Credit Constraint, Interlinked Insurance and Credit Contract and Farmers’ Adoption of Innovative Seeds-Field Experiment of the Loess Plateau

Abstract

:1. Introduction

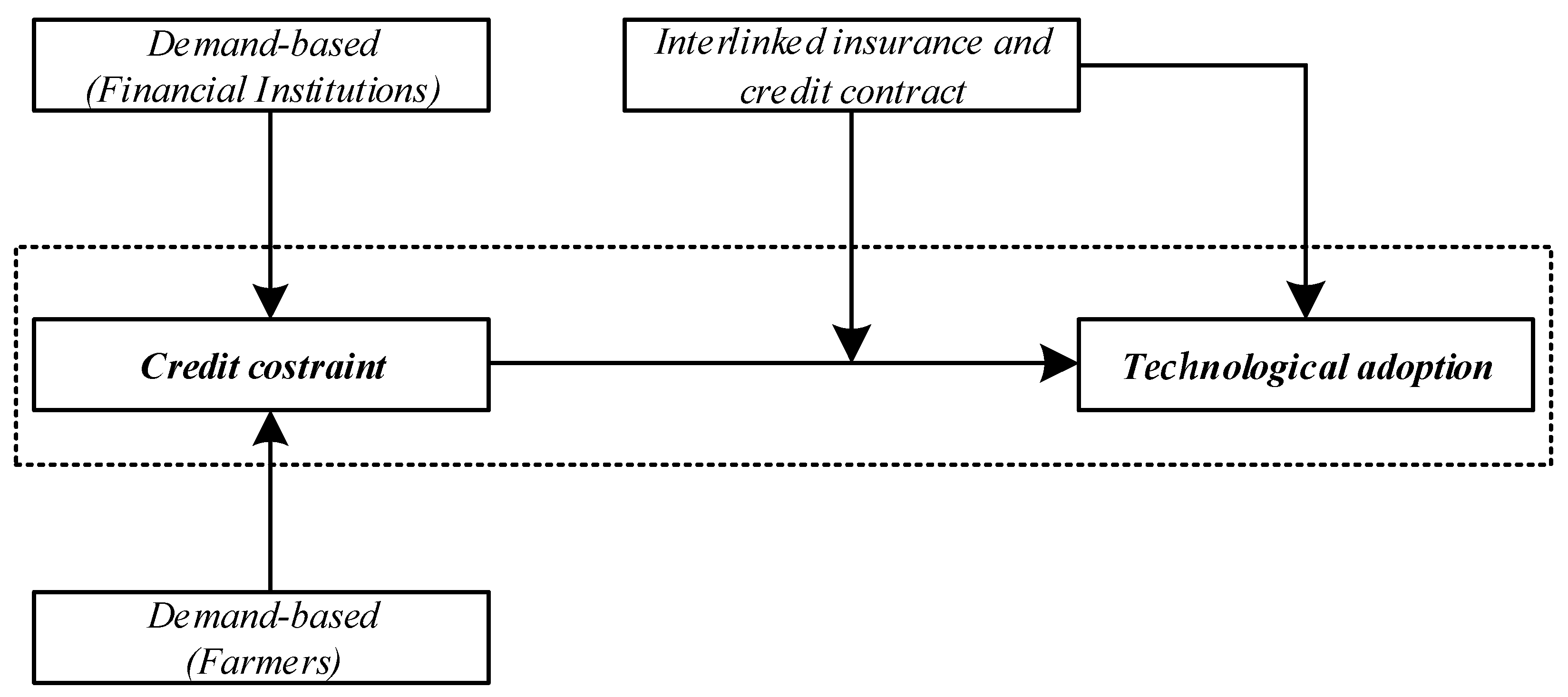

2. Theoretical Analysis

2.1. Credit Constraint and Farmers’ Adoption of Innovative Seeds

2.2. Interlinked Insurance and Credit Contract and Farmers’ Adoption of Innovative Seeds

2.3. Moderating Effects of Interlinked Insurance and Credit Contract

3. Experiment Design

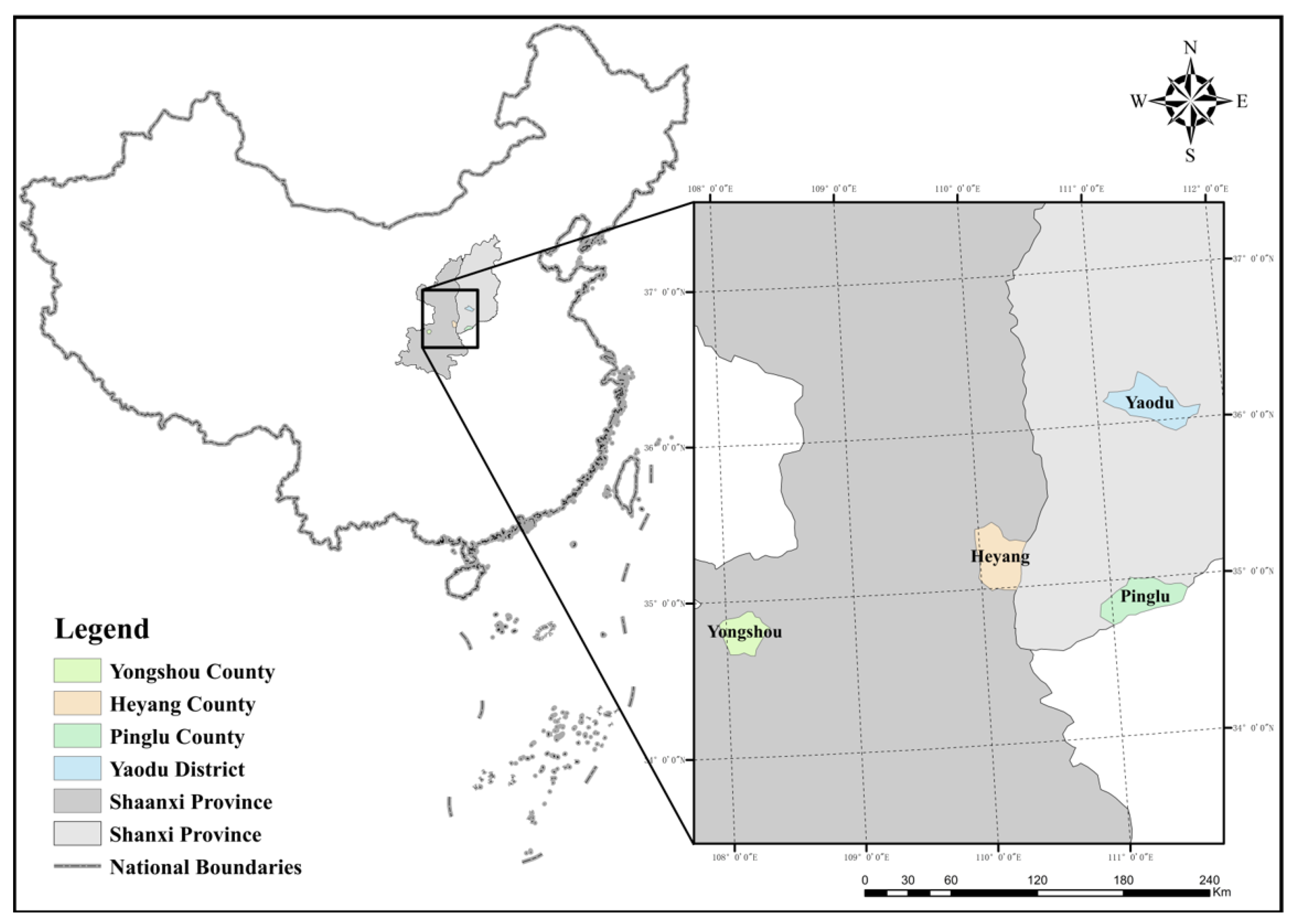

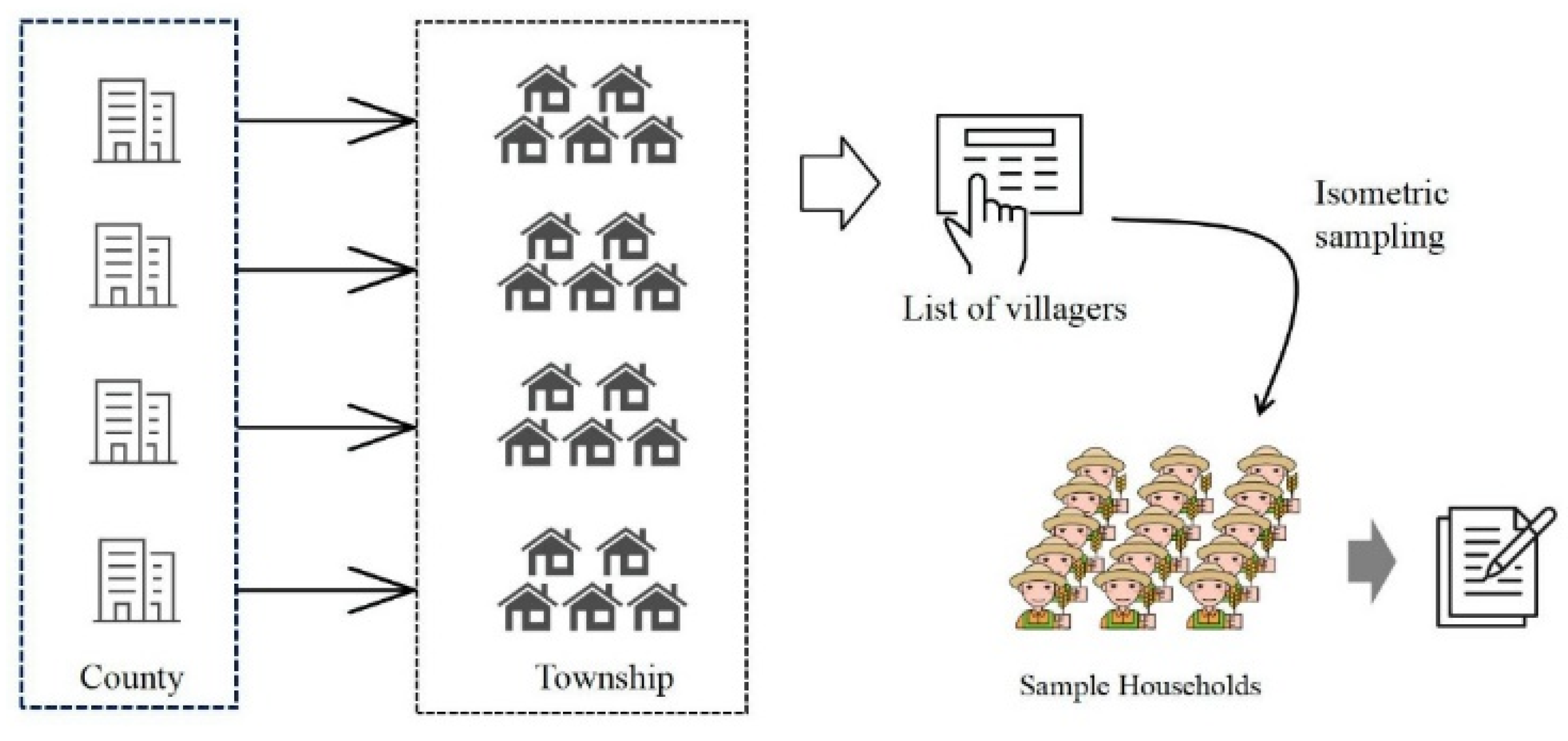

3.1. Experiment Set and Distribution of Samples

3.2. Experimental Design

3.2.1. Research Methodology

3.2.2. Research Methodology

- The setting of groups. (1) Control group. Farmers in this group choose between traditional wheat seeds that do not require credit and innovative wheat seeds that do; (2) Treatment group. Farmers in this group make decisions between traditional wheat seeds that are not financially constrained and innovative wheat seeds that provide interlinked insurance and credit contract.

- The setting of production conditions. Referring to the study of Tang et al. [6], we assume that the farmers owe CNY 4200 in terms of capital and 10 Mu cultivated land at the beginning. In the first year, farmers are required to make a choice of wheat seeds between No. 0 seeds and No. 1 seeds. The differences in seeds, production inputs, and income under different weather conditions for these two kinds of seeds are shown in Table 2. If farmers choose No. 0 seeds, their own capital is enough to satisfy the demand for production; if they choose No. 1 seeds, farmers need to apply for a loan of CNY 1800 and submit collateral worth CNY 1800 (we assume the farmers can afford it). At the end of the year, if the weather is suitable for wheat growth, the farmers who planted No. 1 seeds will obtain the collateral back after repaying the loan; if the weather is bad, the farmers planting No. 1 seeds are unable to repay the loan, and the bank will confiscate the collateral, so farmers will lose CNY 1800. Farmers who do not go bankrupt in the first round of experiments will continue with the second round of experiments, and the final payoff in this experiment will be determined by the remaining funds in each farmer’s hand at the end of the last year.

- The setting of weather conditions. Considering that the weather conditions in the previous year may affect planting plans for the next year, we simplify the weather conditions in the areas into two categories: disaster (bad weather) and normal (good weather). Farmers randomly draw a card from the black box containing four red cards and two black cards; the black card represents bad weather, while the red card represents good weather. According to the local meteorological information, we can know that the incidence of disaster weather is one-third. Farmers are required to determine the natural conditions they face by drawing cards randomly, ensuring that they do not know the weather conditions of the year. Moreover, the loss will be 1.55 times higher than that of normal seeds if bad weather occurs. The main parameters are presented in Table 2.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Experimental Group | Seed Variety | Production Input | Loan | Premium | Planting Income (Good) | Balance (Good) | Planting Income (Bad) | Balance (Bad) |

|---|---|---|---|---|---|---|---|---|

| Control group | No. 0 seeds | 4000 | 0 | 0 | 7000 | 7200 | 0 | 200 |

| No. 1 seeds | 6000 | 1800 | 0 | 12,000 | 10,200 | 0 | −1800 | |

| Treatment group | No. 0 seeds | 4000 | 0 | 0 | 7000 | 7200 | 0 | 200 |

| No. 1 seeds | 6000 | 2000 | 200 | 12000 | 10,000 | 0 | 0 |

- 4

- The experimental process (Appendix B). Before the experiment, we explained to farmers, in text (the experimental instruction manual), the details of the experimental situation, the main parameter, the task arrangements of the experiment, and the relevant requirements. Additionally, the tester continued to demonstrate the experimental process until the farmers fully understand the entire experimental content. To avoid communications between farmers, four farmers were taken by each tester and separated by baffles to ensure the independence of choice. If farmers in the control group choose No. 0 seeds, their own capital is enough to maintain agricultural production. If the weather is suitable for planting (good weather), they earn CNY 7000 and have a balance of CNY 7200. If the weather is not suitable (bad weather), they have no income and a balance of CNY 200. If farmers choose No. 1 seeds, they need to apply for a credit of CNY 1800. Moreover, they are required to provide the banks with equally valued collateral. At the end of the year, they receive the collateral back and obtain a balance of CNY 10,200 if the weather is good. However, if bad weather occurs, farmers who choose No. 1 seeds lose the collateral worth CNY 1800. The loss to farmers is CNY 1800. Since farmers experiencing bad weather in the first year would fall into bankruptcy, we added an exit option in the second year (i.e., withdrawing from agricultural production). The experiment was conducted one more time while other scenarios were the same as in the first year.In the treatment group, a game was implemented to help farmers in the experimental group understand the difference between a traditional insurance contract and an interlinked insurance and credit contract. Next, the farmers were asked to answer some simple test questions to see if they fully understood the contract. If the farmer still did not understand the experiment, the tester explained it in greater detail until they did. In terms of the treatment group, the basic conditions are the same as those in the control group, and the only difference is that the farmers who chose No. 1 seeds were required to purchase an interlinked insurance and credit contract with a premium of CNY 200. Therefore, farmers needed to borrow CNY 2000 from the bank and also provided collateral of CNY 2000. At that point, if the weather was suitable for planting (good weather), they received a satisfactory output. However, if bad weather occurs, the insurance company pays the bank first, and the farmers receive the collateral back. They will have no income and a balance of CNY 0.

- 5

- The measurement of farmers’ risk attitude. Risk attitude is a major force influencing farmers’ decisions and an important factor in the adoption of innovative seeds by farmers due to credit constraints and interlinked insurance and credit contracts [32,56]. In order to obtain accurate information concerning farmers’ risk attitudes, we measured farmers’ risk attitudes through a field experiment. First, farmers were informed that there are three black cards and three red cards in a transparent bag, and the rewards for drawing the black and red cards are shown in Table 3. Then, farmers are required to make their choices. Only the farmers who chose Plan B1 proceeded with the game, as it could help us improve the accuracy of formal experiments and reduce invalid samples.

| Risk Options | Plan A1 | Plan B1 | ||

| Red card | Black card | Red card | Black card | |

| 15 | 20 | 16 | 21 | |

3.3. Control Variables

3.3.1. Selection of Control Variables

3.3.2. Descriptive Statistics of the Variables

3.4. Model Setting

4. Empirical Results

4.1. Baseline Regression

4.1.1. First-Round Experimental Regression Results

4.1.2. Regression Results of the Second Round of Experiments

4.1.3. Robustness Test

4.2. Moderating Effects of Interlinked Insurance and Credit Contract

4.3. Further Analysis of Moderating Effects

5. Discussion

6. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Research Questionnaire

Appendix B. Experimental Design

| Risk Options | Plan A1 | Plan B1 | ||

| Red card | Black card | Red card | Black card | |

| 15 | 20 | 16 | 21 | |

| Options | Plan A2 | Plan B2 | ||

|---|---|---|---|---|

| Red Card | Black Card | Red Card | Black Card | |

| 1 | 20 | 20 | 22 | 18 |

| 2 | 20 | 20 | 23 | 17 |

| 3 | 20 | 20 | 25 | 15 |

| 4 | 20 | 20 | 35 | 15 |

| 5 | 20 | 20 | 37 | 13 |

| 6 | 20 | 20 | 40 | 10 |

| 7 | 20 | 20 | 52 | 8 |

| 8 | 20 | 20 | 54 | 6 |

| 9 | 20 | 20 | 56 | 4 |

| 10 | 20 | 20 | 60 | 0 |

| Options | Plan A3 | Plan B3 | ||

|---|---|---|---|---|

| Red card | Black card | Red card | Black card | |

| 1 | 20 | 20 | 22 | 18 |

| 2 | 20 | 20 | 23 | 17 |

| 3 | 20 | 20 | 25 | 15 |

| 4 | 20 | 20 | 35 | 15 |

| 5 | 20 | 20 | 37 | 13 |

| 6 | 20 | 20 | 40 | 10 |

| 7 | 20 | 20 | 52 | 8 |

| 8 | 20 | 20 | 54 | 6 |

| 9 | 20 | 20 | 56 | 4 |

| 10 | 20 | 20 | 60 | 0 |

| Experimental Group | Seed Variety | Production Input | Loan | Premium | Planting Income (Good) | Balance (Good) | Planting Income (Bad) | Balance (Bad) |

|---|---|---|---|---|---|---|---|---|

| Control group | No. 0 seeds | 4000 | 0 | 0 | 7000 | 7200 | 0 | 200 |

| No. 1 seeds | 6000 | 1800 | 0 | 12,000 | 10,200 | 0 | −1800 | |

| Treatment group | No. 0 seeds | 4000 | 0 | 0 | 7000 | 7200 | 0 | 200 |

| No. 1 seeds | 6000 | 2000 | 200 | 12,000 | 10,000 | 0 | 0 |

| Experimental Group | Seed Variety | Production Input | Loan | Premium | Planting Income (Good) | Balance (Good) | Planting Income (Bad) | Balance (Bad) |

|---|---|---|---|---|---|---|---|---|

| Control group | No. 0 seeds | 4000 | 0 | 0 | 7000 | 7200 | 0 | 200 |

| No. 1 seeds | 6000 | 1800 | 0 | 12,000 | 10,200 | 0 | −1800 | |

| Treatment group | No. 0 seeds | 4000 | 0 | 0 | 7000 | 7200 | 0 | 200 |

| No. 1 seeds | 6000 | 2000 | 200 | 12,000 | 10,000 | 0 | 0 |

| Experimental Group | Seed Variety | Production Input | Loan | Premium | Planting Income (Good) | Balance (Good) | Planting Income (Bad) | Balance (Bad) |

|---|---|---|---|---|---|---|---|---|

| Control group | No. 0 seeds | 560 | 0 | 0 | 980 | 1008 | 0 | 28 |

| No. 1 seeds | 840 | 252 | 0 | 1680 | 1428 | 0 | −252 | |

| Treatment group | No. 0 seeds | 560 | 0 | 0 | 980 | 1008 | 0 | 28 |

| No. 1 seeds | 840 | 280 | 28 | 1680 | 1400 | 0 | 0 |

Appendix C. Pictures of the Research

References

- Serrano-Ruíz, H.; Eras, J.; Martín-Closas, L.; Pelacho, A.M. Compounds released from unused biodegradable mulch materials after contact with water. Polym. Degrad. Stab. 2020, 178, 109202. [Google Scholar] [CrossRef]

- Abd-Elmabod, S.K.; Muñoz-Rojas, M.; Jordán, A.; Anaya-Romero, M.; Phillips, J.D.; Jones, L.; de la Rosa, D. Climate change impacts on agricultural suitability and yield reduction in a Mediterranean region. Geoderma 2020, 374, 114453. [Google Scholar] [CrossRef]

- Jin, J.; Wang, W.; Wang, X. Farmers’ risk preferences and agricultural weather index insurance uptake in rural China. Int. J. Disaster Risk Sci. 2016, 7, 366–373. [Google Scholar] [CrossRef] [Green Version]

- Ji, X.Q.; Qian, Z.H.; Li, Y.Y. Does land operation scale expansion help to improve rice production efficiency?—An analysis based on family farms in Songjiang District, Shanghai. China Rural Econ. 2019, 7, 71–88. [Google Scholar]

- Tadesse, M. Fertilizer adoption, credit access, and safety nets in rural Ethiopia. Agric. Financ. Rev. 2014, 74, 290–310. [Google Scholar] [CrossRef]

- Tang, Y.M.; Yang, Y.; Ge, J.H. Can the “Bank-Insurance Interaction” Promote Farmers’ Technology Adoption?—An empirical analysis based on field experiments. China Rural Econ. 2019, 1, 127–142. [Google Scholar]

- Nakano, Y.; Magezi, E.F. The impact of microcredit on agricultural technology adoption and productivity: Evidence from randomized control trial in Tanzania. World Dev. 2020, 133, 1–13. [Google Scholar] [CrossRef]

- Evenson, R. International diffusion of agrarian technology. J. Econ. Hist. 1974, 34, 51–73. [Google Scholar] [CrossRef]

- Ragasa, C.; Mzungu, D.; Kalagho, K.; Cynthia, K. Impact of interactive radio programming on agricultural technology adoption and crop diversification in Malawi. J. Dev. Eff. 2021, 13, 204–223. [Google Scholar] [CrossRef]

- Adebayo, S.T.; Oyawole, F.P.; Sanusi, R.A.; Afolami, C.A. Technology adoption among cocoa farmers in Nigeria: What drives farmers’ decisions. For. Trees Livelihoods 2021, 31, 1–12. [Google Scholar] [CrossRef]

- Tang, Y.; Yang, Y.; Ge, J.; Chen, J.; Xin, X. The impact of weather index insurance on agricultural technology adoption evidence from field economic experiment in China. China Agric. Econ. Rev. 2019, 11, 622–641. [Google Scholar] [CrossRef]

- Mikula, K.; Izydorczyk, G.; Skrzypczak, D.; Mironiuk, M.; Chojnacka, K. Controlled release micronutrient fertilizers for precision agriculture—A review. Sci. Total Environ. 2020, 712, 136365. [Google Scholar] [CrossRef] [PubMed]

- Jia, R.; Lu, Q. Credit constraint, social capital and water-saving irrigation technology adoption: The case of Zhangye, Gansu. China Popul.-Resour. Environ. 2017, 27, 54–62. [Google Scholar]

- Xu, S. The Political Economy of Seeds: Paradigmatic Shifts of Seed Governance and Seed Marketization in China. Ph.D. Thesis, Hong Kong Polytechnic University, Hong Kong, China, 2019. [Google Scholar]

- Xie, Y.M.; Qi, Q.; Zhao, H.L. A comprehensive insurance-based bancassurance cooperation model: Typical case and theoretical implications. Agric. Econ. Issues 2015, 36, 84–90+111–112. [Google Scholar]

- Gebeyehu, M.G. Effect of Credit Constraints on Intensity of fertilzer adoption and agricultural productivity in amhara region, Ethiopia: An Endogenous Switching Regression Analysis. East. Afr. Soc. Sci. Res. Rev. 2019, 35, 65–100. [Google Scholar] [CrossRef]

- Varshney, D.; Joshi, P.K.; Roy, D.; Kumar, A. Understanding the Adoption of Modern Cultivars in India: Adoption Probability and Use Intensity. J. Agric. Resour. Econ. 2022, 47, 167–189. [Google Scholar] [CrossRef]

- Wei, H.; Xia, Y.; Li, Y. Analysis of Farmers’ Adoption Behavior of Environmentally Friendly Agricultural Technologies under the Perspective of Credit Demand Inhibition. J. Huazhong Agric. Univ. 2020, 1, 56–66+164. [Google Scholar]

- Giné, X.; Yang, D. Insurance, credit, and technology adoption: Field experimental evidence from Malawi. J. Dev. Econ. 2009, 89, 1–11. [Google Scholar] [CrossRef]

- Yu, Q.S.; Zhou, Y.H. Credit Constraint Strength and Farmers’ Well-Being Losses–An Empirical Analysis Based on Cross-Sectional Data from China Rural Finance Survey. China Rural Econ. 2014, 3, 36–47. [Google Scholar]

- Fang, L.; Hu, R.; Mao, H.; Chen, S. How crop insurance influences agricultural green total factor productivity: Evidence from Chinese farmers. J. Clean. Prod. 2021, 321, 128977. [Google Scholar] [CrossRef]

- Freudenreich, H.; Musshoff, O. Insurance for technology adoption: An experimental evaluation of schemes and subsidies with maize farmers in Mexico. J. Agric. Econ. 2018, 69, 96–120. [Google Scholar] [CrossRef]

- Liu, B.C.; Li, M.S.; Guo, Y.; Shan, K. Analysis of the demand for weather index agricultural insurance on household level in Anhui, China. Agric. Agric. Sci. Procedia 2010, 1, 179–186. [Google Scholar] [CrossRef] [Green Version]

- Xu, T.T.; Sun, R. Can policy agricultural insurance alleviate poverty vulnerability–an analysis based on typical village research data. Agric. Technol. Econ. 2022, 2, 126–144. [Google Scholar]

- Diagne, A.; Zeller, M.; Sharma, M.P. Empirical Measurements of Households’ Access to Credit and Credit Constraints in Developing Countries; FCND briefs 90; International Food Policy Research Institute (IFPRI): Washington, DC, USA, 2000. [Google Scholar] [CrossRef]

- Karlan, D.; Osei, R.; Osei-Akoto, I.; Udry, C. Agricultural decisions after relaxing credit and risk constraints. Q. J. Econ. 2014, 129, 597–652. [Google Scholar] [CrossRef] [Green Version]

- Jiang, X.; Chen, S.W. Agricultural insurance, agricultural credit and per capita net income of farm households-an empirical study based on mediating effects. J. Shandong Agric. Univ. 2021, 23, 38–44. [Google Scholar]

- Ye, T.; Liu, Y.; Wang, J.; Wang, M.; Shi, P. Farmers’ crop insurance perception and participation decisions: Empirical evidence from Hunan, China. J. Risk Res. 2017, 20, 664–677. [Google Scholar] [CrossRef]

- Guo, J.; Tan, S.; Kong, X.Z. Regional differences in farmers’ agricultural insurance rejection: Insufficient supply or insufficient demand–a study based on plantation insurance in 12 counties of 6 northern provinces. Agric. Tech. Econ. 2019, 2, 85–98. [Google Scholar]

- Hazell, P.B.R. The appropriate role of agricultural insurance in developing countries. J. Int. Dev. 1992, 4, 567–581. [Google Scholar] [CrossRef]

- Cole, S.; Giné, X.; Vickery, J. How does risk management influence production decisions? Evidence from a field experiment. Rev. Financ. Stud. 2017, 30, 1935–1970. [Google Scholar] [CrossRef] [Green Version]

- Qiu, H.G.; Su, L.F.; Zhang, Y.T.; Tang, J.J. Risk Preference, Risk Perception and Farmers’ Conservation Tillage Technology Adoption. China Rural Econ. 2020, 7, 59–79. [Google Scholar]

- Tang, Y.M.; Xu, T. Weather index insurance and farmers’ technology choice preferences from the perspective of scale heterogeneity—Based on field economics experimental approach. Insur. Res. 2021, 8, 18–34. [Google Scholar] [CrossRef]

- Barnett, B.J.; Barrett, C.B.; Skees, J.R. Poverty traps and index-based risk transfer products. World Dev. 2008, 369, 1766–1785. [Google Scholar] [CrossRef]

- De Nicola, F.; Hill, R.V. Interplay among credit, weather insurance and savings for farmers in Ethiopia. In Proceedings of the American Economic Association Meetings, Chicago, IL, USA, 6–8 January 2012. [Google Scholar]

- Gallenstein, R.A.; Flatnes, J.E.; Dougherty, J.P.; Sam, A.G.; Mishra, K. The impact of index-insured loans on credit market participation and risk-taking. Agric. Econ. 2021, 52, 141–156. [Google Scholar] [CrossRef]

- Farrin, K.; Miranda, M.J. A heterogeneous agent model of credit-linked index insurance and farm technology adoption. J. Dev. Econ. 2015, 116, 199–211. [Google Scholar] [CrossRef]

- Ruzzante, S.; Labarta, R.; Bilton, A. Adoption of agricultural technology in the developing world: A meta-analysis of the empirical literature. World Dev. 2021, 146, 105599. [Google Scholar] [CrossRef]

- Xu, Z.Z.; Zhao, X.F. Practical forms of differentiated technology adoption behaviors of agricultural business entities, the reasons for their formation and their impacts. China Sci. Technol. Forum 2022, 2, 178–188. [Google Scholar] [CrossRef]

- Carter, M.R.; Olinto, P. Getting institutions “right” for whom? Credit constraints and the impact of property rights on the quantity and composition of investment. Am. J. Agric. Econ. 2003, 85, 173–186. [Google Scholar] [CrossRef]

- Berkouwer, S.B.; Dean, J.T. Credit, attention, and externalities in the adoption of energy efficient technologies by low-income households. Am. Econ. Rev. 2022, 112, 3291–3330. [Google Scholar] [CrossRef]

- Shiferaw, B.; Kebede, T.; Kassie, M.; Fisher, M. Market imperfections, access to information and technology adoption in Uganda: Challenges of overcoming multiple constraints. Agric. Econ. 2015, 46, 475–488. [Google Scholar] [CrossRef]

- Tesfaye, M.Z.; Balana, B.B.; Bizimana, J.C. Assessment of smallholder farmers’ demand for and adoption constraints to small-scale irrigation technologies: Evidence from Ethiopia. Agric. Water Manag. 2021, 250, 106855. [Google Scholar] [CrossRef]

- Harou, A.P.; Madajewicz, M.; Michelson, H.; Palm, C.A.; Amuri, N.; Magomba, C.; Weil, R. The joint effects of information and financing constraints on technology adoption: Evidence from a field experiment in rural Tanzania. J. Dev. Econ. 2022, 155, 102707. [Google Scholar] [CrossRef]

- Gao, J.J.; Shi, Q.H. Exploring the change of agricultural production methods in China--based on micro-farmers’ factor input perspective. Manag. World. 2021, 37, 124–134. [Google Scholar] [CrossRef]

- Cheng, Y.; Han, J.; Luo, D. Formal credit constraints under the interaction of supply rationing and demand repression: An examination of the financial demand behavior of 1874 farm households. World Econ. 2009, 5, 73–82. [Google Scholar]

- Balana, B.; Oyeyemi, M. Credit Constraints and Agricultural Technology Adoption: Evidence from Nigeria; International Food Policy Research Institute: Washington, DC, USA, 2020; Volume 64. [Google Scholar]

- Adams, A.; Jumpah, E.T.; Caesar, L.D. The nexuses between technology adoption and socioeconomic changes among farmers in Ghana. Technol. Forecast. Soc. Chang. 2021, 173, 121133. [Google Scholar] [CrossRef]

- Liu, Z.X.; Guo, L.G.; Yang, Y. Information sharing, risk sharing and interaction mechanism of rural banking and insurance. J. Guangdong Inst. Financ. 2010, 25, 63–73. [Google Scholar]

- Li, W.; Xue, C.X.; Yao, S.B.; Zhu, R.X. Farmers’ conservation tillage technology adoption behavior and its influencing factors:an analysis based on 476 farming households in Loess Plateau. China Rural Econ. 2017, 1, 44–57+94–95. [Google Scholar]

- Carter, M.R.; Cheng, L.; Sarris, A. The Impact of Inter-linked Index Insurance and Credit Contracts on Financial Market Deepening and Small Farm Productivity. In Proceedings of the Annual Meeting of the American Applied Economics Association, Pittsburgh, PA, USA, 24–26 July 2011. [Google Scholar]

- Adams, D.W. Effects of finance on rural development. In Undermining Rural Development With Cheap Credit; Routledge: Oxfordshire, UK, 1984; pp. 11–21. [Google Scholar]

- Mellon-Bedi, S.; Descheemaeker, K.; Hundie-Kotu, B.; Frimpong, S.; Groot, J.C.J. Motivational factors influencing farming practices in northern Ghana. NJAS-Wagen. J. Life Sci. 2020, 92, 100326. [Google Scholar] [CrossRef]

- Hill, R.V.; Kumar, N.; Magnan, N.; Makhija, S.; Nicola, F.D.J.; Spielmanb, D.S.; Ward, P.S. Ex ante and ex post effects of hybrid index insurance in Bangladesh. J. Dev. Econ. 2019, 136, 1–17. [Google Scholar] [CrossRef]

- Kassie, M.; Jaleta, M.; Shiferaw, B.; Mmbando, F.; Mekuria, M. Adoption of interrelated sustainable agricultural practices in smallholder systems: Evidence from rural Tanzania. Technol. Forecast. Soc. Chang. 2013, 80, 525–540. [Google Scholar] [CrossRef]

- Wu, H.; Li, J.; Ge, Y. Ambiguity preference, social learning and adoption of soil testing and formula fertilization technology. Technol. Forecast. Soc. Chang. 2022, 184, 122037. [Google Scholar] [CrossRef]

- Wongnaa, C.A.; Awunyo-Vitor, D.; Mensah, A.; Adams, F. Profit efficiency among maize farmers and implications for poverty alleviation and food security in Ghana. Sci. Afr. 2019, 6, e00206. [Google Scholar] [CrossRef]

- Giné, X.; Townsend, R.; Vickery, J. Patterns of rainfall insurance participation in rural India. World Bank Econ. Rev. 2008, 22, 539–566. [Google Scholar] [CrossRef]

- Liang, H.; Chu, Z.; Lyu, Y. Analysis of multi-farmers’ technology adoption behavior. Int. J. Multimed. Ubiquitous Eng. 2016, 11, 267–274. [Google Scholar] [CrossRef]

- Hu, X.Y.; Zheng, W.L. Climate change, agricultural risk and farmers’ agricultural insurance purchasing behavior. J. Soc. Sci. Hunan Norm. Univ. 2021, 2, 95–104. [Google Scholar] [CrossRef]

- Irving, G. Self-Presentation in Everyday Life; Anchor: Toronto, ON, Canada, 1959. [Google Scholar]

- Fan, Y.; Zhang, X.; Yan, J. Analysis of Subjective Reasons Causing Distortion of Questionnaire Results among Subjects. Hum. Resour. Manag. 2011, 1, 156–159. [Google Scholar]

- Li, F.N.; Zhang, J.B.; He, K. Influence of informal institutions and environmental regulations on green production behavior of farm households--Based on 1105 farm household survey data in Hubei. Resour. Sci. 2019, 41, 1227–1239. [Google Scholar]

- Okpukpara, B. Credit constraints and adoption of modern cassava production technologies in rural farming communities of Anambra State, Nigeria. Afr. J. Agric. Res. 2010, 5, 3379–3386. [Google Scholar] [CrossRef]

- Bridle, L.; Magruder, J.; McIntosh, C.; Suri, T. Experimental Insights on the Constraints to Agricultural Technology Adoption; Center for Effective Global Action: Berkeley, CA, USA, 2020. [Google Scholar]

- Hörner, D.; Bouguen, A.; Frölich, M.; Wollni, M. Knowledge and Adoption of Complex Agricultural Technologies: Evidence from an Extension Experiment. World Bank Econ. Rev. 2022, 36, 68–90. [Google Scholar] [CrossRef]

- Oyawole, F.P.; Shittu, A.; Kehinde, M.; Ogunnaike, G.; Akinjobi, L. Women empowerment and adoption of climate-smart agricultural practices in Nigeria. Afr. J. Econ. Manag. Stud. 2020, 12, 105–119. [Google Scholar] [CrossRef]

- Magruder, J.R. An assessment of experimental evidence on agricultural technology adoption in developing countries. Annu. Rev. Resour. Econ. 2018, 10, 299–316. [Google Scholar] [CrossRef]

- Takahashi, K.; Mano, Y.; Otsuka, K. Learning from experts and peer farmers about rice production: Experimental evidence from Cote d’Ivoire. World Dev. 2019, 122, 157–169. [Google Scholar] [CrossRef]

- Benjamin, D. Household composition, labor markets, and labor demand: Testing for separation in agricultural household models. Econom. J. Econom. Soc. 1992, 60, 287–322. [Google Scholar] [CrossRef]

- Chaudhuri, S.; Osborne, T. Financial Market Imperfections and Technical Change in a Poor Agrarian Economy; Italy Working Paper; European University Institute Florence: Fiesole, Italy, 2002. [Google Scholar]

- Bewket, W. Soil and water conservation intervention with conventional technologies in northwestern highlands of Ethiopia: Acceptance and adoption by farmers. Land Use Policy 2007, 24, 404–416. [Google Scholar] [CrossRef]

- Gine, X.; Klonner, S. Credit Constraints as a Barrier to Technology Adoption by the Poor: Lessons from South Indian Small-Scale Fisheries; Palgrave Macmillan: London, UK, 2008. [Google Scholar] [CrossRef]

- Bojnec, Š. Agricultural and rural capital markets in Turkey, Croatia and the FYR of Macedonia. Agric. Econ. 2012, 58, 533–541. [Google Scholar] [CrossRef] [Green Version]

- Mariano, M.J.; Villano, R.; Fleming, E. Factors influencing farmers’ adoption of modern rice technologies and good management practices in the Philippines. Agric. Syst. 2012, 110, 41–53. [Google Scholar] [CrossRef]

| Province | Sample Cities (Counties) | Sample Cities (Counties) | Number of Samples | Percentage |

|---|---|---|---|---|

| Shaanxi Province | Yongshou County | Changning Town, Ganjing Town, Quzi Town, Dian Tou Town, Jianjun Town | 79 | 19.04% |

| Heyang County | Wangcun Town, Lujing Town, Heichi Town, Xinchi Town, Fang Town | 178 | 42.89% | |

| Shanxi Province | Yaodu District | Jindian Town, Tumen Town, Qiaoli Town, Wucun Town, Xiandi Town | 75 | 18.07% |

| Pinglu County | Shengrenjian Town, Zhangdian Town, Sanmen Town, Changle Town, Podi Town | 83 | 20.00% |

| Options | Plan A2 | Plan B2 | ||

|---|---|---|---|---|

| Red Card | Black Card | Red Card | Black Card | |

| 1 | 20 | 20 | 22 | 18 |

| 2 | 20 | 20 | 23 | 17 |

| 3 | 20 | 20 | 25 | 15 |

| 4 | 20 | 20 | 35 | 15 |

| 5 | 20 | 20 | 37 | 13 |

| 6 | 20 | 20 | 40 | 10 |

| 7 | 20 | 20 | 52 | 8 |

| 8 | 20 | 20 | 54 | 6 |

| 9 | 20 | 20 | 56 | 4 |

| 10 | 20 | 20 | 60 | 0 |

| Variables | Meaning and Assignment of Variables | Mean | S.D. |

|---|---|---|---|

| Choice | Choice1: The technology selection in the first round of experimentTraditional seeds = 0, Innovative seeds = 1 | 0.52 | 0.50 |

| Choice2: The technology selection in the second round of experimentTraditional seeds = 0, innovative seeds = 1 | 0.54 | 0.49 | |

| Credit constraint | If CNY 50,000 is needed for production turnaround, how easy is it to borrow? (1 = very difficult; 2 = a little bit difficulty; 3 = okay; 4 = easy; 5 = very easy) | 3.43 | 1.22 |

| Interlinked insurance and credit contract | If the farmer belongs to treatment group, then assign thevalue of 1; otherwise, then assigned 0 | 0.46 | 0.49 |

| Age | The actual age of the respondent, Unit: year | 56.93 | 9.49 |

| Education | Years of education of respondent, Unit: year | 7.51 | 2.89 |

| Leader | Is the head of the household a village official? 1 = Yes; 0 = No | 0.16 | 0.36 |

| Income | Total income of the sample households in the last year., unit: Yuan | 1.42 | 5.53 |

| Number | Number of plots planted with wheat, Unit: block | 4.44 | 29.38 |

| Labor | Number of family agricultural laborers | 2.05 | 0.90 |

| Ratio | Ratio of wheat cultivation area to cultivated area (%) | 0.68 | 0.29 |

| Financial | Are there any family members or relatives working in financial institutions? 1 = Yes; 0 = No | 0.04 | 0.19 |

| Insurance | Did your household take out insurance for growing wheat last year?(1 = yes; 0 = no) | 0.51 | 0.50 |

| Risk | Measured by the Farmers’ Risk Attitude Test | 0.32 | 0.35 |

| Training | Number of times respondents attended training on wheat growing techniques in the past year | 0.69 | 2.42 |

| Information | Does the village provide technological information services for defense against weather hazards? 1 = Yes; 0 = No | 0.52 | 0.50 |

| Distance | How far is your home from the nearest financial institution, such as a rural credit union? Unit: mile | 5.30 | 3.73 |

| Perception | How do you think the local precipitation in the last 5 years? 1 = significantly decreased; 2 = somewhat decreased; 3 = not significantly changed; 4 = somewhat increased; 5 = significantly increased | 2.81 | 0.93 |

| Climate | Do you think the local climate has been warming in the last 30 years? 1 = very disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = very agree | 4.23 | 0.88 |

| Province | 0 = Shanxi, 1 = Shanxi | 0.62 | 0.49 |

| Variables | First Round of Experiments | Second Round of Experiments | ||

|---|---|---|---|---|

| Probit Model | Marginal Effect | Probit Model | Marginal Effect | |

| Credit constraint | −0.4851 *** (0.07) | −0.1932 *** (0.02) | −0.6038 *** (0.08) | −0.2317 *** (0.03) |

| Interlinked insurance and credit contract | 0.6047 ** (0.15) | 0.2369 *** (0.06) | 0.5841 ** (0.16) | 0.2197 ** (0.06) |

| Age | −0.0015 (0.00) | −0.0005 (0.00) | −0.0106 (0.01) | −0.0041 (0.00) |

| Education | 0.0434 * (0.03) | 0.0173 * (0.01) | 0.0487 * (0.03) | 0.0187 * (0.01) |

| Leader | 0.3557 * (0.21) | 0.1391 * (0.08) | 0.1707 (0.22) | 0.0642 (0.08) |

| Income | 0.1392 ** (0.07) | 0.0555 ** (0.03) | 0.3721 ** (0.11) | 0.1427 *** (0.04) |

| Number | −0.0369 (0.02) | −0.0147 (0.01) | −0.0328 (0.03) | −0.0126 (0.01) |

| Labor | −0.0363 (0.08) | −0.0145 (0.03) | 0.0350 (0.08) | 0.0134 (0.03) |

| Ratio | 0.4595 * (0.25) | 0.1831 * (0.10) | 0.3541 (0.26) | 0.1358 (0.10) |

| Financial | −0.4997 (0.39) | −0.1942 (0.14) | −0.6386 * (0.39) | −0.2505 * (0.15) |

| Insurance | −0.0115 (0.16) | −0.0046 (0.07) | 0.0277 (0.17) | 0.0106 (0.07) |

| Risk | 0.5456 ** (0.20) | 0.2174 ** (0.08) | 0.4929 ** (0.21) | 0.1890 ** (0.08) |

| Training | −0.1307 ** (0.05) | −0.0521 ** (0.02) | −0.0474 (0.04) | −0.0182 (0.02) |

| Information | 0.4575 ** (0.16) | 0.1808 ** (0.06) | 0.3464 ** (0.17) | 0.1325 ** (0.06) |

| Distance | −0.0466 ** (0.02) | −0.0186 ** (0.01) | −0.0334 (0.02) | −0.0128 (0.01) |

| Perception | 0.0055 (0.08) | −0.0048 (0.03) | −0.1308 * (0.08) | −0.0501 * (0.03) |

| Climate | 0.0534 (0.09) | 0.0212 (0.04) | −0.0231 (0.09) | −0.0088 (0.04) |

| Distance | 0.1955 (0.18) | 0.0778 (0.07) | 0.2111 (0.19) | 0.0814 (0.08) |

| Weather | −0.1236 (0.16) | −0.0471 (0.06) | ||

| Constant | 0.0354 (0.85) | 1.3755 * (0.88) | ||

| LR chi2 | 132.85 | 165.10 | ||

| Prob > Chi2 | 0.0000 | 0.0000 | ||

| Log likelihood | −220.96063 | −203.4569 | ||

| Pseudo R2 | 0.2311 | 0.2886 | ||

| Number of samples | 415 | 415 | ||

| Variables | First Round of Experiments | Second Round of Experiments | ||||

|---|---|---|---|---|---|---|

| Model Replacement | Excluding Extreme Values | Transformation Samples | Model Replacement | Excluding Extreme Values | Transformation Samples | |

| Credit constraint | −0.8096 *** (0.12) | −0.6013 *** (0.12) | −0.191 *** (0.04) | −1.0125 *** (0.13) | −0.8725 *** (0.13) | −0.169 *** (0.03) |

| Interlinked insurance and credit contract | 1.0284 *** (0.26) | 0.4319 ** (0.17) | 0.304 *** (0.07) | 0.9833 *** (0.27) | 0.4585 ** (0.19) | 0.180 *** (0.06) |

| Weather | −0.2406 (0.27) | −0.3090 (0.19) | −0.0264 (0.06) | |||

| Control Variables | Controlled | Controlled | ||||

| Regional dummy variables | Controlled | Controlled | ||||

| LR Chi2 | 132.69 | 79.00 | 91.14 | 164.21 | 115.68 | 91.14 |

| Prob > Chi2 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Pseudo R2 | 0.2309 | 0.1989 | 0.2445 | 0.2871 | 0.2931 | 0.2499 |

| Log Likelihood | −221.0421 | −159.1246 | −141.2127 | −203.9015 | −139.5304 | −136.7986 |

| Number of samples | 415 | 288 | 275 | 415 | 288 | 275 |

| Variables | First Round of Experiments | Second Round of Experiments | ||||||

|---|---|---|---|---|---|---|---|---|

| Not Available | Available | Not Available | Available | |||||

| Coefficient | Marginal | Coefficient | Marginal | Coefficient | Marginal | Coefficient | Marginal | |

| Credit constraint | −0.3060 *** (0.08) | −0.1219 *** (0.03) | −0.8876 *** (0.14) | −0.3448 *** (0.06) | −0.4645 *** (0.09) | −0.1796 *** (0.04) | −0.8800 ** (0.14) | −0.3250 *** (0.06) |

| Weather | −0.1933 (0.21) | −0.0740 (0.08) | 0.0790 (0.29) | 0.0294 (0.11) | ||||

| Control Variables | Controlled | Controlled | ||||||

| Regional dummy variables | Controlled | Controlled | ||||||

| LR Chi2 | 49.21 | 109.69 | 64.78 | 121.86 | ||||

| Prob > Chi2 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | ||||

| Pseudo R2 | 0.1591 | 0.4223 | 0.2086 | 0.4704 | ||||

| Log Likelihood | −130.0886 | −75.0201 | −122.8414 | −68.5982 | ||||

| Number of samples | 224 | 191 | 224 | 191 | ||||

| Experience p-value | 0.000 | 0.014 | ||||||

| Variables | First Round | Second Round | ||

|---|---|---|---|---|

| Education ≥ 7.5 | Education < 7.5 | Education ≥ 7.5 | Education < 7.5 | |

| Interlinked insurance and credit contract | 0.170 ** (0.07) | 0.140 (0.09) | 0.102 * (0.06) | 0.0830 (0.09) |

| Observations | 247 | 168 | 247 | 168 |

| Variables | First round of Experiments (Marginal Effect) | Second Round of Experiments (Marginal Effect) | ||

|---|---|---|---|---|

| (1) Treatment Group | (2) Control Group | (3) Treatment Group | (4) Control Group | |

| Credit constraint | −0.345 *** | −0.122 *** | −0.325 *** | −0.180 *** |

| (0.06) | (0.03) | (0.06) | (0.04) | |

| Education | −0.0147 | 0.0379 *** | −0.00122 | 0.0281 ** |

| (0.02) | (0.01) | (0.02) | (0.01) | |

| Control Variables | Controlled | Controlled | Controlled | Controlled |

| Regional dummy variables | Controlled | Controlled | Controlled | Controlled |

| Number of samples | 191 | 224 | 191 | 224 |

| LR chi2 | 109.69 | 49.21 | 121.86 | 64.78 |

| Prob > Chi2 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Log likelihood | −75.0201 | −130.0886 | −68.5982 | −122.8414 |

| Pseudo R2 | 0.4223 | 0.1591 | 0.4704 | 0.2086 |

| Variables | Treatment Group | Control Group | Differences | P |

|---|---|---|---|---|

| Education | 7.54 | 7.48 | −0.06 | 0.8212 |

| Risk | 0.2128 | 0.2889 | 0.0761 ** | 0.0171 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, L.; Song, Y.; Wu, H.; Shi, H. Credit Constraint, Interlinked Insurance and Credit Contract and Farmers’ Adoption of Innovative Seeds-Field Experiment of the Loess Plateau. Land 2023, 12, 357. https://0-doi-org.brum.beds.ac.uk/10.3390/land12020357

Yu L, Song Y, Wu H, Shi H. Credit Constraint, Interlinked Insurance and Credit Contract and Farmers’ Adoption of Innovative Seeds-Field Experiment of the Loess Plateau. Land. 2023; 12(2):357. https://0-doi-org.brum.beds.ac.uk/10.3390/land12020357

Chicago/Turabian StyleYu, Leshan, Yan Song, Haixia Wu, and Hengtong Shi. 2023. "Credit Constraint, Interlinked Insurance and Credit Contract and Farmers’ Adoption of Innovative Seeds-Field Experiment of the Loess Plateau" Land 12, no. 2: 357. https://0-doi-org.brum.beds.ac.uk/10.3390/land12020357