Random Risk Factors Influencing Cash Flows: Modifying RADR

1

Department of Theoretical and Applied Economics, Institute of Administration and Postgraduate Education, Lviv Polytechnic National University, 79013 Lviv, Ukraine

2

Department of Economics and Finance, Faculty of Management, Comenius University in Bratislava, 81499 Bratislava, Slovakia

*

Author to whom correspondence should be addressed.

Mathematics 2023, 11(2), 427; https://0-doi-org.brum.beds.ac.uk/10.3390/math11020427

Submission received: 9 November 2022

/

Revised: 4 January 2023

/

Accepted: 10 January 2023

/

Published: 13 January 2023

(This article belongs to the Special Issue Mathematical Methods and Analysis for the Industrial Management and Business, 2nd Edition)

Abstract

:In this article, we focus on considering different risk factors influencing the cash flows of a group of companies. A methodology is suggested for approximated consideration of both seasonal and random fluctuations in the environment, which have some impact on the overall group activity and may be considered via modification of the risk-adjusted discount rates. The main steps of the suggested methodology are described, and the elements of the risk-adjusted discount rate are presented. Although it is the general convention to use the market rate as the discount rate in most cases, under certain circumstances—i.e., stochastic shocks related to the level of interest rates, shifts, and turnabouts in the social environment, as well as the market transformations due to annual/seasonal epidemics, the use of a risk-adjusted discount rate becomes essential. The influence of the seasonal and random changes in the general environment on the companies’ activity through modification of the discount rate is illustrated both numerically and graphically in the article, providing analysis of the impact of exogenous parameters on companies’ output, profits, net present value, and discounted payback period for the initial investment.

MSC:

91-101. Introduction

Market volatility has conditioned the growing necessity of risk analysis and management. In order to limit risk and decrease ambiguity, the risk management process optimises business decisions in line with the identified factors of uncertainty. Environment unpredictability causes challenges that create equally potential losses and possibilities, and it is the task of risk management to assess loss exposure and define the possibility of gains.

A number of works have been dedicated to studying the influence of environmental instability on organisational flexibility and companies’ performance, as well as ensuring corporate security in the context of countering external and internal threats [1,2].

Considering the risk valuation and mitigation possibilities the types of risk are commonly grouped into:

- -

- systematic risk—the overall impact of the market, valid for all economic entities; and

- -

- non-systematic risk—asset-specific or company-specific uncertainty, which may be diversified to a large extent.

In addition, risk types are usually grouped by the following general categories: economic, financial, political, social, and others. According to the level of analysis, economic risks fall into several basic categories—global, strategic, traditional market, and industry risks. Depending on the risk type and category, different risk valuation and mitigation methods are generally applied.

The general risk management process’s key stages, as depicted in Figure 1.

Thus, considering the need for quantitative risk analysis, we suggest taking into account the value of money in time and the risk influence on the group activity in addition to the factors considered in our research before [3]. We introduce a mechanism that adjusts cash flows for the impact of the abovementioned factors, except for inflation, by discounting cash flows generated during the organisation/group activity.

We do not take into account inflation in this study for several reasons. First, since inflation must be adjusted for both the dynamics of cash flows and the discount rate, we neglect its effect on these values. Second, we simplify the modelling and avoid extra debate on what level of inflation to apply, as the cash flows were generated in several countries. The group expenses originate from the three countries, and revenues are generated from sales in different European countries without stable sales shares per country. Various currencies have various expected inflation rates embedded in them, and these differences equally affect the estimates of expected cash flows and discount rates. When dealing with a high-inflation currency, we should expect higher discount rates and cash flows—on the contrary, with a lower-inflation currency, discount rates and cash flows will be lower. Therefore, we removed inflation entirely from the process using real cash flows and real discount rate.

In this work, we would like to focus on estimating intergroup investment efficiency considering random risk factors. Here the risk is being determined as the probability that actual results will differ from planned or expected results or the volatility of returns. We suggest an approach that would be practical and applicable to average-size companies.

The efficiency of an investment project is usually evaluated via four fundamental indicators, such as net discounted income, profitability index, the payback period of investments, and internal rate of return on investment. Still, one of the most effective means to assess the effectiveness of an investment is the net present value (NPV), the total amount of discounted net cash flow received during the study period.

Riskier assets should generally have more significant expected returns to compensate investors for the increased volatility and higher risk. This mechanism of evaluating investments considering their volatility is realised by applying a discount rate to all future net cash flows, reflecting all primary risks related to the company and its activity. The discount rate value is a significant factor that determines the value of performance indicators and therefore affects the final decision on the practicality of investment project implementation. It is often argued that resolving the rate at which it is necessary to capitalise income is essentially a method of trial and error, and as many methods for calculating the discount rate exist as there are definitions of the term itself [1]. Increasing the accuracy of the forecast assessment of an investment project’s effectiveness in an acute shortage of investment resources necessitates additional justification for choosing the discount rate. Typically, risk and return models in finance measure the expected returns on risky activities and investments relative to the risk-free rate. Then the risk creates an expected risk premium that is added to the risk-free rate.

Our approach refers to the Capital Asset Pricing Model (CAPM) [4]—and we will apply a similar idea here with some amendments, considering that the discount rate consists of the following components:

- A risk-free rate, as compensation for delayed consumption or time value of money (rf);

- The premium for market-related risk (rm—rf);

- Adjustment for sovereign risk (rs).

As mentioned above, we omitted the premium related to inflation in this research. We consider the mentioned elements of the discount rate—the real risk-free rate, adjustment for the market-related and product-related risk, and adjustment for sovereign risk, and add a function responsible for random fluctuations, thus building a compound discount rate.

Compound discount rates account for both time and risk and may take the form of a Risk-Adjusted Discount Rate (RADR) determined from a market risk-return model or a Weighted Average Cost of Capital (WACC). The market risk-return model, which is more applicable in our case, attempts to determine from financial market data, a fair return for the investment based on the activity/market uncertainty characteristics [5]. The RADR technique aims to increase the investor’s probability of earning a return over time that is sufficient to compensate for the additional risk associated with specific activities and markets.

Speaking of risk as some level of uncertainty about possible unwanted events that may occur in the future, we need to consider the two dimensions of risk—the probability of the unwanted harmful event and the possible outcomes of that event. Risk analysis also implies using random values to estimate the probability of an adverse event occurring. To build an appropriate model for calculating the discounted cash flows generated within the group of enterprises, we will thus apply a random value and include it into RADR to encounter the random factors influencing the analysed market and the environment within the countries considered.

Many former and recent publications [5,6,7,8,9] suggest approaches for considering risk adjustment as a part of a discounting technique. Some authors concentrate on decomposing the risk into elements and exploring the aspects of risk/uncertainty—i.e., as components of country-specific uncertainty [10]. Theoretical and empirical economists can put more considerable emphasis on macro-level uncertainty [11] or financial markets [12]. Other works investigate the types of distribution characterising risk factors and variables—pointing at the pitfalls of assuming normal risk distribution and suggesting fractal risk distribution [13]. They state that measurements with mild variability may be treated using the normal distribution, but those with wild randomness can only be described correctly using a fractal scale. Some researchers have looked into alternatives to risk adjustment of the discount rate [6].

Our article introduces an application of random risk-influencing factors analysis by applying a random value with conventional normal distribution properties. The normal distribution is widely used in risk analysis [14,15,16] and criticised [13,17] in several works. We pay more attention to the micro-level and try to develop a tool for considering uncertainty and risks in the value of cash flows by modifying a discount rate in the CAPM model. We consider a typical cooperation structure between production and sales units, creating a basis for solving a broad spectrum of tasks within similar microeconomic systems.

Thus, the paper proceeds as follows. In the next section, we describe our general model and the methods. In particular, we discuss the companies’ roles and interrelations, present the key variables, and then describe the methodology. In Section 3, we present our approach to modifying the risk-adjusted discount rate, introduce the random value as a component of the rate, and provide numerical calculations applying different scenarios of the random value distribution along with a graphical representation. Section 4 concludes the paper.

2. Materials and Methods

2.1. General Model

In the previous works [3,18], we presented a general mathematic model describing the economic dynamics of three associated enterprises. We add some of its parts here for better understanding. The model includes exogenous (external) factors, including the market demand for the goods and endogenous (internal) factors. The model presented in our previous works, together with the study of random factors described in the current article, covers all main economic aspects of production-and-sales group operations [19,20,21].

The primary variables used for describing the system status are:

- : retained earnings (accrued profits) over t months for each of the enterprises , where is the index of the enterprises and t stands for the period of calculations (t max = 60 months);

- : own accrued capital of the enterprise

- : accrued invested (accepted) capital over t months from enterprise

- : level of output by production enterprises in month t (total output from the beginning of the activity to the end of month t),.

Thus, basic variables include the Level of Production Orders, Income, and Investments. In descriptions of the dynamics of the system, we introduce some additional variables as functions of the abovementioned:

- : net profit of the enterprise in month t, not considering depreciation and amortization;

- : part of the third enterprise’s net profits, invested into the capital of the enterprise ;

- : part of the enterprise’s three net profits remaining after investing in the capital of other enterprises.

We built a 12-dimensional column vector:. The column vector, , describes the economic status and activity results for each of the enterprises in month t. Components, , of this vector are time-dependent values.

We also consider the influence of exogenous economic factors on the system dynamics, such as product prices, wages, tax rate, level of some fixed costs, etc.:

- : transfer price (the price for which the production enterprise is selling its products to the sales enterprise within the group);

- : the product sales price;

- : monthly fixed general administrative expenses;

- : monthly fixed marketing and sales expenses;

- : variable unit sales costs;

- : labour unit costs;

- : number of direct production personnel;

- ηi: coefficient characterising capital and labour productivity.

During the conjoint activity of the enterprises, their total production output (production orders) is split by the sales enterprise between the production enterprises based on the level of their production costs. The efficiency of each production enterprise activity is estimated here as a parameter proportional to its relative (comparing to the total of two production enterprises) production capacity. Herewith, the levels of ancillary quantities, , are considered, i.e., for enterprise 1, the level of quantity, , is:

where is the maximum possible production capacity of the enterprise (defined based on the total amount of the capital, labour, and efficiency of the enterprise inputs). The function of maximum production capacity relates to a modified Cobb–Douglas production function [22]:

where λ1 and λ2 are parameters characterising the efficiency of the enterprise inputs (capital and labour); λ1 + λ2 = 1; λ1, λ2 > 0.

The production output for enterprise i (i = 1,2) is planned to be equal to the lesser of the two described values, .

Each of the enterprises possesses an initial amount of capital depreciated at given rate, which may increase due to reinvestments of the net profit and is calculated as the sum of own starting capital and reinvested net profit during the period of activity. Increase of the enterprise’s own capital equals

where is the rate of reinvestment of the net profit into the productive capital of the enterprise i, is the rate of depreciation of the capital of enterprise i per month, and is the amount of net profit of enterprise i per month t:

The initial amount of the enterprises’ capital purely reflects the level of its own capital. During the enterprises’ conjoint activity, the sales enterprise (acting as a client at the beginning) also becomes a strategic partner, investing its own resources into the capital of the production enterprises. Increase of the accepted (invested) capital at the beginning of the month t + 1 for production enterprises (union members) is calculated according to the formula:

where is the share of the sales enterprise’s net profit invested into the capital of production enterprise i in month t.

The amount of investments from the side of the strategic partner into the capital of production enterprises, depends on the maximally permissible share of the strategic partner in the capital of the accepting production enterprise for the previous month and the total amount of net profit of the sales enterprise, which is the source of reinvestments. The amounts of investments by the sales enterprise into the capital of enterprise i equals

where is the amount of investment into the capital of enterprise i, defined as the part of total investments in the current month, proportional to the relative capital profitability/return on equity:

, or relative profitability of the production enterprises’ capital (i = 1,2):

- : the amount of investments which allows the production enterprise i to remain the owner of the main share of the total capital, considering the described system of reinvestments;

- : the allowed relative share of the accepted capital in total capital value (defined by the enterprise management).

Net profit of the sales enterprise, , equals the sum of the income from sales and income from financial investments (participation in the capital of the production enterprises), decreased by the sum of fixed monthly costs and variable costs. The latter includes costs related to the sales of goods, ; transport costs, ; costs for delivery of goods from production enterprises to the sale enterprise; and costs of the purchase of the goods at the transfer prices:

where is the income of the sales enterprise from financial investments into the capital of enterprise i, i = 1,2:

Retained earnings of the sales enterprise equal the difference between its net profit and the amount of investments into the capital of production enterprises. Repayment of the financial profit on investments by the accepting enterprises will be performed after all their costs are covered. Thus, the investor is partly involved in covering the costs of production enterprises. The total amount of investments into the capital of production enterprises is related to the total group profit; therefore, each production enterprise is interested in total group success. That is one of preconditions of synergy [23] in the present group structure.

For building the model as a system of differential equations, we assume that time (t) is changing discretely in a step of 1 month: month. Formally going to , we obtain a first-order system of nonlinear differential equations.

We suppose that each of these factors is slightly dependent on time within the scale of the group activity; therefore, the equations describing system dynamics we write as

Considering endogenous parameters as components of a certain vector , i.e., , etc., this system of equations may be written as:

The functions, , depend on the elements of the column vector, , and on the mentioned above factors.

The calculations were performed according to the developed model for defining basic economic indicators of the enterprises. The model was calibrated for values reflecting actual enterprises’ activity.

According to the initial assumptions, the monthly demand for the goods is the sum of an upward trend, component D(t) (t—number of months of the group activity), which we call guaranteed demand, and variable components related to seasonal and random demand fluctuations, considered in our previous research.

The described general model is being applied in this article for a special case— the actual companies’ association, functioning in the area of apparel production and sales, including Danish management, logistics, and sales company, Company 3; a Ukrainian production factory, Company 1; and a Polish production factory, Company 2. The economical parameters of the mentioned companies are considered. In this particular case, the number of enterprises described in the model is n = 3. The indices of enterprises: of production enterprises, Company 1 is i = 1, and Company 2—i = 2; sales enterprise, Company 3 (generating and placing orders) is i = 3.

The trends in developing textile and apparel (T&A) industries during the recent decades included intensive structural changes, such as the relocation of operational activity to developing countries. The model reflects this trend, describing the functions split between the companies. The activity of Company 1 is currently at the stage of growth, while Company 3 is at the stage of maturity. Company 1’s market is fragmented, and the company share is not significant. The market of Company 3 is not fragmented, and the company share is quite substantial.

In this situation, the companies’ affiliation would be aligned with a functional principle, allowing for vertical integration between the collaborating businesses. Value chain strategies in this area, as well as in comparable markets, are continually evolving. Successful businesses are rarely competitive for long [24]. As a result, we hope to contribute to the general study of successful competitive strategies. The purposes set by each of the parties are as follows:

- For Companies 1 and 2: economy on the scale due to vertical integration; benefits from access to resources (financial, material, technical, and also non-material) to strengthen the financial status and technological upgrading of the enterprise; load levelling-out of production capacities during a year; transfer of organisational, production, and sales knowledge; use of the actual practice of research and development (R&D) and manufacturing; and use of partner’s distribution trademark in sales.

- For Company 3: possibility to exploit comparative advantages; risks distribution; potential advantages from entering a new market with lower competition; using growth potential of the less mature market; economy on the scale due to vertical integration; balancing production costs; shared use of non-material resources, such as transfer of knowledge and experience; access to comparatively cheaper resources; and decrease of production costs.

The reason for choosing the mentioned countries was that the companies located there represent a typical scheme within the apparel industry, with a specific role of each company (a company-holding and investor and two companies-producers). In addition, the model has been built using some real numbers from their activity. The suggested original model describes synergetic interrelationships between the analysed entities—showing benefits from their cooperation and measuring the synergetic effect. At the same time, these companies/countries are an example which may be applied across similar countries.

2.2. Methods

2.2.1. Additional Variables

The frames of the general model’s calculations were applied to define the fundamental economic indicators of the enterprises. We pre-defined the companies’ activity parameters and estimated the influence of changes in indicators such as production volume, level of reinvestment and discounting, and the dynamics of these factors. In this work, in a stochastic model containing recurrent differential equations, we also consider other random influences on the fundamental activity indicators that allow valuing potential risks influencing the system.

For simplicity reasons, in our previous works, we have assumed that all the cash flows are the real cash flows adjusted for risk factors (such as market and country risks and inflation, so money value in time was considered not to have any influence on the values within the model). In this work, we would like to focus on risk factor mitigation by incorporating risk valuation into the initial model. The current paper aims to study the effect of different factors impacting the discount rate on the financial results (NPV) of the group’s activity. The major input includes considering random factors in calculating the discount rate.

All values in our model are expressed in one currency, as valuation in financial management or capital budgeting contains an important presumption that cash flows and discount rates in the discounted cash flow (DCF) analysis must be denominated in the same currency. This principle allows the development of estimation mechanisms for dealing with different currencies [24].

In addition to the primary variables used for describing the system status, here we introduce some additional functions of these variables, including:

- : net profit of the enterprise in month t, not considering depreciation and amortization;

- : free cash flow of the enterprise in month t;

- net present value of the cash flows generated within the group in month t, the discounted value of the net profit remaining after investing in the capital of other enterprises;

In addition, we bring in some new variables to allow for risk valuation, such as:

- : risk-adjusted discount rate;

- risk-free rate;

- (: risk premium referred to non-systematic market risk;

- : sovereign risk premium referred to non-systematic country risk;

- : the measure of the systematic risk, the degree to which the group return varies with the overall market return, representing both financial and business risk;

- random value reflecting the factors influencing the discount rate; mean and standard deviation varied for investigation reasons.

Here we introduce a new variable—free cash flow (FCF). is the value of the Free Cash Flow of enterprise i per month t; i = 1, 2. The traditional definition of free cash flow (FCF) is the cash generated by a corporation after accounting for cash outflows to sustain operations and maintain capital assets. In other words, free cash flow is the cash remaining after a company pays for its operating expenses (OpEx) and capital expenditures (CapEx), here accounted as the reinvestments into capital (as in Equation (13)).

where is the level of profit tax in the country of operation for the company i according to officially published data [25,26,27].

As previously stated, adduced calculations were implemented in recurring equations defining the dynamics of the economic system. The equations were linearised differential equations, and research of the system’s solution stability and companies’ activity mode’s influence on various elements and column vector components was carried out, allowing for establishing intervals of their optimum and undesirable values.

2.2.2. Risk-Adjusted Discount Rate

Thus, the key exogenous random components in the current model are the volume of market demand for the products manufactured by the group’s enterprises and the cash flow discount rate adjusted for risk. Exogenous influences depend on actual conditions and different social and economic factors [28] that cannot be accurately predicted and specified by an explicit formula. We consider the influence of such factors by introducing into the system time-dependent random values (random process [29]), which we assume to be normally distributed [30]. We model random deviations using the properties of well-known normally distributed functions. This gives us a better understanding of the nature of the obtained results. The random value we apply reflects the influence of multiple risk factors. Thus, there is reason to believe that it is normally distributed, as “if you take sufficiently large samples from a population, the samples’ means will be normally distributed, even if the population is not normally distributed” [31,32].

In the current article, we introduce a random value to consider multiple risk influences on the system parameters, such as prices, revenue, costs, and profits; the latter is considered in the NPV of the free cash flows analysis.

Risk analysts apply random variables in risk models to evaluate the probability of an adverse event occurring. Using the risk-adjusted discount rate method, the companies calculate the risk-adjusted NPV in the following way: the risk-adjusted discount rate, which could be equal to the risk-free discount rate (for normal risk projects), higher (for above-normal risk projects), or lower (for below-normal risk projects), is applied for calculating the discounted value of the business cash flows. The risk-adjusted discount rate typically includes the risk-free rate plus a risk premium appropriate for the project.

The risk-adjusted discount rate for our model has the following structure:

where —is a random value taking into account random deviations of the exogenous factors related to the companies’ activity (discussed further).

The random value introduced in this article is applied to all components of the RADR above its risk-free level. By modifying its parameters—mean and standard deviation, we can investigate the level of risks that may have a crucial influence on the group’s financial results.

The risk-free interest rate is the value attributed to an investment that assures a return with no risks while accounting for the rate of inflation; that is, a real risk-free rate is modified for the rate of inflation:

rf = (1 + Nominal rf)/(1 + Inflation Rate)

The risk-free rate is usually a function of the policy of the central bank of a sovereign nation. Investments in US bonds are thought to be risk-free since there is a minimal chance of the government defaulting. In general, the risk-free return is equal to the yield on a 10-year US government bond [33]. The level of the risk-free rate of return, therefore, will be set as 3.02% taking into account the recent officially published data [34] and expected inflation of 2022–2027 published by the IMF, as mentioned in [35].

The risk-free rate plays a significant role in the capital asset pricing model (CAPM) [36], which is the most widely applied model for estimating the cost of equity. The risk-free rate provides the minimum rate of return, to which we add the excess return (i.e., the market beta coefficient multiplied by the equity risk premium).

The expected return that an investor obtains (or expects to receive in the future) from owning a risk-laden portfolio rather than risk-free assets is referred to as Market Risk Premium (. In most risk-adjusted models developed from conventional portfolio theory, market risk is the primary type of risk assumed relevant for estimating a cost of equity, and is considered as the risk that cannot be eliminated through diversifying. The decision is made if the investment in securities should take place, and if yes, the rate that the investor will earn beyond the risk-free return offered by government securities is the risk premium. A company’s risk exposure also depends on its life cycle, as young companies possess limited resources to overcome impediments and are far more dependent on macro-environmental factors to remain stable to succeed. The level of market premium is set as according to the published expert recommendations [24,35,37] for our study.

The volatility of an asset—in our case, the group’s activity, reflected by the value of the projected cash flows—is assessed by the beta ( factor concerning the whole market in general. The fluctuations caused in the rate value due to changes in market conditions are denoted by the beta. For example, if the beta is 1.4, it would cause a 140% deviation due to any changes in the general market. The opposite is the case for a beta below 1. For a beta equal to 1, the operations are in complete sync with the changes in the market.

As there is no straightforward method for estimating equity beta, the valuation of private companies using CAPM can be questionable. There are several basic approaches for assessing a private company’s beta, one of which is getting a comparable levered beta from an industry average or from a comparable company (companies) that best mimics the private company’s current business, unlevering this beta factor, and then finding the levered beta for the private company using the company’s target debt-to-equity ratio. As an alternative, the beta can be defined as the company’s earnings and used as a proxy for the company after appropriate adjustments are made [38]. For our model, to encounter the market risk components, we set 1.11 based on the data on average unlevered beta for Apparel Companies [39].

The Sovereign Risk Premium, or Country Risk Premium (CRP) is the expected higher returns for an investor rewarded for being exposed to additional risk as to the result of holding an asset or providing activity in a certain country. Vulnerability to country risk originates from the group’s activity, making sovereign risk a significant component of the valuation of almost every large company with cross-country operations. The group’s risk exposure is linked to the environment where it does business; thus, the level of country risk premium should reflect its operating risk exposure. If the returns/activities across countries have a significant positive correlation, country risk has a market risk component, is not diversifiable, and can require a premium. Currency and country risk are typically associated, with countries with high country risk also having the most volatile currencies. If this is the case, discount rates on investments in these countries will be higher, but this is due to country risk rather than currency risk. Considering the nature and level of sovereign risks, we might assume that equity risk premiums should vary across countries [24,40,41]. The country risk premiums applied are presented in Table 1 below.

The risk-influencing factors may be summarised as follows:

- 3.

- General systematic risk factors:

- Market price changes, reflected in the general attitude of investors;

- Economic recessions;

- Political turmoil;

- Changes in interest rates and interest rate related instruments;

- Changes in the value of foreign currencies;

- Natural disasters;

- Terrorist attacks;

- Other force-majeure factors affecting the whole market.

Systematic risk refers to macroeconomic and overall-political factors that affect the performance of all entities in the overall market.

- 4.

- Market (sometimes called product) unsystematic risk factors that are more closely related to a particular product or service also have different nature, such as:

- Demand risk;

- Price risk;

- Competition risk;

- Customer experience risk;

- Compliance risk;

- Security and fraud risk;

- Reputation risk;

- Operational risk;

- Product liability risk.

Market-specific or unsystematic risk only affects an industry, market segment, or a particular company. Market risk cannot be mitigated via portfolio diversification and is also known as volatility and can be measured using the beta. As mentioned above, the beta measures an investment’s systematic risk relative to the overall market [38].

- 5.

- Sovereign risk factors originating from:

- Stage of the country’s economic growth life cycle, states in early growth being more exposed to risk than mature countries;

- Political situation in the country, including the type of political system, power transfer within the state, and the trustworthiness of the governing institutions—those of inclusive or exclusive type, level of corruption as an implicit tax on income, risk of takeover [42];

- Country’s legal system, including its structure (the protection of property rights measured by an international property rights index) and efficiency (the speed with which legal disputes get resolved);

- State economy’s status and growth prospects (such as the strength of its tax system, fiscal and monetary flexibility, debt burden and liquidity, economic structure/reliance on a particular industry or product, and commodity export dependence on the commodity prices and sales volumes) results in additional risks.

Sovereign risk is measured in several dimensions to incorporate all types of country risk, allowing for comparisons across countries. A direct measure of country risk is the default risk of lending to the government of a state, termed sovereign default risk, and based on the level of the country’s indebtedness compared to GDP, social service commitments, stability, and size of inflows to the government, etc. There is a substantial correlation between sovereign defaults and sovereign ratings. Sovereign ratings are assigned and updated by rating agencies; agencies like Standard and Poor’s assign sovereign ratings considering a congregate of political, economic, and financial/institutional parameters.

Revenue sources and production facilities are both factors that influence a company’s exposure to nation risk. The revenue risk level is proportionate to the revenue coming from each particular country. In addition, a company may be exposed to country risk even if it derives no revenues from that country if its production facilities are located in that country.

Companies may be able to mitigate this risk by purchasing insurance against specific (unfavourable) eventualities and utilising derivatives. A company that uses risk management tools should be less vulnerable to country risk than a company that does not employ these products. However, risk management is not free. Insurance is expensive and will diminish any company’s margins and profits. Although futures contracts are less expensive, organisations that employ them forfeit upside potential while safeguarding against downside risk.

There are numerous debates concerning CRP, and several approaches have been suggested for considering CRP [24,43,44,45]. We applied the so-called “beta approach” for our model, including CRP into the classic CAPM approach and regulating it for the beta factor—as it is assumed that the company’s country risk is proportional to the market risk, that is, it can be measured using the beta factor; moreover, we consider the random fluctuation of the RADR value. The default spread that investors charge for buying bonds issued by the government is the simplest and most often used proxy for the country risk premium. However, alternative approaches may be applied for building the RADR; i.e., the credit swap premium [45] as the measure of sovereign risk may have some advantages.

The three countries’ equity risk premiums applied for modelling rely on the Prof. Damodaran country risk premium (CRP) study [35] and are as mentioned in Table 1.

We apply the risk-adjusted discount rate (RADR), including the abovementioned components, to the net cash flows as follows in Equation (16):

Typical NPV analysis interpretation [46,47] for investment appraisals applies a constant discount rate throughout the whole period of the investment project. We believe such an approach fails to adequately reflect the term structure of risk for investments. Therefore, we suggest applying discount rates that are modified in time and thus reflect the temporal structure of interest rates. The additional adjustments for the discount rates are related to specific project risks and information uncertainty. According to available forecasts [40,41], they are likely to result in the upward-sloping term structure of the discount rates, in the CRP element of the rates in particular—please see Equation (17).

where drs(i) is the monthly growth of the estimated respective CRP for the company (and the country) i.

The projected interest rate levels for the three countries relate to the forecasted country policy rates [24,39], as shown in Table 2.

Although we have not found any exact data forecast in this respect, we suggest to decrease the level of country risk premium in two countries—1 and 2, according (and proportionally) to the expert estimations of the country policy rates decrease.

2.2.3. Scenarios

The model that was built and partly presented in the given article allows us to compare the results of calculations, including and excluding the random factors; we also consider random factors that influence the RADR with different mean and standard deviation levels.

In the next section, we proceed with the analysis of the modified discount rate according to the following steps:

Adding a random value as a coefficient to the discount rate. We consider the random value with normal distribution and further set different parameters for the distribution.

Building scenarios considering the properties of the random value and dynamics of the discount rate itself—namely, we modify:

Mean of the random value: we set the mean in the range [1; 3].

The standard deviation of the random value: we set standard deviation in the range [0; 0.50].

Term structure of the interest rate: we consider scenarios with a fixed level of the rate vs. scenarios with the rate steady increase during the period of analysis.

Seasonal fluctuations of the discount rate: we consider scenarios with no rate fluctuations vs. scenarios including the rate fluctuations during a year (each year during the period of analysis).

Performing numerical calculations within different scenarios, including combinations of the mentioned modifications (point 2 above). The main idea is to define the scenarios that make the most significant impact on the financial result of the group’s activity.

Representing the key variables graphically.

Following the numeric calculations, we proceed with the conclusions regarding the scenarios resulting in the most significant changes in NPV.

3. Results

3.1. Random and Seasonal Discount Rate Fluctuations

We consider the following scenarios regarding the RADR, as shown in Table 3.

The abovementioned scenarios were analysed further below in different combinations and for different values of mean and standard deviation of the random coefficient (numbers in the scenario code refer to the different values of median and standard deviation).

As for the standard deviation and the mean levels, we considered different scenarios concerning general economic and market shock reactions. Thus, the banking crisis of 2008, which resulted in an approximately 25–30 per cent drop in US and EU equity markets, has simultaneously caused a 50% or higher decrease in many emerging markets. A similar situation occurred during the COVID market crisis in 2020 and 2021, with emerging markets undergoing more changes than developed ones.

The biggest world economies experienced a growth decline in 2019; such circumstances as general shakes in economic conditions, increasing competition, negative trends with regards to human resources, and significant regulatory actions may result in the impairment of a company’s goodwill and thus must be considered during the valuation of potential or current investment [48,49,50].

The impact of the pandemic was substantial across the textile and apparel industries. In Europe’s clothing sector, compared to the same period in 2019, production decreased by 37.4 per cent between April and June 2020, when global coronavirus cases peaked. Retail sales of clothing products saw the most dramatic decline, with a 43.5 per cent drop in sales [51].

Therefore, for our investigation, we have accounted for different standard deviation levels—from 0 to 0.5—to consider the abovementioned scenarios.

3.2. Numeric Calculations and Graphical Representation of Results

3.2.1. Impact of the Discount Rate’s Seasonal and Random Fluctuations on the System Dynamics

Before presenting the results of the model application, we consider the values of some critical indices characterising our group during the 5-year (60-month) activity period, shown in Table 4 below.

Although the generally accepted practice is to employ NPV analysis as the primary means of investment valuation, other widespread techniques are used in capital budgeting. They include the internal rate of return (IRR), the alternative modified internal rate of return (MIRR), and discounted payback period (DPP) methods. MIRR assumes positive cash flows will be reinvested at the company’s cost of capital and that the initial outlays are financed at the company’s cost of financing. They are normally used as a complement to NPV analysis. Therefore, we would like to include them here as well. Therefore, IRR was 28% for the whole project, and MIRR was 18%, given that the risk-free rate for reinvestment makes 3.02% and the financing rate is 0.05% [51]. DPP and NPV depend on the scenario conditions presented further.

The outcomes of different scenarios considered for RADR are presented in Table 5.

3.2.2. Graphical Representation of the Dynamics of Key Activity Indicators

We have therefore considered different conditions for RADR by modifying the parameters of the random value z. The analysis showed that the rate variation (standard deviation) does not have a distinct positive or negative impact on the total outcome of each scenario, such as NVP or payback period. Instead, the general upward shift of the rate level (mean) made the most significant negative impact; the critical level of the mean, turning NVP into a negative value, was m = 2 (with standard deviation σ = 0.20), as in scenarios B6–8.

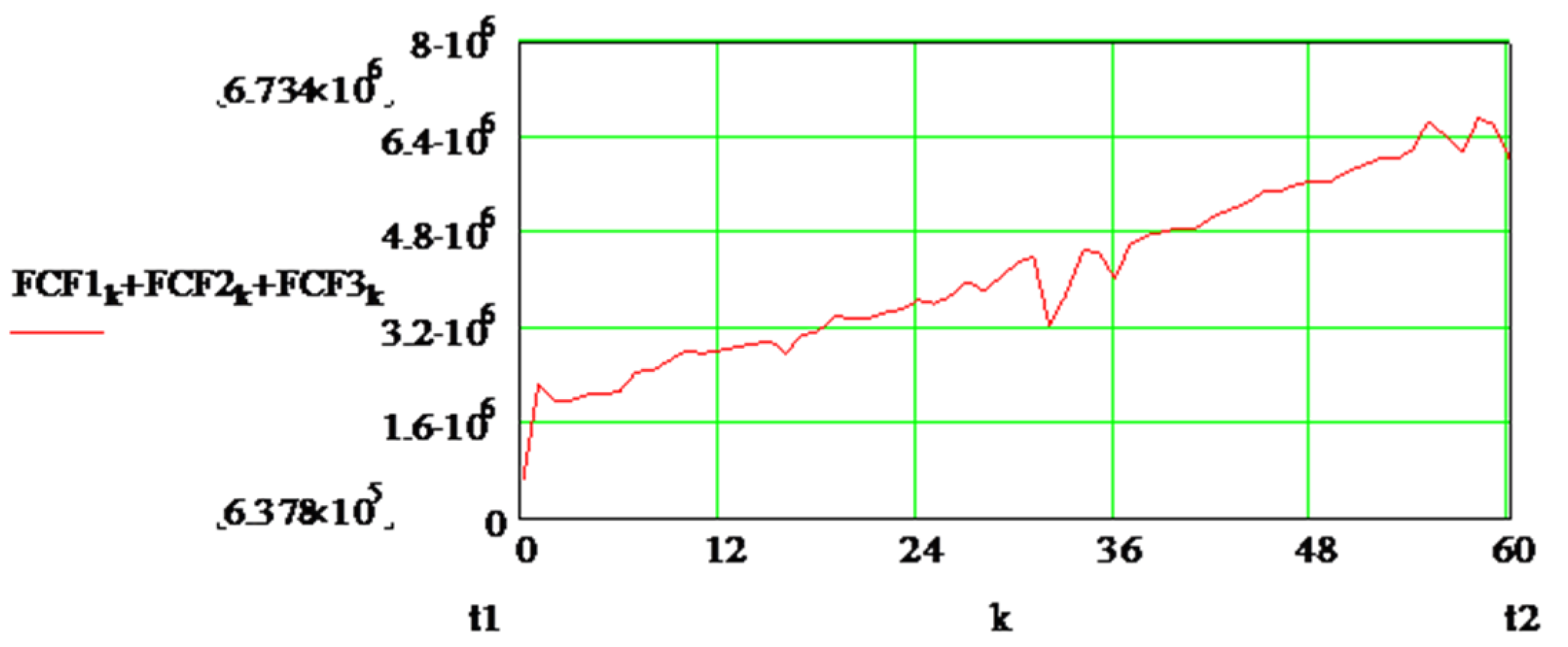

For all the scenarios the sum of non-discounted Free Cash Flows (FCF1 + FCF2 + FCF3) was the same (Figure 2).

In scenario “A”, no random deviations were taken into account, and the NPV was as in Figure 3. In this scenario, RADRs remained stable throughout the whole period, and all the NPV deviations were related to the demand factors and endogenous factors deviations.

Scenario “B”: Figure 4 below shows the behaviour of the random coefficient.

Some details of the above scenarios are presented further. The RADR behaviour for all three companies of the group and the total NPV of their activity are illustrated in Figure 5, Figure 6, Figure 7, Figure 8 and Figure 9.

As a result, qualitative and quantitative risk analysis was carried out in accordance with the general risk management method. The numerical calculations showed that, given a random value with a normal distribution, changes in the mean of the random coefficient had the greatest impact, while changes in the standard deviation were “dampened” throughout the time horizon. The same goes for interest rate seasonal fluctuations—they did not make a substantial impact on the financial result in the time series analysis. Considering the presented data, the risks of a critical character and random factors influencing the mean of discount rates should be monitored in the first place. The social and economic shifts as the result of pandemic, as well as the recent political events in Europe will definitely be encountered as such critical risk factors.

In conclusion, the risk management strategy and risk mitigation methods should contain further diversification of activity—in the given case, it may be implemented through additional product and country diversification, possible insurance, and creating reserves. Monitoring risks and developing feedback on the risk management methods’ efficiency should become a part of regular procedures, and modelling all possible scenarios’ outcomes is an integral part of this process.

4. Discussion

Modelling economic systems’ dynamics creates unique conditions for studying their activity. An adequate economic model allows the investigation of distinct influences of different factors in logical and quantitative correlations and reciprocal effects of several factors in various combinations. Depending on the initial task of the research, a focus can be made on the particular system’s parameters or indicators. With the existing software applications, a possibility arises for experiments with specific techniques without any financial or social risks, as well as for obtaining information while avoiding lengthy statistics processing and dependence on the data availability concerning some external social or climate conditions.

Forecasting an economic unit evolution based on simplifying assumptions within the framework of specific social-economic environments is necessary for elaborating appropriate financial and managerial strategies and developing economic guidelines that will change its future economic behaviour. Sophisticated risk management tools sometimes fail to predict critical environmental changes and protect investors from potential risks. Existing risk models may put too much emphasis on the historic data and not always give adequate risk warnings. We aimed to make economic analysis more forward-looking by comprising the mechanism of considering random values in the system. However, we do not intend to exclude human judgment from risk management and decision making. The managers should review critical underlying assumptions and potential conclusions on a systemic basis.

In addition to the factors modelled in our works before, we suggest considering the value of money in time and risk influence on the group’s activity—and building a mechanism that adjusts cash flows for the impact of the abovementioned factors, except for inflation, through the procedure of discounting cash flows generated during the group’s activity.

Possible further applications of the presented modelling approach include investigating the impact of other external factors on the activity of companies, including environmental and political effects. Uncertainty remains high for the environment due to the pandemic, and supply chain uncertainty creates additional risks for the companies. In addition, political risks remain in focus. Political change and instability do not always impact overseas investors and change might be sudden and insignificant, or slow but substantial. However, foreign investors are then concerned about the impact that any environmental shock, whether the consequence of a violent change in political regime or a slow process of social and political evolution, may have on the value of its activities in certain countries.

Thus, many companies are looking for opportunities to mitigate potential risks by considering them in a timely manner. Therefore, forecasting NPV according to the approach described above is a potential risk management instrument.

An exciting area of applying the presented approach in risk management could cover developing regulation policy. Our modelling approach could supplement the methodology of building a risk map by adding to the numerical risk estimation procedures.

Applying random variables with normal distributions has its advantages and limitations. The advantage is using the conventional approach—a tractable model capturing significant properties of such variables, which are easy to understand and analyse. The limitations consider the concern that normal distribution-based estimates of uncertainty ignore the possibility of sudden movements and discontinuities. Studying the influence of random variables with other types of properties—and comparing the results of such studies—can be the subject of further research.

Author Contributions

Conceptualisation, O.H. and Z.P.; methodology, O.H. and Z.P.; software, O.H.; validation, J.K., O.H. and O.T.; investigation, O.T.; writing—original draft preparation, O.H.; writing—review and editing, Z.P.; visualisation, J.K.; supervision, J.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Lewin, P.; Cachanosky, N. Capital, income, and the time-value of money. In Capital and Finance; Routledge: London, UK, 2020; pp. 7–18. [Google Scholar] [CrossRef]

- Shyra, T.; Shtyrov, O.; Korchynskyy, I.; Zerkal, A.; Skoryk, H. Providing the corporate security strategy in the management system of the enterprise. Bus. Theory Pract. 2020, 21, 737–745. [Google Scholar] [CrossRef]

- Hoshovska, O.; Poplavska, Z.; Kryvinska, N.; Horbal, N. Considering Random Factors in Modeling Complex Microeconomic Systems. Mathematics 2020, 8, 1206. [Google Scholar] [CrossRef]

- Capital Asset Pricing Model (CAPM). WallStreetMojo. Available online: https://www.wallstreetmojo.com/capital-asset-pricing-model-capm/ (accessed on 31 October 2022).

- Samis, M.R.; Laughton, D.; Poulin, R. Risk Discounting: The Fundamental Difference between the Real Option and Discounted Cash Flow Project Valuation Methods; SSRN Scholarly Paper ID 413940; Social Science Research Network: Rochester, NY, USA, 2003. [Google Scholar] [CrossRef]

- Espinoza, D. The Cost of Risk: An Alternative to Risk Adjusted Discount Rates; 2015; Available online: https://www.researchgate.net/publication/304012087_THE_COST_OF_RISK_AN_ALTERNATIVE_TO_RISK_ADJUSTED_DISCOUNT_RATES (accessed on 10 August 2022). [CrossRef]

- Shimbar, A.; Ebrahimi, S.B. Modified-Decoupled Net Present Value: The Intersection of Valuation and Time scaling of Risk in Energy Sector. Environ. Energy Econ. Res. 2017, 1, 347–362. [Google Scholar] [CrossRef]

- Hanafizadeh, P. Robust Net Present Value Formula. 2018. Available online: https://www.researchgate.net/publication/325106046_Robust_Net_Present_Value_Formula#fullTextFileContent (accessed on 8 November 2022).

- Gerlach, R. Bayesian Forecasting for Financial Risk Management, Pre and Post the Global Financial Crisis. J. Forecast. 2012, 31, 681–687. [Google Scholar]

- Ozturk, E.O.; Sheng, X.S. Measuring global and country-specific uncertainty. J. Int. Money Financ. 2018, 88, 276–295. [Google Scholar] [CrossRef]

- Kliesen, K.L. Uncertainty and the Economy. Reg. Econ. 2013, 21, 1–3. [Google Scholar]

- Ortiz, J.; Rodríguez, C. Country Risk and the Mundell-Fleming Model Applied to the 1999–2000 Argentine Experience. J. Appl. Econ. 2002, 5, 327–348. [Google Scholar] [CrossRef] [Green Version]

- Diebold, F.X.; Doherty, N.A.; Herring, R.J. The Known, the Unknown, and the Unknowable in Financial Risk Management: Measurement and Theory Advancing Practice; Princeton University Press: Princeton, NJ, USA, 2010; ISBN 978-0-691-12883-2. [Google Scholar]

- Bosch-Badia, M.-T.; Montllor-Serrats, J.; Tarrazon-Rodon, M.-A. Risk Analysis through the Half-Normal Distribution. Mathematics 2020, 8, 2080. [Google Scholar] [CrossRef]

- Skoglund, J.; Chen, W. Market Risk with the Normal Distribution. In Financial Risk Management; Wiley: Hoboken, NJ, USA, 2015; pp. 21–74. ISBN 978-1-119-13551-7. [Google Scholar] [CrossRef]

- Lo, A.W. The Statistics of Sharpe Ratios. Financ. Anal. J. 2002, 58, 36–52. [Google Scholar] [CrossRef] [Green Version]

- Bohdalova, M.; Gregus, M. Estimating value-at-risk based on non-normal distributions. CBU Int. Conf. Proc. 2015, 3, 188. [Google Scholar] [CrossRef] [Green Version]

- Poplavska, Z.; Goshovska, O. Modeling of Synergetic Interrelations within the Association of Enterprises. Bus. Non-Profit Organ. Facing Increased Compet. Grow. Cust. Demands 2017, 16, 401–414. [Google Scholar]

- Zahraei, S.M.; Teo, C.-C. Optimizing a supply network with production smoothing, freight expediting and safety stocks: An analysis of tactical trade-offs. Eur. J. Oper. Res. 2017, 262, 75–88. [Google Scholar] [CrossRef]

- Jin, M.; DeHoratius, N.; Schmidt, G. In search of intra-industry bullwhips. Int. J. Prod. Econ. 2017, 191, 51–65. [Google Scholar] [CrossRef]

- Loureiro, A.L.D.; Miguéis, V.L.; da Silva, L.F.M. Exploring the use of deep neural networks for sales forecasting in fashion retail. Decis. Support Syst. 2018, 114, 81–93. [Google Scholar] [CrossRef]

- Zellner, A.; Kmenta, J.; Drèze, J. Specification and Estimation of Cobb-Douglas Production Function Models. Econometrica 1966, 34, 784–795. [Google Scholar] [CrossRef] [Green Version]

- Garzella, S.; Fiorentino, R. Synergy Value and Strategic Management: Inside the Black Box of Mergers and Acquisitions; Contributions to Management Science; Springer International Publishing: Berlin/Heidelberg, Germany, 2017. [Google Scholar] [CrossRef]

- Damodaran, A. Country Risk: Determinants, Measures and Implications—The 2021 Edition; SSRN Scholarly Paper ID 3879109; Social Science Research Network: Rochester, NY, USA, 2021. [Google Scholar] [CrossRef]

- Denmark Corporate Tax Rate—2021 Data—2022 Forecast—1981-2020 Historical—Chart. Available online: https://tradingeconomics.com/denmark/corporate-tax-rate (accessed on 8 November 2022).

- Denmark—Corporate—Taxes on Corporate Income. Available online: https://taxsummaries.pwc.com/denmark/corporate/taxes-on-corporate-income (accessed on 8 November 2022).

- Ukraine—Corporate—Taxes on Corporate Income. Available online: https://taxsummaries.pwc.com/ukraine/corporate/taxes-on-corporate-income (accessed on 8 November 2022).

- Jensen, K.; Poulsen, R.T. Changing Value Chain Strategies of Danish Clothing and Fashion Companies, 1970–2013. Erhv. Årbog 2013, 62, 37–56. [Google Scholar]

- Knill, O. Probability Theory and Stochastic Processes with Applications, 2nd ed.; World Scientific: Singapore, 2021; ISBN 978-981-310-948-3. [Google Scholar] [CrossRef] [Green Version]

- Rudas, T. Handbook of Probability: Theory and Applications; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2008; ISBN 978-1-4129-2714-7. [Google Scholar] [CrossRef]

- Draper, D.; Guo, E. The Practical Scope of the Central Limit Theorem. arXiv 2021, arXiv:2111.12267. Available online: http://arxiv.org/abs/2111.12267 (accessed on 14 December 2022).

- Turney, S. Central Limit Theorem|Formula, Definition & Examples. Scribbr. Available online: https://www.scribbr.com/statistics/central-limit-theorem/ (accessed on 16 December 2022).

- Mukherji, S. The Capital Asset Pricing Model’s Risk-Free Rate; SSRN Scholarly Paper ID 1876117; Social Science Research Network: Rochester, NY, USA, 2011; Available online: https://papers.ssrn.com/abstract=1876117 (accessed on 10 November 2022).

- US 10-Year Government Bond Interest Rate. Available online: https://ycharts.com/indicators/us_10year_government_bond_interest_rate (accessed on 8 November 2022).

- Damodaran, A. Country Risk: Determinants, Measures and Implications—The 2022 Edition 2022. Available online: https://deliverypdf.ssrn.com/delivery.php?ID=452119066123064027025121099113095071116022007047022001077092107023122121121099022000107007021119049029017103091117103096028120122012004035040069065113067009090088013082122009020025019000066106098097089087121076088075095027120108109015121114121097&EXT=pdf&INDEX=TRUE (accessed on 31 October 2022).

- Ziemann, V. Portfolio Theory and CAPM. In Physics and Finance; Springer: Cham, Switzerland, 2021; pp. 15–28. ISBN 978-3-030-63642-5. [Google Scholar] [CrossRef]

- Nunes, J.H. Carla Duff & Phelps Recommended U.S. Equity Risk Premium Decreased from 6.0% to 5.5%. Kroll, LLC. Available online: https://www.kroll.com/en/insights/publications/valuation/valuation-insights-first-quarter-2021/duff-and-phelps-recommended-us-equity-risk (accessed on 9 November 2022).

- Figuring out the Beta of a Private Company Investopedia. Available online: https://www.investopedia.com/articles/personal-finance/050515/how-calculate-beta-private-company.asp (accessed on 8 November 2022).

- Total Beta. Available online: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/totalbeta.html (accessed on 8 February 2022).

- Ukraine Interest Rate—2022 Data—1992-2021 Historical—2023 Forecast—Calendar. Available online: https://tradingeconomics.com/ukraine/interest-rate (accessed on 8 November 2022).

- Interest rates—Long-term interest rates forecast—OECD Data. theOECD. Available online: http://data.oecd.org/interest/long-term-interest-rates-forecast.htm (accessed on 8 November 2022).

- Acemoglu, D.; Robinson, J. Why Nations Fail: The Origins of Power, Prosperity and Poverty; Crown: New York, NY, USA, 2012. [Google Scholar]

- Kruschwitz, L.; Löffler, A.; Mandl, G. Damodaran’s Country Risk Premium: A Serious Critique. Bus. Valuat. Rev. 2012, 31, 75–84. [Google Scholar] [CrossRef]

- Horn, M.P.; Emmel, H.; Schmidt, M.; Gatzer, S. Estimating the Country Risk Premium—Presenting an alternative to Damodaran’s country risk premium data base. Corp. Financ. 2015, 5, 157–166. [Google Scholar]

- Ericsson, J.; Jacobs, K.; Oviedo, R. The Determinants of Credit Default Swap Premia. J. Financ. Quant. Anal. 2004, 44, 109–132. [Google Scholar] [CrossRef] [Green Version]

- Wilson, M.; Shailer, G. The Term Structure of Discount Rates and Capital Budgeting Practice. J. Appl. Manag. Account. Res. 2004, 2, 29–40. [Google Scholar]

- Giaccotto, C.; Lin, X.; Zhao, Y. Term structure of discount rates for firms in the insurance industry. Insur. Math. Econ. 2020, 95, 147–158. [Google Scholar] [CrossRef]

- State of Fashion|McKinsey. Available online: https://www.mckinsey.com/industries/retail/our-insights/state-of-fashion# (accessed on 8 November 2022).

- Kohan, S.E. Apparel and Accessories Suffer A Catastrophic 52% Sales Decline in March. Forbes. Available online: https://www.forbes.com/sites/shelleykohan/2020/04/16/apparel-and-accessories-suffer-a-catastrophic-52-percent-decline-in-march-sales/ (accessed on 8 November 2022).

- James; Jackson, K.; Weiss, A.; Schwarzenberg, B.; Nelso, M.; Sutter, M.; Sutherland, D. Global Economic Effects of COVID-19 Updated November 10, 2021 Congressional Research Service. CRS Report R46270. 2021. Available online: https://sgp.fas.org/crs/row/R46270.pdf (accessed on 8 November 2022).

- Coronavirus Impact on Clothing Industry in Europe. 2020. Available online: https://0-www-statista-com.brum.beds.ac.uk/statistics/1131181/coronavirus-impact-on-clothing-industry-europe/ (accessed on 8 November 2022).

- Gorman, M.F.; Brannon, J.I. Seasonality and the production-smoothing model. Int. J. Prod. Econ. 2000, 65, 173–178. [Google Scholar] [CrossRef]

- Getz, D.; Nilsson, P.A. Responses of family businesses to extreme seasonality in demand: The case of Bornholm, Denmark. Tour. Manag. 2004, 25, 17–30. [Google Scholar] [CrossRef]

Figure 1.

Stages of risk management process. Developed by the authors based on different sources.

Figure 2.

Total Free Cash Flow (FCF1 + FCF2 + FCF3) projection for the period of 60 months.

Figure 3.

Graphical representation of RADR (a) and total NVP (b) dynamics during the 60 months for Scenario A (m = 1, σ = 0, interest rate term structure and fluctuations not considered).

Figure 3.

Graphical representation of RADR (a) and total NVP (b) dynamics during the 60 months for Scenario A (m = 1, σ = 0, interest rate term structure and fluctuations not considered).

Figure 4.

Graphical representation of the random value zt dynamics during the 60 months for Scenario B (m = 1, σ = 0.10, interest rate term structure and fluctuations not considered).

Figure 4.

Graphical representation of the random value zt dynamics during the 60 months for Scenario B (m = 1, σ = 0.10, interest rate term structure and fluctuations not considered).

Figure 5.

Dynamics of RADRs (a), and total NPV (b) dynamics for Scenario B1C (m = 1, σ = 0.10; term structure of the interest rate considered; interest rate seasonal rate fluctuations not considered).

Figure 5.

Dynamics of RADRs (a), and total NPV (b) dynamics for Scenario B1C (m = 1, σ = 0.10; term structure of the interest rate considered; interest rate seasonal rate fluctuations not considered).

Figure 6.

Graphical representation of the RADRs (a), and total NPV (b) dynamics for Scenario B3CD (m = 1, σ = 0.30; term structure of the interest rate considered; interest rate seasonal rate fluctuations considered).

Figure 6.

Graphical representation of the RADRs (a), and total NPV (b) dynamics for Scenario B3CD (m = 1, σ = 0.30; term structure of the interest rate considered; interest rate seasonal rate fluctuations considered).

Figure 7.

Graphical representation of the RADRs (a), and total NPV (b) dynamics for Scenario B5 (m = 1.3, σ = 0.20; term structure of the interest rate not considered; interest rate seasonal rate fluctuations not considered).

Figure 7.

Graphical representation of the RADRs (a), and total NPV (b) dynamics for Scenario B5 (m = 1.3, σ = 0.20; term structure of the interest rate not considered; interest rate seasonal rate fluctuations not considered).

Figure 8.

Graphical representation of the RADRs (a), and total NPV (b) dynamics for Scenario B6 (m = 2, σ = 0.20; term structure of the interest rate not considered; interest rate seasonal rate fluctuations not considered).

Figure 8.

Graphical representation of the RADRs (a), and total NPV (b) dynamics for Scenario B6 (m = 2, σ = 0.20; term structure of the interest rate not considered; interest rate seasonal rate fluctuations not considered).

Figure 9.

Graphical representation of the RADRs (a) and total NPV (b) dynamics for Scenario B8 (m = 3, σ = 0.20; term structure of the interest rate not considered; interest rate seasonal rate fluctuations not considered).

Figure 9.

Graphical representation of the RADRs (a) and total NPV (b) dynamics for Scenario B8 (m = 3, σ = 0.20; term structure of the interest rate not considered; interest rate seasonal rate fluctuations not considered).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Country equity risk premiums (CRPs) considered in the model.

| Country (i) | Default Spread | Equity Risk Premium | Country Risk Premium (rs(i)) |

|---|---|---|---|

| Denmark (3) | 0.00% | 6.01% | 0.00% |

| Poland (2) | 1.02% | 7.19% | 1.18% |

| Ukraine (1) | 12.00% | 19.99% | 13.98% |

Table 2.

The current and projected level of the interest rate in the three considered countries.

| Country (i) | Country Policy Rate (2022 Q3) | Country Policy Rate Forecast (2023 Q4) | Country Risk Premium (rs(i)) | Country Risk Premium Forecast |

|---|---|---|---|---|

| Denmark (3) | −0.10% | −0.30% | 0.00% | 0.00% |

| Poland (2) | 6.50% | 6.25% | 1.18% | 1.13% |

| Ukraine (1) | 25.00% | 15.00% | 13.98% | 8.95% |

Table 3.

Scenarios regarding the RADR behaviour.

| Scenario Type | Scenarios Regarding the Discount Rate Behaviour | Assumptions/Techniques |

|---|---|---|

| A | No changes—neither the growth nor the seasonal fluctuations or random deviations are considered for the level of interest rate | RADR remains unchanged during the whole period of analysis |

| B | Random deviations related to the level of interest rate are considered | RADR includes a value characterised by random behaviour with normal distribution; different levels of mean m and standard deviation σ are considered for the analysis |

| C | Interest rate forecasted value considered during the period of analysis | RADR is deemed to change evenly throughout the study—from the given initial level to the respective projected level |

| D | Seasonal rate fluctuations are considered | RADR is considered to fluctuate seasonally during each year of activity; monthly rate deviations are included in the model |

Table 4.

Key indexes of the investment project (all data presented in EUR).

| Year of Activity | 0 | 1 | 2 | 3 | 4 | 5 | Total |

|---|---|---|---|---|---|---|---|

| The initial investment, Mio EUR | −3095 | −3095 | |||||

| Free Cash Flow, Mio EUR | 0.79 | 1.04 | 1.30 | 1.68 | 2.01 | 6.82 | |

| IRR (NVP = 0) | 28% | −75% | −28% | 1% | 18% | 28% | 28% |

| MIRR | 18% |

Table 5.

Numeric results for different RADR scenarios.

| # | Scenario | Conditions Investigated, Rate Volatility (m-Mean, δ-Standard Deviation) | Interest Rate Term Structure (Growth) Considered | Interest Rate Seasonal Fluctuations Considered | NVP, Mio EUR | NVP/Investment Ratio | DPP, Months |

|---|---|---|---|---|---|---|---|

| 1 | A | m = 1, σ = 0 | no | no | 1.073 | 0.347 | 46 |

| 2 | B | m = 1, σ = 0.10 | no | no | 1.096 | 0.354 | 46 |

| 3 | B1 C | m = 1, σ = 0.10 | yes | no | 1.388 | 0.448 | 45 |

| 4 | B2 C | m = 1, σ = 0.20 | yes | no | 1.450 | 0.469 | 44 |

| 5 | B3 C | m = 1, σ = 0.30 | yes | no | 1.482 | 0.479 | 45 |

| 6 | B3 | m = 1, σ = 0.30 | no | no | 1.165 | 0.376 | 46 |

| 7 | B4 C | m = 1, σ = 0.50 | yes | no | 1.279 | 0.413 | 44 |

| 8 | B4 | m = 1, σ = 0.50 | no | no | 1.439 | 0.465 | 43 |

| 9 | B1 D | m = 1, σ = 0.10 | no | yes | 1.357 | 0.438 | 45 |

| 10 | B2 D | m = 1, σ = 0.20 | no | yes | 1.358 | 0.439 | 45 |

| 11 | B3 D | m = 1, σ = 0.30 | no | yes | 1.452 | 0.469 | 45 |

| 12 | B4 D | m = 1, σ = 0.50 | no | yes | 1.263 | 0.408 | 44 |

| 13 | B1 C D | m = 1, σ = 0.10 | yes | yes | 1.609 | 0.520 | 44 |

| 14 | B2 C D | m = 1, σ = 0.20 | yes | yes | 1.596 | 0.516 | 44 |

| 15 | B3 C D | m = 1, σ = 0.30 | yes | yes | 1.701 | 0.550 | 42 |

| 16 | B4 C D | m = 1, σ = 0.50 | yes | yes | 1.519 | 0.491 | 43 |

| 17 | B5 C D | m = 1.3, σ = 0.20 | yes | yes | 1.251 | 0.404 | 46 |

| 18 | B5 | m = 1.3, σ = 0.20 | no | no | 0.656 | 0.212 | 51 |

| 19 | B6 C D | m = 2.0, σ = 0.20 | yes | yes | 0.593 | 0.192 | 53 |

| 20 | B6 | m = 2.0, σ = 0.20 | no | no | −0.086 | −0.028 | over 60 |

| 21 | B7 C D | m = 2.5, σ = 0.20 | yes | yes | 0.526 | 0.17 | 54 |

| 22 | B7 | m = 2.5, σ = 0.20 | no | no | −0.414 | −0.134 | over 60 |

| 23 | B8 C D | m = 3.0, σ = 0.20 | yes | yes | −0.120 | −0.039 | over 60 |

| 24 | B8 | m = 3.0, σ = 0.20 | no | no | −0.757 | −0.245 | over 60 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hoshovska, O.; Poplavska, Z.; Kajanova, J.; Trevoho, O. Random Risk Factors Influencing Cash Flows: Modifying RADR. Mathematics 2023, 11, 427. https://0-doi-org.brum.beds.ac.uk/10.3390/math11020427

AMA Style

Hoshovska O, Poplavska Z, Kajanova J, Trevoho O. Random Risk Factors Influencing Cash Flows: Modifying RADR. Mathematics. 2023; 11(2):427. https://0-doi-org.brum.beds.ac.uk/10.3390/math11020427

Chicago/Turabian StyleHoshovska, Oksana, Zhanna Poplavska, Jana Kajanova, and Olena Trevoho. 2023. "Random Risk Factors Influencing Cash Flows: Modifying RADR" Mathematics 11, no. 2: 427. https://0-doi-org.brum.beds.ac.uk/10.3390/math11020427

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.