Learnings from Regional Market Dynamics of Originator and Biosimilar Infliximab and Etanercept in Germany

, , , ,

, , , ,  , ,

, ,

Abstract

:1. Introduction

- -

- Regional variations in the use of TNF⍺ inhibitor biosimilars in Sweden have been attributed to the extent of actual (discounted/rebated) price differences between biosimilars and the originator product, the engagement of key opinion leaders, the issuance of local guidelines and to gainsharing arrangements [17,18].

- -

- In Germany, biosimilar uptake is also known to vary at the regional level. This was investigated by Blankart et al. for erythropoiesis-stimulating substances, filgrastim and somatropin. Variations in biosimilar uptake were partly attributed to the presence of explicit regional cost-control measures, such as quota regulations [54].

- -

- Although previous studies have characterized regional variations in the uptake of TNF⍺ inhibitor biosimilars in Germany, the reasons behind this variable uptake have not been examined in detail [19].

- -

- This study highlights the influence of prescription and budget control activities (organized at the regional and insurer level) on the variable uptake of infliximab and etanercept biosimilars.

2. Results

2.1. Overview of TNFα Inhibitor Dynamics in the German Healthcare System

2.1.1. The German Market for TNFα Inhibitors

2.1.2. Regulations of the German Market for TNFα Inhibitors

2.2. Analysis of Dispensing Data for TNFα Inhibitors

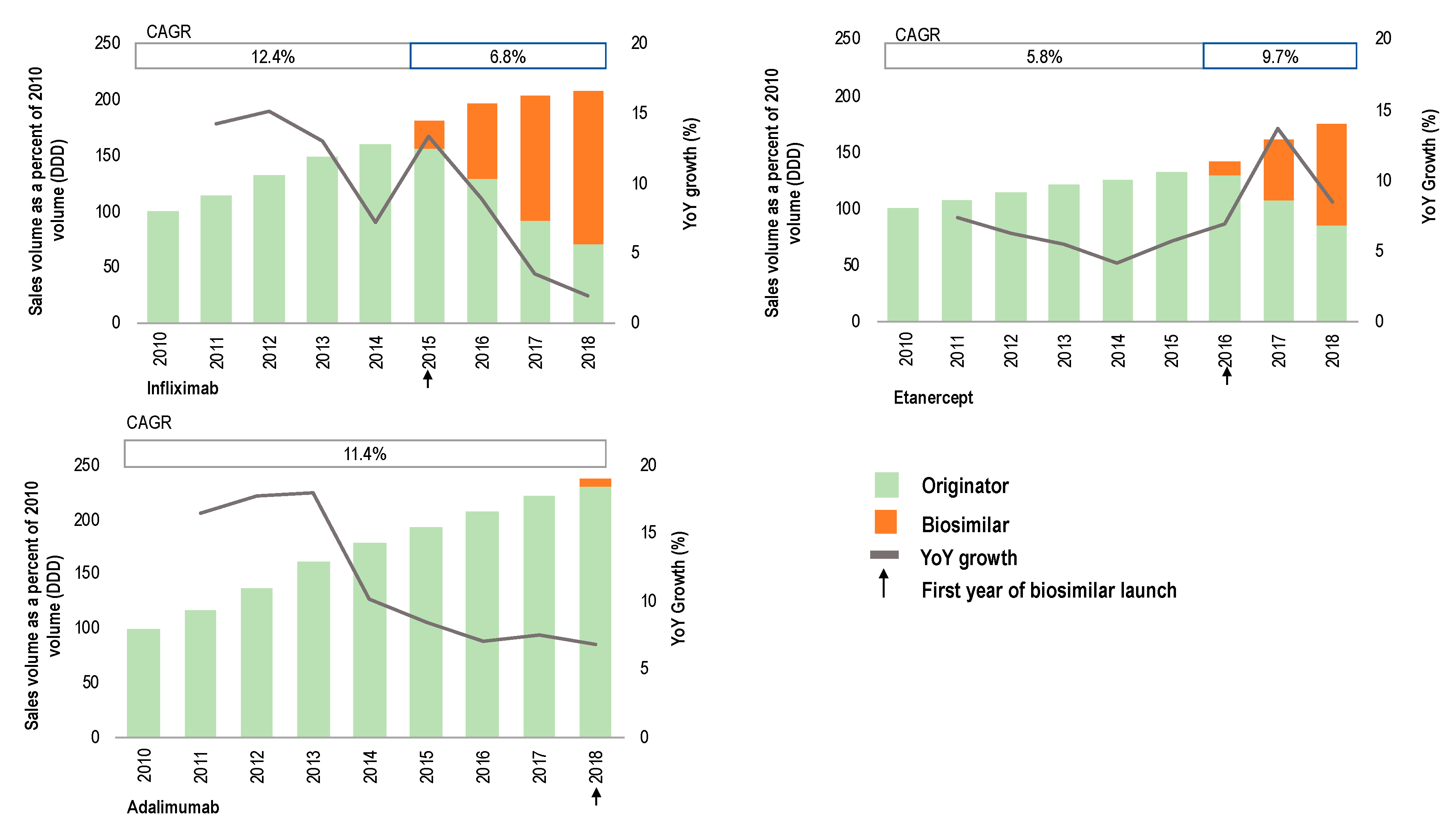

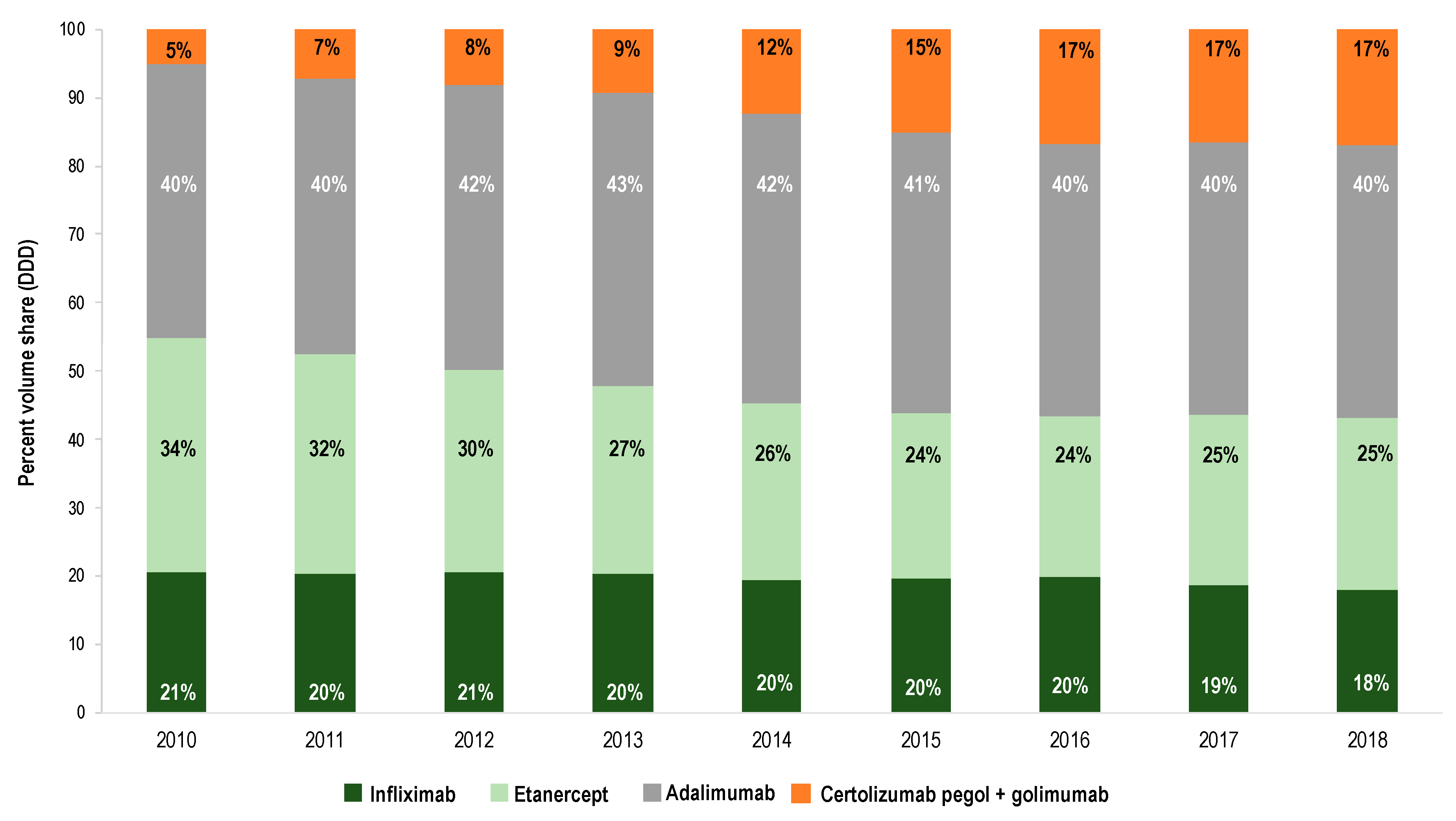

2.2.1. TNFα Inhibitor Products: Evolution in Sales Volume

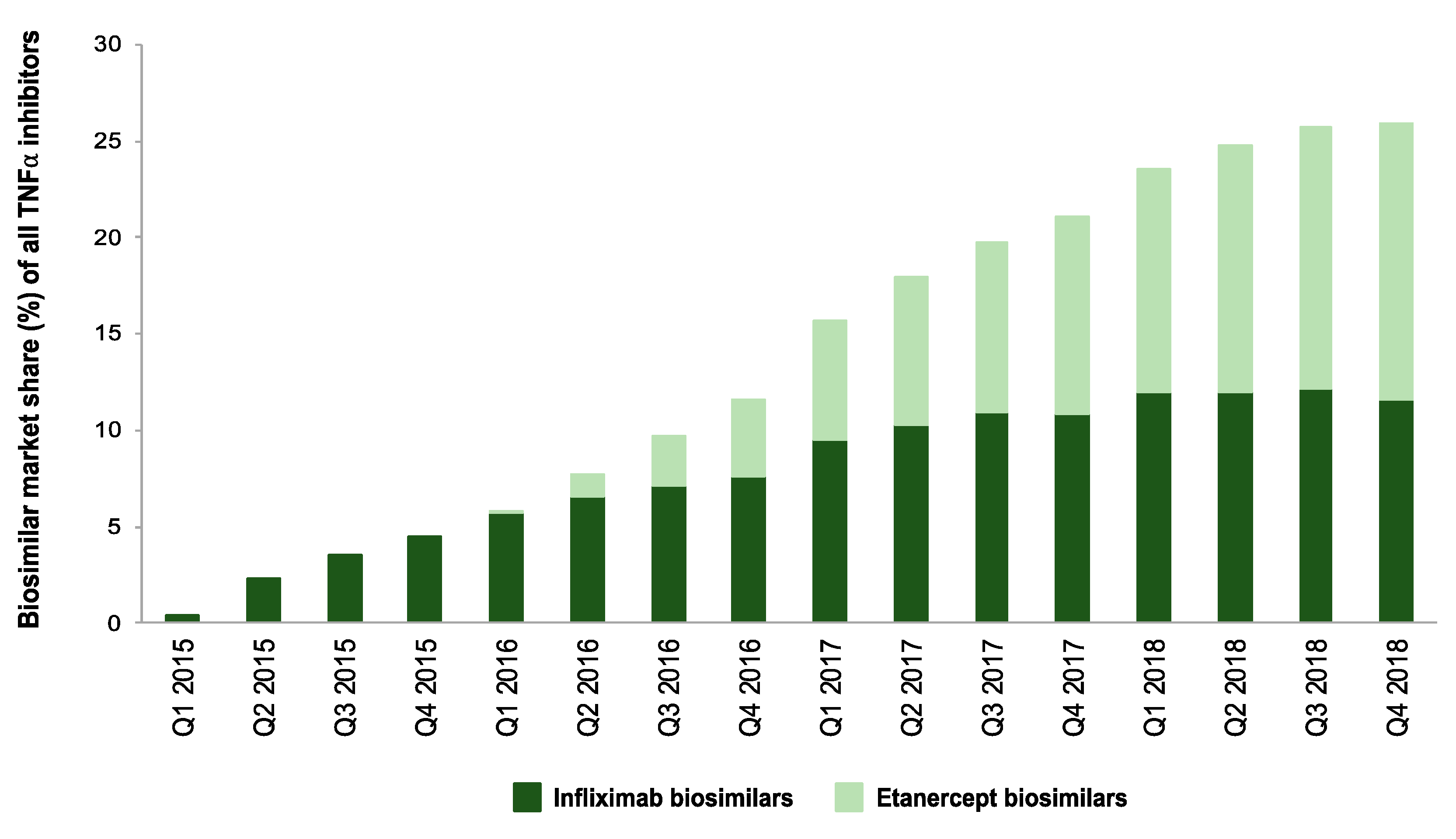

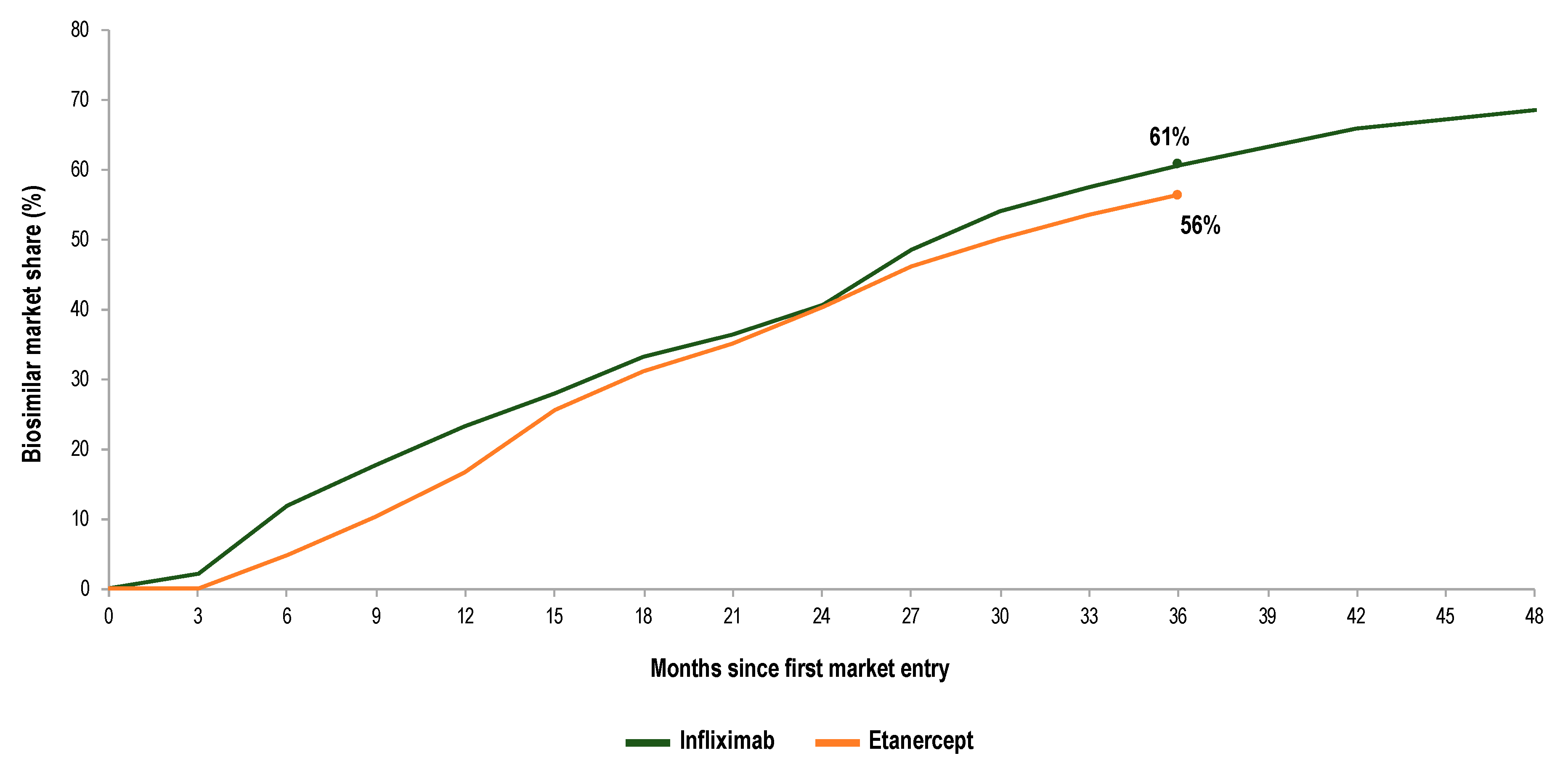

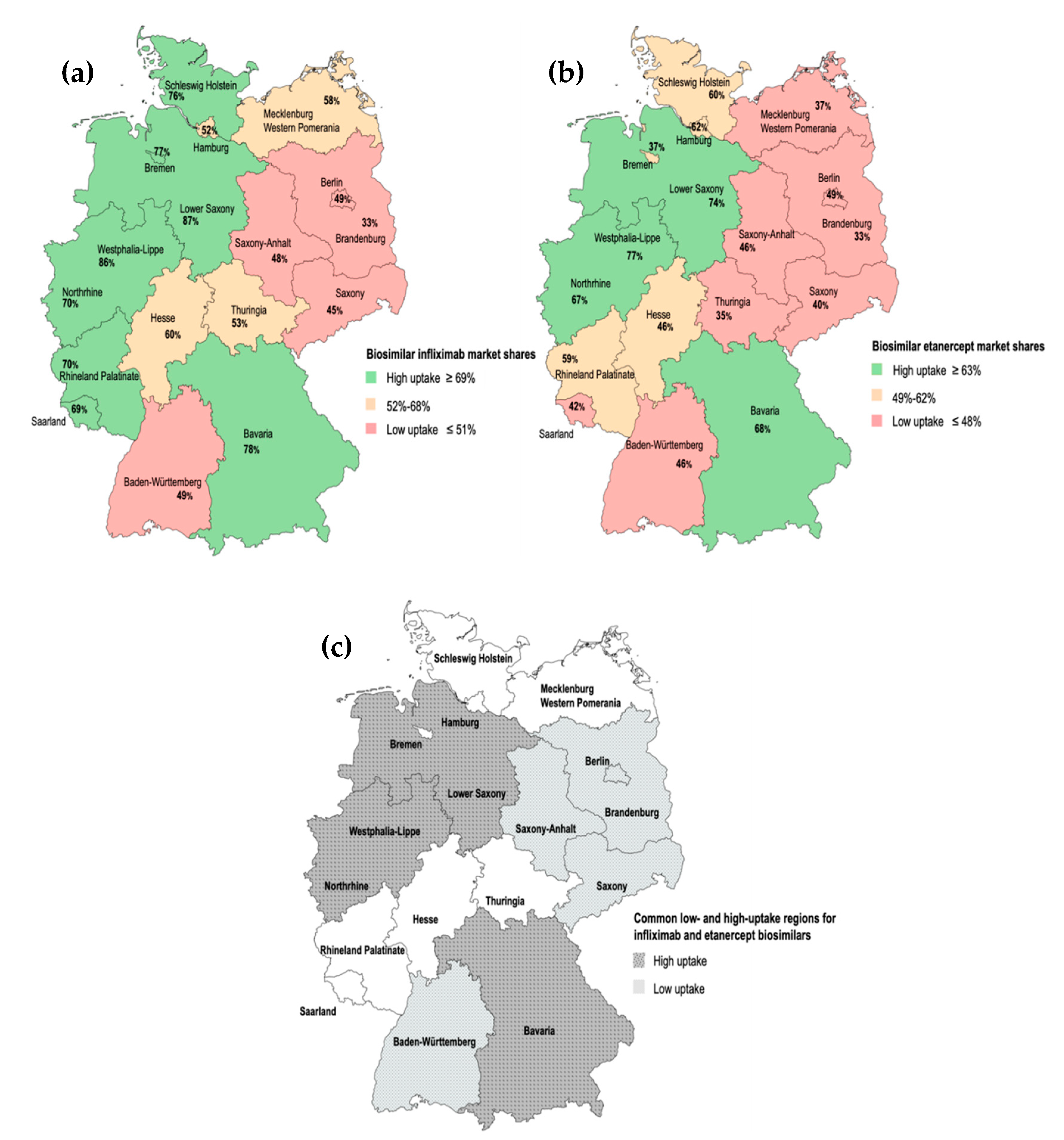

2.2.2. Infliximab and Etanercept Biosimilars and Originators: Evolution in Market Shares for the German Regions

2.3. The Role of Biosimilar Policies and Practices on Biosimilar Uptake: Interview Results

Incentives for Increased Biosimilar Use

3. Discussion

3.1. Incentives for Increased Biosimilar Use

3.2. Study Limitations

3.3. Future Research

4. Materials and Methods

4.1. Literature Review

4.2. Analysis of Dispensing Data for TNFα Inhibitors

4.3. Interviews

5. Conclusions

Availability of Data and Materials

Ethics Approval

Consent to Participate

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Baumgart, D.C.; Misery, L.; Naeyaert, S.; Taylor, P.C. Biological Therapies in Immune-Mediated Inflammatory Diseases: Can Biosimilars Reduce Access Inequities? Front. Pharmacol. 2019, 10. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Edwards, C.J.; Fautrel, B.; Schulze-Koops, H.; Huizinga, T.W.J.; Kruger, K. Dosing down with biologic therapies: A systematic review and clinicians’ perspective. Rheumatology 2018, 57, 589. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Smolen, J.S.; Braun, J.; Dougados, M.; Emery, P.; FitzGerald, O.; Helliwell, P.; Kavanaugh, A.; Kvien, T.K.; Landewé, R.; Luger, T.; et al. Treating spondyloarthritis, including ankylosing spondylitis and psoriatic arthritis, to target: Recommendations of an international task force. Ann. Rheum. Dis. 2014, 73, 6–16. [Google Scholar] [CrossRef] [PubMed]

- IQVIA. Fokus Biosimilars, Ausgabe 5; IQVIA Commercial GmbH & Co. OHG: Frankfurt am Main, Germany, 2019. [Google Scholar]

- Organisation for Economic Co-Operation and Development (OECD). Improving Forecasting of Pharmaceutical Spending—Insights from 23 OECD and EU Countries; OECD: Paris, France, 2019.

- European Medicines Agency (EMA). Guideline on Similar Biological Medicinal Products; European Medicines Agency: London, UK, 2014.

- IQVIA. The Impact of Biosimilar Competition in Europe; IQVIA Commercial GmbH & Co. OHG: Frankfurt am Main, Germany, 2018. [Google Scholar]

- Statistisches Bundesamt (Destatis). Genesis-Online, dl-de/by-2-0. Available online: https://www-genesis.destatis.de/genesis/online (accessed on 30 May 2019).

- IQVIA. Fokus Biosimilars, Ausgabe 1; IQVIA Commercial GmbH & Co. OHG: Frankfurt am Main, Germany, 2018. [Google Scholar]

- Grand View Research. Biosimilars Market Size, Share & Trends Analysis by Product, Application & Region—Global Segment Forecasts 2018-2025; Grand View Research, Inc.: San Francisco, CA, USA, 2018. [Google Scholar]

- IQVIA. Fokus Biosimilars, Ausgabe 2; IQVIA Commercial GmbH & Co. OHG: Frankfurt am Main, Germany, 2018. [Google Scholar]

- European Medicines Agency (EMA). Medicines. Anti-TNF Alpha. Available online: https://www.ema.europa.eu/en/search/search/field_ema_web_categories%253Aname_field/Human/search_api_aggregation_ema_medicine_types/field_ema_med_biosimilar?search_api_views_fulltext=ANTI%20TNF%20ALPHA%20 (accessed on 6 October 2019).

- IQVIA. Fokus Biosimilars, Ausgabe 4; IQVIA Commercial GmbH & Co. OHG: Frankfurt am Main, Germany, 2019. [Google Scholar]

- GaBI Journal Editor; GaBI Online Editor. Patent expiry dates for biologicals: 2018 update. Generics Biosimilars Initiat. J. 2019, 8, 24–31. [CrossRef]

- Bundesministerium für Gesundheit. Gesetzentwurf der Bundesregierung. Entwurf Eines Gesetzes Für Mehr Sicherheit in der Arzneimittelversorgung (GSAV); Bundesministerium für Gesundheit: Bonn, Germany, 2019. [Google Scholar]

- Dranitsaris, G.; Jacobs, I.; Kirchhoff, C.; Popovian, R.; Shane, L.G. Drug tendering: Drug supply and shortage implications for the uptake of biosimilars. Clin. Outcomes Res. 2017, 9, 573–584. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Moorkens, E.; Simoens, S.; Troein, P.; Declerck, P.; Vulto, A.G.; Huys, I. Different Policy Measures and Practices between Swedish Counties Influence Market Dynamics: Part 1-Biosimilar and Originator Infliximab in the Hospital Setting. BioDrugs 2019, 33, 285–297. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Moorkens, E.; Simoens, S.; Troein, P.; Declerck, P.; Vulto, A.G.; Huys, I. Different Policy Measures and Practices between Swedish Counties Influence Market Dynamics: Part 2-Biosimilar and Originator Etanercept in the Outpatient Setting. BioDrugs 2019, 33, 299–306. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Schwabe, U.; Paffrath, D.; Ludwig, W.D.; Klauber, J. Arzneiverordnungs-Report 2019; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Busse, R.; Blümel, M. Germany: Health System Review. Health Systems in Transition; WHO Regional Office for Europe: Copenhagen, Denmark, 2014; Volume 16. [Google Scholar]

- KPMG. Improving Healthcare Delivery in Hospitals by Optimized Utilization of Medicines. A Study into 8 European Countries; KPMG Advisory N.V.: Amstelveen, The Netherlands, 2019. [Google Scholar]

- Simon-Kucher & Partners. Biosimilars im Krankenhaus—Potenziale Besser Nutzen; Simon-Kucher & Partners: Berlin, Germany, 2017. [Google Scholar]

- Gemeinsamer Bundesausschuss. Zusammenfassende Dokumentation über die Änderung der Arzneimittel-Richtlinie (AM-RL): Anlage IX—Festbetragsgruppenbildung; Gemeinsamer Bundesausschuss: Berlin, Germany, 2017. [Google Scholar]

- Brandes, A.; Groth, A.; Gottschalk, F.; Wilke, T.; Ratsch, B.A.; Orzechowski, H.D.; Fuchs, A.; Deiters, B.; Bokemeyer, B. Real-world biologic treatment and associated cost in patients with inflammatory bowel disease. Z. Für Gastroenteologie 2019, 57, 843–851. [Google Scholar] [CrossRef] [PubMed]

- Emery, P.; Solem, C.; Majer, I.; Cappelleri, J.C.; Tarallo, M. A European chart review study on early rheumatoid arthritis treatment patterns, clinical outcomes, and healthcare utilization. Rheumatol. Int. 2015, 35, 1837–1849. [Google Scholar] [CrossRef] [PubMed]

- IQVIA. Advancing Biosimilar Sustainability in Europe. A Multi-Stakeholder Assessment; IQVIA Commercial GmbH & Co. OHG: Frankfurt am Main, Germany, 2018. [Google Scholar]

- Arbeitsgemeinschaft Probiosimilars. Handbuch Biosimilars. Available online: https://probiosimilars.de/img_upload/2019/10/Handbuch-Biosimilars_Oktober-2019.pdf (accessed on 17 October 2019).

- Arzneimittelkommission der Deutschen Ärzteschaft; Wissenschaftlicher Fachausschuss der Bundesärztekammer. Leitfaden “Biosimilars”, 1. Auflage. Available online: https://www.akdae.de/Arzneimitteltherapie/LF/Biosimilars/ (accessed on 17 October 2019).

- Bundesverband Deutscher Krankenhausapotheker e.V. Pressemeldung zu Biosimilars. Available online: https://www.adka.de/en/news/details/pressemeldung-zu-biosimilars-2017-09-01/ (accessed on 17 October 2019).

- Paul-Ehrlich-Institut; Federal Institute for Vaccines and Biomedicines. Position of Paul-Ehrlich-Institut Regarding the Use of Biosimilars. Available online: https://www.pei.de/EN/medicinal-products/antibodies/mab/monoclonal-antibodies-node.html?cms_tabcounter=1 (accessed on 17 October 2019).

- KV Bavaria. Arzneimittelvereinbarung nach § 84 Abs. 1 SGB V für das Jahr 2018. Available online: https://www.kvb.de/fileadmin/kvb/dokumente/Praxis/Rechtsquellen/Arzneimittelvereinbarungen/KVB-RQ-AMV-2018-Arzneimittelvereinbarung.pdf (accessed on 13 October 2019).

- KV Berlin. Arzneimittelvereinbarung nach § 84 Abs. 1 SGB V für das Jahr 2018 für Berlin. Available online: https://www.kvberlin.de/20praxis/60vertrag/10vertraege/arznei_und_heilmittel/arzneimittel_vb_2018.pdf (accessed on 13 October 2019).

- KV Westphalia-Lippe. Arzneimittelvereinbarung nach § 84 Abs. 1 SGB V für das Jahr 2018 für Westfalen-Lippe. Available online: https://www.kvwl.de/arzt/recht/kvwl/amv_hmv/amv_wl_2018.pdf (accessed on 13 October 2019).

- KV Brandenburg. Vereinbarung des Ausgabenvolumens für Arznei- und Verbandmittel nach § 84 Abs. 1 in Verbindung mit Abs. 6 SGB V (Arzneimittelvereinbarung) für das Jahr 2018. Available online: https://www.kvbb.de/praxis/verordnungen/arzneimittel/ (accessed on 13 October 2019).

- KV Baden-Württemberg. Arzneimittelvereinbarung nach § 84 Abs. 1 SGB V für den Bereich der KV Baden-Württemberg für das Jahr 2018. Available online: https://www.kvbawue.de/praxis/vertraege-recht/vertraege-von-a-z/arzneimittel/ (accessed on 13 October 2019).

- KV Bremen. Vereinbarung zur Sicherstellung der Arzneimittelversorgung im Jahr 2018. Available online: https://www.kvhb.de (accessed on 13 October 2019).

- KV Hamburg. Wirkstoffvereinbarung nach § 106b Abs. 1 SGB V i. d. F. des 2. Nachtrages. Available online: https://www.kvhh.net/kvhh/pages/index/p/177/0/g_id/428 (accessed on 13 October 2019).

- KV Mecklenburg Western Pomerania. Kassenärztlichen Vereinigung Mecklenburg-Vorpommern. Available online: https://www.kvmv.de/startseite/ (accessed on 13 October 2019).

- KV Lower Saxony. Arzneimittelvereinbarung 2016, Anlage 1. Available online: https://www.kvn.de/Patienten/Arztsuche.html (accessed on 13 October 2019).

- KV Saxony. Arzneimittelvereinbarung gemäß § 84 SGB V. für das Jahr 2018. Available online: https://www.kvs-Saxony.de/mitglieder/vertraege/arzneimittelvereinbarung-fuer-das-jahr-2018-gem-84-sgb-v/ (accessed on 13 October 2019).

- KV Saxony-Anhalt. Arzneimittelvereinbarung 2019 zur Sicherstellung der Vertragsärztlichen Versorgung mit Arzneimitteln Gemäß § 84 Abs. 1 SGB V für das Jahr 2019. Available online: https://www.kvsa.de/fileadmin/user_upload/PDF/Praxis/Arznei_Heilmittelvolumen_Richtgroessen/20190409_Arzneimittelvereinbarung_2019.pdf (accessed on 13 October 2019).

- KV Schleswig-Holstein. Zielvereinbarung zur Steuerung der Arzneimittelversorgung 2018. Available online: https://www.kvsh.de/fileadmin/user_upload/dokumente/Praxis/Vertraege/Arzneimittelvertraege/Zielvereinbarungen/2018_01_01_Zielvereinbarung_AM_OCR.pdf (accessed on 13 October 2019).

- KV Thuringia. Arzneimittelvereinbarung für das Jahr 2018 nach § 84 Abs. 1 SGB V. Available online: https://www.kv-thuringia.de (accessed on 13 October 2019).

- KV Northrhine. Vereinbarung. Available online: https://www.kvno.de/downloads/verordnungen/arzneimittelvereinbarung2019.pdf (accessed on 13 October 2019).

- KV Rhineland Palatinate. Arzneimittelvereinbarung. Anlage 1. Available online: https://www.kv-rlp.de/mitglieder/vertraege/arznei-und-heilmittel/ (accessed on 13 October 2019).

- KV Saarland. Arznei-, Verband- und Heilmittelvereinbarung für das Jahr 2018. Available online: https://www.kvsaarland.de (accessed on 13 October 2019).

- KV Hesse. Arzneimittel-Vereinbarung nach § 84 SGB V für das Jahr 2018. Available online: https://www.kvHesse.de/fileadmin/user_upload/kvHesse/Mitglieder/Recht_Vertrag/VERTRAG_Arzneimittel-Vereinbarung-2018_17082018.pdf (accessed on 13 October 2019).

- Bocquet, F.; Loubière, A.; Fusier, I.; Cordonnier, A.-L.; Paubel, P. Competition Between Biosimilars and Patented Biologics: Learning from European and Japanese Experience. Pharm. Econ. 2016, 34, 1173–1186. [Google Scholar] [CrossRef] [PubMed]

- Arbeitsgemeinschaft Probiosimilars. Biosimilars in Zahlen. Marktdaten 2019. Available online: https://probiosimilars.de/publikationen/?id=33&date= (accessed on 13 October 2019).

- Moorkens, E.; Vulto, A.G.; Huys, I.; Dylst, P.; Godman, B.; Keuerleber, S.; Claus, B.; Dimitrova, M.; Petrova, G.; Sovic-Brkicic, L.; et al. Policies for biosimilar uptake in Europe: An overview. PLoS ONE 2017, 12, e0190147. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Rémuzat, C.; Kapuśniak, A.; Caban, A.; Ionescu, D.; Radière, G.; Mendoza, C.; Toumi, M. Supply-side and demand-side policies for biosimilars: An overview in 10 European member states. J. Mark. Access Health Policy 2017, 5. [Google Scholar] [CrossRef] [Green Version]

- Rémuzat, C.; Dorey, J.; Cristeau, O.; Ionescu, D.; Radière, G.; Toumi, M. Key drivers for market penetration of biosimilars in Europe. J. Mark. Access Health Policy 2017, 5, 1272308. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Olry de Labry, A.G.E.; Linder, L.; García, L.; Espín, J.; Rovira, J. Biosimilars in the European market. Generics Biosimilars Initiat. J. 2013, 2, 30–35. [Google Scholar] [CrossRef]

- Blankart, K.E.; Arndt, F. Physician-Level Cost Control Measures and Regional Variation of Biosimilar Utilization in Germany. Int. J. Environ. Res. Public Health 2020, 17, 4113. [Google Scholar] [CrossRef] [PubMed]

- Flume, M. Regional management of biosimilars in Germany. Generics Biosimilars Initiat. J. 2016, 5, 125–127. [Google Scholar] [CrossRef]

- Federal Ministry of Health. KM6-statistics. Available online: http://www.gbe-bund.de. (accessed on 30 May 2019).

- Federal Ministry of Justice and Consumer Protection. Available online: https://www.bmjv.de/EN/Home/home_node.html (accessed on 9 November 2019).

- Kassenärztliche Bundesvereinigung (KBV). Available online: https://www.kbv.de/html/about_us.php (accessed on 13 October 2019).

- GKV Spitzenverband. Available online: https://www.gkv-spitzenverband.de (accessed on 15 December 2019).

- ABDATA Pharma Daten Service; ABDA Datenbank and ABDA Artikelstamm. Bi-Monthly Update; Avoxa-Mediengruppe Deutscher Apotheker GmbH: Eschborn, Germany, 2017. [Google Scholar]

- WHO Collaborating Centre for Drug Statistics Methodology. ATC/DDD International Language for Drug Utilization Research: The Anatomical Therapeutic Chemical (ATC) Classification System. Available online: https://www.whocc.no/ (accessed on 30 May 2019).

- Statistische Ämter der Bundes und der Länder; Gemeinsames Statistikportal. Gesundheitswirtschaft. Länderergebnisse Bruttowertschöpfung und Erwerbstätige der Gesundheitswirtschaft 2018. Available online: http://www.statistikportal.de/de/ggrdl/ergebnisse/wertschoepfungs-erwerbstaetigen-ansatz (accessed on 30 May 2019).

- Mouha, Y. Biosimilars: How can We Explain Regional Variations in Their Use?—Market Dynamics of Originator Biological and Biosimilar Infliximab and Etanercept in Germany. Master’s Thesis, KU Leuven, Leuven, Belgium, 2019. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Q1 2015 | Q2 2015 | Q3 2015 | Q4 2015 | Q1 2016 | Q2 2016 | Q3 2016 | Q4 2016 | Q1 2017 | Q2 2017 | Q3 2017 | Q4 2017 | Q1 2018 | Q2 2018 | Q3 2018 | Q4 2018 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| INFLIXIMAB | ||||||||||||||||

| Lower Saxony | 2% | 11% | 17% | 24% | 26% | 34% | 40% | 48% | 74% | 76% | 83% | 84% | 88% | 88% | 87% | 87% |

| Westphalia-Lippe | 3% | 20% | 25% | 33% | 40% | 49% | 57% | 64% | 68% | 73% | 77% | 79% | 83% | 84% | 86% | 86% |

| Bavaria | 2% | 12% | 18% | 25% | 30% | 37% | 38% | 42% | 55% | 66% | 70% | 72% | 75% | 77% | 78% | 78% |

| Bremen | 0% | 3% | 14% | 21% | 24% | 10% | 22% | 38% | 37% | 48% | 53% | 58% | 61% | 71% | 74% | 77% |

| Schleswig Holstein | 2% | 9% | 12% | 13% | 20% | 21% | 25% | 27% | 33% | 40% | 38% | 47% | 55% | 63% | 73% | 76% |

| Rhineland Palatinate | 1% | 11% | 17% | 25% | 25% | 37% | 41% | 47% | 55% | 59% | 60% | 69% | 69% | 70% | 62% | 70% |

| Northrhine | 1% | 13% | 27% | 32% | 40% | 46% | 50% | 53% | 57% | 57% | 61% | 62% | 63% | 67% | 69% | 70% |

| Saarland | 3% | 24% | 22% | 24% | 31% | 33% | 44% | 49% | 61% | 57% | 61% | 63% | 65% | 67% | 67% | 69% |

| Hesse | 6% | 19% | 28% | 38% | 44% | 42% | 43% | 45% | 47% | 52% | 51% | 55% | 55% | 56% | 58% | 60% |

| Mecklenburg Western Pomerania | 0% | 0% | 7% | 8% | 11% | 12% | 12% | 25% | 22% | 28% | 46% | 43% | 42% | 43% | 48% | 58% |

| Thuringia | 1% | 3% | 8% | 15% | 22% | 26% | 24% | 23% | 27% | 36% | 39% | 50% | 54% | 56% | 59% | 53% |

| Hamburg | 0% | 1% | 6% | 11% | 17% | 14% | 16% | 21% | 22% | 25% | 31% | 34% | 39% | 43% | 49% | 52% |

| Baden-Württemberg | 1% | 3% | 8% | 12% | 14% | 14% | 16% | 21% | 27% | 30% | 34% | 41% | 42% | 48% | 47% | 49% |

| Berlin | 0% | 2% | 5% | 10% | 15% | 26% | 29% | 31% | 36% | 36% | 38% | 40% | 43% | 45% | 44% | 49% |

| Saxony-Anhalt | 8% | 29% | 35% | 31% | 27% | 27% | 27% | 25% | 31% | 42% | 43% | 46% | 51% | 53% | 53% | 48% |

| Saxony | 0% | 3% | 4% | 9% | 10% | 14% | 14% | 16% | 18% | 20% | 22% | 29% | 33% | 36% | 40% | 45% |

| Brandenburg | 7% | 21% | 25% | 25% | 27% | 30% | 29% | 31% | 30% | 29% | 28% | 29% | 30% | 33% | 34% | 33% |

| ETANERCEPT | ||||||||||||||||

| Westphalia-Lippe | 0% | 0% | 0% | 0% | 0% | 22% | 38% | 47% | 55% | 59% | 62% | 66% | 71% | 75% | 76% | 77% |

| Lower Saxony | 0% | 0% | 0% | 0% | 0% | 3% | 9% | 25% | 48% | 55% | 61% | 65% | 69% | 70% | 73% | 74% |

| Bavaria | 0% | 0% | 0% | 0% | 0% | 4% | 10% | 17% | 34% | 46% | 50% | 55% | 61% | 63% | 65% | 68% |

| Northrhine | 0% | 0% | 0% | 0% | 0% | 8% | 14% | 20% | 28% | 33% | 39% | 47% | 54% | 59% | 63% | 67% |

| Hamburg | 0% | 0% | 0% | 0% | 0% | 1% | 5% | 11% | 17% | 21% | 22% | 27% | 40% | 49% | 57% | 62% |

| Schleswig Holstein | 0% | 0% | 0% | 0% | 0% | 4% | 7% | 11% | 17% | 22% | 28% | 31% | 44% | 53% | 57% | 60% |

| Rhineland Palatinate | 0% | 0% | 0% | 0% | 0% | 5% | 11% | 19% | 30% | 35% | 40% | 46% | 51% | 53% | 56% | 59% |

| Bremen | 0% | 0% | 0% | 0% | 0% | 3% | 8% | 18% | 28% | 29% | 37% | 39% | 47% | 47% | 54% | 55% |

| Hesse | 0% | 0% | 0% | 0% | 0% | 4% | 13% | 15% | 19% | 22% | 24% | 28% | 32% | 35% | 41% | 50% |

| Saxony-Anhalt | 0% | 0% | 0% | 0% | 0% | 2% | 5% | 7% | 11% | 16% | 21% | 28% | 39% | 44% | 43% | 46% |

| Baden-Württemberg | 0% | 0% | 0% | 0% | 0% | 4% | 11% | 16% | 23% | 26% | 30% | 32% | 37% | 38% | 42% | 46% |

| Saarland | 0% | 0% | 0% | 0% | 0% | 4% | 8% | 10% | 18% | 19% | 19% | 25% | 26% | 34% | 34% | 42% |

| Saxony | 0% | 0% | 0% | 0% | 0% | 1% | 3% | 6% | 9% | 13% | 17% | 24% | 31% | 37% | 39% | 40% |

| Berlin | 0% | 0% | 0% | 0% | 0% | 2% | 6% | 11% | 16% | 19% | 22% | 26% | 28% | 32% | 35% | 37% |

| Mecklenburg Western Pomerania | 0% | 0% | 0% | 0% | 0% | 2% | 4% | 8% | 13% | 16% | 18% | 21% | 26% | 30% | 36% | 37% |

| Thuringia | 0% | 0% | 0% | 0% | 0% | 1% | 2% | 4% | 5% | 9% | 11% | 17% | 23% | 25% | 33% | 35% |

| Brandenburg | 0% | 0% | 0% | 0% | 0% | 3% | 6% | 10% | 12% | 14% | 16% | 19% | 24% | 25% | 31% | 33% |

| Drivers of Biosimilar Use | Factors Facilitating Biosimilar Acceptance |

|---|---|

| Biosimilar prescription quotas: -Efficient monitoring -Presence of a sanctioning mechanism | Efficient communication between stakeholders -Robust reporting capability of regional physician associations |

| Greater cost-savings potential associated to biosimilars | |

| Gainsharing contracts | |

| Position statements/guidelines on the safety of switching |

| Quota Agreements: Characteristics | ||||||

|---|---|---|---|---|---|---|

| Regions | Early Quota Adoption: (Before 2016) | Set Unspecifically for Biosimilars | Set for the Category of TNFα Inhibitors | Set for the Active Substance | Applied Generally to All Prescribers | Applied Differently per Specialty |

| Baden-Württemberg | √ | √ | ||||

| Bavaria | √ | √ | √ | |||

| Berlin | √ | √ | ||||

| Brandenburg | √ | √ | ||||

| Bremen | √ | √ | ||||

| Hamburg | √ | √ | ||||

| Hesse | √ | √ | ||||

| Mecklenburg Western Pomerania: (missing data) | ||||||

| Lower Saxony | √ | √ | √ | |||

| Northrhine | √ | √ | ||||

| Rhineland Palatinate | √ | √ | ||||

| Saarland | √ | √ | ||||

| Saxony | √ | √ | ||||

| Saxony-Anhalt | √ | √ | ||||

| Schleswig Holstein | √ | √ | ||||

| Thuringia | √ | √ | ||||

| Westphalia- Lippe | √ | √ | √ | |||

| English Term | German Term | German Abbreviation |

|---|---|---|

| Drug Commission of the German Medical Association | Arzneimittelkommission der deutschen Ärzteschaft | AkdÄ |

| Federal Association of Statutory Health Insurance Physicians | Kassenärztliche Bundesvereinigung | KBV |

| ADKA - Federal Association of German Hospital Pharmacists | ADKA - Arbeitsgemeinschaft Deutscher Krankenhaus Apotheker e.V. | - |

| Federal Joint Committee | Gemeinsamer Bundesausschuss | G-BA |

| Federal Ministry of Justice and Consumer Protection | Bundesministerium der Justiz und für Verbraucherschutz | BMJV |

| ABDA - Federal Union of German Associations of Pharmacists | ABDA - Bundesvereinigung Deutscher Apothekerverbände e.V. | - |

| German Institute for Drug Use Evaluation | Deutsches Arzneiprüfungsinstitut e.V. | DAPI |

| German law for more safety in the supply of pharmaceuticals | Gesetz für mehr Sicherheit in der Arzneimittelversorgung | GSAV |

| German federal states | Bundesländer | - |

| German Regional Associations of Statutory Health Insurance Accredited Physicians (also referred to in text as PA regions): To be noted: -This paper makes a distinction between the 16 German federal states and the 17 PA regions. Although Germany is divided into 16 federal states, the areas Northrhine and Westphalia-Lippe within the state Northrhine-Westphalia are represented by two independent PA regions. -Dispensing data have been provided/analysed per PA region and the univariate regression study has been conducted with data at the state level. This was due to limitations in data availability for the univariate regression analyses. -When referring to regions formerly forming East Germany, we include Brandenburg, Mecklenburg Western Pomerania, Saxony, Saxony-Anhalt and Thuringia, but not Berlin. This is because we do not have sub regional data to analyze uptake differences between areas formerly forming East and West Berlin. | Kassenärztliche Vereinigungen | KV |

| National Association of Statutory Health Insurance Funds | Gesetzliche Krankenversicherung-Spitzenverband | GKV-SV |

| National advisory agreement on spending targets: (also referred to in text as national-level agreements on prescription targets) | Bundesrahmenvorgaben für die Arzneimittelvereinbarungen | - |

| “Open-house rebate” contracts | Open-House-Rabattverträge | - |

| Private Health Insurance (abbreviated in text as PHI) | Private Krankenversicherung | PKV |

| Regional agreements on prescribing spending targets, supply and economy targets (also referred to in text as regional-level contracts to establish prescribing quotas) | Arzneimittelvereinbarungen | - |

| Sickness Funds (also referred to in text as insurer organizations or insurers) | Krankenkassen | - |

| Social Code Book V (Statutory Health Insurance) | Sozialgesetzbuch V (Gesetzliche Krankenversicherung) | SGB V |

| Statutory Health Insurance (abbreviated in text as SHI) | Gesetzliche Krankenversicherung | GKV |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Moorkens, E.; Barcina Lacosta, T.; Vulto, A.G.; Schulz, M.; Gradl, G.; Enners, S.; Selke, G.; Huys, I.; Simoens, S. Learnings from Regional Market Dynamics of Originator and Biosimilar Infliximab and Etanercept in Germany. Pharmaceuticals 2020, 13, 324. https://0-doi-org.brum.beds.ac.uk/10.3390/ph13100324

Moorkens E, Barcina Lacosta T, Vulto AG, Schulz M, Gradl G, Enners S, Selke G, Huys I, Simoens S. Learnings from Regional Market Dynamics of Originator and Biosimilar Infliximab and Etanercept in Germany. Pharmaceuticals. 2020; 13(10):324. https://0-doi-org.brum.beds.ac.uk/10.3390/ph13100324

Chicago/Turabian StyleMoorkens, Evelien, Teresa Barcina Lacosta, Arnold G. Vulto, Martin Schulz, Gabriele Gradl, Salka Enners, Gisbert Selke, Isabelle Huys, and Steven Simoens. 2020. "Learnings from Regional Market Dynamics of Originator and Biosimilar Infliximab and Etanercept in Germany" Pharmaceuticals 13, no. 10: 324. https://0-doi-org.brum.beds.ac.uk/10.3390/ph13100324