An Empirical Investigation on Determinants of Sustainable Economic Growth. Lessons from Central and Eastern European Countries

Abstract

:1. Introduction

2. Literature Review

2.1. Brief Taxonomy Regarding the Impact of Financial Direct Investments on Economic Growth

2.2. Brief Overview Regarding the Impact of the Banking Sector on Economic Development

2.3. Brief Overview Regarding the Impact of International Trade, Human Capital, Shadow Economy and Other Factors on Economic Growth

2.4. Brief Overview Regarding the Impact of Energy and Technology Transfer on Economic Growth

3. Method and Results

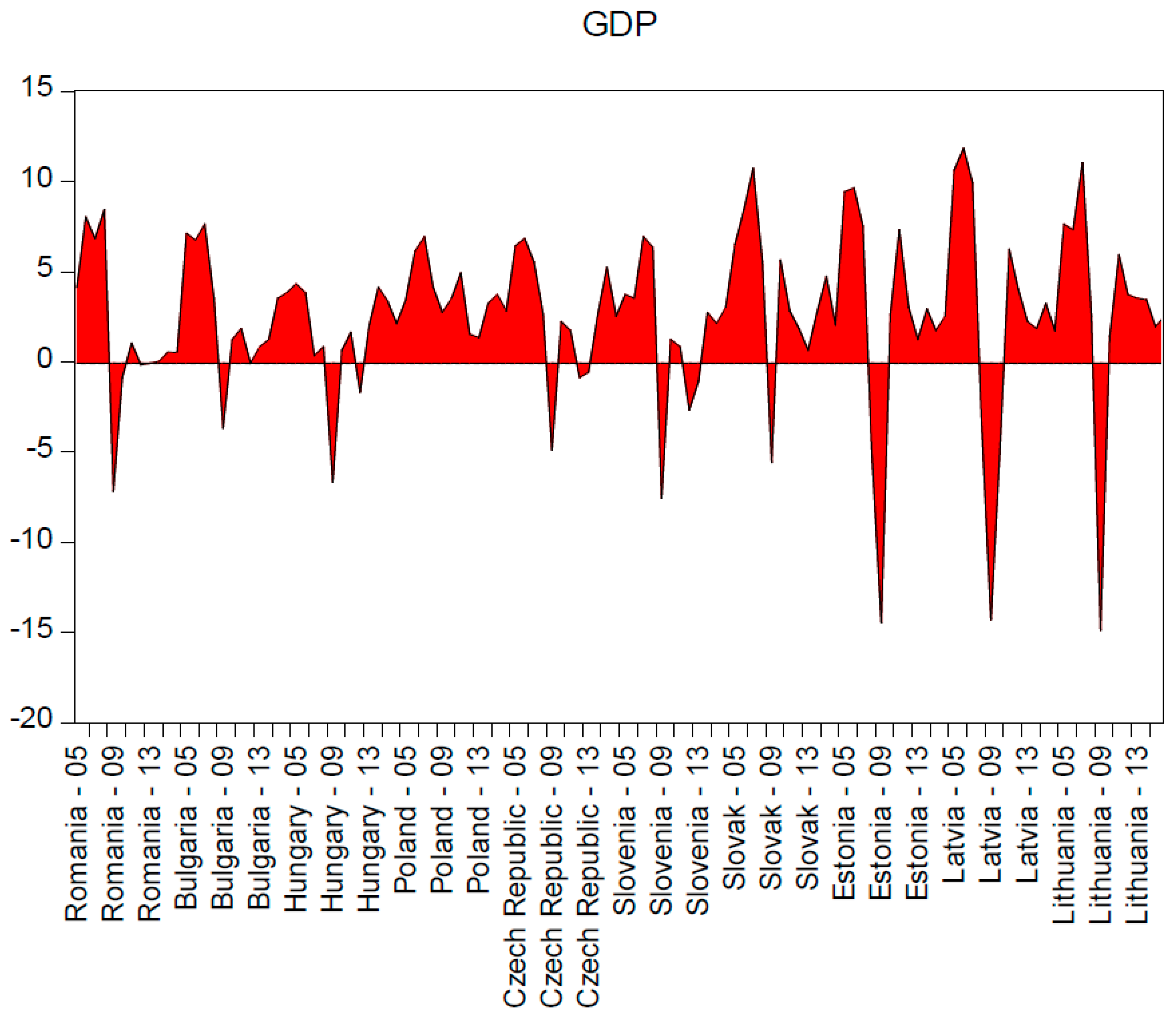

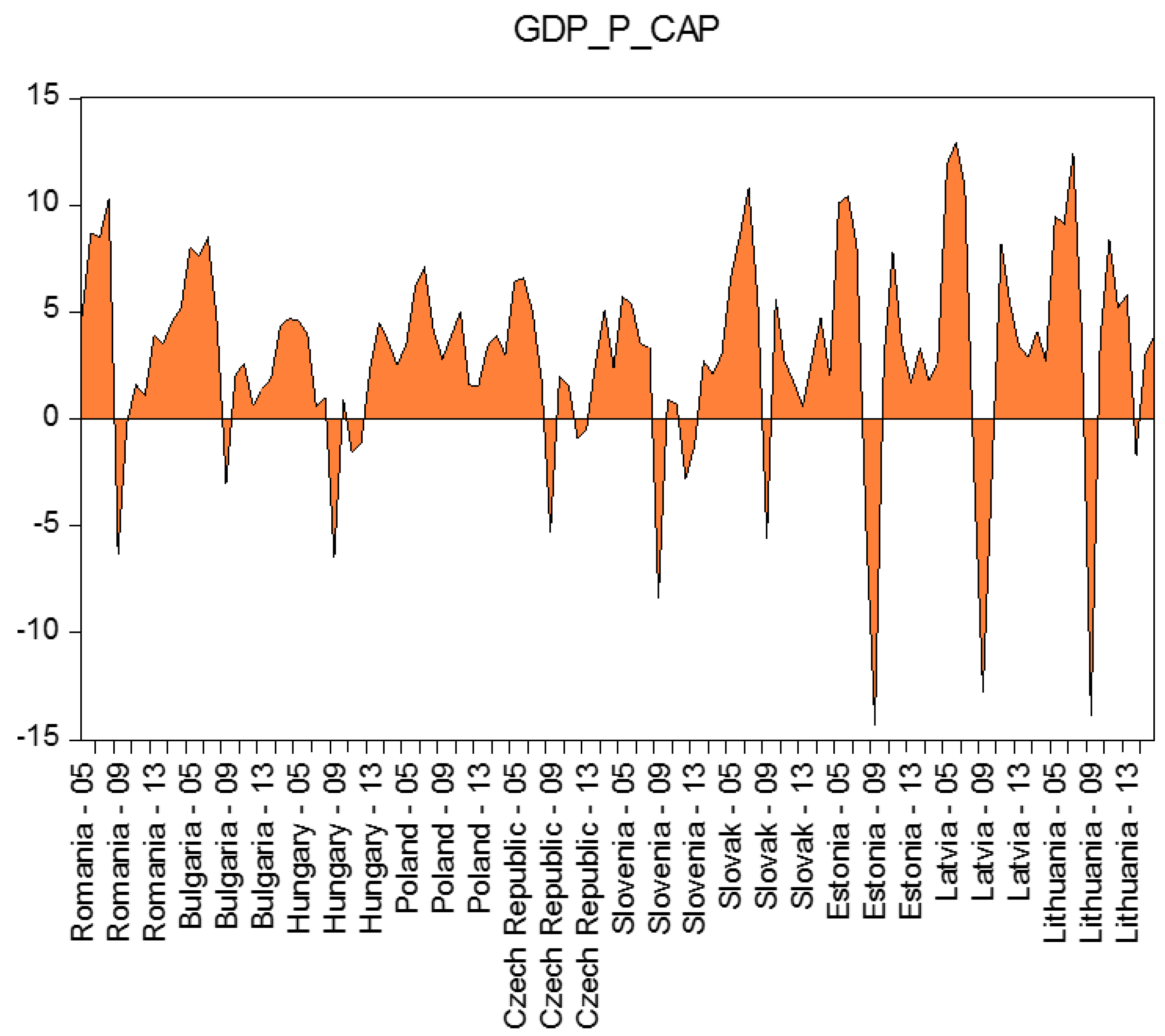

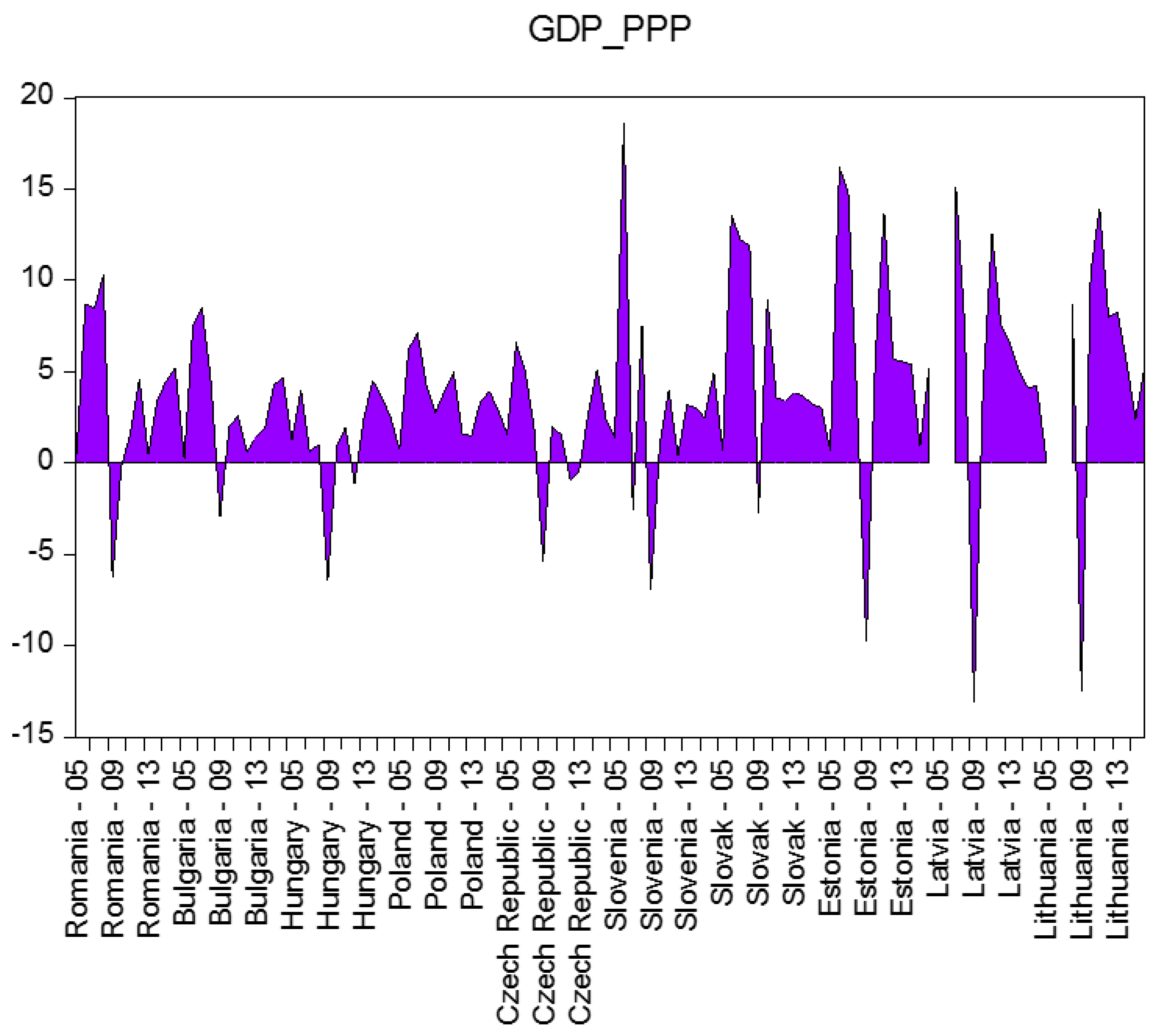

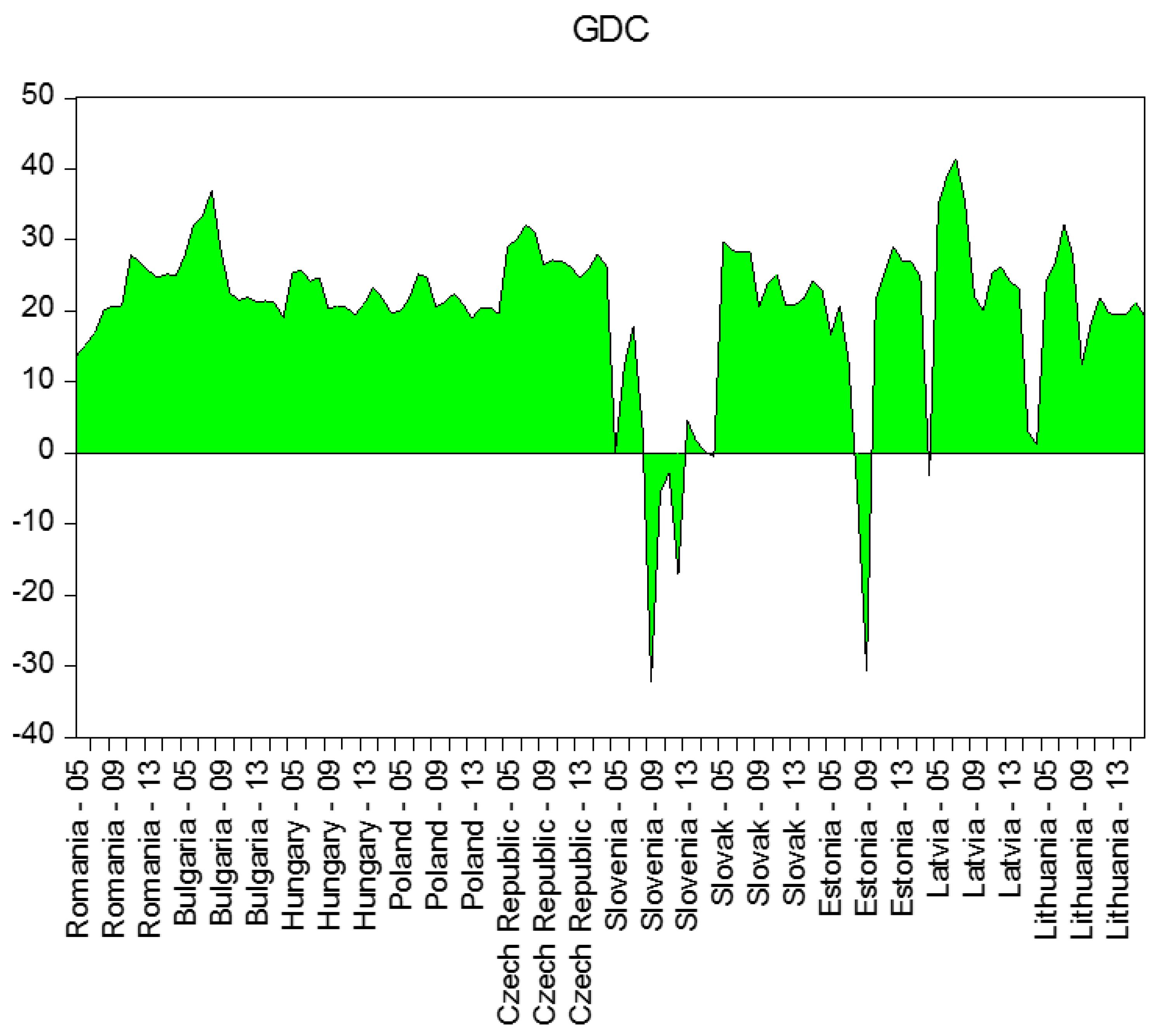

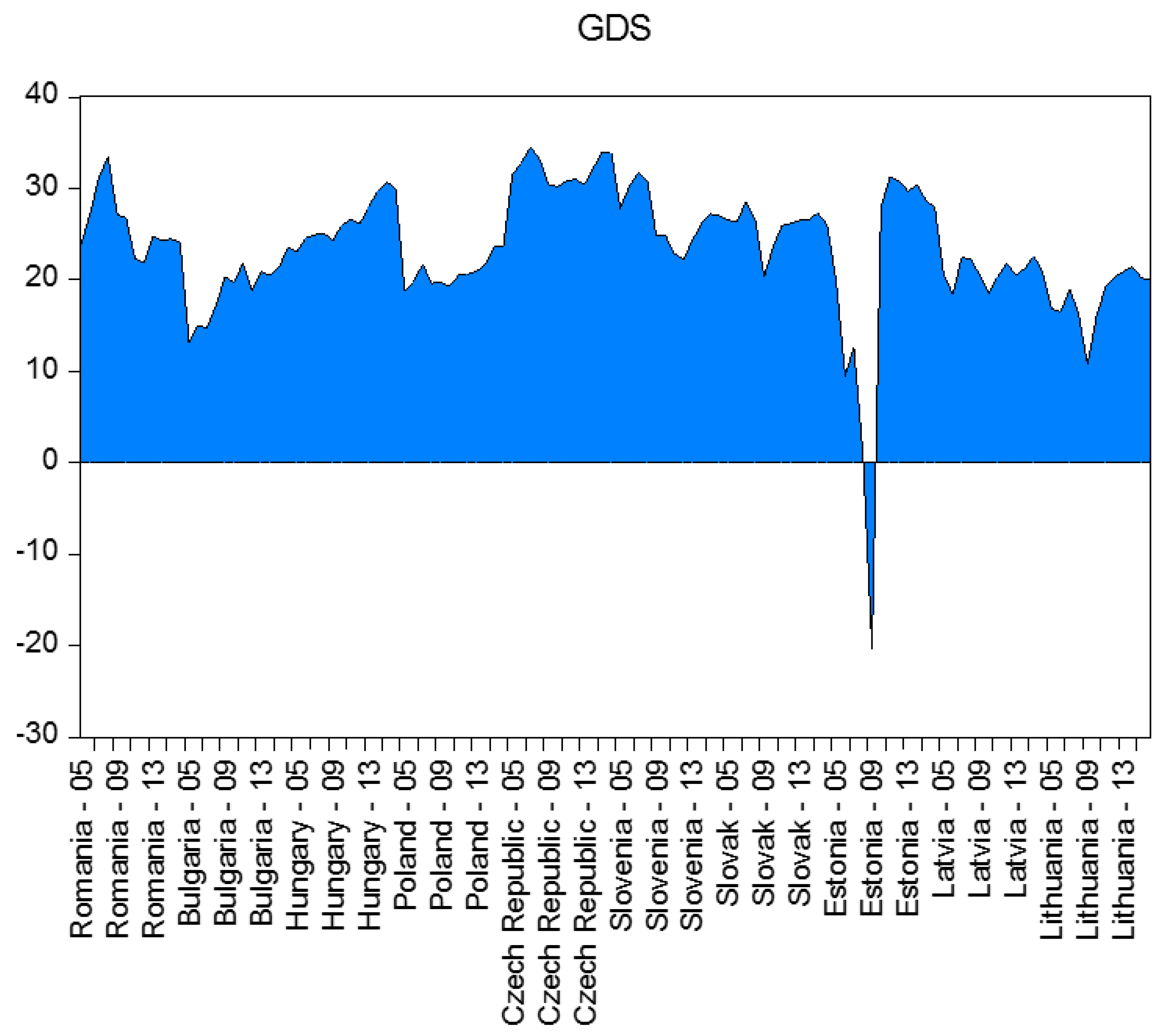

3.1. Analysis of Central Tendency and Variation

3.2. Econometric Models

- a0 represents the intercept;

- ai represents the coefficient parameter, taking values from 1 to 4;

- X represents the independent variable;

- i refers to the country’s activity, taking values from 1 to 10;

- t refers to the analyzed time frame (2005–2016), taking values from 1 to 12;

- represents the fixed effects intended to control for time-invariant country-specific factors;

- represents the fixed effects that control for common shocks (for instance, the global financial crisis);

- is the error term.

3.3. Discussion

3.4. Unit Root and Stationarity, Panel Fully Modified Least Squares (FMOLS) and Dynamic Ordinary Least Squares Methods (DOLS)

3.4.1. Unit Root and Stationarity

3.4.2. Pooled OLS, Fixed Effect, Random Effect, and Hausman Test

3.4.3. Panel Fully Modified Least Squares (FMOLS)

3.4.4. VECM and VAR Analyses

VECM

Wald Test

3.5. Johansen Cointegration Test

3.6. Discussion

4. Conclusions and Policy Implications

- (a)

- Transition to free trade and market economy;

- (b)

- Habit of controlling expenditures, inherited from the previously controlled economy;

- (c)

- Uncertainty of the free market and European Union.

- FDI was neither a blessing nor a curse for national economies;

- The economic crisis did not attract FDI;

- An economy with a sound currency would attract FDI;

- Without incentives such as those given by authorities from Bulgaria, Croatia and Romania, FDI would not enter national economies.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| GDP | gross domestic product |

| GDP_P_CAP | gross domestic product per capita income |

| GDP_PPP | gross purchasing power parity |

| EXPORTS | total exports of goods |

| IMPORTS | total imports of goods |

| FDI_INF | financial direct investment inflow |

| FDI_OUTF | financial direct investment outflow |

| GDS | gross domestic savings |

| GDC | gross domestic capital |

| OECD | Organisation for Economic Co-operation and Development |

| BRICS | Association of five emerging economies: Brazil, Russia, India, China, South Africa |

References

- Andrašic, Jelena, Branimir Vera Mirovic, and Nada Milenkovic. 2020. Investment models in transition process—Case study of countries from region. Ekonomski Pregled 71: 67–85. [Google Scholar] [CrossRef] [Green Version]

- Arain, Hira, Liyan Han, Arshian Sharif, and Muhammad Saeed Meo. 2020. Investigating the effect of inbound tourism on FDI: The importance of quantile estimations. Tourism Economics 26: 682–703. [Google Scholar] [CrossRef]

- Armeanu, Daniel Stefan, Georgeta Vintila, and Stefan Cristian Gherghina. 2018. Empirical study towards the drivers of sustainable economic growth in EU-28 Countries. Sustainability 10: 4. [Google Scholar] [CrossRef] [Green Version]

- Auzairy, Nour Azryani, Kevin Kek Wai Hin, Pang Hui Xian, and Yong Lee Teng. 2020. The impact of China’s investment on Malaysia. Iranian Journal of Management Studies 13: 51–68. [Google Scholar] [CrossRef]

- Balasubramanyam, V. N., M. Salisu, and David Sapsford. 1996. Foreign direct investment and growth in EP and IS Countries. The Economic Journal 106: 92–105. [Google Scholar] [CrossRef]

- Banga, Rashmi. 2006. The export-diversifying impact of Japanese and US foreign direct investments in the Indian manufacturing sector. Journal of International Business Studies 37: 558–68. [Google Scholar] [CrossRef]

- Barry, Frank, and Robert E. Lipsey. 2002. EU accession and prospective FDI flows to CEE countries: A view from Ireland. In Foreign Direct Investment in the Real and Financial Sector of Industrial Countries. Edited by Heinz Herrmann and Robert Lipsey. Berlin: Springer, pp. 187–213. [Google Scholar]

- Batrancea, Larissa-Margareta, Ramona-Anca Nichita, and Ioan Batrancea. 2012. Understanding the determinants of tax compliance behavior as a prerequisite for increasing public levies. The USV Annals of Economics and Public Administration 12: 201–10. [Google Scholar]

- Batrancea, Larissa, Anca Nichita, Ioan Batrancea, and Lucian Gaban. 2018. The strength of the relationship between shadow economy and corruption: Evidence from a worldwide country-sample. Social Indicators Research 138: 1119–43. [Google Scholar] [CrossRef]

- Batrancea, Larissa, Anca Nichita, Jerome Olsen, Christoph Kogler, Erich Kirchler, Erik Hoelzl, Avi Weiss, Benno Torgler, Jonas Fooken, Joanne Fuller, and et al. 2019. Trust and power as determinants of tax compliance across 44 nations. Journal of Economic Psychology 74: 102191. [Google Scholar] [CrossRef]

- Bayar, Yilmaz, Rita Remeikiene, Armenia Androniceanu, Ligita Gaspareniene, and Ramunas Jucevicius. 2020. The shadow economy, human development and foreign direct investment inflows. Journal of Competitiveness 12: 5–21. [Google Scholar] [CrossRef]

- Blonigen, Bruce A. 2005. A review of the empirical determinants of FDI. Atlantic Economic Journal 33: 383–403. [Google Scholar] [CrossRef]

- Blonigen, Bruce A., and Jemery Piger. 2014. Determinants of foreign direct investment. Canadian Journal of Economics 47: 775–812. [Google Scholar] [CrossRef] [Green Version]

- Bruns, Stephan B., and John P. A. Ioannidis. 2020. Determinants of economic growth: Different time different answer? Journal of Macroeconomics 63. [Google Scholar] [CrossRef]

- Cao, Wenming, Shuanglian Chen, and Zimei Huang. 2020. Does foreign direct investment impact energy intensity? Evidence from developing countries. Mathematical Problems in Engineering. [Google Scholar] [CrossRef] [Green Version]

- Chandio, Abbas Ali, Yuansheng Jiang, Fayyaz Ahmad, Waqar Akram, Sajjad Ali, and Abdul Rauf. 2020. Investigating the long-run interaction between electricity consumption, foreign investment, and economic progress in Pakistan: Evidence from VECM approach. Environmental Science and Pollution Research. [Google Scholar] [CrossRef]

- Chetthamrongchai, Paitoon, Kittisak Jermsittiparsert, and Sakapas Saengchai. 2020. How the nexus among the free trade, institutional quality and economic growth affect the trade from ASEAN countries. Entrepreneurship and Sustainability Issues 7: 2079–94. [Google Scholar] [CrossRef] [Green Version]

- Chowdhury, Abdur, and George Mavrotas. 2006. FDI and growth: What causes what? The World Economy 29: 9–19. [Google Scholar] [CrossRef]

- Cieślik, Andrzej. 2019. Determinants of foreign direct investment from EU-15 countries in Poland. Central European Economic Journal 6: 39–52. [Google Scholar] [CrossRef] [Green Version]

- Contessi, Silvio, and Ariel Weinberger. 2009. Foreign direct investment, productivity and country growth: An overview. Federal Reserve Bank of St. Louis Review 91: 61–78. [Google Scholar] [CrossRef] [Green Version]

- Durairaj, Kumarasamy. 2011. Foreign direct investment, export, and economic growth in India: An application of ADRL Model. Asian-African Journal of Economics and Econometrics 10: 245–59. [Google Scholar]

- Eluwole, Kayode Kolawole, Seyi Saint Akadiri, and Andrew Adewale Alola. 2019. Does the interaction between growth determinants a drive for global environmental sustainability? Evidence from world top 10 pollutant emissions countries. Science of the Total Environment 705. [Google Scholar] [CrossRef]

- Falk, Martin, and Mariya Hake. 2008. A Panel Data Analysis on FDI and Exports; FIW Research Reports. Vienna: FIW-Research Centre International Economics.

- Gamidullaeva, Leyla A., Sergey M. Vasin, and Nicholas Wise. 2020. Increasing small-and medium-enterprise contribution to local and regional economic growth by assessing the institutional environment. Journal of Small Business and Enterprise Development 27: 259–80. [Google Scholar] [CrossRef]

- Glaiser, Keith W., and Hristina Atanasova. 1998. Foreign direct investment in Bulgaria: Patterns and prospects. European Business Review 98: 122–34. [Google Scholar] [CrossRef]

- Govori, Florije, and Amant Fejzullahu. 2020. External financial flows and GDP growth. Journal of Developing Societies 36: 57–76. [Google Scholar] [CrossRef]

- Gregory, Paul R., and Robert C. Stuart. 1997. Comparative Economic Systems. Boston: HoughtonMifflin. [Google Scholar]

- Gries, Thomas, and Rainer Grundmann. 2020. Modern sector development: The role of exports and institutions in developing countries. Review of Development Economics 24: 644–67. [Google Scholar] [CrossRef]

- Hertenstein, Peter, Dylan Sutherland, and John Anderson. 2017. Internationalization within networks: Exploring the relationship between inward and outward FDI in China’s auto components industry. Asia Pacific Journal of Management 34: 69–96. [Google Scholar] [CrossRef] [Green Version]

- Hoeck, André, Christian Klein, Alexander Landau, and Bernhard Zwergel. 2020. The effect of environmental sustainability on credit risk. Journal of Asset Management 21: 85–93. [Google Scholar] [CrossRef]

- Hsiao, Frank S. T., and Mei-Chu W. Hsiao. 2006. FDI, exports, and GDP in East and Southeast Asia–Panel data versus time-series causality analyses. Journal of Asian Economics 17: 1082–106. [Google Scholar] [CrossRef]

- Justin, Paul, and Maria M. Feliciano-Cestero. 2020. Five decades of research on foreign direct investment by MNEs: An overview and research agenda. Journal of Business Research. [Google Scholar] [CrossRef]

- Katircioglu, Salih, Nesrin Ozatac, and Nigar Taspinar. 2020. The role of oil prices, growth and inflation in bank profitability. Service Industries Journal 40: 565–84. [Google Scholar] [CrossRef]

- Kleineick, Jonas, Andrea Ascani, and Martijn Smit. 2020. Multinational investments across Europe: A multilevel analysis. Review of Regional Research-Jahrbuch fur Regionalwissenschaft 40: 67–105. [Google Scholar] [CrossRef] [Green Version]

- Kogler, Christoph, Larissa Batrancea, Anca Nichita, Jozsef Pantya, Alexis Belianin, and Erich Kirchler. 2013. Trust and power as determinants of tax compliance: Testing the assumptions of the slippery slope framework in Austria, Hungary, Romanian and Russia. Journal of Economic Psychology 34: 169–80. [Google Scholar] [CrossRef]

- Konstandina, Mamica Skendei, and Geoffrey Gatharia Gachino. 2020. International technology transfer: Evidence on foreign direct investment in Albania. Journal of Economic Studies 47: 286–306. [Google Scholar] [CrossRef]

- Lenka, Sanjaya Kumar, and Pritee Sharma. 2014. FDI as a main determinant of economic growth: A panel data analysis. Annual Research Journal of SCMS 1: 84–97. [Google Scholar]

- Li, Xiaoying, and Xiaming Liu. 2004. Foreign direct investment and economic growth: An increasingly endogenous relationship. World Development 33: 393–407. [Google Scholar] [CrossRef]

- Liu, Xiaming, Chengang Wang, and Yingqi Wei. 2001. Causal links between foreign direct investment and trade in China. China Economic Review 12: 190–202. [Google Scholar] [CrossRef]

- MacKinnon, James, Alfred Haug, and Leo Michelis. 1999. Numerical distribution functions of likelihood ratio tests for cointegration. Journal of Applied Econometrics 14: 563–77. [Google Scholar] [CrossRef]

- Marfatia, Hardik. 2020. Evaluating the forecasting power of foreign country’s income growth: A global analysis. Journal of Economic Studies. [Google Scholar] [CrossRef]

- Maryam, Javeria, and Ashok Mittal. 2019. Foreign direct investment into BRICS: An empirical analysis. Transnational Corporations Review 12: 1–9. [Google Scholar] [CrossRef]

- Melnyk, Leonid, Oleksandr Kubatko, and Sergiy Pysarenko. 2014. The impact of foreign direct investment on economic growth: Case of post communism transition economies. Problems and Perspectives in Management 12: 17–24. [Google Scholar]

- Mutize, Misheck, and McBride Peter Nkhalamba. 2020. A comparative study of economic growth as a key determinant of sovereign credit ratings in Africa. International Journal of Emerging Markets. [Google Scholar] [CrossRef]

- Nam, Jouahn, Joseph Bon Sesay, Kevin Wynne, and Ge Zhang. 2020. Financial efficiency and accounting quality: The impact of institutional micro-factors on FDI. Journal of Policy Modeling 42: 451–65. [Google Scholar] [CrossRef]

- Naveed, Amjad, and Ghulam Shabbir. 2006. Trade openness, FDI and economic growth: A panel study. Pakistan Economic Social Review 44: 137–54. [Google Scholar]

- Nguyen, Thong Trung, Thu Anh Thu Pham, and Huong Thi Xuan Tram. 2020. Role of information and communication technologies and innovation in driving carbon emissions and economic growth in selected G-20 countries. Journal of Environmental Management 261. [Google Scholar] [CrossRef]

- Osinska, Magdalena, Tadeusz Kufel, Marcin Blazejowski, and Pawel Kufel. 2020. Modeling mechanism of economic growth using threshold autoregression models. Empirical Economics 58: 1381–430. [Google Scholar] [CrossRef] [Green Version]

- Paul, Justin, and Gurmeet Singh. 2017. The 45 years of foreign direct investment research: Approaches, advances and analytical areas. The World Economy 40: 2512–27. [Google Scholar] [CrossRef]

- Pegkas, Panagiotis, Christos Staikouras, and Constantinos Tsamadias. 2020. On the determinants of economic growth: Empirical evidence from the Eurozone countries. International Area Studies Review. [Google Scholar] [CrossRef]

- Pilipovic, Ozren, Meta Ahtik, and Nenad Rancic. 2015. FDI inflows in time of crisis – Panel data analysis of FDI inflows to the selected EU member states. Interdisciplinary Management Research 11: 433–66. [Google Scholar]

- Pournarakis, Mike. 2001. Development integration and FDIs in the Balkans. Paper presented at the International Conference on Current Issues for Transition Economies in the Broad Balkan Region, Xanthi, Greek, December. [Google Scholar]

- Pournarakis, Mike, and Nikos C. Varsakelis. 2002. Institutions, internationalization and FDI: The case of economies in Transition. Transnational Corporations 13: 77–94. [Google Scholar]

- Ray, Sarbapriya. 2012. Impact of foreign direct investment on economic growth in India: A cointegration analysis. Advances in Information Technology and Management 2: 164–72. [Google Scholar]

- Reurink, Arjan, and Javier Garcia-Bernardo. 2020. Competing for capitals: The great fragmentation of the firm and varieties of FDI attraction profiles in the European Union. Review of International Political Economy. [Google Scholar] [CrossRef] [Green Version]

- Sengenberger, Werner. 2002. Foreign Direct Investment, Industrial Restructuring and Local Labor Markets in the Transition Economies of Central and Eastern Europe: Issues for Debate. Geneva: United Nations Economic Commission for Europe. [Google Scholar]

- Seraj, Mehdi, Pejman Bahramian, Abdulkareem Alhassan, and Rasool Dehghansadeh Shahabad. 2020. The validity of Rodrik’s conclusion on real exchange rate and economic growth: Factor priority evidence from feature selection approach. Palgrave Communications 6. [Google Scholar] [CrossRef]

- Seyoum, Belay, and Andrea Camargo. 2020. State fragility and foreign direct investment: The mediating roles of human flight and economic decline. Thunderbird International Business Review. [Google Scholar] [CrossRef]

- Sharma, Rajesh, and Pradeep Kautish. 2020. Examining the nonlinear impact of selected macroeconomic determinants on FDI inflows in India. Journal of Asia Business Studies. [Google Scholar] [CrossRef]

- Svejnar, Jan. 2002. Transition economies: Performance and challenges. Journal of Economic Perspectives 16: 3–28. [Google Scholar] [CrossRef] [Green Version]

- Szkorupova, Zuzana. 2014. A causal relationship between foreign direct investment, economic growth and export for Slovakia. Procedia Economics and Finance 15: 123–28. [Google Scholar] [CrossRef] [Green Version]

- te Velde, Dirk Willelm. 2001. Policies towards Foreign Direct Investment in Developing Countries: Emerging Best-Practices and Outstanding Issues. London: Overseas Development Institute. [Google Scholar]

- Tolmacheva, Svetlana V. 2020. International migration & economic development: The case of EU countries. Amazonia Investiga 9: 104–15. [Google Scholar] [CrossRef]

- Tondel, Line. 2001. Foreign Direct Investment during Transition: Determinants and Patterns in Central and Eastern Europe and the Former Soviet Union. Working Paper WP 2001: 9, Chr. Bergen: Michelsen Institute. [Google Scholar]

- Topcu, Mert, and Can Tansel Tugcu. 2020. The impact of renewable energy consumption on income inequality: Evidence from developed countries. Renewable Energy 151: 1134–40. [Google Scholar] [CrossRef]

- Tran, Son, and Lien Nguyen. 2020. Financial development, business cycle and bank risk in Southeast Asian countries. Journal of Asian Finance Economics and Business 7: 127–35. [Google Scholar] [CrossRef]

- Tuselmann, Heinz. 1999. German direct foreign investment in Central and Eastern Europe: Relocation of Germany industry? European Business Review 99: 359–67. [Google Scholar] [CrossRef]

- Uddin, Akther, Hakim Ali, and Mansur Masih. 2020. Institutions, human capital and economic growth in developing countries. Studies in Economics and Finance. [Google Scholar] [CrossRef]

- Wong, David W. H., Harry F. Lee, Simon X. Zhao, and Qing Pei. 2020. Region-specific determinants of the foreign direct investment in China. Geographical Research 58: 126–40. [Google Scholar] [CrossRef]

- Zhang, Yilin, Zhenyu Cheng, and Qingsong He. 2020. Time lag analysis of FDI spillover effect Evidence from the Belt and Road developing countries introducing China’s direct investment. International Journal of Emerging Markets 15: 629–50. [Google Scholar] [CrossRef]

| 1 | The leptokurtic distribution shows a much higher peak around the mean value, and fat tails, or higher densities of values at the extreme ends of the probability curve. The platykurtic distribution shows the exact opposite. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

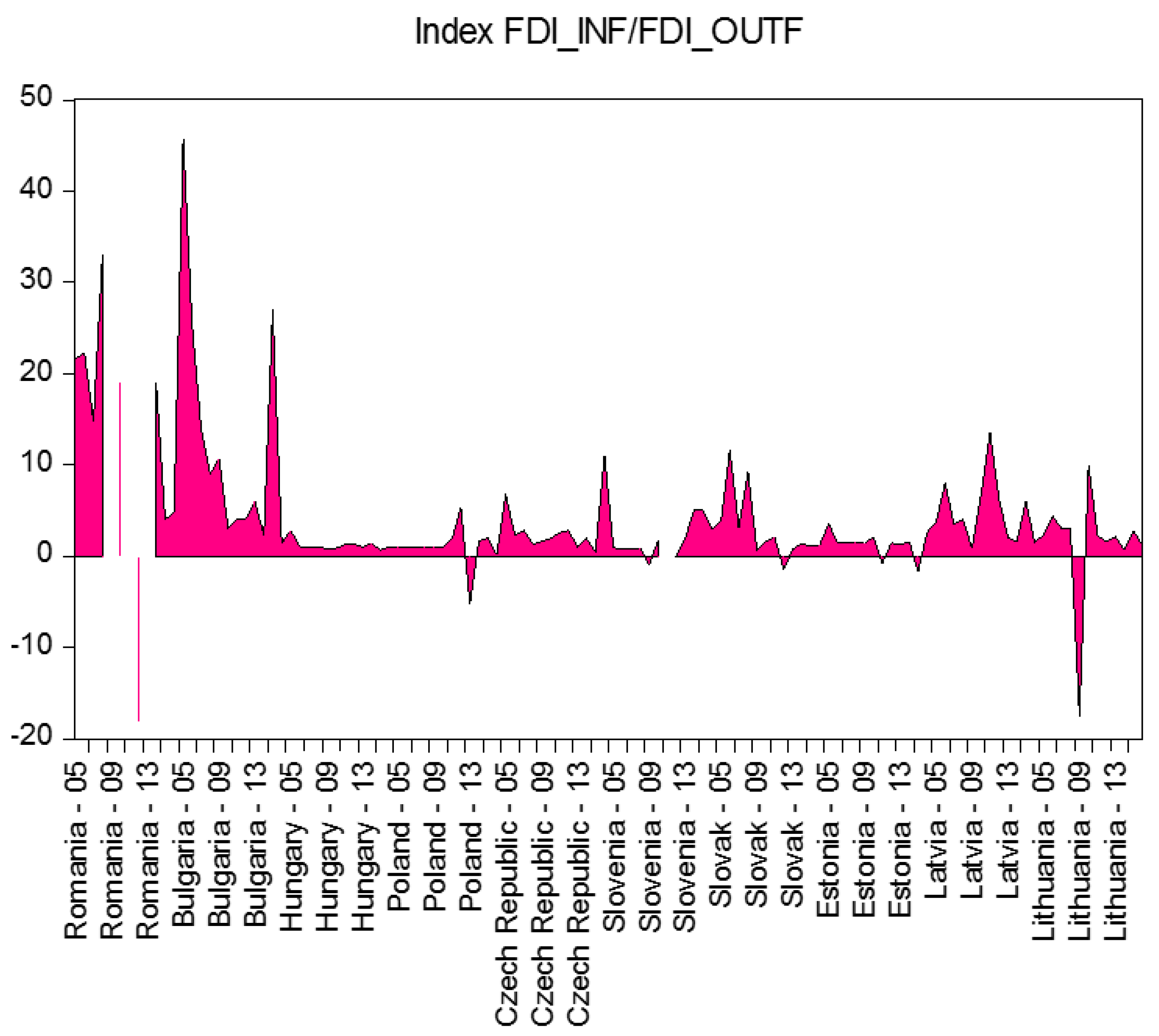

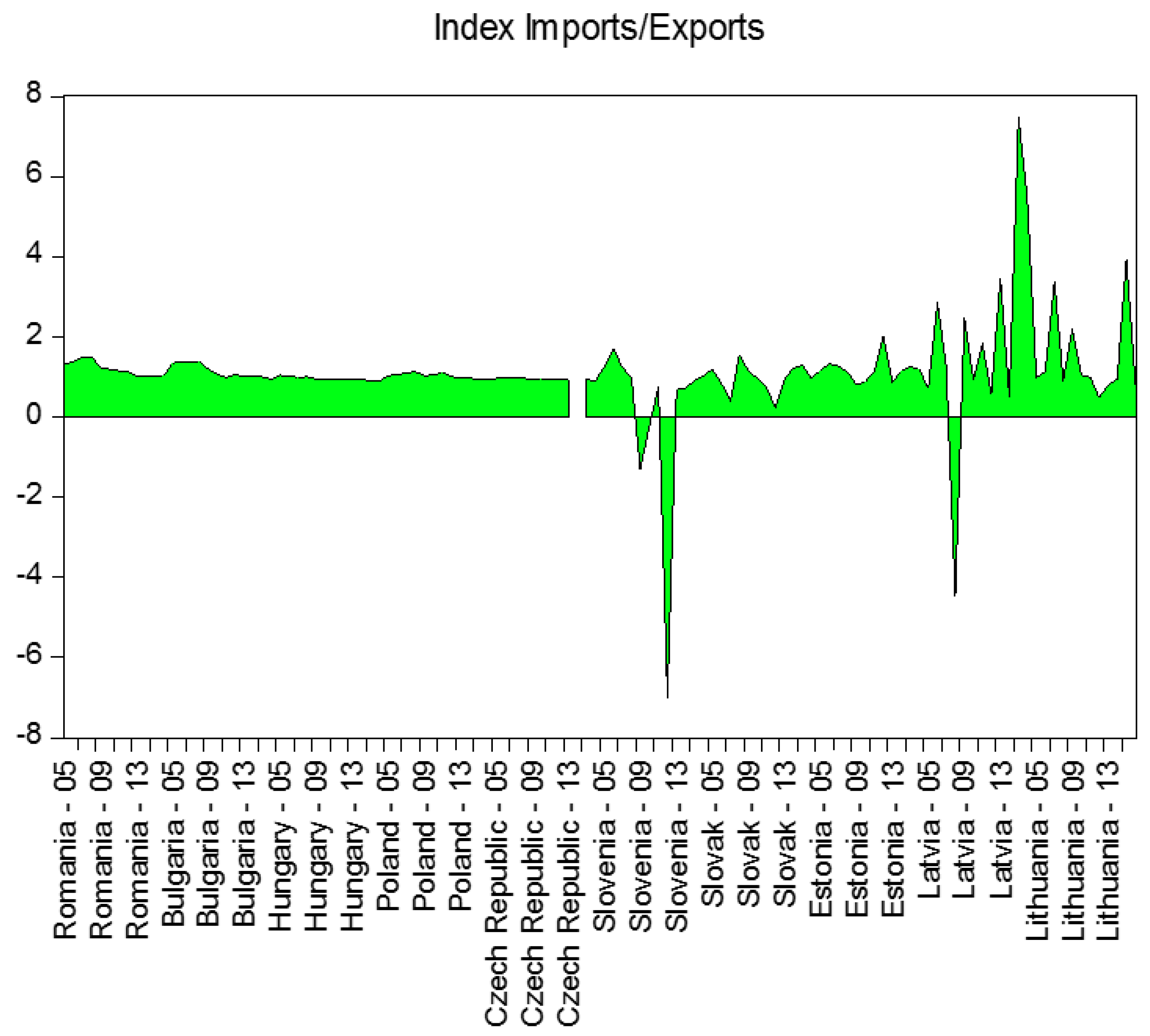

| Variable | GDP | GDP_P_CAP | GDP_PPP | GDS | GDC | EXPORTS | IMPORTS | FDI_INF | FDI_OUTF |

|---|---|---|---|---|---|---|---|---|---|

| Mean | 2.595000 | 3.033333 | 3.701131 | 23.49167 | 20.23833 | 33.37000 | 32.98655 | 5.568333 | 2.817500 |

| Median | 2.800000 | 3.350000 | 3.514668 | 23.75000 | 21.85000 | 28.95000 | 35.70000 | 3.700000 | 1.350000 |

| Maximum | 11.90000 | 12.90000 | 18.56318 | 34.50000 | 41.40000 | 90.20000 | 81.40000 | 54.60000 | 52.70000 |

| Minimum | −14.80000 | −14.30000 | −13.05911 | –20.30000 | –32.20000 | –16.40000 | –32.20000 | –28.00000 | –18.90000 |

| Std. Dev. | 4.641552 | 4.770380 | 5.156009 | 6.913105 | 11.67648 | 28.04579 | 28.48459 | 9.478689 | 8.189988 |

| Skewness | −1.228007 | −1.039220 | −0.154285 | −2.368945 | −2.088830 | 0.427487 | 0.002608 | 2.595301 | 4.530885 |

| Kurtosis | 6.178526 | 5.560661 | 4.840111 | 15.50138 | 8.840930 | 2.035468 | 2.060095 | 15.87023 | 27.45001 |

| Jarque–Bera | 80.67516 | 54.38449 | 16.82592 | 893.6600 | 257.8465 | 8.306515 | 4.380430 | 962.9255 | 3399.593 |

| Probability | 0.000000 | 0.000000 | 0.000222 | 0.000000 | 0.000000 | 0.015713 | 0.111893 | 0.000000 | 0.000000 |

| Observations | 120 | 120 | 116 | 120 | 120 | 120 | 119 | 120 | 120 |

| Model 1: | Model 2: | Model 3: | Model 4: | Model 5: | |

|---|---|---|---|---|---|

| Constant | −5.037878 ** (−2.040909) | −4.610732 ** (−2.163483) | −4.705574 (−1.401286) | 21.28604 *** (29.55628) | 18.24710 *** (29.168833) |

| 0.245422 *** (7.083616) | 0.254232 *** (0.643967) | 0.249404 *** (2.646696) | −0.072846 *** (−3.166139 | 0.496179 *** (6.271028) | |

| −0.043674 (−1.011192) | −0.053029 (−1.528984) | −0.018633 (−0.295489) | 0.131381 *** (6.537375) | −0.451929 *** (−6.556460) | |

| 0.329177 *** (8.189671) | 0.354729 *** (9.250830) | 0.197549 ** (5.027329) | −0.030850 (−0.229545) | 0.153821 *** (2.979367) | |

| −0.305146 *** (−6.764424) | −0.343824 *** (−7.508574) | −0.180761 ** (−4.824277) | 0.032291 (0.255098) | −0.137367 ** (−2.491484) | |

| Prob. > F | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| Cross-section effects | Fixed | Fixed | Fixed | None | Fixed |

| R2 | 0.573761 | 0.514328 | 0.415360 | 0.266779 | 0.763116 |

| Adjusted R-squared | 0.520988 | 0.454197 | 0.340847 | 0.241052 | 0.733787 |

| F-statistic | 10.87235 | 8.553470 | 5.574337 | 10.36958 | 26.01955 |

| Observations | 119 | 119 | 116 | 119 | 119 |

| Panel unit root test: Summary Series: GDP: Sample: 2005–2016: Exogenous variables: Individual effects Automatic selection of maximum lags Automatic lag length selection based on SIC: 0 to 1 Newey–West automatic bandwidth selection and Bartlett kernel | Panel unit root test: Summary Series: D(GDP): Sample: 2005–2016 Exogenous variables: Individual effects Automatic selection of maximum lags Automatic lag length selection based on SIC: 0 to 1 Newey–West automatic bandwidth selection and Bartlett kernel | |||||||

| At Level | At Difference | |||||||

| Method | Statistic | Prob. ** | Cross-sections | Obs. | Statistic | Prob. ** | Cross-sections | Obs. |

| Null: Unit root (assumes common unit root process) | Null: Unit root (assumes common unit root process) | |||||||

| Levin, Lin and Chu t * | −7.53233 | 0.0000 | 10 | 107 | c11.4727 | 0.0000 | 10 | 94 |

| Null: Unit root (assumes individual unit root process) | Null: Unit root (assumes individual unit root process) | |||||||

| Im, Pesaran and Shin W-stat | −3.63088 | 0.0001 | 10 | 107 | −6.28179 | 0.0000 | 10 | 94 |

| ADF-Fisher chi-square | 45.3809 | 0.0010 | 10 | 107 | 75.8515 | 0.0000 | 10 | 94 |

| PP-Fisher chi-square | 36.4986 | 0.0134 | 10 | 110 | 102.528 | 0.0000 | 10 | 100 |

| ** Probabilities for Fisher tests are computed using an asymptotic chi-square distribution. All other tests assume asymptotic normality. | ||||||||

| Null Hypothesis: Stationarity Series: GDP: Sample: 2005–2016: Exogenous variables: Individual effects Newey–West automatic bandwidth selection and Bartlett kernel Total (balanced) observations: 120: Cross-sections included: 10 | Null Hypothesis: Stationarity Series: D(GDP): Sample: 2005–2016 Exogenous variables: Individual effects Newey–West automatic bandwidth selection and Bartlett kernel Total (balanced) observations: 110 Cross-sections included: 10 | |||||||

| At Level | At Difference | |||||||

| Method | Statistic | Prob. ** | Statistic | Prob. ** | ||||

| Hadri Z-stat | 0.63450 | 0.2629 | 5.23213 | 0.0000 | ||||

| Heteroscedastic consistent Z-stat | 1.39141 | 0.0821 | 5.86540 | 0.0000 | ||||

| Pooled OLS | Fixed Effect | Random Effect | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dependent Variable: GDP Method: Panel Least Squares Sample: 2005 2016: Periods included: 12 Cross-sections included: 10 Total panel (balanced) observations: 120 | Dependent Variable: GDP Method: Panel Least Squares Sample: 2005 2016: Periods included: 12 Cross-sections included: 10 Total panel (balanced) observations: 120 | Dependent Variable: GDP Method: Panel EGLS (cross-section random effects) Sample: 2005–2016 Periods included: 12 Cross-sections included: 10 Total panel (unbalanced) observations: 117 | ||||||||||

| Variable | Coefficient | Std. Error | t-statistic | Prob. | Coefficient | Std. Error | t-statistic | Prob. | Coefficient | Std. Error | t-statistic | Prob. |

| C | 1.755956 | 0.587466 | 2.989036 | 0.0034 | −4.367990 | 1.367125 | −3.195019 | 0.0018 | 1.755956 | 0.511377 | 3.433781 | 0.0008 |

| EXPORTS | −0.145173 | 0.046726 | −3.106882 | 0.0024 | −0.073646 | 0.051067 | −1.442138 | 0.1522 | −0.145173 | 0.040674 | −3.569162 | 0.0005 |

| IMPORTS | 0.143618 | 0.047209 | 3.042188 | 0.0029 | 0.252786 | 0.047424 | 5.330282 | 0.0000 | 0.143618 | 0.041094 | 3.494842 | 0.0007 |

| FDI_INF | 0.306682 | 0.081543 | 3.760989 | 0.0003 | 0.351035 | 0.079217 | 4.431308 | 0.0000 | 0.306682 | 0.070981 | 4.320595 | 0.0000 |

| FDI_OUTF | −0.288698 | 0.089749 | −3.216736 | 0.0017 | −0.342035 | 0.087281 | −3.918765 | 0.0002 | −0.288698 | 0.078125 | −3.695361 | 0.0003 |

| R-squared | 0.279053 | R-squared | 0.496466 | R-squared | 0.279053 | |||||||

| Adjusted R-squared | 0.253976 | Adjusted R-squared | 0.434712 | Adjusted R-squared | 0.253976 | |||||||

| F-statistic | 11.12810 | F-statistic | 8.039406 | F-statistic | 11.12810 | |||||||

| Prob(F-statistic) | 0.000000 | Prob(F-statistic) | 0.000000 | Prob(F-statistic) | 0.000000 | |||||||

| Correlated Random Effects—Hausman Test Equation: Untitled test cross-section random effects | ||||||||||||

| Test Summary | Chi-Sq. statistic | Chi-Sq. d.f. | Prob. | Cross-section random effects test comparisons | ||||||||

| Cross-section random | 40.796545 | 4 | 0.0000 | Variable | Fixed | Random | Var. (Diff.) | Prob. | ||||

| Cross-section random effects test comparisons | ||||||||||||

| Variable | Fixed | Random | Var. (Diff.) | Prob. | C | −4.367990 | 1.367125 | −3.195019 | 0.0018 | |||

| EXPORTS | −0.073646 | −0.145173 | 0.000953 | 0.0205 | EXPORTS | −0.073646 | 0.051067 | −1.442138 | 0.1522 | |||

| IMPORTS | 0.252786 | 0.143618 | 0.000560 | 0.0000 | IMPORTS | 0.252786 | 0.047424 | 5.330282 | 0.0000 | |||

| FDI_INF | 0.351035 | 0.306682 | 0.001237 | 0.2073 | FDI_INF | 0.351035 | 0.079217 | 4.431308 | 0.0000 | |||

| FDI_OUTF | −0.342035 | −0.288698 | 0.001515 | 0.1705 | FDI_OUTF | −0.342035 | 0.087281 | −3.918765 | 0.0002 | |||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| EXPORTS | −0.090125 | 0.062650 | −1.438549 | 0.1535 |

| IMPORTS | 0.226418 | 0.055913 | 4.049459 | 0.0001 |

| FDI_INF | 0.327937 | 0.096441 | 3.400383 | 0.0010 |

| FDI_OUTF | −0.327248 | 0.105604 | −3.098812 | 0.0025 |

| R-squared | 0.481717 | |||

| Adjusted R-squared | 0.411533 | |||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C (1) | −1.168900 | 0.129244 | −9.044155 | 0.0000 |

| C (2) | 0.537198 | 0.131821 | 4.075221 | 0.0001 |

| C (3) | 0.070987 | 0.129344 | 0.548823 | 0.5834 |

| C (4) | 0.048034 | 0.066502 | 0.722301 | 0.4705 |

| R-squared | 0.622065 | |||

| Adjusted R-squared | 0.568766 | |||

| Wald Test: System: % | |||

|---|---|---|---|

| Test Statistic | Value | df | Probability |

| Chi-square | 18.17986 | 3 | 0.0004 |

| Null hypothesis: C (2) = C (3) = C (4) = 0 | |||

| Unrestricted Cointegration Rank Test (Trace) | Unrestricted Cointegration Rank Test (Maximum Eigenvalue) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Hypothesized No. of CE(s) | Eigenvalue | Trace Statistic | 0.05 Critical Value | Prob. ** | Hypothesized No. of CE(s) | Eigenvalue | Max-Eigen Statistic | 0.05 Critical Value | Prob. ** |

| None * | 0.557148 | 168.8845 | 69.81889 | 0.0000 | None * | 0.557148 | 73.30672 | 33.87687 | 0.0000 |

| At most 1 * | 0.351002 | 95.57780 | 47.85613 | 0.0000 | At most 1 * | 0.351002 | 38.90924 | 27.58434 | 0.0012 |

| At most 2 | 0.298090 | 56.66856 | 29.79707 | 0.0000 | At most 2 | 0.298090 | 31.85556 | 21.13162 | 0.0011 |

| At most 3 | 0.235800 | 24.81300 | 15.49471 | 0.0015 | At most 3 | 0.235800 | 24.20335 | 14.26460 | 0.0010 |

| At most 4 | 0.006751 | 0.609649 | 3.841465 | 0.4349 | At most 4 | 0.006751 | 0.609649 | 3.841465 | 0.4349 |

| Trace test indicates 2 cointegrating equations at the 0.05 level. * denotes rejection of the hypothesis at the 0.05 level ** MacKinnon et al. (1999) p-values | Max-eigenvalue test indicates 2 cointegrating equations at the 0.05 level. * denotes rejection of the hypothesis at the 0.05 level ** MacKinnon et al. (1999) p-values | ||||||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ioan, B.; Mozi, R.M.; Lucian, G.; Gheorghe, F.; Horia, T.; Ioan, B.; Mircea-Iosif, R. An Empirical Investigation on Determinants of Sustainable Economic Growth. Lessons from Central and Eastern European Countries. J. Risk Financial Manag. 2020, 13, 146. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm13070146

Ioan B, Mozi RM, Lucian G, Gheorghe F, Horia T, Ioan B, Mircea-Iosif R. An Empirical Investigation on Determinants of Sustainable Economic Growth. Lessons from Central and Eastern European Countries. Journal of Risk and Financial Management. 2020; 13(7):146. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm13070146

Chicago/Turabian StyleIoan, Batrancea, Rathnaswamy Malar Mozi, Gaban Lucian, Fatacean Gheorghe, Tulai Horia, Bircea Ioan, and Rus Mircea-Iosif. 2020. "An Empirical Investigation on Determinants of Sustainable Economic Growth. Lessons from Central and Eastern European Countries" Journal of Risk and Financial Management 13, no. 7: 146. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm13070146