1. Introduction

The widespread corruption in society and the failure of businesses worldwide have heightened the necessity for accounting professionals to adhere to strict ethical rules, worrying that accounting fraud could undermine a bank’s operations (

Hazaea et al. 2021). Internal auditing has emerged as a key factor in supporting effective controls and risk management in the aftermath of numerous previous accounting disasters. Furthermore, the IA contributes to risk management in a number of ways through its assurance and advisory duties (

Jarah et al. 2022). Every bank should close the loophole by implementing a decent or high-quality internal auditing system that will oversee and monitor the bank’s policies and practices. Internal audit (IA) is also important since it ensures that the accounting system meets stakeholder needs for accurate financial information. The IA system was and is still thought to ensure the quality of financial statements, and it is envisaged that IA would act as a financial quality security compliance means. Therefore, the IA on the other hand has had little effect on the high percentage of fraudulent financial transactions (

Ogoun and Atagboro 2020). Therefore, internal and external users’ decision-making may be significantly improved by the identification and assessment of risks of accounting mistakes and inaccuracies that go beyond the economic substance of the provided data (

Drábková and Pech 2022).

Furthermore, while economic entities pay auditors to certify that their financial accounts reflect economic reality, the interests they safeguard are not those of the employing businesses. They must safeguard the interests of financial statement users, and in order to do so, they must be completely independent of the consumer who hires those (

Albawwat et al. 2021). The presented information reflects the completeness of the processed data, or the consequence of the data is valuable and relevant (

Jarah and Iskandar 2019). Thus, the function of audit in regulating creative accounting (CA) techniques should be defined by accountability and permanence; auditors should also exhibit independence, impartiality, fairness, competence, and credibility (

Balaciu et al. 2012). Because of the detrimental effects on the financial statements’ reliability, the auditors should specify the rules and processes that the auditor must follow to remedy these activities (

Ghamri 2020). Various CA techniques cause harm to account data users, and in order to make efficient investment and credit decisions, these users demand exact, true, objective, faithful, and credible accounting information (

Bhasin 2016). As a result, data must accurately portray economic events that occurred during the accounting period. They also need to know how the economy is doing right now. When publicly available accounting data are subject to some CA practices, users’ capacity to make good and productive decisions is harmed (

Al Momani and Obeidat 2013).

The goal of the audit quality is to give a fair assessment of the area under investigation, and the sampling procedure is critical to finding any irregularities and including the customer at every level of the IA. In the vocabulary used by the board of directors and top administrators, quality represents a bank’s distinctive performance (

Almatarneh et al. 2022). Regardless of how unique each audit is, the audit technique is similar when it comes to performing audits, with the initial review auditor drafting an audit program and organizing the opening meeting. During the initial meeting, the auditor discusses the audit’s purpose and scope, as well as organizational challenges. Financial statements may be incorrect, and economic data may not reflect reality. Committed errors, the use of CA, or in the worst-case scenario, accounting fraud, could be the source of abnormalities in financial accounts (

Klimczak 2013), where the audit committee has a role in diminishing CA acts when affected by accounting conservatism, according to this study by

Wulandari and Machmuddah (

2022). It also shows evidence that accounting conservatism influences CA. This study has important implications for corporate governance, accounting conservatism, and the audit committee’s role as a supervisor in limiting CA.

Furthermore, the importance of IA can be strengthened by the quality of the audit, the audit team’s competency, IA independence, and management support. The IA on the other hand is in charge of uncovering financial irregularities, specifically through the application of auditing standards (

Betti et al. 2021). The IA’s function in identifying fraud is dependent on his practical abilities and professional training. Despite the importance of IA in fraud detection, most studies concentrate on the role of IA and its effectiveness, rather than the IA responsibility to detect fraud (

Drogalas et al. 2017).

In light of current business conditions, many bank departments have turned to CA methods, utilizing a variety of accounting alternatives available, to beautify financial information in order to improve their financial situation, whether in terms of profitability or financial situation to achieve self-objectives. This has a negative impact on the integrity of financial statements when they are prepared. As a result, the study’s contribution is to determine the nature of these procedures and the amount to which internal auditors might use audit processes to weaken these methods in order to gain confidence in the financial statements contained in the financial statements.

In this study, we will add many topics about IA and its role in limiting the use of CA in banks. The researchers hope to develop new additional information to enrich the theoretical knowledge of the different influences on the role that IA will play in limiting CA activities that violate the spirit of good accounting practices. On a more practical level, the researchers hope that the findings will help bank departments by providing guidance regarding the dangers of CA and the significance of IA in limiting this accounting. The researchers also hope that the findings will help to clarify the idea of CA methods and be useful to decision-makers and policies.

2. Literature Review

The IA is a type of unbiased, independent verification and advice that adds value to a bank’s operations. It assists a bank in achieving its goals by examining and improving the effectiveness of risk management, control, and governance systems in a rigorous and disciplined manner (

Stewart and Subramaniam 2010). Where the IA function in enhancing financial and accounting movement is to determine whether the activity conforms to current norms and requirements, operates in accordance with best practices in the field, and ensures effectiveness in meeting objectives (

Betti et al. 2021). The IA also tries to limit the possibility that internal transactions and operations recorded in the entity’s main and accounting records would result in severe financial results distortions. In addition, the auditors’ primary purpose is to assess the efficiency of the IA, not just to uncover frauds and errors (

Drogalas et al. 2017). In addition, the IA conducts examinations and assessments of all financial accounting components and operations, and to giving information and unbiased opinions to management on the creation of efficient and useful use of public resources and possessions (

Munteanu et al. 2016).

In the same context, IA is viewed as a vital component in the implementation of accounting systems, which will aid in the reduction of the effects of CA (

Ogoun and Atagboro 2020), where the IA gives financial data and financial statements more credibility, and can actively participate in decreasing the problem’s effects. Internal auditors are qualified to detect CA activities since they are expected to have a thorough understanding of the accounting and auditing professions (

Saleh et al. 2021). Moreover, the internal auditors are assumed to be well-qualified to practice auditing and have a sufficient understanding of accounting principles and auditing standards, but if they do not follow their industry’s ethics, they will be unable to provide many advantages to the auditors, as well as reasonable solutions to the CA problem. Because there is evidence that the credit crisis has increased the risk of unethical conduct and fraud (

Al Momani and Obeidat 2013).

Auditors play an important and beneficial function in financial reporting. Moreover, higher ethical standards signal fewer fraudulent actions, which have an influential and positive influence on financial accounts (

Rakipi et al. 2021). Similarly, the CA plays a positive and influential role in financial statements, but it has been negatively correlated, which means that more additional managers involved may reduce the importance of financial statements, where government regulation and international measures play a positive and influential role if financial statements are elastic (

Tassadaq and Malik 2015).

3. Independence and Objectivity

The independence and objectivity of auditors are crucial to the profession. The value and credibility of the auditors’ assurance services are founded on the core ideas of mental independence and an appearance of independence. Independence is defined as freedom from factors that weaken objectivity or the appearance of objectivity (

Lois et al. 2021). Obstacles to objectivity must be removed at the individual auditor, engagement, functional, and regulatory levels. When performing audits, internal auditors must not rely on the judgment of others. Objectivity, on the other hand, is a neutral mental attitude that allows people to carry out tasks with confidence that their work output will be of good quality and that no substantial quality sacrifices will be made (

Stewart and Subramaniam 2010).

The IA is a neutral, independent assurance and consulting activity that provides value and enhances the performance of a bank’s operations. It helps a company achieve its goals by reviewing and enhancing the effectiveness of risk management, control, and governance systems in a rigorous and disciplined manner. This term underlines the significance of independence and objectivity in the work of an IA (

Goodwin and Yeo 2001). Concerns over IA independence and objectivity have sparked an interest in recent years. The importance of IA as a key corporate governance tool and internal consultation service is evolving and growing, which is driving this surge in research (

Madawaki and Ahmi 2021). Internal auditors are in a unique position in this regard, as they provide both internal assurance services and management consulting services. This dual job has sparked considerable criticism since it has the potential to put the internal auditor in a conflicting position. Internal auditors’ ability to exercise true objectivity as employees of the organization has also been questioned (

Stewart and Subramaniam 2010).

5. Professional Care

In today’s business environment, internal auditors face a number of challenges and opportunities, including increasingly intricate and pervasive technology, a need for new skills, a rapidly changing regulatory structure, and a demand for expanding the scope of services, as well as increased competition and globalization (

Endaya and Hanefah 2013). Internal auditors are developing innovative approaches to address difficulties, being more proactive, increasing their services, and otherwise altering the IA paradigm. Accounting scandals, business disasters, changes in corporate share ownership patterns, and regulatory reforms have all driven banks to improve their governance in recent years (

Savčuk 2007). The IA serves as a check on the effectiveness and appropriateness of the bank’s other controls. Senior management appoints internal auditors, and internal auditors report to senior management. Naturally, major banks will have an IA department that reviews the operation of the entire bank operating units on a regular basis (

Endaya and Hanefah 2016). The head of the IA department normally reports to the senior vice president of finance or the executive director, as well as the board of directors. Many boards now have audit committees that collaborate with the director of IA. Therefore, external auditors should examine if IA work has been appropriately planned, overseen, reviewed, and documented (

Yee et al. 2008).

6. Neutrality

The primary perspectives of auditor professional skepticism have formed as neutrality and presumed doubt, and auditors should endeavor to be unbiased in informing their beliefs; there should be no prejudice in either the positive or negative direction. The auditor must seek and assess evidence to confirm management’s assertions while also ruling out other explanations (

Quadackers et al. 2014). Thus, the auditor assumes no prejudice in management’s claims, which is known as neutrality. Presumptive doubt is an auditor’s mindset that assumes some amount of management dishonesty or bias unless evidence proves otherwise. Importantly, there is no agreement on which of these two types of skepticism is most appropriate for auditing (

Nelson 2009). Neutrality is described as freedom from the effects of other people’s behaviors, as well as all other activities that can be influenced directly or indirectly. The audit profession’s independence is critical to its long-term viability.

Therefore, the auditors who are tasked with offering an objective and independent evaluation should not be swayed (

Jakovljević 2021). At both the individual and collective levels, vulnerability to influence by audit banks and audit institutions can lead to a loss of audit independence and audit integrity. Those conducting audit engagements should maintain a high level of objectivity throughout their auditing careers, not only during the audit. Audit professionals’ neutrality, in this view, can be described as their willingness to remain immune to and independent of any internal or external influence based on character. It can be manifested in two ways: mental and physical political independence. The term “mind independence” refers to a state of mind in which an auditor is free of outside influences. It is, in reality, the auditor’s perspective on his impartiality (

Usang Edet Usang and Salim 2018).

7. Creative Accounting (CA)

The CA refers to an accounting practice that follows accounting principles or standards in order to present the company to its stakeholders in the best possible light. As a result, the CA is the process of transforming financial accounting data from what they are to what the financial report preparer intends, either by following current standards or by ignoring some or all of them (

Bhasin 2016). CA refers to accounting procedures that may or may not match the letter of accounting standard standards, but most certainly do not (

Adámiková and Čorejová 2021). Two characteristics that may be present are excessive complication and the use of innovative ways to represent income, assets, and liabilities. The CA is a term that describes a systematic misrepresentation of a bank or organization’s true and fair income, liabilities, and assets (

Yadav 2014), with many describing CA as an intentional kind used by the administration to beautify financial statements and show them without their true vision, to serve a specific category, by exploiting some gaps in international accounting standards (

Al-Olimat and Al Shbail 2021). Every business’s main objective in CA is to enhance and expand its position in the market, whereas, over the years, financial statement fraud has also spread to nations in Central Europe (

Durana et al. 2022).

CA stands for “undesirable practices” that include unethical aspects for attracting capital providers by presenting a dishonest and misleading state of affairs for a specific company. The majority of CA abstract delimitation is based on those two perspectives and the general tendency (

Vladu and Matis 2010). CA refers to the manipulation of financial numbers or the transfer of data, and it was first popularized roughly two decades ago (

Anggreni and Latrini 2021). They’re messing with numbers in order to make a good financial impression. The demand for the finest options is the positive side of earnings management, with the major goal being that the financial statement information reflects a true and fair image of the bank’s financial status (

Ogoun and Atagboro 2020). The practice of CA is still common, leading to low-quality financial reporting, despite the fact that several approaches have been established by scholars and practitioners to identify any manipulation in financial reporting

Abed et al. (

2022b).

The CA is a type of accounting that follows or disregards accounting standards and principles. However, in order to portray the intended picture of the bank, it departs from the basic idea of such standards and values (

Blazek 2021). CA is not illegal, but it is unethical because it fails to satisfy the fundamental goal of financial reporting, which is to present the bank in a fair and objective light (

Adeosun et al. 2021). CA tactics include overstating assets, holding high stocks, decreasing expenses, manipulating depreciation methodologies, and presenting provisions as an asset. Changes in accounting regulations are reflected in CA procedures, which are modified to reduce financial data manipulation. On the other hand, changes in accounting standards usually bring new opportunities for accounting fraud (

Remenarić et al. 2018).

Ghamri (

2020) defines CA as the ability of an accountant to create new accounting methods that aid in finding accounting solutions and achieving goals for the benefit of certain parties, even if they conflict with the interests of other parties and do not ultimately result in the benefit of all parties.

CA also has the ability to skew a company’s core financial performance, making it more difficult for an investor or financial assessor to evaluate and compare the company’s performance to that of other banks (

Olojede and Erin 2021). As a result, CA as a misleading approach contrasts with the fundamental goal of accounting organizations, transforming standard establishing training into a repetitive feature on the one hand and on the other hand (

Vladu and Matis 2010). The public has begun to question the role of auditors in uncovering these practices as the number of CA cases has increased. Theoretically, CA efforts are focused on exploiting gaps in accounting rules in order to prepare financial information reports without violating accounting standards. As a result, ethics is crucial in the audit profession because an auditor’s ethics will influence the audit quality requirements when analyzing financial accounts (

Anggreni and Latrini 2021).

Therefore, Upon the illustration of the previous results and the gap in the studies, the researchers studied the results related to the role of internal audit to reduce the effects of CA on the reliability of financial statements in the Jordanian Islamic Banks, where the internal and external stakeholders can use financial statements to acquire a better understanding of a bank’s financial situation and operating performance. Their correctness and trustworthiness are critical for all stakeholders in a bank to make informed decisions.

Considering the above literature review, the following hypotheses have been formulated:

H1. There is a statistically significant role of the IA combined (independence and objectivity, verifiability, professional care, and neutrality) in the reduced effects of CA on the reliability of financial statements in Jordanian Islamic Banks.

H1.1. There is a statistically significant role of independence and objectivity in the reduced effects of CA on the reliability of financial statements in Jordanian Islamic Banks.

H1.2. There is a statistically significant role of verifiability in the reduced effects of CA on the reliability of financial statements in Jordanian Islamic Banks.

H1.3. There is a statistically significant role of professional care in the reduced effects of CA on the reliability of financial statements in Jordanian Islamic Banks.

H1.4. There is a statistically significant role of neutrality in the reduced effects of CA on the reliability of financial statements in Jordanian Islamic Banks.

10. Hypotheses Test

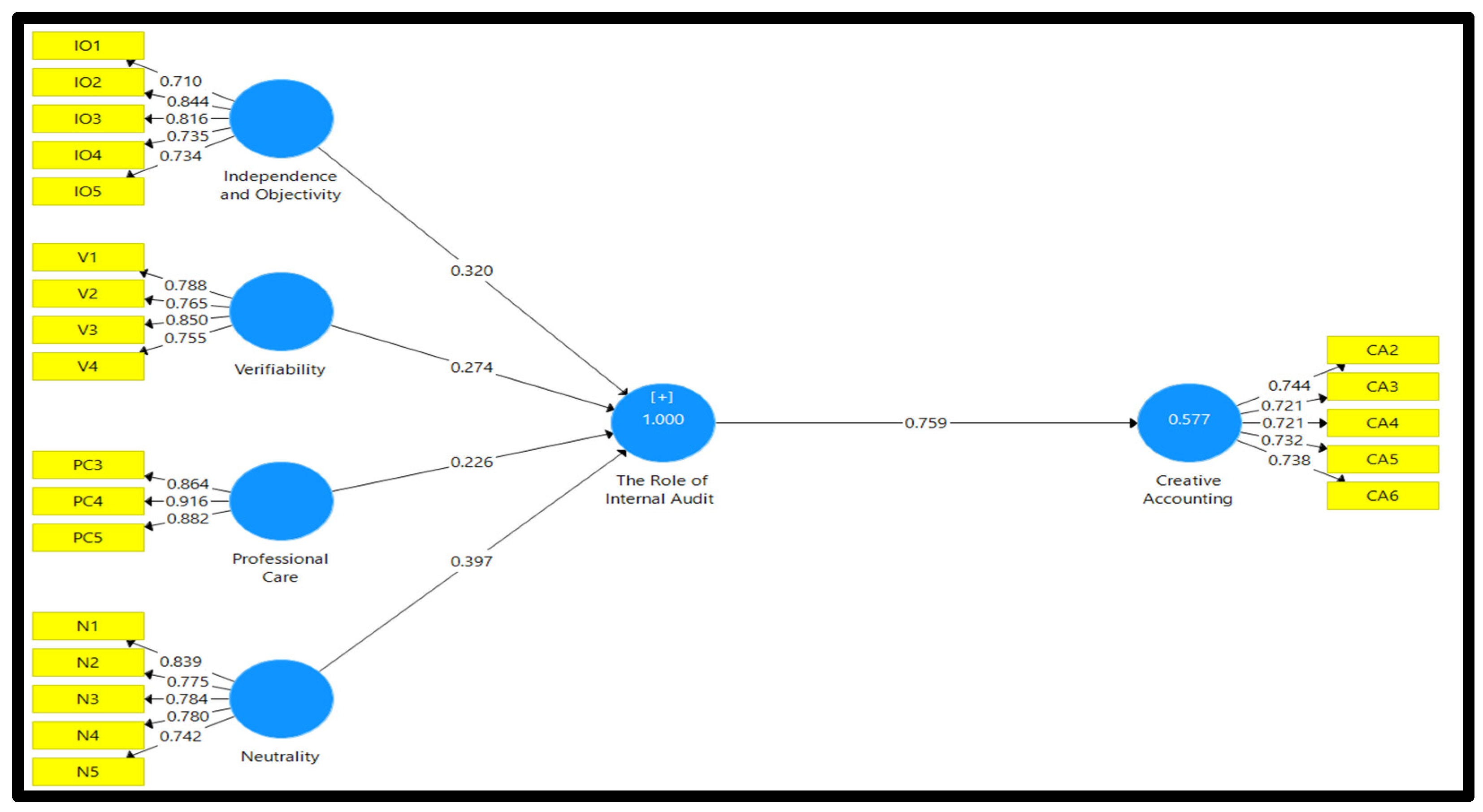

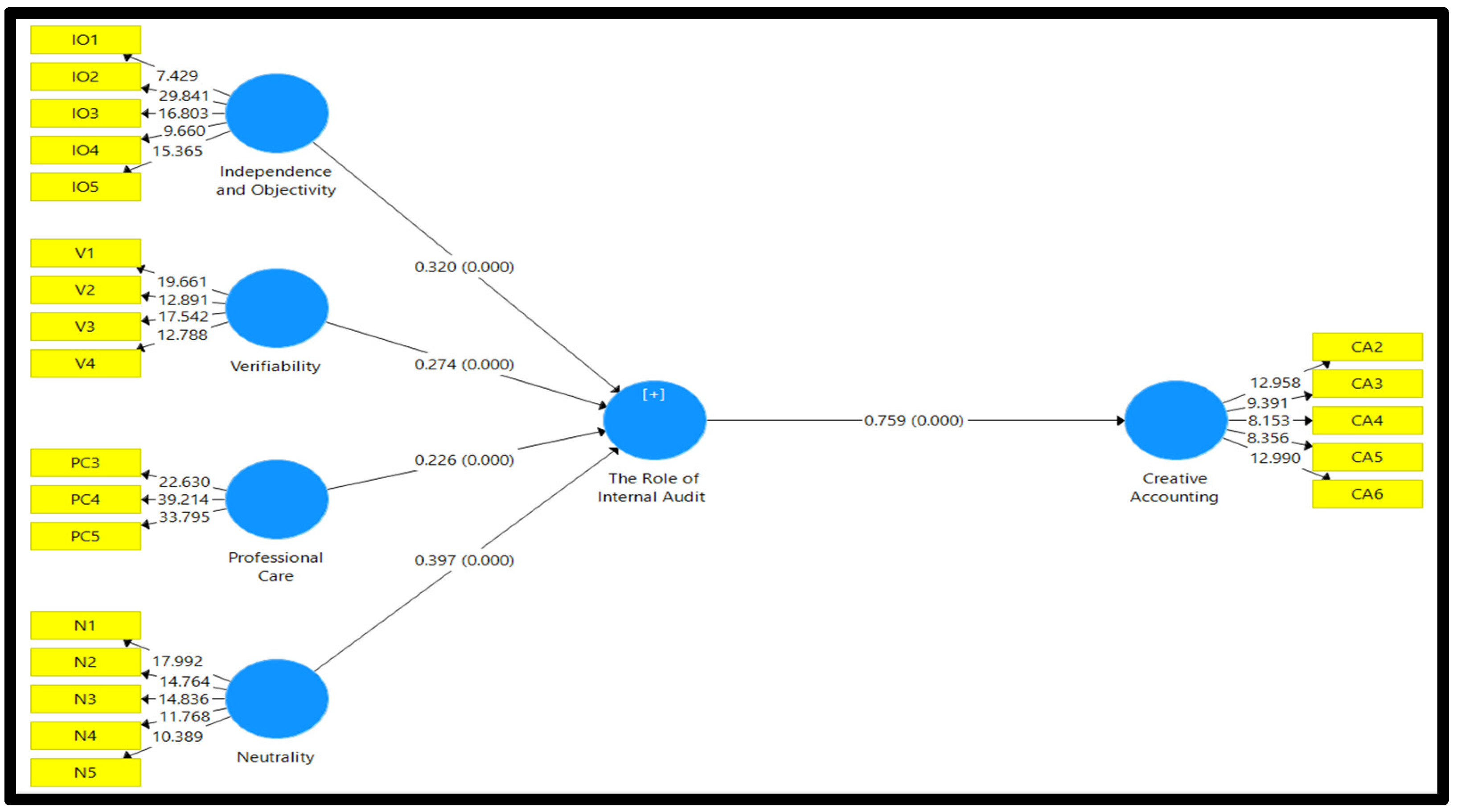

To find the T-Value, bootstrapping with Partial Least Squares 3.3.3 (PLS 3.3.3) software was used to evaluate all hypotheses.

Figure 2 depicts the T-Value for the proposed model.

The

p-value test result to test the variable IA (independence and objectivity, verifiability, professional care, and neutrality) on the reduced effects of CA on the reliability of financial statements was shown in

Figure 2 of the statistical analysis results in this section.

Table 7 shows the results.

According to

Table 7, the combined

p-value of IA (independence and objectivity, verifiability, professional care, and neutrality) = 0.000 and minimized effects of CA on the financial statement’s credibility (

Hair et al. 2014). As a result, it is significant at 0.05. Furthermore, according to

Table 7, the value of beta (internal audit combined (independence and objectivity, verifiability, professional care, and neutrality) = 0.759), which states that changing one part of IA combined (independence and objectivity, verifiability, professional care, and neutrality) will result in (0.759) a change in reduced effects of CA on financial statement reliability. These findings support hypothesis (H1), which indicates that the IA function (independence and objectivity, verifiability, professional care, and neutrality) has a substantial role in reducing the effects of CA on financial statement dependability in Jordanian Islamic Banks.

Table 7 shows a

p-valuefor independence and objectivity, as well as reduced effects of CA on financial statement reliability (

Hair et al. 2014). As a result, it is significant at 0.05. In addition, according to

Table 7, the value of beta (independence and objectivity) = 0.320, which means that changing one component of (independence and objectivity) will result in a change of (0.320) in the lessened effects of CA on financial statement dependability. These findings support hypothesis (H1.1), which indicates that independence and objectivity have a crucial impact on the reduced effects of CA on financial statement dependability in Jordanian Islamic Banks.

According to

Table 7, the

p-value for Verifiability = 0.000 and the lessened effects of CA on the financial statement’s reliability (

Hair et al. 2014). As a result, it is significant at 0.05. In addition, according to

Table 7, the value of beta (Verifiability = 0.274), states that changing one part of (Verifiability) will result in a change in the lessened effects of CA on financial statements’ dependability (0.274). These findings support hypothesis (H1.2), which argues that Verifiability has a crucial influence on the reduced effects of CA on financial statement dependability in Jordanian Islamic Banks.

Table 7 shows that the

p-value among professional care = 0.000 and that CA has a lower effect on the financial statement’s reliability (

Hair et al. 2014). As a result, it is significant at 0.05. In addition, according to

Table 7, the value of beta (professional care = 0.226, which means that changing one part of (professional care) will result in a change in the lessened effects of CA on financial statement reliability (0.226). These findings support hypothesis (H1.3), which states that professional care plays a significant role in reducing the effects of CA on financial statement reliability in Jordanian Islamic Banks.

Finally, according to

Table 7, the

p-value for neutrality = 0.000 and the lessened consequences of CA on the financial statement’s reliability (

Hair et al. 2014). As a result, it is significant at 0.05. Furthermore, according to

Table 7, the value of beta (neutrality = 0.397, means that changing one part of (neutrality) will result in (0.397) a change in the reduced effects of CA on the financial statement’s reliability. These findings support hypothesis (H1.4), which argues that neutrality has a significant role in the reduced effects of CA on financial statement dependability in Jordanian Islamic Banks.

11. Discussion

Bhasin (

2016) asserts that the purpose of CA is still to provide managers, companies, and accountants with an unfair edge. According to

Munteanu et al. (

2016) IA looks at whether the transactions and accounting procedures reported correctly represent the essence of the events that happened and if they are likely to be altered. The results of an IA mission must attest to the accuracy, completeness, and consistency with which financial accounting transactions from primary accounting records and financial statements are shown, as well as the integrity and coherence of the financial accounting system. Based on the factors of

Ghamri (

2020), there were no statistically powerful variations in the external auditors’ assessments of the impact of CA risk on auditing hazards (academic qualification, professional qualification, occupation, and experience). Based on these criteria, there were no statistically significant variations in the external auditors’ assessment of their obligation to uncover CA practices. According to

Balaciu et al. (

2012), the auditors in our sample discovered all the CA procedures in the study rather regularly, with the CA practices affecting financial assets having the lowest prevalence.

Auditor ethics has a considerable detrimental impact on auditors’ capacity to detect CA techniques, according to

Anggreni and Latrini (

2021), meaning that when an auditor detects CA practices in financial reports, the auditor selects to forgo ethics and ignore genuine findings. Meanwhile, audit tenure has a considerable positive impact on auditors’ capacity to detect CA practices in financial statements, meaning that the longer the audit tenure or audit engagement period, the better the auditor’s ability to detect CA practices in financial statements. Furthermore, according to

Akpanuko and Umoren (

2018), the CA is at the center of numerous accounting disputes. It denotes the modification of accounting statistics from what they do in accordance with economic reality to what managers want by exploiting or neglecting current regulations.

Abed et al. (

2022a) found that the audit committee significantly moderates the choice of CA in terms of financial reporting quality in the commercial banking industry. The findings of

Moghadam et al. (

2021) showed a positive and substantial association between intellectual capital and the readability of financial statements, indicating that as firms’ intellectual capital grows, so does the readability of their financial statements. The results of this study by

Dalwai et al. (

2021) show a decline in intellectual capital efficiency associated with improved annual report readability for financial sector firms, and corporate governance mechanisms like dispersed ownership and audit committee size also result in easily readable annual reports that support agency theory.

Drogalas et al. (

2017)’s findings emphasize the importance of IA in detecting accounting fraud, as well as the need for organizations to invest in IA processes and training to improve corporate performance. In addition, the research emphasizes the need for IA and fraud detection for businesses in economically depressed areas.

Abed et al. (

2022b) provide study findings that demonstrate the relationship between the transparency and disclosure factors and the degree of influence for CA determinants.

Shahid (

2016) discovered a favorable association between agency issues and CA but found a negative relationship between CA and corporate governance, ethical value, and future orientation. CA has also been shown to have a significant negative impact on financial reporting accuracy and objectivity. According to the findings of

Jarah and Almatarneh (

2021), a correct knowledge of the organization leads to an increase in job quality. Additionally, the organization regulates and reinforces workers’ efforts on the company’s objective track.

Al-Olimat and Al Shbail (

2021) found that the quality of external audits and institutional governance principles have a statistically significant influence on reducing innovative accounting methods in Jordanian industrial businesses. The capacity of auditors to discover CA methods is influenced by their independence, integrity, objectivity, contingent fees, advertising rights, commission determination, and organizational shape, according to

Al Momani and Obeidat (

2013). The findings of

Seifzadeh et al. (

2021) show a significant and negative relationship between management entrenchment, real and accrual earnings management, comparability, and a positive and significant relationship between management narcissism, overconfidence, and board effort and financial statement comparability. According to

Usman and Usman (

2022), the audit committee mediates the link between the board’s gender diversity, ethnic diversity, reputation, nationality, risk, and CA of the businesses.

13. Limitations and Future Research

Despite making some significant contributions, this study has certain drawbacks. As a result, admitting these limitations helps to the credibility of the current research findings. This study focuses on the variables stated in the conceptual design, with the goal of maintaining a balanced perspective in the diagnostic and interactive usage of the model in Jordanian Islamic banks, where the current study employed just 100 auditors to focus on internal auditors working in Islamic banks in Jordan. As a result, more bank responders may yield better findings. The current study concentrated on three aspects of internal audit. Other internal audit aspects, including audit committees, quality assurance, and improvement initiatives, can be employed. Furthermore, the current study recommends paying attention to activating the role of internal audit within banks because of its positive impact in adding value, improving operational effectiveness, and achieving goals, which contributes to limiting the use of any methods that would jeopardize the bank’s reputation. As a result, the current work might serve as a foundation for future research to improve field knowledge. As noted in earlier sections, the current study contradicted certain previous findings while being consistent with others. However, the shortcomings of the current study can be overcome in future research.

,

,

{kind=link}

{kind=link}