Poland–Turkey Comparison of Mobile Payments Quality in Pandemic Time

1

Faculty of Management, University of Warsaw, Krakowskie Przedmieście 26/28, 00-927 Warsaw, Poland

2

School of Applied Sciences, Usak University, Ankara Izmir Yolu 8. Km Bir Eylül Kampüsü, 64000 Merkez, Turkey

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(9), 426; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14090426

Submission received: 21 July 2021

/

Revised: 1 September 2021

/

Accepted: 2 September 2021

/

Published: 6 September 2021

(This article belongs to the Special Issue FinTech and the Future of Finance)

Abstract

:The main objective of this article is to identify and analyze the use of mobile payments in two countries, Poland and Turkey. The data for the study were collected with the application of the CAWI method in March 2021. The survey covered nearly 650 respondents in total. The basis for comparisons was populations from two culturally distinct countries, Poland and Turkey, which are at a similar level of development as regards the use of the Internet. The studies were carried out simultaneously in both countries and examined the group of young people aged 18–25. The research surveyed the population, which included the most active Internet users who are taking full advantage of the benefits of globalization, which is facilitated by the development of the Internet worldwide. The survey was translated into the respondents’ native languages, initially validated during the pilot studies and then distributed and circulated among the study participants. The obtained findings were subject to comparison, and the differences between the samples were analyzed and commented on to verify the hypotheses formulated in the study. The main limitation of the conducted study was the selection of a random group—the research sample consisted only of members of the academic community. The study presented in the article fills the research gap regarding international comparisons of the use of m-payments in the period of the COVID-19 pandemic. The obtained results indicate the undoubted fact of increased interest in the use of m-payments in e-commerce and e-banking, and even more importantly, differences concerning 40% of the criteria/attributes applied to assess the use of m-payments in both countries. The findings can be used by business practitioners dealing with the development of m-payments. Another potential application is to attempt to bridge the gaps between countries, which may be supported by globalization processes.

1. Introduction

The main purpose of this article is to identify and compare the issue of mobile payments in two countries, Poland and Turkey, in March 2021, from the point of view of the dynamics of changes that have occurred over the last year, i.e., from March 2020, that is, since the beginning of the Covid-19 pandemic. In their article, the authors decided to examine the two countries considering a number of relevant factors. On the one hand, at present, both selected countries experience dynamic growth, which is reflected, for example, in their adoption of new technologies. On the other hand, despite the abovementioned similarity, Poland and Turkey represent different cultural characteristics. Poland is located in the circle of Latin culture, and Turkey lies at the crossroads of Europe and Asia and is under the influence of Latin and Islamic cultures.

Including mobile payments (which are part of the FinTech ecosystem (Krueger 2016)) in the research is also important since the changes occurring in customer behavior and preferences facilitate the development of services provided by organizations operating in the FinTech sector (Górka 2016). They also impact the strategies employed by financial institutions themselves, which can be observed, for example, in changing banks’ strategies (Górka 2018).

The novelty of the presented research consists in the comparison of the perception of the possibilities related to using new technologies as well as determining the similarities and differences between countries considering the impact of the COVID-19 pandemic. So far, articles have mainly focused on examining the impact of a pandemic that was limited to the area of a particular country. There are few comparative analyses focusing on assessing the similarities and differences between individual countries, taking into account their different cultural conditionings and backgrounds. In addition to the theoretical conclusions formulated in the study, the research may be perceived as relevant material for practitioners making business decisions on, inter alia, introducing new technologies as products to markets.

In the absence of effective medicine and an effective vaccine against a rapidly spreading disease, the governments of individual countries tried to reduce the need to provide hospital medical care or spread it over time. This strategy was implemented and applied in various countries in different ways and to varying degrees. This was generally realized through extensive isolation (lockdown) based on so-called social distancing (keeping one’s physical distance and wearing face masks) and movement restrictions, including a curfew as well as:

- A suggestion or requirement to use electronic payments instead of cash in all transactions,

- Closing supermarkets and hypermarkets (shopping malls), with the exception of grocery stores, pharmacies and drugstores, and (temporarily) newsagents and bookstores,

- Closing swimming pools, saunas, solariums and sports facilities,

- Restrictions imposed on bars and restaurants that either could not function at all or operated only by preparing meals to take away or delivering them to clients,

- Closing schools, kindergartens and universities,

- Closing hotels and restaurants located in the facilities,

- Closing cinemas, theatres, museums, art galleries and casinos,

- Closing beauty and hairdressing salons, etc.

The continuation of the actions whose aim is focusing on publicity or propaganda rather than effectiveness continues to this day, and the number of COVID-19 cases is declining due to mass vaccination rather than isolationism and separation of the society members. The abovementioned methods tend to be illusory, and they are convenient mainly from the government’s point of view. The evidence shows this has had disastrous economic consequences to this day, but with one exception. The exception here is the growing position of electronic business in the economy. It would seem that this is an ideal situation for electronic business, or at least for some of its sectors, as the pandemic situation forces customers to stay at home, and the only possible way to reach them is through the use of the Internet. At this point, it is worthwhile to ask the following questions: has it affected the dynamics of online shopping? How has it influenced the development of electronic banking, including electronic payments, especially mobile payments, compared to the previous period?

The sectors that were able to continue their operations using online sales coped with the situation well. The production of goods and the provision of services were not stopped thanks to orders and deliveries arranged via the Internet. Unfortunately, some of the branches, such as hairdressing and beauty salons or sports and recreational activities, were forced to either move to the “grey market” or quickly learn to avoid excessively restrictive and inconsistent regulations. It is very easy to order this type of service via the Internet, and it is very convenient to pay for it; unfortunately, so far, restrictions have been imposed on the abovementioned businesses as regards providing services. Nevertheless, most of the organizations conducting business activity moved to the online market, which at the same time led to the dynamic growth of cooperating industries, e.g., delivery (transport, parcel lockers) or consulting and creating electronic channels of communication with clients, minimizing the financial risk of the activity (Smulski 2020).

According to the latest reports, the last twelve months—sometimes also referred to as the COVID-19 pandemic era—was an exceptional year for the entire sphere of e-commerce, especially its specific extension, i.e., electronic banking. If we regard e-commerce as a conglomerate of information technologies enabling, under certain organizational conditions, the remote provision of broadly understood banking services (Chmielarz 2016), then mobile banking, including mobile payments, may be regarded as its inseparable, inherent component. Mobile payments are treated in this context as the process whereby two parties transfer financial value via a mobile device in exchange for goods or services (Khosrow-Pour 2008). Considering the issue of the development of electronic payments in the era of the pandemic from the perspective of users, the analysts should first identify the available technical infrastructure (mobile devices and related software), then financial facilities (banks and financial tools). In the next step, they should examine the aspects and areas of specific electronic payment applications. The subsequent stages of the process should be reflected in the studies examining the abovementioned research problem.

In this context, it is important to mention that the statistics confirm the need to examine the field of mobile payment applications. In terms of infrastructure, 5.22 billion individuals used smartphones in 2021, which constitutes nearly 67% of the entire world’s population; and from 2020, the number of smartphone users increased by 93 million (1.8%) (Majchrzyk 2020). Smartphones already account for more than half of the devices used (53%; 56% together with tablets), compared to a 44% share of laptops and computers. It is important to note that 35% of smartphone users use banking applications (Kemp 2021). While the technical and financial infrastructure may be similar in different regions, the areas of m-payment application may be quite different. It may be connected with the level of the development of e-commerce in particular markets, perceived risk (Wu et al. 2020), intensity of the use of mobile phones and social media (Hossain et al. 2020), the characteristics and circumstances of consumers in different markets (Chen et al. 2020), and other factors considered in the present study.

The convergence and divergence in terms of the adoption and application of new technologies in different countries is a significant research problem both from an economic and social point of view. The current high dynamics of mobility-related development affects all sectors of the economy. In addition, mobility and worldwide internet solutions support globalization processes, shaping and influencing behavior of individuals and societies in different counties.

Recognizing these differences through international comparisons fills the existing research gap in this regard, in particular in the era of the COVID-19 pandemic.

The structure of the paper is as follows. Initially, the authors present an introduction to the study carried out in both countries, Poland and Turkey. Then, they discuss the role and place of the issue under consideration in the context of relevant literature on the subject. They also point to the existing research gap related to research on e-payments and m-payments in the context of international comparisons. The next section of the paper presents the research methodology applied in the study. The next step includes the analysis and discussion of the obtained findings. The last section of the article contains the conclusions of the study and recommendations concerning further research in the field.

2. Literature Review

In the literature on the subject, it emerges that, so far, the researchers have carried out several studies examining the issues related to the development of Internet solutions in the economy from the point of view of various representatives of the society. The main focus of the abovementioned research was the perception of electronic payment instruments such as e-payments and m-payments by their users. Recent studies have also considered the undoubtedly significant impact of the outbreak of the COVID-19 pandemic on changing consumer behavior in several related areas. The literary output, which is significant from the point of view of the study, is presented below.

One of the articles by L.T.T. Tran (2021) examined the impact of the COVID-19 pandemic on e-commerce solutions and presented the changes in Internet users’ behavior, as perceived by consumers themselves. The article considered the economic benefits of forecasting changes in consumer behavior, with a particular focus on sustainable consumption. The study showed that the fear of the pandemic led to an increase in customer confidence in e-commerce. The analysis was carried out with the use of specific criteria adopted in the research and considered the context of sustainable consumption.

Another study by Naeem and Ozuem (2021) addressed the problem of the impact of the COVID-19 pandemic on behavioral changes, in this case examining both the users of banking services and the banks themselves, in the context of the increasing popularity of electronic banking. The purpose of the study was to find out how the outbreak of the pandemic affected the use of online banking as well as to analyze the problems faced by users in this regard. The research findings may help to raise the awareness of the designers of electronic banking applications to adjust the solutions to the needs and expectations of various customer groups to a greater degree.

The research presented by Kala et al. (2021) examined the aspect of customers’ willingness to use banking mobile applications and presented this issue in the context of circumstances pertaining to a particular country. The case study aimed to establish what factors contribute to the popularity of mobile banking applications among customers in Cameroon. It examined the aspects influencing their decisions to adopt and use the aforementioned solutions. The research revealed that factors such as utilitarian expectations, status gaining, habit and perceived privacy concerns have a significant impact on the intent to use mobile banking solutions. The article also proved that the willingness to learn a new solution affects the subsequent loyalty and satisfaction of users.

The findings of the study carried out in Thailand by Yakean (2020) concerned the aspects of changes in terms of the use of e-payments and m-payments. This article describes the general advantages and disadvantages of the Thai public cashless system in the circumstances of the COVID-19 pandemic. The abovementioned analysis focuses on the instruments such as credit cards, ATMs, mobile and internet banking, e-wallet, PromptPay and QR code.

As part of their research, Filotto et al. (2021) analyzed the perception of banking services by customers focused on the traditional sales channels of banking services in another selected country—in this case, Italy. The article compared traditional banking with online solutions. The results of the research showed that the ease of use and economic advantages seem to be more important in the early stages of using the services provided by banks. In addition, providing information regarding security (e.g., explaining security policies and guarantees) has a significant influence on customers: it encourages them to use the banking services in the first place, and it also helps to maintain customer loyalty with regard to using e-banking solutions.

In this context, it is also important to mention the research on changes in consumer behavior during the COVID-19 pandemic conducted by Kraenzlin et al. (2020) focusing on using payment cards in the retail sector in the Swiss market. The article examined two areas of interest, i.e., place/area of residence and specific sectors of the economy. The article showed the existence of significant changes that persisted after the lockdown was introduced. Marked changes were observed in the areas of tourism and e-commerce. Factors such as the risk of infection, remote work, shopping tourism and the replacement of cash with other payment methods were also identified as important aspects considered in the study. The authors indicated that the COVID-19 crisis strengthened the previously existing trends in terms of the use of payment cards.

In their research, Eger et al. (2021) focused on the changes with regard to shopping preferences in the context of generational changes during the COVID-19 pandemic in the Czech Republic. The research documented changes in consumer behavior patterns that were prevalent at the start of the second wave of the COVID-19 pandemic. The study compared consumers representing different generations: Baby Boomers, Generation X and Generation Y, showing how they changed their purchasing behavior and what shaped their preferences and their concerns during the pandemic crisis. The results showed that the fear factor (health and economic concerns) has a significant impact on customer behavior, both when shopping in a traditional way and engaging in online purchases.

Similar studies conducted by Santosa et al. (2021) concerning the influence the COVID-19 pandemic on people’s lifestyle, including baby boomers and X generation, showed that many of them have started using digital payments for online or offline transactions to minimize contact with others. In the research, authors proved that user satisfaction positively affects inertia. Overall satisfaction and inertia positively affect continuance intention. Therefore, digital payment companies and banks offering digital services can expand their target market beyond Millennials and pay more attention to the older generation like baby boomers and Generation X.

In turn, in their article, Valaskova et al. (2021) presented changes with regard to shopping preferences in the context of generational changes during the COVID-19 pandemic in other Visegrad country—Slovakia. The paper indicated the most important factors impacting consumers’ financial situation, as well as the effects on the continuation of new shopping habits established during the pandemic period. The findings obtained during the research appeared to be consistent with other global studies, confirming both the worldwide impact of the pandemic on consumer behavior and the importance of national studies on consumer shopping behavior.

Interesting studies concerning the influence of the COVID-19 pandemic on Chinese household consumption performed by Liu et al. (2020) showed that there was a significant decline in household consumption during the outbreak period. Analysis showed that the pandemic suppresses consumption in urban households; rural households are, however, less affected. It is important to note that mobile payments promote urban household consumption during the pandemic, while rural households remain unaffected.

The article “User Adoption of E-Payment Services Available in Mobile Wallets in Saudi Arabia during COVID-19 pandemic” indicated the key factors that influence user’s intention to adopt mobile payments. The additional factors discussed were security, trust, facilitating conditions, and lifestyle compatibility. The results indicated that user attitudes and intentions are positively influenced by all of the abovementioned factors. Perceived usefulness, perceived ease of use, lifestyle compatibility and facilitating conditions are direct predictors of user behavior in accepting mobile wallet payments (Alswaigh and Aloud 2021).

Other studies on identification of the factors inducing customers to choose cashless payments made with payment cards at retail and service outlets during the COVID-19 pandemic showed that, in addition to sociodemographic characteristics such as age and level of education, emotionally motivated factors induced by the pandemic have begun to play an important role in the transition to cashless payment (Huterska et al. 2021).

The study by Khatun et al. (2021), which explored the use of mobile banking services to accelerate people’s financial access in Bangladesh due to the emergence of the COVID-19 pandemic, pointed to the fact that the number of registered mobile banking customers has escalated. In the article, the authors showed that mainly government policies regarding different mobile banking transactions such as cash in, cash out, person to person (P2P) transaction, salary and utility bill payments, etc., have significantly increased the people’s digital financial access during the pandemic. Moreover, the recent tendency of Bangladeshi citizens to change their habits towards digital transactions has also contributed to increasing their interest in new technological solutions such as e-banking and m-banking.

In direct research on how the pandemic facilitates mobile payment in China, the authors, Zhao and Bacao (2021), aimed to investigate the technological and mental factors affecting users’ willingness to adopt mobile payments under the COVID-19 pandemic, to expand the domain of technology adoption under the emergency situation. The empirical results showed that users’ technological and mental perceptions conjointly influence their adoption intentions of mobile payment during the COVID-19 pandemic. Moreover, perceived benefits are significantly determined by social influence and trust, corresponding with the situation of the pandemic.

In research examining the factors influencing interest in the cross-border mobile payment use from the user perspective among Chinese citizens travelling to South Korea, the authors show that initial trust, performance expectancy, effort expectancy, facilitating conditions, price value and task technology fit have significant effects on use intention (Wu et al. 2021).

The aspect of the development of the use mobile payments in hospitality sector in the time of the COVID-19 pandemic was analyzed from point of view of customers who see its advantages in terms of not requiring physical contact. However, they may postpone adoption of the solution to wait for a more attractive iteration (Khanra et al. 2021).

The study by Vasenska et al. (2021), which examined changes in FinTech transactions during the COVID-19 crisis in Bulgaria, also pointed to the fact that these types of transactions lead to a reduction of risk involved in contacts with other people. Additionally, the authors of the paper proved that financial transactions using FinTech help customers to save money.

Interesting literature studies have dealt with the issue concerning the establishment and consistency of regulatory actions that may counteract the effects of the pandemic-related crises for the banking sector and consumer finance in Poland and other European Union countries. The conducted research has shown the existence of several social phenomena typical of this kind of global crisis, such as panic buying or reduced creditworthiness of households related to loss of income, unemployment and increased crime rates (Gębski 2021).

3. Methodology

The research was carried out using the CAWI (Computer Assisted Web Interview) method, similarly to other studies conducted during the COVID-19 pandemic. A questionnaire written in English, which is the research tool used in the analysis, was translated into Polish and Turkish with a focus on the clarity and unambiguity of the questions. LimeSurvey software was used to collect the results from the questionnaires.

In the study, the authors adopted the research procedure, which consisted of the following stages:

- Defining the purpose of the study and adopting the appropriate research procedure,

- Building a prototype of the questionnaire including the following steps:

- Identifying the mobile payment infrastructure and the impact of the pandemic on the changes in this area,

- Analyzing and describing the environment in which mobile financial transactions were carried out before and during the pandemic,

- Analyzing the use of the mobile payment infrastructure in Poland and Turkey before the pandemic and its changes during the pandemic,

- Verifying the questionnaire in terms of its comprehensibility and relevance with the participation of a pilot group of active m-payment users,

- On this basis, constructing the final form of the survey, placing and testing it on the servers of the University of Warsaw,

- Selecting a research sample and inviting the respondents to complete a survey questionnaire,

- Collecting data, initial processing of data and analyzing and discussing the findings,

- Calculating indicators of the differentiation of results between the findings in the analyzed countries,

- Drawing conclusions based on the research findings.

- The conducted survey included twenty-six questions. It consisted of three parts:

- Infrastructure information—the mobile device used, the length of time the mobile device is used, the impact of the COVID-19 pandemic on the purchase of a mobile device, and the mobile device operating system,

- Information about the environment in which mobile payments are made—the place (bank) where the respondent holds his or her main account, the impact of the COVID-19 pandemic on opening a bank account, the access to the bank account, the impact of the COVID-19 pandemic on the method of accessing the bank account, using a mobile device to support financial operations, the preferred method of handling financial operations, reasons for not using mobile devices to support financial operations or transactions, the impact of the COVID-19 pandemic on the use of a mobile device to support financial operations/transactions, the time (length) of use of a mobile device to support financial operations/transactions, the time of use of the bank’s mobile application, the advantages of using the bank’s website, the impact of the COVID-19 pandemic on the intensity of using the bank’s website, the advantages of using the bank’s mobile application and the impact of the COVID-19 pandemic on the intensity of using the bank’s mobile application,

- Information on the use of mobile payments during the COVID-19 pandemic—tools used to implement mobile payments during the COVID-19 pandemic, types of mobile payments used, the impact of the COVID-19 pandemic on the number of mobile payments, the advantages of using mobile applications to make payments during the pandemic COVID-19, the advantages of using the website to make mobile payments during the COVID-19 pandemic, the types of mobile payments used during the COVID-19 pandemic and preferences concerning specific forms of delivery before the COVID-19 pandemic and preferences regarding the forms of delivery used during the COVID-19 pandemic.

The simple and transparent form of the questionnaire did not cause great difficulties when completing it, and respondents in a few cases (only 51 people in total from both countries) provided additional comments (e.g., additional forms of mobile payments they also use).

The study carried out with the use of a CAWI (Computer-Assisted Web Interview) method was conducted simultaneously in Poland and Turkey at the beginning of March 2021 on a sample of 645 respondents. In Poland, 395 people answered all the questions of the survey, and in Turkey this share amounted to 250 respondents. Among the study participants in Poland, 72% were women and 28% men. In Turkey, the proportions in the study sample were slightly different—women accounted for 53% of the respondents and men 47%.

The survey was conducted among students of two universities: the University of Warsaw (Poland) and the University of Uşak (Turkey). Considering the population, it was a case of purposeful sampling. However, the selection of respondents from this particular group was based on a random choice: the selected groups were asked to complete the survey questionnaire. This was the reason why all respondents from Poland were aged 19–35, and this age group also constituted over 94% of the Turkish sample. Such demographic characteristics are typical for undergraduate and graduate students. Few people (less than a 6% share) in Turkey were representatives of other age groups. The student community is the most active group when it comes to using smartphones and laptops and performing all commercial operations, including banking and payment transactions. This specific population is most open to technical innovations, and mobile payments are regarded as such. There is also a visible difference between the previously indicated education levels of the respondents—in Poland, secondary education appeared to be a dominant indication in the study (89%, where most of the respondents were undergraduate students), and in Turkey 93% of students had a bachelor’s degree. The demographics reflect the fact that the questionnaire was sent to individuals who participated in MA studies. In Poland, the largest number of respondents came from cities with more than 200,000 inhabitants (41%) and the countryside (23%). In Turkey, 54% also come from cities with more than 200,000 residents, and 18% from cities with 51–200 thousand inhabitants. Seventy-five percent of the surveyed students from Poland study social sciences, i.e., sociology, economics, administration, law and management; 14% of the respondents study exact sciences, including mathematics and computer science; and only 10% of the share are students of banking, finance and accounting. The respondents in Turkey study banking, finance and accounting (44%); 40% of the share are students of social sciences; and 7% of the sample study science. Their financial situation also differs—in Poland, 86% of students consider their situation to be good (I do not complain, but it could be better) or very good (I have enough money to afford everything I need, I can save some money); in Turkey, such opinion is expressed by 28% of the sample. In contrast, in Turkey, the largest number of students (58%) consider their situation to be satisfactory (they still make ends meet) and average (they have enough money to lead a frugal life). Similar differences also exist in terms of the respondents’ professional status. In Turkey, 92% of the surveyed population are only students, and nearly 7% work under a contract of employment, run a business or work part-time. Correspondingly, 49% of respondents in Poland declare studies to be their only occupation, almost 22% perform occasional or temporary work, and more than 22% indicate permanent employment. Among students working full-time or part-time, the greatest number of students have office jobs or administrative positions (Poland—56%, Turkey—27%). Professions related to services are also popular (in Poland they account for 29% of the respondents, and in Turkey they constitute 14% of the share). On the other hand, 15% of respondents in Turkey perform simple physical work (vs. 5% in Poland), and 14% of respondents in Turkey perform jobs in the agricultural sector (vs. 1% in Poland). Professions such as specialists (11%) and managerial staff (10%) are also very popular in Turkey. In Poland, the above-mentioned occupations do not exceed the level of 6%.

Despite functioning in a similar environment, there are differences in the surveyed populations. The differences are established with the application of the calculated indicators of city distance and Euclidean distance (Table 1).

The biggest differences, as already mentioned, result from the discrepancies in the previous education levels declared by the respondents. The difference was caused by the random choice of student groups selected for the survey. In Poland, the respondents were mainly representatives of groups of undergraduate students (declaring having secondary education), and in Turkey they were graduate students (undergraduate education). The percentage differences exceeded 80% in both cases. Therefore, such a high deviation from the standard occurred. The second major difference was the respondents’ assessment of their financial situation—over 86% of respondents in Poland consider their situation to be very good and good, while almost 71% of respondents in Turkey assess it as average, satisfactory or bad. Hence, such high distance indicators were recorded in the study. Smaller differences between the individual criteria (attributes) lead to a lower value of the standard deviation. The presented differences influenced the obtained results.

The research sample was selected in a convenient, purposeful and partially random manner. The convenience resulted from the fact that work at the university and knowledge of the academic environment makes it easier for academics to approach student groups asking them to fill in the questionnaire. In addition, this group is highly motivated to participate in this type of analysis, because in this way the students engage in the research that might be useful in writing and defending their theses. It is a case of purposeful sampling because it is an age group interested in the subject related to the use of internet transactions. Most people in this group use the latest technologies in their everyday life, study and work (over 70% of students at the University of Warsaw are working at the same time). Therefore, this part of the population may be seen as a specific expert group that has knowledge and practical experience in the field of mobile payments and electronic business, often setting the standards of behavior in the future. Additionally, it is important to indicate that it was a case of a partially random selection because invitations to complete the questionnaire were sent out to individual student group selected at random. Therefore, the questionnaire was filled in by individuals with the greatest access to mobile devices and who had generally used them the longest.

All mobile devices such as smartphones and tablets were included in the category of mobile devices, but laptops were excluded from this group. For the purpose of this study, electronic payments were treated as software providing both access to banking services via internet browsers and through advanced applications dedicated to mobile devices.

The Cronbach’s alpha coefficient was used to analyze the data reliability. In all examined questions, Cronbach’s alpha indicates the internal consistency and reliability of the sample (Hinton et al. 2004). The internal consistency of the 25 dependent variables for the two compared countries, based on Cronbach’s coefficient alpha, amounted to 0.71.

Distances were calculated as the absolute distance of each sub-criteria within the criteria, city distance and Euclidean distance.

In addition, hypothesis H0, which was put forward in the study, concerned the lack of difference between Poland and Turkey in terms of the size of individual criteria, against hypothesis H1 regarding the existence of differences, with the assumed probability of 0.05. The adopted hypothesis was based on one of the clear differences between the studied countries, which is the cultural influence. Poland is in the circle of Latin culture, while Turkey is influenced by both Latin and Islamic cultures. In order to prove this hypothesis, the significance level of α was calculated for the probability distribution of the Fisher–Snedecor inverse (right-hand) value. It can be used in the Fisher–Snedecor test to compare the degree of variability of two datasets for two populations (including a study of the distribution of assessment differences in the opinions concerning the impact of the COVID-19 pandemic on electronic payments between Poland and Turkey) and to compare it with the critical value of Kr determined based on test statistics. If K ≤ Kr, then we reject H0 and accept H1; if p ≥ α, then we reject H0 and assume H1 is true. The critical value of p for this distribution is 1.98.

4. Analysis of the Results

In both countries, the most frequently owned mobile device is a smartphone: in the case of Poland, the share amounted to 99%, and in Turkey, it was 98%. On average, the tablet is owned by only about 0.6% of people. More than 94% of respondents in Poland have used mobile devices for over four years, while in Turkey the share was estimated at slightly more than 60%. In the case of mobile devices used for one to four years, such mobile devices in Poland are used by less than 5% of the respondents and in Turkey by more than 20%. It follows that, in Poland, people started to use mobile devices, in particular smartphones, slightly earlier. In addition, 26% of Polish respondents believe that the COVID-19 pandemic did not affect the purchase of this device, a further 59% already had such a device, and 10% say they have bought it regardless of the pandemic. Only less than 5% of respondents in Poland acknowledge the impact of the pandemic on the purchase of a mobile device. Overall, about 95% of students own mobile equipment regardless of the pandemic. In Turkey, more than half (54%) of the respondents already had a mobile device before; 12% bought it, as they declared, regardless of the pandemic; and 7% believe that they purchased it regardless of the pandemic (73% in total). However, as many as 25% of the purchases of mobile equipment were associated with the outbreak of the COVID-19 pandemic.

Interestingly, in Poland, during the pandemic, the quality of the equipment is being revalued, despite some inconveniences related to the teaching methods (cooperation with other devices). For the first time, in relation to the previously conducted research (Chmielarz 2020), devices with the iOS system constitute more than half of the share (53%). The proportions in 2020 in Poland were similar to the current findings in Turkey, i.e., the survey results in Turkey show that there are 2/3 devices with the Android operating system and 1/3 with the iOS operating system. In Poland, it was probably a case of a specific compensation for pandemic restrictions. As can be seen, students in Turkey are more rational about purchasing mobile devices, taking into account the need of coordinating their work with the external environment. The results also show the disappearance of the Windows operating system—the indications, on average, are estimated at 1%. Information about respondents’ mobile devices is directly related to the technology necessary for the implementation of financial mobile operations.

However, mobile payment operations can be performed with the use of a banking website or a mobile application. In each of these options, the bank provides the “basis” on which financial operations/transactions are to be performed. It is difficult in this case to compare banks in Poland and Turkey, but in the case of this study, it is an interesting issue to consider. In both countries, the distribution of responses focused on holding accounts in 4–5 banks. In Poland, the respondents declared using the services of commercial banks with well-developed internet banking (mBank SA 25%, Bank Millenium SA 11%, ING Bank Śląski SA 11%) and the largest state-owned bank, PKO Bank Polski (28%), at which 75% of respondents have their accounts. In Turkey, the respondents indicate holding an account in a state-owned bank Türkiye Cumhuriyeti Ziraat Bankası A.Ş. (43%), which has a long tradition of operating in the market (since 1863); Türkiye İş Bankası A.Ş. (11%), Turkey’s largest bank; Yapı ve Kredi Bankası A.Ş., one of the first domestic commercial banks (9%); and Türkiye Halk Bankası A.Ş. (almost 8%), which together constitute a 71% share of all the responses.

During the COVID-19 pandemic in Poland, 11% of respondents opened a bank account with their bank, and in Turkey, the share was estimated at 30%. In Turkey, the respondents mainly used their mobile applications (85%) to communicate with the bank. In Poland, this constituted 46% of the survey answers, slightly less than in the case of simultaneous use of the mobile application and the bank’s website (48%), while 13% of respondents in Turkey and 6% in Poland access the account only through the bank’s website. During the COVID-19 pandemic, as many as 37% of respondents changed the way of communicating with the bank, mostly to mobile solutions, and only 2% of the survey participants in Poland stated that they have changed the method of accessing banking services in the last period.

The analysis of the financial sectors in both countries allows the authors to describe the ways in which mobile devices are used to service finances. Over 97% of respondents in Poland use mobile devices (smartphones or tablets) to handle their finances. Accordingly, 83% of survey participants in Turkey use mobile devices to handle their finances, and 17% do not use such solutions.

In Poland and Turkey, the services purchased with the use of a mobile application appear to be the most popular option among the respondents. In both countries, the indications are at a similar level (36% each). In order to handle complex, high-value operations and transactions, the respondents in Poland use the services provided by consultants (35%). A similar situation occurs in Turkey (32%). In terms of handling financial operations in Poland, the bank’s website accessed via mobile devices (19%) has a clear 8% advantage. Although all banks in both countries already have versions of websites adapted to the needs of smartphone users, they are usually seen as less convenient or intuitive than applications that are dedicated to this purpose. IVR operations show an almost two-fold advantage (13%) in Turkey (Table 2).

When asked about the reasons for not using mobile devices to manage their financial services, respondents from both countries provided different answers. After reducing them to the common denominator, in Poland, the indications were related to greater convenience, functionality and certainty in using the banking service with a laptop (21%), greater security (21%) and no need to use mobile equipment (14%). In Turkey, the greatest share of responses, in this case, concerned no need to use mobile hardware and software (43%), and 11% of the respondents pointed to creating a budget manually on paper. A similar share indicated the advantages of using a laptop and banking website over using a smartphone or tablet. In total, this applied to a small group of individuals—3% in Poland and 14% in Turkey.

During the COVID-19 pandemic, the situation regarding the use of mobile devices to carry out financial operations has changed dramatically in Turkey. Namely, 77% of Turkish respondents admit that, as far as financial services are concerned, the outbreak of the pandemic was the reason why they started to use mobile solutions. In Poland, less than 15% of the survey participants stated that they resorted to using mobile payments due to restrictions imposed by the COVID-19. This indicates that mobile payments were commonly used in Poland even before the pandemic.

In order to enable further comparative analyses of both samples, the respondents in Poland and Turkey were also asked about the time of use of e-banking websites and m-banking applications. The findings show that the respondents in Poland use the bank’s website mainly for 2 to 4 years (49%) or over 4 years (37%). In Poland, only 13% of respondents declare that they started to use banking websites since the beginning of the pandemic. In Turkey, the largest share (47%) uses the banking website for one to two years (which shows that they only started using it during the pandemic), and 44% of respondents use the bank’s website for 2 to over 4 years.

The findings related to the time of use of m-banking applications in both countries are largely consistent with the previous results concerning the use of e-banking websites. In this case, the majority of Polish respondents (54%) use the bank’s mobile application for two to four years, and 22% (less than half of the share) use it for 1–2 years. By contrast, in Turkey, more than half of the respondents (57%) have been using mobile applications since the outbreak of the COVID-19 pandemic.

Another problem to be explained was the reason why the website was used to communicate with the bank. The results are presented in Table 3.

Respondents from both countries pointed primarily to two aspects: convenience and time saving (around 42% of respondents) and the safety of banking operations (27% on average). Recommendations from friends or family members and recommendations of bank employees also played an important role. In the opinion of survey participants, the intensity of using the bank’s website has not changed (72% of opinions of the respondents from Poland and 61% from Turkey). On the other hand, 19% of survey participants from Poland believe that it has increased slightly (16% from Turkey), and 13% of respondents in Turkey even think that it has decreased slightly (at the expense of banking applications).

A similar question, as in the case of websites, was asked in relation to the bank’s mobile applications. The reasons for using them turned out to be similar in both countries. First of all, for almost half of the respondents (on average, 46%; in Poland, 50%; and in Turkey, 41%), convenience and time saving turned out to be the most important factors. Secondly, the security issues of banking operations were also important: on average, 23%; in Poland, 21%; in Turkey, 26%. The third important reason was recommendations from friends or family members.

According to the opinion of 61% of respondents in Poland and 29% in Turkey, the intensity of using mobile applications since the beginning of the COVID-19 pandemic has not changed. In contrast, in Turkey, the majority (68%) of respondents believe that it has increased slightly or has increased significantly. The view that it has increased slightly is also supported by 30% of m-banking users in Poland.

Among mobile payment systems used by the respondents, which are listed in Table 4, in Poland, BLIK (Polish payment standard) was the most frequently used solution (27%). The most frequently used payment method in Turkey (10%) was Apple Pay, which ranks fourth in Poland. In Poland, electronic payments Dotpay/Przelewy24 took second place with an 18% share of the respondents, and PayU was third in the ranking reaching almost 18% of indications. In Turkey, Google Pay (9%) was second and Pay Pal (6%) was third. Pay Pal in Poland is used by nearly 9% of the respondents. In Turkey, there is a large group of people (26%) who declaratively do not use mobile payments; in Poland, such responses account for less than 2%. Similarly, in Turkey, 21% of respondents say that they use mobile payments but do not remember the specific name of the service provider. The latter appears to be a completely marginal phenomenon in Poland.

Table 4 presents only the “technical” side of the issue under consideration—that is, what electronic payment tools are most often used by respondents. As previously stated, this, naturally, constitutes only a part of electronic financial operations. Nevertheless, a significant research problem that needs to be examined in this context is an area where mobile payment methods are most commonly used. The relevant findings of the analyses are presented in Table 5.

Undoubtedly, the most frequently used mobile services in both countries are online payments on the Internet and parking fees (at the level of 12%). The situation is similar in the case of the purchase of tickets for all journeys (11–12%). In Poland, a similar tendency (12%) may be observed in the case of transfers between persons (Person2Person) and purchases of all kinds of tickets (11%). In the survey conducted in Turkey, 11% of the respondents pointed to the possibilities related to ATM withdrawals and payment of bills and invoices.

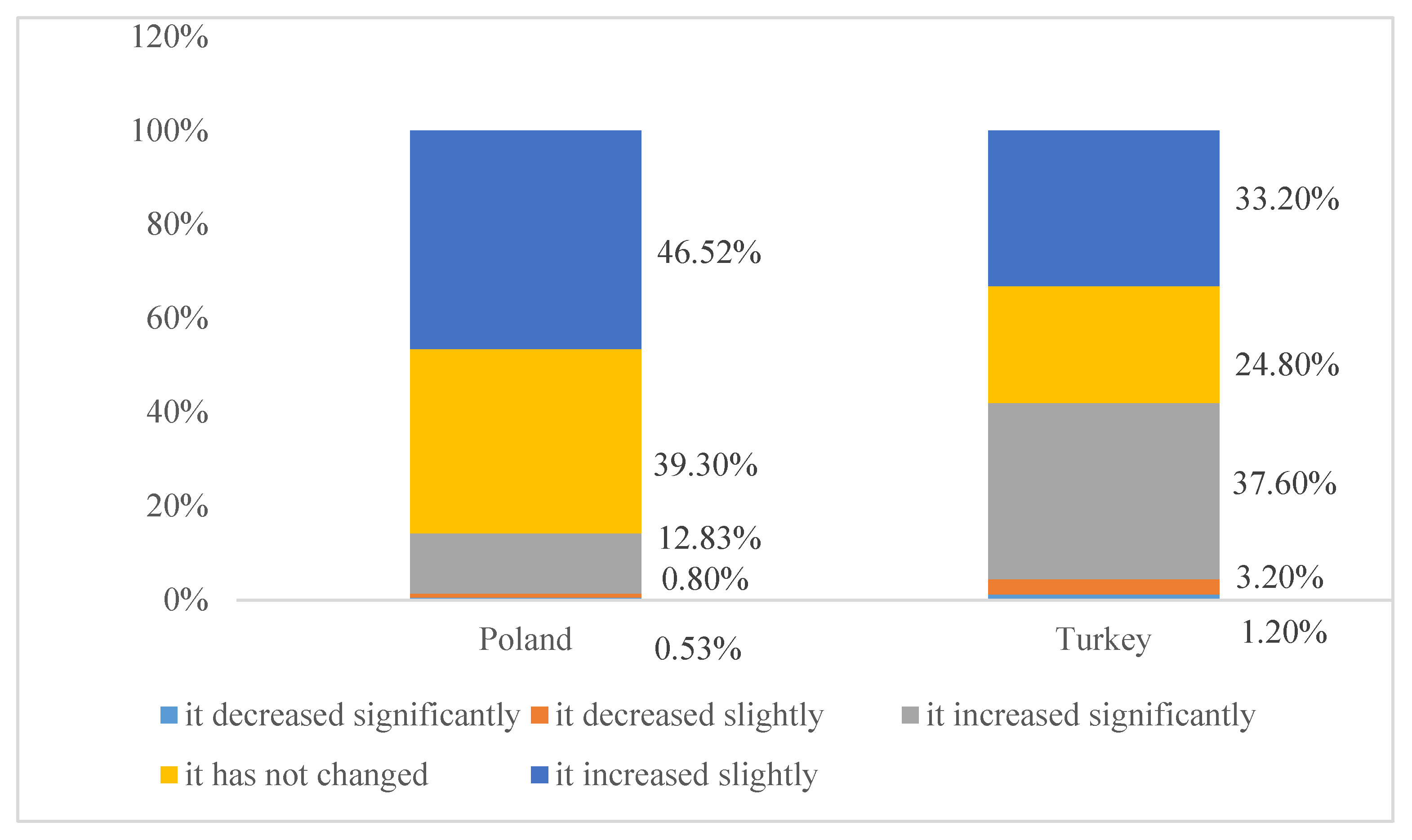

The scale of changes in mobile payments since the beginning of the COVID-19 pandemic was also examined by the authors. The highest number of responses in both countries was obtained by the response “it increased slightly” (47% in Poland, 33% in Turkey). The second position was taken by the opinion “it has not changed” (Poland—39%, Turkey—25%). One may also notice the large share of opinions among the Turkish respondents regarding the category “it increased significantly”—38%. In total, 71% of respondents in Turkey saw an increase in mobile payments since the outbreak of the COVID-19 pandemic; in Poland, the number of such responses was estimated at the level of 60%. On the other hand, in Poland, 14% fewer people than in Turkey perceived changes in terms of the number of mobile payments made during the pandemic (Figure 1).

The next two questions concerned the choice of the bank’s mobile application for payments or the tools available at the bank’s website.

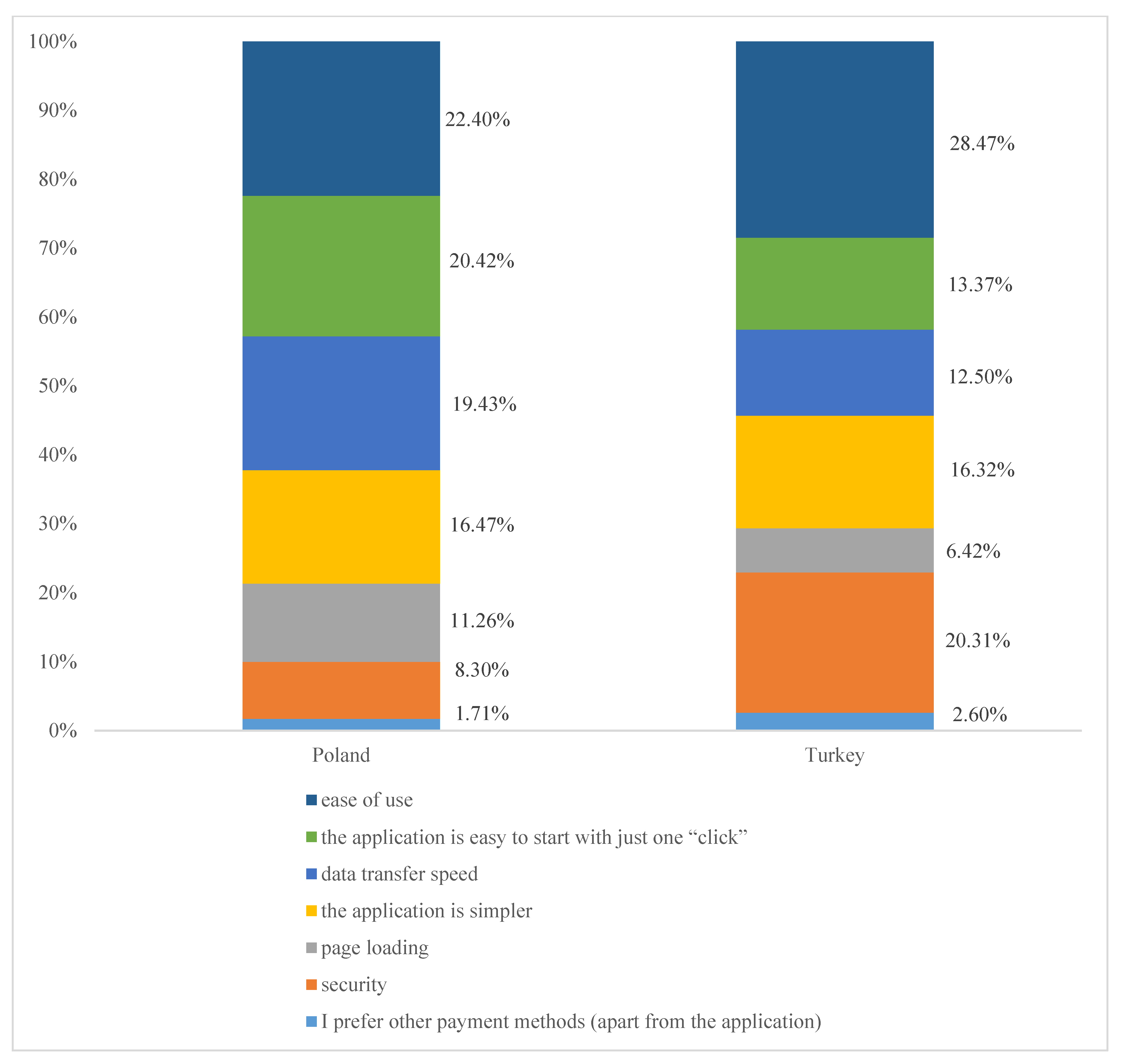

In the first case in Poland, the respondents mainly pay attention to the ease of use (22%), ease of starting the application with one “click” (20%) and data transfer speed (19%). In Turkey, the ease of use also ranked first (28.47%), security took second place (20%) and the simplicity of using the application was the third most common indication in the ranking (16%) (Figure 2).

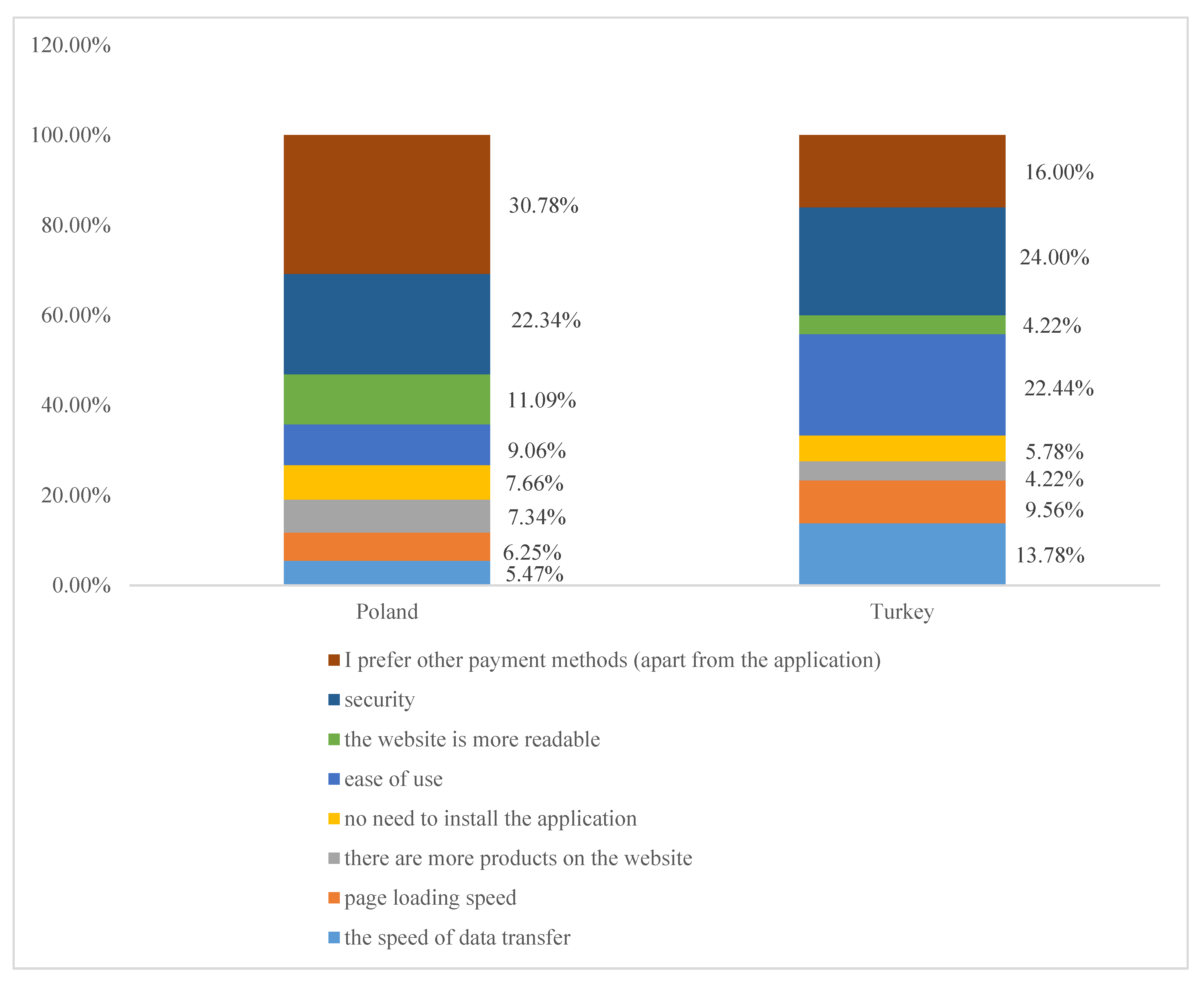

In the second case, the respondents in Poland point to the existence of other forms of payment (31%), security (22%) and greater readability of the website (11%). In Turkey, security (24%), ease of use (22%) and more products and functionalities on the bank’s website (16%) were among the first responses of the survey participants (Figure 3).

In the study, the authors distinguished various types of activities where we deal with mobile payments. The respondents’ opinion regarding the changes that have occurred in mobile payments related to particular areas appears to be one of the most interesting issues in the research. The previously indicated users’ lack of knowledge regarding the provider of mobile payments shows that such services are often perceived primarily through the prism of the functionalities they offer.

In Poland (Table 6), the indication “it decreased significantly” (50% of opinions) concerned mainly purchasing e-tickets and was caused by the closure of cinemas, theatres, music events, etc. In addition, attention was drawn to a significant reduction and a slight reduction (30%) of ticket purchases for all types of journeys due to traffic restrictions and the closure of hotels and restaurants. Additionally, sales from vending machines offering drinks, sweets and sandwiches showed similar tendencies. In turn, traffic restrictions and accumulation of purchases resulted in a slightly lower indication related to payment for purchases in shops and service points (POS) (22%) and a reduction in parking fees (12%). The restrictions imposed on business activity led to a slight reduction in the case of authorization of persons or services. No changes were noticed in terms of mobile top-ups (12%) and ATM withdrawals (10%), caused mainly by the common use of electronic payments. On the other hand, online payments on the Internet (31%), purchases of digital content (movies, games and music) (21%), payment of bills (18%), e-wallet expenses (16%) and use of gift cards (14% of the responses) increased (slightly or significantly).

In Turkey, the opinions of the respondents were very similar, and only the structure of payments for individual products and services changed slightly. First of all, payments for the purchase of e-tickets for cultural events also decreased significantly (31%; 41%, in total with the opinion “it decreased slightly”), similarly to the purchase of tickets for public transport, intercity and rail transport (19%; 41% in total with the opinion “it decreased slightly”). The largest percentage of opinions “it decreased slightly” (19%; 26% together with indications “it decreased significantly”) was recorded with regard to paying for purchases in shops and service points (POS). The total number of mobile phone top-ups also decreased by almost 9%. There were no changes in the amounts of car parking fees (10%), authorization of persons or services (9%), broadly understood access control (9%) and cash withdrawals from ATMs (8%). The largest increase (adding up the indications of “it increased slightly” and “it increased significantly”) was noticed in terms of mobile payments on the Internet (19%), payment of bills and invoices (bill payment, i.e., telecommunications, utilities—18%), purchases in vending machines with drinks, sweets and sandwiches (16%), purchase of a gift card offered by chain stores to be used at specific points of sale (16%) and expenses from the e-wallet for payments and settlements (15%). In Turkey, according to the respondents’ opinions, the changes in mobile payments concerning the distinguished products and services were similar to trends observed in Poland, but their structure was more balanced (Table 7).

The last item examined in the study was the issue of deliveries. It is indirectly related to mobile payments because the price of the product often depends on the choice of the method of delivery of physical goods (e.g., in the case of mobile payment services on the Internet or the use of the e-wallets for payments and settlements). As a result, mobile payments also depend on delivery. However, it is sometimes difficult to directly link the choice of the delivery method with the type of payment made. In Poland, the highest increase was recorded in the case of the collection of physical goods via a parcel locker (previously paid or paid for before collection), i.e., over 8% increase to the level of 52% as well as the direct collection of goods, ordered by a mobile phone, at a pickup point or in store (16%). Deliveries by a specialized delivery company (25%) also became popular. In Turkey, post office delivery (29%), direct collection at a store or a designated pickup point (an indication of 26%, the greatest increase estimated at 12%) and pickup by a specialized delivery company (17%) have become the most popular options. The popularity of collecting the goods directly at the store or from a pickup point may result from the fact that you do not have to pay for delivery in such a case.

5. Discussion of Results

The largest discrepancies in the assessments occurred in the group of indicators concerning the use of mobile payments during the COVID-19 pandemic. The fact that they concerned the tools used to implement mobile payments during the COVID-19 should not come as a surprise. The largest number of respondents in Poland declared using the BLIK mobile payment system, i.e., a Polish payment solution, which is not available in Turkey. There were also differences at the level of 20% in the case of Turkey in such categories as “I use mobile payments, but I do not remember the specific name of the service provider” and “I do not use mobile payments”. There were also significant differences in handling the delivery of physical goods before and during the COVID-19 pandemic. During the COVID-19 pandemic in Poland, deliveries by parcel lockers and specialized delivery companies have prevailed; in Turkey, pickup directly in the store and delivery by post appear to be the most popular options among consumers. A similar situation also existed before the start of the pandemic.

There are also marked differences in the survey section related to the information on the environment in which mobile payments are carried out. In this group, the opinion about the impact of the COVID-19 pandemic concerning the moment when the respondents started using mobile devices is the factor that differentiates the groups of respondents. In Poland, survey participants believe that the COVID-19 pandemic had no impact on the use of mobile payments; in Turkey, the opinion of respondents seems to be quite the opposite. Opinions also differ as to why mobile devices are not used to support financial operations/transactions. In the Turkish group of respondents, it is a lack of interest in this form of service (43%); when the Polish sample was surveyed, the study participants pointed out greater security and convenience; functionality; and confidence in accessing the banking website using a laptop. The method of accessing bank accounts is also worth noticing—in Poland, access is preferred via the bank’s website using a laptop or mobile device or via mobile applications. The place, i.e., the bank where the respondent holds the account used for mobile operations is a separate issue in the survey. It emerges that most of the respondents use the accounts located in the largest domestic banks (and not international banking institutions). Therefore, the data obtained in the surveys were incomparable and only gave an idea of the concentration of mobile financial services in a specific group of banks. The results obtained from comparing the absolute and Euclidean distances confirm the results of the Fisher–Snedecor inverse test. To calculate the critical value of the F distribution, with the assumed probability α = 0.05 and with 24 degrees of freedom of the numerator and denominator for the F distribution, the critical value is Fkr = 1.98. Therefore, the presented hypothesis H0 concerning the lack of statistically significant differences between Poland and Turkey for all calculated values of F < Fkr does not apply in other cases. This situation concerns the time of use of a mobile device, method of accessing a bank account, the impact of the COVID-19 pandemic on the method of accessing a bank account, use of a mobile device to support financial operations/transactions, reasons for not using mobile devices to support financial operations/transactions, the impact of the COVID-19 pandemic on the use of a mobile device to support financial operations/transactions, types of tools used to make mobile payments during the COVID-19 pandemic, types of mobile payments used during the COVID-19 pandemic, preferences concerning forms of delivery before the COVID-19 pandemic and preferences regarding forms of delivery during the COVID-19 pandemic. Nevertheless, the H0 hypothesis was positively verified in fifteen out of twenty-five cases. The criterion/attribute of banks used in the mobile payment process, by definition, turned out to be a separate research problem because the respondents preferred domestic rather than international banks and the responses, as a result, turned out to be incomparable.

Detailed differences between the criteria (attributes) applied in the assessment of mobile payments in Poland and Turkey in 2021 are presented in Table 8.

6. Conclusions

Despite the discrepancies in the random sample, in 60% of cases, no statistically significant discrepancy between the results for Poland and Turkey was found. In the remaining cases, these differences resulted from the earlier development of mobile technologies in Poland. This was also the reason why the COVID-19 pandemic exerted a greater impact on the acceleration of the development of mobile payments in Turkey and, together with other factors, on the acceleration of globalization processes. Even if it was a situation caused by extraordinary circumstances, it still led to a specific levelling of differences, i.e., bridging the gap between the analyzed countries in a relatively short time. It also came as no surprise that during the COVID-19 pandemic, the purchases of e-tickets and tickets for public transport, coaches, etc., as well as paying for purchases in shops and service points (POS), decreased in the analyzed countries.

Additionally, a natural consequence, in this case, was the increase in mobile payments on the Internet, payment of bills and invoices (i.e., telecommunications, utilities, bills), and P2P transfers and downloading digital content (movies, music, computer games), all of which were associated with purchasing processes of products and services.

The impact of the COVID-19 pandemic on mobile payments turned out to be smaller than the common views shared in the surveyed community. The almost complete use of mobile devices within the studied groups is also an interesting phenomenon. The latter also reflects the potential use of such solutions in the area of payment processes. The widespread use of smartphones means that they can largely replace laptops, as evidenced by the responses of the examined population. Despite their limited functionality, in everyday life, they seem to fulfil their role very well. The convenience and popularity of mobile payments appear to support the above claim.

The results obtained in the study depended on the academic environment where the research was conducted. Undoubtedly, the surveyed population is most active in terms of various aspects of Internet activity. However, at present, the findings of the research cannot be easily generalized to include the entire population. The case is different if we consider the immediate future. The examined group is the generation that is most familiar with all types of electronic devices and their use (ICT), and as such, they will set the tone for future developments in this field. However, to obtain a full picture of the situation, both the size of the sample and the social reach of the research should be increased since the present assessments were limited only to students of large universities in Poland and Turkey. If the research were extended to include other social groups, the findings could be generalized. The issue related to using mobile payments and its diversification in countries with different cultures and levels of economic development appears to be significant, and therefore it should also be extended to cover other countries and regions. At this point, another significant aspect of the COVID-19 era emerges:

… The pandemic and subsequent lockdowns made many companies accelerate the process of digital transformation, focusing on the development of online channels […]. Importantly, almost 85% of Poles declare that even after the end of the pandemic, they do not intend to reduce the frequency of e-shopping. Thus, we may expect steady double-digit growth for the coming years….

The cited quotation proves that even though the period of the COVID-19 pandemic did not affect the dynamics of e-payments as much as it seems in the so-called popular opinion, the effects of this increase will also be visible in the future.

The conclusions that have been drawn based on the presented study focused on examining and comparing the use of mobile payments in the surveyed countries. On the one hand, the findings indicate a strong need to continue the comparative analyses of the examined phenomena involving respondents representing different populations and nationalities. On the other, they also point to the necessity to extend such research to include also other areas of ICT use. For example, subsequent studies may consider the impact of the pandemic threat of COVID-19 on changes occurring in terms of the propensity to use cryptocurrencies.

The results of the conducted research and the conclusions drawn on their basis may provide valuable information to organizations planning to introduce new electronic banking solutions in the analyzed markets, in particular mobile payments. The findings may also be useful both from the point of view of the development of the organization and the readiness of its employees to adopt new technologies as well as from the perspective of end customers of such solutions.

Author Contributions

Conceptualization, W.C., M.Z., A.F. and M.A.; methodology, W.C., M.Z., A.F. and M.A.; software, W.C., M.Z., A.F. and M.A.; validation, W.C., M.Z., A.F. and M.A.; formal analysis, W.C., M.Z., A.F. and M.A.; investigation, W.C., M.Z., A.F. and M.A.; resources, W.C., M.Z., A.F. and M.A.; data curation, W.C., M.Z., A.F. and M.A.; writing—original draft preparation, W.C., M.Z., A.F. and M.A.; writing—review and editing, W.C., M.Z., A.F. and M.A.; visualization, W.C., M.Z., A.F. and M.A.; supervision, W.C., M.Z., A.F. and M.A.; project administration, W.C., M.Z., A.F. and M.A.; funding acquisition, W.C., M.Z., A.F. and M.A. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Alswaigh, Noha Y., and Monira E. Aloud. 2021. Factors Affecting User Adoption of E-Payment Services Available in Mobile Wallets in Saudi Arabia. International Journal of Computer Science & Network Security 21: 222–30. [Google Scholar] [CrossRef]

- Chen, Xiaogang, Libo Su, and Darrell Carpenter. 2020. Impacts of Situational Factors on Consumers’ Adoption of Mobile Payment Services: A Decision-Biases Perspective. International Journal of Human–Computer Interaction 36: 1085–93. [Google Scholar] [CrossRef]

- Chmielarz, Witold, ed. 2016. Mobilne Aspekty Technologii Informacyjnych. Warszawa: Wydawnictwo Naukowe Wydziału Zarządzania Uniwersytetu Warszawskiego, ISBN 978-83-65402-25-7. [Google Scholar]

- Chmielarz, Witold. 2020. The Usage of Smartphone and Mobile Applications from the Point of View of Customers in Poland. Information 11: 220. [Google Scholar] [CrossRef] [Green Version]

- Eger, Ludvík, Lenka Komárková, Dana Egerová, and Michal Mičík. 2021. The Effect of COVID-19 on Consumer Shopping Behavior: Generational Cohort Perspective. Journal of Retailing and Consumer Services 61: 102542. [Google Scholar] [CrossRef]

- Filotto, Umberto, Massimo Caratelli, and Fabrizio Fornezza. 2021. Shaping the Digital Transformation of the Retail Banking Industry. Empirical Evidence from Italy. European Management Journal 39: 366–75. [Google Scholar] [CrossRef]

- Gębski, Łukasz. 2021. The Impact of the Crisis Triggered by the COVID-19 Pandemic and the Actions of Regulators on the Consumer Finance Market in Poland and Other European Union Countries. Risks 9: 102. [Google Scholar] [CrossRef]

- Górka, Jakub. 2016. Ewolucja funkcjonalna mobilnego portfela (title in English: Mobile Wallet Functional Evolution). In Obrót Bezgotówkowy w Polsce: Stan Obecny i Perspektywy. Lublin: Wydawnictwo KUL, pp. 119–30. ISBN 978-83-8061-218-1. [Google Scholar]

- Górka, Jakub. 2018. Banki, GAFAM, FinTech w gospodarce współdzielenia—Equilibrium współpracy i konkurencji. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 531: 149–58. [Google Scholar] [CrossRef]

- Hinton, Perry, Isabella McMurray, and Charlotte Brownlow. 2004. SPSS Explained, 1st ed. London: Routledge, ISBN 978-0-415-27409-8. [Google Scholar]

- Hossain, Syed Far Abid, Zhao Xi, Mohammad Nurunnabi, and Khalid Hussain. 2020. Ubiquitous Role of Social Networking in Driving M-Commerce: Evaluating the Use of Mobile Phones for Online Shopping and Payment in the Context of Trust. New York: SAGE. [Google Scholar] [CrossRef]

- Huterska, Agnieszka, Anna Iwona Piotrowska, and Joanna Szalacha-Jarmużek. 2021. Fear of the COVID-19 Pandemic and Social Distancing as Factors Determining the Change in Consumer Payment Behavior at Retail and Service Outlets. Energies 14: 4191. [Google Scholar] [CrossRef]

- Kala, Kamdjoug, Jean Robert, Serge-Lopez Wamba-Taguimdje, Samuel Fosso Wamba, and Ingrid Bive’e Kake. 2021. Determining Factors and Impacts of the Intention to Adopt Mobile Banking App in Cameroon: Case of SARA by Afriland First Bank. Journal of Retailing and Consumer Services 61: 102509. [Google Scholar] [CrossRef]

- Kemp, Simon. 2021. Digital 2021: Global Overview Report. Datareportal. Available online: https://datareportal.com/reports/digital-2021-global-overview-report (accessed on 2 February 2021).

- Khanra, Sayantan, Amandeep Dhir, Puneet Kaur, and Rojers P. Joseph. 2021. Factors Influencing the Adoption Postponement of Mobile Payment Services in the Hospitality Sector during a Pandemic. Journal of Hospitality and Tourism Management 46: 26–39. [Google Scholar] [CrossRef]

- Khatun, Most Nilufa, Sandip Mitra, and Md Nazirul Islam Sarker. 2021. Mobile Banking during COVID-19 Pandemic in Bangladesh: A Novel Mechanism to Change and Accelerate People’s Financial Access. Green Finance 3: 253–67. [Google Scholar] [CrossRef]

- Khosrow-Pour, Mehdi, ed. 2008. Encyclopedia of Information Science and Technology, 2nd ed. Hershey: IGI Global, vol. 8, ISBN 978-1-60566-026-4. [Google Scholar]

- Kraenzlin, Sebastien, Christoph Meyer, and Thomas Nellen. 2020. COVID-19 and Regional Shifts in Swiss Retail Payments. Swiss Journal of Economics and Statistics 156: 14. [Google Scholar] [CrossRef] [PubMed]

- Krueger, Malte. 2016. Mobile Payments: The Second Wave. In Transforming Payment Systems in Europe. Edited by Jakub Górka. Palgrave Macmillan Studies in Banking and Financial Institutions. London: Palgrave Macmillan UK, pp. 214–35. ISBN 978-1-137-54121-5. [Google Scholar]

- Łaptaś, Grzegorz. 2021. W ciągu 5 lat rynek e-commerce w Polsce osiągnie wartość 162 mld zł. Available online: https://www.pwc.pl/pl/media/2021-02-09-analiza-pwc-prognoza-rozwoju-rynku-ecommerce-w-polsce.html (accessed on 27 June 2021).

- Liu, Taixing, Beixiao Pan, and Zhichao Yin. 2020. Pandemic, Mobile Payment, and Household Consumption: Micro-Evidence from China. Emerging Markets Finance and Trade 56: 2378–89. [Google Scholar] [CrossRef]

- Majchrzyk, Łukasz. 2020. Raport digital i mobile na świecie w 2020 roku. Available online: https://mobirank.pl/2020/01/31/raport-digital-i-mobile-na-swiecie-w-2020-roku/ (accessed on 2 February 2021).

- Naeem, Muhammad, and Wilson Ozuem. 2021. The Role of Social Media in Internet Banking Transition during COVID-19 Pandemic: Using Multiple Methods and Sources in Qualitative Research. Journal of Retailing and Consumer Services 60: 102483. [Google Scholar] [CrossRef]

- Santosa, Allicia Deana, Nuryanti Taufik, Faizal Haris Eko Prabowo, and Mira Rahmawati. 2021. Continuance Intention of Baby Boomer and X Generation as New Users of Digital Payment during COVID-19 Pandemic Using UTAUT2. The Journal of Financial Services Research. [Google Scholar] [CrossRef]

- Smulski, Jarosław. 2020. Rynek IT i Telekomunikacji w Polsce, Szanse, Zagrożenia, Bariery Rozwoju. Warszawa: International Data Corporation. [Google Scholar]

- Tran, Lobel Trong Thuy. 2021. Managing the Effectiveness of E-Commerce Platforms in a Pandemic. Journal of Retailing and Consumer Services 58: 102287. [Google Scholar] [CrossRef]

- Valaskova, Katarina, Pavol Durana, and Peter Adamko. 2021. Changes in Consumers’ Purchase Patterns as a Consequence of the COVID-19 Pandemic. Mathematics 9: 1788. [Google Scholar] [CrossRef]

- Vasenska, Ivanka, Preslav Dimitrov, Blagovesta Koyundzhiyska-Davidkova, Vladislav Krastev, Pavol Durana, and Ioulia Poulaki. 2021. Financial Transactions Using FINTECH during the Covid-19 Crisis in Bulgaria. Risks 9: 48. [Google Scholar] [CrossRef]

- Wu, Banggang, Xiaoyu Deng, and Xuebin Cui. 2020. Cash on Delivery or Online Payment: Mobile Channel, Order Size and Payment Methods. Journal of Contemporary Marketing Science 3: 225–42. [Google Scholar] [CrossRef]

- Wu, Run-Ze, Jong-Ho Lee, and Xiu-Fu Tian. 2021. Determinants of the Intention to Use Cross-Border Mobile Payments in Korea among Chinese Tourists: An Integrated Perspective of UTAUT2 with TTF and ITM. Journal of Theoretical and Applied Electronic Commerce Research 16: 1537–56. [Google Scholar] [CrossRef]

- Yakean, Somkid. 2020. Advantages and Disadvantages of a Cashless System in Thailand during the COVID-19 Pandemic. The Journal of Asian Finance, Economics and Business 7: 385–88. [Google Scholar] [CrossRef]

- Zhao, Yuyang, and Fernando Bacao. 2021. How Does the Pandemic Facilitate Mobile Payment? An Investigation on Users’ Perspective under the COVID-19 Pandemic. International Journal of Environmental Research and Public Health 18: 1016. [Google Scholar] [CrossRef] [PubMed]

Figure 1.

The scale of changes in mobile payments in Poland and Turkey since the beginning of the pandemic; source: own study.

Figure 1.

The scale of changes in mobile payments in Poland and Turkey since the beginning of the pandemic; source: own study.

Figure 2.

The advantages of choosing an m-banking application as a mobile payment tool; source: own work.

Figure 2.

The advantages of choosing an m-banking application as a mobile payment tool; source: own work.

Figure 3.

The advantages of choosing a bank’s website as a mobile payment tool; source: own work.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Indicators of differences between the demographic criteria (attributes) in Poland and Turkey in 2021; source: own work.

Table 1.

Indicators of differences between the demographic criteria (attributes) in Poland and Turkey in 2021; source: own work.

| Demographics | Standard Deviation | City Distance | Euclidean Distance |

|---|---|---|---|

| Gender | 11.03% | 38.20% | 7.30% |

| Age | 3.70% | 18.64% | 1.28% |

| Education | 47.55% | 172.42% | 142.16% |

| Place of residence | 4.11% | 34.93% | 3.34% |

| Field of study | 2.91% | 89.64% | 25.78% |

| Financial situation | 9.53% | 115.86% | 29.61% |

Table 2.

Main methods of using mobile devices to access financial services in Poland and Turkey in 2021; source: own work.

Table 2.

Main methods of using mobile devices to access financial services in Poland and Turkey in 2021; source: own work.

| The Way in Which Respondents Handle Their Finances | Poland | Turkey | Average |

|---|---|---|---|

| I use a mobile banking application | 36.06% | 35.75% | 35.91% |

| I contact the hotline—I talk to a consultant | 35.03% | 32.30% | 33.66% |

| I contact the hotline—I use IVR (an automatic system in which basic activities can be performed using telephone buttons, without contacting a consultant) | 6.59% | 12.78% | 9.69% |

| I use text messages (SMSs) | 1.04% | 4.49% | 2.76% |

| I visit the bank’s website | 18.55% | 10.54% | 14.54% |

| I use a virtual bank branch (the website providing communication with a consultant in the form of a written, audio or video chat) | 2.73% | 4.15% | 3.44% |

Table 3.

Reasons for using a website to contact the bank; source: own work.

| Accessing Bank Services via a Website | Poland | Turkey | Average |

|---|---|---|---|

| Convenience and saving time | 41.89% | 41.09% | 41.61% |

| Curiosity, to test the solution | 1.89% | 0.99% | 1.57% |

| It was recommended by a friend or a family member | 4.32% | 5.45% | 4.72% |

| It was recommended by an employee of the bank where I hold my account | 10.81% | 4.46% | 8.57% |

| A friend/family member uses such a form of communication | 11.62% | 12.38% | 11.89% |

| It is trendy/popular | 1.62% | 0.99% | 1.40% |

| A bank’s advertisement encouraged me to use this form of banking | 1.89% | 1.49% | 1.75% |

| Security of banking operations | 24.86% | 32.18% | 27.45% |

| I do not use it | 1.08% | 0.99% | 1.05% |

Table 4.

Mobile payment solutions used in Poland and Turkey; source: own work.

| Types of Mobile Payments | Poland | Turkey | Average |

|---|---|---|---|

| Apple Pay | 11.50% | 10.42% | 10.96% |

| BLIK (Polish Payment Standard) | 26.68% | 0.00% | 13.34% |

| CallPay | 0.00% | 1.79% | 0.89% |

| Cashbill | 0.16% | 0.60% | 0.38% |

| Dotpay/Przelewy24 | 18.31% | 0.89% | 9.60% |

| eCard | 1.02% | 3.27% | 2.15% |

| Fitbit Pay | 0.00% | 0.60% | 0.30% |

| Garmin Pay | 0.00% | 0.60% | 0.30% |

| Google Pay | 3.44% | 9.23% | 6.33% |

| MasterPass account | 0.16% | 6.25% | 3.20% |

| moBilet | 2.27% | 1.19% | 1.73% |

| mobiParking | 0.55% | 0.60% | 0.57% |

| mPay | 1.25% | 1.19% | 1.22% |

| VISA Checkout account | 0.47% | 5.65% | 3.06% |

| Pango | 0.00% | 0.60% | 0.30% |

| PayU | 17.76% | 1.19% | 9.48% |

| PeoPay | 2.74% | 0.60% | 1.67% |

| SkyCash | 2.74% | 0.89% | 1.82% |

| PayPal | 8.61% | 6.25% | 7.43% |

| Ecash | 0.00% | 0.60% | 0.30% |

| I use them, but I do not remember the name | 0.70% | 21.13% | 10.92% |

| I do not use mobile payments | 1.64% | 26.49% | 14.07% |

Table 5.

Mobile payments used by the respondents; source: own work.

| Mobile Payments Used by the Respondents | Poland | Turkey | Average |

|---|---|---|---|

| Purchase of e-tickets (cinema, theatre, music, etc.) | 10.92% | 6.80% | 9.79% |

| Purchase of travel tickets (public transport, train, coach, etc.) | 11.55% | 11.21% | 11.46% |

| Purchase of digital content | 2.23% | 0.83% | 1.85% |

| Car parking fees | 12.32% | 12.22% | 12.29% |

| Online payments on the Internet | 12.32% | 12.22% | 12.29% |

| P2P (person-to-person) transfers | 11.86% | 6.71% | 10.45% |

| Payment of telecommunications, utility, etc., bills and invoices | 7.64% | 11.12% | 8.60% |

| Purchases of drinks, sweets and sandwiches in vending machines | 5.58% | 3.40% | 4.98% |

| Mobile phone top-ups (pre-paid services) | 3.04% | 9.65% | 4.86% |

| e-Wallet for payments and settlements | 0.91% | 4.14% | 1.80% |

| Gift card offered by chain stores to be used at specific points of sale | 2.02% | 2.30% | 2.10% |

| Authorization of persons or services | 2.90% | 0.64% | 2.28% |

| Access control | 1.40% | 0.83% | 1.24% |

| ATM withdrawals | 6.98% | 10.57% | 7.97% |

| Paying for purchases in shops and service points (POS) | 8.34% | 5.15% | 7.46% |

| I do not use any | 0.00% | 2.21% | 0.61% |

Table 6.

The dynamics of changes in mobile payments in Poland during the pandemic according to selected types of activity; source: own work.

Table 6.

The dynamics of changes in mobile payments in Poland during the pandemic according to selected types of activity; source: own work.

| Poland | It Decreased Significantly | It Decreased Slightly | It Has Not Changed | It Increased Slightly | It Increased Significantly |

|---|---|---|---|---|---|

| Purchase of e-tickets (cinema, theatre, music, etc.) | 50.14% | 8.57% | 2.78% | 4.66% | 2.57% |

| Purchase of travel tickets (public transport, train, coach, etc.) | 14.16% | 16.12% | 3.27% | 6.78% | 7.42% |

| Purchase of digital content | 1.13% | 0.82% | 4.95% | 9.60% | 11.67% |

| Car parking fees | 3.40% | 12.24% | 8.57% | 5.93% | 2.37% |

| Online payments on the Internet | 0.00% | 0.00% | 1.50% | 5.37% | 26.11% |

| P2P (person-to-person) transfers | 1.13% | 1.43% | 6.32% | 9.53% | 8.41% |

| Payment of telecommunications, utility, etc., bills and invoices | 0.00% | 0.00% | 6.72% | 7.84% | 10.98% |