The Financial/Accounting Impact of FFP on Participating in European Competitions: An Analysis of the Spanish League

Abstract

:1. Introduction

2. Literature Background

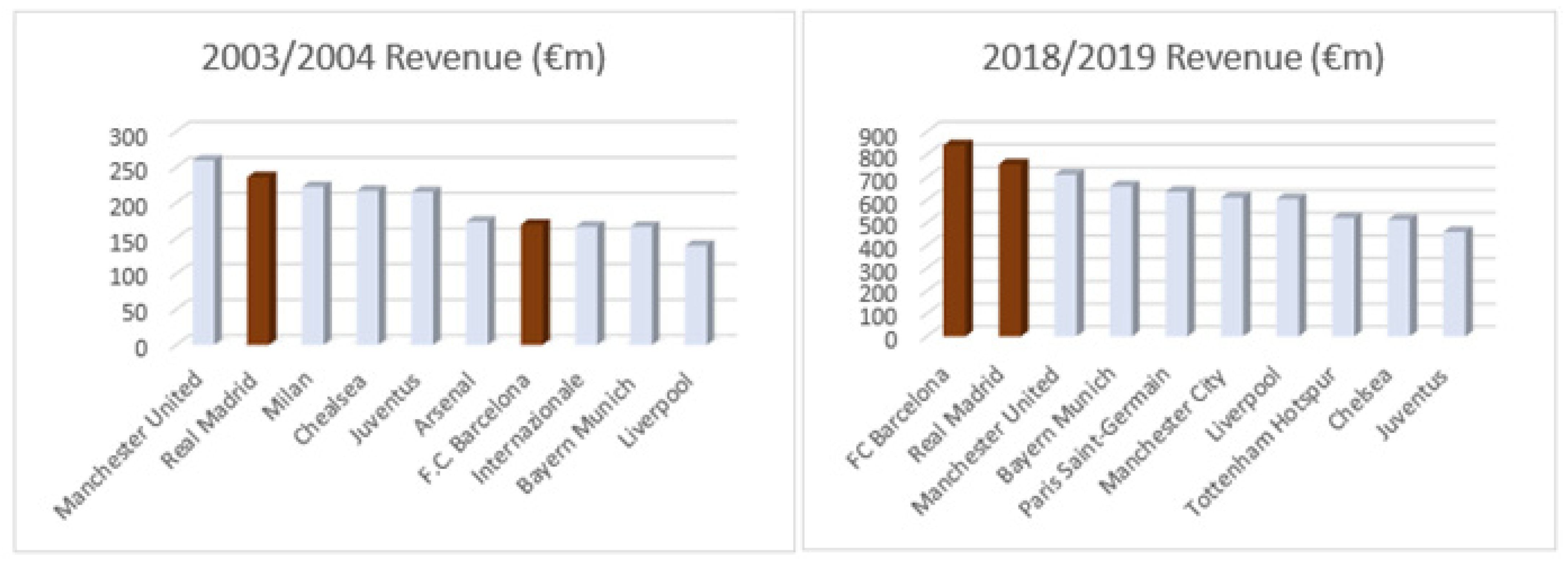

The Impact of FFP

3. Data and Methodology

3.1. The Dataset: The Spanish League

3.2. Data Selection Procedure

- Clubs that participated in the First Division of the Spanish league during the period from 2004 to 2019 (clubs competing in the top division are more likely to participate in European competitions and are those most affected by the FFP regulation).

- Clubs that have participated in at least 13 seasons in the First Division were selected.

3.3. Research Design

3.4. The Test Variable and Grouping Criteria

4. Results and Discussion

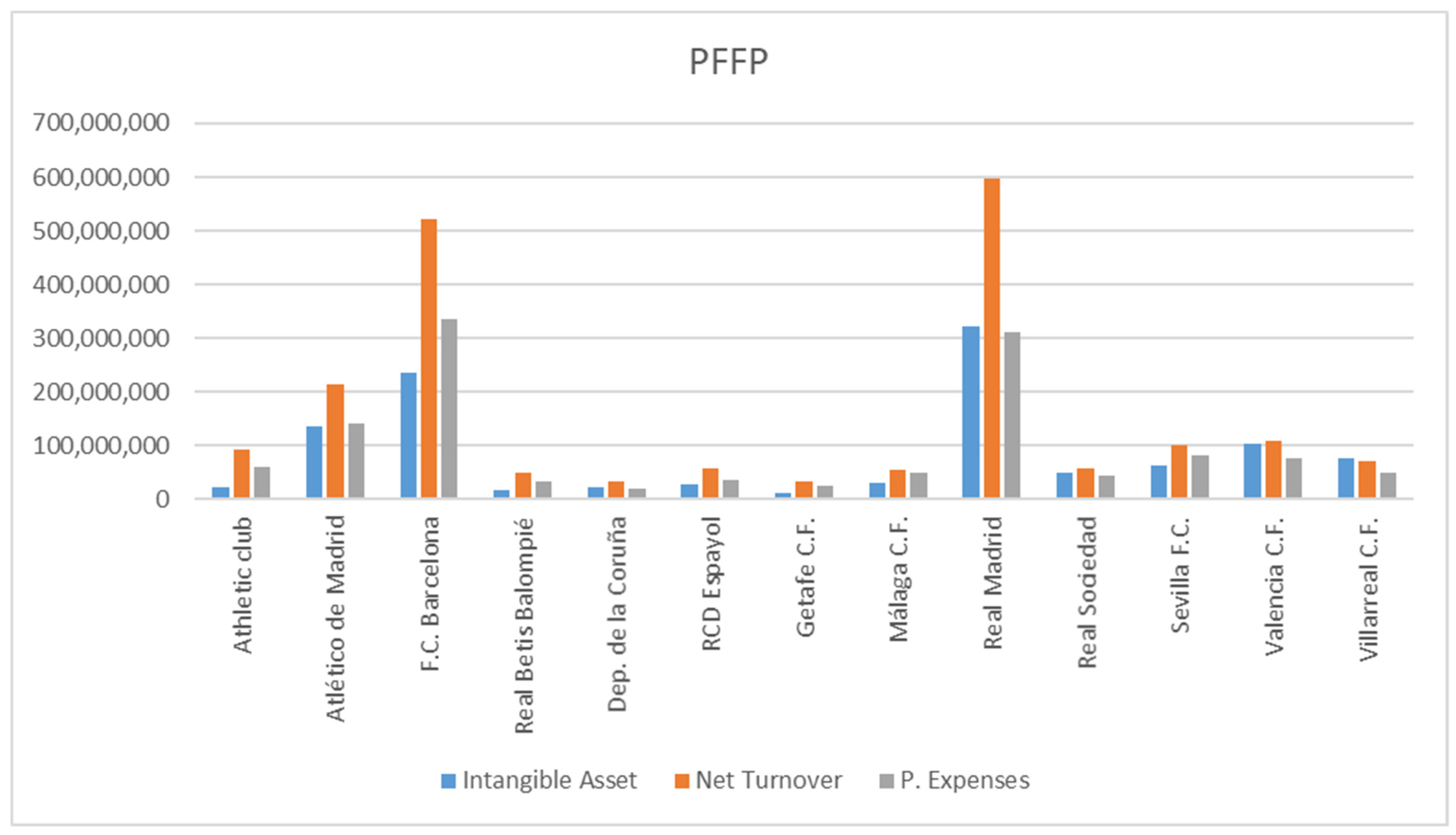

4.1. Analysis of the Spanish League

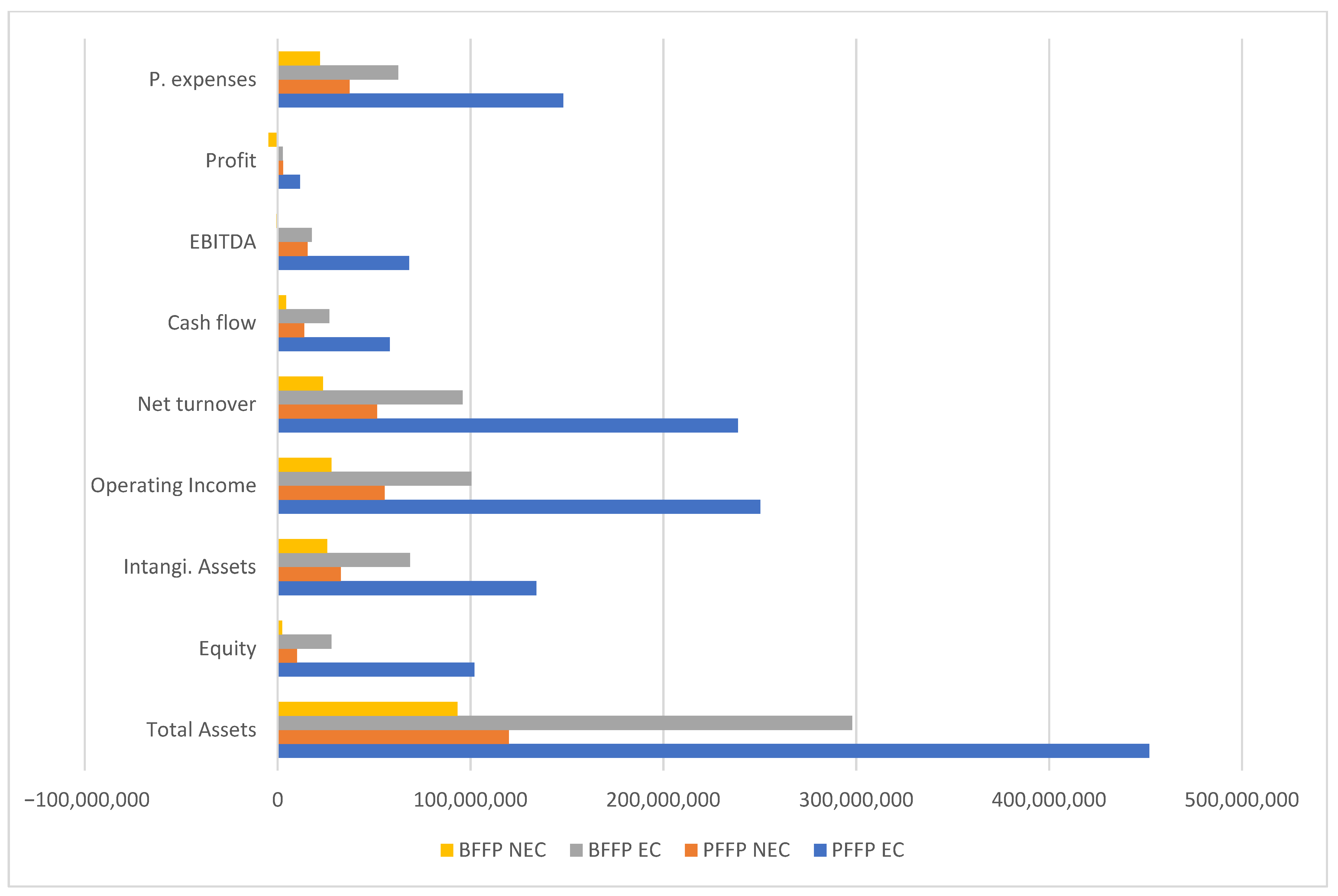

4.2. Difference between EC and NEC

5. Conclusions

5.1. Future Research

5.2. Limitations

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Ratios | Abbreviation | Calculation | Source |

|---|---|---|---|

| Indebtedness | Indeb | (total liabilities − equity)/total liabilities × 100 | SABI |

| Leverage | Lev | (non-current liabilities + financial liabilities)/equity × 100 | SABI |

| personal expenses/operating income | PE/OI | personal expenses/operating income | SABI |

| Average personal expenses | PEA | personal expenses/number of employees | SABI |

| Profit margin | Prof. Marg | EBT/operating income | SABI |

| Registered capital | R. Capital | SABI | |

| return on capital employed | RCE | (EBT + Finance expenses and assimilated expenses)/(equity + non-current liabilities) × 100 | SABI |

| Return On Assets | ROA | (EBT/total assets) × 100 | SABI |

| Return on Equity | ROE | (EBT/equity) × 100 | SABI |

| Return on sales | ROS | (EBIT/net turnover) × 100 | AUTHORS |

| Solvency ratio | Solvency | (current assets/current liabilities) | SABI |

| ratio of financial autonomy | SRFA | (equity/total assets) | SABI |

| 1 | The participation of clubs in both the top division and in European competitions was verified on the official website of the Professional Football League (LFP). |

References

- A.T. Kearney. 2010. The A.T. Kearney EU Football Sustainability Study: Is European Football to Popular to Fail? Düsseldorf: A.T. Kearney. Available online: http://www.atkearney.de/%20content/misc/wrapper.php/id/51071/name/pdf_eu_football_sustainability_study_final_net_%201277724063f532.pdf (accessed on 24 April 2022).

- Aggarwal, Raj, and John W. Goodell. 2014. Cross-national differences in access to finance: Influence of culture and institutional environments. Research in International Business and Finance 31: 193–211. [Google Scholar] [CrossRef]

- Andreff, Wladimir. 2007. French Football: A Financial Crisis Rooted in Weak Governance. Journal of Sports Economics 8: 652–61. [Google Scholar] [CrossRef]

- Ascari, Guido, and Philippe Gagnepain. 2007. Evaluating Rent Dissipation in the Spanish Football Industry. Journal of Sports Economics 8: 468–90. [Google Scholar] [CrossRef]

- Atkinson, Scott E., Linda R. Stanley, and John Tschirhart. 1988. Revenue Sharing as a Incentive in an Agency Problem: An Example from the National Football League. The Rand Journal of Economics 19: 27–43. [Google Scholar] [CrossRef]

- Barajas, Ángel, and Plácido Rodríguez. 2010. Spanish football clubs’ finances: Crisis and player salaries. International Journal of Sport Finance 5: 52–66. [Google Scholar]

- Barajas, Ángel, and Plácido Rodríguez. 2014. Spanish football in need of financial therapy: Cut expenses and inject capital. International Journal of Sport Finance 9: 73–90. [Google Scholar]

- Barros, Carlos Pestana, and Stephanie Leach. 2006. Performance evaluation of the English Premier Football League with data envelopment analysis. Applied Economics 38: 1449–58. [Google Scholar] [CrossRef]

- Barros, Carlos Pestana, and Stephanie Leach. 2007. Technical efficiency in the English Football Association Premier League with a stochastic cost frontier. Applied Economics Letters 14: 731–41. [Google Scholar] [CrossRef]

- Barros, Carlos Pestana, Vincenzo Scafarto, and Antònio Samagaio. 2014. Cost performance of Italian football clubs: Analysing the role of marketing and sponsorship. International Journal of Sports Marketing and Sponsorship 15: 59–77. [Google Scholar] [CrossRef]

- Bernile, Gennaro, and Evgeny Lyandres. 2011. Understanding Investor Sentiment: The Case of Soccer. Financial Management 40: 357–80. [Google Scholar] [CrossRef]

- Birkhäuser, Stephan, Christoph Kaserer, and Daniel Urban. 2019. Did UEFA’s financial fair play harm competition in European football leagues? Review of Managerial Science 13: 113–45. [Google Scholar] [CrossRef]

- Calahorro-López, Alberto, and Melinda Ratkai. 2022. European Football Clubs and Their Finances. A Systematic Literature Review. Spanish Accounting Review. Accepted on April 2022. [Google Scholar]

- Dabscheck, Braham. 1975. Sporting Equality: Labour Market vs. Product Market Control. Journal of Industrial Relations 17: 174–90. [Google Scholar] [CrossRef]

- Davenport, David S. 1969. Collusive Competition in Major League Baseball its Theory and Institutional Development. The American Economist 13: 6–30. [Google Scholar] [CrossRef]

- De la Rosa, Marcos. 2022. El FC Barcelona Activa las Palancas Económicas Que Les Permitirán Fichar en el Mercado. 90 min. Available online: https://www.90min.com/es/posts/fc-barcelona-activa-palancas-economicas-que-les-permitiran-fichar-mercado (accessed on 24 June 2022).

- Deloitte. 2005. Football Money League. The Climbers and the Sliders. Edited by Dan Jones. Manchester: Sports Business Group. Available online: https://www.cies-uni.org/sites/default/files/2005_Deloitte_Football_Money_League.pdf (accessed on 24 June 2022).

- Deloitte. 2020. Eye on the Prize. Football Money League. Edited by Dan Jones. Manchester: Sports Business Group. Available online: https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/sports-business-group/deloitte-uk-deloitte-football-money-league-2020.pdf (accessed on 24 June 2022).

- Dermit-Richard, Nadine, Nicolas Scelles, and Stephen Morrow. 2019. French DNCG management control versus UEFA Financial Fair Play: A divergent conception of financial regulation objectives. Soccer and Society 20: 408–30. [Google Scholar] [CrossRef]

- Dietl, Helmut M., and Egon Franck. 2007. Governance Failure and Financial Crisis in German Football. Journal of Sports Economics 8: 662–69. [Google Scholar] [CrossRef]

- Dimitropoulos, Panagiotis E. 2016. Audit Selection in the European Football Industry under Union of European Football Associations Financial Fair Play. International Journal of Economics and Financial Issues 6: 901–6. [Google Scholar]

- Dimitropoulos, Panagiotis E., and Evangelos Koumanakos. 2015. Intellectual capital and profitability in European football clubs. International Journal of Accounting, Auditing and Performance Evaluation 11: 202. [Google Scholar] [CrossRef]

- Dimitropoulos, Panagiotis E., and Konstantinos Koronios. 2018. Earnings persistence of european football clubs under UEFA’s FFP. International Journal of Financial Studies 6: 43. [Google Scholar] [CrossRef]

- Dimitropoulos, Panagiotis E., and Vincenzo Scafarto. 2021. The impact of UEFA financial fair play on player expenditures, sporting success and financial performance: Evidence from the Italian top league. European Sport Management Quarterly 21: 20–38. [Google Scholar] [CrossRef]

- Dowdy, Shirley, Stanley Wearden, and Daniel Chilko. 2011. Statistics for Research. Hoboken: John Wiley & Sons. [Google Scholar]

- Drut, Bastien. 2011. Economie Du Football Professionnel. Paris: La Dècouverte. [Google Scholar]

- Drut, Bastien, and Gaël Raballand. 2012. Why does financial regulation matter for European professional football clubs? International Journal of Sport Management and Marketing 11: 73–88. [Google Scholar] [CrossRef]

- El-Hodiri, Mohamed, and James Quirk. 1971. An Economic Model of a Professional Sports League. Journal of Political Economy 79: 1302–19. [Google Scholar] [CrossRef]

- Franck, Egon. 2014. Financial Fair Play in Eurpean Club Football-What Is It All about? University of Zurich, Department of Business Administration, UZH Business Working Paper No. 328. Available online: https://ssrn.com/abstract=2284615 (accessed on 24 June 2022).

- Franck, Egon. 2018. European club football after “five treatments” with financial fair play—Time for an assessment. International Journal of Financial Studies 6: 97. [Google Scholar] [CrossRef]

- Franck, Egon, and Markus Lang. 2014. A theoretical analysis of the influence of money injections on risk taking in football clubs. Scottish Journal of Political Economy 61: 430–54. [Google Scholar] [CrossRef] [Green Version]

- Francois, Aurélien, Nadine Dermit-Richard, Daniel Plumley, Rob Wilson, and Natacha Heutte. 2021. The effectiveness of UEFA Financial Fair Play: Evidence from England and France 2008–2018. Sport, Business and Management: An International Journal 12: 342–62. [Google Scholar] [CrossRef]

- Freestone, Christopher John, and Argyro Elisavet Manoli. 2017. Financial fair play and competitive balance in the premier league. Sport, Business and Management: An International Journal 7: 175–96. [Google Scholar] [CrossRef]

- Galariotis, Emilios, Christophe Germain, and Constantin Zopounidis. 2018. A combined methodology for the concurrent evaluation of the business, financial and sports performance of football clubs: The case of France. Annals of Operations Research 266: 589–612. [Google Scholar] [CrossRef]

- Gerhards, Jürgen, and Michael Mutz. 2017. Who wins the championship? Market value and team composition as predictors of success in the top European football leagues. European Societies 19: 223–42. [Google Scholar] [CrossRef]

- Ghio, Alessandro, Massimo Ruberti, and Roberto Verona. 2019. Financial constraints on sport organizations’ cost efficiency: The impact of financial fair play on Italian soccer clubs. Applied Economics 51: 2623–38. [Google Scholar] [CrossRef]

- Gómez, Javier. 2017. Control Económico. Paper presented at the Conference held at El Colegio de Economistas de Madrid, Liga de Fútbol Profesional, Meeting on the Economic Control of the Professional Soccer League, Madrid, Spain, November. [Google Scholar]

- Guzmán, Isidoro, and Stephen Morrow. 2007. Measuring efficiency and productivity in professional football teams: Evidence from the English Premier League. Central European Journal of Operations Research 15: 309–28. [Google Scholar] [CrossRef]

- Kalashyan, Jesse. 2021. The game behind the game: UEFA’s Financial Fair Play Regulations and the need to field a substitute. European Competition Journal 18: 21–81. [Google Scholar] [CrossRef]

- Kuper, Simon, and Stefan Szymanski. 2009. Soccernomics:Why England Loses, Why Germany and Brazil Win, and Why the US, Japan, Australia, Turkey—and Even Iraq—Are Destined to Become the Kings of the World’s Most Popular Sport. Paris: Hachette. [Google Scholar]

- Kusano, Masaki. 2020. Does recognition versus disclosure affect risk relevance? Evidence from finance leases in Japan. Journal of International Accounting, Auditing and Taxation 38: 100303. [Google Scholar] [CrossRef]

- Lago, Umberto, Alessandro Baroncelli, and Stefan Szymanski. 2004. Il Business Del Calcio. Successi Sportivi e Rovesci Finanziari Copertina Flessibile. Milano: EGEA. [Google Scholar]

- León, María. 2021. El Fútbol Español Rompe Su Tabú en Bolsa y Sigue a Premier, Serie A y Bundesliga. La Información. Available online: https://www.lainformacion.com/mercados-y-bolsas/futbol-espanol-rompe-tabu-bolsa-sigue-premier-serie-a-bundesliga/2852394/ (accessed on 8 March 2022).

- Madden, Paul. 2015. Welfare economics of ‘“financial fair play”’ in a sports league with benefactor owners. Journal of Sports Economics 16: 159–84. [Google Scholar] [CrossRef]

- Mann, Henry B., and Donald R. Whitney. 1947. On a test of whether one of two random variables is stochastically larger than the other. The Annals of Mathematical Statistics 18: 50–60. [Google Scholar] [CrossRef]

- Maqueira, Juan M., Sebastián Bruque, and Ákos Uhrin. 2019. Talent management: Two pathways to glory? Lessons from the sports arena. Employee Relations 41: 34–51. [Google Scholar] [CrossRef]

- Mareque, Mercedes, Ángel Barajas, and Francisco Lopez-Corrales. 2018. The impact of union of european football associations (Uefa) financial fair play regulation on audit fees: Evidence from Spanish football. International Journal of Financial Studies 6: 92. [Google Scholar] [CrossRef]

- Morrow, Stephen. 2013. Football club financial reporting: Time for a new model? Sport, Business and Management: An International Journal 3: 297–311. [Google Scholar] [CrossRef]

- Morrow, Stephen. 2014. Financial Fair Play—Implications For Football Club Financial Reporting. Edinburgh: ICAS Institute of Chartered Accountants of Scotland. [Google Scholar]

- Müller, J. Christian, Joachim Lammert, and Gregor Hovemann. 2012. The Financial Fair Play Regulations of UEFA: An Adequate Concept to Ensure the Long-Term Viability and Sustainability of European Club Football? International Journal of Sport Finance 7: 117–40. [Google Scholar]

- Neale, Walter C. 1964. The Peculiar Economics of Professional Sports: A Contribution to the Theory of the Firm in Sporting Competition and in Market Competition. Source: The Quarterly Journal of Economics 78: 1–14. [Google Scholar] [CrossRef]

- Nicoliello, Mario, and Davide Zampatti. 2016. Football clubs’ profitability after the Financial Fair Play regulation: Evidence from Italy. Sport, Business and Management: An International Journal 6: 460–75. [Google Scholar] [CrossRef]

- Olivier, Adoukonou, Andre Florence, and Viviani Jean-Laurent. 2018. Callable convertible bonds in sequential financing: Evidence on the Western European market. Journal of Multinational Financial Management 45: 35–51. [Google Scholar] [CrossRef]

- Olsson, Lars-Chister. 2011. 2 Decisive Moments in UEFA: Lars-Chister Olsson. In The Organisation and Governance of Top Football Across Europe. London: Routledge, pp. 26–40. [Google Scholar]

- Pantuso, Giovanni. 2017. The Football Team Composition Problem: A Stochastic Programming approach. Journal of Quantitative Analysis in Sports 13: 113–29. [Google Scholar] [CrossRef]

- Pedace, Roberto. 2008. Earnings, performance, and nationality discrimination in a highly competitive labor market as an analysis of the English professional soccer league. Journal of Sports Economics 9: 115–40. [Google Scholar] [CrossRef]

- Prigge, Stefan, and Lars Tegtmeier. 2019. Market valuation and risk profile of listed European football clubs. Sport, Business and Management: An International Journal 9: 146–63. [Google Scholar] [CrossRef]

- Ramchandani, Girish, Daniel Plumley, Sophie Boyes, and Rob Wilson. 2018. A longitudinal and comparative analysis of competitive balance in five European football leagues. Team Performance Management 24: 265–82. [Google Scholar] [CrossRef]

- Regoliosi, Carlo. 2016. The accounting treatments in professional football clubs in Italy from a business model perspective. Rivista Italiana Di Ragioneria e Di Economia Aziendale 5: 7. [Google Scholar]

- Rohde, Marc, and Christoph Breuer. 2016. Europe’s Elite Football: Financial Growth, Sporting Success, Transfer Investment, and Private Majority Investors. International Journal of Financial Studies 4: 12. [Google Scholar] [CrossRef]

- Rohde, Marc, and Christoph Breuer. 2018. Competing by investments or efficiency? Exploring financial and sporting efficiency of club ownership structures in European football. Sport Management Review 21: 563–81. [Google Scholar] [CrossRef]

- Rottenberg, Simon. 1956. The baseball players’ labor market. Journal of Political Economy 64: 242–58. [Google Scholar] [CrossRef]

- Sánchez, Borja. 2022. La Liga Denuncia al PSG y al Manchester City Por Incumplir Las Reglas Del Fair Play Financiero. El español. Available online: https://www.elespanol.com/deportes/futbol/20220615/laliga-psg-manchester-city-fair-play-financiero/680432141_0.html (accessed on 24 June 2022).

- Sass, Markus. 2016. Glory Hunters, Sugar Daddies, and Long-Term Competitive Balance Under UEFA Financial Fair Play. Journal of Sports Economics 17: 148–58. [Google Scholar] [CrossRef]

- Schubert, Mathias. 2013. Informations-und Anreizprobleme im Kontext von UEFA Financial Fair Play-Eine institutionenökonomische Analyse Information and incentive problems in the context of UEFA Financial Fair Play-An institutional economics perspective. Sport und Gesellschaft-Sport and Society Jahrgang 10: 260–91. [Google Scholar] [CrossRef]

- Schubert, Mathias. 2014. Potential agency problems in European club football? The case of UEFA Financial Fair Play. Sport, Business and Management: An International Journal 4: 336–50. [Google Scholar] [CrossRef]

- Serby, Tom. 2016. The state of EU sports law: Lessons from UEFA’s ‘Financial Fair Play’ regulations. International Sports Law Journal 16: 37–51. [Google Scholar] [CrossRef]

- Sloane, Peter J. 1969. The economics of professional football: The football club as a utility maximiser. Journal of Political Economy 64: 242–58. [Google Scholar]

- Solberg, Harry Arne, and Kjetil K. Haugen. 2010. European club football: Why enormous revenues are not enough? Sport in Society 13: 329–43. [Google Scholar] [CrossRef]

- Soldevilla, Adriá. 2022. Cómo Funcionan Las Palancas Económicas, Por Qué el Barcelona Seguirá Excedido de Límite Salarial y Por Qué Será Difícil Fichar. Goal. Available online: https://www.goal.com/es-mx/noticias/como-funcionan-las-palancas-economicas-por-que-el-barcelona/blt11190424932c985c (accessed on 24 June 2022).

- Szymanski, Stefan. 2017. Entry into exit: Insolvency in English professional football. Scottish Journal of Political Economy 64: 419–44. [Google Scholar] [CrossRef]

- Szymanski, Stefan, and Daniel Weimar. 2019. Insolvencies in professional football: A German Sonderweg? International Journal of Sport Finance 14: 54–68. [Google Scholar] [CrossRef]

- Szymanski, Stefan, and Ron Smith. 1997. The English football industry: Profit, performance and industrial structure. International Review of Applied Economics 11: 135–53. [Google Scholar] [CrossRef]

- Szymanski, Stefan, and Tim Kuypers. 1999. Winners and Losers, the Business Strategy of Football. London: Penguin. [Google Scholar]

- Terrien, Mickael, Nicolas Scelles, Stephen Morrow, Lionel Maltese, and Christophe Durand. 2017. The win/profit maximization debate: Strategic adaptation as the answer? Sport, Business and Management: An International Journal 7: 121–40. [Google Scholar] [CrossRef]

- Tsalavoutas, Ioannis, and Fanis Tsoligkas. 2021. Uncertainty avoidance and stock price informativeness of future earnings. Journal of International Financial Markets, Institutions and Money 75: 101410. [Google Scholar] [CrossRef]

- UEFA. 2012. UEFA Club Licensing and Financial Fair Play Regulations. Edition 2012. Available online: https://www.uefa.com/multimediafiles/download/tech/uefaorg/general/01/80/54/10/1805410_download.pdf (accessed on 24 June 2022).

- Vrooman, John. 2007. Theory of the beautiful game: The unification of european football. Scottish Journal of Political Economy 54: 314–54. [Google Scholar] [CrossRef]

- Yang, Yan, Shujie Yao, Hongbo He, and Jinghua Ou. 2019. On corporate philanthropy of private firms and trade credit financing in China. China Economic Review 57: 101316. [Google Scholar] [CrossRef]

- Zambrano-Domínguez, Javier. 2022. La Competitividad Del Fútbol Español: Una Cuestión de Iniciativa Regulatoria. Playbook. Available online: https://www.2playbook.com/industria-opina/competitividad-futbol-espanol-cuestion-iniciativa-regulatoria_8249_102.html (accessed on 24 June 2022).

| ITEM | MEAN | Mann–Whitney | |||

|---|---|---|---|---|---|

| BFFP | PFFP | Absolute Dif. | Sig | Null | |

| CashFlow | 16,168,752.02 | 36,683,436.00 | 20,514,683.99 | 0.000 | REJECT |

| EBIT | −8,018,639.11 | 13,301,529.27 | 21,320,168.37 | 0.000 | REJECT |

| EBITDA | 9,036,426.06 | 42,690,271.26 | 33,653,845.20 | 0.000 | REJECT |

| EBT | −10,587,822.65 | 9,694,114.91 | 20,281,937.56 | 0.000 | REJECT |

| Equity | 15,738,755.02 | 57,416,971.38 | 41,678,216.36 | 0.001 | REJECT |

| Employees | 163.31 | 305.46 | 142.15 | 0.000 | REJECT |

| INDEB | 111.40 | 104.04 | 7.36 | 0.007 | REJECT |

| Int Assets | 47,376,647.70 | 85,007,951.67 | 37,631,303.98 | 0.073 | |

| LEV | 1,348.79 | 224.43 | 1,124.37 | 0.100 | |

| Net tur. | 61,473,655.63 | 148,054,965.27 | 86,581,309.64 | 0.000 | REJECT |

| Oper. Income | 65,985,443.72 | 155,832,444.57 | 89,847,000.85 | 0.000 | REJECT |

| P. Expe. | 43,192,013.27 | 94,412,655.82 | 51,220,642.55 | 0.000 | REJECT |

| PE/OI | 76.20 | 68.52 | 7.68 | 0.014 | REJECT |

| PEA | 279.71 | 263.82 | 15.90 | 0.645 | |

| Profit | −886,313.15 | 7,370,680.40 | 8,256,993.5 | 0.000 | REJECT |

| Prof. Marg. | −34.23 | 4.09 | 38.32 | 0.000 | REJECT |

| R. capital | 17,986,560.45 | 56,491,938.32 | 38,505,377.86 | 0.000 | REJECT |

| RCE | 36.43 | 62.27 | 25.84 | 0.000 | REJECT |

| ROA | −13.06 | 6.17 | 19.22 | 0.000 | REJECT |

| ROE | −133.54 | 18.25 | 151.79 | 0.001 | REJECT |

| ROS | −88.48 | 4.42 | 84.06 | 0.000 | REJECT |

| Solvency | 0.67 | 0.65 | 0.02 | 0.609 | |

| SRFA | −11.41 | −4.05 | 7.36 | 0.007 | REJECT |

| T Assets | 200,664,540.11 | 291,107,116.59 | 90,442,576.48 | 0.124 | |

| ITEM | MEAN | Mann–Whitney | |||

|---|---|---|---|---|---|

| NEC | EC | Absolute Dif. | Sig | Null | |

| CashFlow | 4,422,014.62 | 26,822,769.66 | 22,400,755. 4 | 0.000 | REJECT |

| EBIT | −9,696,711.35 | −6,496,666.61 | 3,200,044.75 | 0.495 | |

| EBITDA | −572,667.29 | 17,751,650.27 | 18,324,317.56 | 0.001 | REJECT |

| EBT | −10,771,666.79 | −10,421,080.30 | 350,586.50 | 0.878 | |

| Equity | 2,319,968.97 | 27,909,281.90 | 25,589,312.93 | 0.002 | REJECT |

| Employees | 103.88 | 217.92 | 114.04 | 0.000 | REJECT |

| INDEB | 134.97 | 90.03 | −44.93 | 0.124 | |

| Int Assets | 25,650,929.61 | 68,559,222.82 | 42,908,293.21 | 0.000 | REJECT |

| LEV | −375.72 | 2,912.89 | 3,288.61 | 0.003 | REJECT |

| Net tur | 23,482,324.81 | 95,930,909.16 | 72,448,584.35 | 0.000 | REJECT |

| Oper. Income | 27,951,085.90 | 100,481,721.74 | 72,530,635.84 | 0.000 | REJECT |

| P. Expen. | 21,858,216.27 | 62,541,271.01 | 40,683,054.74 | 0.000 | REJECT |

| PE/OI | 84.62 | 68.57 | 16.05 | 0.020 | REJECT |

| PEA | 241.81 | 314.54 | 72.73 | 0.004 | REJECT |

| Profit | −4,702,029.45 | 2,574,452.78 | 7,276,482.23 | 0.036 | REJECT |

| Prof. Marg. | −48.57 | −21.22 | 27.35 | 0.083 | |

| R. Capital | 9,907,838.86 | 25,488,230.50 | 15,580,391.64 | 0.653 | |

| RCE | 83.81 | −6.54 | 90.35 | 0.438 | |

| ROA | −21.79 | −5.14 | 16.65 | 0.042 | REJECT |

| ROE | 33.88 | −285.39 | 319.27 | 0.341 | |

| ROS | −156.02 | −27.23 | 128.79 | 0.018 | REJECT |

| Solvency | 0.58 | 0.75 | 0.16 | 0.002 | REJECT |

| SRFA | −34.97 | 9.96 | 44.93 | 0.124 | |

| T Assets | 93,316,055.83 | 298,027,118.87 | 204,711,063.04 | 0.000 | REJECT |

| ITEM | MEAN | Mann–Whitney | |||

|---|---|---|---|---|---|

| NEC | EC | Absolute Dif. | Sig | Null | |

| CashFlow | 13,827,578.24 | 58,167,942.30 | 44,340,364.06 | 0.000 | REJECT |

| EBIT | 4,378,329.36 | 21,689,337.18 | 17,311,007.82 | 0.000 | REJECT |

| EBITDA | 15,525,750.87 | 68,224,920.43 | 52,699,169.56 | 0.000 | REJECT |

| EBT | 2,747,020.11 | 16,224,384.01 | 13,477,363.90 | 0.000 | REJECT |

| Equity | 10,033,762.97 | 101,957,187.28 | 91,923,424.31 | 0.000 | REJECT |

| Employees | 175.36 | 435.55 | 260.19 | 0.000 | REJECT |

| INDEB | 133.28 | 76.56 | 56.72 | 0.008 | REJECT |

| Int Assets | 32,696,210.39 | 134,180,988.47 | 101,484,778.08 | 0.000 | REJECT |

| LEV | 209.85 | 238.12 | 28.27 | 0.139 | |

| Net tur | 51,548,372.13 | 238,771,162.82 | 187,222,790.69 | 0.000 | REJECT |

| Oper. Income | 55,413,859.05 | 250,225,914.97 | 194,812,055.92 | 0.000 | REJECT |

| P. Expe. | 37,210,381.03 | 148,182,794.12 | 110,972,413.10 | 0.000 | REJECT |

| PE/OI | 70.39 | 66.77 | 3.62 | 0.379 | |

| PEA | 234.27 | 293.37 | 59.10 | 0.001 | REJECT |

| Profit | 2,738,421.01 | 11,632,359.04 | 8,893,938.03 | 0.002 | REJECT |

| Prof. Marg. | 5.34 | 2.91 | 2.42 | 0.248 | |

| R. Capital | 28,097,762.26 | 83,703,023.71 | 55,605,261.45 | 0.0046 | REJECT |

| RCE | 79.23 | 46.33 | 32.91 | 0.356 | |

| ROA | 8.80 | 3.69 | 5.11 | 0.511 | |

| ROE | 8.86 | 27.07 | 18.21 | 0.001 | REJECT |

| ROS | 2.89 | 5.86 | 2.96 | 0.983 | |

| Solvency | 0.64 | 0.66 | 0.02 | 0.639 | |

| SRFA | −33.28 | 23.44 | 56.72 | 0.008 | REJECT |

| T Assets | 119,916,297.34 | 452,026,486.68 | 332,110,189.34 | 0.000 | REJECT |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Calahorro-López, A.; Ratkai, M.; Vena-Oya, J. The Financial/Accounting Impact of FFP on Participating in European Competitions: An Analysis of the Spanish League. Int. J. Financial Stud. 2022, 10, 81. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10030081

Calahorro-López A, Ratkai M, Vena-Oya J. The Financial/Accounting Impact of FFP on Participating in European Competitions: An Analysis of the Spanish League. International Journal of Financial Studies. 2022; 10(3):81. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10030081

Chicago/Turabian StyleCalahorro-López, Alberto, Melinda Ratkai, and Julio Vena-Oya. 2022. "The Financial/Accounting Impact of FFP on Participating in European Competitions: An Analysis of the Spanish League" International Journal of Financial Studies 10, no. 3: 81. https://0-doi-org.brum.beds.ac.uk/10.3390/ijfs10030081