Finding an Efficient Computational Solution for the Bates Partial Integro-Differential Equation Utilizing the RBF-FD Scheme

Abstract

:1. Introductory Notes

2. RBF-FD: The Weights

3. A New Solution Method

4. The Time-Stepping Solver

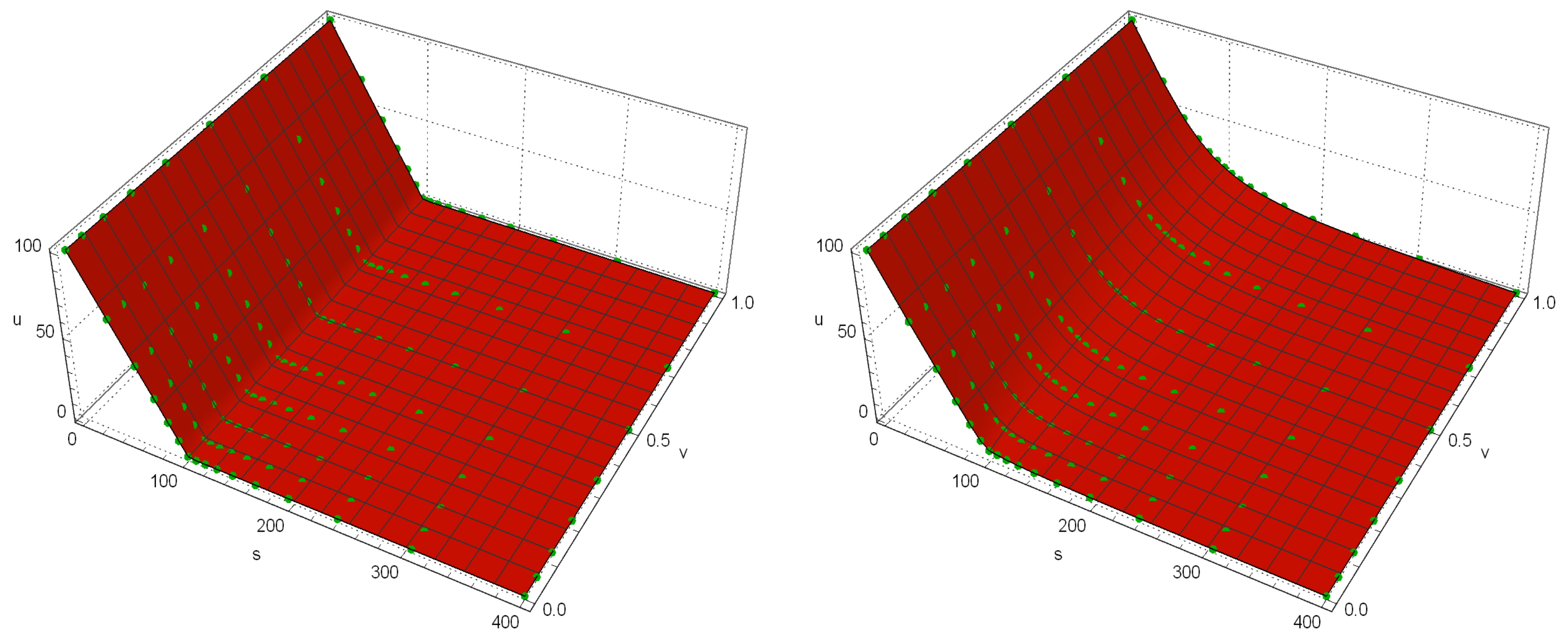

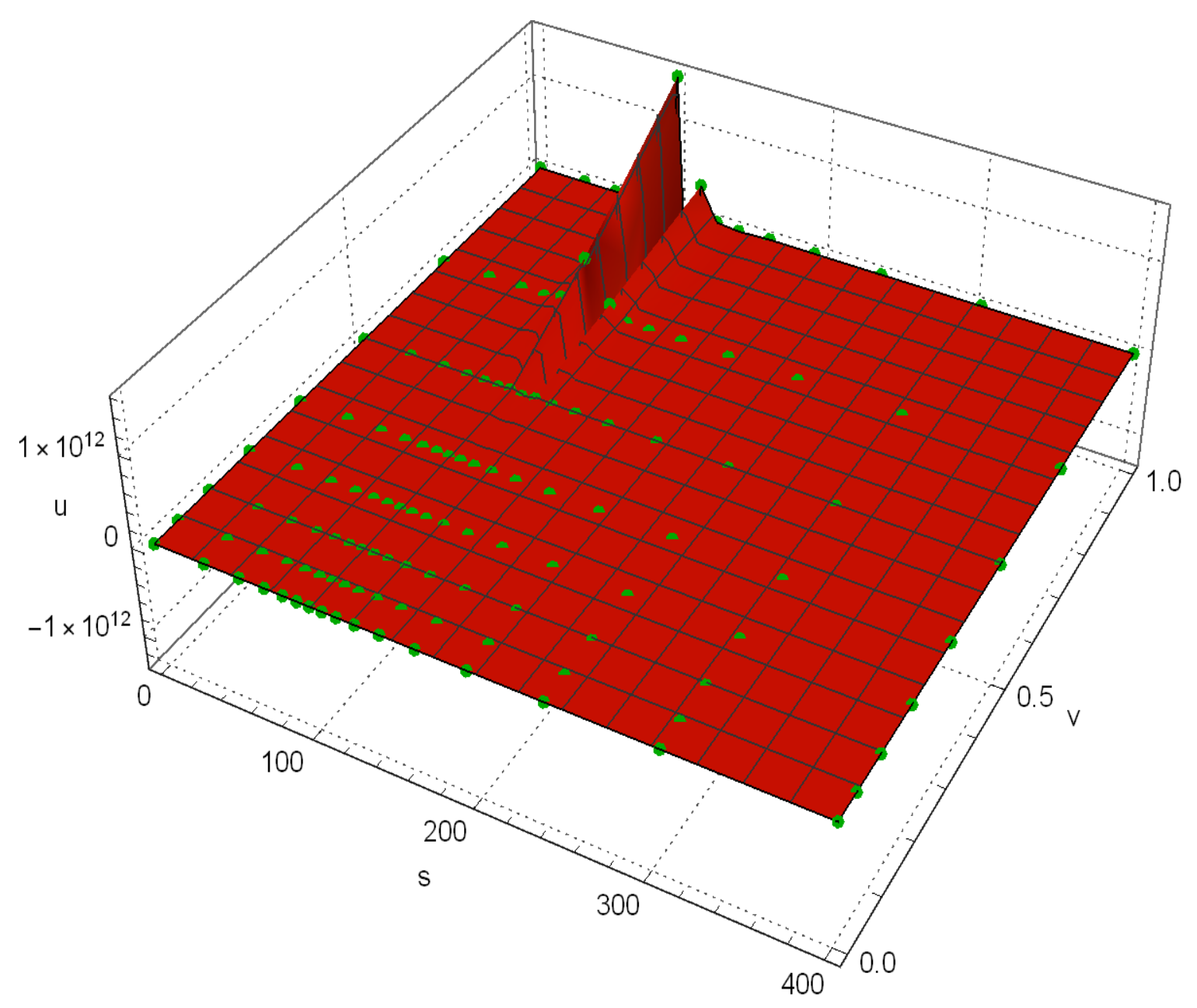

5. Numerical Aspects

- The 2nd-order FD scheme with equidistant stencils for space and the explicit 1st order Euler’s scheme denoted by FDM,

- The method of scalable algebraic multigrid discussed in [34] and shown by AFFT.

- The scheme recently proposed by Soleymani et al. in [21] based on efficient non-uniform procedure denoted by SM.

6. Concluding Remarks

Author Contributions

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Bates, D. Jumps and stochastic volatility: The exchange rate processes implicit in Deutsche mark options. Rev. Fin. Stud. 1996, 9, 69–107. [Google Scholar] [CrossRef]

- Itkin, A. Pricing Derivatives Under Lévy Models: Modern Finite-Difference and Pseudo–Differential Operators Approach, Birkhäuser Basel; Springer: Berlin/Heidelberg, Germany, 2017. [Google Scholar]

- Kim, K.-H.; Sin, M.-G. Efficient hedging in general Black-Scholes model. Finan. Math. Appl. 2014, 3, 1–9. [Google Scholar]

- Ghanadian, A.; Lotfi, T. Approximate solution of nonlinear Black-Scholes equation via a fully discretized fourth-order method. Aims Math. 2020, 5, 879–893. [Google Scholar] [CrossRef]

- Heston, S. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Finan. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef] [Green Version]

- Chang, Y.; Wang, Y.; Zhang, S. Option pricing under double Heston jump-diffusion model with approximative fractional stochastic volatility. Mathematics 2021, 9, 126. [Google Scholar] [CrossRef]

- Gómez-Valle, L.; Martínez-Rodríguez, J. Including jumps in the stochastic valuation of freight derivatives. Mathematics 2021, 9, 154. [Google Scholar] [CrossRef]

- Liu, J.; Yan, J. Convergence rate of the high-order finite difference method for option pricing in a Markov regime-switching jump-diffusion model. Fractal Fract. 2022, 6, 409. [Google Scholar] [CrossRef]

- Chen, K.-S.; Huang, Y.-C. Detecting jump risk and jump-diffusion model for Bitcoin options pricing and hedging. Mathematics 2021, 9, 2567. [Google Scholar] [CrossRef]

- Hellmuth, K.; Klingenberg, C. Computing Black Scholes with uncertain volatility-a machine learning approach. Mathematics 2022, 10, 489. [Google Scholar] [CrossRef]

- Ballestra, L.; Sgarra, C. The evaluation of American options in a stochastic volatility model with jumps: An efficient finite element approach. Comput. Math. Appl. 2010, 60, 1571–1590. [Google Scholar] [CrossRef] [Green Version]

- Ballestra, L.; Cecere, L. A fast numerical method to price American options under the Bates model. Comput. Math. Appl. 2016, 72, 1305–1319. [Google Scholar] [CrossRef]

- Kluge, T. Pricing Derivatives in Stochastic Volatility Models Using the Finite Difference Method. Ph.D. Thesis, TU Chemnitz, Chemnitz, Germany, 2002. [Google Scholar]

- in ’t Hout, K.J.; Foulon, S. ADI finite difference schemes for option pricing in the Heston model with correlation. Int. J. Numer. Anal. Model. 2010, 7, 303–320. [Google Scholar]

- Balajewicz, M.; Toivanen, J. Reduced order models for pricing European and American optionsunder stochastic volatility and jump-diffusion models. J. Comput. Sci. 2017, 20, 198–204. [Google Scholar] [CrossRef]

- Duffy, D. Finite Difference Methods in Financial Engineering: A Partial Differential Equation Approach; Wiley: England, UK, 2006. [Google Scholar]

- Düring, B.; Fournié, M. High-order compact finite difference scheme for option pricing in stochastic volatility models. J. Comput. Appl. Math. 2012, 236, 4462–4473. [Google Scholar] [CrossRef]

- Soleymani, F.; Ullah, M. A multiquadric RBF-FD scheme for simulating the financial HHW equation utilizing exponential integrator. Calcolo 2018, 55, 51. [Google Scholar] [CrossRef]

- Milovanović, S.; von Sydow, L. A high order method for pricing of financial derivatives using radial basis function generated finite differences. Math. Comput. Simul. 2020, 174, 205–217. [Google Scholar] [CrossRef] [Green Version]

- Milovanović, S.; von Sydow, L. Radial basis function generated finite differences for option pricing problems. Comput. Math. Appl. 2018, 75, 1462–1481. [Google Scholar] [CrossRef]

- Soleymani, F.; Barfeie, M. Pricing options under stochastic volatility jump model: Astable adaptive scheme. Appl. Numer. Math. 2019, 145, 69–89. [Google Scholar] [CrossRef]

- Soleymani, F.; Zhu, S. RBF-FD solution for a financial partial-integro differential equation utilizing the generalized multiquadric function. Comput. Math. Appl. 2021, 82, 161–178. [Google Scholar] [CrossRef]

- Soleymani, F.; Itkin, A. Pricing foreign exchange options under stochastic volatility and interest rates using an RBF-FD method. J. Comput. Sci. 2019, 37, 101028. [Google Scholar] [CrossRef] [Green Version]

- Itkin, A.; Soleymani, F. Four-factor model of quanto CDS with jumps-at-default and stochastic recovery. J. Comput. Sci. 2021, 54, 101434. [Google Scholar] [CrossRef]

- Fasshauer, G. Meshfree Approximation Methods with MATLAB; World Scientific Publishing Co.: Singapore, 2007. [Google Scholar]

- Bayona, V.; Moscoso, M.; Carretero, M.; Kindelan, M. RBF-FD formulas and convergence properties. J. Comput. Phys. 2010, 229, 8281–8295. [Google Scholar] [CrossRef]

- Meyer, G. The Time-Discrete Method of Lines for Options and Bonds, A PDE Approach; World Scientific Publishing: Hackensack, NJ, USA, 2015. [Google Scholar]

- Knapp, R. A method of lines framework in Mathematica. J. Numer. Anal. Indust. Appl. Math. 2008, 3, 43–59. [Google Scholar]

- Salmi, S.; Toivanen, J. An iterative method for pricing American options under jump-diffusion models. Appl. Numer. Math. 2011, 61, 821–831. [Google Scholar] [CrossRef] [Green Version]

- Michel, V.; Thomann, D. TVD-MOOD schemes based on implicit-explicit time integration. Appl. Math. Comput. 2022, 433, 127397. [Google Scholar]

- Shymanskyi, V.; Protsyk, Y. Simulation of the heat conduction process in the Claydite-Block construction with taking into account the fractal structure of the material. In Proceedings of the 2018 IEEE 13th International Scientific and Technical Conference on Computer Sciences and Information Technologies (CSIT), Lviv, Ukraine, 11–14 September 2018. [Google Scholar]

- Sayfidinov, O.; Bognár, G.; Kovács, E. Solution of the 1D KPZ equation by explicit methods. Symmetry 2022, 14, 699. [Google Scholar] [CrossRef]

- Butcher, J. Numerical Methods for Ordinary Differential Equations, 2nd ed.; Wiley: England, UK, 2008. [Google Scholar]

- Salmi, S.; Toivanen, J.; von Sydow, L. An IMEX-scheme for pricing options under stochastic volatility models with jumps. SIAM J. Sci. Comput. 2014, 36, 817–834. [Google Scholar] [CrossRef] [Green Version]

- Mangano, S. Mathematica Cookbook; O’Reilly Media: Newton, MA, USA, 2010. [Google Scholar]

- Wellin, P.; Gaylord, R.; Kamin, S. An Introduction to Programming with Mathematica; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Giles, M.; Carter, R. Convergence analysis of Crank-Nicolson and Rannacher time-marching. J. Comput. Financ. 2006, 9, 89–112. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Solver | m | n | N | u | Time | ||

|---|---|---|---|---|---|---|---|

| FDM | |||||||

| 20 | 20 | 400 | 401 | 8.700 | 1.94E-1 | 0.87 | |

| 40 | 25 | 1000 | 2001 | 8.597 | 2.97E-1 | 2.33 | |

| 40 | 40 | 1600 | 2001 | 8.673 | 2.20E-1 | 4.92 | |

| 65 | 45 | 2925 | 4001 | 8.860 | 3.39E-2 | 14.07 | |

| 80 | 50 | 4000 | 10,001 | 8.874 | 2.03E-2 | 31.09 | |

| AFFT | |||||||

| 10 | 10 | 100 | 251 | 8.346 | 5.48E-1 | 0.41 | |

| 15 | 15 | 225 | 251 | 8.698 | 1.96E-1 | 0.54 | |

| 25 | 20 | 500 | 401 | 8.860 | 3.47E-2 | 0.56 | |

| 30 | 30 | 900 | 601 | 8.870 | 2.43E-2 | 1.49 | |

| 50 | 30 | 1500 | 2001 | 8.885 | 9.62E-3 | 4.46 | |

| 80 | 30 | 2400 | 5001 | 8.890 | 4.32E-3 | 11.49 | |

| SM | |||||||

| 10 | 10 | 100 | 251 | 8.388 | 5.06E-1 | 0.55 | |

| 15 | 15 | 225 | 251 | 8.746 | 1.47E-1 | 0.81 | |

| 25 | 20 | 500 | 401 | 8.877 | 1.71E-2 | 1.83 | |

| 30 | 30 | 900 | 601 | 8.888 | 6.09E-3 | 3.64 | |

| 80 | 30 | 2400 | 2501 | 8.894 | 8.19E-4 | 27.19 | |

| RBF-FD-PM | |||||||

| 10 | 10 | 100 | 251 | 8.389 | 5.05E-1 | 0.52 | |

| 15 | 15 | 225 | 251 | 5.753 | 1.41E-1 | 0.80 | |

| 25 | 20 | 500 | 401 | 8.876 | 1.88E-2 | 1.69 | |

| 30 | 30 | 900 | 601 | 8.889 | 5.56E-3 | 3.29 | |

| 80 | 30 | 2400 | 2501 | 8.894 | 6.69E-4 | 25.74 |

| Solver | m | n | N | at | at | at | Time | |

|---|---|---|---|---|---|---|---|---|

| FDM | ||||||||

| 8 | 5 | 40 | 26 | 4.54E0 | 3.10E0 | 3.56E-1 | 0.37 | |

| 16 | 8 | 128 | 51 | 1.23E0 | 1.31E-1 | 1.02E0 | 0.52 | |

| 32 | 16 | 512 | 101 | 1.34E-1 | 2.77E-1 | 2.26E-1 | 1.49 | |

| 32 | 32 | 1024 | 201 | 1.25E-1 | 2.02E-1 | 2.23E-1 | 2.93 | |

| 64 | 32 | 2048 | 501 | 5.35E-3 | 5.85E-2 | 1.87E-2 | 9.47 | |

| SM | ||||||||

| 8 | 5 | 32 | 51 | 2.57E-1 | 7.48E-1 | 7.13E-1 | 0.55 | |

| 16 | 8 | 128 | 101 | 7.31E-2 | 2.51E-1 | 3.89E-2 | 0.81 | |

| 32 | 16 | 512 | 501 | 2.18E-3 | 6.02E-3 | 5.64E-3 | 2.40 | |

| 64 | 32 | 2048 | 1001 | 1.79E-3 | 6.24E-4 | 1.39E-3 | 16.71 | |

| RBF-FD-PM | ||||||||

| 8 | 5 | 32 | 51 | 2.49E-1 | 6.89E-1 | 7.11E-1 | 0.50 | |

| 16 | 8 | 128 | 101 | 6.25E-2 | 2.39E-1 | 3.84E-2 | 0.76 | |

| 32 | 16 | 512 | 501 | 2.07E-3 | 5.44E-3 | 5.04E-3 | 2.11 | |

| 64 | 32 | 2048 | 1001 | 1.08E-3 | 5.81E-4 | 1.04E-3 | 15.34 |

| Solver | m | n | at | at | at |

|---|---|---|---|---|---|

| AFFT | 17 | 9 | 1.08E0 | 1.57E0 | 1.96E-1 |

| 33 | 17 | 2.80E-2 | 5.20E-1 | 1.38E-1 | |

| 65 | 33 | 4.78E-3 | 1.25E-1 | 2.84E-2 | |

| 129 | 65 | 7.38E-3 | 3.09E-2 | 5.25E-3 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Farahmand, G.; Lotfi, T.; Ullah, M.Z.; Shateyi, S. Finding an Efficient Computational Solution for the Bates Partial Integro-Differential Equation Utilizing the RBF-FD Scheme. Mathematics 2023, 11, 1123. https://0-doi-org.brum.beds.ac.uk/10.3390/math11051123

Farahmand G, Lotfi T, Ullah MZ, Shateyi S. Finding an Efficient Computational Solution for the Bates Partial Integro-Differential Equation Utilizing the RBF-FD Scheme. Mathematics. 2023; 11(5):1123. https://0-doi-org.brum.beds.ac.uk/10.3390/math11051123

Chicago/Turabian StyleFarahmand, Gholamreza, Taher Lotfi, Malik Zaka Ullah, and Stanford Shateyi. 2023. "Finding an Efficient Computational Solution for the Bates Partial Integro-Differential Equation Utilizing the RBF-FD Scheme" Mathematics 11, no. 5: 1123. https://0-doi-org.brum.beds.ac.uk/10.3390/math11051123