Estimating the Efficiency and Impacts of Petroleum Product Pricing Reforms in China

1

College of Resources and Environmental Sciences, Hunan Normal University, Changsha 410081, Hunan, China

2

Institute of Finance and Economics Research, School of Urban and Regional Science, Shanghai University of Finance and Economics, Shanghai 200433, China

3

China Center for Energy Economics Research, School of Economics, Xiamen University, Xiamen 361005, Fujian, China

*

Authors to whom correspondence should be addressed.

Sustainability 2018, 10(4), 1080; https://0-doi-org.brum.beds.ac.uk/10.3390/su10041080

Submission received: 22 February 2018

/

Revised: 28 March 2018

/

Accepted: 3 April 2018

/

Published: 4 April 2018

Abstract

:The efficiency and effects analysis of a new pricing mechanism would have significant policy implications for the further design of a pricing mechanism in an emerging market. Unlike most of the existing literature, which focuses on the impacts to the macro-economy, this paper firstly uses an econometrics model to discuss the efficiency of the new pricing mechanism, and then establishes an augmented Phillips curve to estimate the impact of pricing reform on inflation in China. The results show that: (1) the new pricing mechanism would strengthen the linkage between Chinese oil prices and international oil prices; (2) oil price adjustments are still inadequate in China. (3) The lag in inflation is the most important factor that affects inflation, while the impact of the Chinese government’s price adjustments on inflation is limited and insignificant. In order to improve the efficiency of the petroleum products pricing mechanism and shorten lags, government should shorten the adjustment period and diminish the fluctuation threshold.

1. Introduction

At the present stage of development, economic growth in China is facing the constraints of energy supply and environmental degradation, as well as energy demand rigidity, which results from the processes of industrialization and urbanization. In order to form a reasonable and effective “energy triangle” equilibrium relationship (The concept of “energy triangle” is proposed in the “Global Energy Architecture Performance Index Report 2013” by the World Economic Forum. The energy triangle means to promote economic growth in an environmentally-friendly way, to supply energy to human beings, and to ensure energy security) and to solve the contradiction between economy, energy, and environment, it is necessary to reform the energy pricing mechanism [1]. Moreover, the quest for energy subsidies reform that have resulted from global climate change will also promote energy price reform in China. The Chinese government has paid special attention to energy pricing mechanism reform. The State Council regarded price reforms of resource products as a top priority for economic innovation, which has been written into the “Government Work Report” for several years.

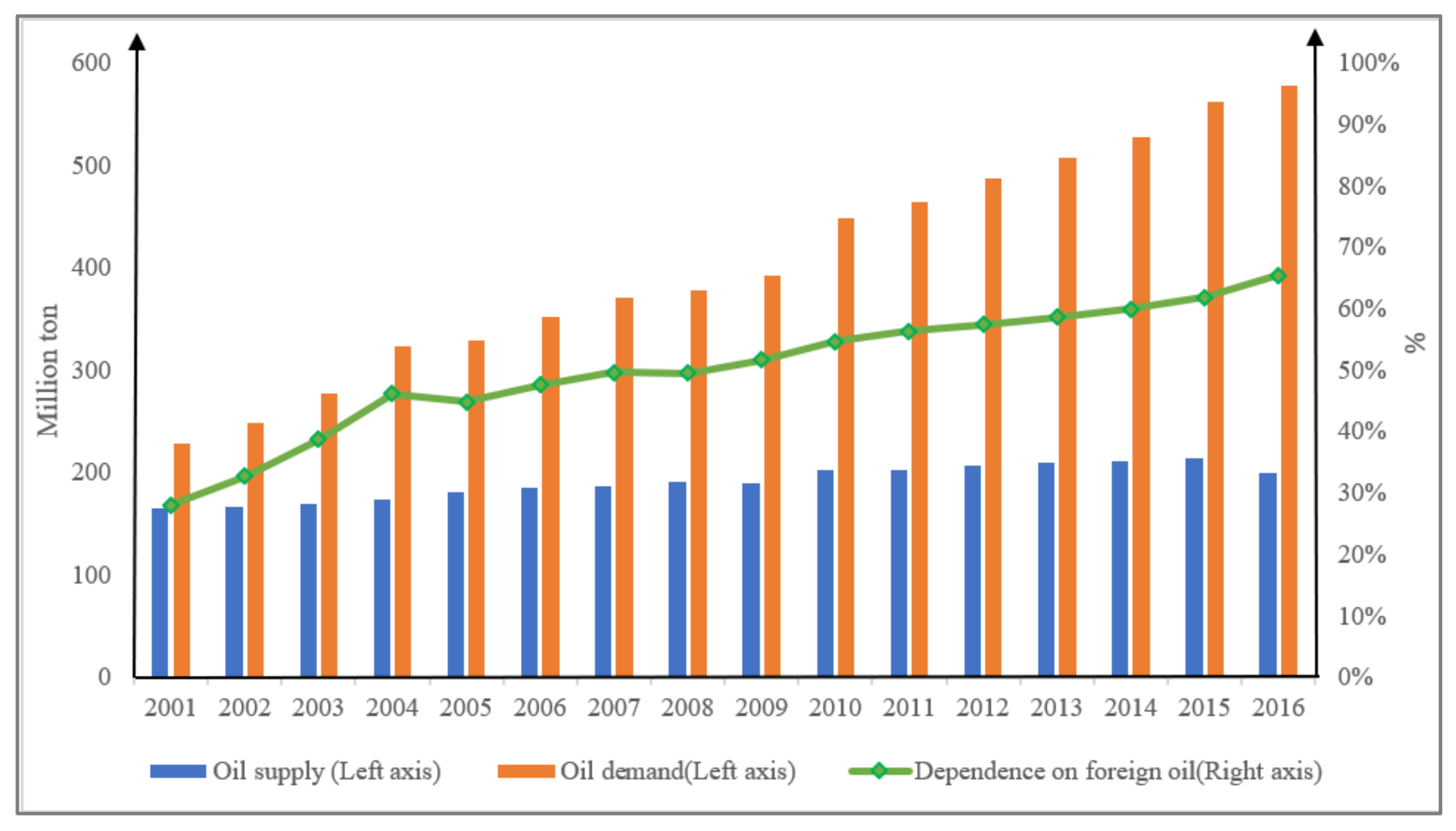

Petroleum is an important resource that relates economic development and strategic security in China [2]. In the past ten years, the annual growth rate of petroleum consumption in China has reached 6.7%, and the consumption level is only second to that of the U.S. The dependence on foreign oil was approximately 60% in 2014 (Figure 1). According to “The Development Report of Oil and Gas Industry Domestic and Overseas in 2011”, dependence on foreign oil will reach 67% in 2020 and 70% in 2030, which indicates that petroleum security is facing a serious challenge in China.

As the largest developing country in the world, China’s economic structure is out of balance to a certain extent and the financial system is not sound enough. What is more, we have not established a mature oil futures market and our ability to resist risk is weak. To ensure sound and rapid economic growth, it is vital for China to implement the oil reform program cautiously. As we all know, oil is the blood of industrial development and a sharp fluctuation on oil prices will affect economic development [3]. Therefore, the Chinese government (National Development and Reform Commission) has been in charge of oil price reform from 2003 to now.

With the increase in dependence on foreign oil in China, Chinese prices of petroleum products are potentially influenced by international oil prices. Among all energy price reforms, petroleum products price reform may be the most significant. From May 2009, the Chinese government began to adopt the new petroleum products pricing mechanism. When the average prices of international crude oil exceed 4% within 22 successive weekdays, the prices of Chinese petroleum products should be adjusted accordingly. However, the contradiction between supply and demand of petroleum products often occurs after implementing this mechanism, since the oil pricing mechanism is so rigid that the speculators could calculate the price of oil through the mechanism. If speculators predict that oil price will go up, they will store more oil before the price adjustment. Similarly, if they predict that oil price will fall, they will reduce their current oil consumption and store more oil after the price adjustment. This makes the supply and demand of oil imbalanced, which may lead to a sharp fluctuation of oil price. Furthermore, it has adverse impact on the development of the manufacturing industry and the macro-economy. What is the performance of the new petroleum products pricing mechanism? Is it effective or not? And why? What is the impact of this mechanism on the Chinese economy? All of these issues should be solved for further petroleum products price reform. Therefore, it is imperative to conduct an in-depth study on the petroleum products pricing mechanism in China. In this paper, we try to estimate the effectiveness and effect of the petroleum products pricing reform, and provide some theoretical basis and decision-making reference for the further pricing reform and design in China. This paper differs from the previous one in the following points: Firstly, it seems that less attention has been paid to the price of petroleum products and it is seldom a separate issue in China. Hence, we try to estimate the effectiveness and effect of the petroleum products pricing reform separately. Secondly, unlike most of the existing literature, which focuses on the impact on the macro-economy, we discuss the effectiveness and effect of the petroleum products pricing mechanism quantitatively. Thirdly, we also study the relationship between petroleum products prices and inflation of the macro-economy, and establish an augmented Phillips curve to estimate the impacts of price reform on inflation.

The remainder of this paper is organized as follows: Section 2 reviews the related literatures. Section 3 applies an econometric model to test the influences of the existing pricing mechanism on the relationship between Chinese petroleum products prices and world oil prices. Section 4 analyzes the effectiveness of the new pricing mechanism. Section 5 estimates the impact of oil price change on inflation under the framework of the augmented Phillips curve. Section 6 provides conclusions and policy suggestions.

2. Literature Review

Researchers have been interested in investigating oil price volatility and shocks for a long time. Studies find that there is a long-term relationship between oil prices and petroleum products prices [4,5]. According to the “Rockets and Feathers Hypothesis” (RFH) firstly termed by Bacon [6], the transmission mechanism of positive and negative changes in the price of oil to the price of gasoline/diesel is asymmetric. Many studies find that the responses of petroleum products price to increases in crude oil price are quicker than a crude oil price decrease [7,8,9,10,11,12,13,14] and the asymmetric effects are more evident when the oil price shocks are larger [15]. Borenstein and Shepard [16] confirm that asymmetric price adjustments in the gasoline market could be attributed to the suppliers’ production adjustment costs. However, the disaggregation of the data allowed the study to show that the asymmetry is not a national problem [17]. Some other studies show that there is no evidence of price asymmetry [18,19,20,21,22]. On the same topic Venditti [23] found that there is some compelling evidence of asymmetries in the adjustment of retail gasoline prices for the U.S. but such evidence appears to be quite mixed for the Euro area. In addition, Brewer et al. [24] links asymmetric price responses directly to firm profits and characterizes the economic significance of asymmetric pricing in the retail gasoline industry.

Price control has been proved to drive the petroleum price to increase [25,26], and the petroleum products pricing mechanisms in most countries have transformed from price control mechanisms into market competition mechanisms. However, in developing countries, oil price is often controlled by the government. A review carried out by the IMF finds that, among 48 developing and emerging economies under consideration, only 16 countries have implemented a liberalized pricing mechanism, nine countries set prices according to an automatic formula, and 16 other countries directly control and adjust the prices on an ad hoc basis [27]. Coady et al. [28] also find that up to mid-2008, the level of pass-through of international oil price variation was very low in many emerging and developing countries. In Indonesia, during 2004–2008, the pass-through of international prices to domestic gasoline and diesel prices was estimated to be 57.9% and 58.8%, respectively, and only 20.9% to kerosene price [29]. However, Dedeoğlu and Kaya [30] identified an increasing trend in the pass-through of oil prices to domestic prices in Turkey.

Many studies related to oil price in China are focused on the macroeconomic effects of oil price shocks, and many empirical researches support that there exists a strong relationship between oil price shock and the macroeconomy in China [3,31,32,33,34]. Zhao et al. [35] established a dynamic stochastic general equilibrium (DSGE) model and found that oil supply shocks mainly produced shorter effects on China’s output and inflation, and demand shocks that were specific to the crude oil market contributed the most to the fluctuations in China’s output and inflation.

It seems that less attention has been paid to the petroleum products price and seldom is it taken as a separate issue in China. However, it is very important for the further improvement of the pricing mechanism, which would affect the economy to some extent [36]. Therefore, unlike most of the existing literature, which focuses on the impact on the macro-economy, in this paper we discuss the effectiveness and effect of the petroleum products pricing mechanism quantitatively in China, and investigate the petroleum products pricing mechanism firstly based on an econometrics model. As gasoline and diesel oil are the main petroleum products, and data of gasoline and diesel oil are readily available, the petroleum products discussed in this paper indicate gasoline and diesel oil.

3. The Influences of Petroleum Products Price Fluctuation

3.1. The History of Domestic and Foreign Petroleum Products Pricing Mechanism

As Table 1 shows, before 1998, the central government implemented the Chinese oil price. And the Chinese government started the market-oriented reform of the petroleum products pricing mechanism in 1998. The process can be divided into three phases approximately:

The first phase (1998–2005): The mechanism suggested that domestic petroleum products prices should be adjusted according to the international petroleum products prices. The government-guided prices were adopted.

The second phase (2006–2008): The government decided to adjust the domestic petroleum products prices according to international crude oil prices. The government set the average crude oil prices of Brent, Dubai, and Cinta as the benchmark price, and then added costs, reasonable profits and tariffs to obtain the basic oil price. However, as the international prices increased rapidly, the petroleum products pricing mechanism established in 2006 was not fully implemented.

The third phase (2008–): From 8 May 2009, the new petroleum products pricing mechanism was put into operation. The core of the new mechanism is “22 weekdays + 4%”. On 26 March 2013, the government improved the petroleum products pricing mechanism, in which the price adjustment period transferred from 22 weekdays to 10 weekdays, and the amplitude constraint was eliminated.

In Table 2, we conclude the oil pricing policy of Japan, US, and South Korea. With an abundant oil resource, the US implemented a relative liberal oil pricing policy except during the first oil crisis stage.

However, the oil resources endowment of Japan was so poor that they tried many mechanisms to improve their pricing system and ensure energy security. Korea’s oil resources endowment and the reform of their oil pricing mechanism was similar to Japan.

3.2. The Relationship between Domestic Petroleum Products Prices and International Oil Prices

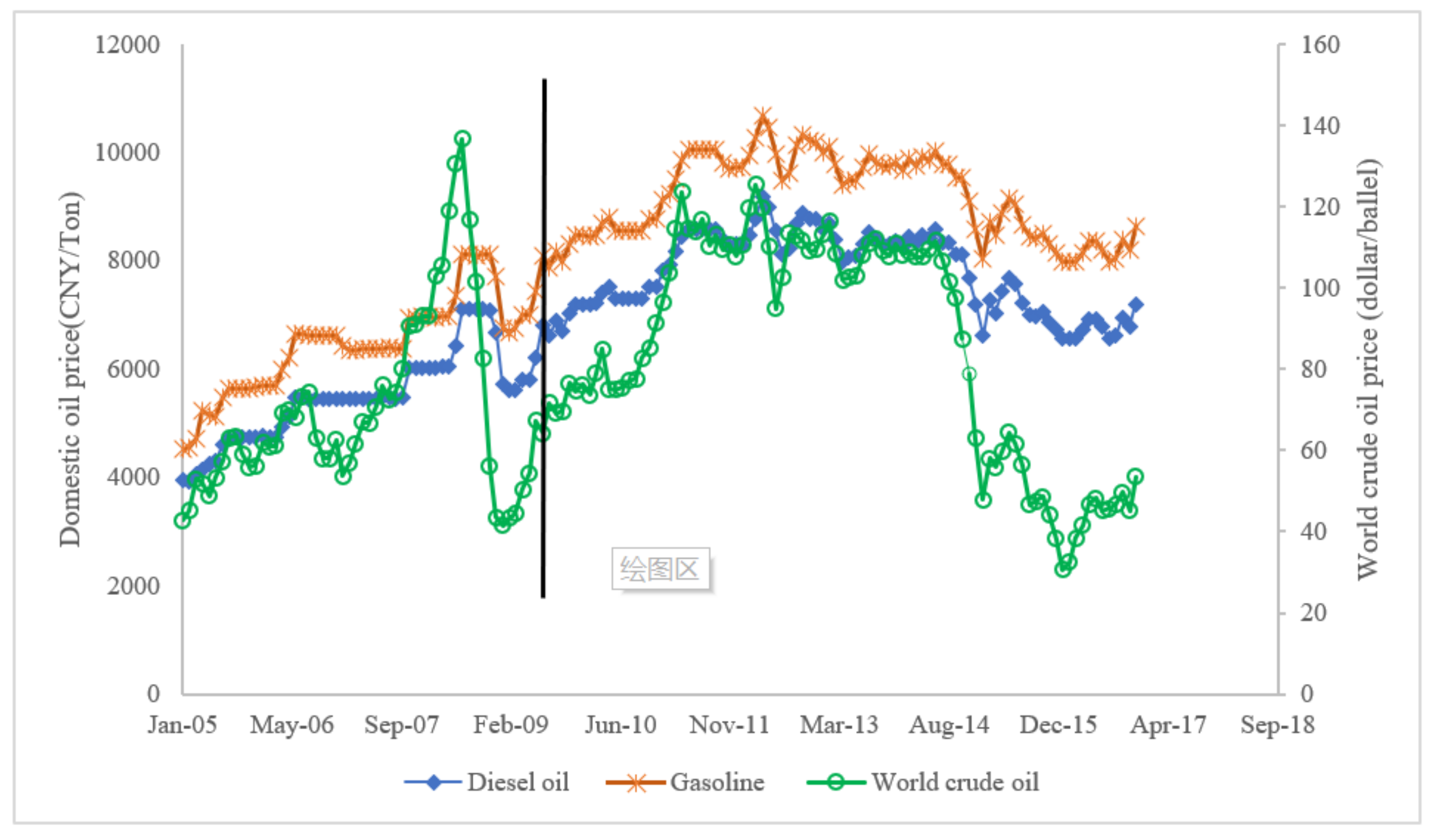

Before the existing pricing mechanism was adopted, domestic gasoline and diesel oil prices changed with international oil prices, but at a much slower speed. The deviation between these two, in terms of both timing and degree, was most dramatic when international oil prices rose sharply and reached its historical high in June 2008 and then dropped dramatically within the following six months, while the domestic gasoline and diesel oil prices rose and dropped only modestly [37]. The price changes taken by the governments are characterized by low frequency, small fluctuation, and long lag. Under the existing pricing mechanism, the fluctuation trend of domestic petroleum products prices is generally consistent and closed with the changes in international crude oil prices, and it has become more responsive to international oil price change over time (Figure 2).

However, Figure 2 also indicates that there still exists a lag in domestic petroleum products prices adjustments. According to the pricing mechanism, the adjustment benchmark is the moving average of oil prices in 22 weekdays, which means that the minimum adjustment interval of domestic petroleum products prices will be 30 days. This design would inevitably weaken the wave crest and wave trough. On the other hand, considering the negative impacts of oil price fluctuation, the government will interfere with the pricing mechanism. All of this will lead to the lag in the pass-through of international oil price variation to China’s domestic petroleum products prices. The following part of this paper will apply an econometric model to test the influence of the existing pricing mechanism on the relationship between international crude oil prices and domestic petroleum products prices.

3.3. The Influences of the Pricing Mechanism

In order to analyze the influences of the existing pricing mechanism on the relationship between international oil price and Chinese petroleum products prices, it is necessary to compare their relationship before and after implementing the pricing mechanism. The econometric model is established as follows:

where is the retail price of domestic petroleum products; is the international crude oil price; L indicates logarithm.

The choice of the time intervals before and after the pricing mechanism is based on the time of the reform. The existing pricing mechanism was implemented on 8 May 2009. So the time interval before the pricing mechanism is from 2005 M1 to 2009 M5, while the time interval after the pricing mechanism is from 2009 M6 to 2013 M6. The international crude oil price is the weighted average of crude oil prices in Brent, Dubai, and Cinta. As the weights are not announced clearly in the pricing mechanism, we choose 1/3 as the weight for each type of price. The international crude oil prices are obtained from Energy Information Administration (EIA), the gasoline and the diesel prices are obtained from the CEIC China Economic Database.

We first verify the stationary properties by unit root texts. The result of the augmented Dickey–Fuller (ADF) test is presented in Table 3.

The ADF test indicates that the prices of domestic diesel, gasoline, and international crude oil are non-stationary, but the first difference of the series is stationary. We then apply the maximum likelihood method to conduct the cointegration test. The results are shown in Table 4.

Table 4 shows that there is long-term relationship between domestic gasoline price and international crude oil prices, while no long-term relationship can be observed between domestic diesel oil price and international oil price. The cointegration coefficient of gasoline before implementing the existing pricing mechanism (0.219) is smaller than that after the implementation (0.405). The result indicates that the existing pricing mechanism could strengthen the relationship between gasoline price and world oil price, yet has no obvious effects on the relationship between diesel oil price and world oil prices.

4. The Frequency and Amplitude of Petroleum Products Prices Adjustment

The analyses above show that the existing petroleum products pricing mechanism strengthens (could strengthen) the linkage between domestic petroleum products prices and international crude oil prices. However, because of government interference, mechanism defects, and the drawbacks of the mechanism, there is still a time lag in China’s domestic petroleum products price adjustment. This section will analyze the efficiency of the existing pricing mechanism from two sides: price adjustment frequency and amplitude.

4.1. The Price Adjustment under the Petroleum Products Pricing Mechanism

4.1.1. The Frequency of Petroleum Products Prices Adjustments

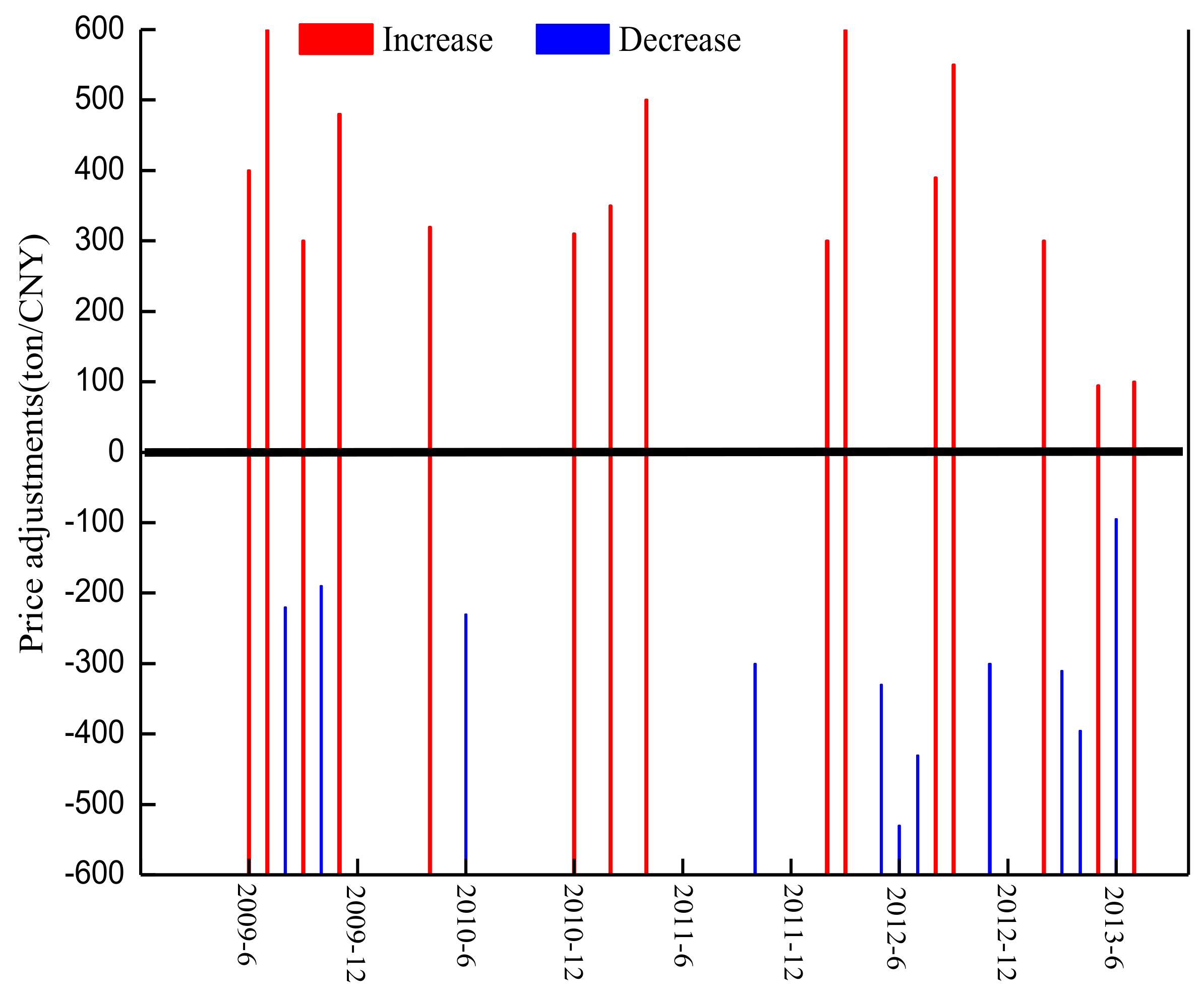

Reviewing the process of oil pricing reform, from 2009 to 2013, the Chinese government adopted the “4% + 22 weekdays” oil pricing mechanism. The purpose for writing this paper is to estimate the efficiency of petroleum product pricing reforms in China. Therefore, we used the data from 2009 to 2013 to conduct the statistical analysis instead of newer data to study the effects of oil pricing reform in this phase. According to the announcement published by the National Development and Reform Commission (NDRC), we find that from 8 May 2009, when the existing petroleum products pricing mechanism was adopted until the second quarter of 2013, the prices of Chinese petroleum products have been adjusted 27 times, among which 16 times are increments and 11 times are decrements. In 2009, the prices were adjusted 6 times, 4 times in 2010, 3 times in 2011, 8 times in 2012, and 8 and 6 times in the first two quarters of 2013 (Figure 3).

4.1.2. The Amplitude of Price Adjustments

The amplitude of the price adjustments is an important index that reflects the linkage between domestic and international oil prices, which is usually measured by the index of pass-through. The pass-through is defined as the ratio of the absolute change in the tax-inclusive prices to that of the benchmark price over the same period [28]. The benchmark price generally denotes the international oil prices, which is on a free-on-board basis, excluding net taxes and transportation costs. The pass-through is widely used to analyze the responses of domestic oil price to international price volatility, which could estimate the market degree of oil [28,29]. The formula can be explicitly written as:

where is the pass-through; and are the prices of domestic petroleum products in period and respectively, is the period interval; and are the prices of international petroleum products in period and separately.

Since the petroleum products and crude oil are different kinds of oil, the absolute changes in their prices are different. Therefore, we define the pass-through as the ratio of the variation rate in domestic retail prices to that of world average crude oil prices. The formula is expressed as follows:

The pass-through of international crude oil prices to petroleum products prices can be calculated by Formula (3) and the results are as shown in Table 5.

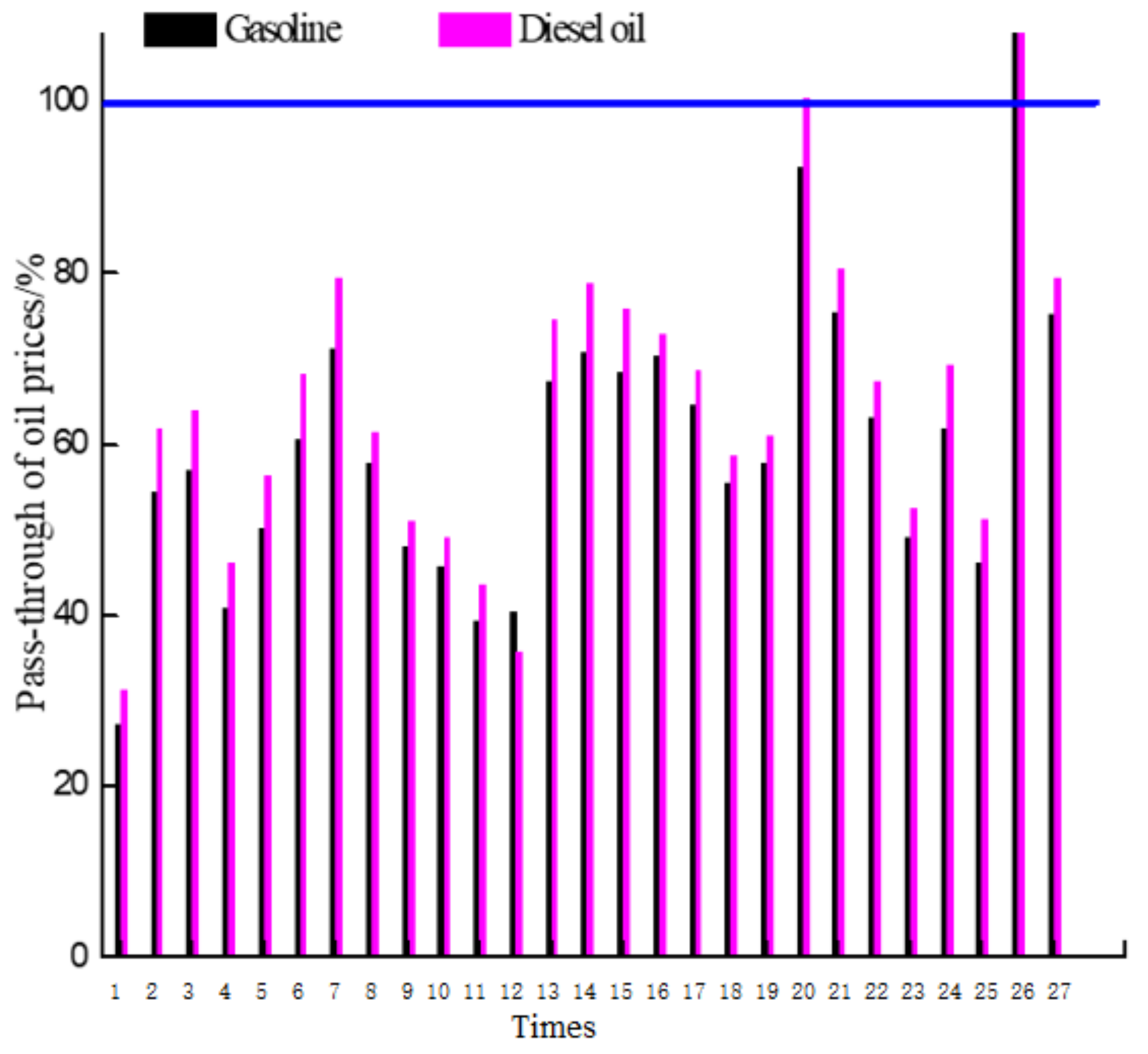

The results in Table 5 show that the price adjustment amplitude of China’s domestic petroleum products is smaller than that of international crude oil prices, except for the price adjustment on 7 June 2013. The change in international oil price is not totally transmitted to the domestic petroleum products price. In addition, the change of international oil price exerts more influence on diesel price than gasoline price (Figure 4).

It is very common for a developing country to regulate petroleum products price. An investigation of 131 countries carried out by the IMF found that the pass-through level of the sharp rise in international prices was very low in many emerging and developing countries. In terms of gasoline and diesel oil, about two-thirds and one-half of countries, respectively, failed to transmit an international price increase completely [28]. The price control, usually in the form of suppressing the price of domestic petroleum products (i.e., energy subsidies), has some positive effects on promoting economic development and alleviating energy poverty by providing access to affordable modern energy services. However, subsidies on petroleum products tend to be regressive, high-income households consume more gasoline and diesel oil. The distributional effect of removing subsidies for petroleum products is progressive [38].

4.2. The Price Adjustments of Petroleum Products without Government Intervention

As a pricing mechanism is not the unique criterion for price adjustment, the government will take some other factors into account when adjusting price. In order to analyze the difference between the theoretical and the actual operation of the existing mechanism, this paper will further analyze the supposed frequency and amplitude of price adjustments if the existing pricing mechanism is strictly followed. Due to the lack of a explicit rule about the price adjustment amplitude, it is supposed that the government follows the fluctuation amplitude of international petroleum price. The results are shown in Table 6.

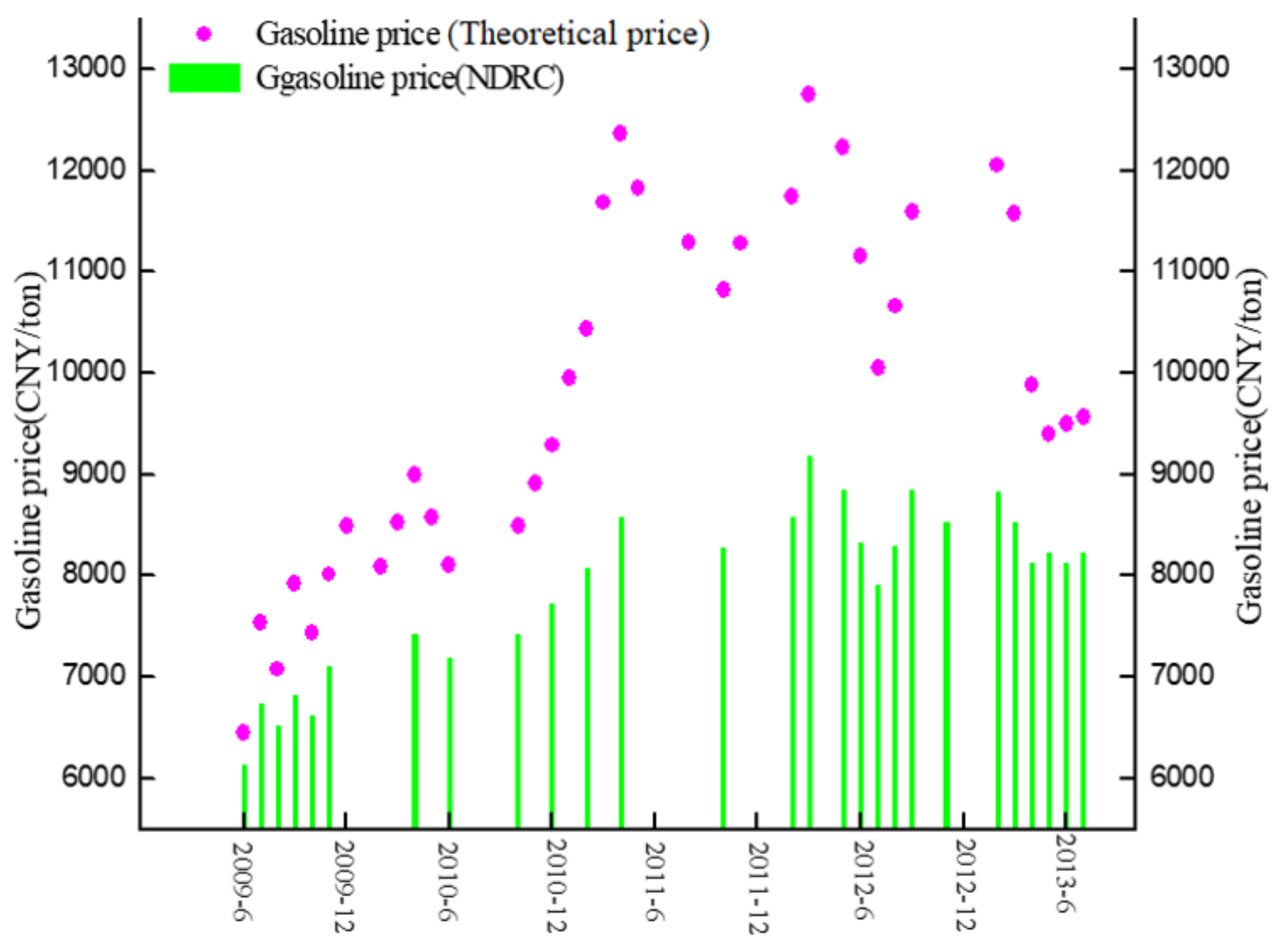

If the Chinese government had adjusted the prices strictly according to the existing petroleum products pricing mechanism, the adjustment frequency would have been higher (Figure 5). From the implementation of the existing pricing mechanism to the end of June, 2013, the price should have been adjusted 38 times, 11 times more than the actual situation. In the adjustments, there should be 23 price increments, 7 times more than the actual situation, and 15 price decrements, 4 times more than the actual situation. The reason why the actual price increase is less frequent may lie in the administrative operation. On the one hand, the decision-making of a price adjustment would result in the adjustment lag. On the other hand, in order to avoid the influences of an oil price increase on the general price level and economy, the government may postpone or call-off some price increases. In addition, there are another two reasons. Firstly, the international crude oil price has showed a long-term growing trend, increasing from about $40 per barrel at the beginning of 2009 to nearly $120 per barrel in February, 2012. Secondly, it is easier for price to surpass the upward threshold than to drop below the downward threshold. Therefore, the “rockets and feathers” phenomenon in China’s petroleum products price adjustments is not only caused by the characteristic of oil price fluctuation, but also by the deficiency of the pricing mechanism. From 2009 to 2013, the NDRC implemented the “22 weekdays + 4%” oil pricing mechanism. If the original price is 100 yuan per ton and the international oil price rises 4 yuan per ton in 22 working days, then the price is adjusted to 104 yuan per ton. When the international oil price starts to fall, we assume that we can adjust the price if the oil price falls 4 yuan, but in fact, it should decrease 4.16 to reach the limit of 4%. Because of the fixed oil pricing mechanism, the “rockets and feathers” phenomenon happens frequently.

Table 6 also indicates that if the price adjustments strictly follow the existing pricing mechanism, the ex-factory prices of domestic petroleum products would be much higher than the regulated price decided by the NDRC (Figure 5). At the end of June, 2013, the ex-factory prices of gasoline was CNY 9567 per ton, much higher than CNY 8225 per ton, which was adjusted by the government on 22 June 2013. In 2011, the prices of Chinese petroleum products should have been increased by 20%, and the gasoline price should have been increased by CNY 1700 per ton. However, considering the pressure on the general price level, the petroleum products prices were only adjusted two times for price increase and experienced one period of price reduction, and the accumulative price changes were CNY 550 per ton for gasoline. Therefore, the existing pricing mechanism could not enhance the conductivity between domestic petroleum products prices and world crude oil prices effectively.

5. The Impacts of Petroleum Products Price Adjustments on Inflation

There is a consensus among economists that changes in oil prices can exert significant influences on inflation [39,40,41]. The petroleum products pricing mechanism reform, which pushes up the price, may affect CPI by pushing up price. This is one of the reasons that the government controls the price adjustment amplitudes and postpones the adjustment. The rest of this paper will analyze the impacts of the petroleum products price adjustments on inflation by the augmented Phillips curve model.

5.1. The Augmented Phillips Curve Model

The Phillips curve is a classical model used to study inflation, and the augmented Philips curve is widely used to estimate the level of global oil prices that transmits to the inflation rate. Hooker [42] identifies a structural break in the U.S. Phillips curve and found that oil price pass-through has become negligible since 1980. LeBlanc and Chinn [43] adopt a similar Phillips curve framework to analyze the data from G5 countries, and obtain similar findings. They find that the current oil price increase is likely to have a modest effect on inflation in the U.S., Japan, and Europe. According to their study, a 10 percent increase in oil price would lead to a direct inflationary increase of about 0.1–0.8 percent in the U.S. and the E.U. Chen [44] uses this model to investigate oil price pass-through to inflation in 19 industrialized countries and finds the pass-through of oil prices to domestic prices to be unstable over time and declining recently. Chou and Tseng [45] also find that international oil price has a significant and long-term pass-through effect on inflation in Taiwan, while the short-term pass-through effect is not significant. As suggested by Hooker [42], a typical augmented Philips curve can be presented as:

where refers to the inflation rate, is the output, is the Hodrick-Prescott filtered trend of , is the output gap; is the average global crude oil prices; is a first-order difference equation. Since the Chinese government does not announce the core inflation rate, the GDP deflator index or CPI are usually used to replace the inflation rate. However, the GDP deflator index cannot measure the price changes of final products, so CPI is a better proxy. This paper uses the change rate of CPI () to measure inflation ().

In order to analyze the impact of petroleum products price adjustment on inflation, a price adjustment is introduced into the augmented Philips curve as a variable. As the price of petroleum products is controlled by the government, this variable is not continuous. The variable of the price adjustment is set as a dummy variable .

In addition, many studies find that the impact of oil price fluctuations on the economy is asymmetric. The economy is more responsive to increases in oil prices than to unexpected price decreases. Therefore, two dummy variables D1 and D2 are introduced in the former Equation (5), to represent the price rise and price reduction, respectively. Then we obtain Equation (6):

where

Chen [44] points out that there might be a long-run equilibrium for oil price, CPI, and output. The co-integration model is established as follows:

where coefficient refers to full pass-through in the long term. Moreover, to illustrate the information concerning the long-run equilibrium relationship, an error correction model of the augmented Phillips curve is estimated as follows:

where is the error correction term, ; is the adjustment coefficient in the error correction model, measuring the required adjustment for long-term equilibrium from short-term disequilibrium.

5.2. The Empirical Results

5.2.1. Data Resource

The data used in this study is based on monthly data from 2005 M1 to 2013 M6. In general, GDP is the most commonly used variable to represent output. However, this variable is presented quarterly in China. Chou and Tseng [45] use the producer’s price, including the industrial producing index for manufacture production, as a proxy variable for output. But it might not be proper to use the relative variable of index to replace the absolute variable of GDP in China. We reckon the industrial value could be added as a better proxy for GDP. Given the weight of industrial output in GDP, this measurement should serve as a good proxy for the overall output of the Chinese economy while resulting in a rich variation, given its monthly frequency [37]. The international crude oil price is the weighted average of prices of Brent, Dubai, and Cinta. The international oil prices are obtained from the EIA and data for the other variables are obtained from the CEIC China Economic Database.

5.2.2. The Results of the Model

The ADF test indicates that not all the variables are non-stationary, but the first difference of the series is stationary. Then, the maximum likelihood method is used to conduct the cointegration test. The result shows that at the 5% significance level, there is no long-run equilibrium relationship among the inflation rate, output, and international oil prices (Table 7).

Table 7 also indicates that the error correction model of the augmented Phillips curve is not reasonable. The augmented Phillips curve used is presented in Formula (6). According to the information rules of AIC and SC, the best lag order is first order, k = 1. The results are as follows (Table 8).

The results show that the stickiness of inflation is the main factor affecting inflation in the short-term. The lag of oil price fluctuation has little influence on inflation rate, and it is not significant even at a 10% significance level. Some studies support the idea that the volatility in oil prices do not seem to be contagious for the volatility in overall inflation [42,46]. Cavalcanti and Jalles [47] find that oil price shocks accounted for a very small fraction of the inflation and output growth rate volatility in Brazil. The significantly positive effects of the oil price shock are only on energy-intensive CPIs [48]. Zhang and Xie [37] pointed out that the basic features of the Chinese economy, with coal as the dominant source of energy, might be the main reason why the economy is robust in the face of oil price shock, domestic or international. In addition, the transportation fuel expenditure only accounts for 8% of the total inflation in China. Table 6 also shows that there are two characteristics of the coefficient of price adjustments. The first is the coefficient of price increase is negative while that of price decrease is positive, which is contrary to expectation. The possible reason may be due to the nature of the mechanism itself. The time lag of price pass-through is longer than one month, due to the government’s price control, especially when there is over-capacity in the industry. Secondly, the price adjustment has little or even negligible impact on inflation. Therefore, the price adjustment of petroleum products, whether it is an increase or a decrease, cannot affect the price level significantly. Zhang and Xie [37] also find that the effect of the mechanism on the Chinese economy was very limited.

6. Conclusions and Suggestions

6.1. Conclusions

The new petroleum products pricing mechanism is regarded as a breakthrough in China’s domestic oil pricing reform. This paper applied an econometric model to discuss the efficiency of the new pricing mechanism and established an augmented Phillips curve to estimate the impacts of price reform on inflation. The main conclusions can be drawn as follows:

Firstly, the pricing mechanism could strengthen the linkage between gasoline price and international oil prices. However, its effects on the relationship between diesel oil price and world oil prices are not obvious. The development of heavy industry consumes much diesel oil, which means diesel oil is very important for economic development. The sharp fluctuation on diesel price has a great impact on industrial development. As we all know, diesel price will affect the cost of companies. If the government adjusts the diesel oil price frequently, companies will try their best to predict the diesel price. Managers may reduce their time for considering production and innovation, which will affect the development of the companies and the national economies. That is why the government may be more cautious about the reform of diesel price, and China’s diesel price is not as correlated to the world oil price as gasoline.

Secondly, the price adjustment of petroleum products is not adequate. If the government fully followed the pricing mechanism, price adjustments should have been conducted 38 times, 11 times more than the real situation. Of all the theoretical adjustments, 23 times are price increments, 7 times more than the real situation, and 15 times are price reductions, 4 times more than the real situation. In addition, the amplitudes of the government adjustments are much smaller than the fluctuation in international oil prices.

Thirdly, the impact of the government’s price adjustment on inflation, regardless of whether it is an increase or a decrease, is limited and insignificant. The impact of international oil price fluctuation on inflation is also insignificant.

6.2. Policy Implications

The long adjustment interval and government interventions lead to a lag in the pass-through of international oil prices in reality. Shortening the price adjustment period and improving the price adjustment frequency are effective ways to reduce speculation. Furthermore, the government should change the administrative approval pattern to make the pricing mechanism more flexible.

The other deficiency of the existing petroleum products pricing mechanism is the lack of diaphaneity. There are no explicit explanations about the weights of the crude oil prices adopted as the benchmark, as well as the pass-through level. In addition, issues such as oil price choice, price change monitoring, and subsidy scheme design need to be specified.

The impact of petroleum products price adjustment on inflation is an important factor that the government takes into consideration when deciding whether and how to carry out oil price adjustments. In fact, a price adjustment does have some influences on inflation, but the influences are limited. The Group of China’s Growth and Macroeconomic Stability (2008) finds that GDP is still the root cause of inflation and that the impacts of external shocks, such as world oil prices and food prices, are partial and insignificant. Therefore, the government should adjust prices according to the pricing mechanism and avoid external disturbances. Once energy price becomes a macro-policy tool, oil price reform, and even energy price reform, will get stranded due to other economic and social factors. In addition, financial policy, monetary policy, energy policy, the degree of openness and other related factors, will affect the pass-through of world oil prices to domestic inflation. Furthermore, more supplementary measures and policies, such as breaking the monopoly of the oil industry, establishing ordered competition, improving the supervision mechanism and introducing targeted subsidies, should be designed to support the pricing reform of Chinese petroleum products.

This paper also has some limitations. Firstly, we only used the data from 2009 to 2013 to study the effects of oil pricing reform in this phase. Secondly, we did not establish a theoretical model to study the oil pricing mechanism and whether it is effective or not. In the future, we will try our best to solve these problems.

Acknowledgments

The paper is supported by the National Natural Science Foundation of China (71503155 and 71673230), Shanghai Social Science Foundation (2015110478), the National Social Science Foundation Project of China (No. 16BJL063).

Author Contributions

All authors contributed to the model construction. Zhujun Jiang provided the core idea and provided key advice pertaining to the results. Chuxiong Deng wrote the entire manuscript. Chuanwang Sun helped check the manuscript and wrote the policy recommendations.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Buus, T. Energy Efficiency and Energy Prices: A General Mathematical Framework. Energy 2017, 139, 743–754. [Google Scholar] [CrossRef]

- Zhang, K. Target Versus Price: Improving Energy Efficiency of Industrial Enterprises in China; Department of Energy and Mineral Engineering, The Pennsylvania State University: State College, PA, USA, 16 June 2014. [Google Scholar]

- Tang, W.Q.; Wu, L.B.; Zhang, Z.X. Oil price shock and their short-and long-term effects on the Chinese economy. Energy Econ. 2010, 32, S3–S14. [Google Scholar] [CrossRef]

- Gjølberg, O.; Johnsen, T. Risk management in the oil industry: Can information on long-run equilibrium prices be utilized? Energy Econ. 1999, 21, 517–527. [Google Scholar] [CrossRef]

- Asche, F.; Gjolberg, O.; Volker, T. Price relationships in the petroleum market: An analysis of crude oil and refined product prices. Energy Econ. 2003, 25, 289–301. [Google Scholar] [CrossRef]

- Bacon, R.W. Rockets and feathers: The asymmetric speed of adjustment o tail gasoline prices to cost changes. Energy Econ. 1991, 13, 211–218. [Google Scholar] [CrossRef]

- Borenstein, S.; Cameron, A.C.; Gilbert, R. Do gasoline prices respond asymmetrically to crude oil price changes? Q. J. Econ. 1997, 112, 305–339. [Google Scholar] [CrossRef]

- Balket, N.S.; Brown, S.P.A.; Yucel, M.K. Crude oil and gasoline prices: An asymmetric relationship? Econ. Financ. Policy Rev. 1998, 1, 2–11. [Google Scholar]

- Tappata, M. Rockets and feathers: Understanding asymmetric pricing. RAND J. Econ. 2009, 40, 673–687. [Google Scholar] [CrossRef]

- Douglas, C. Do gasoline prices exhibit asymmetry? Not usually! Energy Econ. 2010, 32, 918–925. [Google Scholar] [CrossRef]

- Peltzman, S. Prices rise faster than they fall. J. Polit. Econ. 2000, 108, 466–502. [Google Scholar] [CrossRef]

- Chou, K.W.; Sun, S.H. Crude oil prices, exchange rates, and the asymmetric response of retail gasoline prices in Taiwan. Br. J. Econ. Financ. Manag. Sci. 2012, 3, 82–91. [Google Scholar]

- Atil, A.; Lahiani, A.; Nguyen, D.K. Asymmetric and nonlinear pass-through of crude oil prices to gasoline and natural gas prices. Energy Policy 2014, 65, 567–573. [Google Scholar] [CrossRef]

- Polemis, M.L.; Tsionas, M.G. An alternative semiparametric approach to the modelling of asymmetric gasoline price adjustment. Energy Econ. 2016, 56, 384–388. [Google Scholar] [CrossRef]

- An, L.; Jin, X.Z.; Ren, X.M. Are the macroeconomic effects of oil price shock symmetric? A Factor-Augmented Vector Autoregressive approach. Energy Econ. 2014, 45, 217–228. [Google Scholar] [CrossRef]

- Borenstein, S.; Shepard, A. Sticky prices, inventories, and market power in wholesale gasoline markets. RAND J. Econ. 2002, 33, 116–139. [Google Scholar] [CrossRef]

- Silva, A.S.; Vasconcelos, C.R.F.; Vasconcelos, P.S.; Mattos, R.S. Symmetric transmission of prices in the retail gasoline market in Brazil. Energy Econ. 2014, 43, 11–21. [Google Scholar] [CrossRef]

- Manning, D.N. Petrol Prices, Oil Rises and Oil Price Falls: Some Evidence for the UK Since 1972. Appl. Econ. 1991, 23, 1535–1541. [Google Scholar] [CrossRef]

- Godby, R.; Lintner, A.M.; Stengos, T.; Wandscheider, B. Testing for asymmetric pricing in the Canadian retail gasoline market. Energy Econ. 2000, 22, 349–368. [Google Scholar] [CrossRef]

- Kaufmann, R.K.; Laskowski, C. Causes for an asymmetric relation between the price of crude oil and refined petroleum products. Energy Policy 2005, 33, 1587–1596. [Google Scholar] [CrossRef]

- Kilian, L.; Vigfusson, R. Nonlinearities in the Oil Price-Output Relationship. Macroecon. Dyn. 2011, 15, 337–363. [Google Scholar]

- Greenwood-Nimmo, M.; Shin, Y. Taxation and the asymmetric adjustment of selected retail energy prices in the UK. Econ. Lett. 2013, 121, 411–416. [Google Scholar] [CrossRef]

- Venditti, F. From oil to consumer energy prices: How much asymmetry along the way? Energy Econ. 2013, 40, 468–473. [Google Scholar] [CrossRef]

- Brewer, J.; Nelson, D.M.; Overstreet, G. The economic significance of gasoline wholesale price volatility to retailers. Energy Econ. 2014, 43, 274–283. [Google Scholar] [CrossRef]

- Phelps, C.E.; Smith, R.T. Petroleum Regulation: The False Dilemma of Decontrol; RAND Corporation: Santa Monica, CA, USA, 1977. [Google Scholar]

- Rogers, R.P. The effect of the energy policy and conservation act (EPCA) regulation on petroleum product prices, 1976–1981. Energy J. 2003, 24, 63–94. [Google Scholar] [CrossRef]

- Coady, D.; Kpodar, K.; Gillingham, R.; El-Said, M.; Newhouse, D.L.; Medas, P.A. The Magnitude and Distribution of Fuel Subsidies: Evidence from Bolivia, Ghana, Jordan, Mali, and Sri Lanka; IMF Working Paper 06/247; International Monetary Fund: Washington, DC, USA, 2006. [Google Scholar]

- Coady, D.; Gillingham, R.; Ossowski, R.; Piotrowski, J.; Tareq, S.; Tyson, J. Petroleum Product Subsidies: Costly, Inequitable, and Rising; International Monetary Fund: Washington, DC, USA, 2010. [Google Scholar]

- Mourougane, A. Phasing out Energy Subsidies in Indonesia; Working Papers, No. 808; OECD Economics Department: Paris, France, 2010. [Google Scholar]

- Dedeoğlu, D.; Kaya, H. Pass-through of oil prices to domestic prices: Evidence from an oil-hungry but oil-poor emerging market. Econ. Model. 2014, 43, 67–74. [Google Scholar] [CrossRef]

- Huang, Y.; Guo, F. The role of oil price shocks on China’s real exchange rate. China Econ. Rev. 2007, 18, 403–416. [Google Scholar] [CrossRef]

- Faria, J.R.; Mollick, A.V.; Albuquerque, P.H.; León-Ledesma, M.A. The effect of oil price on China’s exports. China Econ. Rev. 2009, 20, 793–805. [Google Scholar] [CrossRef]

- Beirne, J.; Beulen, C.; Liu, G.; Mirzaei, A. Global oil prices and the impact of China. China Econ. Rev. 2013, 27, 37–51. [Google Scholar] [CrossRef]

- Ju, K.Y.; Zhou, D.Q.; Zhou, P.; Wu, J.M. Macroeconomic effects of oil price shocks in China: An empirical study based on Hilbert-Huang transform and event study. Appl. Energy 2014, 136, 1053–1066. [Google Scholar] [CrossRef]

- Zhao, L.; Zhang, X.; Wang, S.Y.; Xu, S.Y. The effects of oil price shocks on output and inflation in China. Energy Econ. 2016, 53, 101–110. [Google Scholar] [CrossRef]

- Zhang, K.; Olawoyin, R.; Nieto, A.; Kleit, A.N. Risk of commodity price, production cost and time to build in resource economics. Environ. Dev. Sustain. 2017, 2, 1–24. [Google Scholar] [CrossRef]

- Zhang, J.; Xie, M.J. China’s oil product pricing mechanism: What role does it play in China’s macroeconomy? China Econ. Rev. 2016, 38, 209–221. [Google Scholar] [CrossRef]

- Jiang, Z.J.; Ou, Y.X.L.; Huang, G.X. Distributional impacts of the elimination of fossil fuel subsidies. China Econ. Rev. 2015, 33, 111–122. [Google Scholar] [CrossRef]

- Ajmera, R.; Kook, N.; Crilley, J. Impact of commodity price movements on CPI inflation. Mon. Labor Rev. 2012, 29, 29–43. [Google Scholar]

- Bachmeier, L.J.; Cha, I. Why don’t oil shocks cause inflation? Evidence from disaggregate inflation data. J. Money Credit Bank. 2011, 43, 1165–1183. [Google Scholar] [CrossRef]

- Nixon, D.; Smith, T. What Can the Oil Futures Curve Tell Us about the Outlook for Oil Prices; Bank of England Quarterly Bulletin: London, UK, 2012; Volume 52, pp. 39–47. [Google Scholar]

- Hooker, M.A. Are oil shocks inflationary? Asymmetric and nonlinear specifications versus changes in regime. J. Money Credit Bank. 2002, 34, 540–561. [Google Scholar] [CrossRef]

- LeBlanc, M.; Chinn, M.D. Do high oil prices presage inflation? Bus. Econ. 2004, 39, 38–48. [Google Scholar]

- Chen, S.S. Oil price pass-through into inflation. Energy Econ. 2009, 31, 126–133. [Google Scholar] [CrossRef]

- Chou, K.W.; Tseng, Y.H. Pass-through of oil prices to CPI inflation in Taiwan. Int. Res. J. Financ. Econ. 2011, 69, 73–83. [Google Scholar]

- Valcarcel, V.J.; Wohar, M.E. Changes in the oil price-inflation pass-through. J. Econ. Bus. 2013, 68, 24–42. [Google Scholar] [CrossRef]

- Cavalcanti, T.; Jalles, J.T. Macroeconomic effects of oil price shocks in Brazil and in the United States. Appl. Energy 2013, 104, 475–486. [Google Scholar] [CrossRef]

- Gao, L.P.; Kim, H.; Saba, R. How do oil price shocks affect consumer prices? Energy Econ. 2014, 45, 313–323. [Google Scholar] [CrossRef]

Figure 1.

Oil demand and supply in China. Source: The data of oil supply and demand are from the China Statistical Yearbook 2017, the dependence on foreign oil is calculated by the authors.

Figure 1.

Oil demand and supply in China. Source: The data of oil supply and demand are from the China Statistical Yearbook 2017, the dependence on foreign oil is calculated by the authors.

Figure 2.

Trend of world crude oil price and domestic gasoline and diesel price. Notes: (1) The world oil price is the weighted average price of Brent, Dubai, and Cinta; (2) The dotted line indicates the nodal points of implementing the existing petroleum products pricing mechanism. Source: The gasoline and diesel oil prices are obtained from the Wind Database; the world oil prices are obtained from the International Monetary Fund (IMF).

Figure 2.

Trend of world crude oil price and domestic gasoline and diesel price. Notes: (1) The world oil price is the weighted average price of Brent, Dubai, and Cinta; (2) The dotted line indicates the nodal points of implementing the existing petroleum products pricing mechanism. Source: The gasoline and diesel oil prices are obtained from the Wind Database; the world oil prices are obtained from the International Monetary Fund (IMF).

Figure 3.

Price adjustments under the existing pricing mechanism.

Figure 4.

Pass-through of petroleum products prices.

Figure 5.

The contrast of the ex-factory gasoline prices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Oil pricing mechanism reform of China.

| Time | Pricing Mechanism | Illustration |

|---|---|---|

| Before 1982 | Planned price stage | The price is formulated, adjusted, and strictly implemented by the government. |

| 1982–1994 | Two track stage | Many kinds of price forms, such as flat price, high price in plan, high price out of plan, and so on. |

| 1994–1998 | Single price stage | Unified implementation of national pricing. |

| 1998.6–2001.11 | Linked to the Singapore market stage | Adjust the price of gasoline and diesel oil if it has been fluctuated more than 5% of the Singapore market. |

| 2001.11–2006.3 | Multi market linkage stage | Weighted average value of Singapore, Rotterdam and New York market prices (6:3:1). |

| 2008.12.18 | Fuel consumption tax stage | Oil price included fuel consumption tax. |

| 2009.5.7 | 22 weekdays + 4% | Adjust the oil price if the moving average price of crude oil in the international market has changed more than 4% for 22 consecutive weekdays. |

| 2013.3 | 10 weekdays | Adjust the price every 10 weekdays, and cancel the fluctuation range of 4%. |

Data sources: Official website of the national development and Reform Commission.

Table 2.

Oil pricing mechanism reform of foreign countries.

| Countries | Time | Pricing Policy | Illustration |

|---|---|---|---|

| US | Before 1973 | Liberal oil pricing policy. | None restriction. |

| 1973–1981 | Emergency oil distribution act. | The first oil crisis broke out, and the United States government set up a pricing system to control the oil price. | |

| After 1981 | Liberal oil pricing policy. | None restriction. | |

| Japan | 1952–1962 | Restricting oil consumption and considering adjust the dominant energy. | Considering the adjustment of energy strategy. |

| 1962–1972 | Liberalization of oil trade. | Determining oil as the dominant source of energy. | |

| 1973–1985 | Formulating a safety system for oil supply. | Controlling oil consumption and formulating the policy of protecting supply and reducing consumption. | |

| 1986–1995 | Mitigating the control of oil production. | Import liberalization of heavy oil. | |

| 1996–2002 | Mitigating the control of oil circulation. | Releasing the oil export restrictions. | |

| After 2003 | Expanding the ownership of external oil. | To improve energy security. | |

| South Korea | Before 1994 | Administrative pricing policy. | The government implemented the oil pricing policy. |

| 1994 | Linked with international crude oil price. | Oil prices are adjusted on the basis of last month’s import of crude oil. | |

| 1995 | Linked with international price of refined oil. | Domestic oil price was dependent on international refined oil price. | |

| 1996 | The registration management system of the gas station and the examination system of the importer’s qualification. | Controlling oil consumption. | |

| After 1997 | Liberal oil policy. | None restriction. |

Table 3.

The test on the augmented Dickey–Fuller (ADF) unit root of variables.

| Variable | Before a | After b | ||

|---|---|---|---|---|

| Standard Statistics | First Order Difference Statistics | Standard Statistics | First Order Difference Statistics | |

| −2.630 * | −5.184 *** c | −2.267 | −4.862 *** | |

| −2.300 | −4.777 *** | −2.386 | −4.792 *** | |

| −2.679 * | −3.668 *** | −1.815 | −5.904 *** | |

Notes: a the period “before” is from 2005 M1 to 2009 M5; b the period “after” is from 2009 M6 to 2013 M6; c *, **, *** stand for that under the significance levels of 10%, 5% and 1%, respectively; the null hypothesizes are rejected.

Table 4.

The influences of the pricing mechanism on petroleum products price.

| Variable | Before the Implementation | After the Implementation | ||

|---|---|---|---|---|

| Gasoline | Diesel | Gasoline | Diesel | |

| C | 7.928 (20.754) | - | 7.296 (80.176) | - |

| 0.219 (2.406) | - | 0.405 (20.250) | - | |

Note: the figures in the brackets indicate the t statistics.

Table 5.

The pass-through of petroleum products prices.

| Time | Change Rate of International Crude Oil Price a | Gasoline | Diesel | ||

|---|---|---|---|---|---|

| Rate of Change | Rate of Change | ||||

| 2009-6-1 | 0.257 | 0.070 | 0.272 | 0.080 | 0.312 |

| 2009-6-30 | 0.180 | 0.098 | 0.544 | 0.111 | 0.618 |

| 2009-7-29 | −0.058 | −0.033 | 0.568 | −0.037 | 0.638 |

| 2009-9-2 | 0.113 | 0.046 | 0.408 | 0.052 | 0.461 |

| 2009-9-30 | −0.056 | −0.028 | 0.502 | −0.031 | 0.563 |

| 2009-11-9 | 0.120 | 0.073 | 0.604 | 0.082 | 0.680 |

| 2010-4-14 | 0.063 | 0.045 | 0.711 | 0.050 | 0.793 |

| 2010-6-1 | −0.054 | −0.031 | 0.578 | −0.033 | 0.615 |

| 2010-10-26 | 0.067 | 0.032 | 0.479 | 0.034 | 0.510 |

| 2010-12-22 | 0.091 | 0.042 | 0.457 | 0.045 | 0.491 |

| 2011-2-19 | 0.115 | 0.045 | 0.393 | 0.050 | 0.435 |

| 2011-4-7 | 0.153 | 0.062 | 0.404 | 0.055 | 0.356 |

| 2011-10-9 | −0.052 | −0.035 | 0.672 | −0.039 | 0.746 |

| 2012-2-8 | 0.051 | 0.036 | 0.708 | 0.040 | 0.789 |

| 2012-3-20 | 0.102 | 0.070 | 0.683 | 0.078 | 0.758 |

| 2012-5-10 | −0.051 | −0.036 | 0.703 | −0.037 | 0.727 |

| 2012-6-9 | −0.093 | −0.060 | 0.645 | −0.064 | 0.685 |

| 2012-7-11 | −0.091 | −0.050 | 0.555 | −0.053 | 0.585 |

| 2012-8-10 | 0.085 | 0.049 | 0.579 | 0.052 | 0.610 |

| 2012-9-11 | 0.072 | 0.066 | 0.923 | 0.072 | 1.004 |

| 2012-11-16 | −0.047 | −0.035 | 0.754 | −0.037 | 0.804 |

| 2013-2-25 | 0.056 | 0.035 | 0.630 | 0.038 | 0.673 |

| 2013-3-27 | −0.072 | −0.035 | 0.491 | −0.037 | 0.524 |

| 2013-4-25 | −0.075 | −0.046 | 0.618 | −0.052 | 0.691 |

| 2013-5-10 | 0.025 | 0.012 | 0.460 | 0.013 | 0.511 |

| 2013-6-7 | −0.009 | −0.012 | 1.335 | −0.012 | 1.404 |

| 2013-6-22 | 0.016 | 0.012 | 0.752 | 0.013 | 0.794 |

Note: a The world average crude oil price is the average of Brent, Dubai, and Cinta; b The period is from 2009 M5 to 2013 M6 for gasoline and diesel oil.

Table 6.

The theoretical gasoline and diesel oil price (yuan/ton).

| Time | Gasoline | Diesel | Time | Gasoline | Diesel |

|---|---|---|---|---|---|

| 2009-6-1 | 6447 | 5615 | 2011-5-27 | 11,818 | 10,292 |

| 2009-7-1 | 7535 | 6562 | 2011-8-25 | 11,288 | 9830 |

| 2009-7-31 | 7077 | 6163 | 2011-10-18 | 10,825 | 9427 |

| 2009-8-28 | 7915 | 6893 | 2011-11-17 | 11,281 | 9824 |

| 2009-9-30 | 7430 | 6471 | 2012-2-13 | 11,738 | 10,222 |

| 2009-10-30 | 8010 | 6976 | 2012-3-14 | 12,743 | 11,097 |

| 2009-12-1 | 8485 | 7390 | 2012-5-4 | 12,229 | 10,650 |

| 2010-2-15 | 8088 | 7043 | 2012-6-5 | 11,149 | 9709 |

| 2010-3-17 | 8528 | 7427 | 2012-7-5 | 10,046 | 8749 |

| 2010-4-19 | 8994 | 7832 | 2012-8-6 | 10,661 | 9285 |

| 2010-5-25 | 8576 | 7468 | 2012-9-5 | 11,587 | 10,090 |

| 2010-6-24 | 8103 | 7057 | 2013-2-15 | 12,054 | 10,497 |

| 2010-10-6 | 8492 | 7396 | 2013-3-20 | 11,568 | 10,074 |

| 2010-11-5 | 8907 | 7757 | 2013-4-10 | 10,851 | 9450 |

| 2010-12-17 | 9288 | 8089 | 2013-4-24 | 9885 | 8609 |

| 2011-1-20 | 9952 | 8667 | 2013-5-8 | 9401 | 8187 |

| 2011-2-21 | 10,436 | 9088 | 2013-5-22 | 9561 | 8326 |

| 2011-3-23 | 11,681 | 10,172 | 2013-6-5 | 9499 | 8273 |

| 2011-4-21 | 12,360 | 10,764 | 2013-6-19 | 9567 | 8331 |

Table 7.

Johansen cointegration test.

| Number of Cointegrating Equation | Trace Statistic | 5% Critical Value | Max-Eigen Statistic | 5% Critical Value |

|---|---|---|---|---|

| None | 23.582 | 29.797 | 18.557 | 21.132 |

| At most 1 | 5.026 | 15.495 | 4.275 | 14.265 |

| At most 2 | 0.750 | 3.841 | 0.750 | 3.841 |

Table 8.

The impacts of price adjustments on inflation.

| Variables | Coefficient |

|---|---|

| C | 0.045 (0.279) |

| 0.993 (21.784) | |

| (−1) | 0.018 (1.257) |

| −0.026 (−0.918) | |

| 0.026 (0.717) | |

| −0.001 (−1.380) |

Note: the figures in the brackets are t statistics.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Deng, C.; Jiang, Z.; Sun, C. Estimating the Efficiency and Impacts of Petroleum Product Pricing Reforms in China. Sustainability 2018, 10, 1080. https://0-doi-org.brum.beds.ac.uk/10.3390/su10041080

AMA Style

Deng C, Jiang Z, Sun C. Estimating the Efficiency and Impacts of Petroleum Product Pricing Reforms in China. Sustainability. 2018; 10(4):1080. https://0-doi-org.brum.beds.ac.uk/10.3390/su10041080

Chicago/Turabian StyleDeng, Chuxiong, Zhujun Jiang, and Chuanwang Sun. 2018. "Estimating the Efficiency and Impacts of Petroleum Product Pricing Reforms in China" Sustainability 10, no. 4: 1080. https://0-doi-org.brum.beds.ac.uk/10.3390/su10041080

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.