Direct and Indirect Effects of Investment Incentives in Slovakia

1

Faculty of Business Economics in Košice, University of Economics in Bratislava, Tajovského 13, 04130 Košice, Slovakia

2

Faculty of Informatics and Statistics, University of Economics, nám. W. Churchilla 1938/4, 130 67 Prague, Czech Republic

3

Faculty of Engineering and Science, Aalborg University, A. C. Meyers Vænge 15, 2450 Copenhagen, Denmark

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(2), 56; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14020056

Submission received: 7 January 2021

/

Revised: 21 January 2021

/

Accepted: 28 January 2021

/

Published: 1 February 2021

(This article belongs to the Special Issue Foreign Direct Investment – Under the Sign of Profit or Sustainable Development?)

Abstract

:Countries trying to attract foreign direct investment often use various tools to influence the foreign investor’s allocation decision including public subsidies in the form of investment incentives. However, the effects associated with providing these incentives are often questioned, especially in light of the need to achieve at least a minimum level of attractiveness of the business environment. The primary aim of the present study was to examine the effects of investment incentives on foreign direct investment inflows (direct effect) and on selected macroeconomic variables (indirect effects) under the conditions in Slovakia. Findings showed that the preference of specific forms of investment incentives by the government of the Slovak Republic changed slightly in the observed period of 2002–2019. The results of the regression analysis further suggest that while financial incentives have a positive statistically significant direct effect on foreign direct investment inflows, in the case of fiscal incentives, this effect is the opposite. In terms of indirect effects of investment incentives, only a reduction in the unemployment rate through foreign direct investment was found. The study contributes to the literature by providing evidence on the effects of various forms of investment incentives and by offering some implications for investment promotion policy.

1. Introduction

Topics connected with foreign direct investment have gained significant attention in the empirical literature in the recent years, especially in the context of transforming countries aiming to sustain their economic growth through various channels including foreign investment presence (e.g., Batrancea et al. 2020). Based on this, huge attention has been paid to factors determining the inflow of foreign direct investment (FDI) into particular country, with special emphasis on the Central European countries that became attractive investment locations of western investors in the last decade (e.g., Gauselmann et al. 2011; Gorbunova et al. 2012; Wach and Wojciechowski 2016). Based on Dunning’s (1981) eclectic theory, FDI is influenced by three sets of advantages, of which specific location advantages are considered as home country investment determinants. Location decision-making, in turn, contributes to the formation of the economic and social landscape (Sucháček et al. 2017). A detailed investigation of the effects of these location factors, especially those forming economic advantage, on attracting FDI is subject to wide discussion in the literature. With regard to the Central and Eastern European countries, factors such as production costs (e.g., Riedl 2010; Gauselmann et al. 2011), market size, trade openness (e.g., Janicki and Wunnava 2004; Galego et al. 2004; Demirhan and Masca 2008), and other macroeconomic variables (e.g., Plikynas and Akbar 2006; Bobenič Hintošová et al. 2018) have most frequently been examined. Another stream of literature also includes institutional factors such as the infrastructure, government spending, rule of law, corruption or shadow economy (e.g., Gorbunova et al. 2012; Chanegriha et al. 2017; Tintin 2013; Wach and Wojciechowski 2016; Bailey 2018; Bilan et al. 2019) to the models of inward FDI determinants.

With regard to the countries in transition, particularly those entering the European Union in the last few waves, special attention has been paid to the impact of this accession on the FDI flow and presence. That EU membership was an important anchor, notably for small Central European countries, was highlighted by Tintin (2013), who showed that EU membership itself significantly increased FDI inflows while reducing the impact of gross domestic product (GDP) size on these flows. Hence, EU membership can, to some extent, compensate for country size disadvantage, and consequently lead to attracting more FDI. Similar results regarding a positive association between EU membership and FDI inflows can also be found in works by Estrin and Uvalic (2014) or Tokunaga and Iwasaki (2017).

However, it is often unclear whether superior FDI inflows are the consequence of EU membership per se or higher institutional quality that is necessary for EU admission. Hence, we consider that policy stance and institutional environment, in particular factors like pro-investment policy and investment incentives and their forms, are slightly underexamined in the empirical literature. One important reason for this may be the limited availability of detailed data on the structure and amount of investment incentives. An exception in this regard is Slovakia, a Central European country that received a total FDI inflow of USD 51 billion in absolute terms in the period of 2003–2019. Many of these investments have been supported by a package of investment incentives provided by the government, the list of which is publicly available. However, there is insufficient evidence of the effects of these incentives on FDI inflows, especially when we take into account the fact that the incentive is often granted after the foreign investor´s localization decision is already adopted. Moreover, since the system of investment incentives varies across individual countries, it is reasonable to predict that the effects of investment promotion policy on the development of the particular country may also be country-specific.

Hence, we pose the following research question: How do different forms of investment incentives affect foreign direct investment inflows and macroeconomic performance in a small open economy? The present paper aims to enrich the existing literature by evaluating the effects of fiscal and financial investment incentives on inward FDI (direct effect) and on selected macroeconomic variables (indirect effects) under the conditions in Slovakia. In addition, some studies (e.g., Ruane 2008) point to the fact that investment incentives can only have visible effects if they are accompanied by an overall friendly business environment. Hence, our study also examines the role of the level of business environment in attracting inward FDI and sustaining macroeconomic performance. The analysis covers the period of 2002–2019 and regression analysis was used as the primary methodology.

The rest of the paper is organized as follows. Section 2 reviews the literature connected with the effects of investment incentives on FDI inflows and other variables; Section 3 introduces the dataset and the empirical methodology; Section 4 presents our empirical findings and their discussion, followed by the concluding remarks.

2. Literature Review

The effects brought by investment incentives in the form of public subsidies are most frequently examined directly (i.e., on the basis of their ability to attract inward FDI). Since there are several examples that investment incentives have attracted significant foreign investments, especially in the case of transition countries, this aspect is reflected in the positive findings of the empirical literature. In the Czech context, it is generally stated that the provision of investment incentives is in most cases effective (Cedidlová 2013) and positively related to the development of regions (Hlaváček and Janáček 2019). Similarly, in the Slovak context, investment incentives are considered as a basic tool to support foreign investment activities (Fabuš and Csabay 2018). However, this conclusion seems to require stronger empirical underpinning. When comparing Central European and Baltic countries, the results of the study by Šimelyté and Liučvaitiené (2012) favor the first group of countries, since their combination of fiscal incentives, together with financial ones, attract more FDI. The combination of the two policies for attracting FDI, namely the government´s immediate and certain lump-sum cost of the subsidy and tax rate reduction, as a possibly optimal investment promotion policy under certain circumstances, was also highlighted in the study by Tian (2018). However, Sarkar (2012) points to the interesting fact that governments provide financial investment incentives to companies and at the same time imposes taxes on their profits.

When distinguishing particular forms of investment incentives, fiscal incentives, especially tax-related, are considered more important for attracting and benefiting from foreign direct investment (Edwards and Newton 2016) and thus have received significantly more attention in the literature, perhaps also due to availability of data regarding taxes. A study by Azémar and Desbordes (2010) highlighted the importance of fiscal incentives and deregulation of labor markets in attracting FDI. Results achieved by Van Parys and James (2010), on one hand, showed that reduced complexity of the tax system helped to attract FDI, however, the tax holidays, as one of the most popular fiscal incentives, had no robust positive relationship to FDI. More recent studies show similar ambiguities. Ślusarczyk (2018) concluded that the tax incentives provided by the Polish government are considered to be a crucial factor in influencing the decision of foreign investors to allocate their investments to Poland. On the other hand, Hsu et al. (2019) provided a rationale for the termination of the tax incentives in China, since they proved that these incentives were not a sufficient determining factor of inward FDI.

In addition to the direct effects of investment incentives associated with an increase in inward foreign direct investment, other indirect effects are also expected, leading to increased productivity and the creation of new jobs, which should in turn lead to economic welfare and prosperity. However, the findings in this regard are rather ambiguous. The estimation results obtained by Yanikkaya and Karaboga (2017) showed that investment incentives had a negative or, at best, no positive effect on the selected macroeconomic variables. Although Musil and Hedija (2020)—only on a basis of a correlation analysis—demonstrated a statistically significant positive relationship between investment incentives and GDP growth, they also pointed to a non-statistically significant relationship between investment incentives and the output gap. Thus, they generally concluded that the investment promotion policy did not react flexibly to the current needs of the Czech economy. However, similar or possibly more detailed study conducted in the Slovak context is missing in the existing literature.

Investment incentives per se are thus often questioned as an effective tool for attracting FDI. As indicated by Havránek and Iršová (2010), the governments of host countries often use investment incentives as a tool addressed to foreign investors in order to compensate for shortcomings such as the existence of a high burden of employment costs and/or insufficient labor productivity in the host country. In a similar sense, a review study by Munongo et al. (2017) concluded that most of the empirical studies that they had explored suggested a combination of incentives with other factors such as macroeconomic conditions, infrastructure, and transparent institutions in an effort to effectively attract FDI. Similarly, a meta-analytic review by Bailey (2018) concluded that “good government” attracts FDI. However, governments that successfully attract foreign direct investment provide, in addition to various forms of investment incentives, at least a stable political environment with predictable and reliable public institutions that allow foreign investors to reap country-specific benefits. Hence, investment incentives can be considered effective only in cases where the business environment of the host country is considered satisfactory.

The outlined controversies and literature gaps led us to investigate the issue in more detail by considering the direct and indirect effects of different forms of investment incentives as well as the quality level of the overall business environment, under the conditions of a small open economy. On a basis of the literature review, we hypothesize that investment incentives effect FDI inflows and macroeconomic performance, however, the magnitude and the strength of the relationship between particular forms of investment incentives on one hand, and their direct and indirect effects on the other hand, might be different.

3. Data and Methodology

Inspired by the review study by Liou (2012), which analyzed the successes of incentive policies in attracting FDI and increasing economic growth, in our study, we evaluated similar effects of investment incentives provided by the Slovak government in the period of 2002–2019. More specifically, the aim of our research was to examine the effects of fiscal and financial investment incentives as well as the level of business environment on the inward FDI (direct effect) and on the selected macroeconomic variables (indirect effects).

To study the effects of investment incentives and other variables, we followed the approach by Agu et al. (2015) by using an ordinary least square (OLS) technique in a multiple form and decomposition of investment incentives into particular components (forms). Following this, regression models were constructed to study the direct effects of investment incentives and other variables.

FDIt = β0 + β1logFisIIt−1 + β2logFinIIt−1 + β3GDPGRt−1 + β4IEFt−1 + εt

FDIt = β0 + β1logFisIIt−1 + β2logFinIIt−1 + β3GDPGRt−1 + εt

As the dependent variable, the total volume of foreign direct investment inflow (FDI) was used. Data on FDI inflow were taken from the World Bank database. As independent variables, the total volume of fiscal investment incentives (FisII) as well as financial investment incentives (FinII) provided in individual years were used. Data on provided investment incentives in the structure of fiscal and financial incentives were calculated according to the data given in the list of entities to which investment incentives were provided, as published by the Ministry of Economy of the Slovak Republic. The level of economic growth was expressed by the growth of GDP (GDPGR) based on the data published by the Statistical Office of the Slovak Republic. In addition, the quality of overall business environment in the country was measured through the Index of Economic Freedom (IEF). When using the index, higher values are associated with a higher level of economic freedom. Data on the Index of Economic Freedom were taken from the Heritage Foundation.

Regression models were constructed to study the indirect effects of investment incentives and other variables.

where the dependent variables used were the volume of GDP (GDP), unemployment rate (UR), and level of average nominal monthly wage (Wage). The input data were taken from the Statistical Office of the Slovak Republic. As independent variables, besides those in models (1) and (2), we also used the volume of inward FDI (FDI), the volume of GDP (GDP), unemployment rate (UR), and the level of average nominal monthly wage (Wage).

GDPt = β0 + β1logFisIIt−1 + β2logFinIIt−1 + β3FDIt−1 + β4IEFt−1 + β5URt−1 + β6Waget−1 + εt

URt = β0 + β1logFisIIt−1 + β2logFinIIt−1 + β3FDIt−1 + β4IEFt−1 + β5logGDPt−1 + β6Waget−1 + εt

Waget = β0 + β1logFisIIt−1 + β2logFinIIt−1 + β3FDIt−1 + β4IEFt−1 + β5logGDPt−1 + β6URt−1 + εt

In models (1)–(5), all the independent variables were used with a one-year lag (similar to the study by(Bevan and Estrin 2004), since we expected a delay in the effect of independent variables on attracting foreign investors and influencing macroeconomic conditions. Since volumes of investment incentives are in absolute numbers and based on summary statistics are skewed to the right, we followed the suggestion of Osborne (2002) and applied logarithmic transformation of these data.

Descriptive statistics of the aforementioned variables are provided in Table 1, and the correlation matrix in Table 2. Pearson correlation coefficients were used in the correlation matrix. In addition to coefficients estimated in the OLS regressions, we also conducted R2, R2adj, Durbin-Watson, and Granger tests. Calculations were conducted in IBM SPSS 22.

4. Results and Discussion

Slovakia is a small open Central European country that has undergone a process of economic transformation within which foreign investment presence is considered to play a crucial role. However, other Central European countries have also embarked on a comparable systematic economic transformation, relying on similar comparative advantages such as favorable geographic location, relatively low labor costs and high labor productivity, stable political environment, etc. Hence, an individually determined system of investment incentives has often become a decisive factor in attracting foreign investment. Examples of investment projects that initially considered all the Central European countries as appropriate locations, however, based on the provision of a generous package of investment incentives were finally allocated in Slovakia, are the investments of PSA Peugeot Citroën or KIA.

The structure and conditions for the provision of investment incentives are slightly different within Central European countries, since they can be considered as a tool of competitive struggle in attracting FDI. For Hungary, besides standard cash subsidies, tax incentives, low-interest loans, or land available for free or at reduced prices, special VIP subsidies and strategic agreements individually negotiated with the Hungarian government are typical. In addition, Poland has also established administratively separate Special Economic Zones with rich investment incentives and preferential terms designed mainly for foreign investors. However, detailed data on the volume and structure of investment incentives in these countries are not available.

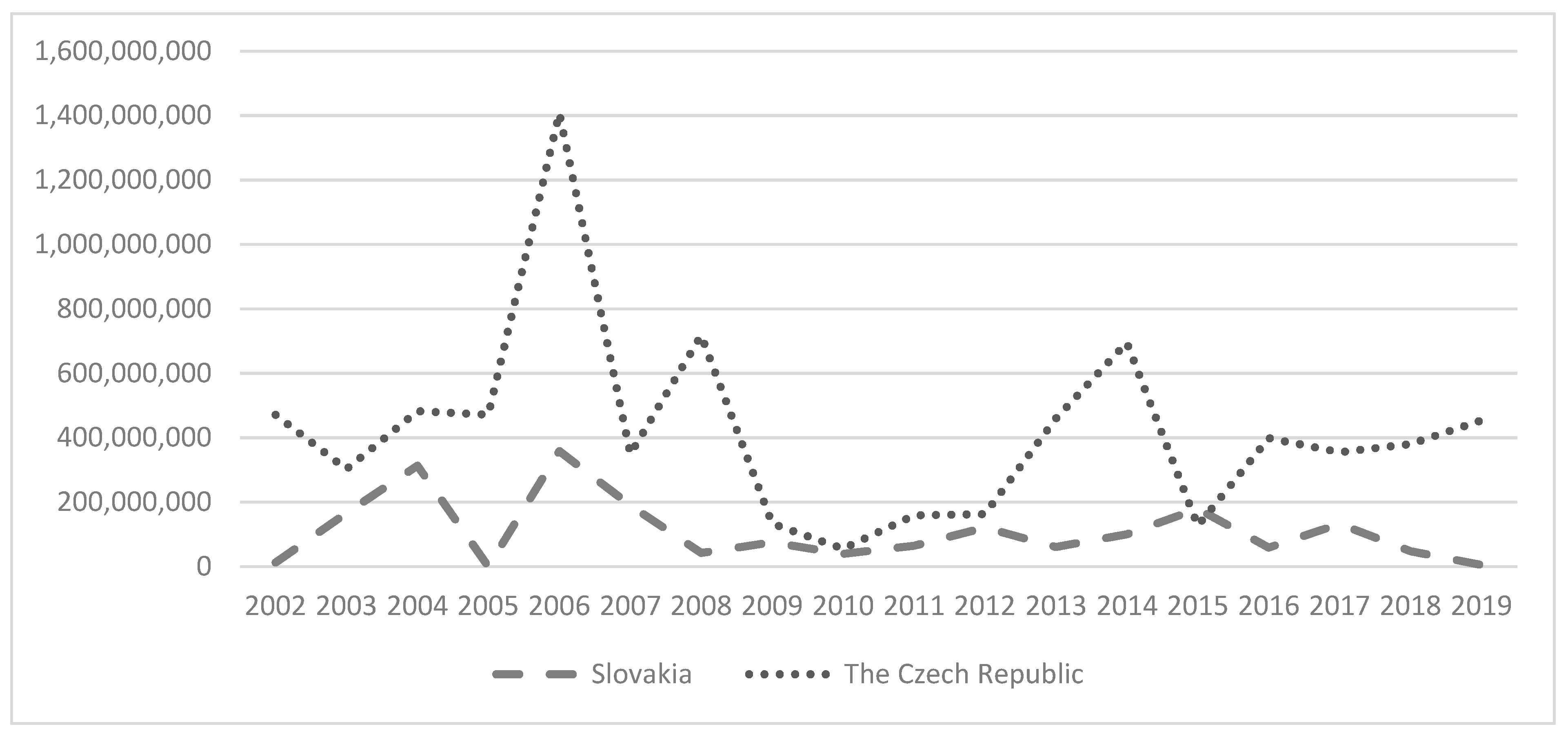

The most similar investment incentive schemes are applied in the Czech Republic and Slovakia, basically distinguishing fiscal and financial incentives. Figure 1 provides a comparison of the development of the total volume of provided investment incentives in these countries for the period of 2002–2019. A more detailed comparison of the structure of investment incentives was not possible due to the unavailability of detailed data for the Czech Republic.

Figure 1 shows that the amount of provided investment incentives was significantly higher in the Czech Republic, especially in the first half of the reported period. Even if we take into account the fact that the Czech Republic is approximately two times bigger than Slovakia in terms of population size, the difference in the amount of provided investment incentives was still significant. While in the Czech Republic the total amount of €7.5 billion was provided for investment incentives in the observed period, in the Slovak Republic, it was less than €2 billion. A similar disparity is evident in terms of the number of supported projects as the ratio was 926 Czech projects to 213 Slovak projects. However, while more than 85% of supported projects were implemented by foreign investors in Slovakia, in the Czech Republic, it was only about 43%. Thus, it appears that Slovakia is concentrating more on supporting foreign investment compared to domestic ones.

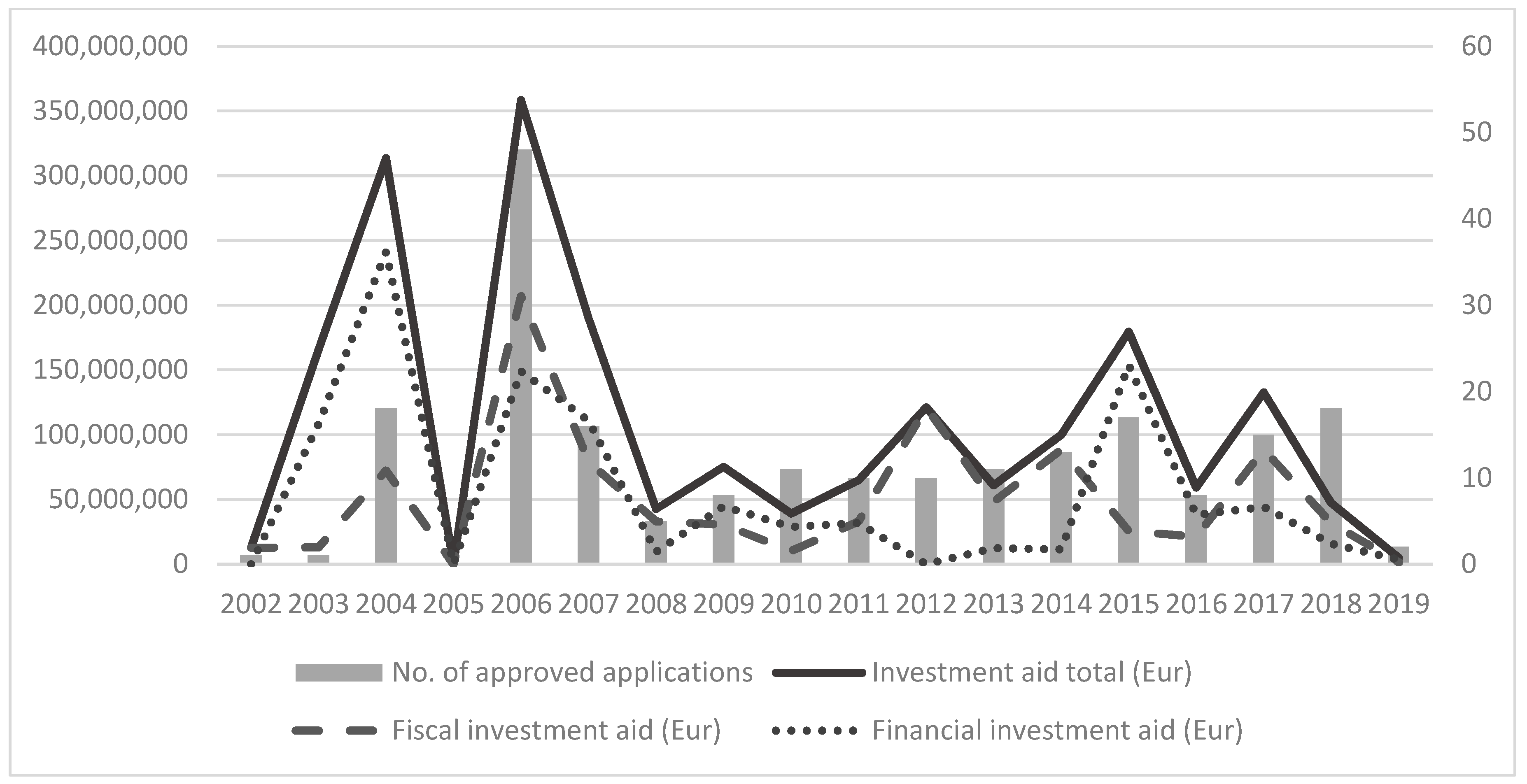

Under the conditions of the Slovak Republic, two basic forms of investment incentives are usually provided by the government: financial incentives in the form of grants for tangible and intangible fixed assets as well as contributions for new jobs creation, and fiscal incentives in the form of corporate income tax relief. The preference of the particular form of investment incentive is not defined in the legislation; however, there are precise conditions that shall be fulfilled for provision of the particular form of incentives. In practice, the majority of investment projects (54%) receive a package of investment incentives consisting of at least two forms, combining fiscal and financial incentives. The potentially supported projects should fall into one of the defined categories, namely an industrial production, a technology center, a combination of industrial production, and a technology center and a business services center.

Figure 2 shows the development of the provided investment incentives across the whole monitored period from 2002 to 2019 including the structure as well as the number of approved applications.

Due to significant changes in legislation, the provision of investment incentives can be assessed in two basic periods, before and after 2007. In the first observed period (i.e., 2002–2007), a total of 84 applications for investment incentives in the total amount of €1040 million were approved. Almost 60% of this amount was provided in the form of financial incentives and the rest as corporate income tax relief. In the second observed period (i.e., 2008–2019), a total of 129 applications for investment incentives in the total amount of almost €928 million were approved. Compared to the previous period, more investment projects were supported, but the total amount of provided investment incentives was lower, which means that smaller investment projects were supported, especially in marginalized regions. In terms of the structure of investment incentives, the ratio between financial and fiscal stimuli changed significantly compared to the previous period. The government began to prefer fiscal incentives with less immediate impact on the state budget, which was reflected in the share of fiscal incentives on the total amount of investment incentives of almost 58%.

The descriptive statistics of all the variables used within our analysis is provided in Table 1. With regard to the ratio of the particular forms of investment incentives during the whole observed period, the average values showed that a slightly higher amount was provided in the form of financial investment incentives. The average inflow of FDI to Slovakia was positive and reached an amount slightly exceeding USD 3 billion. In terms of the level of economic freedom, the country reported an average score of 66.67 points and moved around the 60a place in the ranking of the Heritage Foundation. From the selected macroeconomic variables point of view, Slovakia reported a relatively high unemployment rate of 12.6%, relatively low average nominal monthly wage of €760, and the GDP growth reached an average level of 3.9 percent in the observed period.

Within our research, our interest was to more deeply study the direct and indirect effects associated with the provision of particular forms of investment incentives. The empirical results of model (1) and model (2) (i.e., showing the direct effects of investment incentives and other variables including level of economic freedom in Slovakia on FDI inflows) are shown in Table 3.

Fiscal and financial investment incentives and GDP growth have a significant impact on FDI inflows in the following year, though the impact of fiscal investment incentives is negative. If a bivariate analysis was performed, directions of the relationships would remain the same, but the fiscal nor financial investment incentives alone would not be significant.

The Table 4 further reports empirical results of the models (3)–(5), i.e., showing indirect effects of investment incentives and other variables on the selected macroeconomic variables.

As expected, based on the correlation matrix, wages significantly influenced GDP, and no other significant impact was identified. The unemployment rate was found to be influenced by FDI inflows, and no other significant impact was identified. The impact of FDI was negative (i.e., FDI inflows increased employment). Wages could be explained by GDP and IEF, and no other significant impact was identified.

Based on the results, FDI inflow to Slovakia seemed to be significantly and positively influenced only by the financial form of investment incentives. This finding confirms the explanation offered by Burger et al. (2012) that foreign investors value financial incentives, especially grants and subsidies, as these are usually provided at the beginning or during the investment process, not only when the investment is profitable, as in the case of fiscal incentives. However, managerial preferences of particular forms of incentives can be influenced by a set of factors such as the national, cultural, or institutional characteristics of the particular investor (Poor et al. 2019).

On the other hand, fiscal incentives seem to have had a negative statistically significant impact on inward FDI. As indicated by Azémar and Dharmapala (2019), the effectiveness of tax incentives depends mainly on the tax regime of the investor’s home country, especially if it imposes worldwide taxation on income from abroad. Absence of tax sparing provisions in bilateral tax treaties can cause nullification of host country tax incentives by home country taxation. In addition, Munongo et al. (2017) pointed to other problems associated with tax incentives such as difficulties associated with the administration of tax incentives, misallocation of resources, and potential corruption, as a result of which they may be unattractive to investors.

Regarding the overall business environment assessed by the Index of Economic Freedom, we did not demonstrate its significant impact on FDI inflows. However, we used the values of the overall composite index without distinguishing specific dimensions describing different aspects of the business environment. Based on previous studies (e.g., Sambharya and Rasheed 2015), it is reasonable to assume that some of the dimensions are important determinants of FDI inflows. Part of the evidence for this is the statistically significant positive impact of GDP growth as a measure of economic progress in the country on inward FDI.

When analyzing the other effects of investment incentives on selected macroeconomic variables, like in the study by Yanikkaya and Karaboga (2017), no statistically significant relationship was identified. There was only one indirect statistically significant relationship through the inward FDI that negatively affected the unemployment rate. This finding is a consequence of the direction of FDI to labor-intensive sectors, as a result of which the unemployment rate is lowering. Similar conclusions have also been made by Táncošová (2019). With regard to other statistically significant relationships, there was a positive bi-directional relationship between wages and macroeconomic performance measured by GDP. A negative relationship between the Index of Economic Freedom and the level of average nominal monthly wage can be explained by the fact that while the development of the business environment fluctuated, nominal average wages gradually increased due to the huge pressure on the increase in the minimal wage.

Our results have some implications for investment promotion policy. Since fiscal incentives are not a sufficient determinant of FDI inflow into Slovakia, they should be subjected to promotion policy and tax reform, as in the case of China, as justified by the study of Hsu et al. (2019). Greater emphasis should be placed on financial incentives as their advantages over fiscal ones also lie in the possibility of greater impact on the incentive recipient and the related monitoring of the specific strategic goals of the incentive provider. According to Šestáková (2008), they also make it possible to compensate investors differently in the case of structural disadvantages and risks.

At the same time, we agree with the conclusions of Szent-Iványi (2017) that investment promotion policy in Visegrad countries including Slovakia is lagging behind and in this context, several fundamental changes would be appropriate. In addition to attracting more targeted foreign investment, more active post incentive cooperation with investors already operating in the country, accompanied by the provision of various services and support for reinvestment in order to prevent the so-called stimulus tourism, would be particularly appropriate. Hence, as suggested by Barbu and Boitan (2020), it is necessary to promote good public governance, since it exerts effects on the economy in general that can also be specifically reflected in more significant indirect effects associated with the provision of investment incentives.

5. Conclusions

The present study was primarily aimed at the examination of the direct and indirect effects associated with the provision of investment incentives in Slovakia. Our descriptive analysis first showed that while more financial incentives were provided up to 2007, attracting especially significant foreign investments, however, after a change in legislation, this trend was slightly modified as the government of the Slovak Republic began to prioritize fiscal incentives in the form of corporate income tax relief with an indirect impact on the state budget. In most cases, however, investors were provided with a whole package of incentives consisting of both financial and fiscal ones.

Our subsequent regression analysis focused on examining the effects associated with the provision of investment incentives. The results showed a positive statistically significant direct effect of financial incentives on inward FDI. Financial subsidies in the form of grants for tangible fixed assets and intangible fixed assets and/or contribution for newly-created jobs are attracting foreign investors to allocate their investment in Slovakia. On the other hand, fiscal incentives seem to have rather the opposite effect on FDI inflows, which can be connected with the various tax regimes applied by the investors’ home countries. Further research of tax sparing provisions within bilateral tax treaties could provide a deeper explanation of this negative association.

In addition, we also examined the impact of business environment measured by the level of the overall economic freedom in the country on FDI inflows; however, no statistically significant results were found, probably due to the consideration of the values of the overall index. It is reasonable to assume that foreign investors, when placing an investment in a particular country, assess individual partial aspects of the environment such as the level of economic growth as we have shown, which we consider important to investigate further. With regard to the other macroeconomic effects of investment incentives, we identified only one indirect effect on the lowering of unemployment rate through inward FDI.

The findings indicate the need to reconsider the change in pro-investment policy with greater emphasis on financial incentives. However, they need to be linked to the fulfillment of specific strategic objectives in the longer term and in relation to other post-incentive benefits that would more intensively connect the investor with the host country. In this respect, further research aimed at analyzing the reduction of regional disparities under the influence of provided investment incentives may be very important.

The main limitations of the study lie in covering a relatively short period of time and the focus on a single-country analysis. Extended time series data or cross-country data would probably bring more pronounced results. However, data on investment incentives in a detailed structure were only available for Slovakia, where investment incentives began to be provided from 2002.

Although these results are limited to the conditions of Slovakia, the study provides a significant contribution to the literature on the direct and indirect effects of various forms of investment incentives and also brings some implications for investment promotion policy.

Author Contributions

Conceptualization, A.B.H. and T.B.; methodology, A.B.H. and F.S.; software, F.S.; validation, A.B.H., F.S. and T.B.; formal analysis, F.S.; investigation, A.B.H.; resources, T.B.; data curation, F.S.; writing—original draft preparation, A.B.H.; writing—review and editing, A.B.H. and F.S.; visualization, T.B.; supervision, F.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Conflicts of Interest

The authors declare no conflict of interest.

References

- Agu, Sylvia Uchenna, Ifeoma Mary Okwo, Okelue David Ugwunta, and Adeline Idike. 2015. Fiscal policy and economic growth in Nigeria: Emphasis on various components of public expenditure. SAGE Open 5: 21–36. [Google Scholar] [CrossRef]

- Azémar, Céline, and Dhammika Dharmapala. 2019. Tax sparing agreements, territorial tax reforms, and foreign direct investment. Journal of Public Economics 169: 89–108. [Google Scholar] [CrossRef]

- Azémar, Céline, and Rodolphe Desbordes. 2010. Short-run strategies for attracting foreign direct investment. World Economy 33: 928–57. [Google Scholar] [CrossRef] [Green Version]

- Bailey, Nicholas. 2018. Exploring the relationship between institutional factors and FDI attractiveness: A meta-analytic review. International Business Review 27: 139–48. [Google Scholar] [CrossRef]

- Barbu, Teodora Cristina, and Iustina Alina Boitan. 2020. Financial system performance in European Union countries: Do country’s governance indicators matter? Journal of Business Economics and Management 21: 1646–64. [Google Scholar] [CrossRef]

- Batrancea, Ioan, Malar Mozi Rathnaswamy, Lucian Gaban, Gheorghe Fatacean, Horia Tulai, Ioan Bircea, and Mircea-Iosif Rus. 2020. An empirical investigation on determinants of sustainable economic growth: Lessons from Central and Eastern European countries. Journal of Risk and Financial Management 13: 146. [Google Scholar]

- Bevan, Alan A., and Saul Estrin. 2004. The determinants of foreign direct investment into European transition economies. Journal of Comparative Economics 32: 775–87. [Google Scholar] [CrossRef]

- Bilan, Yuriy, Tatiana Vasylieva, Sergij Lyeonov, and Inna Tiutiunyk. 2019. Shadow economy and its impact on demand at the investment market of the country. Entrepreneurial Business and Economics Review 7: 27–43. [Google Scholar] [CrossRef]

- Bobenič Hintošová, Aneta, Michaela Bruothová, Zuzana Kubíková, and Rastislav Ručinský. 2018. Determinants of foreign direct investment inflows: A case of Visegrad countries. Journal of International Studies 11: 222–35. [Google Scholar] [CrossRef]

- Burger, Anže, Andreja Jaklič, and Matija Rojec. 2012. The effectiveness of investment incentives: The Slovenian FDI co-financing grant scheme. Post-Communist Economies 24: 383–401. [Google Scholar] [CrossRef]

- Cedidlová, Miroslava. 2013. The effectiveness of investment incentives in certain foreign companies operating in the Czech Republic. Journal of Competitiveness 5: 108–20. [Google Scholar] [CrossRef]

- Chanegriha, Melisa, Chris Stewart, and Chris Tsoukis. 2017. Identifying the robust economic, geographical and political determinants of FDI: An extreme bounds analysis. Empirical Economics 52: 759–76. [Google Scholar] [CrossRef] [Green Version]

- Demirhan, Erdal, and Mahmut Masca. 2008. Determinants of foreign direct investment flows to developing countries: A cross-sectional analysis. Prague Economic Papers 17: 356–69. [Google Scholar] [CrossRef] [Green Version]

- Dunning, John H. 1981. International Production and the Multinational Enterprise. London: Allen & Unwin. [Google Scholar]

- Edwards, Jon, and Sarah Newton. 2016. Enhancing regulatory, financial, fiscal investment incentives as a means of promoting foreign direct investment. In Analyzing the Relationship between Corporate Social Responsibility and Foreign Direct Investment. Edited by Marianne Ojo. Hershey: IGI Global, pp. 191–201. [Google Scholar]

- Estrin, Saul, and Milica Uvalic. 2014. FDI into transition economies: Are the Balkans different? Economics of Transition 22: 281–312. [Google Scholar] [CrossRef]

- Fabuš, Michal, and Marek Csabay. 2018. State aid and investment: Case of Slovakia. Entrepreneurship and Sustainability Issues 6: 480–88. [Google Scholar] [CrossRef]

- Galego, Aurora, Carlos Vieira, and Isabel Vieira. 2004. The CEEC as FDI attractors: A menace to the EU periphery? Emerging Markets Finance and Trade 40: 74–91. [Google Scholar] [CrossRef]

- Gauselmann, Andrea, Mark Knell, and Johannes Stephan. 2011. What drives FDI in Central–Eastern Europe? Evidence from the IWH-FDI-Micro database. Post-Communist Economies 23: 343–57. [Google Scholar] [CrossRef]

- Gorbunova, Yulia, Davide Infante, and Janna Smirnova. 2012. New evidence on FDI determinants: An appraisal over the transition period. Prague Economic Papers 21: 129–49. [Google Scholar] [CrossRef]

- Havránek, Tomáš, and Zuzana Iršová. 2010. On the intensity of international subsidy competition for FDI. Theoretical and Applied Economics 17: 25–54. [Google Scholar]

- Hlaváček, Petr, and Julius Janáček. 2019. The influence of foreign direct investment and public incentives on the socio-economic development of regions: An empirical study from the Czech Republic. E+M 22: 4–19. [Google Scholar] [CrossRef]

- Hsu, Minchung, Junsang Lee, Roberto Leon-Gonzalez, and Yanqing Zhao. 2019. Tax incentives and foreign direct investment in China. Applied Economics Letters 26: 777–80. [Google Scholar] [CrossRef]

- Janicki, Hubert P., and Phanindra V. Wunnava. 2004. Determinants of foreign direct investment: Empirical evidence from EU accession candidates. Applied Economics 36: 505–9. [Google Scholar] [CrossRef]

- Liou, Kuotsai Tom. 2012. Incentive policies and China’s economic development: Change and challenge. Journal of Public Budgeting, Accounting and Financial Management 24: 114–35. [Google Scholar] [CrossRef]

- Munongo, Simon, Olusegun Ayo Akanbi, and Zurika Robinson. 2017. Do tax incentives matter for investment? A literature review. Business and Economic Horizons 13: 152–68. [Google Scholar] [CrossRef] [Green Version]

- Musil, Petr, and Veronika Hedija. 2020. Investment incentives as instrument of motivation of firms and economic stabilization. Entrepreneurship and Sustainability Issues 8: 578–89. [Google Scholar] [CrossRef]

- Osborne, Jason W. 2002. Notes on the use of data transformations. Practical Assessment, Research, and Evaluation 8: 1–7. [Google Scholar]

- Plikynas, Darius, and Yusaf H. Akbar. 2006. Neural network approaches to estimating FDI flows: Evidence from Central and Eastern Europe. Eastern European Economics 44: 29–59. [Google Scholar] [CrossRef]

- Poor, József, Ildikó Éva Kovács, Karoliny Zsuzsa, and Renata Machova. 2019. Global, regional and local similarities and differences in HRM in light of CRANET researches (2008–2016). Journal of Eastern European and Central Asian Research 6: 1–23. [Google Scholar] [CrossRef] [Green Version]

- Riedl, Aleksandra. 2010. Location factors of FDI and the growing services economy. Economics of Transition 18: 741–61. [Google Scholar] [CrossRef]

- Ruane, Maria Claret M. 2008. Attracting foreign direct investments: Challenges and opportunities for smaller host economies. Journal of International Business Research 7: 65–74. [Google Scholar]

- Sambharya, Rakesh B., and Abdul A. Rasheed. 2015. Does economic freedom in host countries lead to increased foreign direct investment? Competitiveness Review 25: 2–24. [Google Scholar] [CrossRef]

- Sarkar, Sudipto. 2012. Attracting private investment: Tax reduction, investment subsidy, or both? Economic Modelling 29: 1780–85. [Google Scholar] [CrossRef]

- Šestáková, Monika. 2008. Konkurencia medzi štátmi v oblasti získavania a udržania zahraničných investícií. Bratislava: Ekonomický ústav SAV. [Google Scholar]

- Šimelyté, Agné, and Aušra Liučvaitiené. 2012. Foreign direct investment, policy-friendly business environment in R&D sectors: Baltic states versus Visegrad countries. Journal of East-West Business 18: 66–93. [Google Scholar]

- Ślusarczyk, Beata. 2018. Tax incentives as a main factor to attract foreign direct investments in Poland. Administratie si Management Public 30: 67–81. [Google Scholar] [CrossRef]

- Sucháček, Jan, Petr Seďa, Václav Friedrich, and Jaroslav Koutský. 2017. Regional aspects of the development of largest enterprises in the Czech Republic. Technological and Economic Development of Economy 23: 649–66. [Google Scholar] [CrossRef]

- Szent-Iványi, Balázs. 2017. Investment promotion in the Visegrad four countries: Post-FDI challenges. In Condemned to Be Left behind? Can Central Eastern Europe Emerge from Its Low-Wage FDI-Based Growth Model? Edited by Galgoczi Béla and Jan Drahokoupil. Brussels: ETUI, pp. 171–87. [Google Scholar]

- Táncošová, Judita. 2019. The role of foreign direct investment in the economy of Slovakia. Entrepreneurship and Sustainability Issues 6: 2127–35. [Google Scholar] [CrossRef]

- Tian, Yuan. 2018. Optimal policy for attracting FDI: Investment cost subsidy versus tax rate reduction. International Review of Economics and Finance 53: 151–59. [Google Scholar] [CrossRef]

- Tintin, Cem. 2013. The determinants of foreign direct investment inflows in the Central and Eastern European Countries: The importance of institutions. Communist and Post-Communist Studies 46: 287–98. [Google Scholar] [CrossRef]

- Tokunaga, Masahiro, and Ichiro Iwasaki. 2017. The determinants of foreign direct investment in transition economies: A meta-analysis. The World Economy 40: 2771–831. [Google Scholar] [CrossRef]

- Van Parys, Stefan, and Sebastian James. 2010. The effectiveness of tax incentives in attracting investment: Panel data evidence from the CFA Franc zone. International Tax and Public Finance 17: 400–29. [Google Scholar] [CrossRef]

- Wach, Krzysztof, and Liwiusz Wojciechowski. 2016. Determinants of inward FDI into Visegrad countries: Empirical evidence based on panel data for the years 2000–2012. Economics and Business Review 2: 34–52. [Google Scholar] [CrossRef] [Green Version]

- Yanikkaya, Halit, and Hasan Karaboga. 2017. The effectiveness of investment incentives in the Turkish manufacturing industry. Prague Economic Papers 26: 744–60. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Development of the total volume of provided investment incentives in Slovakia and the Czech Republic. Source: Own processing based on data from Ministry of Economy of the Slovak Republic and www.czechinvest.org.

Figure 1.

Development of the total volume of provided investment incentives in Slovakia and the Czech Republic. Source: Own processing based on data from Ministry of Economy of the Slovak Republic and www.czechinvest.org.

Figure 2.

Development of provided investment incentives in Slovakia. Source: Own processing based on data from Ministry of Economy of the Slovak Republic.

Figure 2.

Development of provided investment incentives in Slovakia. Source: Own processing based on data from Ministry of Economy of the Slovak Republic.

{kind=link}

{kind=link}

Table 1.

Descriptive statistics.

| Range | Minimum | Maximum | Mean | Std. Deviation | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| FisII | 206,950,023.00 | 0.00 | 206,950,023.00 | 50,981,809.2778 | 51,962,797.98420 | 1.781 | 3.772 |

| FinII | 241,028,314.00 | 0.00 | 241,028,314.00 | 55,763,398.9444 | 68,574,438.88813 | 1.517 | 1.751 |

| FDI | 6,064,345,209.70 | −362,908,482.70 | 5,701,436,727.00 | 3,061,536,539.4556 | 1,801,485,985.58198 | −0.183 | −1.181 |

| IEF | 11.00 | 59.00 | 70.00 | 66.6722 | 3.20511 | −1.249 | 1.343 |

| UR | 12.80 | 5.80 | 18.60 | 12.6167 | 3.74468 | −0.181 | −0.591 |

| Wage | 643.52 | 448.48 | 1092.00 | 760.4989 | 181.31333 | −0.098 | −0.600 |

| GDP | 56,841.70 | 37,329.50 | 94171.20 | 67,787.6333 | 16,238.34690 | −0.383 | −0.581 |

| GDPGR | 16.30 | −5.50 | 10.80 | 3.9722 | 3.42049 | −0.765 | 3.045 |

The correlation matrix of the used variables is presented in Table 2.

Table 2.

Correlation matrix.

| FisII | FinII | FDI | IEF | UR | Wage | GDP | GDPGR | |

|---|---|---|---|---|---|---|---|---|

| FisII | 1 | 0.349 | 0.222 | 0.301 | 0.021 | −0.076 | −0.031 | 0.240 |

| FinII | 0.349 | 1 | 0.200 | −0.048 | 0.280 | −0.369 | −0.350 | 0.370 |

| FDI | 0.222 | 0.200 | 1 | 0.222 | −0.042 | −0.246 | −0.211 | 0.465 |

| IEF | 0.301 | −0.048 | 0.222 | 1 | −0.335 | 0.314 | 0.379 | −0.025 |

| UR | 0.021 | 0.280 | −0.042 | −0.335 | 1 | −0.868 ** | −0.878 ** | 0.157 |

| Wage | −0.076 | −0.369 | −0.246 | 0.314 | −0.868 ** | 1 | 0.993 ** | −0.367 |

| GDP | −0.031 | −0.350 | −0.211 | 0.379 | −0.878 ** | 0.993 ** | 1 | −0.316 |

| GDPGR | 0.240 | 0.370 | 0.465 | −0.025 | 0.157 | −0.367 | −0.316 | 1 |

Note: The asterisks denote the statistical significance of coefficients at a level of 1% (**), based on p-values.

Table 3.

Regression results of models (1)–(2).

| Variable | Model (1) | Model (2) |

|---|---|---|

| Constant | 4,574,043,665.940 (0.620) | 4,191,869,255.855 ** (2.981) |

| logFisII | −572,785,105.569 ** (−2.621) | −571,430,387.438 ** (−2.740) |

| logFinII | 139,807,022.215 * (2.182) | 302,838,401.426 ** (2.369) |

| GDPGR | 242,584,136.357 ** (2.451) | 242,940,018.348 ** (2.561) |

| IEF | −5,771,047.605 (−0.053) | |

| R2 | 0.589 | 0.588 |

| adjusted R2 | 0.451 | 0.493 |

| Durbin-Watson test | 2.243 | 2.244 |

| Granger test | 0.047 | 0.018 |

Note: t-statistics in parentheses. The asterisks denote statistical significance: * at a level of 10% and ** at a level of 5%.

Table 4.

Regression results of models (3)–(5).

| Variable | Model (3) | Model (4) | Model (5) |

|---|---|---|---|

| Constant | 2622.125 (0.150) | 88.457 (0.548) | −6029.378 *** (−7.515) |

| logFisII | −120.196 (−0.306) | 0.387 (1.220) | −5.394 (−1.116) |

| logFinII | 202.430 (0.779) | −0.234 (−1.193) | 2.538 (0.803) |

| FDI | 3.474 × 10−7 (0.815) | −7.723 × 10−10 ** (−2.716) | 2.392 × 10−9 (0.454) |

| IEF | 28.589 (0.126) | 0.279 (0.861) | −13.858 *** (−4.232) |

| UR | −60.428 (−0.152) | −3.492 (−0.709) | |

| Wage | 86.832 *** (10.259) | −0.010 (−0.388) | |

| logGDP | −18.031 (−0.439) | 1620.875 *** (9.212) | |

| R2 | 0.983 | 0.818 | 0.981 |

| adjusted R2 | 0.973 | 0.708 | 0.969 |

| Durbin−Watson test | 1.961 | 1.253 | 2.190 |

| Granger test | 0.501 | 0.627 | 0.220 |

Note: t-statistics in parentheses. The asterisks denote statistical significance: ** on a level of 5% and *** on a level of 1%.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Bobenič Hintošová, A.; Sudzina, F.; Barlašová, T. Direct and Indirect Effects of Investment Incentives in Slovakia. J. Risk Financial Manag. 2021, 14, 56. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14020056

AMA Style

Bobenič Hintošová A, Sudzina F, Barlašová T. Direct and Indirect Effects of Investment Incentives in Slovakia. Journal of Risk and Financial Management. 2021; 14(2):56. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14020056

Chicago/Turabian StyleBobenič Hintošová, Aneta, František Sudzina, and Terézia Barlašová. 2021. "Direct and Indirect Effects of Investment Incentives in Slovakia" Journal of Risk and Financial Management 14, no. 2: 56. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14020056