Rules for Fractional-Dynamic Generalizations: Difficulties of Constructing Fractional Dynamic Models

1

Skobeltsyn Institute of Nuclear Physics, Lomonosov Moscow State University, Moscow 119991, Russia

2

Faculty “Information Technologies and Applied Mathematics”, Moscow Aviation Institute (National Research University), Moscow 125993, Russia

Mathematics 2019, 7(6), 554; https://0-doi-org.brum.beds.ac.uk/10.3390/math7060554

Submission received: 9 May 2019

/

Revised: 4 June 2019

/

Accepted: 4 June 2019

/

Published: 18 June 2019

(This article belongs to the Special Issue Mathematical Economics: Application of Fractional Calculus)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:This article is a review of problems and difficulties arising in the construction of fractional-dynamic analogs of standard models by using fractional calculus. These fractional generalizations allow us to take into account the effects of memory and non-locality, distributed lag, and scaling. We formulate rules (principles) for constructing fractional generalizations of standard models, which were described by differential equations of integer order. Important requirements to building fractional generalization of dynamical models (the rules for “fractional-dynamic generalizers”) are represented as the derivability principle, the multiplicity principle, the solvability and correspondence principles, and the interpretability principle. The characteristic properties of fractional derivatives of non-integer order are the violation of standard rules and properties that are fulfilled for derivatives of integer order. These non-standard mathematical properties allow us to describe non-standard processes and phenomena associated with non-locality and memory. However, these non-standard properties lead to restrictions in the sequential and self-consistent construction of fractional generalizations of standard models. In this article, we give examples of problems arising due to the non-standard properties of fractional derivatives in construction of fractional generalizations of standard dynamic models in economics.

Keywords:

fractional calculus; fractional dynamics; fractional generalization; long memory; non-locality; mathematical economics; economic theoryMSC:

26A33 Fractional derivatives and integrals; 91B02 Fundamental topics (basic mathematics, applicable to economics in general)1. Introduction

In mathematics, in addition to derivatives and integrals of integer order, fractional differentiation and integration of non-integer orders (for example, see the comprehensive encyclopedic-type monograph [1], the unsurpassed monograph on generalized fractional calculus [2], the very important and remarkable books on fractional calculus and fractional differential equations [3,4,5]). These operators have been known for several centuries (for example, see comments to Chapters in [1], the first description of the history of fractional calculus (FC), written 150 years ago [6], brief history of FC [7,8,9], and the first review of history of generalized fractional calculus [10]). The recent history of fractional calculus is described in [11], the chronicles and science metrics of recent development of FC [12,13,14], and some pioneers in applications of FC [15]. The fractional differential equations are a powerful tool to describe processes with long memory and spatial non-locality. Recently, the fractional calculus and fractional differential equations have become actively used to describe various phenomena in natural and social sciences. The most important results in this area are collected in the eight-volume encyclopedic handbook on fractional calculus and its applications [16].

At the present time, in some works, fractional differential equations of dynamic models, which are intended to describe physical and economic processes, are proposed without carefully deducing them from some physical and economic assumptions, interpretations and generalizations of concepts. The fractional differential equations are obtained by simply replacing the integer derivatives with fractional derivatives of non-integer order in the equations of standard model. Moreover, it is usually not discussed how such fractional equations can be obtained and justified. After obtaining the solutions of fractional differential equations, which can be presented in an analytical or approximate form, the physical/economic interpretation and analysis of these solutions is not carried out. This way of obtaining fractional generalizations of standard dynamic models can be called a formal generalization, which is a mathematical exercise, and it cannot be considered as mathematical models of the natural and social processes.

In our opinion, the goals of fractional generalizations of models in natural and social sciences cannot be reduced only to a mathematical consideration of fractional differential equations and its solutions. In case of this reduction, the connection with the physics and economics is lost, and it leads to the fact that the results of such generalizations cannot be used directly in these areas of science. The mathematical analysis of fractional differential equations and its solutions should be a bridge, connecting the initial economic or physical assumptions and concepts on the one side, and economic or physical interpretations, effects and conclusions on the other side. All this leads to the need to formulate rules and principles that are important for the development of applications of fractional calculus in natural and social sciences.

Let us formulate basic rules (the principles of fractional-dynamic generalizer) for constructing fractional generalizations of standard dynamic models, i.e., models that are described by differential equations of integer orders.

- (1)

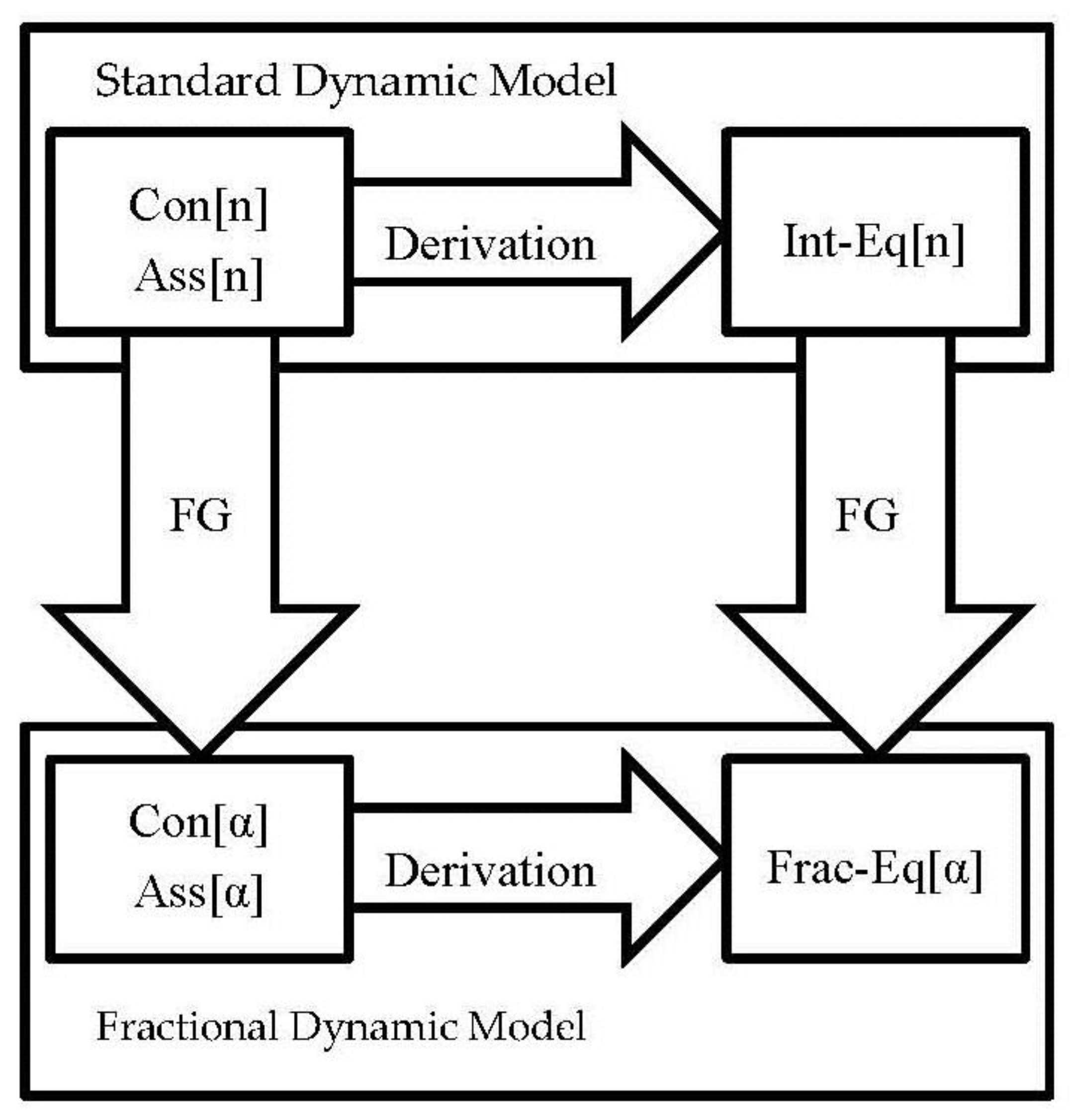

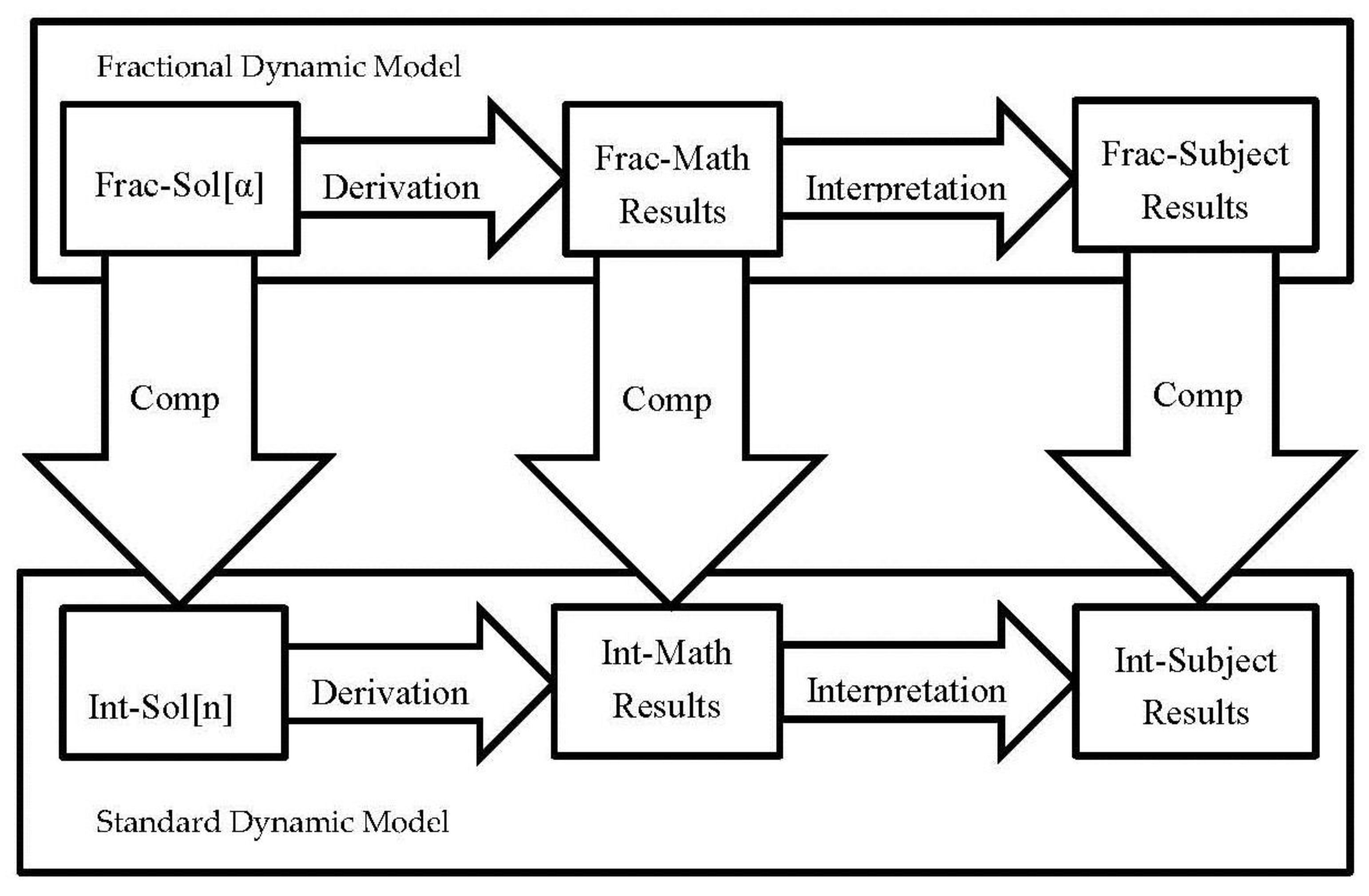

- Derivability Principle:It is not enough to generalize the differential equations describing the dynamic model. It is necessary to generalize the whole scheme of obtaining (all steps of derivation) these equations from the basic principles, concepts and assumptions. In this sequential derivation of the equations we should take into account the non-standard characteristic properties of fractional derivatives and integrals. If necessary, generalizations of the notions, concepts and methods, which are used in this derivation, should also be obtained.The derivability principle states that we should realize a correct fractional generalization of the derivation of the model equations. It is necessary to generalize not only and not so much the differential equation of the model itself, but a generalization of all steps of deriving the standard (non-fractional) equations of the model. In the general case, this will not be an equation that is obtained by simply replacing the integer derivatives with fractional derivatives of non-integer order. Often, the consistent construction of a fractional-dynamic model is associated with the need to introduce new concepts and notions that generalize the concepts and notions of standard models. Note that fractional generalizations of basic concepts are not so much a part of this particular model, but in fact are the common basis of different models, and basis of all fractional dynamics (fractional mathematical economics), and not just the model. An important part of this derivation is the need to take into account the non-standard characteristic properties of fractional derivatives and integrals [17,18,19,20,21,22]. These properties include (a) violation of the standard chain rule (for example, see [3], pp. 97–98, [5], pp. 35–36, [19] and Section 2.1); (b) violation of the standard semi-group property for orders of derivatives (see [1], pp. 46–47, [5], p. 30, and Section 2.2); (c) violation of the standard product (Leibniz) rule (for example, see [1], pp. 280–284, [3], pp. 91–97, [5], pp. 33, 59, [17,20,22] and Section 2.3); (d) violation of the standard semi-group property for dynamic maps (see the explanations and references in Section 2.4). These properties narrow the field for maneuver and make it difficult to obtain fractional generalizations. These non-standard properties are obstacles that must be overcome to build correct fractional dynamic models. At the same time, these non-standard properties allow us to get correct fractional dynamic models to describe non-standard effects, processes and phenomena. Schematically, this principle is represented by Figure 1.

- (2)

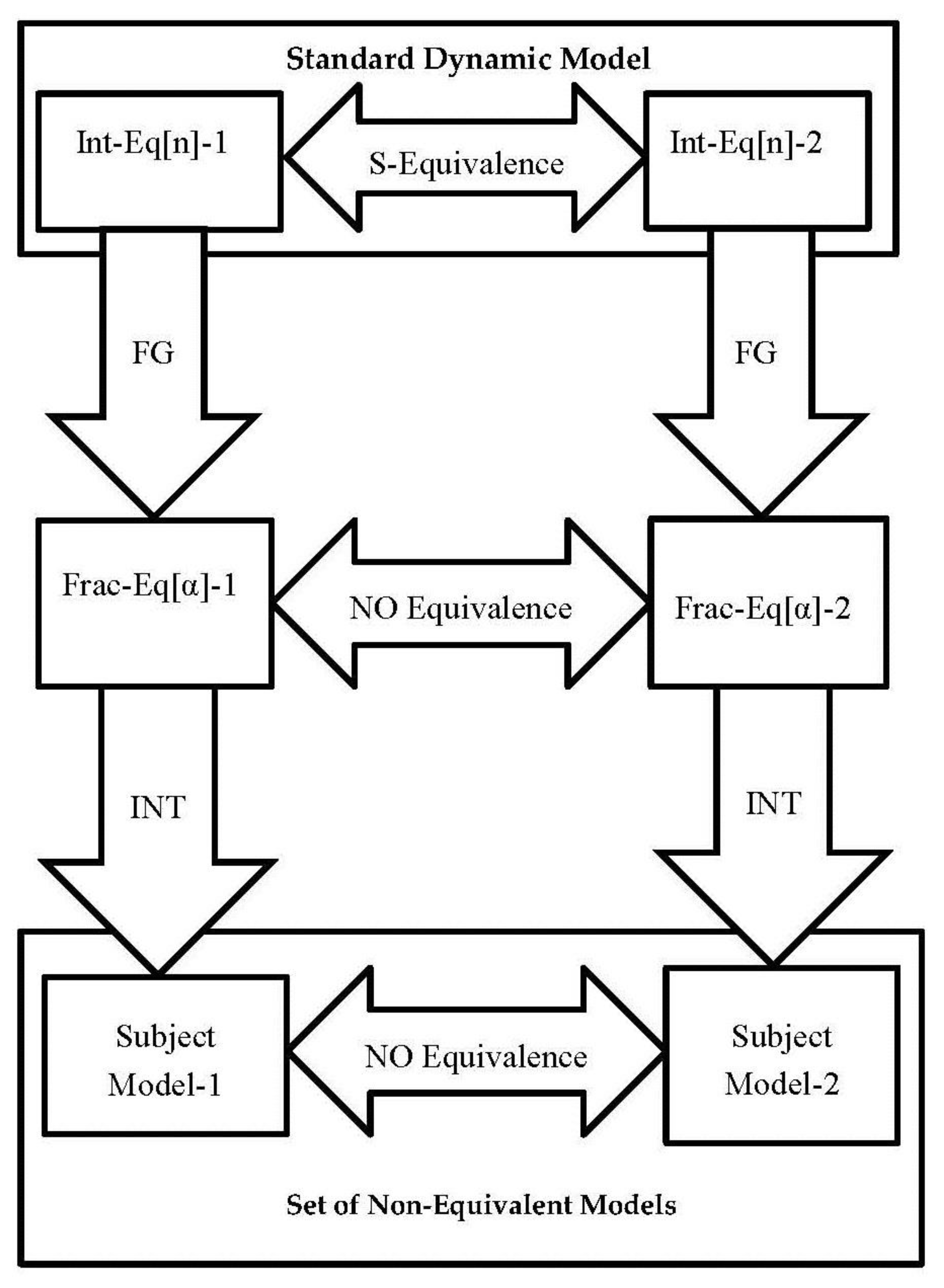

- Multiplicity Principle:For one standard model, there is a set of fractional dynamical generalizations, due to the existence of various types of fractional operators and violation of s-equivalence for fractional differential equations.In addition to existence a large number of different types of fractional derivatives and integrals, the violation of the standard rules generate an additional uncertainty of fractional generalizations. Fractional generalizations of solution-equivalent (s-equivalent) representations of integer-order differential equations of standard models, as a rule, lead to different fractional differential equations that have non-equivalent solutions. This situation is partially analogous to the fact that quantization of equivalent classical models leads to nonequivalent quantum theories. As a result, fractional generalizations of one standard model (which is represented by s-equivalent differential equations of integer order) can lead to different fractional-dynamic models that will predict different behaviors of a process and only some of them may be useful in a given context. We can state that for one standard model, there is a family of fractional dynamical generalizations, due to the existence of various types of fractional operators and violation of s-equivalence for fractional differential equations. In this regard, it is important to investigate and describe the properties of solutions of fractional dynamic equations, which are (qualitatively and/or quantitatively) the same, and the properties of solutions that are (first of all, qualitatively) different. Schematically, this principle is given by Figure 2.

- (3)

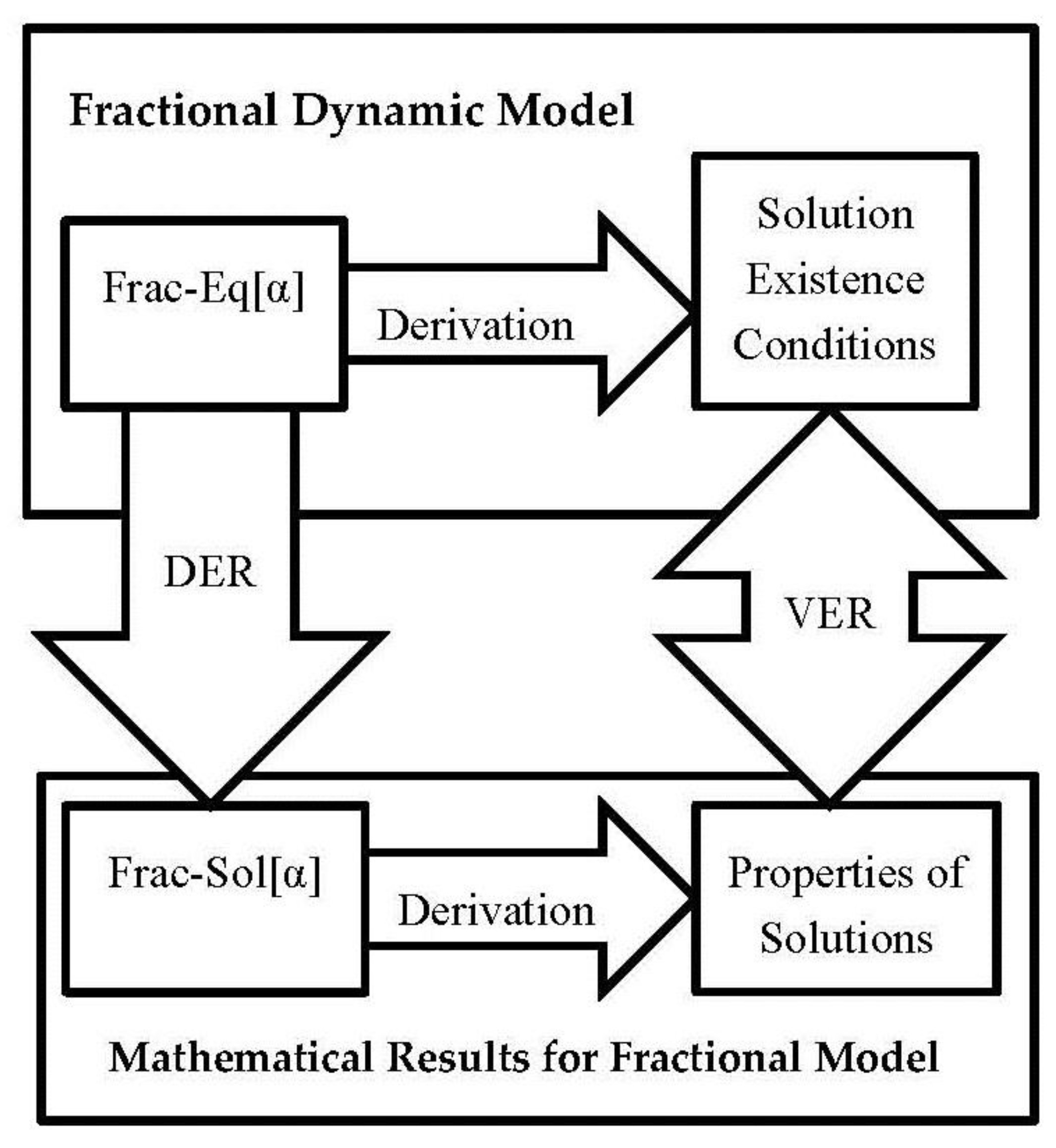

- Solvability Principle:The properties of process types (such as long memory, spatial nonlocality, distributed delay, distributed scaling) and the properties of the corresponding types of fractional operators must be taken into account in the existence of solutions, and in obtaining correct analytical and numerical solutions.The solvability principle states that the existence of solution, and the possibility of obtaining an exact analytical solution or correct numerical solutions for some conditions. Obviously, the existence conditions should allow us to obtain solutions for those cases and properties that the described process has. In addition, we should take into account that different types of fractional derivatives and integrals are known in fractional calculus [1,2,4]. Therefore, in fractional dynamic generalization, it is important that type of fractional operators correspond to the type of natural or social process. It should be noted that not all well-known fractional operators can describe the long memory and spatial non-locality (see Section 2.5 of this paper). For example, some fractional operators can be used to describe the distributed lag (time delay) and the distributed scaling (dilation) and they are not suitable for memory and non-locality. Additionally, we need to verify the existence condition for properties of solutions obtained. For example, if we describe processes with long memory then derivation of numerical solution must take into account not only local information, but the numerical scheme must contain memory terms. Schematically, this principle is represented by Figure 3.

- (4)

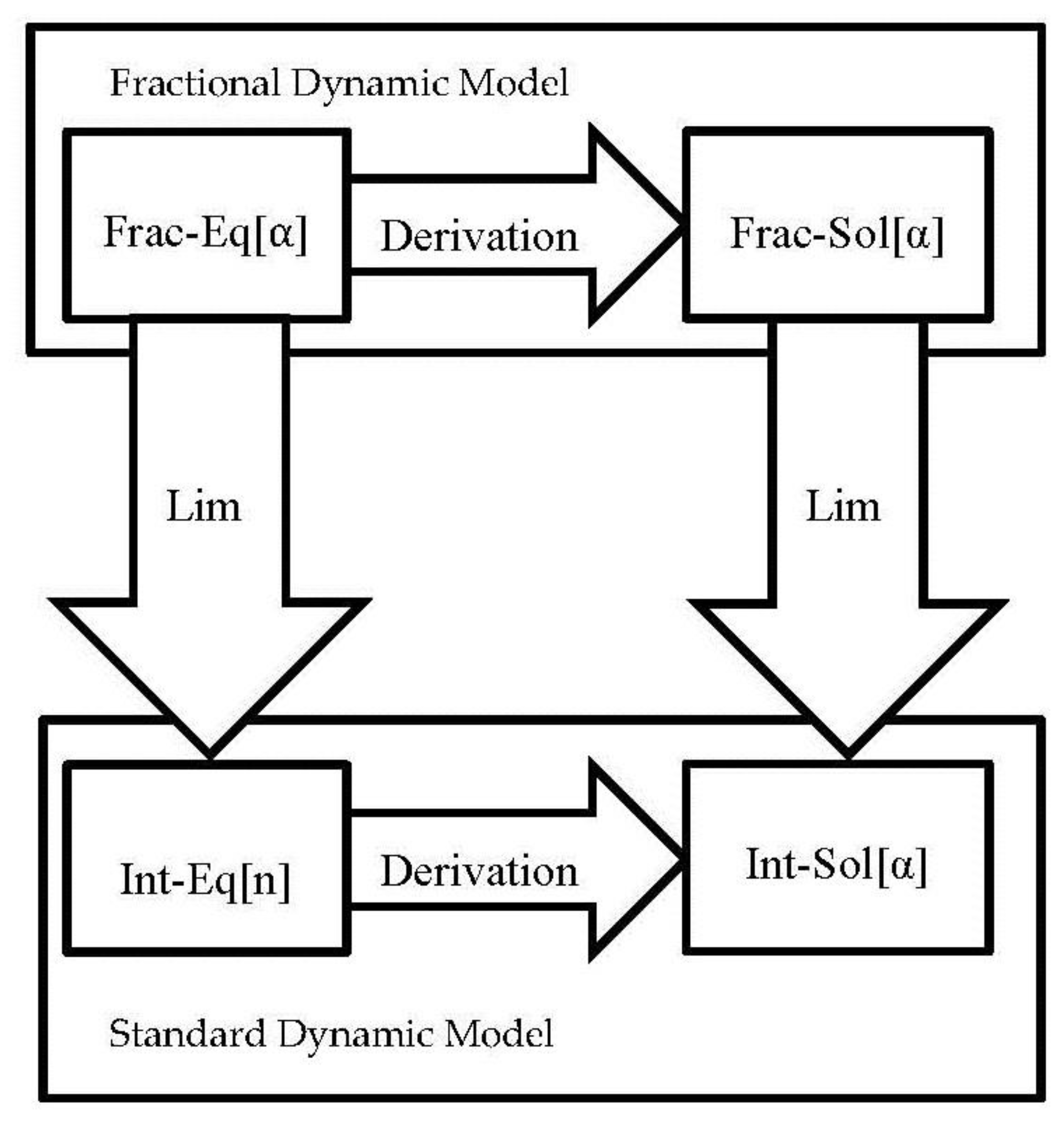

- Correspondence Principle:The limiting procedure, when orders of fractional derivatives tend to integer values, applied to the equations of the fractional dynamic model and their solutions, should give the standard model equations and their solutions.The correspondence principle means a possibility of obtaining equations and solutions of standard model by using a limit procedure, when the orders of the fractional derivatives tend to an integer values. The principle of correspondence must be fulfilled both for the equation itself and for its solution. It should be noted if the order of the derivative tends to the integer value, then the limit on the left and the limit on the right can give different results in the general case. Schematically, this principle is depicted in Figure 4.The Correspondence Principle can also be represented by the formal expression:where It should be noted that the limit on the left and the limit on the right do not coincide in the general case:

- (5)

- Interpretability Principle:The subject (physical, economic) interpretation of the mathematical results, including solutions and its properties, should be obtained. Differences, and first of all qualitative differences, from the results based on the standard model should be described.The subject interpretation of the solutions should be obtained. The properties of solutions should be described in details with their economic or physical meaning (interpretation). It is important to have an interpretability of mathematical results. The differences between results, which were obtained for the proposed generalization and the standard model, should be clearly indicated. An important purpose is to find qualitative differences between the properties of solutions for the fractional dynamic model and the properties of the solutions of the standard model. Schematically, this principle is given by Figure 5.

The proposed five principles are designed primarily to eliminate errors that are usually made when building fractional dynamic generalizations of standard models. The most important element is the requirement that in fractional generalization of economic (or physical) model the “output” of the research should be an economic (physical) conclusions (phenomena, effects) and new economic (physical) effects that are a consequence of subject assumptions on the “input”. Here, mathematics (fractional calculus) is the tool that mathematically strictly connects “economic/physical input” and “economic/physical output”. If mathematical equations and solutions are not rigidly connected with subject “input” and “output”, they will fly away into “airless space”. In this case, the results will turn from economics and physics into formal manipulations, which may not even have mathematical value from the point of view of pure mathematics (fractional calculus).

An important goal of fractional generalizations is to obtain qualitatively new effects and phenomena in natural and social sciences. The results obtained in a science by using the new mathematical apparatus (fractional calculus) should give qualitatively new results and predict new effects and phenomena for this science. First of all, it is precisely such qualitatively new results are interesting in the first place.

In this paper, we illustrate these rules (principles) by using examples of fractional generalizations of standard economic models.

In Section 2 of this paper, we describe the non-standard rules for fractional operators of non-integer orders. The violation of the standard chain rule is described in Section 2.1. The violation of the standard semi-group property for orders of derivatives is discussed in Section 2.2. We consider the violation of the standard product (Leibniz) rule in Section 2.3. The violation of the standard semi-group property for dynamic maps is described in Section 2.4. A correspondence between the types of fractional operators of non-integre orders and the types of phenomena is discussed in Section 2.5.

In Section 3, we consider an application of the Derivability Principle and we give examples of the problem with the violation of the standard rules for fractional operators of non-integer orders. In Section 3.1, to illustrate problems that are connected with the non-standard form of the chain rule, we consider a fractional generalization of the Kaldor-type model of business cycles. In Section 3.2, problem with violation of the standard semi-group rule for orders of derivatives is shown for the fractional generalization of the Phillips model of the multiplier-accelerator. In Section 3.3, to illustrate the problems arising from the non-standard form of the product (Leibniz) rule, we consider the fractional generalization of the standard Solow–Swan model. In Section 3.4, the problem with the violation of the standard semi-group property of dynamic map is described using the examples of fractional generalization of the dynamic Leontief (intersectoral) model and logistic growth model. In Section 3.4, the definitions of new economic concepts and notions are described.

In Section 4, the Solvability Principle and the Correspondence Principle are discussed and some examples are suggested. In Section 4.1, we discuss the Solvability Principle by using the general fractional calculus as an example. In Section 4.2, for illustration we consider the distributed lag fractional calculus and growth-relaxation equations with gamma distributed delay time. In Section 4.3, a simple example of the Correspondence Principle for the case, when the order of the derivative tends toward integer values from the left and from the right, is considered. In Section 4.4, the Solvability Principle is discussed by using example from numerical simulation of fractional differential equations.

In Section 5, we describe some problems (“Non-Equivalence” and “Unpredictability”) of fractional generalizations that are associated with non-equivalent fractional equations, which are formal generalization of equivalent differential equations of integer orders. In Section 5.1, we give definitions of equivalence of equations by solutions (s-equivalence). In Section 5.2, we illustrate non-equivalence of fractional generalization for relaxation and growth differential equations. In Section 5.3, we describe non-equivalence of fractional generalization of the fractional logistic equation that in economics describes growth in a competitive environment with memory. In Section 5.4, we formulate that fractional generalization of standard model can generate non-equivalent models.

In Section 6, we consider example of application of the Interpretability Principle by describing some examples of new effects and phenomena in economics. In Section 6.1, we describe a simple economic model with memory. Fractional differential equation, its solution and asymptotic behavior are proposed. In Section 6.2, we give an interpretation of the mathematical results by using suggested new concept of the warranted rate of growth with memory. In Section 6.3, we describe the interpretation of mathematical results in the form of economic phenomena for economic growth and decline with memory. In Section 6.4, we describe an interpretation of relaxation of economic processes with memory.

In Section 7, we give a short conclusion.

2. Non-Standard Properties of Fractional Derivatives

In this section we describe some properties (rules) of fractional derivatives causing problems when constructing fractional generalizations of standard dynamic models.

The fractional derivatives of non-integer orders have a set of non-standard properties and rules such as the violation of the standard product (Leibniz) and the standard chain rules, the violation of semigroup rules for orders of the derivatives and the violation of semigroup rules for dynamical map. The non-standard properties of fractional derivatives should be taken into account, when constructing fractional generalization of dynamic models. These properties create problems in realization of the derivability principle.

2.1. Violation of Standard Chain Rule

The standard chain rule for the first order derivative has the form:

where is the derivative of first order. The standard chain rule for the derivative of integer order can be written by the equation:

which is called the Faá di Bruno’s formula [23].

The standard chain rules shown in Equations (4) and (5) are not satisfied for fractional derivatives of non-integer orders. Foe example, the chain rule for the Riemann–Liouville fractional derivative of the order (see equation (2.209) in section 2.7.3 of [3], pp. 97–98, [5], pp. 35–36, and [19]) has the form:

where , and are derivatives of integer orders, ∑ extends over all combinations of non-negative integer values of , , …, such that and .

The chain rules for other type of fractional derivatives have a similar form. We see that standard chain rules (4) and (5) do not satisfied for fractional derivatives of non-integer order.

2.2. Violation of Semi-Group Rule for Orders of Derivatives

The standard semi-group rule for orders of integer-order derivatives has the form of the equality:

which holds for , if the function is smooth or is a continuous function that has continuous first derivatives (for example, ). It is well known that this property may be broken for discontinuous functions and if the derivatives are not continuous.

For fractional derivatives, the standard semi-group rule (7) is not satisfied in the general case (for example, see [1], pp. 46–47 and [5], p. 30). For example, the Caputo fractional derivatives of the orders satisfy the equality:

where and are the Caputo fractional derivative of the orders is defined by the equation:

where is the gamma function. Equality (8) means the violation of the semi-group property for orders of derivatives, i.e., in general, we have the inequality:

if the orders of these fractional derivatives are non-integer. In the order of the Caputo fractional derivative in (10) is non-integer and the order , then we have the equality If the order and is non-integer, then the standard semi-group property is violated, i.e., the inequality holds in general.

2.3. Violation of the Standard Product Rule

The standard product (Leibniz) rule for first-order derivative has the form:

The standard product rule for the derivative of integer order has the form:

The Leibniz rule for derivative of non-integer order cannot have the simple form:

A violation of relation in Equation (13) is a characteristic property of all derivatives of integer-orders greater than one and for all types derivatives of the non-integer order (for example, see [1], pp. 280–284, [3], pp. 91–97, [5], p. 33, 59, and [17,20,22]). In [17], the following theorem has been proved:

Theorem 1

(“No violation of the Leibniz rule. No fractional derivative”).If a linear operatorsatisfiesthe product rule in the form of Equation (13), then the operatoris the differential operator of first order, that can be represented in the form, whereis function on.

As a result, we can states that derivatives of non-integer orders cannot satisfy the standard product rule of Equation (13). For example, the fractional generalization of the Leibniz rule for the Riemann–Liouville derivatives has the form (see section 15 in [1], pp. 277–284), of the infinite series:

where and are analytic functions on [a, b] (see theorem 15.1 in [1]), is the Riemann–Liouville derivative; is derivative of integer order . It should be noted that the sum of Equation (14) is infinite and it contains the fractional integrals of non-integer orders for the values .

2.4. Violation of the Standard Semi-Group Rule for Dynamic Maps

Let us consider linear ordinary differential equation equations of first order in the form:

where is an unknown function (with values in a Banach space) and is a constant linear bounded operator acting in the space (or is the linear operator having an everywhere dense domain of definition in the Banach space). We can consider the Cauchy problem of finding a solution of Equation (15) for satisfying the given initial condition . A unique solution of the Cauchy problem exists for the differential equation of first order (Equation (15)) with a constant bounded operator and it can be written (for example, see [24], pp. 119–157) in the form:

where the operator is defined by the series:

which converges in the operator norm. The operator is called the dynamic map or the phase flow [25].

A family of bounded linear operators , depending on the parameter forms a semi-group if the condition and the equality:

hold for all where Equation (18) is the standard semi-group rule for dynamical map. The set is called one-parameter dynamical semi-group. In quantum theory the operator is called the infinitesimal generator of the quantum dynamical semi-group (see classical papers [26,27,28,29]). The class of differential equations for which is a generator for a semigroup of class () coincides with the class of differential equations for which the Cauchy problem is uniformly correct [24].

Daftardar-Gejji and Babakhani [30] (see also [31] and [4], p. 142) have studied the existence, uniqueness, and stability of solutions for the fractional differential equations:

where is the Caputo fractional derivative of the order , . is the column vector and . is real square matrix. They obtained the unique solution of Equation (19) in the form:

where the operator is defined by the series:

Here, is the Mittag–Leffler function with matrix arguments [32].

For , we have . Therefore, we have .

The standard semi-group rule (Equation (18)) for dynamical maps does not hold for non-integer values of , i.e., we have the inequality:

that follows from the property of the Mittag–Leffler function (for example, see [33,34], and some additional information in [35,36,37]) in the form:

As a result, the dynamical maps with cannot form a semigroup.

The operator describes the dynamical map with power-law fading memory for non-integer values of . The violation of the standard semigroup rule for dynamical maps is a characteristic property of dynamics with memory. We can only state that the set of the dynamical map with memory forms a dynamical groupoid [34,37] for on-integer values of .

It should be noted that the fractional differential Equation (19) describes the fractional generalization of N-level open quantum system and the Leontief dynamic model of N-sectors in economy, in which the power-law memory is taken into account (see Section 3.4.1).

2.5. What Effects Are Fractional Derivatives Described?

In fractional calculus, many different types of fractional derivatives and integrals are known [1,2,3,4]. In construction of a fractional generalization of a standard dynamic model, an important part of the work is an adequate choice of the type of the fractional derivative or/and integral. First of all, fractional operators must correspond to the type of process to be described. It is well known that fractional derivatives and integrals are a powerful tool for describing processes with memory and nonlocality. However, not all fractional operators can describe the effects of memory (or non-locality). In application of the generalized and general fractional operators, an important question arises about the correct subject interpretation of these operators (for example, see informational [38], physical [39], and economic [40,41,42] interpretations). It is important to emphasize that not all fractional operators can describe the processes with memory (for example, see [43,44,45,46]). It is important to clearly understand what type of phenomena a given operator can describe. Let us give some examples for illustration.

2.5.1. First Example: Kober and Erdelyi–Kober Operators

The Kober fractional integration of non-integer order [1,2,4] can be interpreted as an expected value of a random variable up to a constant factor (for example, see [43,45] and section 10 in [46]), where the random variable describes scaling (dilation) with the gamma distribution. The Erdelyi–Kober integral operator, the differential operators of Kober and Erdelyi–Kober type have analogous interpretation [43,45,46]. As a result, these operators are integer-order operator with continuously distributed scaling (dilation), and these operators cannot describe the memory. Note that the fractional generalizations of the Kober and Erdelyi–Kober operators, which can be used to describe memory and distributed scaling (dilation) simultaneously, were proposed in [46].

The Kober fractional integral of the order [4], p. 106, is defined as:

where is the order of integration and . Using the variable , this operator can be represent by the equation:

where is the operator [1], pp. 95–96 and [4], p. 11 such that and is the probability density function (pdf) of the beta-distribution such that:

for and if , where is the beta function. We see that the Kober integral operator describes beta distributed scaling up to numerical factor. For details see [43,45] and section 10 in [46].

2.5.2. Second Example: Causality Principle and Kramers–Kronig Relations

To describe processes with memory [47,48,49], the operators should satisfy the causality principle. For natural and social processes with memory, the causality can be described by the Kramers–Kronig relations [50]. The Riesz fractional operators (see section 2.10 of [4]) cannot be used to describe memory since this operator violates the causality principle. The Riesz fractional operators can be used to describe power-law non-locality and power-law spatial dispersion (for example, see [51,52]).

The principle of causality is represented in the form of the Kramers–Kronig relations (the Hilbert transform pair) by using the Fourier transforms. Let us consider the Fourier transform of the memory function . In general, is the complex function where the real part and the imaginary part are real-valued functions. The Kramers–Kronig relations state that the real part and the imaginary parts of the memory function are not independent, and the full function can be reconstructed given just one of its parts. Let us assume that the function is analytic in the closed upper half-plane of frequency and vanishes like or faster as . The Kramers–Kronig relations are given by:

where denotes the Cauchy principal value. For details see [50].

2.5.3. Third Example: Abel-type Operator with Kummer Function in Kernel

The Abel-type fractional integral (and differential) operator with Kummer function (or the three parameter Mittag–Leffler functions) in the kernel (see the classic book [1] and equation (37.1) in [1], p. 731) can be interpreted as the Riemann–Liouville fractional integral (and derivatives) with gamma distribution of delay time [43,53,54].

It is known that the Abel-type (AT) fractional integral operator with Kummer function in the kernel (see equation (37.1) in [1], p. 731) is defined by the equation:

and is the confluent hypergeometric Kummer function. Using equality the memory kernel in Equation (29) can be expressed through the three parameter Mittag–Leffler functions .

The fractional integration with the gamma distributed lag in the form:

where * denotes the Laplace convolution, is the Riemann–Liouville fractional integral [1,4], is the probability density function (weighting functions) of the gamma distribution:

for and for , where is the shape parameter and is the rate parameter. Equation (30) can be written thought the Laplace convolution of memory and weighting functions:

where is the kernel of the Riemann–Liouville fractional integral. The associativity of the Laplace convolution allows us to represent operator in the form:

where is the memory-and-lag function of the form:

where is the confluent hypergeometric Kummer function.

As a result, we obtain the relation:

This equation shows that the AT fractional integral can be expressed through the Riemann–Liouville fractional integral with gamma distributed lag for wide range of parameters.

2.5.4. Fourth Example: Abel-type Operator with Kummer Function in Kernel

In application it is important to have conditions for the operator kernel, which make it possible to assign this operator to one or another type of phenomena or processes. For example, it is obvious that the kernels of general fractional convolution operators satisfying the normalization condition will describe distributed delays in time (lag), and not memory (for example, see [44,46], and some additional comments in [53,54,55]). It is well known in physics that the time delay is related to the finite speed of the process and not to the memory. For example, the Caputo–Fabrizio operators, which were misinterpreted as fractional derivatives of non-integer orders, are integer-order derivatives with the exponentially distributed delay time [43,44]. Therefore, these operators cannot be used to describe processes with memory. Note that the fractional derivatives with exponentially distributed is suggested in [43] and then applied in economics [53,54,55].

2.5.5. Fifth Example: Fractional operators with Uniform Distributed Order

The continual fractional derivatives and integrals were proposed by A.M. Nakhushev [56,57]. The fractional operators, which are inversed to the continual fractional integrals and derivatives, have been proposed by A.V. Pskhu [58,59]. In papers [47,60], we proved that the fractional integrals and derivatives of the uniform distributed order can be expressed (up to a numerical factor) thought the continual fractional integrals and derivatives that were suggested by A.M. Nakhushev. Therefore, the proposed fractional integral and derivatives of uniform distributed order we called in our paper [60] as the Nakhushev fractional integrals and derivatives. The corresponding inverse operators, which contain the two parameter Mittag–Leffler functions in the kernel, were called as the Pskhu fractional integrals and derivatives [60].

For example, the Riemann–Liouville fractional integral of distributed order is defined as:

where , and the weight function ρ(α) satisfies the normalization condition:

In Equation (36) the integration with respect to time and the integration with respect to order can be permuted for a wide class of functions . As a result, Equation (36) is written in the form:

where the kernel is defined by the equation:

where . In the simplest case, we can use the continuous uniform distribution (CUD) that is defined by the expression:

For the probability density function (Equation (40)), the memory function (Equation (39)) has the form:

As a result, the fractional integral of uniform distributed order is defined by the equation:

where . The fractional integrals and derivatives of the uniform distributed order can be expressed thought the continual fractional integrals and derivatives, which have been suggested by A.M. Nakhushev [56,57].

2.5.6. Sixth Example: Left-Sided and Right-Sided Fractional Operators

The right-sided Riemann–Liouville, Liouville, and Caputo fractional derivatives [4] cannot describe the memory processes. Using only the left-sided derivatives of bon-integer orders, we take into account the history of changes of variable in the past, that is for . The right-sided operators are defined by integration over where is the present moment of time. Using right-sided operators actually means that the present state depends on the future states, and not on the past states of the process.

2.5.7. Seventh Example: Fading Memory, Spetial Non-Locality, Time Delay (Lag), Scaling

Fractional calculus approach allows us to describe the spatial non-locality and fading memory of power-law type, the openness of processes and systems, intrinsic dissipation, long-range interactions, and some other type of phenomena. The most well-known phenomena in physics that can be described by fractional differential equations, are the fractional relaxation-oscillation, fractional diffusion-wave, fractional viscoelasticity, spatial and frequency dispersion of power type, nonexponential relaxation, anomalous diffusion, and some others [61,62].

As a result, we can state that the following type of phenomena can be independent of each other:

- scaling (dilation) (for example, see section 9 in [43] and references therein).

As a result, these phenomena are described by certain types of operator kernels. For other types of processes and phenomena, we do not have mathematical conditions on the kernel of operators, which allow us to uniquely identify one or another type of process. In this part of applied mathematics, the fractional calculus requires its development. Mathematically strict conditions on the operator kernels are necessary to initially distinguish between various types of processes and phenomena. It should be emphasized that we must first clearly distinguish between the types of processes and phenomena, but simply list various examples of their specific manifestations in the reality surrounding us, described by the natural and social sciences. It is necessary to establish a clear correspondence between the types of operator kernels and the types of phenomena.

3. Examples of Problems from Non-Standard Properties of Fractional Derivatives

In this section, we present examples illustrating the problems and difficulties of fractional generalization of standard dynamic models, which arise from non-standard properties of fractional derivatives. As an example of the problem with the non-standard form of the chain rule, we consider a fractional generalization of the Kaldor-type model of business cycles. Problem with the violation of the standard semi-group rule for orders of derivatives is shown for the fractional generalization of the Phillips model of the multiplier-accelerator. To illustrate the problems arising from the non-standard form of the product (Leibniz) rule, we consider the fractional generalization of the standard Solow–Swan model. Problem with the violation of the standard semi-group property of dynamic map is described on the examples of fractional generalization of the dynamic Leontief (intersectoral) model and logistic growth model.

3.1. Example of Problems with Chain Rule: Kaldor-Type Model of Business Cycles and Slutsky Equation

In this subsection, we demonstrate that the violation of the standard chain rule gives a restriction in fractional generalization of dynamic models. For this purpose, we consider a fractional generalization of the Kaldor-type model of business cycles and the economic model [66,67,68] based on the van der Pol equation [69,70].

Economic models, which are based on the van der Pol equation, are considered as prototypes of model for complex economic dynamics [69,70]. Nonlinear dynamic models are used to explain irregular and chaotic behavior of complex economic and financial processes (for example, see the business cycle theory [71,72], nonlinear economic dynamics and chaos [73,74], and stabilization [75]). Some models of business cycles, which are based on the Kaldor nonlinear investment-savings functions [69,70,71,72] and the Goodwin nonlinear accelerator-multiplier (for example, see the Goodwin’s paper [76], and [77,78,79]), can be reduced to the van der Pol equation, which describes damped oscillations [69,70,71,72].

3.1.1. Standard Kaldor-Type Model of Business Cycles

In the framework of Keynesian approach to theory of national income, Nicholas Kaldor formulated [66,67,68] the first nonlinear model of endogenous business cycles in 1940. Kaldor consider the interactions between the investment and the savings , where denotes national income. Using the fact that the linear functions and cannot describe processes of business cycle, Kaldor proposed nonlinear form for and , which leads to oscillatory processes of business cycles [69,70].

Let us derive the equation of the Kaldor model of business cycles by using approach proposed by Chang and Smyth [68] (see also [70,71,72]). In the Kaldor model, instead of the standard accelerator equation the dependence of investments on the rate of change of national income is considered in the form:

which takes into account the savings, where denotes the capital stock, is the national income, is the accelerator coefficient and denotes its time derivatives of first order. The parameter is an adjustment coefficient. In this model assumes that and .

Differentiation of Equation (43) with respect to time and using the standard chain rule, we obtain:

In the paper [68] it is assumed that the actual change in the capital stock is determined by savings decisions, such that:

where denotes the time derivatives of first order of the capital stock . Substitution of Equation (45) into Equation (44) gives:

In the paper [68], it is also assumed that the function is linear in and savings is independent of the capital stock, i.e., the function . In this case, the expression is independent of the capital stock and Equation (46) takes the form:

Using the variable , where is the equilibrium value, Equation (47) can be rewritten [70] in the form of the Lienard equation:

which is used in mechanics to describe the dynamics of a spring-mass system.

Assuming symmetric shapes of the investment and savings functions, the parabolic form of the function of their difference, , and the linear form of , we obtain the Van der Pol equation:

This equation is used in economic modeling of the business cycles in the framework of nonlinear economic models with continuous-time. The Van der Pol Equation (49) can be written in the two-dimensional form:

This form of the Van der Pol equation is used in computer simulation on the phase space.

3.1.2. Fractional Generalization of Kaldor-Type Model of Business Cycles

To generalize Equation (49) for the case of processes with memory, we cannot simply replace the derivatives of integer order by fractional derivatives to get the fractional Van der Pol equation:

where . The fractional generalization of the Van der Pol equation are considered in physics (for example, see [80,81,82]) and in economics [83,84].

To correctly generalize the standard model, it is necessary to take into account the process of obtaining Equations (49) and (50) from Equation (43). Note that the replacement of the derivatives of the integer order in Equations (43) and (44) by fractional derivatives also does not allow obtaining the fractional differential Equation (51). This is because, when deriving Equation (49) from Equations (43) and (44), we must use the standard chain rules in the form:

where .

The chain rule for fractional derivative has more complicated form (see equation (2.209) in section 2.7.3 of [3,19]). As a result, we should restrict ourselves to the assumption of the presence of a memory only for Equation (43). Let us assume that the excess of investment over saving, i.e., the difference is determined by changes in the growth rate of the national income in the past:

where the time variable is considered as dimensionless variable. For the case Equation (53) gives Equation (43) of the standard model.

The memory with one-parameter power-law fading is described [47,48,60] by the function:

where is the gamma function and 0 and is the Caputo fractional derivative:

where for and for , and the function has integer-order derivatives , , that are absolutely continuous.

Equation (53) with kernel (54) can be rewritten through the Caputo fractional derivative:

Action of the first-order derivative . with respect to time on Equation (56) and using the standard chain rule, we obtain:

Substituting Equation (45) into Equation (57) gives:

Using the assumptions that are proposed in the paper [68], Equation (58) takes the form:

and:

Note that since the standard semi-group rule for order of derivatives is violated in general.

To obtain two-dimensional form of fractional differential Equation (60), we can use the Riemann–Liouville fractional derivative that is defined by the equation:

Using Equation (61), we can get the equalities:

This allows us to rewrite Equation (60) as:

As a result, the Kaldor-type model of business cycles with power-law memory can be described by the fractional Van der Pol Equation (63). Equation (63) can be written in the two-dimensional form:

3.1.3. Fractional Generalization of Slutsky Equation

The Slutsky Equation (see classical paper [85], and its available copies [86,87,88,89]), which is used in microeconomics [90,91,92], allows us to calculate the unobservable functions (compensated (Hicksian) demand function) from observable functions such as the derivatives of the ordinary (Marshallian) demand function with respect to price and income. The difficulties of the fractional generalization of the standard Slutsky equation is connected with the using the chain rule in the derivation of this equation in microeconomics.

Let us describe the derivation of the standard Slutsky equation. For simplification we will assume that there are only two goods ( and ). In microeconomics, two type demand function are used: the compensated demand function, and the ordinary (uncompensated) demand function, . The compensated (Hicksian) demand function describes the demand of a consumer over a bundle of goods ( and ) that minimizes their expenditure while delivering a fixed level of utility. The compensated demand functions are convenient from a mathematical point of view since these functions do not require income or wealth to be represented. In addition, the function is linear in , which gives a simpler optimization problem. Unfortunately these functions are not directly observable. The uncompensated (Marshallian) demand functions are convenient from an economic point of view. However, this convenience is due to the fact that the uncompensated demand function describes demand given prices and income that are easier to observe directly in economics.

The compensated (Hicksian) demand function is defined by the equation

where is the expenditure function that gives the minimum wealth required to get to a given utility level. Equation (65) is obtained by inserting that expenditure level into the demand function, . Note that the variables enter into the ordinary demand function in (65) in two places.

In 1915, Evgeny E. Slutsky proposed [85,86,87,88,89] an equation that allows us to calculate the compensated (Hicksian) demand function from observable functions, namely, the derivative of the Marshallian demand with respect to price and income.

To derive the Slutsky equation, we apply the partial differentiation of Equation (65) with respect to . This allows us to obtain the equation:

where we use the standard chain rule. Then we should change the notation and taking into account two following economic effects. The first, we take into account the substitution effect that mathematically is represented by the equality:

that indicates movement along a single indifference curve (). The second, we take into account the income effect in the form:

because changes in income or expenditures is the same thing in the function . Then we can use the Shephard’s lemma in the form:

Substitution of Equations (67)–(69) into Equation (66) gives the Slutsky equation:

where we should see that at the utility-maximizing point .

In fractional generalization of the Slutsky equation, the violation of the standard chain rule leads to the equation:

which has a significant complication of the form in compared to the standard equation. In the fractional Slutsky equation ∑ extends over all combinations of non-negative integer values of , , …, such that and .

In addition, the fractional Slutsky equation does not make much sense from an economic point of view, if we consider it as a description of the relationship of compensated (Hicksian) demand function and ordinary (Marshallian) demand function. The standard equation describes the connection these functions in full and this connection is local.

However, the Slutsky fractional equation is important from the other point of view. It is known that the standard Slutsky equation can be represented in terms of elasticity. In this form the Slutsky equation describes a connection of the compensated (Hicksian) price elasticity, the (uncompensated) price elasticity, and the income elasticity of goods. The proposed fractional Slutsky equation describes a connection of the fractional Hicksian elasticity of non-integer order [93,94,95,96] and the Marshallian (uncompensated) price and income elasticities, which are special cases of the fractional elasticity [93,94,95,96] for .

In this regard, we note that the fractional elasticity of a non-integral order can be represented as an infinite sum of elasticities of a higher order, using an equation expressing a fractional derivative in view of the infinite sum of the derivatives of integer orders (see lemma 15.3 in [1], p. 278).

3.2. Example of Problems with Semi-Group Rule for Orders of Derivatives: Phillips Model of Multiplier-Accelerator

Let us consider a fractional generalization of the standard Phillips model of the multiplier-accelerator to demonstrate the fact that the semi-group rule for orders of fractional derivatives gives a restriction in the construction of such generalizations.

The Phillips model of the multiplier-accelerator has been proposed by Alban W.H. Phillips [97,98] (see also [55,78,79,99]) in 1954 as a generalization of the Harrod–Domar macroeconomic growth model with continuous time. The standard Phillips model is described by the ordinary differential equation of second order in the form:

where and is the national income; is the marginal propensity to save; is the investment coefficient; is the speed of response of output to changes in demand; is the speed of response of induced investment to changes in output. The autonomous expenditure is assumed [78,79] to be constant ().

The formal generalization of Equation (72) by replacing the derivatives of integer orders by fractional derivatives has the form:

where and is the Caputo fractional derivative, for example. Such a generalization does not take into account how the standard Phillips equation was obtained. It does not take into account what assumptions are used in the basis and what economic concepts were applied for the derivation of equation of standard model.

Let us briefly describe the process of obtaining the standard equation. The first assumption is form of equation of the investment accelerator [78], p. 72. The value of the actual induced investment at time in response to changes in output is given by:

The second assumption is the equation for the total demand in the form:

where is the planned consumption, and we can use , the marginal propensity to save instead of the marginal propensity to consume . Then we have the equation:

The third assumption is the multiplier equation [78], p. 73, in the form

The equations of the standard model are Equations (74), (76)–(77). A differential equation for income is obtained by eliminating and from the system of Equations (75)–(77). Substitution of Equation (76) into Equation (77) allows us to obtain the expression for the induced investment in the form:

Substituting Equation (78) into Equation (76) under the assumption that the autonomous expenditure is constant, we obtain Equation (72) of the standard Phillips model by the first-order differentiation.

The type of Equations (74), (76), and (77), which are used in the derivation of the standard model Equation (72), gives an impression that it is possible to propose a fractional generalization of the standard model using a formal replacement of the derivatives of first order by fractional derivatives in Equations (74) and (77). This gives the following system of equations:

where the orders of fractional derivatives do not necessarily coincide, and .

The last two equations of system (79) give an expression for the function in the form:

Substituting Equation (80) in the first equation of system (79) under the assumption that the autonomous expenditure is constant, we obtain the equation:

For the case , we have the equation:

where

As a result, we see that in general case the fractional generalization of the Phillips model can be described by Equation (82) instead of Equation (73). We can also see that Equation (82) cannot contain as it used in Equation (73). In addition, the violation of the standard semi-group rule for the orders of derivatives led us to the fact that we have instead of .

It should be emphasized that the generalization given by equation system (79) is formal and does not reflect the economic sense of the original Equations (74) and (77) of the standard model. In Equations (74) and (77), the derivatives of the functions to the left of the equal sign in reality are part of the operator of the exponential distributed lag [78], pp. 72–74.

The standard Phillips model of the multiplier-accelerator takes into account two continuously distributed lags. The first lag characterize the output responding to demand with speed . The second lag describes the induced investment responding to changes in output with speed . These economic accelerator and multiplier can be described by the following operators.

The integer-order derivative with exponentially distributed lag can be defined [46] by the first-order equation:

where . For , we have:

In reality, the first and third assumptions of the standard model, which are described by Equations (74) and (77), should be written [78], pp. 25–27, in the form of the equations:

and:

In standard macroeconomic models, the differential equations of exponentially distributed lag are used in the form of Equations (74) and (77) instead of equations with integro-differential operators in the form of Equations (86) and (87). Equations (74) and (77) are called the differential equations of the exponential lag [78], p. 27. In economics, the use of differential equations of integer orders instead of the integro-differential operators (86) and (87) is caused by the fact that there are considerable difficulties in handling the integrals in Equations (86) and (87). It is seen that equations with continuously distributed lag are equivalent to differential equations of integer orders under certain conditions. These differential equations are easier to handle in comparison with equations that contain integro-differential operators of the distributed lag.

As a result, to obtain a correct generalization of the standard Philips model, we should use the fractional derivative with exponentially distributed lags [46,55] instead of the integer-order operators with exponentially distributed lags. For example, we can use the Caputo fractional derivative with exponentially distributed lag:

where is the rate parameter of exponential distribution and is the Caputo fractional derivative of the order .

Another generalization method is to account for memory effects instead of the distributed lag effect [55]. This generalization assumes to use fractional derivatives (without distributed lag) instead of integer-order operators (86) and (87).

Self-consistent constructions of different fractional generalizations of the standard Phillips model of the multiplier-accelerator were proposed in the work [55].

At the same time, Equation (73), which is a formal fractional generalization of the equation of the standard Phillips model, does not have economic significance due to the violation of the principle of derivability.

3.3. Example of Problems with Product Rule: Solow–Swan Model

In this subsection, we consider a fractional generalization of the standard Solow–Swan model (see, classical papers [100,101,102], and books [103,104]) to demonstrate the fact that the violation of the standard product (Leibniz) rule for fractional derivatives [17,20,22], which is main characteristic property of these operators, gives a restriction in the construction of such generalizations.

The standard Solow–Swan model with continuous time is represented in the form of the single nonlinear ordinary differential equation:

which describes how an increase of capital stock leads to an increase of per capita production, when the supply of labor changes as at a constant rate . Here is the per capita capital; is capital expenditure; is the capital retirement ratio; is the rate of accumulation. The function describes the labor productivity, which is usually considered in the form with .

The formal generalization, which is realized by replacing the first-order derivative by the fractional derivative in Equation (89), has the form:

where is the Caputo fractional derivative, for example.

Unfortunately, the consistent construction of the fractional generalization of the standard model Equation (89) cannot give a fractional differential equation in the form of Equation (90). In order to prove this statement, we first briefly describe the consistent construction of the equation for the standard Solow model.

3.3.1. Standard Solow Model with Continuous Time

The Solow model, which is also called the Solow–Swan model, is a dynamic single-sector model of economic growth (see, Solow and Swan articles [100,101,102], and books [103,104]). In this model, the economy is considered without structural subdivisions. The economy produces only universal products, which can be consumed both in the non-production and production sectors. As a universal product, one can consider a monetary value of the entire economy. Exports and imports are not taken into account. This model describes the capital accumulation, labor or population growth, and increases in productivity, which is commonly called the technological progress. The Solow model can be used to estimate the separate effects on economic growth of capital, labor and technological change.

The Solow model is a generalization of the Harrod–Domar model, which includes a productivity growth as new effect. This relatively simple growth models was independently proposed by Robert M. Solow and Trevor W. Swan in 1956 [100,101]. In 1987 Solow was awarded the Nobel Memorial Prize in Economic Sciences for his contributions to the theory of economic growth [105]. Mathematically, the Solow–Swan model is actually represented by one nonlinear ordinary differential equation (Equation (89), which describes the evolution of the per capita stock of capital. Now it is a classical nonlinear economic model that is actively used in economics [106,107,108,109].

In the Solow model, the state of the economy is given by the following five endogenous state variables (defined within the model): is the final product (production capacity), is the labor input (available labor resources), describes the capital reserves (capital expenditure, production assets), is the investment (investment rates), and is the amount of non-productive consumption (instant consumption). All variables are functions of time , which is assumed to be continuous. In addition, the Solow model uses exogenous indicators (defined outside the model): is the rate of increase in labor resources; is the capital retirement ratio; is the rate of accumulation (the share of the final product used for investment). These exogenous indicators are considered constant in time. The rate of accumulation is considered as a controlling parameter. It is assumed that the production and labor resources are fully used in the production of the final product. The final product at each moment in time is a function of the capital and labor: . This production function of the national economy is often specified to be a function of the Cobb–Douglas type. It is assumed that is a linearly homogeneous function satisfying the constant scale, i.e.:

The final product is used for non-productive consumption and investment: . The accumulation rate is the fraction of the final product used for investment, i.e., . Therefore, we have the multiplier equation .

If we assume that the increase in labor resources is proportional to the available labor resources, then taking into account the growth rate of employed , we can write the differential equation:

where is the derivative of first order. Equation (92) with the initial condition , has the solution , where is the labor resources at the beginning of observation at t = 0. The equation of labor resources can also be considered in the form of the logistic equation (for example, see [106]).

Capital stock may change for two reasons: investment causes an increase in capital stock; depreciation or disposal of capital causes a decrease in its reserves. If we assume that the retirement of capital occurs with a constant retirement rate of , then the capital dynamics is described by the equation . Finally, taking into account and , we obtain:

To obtain the equation of the standard Solow model, the following relative variables are introduced. The per capita capital (capital endowment) is defined as The labor productivity is:

where we use the property (Equation (91)) of the linear homogeneity of the production function.

The dynamics of the output of the final product depends on the amount of the capital per employed person, the per capita capital .

Substitution of into Equation (93) gives:

Using the standard product (Leibniz) rule:

and the property of the linearly homogeneity (Equation (91)), Equation (95) is rewritten in the form:

Using Equation (92) for the labor resources, we obtain:

Equation (98) is the standard Solow–Swan model.

The behavior of the indicators of the standard Solow–Swan model is determined by the ordinary differential equation (Equation (98)) of the first order and the dynamics of labor resources (Equation (92)). The Cauchy problem, which consists of Equation (97) and an initial condition, has a unique solution.

3.3.2. Fractional Generalization of Solow Model

A fractional generalization of the labor resource Equation (92) and obtaining a solution to this fractional differential equation is not difficult. If we take into account this consistent derivation of Equation (98) of the standard model, we see that we cannot use the standard product (Leibniz) rule for fractional derivative. Therefore, we cannot obtain a fractional generalization of the differential Equation (98) for the per capita capital because of a violation of the standard Leibniz rule for fractional derivatives of non-integer orders.

We emphasize that the violation of the standard product rule is a characteristic property of all derivatives of non-integer order. Note that the implementation of the standard product rule for an operator means that this operator is a differential operator of integer order [17], and such operators cannot describe the effects of memory and nonlocality.

As a result, the fractional generalization of the standard Solow–Swan model, which will take into account the power-law memory effects, should be represented as the system of the fractional differential equation:

The fractional dynamics of the per capita capital will be described as the ratio of solutions of these two fractional differential equations.

For production function of the national economy in the form the Cobb–Douglas function , we have the system (99) in the form:

The fractional differential equation with , which describes the labor resources, has the solution (theorem 5.15 of [4], p. 323) in the form:

where is integer-order derivatives of orders at , and is the two-parameter Mittag–Leffler function [32]. In the case () Equation (101) takes the form:

For , we obtain the standard solution , where .

Using Equation (102) that describes fractional dynamics of the labor resources, we can obtain the nonlinear fractional differential equation for the capital expenditure in the form:

In the case , this equation takes the form:

The question of the existence of solutions of nonlinear fractional differential Equations (103) and (104) and computer modeling of capital expenditure dynamics remains open at the present time.

Note that the nonlinear fractional differential Equations (103) and (104) can be represented as Volterra integral equations by using the results of the papers of Kilbas and Marzan [110,111]. In the space of continuously differentiable function the Cauchy problem for fractional differential equation:

where , is equivalent (see Theorem 3.24 of [4], pp.199–202, to the Volterra integral equation:

if the function with and , the variable , where for integer values of and for non-integer values of .

At the same time, Equation (90), which is a formal fractional generalization of the equation (Equation (89)) of the standard model, does not have economic significance due to the violation of the principle of derivability.

3.4. Example of Problem with Semi-Group Rule of Dynamic Map: Dynamic Leontief Model and Logistic Growth Model

In this subsection, we consider fractional generalizations of the standard dynamic Leontief model and logistic growth model to demonstrate that the violation of the standard semi-group rule of dynamic map for fractional derivatives creates a restriction in the construction of such generalizations.

3.4.1. Dynamic Leontief (Intersectoral) Model

One of the famous multidimensional economic models is the dynamic intersectoral model that was proposed Wassily W. Leontief [112,113] in 1951. The Royal Swedish Academy of Sciences has awarded the 1973 year’s Prize in Economic Science in Memory of Alfred Nobel to W.W. Leontief for “the development of the input-output method and for its application to important economic problems” [114]. The Leontief dynamic model is an economic model of growth of gross national product and national income [115,116].

The fractional generalization of the dynamic Leontief (intersectoral) model was proposed in [117,118] in 2017 and in the works [119,120] for the case of time-dependent direct material costs and the incremental capital intensity of production.

Let us give the first example from the econophysics approach based on [117,118], and [119,120]. The fractional generalization of the equation for the dynamic Leontief (intersectoral) model [92,93] has the form:

where the vector describes the gross product (gross output) in monetary terms, where are production sectors; the matrix describes the direct material costs; the matrix describes the incremental capital intensity of production; the matrix E is the unit diagonal matrix of n-th order; the matrix is defined by the equation

Equation (107) describes dynamics of the sectoral structure of the gross products in the closed dynamic intersectoral model with power-law memory (for details, see [117,118], and [119,120]). The solution of Equation (107) with constant operator has the form:

where the operator is defined through the Mittag–Leffler function with matrix arguments by the equation . Therefore, for the operator , which describes the dynamic map with power-law memory, we have the inequality:

which means the violation of the standard semi-group rule for non-integer values of (for example, ).

For the general case of the time-dependent matrix , the solutions of Equation (110) are given in [119,120]. To obtain these solutions, we proposed new concepts of the memory-ordered exponential and memory-ordered product, which are a generalization to processes with memory of such well-known concepts in quantum physics as time-ordered exponential (T-exponential) and time-ordered product (T-product) [121,122].

3.4.2. Logistic Growth with Memory

The second example is taken from the economic model of logistic growth [104,123]. In economic growth models, the competition effects are taken into account by assuming that price is a function of the value of output. Model of natural growth in a competitive environment is often called a model of logistic growth. The variables of this model are the function that describes the value of output at time t; the price is considered as a function of released product , i.e., . It is often assumed that this function is linear, i.e., , where is the price, which is independent of the output and the parameter is the margin price. In addition, it is assumed that all manufactured products are sold (the assumption of market unsaturation). The equation of this model is the differential equation of the first order in the form:

where is the accelerator coefficient, is the marginal productivity of capital (rate of acceleration), is the norm of net investment ) that describes the share of income, which is spent on the net investment.

If and , we can use the variable and the parameter , which are defined by the equations and Then Equation (110) of the logistic growth model is represented in the form:

The fractional generalization of the logistic growth model with power-law memory [123] gives the fractional differential equation:

where is the Caputo fractional derivative. Equation (112) is the logistics fractional differential equation.

The solution of nonlinear fractional differential equations is a difficult problem. Recently, Bruce J. West has published the paper [124], where he proposed an analytical expression of the solution for the fractional logistic equation with in the form:

where is the Mittag–Leffler function [4], p. 42. As it has been proved by I. Area, J. Losada, J. Nieto in [125], the function (113) is not the solution to (11). The main reason is the violation the semi-group property by the Mittag–Leffler function, i.e., we have (for example, see [33,34], and [35,36,37]) the inequality:

for , and real constant . In [125] it has been proved that Equation (113), which is proposed in [124], is not an exact solution of the fractional logistic Equation (112).

As a result, we see that the violation of the standard semi-group property for the dynamic map us an important property of processes with memory that should be taken into account in dynamic models. Neglect of this non-standard property of the dynamical map can lead to errors.

3.4.3. Principle of Optimality for Processes with Memory

The principle of optimality, which was originally proposed for dynamic programming by Belmann, is very important for describing economic processes. The Bellman principle of optimality states that any tail of an optimal trajectory is optimal too.

In considering optimal growth trajectories of economy, a concept known as the optimality principle is very useful. Let us give the standard principle of optimality that describes processes without memory (for example, see section 11.2 of [92]):

Principle of Optimality.

Any optimal behavior has the property that whatever the initial state and corresponding (initial) solution are, the subsequent solutions must constitute the optimal behavior with regards to the state resulting from the initial solution.

Applied to economic growth theories, the optimality principle leads to the following conclusion. If the trajectory is optimal, starts from point and passes through on the way to the end point , then part of the trajectory from to will be optimal with respect to the initial point .

The implementation of the principle of optimality is based on the semi-group rule of dynamic map. The violation of the standard semi-group rule of dynamic map for dynamics with memory leads to violation of the standard principle of optimality.

Mathematically, the violation of the standard optimality principle is represented by the violation of the semi-group rule of dynamic map.

Economically the reason for the violation of the standard principle of optimality is the cutting off of part of the history of this process (that is, starting from the beginning of this process, but at a different time point). In other words, if you put in place of the general director, whose age is 40 years old, his same age 15 years, the company will develop differently.

As a result, we can formulate the following statement:

Principle of Optimality in Processes with Memory.

For economic processes with memory, any optimal behavior has the property that whatever the initial state and corresponding (initial) solution are, the subsequent solutions cannot constitute the optimal behavior with regards to the state resulting from the initial solution. We can state that if there is no violation of the standard principle of optimality, then there is no memory in the process “No Violation of Optimality Principle. No Memory”.

For economic growth models, the suggested optimality principle in processes with memory leads to the following statement. If the trajectory is optimal, starts from point and passes through on the way to the end point , then part of the trajectory from to cannot be optimal with respect to the initial point in general.

This principle actually means that the implementation of the standard optimality principle for economic processes with memory in the general case is equivalent to the lack or absence of memory in this process.

3.5. Generalizations of Economic Notions and Concepts

Derivability Principle states that it is not enough to get a fractional generalization of the differential equations of economic model. It is necessary to generalize the whole scheme (all steps) of obtaining these equations from the basic principles, concepts and assumptions that is used in economic theory for standard model. In this sequential derivation of the equations, we should take into account the non-standard characteristic properties of fractional derivatives and integrals. Another important requirement of the derivability principle is the need to generalize economic the notions, concepts and methods, which were used in the derivation of standard model.

It should be noted that formal replacements of derivatives of integer order by fractional derivatives in standard differential equations, and then solutions of these fractional differential equations cannot be considered as a correct and self-consistent fractional generalization of the standard dynamic models in different sciences.

A very important part of the fractional generalization of dynamic models is the inclusion of memory and non-locality into the economic theory and into the basic economic concepts and methods. А fractional generalizations of basic economic concepts and notions are not so much a part of this particular economic model, but in fact are the common basis of different models, and basis of fractional mathematical economics, and not just an economic model.

The concept of memory for economics is considered in [47,48,49,50] and [126,127,128,129,130,131]. The fractional dynamic models should be constructed on this conceptual basis. The most important task of studies of such fractional generalizations is also the search for qualitatively new effects and phenomena caused by memory and non-locality in the behavior of processes.

Let us give a list of some standard notions of economic theory, the generalization of which were proposed to describe the processes with memory and non-locality in the last years.

The list of these new notions and concepts primarily include the following:

The use of these notions and concepts makes it possible us to construct fractional generalizations of some economic models. A brief description of the history of the use of fractional calculus in economics is proposed as a separate article [149].

4. Example of Application of the Solvability and Correspondence Principles

The Solvability Principle assumes the existence of solution, and the possibility of obtaining an exact analytical solution or a correct numerical solution for some conditions. Obviously, these conditions for the existence of solutions should allow us to describe the processes considered in natural and social sciences.

The Correspondence Principle assumes that in the limit cases of integer orders the solution (and equation) should exist and the expression of this solution (and equation) should give expression of the standard solution. The principle of correspondence must be performed both for the fractional differential equation itself and for its solution.

4.1. Solvability Principle: Example from General Fractional Calculus

A general concept of fractional calculus was proposed by Anatoly N. Kochubei [150] on the basis of the differential-convolution operator. The general fractional calculus is described in the works [150,151], where author describes the conditions under which the general operator has a right inverse (a kind of a fractional integral) and produce, as a kind of fractional derivative, equations. A solution of the relaxation equations with the Kochubei fractional derivative with respect to the time variable is described. As a special case of the general fractional operators, the fractional derivatives and integrals of distributed order are considered in [150,151].

In the works about the general fractional calculus [150,151] the Cauchy problem (A) is considered for Equation (, where (see [151], p. 112). In Section 6 “Relaxation equations”, Theorem 4 states that this Cauchy problem has a solution , which is continuous on , infinitely differentiable and completely monotone on , if the Kochubei conditions (*) hold. The works [150,151] consider only the case of relaxation, i.e., . The case of growth () is not discussed.

In the economics, different growth models are actively studied. In the simplified form, these growth models can be described by the ordinary differential equation , where The fractional generalization of these models, in which the memory function is taken into account, can be described by the Equation ( with , i.e., “relaxation equations” is replaced by “growth equations”.

It is known that for the Caputo fractional derivative, which is a special case of the Kochubei fractional derivatives, the Cauchy problem (A) has a solution , for all real i.e., for and (see theorem 4.3 in [4], p. 231).

Therefore, the following questions, which are important for describing processes with memory in economics, arise within the framework of general fractional calculus.

- Is there a mathematical reason for using only the condition in general calculus, when the Caputo fractional derivative there is no such restriction?

- Could we tell something under what conditions on the memory function, which is described by the kernel of the general fractional derivative, the solution exists for ?

- Is it possible to specify a wider class of operators than the fractional Caputo derivative for the existence of solutions of growth equations?

- Do the conditions of existence of solutions for the general relaxation equation and the general growth equation coincide?