in the transmission of volatility from oil to gasoline [39]. Findings of asymmetry may depend on the frequency at which volatility data is sampled [40].

One study reaches an intriguing conclusion: The “rockets and feathers” hypothesis tells the dominant story of oil–gasoline asymmetry, but not the exclusive story [28]. When oil prices are falling, on average, gasoline prices follow a contrary “boulders and balloons” dynamic by which gasoline more swiftly tracks oil price declines than increases. The reversal in the polarity of oil–gasoline asymmetry strongly suggests that volatility transmission between crude oil and refined fuels varies over time. Indeed, the presence of opposite tendencies, based on the timing of the broader business cycle, suggests that asymmetry, persistence, and cyclicality in volatility must be understood in the context of other capital markets and the macroeconomy [41,42].

Though literature on the price dynamics of gasoil is relatively sparse and inconclusive, national fuel mix policies appear to account for some of this fuel’s differences relative to gasoline [43]. The European Union [44] and the United Kingdom [45] both nudge their transportation sectors to favor gasoil over gasoline. With mixed success, the United States has maintained a heating oil reserve to stabilize prices for this variant of gasoil, widely used to heat homes in the northeastern region of that country [46]. Home heating can be expected to be one of the least elastic sources of demand for gasoil, at least over short time horizons, for households that depend on this fuel.

2.2. Comovement and Volatility Spillovers within Commodity Markets

2.2.1. The Financialization of Commodities and Hedging Strategies

As a prime outgrowth of the coordination of commodity markets with other aspects of global finance [5], comovement and volatility spillovers among commodities warrant careful evaluation [47]. Commodity futures have become popular tools for diversification [48,49]. Tools for managing financial risk in other capital markets apply directly to energy-related commodity markets [50]. Commodities as safe havens can offset turbulence from other asset classes, from equities to currencies [51]. The “universe of financial assets,” spanning diverse “investment strategies,” heightens the importance of “risk transfer between oil” and markets for other “global, large and liquid” assets [52] (p. 56).

Unstable energy prices often induce investors to hold other assets alongside energy commodities. Hedging strategies and portfolio rebalancing enable investors to manage comovement [53]. At a minimum, oil price shocks affect non-energy commodities [54,55,56,57]. A study of volatility in oil and refined fuel should therefore consider comovement and volatility spillovers linking energy with other commodity classes, especially metals and agricultural products.

2.2.2. Precious Metals

The traditional role of precious metals as hedges against inflation and economic turbulence [58] casts those commodities in sharp relief against crude oil and refined fuels [59,60,61]. Markets for oil are more volatile than markets for gold and silver [62]. Precious metals exhibit hedging and safe haven properties vis-à-vis energy [49,59,63,64]. Connections between gold and oil extend to other financial instruments [60,65].

Financial risk may not run equally between two markets. Among instances of volatility spillover in commodity markets [66,67,68], the propensity of oil to transmit volatility to precious metals poses the greatest challenge to investors in energy-related commodities [69,70,71,72]. As the global financial crisis of 2008–2009 demonstrated, precious metal returns may be more sensitive to disaggregated structural oil shocks [72].

2.2.3. Base Metals

Because oil prices heavily affect input costs for industrial processes using base metals, connections between energy markets and metals extend beyond gold, silver, platinum, and palladium [73,74]. Although one study identified platinum, gold, and silver as net transmitters of volatility to oil [60], such spillover may not persist across all periods and market states. Indeed, traditional distinctions between precious and base metals may not hold across all financial conditions. Tin, gold, nickel, lead, and aluminum transmit return and volatility to oil markets. Copper, zinc, and platinum are net receivers—but only “at certain specific moments” [75] (p. 12). Time-varying fluctuations became especially pronounced during the global financial crisis [60] and the COVID-19 pandemic [75].

2.2.4. Agricultural Commodities

Energy markets also transmit volatility to agricultural commodities [3,71,76,77,78,79]. The dependence of agricultural commodity markets on energy prices varies over time [80]. A structural break appears to have shifted the relationship between oil and agricultural commodities after 2006 [81]. Sources differ in attributing the disruption to a change in biofuels policy [76] or to a broader crisis in food crops [78].

The relationship may vary more subtly over time [80]. During periods such as the financial crisis of 2008–2009, oil and agricultural commodity markets crash simultaneously. Connectedness likewise strengthened during the COVID-19 pandemic [82]. Under normal economic conditions, however, these markets move in opposite directions. This pattern implies that hedging will fail in the very conditions when hedges would prove most valuable. The counterbalancing effect also denies investors the opportunity to realize excess profits in both markets.

These conclusions are neither universal nor inevitable. A different study focusing on common crisis periods such as the global financial crisis and the pandemic rejects two key conclusions of other studies [83]. Oil and crops have a bidirectional relationship in which each class of commodities transmits volatility to the other with roughly equal probability over long time horizons. As a surprising consequence, oil and agricultural prices remained relatively stable throughout the pandemic.

Certain crops (particularly corn and soybeans) either compete directly against crude oil as a renewable substitute or serve as a complementary product [84]. A third crop, sugarcane, affects these markets because of its substitutability for corn [85]. Conventional wisdom holds that high oil prices invite competition from corn-based ethanol and soybean-based biodiesel [86].

This relationship, like many others, appears to depend on the state of the market: Spillovers from oil to agricultural and biofuel markets are stronger when oil prices are higher [87]. Conversely, concerns over the diversion of common-pool resources used in agriculture from food to fuel production reach their peak during economic crises [88].

Closer scrutiny of the impact of biofuel policies on oil and gasoline price variability [89] has not found conclusive evidence that energy markets spur volatility in corn [90] or that policy-stimulated demand for biofuels has elevated prices or volatility in agricultural markets [91]. The answer to the conundrum may lie in the limited economic impact of biofuel policies. If such policies were abolished around the world, biofuel demand would implode without materially affecting overall demand for agricultural commodities [92].

2.2.5. The Geopolitics of Energy-Related and Agricultural Commodities

The prominence of oil and export crops in many developing economies heightens the economic, political, and diplomatic sensitivity of volatility spillovers involving those markets [3]. Connectedness between these commodities bridge distant geographic markets, such as Chinese crops and crude oil, whether around the world [93] or specifically in the United States [94]. As a rule, however, research on the impact of oil price volatility on developing countries that import rather than export petroleum remains limited [95].

A global study spanning 157 countries at different stages of development attributed 40 percent of income volatility to oil price fluctuation [96]. Though “the adverse effects of [price] instability” are often “much more severe” in developing countries, those governments can rarely afford “the extensive support programs that typify the agricultural sectors of the developed world” [97] (p. 1729). Dependence on natural resource extraction is so often associated with stunted economic development that this paradox is known as the “resource curse” [98,99,100,101].

Geopolitical tension from oil divides importing and exporting countries [102,103]. Importing countries must rely on insecure foreign sources of an economic lifeblood [104], while global trade and politics drive fiscal policy and economic cycles in exporting countries [105]. The rapid emergence of China portends the revival of a Great Game among global superpowers in central Asia and other oil-rich regions [106].

Again, however, the economic effects are asymmetrical. Economic reactions to energy price shocks in exporting countries are greater and more persistent than in importing countries [107]. In the long run, both oil-importing and -exporting countries stand to lose. At least among OECD countries, oil price volatility stunts economic growth in net importers, while oil price uncertainty hurts net exporters [108]. Furthermore, to the extent that oil price volatility suppresses international trade and globalization, the ensuing reduction of global welfare harms all countries [109].

2.3. Broader Financial and Macroeconomic Effects of Oil and Fuel Price Volatility

2.3.1. Financial Markets beyond Commodities

Oil markets transmit volatility to other capital markets, including equity markets [110,111]. Although one study concludes that the American stock market is neither a net transmitter nor a net receiver of volatility relative to oil or precious metals [60], others have found spillover effects in smaller economies such as Iran [112] and South Korea [113].

Stock returns and stock market volatility in oil-exporting countries such as Qatar, Saudi Arabia, and Venezuela are assuredly affected by oil prices [114]. These effects follow a regime-switching framework based on the cyclical state of these countries’ equity markets—specifically, whether stocks in oil-producing countries are in a bull or bear market [114]. Some sources advise investors in oil-exporting countries to increase their allocation to oil [115,116].

The relationship between oil price volatility and the equity market may depend on the cyclicality of both markets. The “relationship between oil prices and US equities could depend on both the nature of oil price shocks and how well the US stock market is performing” [117] (p. 6). Complete understanding of the mutual dependence of oil prices and broader capital markets requires not only some understanding of cyclicality in commodity and equity markets, but also a principled way of identifying critical periods within financial history.

To like effect, structural heterogeneities in foreign exchange markets coincide with geopolitical and economic impacts [118]. In conjunction with broader macroeconomic phenomena, oil markets exert dynamic influence on trade in currencies [118]. Portfolio management and other forms of risk management therefore hinge on the relationship between oil prices, exchange rates, and the business cycle.

2.3.2. Macroeconomic Effects

Oil price volatility impairs economic growth [119]. Like many other phenomena connected to oil and fuel markets, the macroeconomic effects of disruptions in energy-related markets are asymmetrical. Oil price increases stunt economic growth more deeply than corresponding decreases in price spur economic activity [120,121]. Even sharp price drops may reduce aggregate output in oil-importing countries by raising uncertainty or inducing inefficient reallocation of resources [122].

Macroeconomic uncertainty spurred by oil price volatility varies over time. Volatility typically peaks during financial crises and recessions [123]. Nonlinear measures capture the overall economic effects of oil price shocks [124]. Oil price volatility in the wake of economic, geopolitical, and natural disturbances often combines short-term perturbations with longer-term macroeconomic factors [125].

A useful trichotomy summarizes the macroeconomic component of oil price volatility [126]. First, “most commodity prices are endogenous with respect to the global business cycle” [127] (p. 313). Second, demand shocks cause slow but sustained changes in price. Third, and in stark contrast, supply shocks have immediate but small and ultimately evanescent price impacts. In oil-related markets, crises and recessions generally reduce demand over a sustained period, while geopolitical events and natural disasters tend to disrupt supplies on an acute basis.

This rigidly logical approach to evaluating the macroeconomic effects of oil and fuel price volatility does leave room for potentially exogenous factors to affect uncertainty. Oil “price uncertainty,” conditioned “on macroeconomic uncertainty,” might be a more complete and “suitable measure of uncertainty” than purely volatility-based measures [127] (p. 325). As a matter of broad theory, if not empirical precision, uncertainty may depend more heavily on the predictability of energy-related markets than on their volatility [127].

2.4. Identifying Cyclicality and Critical Periods in Energy Markets, Finance, and the Real Economy

Comprehensive financialization strengthens the connections linking commodities, capital markets, and the broader economy. These relationships reinforce other centrifugal tendencies throughout economics. For instance, asset pricing models should account for tangible assets and human capital as well as financial instruments [128]. The behavior of a firm is likewise influenced by that of its upstream suppliers, downstream purchasers, and competitors in geographically and technologically adjacent markets [129].

Appropriately enough, efforts to track economic cyclicality span stock markets and macroeconomic policymaking. These two domains, neither more than a single degree removed from commodity markets, have invited many efforts to define critical periods. Even though this article applies unsupervised machine language rather than conventional econometric methods, it is motivated by the same desire to trace economic cyclicality in commodity markets, particularly for crude oil and refined fuels.

Stock markets provide the narrower and methodologically simpler basis for comparison. Technical stock analysis typically defines bull and bear markets, respectively, as a market-wide price increase of at least 20 percent since the previous trough or a market-wide decrease of at least 20 percent since the previous peak [130,131,132]. A 10 percent decline is typically described as a “correction” [133]. Designations of bull and bear cycles within market trends can be made only in retrospect, and there is no justification for these arbitrary 10 and 20 percent thresholds beyond the conventions of technical analysis and financial journalism.

For its part, the Business Cycle Dating Committee of the National Bureau for Economic Research (NBER) tracks recessions and recoveries in the United States [134,135,136,137]. The NBER’s methodology relies on a dynamic-factor, Markov-switching model that examines non-farm payroll employment, the index of industrial production, real personal income, and real manufacturing and trade sales [134,136].

Figure 1 describes the NBER’s announcements regarding the arrival and departure of recessions in the United States [138,139]. It depicts smoothed recession probabilities as they rise and ebb. Notably, only two periods from 2000 through 2020 have exceeded 50 percent according to the NBER: the financial crisis of 2008–2009 and the COVID-19 pandemic. The “dot-com” crisis of 2001 approached but did not exceed a 50 percent probability of recession. As is evident in the shaded areas of Figure 1, however, the NBER did define March through November 2001 as a recession.

One can also frame this problem as the mirror image of an event study [140,141]. An event study traces abnormal effects to determine the duration of a suspected market disturbance. Event studies of oil price shocks [142,143], for instance, have evaluated OPEC announcements [144,145] and storms [146]. Conversely, temporal clustering uses economic anomalies to extract events for further examination amid the flow of financial history.

The timing of recession announcements presents an economically significant issue in its own right [147]. By the NBER’s own admission, its business cycle dating committee’s “approach to determining the dates of turning points is retrospective” [148]. Before definitively identifying a peak, “the committee tends to wait to identify a peak until a number of months after it has actually occurred” [148]. Likewise, the committee does not immediately announce a trough. Rather, the committee “waits until it is confident that an expansion is underway” [148].

Under this methodology, announcements of recessions and recoveries are not aligned in time with actual economic activity [149]. In the three decades from 1980 to 2010, “the lag between the determined start of [a] recession” and the NBER’s “peak announcement” has averaged 9 months [150] (p. 645). At a bit more than 15 months, the lag between a trough and its announcement is longer still [150].

The lag between actual macroeconomic phenomena and their announcements creates an opportunity for machine learning, artificial intelligence, and other automated methods for evaluating economic data. For instance, the United States publishes its official Consumer Price Index on a monthly basis, with a delay of several weeks between the gathering of price data by. the Bureau of Labor Statistics and the announcement of each new CPI reading [151]. By contrast, the Massachusetts Institute of Technology’s Billion Prices Project reports a comparable price index on a daily basis [151].

This article develops a methodology for identifying critical periods in energy-related commodity markets. The literature on oil and fuel markets emphasizes volatility and the connectedness of oil and oil-based fuels with other commodities, other financial markets, and the macroeconomy. Instead of defining cycles akin to bull and bear markets or macroeconomic expansions and recessions, this article will try to distinguish between critical and normal periods of trading within markets for petroleum-related commodities. In seeking a crisis-based approach to understanding temporal shifts in these markets, this article aims at an intermediate level of mathematical rigor between the extremes represented by technical definitions of bull and bear markets and the NBER’s recession-and-recovery methodology.

Qualitative distinctions between peaks and troughs, expansionary and recessionary cycles, and critical periods dissolve upon closer mathematical inspection. Critical points in calculus identify points within the domain of a function where the derivative or gradient is zero (assuming that the function is differentiable at those points). Peaks and troughs as maxima and minima constitute critical points in a univariate function. In a multidimensional space representing returns on more than one asset, critical points also include saddle points, where all slopes in orthogonal directions are zero, but no local extremum is attained. In this mathematically informed sense, the methods described and applied in this article cast a wider net than methods dedicated of finding peaks and troughs within a single time series.

The second derivative of logarithmic returns on a financial asset is related to volatility through the Taylor series expansion [152,153]. Points within the domain of a function where the second derivative is zero indicate inflection or undulation. Methods focusing on financial volatility may therefore find inflection and undulation points as well as critical points. These observations are not meant to suggest that this article consciously seeks to find all critical and inflection points in a strictly mathematical sense. Rather, this analogy simply offers a conceptually helpful way of understanding similarities as well as meaningful differences between traditional peak-and-trough approaches and this article’s clustering methods.

As with stock markets and the broader economy, cyclicality in commodity prices has drawn scholarly attention [154]. Efforts to sharpen forecasting and the understanding of the dependence structure in oil and adjacent markets have highlighted differences between normal trading and economic turmoil [155]. The question is whether existing and novel “econometric tools” can generate reliable volatility forecasts when “periods of heightened volatility in crude oil markets are recurrent” [156] (p. 622).

Conventional econometric tools include unit root tests [157,158]. Those tests aided the discovery of structural breaks in 1990 and 2008, coinciding with the first Gulf War and the global financial crisis [17]. Technical analysis inspired by conventional methods for identifying bull and bear cycles in equity markets [159] has aided the search for cyclical effects in oil-based markets, at higher [4] as well as lower frequencies [160].

Computational tools abound amid economic “big data” [151]. Although some sources have mined linguistic [161] and Internet search data [16,162] in search of novel insights, this article uses machine learning and artificial intelligence to answer a more fundamental question: Whether financial economics can detect oil price fluctuation and its impact on the relationship between risk and return [163].

This article applies unsupervised machine learning to conditional volatility in commodity markets over two decades. An ensemble of clustering methods can identify episodes in commodity markets (especially those related to energy) warranting closer examination. Some episodes, particularly the global financial crisis and the COVID-19 pandemic, reflect a broader, more durable demand shock. Other episodes may last mere days. Such acute events should be expected more often within a confined subset of commodities, such as crude oil and refined fuels. These acute events typically involve geopolitical or natural calamities that disrupt supplies of oil and its downstream derivatives.

3. Materials and Methods

3.1. Data

3.1.1. Data Sources and Preprocessing

This article draws its raw data from sources used in [1]. Thomson Reuters’ DataStream provided price data on a range of precious metals, base metals, energy commodities, and agricultural commodities. Specifically, this article relies upon daily prices from 18 September 2000 through 31 July 2020 for gold, silver, platinum, palladium (precious metals); copper, zinc, tin, lead, nickel, aluminum (base metals); Brent, West Texas intermediate crude (WTI), gasoil, gasoline (energy commodities); and palm oil, wheat, corn, soybeans, coffee, cocoa, cotton, and lumber (agricultural commodities).

The preprocessing pipeline took two further steps. Transforming daily prices into continuous logarithmic returns shortened all series by a single day: 18 September 2000. The resulting log return data (as well as the conditional volatility data derived from log returns) therefore covered the period from 19 September 2000 to 31 July 2020. Two additional days were excluded. On 20 April 2020, WTI closed at –37.63. This event rendered it mathematically impossible to calculate the log return for WTI on that day and the next, 21 April 2020. Those two trading dates were also omitted.

The second preprocessing step involved forecasts of conditional volatility from log returns. We calculated the conditional, time-variant volatility for all 22 commodities according to a GJR-GARCH(1, 1, 1) process using Student’s t distribution [1,164]. The mathematical underpinnings of GJR-GARCH(1, 1, 1) have been thoroughly documented [165,166]. GJR-GARCH outperforms alternative time-series models in forecasting financial markets [167].

For purposes of analysis and discussion, we aggregated log return and volatility data according to a precalculated ontology of commodity markets. The vocabulary of commodities trading distinguishes between mined, nonrenewable “hard” commodities (such as metals and fossil fuels) and grown, renewable “soft” commodities [20,88,168,169]. The term “soft” is sometimes reserved for tropical crops such as cocoa, coffee, and sugar [170]. We adopt that narrower definition of “softs” and describe the temperate commodities of wheat, corn, and soybeans as “crops.” Because cotton and lumber span tropical and temperate climates, these commodities can be assigned to either agricultural subcategory. Results from the clustering of log returns support the classification of cotton and lumber as tropical or semitropical softs [1].

These distinctions, paired with traditional divisions among metals and fuels, can be summarized as a traditional ontology of commodities trading:

- Energy (crude oil and refined fuels): Brent, WTI, gasoil, gasoline;

- Precious metals: Gold, silver, platinum, palladium;

- Base metals: Copper, zinc, tin, lead, nickel, aluminum;

- Temperate crops: Wheat, corn, soybeans;

- Tropical and semitropical “softs”: Cocoa, palm oil, coffee, cotton, lumber.

3.1.2. Visualizations of Logarithmic Return and Conditional Volatility Data

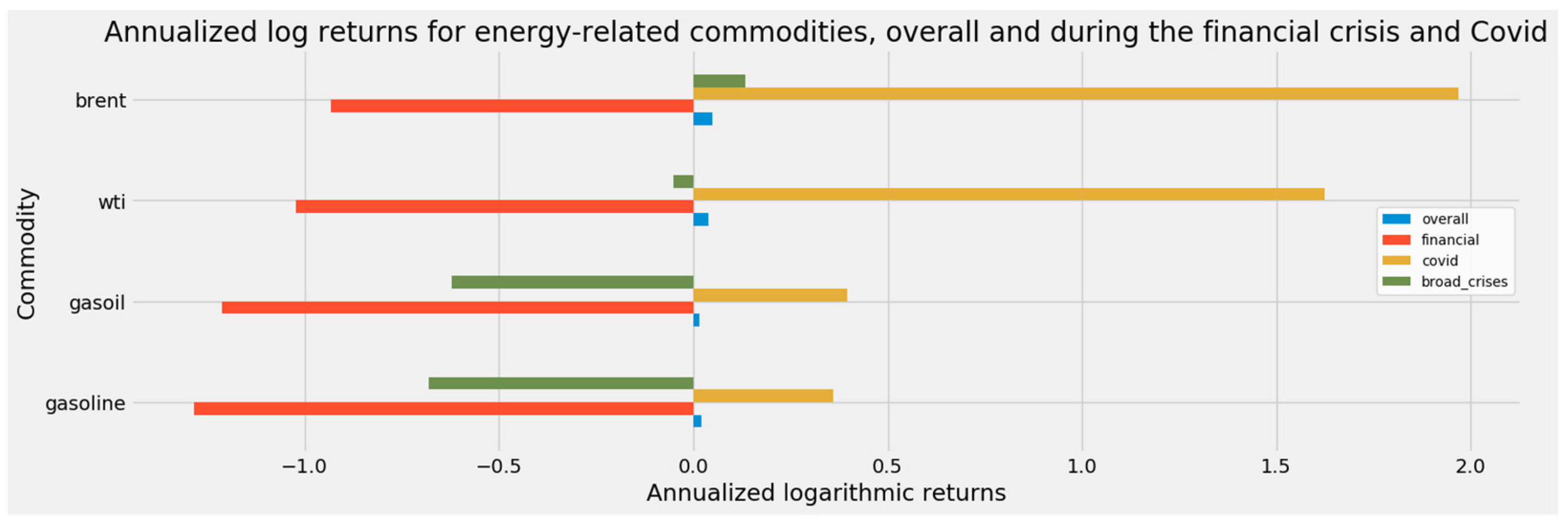

This subsection visualizes this article’s core data. Although log return and conditional volatility calculations were performed on all 22 commodities, this article compares only energy-related commodities with one another on an individual basis. This article compares crude oil and refined fuels as an asset class alongside the aggregate categories for metals and agricultural commodities.

Figure 2a depicts cumulative log returns for commodities as asset classes. Relative to other classes, energy-related commodities show many sharper price movements. Figure 2b illustrates cumulative log returns for individual crude oil and fuel markets. Although comovement among individual oil and fuel markets is far tighter (as one should expect) than among broad classes of commodities, sharper upward and downward price spikes, particularly for gasoline, are evident to the naked eye.

Figure 3a,b depict conditional volatility. By analogy to Figure 2a,b, Figure 3a portrays the five broad classes of commodities, while Figure 3b focuses on the four individual energy-related markets. Visibly greater volatility in energy markets dominates Figure 3b. Relative to crude oil markets and even gasoil, the market for gasoline is palpably more volatile. These acute volatility spikes confirm the intuition motivating the conventional exclusion of food and fuel prices from core inflation indices used in the making of macroeconomic policy [171,172,173,174].

3.2. Clustering Methods

3.2.1. General Considerations

Many applications within economics and finance exploit clustering and related forms of unsupervised machine learning [175,176,177,178]. This article applies five clustering methods: Spectral, mean-shift, affinity propagation, k-means, and hierarchical agglomerative clustering. Each of these methods is available in the SciKit-Learn package for Python. The implementation of hierarchical agglomerative clustering in Scipy generated visually distinctive dendrograms for that method.

Previous research had established that temporal clustering should be based on conditional volatility rather than logarithmic returns [1]. All five clustering methods were applied to volatility data arrayed in n rows of trading days and p columns corresponding to the number of distinct commodity markets. For the full volatility array covering all 22 commodities, p = 22. For the energy-specific subarray, p = 4. The two arrays, however, had the same number of trading days: n = 5182.

For both the full 5182 × 22 array and the energy-specific 5182 × 4 subarray, clustering results underwent a crude aggregation inspired by voting classifiers in machine learning [179]. Since clustering of the full 5182 × 22 array reached rough consensus on the financial crisis of 2008–2009 and the COVID-19 pandemic as the two periods of interest, that analysis relied on the union and the intersection of the five sets of clustering results. Using the union of sets is tantamount to allowing a single vote to drive a positive result. The intersection of those sets indicates unanimity. These set theory concepts therefore define the logical extremes of voting methodologies [180,181].

Greater variability in the results for the energy-specific 5182 × 4 subarray required a more flexible approach. For that array, this article aggregated all positive results registered by two or more of the five clustering methods. The most generous voting method, consisting of the union of all positive results, generated a wider range of dates. Though unexamined in this article, those results remain available for future research.

The balance of this subsection will describe each of the five clustering methods.

3.2.2. Spectral Clustering

Spectral clustering operates on a projection of the normalized Laplacian [182,183]. Since this article’s conditional volatility arrays represent 4 or 22 commodity markets as simple functions of a common vector of trading dates, the Laplacian (Δf = ∇2f) is the sum of the partial second derivatives for each of those variables.

Spectral clustering should work very well with financial data. This method exposes individual clusters within highly non-convex structures [184,185]. Since each volatility vector is plotted against the same vector of trading dates, the resulting arrays of volatility forecasts by date are tantamount to overlapping curves on a two-dimensional plane. Spectral clustering therefore excels precisely where conventional statistical measures of central tendency and variability fail to describe the shape of the data to be clustered.

These properties have made spectral clustering especially popular in computer vision and image processing [186,187]. The ability of spectral clustering to detect blobs and edges suggests potential success with economic time series. In mathematical terms, image and time-series data are quite similar. Unlike documents that have been vectorized for natural language processing, these data sources consist of perfectly dense arrays whose columns observe the same scale, or at least nearly so. Still images and simple, harmonized arrays of economic time series can be rendered in a nominally two-dimensional format.

Spectral clustering generated the fewest discrete clusters. Consequently, the spectral method may be regarded as setting the most conservative clustering baseline.

3.2.3. Mean-Shift Clustering

An extension of more traditional pattern-recognition algorithms, mean-shift clustering uses nonparametric techniques to identify deviant blobs in an otherwise smooth space [188]. Alongside k-means, mean-shift is one of two centroid-based methods in this article. The distinctive process that gives mean-shift its name relies on a recursive updating of potential centroids that would represent the mean of the points within a given region. A final postprocessing stage eliminates near-duplicates before reporting the final list of centroids. Hybridizing the mean-shift method with agglomeration can reduce the computation cost of mean-shift clustering [189].

3.2.4. Hierarchical Agglomerative Clustering

Hierarchical clustering methods decompose and arrange mathematical objects according to dendrograms, or trees expressing phylogenetic relationships [190,191,192]. The agglomerative method begins from the “bottom” of a dataset and combines instances into clusters until all data has been assigned to a single, overarching cluster [193].

Bottom-up agglomeration is less computationally demanding than top-down division [194,195]. Four methods for computing distances in hierarchical clustering are widely used: Ward’s method and single-, average-, and complete-linkage [196,197,198,199].

In economics and finance, hierarchical clustering has evaluated stock markets [200,201], buildings and real estate [202,203], broader financial indicators [204], and the relationship between financial markets and the real economy [177]. Hierarchical clustering of cryptocurrency markets [205] intensifies the urgency of research into this asset class during market turbulence [206].

One source has used hierarchical clustering to identify correlation patterns similar enough to comprise distinct market states [207]. Aside from our own work [1] and the use of multidimensional scaling to evaluate comovement among commodities during subjectively defined crises [164], this application of hierarchical clustering represents the most extensive effort to classify periods in financial history through unsupervised machine learning.

3.2.5. Affinity Propagation

Affinity propagation identifies typical cluster members by exchanging quantitative messages between data pairs until the algorithm converges on a high-quality set of exemplars [208,209,210]. This property distinguishes affinity propagation from mean-shift and k-means clustering, which are centroid-based methods.

Under SciKit-Learn’s default settings, however, affinity propagation generates far too many distinct exemplars. To the extent that other methods (specifically spectral, mean-shift, and hierarchical clustering) can better estimate the optimal number of clusters, an instance of affinity propagation can alter the element preference from its default value of the median of the array of input similarities [211]. To a limited extent, this adjustment enables affinity propagation to alter the number of clusters that it finds.

Affinity propagation spans an impressive range of applications. Affinity propagation is used to cluster microarray and gene expression data [212,213,214] and in sequence analysis [215]. Applications beyond bioinformatics [216] include natural language processing [217,218,219] and computer vision [220,221]. Especially if calibrated so that element preference yields something close to the optimal number of exemplars, this versatile clustering method should accommodate financial time series.

3.2.6. k-Means Clustering

One of the oldest clustering algorithms [222], k-means clustering remains a popular way to partition mathematical space [223]. k-means clustering excels in detecting fraud [224] and firms at risk of default or failure [225]. Other financial applications include the forecasting of returns and the management of investment risk [176,226,227,228]. Our own previous research on commodity markets relied heavily on k-means clustering [1].

k-means clustering does require more careful handling. More than other methods, k-means clustering depends on algorithms for determining the ideal number of clusters [229,230]. In addition to k, the optimal number of clusters, this centroid-based method depends entirely on randomized instantiation [231]. To ensure replicability of results, this article seeded SciKit-Learn’s pseudo-random number generator with the value of 1. Finally, k-means clustering cannot detect objects lacking a hyper-ellipsoidal shape [232].

3.3. t-Distributed Stochastic Neighbor Embedding (t-SNE)

This article uses a single method of manifold learning: t-distributed stochastic neighbor embedding, or t-SNE [233,234,235]. t-SNE reduces distances between similar instances and maintains distances between dissimilar instances. Although this article applies t-SNE solely for visualization, t-SNE can be a valuable form of unsupervised learning on its own. Preprocessing with t-SNE can detect and remove outliers in preparation for the application of convolutional neural networks to computer vision [236].

4. Results, Part 1: Temporal Clustering

Clustering results differ dramatically according to the underlying array of conditional volatility forecasts. This section accordingly separates results for the full 5182 × 22 array of all commodities from results based on the smaller 5182 × 4 energy-specific array.

Differences among clustering methods are also stark. Clustering differs from classification through supervised machine learning in a crucial respect. Clustering results do not correspond to a priori labels assigned by a human. Analyst judgment therefore plays a subtler role. Each clustering method must be evaluated on its own terms. Moreover, each method’s results must be evaluated in light of all others and against the backdrop of unavoidably subjective judgment. Each method’s underlying mathematics, however, offers principled guidance on the exercise of that discretion.

4.1. Temporal Clustering of the Full Array of Conditional Volatility Forecasts

4.1.1. The Naïve Biennial Baseline

The naive clustering of all 20 years of commodities trading data provides a valuable starting point. Consider the possibility that a fixed and predetermined period of time should define each segment of financial interest. This hypothetical is far from absurd; monthly, quarterly, or annual reporting slices financial time in precisely this way. In the interest of convenience, we select intervals of two calendar years each.

Figure 4 establishes a visual baseline for all temporal clustering. Consistent reliance on t-SNE to reduce all 22 dimensions produces a uniform three-dimensional projection of conditional volatility forecasts. Synthetic centroids generated by the average of all observations for each biennium supply a rough sense of those two years.

Cluster 9 is particularly interesting because the 2019–2020 biennium includes the global maximum for cumulative log returns on precious metals and the global minimum in cumulative log returns on oil and fuels. That cluster’s synthetic centroid falls very near the global center. Its corresponding observations, in cyan, stretch across the financial firmament, as measured by its width across the zeroth t-SNE dimension.

Expanding all spheres from Figure 4 and Figure 5 reveals the futility of arbitrary biennial clusters. If spherical radii corresponding to each cluster define the mean distance of each observation from its corresponding synthetic centroid, then the size of each sphere and its overlap with other spheres suggest the extent to which each cluster is internally cogent and externally distinct. Internal cogency, if present, should reveal itself through contiguous or nearly contiguous clusters in an ordered, one-dimensional projection along a temporal axis. An ordered, horizontal representation would indeed display 10 perfectly contiguous, nonoverlapping clusters. That is an artifact of the arbitrary definition of those clusters, however, and not any mathematical property captured by t-SNE.

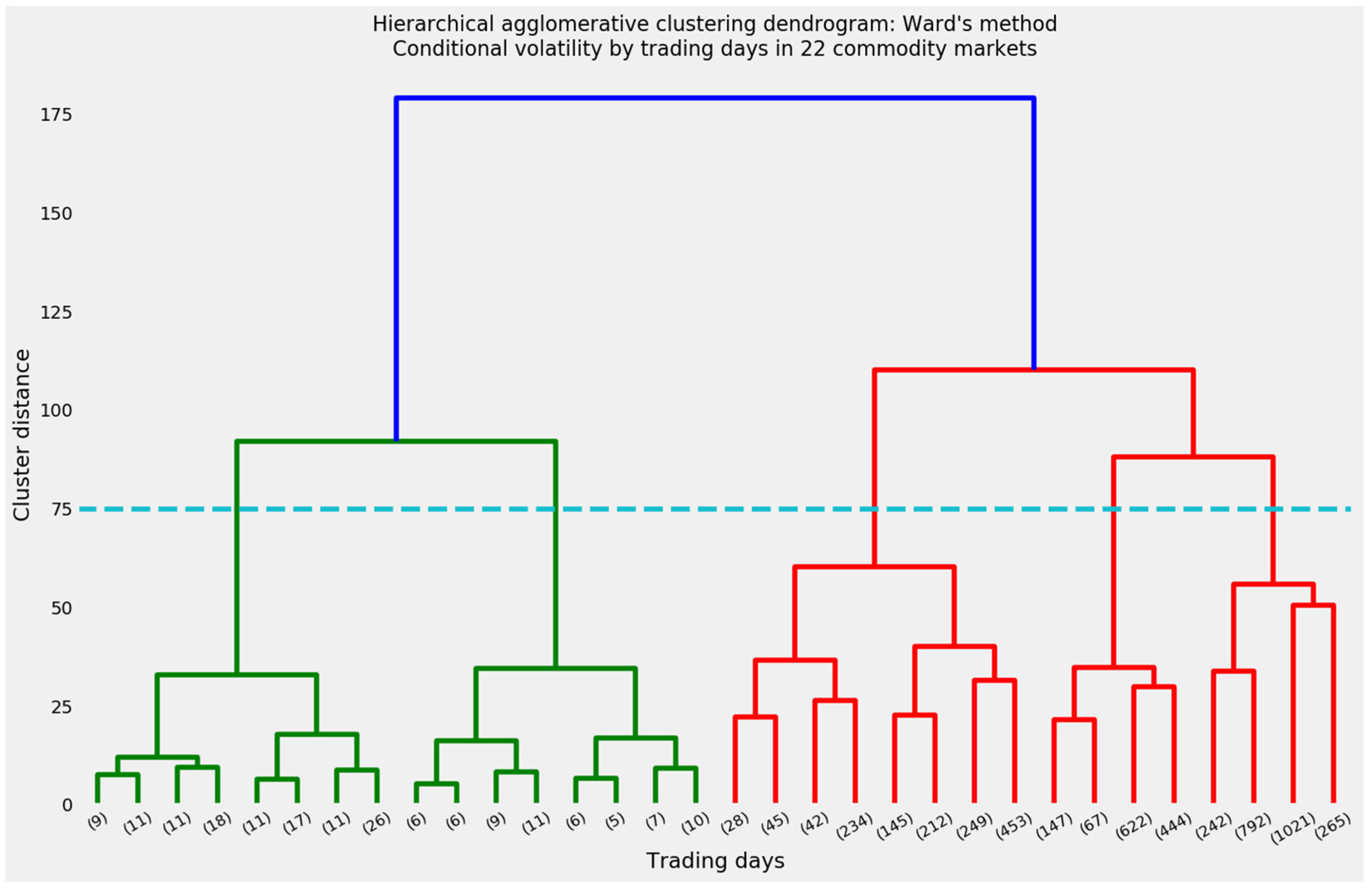

4.1.2. Spectral Clustering

Spectral clustering of all conditional volatility forecasts identifies eight clusters. Although this method does not generate centroids, finding the mean of each cluster’s members in the three-dimensional t-SNE manifold produces synthetic centroids.

Figure 6 reveals the complete t-SNE manifold of spectral clusters. Clusters 1, 2, 3, and 5 appear in a tight group at upper left. Clusters 1 and 2 contain only two days each, while cluster 3 adds only nine more. The tiny size of these clusters is implied by their compactness.

Two other groupings also stand out. Clusters 4 and 7 occupy the lower foreground. Cluster 6 stands alone. As with clusters 1, 2, and 3, a tight radius implies that cluster 6 consists of a small number of days. Indeed, cluster 6 contains only 22 days.

The vast majority of trading days—4920 out of 5182—belong to cluster 0. The t-SNE manifold suggests that cluster 0 may be the fallback cluster representing ordinary trading days, when volatility levels do not substantially deviate from their central tendency.

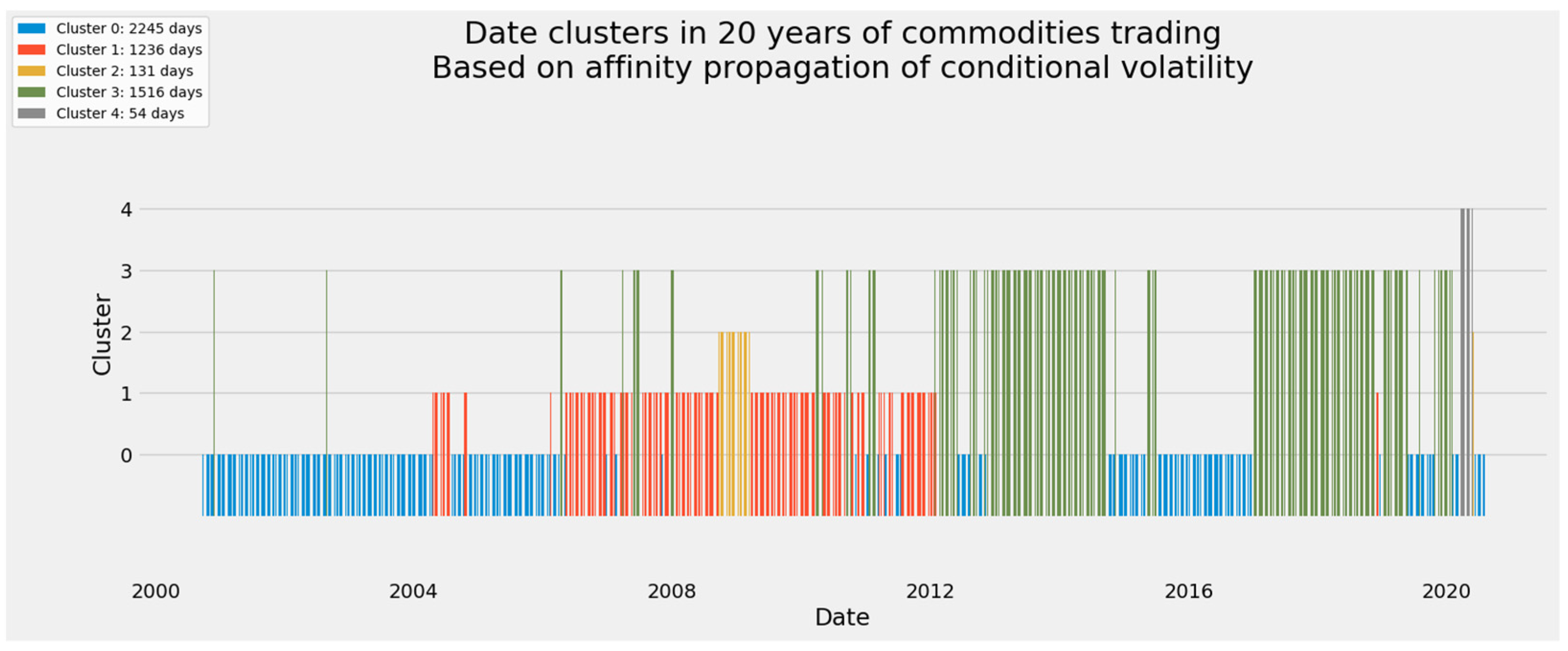

The most useful representation of temporal clusters, of course, is the one plotted against the ordered vector of dates. Figure 7 reveals how the eight spectral clusters almost perfectly identify two critical periods of interest from 2000 to 2020. The height of the bars communicates categorical rather than ordinal or numerical information. Because of the fortuity that spectral clustering assigned the number 0 to the default, catch-all category, all clusters numbered 1 and above identify periods of interest.

Spectral clustering identified the financial crisis of 2008–2009 and the COVID-19 pandemic. Almost miraculously, six of the remaining seven clusters are perfectly contiguous. Instances from cluster 5, though split by clusters 1, 2, and 3, joined those other clusters to form a continuum covering the beginning of the pandemic. Cluster 6 covers the final 22 days in the dataset. Whether those days belong with the earliest phase of the pandemic or instead indicate a transition toward noncritical cluster 0 may be inferred from the location of cluster 6 in Figure 6 as well as the statistical summary of each cluster.

The resolution of Figure 7, however, is not sharp enough to reveal additional insights. Cluster 5 consists of two subclusters separated by nearly 19 years. The earliest instances in cluster 5 occur in 25–28 September 2001, exactly two weeks after the terrorist attacks of 11 September 2001. The remaining 67 days in cluster 5 started in March 2020, coinciding with the outbreak of COVID-19 in Europe and North America. This represents evidence, however faint, that an event unequivocally related to energy markets might sway the commodities market as a whole.

4.1.3. Mean-Shift Clustering

Mean-shift clustering generated results remarkably similar to spectral clustering. In certain respects, mean-shift clustering might be even more parsimonious.

Figure 8 identifies two periods of potential interest: The tight clump formed by clusters 2, 4, and 5 at left and the looser pair of clusters 1 and 3 at bottom. Because t-SNE manifolds are shaped by their underlying data, Figure 8 can be compared directly with other t-SNE manifolds. Figure 4, Figure 5 and Figure 6 make it apparent that clusters 2, 4, and 5 correspond to COVID-19, while clusters 1 and 3 track the financial crisis of 2008–2009.

The ordered timeline in Figure 9 confirms these intuitions. Clusters 2, 4, and 5 indeed cover the COVID-19 pandemic. Notably, the final 39 trading days (9 June through 31 July 2021) fall within cluster 0. Mean-shift results suggest that the final 22 days might be better classified as “ordinary” trading days rather than part of the COVID-19 crisis.

4.1.4. Hierarchical Agglomerative Clustering

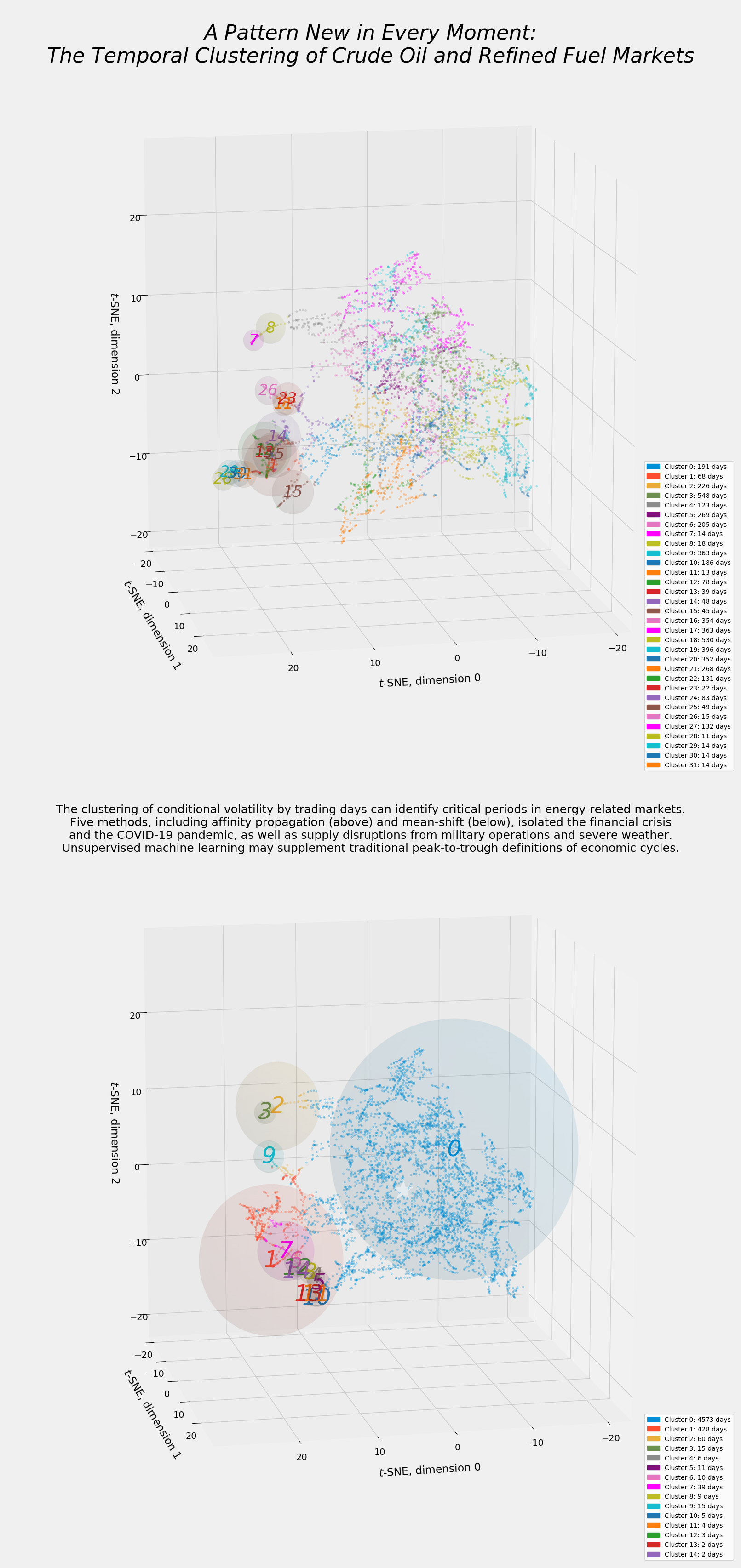

The visual signature of hierarchical clustering is the dendrogram. The dendrogram has the added benefit of offering principled guidance on the optimal number of clusters.

Figure 10 displays the dendrogram for hierarchical agglomerative clustering using Ward’s method and Euclidean distances. The height of the branches offers guidance on the ideal number of clusters. In principle, the ideal number of hierarchical clusters may be as low as two. The height of the blue branches exceeds the vertical distance between any other set of splits. Splitting this dataset into two temporal clusters is tantamount to the binary classification between crises and ordinary (or non-critical) periods.

The dotted horizontal line in Figure 10 intersects five vertical branches. The comfortable vertical distance on either side of 75 implies that 5 is a near-optimal number, if we are unwilling to abandon multiclass in favor of binary clustering. In any event, the logic of agglomeration makes it easy to rearrange the five clusters as two.

Hierarchical agglomerative clustering in Python can designate an arbitrary number of clusters, k ∈ [1, n]. Having determined k = 5, we can project the t-SNE manifold in three dimensions as well as the ordered timeline.

The three-dimensional t-SNE manifold of hierarchical clustering results differs in striking ways from its spectral and mean-shift counterparts. Figure 11 divides noncritical trading days more evenly among three clusters: 0, 1, and 2. Clusters 3 and 4 are the outliers. Cluster 3 surely represents the financial crisis, while cluster 4 captures COVID-19.

The ordered timeline in Figure 12 confirms the intuitive interpretation of the t-SNE manifold. Again, departures from ordinary trading are designated by higher-numbered clusters. The spike for cluster 3 coincides with the financial crisis, while cluster 4 rises during the COVID-19 pandemic.

4.1.5. Affinity Propagation

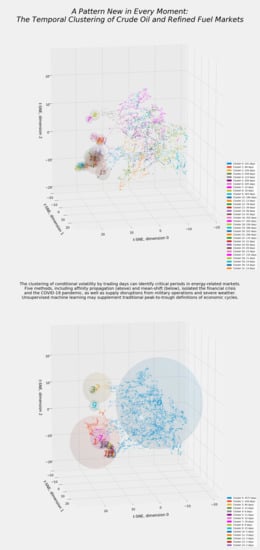

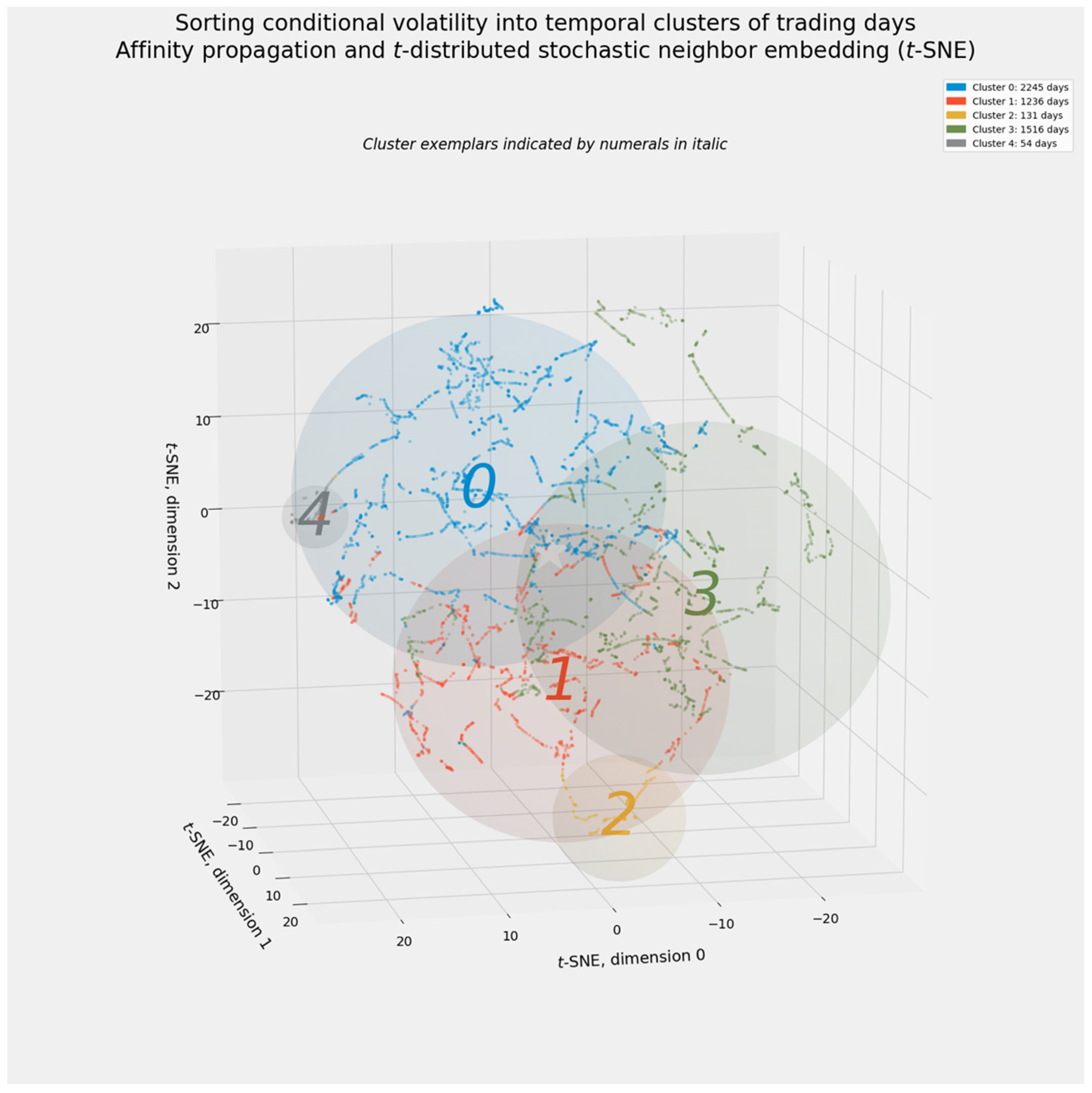

The final two clustering methods, affinity propagation and k-means clustering, require more computation and discretionary judgment. These difficulties arise from a simple difference: Default settings for affinity propagation and k-means clustering generate a larger number of smaller clusters. Worse, many of those clusters cover non-consecutive days, despite their relatively small size.

Adjusting the element preference matrix enables affinity propagation to generate a desired number of exemplars. This trait of affinity propagation is not infinitely elastic. Nevertheless, a simple matrix of element preferences generated five clusters, the same value of k in hierarchical agglomerative clustering. Those element preferences consisted of the median (not mean) of each vector of volatility forecasts, uniformly scaled by −3000.

Figure 13 shows how closely affinity propagation, once nudged toward five clusters, resembles hierarchical agglomerative clustering. Critical days appear in clusters 2 and 4, which respectively define the financial crisis and the pandemic.

Figure 14 places these clusters within an ordered timeline. Cluster 2, however, covers not only the financial crisis of 2008–2009 but also the three days immediately following cluster 4′s definition of the pandemic. Consistent with other clustering results, this minor deviation from perfect contiguity suggests that volatility during the COVID-19 crisis drifted toward conditions characterizing the longer-lasting “great recession.”

4.1.6. k-Means Clustering

This article’s exercise in k-means clustering on all conditional volatility forecasts duplicates the temporal clustering in [1], with a salient difference: The value of k, now fixed at six, is the average number of clusters found by other methods (Figure 15). Conventional methods for optimizing k did not prove particularly satisfying. It remains possible to determine k through other clustering methods.

Like mean-shift clustering, k-means clustering relies on the stochastic instantiation of centroids. k-means clustering, however, generates the least contiguous and the least visibly cogent set of clusters. Figure 16 reveals only two wholly contiguous clusters (1 and 4), which coincide with the financial crisis and the pandemic.

4.1.7. The Union and Intersection of Clustering Results for the Full Volatility Array

Though similar, these five clustering methods differ subtly, just enough to require human intervention. Some methods confine all results for the financial crisis or the pandemic to a single cluster. Others divide results among as many as four clusters. Affinity propagation associated three days after its COVID cluster with the earlier financial crisis.

Prior intuitions about any particular clustering method are just that: prior intuitions. The “no-free-lunch” theorem of machine learning posits that no single method can be expected to outperform others in every task [237]. Moreover, machine-learning ensembles typically outperform any individual model [238]. Some method of aggregating results from different clustering models seems advisable.

Elementary set theory provides a simple solution. The union of all clustering results identifies a critical period as long as any method assigns a date to a critical period. The intersection of those results demands agreement among all methods. Given the simplicity of finding agreement over exactly two periods—the financial crisis and the pandemic—these opposite extremes of any plausible voting algorithm define the range of answers.

Figure 17 depicts this simple voting algorithm’s parsimonious results. The union of all results defines the financial crisis as 16 September 2008 to 24 April 2009. The intersection of those results narrows the timeframe so that it runs from 16 October 2008 to 17 March 2009.

The definition of the COVID-19 pandemic is likewise perfectly contiguous by either criterion. The union of results defines the COVID crisis as 10 March to 1 July 2020. The narrower intersection of those sets also begins on 10 March but ends on 26 May 2020.

4.2. Temporal Clustering of the Energy-Specific Array of Conditional Volatility Forecasts

We now apply all five clustering methods to the energy-specific 5182 × 4 subarray of conditional volatility forecasts. The smaller size of this array nudges all methods toward finding more clusters. That property makes some clustering models more difficult to manage. On the other hand, the relative stability of clustering on the grand array of 22 commodities suggests that this suite of unsupervised machine-learning methods can be successfully extended to larger financial markets (including equity markets with hundreds or thousands of stocks) and to arrays of macroeconomic indicators.

Dispensing with the naïve clustering of observations by arbitrary two-year periods, we begin with spectral clustering and progress through all other methods.

4.2.1. Spectral Clustering

Figure 18 reports spectral clustering results for the time periods within the subarray of energy-specific conditional volatility.

On the energy-specific subarray, as with the full array, spectral clustering is a very conservative method. It finds fewer and smaller clusters apart from a single large cluster of ordinary observations. In Figure 18, clusters 1 through 6 adhere together during the COVID-19 pandemic. Cluster 7 stands apart in time and contains 17 consecutive trading days. Cluster 0 accounts for nearly 99 percent of the full 5182 days.

Figure 19′s ordered timeline reveals that cluster 7 does not overlap any period associated with the financial crisis of 2008–2009. Rather, cluster 7 consists of 17 days in August and September 2005. This is the first energy-specific event not identified by the broader array of all commodities. As will become apparent, these days coincided with Hurricane Katrina, which profoundly affected oil production and gasoline refining in and near the Gulf of Mexico [239,240]. Indeed, an enduring structural break between crude oil and spot gasoline prices is attributed to this event [241].

4.2.2. Mean-Shift Clustering

Relative to spectral clustering, the mean-shift method finds nearly twice as many clusters. More intriguingly, mean-shift clusters deviating from the central tendency of energy-specific volatility gather on a single side of the three-dimensional t-SNE manifold.

Figure 20 shows how mean-shift clustering is based on centroids. The centroids indicated by numerals are visibly distinct from the apparent center of gravity for each cluster within the t-SNE manifold’s stylized three-dimensional space. Clusters 0 and 1, the two largest, exhibit the greatest apparent dislocation between centroids and individual instances. All other clusters, except perhaps clusters 2 and 7, are more likely to identify brief, compact events in the trading in crude oil and refined fuels. Such events likely arise from supply disruptions, as opposed to longer-lasting shifts in demand associated with broader crises affecting all commodities.

Figure 21 renders mean-shift results on an ordered timeline. Mean-shift clustering is manifestly more sensitive than spectral clustering. Cluster 0 plays its usual role as the fallback category. All clusters numbered higher than 1 are much smaller, containing (in two instances) as few as two days. Pronounced spikes are associated with the global financial crisis and the pandemic, as well as a previously undetected 2016 event.

Clusters 1 and 2, as the second- and third-largest clusters among the 15, fall between the extremes represented by cluster 0 and collectively by clusters 3 through 14. In addition to indicating several periods in the early 2000s, Cluster 1 brackets better known, already identified volatility events. It may be reasonably surmised that this cluster indicates the beginning or the end of distinctive events. Its appearance at the end of the peak of the pandemic reinforces what all-commodity clustering has already suggested: The pandemic arrived suddenly and began to relax almost as quickly.

Cluster 2 recurs on multiple occasions in the first half of this 20-year period and again in 2015. Those 60 trading days should share characteristics that distinguish them from the financial crisis, the 2016 event, and the pandemic.

Recombining mean-shift clusters from 15 into four—0, 1, 2, and all clusters numbered 3 or higher—provides a clearer picture. Figure 22 reports this summarized timeline.

4.2.3. Hierarchical Agglomerative Clustering

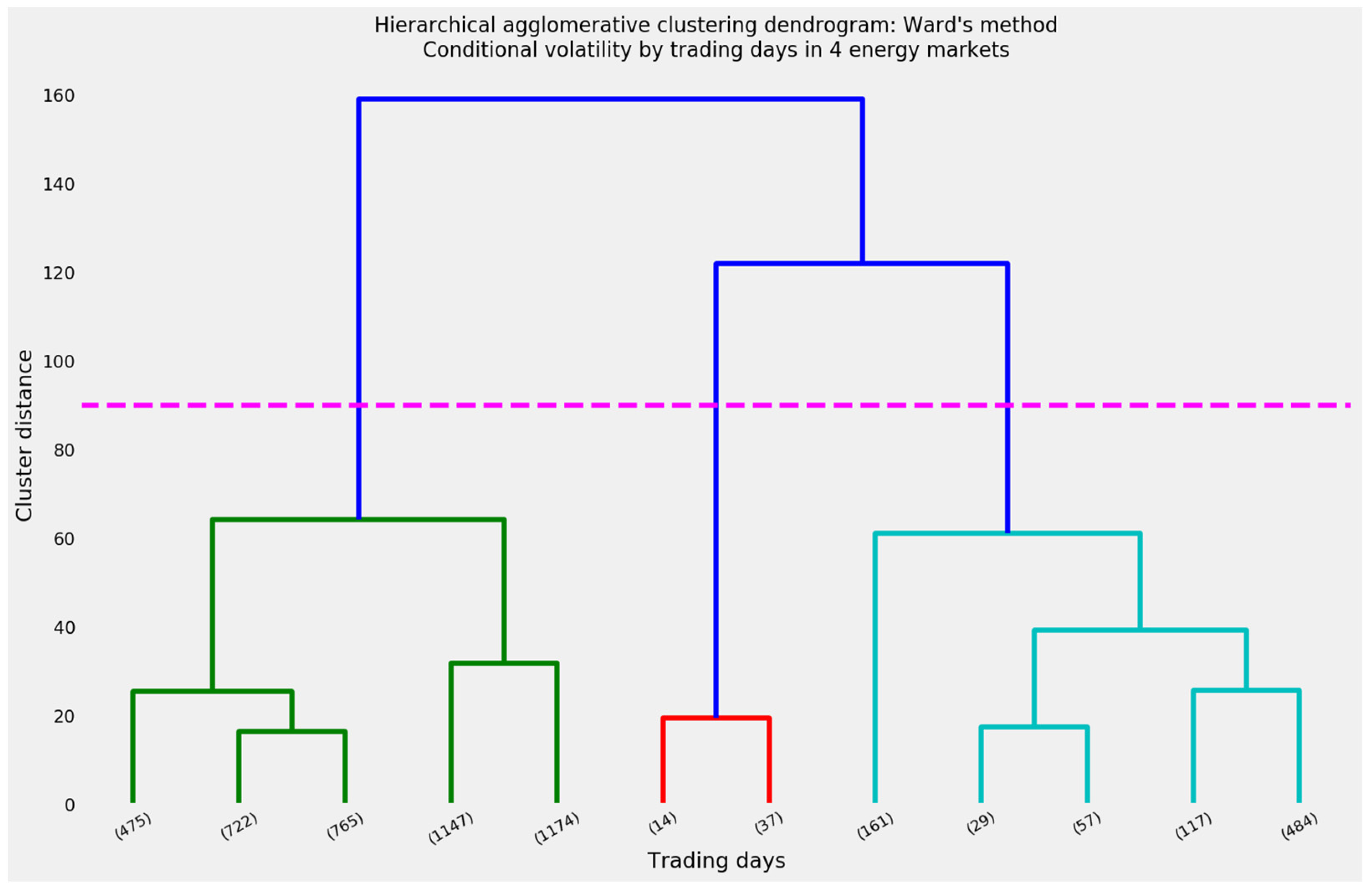

As a matter of visual interpretability as well as mathematical logic, hierarchical clustering begins with a dendrogram. Figure 23 suggests that the ideal number of clusters may be as low as three: A concentrated cluster of 51 trading days (not necessarily consecutive) in the middle in red, a moderately large supercluster of 848 days at right in cyan, and a very large supercluster of the remaining 4283 days at left in green. Deviating from cluster distance as a guide to the optimal value of k yields the 12 clusters along the bottom.

Distances within these 12 clusters average less than 30, as opposed to the distance of 60 separating a three-cluster configuration from its five-cluster alternative. Even so, many of these clusters will exhibit so little contiguity that it will take considerably more analyst judgment to cogently interpret hierarchical clustering.

The t-SNE manifold of hierarchical clustering in Figure 24 looks decidedly unlike the manifolds for spectral and mean-shift clustering. The affinity propagation and k-means manifolds will exhibit a shape similar to the hierarchical results. The greatest difference lies in the relative sizes and overlapping locations of the spheres representing the clusters. Aside from clusters 9, 2, 10, and perhaps 5, these clusters have large radii and overlap their neighbors. The centroids are synthetic, as in spectral clustering, and not stochastically instantiated, as in k-means. Overlapping spheres suggest that the adjoining clusters will not be perfectly contiguous, or even close to being so.

The ordered timeline in Figure 25 confirms these fears. Cluster 0, the closest representation of normal trading, has shorter stretches of uninterrupted, contiguous cogency than the default, background trading clusters under the spectral or mean-shift methods. Cluster 1, which appears during the financial crisis and the pandemic, also appears in 2001. Reducing the total number of clusters below the 15 clusters generated by mean-shift did not bring visible order to the timeline. Additional analyst judgment seems advisable.

Figure 26, the revised manifold, highlights the six smallest hierarchical clusters. A principled case can be made to include cluster 8, the seventh smallest among 12, because of its proximity to cluster 5 in the t-SNE manifold and in Figure 23′s dendrogram. On the other hand, cluster 8 adds 484 days to the 415 total days in clusters 1, 2, 5, 7, 9, and 10. At 415 total days, those clusters comprise almost exactly 8 percent of the 5182 trading days. Adding 484 days from cluster 8 would raise the share of critical trading days to more than 17 percent. For the sake of comparison, mean-shift clustering identified 609 trading days of interest, while spectral clustering found only 70.

Whether critical periods in energy commodity trading comprise 8 or 17 percent of an entire timeframe requires delicate analyst judgment. An incidental benefit of forecasting conditional volatility through GARCH is the ability to estimate the degrees of freedom for the t-distribution that best fits each series of returns. Figure 27 shows that the estimated degrees of freedom for energy-related commodities ranged between 3.03 (WTI) and 3.71 (gasoil). For an equally weighted market basket of oils and refined fuels, ν ≈ 3.51.

The degrees of freedom estimate enables the cumulative distribution function for Student’s t-distribution with location = 0 and scale = 1 to describe the size of the tails at a given value of ν. At this dataset’s estimates for ν, the two-tailed estimate for F(x | |x| > 2) ranges from 0.121634 for gasoil to 0.138395 for WTI. The estimate is 0.125950 for the equally weighted market basket. The one-tailed estimate would be exactly half of those values. The one-tailed estimate for F(x | x > 2) might be justified on the reasoning that volatility is invariably non-negative and that outliers found through clustering are likely to exhibit extremely high rather than extremely low volatility. That rationale, to say nothing of methodological conservatism, supports a smaller number of clusters.

By either measure, the six or seven smallest clusters occupy a distinct edge within Figure 26. All of the candidate clusters lie a palpable distance from the t-SNE manifold’s center of gravity. This is intriguing (if not altogether conclusive) visual evidence that a size-based criterion can successfully isolate outliers among trading days.

Figure 28 simplifies the ordered timeline in Figure 25 by reducing the more conservative six-cluster interpretation of hierarchical clustering into binary classification. Those six clusters have been aggregated into a single “critical” supercluster, while all other days are classified as a normal, noncritical background. In addition to the financial crisis and the pandemic, simplified hierarchical clustering identifies periods of interest in 2000, 2001, 2003, 2005, 2015, and 2016.

4.2.4. Affinity Propagation

The smaller size of the energy-specific subarray created immense difficulty with affinity propagation. Scaling the element preference matrix according to the median values for each series cannot reduce the number of clusters close to the range of eight to 15, the number of clusters found by the spectral and mean-shift methods. More aggressive efforts prevented the algorithm from converging. The smallest number of viable clusters in affinity propagation appears to be 32.

Affinity propagation generates a beautiful but deadly t-SNE manifold (Figure 29). The large number of overlapping clusters, many enveloped in spheres with moderate to large radii, suggests that this method yields highly atomized, noncontiguous clusters.

Figure 30 displays an ordered timeline whose clusters are extremely hard to interpret. Affinity propagation is even more chaotic than hierarchical clustering (Figure 25). The larger the number of clusters, the likelier that individual clusters will splinter internally. Identifying financially meaningful groups of trading days requires extensive work.

Experience with more tractable clustering methods suggests a way forward. Critical and ordinary trading days are not uniformly distributed. The very process used to forecast volatility—GJR(1, 1, 1)-GARCH—presumes heteroskedasticity in the sequence of logarithmic returns. All else being equal, clusters identifying extreme levels of volatility are likely to be smaller than clusters describing lower background levels.

A viable filter therefore consists of tagging affinity propagation clusters for further evaluation until the cumulative number of trading days reaches a certain threshold. The 415 out of 5182 days selected by hierarchical clustering provide a workable benchmark. Isolating the 14 smallest among 32 clusters yields 384 trading days, roughly 7.4 percent of the total. Adding a 15th cluster would add the 78 days from cluster 12 and raise the number of potentially critical days to 459, or nearly 8.9 percent. Because cluster 12 is so close to the 14 even smaller clusters, we included it. Fortuitously, that choice ultimately made no difference in aggregation through voting.

Figure 31 isolates the 15 smallest affinity propagation clusters. As expected, these clusters occupy the left edge of the t-SNE manifold and resemble the critical clusters chosen by hierarchical clustering (Figure 26). Four subgroups are evident: Two appear closer to the top: Clusters 7 and 8 in one supercluster and clusters 11, 23, and 26 in another beneath it. Clusters 28 through 31 occupy the far upper left. Finally, clusters 1, 12 through 15, and 25 comprise a more diffuse but still distinct supercluster at lower left.

Figure 32 isolates these four superclusters. The first three superclusters cover contiguous or nearly contiguous periods corresponding to energy-trading events in 2005, 2016, and 2020. The last of these plainly covers the COVID-19 pandemic—specifically, its frantic first weeks. Clusters in 2005 and 2016, wholly distinct from the financial crisis and the pandemic, imply the occurrence of events quantitatively distinct from the fourth supercluster. Those clusters unite several events in the early 2000s and the back half of the pandemic with the financial crisis.