1. Introduction

Since 2014, the Russian-Ukrainian conflict has been at the epicenter of geopolitical debate at a worldwide level. The outbreak of this war took place in February 2014 following the Ukrainian ‘Revolution of Dignity’ and led to the Russian annexation of Crimea in 2014 as well as the war in Dunbas (2014 up to the present). The interest in this conflict has been vividly resuscitated and more actively stimulated in the economic and financial fields since the full-scale invasion of Russia in Ukraine on 24 February 2022

1. This has led to heated debate and controversies about whether the advanced economies of the West should apply hard economic measures against Russia and the extent by which this could result in detrimental consequences for monetary and fiscal matters in a global context.

The Dunbas war since its early initiation has proven to be detrimental for Ukraine as over 10,000 casualties and severe economic recessions have followed (

Bluszcz and Valente 2022). In the 2014 invasion, Russia succeeded in the annexation of Crimea and Russian separatists took over part of the Dunbas of south-eastern Ukraine, consisting of Luhansk and Donetsk oblasts. Since 2021, Russia had been accumulating a powerful military force along its border with Ukraine and the Russian invasion took place on 24 February 2022 with Vladimir Putin claiming that he was trying to prevent the eastward expansion of the North Atlantic Treaty Organization (NATO) that was regarded as threatening Russia’s national security. This invasion launched a new epoch of highly elevated geopolitical risk that led to 6.8 million Ukrainians leaving the country.

A significant strand of the literature has focused on investigating whether war or terrorist acts limit economic growth (

Razek and McQuinn 2021;

Nguyen et al. 2022) and result in intense volatility in financial markets (

Kollias et al. 2013;

Antonakakis et al. 2017;

Kyriazis 2021;

Chiang 2022;

Economou and Kyriazis 2022). When it comes to the Russian-Ukrainian conflict, emphasis should be given to the very large inflationary pressures

2, the food and energy deficiency (

Saâdaoui et al. 2022;

Del Lo et al. 2022) and the huge fluctuations in international markets (

Umar et al. 2022b) that the conflict has brought to the surface. This has happened as Russia and Ukraine are among the largest suppliers of agricultural commodities such as corn and wheat, fertilizers (

Ben Hassen and Bilali 2022) and energy (oil and natural gas) (

Umar et al. 2022a) in a global context. Arguably, the size and duration of the inflationary spiral that the Russian-Ukrainian war has brought about at a worldwide level has been one of the primordial concerns of policymakers, consumers, investors and the political and financial press. Apart from that, geopolitical uncertainty has proved to be an increasingly important determinant of financial (in)stability and the quality of life around the globe. This gives credence to the notion that geopolitical uncertainties could be the main source of stress in modern economies.

Providing a clear picture of the extent to which the Russian-Ukrainian conflict has been influential on financial markets at a global scale has been the motivation for our study. Estimations of efficient frontiers concerning portfolios of four different financial sectors and based on 13 alternative levels of risk appetite took place during the period since the Russian invasion (24 February 2022) up to the conquest of Mariupol (17 May 2022)

3. This region is considered to be a benchmark for the future of Ukrainian territories as it constitutes a land corridor between Crimea and Donbas and is a key port on the Black Sea without which the Ukrainian economy is in danger of being paralyzed

4. For the purposes of clearer and direct view of the war’s impacts on different categories of financial assets, four separate portfolios are examined. These are constructed of conventional assets of primordial importance such as national currencies, precious metals and fuel and agricultural commodities, as well as by modern and sophisticated forms of investments such as cryptocurrencies.

Estimations are conducted based on the highly reliable methodology of

Sharpe (

1966) that has been adopted in numerous high-quality studies (

Behr et al. 2013;

Kourtis 2016;

Kircher and Rösch 2021) and has been advanced for Efficient Portfolio construction (

Bodnar and Schmid 2009;

Bailey and de Prado 2012;

Chiu 2022). This allows us to strengthen research and make a quantum leap forward towards understanding investment behaviour during elevated geopolitical risk. Moreover, this study sheds light on the impact of risk appetite on better managing investors’ portfolios during the newly triggered Russian-Ukrainian war. In order to accomplish this, 13 alternative types of investors with differing risk-aversion levels are examined. To the best of our knowledge, this paper is the first one to investigate risk-aversion impacts on risk-adjusted performance in such a variety of portfolios’ constituents during the recent Russian-Ukrainian conflict.

This study contributes to the literature in a multifold manner. Firstly, this is the first study that puts under scrutiny such a large spectrum of conventional and modern financial assets with respect to the Russian-Ukrainian war. Moreover, the nexus of financial markets and investors’ risk-return is examined through the prism of the newly aroused tensions between Russia and Ukraine. This paper is among the very few academic papers investigating the period since the Russian invasion on 24 February 2022. Thirdly, the impacts of risk preferences on risk-adjusted performance during turbulent periods characterized by remarkably high inflationary pressures are placed under scrutiny. Moreover, this study enables the interested reader to distinguish whether geopolitical risk could indeed become the most influential determinant of out of the ordinary economic or financial phenomena.

The remainder of this paper is structured as follows.

Section 2 provides the literature review on findings regarding the nexus of geopolitical risk for national currencies, precious metals and fuel, agricultural commodities, as well as innovative cryptocurrencies.

Section 3 lays out the data and methodologies employed for estimations. The estimation outcomes and the economic and financial implications are offered and analyzed in

Section 4. Finally,

Section 5 concludes and presents avenues for further research.

2. Literature Review

An important number of academic studies have centered their interest on the nexus between geopolitical risk and financial markets. Moreover, high-quality academic papers have focused on investigating whether geopolitical uncertainty should be considered to be a major determinant of returns and volatility in popular investments such as currencies, precious metals and fuel, commodities and cryptocurrencies. Despite this, the impacts of the recent Russian-Ukrainian conflict (that started on 24 February 2022) on financial markets remains almost entirely unexplored. In order to elaborate on the arguments put forward by the aforementioned strands of the literature, we dwell on specific papers that are relevant to our study.

Studies with meaningful findings on the linkages of geopolitical risk (GPR) with national currencies have been brought to the surface.

Kisswani and Elian (

2021),

Iyke et al. (

2022),

Kyriazis and Economou (

2021) and

Duan et al. (

2021) are among the influential studies on this topic.

Kisswani and Elian (

2021) reveal that the global geopolitical risk index exerts short-run asymmetric impacts on the national currencies of the Republic of Korea and the United Kingdom. In addition, evidence shows that this index triggers symmetric long-run influences on all the five currencies examined. Thereby, the Canadian dollar, the Chinese yean, the Japanese yen, the Korean won and the British pound are receivers of impacts from geopolitical uncertainties. Furthermore,

Iyke et al. (

2022) support the argument that geopolitical risk can prove useful for predicting exchange rate returns with high accuracy. More specifically, it is estimated that 59% of exchange returns and 88% of currency values are efficiently predicted with in-sample and out-of-sample tests, respectively. Thereby, adopting geopolitical risk in forecasting models results in achieving higher profitability from investments in currency values, as GPR is a significant determinant of successful trading.

In a somewhat different vein,

Kyriazis and Economou (

2021) provide evidence that Turkish geopolitical uncertainty constitutes a generator of appreciation of the Turkish lira with respect to the US dollar, the Swiss franc and the Swedish krona. On the contrary, the Turkish currency has been seen to devalue with respect to the British pound, the Euro, the Mexican Peso, the Russian ruble and the Norwegian krona during the Erdoğan administration. By also focusing on developing and inflationary economies,

Duan et al. (

2021) detect medium-run co-movements between geopolitical uncertainty and currency values in Venezuela. Exchange rates are found to be significantly affected by hyperinflation that leads to currency depreciation. Lower values of the national currency are also revealed to emerge due to the higher geopolitical risk that appears in oil-dependent economies.

The second stream of research related to this investigation lies in the nexus between geopolitical risk and precious metals, as well as fuels and natural resources. Among others,

Antonakakis et al. (

2017);

Cunado et al. (

2020) and

Khan et al. (

2021) focus on the linkages between geopolitical uncertainty and oil prices and

Su et al. (

2021) on the connection of GPR with renewable energy. Moreover,

Dogan et al. (

2021) look into the connection between geopolitical risk and natural resources. Furthermore,

Baur and Smales (

2020),

Triki and Maatoug (

2021) and

Chiang (

2022) center their interest on the examination of the relations between geopolitical risk and precious metals.

In terms of higher precision,

Antonakakis et al. (

2017) provide evidence that geopolitical risk is the type of uncertainty that causes negative impacts on oil’s returns and volatility from 1899 to 2016. Moreover, it is supported that geopolitical uncertainty negatively affects the covariance between oil and stocks. With a similar mentality,

Cunado et al. (

2020) argue that higher geopolitical risk has led to reduction in oil prices since 1974. More specifically, the GPR is revealed to generate negative impacts on oil demand, representing global economic activity. These findings are in contrast with conventional beliefs about geopolitical shocks driving up prices, which mainly emanate from the connection between tensions in the Middle East and elevated oil prices. Moreover,

Khan et al. (

2021) reveal that geopolitical risk generates impacts on oil prices in the medium run. Apart from that, it is found that geopolitical risk is influential for the nexus between oil prices and financial liquidity when the same horizon is under scrutiny. It is noted that geopolitical uncertainty leads to this linkage becoming more intense and prolonged when its impact is considered. When it comes to

Del Lo et al. (

2022), they support the view that financial markets (and especially commodity markets) of a large panel of countries are negatively affected by the Russo-Ukrainian conflict and higher volatility is caused due to geopolitical tensions. In a somewhat similar vein,

Umar et al. (

2022b) argue that this conflict has been influential in terms of connectedness among financial markets internationally. Gold is found to be a net receiver of shocks while European equities and Russian bonds are revealed to be net transmitters to safe haven assets. This is partly in contrast with

Umar et al. (

2022a) who provide evidence indicating that most assets display a mix of positive and negative aspects with geopolitical risk. These effects are found to be related to the type of market and market conditions. With a similar mentality,

Będowska-Sójka et al. (

2022) provide evidence that gold, silver, the Swiss franc, green bonds, and real estate display hedging abilities towards geopolitical uncertainty stemming from the Russian-Ukrainian war. Nevertheless, hedging abilities are not uniform as they depend on scales from high- to low-frequency.

In addition,

Su et al. (

2021) identify a two-way causality and a mutual relation between geopolitical risk and renewable energy. It is detected that GPR can be a transmitter of both positive and negative impacts towards this type of energy. Estimations reveal that renewable energy could act beneficially in reducing geopolitical tensions. Moreover,

Dogan et al. (

2021) argue that geopolitical uncertainty nourishes negative impacts on the rents of natural resources for a group of 18 developing countries during a period that spans over 25 years. The middle and upper quantiles are found to be receivers of stronger effects from GPR. Furthermore, geopolitical uncertainty brings about less mixed results than economic policy uncertainty. It is supported that lowering geopolitical risk should constitute one of the primordial targets in developing countries.

When it comes to empirical studies of precious metals,

Baur and Smales (

2020) argue that gold and silver exhibit safe haven properties in a consistent manner and this proves to be useful for confronting the effects of geopolitical risks on investors’ portfolios. The usefulness of precious metals as safe havens against GPR is found to be more emphasized concerning geopolitical threats, not acts. Among precious metals, only gold and silver are found to be capable of constituting safe havens against both normal and extreme geopolitical events. Moreover, the level of hedging capabilities is found to be significantly higher in such metals in comparison with other financial assets. Similarly,

Triki and Maatoug (

2021) support that the representative S&P500 index exhibits a weaker connection with gold when geopolitical uncertainty is low, while this is stronger during geopolitically riskier eras. This fortifies the notion that gold presents diversifying and safe haven abilities during periods characterized by elevated risk of conflict. The safe haven role of gold against the volatility of the S&P500 index is found to be noteworthy during such intense periods. In a somewhat similar vein,

Chiang (

2022) provides evidence that gold serves efficiently as a hedging instrument against inflation. Higher inflation rates lead to increases in gold values. Moreover, it is argued that crises are beneficial for gold returns. Apart from that, gold is revealed to act as a hedge against currency depreciation while gold and stock prices exhibit complementarity in the majority of countries, which puts into doubt gold’s hedging abilities against stock markets. Most importantly, high geopolitical or economic uncertainty render gold more popular due to its safe haven role.

To be more precise,

Tiwari et al. (

2021) focus on determinants of portfolio performance and support the view that powerful co-movements take place between energy markets and agricultural markets while geopolitical risk is negatively influential on this nexus. Geopolitical uncertainty is considered to be responsible for bear markets in the energy sector while agricultural commodities exhibit hedging capabilities against these downwards tendencies. Corn, oats and wheat are revealed to be the most efficient agricultural commodities to improve investors’ portfolios. By also centering interest on improving relevant portfolios’ risk–return trade-off,

Mitsas et al. (

2022) estimate that geopolitical acts exert negative impacts on returns of sugar futures. Moreover, they provide evidence that geopolitical threats result in weak positive effects on the volatility of corn futures. Overall, geopolitics could prove useful for diversification in portfolios with commodities. This possibility is more pronounced during bull markets.

The nexus of agricultural products in portfolios through the prism of geopolitical risk are also placed under scrutiny in

Gong and Xu (

2022) and

Yang et al. (

2022). More specifically,

Gong and Xu (

2022) estimate that geopolitical uncertainty is the determinant force on significant dynamic linkages between commodity markets. This influence is revealed to be positive on the net spillovers of energy, agriculture and livestock commodities, whereas metals are receivers of negative impacts. Moreover, geopolitical acts are found to be more important than geopolitical threats for dynamic connectedness among markets. In a similar vein,

Yang et al. (

2022) argue that geopolitical risk displays significant time-varying impacts both on the aggregate commodity index and its subcategories. More specifically, geopolitical threats and geopolitical acts provide impacts of mixed direction, which are more emphasized during short periods. The agricultural commodities markets are revealed to be negatively influenced by geopolitical risk while these impacts became slightly positive during the Trump administration. Apart from that, geopolitical uncertainty proved to be less influential during the COVID-19 pandemic.

The fourth strand of academic research relevant to this study concerns the nexus between geopolitical risk and cryptocurrencies. Some of the most influential papers on this topic include

Aysan et al. (

2019),

Al Mamun et al. (

2020),

Su et al. (

2020),

Colon et al. (

2021) and

Selmi et al. (

2022). More specifically,

Aysan et al. (

2019) estimate that geopolitical tendencies are influential on Bitcoin’s returns and volatility both in a positive and a negative manner. It is argued that the positive nexus is more pronounced during periods of high geopolitical risk. This is the reason why Bitcoin should be a constituent of portfolios for achieving diversification during downwards movements in markets. This gives credence to the usefulness of this leading cryptocurrency as a hedging instrument during turbulent eras in geopolitics. In a similar vein,

Su et al. (

2020) support the view that a positive but also a negative nexus is traced between geopolitical risk and Bitcoin. Positive impacts of geopolitical risk on Bitcoin reinforce the viewpoint that this major cryptocurrency could act as a hedge against geopolitical uncertainty. It is argued that during periods of intense geopolitical risk Bitcoin can serve as a financial tool for portfolio optimization that could improve risk-adjusted performance.

In a similar vein,

Al Mamun et al. (

2020) argue that periods with high levels of economic policy uncertainty are the most important for tracing the impact of geopolitical risk on financial assets such as Bitcoin. Geopolitical risk is estimated to be by far the most significant determinant, among other uncertainties, of Bitcoin’s volatility and risk premia. Bitcoin is found to be positively correlated with gold during extremely stressed periods and it is only in these cases that Bitcoin serves as a safe haven in investors’ portfolios. Furthermore,

Colon et al. (

2021), by centering interest on 25 top cryptocurrencies, argue that in most cases they can function as powerful hedges against geopolitical risk. Their safe haven capacities against such risk are revealed to be stronger than their corresponding capacities against economic policy uncertainty. Nevertheless, mixed findings are raised regarding the connection between geopolitical uncertainty and cryptocurrencies depending on the estimation methodologies adopted. In tandem with previous findings,

Selmi et al. (

2022) provide evidence that Bitcoin as well as gold present the ability to serve as safe havens against low-performing assets in times when geopolitical risk is elevated due to war episodes. Bitcoin is revealed to be resilient against the consequent market crashes due to its negative nexus with risky assets. Nevertheless, the hedging capabilities of Bitcoin against geopolitical uncertainty are not stable as time evolves.

3. Data and Methodology

This paper undertakes the strenuous task of investigating whether and how the Russian-Ukrainian conflict has been influential on the profitability of portfolios of international investors. Emphasis is given to the risk-return trade-off in portfolios that consist of major national currencies as well as national currencies of countries closely linked with this war. Moreover, estimations take place regarding precious metals as well as fuels of major importance that have been tightly connected with the Russian and the Ukrainian economies but are also widely used by a large spectrum of countries at a global level. Apart from these, this study focuses interest on agricultural commodities, as the Russian-Ukrainian conflict has triggered a spectacular increase in relevant market values that has brought the global economy to the edge of a food crisis. To include modern forms of investments in this analysis, cryptocurrencies are also considered for estimation. Such innovative forms of investments become particularly popular when the breakout of crises of all types render conventional investment tools less profitable.

In terms of higher contemporary relevance, data on eight major national currencies have been downloaded. To be more precise, the Euro (EUR), the British Pound (GBP), the Swiss Franc (CHF), the Chinese Yuan (CNY), the Japanese Yen (JPY), the Canadian Dollar (CAD), the Australian Dollar (AUD) and the Dollar of New Zealand (NZD) have been adopted as major currencies. Moreover, the Russian Ruble (RUB) and the Turkish Lira (TRL) are under scrutiny due to the relevance of these countries to the Russian-Ukrainian war. This conflict has led to large fluctuations in currency values and higher levels of uncertainty for relevant investors

5. When it comes to the precious metals under consideration, data from the Bloomberg indices on gold, silver, aluminum, copper and nickel are extracted. These indices are considered to be highly representative of the worldwide market values of these metals. Moreover, data regarding the Bloomberg indices on WTI Crude Oil and natural gas are downloaded and used, as extreme volatility in fuel prices has been one of the primary consequences of this war that have resulted in a cost burden for numerous economic activities to a worldwide extent

6,7.

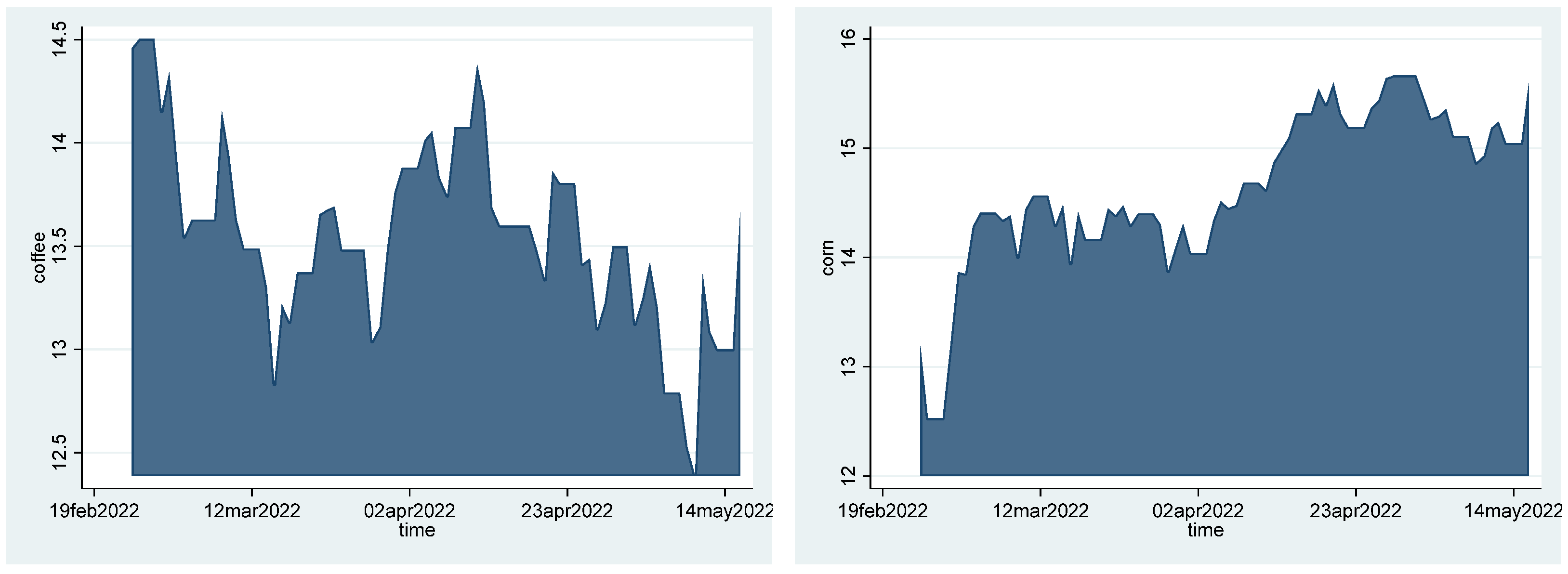

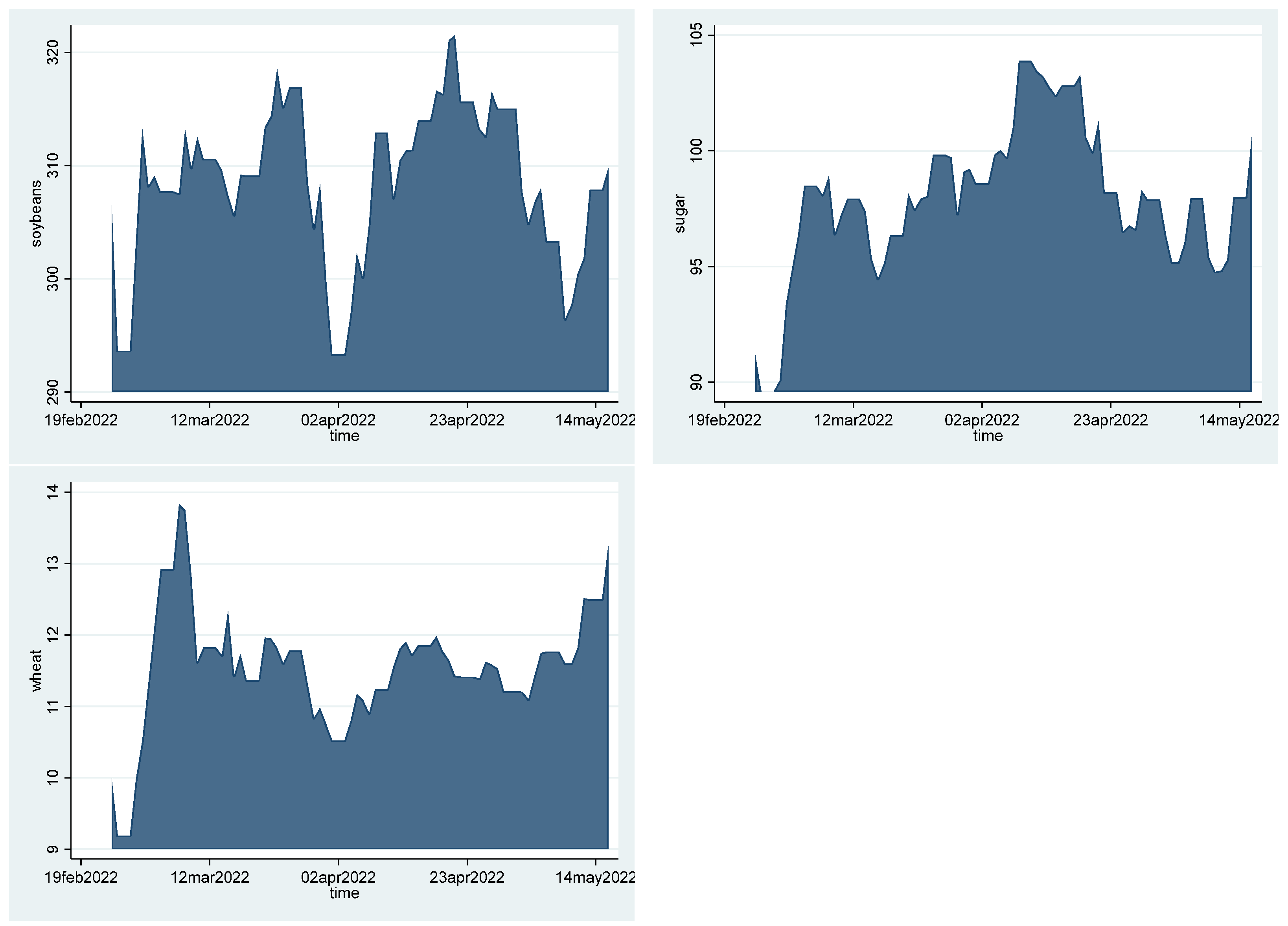

In addition, an array of agricultural commodities comes under scrutiny, as the Russian-Ukrainian conflict has led to great shortages of such products (

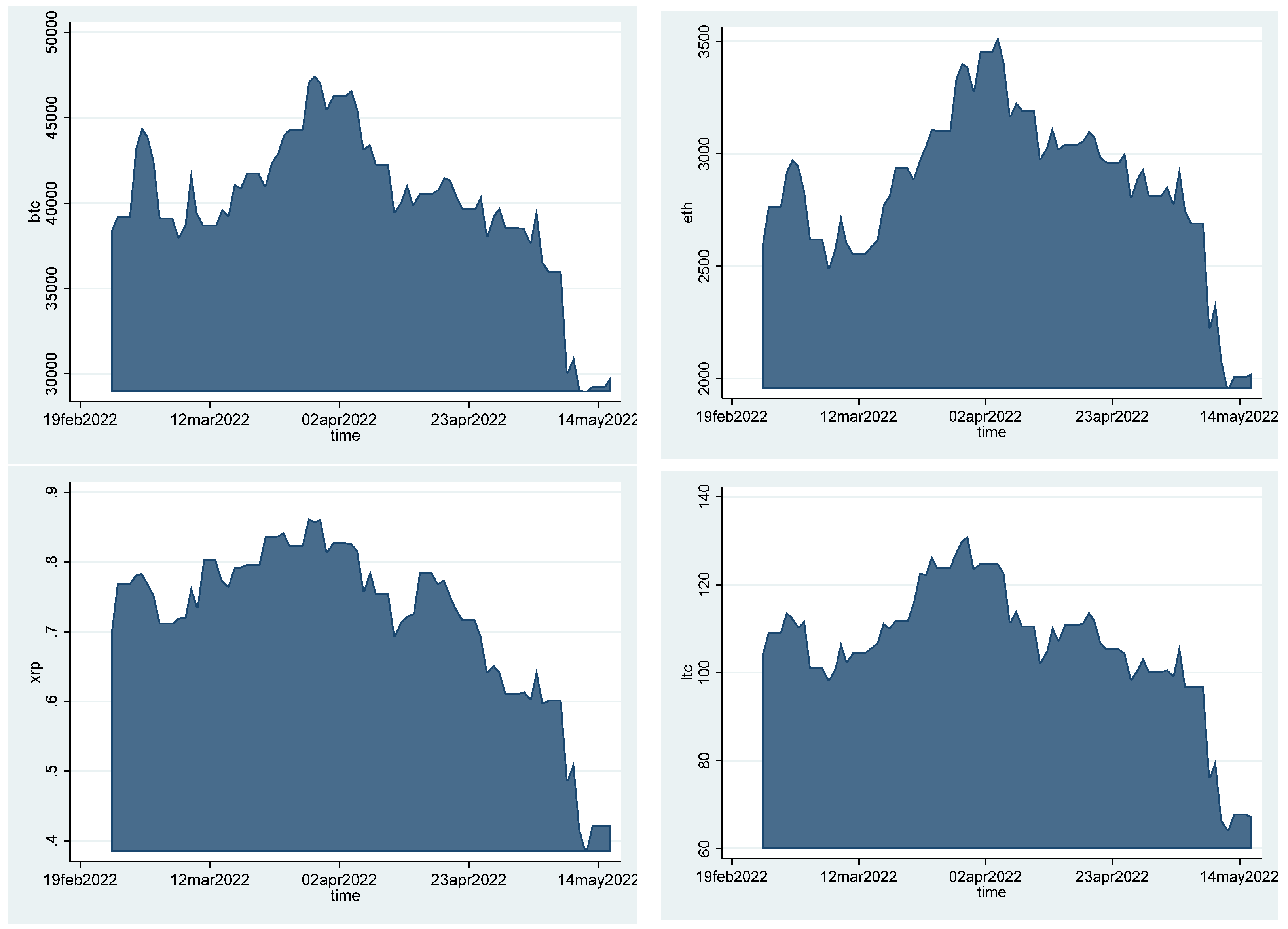

Ben Hassen and Bilali 2022) Therefore, data from the respective Bloomberg indices concerning coffee, corn, soybeans, sugar and wheat are also employed. Lastly, but far from least, the market values of the four most prominent cryptocurrencies (Bitcoin, Ethereum, Ripple and Litecoin) are used for estimations. This enables the examination of geopolitical impacts not only on traditional assets but also on modern and sophisticated ones that become favorites for investors to a rapidly proliferating extent. All daily values for cryptocurrencies are extracted from the coinmarketcap.com website that has been used as a trustworthy source in a large number of prestigious papers (

Gandal et al. 2018;

Gkillas and Katsiampa 2018;

Beneki et al. 2019;

Papadamou et al. 2021a,

2021b;

Vidal-Tomás 2022).

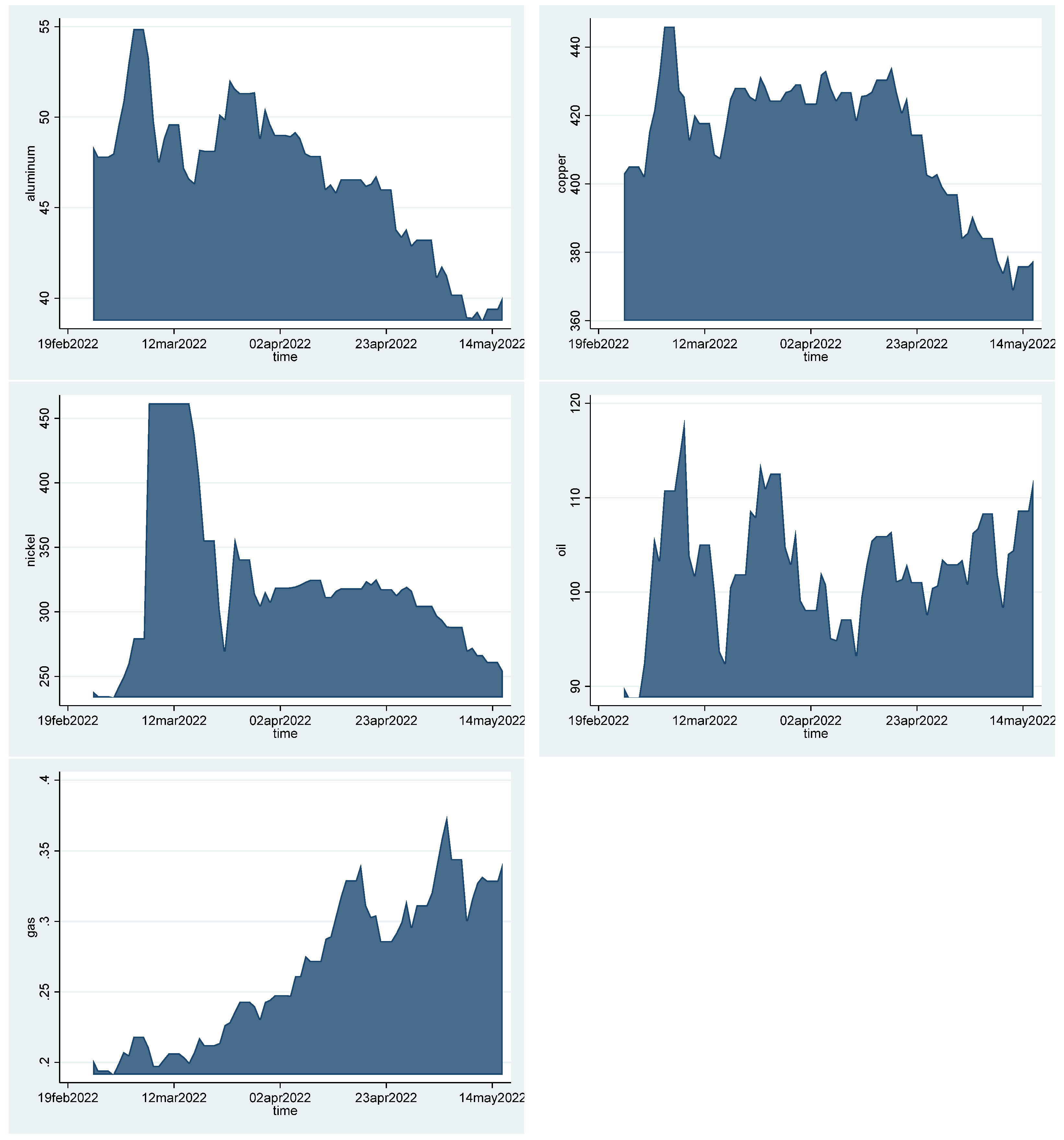

Table 1 illustrates the descriptive statistics of the variables under consideration. It can be seen that the Russian ruble is the most volatile among national currencies. Moreover, silver appears to be significantly more volatile than gold and nickel is the most volatile among metals. Crude oil and natural gas are also revealed to present large fluctuations in market values. Moreover, Bitcoin is found to be the riskiest among cryptocurrencies. As concerns the skewness and kurtosis metrics, no extreme phenomena of asymmetry are detected. Moreover,

Table A1,

Table A2,

Table A3 and

Table A4 in

Appendix A display the correlation matrices of the four portfolios with the alternative types of financial assets and

Figure A1,

Figure A2,

Figure A3 and

Figure A4 illustrate the market values of variables of each category.

As concerns the methodology, portfolio optimization is employed, which concentrates on improving the risk-return nexus for investors. It should be emphasized that a typical portfolio is characterized by its mean return and its overall volatility. The mean return of the portfolio is calculated by multiplying the weight of each asset (

) in the portfolio with the mean return of this asset

as can be seen in Equation (1) if the portfolio consists of two assets

while the overall volatility of the portfolio is estimated by the standard deviation of the portfolio as presented in Equation (2) when the portfolio consists of two assets

where

represents the correlation coefficient between the two assets considered.

For the purposes of conducting Sharpe’s optimization, a series of estimations should take place. First of all, data on daily closing prices are employed for estimating daily returns. Returns are calculated by using the closing prices (market values) of assets, according to Equation (3).

Moreover, the mean of returns of each stock is estimated and each mean is subtracted from returns to arrive at the excess returns for each stock as can be seen in Equation (4).

Thereby, the matrix of excess returns is obtained and this is used for constructing the transpose matrix of excess returns. Furthermore, by multiplying the excess returns matrix (

A) with the transpose of the excess returns matrix (

A’) and dividing by the number of observations of each time series (

N), the variance-covariance matrix is estimated by Equation (5)

The next step is to multiply the matrix of mean excess returns with the matrix of weights

primarily assigned based on risk-averse, risk-indifferent or risk-loving character. This would give the mean return of the portfolio. Moreover, by multiplying this weights matrix

with the variance-covariance matrix

and the transpose of the weights matrix (

), the variance of the portfolio is obtained as presented in Equation (6).

Sharpe’s optimization serves for finding the optimal weights that would maximize portfolio returns and at the same time minimize portfolio risk (

Sharpe 1964,

1966,

1992;

Behr et al. 2013;

Kourtis 2016;

Kircher and Rösch 2021). Maximization of Sharpe’s ratio takes place (Equation (7)) under the constraints that each weight takes no larger value than 1 and no lower value than 0 (Equation (8)) and that the sum of all weights should indispensably be equal to 1 (Equation (9)).

such that:

The estimation of optimal portfolios is conducted through the lens of subjective risk-preferences for a large spectrum of risk-aversion levels. For the purposes of risk-adjusted efficiency analysis from the perspective of different types of investors, the highly influential methodology of Efficient Portfolio construction (

Elton et al. 1978;

Bodnar and Schmid 2009;

Bailey and de Prado 2012;

Chiu 2022) is adopted. In other words, a set of four alternative (based on different sectors of financial assets) sets of optimal portfolios (based on different risk levels) is estimated and this results in the optimal set of portfolios, which is called the Efficient Frontier of optimal portfolios. The maximum risk aversion is at the state where the risk-seeking parameter

takes the value of zero while the minimum risk-aversion level holds when

equals one. This allows for the Efficient Frontier to be accurately depicted. Each combination (point) of expected returns and standard deviation that lays below this frontier should be rejected no matter which are the risk preferences of investors. It should be noted that the strenuous task of estimating Efficient Frontiers takes place four times for safely depicting the optimal portfolios consisting of national currencies, precious metals and fuel, agricultural commodities and cryptocurrencies.

4. Outcomes from Estimations

For the purposes of estimating the optimal asset allocation in a portfolio that consists of major national currencies and currencies of countries related to the Russian-Ukrainian conflict, ten national currencies of primary importance and relevance are taken into account. Moreover, portfolio optimization takes place for 13 varying levels of risk-aversion on the part of investors.

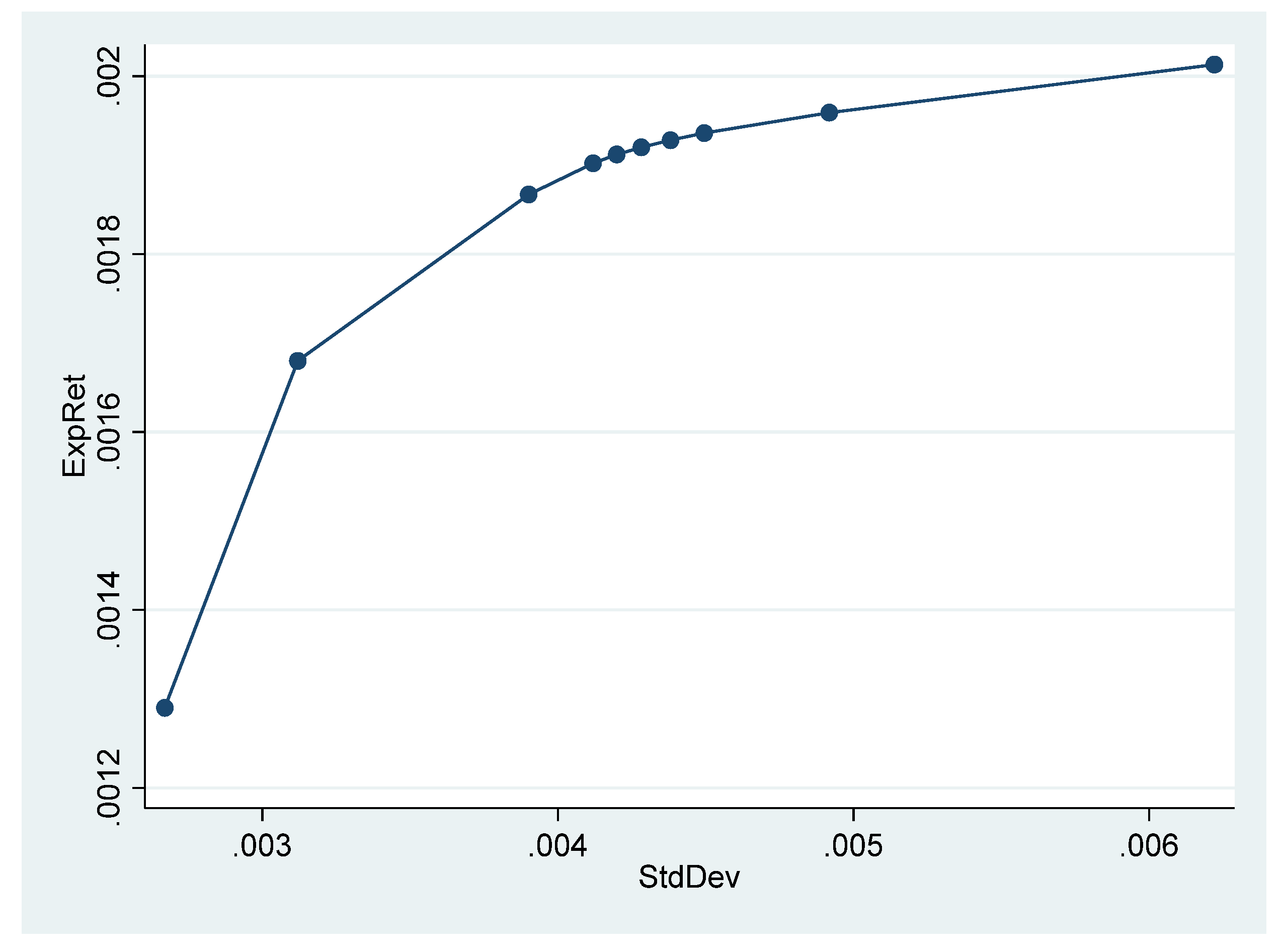

Figure 1 displays the efficient portfolio derived by conducting optimization procedures based on the Sharpe optimization techniques.

It should be emphasized that the risk-aversion level

takes values ranging from zero (maximum risk-aversion) to one (minimum risk-aversion). Higher levels of risk-aversion are revealed to generate higher levels of portfolio’s expected return but also higher levels of portfolio’s standard deviation, which constitutes the measure of a portfolio’s risk. In terms of higher precision,

Table 2 displays the optimal weights by which the national currencies should be included in each of the potential optimal portfolios.

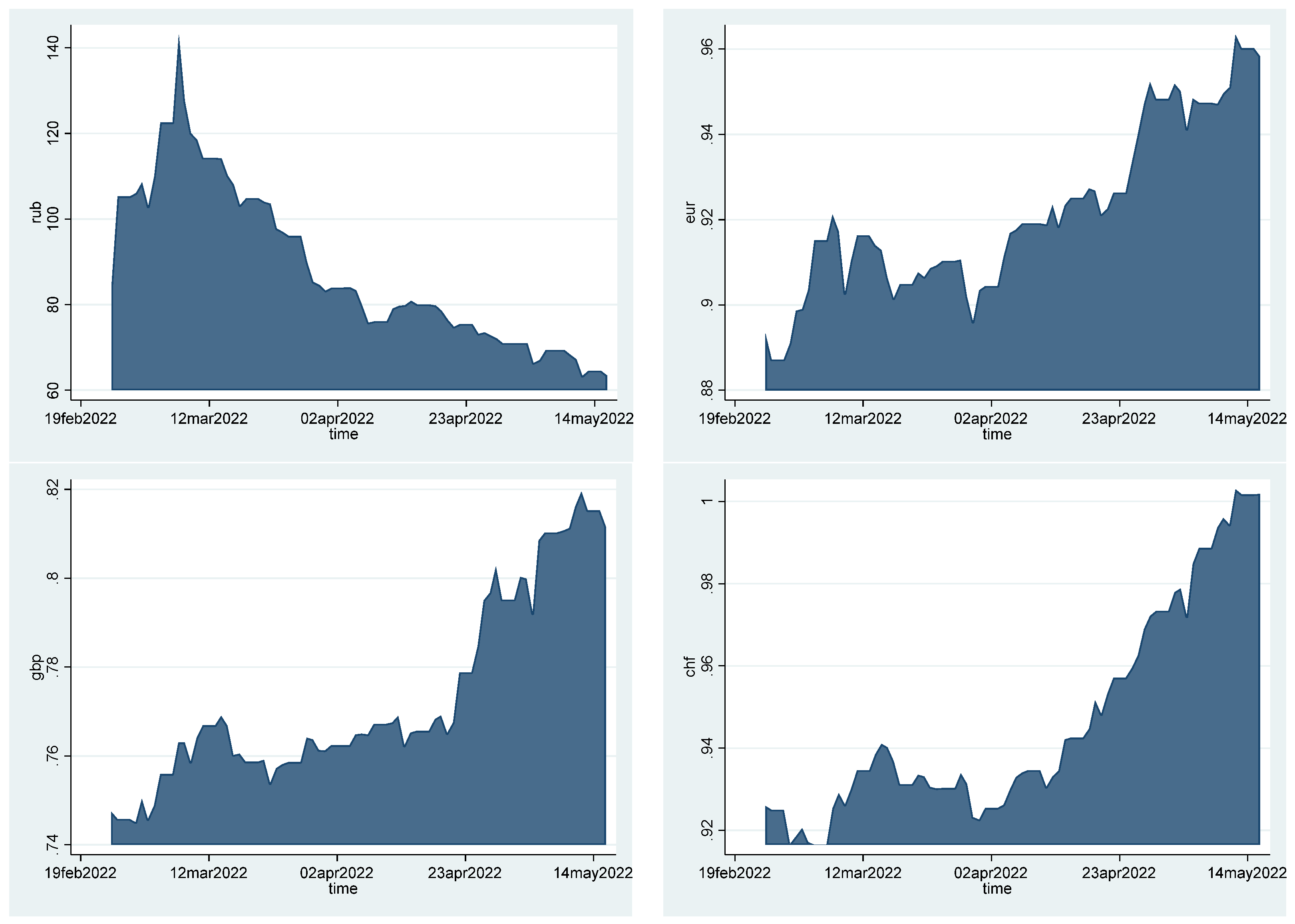

Estimations of the optimal asset allocation in a portfolio consisting of major national currencies and national currencies relevant to the Russian-Ukrainian war have brought to the surface a number of fruitful findings. More specifically, the optimal portfolio for investors with extremely high risk aversion (

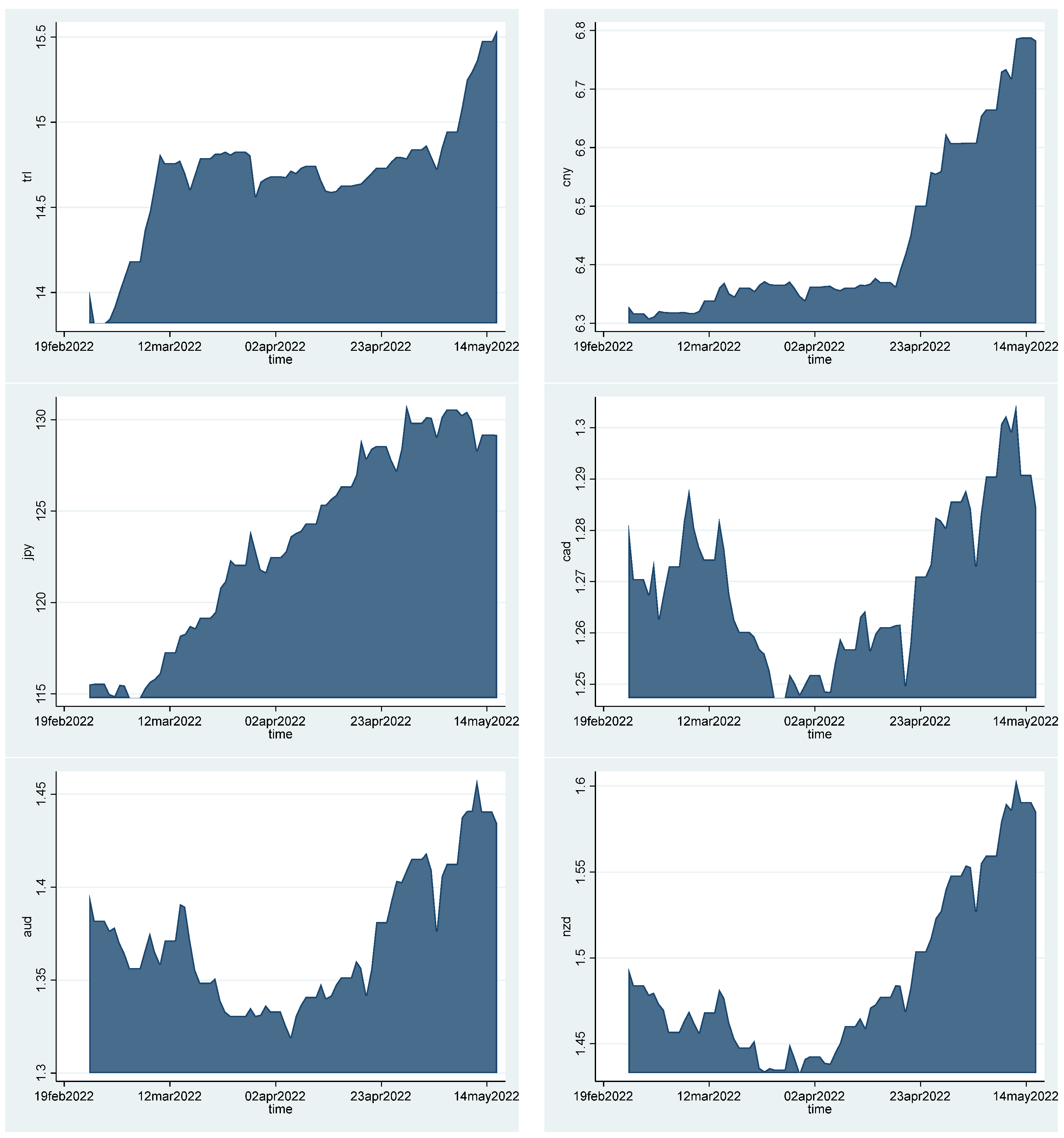

) should mainly consist of the Chinese yuan (52.2%). The remaining constituents of this low-risk optimal portfolio should be the Japanese yen (10.2%), the Turkish lira (15.76%), the Euro (1.5%), the Swiss franc (1.48%) and the Russian ruble (0.56%). These findings are corroborated by the graphs of the market values of the Chinese yuan and the Japanese yen in

Figure A1 in

Appendix A where it is evident that they present abrupt and large increases. Notably, the good performance of the Turkish lira with regard to other currencies partly abides by the findings of

Kyriazis and Economou (

2021). It should be emphasized that, as the level of risk-aversion decreases even slightly, the Chinese yuan does not form part of the optimal portfolio while larger shares of the Japanese yen and the Turkish lira should be included for the best possible risk-return trade-off to be achieved. Moreover, emphasis should be given to the point that risk-neutral investors as well as risk-loving speculators hold the same synthesis in their optimal portfolios, which is the allocation of all their money into the Japanese yen.

It is easily observable that the Russian ruble does become part of the synthesis of optimal portfolios to a significant extent. This could be attributed to the high volatility it presents during the conflict and the abrupt decrease in market values that it experienced, particularly during the first week of this war. Moreover, it is evident that national currencies of countries that are not directly connected with the war are not constituents of the optimal allocation for a range of risk-aversion levels. Therefore, the Canadian dollar, the Australian dollar and the dollar of New Zealand make only minor contribution to amelioration of the portfolio’s risk-adjusted performance during this major geopolitical event.

It should be underlined that the Minimum Variance Portfolio (MVP) that corresponds to the highest level of risk-aversion and the lowest standard deviation generates a portfolio’s expected return equal to 0.0129% and a risk equal to 0.00267. Intriguingly, the portfolio with the highest level of risk appetite () achieves an expected return equal to 0.201% and risk equal to 0.00622. This gives credence to the notion that significantly higher levels of risk suffered by risky portfolios consisting of currencies do not lead to proportionally higher level of profitability. Thereby, the risk-return trade-off is not improved as much as risk-lovers would wish when risky optimal portfolios are constructed.

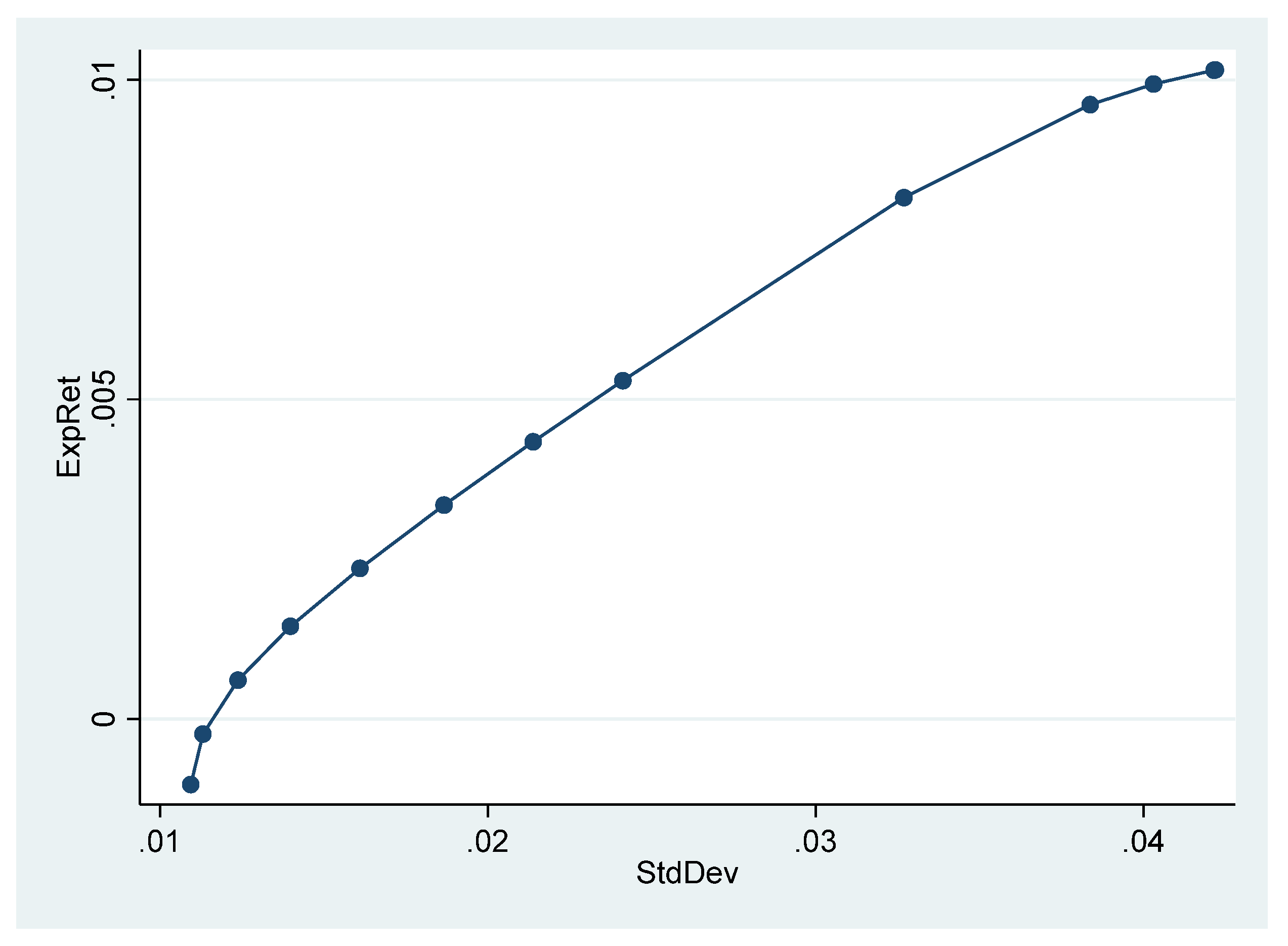

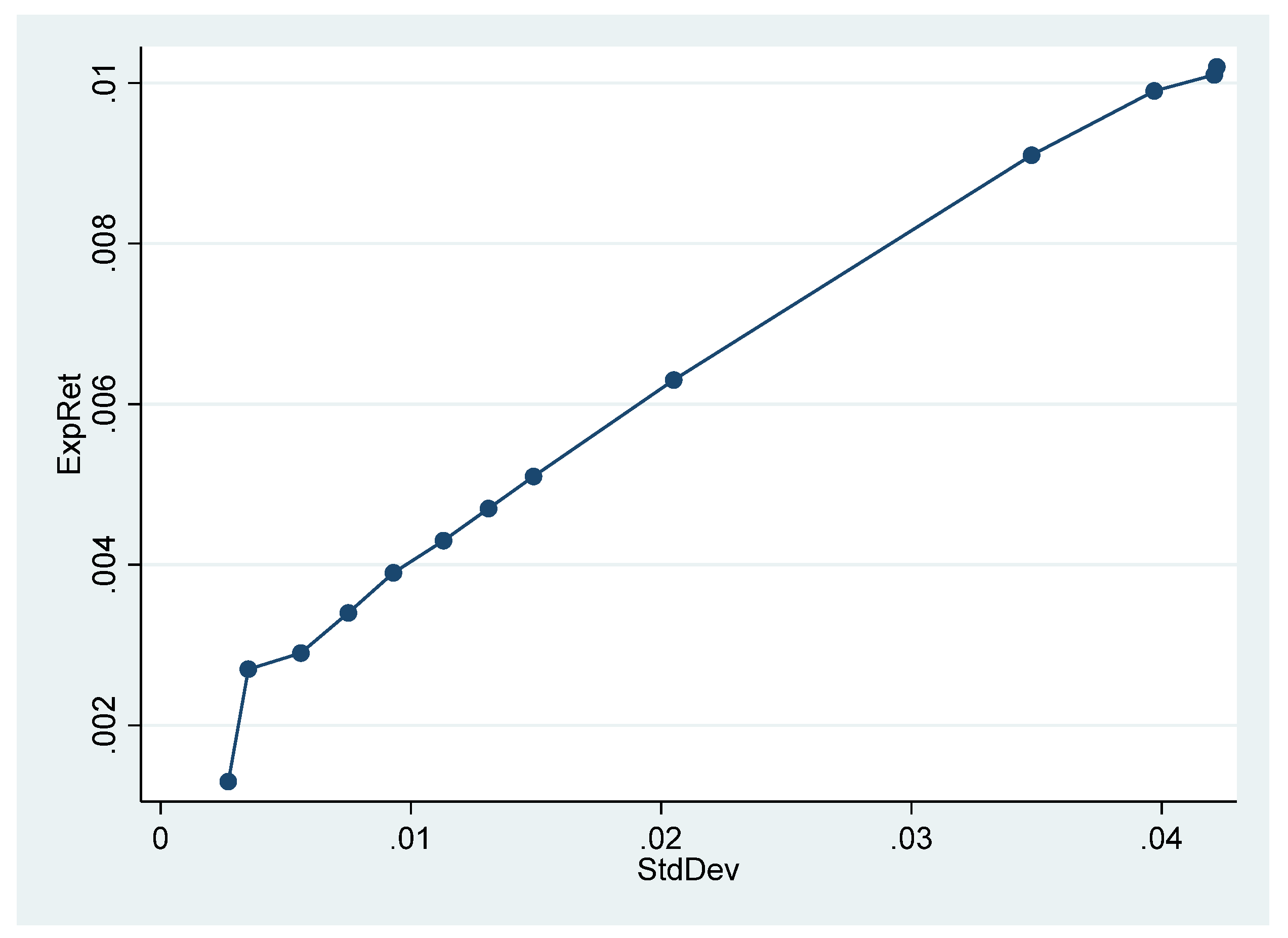

The Efficient Frontier for investors in different types in precious metals and fuel is depicted in

Figure 2. Moreover, the optimal allocation of different levels of risk-aversion is illustrated in

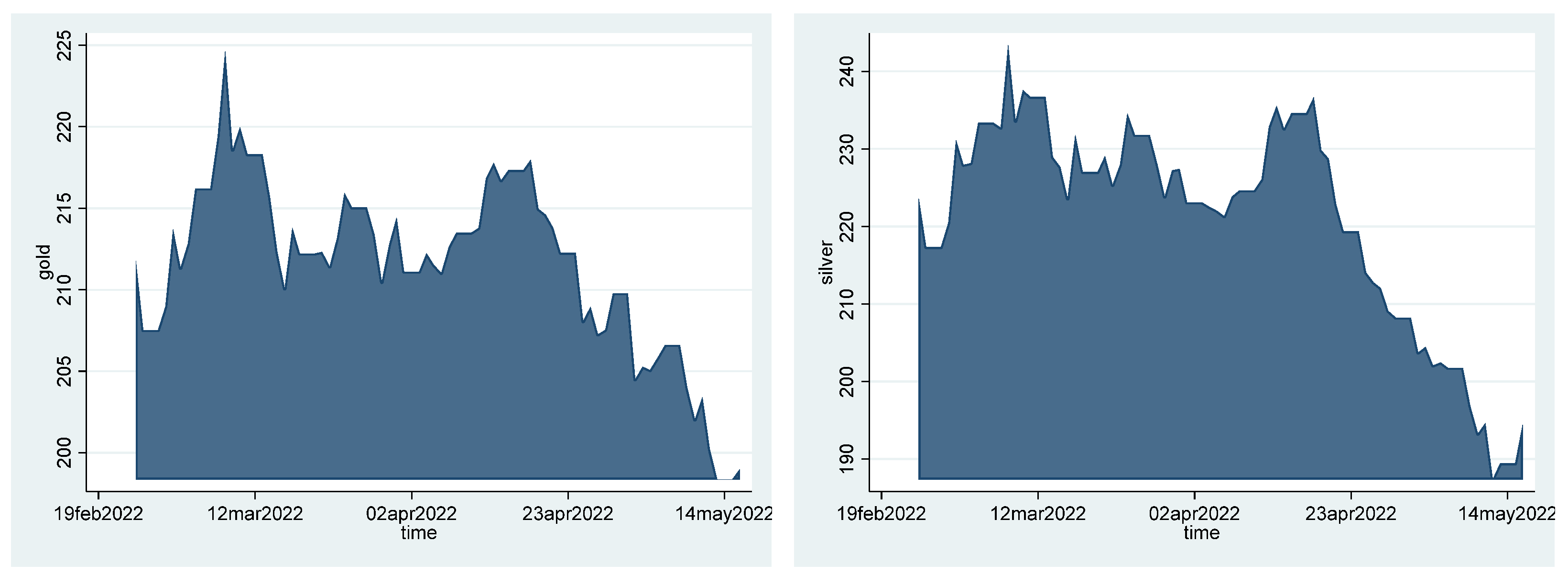

Table 3. Interestingly, the Minimum Variance Portfolio generates negative returns (equal to −0.103%) and risk equal to 0.010941. The composition of this lowest-risk optimal portfolio is gold: (78.24%), copper (21.75%) and aluminum (0.76%). Thereby, gold and copper are confirmed to act as safe havens during the Russian-Ukrainian conflict. The safe haven abilities of gold during elevated geopolitical tensions corroborate the findings of

Triki and Maatoug (

2021).

It should be highlighted that for slightly lower levels of risk-aversion the optimal weights of gold, copper and aluminum decrease while higher weights are assigned to natural gas, oil and nickel. More specifically, a lower risk-aversion level (

) brings about the following synthesis: gold (58.09%), copper (9.56%), nickel (3.03%), oil (1.44%) and natural gas (27.89%). This is somewhat in contrast with slightly lower risk-aversion levels (

) that result in gold (45.67%), copper (3.55%), nickel (4.46%), oil (8.14%) and natural gas (41.38%) being the optimal weighting scheme. Remarkably, oil is increasingly influential until high to modest risk-aversion levels (

) are considered but then its importance fades out. On the other hand, natural gas proves to be the most influential factor for profitability and this is the reason why profit-seekers with intense appetite for risk (

) should optimally select to invest all their resources in natural gas. Notably, this optimal portfolio presents expected returns equal to 1.016% and standard deviation takes the value of 0.04219. The high weighting that natural oil exhibits in optimal portfolios is in accordance with its market value becoming approximately double during the war as can be seen in

Figure A2 in the

Appendix A.

It is noteworthy that highest risk-aversion levels lead to negative returns and that the riskier portfolio bears approximately four times as high the volatility of the safest portfolio. Moreover, it is noticeable that the safest portfolio with precious metals and fuel performs significantly worse than the optimal portfolio of national currencies with the same level of risk-aversion. By contrast, the riskier among optimal portfolios with precious metals and fuel achieves expected returns that are five times as high compared to the corresponding optimal portfolio with national currencies.

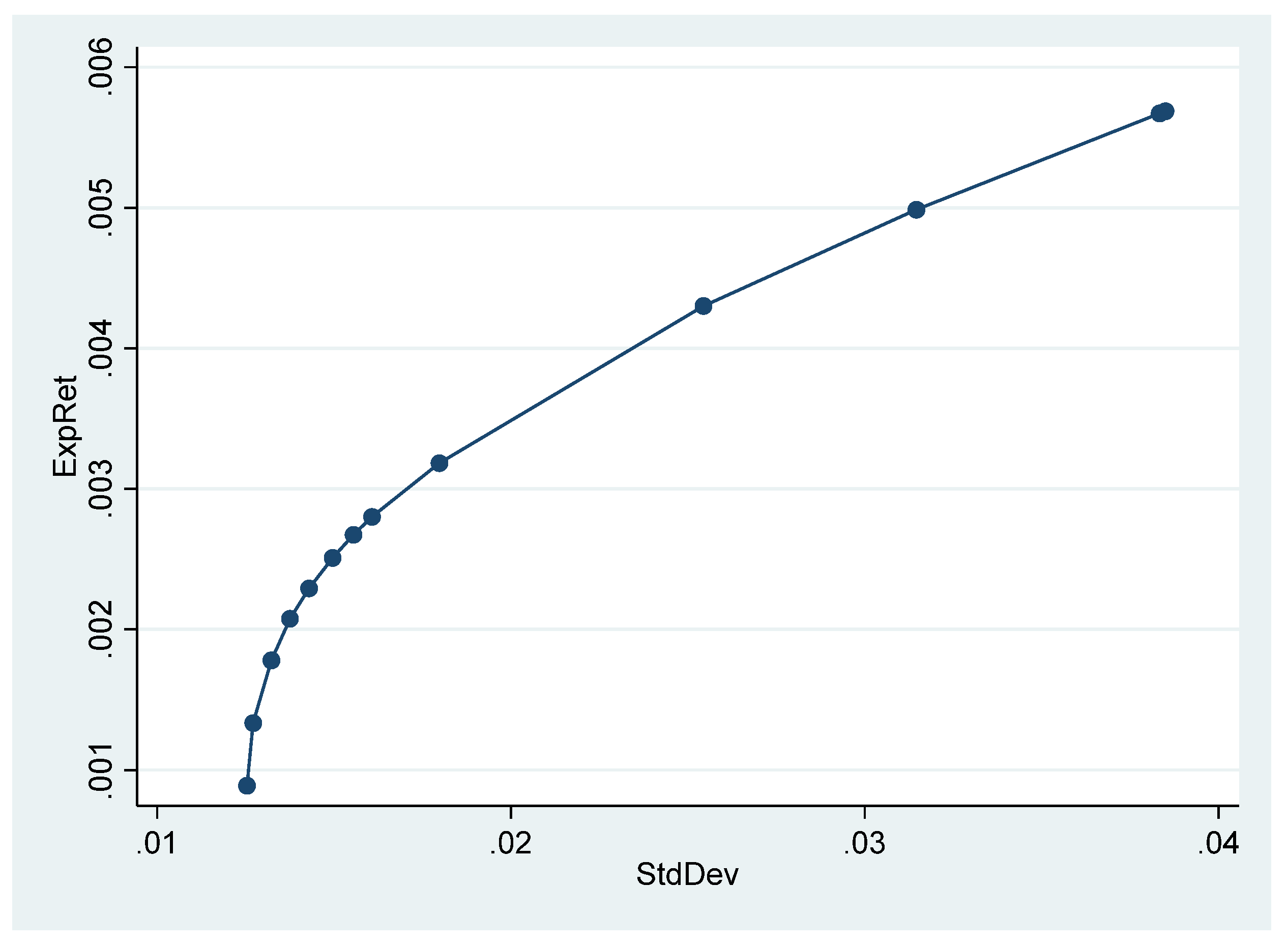

When it comes to investigating the optimal allocations in agricultural commodities portfolios for different levels of risk appetite during the Russian-Ukrainian war, the Efficient Frontier is laid out in

Figure 3 while analytical results are exposed in

Table 4. Interestingly, the optimal portfolio with the highest level of risk-aversion exhibits expected return equal to 0.089% and standard deviation takes the value of 0.01254. It should be underlined that this portfolio is characterized by worse risk-adjusted performance than the respective Minimum Variance Portfolios that are comprised of national currencies or precious metals and fuel. Interestingly, this portfolio has a range of agricultural commodities as its constituents with soybeans and sugar holding the largest weights (37.38% and 36.62%, respectively). Interestingly, coffee (18.37%) and corn (7.64%) also form part of this low-risk portfolio. Investors should also be aware that the optimal weights of sugar and corn increase while those of coffee and soybeans decrease when risk-aversion weakens but still exists at considerable levels.

Somewhat surprisingly, soybeans present zero contribution to the optimal portfolios of risk-indifferent levels whereas corn and wheat are estimated to be the only suitable constituents of these types of investment portfolios. To be more precise, when

, the optimal synthesis is soybeans (54.11%) and wheat (45.89%) but when tendency towards risk increases (

then wheat takes the lead and the optimal composition becomes soybeans (27.36%) and wheat (72.64%). This reinforces the viewpoint that wheat is the most important nutritional material whose lower supply elevates prices by such an extent that this renders it the steam-engine of profitability. This is also evident in the case of the most risk-seeking optimal portfolio that is constructed by fully investing in wheat. It should be noted that the emergence of corn and wheat as very good performers and important constituents of optimal portfolios during periods of high geopolitical risk abides by the findings of

Tiwari et al. (

2021).

It is worth mentioning that the optimal portfolio of agricultural commodities that is characterized by the highest risk appetite generates expected returns equal to 0.569 and presents standard deviation taking the value of 0.0385. Arguably, these returns are almost six times as large as those derived by the Minimum Variance Portfolio while risk is approximately three times as large. This indicates that higher levels of risk-seeking represent opportunities for amelioration in terms of risk-adjusted performance in optimal portfolios.

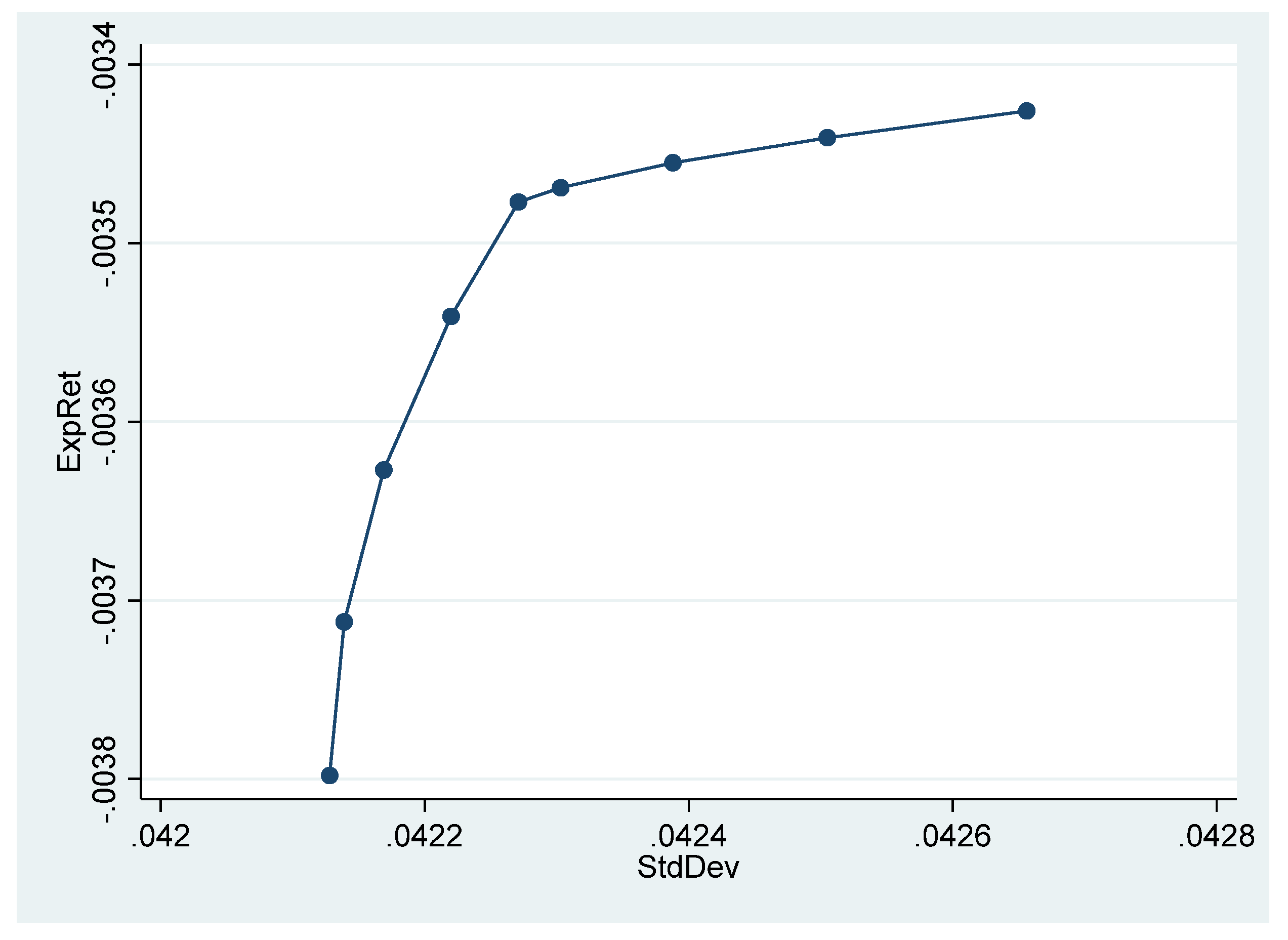

Interesting findings are also revealed based on the estimations concerning the Efficient Frontier emanating from portfolios including major cryptocurrencies.

Figure 4 displays the Efficient Frontier graphically and

Table 5 provides the optimal weights of the cryptocurrencies examined concerning each separate risk-aversion level.

It should indispensably be highlighted that all optimal portfolios with cryptocurrencies are characterized by negative levels of expected returns which are accompanied by high levels of risk. First of all, the Minimum Variance Portfolio indicates expected returns equal to −0.38% and risk measure equal 0.04213. Emphasis should also be given to the result that optimal portfolios with the highest level of risk-aversion do not have many differences as regards returns and volatility from optimal portfolios characterized by risk neutrality or high levels of risk-seeking. To be more precise, when , expected returns take the value of −0.347% and risk equals 0.0423 while the most risky optimal portfolio () displays returns and volatility with values of −0.343 and 0.04266, respectively.

It is worth noticing that Bitcoin is the most preferable asset in all levels of risk-aversion. More specifically, the Minimum Variance Portfolio mainly comprises Bitcoin (91.19%) while it should be highlighted that optimal portfolios with somewhat higher risk appetite (ranging from

to

) estimate Bitcoin to be the only appropriate investment for profit-maximizing with respect to risk. Moreover, risk-neutral towards risky portfolios adopt Ethereum in tandem with Bitcoin for the purposes of achieving the optimal nexus between profitability and volatility. More specifically, the risk-neutral portfolios (

) assign to Bitcoin weights of 96.23% and 89.52%, respectively, while the remaining money resources should be allocated to Ethereum. Notably, the most risky portfolio (

) is comprised of Bitcoin by approximately three quarters of the overall portfolio’s value while Ethereum holds slightly less than a quarter of the total amount. The necessity of including Bitcoin in portfolios during geopolitically turbulent period is in tandem with the findings of

Aysan et al. (

2019),

Su et al. (

2020) and

Al Mamun et al. (

2020). Investors should keep in mind that Litecoin does not constitute one of the optimal financial choices during the Russian-Ukrainian war. Moreover, it is of primary importance that the nexus of Bitcoin with Ripple or Ethereum makes it function as a safe haven or a top gainer when adopted in pairs with them. Overall, it can be argued that investing in agricultural commodities is the best investment decision that could be made when separate categories of investments are considered. This is valid as this category of financial assets presents the Efficient Frontier with the highest absolute returns, the lowest volatility, and the highest risk-adjusted performance at all levels of risk-aversion. Investors in agricultural commodities should also be aware that sugar and soybeans form the optimal investment tools if conservative investors are under scrutiny while wheat and corn are preferable if they are risk-seekers.

The second best-performing set of portfolios is that employing national currencies as its constituents. Beyond doubt, the Japanese yen is revealed to be the most important currency for profit maximization and the Turkish lira follows but only at low-risk and modest-risk levels. Notably, the currencies of advanced economies play a more minor role than expected and this could be attributed to their stability while the Russian ruble is too volatile to be considered as an optimal investment.

Among the Efficient Frontiers investigated, it is the one that is constructed of cryptocurrency investments that proves to be the worst performing. This strengthens the belief that, despite over 9000 cryptocurrencies being in circulation, it is the highest-capitalized Bitcoin that still has the leading role. The poor performance of Bitcoin during the Russian-Ukrainian conflict brings to the forefront the similarities that have intensified between modern forms of liquid investments and traditional financial assets even during crises when risk appetite becomes more intense and new tools for escaping bear markets are considered.

Apart from estimations concerning national currencies, precious metals and fuel, agricultural commodities and cryptocurrencies separately, optimal portfolios combining all these assets categories have been constructed. The Efficient Frontier of these portfolios is illustrated in

Figure 5 and the outcomes are displayed in

Table 6,

Table 7 and

Table 8.

Estimations concerning portfolios containing all the types of financial assets considered in this study indicate that the Japanese yen and natural gas should be the main constituents of the optimal portfolios for the majority of the risk-aversion levels under scrutiny. To be more precise, the Minimum Variance Portfolio is the only optimal portfolio that consists of a large array of assets: Russian ruble (0.5%), Euro (2.23%), Great Britain pound (1.16%), Swiss franc (3.21%), Turkish lira (18.56%), Chinese yuan (15.77%), Japanese yen (34.11%), Canadian dollar (9.18%), Australian dollar (4.2%), gold (0.01%), copper (4.79%), natural gas (1.06%), coffee (2.96%), corn (0.03%), soybeans (0.3%), wheat (0.33%), Bitcoin (1.6%). On the other hand, the riskiest portfolio considered reveals that risk-lovers should only invest in natural gas. It is noticeable that the MVP presents returns equal to 0.131% and standard deviation equal to 0.00274 while the riskiest portfolio generates profits almost eight times as high (equal to 1.016%) and risk approximately fifteen times as high (equal to 0.04219). Thereby, the riskier the optimal portfolio with all assets examined, the poorer its risk-adjusted performance.

It should also be underlined that the Minimum Variance Portfolio in this case is found to be the safest (indicated by the lowest standard deviation) among all the cases of MVPs investigated. Therefore, the combination of all types of assets permits the decrease in the risk suffered by risk-averters. Notably, the expected return generated by this Minimum Variance Portfolio is higher than the others and this highlights the need of risk-averters to diversify their portfolios by including as many types of assets as possible.

When it comes to examination of the riskiest portfolios, emphasis should be given to the same synthesis of the riskiest optimal portfolio in the case when only precious metals and fuels are under scrutiny, as well as when all types of assets are examined. Only natural gas as the appropriate investment asset is found in both cases. Evidence reveals that this outperforms the riskiest portfolios only of national currencies, agricultural commodities or cryptocurrencies. This outcome does not abide by the findings of the vast majority of earlier academic work that do not assign great importance to natural gas for the purposes of profit-making.

It is noteworthy that gold is not considered to be the only safe haven when a range of assets is examined. This is partly in accordance with the findings of

Będowska-Sójka et al. (

2022). National currencies such as the Turkish lira and the Japanese yen are revealed to be able to hedge risk by other assets in a more efficient way than gold during the Russian-Ukrainian conflict. Moreover, natural gas is found to have taken the lead from cryptocurrencies in generating profits in geopolitically turbulent eras and this is the reason why risk lovers should prefer this fuel for ameliorating their portfolios’ performance.

5. Conclusions

Studying the optimal allocation of investment portfolios with alternative asset categories and different levels of risk appetite during major geopolitical crises is of the utmost importance for shedding light on geopolitical impacts on financial markets. Moreover, providing a spectrum of efficient frontiers for alternative investment mentalities results into deeper understanding of the complexity of financial decisions in the effort to ameliorate the risk-return trade-off during periods of great instabilities. This paper builds on and contributes to both these strands of research and provides fruitful findings for interested investors. The latter acquire a clearer picture and a bird’s-eye view as a perspective on satisfactory risk-adjusted performance that major war tensions can bring about at a worldwide level.

This paper places under scrutiny twenty two conventional and four modern financial assets of major importance in terms of market capitalization and popularity during the period of the newly spurred Russian-Ukrainian conflict. The period covered spans from the Russian invasion of Ukraine (24 February 2022) until the conquest of Mariupol (17 May 2022). This period of extremely elevated geopolitical risk with worldwide monetary, financial, political and geopolitical consequences is examined, as it is considered to be a benchmark for the evolution of a series of risky geopolitical events.

Estimations based on Sharpe’s optimization procedures and the construction of efficient frontiers for alternative levels of risk appetite and different sectors of constituents reveal that gold (and to a lower extent copper) as well as the Chinese yuan, corn and soybeans prove to be safe haven instruments. Remarkably, Bitcoin also constitutes a safe haven. Moreover, it should be underlined that natural gas, the Japanese yen, wheat and the combination of Bitcoin and Ethereum are found to be generators of profits in optimal portfolios. In addition, investing in agricultural commodities is estimated to form the best investment choice, whereas it is shocking to note that the cryptocurrency portfolio is the worst among the portfolios examined. It should be emphasized that from an overall perspective- large levels of risk appetite fail to result in significantly higher portfolios returns than levels of high or modest risk aversion. This corroborates the concept that only a few drivers of profitability could be considered as top gainers and that portfolio returns would be disappointing without their existence.

This study contributes to the view that better understanding of certain investments among a large array of conventional and modern financial assets could be efficiently employed in order to counterbalance the detrimental impacts that the Russian-Ukrainian war has had concerning investors’ returns. The financial depiction of newly aroused tensions between Russia and Ukraine has been under investigation by significant academic research up to the present. To the best of our knowledge, this is the first paper that undertakes the strenuous task of placing under scrutiny the optimal decision-making of investors during this benchmark period that could be the trigger for perpetual geopolitical uncertainty. Interested investors should be aware that gold exhibits safe haven abilities during periods of high geopolitical risk. Moreover, agricultural commodities are found to be the strongest generator of profits due to the powers of limited supply that appear when agricultural-oriented and export-led economies make war. In the same vein, forms of energy prove to be wealth-generators when these countries are also major suppliers of energy. Apart from that, major national currencies of advanced countries in developing regions not involved in the war are found to be profitable investments. Moreover, risky investments such as cryptocurrencies fade as attractive investment tools during geopolitical crisis. with economic and financial consequences such as motives for survival by ensuring agricultural products and heating overcome speculation initiatives.

When all types of assets are considered for formulating the optimal portfolio, investing in a large array of different types of assets is found to be beneficial for risk-averters. National currencies such as the Turkish lira and the Japanese yen are revealed to be capable of acting as safe havens by taking over the role of gold. As concerns risk lovers, they should allocate all their resources to natural gas as this is the main profit-generator during periods of elevated geopolitical risk.

This paper provides a compass for optimal asset allocation and adjustment of investors’ portfolios when geopolitical risk is so high that conventional beliefs about appropriate hedging instruments and risk-loving favorites fail to be verified. Potential avenues for further research in this field of study should include the thorough investigation of spillover impacts on returns and volatility in financial markets by advanced methodologies and how this is influential on investors’ wealth. Moreover, methods of minimizing the negative impacts of geopolitical risk on optimal asset allocation should be further elaborated by sophisticated asset weighting specifications. Interdependencies between geopolitical risk and financial markets could be examined by adopting advanced methodologies such as the Ensemble Empirical Mode Decomposition (EEMD)-Based Transfer Entropy Analysis (

Agyei et al. 2022), the Improved Ensemble Empirical Mode Decomposition with Adaptive Noise (ICEEMDAN)-Induced Transfer Entropy Analysis (

Bossman 2021;

Bossman et al. 2022), quantile-on-quantile regressions (

Umar et al. 2022a), the TVP-VAR methodology as in

Balcilar et al. (

2021) and wavelet coherence analysis (

Będowska-Sójka et al. 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}