Quantum Value Valuation Continuum

Département de Stratégie, Responsabilité Sociale et Environnementale, École des Sciences de la Gestion, Université du Québec à Montréal, Montréal, QC H3C 3P8, Canada

Quantum Rep. 2024, 6(1), 74-89; https://0-doi-org.brum.beds.ac.uk/10.3390/quantum6010006

Submission received: 22 December 2023

/

Revised: 18 January 2024

/

Accepted: 29 January 2024

/

Published: 2 February 2024

(This article belongs to the Special Issue New Reports on Quantum Mechanics: Discoveries, Promising Trends, and Technological Innovations)

Abstract

:Price, cost, and income (PCI) methods are traditionally used to approximate the value state of an economic commodity such as a property. Based on the estimates of these methods, we explore how quantum theory represents the fundamental process of value valuation in practice. We propose that the mathematical formalism of quantum theory is a promising view and measure of economic value. To ground our exploration, we first map traditional PCI estimates onto three-dimensional spherical coordinates, which were then transformed into two-dimensional quantum states using the Bloch sphere. This step enabled the computation of eigenvalues and eigenvectors of the Hamiltonian matrix, from which the value state measures were derived. The results exhibit practical applications as well as fundamental insights into potential connections between economic and quantum value states.

1. Introduction

Classical economics has used linear and statistical models to algorithmically approximate value, yet has borrowed methodologies from theoretical mathematics and, as we emphasize in this work, physics. Classical economics acknowledges that the subjective factors of value complicate the valuation process by algorithmic methods. In light of this, the tangible aspects of commodity value, as represented by price, cost, and income (PCI), do not sufficiently encapsulate the subjective factors which agents use while transacting on the free market. As such, we propose that the valuation process of a commodity is like that of information in quantum matter. This is like an observer–object relationship, where interaction from an observer’s measurement process influences the state of a quantum object. To clarify this relationship, we must first define value, which means some agreed-upon amplitude of importance among multiple agents. We argue that the components of value, represented by known quantities like PCI (which we call information), and probabilistic and subjective criteria (also called expectation), are inversely related to each other.

The information on a commodity’s objective properties contained in PCI quantities does not fully express the expectations of the evaluator. In this sense, expectations are an evaluator’s subjective valuation of a commodity or event before the moment for final valuation. Expectation is an unknown quantity and can only be realized upon negotiation, notably between buyers and sellers. When PCI fully represents a commodity’s value, expectations, or unknown value, are zero, and the information fully represents the value. In this work, we will frequently revisit the idea that this valuation process is similar to how a quantum object’s multiple wave functions collapse into a single state with measurement upon observation. This leads us to the physics debate of whether the theoretical information in particle properties represents a concrete reality, as is the case in subjective and objective measures of value. This question is of central importance in the physical world and thus directly pertinent to our discussion of subjective value.

The debate over whether matter is a wave or a particle continues to stir discussions about whether the quantum state is indicative of an actual physical reality (ontic) or merely reflects our knowledge (epistemic) of that reality [1,2]. The dominant position in physics is that of the ontic reality, yet despite this prevailing view, the key mathematical object of the wave function [3,4] does not always directly represent the underlying ontic reality [1]. The reality of a quantum state can be determined based on whether its probability distributions overlap. More specifically, when these distributions are mutually exclusive, the quantum state is considered ontologically real; if they intersect, the state veers towards an epistemic or theoretical nature, signifying a quantum state with a less definitive reality [5]. To determine the quantum state of a particle’s property, like momentum or position, experiments or calculations can be performed. Quantum states can either be known or unknown, yet particles can also exist in mixed states [6]. Floridi [7] asserted that ontic and epistemic perspectives are reconcilable, an idea that has been garnering incremental acknowledgment and support [8,9]. In this paper, we apply theoretical constructs in quantum physics to the nature of value valuation in commodities markets, specifically real estate. The binary/mixed states of valuation can be modelled by the discourse in quantum physics. We bridge the gap between theoretical and practical constructs by calculating ontic observable (information) and epistemic subjective observer information. We argue that like the quantum particle, this negotiation between subjective value assessments and objective criteria intersects into a known value state, collapsing into full information. This is the point at which value is transacted and agreed upon momentarily among multiple actors in the free market.

While classical economics acknowledges the probabilistic nature of value, the field has traditionally relied on algorithmic or statistical models to handle subjectivity. Classic decision theory posits that rational economic agents optimize for the utility function, which can be represented as an optimal selection probability distribution [10,11,12,13]. This idea can be modelled using a Bayesian probability, suggesting that optimal selection is a function of increasing knowledge [14,15,16]. However, Quantum Probability Theory (QPT) suggests a novel and seemingly more fitting framework for elucidating the processes of information processing and the probabilistic decisions that humans make regarding desired events [17,18,19,20,21]. QPT predicts probabilities for different experimental outcomes and accounts for the existence of subjective variables, such as the observer’s measurement process [22,23]. It is posited that each quantum entity persists in a wave-like state of multiple potential unknown quantum states, hence the term “superposition” until the particle is observed [24]. At the instant of measurement, the state assumes one of these many potential states. This phenomenon is not restricted to theoretical particles and is said to occur even in mental processes [25,26], yet this point remains contentious [27]. Nonetheless, the wavefunction collapse theory, notably through the lens of the Copenhagen or von Neumann–Wigner interpretation, alludes to observation or even consciousness as a critical factor in the collapse during measurement [28], and we and Penrose [29] propose that they occur simultaneously.

Gibbs’ [30] entropy, which bridged classical and quantum statistical mechanics, inspired von Neumann [25] to formalize quantum entropy [31]. Following early [32,33,34,35,36] and more contemporary [37,38,39,40,41,42] contributions, this work posits that quantum theory is a more promising avenue for comprehending value and a more appropriate framework for its measurement than traditional systems of value valuation. Scientists have applied entropy and quantum theory to reveal how people make decisions in terms of subjective expectation and information [43,44,45]. Quantum Decision Theory (QDT) seems to indicate that neural processes are strikingly well-modelled using the rational decision probability theory [46,47]. In simpler terms, QDT suggests that the way our brains make decisions can be effectively described using the same probability theories that are considered in quantum mechanics. Therefore, QDT can model and measure the average effect of subjectivity on people’s decisions [48]. Accordingly, Yukalov and Sornette [49] demonstrate that behavioural probabilities share many common features with quantum probabilities, suggesting that QDT applies to the description of decision making. Subjective preferences vary as a function of the Hamiltonian matrix [42], which Abel [50] has used to represent value. Abel [50], states that “Value drives an individual to consider different choices if it is not the evaluation of their relative value for each choice?” Additionally, Baaquie [51], Zhang and Huang [52], and Athalye and Haven [53] provide new perspectives on quantum formalism, which Özdilek [54] further explains by suggesting their relationship to the quantum state.

In this study, we explore the integration of quantum theory and measurement principles with traditional economic valuation methods. We initially explain how the value of a commodity, like a house, can be assessed using three primary approaches of PCI. Traditionally, while single-method assessments have often met practical needs for investment or taxation, we propose that the simultaneous application of PCI provides a more comprehensive valuation, encompassing various contexts. The multi-variable decisions related to housing value make PCI a suitable starting point for our analysis as compared to simpler commodities. Despite their widespread application, traditional three-system valuation methods merely provide approximate values, and there is significant variation when comparing results across these methods. As a secondary aim, we applied the quantum approach to that practical issue, delineating the methodologies and potential limitations. Our primary aim is to express the fundamentals of the valuation in terms of quantum phenomena. Drawing from Heisenberg’s Uncertainty Principle [55], a fundamental concept of quantum mechanics, we suggest that value is inherently subjective and non-deterministic.

This work delves specifically into the role of value and measurement in quantum theory, extending beyond classical economic value measures. In the sections that follow, we aim to explore whether quantum mathematical formalism fundamentally represents value estimation in general. We rely on the use of practical examples to relate these seemingly distant fields. Our approach begins where classical evaluation ends. By first considering the PCI estimates, we ground the assessment firmly in the realm of classical economics. We then compare these measurements of value to those generated via quantum methods, resulting in an adjusted value state for a property. We use historical PCI data as a basis for initial comparison among similar properties. Then, we represent these in three-dimensional spherical coordinates which are in turn converted into a two-dimensional quantum state using the Bloch sphere. We next extract eigenvalues and eigenvectors from these data, applying the entropy of Hamiltonian energy, in a similar way to von Neumann’s original quantum entropy [25], to generate new value state estimates. The results align well with expectations set by classical methods and demonstrate practical consistency.

2. Classic Value Valuation

Economics and real estate appraisal are mainly concerned with value measure [56,57,58]. In North America, property valuation has been well-organized and improving for more than a century, benefiting from the works of classical economists [59,60,61,62,63,64] and contemporary authors [65,66,67]. Reliable estimates of property value are essential for a wide range of agents, including property owners and managers, investors, providers of public goods and services, constructors, buyers, sellers, and institutions [68,69,70].

Experts in evaluation often use much simpler methods than either economists or physicists would use for market value estimation or state determination, respectively. Valuation methods and theories have set the standard for current practices, refined over centuries of debate [71]. Despite this deep interest, the nature of value is still unclear. As Robinson ([72], p. 26) concisely noticed: “Like all metaphysical concepts, when you try to pin [value] down it turns out to be just a word”. A survey of the literature reflects this sentiment: there are many definitions of value, especially when considered together with practical notions of price, cost, and income. Furthermore, PCI components are confused among themselves as well as with the value itself [71].

To begin with a traditional perspective, classical economics distinguishes between subjective use value and objective exchange value [73]. Following the Industrial Revolution, mainstream economics advocated for exchange value, given its objective and practical basis. Exchange value could be more easily understood in terms of PCI observables. Thus, this view suggests that scarcity and subjective utility are the main drivers of value [74]. We espouse the view that the complex nature of value is a result of its intangibility, more comprehensively understood as a dynamic and probabilistic “state” [67].

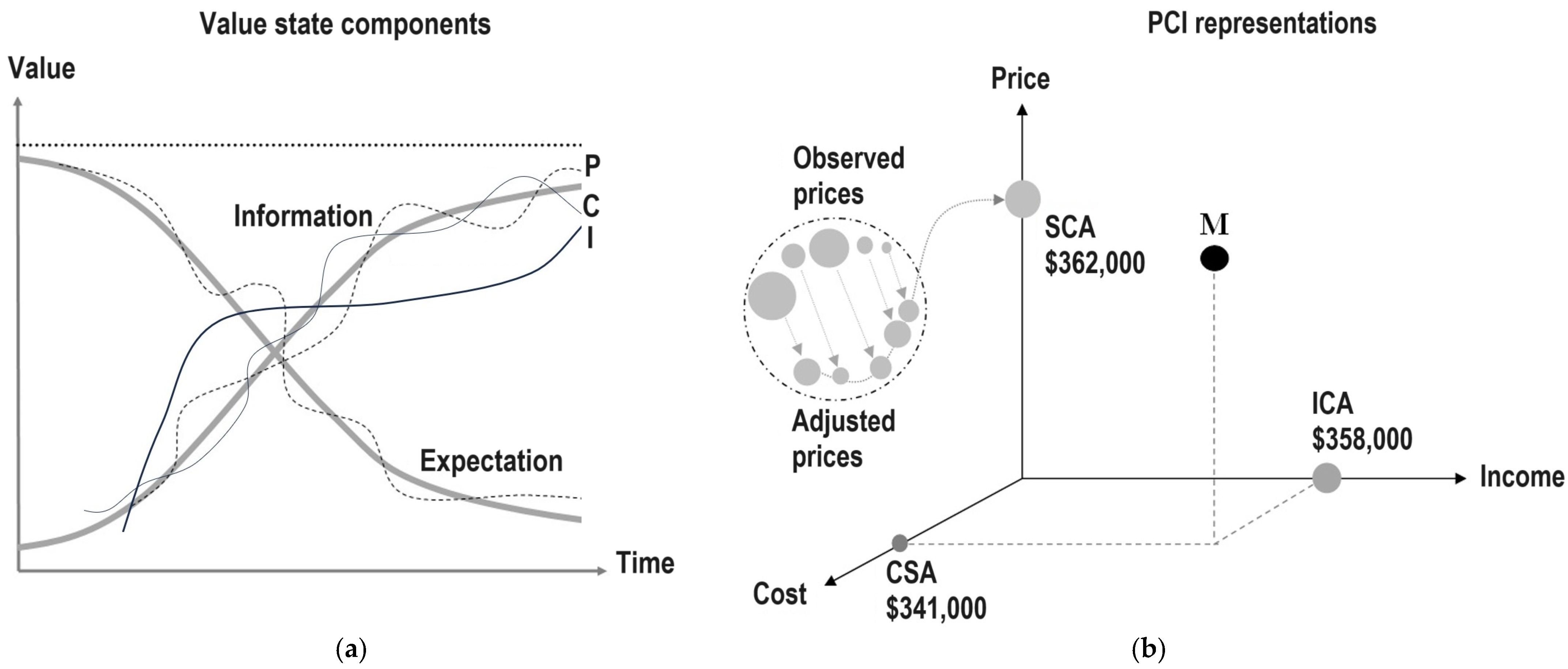

We suggest that this model best represents what happens when humans judge an object’s value. This value is determined based on prior expectations, or experiences, which are then updated as more information about the object is acquired. Thus, an aspect of value is represented by this inherent future uncertainty, raising “expectations”. Expectation exists if only an outcome is uncertain or probable [75]. The fulfillment of expectation is with the disclosure of novel information that corresponds to it, which in turn updates value dynamics. In this framework, the more uncertain an outcome is, the greater its attractive power and, consequently, its perceived value. Conversely, when an outcome is certain, expectation ceases to exist, leaving only the available information to define value, as depicted in Figure 1a. The logistic growth of theoretical information reflects the fact that an event has a limited amount of available information. The maximum value is entirely composed of undisclosed information, called expectation, and entirely consumed expectation, called information. As more information is acquired on the object’s value state, the expectation of value for that object or event decreases. Information gathered builds new expectations for other events or objects. This perpetuates the value valuation cycle. The dotted lines around the theoretically decreasing/increasing smooth curves consider that there are variations in expectation/information per individual, which can arise due to memory imperfection, information losses, or other adjustments. It is critical to note that the value of a commodity, represented by the horizontal dotted line, remains constant. This is analogous to the principle of conservation of energy, where the total energy of the system remains constant.

The conception of value put forth in this manuscript is, as previously mentioned, reminiscent of the universal law of Conservation of Energy. In a similar way that the movement and quantity of matter set the limit for the total energy of an object, so too does value define the total energy limit of a commodity. In this case, potential energy is represented as unknown information (also called expectation), while kinetic energy is represented as a final decision (simply called information). In this sense, value is determined at the moment of transaction, whereupon the buyer’s and seller’s expectation, or range of potential values, collapse into a singular, decided-upon value. In this context, PCI are three different types of competing economic information, which comprise the total, constant value state of the commodity in question. For instance, the price is a latent expression of value because it is determined by economic agents which each originally had a personal use value. Each negotiated price is a subjective statement of value to the user, all of which are incorporated within a market of similar commodities [76]. Supply and demand side agents follow a complex pattern of seeking, comparing, and evaluating the information on the subject commodity, with several offers leading to a final “expressed price”. Cost is also an economic expression of value that takes place at the moment of commodity production. Additionally, the concept of income is also a distinct expression of value, reflecting a commodity’s net rewards, projected into the future.

The Appraisal Institute [76] identifies three key approaches to valuing a property in real estate [77,78], each of which emphasizes different aspects of the PCI. These methods include the Sales Comparison Approach (SCA), the Cost Summation Approach (CSA), and the Income Capitalization Approach (ICA). The SCA evaluates a subject property’s market value state by its comparison to those that are similar, which are called comparables, using their realized prices as benchmarks. The CSA, on the other hand, bases value on the current cost of replacing or reproducing the same subject property, reflecting present economic conditions. Finally, the ICA assesses value by projecting future income streams and expenses over the subject property’s economic lifespan.

The three-dimensional xyz coordinates in Figure 1b illustrate the results of the application of triadic approaches and their corresponding PCI observables. After a series of computations and adjustments, this process generates three market estimations of value for the same subject property. The SCA supposes a market price of USD 362,000, based on the identification of four comparable properties. Given that these comparables have different structural, spatial, financial, and temporal attributes, adjustment processes were performed on their prices in the intermediary steps to make them similar to the subject property. This process is emphasized in the boxed region. Note that the sizes of the circles scale in proportion to observed prices used in the SCA. The same process is followed by CSA and ICA evaluation, although for simplicity, these are not illustrated in Figure 1b. Market prices were calculated to be USD 358,000 and USD 341,000 for the ICA and CSA, respectively.

During the last step of the real estate evaluation process, the most probable value is decided upon by considering the three PCI values collectively. The process of classical evaluation usually ends at this step, and one of the results is selected. For example, if the estimated market price of USD 362,000 is chosen based on the SCA, then the approach must be justified in its use compared to the two unused alternate alternatives. In this instance, a common justification for the SCA would be simply to cite comparable property values that command a similarly high price [79,80]. Despite this justification, the same property could be evaluated with either the CSA or the ICA, or a combination of both [81,82]. Importantly, the more of these valuation results are considered, the more accurate the value of the commodity. While this recommendation is rational, there are no practical standards for this in the literature. If the triadic estimates systematically converge to the same value, any one of the approaches could be considered reliable. However, this is rarely the case, and differences in triadic value estimates for a single property are often significant.

Recognizing the limitations of traditional methods, we can apply quantum methods to PCI estimates to converge on a more appropriate value state. The PCI point of convergence in a three-dimensional representation is identified as a state coordinate point M in Figure 1b. It is important to note that this intersection, a unique PCI estimate, may not yet be reliable. Each approach’s potential inaccuracies could shift the ‘M’ coordinate to a different probabilistic value state. By representing multiple such ‘M’ coordinates for identical or very similar properties, we create a spectrum or a space of potential value states. Within this space, quantum theory aids in identifying the most probable value, offering a more comprehensive and accurate valuation.

3. Quantum Value Valuation

Before presenting the basic equations in this section, we need to first specify normalization and transformation intermediary steps. The initial empirical data we use are not related to the physical properties of matter, but rather to a value state attached to a physical commodity with its constituent PCI information. The first operation consists of computing PCI’s probabilities, assuming they show a Gaussian behaviour [83,84,85].

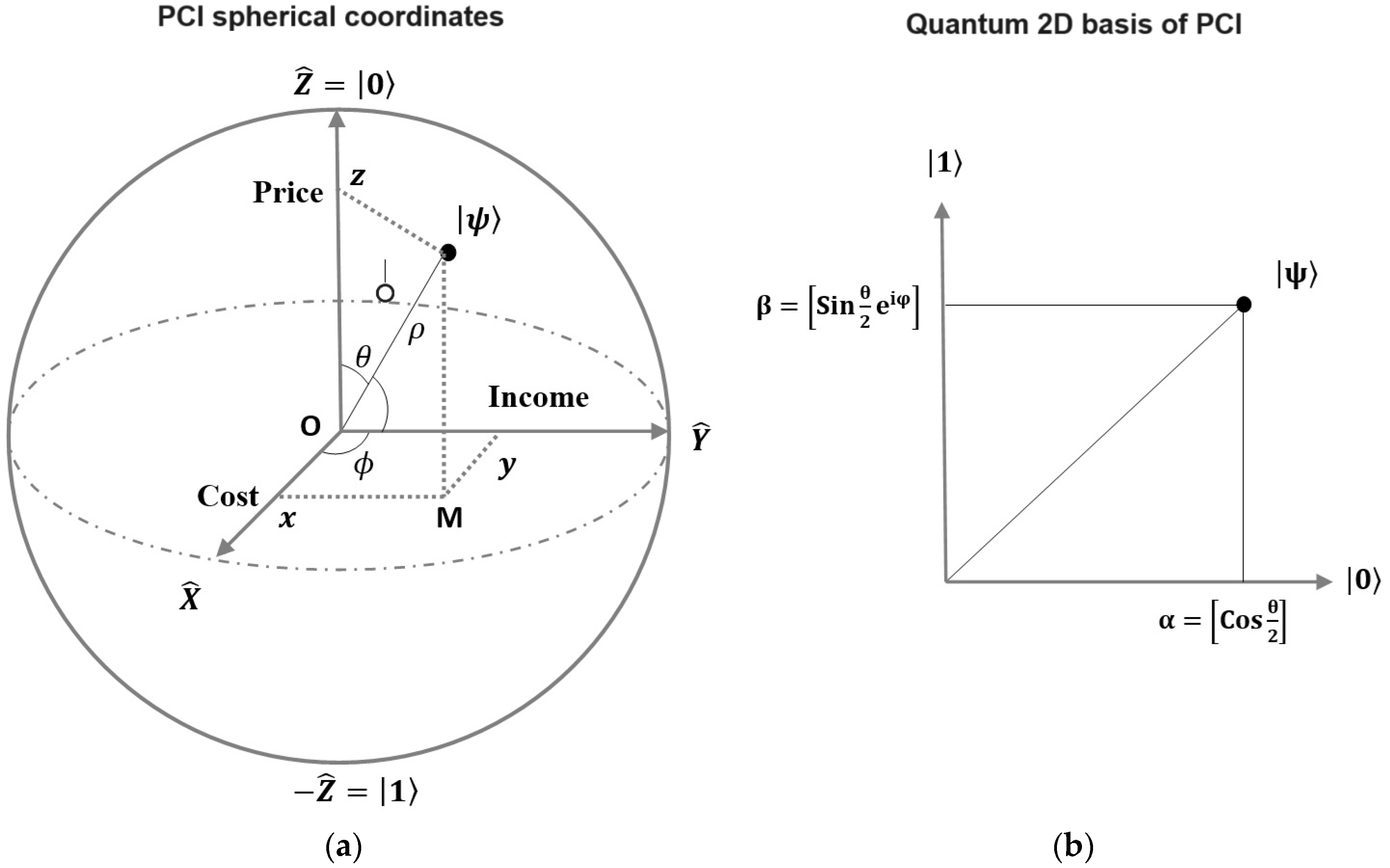

We can then represent these probabilities by their following spherical coordinates as follows.

The value conceived by the brain (is this the best word to use, can we say human, or negotiator) is theoretical and is nearly impossible to directly measure or identify using physical systems, which was the basis of converting these real PCI data into quantum data. Consistent with this idea, as depicted in Figure 2, we used the Bloch sphere to convert the observed PCI spherical coordinates in a quantum 2D basis [86,87]:

with, et .

The intrinsically subjective value, approximately represented by its PCI observables, no longer persists as a simple real function but is represented by a Hermitian operator acting within a Hilbert space. The measurement associated with this physical quantity corresponds to one of the real eigenvalues of this operator. It is crucial to note that in the non-deterministic domain of quantum mechanics, the state of the system only makes it possible to reproducibly predict the respective probabilities of the various possible results following the reduction of the wave function during measurement [88]. This fundamental principle states that certain quantum properties are intrinsically exclusive, thus establishing a deep connection between the uncertainty inherent in these systems and the nature of the information available [89].

Following the transformation, the quantum state responds to its universal representation of a q-bit [90]:

with and and representing the sum of the probability of each component, where is a q-bit quantum state. The q-bit is a superposition of and . If , we need to use and such that the sum of probabilities is .

Following computations of and , we proceed to the identification of the Hamiltonian matrix in order to compute Eigenvalues and [50]. Once in the quantum framework, one can assume that the Hamiltonian matrix embeds all of the system’s energy , resulting in the following domain which encapsulates the value state:

At this step, we apply the Schrödinger [34] equation, which makes use of the Hamiltonian operator [91]:

where is the quantum operator, is the basic eigenvector of the system, and is the Hamiltonian matrix. In the following section, we replaced in Equation (5) with for simplicity and uniformization of notations.

We must also consider the following equation from Louis De Broglie, which is the general solution of Schrödinger’s equation:

with representing eigenvectors and representing eigenvalues in the Hamiltonian matrix.

To demonstrate the effectiveness of our methodology, we used an example of a Hermitian Hamiltonian matrix, which is expressed in the following form:

The determination of the energy of the Hamiltonian matrix is based on the following formula:

The computation of Eigenvalues gives

The Eigenvectors are defined by

According to Louis de Broglie’s formula and Formulas (9) and (10), we deduce the following:

From Formula (11), by replacing and with their value, we obtain

By identifying and , we can deduce their relationship with the energies and :

where,

The solution of Equations (14) and (15) is

with , and the module of the two terms gives

The Planck constant is related to the quantization of light and matter, which is a subatomic-scale constant [92]. To make them visible, we operate a change of scale by replacing with , as well as considering , and then the Formula (17) becomes

We deduced that and .

The sum of the entropies of these eigenvalues, extracted from the Hamiltonian matrix , determines the entropy value which adequately approximates the value state. While entropy in general indicates the direction of value [93], von Neumann’s [25] quantum entropy offers a single value state by minimizing uncertainty. Moreover, the value state in which we are interested can be estimated using the mathematical formalism of a quantum state, which accounts for inherent subjectivity in unknown value states. The application of von Neumann [25] entropy to the eigenvalues and is the following (there are several properties of von Neumann’s entropy that can be found in Facchi et al., [94]):

von Neumann entropy is directly defined by the density matrix. The entropy in Equation (19) uses eigenvalues of the Hamiltonian matrix of energy, which can be considered, by analogy, parallel to that of von Neumann in the density matrix. In quantum mechanics, the Hamiltonian operator represents the system’s total energy. This concept aligns with classical mechanics, where the Hamiltonian is the sum of operators corresponding to the kinetic and potential energies of a system. Its energy spectrum, or its set of energy eigenvalues, reflects the possible total energy outcome measurements.

Following the elaboration of these formulas, we present the results in Section 4.

4. Quantum Value Results

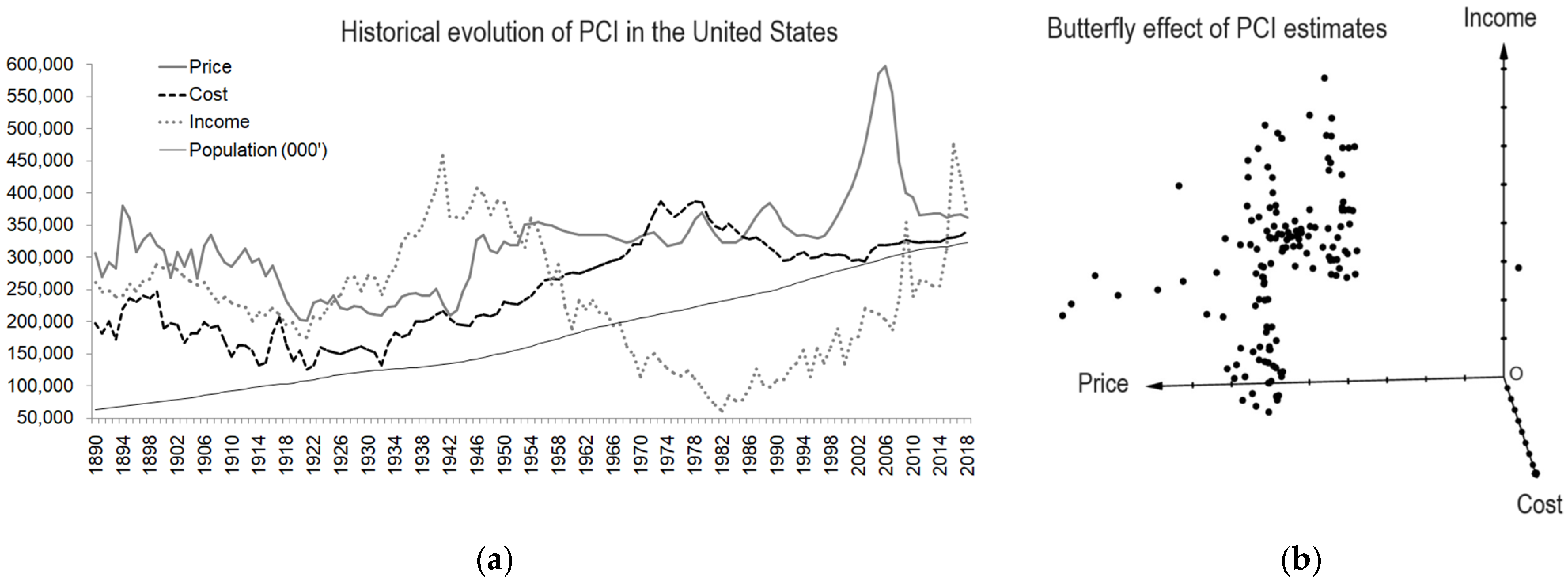

To demonstrate the reliability and utility of a quantum measure of value state, we initially considered a unique historical database from Shiller [95], which was used in the book Irrational Exuberance. Freely available online, these data encapsulate the average US housing price and cost indices and capitalization rates. All three indices are inflation-corrected, further modified, and regularly updated. We viewed these indices and rates as suitable proxies for PCI, requiring only minor adjustments, and used the PCI market value estimations of a typical house in 2018 for the same US market as a benchmark. With this reference point in mind, we re-adjusted Shiller’s data, processing the PCI evaluations of the same house 148 times. We then applied three types of yearly constants in a final adjustment to adjust PCI values spanning from 1870 to 2018. Accordingly, Shiller’s average price index is multiplied by a constant amount of USD 3068, resulting in an SCA of USD 362,000 in 2018. In the case of the CSA, the constant was USD 3852 resulting in an estimate of USD 341,000 for the same year. In the ICA, a yearly net operating income of USD 8939 was divided by the varying capitalization rates from Shiller’s data, which resulted in the estimate of USD 358,000 for 2018, as shown in Table 1.

Before delving into the quantum measurement of value states, it is worth highlighting that the prepared data on PCI in Figure 3a do not give noticeable clues about where the value state could be. On the contrary, we observe that PCI estimates vary significantly, converging only on rare occasions. This is particularly true for SCA and CSA, while ICA often has a negative correlation with the others. It should be noted that had we proceeded with evaluations for each case, global trends would not differ from what can be seen in Figure 3a. Visualizing these data using GeoGebra [96] indicates that there is a dispersion of PCI estimates. We see that the data display an interesting dispersion, reminiscent of the Lorenz [97] butterfly effect in Figure 3b. To confirm this observation, more points would need to be analyzed in the future.

Figure 3a,b raise questions as to why there are differences in the estimated market values after all the adjustments have been made. Are the 148 repeats, including corrections of temporal variation, sufficient to account for this variation? Should not the PCI observables and the concurrent estimations of the triadic methods sufficiently allow accurate valuations of the same property? Is a simple or a weighted average, or any other robust statistical method, sufficient to acquire accurate valuation? The short answer to these questions is that PCI components fundamentally lack the informational resolution needed to determine true market value. This is an example of the fundamental limitation of the classical triadic evaluation methods. Most importantly, the classical interpretation is limited by the accuracy of the data coming from the market, knowing that each PCI is originally an average of thousands of transactions in the US housing market. Although individuals’ subjective use values are expressed in rational PCI exchange values, there is still uncertainty in the value state.

To address these challenges and provide potential solutions, we applied quantum measurement formalism to the same dataset. Each line in the dataset is an observable of triadic estimates, normalized and transformed through several steps to eventually represent a quantum state in two dimensions. It should be noted that each line of 148 cases in the dataset leads to the estimation of a quantum value state. Initially, it is unclear which of these cases reflects the most accurate quantum value state.

Corresponding Gaussian probabilities are computed and normalized using their maximums to generate cartesian xyz coordinates. As we explained above, these coordinates go into a Bloch transformation. After this, and states are computed with their corresponding angles and in columns 7 to 10. The correspondence of observed xyz vectors is a quantum state in two dimensions. For each PCI, we found a quantum state of value for a total of 148 estimates of the same property. In the next step of computations, and are used in the Hamiltonian matrix that generated eigenvalues (columns 11 and 12). Hamiltonian matrix embeds the total energies of PCI as expressions of value state. This matrix generates kinetic and potential energies of that system based on PCI observables. The computation of these Eigenvalues or energies is necessary for the application of von Neumann’s quantum entropies, which extracts the total quantum information held in and .

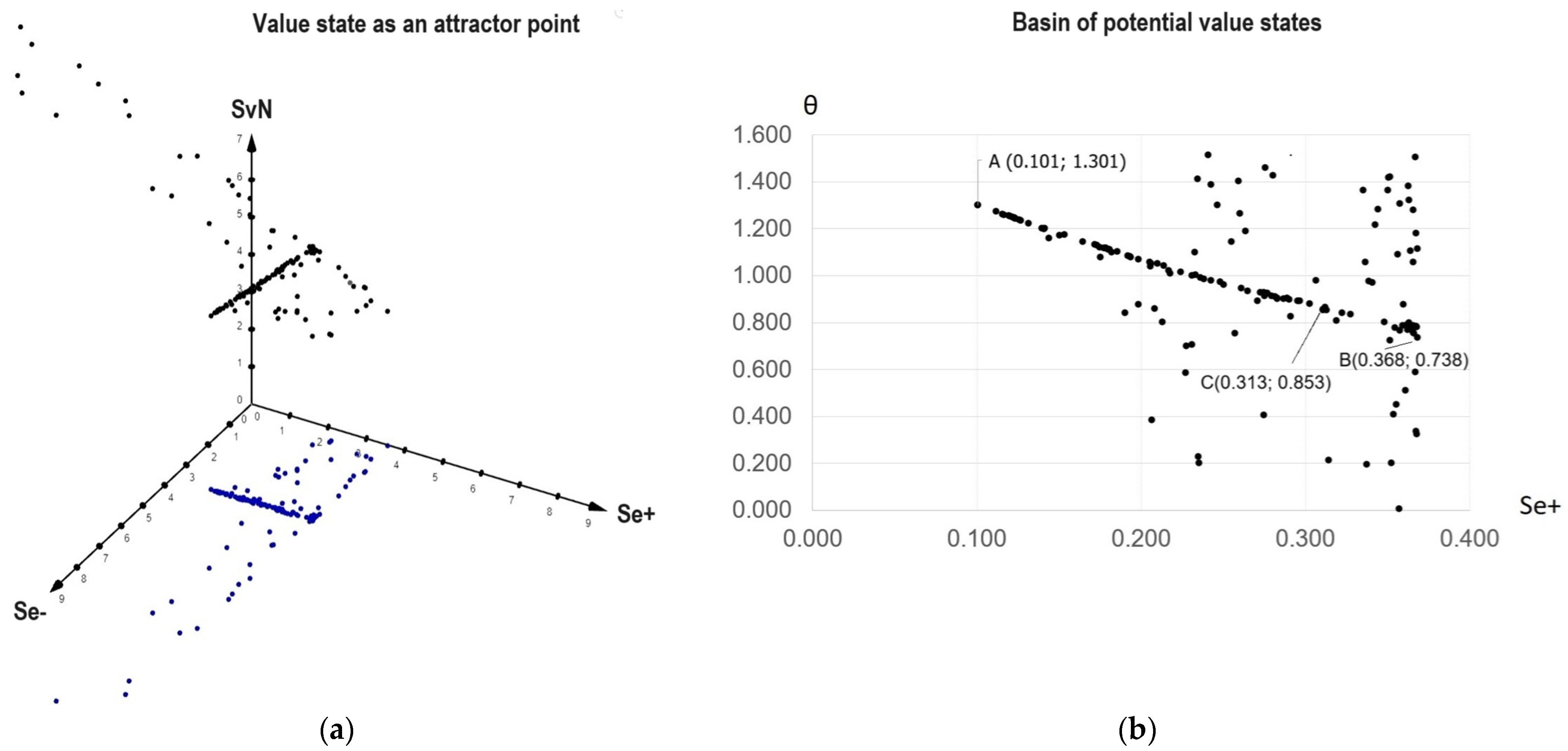

Von Neumann’s quantum entropy computations, based on these Eigenvalues, lead to and quantum entropies in columns 13 to 15. Von Neumann’s extracts the information in kinetic energy, although has extracted information in potential energy. The computation of this quantum information determines the direction of the value state. In Figure 4a, we represent the 3D information from the GeoGebra, where coordinates x, y, and z are represented by , y, and , respectively. Interestingly, the resulting geometric figure resembles an attractor system, in which a quantum object in the form of a “fly”, with its characteristic head and tail, seems to indicate a basin of potential values (for the explanations of value and attractor points, see Özdilek [98]).

The projection on a horizontal plane with and in Figure 4b provides a similar scheme, with A and B attractor points representing the head and tail. Here, we observe a clear linear trend spanning from attractor points A ( to B (. Because we consider this to be the basin of potential value states, every point along that linear basin can be a solution with a higher probability of true value compared to surrounding “outliners”. Sampling points along the linear basin filter other distant points, further narrowing the basin, in which states are predictable with higher probabilities. Doing so reduces the number of viable values, leaving point A as the sole attractor in the system.

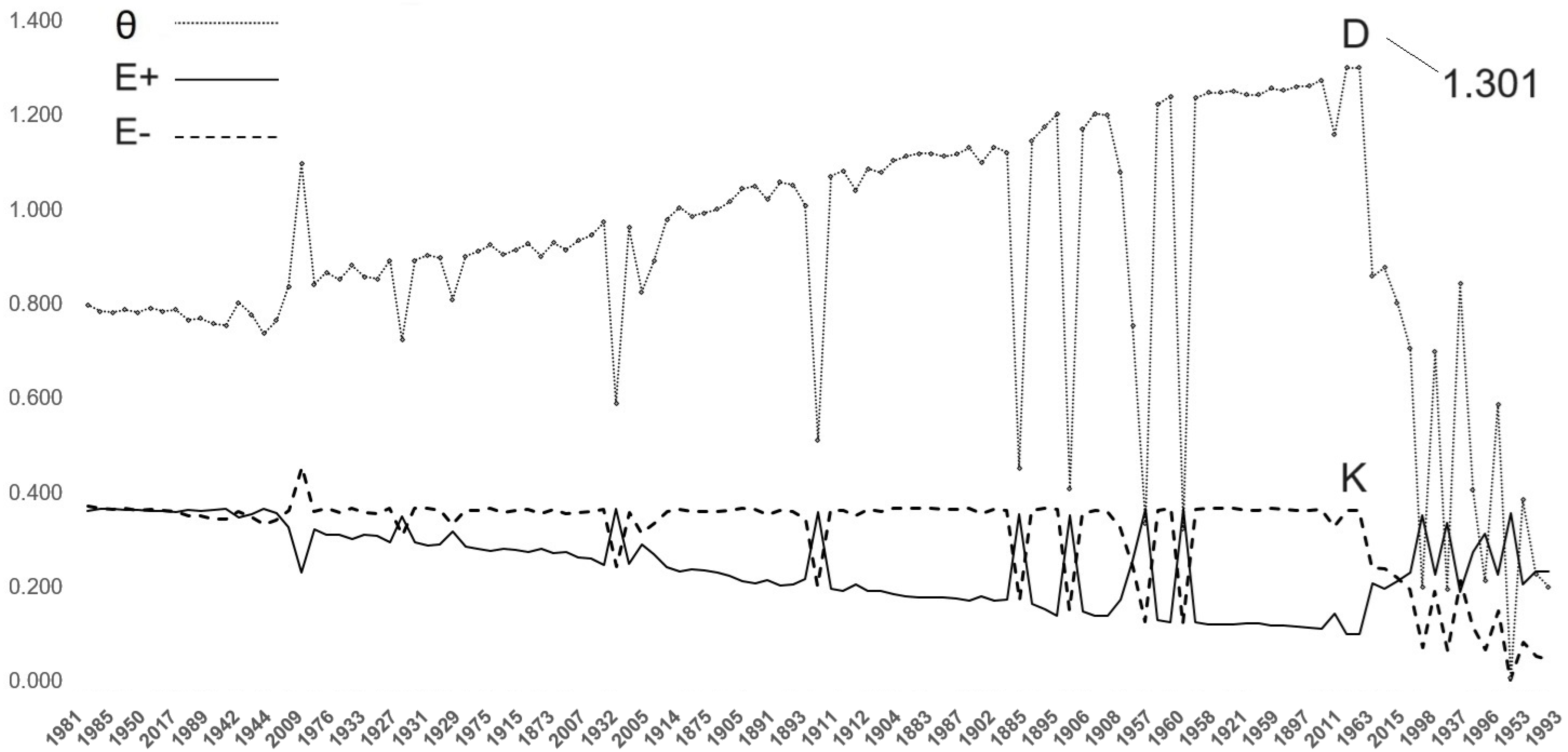

In addition to geometrical and attractor point basis, we can also locate value state considering the relationship between and in the function of an increasing angle (computed as shown in Figure 5. The (as equivalent of value) points in the direction of a (mental) value state or comes closer to it as the one, among other potential states, holding the maximum information extracted from and using the application of von Neumann’s quantum entropies and . According to the principle of conservation of energy, encompassed by dynamically varying kinetic E+ and potential E- energies, the kinetic energy is inversely proportional to potential energy, maintaining a total energy constant. The information extracted by from comes to a saturation point in D, while the available information or the residual expectation is extractable by from , and stops at point K. Increases in kinetic energy are stabilized when potential energy is almost empty. Points D and K have the same perpendicular values for and . D and K point out and which determine by their superposition. If we measure state, there is collapse either on or . At point K, the potential value decreases to zero, at which point kinetic energy reaches its maximum value and the value state is constant. The data were organized by increasing the values of Teta, resulting in a sequence that was not chronologically ordered. Our primary objective was to identify the maximum of the Kinetic energy ( and ) and the minimum of the potential energy ( and ). We achieved this objective by locating the Teta value that corresponded to the total energy, which corresponded to the total value.

We can consider a comparative approach from an expert perspective to determine if quantum formalism accurately identifies values. An expert analyzing 148 value states would recognize that a classical valuation falls near the value predicted by the entropy of the Hamiltonian energy. Although this approach falls outside of related computations, by employing a total distance between PCI estimates, we indicate a well-crafted case for standard valuation. What it indicates is that the property’s value state estimations should converge for 148 cases, considering that all three different approaches use the same property. If the method performs well according to the theoretical assumption, the resulting distance decreases. Accordingly, the estimation in the last column of Table 1 is the most reliable with a total divergence of USD 21,378, matching the quantum approach.

It should also be noted that there is an even lower dPCI distance for the sixth case, USD 18,821, represented by point C in Figure 4b (. There are three potential issues when considering aligning value states on point C. First, compared to point A, which visually seems to be a point of attraction towards which other value states might converge, point C diverges considerably from the trend curve of Figure 5, landing in the collapsing region after point D. Even though this dPCI is the lowest, an expert would consider this a poor estimate (as estimated PCI values are around USD 220,000, very far from what experience would suggest). We assume that the result in point A represents a reliable pointwise estimate, as indicated by visually attractive points and energy conservation measurements.

5. Discussion

The quantum probability theory, decision theory, and mathematical formalism of von Neumann’s quantum entropy inspired this work’s exploration of the basis of value valuation. By using practical examples from economics, specifically real estate valuation, we were able to integrate these theories into practical measures. The methodology of applying the Bloch transformation to historical PCI data, and then employing quantum entropy to the eigenvalues derived from a Hamiltonian matrix, resulted in a space of probable quantum states of value. In this space, a limited number of values constituted a basin of attraction, one of which emerged as a solution to quantum entropy.

The results presented in this study are consistent with those who find that quantum theory can accurately represent uncertainties within their fields. This has resulted in various theories which implicate quantum phenomena in psychological fields, such as the strange attractors theory [99], the visual/geometric orientations theory of value dynamics [100], and the integral features of the brain theory of value computation [101]. Our results are bounded by fundamentals such as the conservation of energy [102], and the related conservation of value [103]. Furthermore, expert opinion [67] contributes to our methodology. These natural laws impart a geometric structure to the dataset, fundamentally relying on the data-driven approximations of quantum mechanical processes [104].

The results are particularly relevant to the classical system of valuation, which often struggles to determine a final value when two or three PCI opinions are used in its approximation. In those instances when multiple valuation methods are used, the traditional approach is incapable of providing a final estimate. These estimates are often reconciled using a weighted or unweighted average, where weights are subjectively formulated. The most common option, however, is to consider a value estimate using only a single method. The chosen method is then justified based on some criteria, which may or may not yield the best approximation to market value, as the available method is often just limited by the quality of the data or circumstance that happens to be available. By contrast, we demonstrate that the quantum entropy approach provides a quasi-pointwise estimate, without using averages, allowing for more accurate value determination.

The primary goal of this manuscript was to explore the conceptual and practical connections between economic and quantum value valuation. We then showcased its applicability using relevant examples and applied the theoretical frameworks to practical decision making. It is interesting to note that the inherent subjectivity of valuation, which involves the mechanisms of expectational decisions and informational evaluations, is well-suited to quantum valuation. The classic systems of evaluation, which rely on partially extracting information from PCI observables, fall short of determining the true value state. By contrast, quantum measurement, through the transformation of these PCI observables, has the potential to extract more precise information from PCI, which we show results in a nearly exact value estimation. Our interest in these results will encourage further exploration into whether value itself is inherently quantum. This exploration revealed that the formalism of quantum theory offers both conceptual and practical foundations for describing the subjective experience in the value valuation system.

6. Conclusions

The classic economic systems of evaluation based on PCI methods focus on practical needs, which rely on PCI estimates. Recent efforts in this field have been aimed at improving the technical aspects of measuring components, ignoring the foundational meanings of value valuation systems. This trend has led to a modelling culture that almost prescribes market behaviour within these models, neglecting the genuine impact of individual subjective decisions. Physics, by contrast, focuses on understanding the fundamental properties of matter, relying on rigorous methodology. Both fields, we believe, grapple with the interplay of subjective expectation and information, components compatible with the concept of value state.

Scientific progress is made possible when its practitioners prioritize experimentation, and by extension, are willing to incur risk. By contrast, current economics may have reached the limits of its models, relying on self-referential data. This risk aversion, while it may have been beneficial in the short term, has caused long-term confusion by reducing the accuracy of these models, as exemplified by the outdated concepts and methods of valuation. By mimicking methodologies used in physics, where issues are met with the direct measurement of reality, we can answer seemingly “strange” behaviours of value by considering the characteristics of quantum matter.

A concluding remark can be made on the role that risk plays in commodity value and the decision-making process by economic agents. Economic agents have an inherently conservative risk profile or low tolerance for loss. While we acknowledge everyone’s risk profile is different, we assume that all agents match the appropriate level of risk on either side, buyer, or seller at the moment of transaction. Therefore, for our purposes, we assume that conservative valuation or risky valuation from the observer, before the transaction, will favor the observer as if they were a rational participant in the market. Our method can be refined for better performance and updated with the subjective risk appetite of the evaluator. In our examples, we used historical data on the PCI expressions of the market, which were the average expressions of buyers’ and sellers’ risk profiles. Each participant’s risk appetite was based on their level of knowledge or experience (information), impulsivity, culture, gender, etc. While we acknowledge it is difficult to assess subjective risk, by improving our assessment of risk appetites, as guided by QDT, we are motivated to continue to refine our method’s performance.

Finally, this work is an exploration of how value is fundamentally understood, as well as a call for a broader revaluation of how practitioners understand and measure value in economics. We re-conceptualize how value is assessed by invoking mechanisms used in human judgement, which have been honed over evolutionary history and therefore have a basis in nature. Accordingly, we consider that the value valuation continuum is more than a theoretical construct; it is a practical framework that has the potential to question our approach to economic valuation, offering insights that are as relevant to the academic as they are to the practitioner. While we concede that our primary objective in this work was primarily theoretical, we propose that valuation decisions can be considered in an alternative way if we factor quantum physics theory into traditional systems. The results of the method we developed can be used in practice by experts who aim to predict economics after they have compared them to the traditional triadic methods of valuation. The method we proposed can also be used by cities that must calculate the accurate property values, notably for taxation purposes. The quantum value state is not only accurate in the short term but it also considers the long-term evolution of the whole market based on historical data trends. By bridging the gap between quantum physics and economics, we pave the way for more innovative, accurate, and meaningful approaches to understanding the essence of value and its measure in our ever-evolving economic landscape.

Funding

This research received no external funding.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The author declares no conflict of interest.

References

- Harrigan, N.; Spekkens, R.W. Einstein, Incompleteness, and the Epistemic View of Quantum States. Found. Phys. 2010, 40, 125–157. [Google Scholar] [CrossRef]

- Poudel, R.C. A unified science of matter, life and evolution. Philos. Trans. R. Soc. A 2023, 381, 20220291. [Google Scholar] [CrossRef] [PubMed]

- Spekkens, R.W. Evidence for the epistemic view of quantum states: A toy theory. Phys. Rev. A 2007, 75, 03210. [Google Scholar] [CrossRef]

- Coles, P.; Kaniewski, J.; Wehner, S. Equivalence of wave–particle duality to entropic uncertainty. Nat. Commun. 2014, 5, 5814. [Google Scholar] [CrossRef] [PubMed]

- Pusey, M.F.; Barrett, J.; Rudolph, T. On the reality of the quantum state. Nat. Phys. 2012, 8, 475–478. [Google Scholar] [CrossRef]

- Knee, G.C. Towards optimal experimental tests on the reality of the quantum states. New J. Phys. 2017, 21, 023004. [Google Scholar] [CrossRef]

- Floridi, L. The Philosophy of Information; Oxford University Press: Oxford, UK, 2011. [Google Scholar]

- Leifer, M.S. ψ-Epistemic Models are Exponentially Bad at Explaining the Distinguishability of Quantum 33 States. Phys. Rev. Lett. 2014, 112, 160404. [Google Scholar] [CrossRef]

- Ringbauer, M.; Duffus, B.; Branciard, C.; Cavalcanti, E.G.; White, A.G.; Fedrizzi, A. Measurements on the reality of the wave function. Nat. Phys. 2015, 11, 249–254. [Google Scholar] [CrossRef]

- Kahneman, D.; Tvrersky, A. Prospect Theory: An Analysis of Decision under Risk. Econometrica 1979, 47, 263–292. [Google Scholar] [CrossRef]

- Khrennikov, A. Quantum-like brain: Interference of minds. Biosystems 2006, 84, 225–241. [Google Scholar] [CrossRef]

- Binmore, K. Rational Decisions; Princeton University Press: Princeton, NJ, USA, 2009. [Google Scholar]

- Bruza, P.; Kitto, K.; Nelson, D.; McEvoy, C. Is there something quantum-like about the human mental lexicon? J. Math. Psychol. 2009, 53, 362–377. [Google Scholar] [CrossRef]

- Lambert, M.A.; Zamir, S.; Zwirn, H. Type indeterminacy: A model of the KT (Kahneman–Tversky)-man. J. Math. Psychol. 2009, 53, 349–361. [Google Scholar] [CrossRef]

- Van den Noort, M.; Lim, S.; Bosch, P. On the need to unify neuroscience and physics. Neuroimmunol Neuroinflamm. 2016, 3, 271. [Google Scholar] [CrossRef]

- Bond, R.L.; He, Y.-H.; Ormerod, T.C. A quantum framework for likelihood ratios. Int. J. Quantum Inf. 2018, 16, 1850002. [Google Scholar] [CrossRef]

- Tversky, A.; Kahneman, D. Extensional versus intuitive reasoning: The conjunction fallacy in probability judgment. Psychol. Rev. 1983, 90, 293–315. [Google Scholar] [CrossRef]

- Khrennikov, A. Ubiquitous Quantum Structure: From Psychology to Finances; Springer: Berlin/Heidelberg, Germany, 2010; ISBN 978-3-642-42495-3. [Google Scholar]

- Busemeyer, J.R.; Bruza, P.D. Quantum Models of Cognition and Decision; Cambridge University Press: Cambridge, UK, 2012. [Google Scholar]

- Pothos, E.M.; Busemeyer, J.R. Can quantum probability provide a new direction for cognitive modeling. Behav. Brain Sci. 2013, 36, 255–274. [Google Scholar] [CrossRef] [PubMed]

- Wang, Z.; Busemeyer, J.R.; Atmanspacher, H.; Pothos, E.M. The potential of using quantum theory to build models of cognition. Topics Cogn. Sci. 2013, 5, 672–688. [Google Scholar] [CrossRef]

- Khrennikov, A. Contextual Approach to Quantum Formalism; Fundamental Theories of Physics; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2009; Volume 160, ISBN 978-1-4020-9592-4. [Google Scholar]

- Busemeyer, J.R.; Pothos, E.; Franco, R.; Trueblood, J.S. A quantum theoretical explanation for probability judgment ‘errors’. Psychol. Rev. 2011, 118, 193–218. [Google Scholar] [CrossRef]

- Shimony, A. Search for a Naturalistic World View: Volume II, Natural Science and Metaphysics; Cambridge University Press: Cambridge, UK, 1993. [Google Scholar]

- Von Neumann, J. Mathematical Foundations of Quantum Mechanics; Princeton University Press: Princeton, NJ, USA, 1932. [Google Scholar]

- Wigner, E.P. Remarks on the mind-body questions. In Symmetries and Reflections, Scientific Essays; Wigner, E.P., Ed.; Indiana University Press: Bloomington, IN, USA, 1967; pp. 171–184. [Google Scholar]

- Jabs, A. A conjecture concerning determinism, reduction, and measurement in quantum mechanics. Math. Found. 2016, 3, 279–292. [Google Scholar] [CrossRef]

- Faye, J. Copenhagen Interpretation of Quantum Mechanics. The Stanford Encyclopedia of Philosophy; Zalta, E.N., Ed.; Metaphysics Research Lab, Stanford University: Stanford, CA, USA, 2019. [Google Scholar]

- Penrose, R. Shadows of the Mind: A Search for the Missing Science of Consciousness; Oxford University Press: Oxford, UK, 1996. [Google Scholar]

- Gibbs, J.W. Elementary Principles in Statistical Mechanics; Charles Scribner’s Sons: New York, NY, USA, 1902. [Google Scholar]

- Jaynes, E.T. Information Theory and Statistical Mechanics. Phys. Rev. Ser. I 1957, 106, 620–630. [Google Scholar] [CrossRef]

- Bohr, N. The Quantum of Action and the Description of Nature; Cambridge University Press: Cambridge, UK, 1934; Volume 17. [Google Scholar]

- Dirac, P.A.M. A new notation for quantum mechanics. In Mathematical Proceedings of the Cambridge Philosophical Society; Cambridge University Press: Cambridge, UK, 1939; Volume 35, pp. 416–418. [Google Scholar]

- Schrödinger, E. What Is Life? Cambridge University Press: Cambridge, UK, 1944. [Google Scholar]

- Akerlof, G. The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism. Quar. J. Econ. 1970, 84, 488–500. [Google Scholar] [CrossRef]

- Wigner, E.P. Quantum Theory and Measurement; Wheeler, J.A., Zurek, W.H., Eds.; Princeton University Press: Princeton, NJ, USA, 1983; pp. 260, 325. [Google Scholar]

- Jung, C.G.; Pauli, W. Atom and the Archetype: Pauli/Jung Letters, 1932–1958; Meier, C.A., Ed.; Princeton University Press: Princeton, NJ, USA, 2001. [Google Scholar]

- Busemeyer, J.R.; Wang, Z.; Townsend, J.T. Quantum dynamics of human decision-making. J. Math. Psychol. 2006, 50, 220–241. [Google Scholar] [CrossRef]

- Manousakis, E. Founding quantum theory on the basis of consciousness. Found. Phys. 2006, 36, 795. [Google Scholar] [CrossRef]

- Stapp, H.P. Mindful Universe: Quantum Mechanics and the Participating Observer; Springer: Berlin, Germany, 2007. [Google Scholar]

- Asano, M.; Basieva, I.; Khrennikov, A.; Ohya, M.; Tanaka, Y. A quantum like model of selection behavior. J. Math. Psychol. 2017, 78, 2–12. [Google Scholar] [CrossRef]

- Pothos, E.M.; Busemeyer, J.R. Quantum cognition. Annu. Rev. Psychol. 2022, 73, 749–778. Available online: https://en.wikipedia.org/wiki/Quantum_cognition (accessed on 1 December 2023). [CrossRef] [PubMed]

- Deutsch, D.L. Quantum theory of probability and decision. Proc. R. Soc. A 1999, 455, 3129–3137. [Google Scholar] [CrossRef]

- Favre, M.; Wittwer, A.; Heinimann, H.R.; Yukalov, V.I.; Sornette, D. Quantum Decision Theory in Simple Risky Choices. PLoS ONE 2016, 11, e0168045. [Google Scholar] [CrossRef] [PubMed]

- Yukalov, V.I. Evolutionary Processes in Quantum Decision Theory. Entropy 2020, 22, 681. [Google Scholar] [CrossRef]

- Hameroff, S.; Marcer, P. Quantum Computation in Brain Microtubules? The Penrose—Hameroff ‘Orch OR’ Model of Consciousness. Philos. Trans. Math. Phys. Eng. Sci. 1998, 356, 1869–1896. [Google Scholar]

- Hameroff, S.; Penrose, R. Consciousness in the universe—A review of the Orch OR Theory. Phys. Life Rev. 2014, 11, 39–78. [Google Scholar] [CrossRef]

- Vincent, S.; Kovalenko, T.; Yukalov, V.I.; Sornette, D. Calibration of Quantum Decision Theory, Aversion to Large Losses and Predictability of Probabilistic Choices. 2016. Available online: http://ssrn.com/abstract=2775279 (accessed on 28 October 2023).

- Yukalov, V.I.; Sornette, D. Quantum Probabilities as Behavioral Probabilities. Entropy 2017, 19, 112. [Google Scholar] [CrossRef]

- Abel, C.R. The quantum foundations of utility and value. Philos. Trans. R. Soc. A 2023, 381, 20220286. [Google Scholar] [CrossRef]

- Baaquie, B.E. Quantum Finance; Cambridge University Press: Cambridge, UK, 2004. [Google Scholar]

- Zhang, C.; Huang, L. A quantum model for the stock market. Phys. A 2010, 389, 5769–5775. [Google Scholar] [CrossRef]

- Athalye, V.; Haven, E. Causal viewpoint and ensemble interpretation: From physics to the social sciences. Philos. Trans. R. Soc. A 2023, 381, 20220279. [Google Scholar] [CrossRef]

- Özdilek, Ü. Value Is a (Quantum) State. J. Creat. Value 2020, 6, 34–46. [Google Scholar] [CrossRef]

- Heisenberg, W. The Physical Principles of the Quantum Theory; Dover Publications: New York, NY, USA, 1927. [Google Scholar]

- Beum, A.; Mackmin, D. The Income Approach to Property Valuation; Routledge: London, UK, 1989. [Google Scholar]

- Wiltshaw, D.G. Econometric, linear programming and valuation. J. Prop. Res. 1991, 8, 123–132. [Google Scholar] [CrossRef]

- Richard, M.B.; Silas, J.E. Basic Real Estate Appraisal, 4th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 1998. [Google Scholar]

- Marshall, A. Principles of Economics, 8th ed.; MacMillan Company Ltd.: London, UK, 1890. [Google Scholar]

- Hurd, R.M. Principles of City Land Values; The Record and Guide: New York, NY, USA, 1903. [Google Scholar]

- Babcock, F.M. The Appraisal of Real Estate; The Macmillan Company: New York, NY, USA, 1924. [Google Scholar]

- Bonbright, J.C. The Valuation of Property: A Treatise on the Appraisal of Property for Different Legal Purposes; McGraw-Hill: New York, NY, USA, 1937. [Google Scholar]

- Ratcliff, R.U. Modern Real Estate Valuation, Theory and Application; Democrat Press: Santa Rosa, CA, USA, 1965. [Google Scholar]

- Wendt, P.F. Real Estate Appraisal: A Critical Analysis of Theory and Practice; Holt: New York, NY, USA, 1956. [Google Scholar]

- Burton, J.H. Evolution of the Income Approach, Chicago; American Institute of Real Estate Appraisers: Chicago, IL, USA, 1982. [Google Scholar]

- Cannon, M.Y. The role of the real estate appraiser and assessor in valuing real property for ad valorem assessment purposes. Apprais. J. 2002, 70, 214–219. [Google Scholar]

- Özdilek, Ü. Scientific basis of value and valuation. J. Rev. Pricing Manag. 2019, 18, 266–277. [Google Scholar] [CrossRef]

- Clapp, J.M.; Giaccotto, C. Evaluating house price forecasts. J. Real Estate Res. 2002, 24, 1–25. [Google Scholar] [CrossRef]

- Joslin, A. An investigation into the expression of uncertainty in property valuation. J. Prop. Invest. Financ. 2005, 23, 269–285. [Google Scholar] [CrossRef]

- Sirmans, S.G.; Macpherson, D.A.; Zietz, E.N. The Composition of Hedonic Pricing Models. J. Real Estate Lit. 2005, 13, 3–43. [Google Scholar] [CrossRef]

- Landreth, H.; Colander, D.C. History of Economic Thought, 4th ed.; Houghton Mifflin Company: Boston, MA, USA, 2002. [Google Scholar]

- Robinson, J. Economic Philosophy; Aldine: Chicago, IL, USA, 1962. [Google Scholar]

- Jia, T.; Macare, C.; Desrivières, S.; Gonzalez, D.A.; Tao, C.; Ji, X.; Ruggeri, B.; Nees, F.; Banaschewski, T.; Barker, G.J.; et al. Neural basis of reward anticipation and its genetic determinants. Proc. Nat. Acad. Sci. USA 2016, 113, 3879–3884. [Google Scholar] [CrossRef]

- Arrow, K.J. Uncertainty and the Welfare Economics of Medical Care. Am. Econ. Rev. 1963, 53, 941–973. [Google Scholar]

- Georgescu-Roegen, N. The Entropy Law and the Economic Process; Harvard University Press: Cambridge, MA, USA, 1971. [Google Scholar]

- Appraisal Institute. The Appraisal of Real Estate; Appraisal Institute: Chicago, IL, USA, 2020. [Google Scholar]

- Pagourtzi, E.; Assimakopoulos, V.; Hatzichristos, T.; French, N. Real estate appraisal: A review of valuation methods. J. Property Inv. Fin. 2003, 21, 383–401. [Google Scholar] [CrossRef]

- Mooya, M.M. Real Estate Valuation Theory; Springer: Berlin, Germany, 2018. [Google Scholar] [CrossRef]

- Mundy, B. The Scientific Method and the Appraisal Process. Apprais. J. 1992, 60, 493–499. [Google Scholar]

- Hodges, M.B. Three Approaches? Apprais. J. 1993, 75, 553–564. [Google Scholar]

- Westphal, M.; Brannath, W. Evaluation of multiple prediction models: A novel view on model selection and performance assessment. Stat. Meth. Med. Res. 2020, 29, 1728–1745. [Google Scholar] [CrossRef]

- Rothe, S.; Kudszus, B.; Söffker, D. Does Classifier Fusion Improve the Overall Performance? Numerical Analysis of Data and Fusion Method Characteristics Influencing Classifier Fusion Performance. Entropy 2019, 21, 866. [Google Scholar] [CrossRef]

- Case, K.E.; Robert, J.S. The efficiency of the market for single-family homes. Am. Econ. Rev. 1989, 79, 125–137. [Google Scholar]

- Shimizu, C.; Nishimura, K.G.; Asami, Y. Search and Vacancy Costs in the Tokyo Housing Market: An Attempt to Measure Social Costs of Imperfect Information. Rev. Urban Reg. Dev. Stud. 2004, 16, 210–230. [Google Scholar] [CrossRef]

- McMillen, D.P. Changes in the Distribution of House Prices over Time: Structural Characteristics, Neighborhood, or Coefficients? J. Urb. Econ. 2008, 64, 573–589. [Google Scholar] [CrossRef]

- Nielsen, M.A.; Isaac, C. Quantum Computation and Quantum Information, Repr. ed.; Cambridge University Press: Cambridge, UK, 2001; p. 700. ISBN 978-0-521-63503-5. [Google Scholar]

- Gonchenko, S.V.; Gonchenko, A.S.; Ovsyannikov, I.; Turaev, D.V. Examples of Lorenz-like Attractors in Hénon-like Maps. Mat. Model. Nat. Phenom. 2013, 8, 48–70. [Google Scholar] [CrossRef]

- Cini, M.; De Maria, M.; Mattioli, G.; Nicolo, F. Wave packet reduction in quantum mechanics: A model of a measuring apparatus. Found. Phys. 1979, 9, 479–500. [Google Scholar] [CrossRef]

- Horváth, I. The Measure Aspect of Quantum Uncertainty, of Entanglement, and the Associated Entropies. Quantum Rep. 2021, 3, 534–548. [Google Scholar] [CrossRef]

- Basieva, I.; Khrennikova, P.; Pothos, E.M.; Asano, M.; Khrennikov, A. Quantum-like model of subjective expected utility. J. Math. Econ. 2018, 78, 150–162. [Google Scholar] [CrossRef]

- Pothos, E.M.; Busemeyer, J.R. A quantum probability explanation for violations of the ‘rational’ decision theory. Proc. R. Soc. B 2009, 276, 2171–2178. [Google Scholar] [CrossRef]

- Butto, N. The Origin and Nature of the Planck Constant. J. High Energy Phys. Gravit. Cosmol. 2021, 7, 324–332. [Google Scholar] [CrossRef]

- Özdilek, Ü. The Role of Thermodynamic and Informational Entropy in Improving Real Estate Valuation Methods. Entropy 2023, 25, 907. [Google Scholar] [CrossRef]

- Facchi, P.; Gramegna, G.; Konderak, A. Entropy of Quantum States. Entropy 2021, 23, 645. [Google Scholar] [CrossRef]

- Shiller, R.J. Irrational Exuberance, 3rd ed.; Princeton University Press: Princeton, NJ, USA, 2015. [Google Scholar]

- GeoGebra: In Wikipedia. Available online: https://es.wikipedia.org/wiki/GeoGebra#:~:text=Es (accessed on 20 December 2023).

- Lorenz, E.N. Deterministic Nonperiodic Flow. J. Atmos. Sci. 1963, 20, 130–141. [Google Scholar] [CrossRef]

- Özdilek, Ü. Value order in disorder. Int. J. Dyn. Control 2022, 10, 1395–1414. [Google Scholar] [CrossRef]

- Geller, M.R. Proposal for a Lorenz qubit. Sci. Rep. 2023, 13, 14106. [Google Scholar] [CrossRef]

- Dehaene, S.; Brannon, E. Space, Time and Number in the Brain: Searching for the Foundations of Mathematical Thought; Elsevier Science: Amsterdam, The Netherlands, 2011. [Google Scholar]

- Hodgson, D. Art, perception and information processing: An evolutionary perspective. Rock Art Res. 2000, 17, 3–34. [Google Scholar]

- Kim, P. Energy conservation theory for second language acquisition (ECT-L2A): A partial validation of kinetic energy–aptitude and motivation. Front. Phys. 2023, 11, 1166949. [Google Scholar] [CrossRef]

- Özdilek, Ü. Art Value Creation and Destruction. Integr. Psychol. Behav. Sci. 2023, 57, 796–839. [Google Scholar] [CrossRef]

- Kumar, A.; Sarovar, M. Shining light on data: Geometric data analysis through quantum dynamic. arXiv 2022, arXiv:2212.00682v2. [Google Scholar]

Figure 1.

(a) Value state components, (b) PCI representations.

Figure 2.

(a) PCI spherical coordinates, (b) Quantum 2D basis of PCI.

Figure 3.

(a) Historical evolution of PCI in the United States; (b) Butterfly effect of PCI estimates.

Figure 3.

(a) Historical evolution of PCI in the United States; (b) Butterfly effect of PCI estimates.

Figure 4.

(a) Value state as an attroctor point, (b) Basin of potential value states.

Figure 5.

Evolution of entropies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Main steps of quantum value state computations.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Price | Cost | Income | Pnorm | Cnorm | Inorm | α | β | θ | ρ | dPCI | ||||||

| 1 | 234,509 | 202,654 | 199,670 | 0.525 | 0.836 | 0.926 | 1.242 | 0.538 | 0.883 | 0.476 | 0.608 | 0.370 | 0.303 | 0.368 | 0.670 | 47,207 |

| 2 | 240,700 | 202,940 | 195,996 | 0.579 | 0.838 | 0.909 | 1.246 | 0.558 | 0.893 | 0.471 | 0.622 | 0.394 | 0.295 | 0.367 | 0.662 | 58,518 |

| 3 | 230,328 | 202,179 | 197,442 | 0.490 | 0.833 | 0.916 | 1.223 | 0.526 | 0.868 | 0.482 | 0.589 | 0.380 | 0.312 | 0.368 | 0.679 | 43,289 |

| 4 | 241,611 | 201,513 | 204,618 | 0.587 | 0.828 | 0.946 | 1.272 | 0.553 | 0.905 | 0.467 | 0.634 | 0.348 | 0.289 | 0.367 | 0.656 | 54,556 |

| 5 | 243,420 | 200,942 | 215,313 | 0.603 | 0.824 | 0.979 | 1.301 | 0.555 | 0.915 | 0.458 | 0.652 | 0.309 | 0.279 | 0.363 | 0.642 | 50,936 |

| 6 | 219,572 | 200,751 | 219,664 | 0.402 | 0.823 | 0.988 | 1.254 | 0.492 | 0.853 | 0.475 | 0.587 | 0.286 | 0.313 | 0.358 | 0.671 | 18,821 |

| 7 | 222,662 | 199,515 | 222,759 | 0.427 | 0.813 | 0.993 | 1.260 | 0.493 | 0.854 | 0.473 | 0.592 | 0.281 | 0.311 | 0.357 | 0.667 | 23,147 |

| 8 | 251,408 | 198,183 | 226,217 | 0.672 | 0.804 | 0.997 | 1.329 | 0.570 | 0.936 | 0.446 | 0.676 | 0.290 | 0.265 | 0.359 | 0.624 | 58,885 |

| 9 | 282,051 | 199,705 | 232,263 | 0.904 | 0.815 | 1.000 | 1.424 | 0.673 | 1.079 | 0.410 | 0.780 | 0.302 | 0.193 | 0.362 | 0.555 | 96,227 |

| 10 | 320,414 | 199,515 | 243,265 | 0.995 | 0.813 | 0.992 | 1.457 | 0.716 | 1.147 | 0.399 | 0.818 | 0.315 | 0.164 | 0.364 | 0.528 | 143,417 |

| 12 | 362,000 | 341,000 | 358,000 | 1.000 | 1.000 | 1.000 | 1.538 | 0.796 | 1.301 | 0.377 | 0.894 | 0.315 | 0.101 | 0.364 | 0.464 | 21,378 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Özdilek, Ü. Quantum Value Valuation Continuum. Quantum Rep. 2024, 6, 74-89. https://0-doi-org.brum.beds.ac.uk/10.3390/quantum6010006

AMA Style

Özdilek Ü. Quantum Value Valuation Continuum. Quantum Reports. 2024; 6(1):74-89. https://0-doi-org.brum.beds.ac.uk/10.3390/quantum6010006

Chicago/Turabian StyleÖzdilek, Ünsal. 2024. "Quantum Value Valuation Continuum" Quantum Reports 6, no. 1: 74-89. https://0-doi-org.brum.beds.ac.uk/10.3390/quantum6010006