China’s Rare Earths Supply Forecast in 2025: A Dynamic Computable General Equilibrium Analysis

Abstract

:1. Introduction

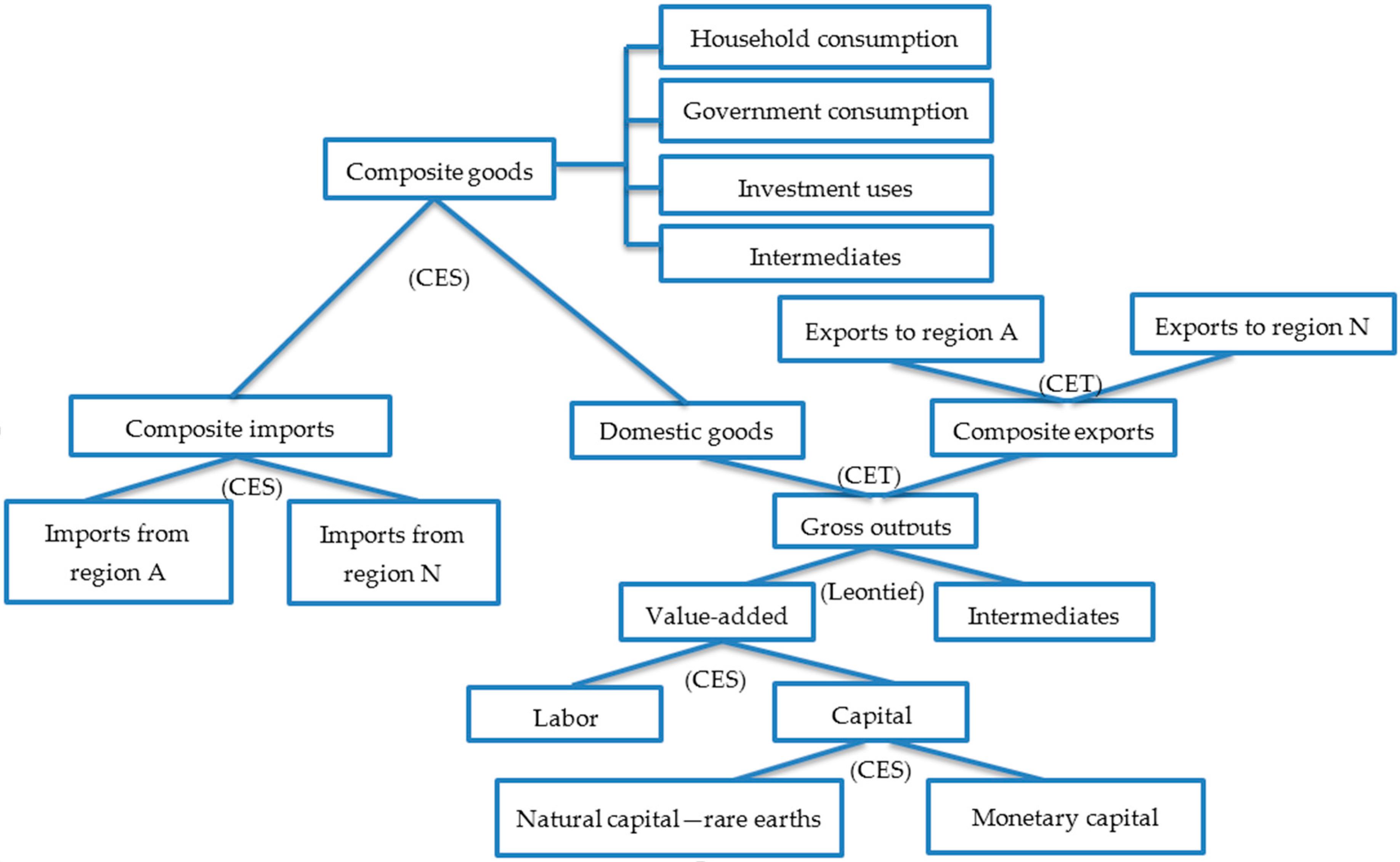

2. China’s DCGE Model for Rare Earths Supply Forecast

2.1. Supply Module

2.2. Demand Module

2.3. Closure, Equilibrium, and Dynamic Module

2.4. Data and Model Calibration

2.5. Forecast Scenarios

- (S0)

- Baseline scenario: under current policies, the growth rates of total investment and labor from 2010 to 2025 are assumed to have had an average growth rate over the past ten years; the substitution elasticity of the CET function for the mining and processing of the rare earths sector is assumed to be the same as other minerals without export controls.

- (S1)

- Easing supply scenario: in addition to S0, the growth rate of total investment in strategic emerging industry (the growth in total investment can improve the production capacities, which has an effect on the production volume. In our DCGE model, total production capacity of China’s economy is determined by the constraint of total capital and labor endowments at a given technology level. For every sector, we adopt a common assumption in DCGE that there has no excess demand or supply of goods and factors in the competitive markets. This means under the constraints of total capital and labor endowments, the production capacity is totally used for production for every sector. Therefore, if capital and labor have an increase from 2010 to 2025, the production capacity will also be enhanced. The CES production function in our model implies that the production volume is determined by the relationship between product price and factor (e.g., capital and labor) price. In our simulation, the growth in the investment is used to increase the capital for sectors and expand production capacity. In addition, the labor increase can also expand production capacity for sectors. Therefore, in our study, the improvement of production capacities is represented by the exogenous growth of investment and labor.) from 2010 to 2025 is assumed to be two times the average growth rate of the past ten years. Under S11, the technologies on substitution and recycling are assumed to be unchanged. Under S12, the technologies are assumed to improve for all the sectors except sectors 12 and 13.

- (S2)

- Tight supply scenario: in addition to S1, because the Chinese government is focusing on the domestic regulation of rare earths by increasing the resources tax or enforcing environmental taxes, the resource and environmental taxes from 2010 to 2025 are assumed to be two times the current weighted average resource tax, which is 12.0%. Under S21, the technologies on substitution and recycling are assumed to be unchanged. Under S22, the technologies are assumed to improve for all the sectors except sectors 12 and 13.

3. Results

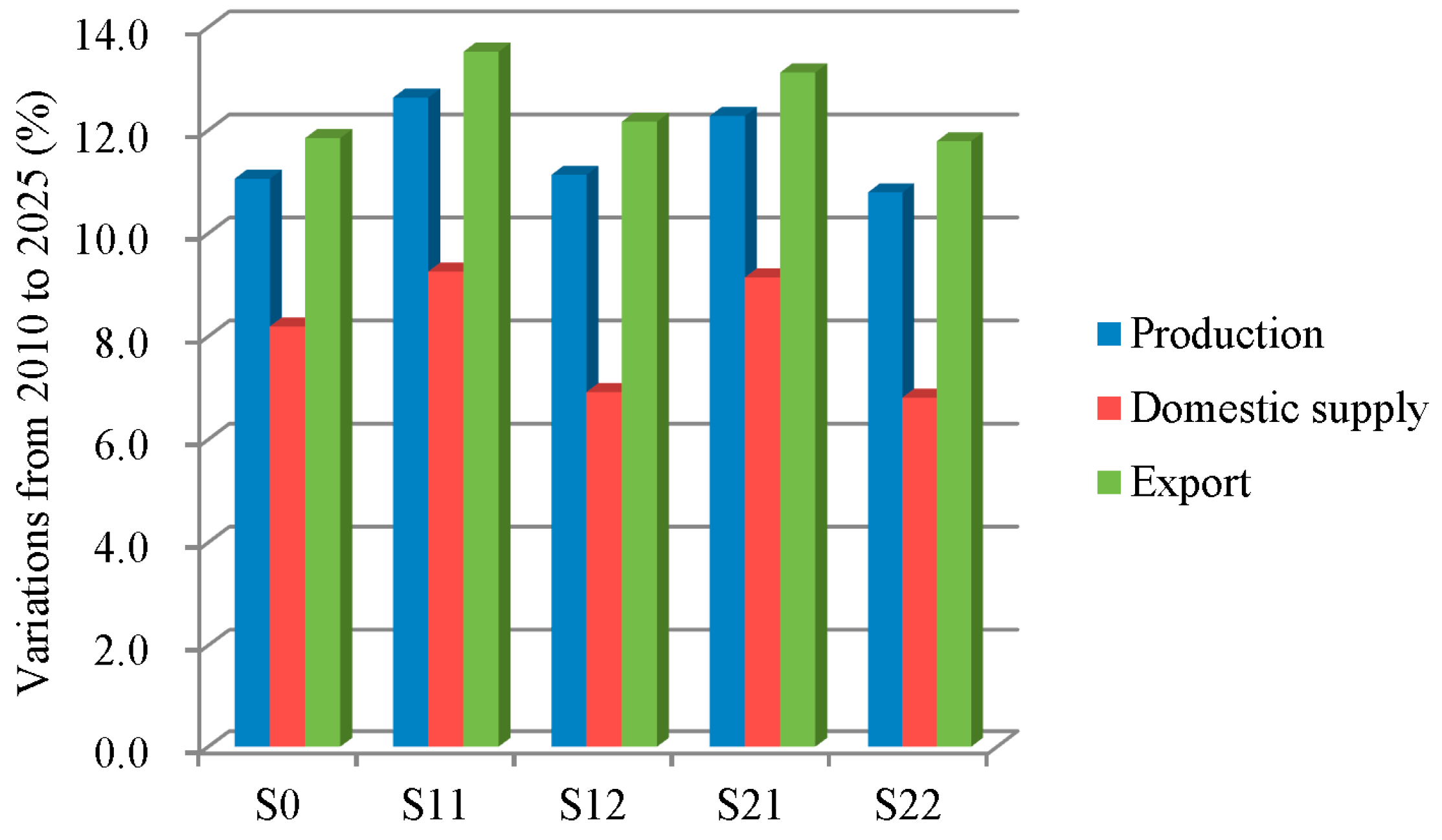

3.1. Total Supply Forecast

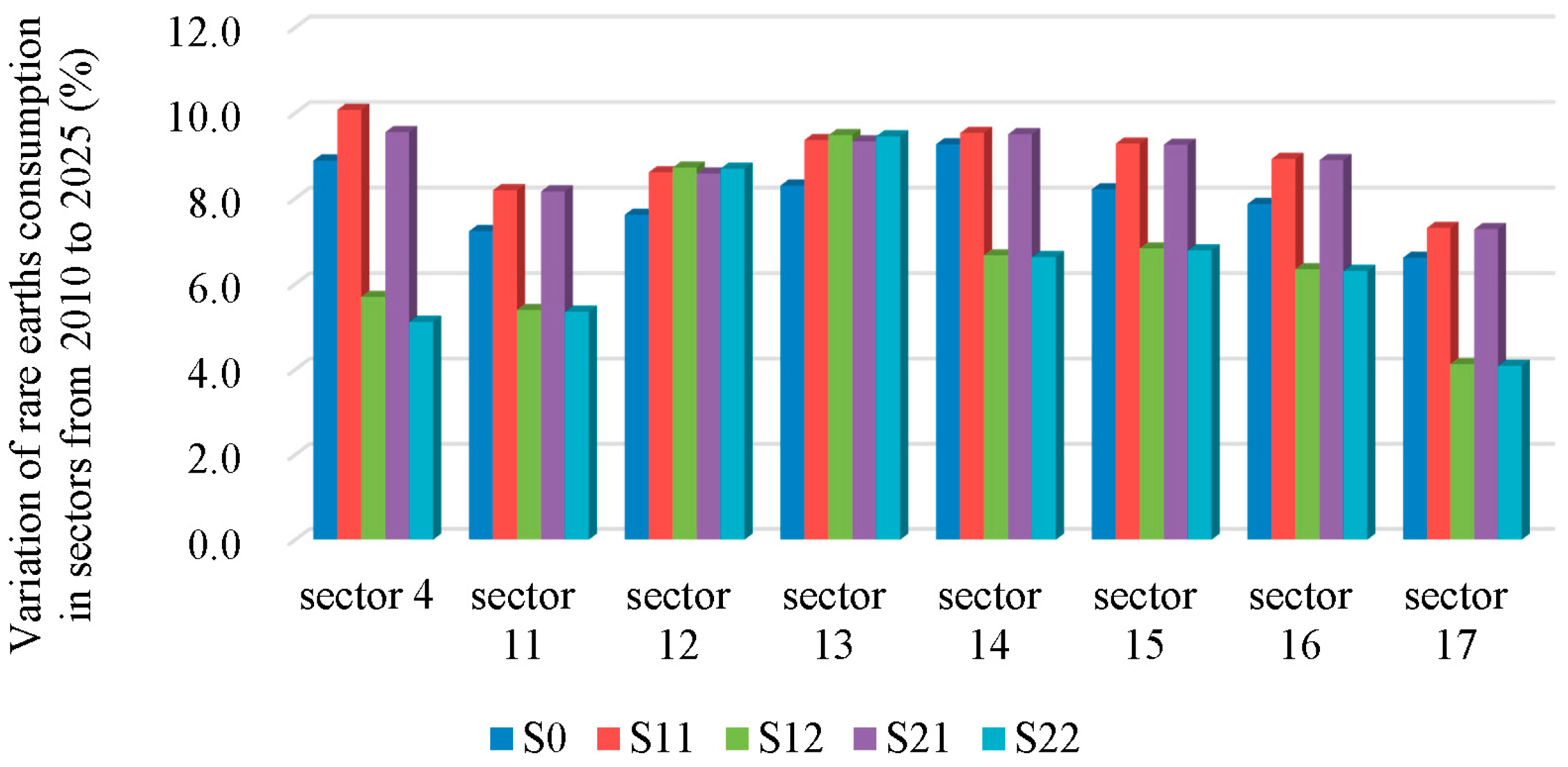

3.2. Sectoral Supply Forecast

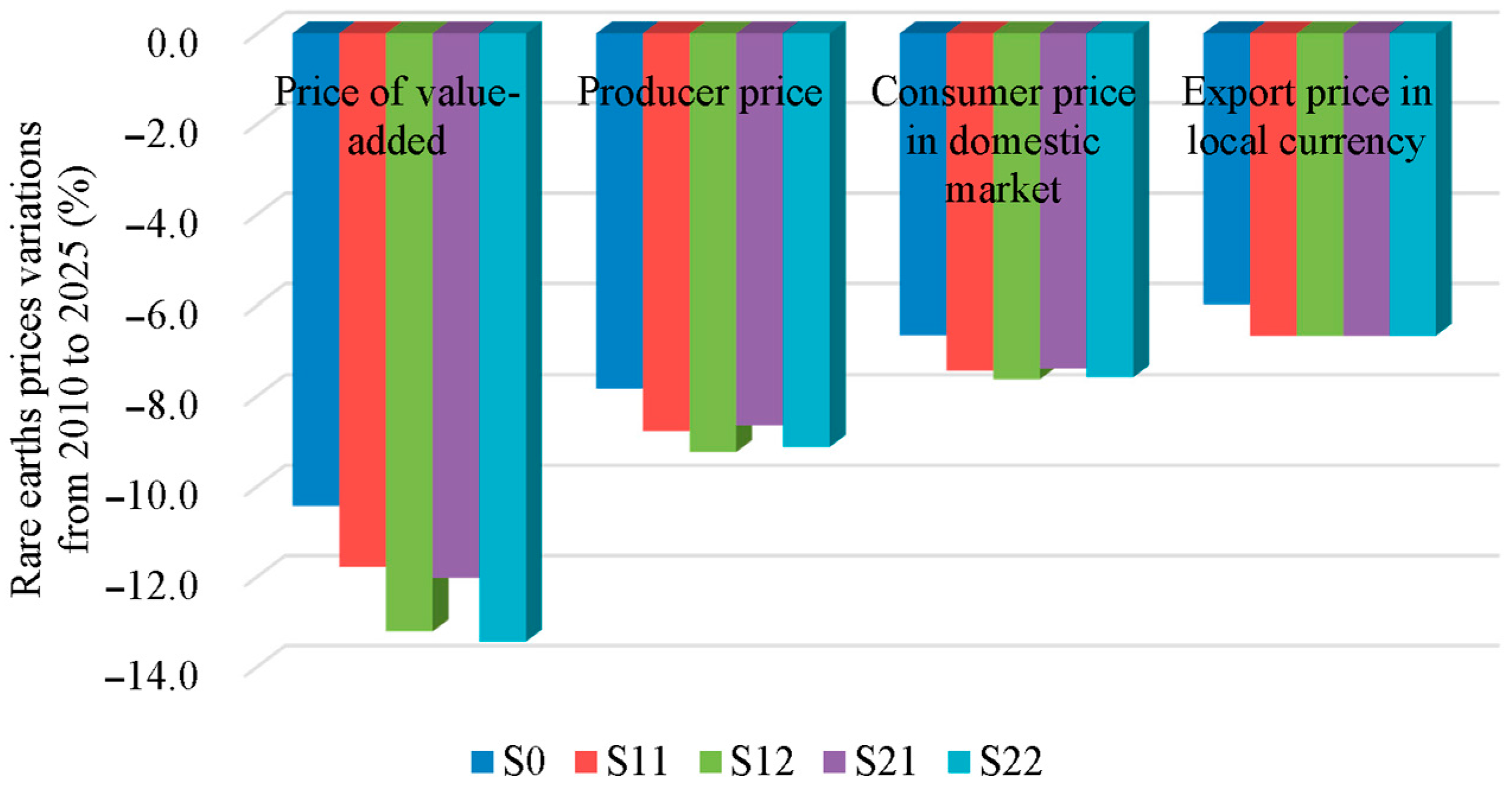

3.3. Price Change Forecast

3.4. Comparisons of the Variations before and after the Abolition of Export Regulations

4. Conclusions and Policy Implications

- (1)

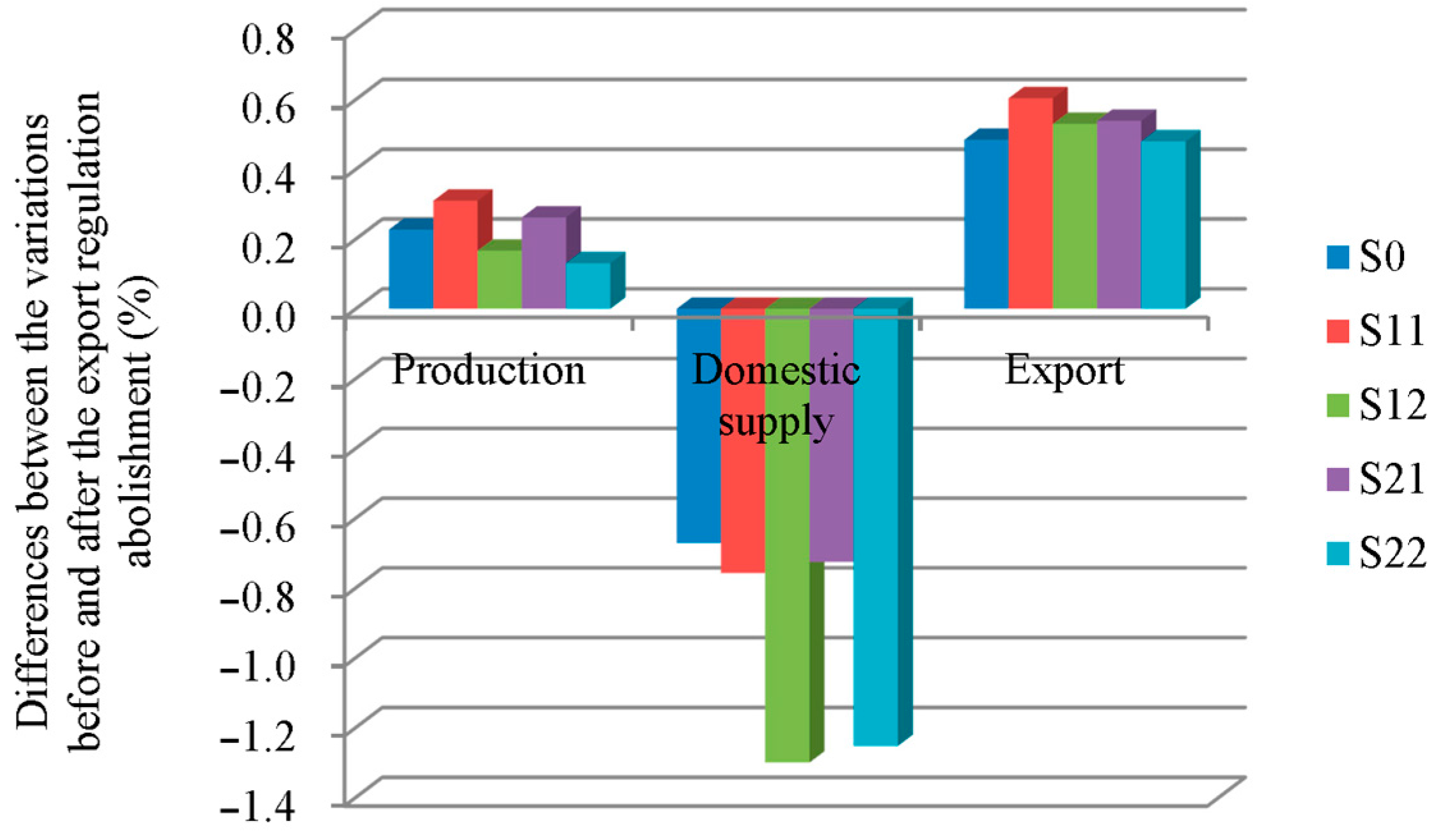

- China’s rare earths supply will resume its growth trend in the future. The production of rare earths in China will reach 116,335–118,260 tons REO in 2025 based on recent extraction control from 2011 to 2015. In 2016, the Ministry of Land and Resources of the People’s Republic of China released its extraction control on rare earths, which was 105,000 tons REO (the same as the 2015 amount). However, production will increase for the following reasons: first, an increase in foreign demand will lead to a decrease in domestic supply, which will prompt the loosening of extraction control and intensify recycling. According to Figure 2, the increase in exports is larger than that in domestic supply; second, domestic demand for rare earths will grow in strategic emerging industries such as clean energy and electric vehicles.

- (2)

- Due to the investment on strategies emerging industries, the mining and processing of rare earths (sector 4), the manufacture of transport equipment (sector 14), the manufacture of general and special purpose machinery (sector 13), and the manufacture of electrical machinery and equipment (sector 15) will be the most important targets of the future supply of rare earths in China. However, because of few alternatives and low recycling efficiency, the domestic supply will focus on the manufacture of non-metallic mineral and metal products (sector 12) and the manufacture of general and special purpose machinery (sector 13).

- (3)

- The number of mining projects of rare earths will decrease in the short and medium term due to technological improvement on substitution and recycling and regulatory policies intervention.

- (4)

- The elimination of export regulations, including export quotas and export taxes, will have a negative impact on China’s future domestic supply of rare earths. Compared to the situation with export regulations, production would increase by 0.1%–0.3% while domestic supply would decrease by 0.7%–1.3%. The same is true in the sectoral supply of rare earths.

- (5)

- Policy conflicts will affect China’s future rare earths supply. In addition to the executive order type of policy instruments such as extraction control, the Chinese government also adopts economic policy instruments, such as resource taxes, to regulate rare earths supply. However, when the government increases investment or gives subsidies to strategic emerging industries, the regulatory effects of these tax policy instruments will be greatly reduced.

Acknowledgments

Author Contributions

Conflicts of Interest

References

- McLellan, B.C.; Corder, G.D.; Ali, S.H. Sustainability of rare earths—An overview of the state of knowledge. Minerals 2013, 3, 304–317. [Google Scholar] [CrossRef]

- Xie, F.; Zhang, T.A.; Dreisinger, D.; Doyle, F. A critical review on solvent extraction of rare earths from aqueous solutions. Miner. Eng. 2014, 56, 10–28. [Google Scholar] [CrossRef]

- Hower, J.C.; Granite, E.J.; Mayfield, D.B.; Lewis, A.S.; Finkelman, R.B. Notes on contributions to the science of rare earth element enrichment in coal and coal combustion byproducts. Minerals 2016, 6, 32. [Google Scholar] [CrossRef]

- Wang, X.B.; Lei, Y.L.; Ge, J.P.; Wu, S.M. Production forecast of China’s rare earths based on the Generalized Weng model and policy recommendations. Resour. Policy 2015, 43, 11–18. [Google Scholar] [CrossRef]

- U.S. Geological Survey (USGS). Mineral Commodity Summaries—Rare Earths. 2016. Available online: http://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/mcs-2016-raree.pdf (accessed on 23 July 2016). [Google Scholar]

- Han, A.P.; Ge, J.P.; Lei, Y.L. An adjustment in regulation policies and its effect on market supply: Game analysis for China’s rare earths. Resour. Policy 2015, 46, 30–42. [Google Scholar] [CrossRef]

- Wübbeke, J. Rare earth elements in China: Policies and narratives of reinventing an industry. Resour. Policy 2013, 38, 384–394. [Google Scholar] [CrossRef]

- Zhang, L.; Guo, Q.; Zhang, J.B.; Huang, Y.; Xiong, T. Did China’s rare earth export policies work?—Empirical evidence from USA and Japan. Resour. Policy 2015, 43, 82–90. [Google Scholar] [CrossRef]

- Dadwal, S.R. The Sino-Japanese rare earths row: Will China’s loss be India’s gain? Strateg. Anal. 2011, 35, 181–185. [Google Scholar] [CrossRef]

- Liu, H.W.; Maughan, J. China’s rare earths export quotas: Out of the China-raw materials gate, but past the WTO’s finish line? J. Int. Econ. Law 2012, 15, 971–1005. [Google Scholar] [CrossRef]

- Ting, M.H.; Seaman, J. Rare earths: Future elements of conflict in Asia? Asian Stud. Rev. 2013, 37, 234–252. [Google Scholar] [CrossRef]

- Qin, J.Y. Judicial authority in WTO law: A commentary on the Appellate Body’s decision in China-rare earths. Chin. J. Int. Law 2014, 13, 639–651. [Google Scholar] [CrossRef]

- Bond, E.W.; Trachtman, J. China-rare earths: Export restrictions and the limits of textual interpretation. World Trade Rev. 2016, 15, 189–209. [Google Scholar] [CrossRef]

- Chen, Z.H. Global rare earth resources and scenarios of future rare earth industry. J. Rare Earths 2011, 29, 1–6. [Google Scholar] [CrossRef]

- Zhang, M.G.; Chen, Y.H. Supply and demand of global rare earth resources and China’s rare earth industry policy. Nonferr. Met. Sci. Eng. 2012, 4, 70–74. [Google Scholar] [CrossRef]

- Hurst, C. China’s Rare Earth Elements Industry: What Can the West Learn? Institute for the Analysis of Global Security: Washington, DC, USA, 2010. [Google Scholar]

- Kingsnorth, D.J. An Overview of the Rare Earths Market; IMCOA: Kingaroy, Australia, 2010. [Google Scholar]

- Waschik, R.; Fraser, I. A computable general equilibrium analysis of export taxes in the Australian wool industry. Econ. Model. 2007, 24, 712–736. [Google Scholar] [CrossRef]

- Ge, J.P.; Lei, Y.L.; Suminori, T. Non-grain fuel ethanol expansion and its effects on food security: A computable general equilibrium analysis for China. Energy 2014, 65, 346–356. [Google Scholar] [CrossRef]

- Devarajan, S. Natural resources and taxation in computable general equilibrium models of developing countries. J. Policy Model. 1988, 10, 505–528. [Google Scholar] [CrossRef]

- Xie, J.; Saltzman, S. Environmental policy analysis: An environmental computable general-equilibrium approach for developing countries. J. Policy Model. 2000, 22, 453–489. [Google Scholar] [CrossRef]

- Böhringer, C.; Conrad, K.; Löschel, A. Carbon taxes and joint implementation. An applied general equilibrium analysis for Germany and India. Environ. Resour. Econ. 2003, 24, 49–76. [Google Scholar] [CrossRef]

- Rose, A.; Liao, S.Y. Modeling regional economic resilience to disasters: A computable general equilibrium analysis of water service disruptions. J. Reg. Sci. 2005, 45, 75–112. [Google Scholar] [CrossRef]

- Zhang, Z.K.; Guo, J.E.; Qian, D.; Xue, Y.; Cai, L.P. Effects and mechanism of influence of China’s resource tax reform: A regional perspective. Energy Econ. 2013, 36, 676–685. [Google Scholar] [CrossRef]

- Silviu, D.A. Simulating the economic impact of resources depletion using a computable general equilibrium model for Romania. Procrdia Econ. Financ. 2015, 22, 618–626. [Google Scholar] [CrossRef]

- Tang, L.; Shi, J.R.; Yu, L.; Bao, Q. Economic and environmental influences of coal resource tax in China: A dynamic computable general equilibrium approach. Resour. Conserv. Recycl. 2015. [Google Scholar] [CrossRef]

- Xu, X.L.; Xu, X.F.; Chen, Q.; Che, Y. The impact on regional “resource curse” by coal resource tax reform in China—A dynamic CGE appraisal. Resour. Policy 2015, 45, 277–289. [Google Scholar] [CrossRef]

- Polo, C.; Sancho, F. Insights or forecasts? An evaluation of a computable general equilibrium model of Spain. J. Forecast. 1993, 12, 437–448. [Google Scholar] [CrossRef]

- Blake, A.; Durbarry, R.; Eugenio-Martin, J.L.; Gooroochurn, N.; Hay, B.; Lennon, J.; Scinclari, M.T.; Sugiyarto, G.; Yeoman, I. Integrating forecasting and CGE models: The case of tourism in Scotland. Tour. Manag. 2006, 27, 292–305. [Google Scholar] [CrossRef]

- Armington, P.S. A theory of demand for products distinguished by place of production. Staff Pap. (IMF Econ. Rev.) 1969, 16, 159–178. [Google Scholar] [CrossRef]

- Hosoe, N.; Gasawa, K.; Hashimoto, H. Textbook of Computable General Equilibrium Modeling: Programming and Simulations; Palgrave Macmillan: Basingstoke, UK, 2010. [Google Scholar]

- Krinsky, I. The small country assumption: A note on Canadian exports. Appl. Econ. 1983, 15, 73–79. [Google Scholar] [CrossRef]

- Bao, Q.; Tang, L.; Zhang, Z.X.; Wang, S.Y. Impacts of border carbon adjustments on China’s sectoral emissions: Simulations with a dynamic computable general equilibrium model. China Econ. Rev. 2013, 24, 77–94. [Google Scholar] [CrossRef]

- Tang, L.; Shi, J.R.; Bao, Q. Designing an emissions trading scheme for China with a dynamic computable general equilibrium model. Energy Policy 2016, 97, 507–520. [Google Scholar] [CrossRef]

- Ye, R.S.; Wu, Y.D. Study on the Strategic Development and Export Regulation Policy of China’s Rare Earths; Science Press: Beijing, China, 2014. [Google Scholar]

- Zhong, S.; Shen, L.; Sha, J.H.; Okiyama, M.; Tokunaga, S.; Liu, L.T.; Yan, J.J. Assessing the water parallel pricing system against drought in China: A study based on a CGE model with multi-provincial irrigation water. Water 2015, 7, 3431–3465. [Google Scholar] [CrossRef]

- Moroney, J.R.; Trapani, J.M. Factor demand and substitution in mineral-intensive industries. Bell J. Econ. 1981, 12, 272–284. [Google Scholar] [CrossRef]

- Markandya, A.; Pedroso-Galinato, S. How substitutable is natural capital? Environ. Resour. Econ. 2007, 37, 297–312. [Google Scholar] [CrossRef]

- Wesseh, P.K., Jr.; Lin, B.Q.; Appiah, M.O. Delving into Liberia’s energy economy: Technical change, inter-factor and inter-fuel substitution. Renew. Sustain. Energy Rev. 2013, 24, 122–130. [Google Scholar] [CrossRef]

- Saunders, H.D. Toward a neoclassical theory of sustainable consumption: Eight golden age propositions. Ecol. Econ. 2014, 105, 220–232. [Google Scholar] [CrossRef]

- Zha, D.L.; Ding, N. Elasticities of substitution between energy and non-energy inputs in China power sector. Econ. Model. 2014, 38, 564–571. [Google Scholar] [CrossRef]

- Massari, S.; Ruberti, M. Rare earths elements as critical raw materials: Focus on international markets and future strategies. Resour. Policy 2013, 38, 36–43. [Google Scholar] [CrossRef]

- Schüler, D.; Buchert, M.; Liu, R.; Dittrich, S.; Merz, C. Study on Rare Earths and Their Recycling; Öko-Institut e.V.: Darmstadt, Germany, 2011. [Google Scholar]

- Aston, A. China’s Rare-Earth Monopoly. MIT Technology Review. 15 October 2010. Available online: http://www.arafuraresources.com.au/about_re.html (accessed on 16 August 2011).

- Binnemans, K.; Jones, P.T.; Blanpain, B.; Gerven, T.V.; Yang, Y.X.; Walton, A.; Buchert, M. Recycling of rare earths: A critical review. J. Clean. Prod. 2013, 51, 1–22. [Google Scholar] [CrossRef]

- Tanaka, M.; Oki, T.; Koyama, K.; Narita, H.; Oishi, T. Recycling of rare earths from scrap. In Handbook on the Physics and Chemistry of Rare Earths; Bunzli, J.C.G., Pecharsky, V.K., Eds.; Elsevier: Amsterdam, The Netherlands, 2013; Volume 43, pp. 159–212. [Google Scholar]

- Reck, B.K.; Graedel, T.E. Challenges in metal recycling. Science 2012, 337, 690–695. [Google Scholar] [CrossRef] [PubMed]

- Sumitomo Corp. Sumitomo Corporation Embarks on a Rare-Earth Recovery Project in the Republic of Kazakhstan. SC News. 12 August 2009. Available online: http://www.sumitomocorp.co.jp/english/news/detail/id=26218 (accessed on 15 August 2016).

- Tabuchi, H. Japan Recycles Minerals From Used Electronics. New York Times. 4 October 2010. Available online: http://www.nytimes.com/2010/10/05/business/global/05recycle.html?_r=0 (accessed on 15 August 2016).

- Marshall, J. Why Rare Earths Recycling Is Rare. Ensia. 7 April 2014. Available online: http://ensia.com/features/why-rare-earth-recycling-is-rare-and-what-we-can-do-about-it/ (accessed on 15 August 2016).

- Golev, A.; Scott, M.; Erskine, P.D.; Ali, S.H.; Ballantyne, G.R. Rare earths supply chains: Current status, constraints and opportunities. Resour. Policy 2014, 41, 52–59. [Google Scholar] [CrossRef]

- Free, K. The Future of Rare Earth Recycling. Scienceline, 3 March 2014. Available online: http://scienceline.org/2014/03/the-future-of-rare-earth-recycling/ (accessed on 15 August 2016).

- U.S. Department of Energy (DOE). Critical Materials Strategy. 2011. Available online: http://energy.gov/sites/prod/files/DOE_CMS2011_FINAL_Full.pdf (accessed on 15 August 2016). [Google Scholar]

- U.S. Geological Survey (USGS). Mineral Commodity Summaries—Rare Earths. 2011. Available online: http://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/index.html (accessed on 23 July 2016). [Google Scholar]

- Liu, M.X.; Tao, R.; Yuan, F.; Cao, G.Z. Instrumental land use investment-driven growth in China. J. Asia Pac. Econ. 2008, 13, 313–331. [Google Scholar] [CrossRef]

- Fu, F.; Ma, L.W.; Li, Z.; Polenske, K.R. The implications of China’s investment-driven economy on its energy consumption and carbon emissions. Energy Convers. Manag. 2014, 85, 573–580. [Google Scholar] [CrossRef]

- Mancheri, N.A. World trade in rare earths, Chinese export restrictions, and implications. Resour. Policy 2015, 46, 262–271. [Google Scholar] [CrossRef]

- Overholt, W.H. China in the global financial crisis: Rising influence, rising challenges. Wash. Q. 2010, 33, 21–34. [Google Scholar] [CrossRef]

- Chen, Z.H. Rare earth market overview in 2014 and market prospect for 2015. In Proceedings of the China Rare Earth Market Conference, Haikou, China, 25–27 March 2015.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sector Code | Sector/Commodity | Sector Code | Sector/Commodity |

|---|---|---|---|

| 1 | Agriculture | 14 | Manufacture of transport equipment |

| 2 | Mining and washing of coal | 15 | Manufacture of electrical machinery and equipment |

| 3 | Extraction of petroleum and natural gas | 16 | Manufacture of electronic equipment |

| 4 | Mining and processing of rare earths | 17 | Other manufactures |

| 5 | Mining and processing of other metal ores | 18 | Production and supply of electric power and heat power |

| 6 | Mining and processing of nonmetal ores | 19 | Production and supply of gas |

| 7 | Manufacture of food | 20 | Production and supply of water |

| 8 | Manufacture of textiles | 21 | Construction |

| 9 | Manufacture of wood products | 22 | Transportation services |

| 10 | Processing of petroleum and coke | 23 | Wholesale, retail trade, hotel and restaurant |

| 11 | Manufacture of chemical products | 24 | Financial services |

| 12 | Manufacture of non-metallic mineral and metal products | 25 | Education, health, culture and sports |

| 13 | Manufacture of general and special purpose machinery | 26 | Other services |

| Sector Code | Substitution Elasticities of CET Function | Substitution Elasticities of Armington Function | Substitution Elasticities between Capital Composite and Labor | Substitution Elasticities between Natural Capital and Monetary Capital | Income Elasticities of Rural Household | Income Elasticities of Urban Household |

|---|---|---|---|---|---|---|

| 1 | 3.60 | 3.00 | 0.80 | 0.50 | 0.85 | 0.37 |

| 2 | 4.60 | 3.70 | 0.80 | 0.50 | 0.25 | 0.86 |

| 3 | 4.60 | 3.70 | 0.80 | 0.50 | 0.25 | 0.86 |

| 4 | 4.60 | 3.70 | 0.80 | 0.50 | 0.25 | 0.86 |

| 5 | 4.60 | 3.70 | 0.80 | 0.50 | 0.25 | 0.86 |

| 6 | 4.60 | 3.70 | 0.80 | 0.50 | 0.25 | 0.86 |

| 7 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 8 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 9 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 10 | 4.60 | 3.70 | 0.80 | 0.50 | 0.25 | 0.86 |

| 11 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 12 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 13 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 14 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 15 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 16 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 17 | 4.60 | 3.80 | 0.80 | 0.50 | 0.94 | 0.81 |

| 18 | 4.60 | 4.40 | 0.80 | 0.50 | 0.99 | 0.86 |

| 19 | 4.60 | 4.40 | 0.80 | 0.50 | 0.99 | 0.86 |

| 20 | 4.60 | 4.40 | 0.80 | 0.50 | 0.99 | 0.86 |

| 21 | 3.80 | 1.90 | 0.80 | 0.50 | 1.23 | 1.23 |

| 22 | 2.80 | 1.90 | 0.80 | 0.50 | 0.99 | 0.86 |

| 23 | 2.80 | 1.90 | 0.80 | 0.50 | 1.08 | 0.82 |

| 24 | 2.80 | 1.90 | 0.80 | 0.50 | 1.27 | 0.86 |

| 25 | 2.80 | 1.90 | 0.80 | 0.50 | 1.08 | 0.82 |

| 26 | 2.80 | 1.90 | 0.80 | 0.50 | 1.08 | 0.82 |

| Items for Forecast Scenarios | Subdivision of Items for Forecast Scenarios | S0 | S1 | S2 | ||

|---|---|---|---|---|---|---|

| - | S11 | S12 | S21 | S22 | ||

| Growth rate of total investment (%) | Primary industry | 14.3 | 14.3 | 14.3 | 14.3 | 14.3 |

| Secondary industry | 19.5 | 38.9 for SEI | 38.9 for SEI | 38.9 for SEI | 38.9 for SEI | |

| 19.5 for others | 19.5 for others | 19.5 for others | 19.5 for others | |||

| Tertiary industry | 20.0 | 20.0 | 20.0 | 20.0 | 20.0 | |

| Growth rate of total labor (%) | - | 0.6 | 0.6 | 0.6 | 0.6 | 0.6 |

| Substitution elasticity between rare earths and capital | - | 0.5 | 0.5 | 0.5 for sector 12 and 13 | 0.5 | 0.5 for sector 12 and 13 |

| - | 0.8 for others | 0.8 for others | ||||

| Substitution elasticity of CET function for sector 4 | - | 4.6 | 4.6 | 4.6 | 4.6 | 4.6 |

| Resource and environmental tax (%) | - | 12.0 | 12.0 | 12.0 | 23.9 | 23.9 |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ge, J.; Lei, Y.; Zhao, L. China’s Rare Earths Supply Forecast in 2025: A Dynamic Computable General Equilibrium Analysis. Minerals 2016, 6, 95. https://0-doi-org.brum.beds.ac.uk/10.3390/min6030095

Ge J, Lei Y, Zhao L. China’s Rare Earths Supply Forecast in 2025: A Dynamic Computable General Equilibrium Analysis. Minerals. 2016; 6(3):95. https://0-doi-org.brum.beds.ac.uk/10.3390/min6030095

Chicago/Turabian StyleGe, Jianping, Yalin Lei, and Lianrong Zhao. 2016. "China’s Rare Earths Supply Forecast in 2025: A Dynamic Computable General Equilibrium Analysis" Minerals 6, no. 3: 95. https://0-doi-org.brum.beds.ac.uk/10.3390/min6030095