Dependence Structures between Sovereign Credit Default Swaps and Global Risk Factors in BRICS Countries

Abstract

:1. Introduction

2. Empirical Review, Materials and Methods

2.1. Empirical Literature Review

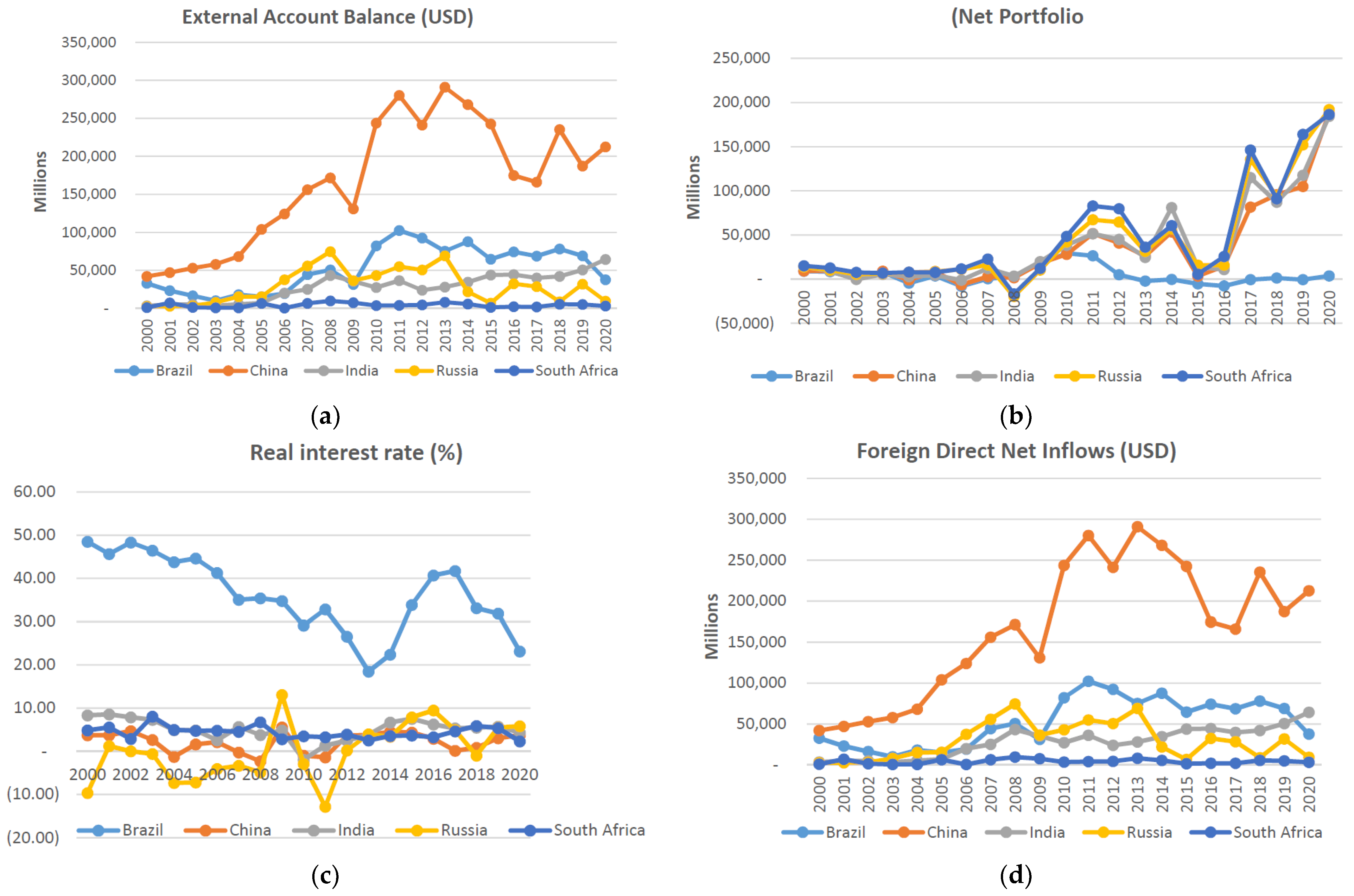

2.2. Data Description, Transformations, and Visual Inspections

2.2.1. Data Scoping, Collection Frequency, and Transformations

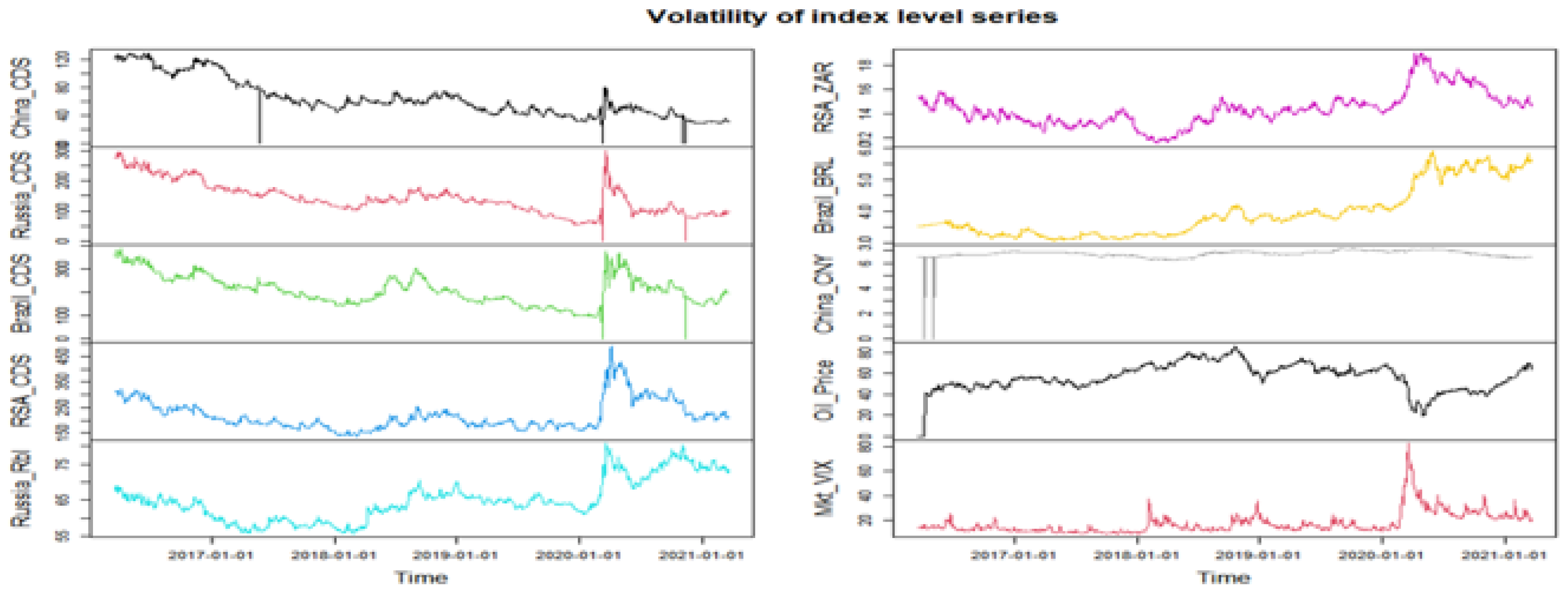

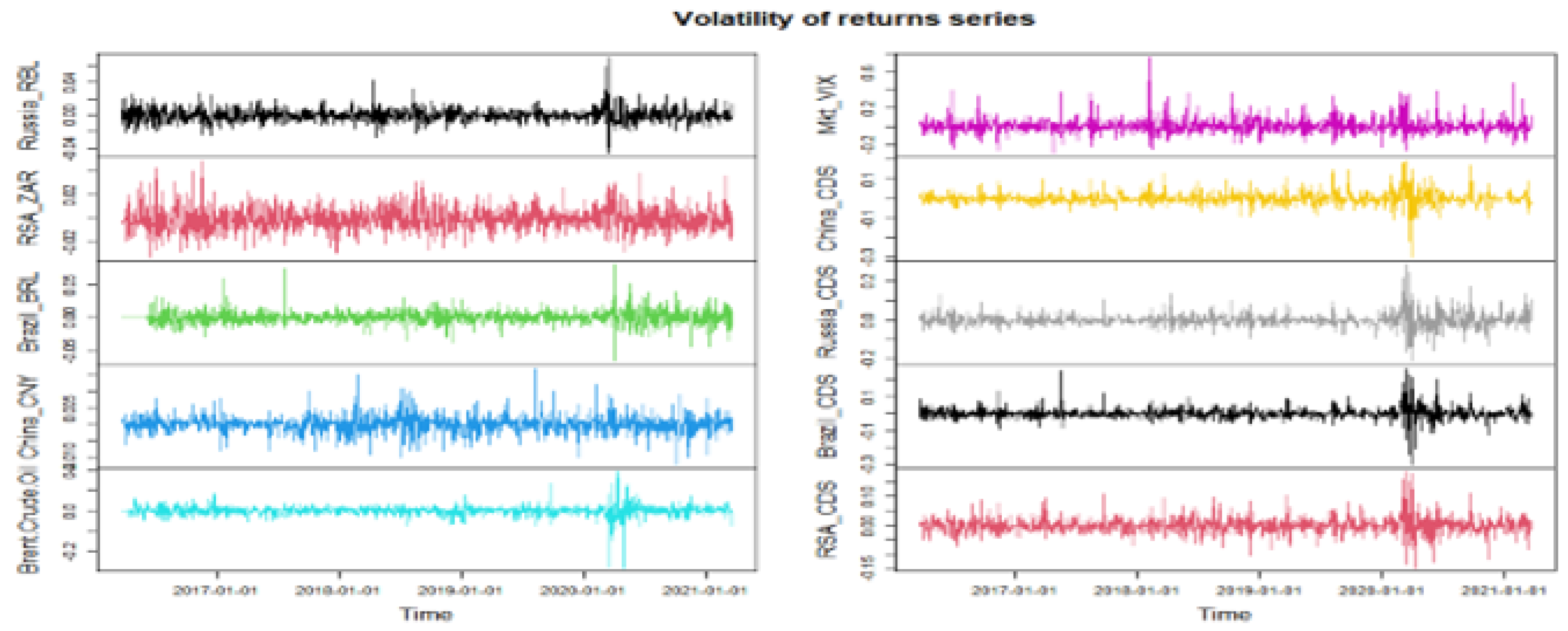

2.2.2. Visual Inspection of Daily Volatilities and Changes in CDS and Global Risks

2.3. The Optimal Copula

2.3.1. Optimal Copulas Using VineCopula Package

2.3.2. Pairwise Tail-Dependence of Sovereign CDS and Global Risks

3. Results Discussion and Interpretation

3.1. Exploratory Analysis of Daily Returns Structure

{kind=link}

{kind=link}

{kind=link}

| Descriptive Statistics: First Difference of Each Variable | Volatility: Oil Price and Currency | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Parameter Estimate | dRSA_CDS | dRussia_CDS | dChina_CDS | dBrazil_CDS | dVIX | dCrude_Oil | CHN_Yuan | BRA_Real | RSA_Zar | RUS_Rbl |

| Mean | 0.000 | −0.001 | −0.001 | −0.001 | 0.0 | 0.000 | 0.00 | 0.00 | 0.00 | 0.00 |

| Min | −0.148 | −0.208 | −0.297 | −0.299 | −0.30 | −0.28 | −0.012 | −0.065 | −0.03 | −0.05 |

| Max | 0.186 | 0.283 | 0.190 | 0.267 | 0.768 | 0.191 | 0.017 | 0.800 | 0.049 | 0.070 |

| Std. Dev (%) | 2.842 | 3.423 | 3.187 | 3.502 | 8.490 | 2.612 | - | - | - | - |

| Kurtosis | 6.000 | 10.830 | 10.820 | 17.220 | 8.860 | 24.83 | 3.690 | 6.980 | 1.010 | 7.320 |

| Skewness | 0.620 | 0.890 | 0.330 | 1.140 | 1.560 | −1.47 | 0.330 | 0.580 | 0.390 | 0.890 |

| J–B Stat | 2049 *** | 6570 *** | 6409 *** | 16,441 *** | 4808 *** | 34,065 *** | 766 *** | 2696 *** | 88 *** | 3094 *** |

| ADF Test | −23.78 | −25.171 | −24.959 | −23.328 | −28.1 | −24.376 | - | - | - | - |

| Cor_dCrude Oil | 0.001 | −0.015 | −0.029 | 0.055 | 0.069 | 1.0 | −0.003 | −0.069 | −0.03 | −0.01 |

| Cor_dMkt_VIX | 0.297 | 0.225 | 0.096 | 0.378 | 1.0 | 0.069 | 0.009 | 0.000 | −0.01 | −0.02 |

3.2. Linear Dependence Structures—Simple Linear Correlation Measure

| Linear Dependence: Spearman Correlation for Sovereign CDS Spreads and Risk Factors | |||||||

|---|---|---|---|---|---|---|---|

| Daily Log Changes | Daily Volatility of Oil Price and Exchange Rate | ||||||

| dVIX | dCrude_Oil | Crude_Oil | CHN_Yuan | BRA_Real | RSA_Zar | RUS_Rbl | |

| dRSA_CDS | 0.297 | 0.001 | 0.004 | - | - | −0.018 | - |

| dRussia_CDS | 0.225 | −0.015 | −0.012 | - | - | - | 0.154 |

| dChina_CDS | 0.096 | −0.029 | −0.027 | 0.026 | - | - | - |

| dBrazil_CDS | 0.378 | 0.055 | 0.058 | −0.042 | - | - | |

| Corr_dCrudeOil | 0.069 | 1.0 | 1 | −0.003 | −0.069 | −0.033 | −0.058 |

| Corr_dMkt_VIX | 1.0 | 0.069 | 0.069 | 0.009 | 0.000 | −0.010 | −0.330 |

3.3. Analysis of Empirical Results: Tail Dependence Structures for BRICS Countries

3.3.1. Pairwise Tail Dependence of Risk Factors and Sovereign CDS

| Parameter Estimate | Oil Price Volatility | Global Markets Sentiment (dVIX) | Exchange Rate Volatility | |||

|---|---|---|---|---|---|---|

| Dependency Type | Spearman | Copula | Spearman | Copula | Spearman | Copula |

| Brazilian CDS | 0.058 | 0.093 | 0.378 | 0.347 | −0.042 | −0.047 |

| Copula_family | - | surJoe | - | surBB1/Gumbel | - | Student-t |

| Chinese CDS | −0.027 | −0.028 | 0.096 | 0.314 | 0.026 | 0.038 |

| Copula_family | - | Student-t | - | TawnT1 | - | Student-t |

| Russian CDS | −0.012 | −0.004 | 0.225 | 0.268 | 0.154 | 0.165 |

| Copula_family | - | Student-t | - | surBB7/Clayton | - | Student-t |

| South African CDS | 0.004 | 0.009 | 0.297 | 0.258 | −0.018 | 0.006 |

| Copula_family | - | Student-t | - | surBB1 | - | Student-t |

3.3.2. Comparison of Tail Dependence Structures within and across BRICS Countries

4. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Aas, Kjersti. 2004. Modelling Dependence Structure of Financial Assets: A Survey of Four Copulas. Oslo: Norwegian Computing Center, pp. 22–30. [Google Scholar]

- Aas, Kjersti, and Daniel Berg. 2009. Models for construction of multivariate dependence-a comparison study. European Journal of Finance 15: 639–59. [Google Scholar] [CrossRef]

- Aas, Kjersti, Claudia Czado, Arnoldo Frigessi, and Henrik Bakken. 2009. Pair-copula constructions of multiple dependence. Insurance: Mathematics and Economics 44: 182–98. [Google Scholar] [CrossRef] [Green Version]

- Akaike, Hirotugu. 1973. Information Theory and an Extension of the Maximum Likelihood Principle. In Proceedings of the 2nd International Symposium on Information Theory. Edited by Boris Nikolaevich Petrov and Frigyes Csaki. Budapest: Akademiai Kiado, pp. 267–81. [Google Scholar]

- Alter, Adrian, and Andreas Beyer. 2014. The dynamics of spill-over effects during the European sovereign debt turmoil. Journal of Bank Finance 42: 134–53. [Google Scholar] [CrossRef] [Green Version]

- Ang, Andrew, and Joseph Chen. 2002. Asymmetric correlations of equity portfolios. Journal of Financial Economics 63: 443–94. [Google Scholar] [CrossRef]

- Augustin, Patrick, Mikhail Chernov, and Dongho Song. 2020. Sovereign credit risk and exchange rates: Evidnce from CDS quanto spreads. Journal of Financial Economics 137: 129–51. [Google Scholar] [CrossRef]

- Ballester, Laura, and Ana González-Urteaga. 2020. Is there a connection between Sovereign CDS spreads and the stock market? Evidence for European and US Returns and Volatilities. Mathematics 8: 1667. [Google Scholar] [CrossRef]

- Barberis, Nicholas, Andrei Shleifer, and Jeffrey Wurgler. 2005. Comovement. Journal of Financial Economics 75: 283–317. [Google Scholar] [CrossRef] [Green Version]

- Bauwens, Luc, Christian M. Hafner, and Sebastien Laurent. 2012. Handbook of Volatility Models and Their Applications. Hoboken: John Wiley & Sons, vol. 3. [Google Scholar]

- Blommestein, Hans, Sylvester Eijffinger, and Zongxin Qian. 2016. Regime-dependent determinants of Euro area sovereign CDS spreads. Journal of Financial Stability 22: 10–21. [Google Scholar] [CrossRef]

- Blum, Peter, Alexandra D. C. Dias, and Paul Embrechts. 2002. The art of dependence modelling: The latest advances in correlation analysis. In Alternative Risk Strategies. London: Risk Books. [Google Scholar]

- Boubaker, Heni, and Nadia Sghaier. 2013. Portfolio optimization in the presence of dependent financial returns with long memory: A copula-based approach. Journal of Banking & Finance 37: 361–77. [Google Scholar]

- Bouye, Eric, Valdo Durrlemann, Ashkan Nikeghbali, Gaël Riboulet, and Thierry Roncalli. 2000. Copulas for Finance—A Reading Guide and Some Applications. Technical Report. Paris: Credit Lyonnais. [Google Scholar]

- Brechmann, Eike Christian. 2010. Truncated and Simplified Regular Vines and Their Applications. Diploma thesis, Technische Universitaet Muenchen, Munich, Germany. [Google Scholar]

- Caillault, Cyril, and Dominique Guegan. 2005. Empirical estimation of tail dependence using copulas: Application to Asian markets. Quantitative Finance 5: 489–501. [Google Scholar] [CrossRef]

- Choe, Geon Hoe, So Eun Choi, and Hyun Jin Jang. 2020. Assessment of time-varying systemic risk in credit default swap indices: Simultaneity and contagiousness. North American Journal of Economics 54: 100907. [Google Scholar] [CrossRef]

- CIA Factbook. 2021. Available online: https://www.cia.gov/the-world-factbook/countries/ (accessed on 1 June 2021).

- Embrechts, Paul, Alexander McNeil, and Daniel Straumann. 2001. Correlation and dependency in risk management: Properties and pitfalls. In Value at Risk and Beyond. Cambridge: Cambridge University Press. [Google Scholar]

- Embrechts, Paul, Filip Lindskog, and Alexander McNeil. 2003. Modelling dependence with copulas and applications to risk management. In Handbook of Heavy-Tailed Distributuions in Finance. Edited by Svetlozar T. Rachev. Amsterdam: Elsevier. [Google Scholar]

- Fermanian, Jean-David, and Olivier Scaillet. 2002. Non-parametric estimation of copulas for time series. Journal of Risk 4: 25–54. [Google Scholar]

- Fischer, Matthias, Christian Kock, Stephan Schluter, and Florian Weigert. 2009. Multivariate copula models at work. Quantitative Finance 9: 839–54. [Google Scholar] [CrossRef] [Green Version]

- Galariotis, Emilios C., Panagiota Makrichoriti, and Spyrou Spyroub. 2016. Sovereign CDS spread determinants and spill-over effects during financial crisis: A panel VAR approach. Journal of Financial Stability 26: 62–77. [Google Scholar] [CrossRef] [Green Version]

- Giacomini, Enzo, Wolfgang K. Hardle, and Vladimir Spokoiny. 2009. Inhomogeneous dependence modeling with time-varying copulae. Journal of Business & Economic 27: 224–34. [Google Scholar]

- Grammatikos, Theoharry, and Robert Vermeulen. 2012. Transmission of the financial and sovereign debt crises to the EMU: Stock prices, CDS spreads and exchange rates. Journal of International Money and Finance 31: 517–33. [Google Scholar] [CrossRef]

- Hair, Joseph F., Thomas G. Hult, Christain M. Ringle, and Marko Sarstedt. 2017. A Primer on Partial Least Squares Structural Equation Modelling (PLS–SEM). Thousand Oaks: Sage. [Google Scholar]

- Hansen, Peter R., and Asger Lunde. 2005. A forecast comparison of volatility models: Does anything beat a GARCH (1,1)? Journal of Applied Econometrics 20: 873–89. [Google Scholar] [CrossRef] [Green Version]

- Hasebe, Takuya. 2013. Copula-based maximum-likelihood estimation of sample-selection models. The Stata Journal 13: 547–73. [Google Scholar] [CrossRef] [Green Version]

- Heinen, Andreas, and Alfonso Valdesogo. 2009. Asymmetric CAPM Dependence for Large Dimensions: The Canonical Vine Autoregressive Copula Model. Technical Report. Available online: https://ssrn.com/abstract=1297506 (accessed on 14 December 2020).

- Hong, Han, and Bruce Preston. 2005. Nonnested Model Selection Criteria. Paper Working. Stanford: Department of Economics, Stanford University. [Google Scholar]

- Iuga, Iulia Christina, and Anastasia Mihalciuc. 2020. Major Crises of the XXIst Century and Impact on Economic Growth. Sustainability 12: 9373. [Google Scholar] [CrossRef]

- Joe, Harry. 1996. Families of m-variate distributions with given margins and m(m-1)/2 bivariate dependence parameters. In Distributions with Fixed Marginals and Related Topics. Edited by Schweizer Berthold and Michael D. Taylor. Hayward: Institute of Mathematical Statistics, pp. 120–41. [Google Scholar]

- Joe, Harry. 1997. Multivariate Models and Dependence Concepts. London: Chapman and Hall. [Google Scholar]

- Joe, Harry, Haijun Li, and Aristidis K. Nikoloulopoulos. 2010. Tail dependence functions and vine copulas. Journal of Multivariate Analysis 101: 252–70. [Google Scholar] [CrossRef] [Green Version]

- Jondeau, Eric, and Michael Rockinger. 2006. The copula-GARCH model of conditional dependencies: An international stock market application. Journal of International Money and Finance 25: 827–53. [Google Scholar] [CrossRef] [Green Version]

- Jondeau, Eric, Ser Huang Poon, and Michael Rockinger. 2007. Financial Modeling under Non-Gaussian Distributions. London: Springer. [Google Scholar]

- Kalbaska, Alesia, and Mateusz Gatkowski. 2012. Eurozone sovereign contagion: Evidence from the CDS market (2005–2010). Journal of Economics & Behavioural Organ 83: 657–73. [Google Scholar]

- Lokshin, Michael, and Zurab Sajaia. 2004. Maximum likelihood estimation of endogenous switching regression models. Stata Journal 4: 282–89. [Google Scholar] [CrossRef] [Green Version]

- Longin, Francois, and Bruno Solnik. 2001. Extreme correlation of international equity markets. The Journal of Finance 56: 649–76. [Google Scholar] [CrossRef]

- Lovreta, Lidija, and Joaquín López Pascual. 2020. Structural breaks in the interaction between bank and sovereign default risk. SERIEs 11: 531–59. [Google Scholar] [CrossRef]

- Manner, Hans. 2007. Estimation and Model Selection of Copulas with an Application to Exchange Rates. Maastricht: Maastricht University. [Google Scholar]

- McNeil, Alexander, Rudiger Frey, and Paul Embrechts. 2002. Extreme Co-Movements between Financial Assets. Technical Report. New York: Columbia University. [Google Scholar]

- Min, Aleksey, and Claudia Czado. 2010. Bayesian inference for multivariate copulas using pair-copula constructions. Journal of Financial Econometrics 8: 511–46. [Google Scholar] [CrossRef]

- Nelsen, Roger B. 2006. An Introduction to Copulas, 2nd ed. New York: Springer. [Google Scholar]

- Nikoloulopoulos, Aristidis K., Harry Joe, and Haijun Li. 2010. Vine copulas with asymmetric tail dependence and applications to financial return data. Computational Statistics and Data Analysis 56: 3659–73. [Google Scholar] [CrossRef]

- Schirmacher, Doris, and Ernesto Schirmacher. 2008. Multivariate Dependence Modeling Using Pair-Copulas, Technical Report. Enterprise Risk Management Symposium.

- Tabak, Benjamin M., Rodrigo Castro Miranda, and Mauricio Da Silva Medeiros Jr. 2016. Contagion in CDS, banking and equity markets. Economic Systems 40: 120–34. [Google Scholar] [CrossRef]

- Wang, Alan T., Seng-Yeng Yang, and Nien-Tzu Yang. 2013. Information transmission between sovereign debt CDS and other financial factors—The case of Latin America. North American Journal of Economics and Finance 26: 586–601. [Google Scholar] [CrossRef]

- Wang, Zhouwei, Qicheng Zhao, Min Zhu, and Tao Pang. 2020. Jump Aggregation, Volatility Prediction, and Nonlinear Estimation of Banks’ Sustainability Risk. Sustainability 12: 8849. [Google Scholar] [CrossRef]

- World Bank. 2021. Available online: https://data.worldbank.org/indicator/BX.KLT.DINV.CD.WD?end=2019&locations=BR-RU-CN-ZA-IN&start=2002&view=chart (accessed on 1 June 2021).

- Yang, Lu, Lei Yang, and Shigeyuki Hamori. 2018. Determinants of dependence structures of sovereign credit default swap spreads between G7 and BRICS countries. International Review of Financial Analysis 59: 19–34. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rikhotso, P.M.; Simo-Kengne, B.D. Dependence Structures between Sovereign Credit Default Swaps and Global Risk Factors in BRICS Countries. J. Risk Financial Manag. 2022, 15, 109. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15030109

Rikhotso PM, Simo-Kengne BD. Dependence Structures between Sovereign Credit Default Swaps and Global Risk Factors in BRICS Countries. Journal of Risk and Financial Management. 2022; 15(3):109. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15030109

Chicago/Turabian StyleRikhotso, Prayer M., and Beatrice D. Simo-Kengne. 2022. "Dependence Structures between Sovereign Credit Default Swaps and Global Risk Factors in BRICS Countries" Journal of Risk and Financial Management 15, no. 3: 109. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15030109