The Seasonal Fluctuation of Timber Prices in Hyrcanian Temperate Forests, Northern Iran

,

,

,

,  and

and

Abstract

:1. Introduction

2. Materials and Methods

2.1. Study Area and Data Source

2.2. Calculations

2.2.1. Unit Root Test

2.2.2. Multiple Linear Regression Analysis

2.2.3. Decomposition of the Price Time Series

2.3. Similarity of the Seasonal Indices of Timber Price and Construction Activity

3. Results

3.1. Descriptive Statistics

3.2. ADF Test

3.3. The Linear Regression Parameter

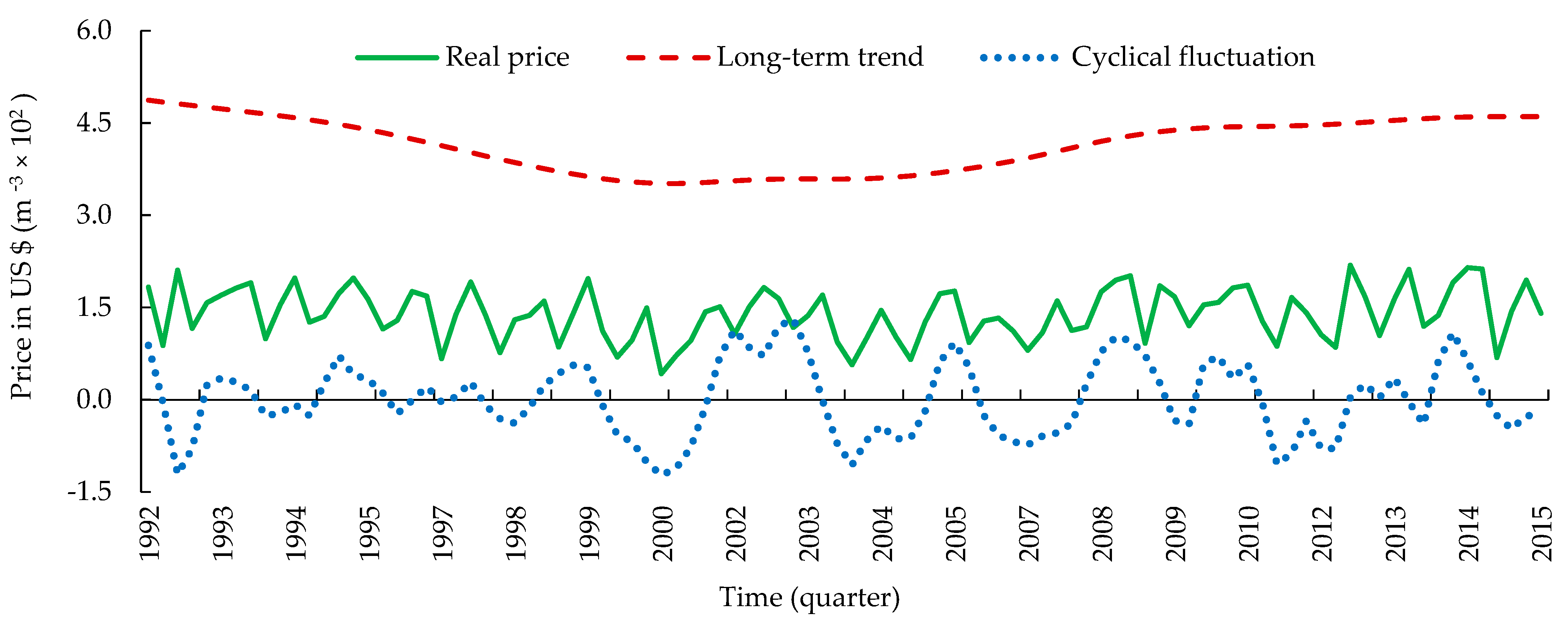

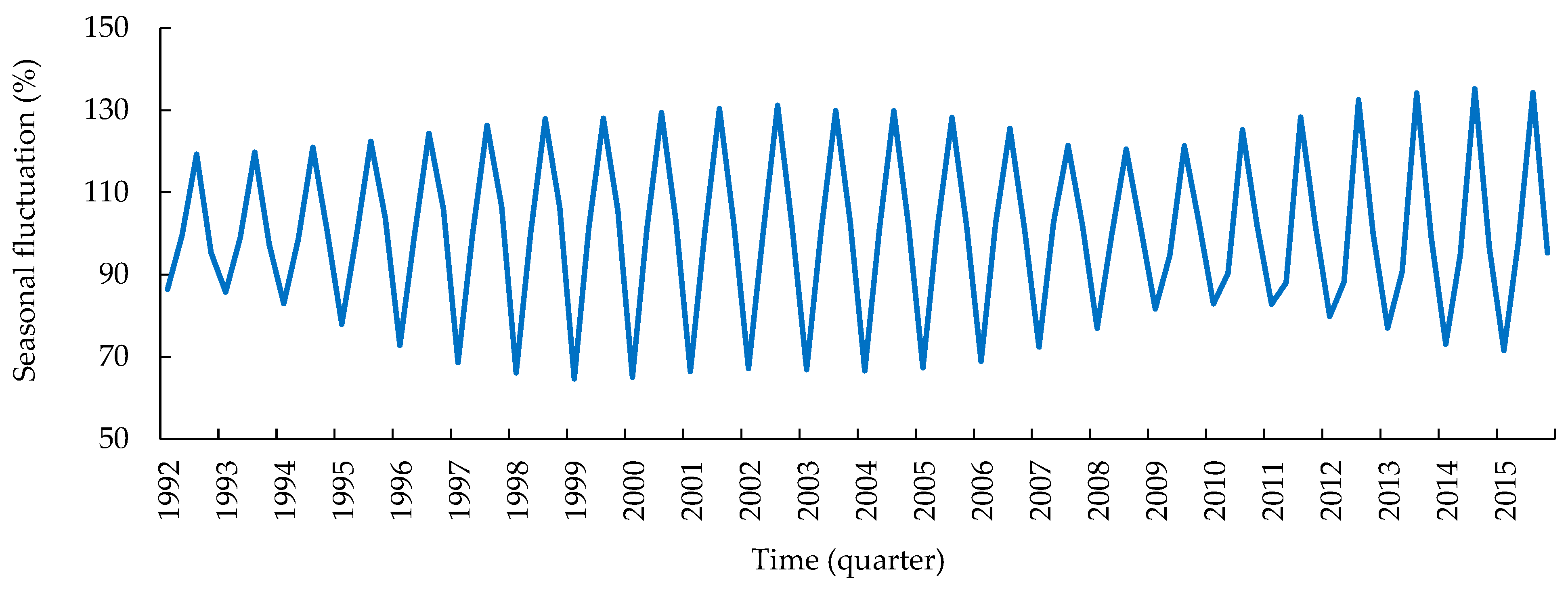

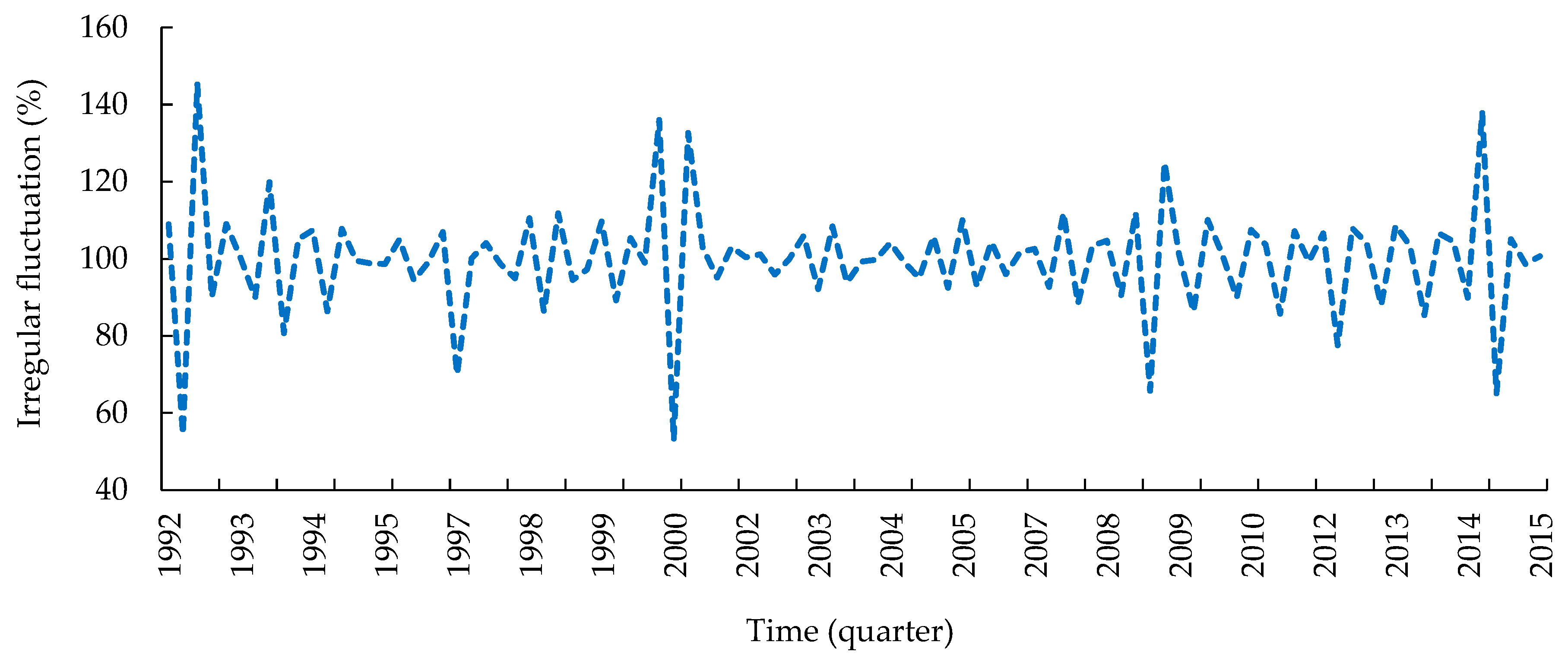

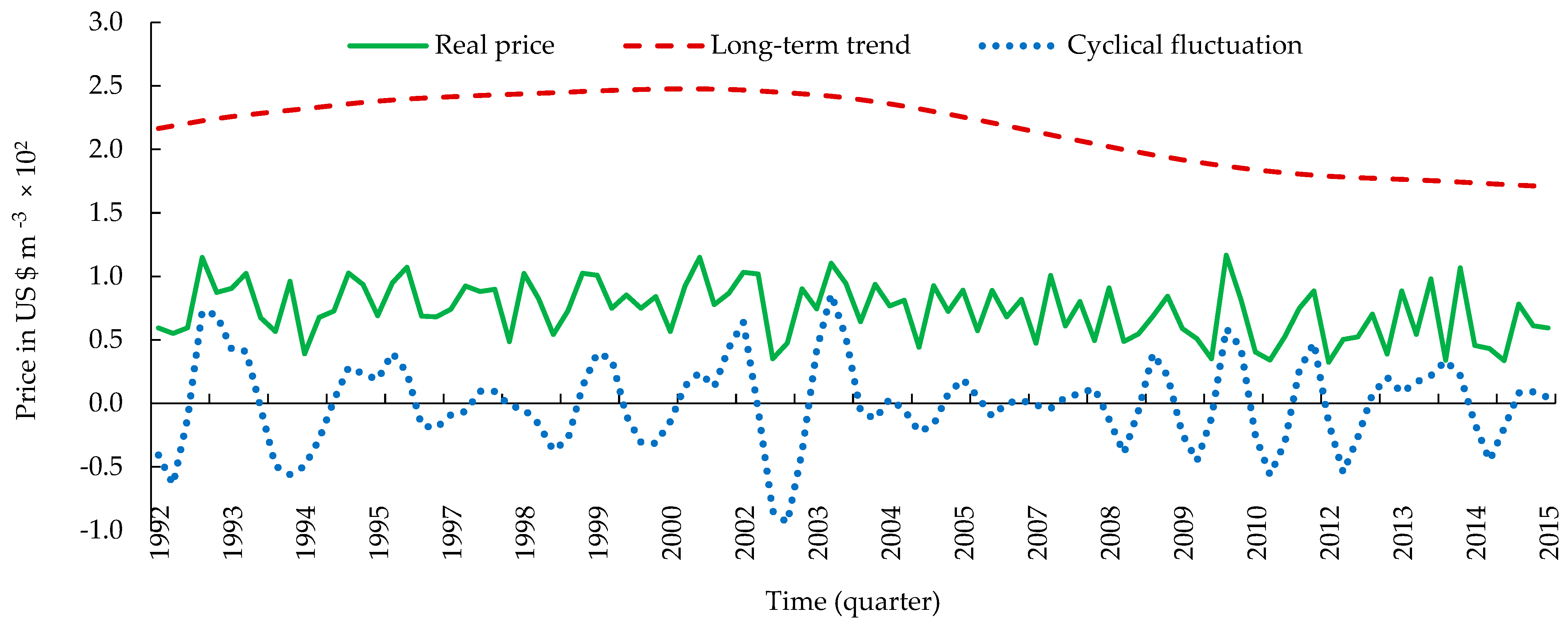

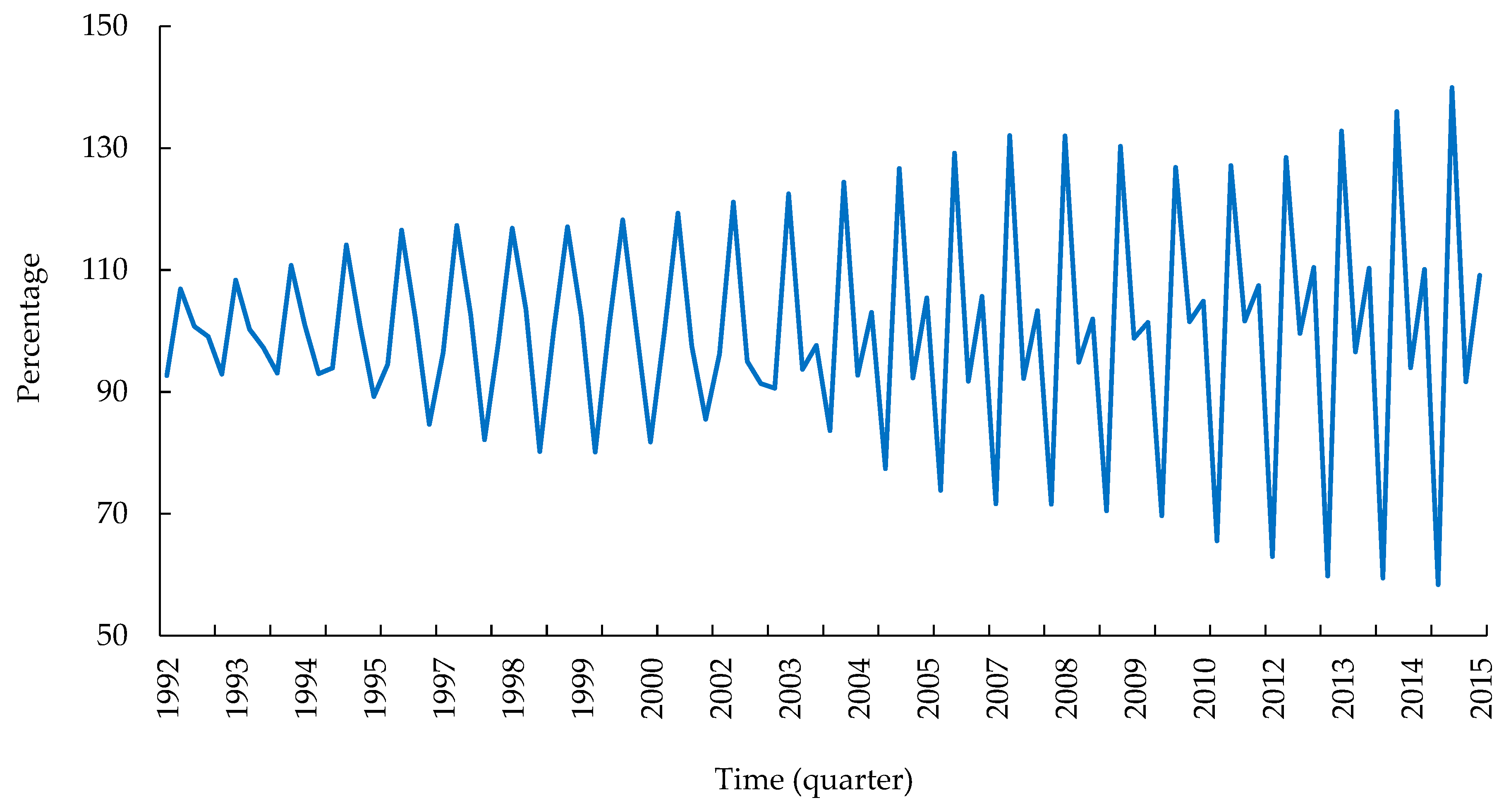

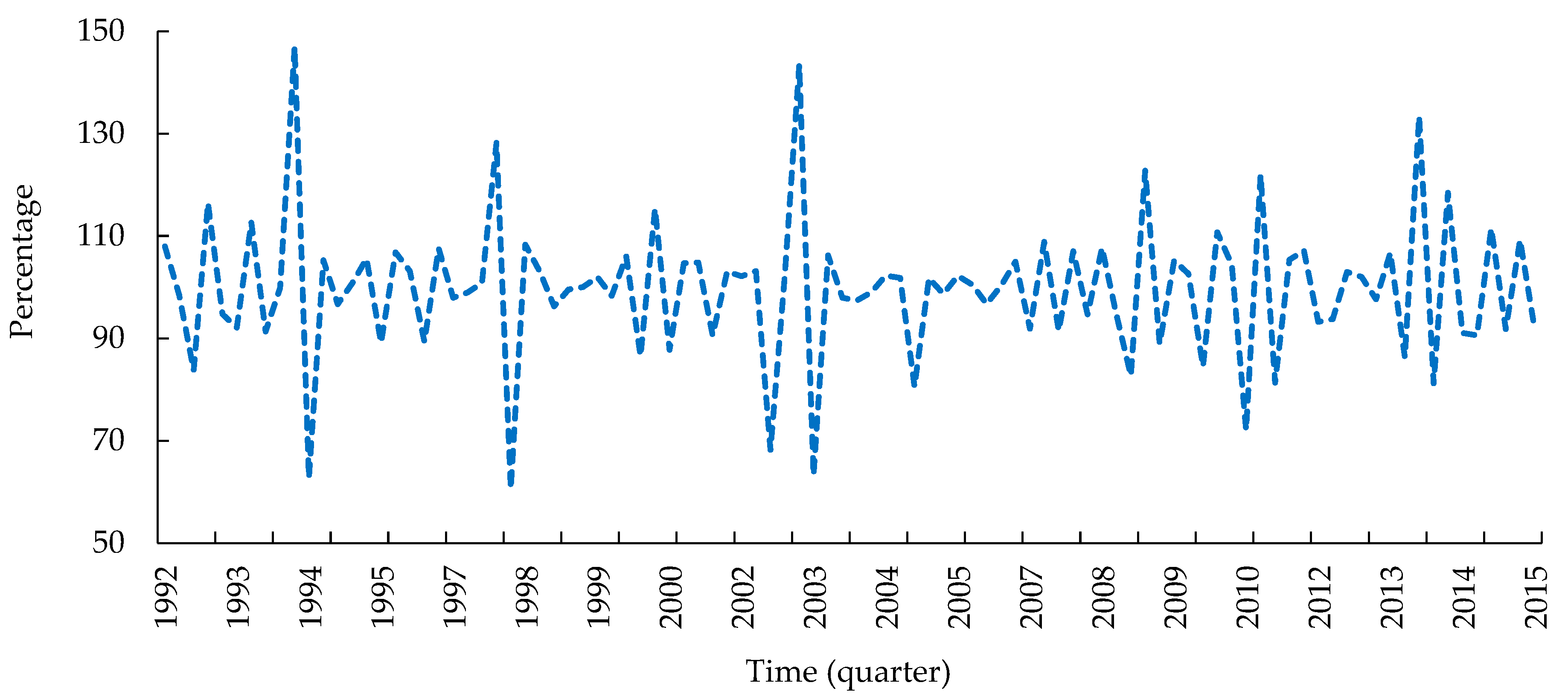

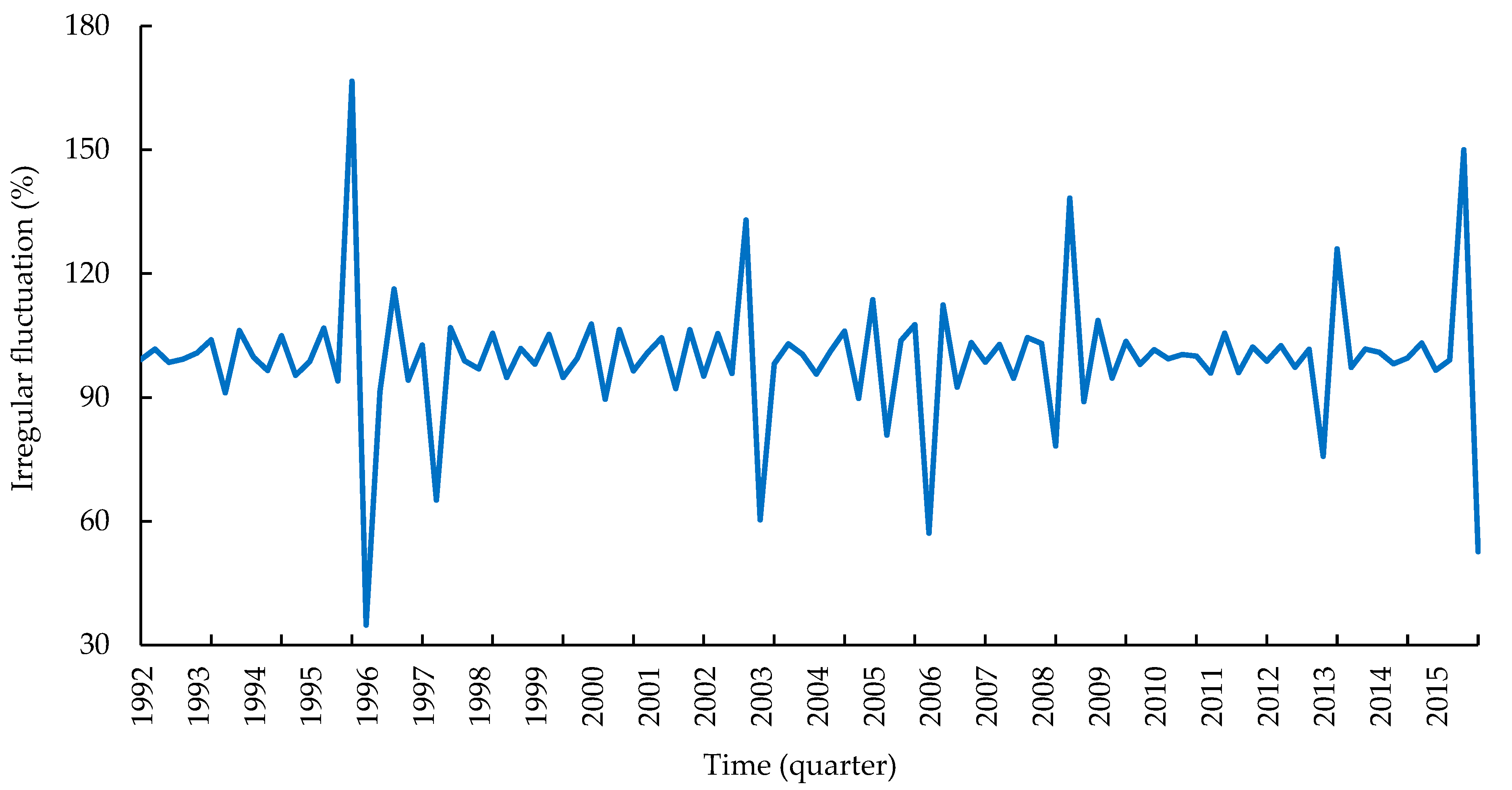

3.4. Fluctuation of Timber Price

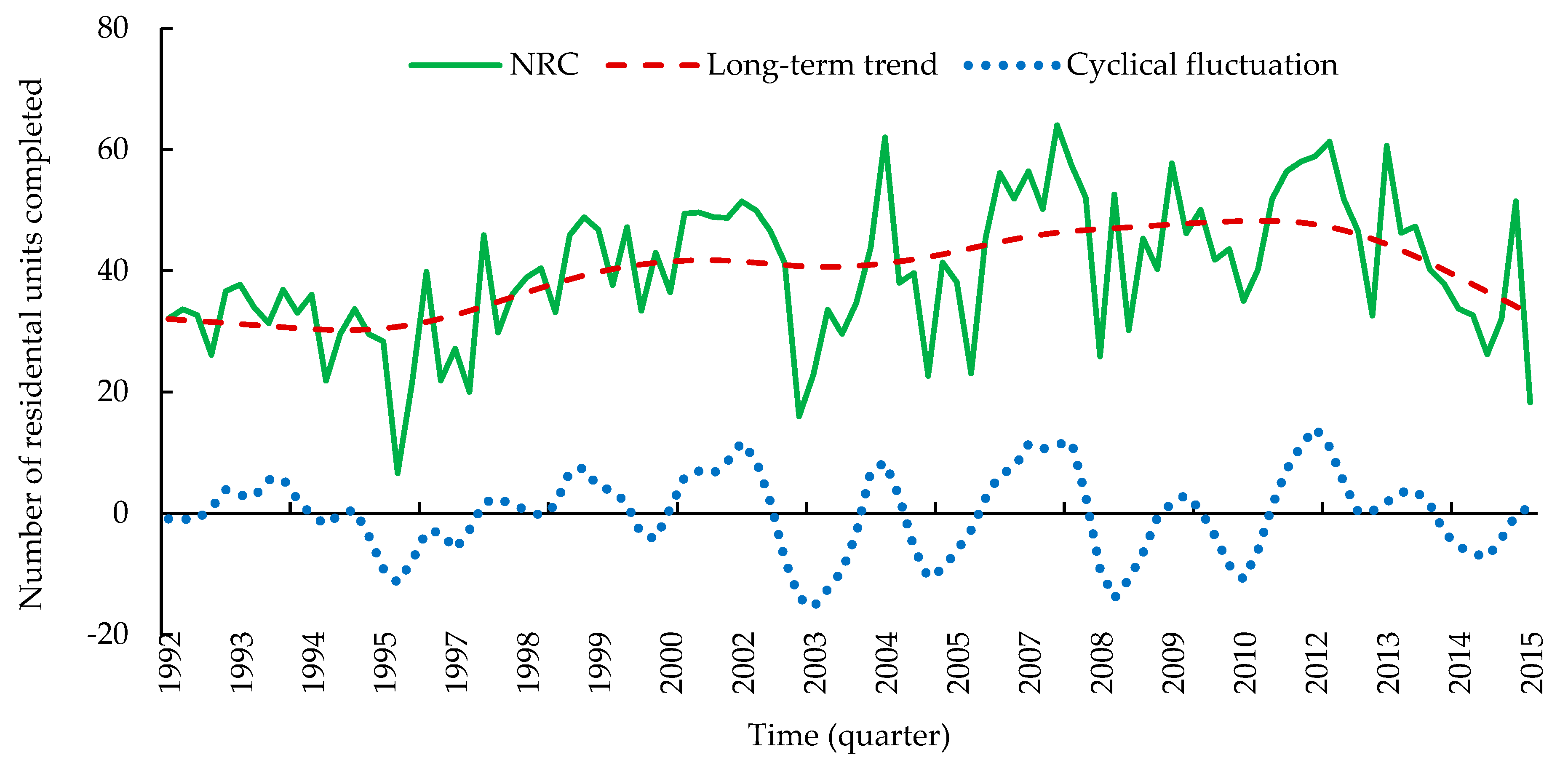

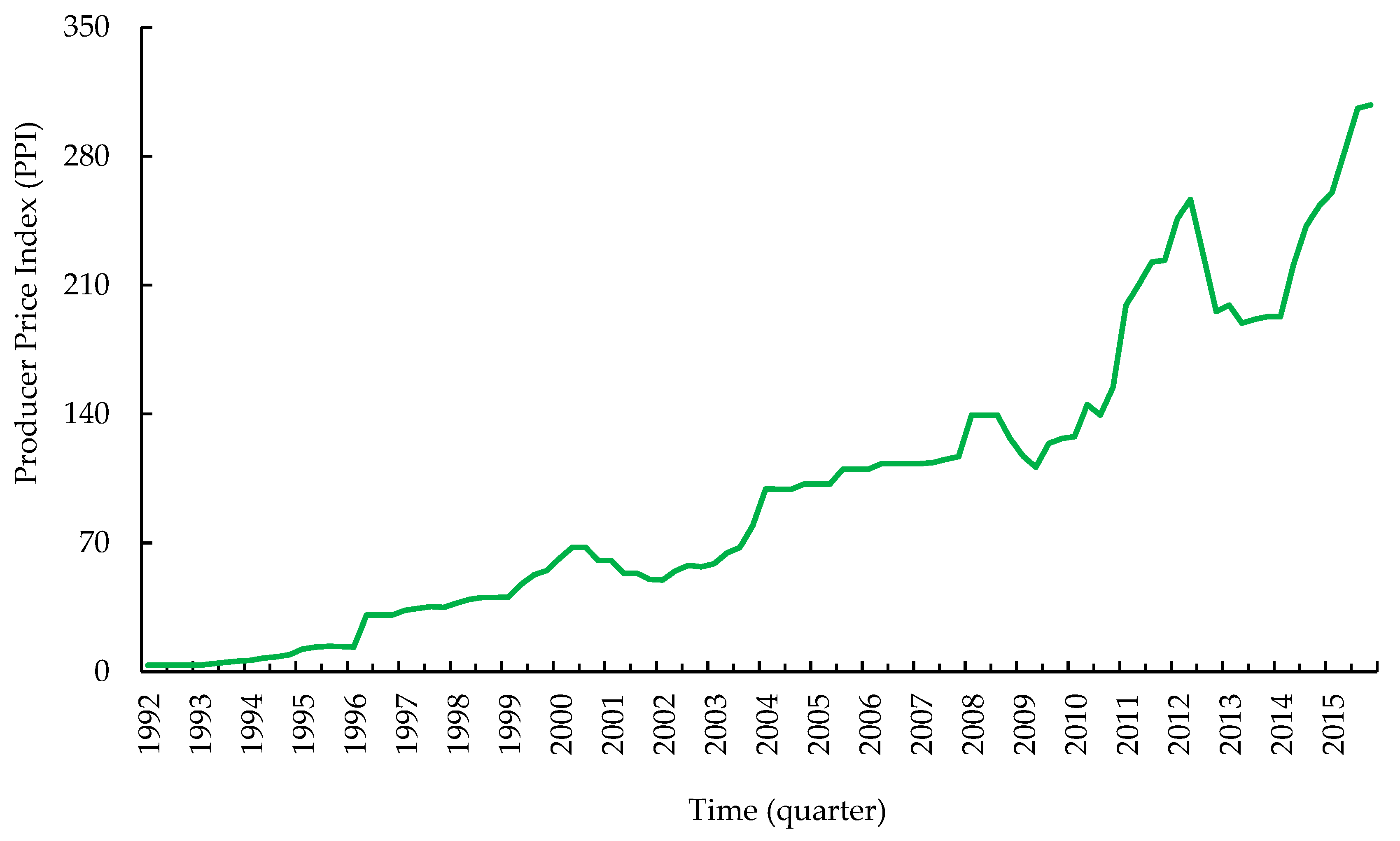

3.5. Fluctuation of the Construction Activities

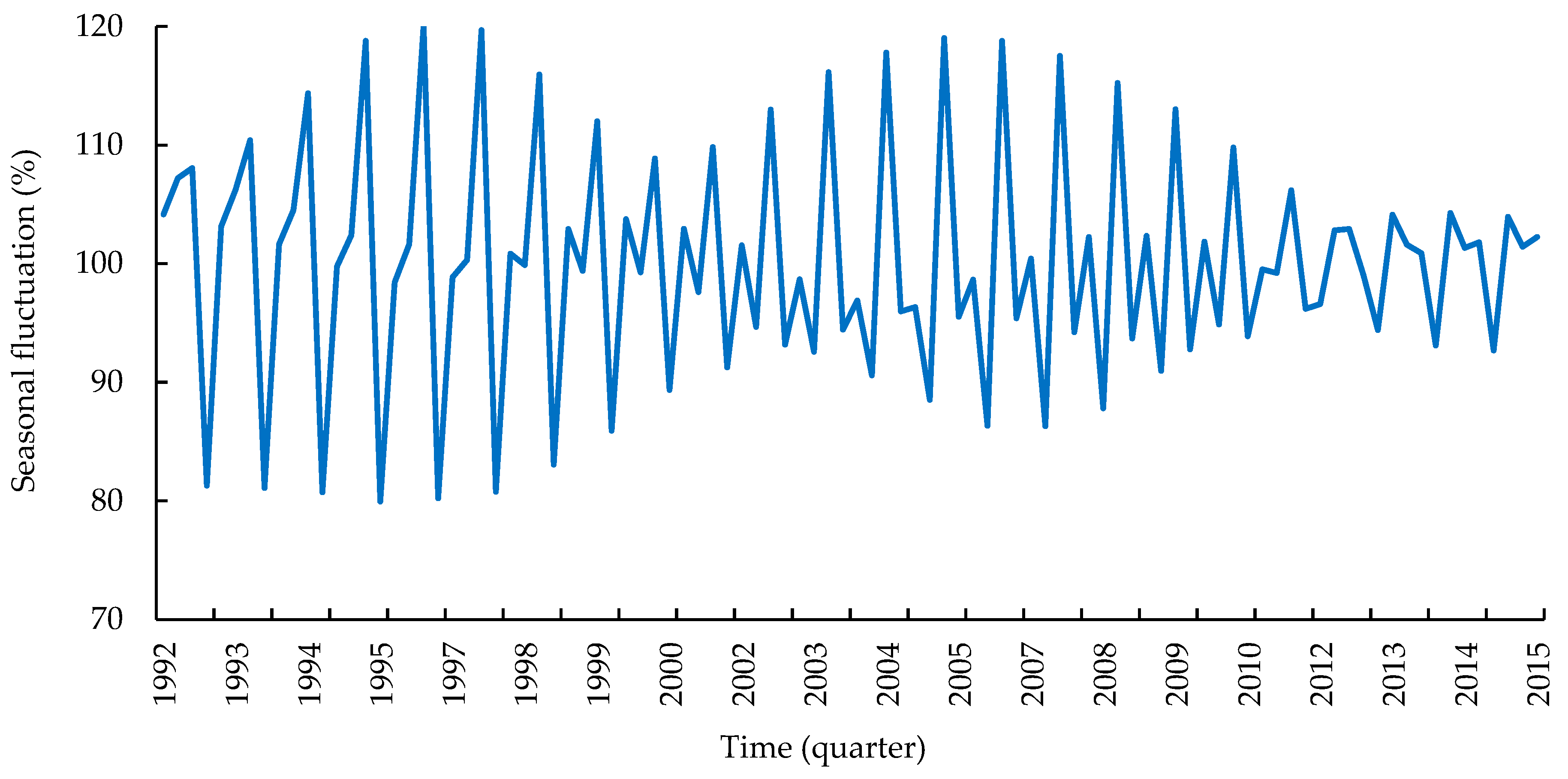

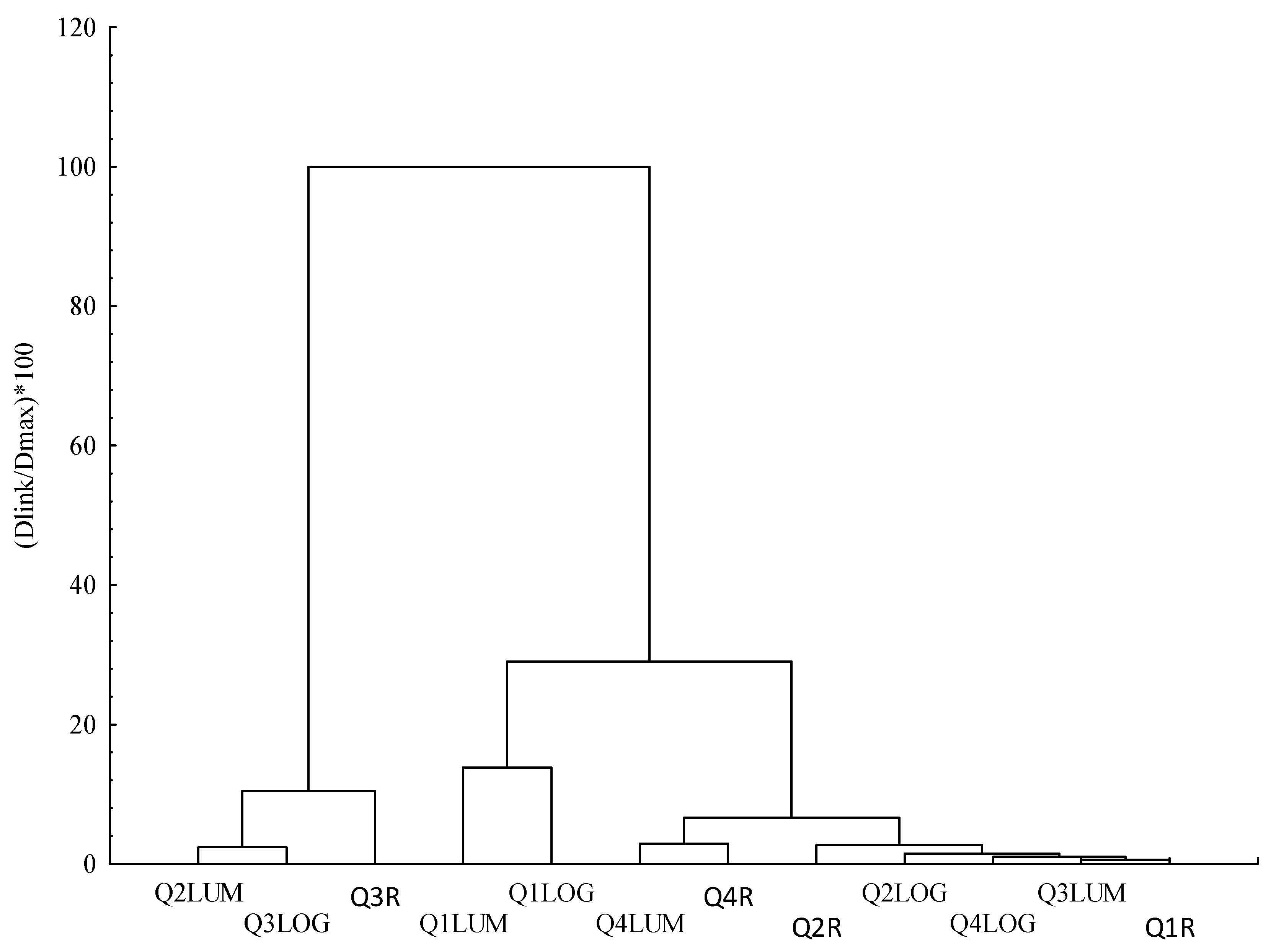

3.6. Similarity of Seasonal Index Patterns

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| t-Statistics | p-Value | |

|---|---|---|

| ADF test statistics | −3.20 | 0.023 |

| Test critical values at the 5% level | −2.89 | - |

| t-Statistics | p-Value | |

|---|---|---|

| ADF test statistics | −3.95 | 0.003 |

| Test critical values at the 5% level | −2.89 | - |

References

- Antonoaie, V. The Effects of the Euro Adoption on the Timber Market in Romania. Bull. Transilv. Univ. Brasov. Econ. Sci. Ser. V 2013, 6, 29–36. [Google Scholar]

- Gejdoš, M.; Danihelová, Z. Valuation and Timber Market in the Slovak Republic. Procedia Econ. Financ. 2015, 34, 697–703. [Google Scholar] [CrossRef]

- Jaunky, V.C.; Lundmark, R. Dynamics of Timber Market Integration in Sweden. Forests 2015, 6, 4617–4633. [Google Scholar] [CrossRef]

- Poljanec, A.; Kadunc, A. Quality and Timber Value of European Beech (Fagus sylvatica L.) Trees in the Karavanke Region. Croatian J. For. Eng. 2013, 34, 151–165. [Google Scholar]

- Suchomel, J.; Gejdoš, M.; Ambrušová, L.; Šulek, R. Analysis of Price Changes of Selected Roundwood Assortments in Some Central Europe Countries. J. For. Sci. 2012, 58, 483–491. [Google Scholar] [CrossRef] [Green Version]

- Toppinen, A.; Toivonen, R. Roundwood Market Integration in Finland: A Multi-variate Cointegration Analysis. J. For. Econ. 1998, 4, 241–265. [Google Scholar]

- Toppinen, A.; Viitanen, J.; Leskinen, P.; Toivonen, R. Dynamics of Roundwood Prices in Estonia, Finland and Lithuania. Balt. For. 2005, 11, 88–96. [Google Scholar]

- Gökhan, Ş.; Gungor, E. Determination of the Seasonal Effect on the Auction Prices of Timbers and Prediction of Future Prices. Bartın Orman Fakültesi Derg. 2018, 20, 266–277. [Google Scholar]

- Kożuch, A.; Banaś, J. The Dynamics of Beech Roundwood Prices in Selected Central European Markets. Forests 2020, 11, 902. [Google Scholar] [CrossRef]

- Banaś, J.; Utnik-Banaś, K. Evaluating a Seasonal Autoregressive Moving Average Model with an Exogenous Variable for Short-Term Timber Price Forecasting. For. Pol. Econ. 2021, 131, 102564. [Google Scholar] [CrossRef]

- Prestemon, J.P.; Pye, J.M.; Holmes, T.P. Temporal Aggregation and Testing for Timber Price Behavior. Nat. Resour. Model. 2004, 17, 123–162. [Google Scholar] [CrossRef]

- Størdal, S. Efficient Timber Pricing and Purchasing Behavior in Forest Owners’ Associations. J. For. Econ. 2004, 10, 135–147. [Google Scholar] [CrossRef]

- Accastello, C.; Blanc, S.; Mosso, A.; Brun, F. Assessing the Timber Value: A Case Study in the Italian Alps. For. Pol. Econ. 2018, 93, 36–44. [Google Scholar] [CrossRef]

- Fornea, M.; Bîrda, M.; Borz, S.A.; Popa, B.; Tomašić, Ž. Harvesting Conditions, Market Particularities or Just Economic Competition: A Romanian Case Study Regarding the Evolution of Standing Timber Contracting Rates. Šumarski List 2018, 142, 499–507. [Google Scholar]

- Carter, D.R.; Newman, D.H. The Impact of Reserve Prices in Sealed Bid Federal Timber Sale Auctions. For. Sci. 1998, 44, 485–495. [Google Scholar]

- Leefers, L.A.; Potter-Witter, K. Timber Sale Characteristics and Competition for Public Lands Stumpage: A Case Study from the Lake States. For. Sci. 2006, 52, 460–467. [Google Scholar]

- Rissman, A.R.; Geisler, E.; Gorby, T.; Rickenbach, M.G. “Maxed Out on Efficiency”: Logger Perceptions of Financial Challenges Facing Timber Operations. J. Sustain. For. 2022, 41, 115–133. [Google Scholar] [CrossRef]

- Newman, D.H.; Gilbert, C.B.; Hyde, W.F. The Optimal Forest Rotation with Evolving Prices. In Economics of Forestry; Routledge: London, UK, 2018; pp. 213–220. [Google Scholar]

- Zwirglmaier, K. Seasonal Influence in Determinants of Timber Supply and Demand. In Proceedings of the Managerial Economics and Accounting Conference, Hamburg, Germany, 21–23 October 2009; pp. 21–23. [Google Scholar]

- Conrad, J.L., IV.; Demchik, M.C.; Vokoun, M.M. Effects of Seasonal Timber Harvesting Restrictions on Procurement Practices. For. Prod. J. 2018, 68, 43–53. [Google Scholar] [CrossRef]

- Kolis, K.; Hiironen, J.; Ärölä, E.; Vitikainen, A. Effects of Sale-Specific Factors on Stumpage Prices in Finland. Silva Fenn. 2014, 48, 18. [Google Scholar] [CrossRef] [Green Version]

- Michinaka, T.; Kuboyama, H.; Tamura, K.; Oka, H.; Yamamoto, N. Forecasting Monthly Prices of Japanese Logs. Forests 2016, 7, 94. [Google Scholar] [CrossRef] [Green Version]

- Han, X.; Kant, S.; Xie, Y. Bidder’s Private Value Distributions in Standing Timber Auctions in the Jiangxi Province of China. Canad. J. For. Res. 2018, 48, 1441–1455. [Google Scholar] [CrossRef]

- Préget, R.; Waelbroeck, P. Timber Appraisal from French Public Auctions: How to set the Reserve Price When There Are Unsold Lots? In Proceedings of the International Conference of the Scandinavian Society of Forest Economics, Uppsala, Sweden, 23–26 May 2006. [Google Scholar]

- Puttock, G.D.; Prescott, D.M.; Meilke, K.D. Stumpage Prices in Southwestern Ontario: A Hedonic Function Approach. For. Sci. 1990, 36, 1119–1132. [Google Scholar]

- Li, L.; Shen, Y.; Xu, X.; Zhang, Y.; Gu, G. Stumpage Price Determination in China’s Collective Forest Region, Zhejiang as an Example. For. Pol. Econ. 2020, 117, 102215. [Google Scholar] [CrossRef]

- Rosen, S. Hedonic Prices and Implicit Markets: Product Differentiation in Pure Competition. J. Politic. Econ. 1974, 82, 34–55. [Google Scholar] [CrossRef]

- Chen, H.; He, Z.; Hong, W.; Liu, J. An Assessment of Stumpage Price and the Price Index of Chinese Fir Timber Forests in Southern China Using a Hedonic Price Model. Forests 2020, 11, 436. [Google Scholar] [CrossRef] [Green Version]

- Kim, H.; Cieszewski, C. The Analysis of Pine Stumpage Prices Based on Timber Sale Characteristics of the Southern United States. J. For. Environ. Sci. 2015, 31, 38–46. [Google Scholar] [CrossRef]

- Dahal, P.; Mehmood, S.R. Determinants of Timber Bid Prices in Arkansas. For. Prod. J. 2005, 55, 88–94. [Google Scholar]

- Dunn, M.A.; Dubois, M.R. Determining Econometric Relationships Between Timber Sale Notice Provisions and High Bids Received on Timber Offerings from the Alabama Department of Conservation/State Lands Division. In Proceedings of the 1999 Southern Forest Economics Workshop, Starkville, MS, USA, 18–20 April 1999; pp. 83–90. [Google Scholar]

- Brown, R.N.; Kilgore, M.A.; Coggins, J.S.; Blinn, C.R. The Impact of Timber-Sale Tract, Policy, and Administrative Characteristics on State Stumpage Prices: An Econometric Analysis. For. Pol. Econ. 2012, 21, 71–80. [Google Scholar] [CrossRef]

- Wear, D.N.; Prestemon, J.P.; Foster, M.O. US Forest Products in the Global Economy. J. Forestry 2016, 114, 483–493. [Google Scholar] [CrossRef]

- MacKay, D.G.; Baughman, M.J. Multiple Regression-Based Transactions Evidence Timber Appraisal for Minnesota’s State Forests. North. J. Appl. For. 1996, 13, 129–134. [Google Scholar] [CrossRef] [Green Version]

- Shiskin, J. The X-11 Variant of the Census Method II Seasonal Adjustment Program; US Government Printing Office: Washington, DC, USA, 1967.

- Reimer, J.J. An Investigation of Log Prices in the US Pacific Northwest. For. Pol. Econ. 2021, 126, 102437. [Google Scholar] [CrossRef]

- Matsushta, K. The Seasonal Fluctuation of the Forest Products Price (II). Mem. Fac. Agric. Kagoshima Univ. 1992, 29, 121–133. [Google Scholar]

- Fathizadeh, O.; Sadeghi, S.M.M.; Holder, C.D.; Su, L. Leaf Phenology Drives Spatio-Temporal Patterns of Throughfall under a Single Quercus castaneifolia CA Mey. Forests 2020, 11, 688. [Google Scholar] [CrossRef]

- Rahbarisisakht, S.; Moayeri, M.H.; Hayati, E.; Sadeghi, S.M.M.; Kepfer-Rojas, S.; Pahlavani, M.H.; Kappel Schmidt, I.; Borz, S.A. Changes in Soil’s Chemical and Biochemical Properties Induced by Road Geometry in the Hyrcanian Temperate Forests. Forests 2021, 12, 1805. [Google Scholar] [CrossRef]

- Deljouei, A.; Abdi, E.; Marcantonio, M.; Majnounian, B.; Amici, V.; Sohrabi, H. The impact of forest roads on understory plant diversity in temperate hornbeam-beech forests of Northern Iran. Environ. Monit. Assess. 2017, 189, 1–15. [Google Scholar] [CrossRef] [PubMed]

- Deljouei, A.; Sadeghi, S.M.M.; Abdi, E.; Bernhardt-Römermann, M.; Pascoe, E.L.; Marcantonio, M. The Impact of Road Disturbance on Vegetation and Soil Properties in a Beech Stand, Hyrcanian Forest. Eur. J. For. Res. 2018, 137, 759–770. [Google Scholar] [CrossRef]

- Nasiri, V.; Darvishsefat, A.A.; Arefi, H.; Griess, V.C.; Sadeghi, S.M.M.; Borz, S.A. Modeling Forest Canopy cover: A Synergistic Use of Sentinel-2, Aerial Photogrammetry Data, and Machine Learning. Remote Sens. 2022, 14, 1453. [Google Scholar] [CrossRef]

- Moradi, F.; Darvishsefat, A.A.; Pourrahmati, M.R.; Deljouei, A.; Borz, S.A. Estimating Aboveground Biomass in Dense Hyrcanian Forests by the Use of Sentinel-2 Data. Forests 2022, 13, 104. [Google Scholar] [CrossRef]

- Haghshenas, M.; Marvi Mohadjer, M.R.; Attarod, P.; Pourtahmasi, K.; Feldhaus, J.; Sadeghi, S.M.M. Climate Effect on Tree-Ring Widths of Fagus orientalis in the Caspian Forests, Northern Iran. Fore. Sci. Technol. 2016, 12, 176–182. [Google Scholar] [CrossRef] [Green Version]

- Attarod, P.; Kheirkhah, F.; Khalighi Sigaroodi, S.; Sadeghi, S.M.M. Sensitivity of Reference Evapotranspiration to Global Warming in the Caspian Region, North of Iran. J. Agric. Sci. Technol. 2015, 17, 869–883. [Google Scholar]

- Economic Time Series Database. The Number of Residential Units Completed by the Private Sector of Urban Areas. Available online: https://www.cbi.ir/page/8020.aspx (accessed on 3 December 2019).

- Dennis, D.F. Trends in New Hampshire Stumpage Prices: A Supply Perspective. North. J. Appl. For. 1989, 6, 189–190. [Google Scholar] [CrossRef]

- Fuhrmann, M.; Dißauer, C.; Strasser, C.; Schmid, E. Analysing Price Cointegration of Sawmill by-Products in the Forest-Based Sector in Austria. For. Pol. Econom. 2021, 131, 102560. [Google Scholar] [CrossRef]

- McCullough, B.D. Econometric Software Reliability: EViews, LIMDEP, SHAZAM and TSP; JSTOR: New York, NY, USA, 1999. [Google Scholar]

- Hultkrantz, L.; Andersson, L.; Mantalos, P. Stumpage Prices in Sweden 1909–2012: Testing for Non-Stationarity. J. For. Econ. 2014, 20, 33–46. [Google Scholar] [CrossRef] [Green Version]

- Rougieux, P.; Jonsson, R. Impacts of the FLEGT Action Plan and the EU Timber Regulation on EU Trade in Timber Product. Sustainability 2021, 13, 6030. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, X.; Guo, Z. Estimation of Tree Height and Aboveground Biomass of Coniferous Forests in North China Using Stereo ZY-3, Multispectral Sentinel-2, and DEM Data. Ecol. Indic. 2021, 126, 107645. [Google Scholar] [CrossRef]

- Assogba, N.P.; Zhang, D. The Conservation Reserve Program and Timber Prices in the Southern United States. For. Pol. Econom. 2022, 140, 102752. [Google Scholar] [CrossRef]

- Shook, S.R.; Plesha, N.; Nalle, D.J. Does Cointegration of Prices of North American Softwood Lumber Species Imply Nearly Perfectly Substitutable Products? Canad. J. For. Res. 2009, 39, 553–565. [Google Scholar] [CrossRef]

- Neter, J.; Wasserman, W. Applied Linear Statistical Models; Richard, D., Ed.; Irwin: Homewood, IL, USA, 1974. [Google Scholar]

- Gujarati, D.N. Basic Econometrics; Tata McGraw-Hill Education: New York, NY, USA, 2009. [Google Scholar]

- Banaś, J.; Kożuch, A. The Application of Time Series Decomposition for the Identification and Analysis of Fluctuations in Timber Supply and Price: A Case Study from Poland. Forests 2019, 10, 990. [Google Scholar] [CrossRef] [Green Version]

- Hodrick, R.J.; Prescott, E.C. Postwar US Business Cycles: An Empirical Investigation. J. Money Credit. Bank. 1997, 29, 1–16. [Google Scholar] [CrossRef]

- Ravn, M.O.; Uhlig, H. On Adjusting the Hodrick-Prescott Filter for the Frequency of Observations. Rev. Econ. Stat. 2002, 84, 371–380. [Google Scholar] [CrossRef] [Green Version]

- Matsushita, K. The Seasonal Fluctuation of the Forest Products Price (I). Mem. Fac. Agric. Kagoshima Univ. 1992, 28, 153–163. [Google Scholar]

- Kuuluvainen, J.; Karppinen, H.; Ovaskainen, V. Landowner Objectives and Nonindustrial Private Timber Supply. For. Sci. 1996, 42, 300–309. [Google Scholar]

- Buongiorno, J.; Balsiger, J. Quantitative Analysis and Forecasting of Monthly Prices of Lumber and Flooring Products. Agric. Syst. 1977, 2, 165–181. [Google Scholar] [CrossRef]

- Niquidet, K.; Van Kooten, G.C. Transaction Evidence Appraisal: Competition in British Columbia’s Stumpage Markets. For. Sci. 2006, 52, 451–459. [Google Scholar]

- Zimmermann, K.; Schuetz, T.; Weimar, H. Analysis and Modeling of Timber Storage Accumulation After Severe Storm Events in Germany. Eur. J. For. Res. 2018, 137, 463–475. [Google Scholar] [CrossRef]

- Devadoss, S. An Evaluation of Canadian and US Policies of Log and Lumber Markets. J. Agric. Appl. Econ. 2008, 40, 171–184. [Google Scholar] [CrossRef] [Green Version]

- van Kooten, G.C.; Johnston, C. Global Impacts of Russian Log Export Restrictions and the Canada—US Lumber Dispute: Modeling Trade in Logs and Lumber. For. Pol. Econ. 2014, 39, 54–66. [Google Scholar] [CrossRef]

- Fruteau, C.; Voelkl, B.; van Damme, E.; Noë, R. Supply and Demand Determine the Market Value of Food Providers in Wild Vervet Monkeys. Proc. Nat. Acad. Sci. USA 2009, 106, 12007–12012. [Google Scholar] [CrossRef] [Green Version]

- Morland, C.; Schier, F.; Janzen, N.; Weimar, H. Supply and Demand Functions for Global Wood Markets: Specification and Plausibility Testing of Econometric Models within the Global Forest Sector. For. Pol. Econ. 2018, 92, 92–105. [Google Scholar] [CrossRef]

- Bayatkashkoli, A.; Faezipour, M.; Azizi, M.; Gholezadeh, H. Price Index Trend of Wood and Its Products in Iran. Pajouhesh Sazandegi 2009, 21, 19–27. [Google Scholar]

- Saeed, A. Fundamentals of Practical Economics in Forest Management; University of Tehran Press: Tehran, Iran, 1992. [Google Scholar]

- Demchik, M.C.; Conrad, J.L., IV.; McFarlane, D.; Vokoun, M. Wisconsin Timber Sale Availability as Impacted by Seasonal Harvest Restrictions. For. Sci. 2018, 64, 74–81. [Google Scholar] [CrossRef]

- DAŞDEMİR, İ. Açık artırmalı kayın tomruk satış fiyatını etkileyen faktörler. Bartın J. Faculty For. 2008, 10, 1–12. [Google Scholar]

- Abdi, E.; Samdaliry, H.; Ghalandarayeshi, S.; Khoramizadeh, A.; Sohrabi, H.; Deljouei, A.; Kvist Johannsen, V.; Etemad, V. Modeling Wind-Driven Tree Mortality: The Effects of Forest Roads. Austrian J. For. Sci. 2020, 137, 1–21. [Google Scholar]

| Variables | Minimum | Maximum | Mean | SD (±) |

|---|---|---|---|---|

| High-value species sawlog price (US $ m−3) | 42.0 | 219.0 | 140.1 | 42.1 |

| High-value species lumber price (US $ m−3) | 32.4 | 116.6 | 73.5 | 22.2 |

| Construction activities (unitless) | 6611 | 64,034 | 39,900 | 11,661 |

| Coefficient | SE (±) | t-Statistic | p-Value | Elasticity of Sawlog Price (%) | R2 | |

|---|---|---|---|---|---|---|

| Intercept | 142.3 | 6.7 | 21.2 | 0.0000 * | - | 0.41 |

| Spring | −38.8 | 9.5 | −4.08 | 0.0001 * | −6.9 | |

| Summer | −6.6 | 9.5 | −0.70 | 0.49 ns | - | |

| Autumn | 36.7 | 9.5 | 3.86 | 0.0002 * | 6.5 | |

| Winter | 2.9 | 9.9 | 0.3 | 0.77 ns | - |

| Coefficient | SE (±) | t-Statistic | p-Value | Elasticity of Lumber Price (%) | R2 | |

|---|---|---|---|---|---|---|

| Intercept | 72.0 | 4.1 | 17.7 | 0.000 * | - | 0.22 |

| Spring | −10.5 | 5.7 | −1.8 | 0.070 ns | - | |

| Summer | 17.9 | 5.7 | 3.1 | 0.000 * | 6.1 | |

| Autumn | −1.3 | 5.7 | −0.2 | 0.820 ns | - | |

| Winter | −2.0 | 5.3 | −0.40 | 0.70 ns | - |

| Model | VIF | DW | Jarque–Bera Statistic | p-Value |

|---|---|---|---|---|

| Sawlog price model | 1.50 | 1.50 | 0.08 | 0.96 ns |

| Lumber price model | 1.50 | 1.69 | 1.91 | 0.38 ns |

| Source | Sum of Squares | Degrees of Freedom | Mean Square | F-Value |

|---|---|---|---|---|

| Between seasons | 40.8 | 3 | 13.6 | 58.32 *** |

| Residual | 21.5 | 92 | 0.2 | - |

| Total | 62.3 | 95 | - | - |

| Source | Sum of Squares | Degrees of Freedom | Mean Square | F-Value |

|---|---|---|---|---|

| Between seasons | 21.5 | 3 | 7.2 | 21.45 *** |

| Residual | 30.7 | 92 | 0.333 | - |

| Total | 52.2 | 95 | - | - |

| Span in Quarters (Q) | Sawlog | Lumber | NRC | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Irregular (%) | Cyclic (%) | Seasonal (%) | Irregular (%) | Cyclic (%) | Seasonal (%) | Irregular (%) | Cyclic (%) | Seasonal (%) | |

| 1 | 32 | 6 | 62 | 27 | 11 | 62 | 57 | 12 | 31 |

| 2 | 15 | 15 | 70 | 21 | 34 | 46 | 38 | 39 | 23 |

| 3 | 15 | 24 | 61 | 14 | 37 | 49 | 29 | 47 | 24 |

| 4 | 38 | 62 | 0 | 39 | 61 | 0 | 33 | 66 | 0 |

| Average | 25 | 27 | 48 | 25 | 36 | 39 | 39 | 41 | 20 |

| Source | Sum of Squares | Degrees of Freedom | Mean Square | F-Value |

|---|---|---|---|---|

| Between seasons | 8.5 | 3 | 2.80 | 10.08 *** |

| Residual | 25.8 | 92 | 0.28 | - |

| Total | 34.3 | 95 | - | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Heshmatol Vaezin, S.M.; Moftakhar Juybari, M.; Sadeghi, S.M.M.; Banaś, J.; Marcu, M.V. The Seasonal Fluctuation of Timber Prices in Hyrcanian Temperate Forests, Northern Iran. Forests 2022, 13, 761. https://0-doi-org.brum.beds.ac.uk/10.3390/f13050761

Heshmatol Vaezin SM, Moftakhar Juybari M, Sadeghi SMM, Banaś J, Marcu MV. The Seasonal Fluctuation of Timber Prices in Hyrcanian Temperate Forests, Northern Iran. Forests. 2022; 13(5):761. https://0-doi-org.brum.beds.ac.uk/10.3390/f13050761

Chicago/Turabian StyleHeshmatol Vaezin, Seyed Mahdi, Mohammad Moftakhar Juybari, Seyed Mohammad Moein Sadeghi, Jan Banaś, and Marina Viorela Marcu. 2022. "The Seasonal Fluctuation of Timber Prices in Hyrcanian Temperate Forests, Northern Iran" Forests 13, no. 5: 761. https://0-doi-org.brum.beds.ac.uk/10.3390/f13050761