From White Collar to Influencer Marketing? How Banks Can Reach Young Customers

Faculty of Management, Seeburg Castle University, 5201 Seekirchen, Austria

*

Author to whom correspondence should be addressed.

Int. J. Financial Stud. 2022, 10(3), 79; https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10030079

Submission received: 5 August 2022

/

Revised: 30 August 2022

/

Accepted: 5 September 2022

/

Published: 9 September 2022

Abstract

:Banks distribute intangible services, so that traditional marketing instruments are often limited concerning their effectiveness to reach new clients, especially teenagers and young adults. With respect to this relevant practical problem, we used survey data for the relevant group (n = 302) in Austria to investigate whether influencer marketing could be a banking strategy to reach the young generation. Due to the particular complexity of a financial product, we assume that the credibility and trustworthiness of an influencer can lead to respondents being more willing to engage with financial products. Based on our survey results, we can provide first evidence that influencer marketing also has untapped potential for banks. Although our respondents revealed a certain skepticism towards this form of marketing, the results indicate a weak positive correlation between influencer marketing, customer engagement with the subject of financial products and ultimately the purchase of financial products. In this respect, our results are of particular interest to decision-makers in banks. However, they are also relevant for the whole of society. If influencer marketing works for financial products, then other topics that are particularly sensitive, e.g., health care, could be addressed accordingly.

1. Introduction

The media landscape has changed significantly in recent years and is currently undergoing a major transformation in the age of digitization (Kozinets et al. 2010). Since 2005 at the latest, influencers, bloggers, vloggers, YouTubers or Instafamous have occupied an increasingly prominent position in public communication (Ye et al. 2021). The protagonists have a considerable influence on forming the opinion of broad sections of the population. Young people in particular are consuming information less and less via traditional media, but are increasingly substituting them with social media channels (e.g., Gottfried and Shearer 2016; Lou and Yuan 2019). Freberg et al. (2011, p. 90) defines social media influencers as “a new type of independent third-party endorser who shape audience attitudes through blogs, tweets, and the use of other social media.” Unsurprisingly, this development is also influencing corporate marketing (Ye et al. 2021), so more attention is paid to influencer marketing in the academic literature. Haenlein et al. (2020) emphasize the economic importance of influencer marketing and calculated the value of the industry to be worth $10 Billion in 2020.

With this paper, we aim to provide initial evidence for a Western European country to reduce the gap that exists in bank marketing literature and practice to date. Overall, we aim to examine two central research questions:

- What impact does influencer marketing have on customers regarding their purchase decision process of financial products?

- To what extent can influencer marketing determine the customer’s engagement with financial products?

On the one hand, our results are important for researchers in the field of bank marketing, as well as for sales experts and decision-makers in banks. On the other hand, our findings may also be relevant for firms in related industries, such as the insurance industry and the healthcare sector.

The remainder of the paper is structured as follows: Section 2 serves as a theoretical framework to derive our hypotheses and to present the relevant characteristics of the relationship between influencer marketing and financial products. Section 3 presents our empirical results. These are then discussed and practical implications are derived in Section 4. Finally, Section 5 summarizes our results.

2. Background, Literature and Hypotheses

2.1. Banking and Bank Marketing in Austria

Vrontis et al. (2021) show that the most samples studied in the field of influencer marketing are based on US data. They identify only one study from Germany and one from Austria. Our survey focuses on the Austrian banking market, which is considered one of the most competitive banking markets in Europe. In 2019, there were 573 credit institutions in Austria, with 2521 residents per banking office in Austria and 3521 branches. Consolidated total assets across all banks amounted to EUR 1.03 trillion (OeNB 2020; Statista 2020b). Erste Group Bank AG was the largest bank in Austria with total assets of around EUR 245.69 billion in 2019 (Statista 2020a).

With respect to bank marketing, the sector has been characterized in recent years by various changes regarding the use of new advertising channels. For example, Erste Bank and Sparkassen Group (savings banks) has been able to generate a great deal of attention with its new slogan and the #glaubandich (“#believe in yourself”) campaign (Erste Bank Group AG 2020). Beyond this, it can also be seen that Austrian banks have made greater use of social media in recent years. Their social platforms, which are well filled with content, indicate this. However, a gap in the marketing mix compared to other industries also becomes visible (PwC 2018).

However, until today, banks have mainly relied on traditional advertising, whether on TV, radio or in print, to reach their customers and inform them about financial pro-ducts. Thus, influencer marketing is not yet widespread in banks. Due to the focus of our study, we examine the opportunities for banks using influencer marketing in the retail sector, where social media can be used for a broad communication.

At a time when social media users are increasingly focused on sharing, this culture of communication and feedback poses challenges for bank marketing, because traditional strategies do not offer the opportunity for immediate feedback from customers (Grabs et al. 2017).

A study conducted by social media market researchers from BuzzValue in 2017 shows that Austrian banks maintain their customer communication through their social media presence. Active communication on platforms like Facebook and Co shows that major Austrian banks were already very well positioned five years ago, and it has become a fixed component of their marketing mix. The following banks were represented in the top four here: Erste Bank, BAWAG PSK, Unicredit Bank Austria and Raiffeisen Bank. Even then, the study indicated that the group to highlight was the target group of young people, as this is where the highest number of interactions occurred. This is due to young people and students being the main users of social media platforms (BuzzValue 2017).

2.2. Influencer Bank Marketing and Its Opportunities

A recent literature review by Ye et al. (2021), which dates the first article on influencer marketing back to 2003, shows that scientific research recognized its potential already at an early stage. Another systematic review by Vrontis et al. (2021) shows us that we have seen an immense increase in scientific publications in this field between 2015 and 2020, so the topic still seems to be of great interest and various research needs can be identified. In our understanding of influencer marketing, we follow Martínez-López et al. (2020, p. 579) who define it “as the use of influential opinion leaders (influencers), celebrity or non-celebrity, with many followers on social platforms, to foster positive attitudinal and behavioral responses in their followers (consumers) regarding the brand’s interests by using posts shared on such platforms, and which also allows influencers and followers to participate in the co-creation of the brand image on social media”.

Most of the literature concerning influencer marketing deals with fashion, beauty, luxury, travel, games, food, or fitness (Ye et al. 2021). From a theoretical perspective, it is hardly surprising that topics such as “health” or “finance” have received little attention to date, as these are generally sensitive topics that many people tend to avoid.

Financial products are highly complex and require a corresponding basic economic education. In addition, the customer-bank relationship is characterized by a high level of trust which is particularly true for new forms of banking transactions such as electronic or mobile banking (Skvarciany and Jureviciene 2017). However, if we assume with the literature that young people trust in the influencers that they follow online, the question arises of what potential can arise for banks if they integrate influencer marketing for this target group into the marketing mix.

We agree with Taylor (2020) that we do need more research on influencer marketing. Therefore, we would like to explore two sub-areas of the topic:

- The hardly used influencer marketing in banks, and

- the adequacy of classic bank marketing regarding young adults.

Generally, young adults are not very interested in financial products (Koch 2018). Interest in financial products usually arises when there is an actual reason, e.g., buying a car, home furnishings or property (Papon 2019). Thus, the crucial question for banks is how to reach this target group. Literature shows that influencer marketing works very well to get in touch with young customers in other industries (Ye et al. 2021). However, the financial industry has numerous peculiarities that make it difficult to address young adults. Bank services are obviously not physical products (e.g., Waschbusch and Hastenteufel 2020). They are often complexly structured contracts that justify an investment or financing. If customers want to make decisions on their own responsibility, this requires at least some economic and financial education (Serena and Hastenteufel 2022). Moreover, there is an asymmetrical distribution of information between a bank and its customers with regard to the opportunities and risks of a financial product, particularly in the case of investments. On the one hand, this can be reduced by screening on the part of the customer, but this leads to high familiarization costs in the subject matter. On the other hand, banks can send signals that they will not exploit the information advantage to the detriment of the customer. Trust is a bridge here that can persuade the customer to buy a product, even though he does not have the necessary information (Waschbusch et al. 2018). Assuming that especially young adults have little contact with banks, mediators are needed. For example, parents could report positive experiences with the bank, so that trust is acquired secondarily. For us, the question arises whether influencers could also take on such a mediator function.

2.3. Engagement in Financial Products, Information, and Uncertainty

When young people are faced with the decision to engage in banking products, there are several challenges. First of all, due to their young age, they often lack experience and knowledge to understand these products. Dealing with the content leads to high costs, especially in terms of alternative time use. These costs are incurred today. The benefits of dealing with financial products and concluding, for example, a pension plan, are also difficult for the decision-maker to assess. Moreover, decision-makers face uncertainty and also have difficulties in processing information sufficiently, so that they are subject to bounded rationality in this respect (Simon 1955, 1956, see also Oehler and Wendt 2018). A typical problem is, for example, that potential benefits would only be incurred in much later periods, so that we must also consider the well-known decision anomalies shown by psychological research (e.g., Tversky and Kahneman 1974; Kahneman and Tversky 1979) when analyzing the decisions by young people to engage in financial products. In a large number of cases, this decision-making problem can probably lead to the result that people do not engage in financial products. In this sense, influencers could help to provide the necessary information and—at least from the subjective perspective of the young customer—to reduce uncertainty about the benefits.

From a theoretical point of view, we follow Kim and Kim (2021) who explain influencer marketing by the social exchange theory proposed by (Thibaut and Kelley 1959; Homans 1961). If human behavior is considered as an exchange relationship, there is reciprocity in the sense of gift and return (Malinowski 1922; Mauss 1966). Thus, if an individual invests resources—e.g., money, time, or reputation—in a relationship, the transaction partner will direct his or her behavior in such a way that a corresponding counter-gift is made (Kim and Kim 2021). In the case of influencer marketing, the influencer provides new information about a company, a product or a service. To maintain reciprocity, followers like or recommend the influencer and/or the product.

Thus, the basis for H1 is the fact that more and more followers are turning to influencers for information. Information acquisition is also part of the purchase decision process (Kotler et al. 2007). The purpose of this hypothesis is to prove the connection between information acquisition from influencers, and the consequence that followers subsequently engage more with financial products.

Hypotheses 1 (H1).

There is a correlation between influencer information acquisition and engagement with an advertised financial product.

Following McCracken (1986) we assume that famous people can bring about positive associations with products. The persuasiveness of an influencer depends fundamentally on his or her personality and character traits as well as his or her image (Lou and Yuan 2019). The ideal image of an influencer includes characteristics such as trustworthiness, authenticity, credibility, and charisma (Deges 2018; Jin et al. 2019; Chopra et al. 2021). Followers engage with the recommendations made, trust the judgment, and are thus impressionable (Bakker 2018). Both for influencer marketing in general and due to the importance of the topic for a person’s entire life, the characteristics, credibility and trustworthiness are of outstanding importance (e.g., Jin et al. 2019; Kim and Kim 2021).

While credibility means a “communicator’s positive characteristics that affect the receiver’s acceptance of a message” (Ohanian 1990, p. 41), the term “trustworthiness” means how reliable, honest and dependable the influencer is perceived by the receivers of the information (Ohanian 1990; Jin et al. 2019).

Therefore, we understand credibility as the basis for trustworthiness, but only when both are present. Followers believe and trust the influencers and rely on their judgments and recommendations (Helm 2013). Based on the crucial importance of credibility and trustworthiness for the effectiveness of influencer marketing pointed out by previous studies (e.g., Merz 2019; Lou and Yuan 2019; Kim and Kim 2021), we derive the following hypotheses:

Hypotheses 2 (H2).

The more credible an influencer is, the easier it is to influence people in terms of buying behavior.

Due to the complexity of financial products, it is said to be a credence good (Nelson 1970; Darby and Karni 1973; Ford et al. 1990), as customers cannot observe the quality due to lack of information (e.g., Oehler and Wendt 2018). This results in a particularly strong information asymmetry between the bank as producer of the financial service and the customer on the demand side. Due to the required financial education (Serena and Hastenteufel 2022), an examination of the quality of, for example, an investment fund from a customer’s point of view is hardly possible, or only possible with very high training costs (e.g., Jost 2011).

Nevertheless, to conclude a contract, the agency problem must be at least partially overcome by signals. This requires a high degree of trust from the customer. Young people in particular only have little experience with banking services, therefore mediators are needed. Based on the literature focusing on other industries (e.g., Lee 2021), we assume that influencers can fulfill this function if they themselves have the corresponding characteristics, or are perceived by respondents to be particularly credible. If we further assume with H2 that credibility has an impact on a consumer’s buying behavior, we can conclude that influencers who are perceived as particularly credible by their followers and who promote financial products, can transfer this perception to the financial products they promote (e.g., Lou and Yuan 2019). Therefore, H3 is:

Hypotheses 3 (H3).

Influencer perceived credibility and people’s intentions to buy the financial products advertised are related.

From a rational choice perspective, a youth or a young adult will decide to engage in financial products if the expected benefits exceed the costs incurred. Both are generally uncertain; the costs are primarily training costs and the opportunity costs of spending time elsewhere (e.g., Becker 1965). Due to the low level of knowledge and incomplete information, it is often difficult to estimate the benefits for the relevant target group, especially because possible benefits—for example, in the case of old-age provision—do not occur until well into the future. By promoting a financial product, the influencer can send a signal for the benefit, which provides the decision-maker with additional information. However, it is crucial that the source of information is trustworthy for the adolescent or young adult. We derive our hypothesis 4 from this simple economic consideration.

Hypotheses 4 (H4).

Influencer perceived trustworthy and people’s intentions to engage with advertised financial products are related.

Furthermore, we want to explore an effect relationship between the higher trustworthiness of the influencer compared to traditional advertising and the purchase decision with H5.

Hypotheses 5 (H5).

People who consider influencers more trustworthy than traditional advertising are more likely to buy the financial products advertised.

Finally, we want to clarify whether people who have bought products promoted by influencers and have had a positive experience, will again rely on the recommendation of influencers; and whether people who have not yet bought any products recommended by influencers would rely on the recommendations of influencers or not.

Hypotheses 6 (H6).

In terms of willingness to buy promoted financial products, people who have already bought products advertised by influencers differ from those who have no experience buying advertised products.

3. Empirical Study

3.1. Study Design and Sample

To investigate the topic empirically, we use a one-time standardized online survey (Appendix A). People who are between 18 and 30 years old and have an Instagram account form the population for the survey. This age cohort was specifically defined because people are legally considered to be at least 18 years old, and have mostly started studying or are working their first jobs. Additionally, this age cohort has had first contacts with financial products and now has to make decisions independently. The age restriction was 30 years, as the majority at this age have already completed their studies and/or have already gained their first professional experience, so it can be assumed that they will take care of financial matters independently in the years to come. Another reason for this age group definition is that the main target group of influencers is also in this age range.

The first block of questions from the main section contains eleven questions and is dedicated to influencer marketing. We want to examine how much the subjects are engaged with influencer marketing and how much they trust the recommendations of influencers. Certain statements dedicated to the role model function, trust function or general functions of influencers are to be rated from “fully agree” to “strongly disagree”. In addition to using a 5-point Likert scale, there are also yes/no questions, such as whether a product has ever been purchased because of influencer marketing. Furthermore, there are questions with multiple answers to be chosen, such as in which subject areas they follow influencers.

The second block of eleven questions focusses on the behavior and engagement with financial products and the financial behavior of the subjects. In addition to the questions regarding the engagement and interest in financial products, this part attempts to determine whether influencer marketing should be used to market financial products, and which financial products specifically might be relevant in this context. This block of questions again contains single as well as multiple choice questions and statements that are to be evaluated with a 5-point Likert scale ranging from “completely agree” to “completely disagree”.

The last part of the questionnaire is dedicated to socio-demographic data. Additionally, gender, age and the highest school-leaving qualification were collected. To ensure that the final questionnaire reached the desired target group, the link to the survey was distributed via Instagram, Facebook, LinkedIn, and also via WhatsApp. This helped us to create a snowball effect.

The survey period was set from 4 August 2020 to 15 August 2020 and at the end of this period a final sample of 302 participants was collected. Regarding our final sample, we can note that especially people between the age of 24–28 participated in the survey and therefore they represent the biggest age group with 179 participants, which accounts for 59.3% of respondents. This is followed by the group of 20–23-year-olds with 71 people (=23.6%), for the 29 and 30-year-olds there are 38 participants (=12.6%). The last group are the 18–19-year-olds, with only 14 participants (=4.7%). The average age of the participants is 24.98 years.

The level of education of the respondents can be classified as high. The high percentage of high school graduates (n = 98) and college graduates (n = 183) can be attributed to the age of the participants. The percentage of respondents who have an apprenticeship degree is only 3.3%. Moreover, only 2.6% of the people questioned have a compulsory education degree. The smallest group in the sample is made up of the three respondents who stated that they had another degree.

3.2. Findings

3.2.1. Descriptive Statistics

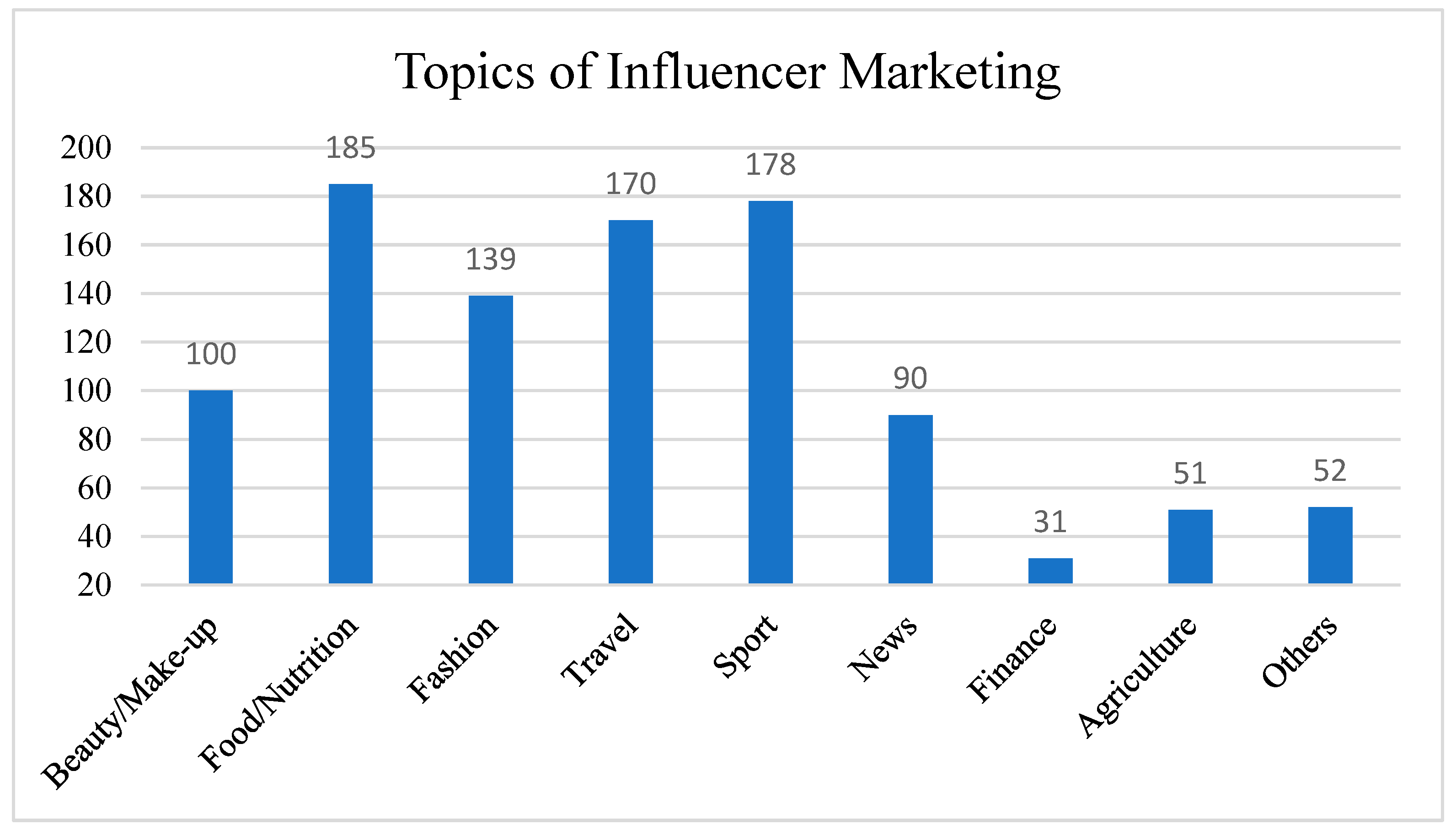

At the beginning of the survey, a question was used to find out in which area the subjects follow influencers or also consider them useful. With the help of the function “Define variable sets for multiple answers”, it was examined which subject areas were most frequently indicated. The first places are as visible in Figure 1: food/nutrition in first place with 185 answers, followed by sports with 178 and travel with 170 answers and fashion with 139 answers. Surprisingly, despite the high female participation rate, beauty is in 5th place with only 100 responses.

The results are almost identical to the surveys conducted by PwC and Mindshare, with the exception of beauty, as this topic is not among the top three in this survey. As expected, the topic “finance” is in last place with 31 responses, again an indication that influencer marketing is not yet used in this sector. For this reason it does not yet have any significance for followers, and there seems to be potential for this new topic in which influencers can reposition themselves.

On the topics of credibility and trust (questions 3–11), participants were shown specific statements to rate on a 5-point Likert scale from “1 = agree” to “5 = disagree.” The results show that the majority of participants answered “partly agree” when it comes to whether respondents were interested in advertised products (49.7%), believe the judgment of influencers (37.7%), can be convinced to buy the product (39.1%) and in that sense, also see influencers as role models (44.7%). In contrast, there are only 58 participants (19.2%) who see influencers as a person of trust—30.5% of respondents do not trust the influencers at all. Almost 50% of the participants could not decide whether they consider influencers to be credible or not.

The second focus of the survey was on financial products. The first three statements, which were to be rated on a 5-point Likert scale, were an attempt to evaluate the respondents’ insights into their interest in and involvement with financial products. Several studies conducted, including those by Erste Bank and BAWAG, show that financial literacy and knowledge of financial products are weak among young adults (BAWAG Group 2019; Erste Bank der österreichischen Sparkassen 2018). As expected, the interest in financial topics increases on average the older the respondent is. In the smaller group of 18–19 years, no one agreed to be very interested in or concerned with financial products. Table 1 and Table 2 summarize these results.

The higher the school-leaving qualification, the more likely the respondents are to be interested in financial products or to deal with them. Among university graduates, however, there is a tendency for higher interest in, than actual involvement with, financial products. It can therefore be concluded that the interest undoubtedly exists, but that the appropriate form of marketing or information is still insufficient for those people to actually engage with financial products.

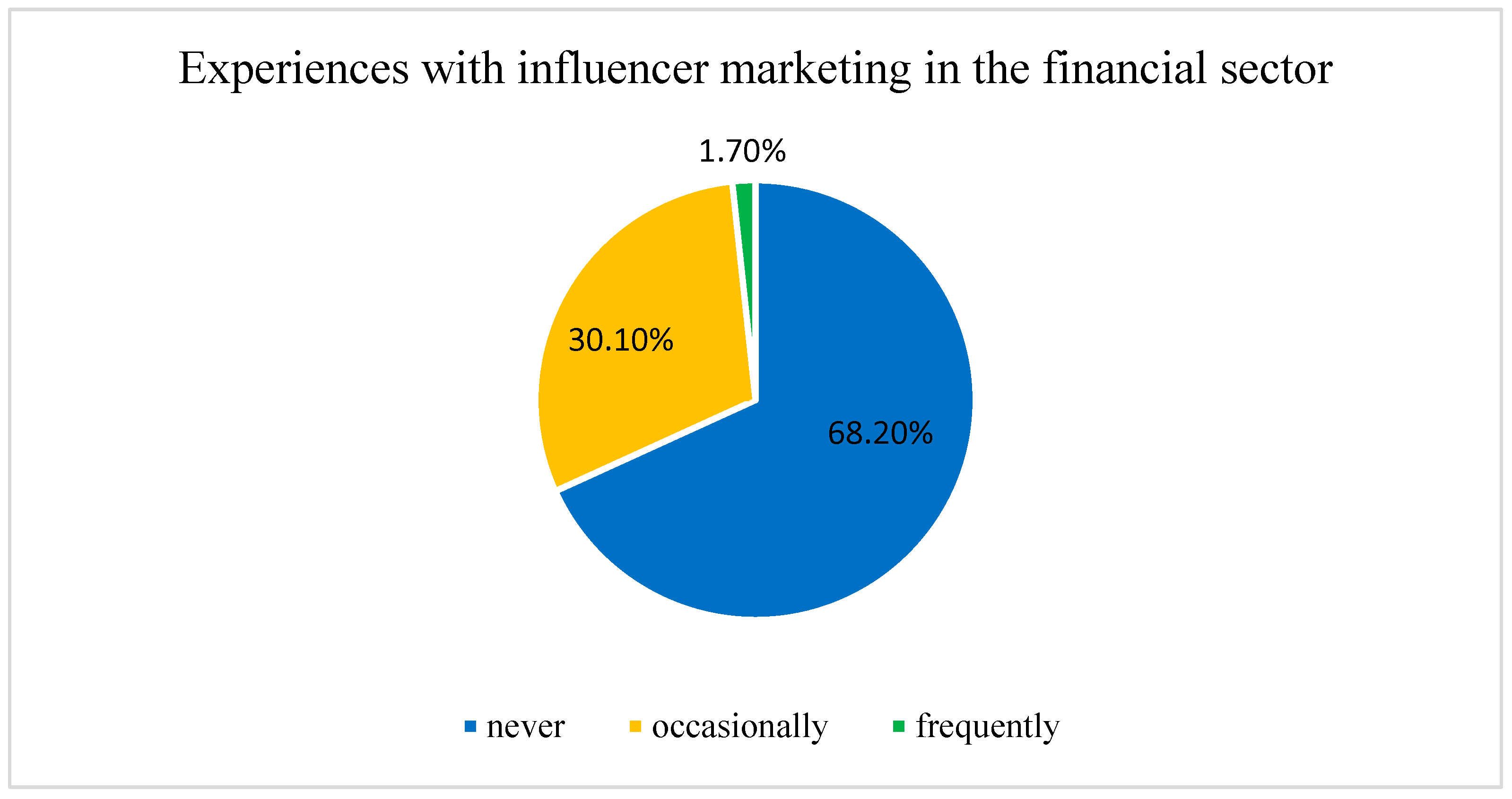

At the beginning of the second part of the survey, participants were asked whether they had already noticed influencer marketing by banks. A clear picture emerged here, confirming that there are no real influencers for the financial sector to date.

Figure 2 illustrates the result, which states that 68.2% of the respondents have not yet recognized influencer marketing in the financial sector, 30.1% did so occasionally, and only 1.7% did frequently. At first glance, it seems inconclusive that almost a third stated that they have occasionally perceived influencer marketing for financial products, although on the part of the literature it was repeatedly mentioned that there is hardly any influencer marketing of Austrian banks. From a theoretical point of view this is true, yet three possible reasons can be given in practice that can explain the 30.1%. First, there have been isolated collaborations between an influencer and a bank in the past, for example the cooperation with Tatjana Kreuzmayr and Erste Bank. Secondly, it is possible that the respondents also understand influencer marketing to mean web blogs and financial blogs, of which there are quite a few that provide information about financial products.

Probably the most important information for our study comes from the question of whether influencers should advertise financial products, and whether there is approval for this on the part of followers.

However, we find that there is currently a clear opinion against influencer marketing as a form of marketing for financial products (70%). Only 30% see a new opportunity in this form of marketing. In a next step, it was analyzed whether there are differences between the age groups. The results show that in almost every age group, more people reject influencer marketing in banks. The outliers here were test subjects aged 18 or 19—here the “yes/no” answers were almost the same or the same. Even if it is clear at first glance that influencer marketing is not desired, the 30% who agreed should not be underestimated—it is still more than a quarter who are in favor of the new form of marketing. Thus, this marketing strategy can be successful. However, the aversive tendency towards influencers is also reflected by 76.5% of the respondents who would not or rather not buy financial products even if they were recommended by influencers.

For further analysis, the subjects were divided into two groups—the division was based on question 4 of the survey: Have you bought products recommended by influencers in the last two years?

- group 1 “yes, already bought at least one product” (n = 198)

- group 2 “no, never bought a product before” (n = 194)

If we compare both groups in terms of their behavior and their attitude toward influencer marketing in banks, a surprising picture emerges. Since 65.5% of the test subjects already have experience with influencer marketing, one could assume that they also approve of influencer marketing for financial products (198, 65.5% of 302). However, the results show that only 32% of group 1, who have experience with the purchase of advertised products through influencers, also consider influencer marketing useful for banks and 68% are against influencer marketing in this area. A similar result can also be seen in group 2, where 72% of the people questioned are against influencer marketing. This is an obvious result, since those people have not yet purchased any products advertised by influencers and therefore have no experience with them. For the second group, the result could be explained by the lack of experience in this respect.

In the following analysis, groups 1 and 2 were also compared with the results of the questions whether they would buy or deal with financial products advertised by influencers. To recall the descriptive results: 3/4 of all respondents stated that they would not/rather not buy financial products, even if they were presented and recommended by influencers. The new result shows a similar picture, with just under 74% of group 1 fully disagreeing with the statements that they would buy financial products advertised by influencers. There is no respondent in either group 1 or group 2 who fully agreed to the statement.

Therefore, we further analyze why some people buy influencer products in general but do not want financial products promoted by influencers. Since the result is very clear, both groups were additionally compared with the results regarding the engagement with financial products. Possibly, the purchase of financial products is too risky, and people therefore tend to engage more with the products before finally buying.

The results confirm the assumptions: People in group 1 are tempted to look more closely at financial products when the financial products are presented by influencers. Four subjects answered, “fully agree”. Overall, as many as 31% agreed and just under 44% of them disagreed. Based on this, it is possible that influencers are considered an important source of information for group 1—however, this assumption cannot be confirmed, as 36.9% of group 1 “strongly disagree”. Even more skeptical are the people of group 2, who have no experience with influencer products so far; here, too, the subjects who do not allow themselves to be enticed by influencers to engage with financial products are in the majority (69.2%).

Thus, it can already be concluded from the descriptive results that for those subjects in group 2, influencer marketing is not the right strategy to get in touch with them to entice them to buy or deal with financial products. For people questioned who are already experienced with advertised products, it is shown that they can be reached with this type of marketing, but for topics which were not covered so far by influencer marketing, it is more a type of incentive for an engagement, but not for a final purchase. Here, however, the question cannot be answered whether the failure to make a purchase is related to the serious topic of financial products, or the reason that influencer marketing has not yet been used for financial products and therefore lacks experience.

3.2.2. Hypotheses Testing

To test our hypotheses, we apply different statistical tests depending on the scale levels. The significance level was assumed to be an error probability of 5%, which means that a result can be considered significant if p (error probability) is less than or equal to 5% (p ≤ 0.05).

Table 3 shows the result with r value of 0.246. The p-value of 0.000 is smaller than the established 0.05 (p < 0.05) and therefore the result is significant. It follows that we can reject H0. Thus, a relationship between influencer information acquisition and engagement with financial products can be confirmed.

To answer H2, the first step was to create a new variable for buying behavior called “Buying behavior NEW”. This new variable is composed of two items from the questionnaire “If the influencer convinces me, I buy the product” and “It happens that I am influenced”. The dependent variable “Buying behavior _NEW” and the independent variable “Credibility”, both of which are again interval scaled and have a metric scale level, are therefore subjected to a Pearson correlation test to show whether there is a correlation and whether the hypothesis is consequently accepted or rejected.

Table 4 shows that we can accept H1, since the two-sided significance has a value of 0.000 and is thus lower than the required 5%. (p < 0.05). Furthermore, there is a positive medium correlation (r = 0.479) between the variables. Consequently, it can be confirmed that the more credible an influencer is, the easier it is for his or her followers to be influenced in their purchasing behavior.

Obviously, our result is significant. Furthermore, there is a moderately weak positive correlation (r = 0.310) between credibility and the consequence of buying a financial product advertised or recommended by influencers (Table 5). Therefore, we reject H0 again and we can accept the hypothesis that the more credible an influencer is, the more likely people are to buy the financial products advertised.

H4 is basically the same as H3, except that in this case we wanted to find out whether people also engage with financial products if they consider an influencer to be trustworthy. As already described in the testing of the third hypothesis, the variable “engagement with advertised financial products” is the dependent variable, which is interval-scaled, and the variable “trusted person”, which is new in this case, is also interval-scaled with a metric scale level.

As with the previous hypothesis, the result is significant (p = 0.000) and there is a weak positive correlation (r = 0.293) between the two variables (Table 6). It follows that H0 can be rejected and H1 is accepted, which states that people are more likely to engage in the advertised financial products if they consider an influencer to be trustworthy.

H5 is also a correlation hypothesis, consisting of the independent variable “influencers more trustworthy than traditional advertising” and the dependent variable “buy advertised financial product”. Both variables are interval-scaled and therefore have a metric scale level, which is why a Pearson correlation test is used.

We can see that the variables are positively correlated (r = 0.261) and the p-value is 0.000 (p < 0.05) and thus (Table 7), significant, which leads to rejecting H0 and confirming H1.

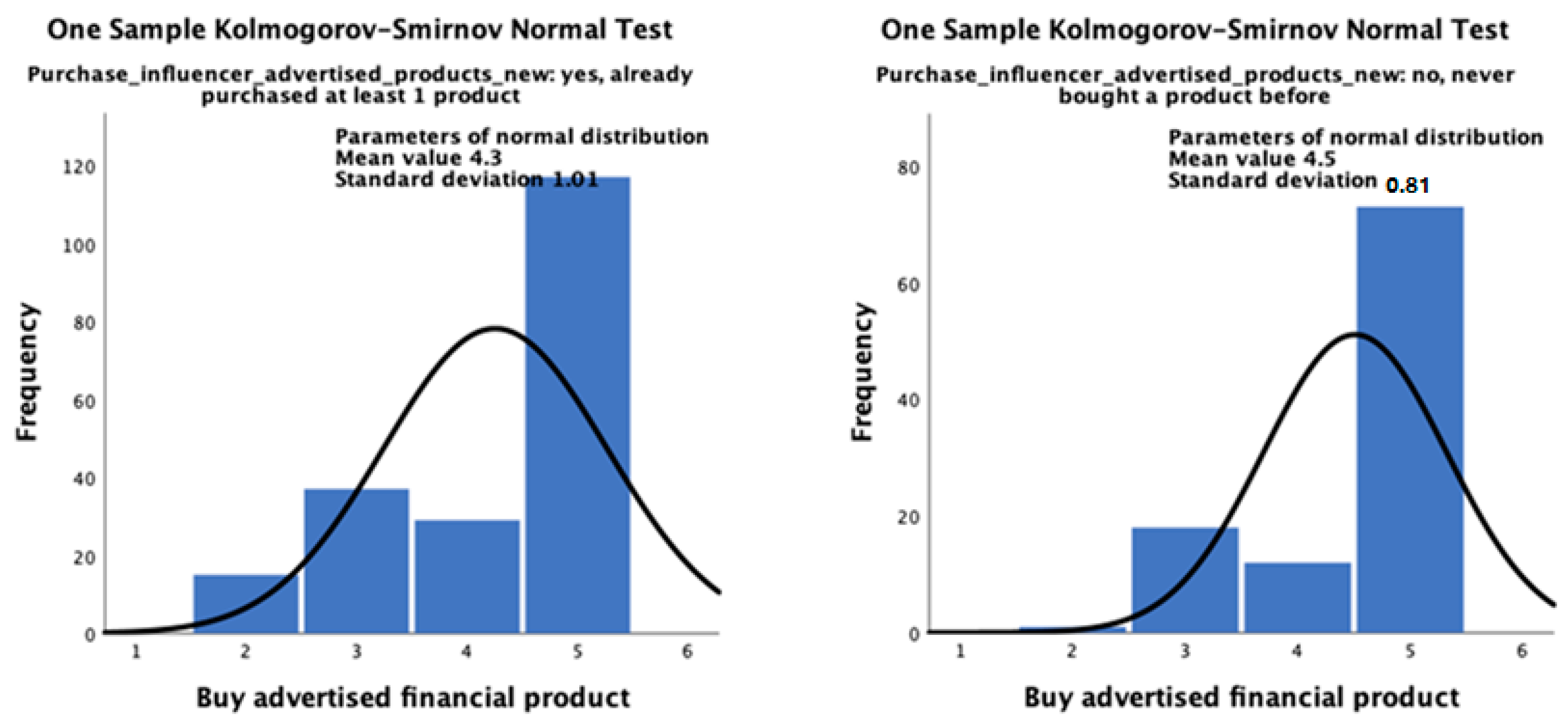

To be able to test H6 which is a difference hypothesis, a new variable “purchase_influencer_reviewed_products_new” was created in the first step to generate two independent samples. The response options “yes, once”; “yes, 2–10 times”; “yes, more than 10 times” were coded into group 1 “yes, already bought at least 1 product” as well as “no, never bought a product” into group 2.

The hypothesis includes the new nominally scaled variable as well as an interval scaled variable “purchase of advertised financial products.” These two scale levels require the t-test. Before this test can be performed, the mean of both independent samples is first tested for the dependent variable “buy advertised financial product”. The results of the Kolmogorov-Smirnov normality test applied to both samples show that there is no normal distribution in either sample (Figure 3).

Since there is no normal distribution, the Mann–Whitney U test is used for indepen-dent samples. The analysis shows that there is a significant difference between the two control groups (already bought a product, not yet bought a product) regarding the willingness to buy an advertised financial product (Table 8). We can see that the asymptotic significance has a value of 0.037, which is less than 0.05. The difference between the two control groups is therefore not significant. The results show that we can confirm H6. That is, people who have already bought influencer-promoted products in the past two years also tend to buy advertised financial products. Exactly the same applies to people who have not yet bought any products—they also tend not to buy any advertised financial products in the future.

4. Discussion

4.1. General Considerations and Practical Implications

The present paper has focused on the opportunity to reach young adults with influencer marketing. The strategy of relying on influencers in a bank’s marketing mix could counteract the problem of declining trust in advertising on the one hand, and the lack of financial knowledge among young adults in Austria, on the other.

We find that influencer marketing for certain financial products should be included in the marketing concept of banks, because the tests of the hypotheses demonstrate a weak positive correlation between influencer marketing, employment, and the purchase of financial products. Thus, the skepticism towards influencer marketing in banks that has existed so far proves to be unfounded. What matters is to introduce influencer marketing so that it is accepted and recognized by potential customers. Even in the consumer goods sector, it was unthinkable to buy products promoted by influencers until a few years ago. The introduction of influencer marketing has led to positive brand and sales effects here.

The testing of our hypotheses revealed that the two essential factors that can also be found in literature. Credibility and trustworthiness play an important role in the decision-making process for a purchase or have a great influence on the behavior of customers. As mentioned in the theoretical section of this paper, people have always relied on the principle of word of mouth and, therefore, on the judgments and recommendations of people they consider credible or trustworthy. This trend does not stop with influencers—on the contrary, influencers continue this trend and are a social virtual contact person to whom many followers attribute the same characteristics as to a real contact person.

The testing of the relevant hypothesis also showed that there is a positive correlation between the credibility of an influencer and the purchase of a product. Due to the high number of respondents who stated that they purchased products when they were advertised by influencer marketing, it can be deduced that influencers—in relation to all products and services—basically have a great influence on the willingness to buy.

For financial products, however, the picture is initially different: More than three quarters of the respondents stated that they would not buy any financial products advertised this way. This is contradicted by the result of the test of the third hypothesis, which can prove an albeit weak connection between credibility and the purchase of advertised financial products. Especially in the phase of information gathering, a phase of the purchase decision process (Kotler et al. 2007), influencers play an important role, as they are used as a source of information. Further confirmation of the impact of influencers is shown by the fact that individuals rely on experience purchases for products promoted by influencers, and would buy such products again. This applies to financial products as well.

After 65.6% of all people questioned already bought products promoted by influencers, one can assume that this trend will continue. Additionally, influencer marketing is increasingly used in the financial sector which can have a positive effect on the purchase of financial products. Although the influence on so-called everyday products is currently much higher than on financial products, the impact of influencers plays a smaller, but not negligible, role in the financial sector.

Although descriptive results at this point again indicate that people primarily rely on the opinion of their family, their friends and experts, a positive correlation between information acquisition from influencers and engagement with advertised financial products (H1) as well as the trustworthiness of influencers (H4) could be demonstrated. According to this, influencers currently have a small influence on active engagement with this topic, although they are not considered the first source of information about financial products. The people questioned primarily focus on their parents, their friends and on experts when acquiring information. However, obtaining information via influencers is also a tool the age cohort surveyed would use. A positive correlation could be demonstrated in this regard. The correlation applies not only to the acquisition of information but also to further involvement with financial products (H1). A positive correlation with information acquisition was also demonstrated with regard to the trustworthiness of influencer (H4). Accordingly, although influencers are not regarded as the first source of information on financial products, they do have a certain influence on active engagement with financial topics.

Although the majority of respondents (approx. 70%) would reject influencer marketing for financial products, they are very likely to be purchased if they have previously been advertised by influencers. This leads to the conclusion that influencer marketing is generally endorsed and has a purchase-attracting effect. It can be assumed that people cannot currently imagine it, because on the one hand financial products are a serious, sometimes risky topic and there is currently no influencer marketing, they therefore do not know what it would be like if there were financial influencers for products in this area. Just a few years ago, it was basically unthinkable to buy products at all due to this new form of marketing.

Furthermore, the results show that the correlation between influencer marketing and engagement with financial products is higher than the correlation between influencer marketing and the purchase decision. Since engagement and information gathering is a preliminary stage of the purchase decision, it can be assumed that customers do gather information via influencers, but want to have the final purchase decision secured by a consultation at the bank. From this, we conclude that the increasing acceptance of influencer marketing in general can also be used for the promotion of financial products. This is reflected in the fact that more than a quarter of the respondents have a positive attitude toward influencer marketing for financial products. Since banks have so far relied on traditional marketing tools such as advertising with testimonials, and it has been proven that trust in advertising is declining, banks should follow the trend and rely on influencer marketing.

An important argument for the use of influencer marketing is that due to the low emotional impact, financial products fundamentally require explanation. So far, however, banks have hardly used the opportunities that could arise from this—e.g., short explanatory videos by young employees in collaboration with well-known influencers.

Following our survey results, it could be a new strategy for banks to use influencer marketing in a small way and initially only for certain areas. They could also be used to market the classic financial products such as current and credit accounts, which were the most frequently mentioned products by the people questioned. However, it must be noted that one should proceed very cautiously and gradually here, since generally skepticism is still present with the topic. The finding is that individuals need to get used to that new form of marketing to embrace it, as it is completely new to rely on the opinions and judgments of influencers in a financial topic area.

With respect to the evidence from other industries and our own findings regarding the impact of influencers on consumer decisions, our study indicated that the relevant target group of young adults as bank customers can also be positively influenced by financial influencers. This does not automatically mean that they finally buy the products from the corresponding bank. Rather, it is probably sufficient that influencers act as mediators to highlight the importance of financial services, financing, pension planning etc., so that consumers initially engage with these services.

4.2. Limitations and Future Research

As with any empirical study, the results presented here include some limitations. When interpreting our results to derive implications for bank’s individual marketing strategy, it is essential to consider that our sample is obviously not representative for the population of all Instagram users between the ages of 18–30. It is also neither representative for Austria, and certainly not for other countries. We are aware of this, but still see added value in the study as a first indication that it can be an opportunity for banks to build up influencer marketing, at least that is what our respondents signal. Therefore, further research should attempt to collect representative data for larger regions (e.g., Western Europe) or analyze influencer marketing in the banking sector by cross-cultural studies so that evidence-based recommendations for action can be derived for the financial sector. However, it must also be kept in mind here that the decision is a business policy decision that affects the future. Therefore, even statistically representative but past-related data can only serve as a limited indicator.

Another limitation is the selection of participants; it would certainly have been interesting to expand the target group. For future research it could therefore be an interesting task to include those people who do not have an Instagram account. Our results show that many of the respondents in the age range do not have an Instagram account and were therefore not be included in our final sample.

Furthermore, it is important to emphasize that the survey period was at a time when the world was still in the early stages of the COVID-19 pandemic. Government measures to control the incidence of infection restricted face-to-face contact in many countries and therefore, had an impact on the economy and the way people interacted (e.g., Cosma et al. 2021). It is possible that this also influenced the use of social media in general. For example, adolescents may have spent more time on these platforms due to lack of alternatives during the COVID-19 pandemic. It is therefore conceivable that the development was even accelerated by the pandemic (e.g., Batool et al. 2021). Finally, our results are purely correlational, which limits the significance. Future research should undertake more extensive statistical investigations.

The significance and relevance of influencer marketing will become increasingly important in all areas and industries in the future. Consequently, the influence on behavior will increase, especially in the purchase decision process of young adults, because these generations are digital natives and are used to following influencers.

Therefore, it seems to be important that banks start to include influencer marketing in their marketing and communication concept. First and foremost, it is important to find the right influencer who can identify with the financial topic. The influencer must appear credible and authentic to reach customers and encourage them to engage with financial products.

We can identify a huge potential for further research within this field. In a further step, the pricing policy of the marketing mix, which was not examined in this research, should also be analyzed—here, the question arises whether an increased willingness to pay, which generally increases due to influencers, also applies to financial products. In this respect, it might be interesting to find out how high the willingness to pay is to buy certain financial products and, thus, to obtain an emotional status—conveyed by influencers. The first steps in this direction have already been taken with credit cards, but without influencer marketing. Black credit cards or platinum cards promise additional benefits that indirectly ascribe a certain status and sense of power. Here, a clear possibility and possibly even necessity of charging for a financial product with emotional value can be established. How will this change if influencers specifically recommend those products to young adults? Will young adults follow the recommendations and be less sensitive to price changes? Would this customer group also possibly buy overpriced financial products, just as they already buy overpriced consumer goods, only to be able to say they are just as well financially positioned and secured as their favorite influencers?

5. Conclusions

This study developed initial findings on the potential of influencer marketing for the banking industry. At a first glance, it may seem irritating when banks resort to influencers. However, we are investigating the topic for a customer target group between the ages of 18 and 30, who, on the one hand, show high potential for the next periods, but on the other hand, often do not have a particularly high interest in financial products. In this respect, influencers can possibly take on a mediating function. The results presented in this paper could also be relevant for similar industries, which also do not cover the typical influencer products. Thus, the findings have shown that influencer marketing has an impact, even if it does not seem so at first glance. The results of this study provide important insights, especially for insurance companies and fintechs. The different types of insurance products such as life, health, and accident insurance have, according to the underlying study, a high value among 18 to 30-year-olds. This is evident from the fact that the subjects would like to see influencer marketing for precisely these products.

Although our findings can potentially help to reduce the underlying research gap within the banking industry, it should be clear that the sample is not representative. Therefore, our study can only be understood as a first step in the field of bank influencer marketing.

Author Contributions

Conceptualization, N.W. and M.R.; methodology, N.W.; software, N.W.; validation, M.R.; investigation, N.W.; resources, N.W., M.R.; data curation, N.W.; writing—original draft preparation, N.W., F.F.; writing—review and editing, F.F.; visualization, N.W., F.F.; supervision, M.R., F.F.; project administration, F.F. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Available on request.

Acknowledgments

We would like to thank two anonymous reviewers for constructive and valuable feedback that helped us to improve the paper. Additionally, we are grateful to Jesscia Hastenteufel for her helpful comments.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

References

- Bakker, Diederich. 2018. Conceptualising Influencer Marketing. Journal of Emerging Trends in Marketing and Management 1: 79–87. [Google Scholar]

- Batool, Maryam, Huma Ghulam, Muhammad A. Hayat, Muhammad Z. Naeem, Abdullah Ejaz, Zulfiqar A. Imran, Cristi Spulbar, Ramona Birau, and Tiberiu H. Gorun. 2021. How COVID-19 Has Shaken the Sharing Economy? An analysis using Google trends data. Economic Research-Ekonomska Istraživanja 34: 2374–86. [Google Scholar] [CrossRef]

- BAWAG Group. 2019. Umfrage zu Wirtschaftswissen: 83% der jungen Erwachsenen fühlen sich in Geldfragen nicht Sattelfest. Available online: https://www.bawagpsk.com/BAWAGPSK/Ueber_uns/Presse/517298/umfrage-junge-erwachsene-geldfragen.html (accessed on 4 July 2020).

- Becker, Gary S. 1965. A Theory of the Allocation of Time. The Economic Journal 75: 493–517. [Google Scholar] [CrossRef]

- BuzzValue. 2017. Österreichs Banken im Social Media Check. Available online: https://www.buzzvalue.at/single-post/2017/11/28/österreichs-banken-im-social-media-check (accessed on 12 July 2020).

- Chopra, A., V. Avhad, and S. Jaju. 2021. Influencer Marketing: An Exploratory Study to Identify Ante-cedents of Consumer Behavior of Millennial. Business Perspectives and Research 9: 77–91. [Google Scholar] [CrossRef]

- Cosma, Alina, Jan Pavelka, and Petr Badura. 2021. Leisure Time Use and Adolescent Mental Well-Being: Insights from the COVID-19 Czech Spring Lockdown. International Journal of Environmental Research and Public Health 18: 12812. [Google Scholar] [CrossRef]

- Darby, Michael R., and Edi Karni. 1973. Free Competition and the Optimal Amount of Fraud. The Journal of Law and Economics 67: 67–88. [Google Scholar] [CrossRef]

- Deges, Frank. 2018. Quick Guide. Influencer Marketing. Wie Sie durch Multiplikatoren mehr Reich-weite und Umsatz erzielen. Wiesbaden: Springer Gabler. [Google Scholar]

- Erste Bank der österreichischen Sparkassen. 2018. Studienpräsentation: Das Sparverhalten der ÖsterreicherInnen. Available online: https://docplayer.org/113523414-Das-sparverhalten-der-oesterreicherinnen-2018.html (accessed on 30 July 2020).

- Erste Bank Group AG. 2020. Jahresfinanzbericht 2019. Available online: https://www.erstegroup.com/de/investoren/berichte/finanzberichte (accessed on 11 March 2021).

- Ford, Gary T., Darlene B. Smith, and John L. Swasy. 1990. Consumer Skepticism of Advertising Claims: Testing Hypotheses from Economics of Information. Journal of Consumer Research 16: 433–41. [Google Scholar] [CrossRef]

- Freberg, Karen, Kristin Graham, Karen McGaughey, and Laura A. Freberg. 2011. Who Are the Social Media Influencers? A Study of Public Perceptions of Personality. Public Relations Review 37: 90–92. [Google Scholar] [CrossRef]

- Gottfried, Jeffrey, and Elisa Shearer. 2016. News Use across Social Media Platforms 2016. Pew Research Center. May 26. Available online: http://www.journalism.org/2016/05/26/news-use-across-social-media-platforms-2016/ (accessed on 30 July 2020).

- Grabs, Anne, Karim-P. Bannour, and Elisabeth Vogl. 2017. Follow Me! Erfolgreiches Social Media Marketing Mit Facebook. Bonn: Twitter und Co. Reihnwerk Verlag. [Google Scholar]

- Haenlein, Michael, Ertan Anadol, Tyler Farnsworth, Harry Hugo, Jess Hunichen, and Diana Weltey. 2020. Navigating the New Era of Influencer Marketing: How to be Successful on Instagram, TikTok, & Co. California Management Review 63: 5–25. [Google Scholar]

- Helm, Sabrina. 2013. Kundenbindung und Kundenempfehlungen. In Handbuch Kundenbindungsmanagement. Edited by Manfred Bruhn and Christian Homburg. Wiesbaden: Springer Gabler, pp. 135–54. [Google Scholar]

- Homans, George C. 1961. Social Behavior: Its Elementary Forms. New York: Harcourt, Brace and World. [Google Scholar]

- Jin, S. Venus, Aziz Muqaddam, and Ehri Ryu. 2019. Instafamous and social media influencer marketing. Marketing Intelligence and Planning 37: 567–79. [Google Scholar] [CrossRef]

- Jost, Peter-J. 2011. The Economics of Organization and Coordination. Cheltenham and Northampton: Edward Elgar. [Google Scholar]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect Theory: An Analysis of Decision under Risk. Econometrica 47: 263–91. [Google Scholar] [CrossRef]

- Kim, Do Youn, and Hye-Young Kim. 2021. Trust me, trust me not: A nuanced view of influencer marketing on social media. Journal of Business Research 134: 223–32. [Google Scholar] [CrossRef]

- Koch, Robert. 2018. Sparstudie: ÖsterreicherInnen stecken Geld in Konsum statt in Altersvorsorge. Available online: https://socialcommunitybanking.wordpress.com/2018/10/31/sparstudie-oesterreicherinnen-stecken-geld-in-konsum-statt-in-altersvorsorge/ (accessed on 4 July 2020).

- Kotler, Philip, Kevin L. Keller, and Friedhelm Bliemel. 2007. Marketing Management. München: Pearson. [Google Scholar]

- Kozinets, Robert V., Kristine De Valck, Andrea C. Wojnicki, and Sarah J. S. Wilner. 2010. Networked narratives: Understanding word-of-mouth marketing in online communities. Journal of Marketing 74: 71–89. [Google Scholar] [CrossRef]

- Lee, Jin K. 2021. The effects of team identification on consumer purchase intention in sports influencer marketing: The mediation effect of ad content value moderated by sports influencer credibility. Cogent Business and Management 8: 1957073. [Google Scholar] [CrossRef]

- Lou, Chen, and Shupei Yuan. 2019. Influencer Marketing: How Message Value and Credibility Affect Consumer Trust of Branded Content on Social Media. Journal of Interactive Advertising 19: 58–73. [Google Scholar] [CrossRef]

- Malinowski, Bronislaw. 1922. Argonauts of the Western Pacific. New York: Holt, Reinhart and Winston. [Google Scholar]

- Martínez-López, Francisco J., Rafael Anaya-Sánchez, Marisel Fernández Giordano, and David Lopez-Lopez. 2020. Behind influencer marketing: Key marketing decisions and their effects on followers’ responses. Journal of Marketing Management 36: 579–607. [Google Scholar] [CrossRef]

- Mauss, Marcel. 1966. The Gift. London: Cohen and West Ltd. [Google Scholar]

- McCracken, Grant. 1986. Culture and consumption: A theoretical account of the structure and movement of the cultural meaning of consumer goods. Journal of Consumer Research 13: 71–84. [Google Scholar] [CrossRef]

- Merz, Julia. 2019. From Trusted Friend to Trusted Brand? Influencer Marketing Between Trust and Mistrust. In Media Trust in a Digital World. Edited by Thomas Osburg and Stephanie Heinecke. Cham: Springer. [Google Scholar] [CrossRef]

- Nelson, Philipp. 1970. Information and Consumer Behavior. The Journal of Political Economy 78: 311–29. [Google Scholar] [CrossRef]

- Oehler, Andreas, and Stefan Wendt. 2018. Trust and Financial Services: The Impact of Increasing Digitalisation and the Financial Crisis. In The Return of Trust? Institutions and the Public after the Icelandic Financial Crisis. Edited by Throstur O. Sigurjonsson, David L. Schwarzkopf and Murray Bryant. Bingley: Emerald Publishing Limited, pp. 195–211. [Google Scholar] [CrossRef]

- OeNB. 2020. Fakten zu Österreich und seinen Banken. Available online: https://www.oenb.at/dam/jcr:ab423ff5-0b29-406f-9cca-e738a2a5f976/Fakten_zu_Oesterreich_Oktober_2020_screen.pdf (accessed on 8 February 2021).

- Ohanian, Roobina. 1990. Construction and Validation of a Scale to Measure Celebrity Endorsers’ Perceived Expertise, Trustworthiness, and Attractiveness. Journal of Advertising 19: 39–52. [Google Scholar] [CrossRef]

- Papon, Kerstin. 2019. Junge Leute beschäftigen sich erst mit Finanzthemen, wenn sie müssen. Frankfurter Allgemeine Zeitung. Available online: https://www.faz.net/aktuell/finanzen/junge-leute-und-finanzen-interesse-nur-bei-konkretem-anlass-16540572.html (accessed on 18 August 2020).

- PwC. 2018. Zwischen Entertainer und Werber—Wie Influencer unser Kaufverhalten beein- flus-sen. Available online: https://www.pwc.de/de/handel-und-konsumguter/zwischen-entertainer-und-werber.html (accessed on 10 July 2020).

- Serena, Manuela, and Jessica Hastenteufel. 2022. Finanzielle Bildung als Schlüssel zur Finanziellen Freiheit. Wiesbaden: Springer. [Google Scholar]

- Simon, Herbert A. 1955. A behavioral model of rational choice. Quarterly Journal of Economics 69: 99–118. [Google Scholar] [CrossRef]

- Simon, Herbert A. 1956. Rational choice and the structure of environments. Psychological Review 63: 129–38. [Google Scholar] [CrossRef]

- Skvarciany, Viktorija, and Daiva Jureviciene. 2017. Factors influencing customer trust in mobile banking: Case of Latvia. Economics and Culture 14: 69–76. [Google Scholar] [CrossRef]

- Statista. 2020a. Die zehn größten Banken in Österreich nach Bilanzsimmer im Jahr 2019. Available online: https://de.statista.com/statistik/daten/studie/288090/umfrage/banken-in-oesterreich-nach-ihrer-bilanzsumme/ (accessed on 8 February 2021).

- Statista. 2020b. Statistiken zur Bankenbranche in Österreich. Available online: https://de.statista.com/themen/3549/bankenbranche-in-oesterreich/ (accessed on 8 February 2021).

- Taylor, Charles R. 2020. The urgent need for more research on influencer marketing. International Journal of Advertising 39: 889–91. [Google Scholar] [CrossRef]

- Thibaut, John W., and Harold H. Kelley. 1959. The Social Psychology of Groups. New York: Wiley. [Google Scholar]

- Tversky, Amos, and Daniel Kahneman. 1974. Judgment under uncertainty: Heuristics and biases. Science 185: 1124–31. [Google Scholar] [CrossRef]

- Vrontis, Demetris, Anna Makrides, Michael Christofi, and Alkis Thrassou. 2021. Social media influencer marketing: A systematic review, integrative framework and future research agenda. International Journal of Consumer Studies 45: 617–44. [Google Scholar] [CrossRef]

- Waschbusch, Gerd, and Jessica Hastenteufel. 2020. Bankmarketing. In Gabler Banklexikon: Bank—Börse—Finanzierung, 14th ed. Edited by Luwdwig Gramlich, Peter Gluchowski, Andreas Horsch, Klaus Schäfer and Gerd Waschbusch. Wiesbaden: Springer Gabler, pp. 230–232. [Google Scholar]

- Waschbusch, Gerd, Hannes Schuster, and Susen C. Berg. 2018. Banken und Vertrauen: Eine Grundlagenuntersuchung zur Bedeutung des Vertrauens in der Ökonomie am Beispiel des Kreditgewerbes. Baden-Baden: Nomos. [Google Scholar]

- Ye, Guoquan, Liselot Hudders, Steffi de Jans, and Marijke De Veirman. 2021. The Value of Influencer Marketing for Business: A Bibliometric Analysis and Managerial Implications. Journal of Advertising 50: 160–78. [Google Scholar] [CrossRef]

Figure 1.

Topics of Influencer Marketing.

Figure 2.

Experience with influencer marketing in the financial sector.

Figure 3.

Kolmogorov-Smirnov norm test H6.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

School education and interest in financial products.

| Fully Agree | Partly Agree | Neither | Partly Disagree | Strongly Disagree | Total | |

|---|---|---|---|---|---|---|

| mandatory school leaving certificate | 0 | 1 | 1 | 5 | 1 | 8 |

| completion of apprenticeship | 2 | 3 | 1 | 2 | 2 | 10 |

| school leaving qualification | 11 | 29 | 14 | 28 | 16 | 98 |

| academic (Bachelor/Master) | 37 | 62 | 10 | 34 | 40 | 183 |

| other | 0 | 0 | 2 | 0 | 1 | 3 |

| total | 50 | 95 | 28 | 69 | 60 | 302 |

Table 2.

School education and engagement in financial products.

| Fully Agree | Partly Agree | Neither | Partly Disagree | Strongly Disagree | Total | |

|---|---|---|---|---|---|---|

| mandatory school leaving certificate | 0 | 1 | 1 | 4 | 2 | 8 |

| completion of apprenticeship | 1 | 3 | 1 | 1 | 3 | 10 |

| school leaving qualification | 5 | 30 | 16 | 23 | 24 | 98 |

| academic (Bachelor/Master) | 35 | 45 | 15 | 45 | 43 | 183 |

| other | 0 | 0 | 2 | 0 | 1 | 3 |

| total | 41 | 79 | 36 | 73 | 73 | 302 |

Table 3.

Correlations H1.

| Engagement with Acquired Financial Products | Source of Information | ||

|---|---|---|---|

| engagement with acquired financial products | correlation according to Pearson | 1 | 0.246 ** |

| Significance (2-sided) | 0.000 | ||

| N | 302 | 302 | |

| source of information | correlation according to Pearson | 0.246 ** | 1 |

| Significance (2-sided) | 0.000 | ||

| N | 302 | 302 |

** The correlation is significant at the 0.01 level (2-sided).

Table 4.

Correlations H2.

| Credibility | Buying Behavior_NEW | ||

|---|---|---|---|

| credibility | correlation according to Pearson | 1 | 0.479 ** |

| significance (2-sided) | 0.000 | ||

| N | 302 | 302 | |

| buying behavior_NEW | correlation according to Pearson | 0.479 ** | 1 |

| significance (2-sided) | 0.000 | ||

| N | 302 | 302 |

** The correlation is significant at the 0.01 level (2-sided).

Table 5.

Correlations H3.

| Credibility | Buy Advertised Financial Product | ||

|---|---|---|---|

| credibility | correlation according to Pearson | 1 | 0.310 ** |

| Significance (2-sided) | 0.000 | ||

| N | 299 | 299 | |

| buy advertised financial product | correlation according to Pearson | 0.310 ** | 1 |

| significance (2-sided) | 0.000 | ||

| N | 299 | 299 |

** The correlation is significant at the 0.01 level (2-sided).

Table 6.

Correlations H4.

| Engagement with Acquired Financial Products | Person of Trust | ||

|---|---|---|---|

| engagement with acquired financial products | correlation according to Pearson | 1 | 0.293 ** |

| significance (2-sided) | 0.000 | ||

| N | 299 | 299 | |

| person of trust | correlation according to Pearson | 0.293 ** | 1 |

| significance (2-sided) | 0.000 | ||

| N | 299 | 299 |

** The correlation is significant at the 0.01 level (2-sided).

Table 7.

Correlations H5.

| Influencers More Trustworthy Than Traditional Advertising | Buy Advertised Financial Product | ||

|---|---|---|---|

| influencers more trustworthy than traditional advertising | correlation according to Pearson | 1 | 0.261 ** |

| significance (2-sided) | 0.000 | ||

| N | 299 | 299 | |

| buy advertised financial product | correlation according to Pearson | 0.261 ** | 1 |

| significance (2-sided) | 000 | ||

| N | 299 | 299 |

** The correlation is significant at the 0.01 level (2-sided).

Table 8.

Mann–Whitney U test H6.

| Summary Mann–Whitney U Test | |

|---|---|

| N | 302 |

| Mann–Whitney U | 11,592.000 |

| Wilcoxon-W | 17,502.000 |

| test statistic | 11,592.0000 |

| standard error | 621.252 |

| standardized test statistic | 2.086 |

| asymptotic Sig. (two-sided test) | 0.37 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Walzhofer, N.; Riekeberg, M.; Follert, F. From White Collar to Influencer Marketing? How Banks Can Reach Young Customers. Int. J. Financial Stud. 2022, 10, 79. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10030079

AMA Style

Walzhofer N, Riekeberg M, Follert F. From White Collar to Influencer Marketing? How Banks Can Reach Young Customers. International Journal of Financial Studies. 2022; 10(3):79. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10030079

Chicago/Turabian StyleWalzhofer, Nicole, Marcus Riekeberg, and Florian Follert. 2022. "From White Collar to Influencer Marketing? How Banks Can Reach Young Customers" International Journal of Financial Studies 10, no. 3: 79. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10030079

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.