Does the Volatility of Oil Price Affect the Structure of Employment? The Role of Exchange Rate Regime and Energy Import Dependency

Doctoral School, Cracow University of Economics, 31-510 Cracow, Poland

Energies 2022, 15(19), 6895; https://0-doi-org.brum.beds.ac.uk/10.3390/en15196895

Submission received: 23 August 2022

/

Revised: 13 September 2022

/

Accepted: 15 September 2022

/

Published: 21 September 2022

(This article belongs to the Special Issue Global Market for Crude Oil II)

Abstract

:The volatility of oil price as a key energy resource for modern economies has a significant impact on the macroeconomic situation. In addition to affecting aggregated production, consumption, employment and inflation, oil shocks can affect the economy in a more nuanced way. One consequence of the turmoil in the oil market may be a shift in the employment structure between the tradable and non-tradable sectors, which we investigate in this paper. The aim of this study is to test how oil price volatility affects the structure of employment in Central and Eastern European countries. Our main hypothesis is that oil price volatility causes a temporal employment reallocation between tradable and non-tradable sectors. To verify this assumption, we created Interacted Panel VAR (IPVAR), which showed that the shocks of oil price volatility affect the employment structure and this impact is conditioned by the level of dependence on energy imports and the exchange rate regime. The constructed impulse response functions showed that, in general, oil price volatility causes a temporal fall in relative employment in the manufacturing (tradable) sector. For periods of an above-average import of energy, the exchange rate regime does not matter for the response of the structure of employment. Inversely, when countries are less dependent on imports of energy, the exchange rate regime matters for shock absorption—for floats, oil price shocks cause a temporal fall in relative employment in manufacturing, whereas for pegs, there is a slight relative increase in employment in manufacturing.

1. Introduction

The oil crisis of the1970s entailed extensive research on the impact of oil price fluctuations on economies [1]. High oil prices combined with poor economic performance in the USA triggered research that resulted in the publication of many seminal papers linking both phenomena. Hence, the period of the 1970s was full of research touching upon the linkages between the oil market and the real economy [2]. Although the subsequent oil shocks did not cause such major economic turmoil as in the 1970s [3], the oil market may still exert impact on economies. It should be emphasized that large shocks affect many countries at the same time, which means that they can shape the global economic situation. Nowadays, as a result of the Russian invasion of Ukraine, the prices of energy have risen to historically high levels. By the end of the first quarter of 2022, the price of crude oil had doubled, and these tendencies of increased energy prices do not seem to be reversing [4]. Considering the current high prices of brent oil and heralded energy shortages in Europe, the issue of energy supply shocks seems to gain importance again.

Oil price fluctuations have many implications for economies. There are many studies examining the impact of oil prices on global production [5], consumption [6] and inflation [7]. One such strand of this literature is the influence of oil price on the labor market. In general, we can suppose that increasing prices of oil will lead to a reduction in production and employment, but oil price turmoil can also change the labor market in a more indiscernible manner. There are some indications that oil price volatility can affect the structure of employment and lead to job reallocation between different sectors and industries.

The beginnings of research on the role of oil shocks in labor reallocation can be found in the work of Lilien [8], who pointed to the fact that a considerable fraction of unemployment can be explained by the industry-level dispersion of employment growth. These findings were extended by Loungani [9], who proved that the processes of employment reallocation between different industries was highly determined by sharp oil price increases in the 1950s and 1970s. According to a neoclassical model of unemployment and business cycle by Hamilton [10], even a small disruption on the markets of primary commodities, such as energy, can result in fluctuations of aggregate employment. An interesting development of this model is the question how fluctuations of energy supply affect the structure of employment. This model is based on papers by Davis [11] and Loungani [9], in which shortages of energy on the market caused sectoral imbalances. In the model by Hamilton [10], an increase in the price of energy results in reduced consumption of energy-intensive goods. In an environment of relatively high labor mobility, this will lead to employment reallocation to labor-intensive industries.

Empirical research on the relationship between the oil market and employment reallocation seem to be in line with the theoretical models. In the work of Davis and Haltiwanger [12], employment growth and unemployment rates are characterized by temporal asymmetry, whereas production and its growth rate are not. According to the authors, it is indicative of the existence of cycles that lead to sectoral shifts of production. One of the factors affecting employment shifts are oil shocks that account for 20–25% variability of employment growth in the manufacturing sector—in the short-run, job destruction is much more sensitive to oil shocks than job creation, which results in the reallocation of employment. In the same manner, Uri [13] explained a fraction of turmoil in agricultural employment in the United States. According to Papapetrou [14], oil price shock had an immediate negative impact on industrial employment and production in Greece. Ewing and Thompson [15] showed that there is contemporaneous negative correlation between crude oil prices and unemployment cycles. In a study by Koirala and Ma [1], different sectors responded differently to oil shocks, which also suggests that the oil can influence the reallocation of labor between different sectors. In turn, Herrera et al. [16] touched upon the adjustment process of oil shock absorbing. The authors showed that in the first year, after oil price decrease, net employment decreases as employees move from closing jobs to expanding ones in manufacturing and in services, but in the next year, job creation exceeds job destruction, contributing to the increase in net employment.

Interestingly, it is not always the level of oil price that can affect employment—uncertainty about future price and its volatility can also exert impact on the labor market. In a nutshell, oil prices fluctuations can affect the costs of production, affect consumer prices and spark uncertainty that leads to postponing investments and cutting on production, which exerts pressure on the labor market [17]. Elder [18] showed that oil price uncertainty affects private sector unemployment. Moreover, there are differences in employment fluctuations between sectors producing goods and services. In manufacturing industries that are typically producing tradable goods, global shocks can lead to relative price changes [19]. Hence, oil price volatility may affect services (as a proxy for non-tradable sector) and manufacturing differently. In turn, in a study by Michieka and Gearhart [20], fluctuations of oil price affect employment in natural resources and mining, trade, and transportation in the USA. In the work of Jo [5] oil price uncertainty shocks (proxied by the crude oil volatility index) are causing global slowdown in economic activity. Interestingly, in this paper, uncertainty solely causes a decline in the industrial production growth rate, irrespective of actual price-level changes. It means that the price of oil does not have to go up to cause employment fluctuations—it can be the volatility that sparks changes in the labor market.

Although there is a lot of research on the relationship between oil price and the labor market, they have some key drawbacks. Michieka and Gearhart [20] claimed that the current literature ignores the aspect of sectoral employment changes in response to oil price fluctuations. Papers that are devoted to the question of the labor market effects of oil shocks in sectors [18,20] are based on models for individual sectors/industries, which gives only a partial picture of employment reallocation. Additionally, existing studies are based on dated empirical methods and there is a need to employ new, advanced econometric techniques in the studies. Moreover, most of the research on the topic are for the USA, but there are few works that focus on countries that are not exporters of oil (in these countries oil price shocks are highly exogenous factors and can bring different economic outcomes). A peripheral research issue for non-oil exporting countries is the role of the level of energy import dependency, which is not often considered in empirical studies. Another question—suggested, for example, by Koirala and Ma [1]—is the role of exchange rate as an external shock absorber.

The aim of this study is to test how oil price volatility affects the structure of employment in Central and Eastern European (CEE) countries, including Czechia, Estonia, Hungary, Latvia, Lithuania, Poland, Slovakia and Slovenia. To do this, we incorporate the Interacted Panel VAR (IPVAR) model introduced by Towbin and Weber [21] and create impulse response functions, showing how oil price volatility shocks affect the index of employment structure (employment in manufacturing to employment in services as a proxy for tradable and non-tradable sectors, respectively). In this modeling framework, we depart from investigating employment in individual sector and create an index that provide more general picture of employment reallocation in response to oil price volatility shocks. Additionally, thanks to the use of the IPVAR model, we can control for the role of the de facto exchange rate regime and the level of energy import dependency in the CEE region. Our main hypothesis is that oil price volatility causes a temporal employment reallocation between tradable and non-tradable sectors. Our detailed hypothesis is that the exchange rate regime and the level of energy import dependency matter for the final effect of employment reallocation. These hypotheses will be verified on the basis of the analysis of the impulse response functions created for the proposed IPVAR model.

The results of the research showed that oil price volatility has a short-term impact on the structure of employment in the CEE region. In our baseline model (without interaction terms), oil price volatility shock causes a relative fall in employment in manufacturing that lasts for the first five quarters, and afterward there is a relative increase in employment in manufacturing that lasts for the following six to seven quarters. After this period, the relationship between employment in manufacturing and services returns to the pre-shock stability. Nevertheless, our extended models with interaction terms show that the relationship between the oil market and the employment structure is dependent on the level of energy imports and the exchange rate regime. In periods of exceptionally high energy import dependency (above 30th percentile), oil price volatility shocks cause a relative fall in employment in manufacturing, but for periods of lower import of energy, these effects are weaker. Additionally, we show that for periods of above-average import of energy, the exchange rate regime does not matter for the response of the structure of employment. Inversely, when countries are less dependent on imports of energy, the exchange rate regime matters for shock absorption—for floats, oil price shocks cause a temporal fall in relative employment in manufacturing, whereas for pegs, there is a slight relative increase in employment in manufacturing that lasts for approximately 10 quarters after the initial shock.

We contribute to the literature by providing a more general picture of employment reallocation in response to oil price shocks. Additionally, thanks to the use of the IPVAR model, we control for the role of exchange rate regime and energy import dependency in absorbing oil price volatility shocks on the labor market. Our study proved that the relationship between oil price volatility and employment reallocation is not as straightforward as in previous research. We also showed that exchange rate regime and the level of energy import dependency can magnify and reduce employment fluctuations.

The rest of the paper is structured as follows: the second section presents empirical strategy and data; in the third part, we present the results of empirical analysis; and in the last section, our results are discussed.

2. Materials and Methods

Our econometric method is the Interacted Panel VAR (IPVAR) model from Towbin and Weber [21]. The main advantage of this model is the possibility to employ interaction terms that affect the relationship between selected endogenous variables in our research. In standard VAR modeling, we can add exogenous dummy variables, but they have influence on the whole system of equations. In the IPVAR model, we can choose which equations are affected by our interaction terms. Moreover, in the case of employing an exchange rate regime dummy, we do not have to divide our sample into countries with pegs and floats because in the IPVAR modeling framework, interaction terms for each country can be time variant [22]. Finally, we can introduce two interaction terms in the same model to test how the employment structure is affected by oil price volatility, controlling for the role of exchange rate regime and energy import dependency at the same time.

In our baseline specification, we do not introduce the interaction terms in order to check the impulse response for the whole region of CEE. The model for the i-th country and L lags takes the following recursive form:

where is a lower triangular matrix (with ones on the main diagonal), is a vector of explanatory variables, is a vector with cross-country heterogenous intercepts, denotes a matrix with coefficients up to lag L, and is a vector of residuals that are assumed to meet the white noise conditions (uncorrelated across countries and normally distributed).

In the next step, we create the model, including the interaction terms:

where is a matrix of interaction terms.

As the recursive form of models given in (1) and (2) implies that error terms are not cross-country correlated, we can proceed with simple equation-by-equation OLS estimation. In order to create impulse response functions, we use Cholesky decomposition with variables ordered from the least to the most endogenous. We are aware that the use of Cholesky decomposition makes the system of equations vulnerable to the ordering of variables. However, following the seminal paper by Blanchard and Gali [3]—which had very similar variables and methodology—we decided to utilize this method of decomposition. In this paper, the model for employment has oil shocks as the first variable and the last one is the employment variable, which is preceded by the GDP variable. Hence, the vector of endogenous variables for the i-th country takes the following form:

where is external variable (logarithm of oil price volatility), is internal variable (GDP growth rate), and is our second internal variable (the employment structure index).

We analyze the role of oil price volatility in shaping the structure of employment in the countries of Central and Eastern Europe (Czechia, Estonia, Hungary, Lithuania, Latvia, Poland, Slovakia and Slovenia). In the study, we use quarterly data at levels ranging from Q1-2006 to Q4-2021 (64 observations) employed in our IPVAR model with four lags.

2.1. External Variable—Oil Price Volatility

To capture the role of oil price uncertainty, we extract brent oil quarterly prices from the Federal Reserve Bank of St. Louis database. In the next step, we create a volatility index based on the following formula presented in Broto et al. [23]:

where is the sum of the squares of the differences between the value of the oil price in period t and the average value of oil price for periods k to t, and n is the number of periods in a year. In order to obtain the stationarity of the variable, the calculated logarithms of the data obtained form (4).

2.2. First Internal Variable—GDP Growth Rate

Our second variable is GDP growth rate (quarter to quarter). This variable is introduced in the model in order to control for job reallocation affected by internal factors. In our modeling framework, GDP growth and employment interact with each other—job reallocation results in increased productivity contributing to economic growth rate, and GDP growth can result in job creation. The GDP variable appears also in similar papers by Blanchard and Gali [3] and Jo [5]. The data were extracted from the Eurostat database.

2.3. Second Internal Variable—Employment Structure

Our second internal variable is the index of employment structure calculated as employment in manufacturing divided by employment in services. In our modeling framework, employment in manufacturing is a proxy for the production of tradable goods, whereas employment in services approximate for production in non-tradable sectors.

The advantage of this index is that it shows the structure of employment in a country, and this measure is normally distributed and stationary at levels. In our modeling framework, employment in manufacturing and services are in a stable relationship that is temporarily affected by external (or internal) shocks, such as oil price volatility. As far as we know, this is the first paper in this field of research to utilize such an index.

2.4. Interaction Terms

We include two interaction terms in the form of dummy variables. The first one is the energy import dependency index taken from the Eurostat database. This variable shows the share of energy demand that is imported to a country. We suppose that higher external energy sources dependency will magnify the external energy shocks in economies; hence, we employ this dummy variable depending on the share of energy import. We define this dummy as 1 for periods when the energy import dependency index is above or under a given percentile for a country.

The next interaction term is the de facto exchange rate regime extracted from Ilzetzki et al. [24]. As pointed out in the Introduction, other authors suggest that the exchange rate can also affect the relationship between oil prices and employment (see [1]). For our dummy, the floating regime takes the value of one, and the pegged regime takes the value of zero.

3. Results

According to Towbin and Weber [21], all of the variables for IPVAR modeling need to be integrated at the same level, thus we have to perform the stationarity test. We decided to conduct the Im–Pesaran–Shin unit root test for heterogenous panels [25]. The obtained results are presented in Table 1.

As we can see, for 5% level of significance, all of the variables have no unit root. It means that all of the data are stationary at levels, and we can employ them in our IPVAR models.

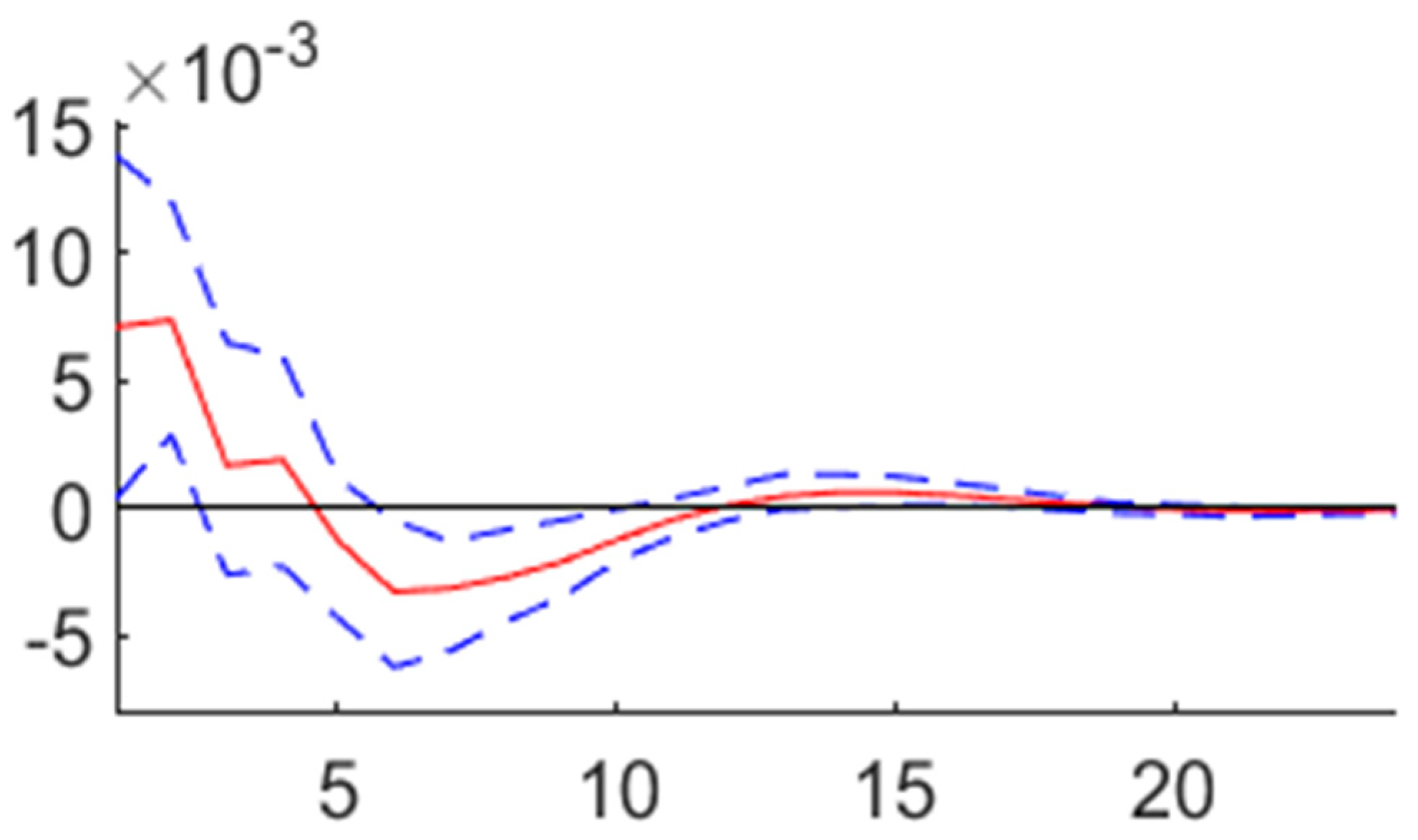

In the next step, we proceed with our first model with three endogenous variables and no interaction terms. The impulse response function of the employment index to the shock in oil price volatility is presented in Figure 1.

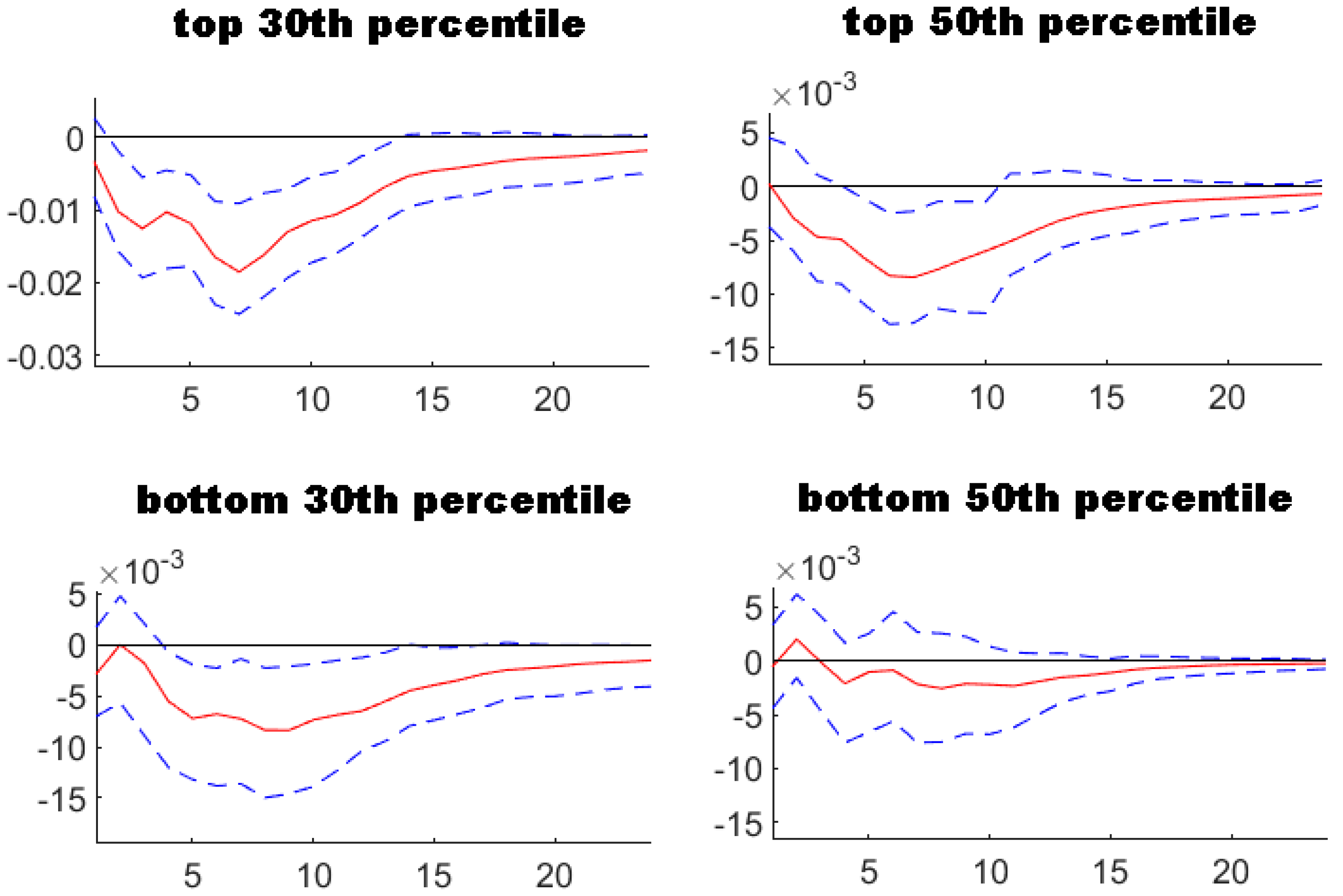

In the first reaction to the shock, the value of the employment index is above zero, which means that the oil price volatility shock results in relatively higher employment in the manufacturing sector. After 5 quarters we can see increasing employment in services, but the shock dies out after approximately 12 quarters. These results hold for the whole region of CEE. However, we need to take a closer look at these processes. Hence, in the next step, we estimate models in which we control for the role of energy import dependency and the exchange rate regime. Figure 2 shows the impulse response function estimated with the interaction term of import energy dependency.

As we can see, the models with interaction terms gave different results than the baseline specification. Energy import dependency has the biggest impact on the relationship between oil price volatility and employment structure in periods with energy imports dependency above the 30th percentile. It means that for periods with energy import dependency above its top 30th percentile, the effect of job structure fluctuation is the biggest—for these periods, oil price shocks cause job reallocation from manufacturing to services. The average value of the index of employment for the CEE countries in the period investigated equals 0.34, and the impulse response function for periods of the top 30th percentile of energy import dependency shows a fall by 0.02. It means that in response to oil volatility shocks, employment in manufacturing drops on average by 5.9% more than employment in services (the index falls from 0.34 to 0.32). Generally, for the remaining specifications, the impulses follow a similar direction (relative decline in employment in the manufacturing sector), but the impact of external oil shocks on the structure of employment is much smaller. These results suggest that the relationship between energy import dependency and the employment reallocation effects of oil shocks is not linear—employment fluctuations are the biggest when energy import dependency is exceptionally high, but for other periods the level of energy imports seems to be of minor importance for job reallocation. The observed regularities favor our threshold approach in capturing the role of energy import dependency. Interestingly, interaction terms in IPVAR models do not have to be dummy variables. If we assume that the relationship between endogenous variables and interaction terms is linear, we can employ real values of the interaction term (see [21]).

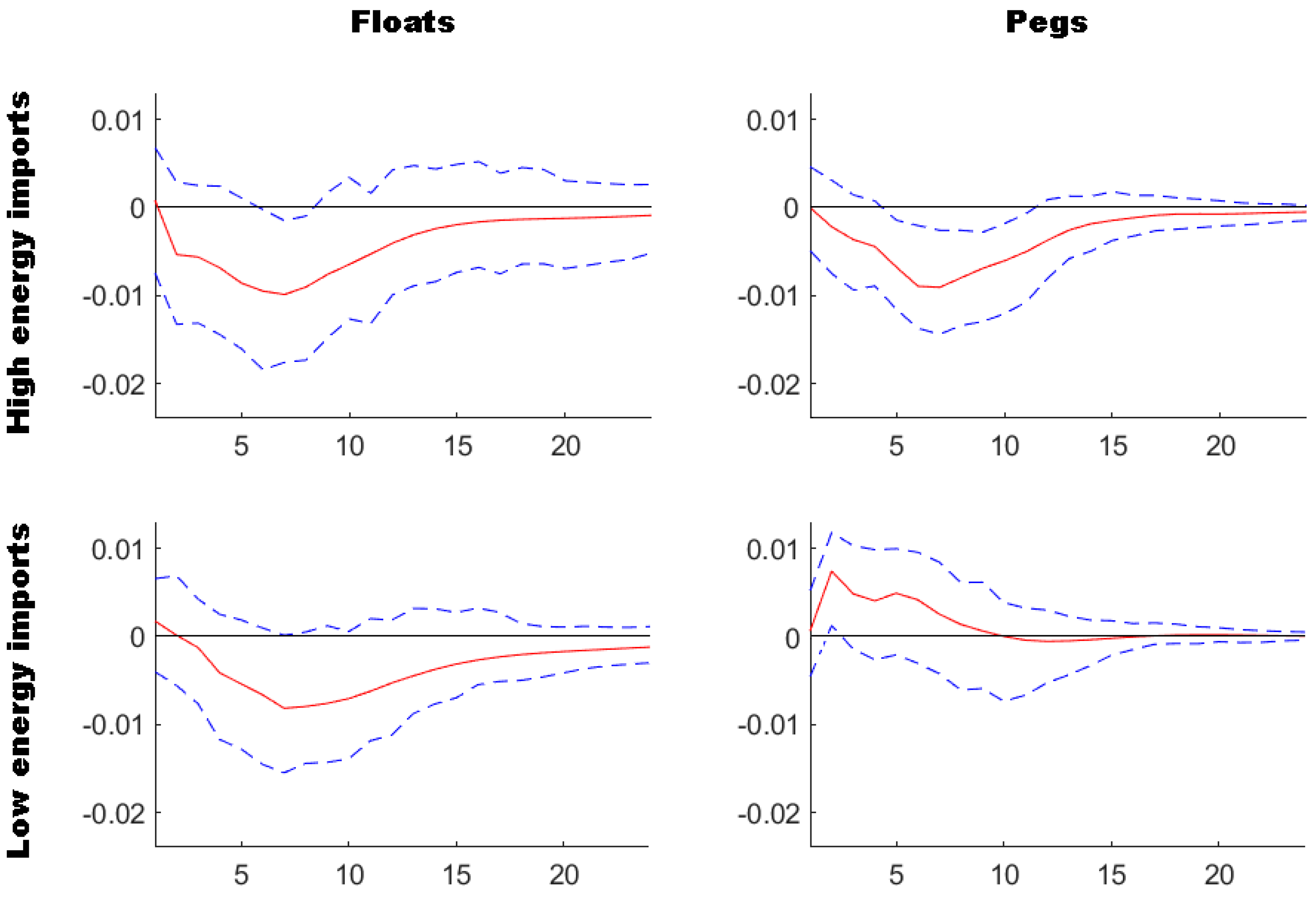

In the final model, we add our second interaction term—the exchange rate regime dummy. The impulse response functions are presented in Figure 3.

Comparing impulse response functions in the first row, we can see that for periods with high energy import dependency (defined as energy import dependency above 50th percentile), the de facto exchange rate regime does not matter for shock absorbing. Overall, in times of high import of energy, oil price volatility shocks cause a decrease in the value of the employment index, which means that relative employment in the manufacturing sector falls. The minimum of the impulse response function for both exchange rate regimes is in the 6th–7th quarters, when the changes in the structure of employment are the sharpest. As was noted, the average value of the employment index is 0.34, which means that for periods of above average energy import dependency, employment in manufacturing drops on average by 3% more than employment in services (a decrease of about 0.01) irrespective of the exchange rate regime. However, after the 6th–7th quarter, the functions start to go up, and after a few following quarters, the impulses seem to die out.

In the case of impulse response functions for periods of relatively low energy import dependency (defined as energy import dependency under the 50th percentile), we can see that the shock causes different reactions of employment depending on the exchange rate regime. For floats, the impulse response function is similar to the one obtained for periods of high energy import dependency—there is a relative increase in the role of employment in services that is the biggest in the 7th and 8th quarters. For pegs, in periods of low energy import dependency, the function is completely different than for the other specifications. As we can see, oil price volatility shocks cause a temporal increase in the role of employment in the manufacturing sector instead of employment in services. There are also other differences—the peak of the impulse response function appears earlier than for the other specification (two quarters after the initial shock). It means that for pegs, the reaction of the structure of employment is more abrupt than for floats, but at the same time, the value of the index returns to its pre-shock value quicker (the impulse dies out after approximately 15 quarters).

4. Conclusions and Discussion

To sum up, the main conclusion of our empirical study is that oil price volatility affects the structure of employment in countries of Central and Eastern Europe. In our baseline model (without interaction terms), oil price volatility shock causes a relative fall in employment in manufacturing that lasts for the first five quarters, and afterwards there is a relative increase in employment in manufacturing that lasts for the following six to seven quarters. After this period, the relationship between employment in manufacturing and services returns to the pre-shock stability. Nevertheless, our extended models with interaction terms show that the relationship between the oil market and the employment structure is dependent on the level of energy imports and the exchange rate regime. In periods of exceptionally high energy import dependency (above 30th percentile), oil price volatility shocks cause a relative fall in employment in manufacturing (employment in manufacturing drops on average by 5.9% more than employment in services), but for periods of lower import of energy, these effects are weaker. Additionally, we show that for periods of above average import of energy, the exchange rate regime does not matter for the response of the structure of employment. For periods of above average energy import dependency, employment in manufacturing drops on average by 3% more than employment in services irrespective of the exchange rate regime. Inversely, when countries are less dependent on imports of energy, the exchange rate regime matters for shock absorption—for floats, oil price shocks cause a temporal fall in relative employment in manufacturing, whereas for pegs, there is a slight relative increase in employment in manufacturing that lasts for approximately 10 quarters after the initial shock.

Our study confirmed the latest findings about sectoral changes of employment in response to oil price shock presented by Michieka and Gearhart [20] and Elder [18]. Nevertheless, our results go beyond the framework of examining individual industries and sectors separately. In this paper, we managed to test how the volatility of oil prices affects the employment structure broken down into the tradable and non-tradable sectors. Our impulse response functions showed that the relationship between employment in these sectors is subject to periodic fluctuations due to the volatility of oil prices. Additionally, we proved that exchange rate regime and the level of energy import dependency matter for the final effect on the labor market.

However, we are aware of the limitations of this study. First of all, we have only tested a small group of countries, so we cannot draw more general conclusions about the relationship between the oil market and the labor market. Secondly, our sensitivity analysis was limited only to checking how the model reacts to different levels of energy import dependency. We only used one measure of oil price volatility in this paper, and we cannot rule out that other measures of volatility or uncertainty may give different results. Additionally, in our study, we did not take into account the volatility of prices of other energy sources, which could also have been important for the results obtained.

Nevertheless, the results of our analysis have some implications for both policymakers and other researchers. First of all, we show that the volatility of oil price exerts impact on the labor market in non-oil exporting countries. The turmoil in the oil market affects not only production and employment, but can also affect the labor market in a more nuanced way. This means that the stability of the relationship between the tradable and non-tradable sectors (proxied by the manufacturing sector and services, respectively) is disturbed in periods of high volatility in oil prices. From a political point of view, this is of great importance given the country’s dependence on international trade. External shocks can entail changes in terms of employment, wages and prices between the tradable and non-tradable sectors—in times of energy market shocks policymakers face the challenge of preventing the build-up of inequalities within countries. Hence, in times of oil shocks the diagnosis of the dynamics of changes between these sectors gains in importance.

The obtained results of the study are of particular importance given the fact that by the end of the first quarter of 2022, the price of crude oil had doubled, and these tendencies of increased energy prices do not seem to be reversing [4]. The presented impact of oil shocks on the labor market highlights the importance of the energy policy of Central and Eastern European countries. The obtained results show how important for macroeconomic stability the diversification of energy sources is, both in terms of the share of individual types of energy in the energy mix and the region of origin of the imported energy. This issue additionally emphasizes the need to reduce energy imports and to increase the production of local renewable energy in the region, which is the responsibility of policymakers.

Another question is the role played by the level of energy import dependency and exchange rate regime that has to be taken into account by policymakers. In our study, we proved that for periods of exceptionally high levels of energy import dependency, the employment reallocation is significantly bigger, which should be calculated as a cost of high external energy dependency of these countries. Hence, policymakers need to take account of the fact that in times of oil price volatility, the level of energy dependency is not neutral to the labor market in countries from Central and Eastern Europe. The same also applies to exchange rate regimes that also matter for absorption of oil shocks. We showed that for periods of relatively low energy import dependency, the de facto exchange rate regime matters for the labor market. For pegs and floats, oil price volatility can result in different adjustment processes that vary in terms of the strength, direction, and duration, which policymakers should also bear in mind.

We also have some remarks for other researchers. First of all, we show that the relationship between oil price and the labor market is not as straightforward as one can think. We proved that the effect of oil price volatility shocks on the structure of employment is conditioned by the exchange rate regime and the level of energy import dependency, but the intricacies of these regularities require more in-depth consideration using alternative econometric approaches and measures.

Another interesting direction for other researchers may also be to study the impact of the price volatility of other energy sources. Individual countries may differ from each other in terms of the share of oil in their energy mix; therefore, for some countries, considering other energy sources in the study may also bring interesting results.

One of the side issues in our research is how to include the variable of employment in the VAR class models. In the case of a simple measure, such as a number of employees, building the model at levels would be difficult due to the high risk of non-stationarity of time series, which would result in the need to build the model for first differences of time series (which entails significant information loss). If, on the other hand, we construct a simple employment index as the value of employment in manufacturing to employment in services, we can obtain an intuitive index that is likely to meet the assumption of stationarity for data at levels. We think that this hint can be very useful for other researchers.

Funding

This publication was financed from the subsidy No. 59/GAE/2020/POT granted to the Cracow University of Economics and from the author’s own funds.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Koirala, N.P.; Ma, X. Oil price uncertainty and U.S. employment growth. Energy Econ. 2020, 91, 104910. [Google Scholar] [CrossRef]

- Barsky, R.B.; Kilian, L. Oil and the Macroeconomy Since the 1970s. J. Econ. Perspect. 2008, 18, 115–134. [Google Scholar] [CrossRef]

- Blanchard, O.J.; Gali, J. The macroeconomic effects of oil shocks. Why are the 2000s so different from the 1970s? NBER Work. Pap. 2007, 13368. [Google Scholar] [CrossRef]

- Ari, A.; Arregui, N.; Black, S.; Celasun, O.; Iakova, D.; Mineshima, A.; Mylonas, V.; Parry, I.; Teodoru, I.; Zhunussova, K. Surging Energy Prices in Europe in the Aftermath of the War: How to Support the Vulnerable and Speed up the Transition Away from Fossil Fuels. IMF Working Papers 2022, WP/22/152. pp. 1–41. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4184693 (accessed on 22 August 2022).

- Jo, S. The Effects of Oil Price Uncertainty on Global Real Economic Activity. J. Money Credit Bank. 2014, 46, 1113–1135. [Google Scholar] [CrossRef]

- De Michelis, A.; Ferreira, T.R.; Iacoviello, M. Oil Prices and Consumption Across Countries and U.S. States. Int. Financ. Discuss. Pap. 2019, 1263, 1–36. [Google Scholar]

- Choi, S.; Furceri, D.; Loungani, P.; Mishra, S.; Poplawski-Ribeiro, M. Oil prices and inflation dynamics: Evidence from advanced and developing economies. J. Int. Money Financ. 2019, 82, 71–96. [Google Scholar] [CrossRef]

- Lilien, D.M. Sectoral Shifts and Cyclical Unemployment. J. Political Econ. 1982, 90, 777–793. [Google Scholar] [CrossRef]

- Loungani, P. Oil Price Shocks and the Dispersion Hypothesis. Rev. Econ. Stat. 1986, 68, 536–539. [Google Scholar] [CrossRef]

- Hamilton, J.D. A Neoclassical model of Unemployment and the Business Cycle. J. Political Econ. 1988, 96, 593–617. [Google Scholar] [CrossRef]

- Davis, S.J. Allocative Disturbances and Temporal Asymmetry in Unemployment Rate Fluctuations; Chicago Graduate School of Business Paper; Chicago Graduate School of Business: Chicago, IL, USA, 1988; pp. 1–33. [Google Scholar]

- Davis, S.J.; Haltiwanger, J. Driving forces and employment fluctuations. NBER Work. Pap. 1996, 5775, 1–61. [Google Scholar]

- Uri, N.D. Changing crude oil price effects on US agricultural employment. Energy Econ. 1996, 18, 185–202. [Google Scholar] [CrossRef]

- Papapetrou, E. Oil price shocks, stock market, economic activity and employment in Greece. Energy Econ. 2001, 23, 511–532. [Google Scholar] [CrossRef]

- Ewing, B.T.; Thompson, M.A. Dynamic cyclical comovements of oil prices with industrial production, consumer prices, unemployment, and stock prices. Energy Policy 2007, 45, 5535–5540. [Google Scholar] [CrossRef]

- Herreraa, A.M.; Karakib, M.B.; Rangarajuc, S.K. Where do jobs go when oil prices drop? Energy Econ. 2017, 64, 469–482. [Google Scholar] [CrossRef]

- Kisswani, A.M.; Kisswani, K.M. Modeling the employment–oil price nexus: A non-linear cointegration analysis for the U.S. market. J. Int. Trade Econ. Dev. 2019, 28, 902–918. [Google Scholar] [CrossRef]

- Elder, J. Employment and energy uncertainty. J. Econ. Asymmetries 2020, 21, e00159. [Google Scholar] [CrossRef]

- Ewing, B.T.; Yang, B. Manufacturing and non-manufacturing employment, exchange rate and oil price: A US state-level time series analysis. Int. J. Econ. Soc. Res. 2009, 5, 1–22. [Google Scholar]

- Michieka, N.M.; Gearhart, R.S., III. Oil price dynamics and sectoral employment in the U.S. Econ. Anal. Policy 2019, 62, 140–149. [Google Scholar] [CrossRef]

- Towbin, P.; Weber, S. Limits of floating exchange rates: The role of foreign currency debt and import structure. J. Dev. Econ. 2013, 101, 179–194. [Google Scholar] [CrossRef]

- Dąbrowski, M.A.; Wróblewska, J. Insulating property of the flexible exchange rate regime: A case of Central and Eastern European countries. Int. Econ. 2020, 162, 34–49. [Google Scholar] [CrossRef]

- Broto, C.; Díaz-Cassou, J.; Erce, A. Measuring and explaining the volatility of capital flows to emerging countries. J. Bank. Financ. 2011, 35, 1941–1953. [Google Scholar] [CrossRef]

- Ilzetzki, E.; Reinhart, C.M.; Rogoff, K. Exchange Rate Arrangements in the 21st Century: Which Anchor Will Hold? Q. J. Econ. 2019, 134, 599–646. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, H.M.; Shin, Y. Testing for unit roots in heterogeneous panels. J. Econom. 2003, 115, 53–74. [Google Scholar] [CrossRef]

Figure 1.

Impulse response function for the baseline specification. Note: the area between the dotted lines represents the 90% confidence interval.

Figure 1.

Impulse response function for the baseline specification. Note: the area between the dotted lines represents the 90% confidence interval.

Figure 2.

Impulse response functions with an interaction term of different levels of energy import dependency. Notes: the area between the dotted lines represents the 90% confidence interval.

Figure 2.

Impulse response functions with an interaction term of different levels of energy import dependency. Notes: the area between the dotted lines represents the 90% confidence interval.

Figure 3.

Impulse response functions with interaction terms of energy import dependency and exchange rate regime. Notes: the area between the dotted lines represents the 90% confidence interval.

Figure 3.

Impulse response functions with interaction terms of energy import dependency and exchange rate regime. Notes: the area between the dotted lines represents the 90% confidence interval.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Im–Peasaran–Shin test for stationarity.

| Variable | t-Statistic | p-Value |

|---|---|---|

| ln(oil price volatility) | −1.74 | 0.041 ** |

| GDP growth rate | −20.35 | <0.01 *** |

| Employment index | −3.15 | <0.01 *** |

Notes: test conducted for data at levels, Schwarz criterion, max lags: 4. *, ** and *** denote 10%, 5%, and 1% level of significance, respectively.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Adamczyk, P. Does the Volatility of Oil Price Affect the Structure of Employment? The Role of Exchange Rate Regime and Energy Import Dependency. Energies 2022, 15, 6895. https://0-doi-org.brum.beds.ac.uk/10.3390/en15196895

AMA Style

Adamczyk P. Does the Volatility of Oil Price Affect the Structure of Employment? The Role of Exchange Rate Regime and Energy Import Dependency. Energies. 2022; 15(19):6895. https://0-doi-org.brum.beds.ac.uk/10.3390/en15196895

Chicago/Turabian StyleAdamczyk, Piotr. 2022. "Does the Volatility of Oil Price Affect the Structure of Employment? The Role of Exchange Rate Regime and Energy Import Dependency" Energies 15, no. 19: 6895. https://0-doi-org.brum.beds.ac.uk/10.3390/en15196895

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.