Estimating the Impacts of Proximity to Public Transportation on Residential Property Values: An Empirical Analysis for Hartford and Stamford Areas, Connecticut

Abstract

:1. Introduction

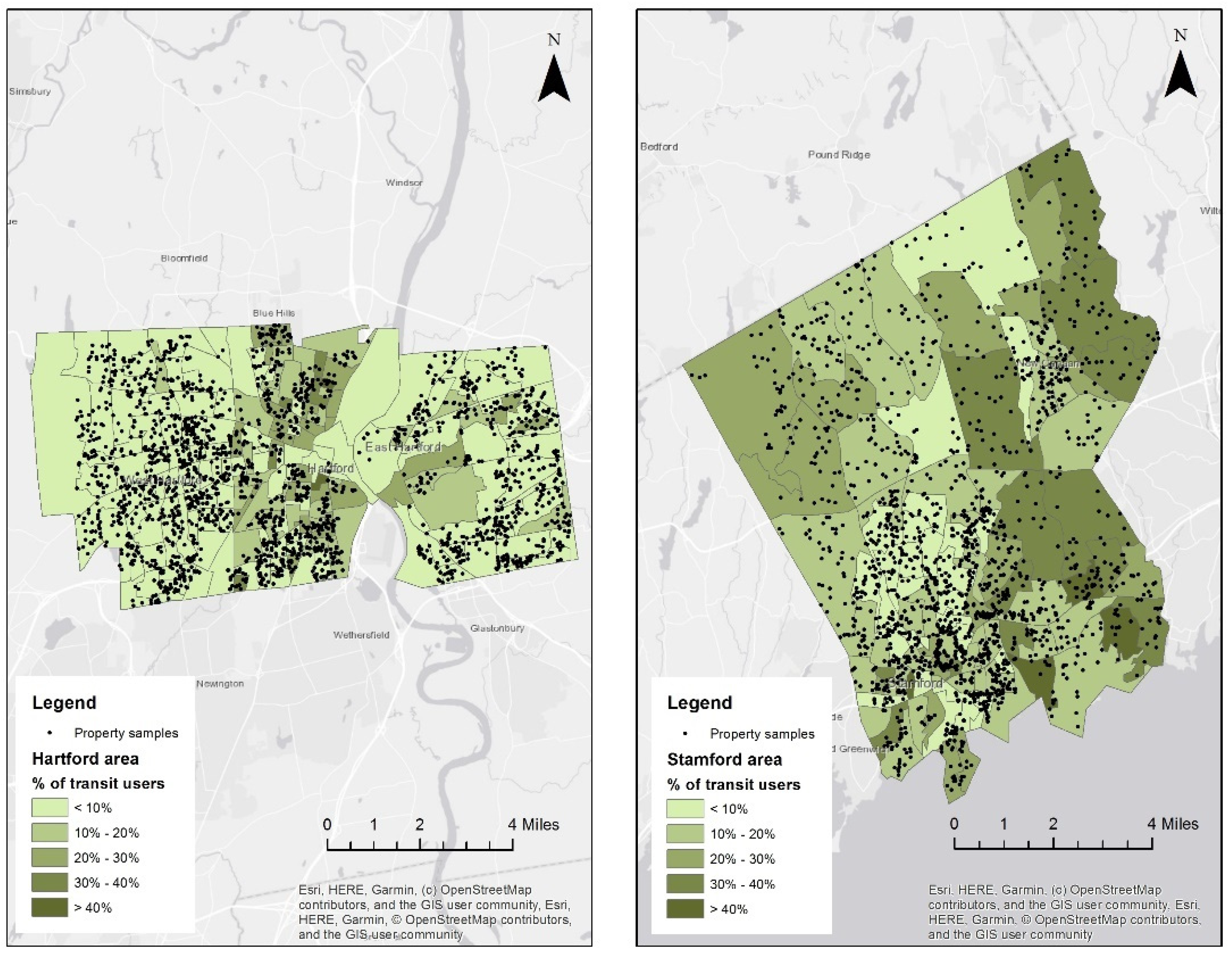

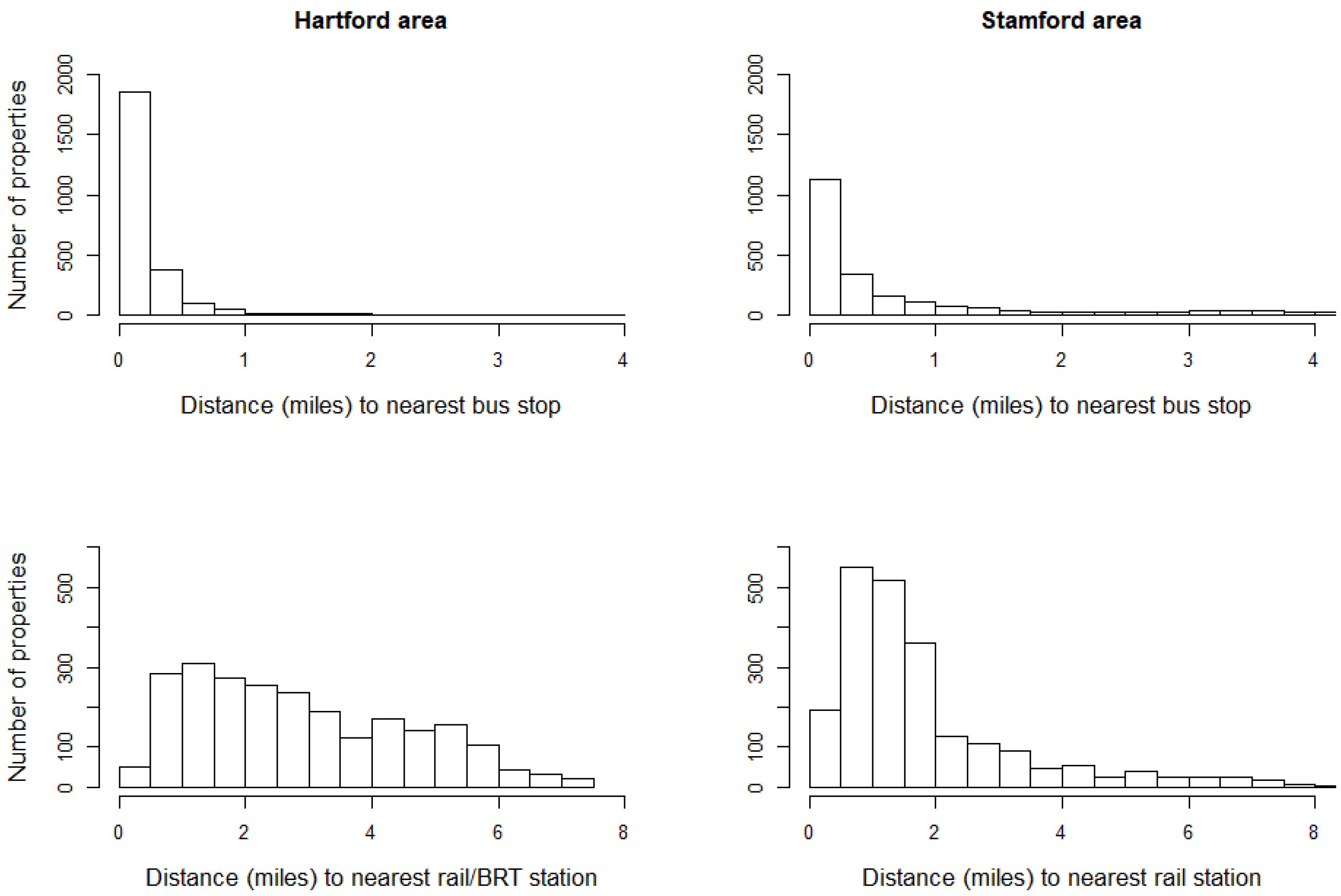

2. Study Area and Data

3. Methods

3.1. Hedonic Price Model

3.2. Global Regression Analysis—Ordinary Least Squares

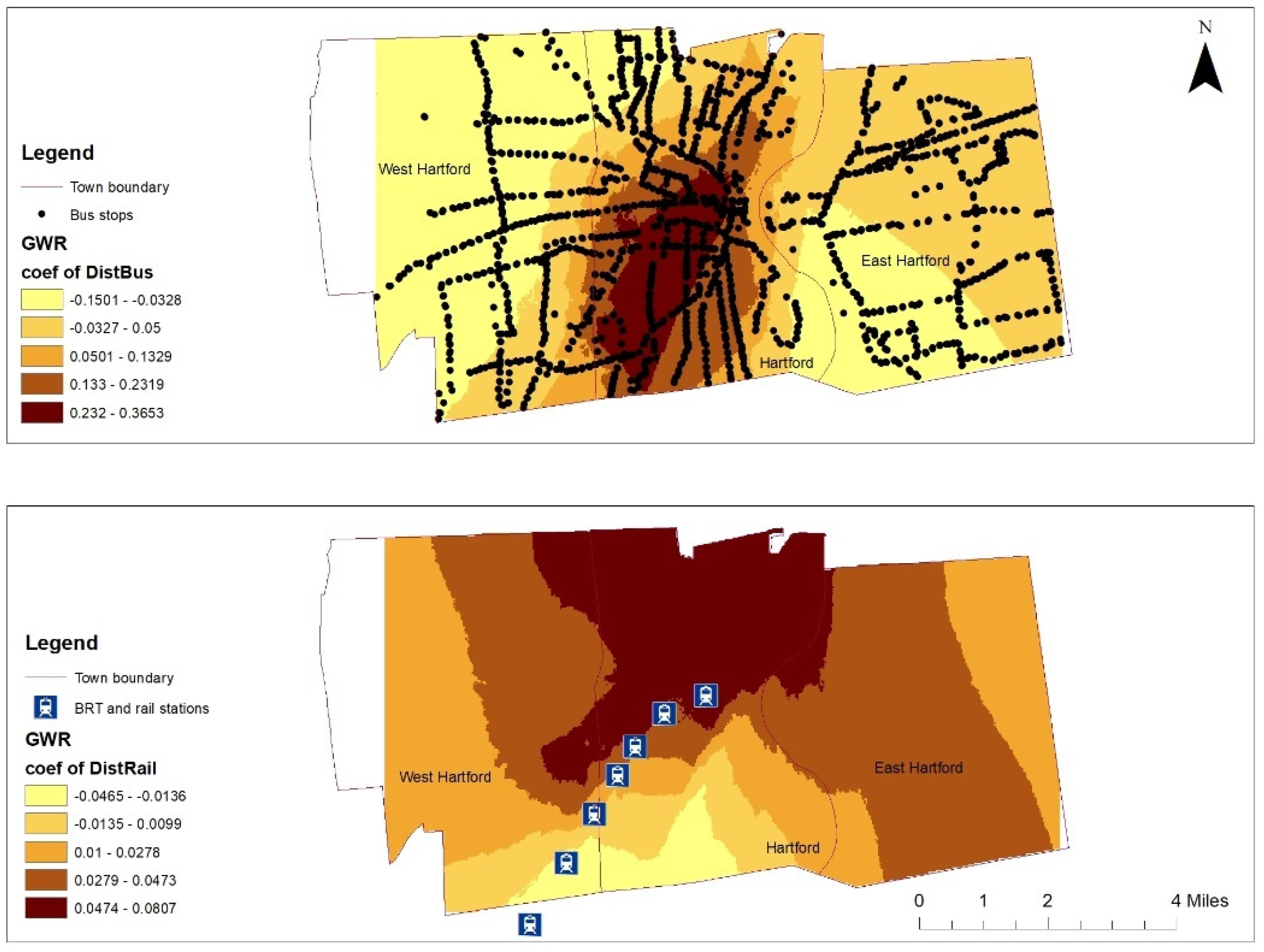

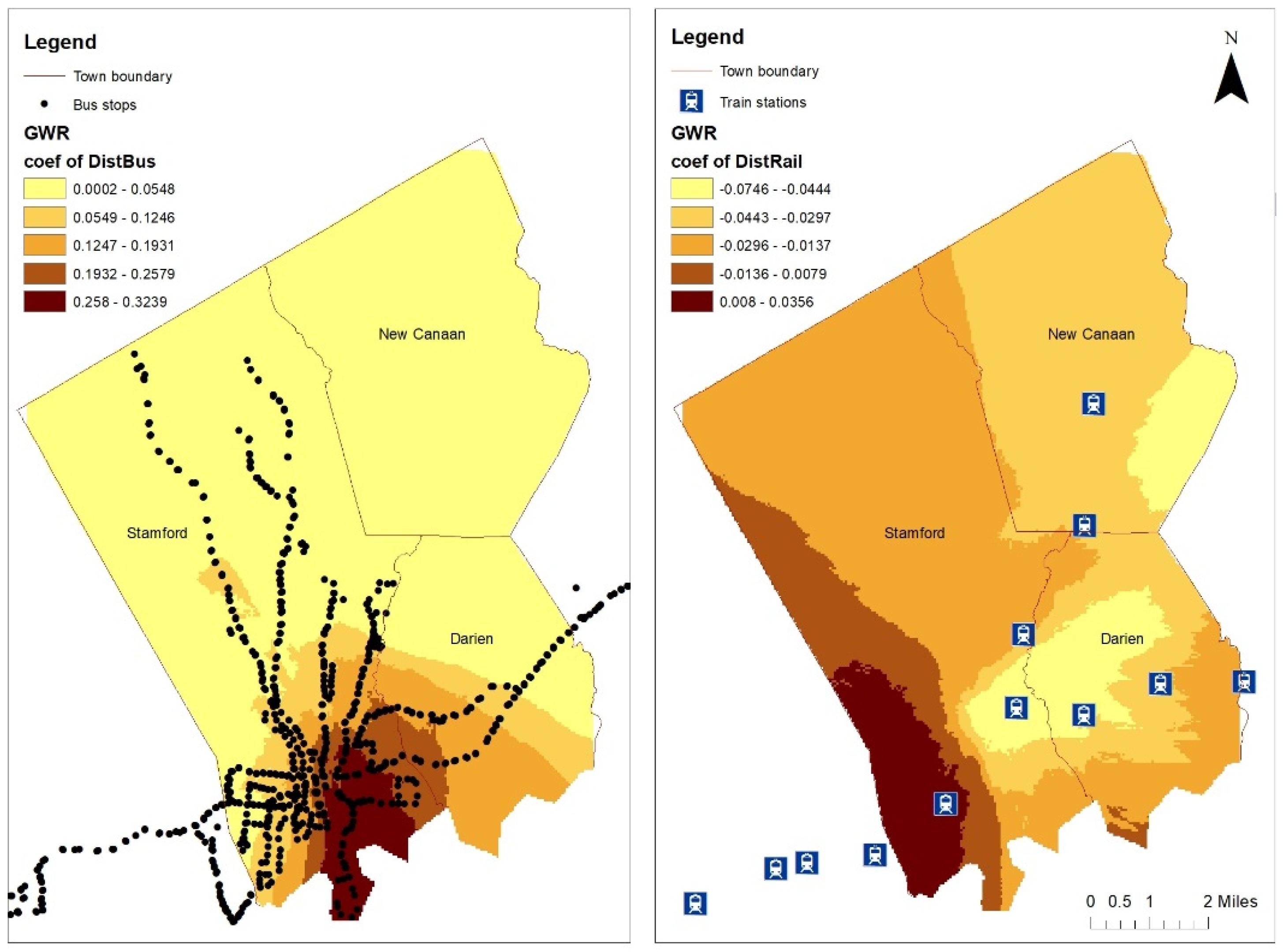

3.3. Local Regression Analysis—Geographically Weighted Regression

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Federal Transit Administration. Federal Transit Administration Annual Report on Funding Recommendations: Fiscal Year 2020. 2019. Available online: https://www.transit.dot.gov/funding/grant-programs/capital-investments/annual-report-funding-recommendations (accessed on 19 December 2019).

- FTA Office of Budget and Policy. 2017 National Transit Summary and Trends. 2018. Available online: https://www.transit.dot.gov/ntd/annual-national-transit-summaries-and-trends (accessed on 19 December 2019).

- Ransom, M.R. The effect of light rail transit service on nearby property values: Quasi-experimental evidence from Seattle. J. Transp. Land Use 2018, 11. [Google Scholar] [CrossRef]

- Cervero, R.; Duncan, M. Transit’s Value-Added Effects: Light and Commuter Rail Services and Commercial Land Values. Transp. Res. Rec. 2002, 1805, 8–15. [Google Scholar] [CrossRef]

- Xiao, Y. Hedonic Housing Price Theory Review. In Urban Morphology and Housing Market; Xiao, Y., Ed.; Springer: Singapore, 2017; pp. 11–40. [Google Scholar]

- D’Acci, L. Quality of urban area, distance from city centre, and housing value. Case study on real estate values in Turin. Cities 2019, 91, 71–92. [Google Scholar] [CrossRef]

- Zhong, H.; Li, W. Rail transit investment and property values: An old tale retold. Transp. Policy 2016, 51, 33–48. [Google Scholar] [CrossRef]

- Pilgram, C.A.; West, S.E. Fading premiums: The effect of light rail on residential property values in Minneapolis, Minnesota. Reg. Sci. Urban Econ. 2018, 69, 1–10. [Google Scholar] [CrossRef]

- Bowes, D.R.; Ihlanfeldt, K.R. Identifying the Impacts of Rail Transit Stations on Residential Property Values. J. Urban Econ. 2001, 50, 1–25. [Google Scholar] [CrossRef]

- Gallo, M. The Impact of Urban Transit Systems on Property Values: A Model and Some Evidences from the City of Naples. J. Adv. Transp. 2018. [Google Scholar] [CrossRef]

- Martínez, L.M.; Viegas, J.M. Effects of Transportation Accessibility on Residential Property Values: Hedonic Price Model in the Lisbon, Portugal, Metropolitan Area. Transp. Res. Rec. 2009, 2115, 127–137. [Google Scholar] [CrossRef]

- Li, Z. The impact of metro accessibility on residential property values: An empirical analysis. Res. Transp. Econ. 2018, 70, 52–56. [Google Scholar] [CrossRef]

- Pan, Q. The impacts of an urban light rail system on residential property values: A case study of the Houston METRORail transit line. Transp. Plann. Technol. 2013, 36, 145–169. [Google Scholar] [CrossRef]

- Pan, Q.; Pan, H.; Zhang, M.; Zhong, B. Effects of Rail Transit on Residential Property Values: Comparison Study on the rail transit Lines in Houston, texas, and Shanghai, China. Transp. Res. Rec. 2014, 2453, 118–127. [Google Scholar] [CrossRef]

- Perdomo Calvo, J.A. The effects of the bus rapid transit infrastructure on the property values in Colombia. Travel Behav. Soc. 2017, 6, 90–99. [Google Scholar] [CrossRef] [Green Version]

- Cervero, R.; Kang, C.D. Bus rapid transit impacts on land uses and land values in Seoul, Korea. Transp. Policy 2011, 18, 102–116. [Google Scholar] [CrossRef] [Green Version]

- Mulley, C.; Ma, L.; Clifton, G.; Yen, B.; Burke, M. Residential property value impacts of proximity to transport infrastructure: An investigation of bus rapid transit and heavy rail networks in Brisbane, Australia. J. Transp. Geogr. 2016, 54, 41–52. [Google Scholar] [CrossRef] [Green Version]

- Ma, L.; Ye, R.; Titheridge, H. Capitalization Effects of Rail Transit and Bus Rapid Transit on Residential Property Values in a Booming Economy: Evidence from Beijing. Transp. Res. Rec. 2014, 2451, 139–148. [Google Scholar] [CrossRef]

- Stokenberga, A. Does Bus Rapid Transit Influence Urban Land Development and Property Values: A Review of the Literature. Transp. Rev. 2014, 34, 276–296. [Google Scholar] [CrossRef]

- Shen, Q.; Xu, S.; Lin, J. Effects of bus transit-oriented development (BTOD) on single-family property value in Seattle metropolitan area. Urban Stud. 2018, 55, 2960–2979. [Google Scholar] [CrossRef]

- Wang, Y.; Potoglou, D.; Orford, S.; Gong, Y. Bus stop, property price and land value tax: A multilevel hedonic analysis with quantile calibration. Land Use Policy 2015, 42, 381–391. [Google Scholar] [CrossRef] [Green Version]

- Song, Y.; Knaap, G. New urbanism and housing values: A disaggregate assessment. J. Urban Econ. 2003, 54, 218–238. [Google Scholar] [CrossRef]

- Des Rosiers, F.; Thériault, M.; Voisin, M.; Dubé, J. Does an Improved Urban Bus Service Affect House Values? Int. J. Sustain. Transp. 2010, 4, 321–346. [Google Scholar] [CrossRef]

- Yang, L.; Zhou, J.; Shyr, O.F.; Huo, D. Does bus accessibility affect property prices? Cities 2019, 84, 56–65. [Google Scholar] [CrossRef]

- US Census Bureau, Top 10 Metro Areas by Percentage of Workers Who Commute by Public Transportation. Available online: https://www.census.gov/library/visualizations/interactive/public-transport.html (accessed on 28 November 2019).

- US Census Bureau, 2013–2017 American Community Survey 5-Year Estimates. Available online: https://www.census.gov/programs-surveys/acs (accessed on 17 December 2019).

- CTtransit, about Cttransit—Connecticut DOT-Owned Bus Service. Available online: https://www.cttransit.com/about (accessed on 6 December 2019).

- OpenStreetMap Contributors. Planet Dump Data File of 25 March 2019. Available online: https://planet.openstreetmap.org (accessed on 30 March 2019).

- Lancaster, K.J. A New Approach to Consumer Theory. J. Political Econ. 1966, 74, 132–157. [Google Scholar] [CrossRef]

- Hutcheson, G. Ordinary Least-Squares Regression. In The SAGE Dictionary of Quantitative Management Research; Moutinho, L., Hutcheson, G., Eds.; SAGE Publications: London, UK, 2011; pp. 224–228. [Google Scholar]

- Brunsdon, C.; Fotheringham, A.S.; Charlton, M.E. Geographically Weighted Regression: A Method for Exploring Spatial Nonstationarity. Geogr. Anal. 1996, 28, 281–298. [Google Scholar] [CrossRef]

- Fotheringham, A.S.; Charlton, M.E.; Brunsdon, C. Geographically Weighted Regression: A Natural Evolution of the Expansion Method for Spatial Data Analysis. Environ. Plann. A 1998, 30, 1905–1927. [Google Scholar] [CrossRef]

- Fotheringham, A.S.; Brunsdon, C.; Charlton, M. Geographically Weighted Regression: The Analysis of Spatially Varying Relationships; Wiley: Chichester, UK, 2002. [Google Scholar]

- US Census Bureau, QuickFacts Data Access Tool. Available online: https://www.census.gov/data/data-tools/quickfacts.html (accessed on 27 November 2020).

- Bertolaccini, K.; Lownes, N.E.; Mamun, S.A. Measuring and mapping transit opportunity: An expansion and application of the Transit Opportunity Index. J. Transp. Geogr. 2018, 71, 150–160. [Google Scholar] [CrossRef]

- Mamun, S.A.; Lownes, N.E.; Osleeb, J.P.; Bertolaccini, K. A method to define public transit opportunity space. J. Transp. Geogr. 2013, 28, 144–154. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Hartford Area | Stamford Area | |||||||

|---|---|---|---|---|---|---|---|---|

| Variables | Min | Mean | Max | Std. dev | Min | Mean | Max | Std. dev |

| Price (US Dollars) | 10,000 | 221,776 | 1,015,000 | 134,728 | 97,221 | 795,096 | 7,250,000 | 768,500 |

| log10 (Price) | 4 | 5.263 | 6.006 | 0.2852 | 4.988 | 5.773 | 6.860 | 0.3181 |

| Bedroom | 1 | 3.609 | 16 | 1.7688 | 1 | 3.292 | 19 | 1.4026 |

| Bathroom | 1 | 2.066 | 10.5 | 0.9026 | 1 | 2.669 | 13 | 1.4031 |

| Size (ft2) 1 | 450 | 2026 | 8778 | 1027 | 368 | 2690 | 11,615 | 1759 |

| Price per square foot ($) | 10.96 | 115.39 | 482.80 | 52.83 | 63.01 | 290.97 | 1809.78 | 131.44 |

| Age (years) | 0 | 72.45 | 326 | 30.42 | 0 | 54.11 | 318 | 32.58 |

| Median income ($) | 12,528 | 74,484 | 250,000 | 47,188 | 13,542 | 134,724 | 250,000 | 67,680 |

| Education attainment (%) | 0 | 37.12 | 90.79 | 27.23 | 2.44 | 60.50 | 95.49 | 19.99 |

| Distance to bus stop (mi) | 0.0001 | 0.1912 | 2.2795 | 0.2132 | 0.0001 | 0.8189 | 7.6793 | 1.3255 |

| Distance to rail/BRT (mi) | 0.0846 | 2.8524 | 7.3078 | 1.6967 | 0.0422 | 1.8164 | 8.8059 | 1.5181 |

| Hartford Area | Stamford Area | |

|---|---|---|

| Moran’s Index | 0.422165 | 0.431365 |

| Expected Index | −0.000420 | −0.000452 |

| Variance | 0.000089 | 0.000151 |

| z-score | 44.812825 | 35.183734 |

| p-value | 0.000000 | 0.000000 |

| Hartford Area 1 | Stamford Area 2 | |||||

|---|---|---|---|---|---|---|

| Variables | Coef. | t | VIF | Coef. | t | VIF |

| Intercept | 4.720336 | 282.0682 *** | ------ | 5.137391 | 381.7693 *** | ------ |

| Bedroom | 0.012695 | 3.5708 *** | 2.910574 | 0.045334 | 12.5285 *** | 2.7107 |

| Bathroom | 0.033340 | 4.7626 *** | 2.938495 | 0.059512 | 12.8142 *** | 4.468890 |

| Size (ft2) | 0.000087 | 11.9101 *** | 4.143778 | 0.000045 | 11.6787 *** | 4.751940 |

| Age (years) | −0.000389 | −2.7475 *** | 1.368485 | −0.000299 | −2.9569 *** | 3.848668 |

| Median income ($10,000) | 0.003194 | 2.1561 *** | 3.712073 | 0.013539 | 13.9894 *** | 2.791030 |

| Education attainment (%) | 0.005742 | 22.2352 *** | 3.641046 | 0.001828 | 7.0958 *** | 1.138478 |

| Distance to bus stop (mi) | −0.042203 | −2.0813 *** | 1.376087 | 0.013539 | 4.9088 *** | 1.406633 |

| Distance to rail/BRT (mi) | 0.018221 | 7.1698 *** | 1.368409 | −0.036377 | −15.4941 *** | 1.336960 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, B.; Li, W.; Lownes, N.; Zhang, C. Estimating the Impacts of Proximity to Public Transportation on Residential Property Values: An Empirical Analysis for Hartford and Stamford Areas, Connecticut. ISPRS Int. J. Geo-Inf. 2021, 10, 44. https://0-doi-org.brum.beds.ac.uk/10.3390/ijgi10020044

Zhang B, Li W, Lownes N, Zhang C. Estimating the Impacts of Proximity to Public Transportation on Residential Property Values: An Empirical Analysis for Hartford and Stamford Areas, Connecticut. ISPRS International Journal of Geo-Information. 2021; 10(2):44. https://0-doi-org.brum.beds.ac.uk/10.3390/ijgi10020044

Chicago/Turabian StyleZhang, Bo, Weidong Li, Nicholas Lownes, and Chuanrong Zhang. 2021. "Estimating the Impacts of Proximity to Public Transportation on Residential Property Values: An Empirical Analysis for Hartford and Stamford Areas, Connecticut" ISPRS International Journal of Geo-Information 10, no. 2: 44. https://0-doi-org.brum.beds.ac.uk/10.3390/ijgi10020044