1. Introduction

One of the main tasks of the state economic policy is to ensure the proper level of the population welfare. The solution for this task must be achieved, first of all, through the creation of such economic conditions in which every citizen can independently provide a high standard of his life. However, in any society, there are categories of people who, for various reasons, cannot do this. The state social welfare system is called to solve the problem of life support for such people.

The state social security systems in different countries differ significantly among themselves, in particular, by volume and structure of social expenditures. However, the main sources of formation and directions of financial resources distribution, which are directed towards social protection of the population, in many countries, are largely similar. Similar are the problems which are faced by many countries when organizing the social security of their population. First of all, these problems relate to a lack of funds to finance large-scale social welfare programs, and an increase in the number of people who need social protection [

1].

The increase in potential recipients of state social assistance is conditioned by many different factors: political, economic, demographic, etc. In particular, these factors include the population aging in many countries, level growth of citizens differentiation in terms of their incomes, increased unemployment, the influx of migrants and refugees, and others [

2].

Taking into account the actual tendency to increase the burden on the state social security systems of many countries, it is important to assess the ability of these systems to maintain an adequate level of their sustainability under the influence of various factors. Among these factors we can highlight the labor-saving technological changes in economics that have a direct impact on the unemployment rate and, accordingly, on the size of revenues and expenditures of state social security funds.

At the present time, there are many scientific publications devoted to the study of the regularities of technological changes [

3,

4,

5,

6] and problems of state social security system [

7,

8,

9,

10,

11,

12,

13]. However, the question of assessing the impact of technological changes on the sustainability of state social security systems needs more detailed research. In particular, the mechanism of impact of technological changes is insufficiently investigated and, accordingly, there are the gaps in its quantitative assessment. Accordingly, this situation complicates the development of practical recommendations for ensuring the sustainability of state social security systems of different countries in the context of technological changes in their economies.

Thus, the study of the impact of technological changes on the sustainability of state social security systems requires simultaneous consideration of two scientific areas: the regularities of technological change, and the mechanism of state social security system functioning. In order to establish a link between these two scientific areas, it is appropriate to rely on the concept of considering technological changes as one of the main factors influencing the quality of people’s life. At the same time, such influences can be not only positive, but also negative. In particular, the negative effects of technological changes include the increase of social risks [

14]. At present, the concept of a special role of the state for offseting these risks is generally accepted. The state social security system is built on this concept.

The risk of loss of work has one of the main places among the social risks. There are different opinions in the scientific literature about the possible impact of technological changes on the unemployment rate [

15,

16,

17,

18,

19,

20,

21,

22]. Most scientists believe that there is such possible impact, at least in the short term. However, we do not reject the possible compensatory effects that reduce the level of technological unemployment, in particular, the increasing the demand for workers in those industries that are associated with the manufacture of machine-building products.

Taking into account the above, this research is based on the concept of social security as one of the main functions of the state, and on the consideration of technological changes as a source of social risks, in particular, the risk of loss of work.

The main task of our research was to develop methodological principles for assessing the impact of technological changes on the sustainability of the state social security system. In solving this task, we received several results that have scientific novelty.

Firstly, we investigated the mechanism of the impact of labor-saving technological changes on the sustainability of the state social security system. For this purpose, we analyzed the impact of these changes on the magnitude of revenues and expenditures of state budget, municipal budgets, and state social security funds.

Secondly, we identified the main effects that are conditioned by the impact of labor-saving technological changes on the sustainability of the state social security system. In particular, one of these effects is caused by the growth of natural volumes of production. The second effect is due to the replacement of part of the labor costs by part of the firm’s profits.

Thirdly, we developed an indicator for assessing the impact of labor-saving technological changes on the sustainability of the state social security system, built a model of this indicator, and established the feasibility of its use in management practice.

It should be noted that the question of assessing the impact of technological changes on the sustainability of the state social security system is relevant to many countries of the world. However, it is most important for those countries where, on the one hand, there is a problem with the sustainability of the state social security system, and on the other hand, there are large-scale labor-saving changes, or at least, there is a large potential for such changes in the near future. In particular, these countries include the developing countries. In many of these countries, the level of technological development is still not high; however, there are tendencies to its increase. Among these countries, we can indicate Ukraine.

Ukraine, at the present time, belongs to the countries of the world with the most extreme conditions of its existence. Starting from 2014, military action has been lasting in the eastern region. The government of Ukraine temporarily lost control over part of its territory, and more than a million inhabitants of these areas were forced to move to the territory controlled by the government [

23,

24,

25]. This has caused the additional burden on the state social security system of Ukraine and exacerbated the problem of unemployment. It should be noted that the official unemployment rate among the economically active population of Ukraine is quite high—in the first quarter of 2017, it was 10.1%. At the same time, in the first quarter of 2017, the average unemployment rate in the EU countries was 8.3%, and in the United States, 4.9% [

26].

The stated purpose of this study is an assessment of the technological changes’ impact on the sustainability of the state social security system of Ukraine. The achievement of this purpose has caused the necessity of solving a number of tasks that are described in the relevant parts of this work. Therefore, in Chapter 2, the analysis of literature on the subject of research is conducted. Chapter 3 presents the methodological principles for assessing the impact of technological changes on the sustainability of the state social security system. In Chapter 4, an empirical analysis of this problem was conducted on the example of Ukraine. The Chapter 5 describes the obtained results and summarizes the conclusions from the conducted research.

2. Literature Review

The issue of technological change is at the center of many scientists’ attention, which is conditioned by the significant role played by these changes in the modern economy. In particular, a significant number of publications is devoted to the study of factors that determine these changes and the patterns of their course [

10,

11,

27], the study of the processes of technological innovations’ diffusion, in particular, their spatial distribution [

28,

29,

30,

31,

32,

33,

34,

35,

36,

37], and the impact of technological changes on the competitiveness of products and enterprises. Particular interest belongs to the phenomenon of technological jumps that occurs as a result of the spread of technology innovations between countries [

38]. At the same time, the authors are mainly considering the following types of technological changes: material-saving, energy-saving, labor-saving, and capital-saving, as well as technological changes that lead to improved product quality. Particular attention is paid to energy-saving and productive technological changes, taking into account the influence these changes make on the rates and proportions of economic growth in many countries of the world. In particular, with respect to labor-saving technological changes, researchers have thoroughly described the characteristic features of labor-saving technologies [

16,

17], the essence is investigated, features and conditions of the emergence of economically efficient technological changes, both at the level of individual firms and industries, and the economy as a whole [

18,

39,

40], the tendencies of automation and robotization of production and service delivery processes are considered [

19,

41,

42].

It should be noted that the scale and pace of the new technologies’ introduction are determined by the influence of various factors [

41,

43]. Ultimately, these factors are reflected in the magnitude of the financial results that are obtained by the owners of firms as a result of the replacement of old technologies with new ones. It should be taken into consideration that the introduction of energy-saving and labor-saving technologies often entails the need to invest substantial amounts of investment. Taking this into account, evaluation of the efficiency and feasibility of new technologies introducing by enterprises requires the use of indicators and methods for assessing the effectiveness of investment projects, which are described, in particular, in [

18,

40,

41,

42,

44]. However, specifics of the relevant technological processes should be taken into account, the implementation of which involves investments [

5,

17,

18,

40]. Under these conditions, it is possible to build sufficiently adequate economic and mathematical models of technological change. These models, which in particular are presented in [

5,

31,

33,

34], give an opportunity to explain the technological developments that have taken place in recent years in the economies of different countries, and to assess the impact of technological change on the performance indicators of individual firms and industries and on macroeconomic indicators.

Considering the impact of economically efficient technological changes on key macroeconomic indicators, most researchers are primarily studying the impact of these changes on unemployment. The issue of unemployment is devoted to a significant number of scientific works, in which the authors investigate the nature of this phenomenon [

45,

46,

47,

48], find out its causes [

20,

46,

49], provide a classification of unemployment types [

20,

47,

50,

51], etc. Particular attention is paid to this kind of unemployment, which is directly conditioned by labor-saving technological changes, such as technological unemployment. In the opinion of many authors, there are significant risks that if the current tendency continues to strengthen the automation of production, technological unemployment will increase substantially [

20,

46,

47,

48,

51,

52,

53]. In this regard, scientists offer a variety of recommendations for the state policy improvement of unemployment combating [

21,

53], paying particular attention to the issue of workers redundancy who have lost their jobs [

54,

55,

56,

57,

58].

The growth in the number of people who lost their jobs naturally causes an additional burden on the state social security system. In particular, this is due to the need to pay such unemployment benefits to such people, and to finance expenditures for their retraining. In addition, a decrease in the number of employees entails a reduction in the number of taxpayers on income and contributions to state social insurance funds. It should be noted that the problem of state social security systems’ functioning is considered in many scientific works, in particular [

7,

8,

55,

59,

60,

61,

62,

63,

64,

65,

66,

67,

68,

69,

70]. At the same time, scientists pay special attention to issues of retirement provision [

9,

10,

63,

64,

65,

66,

67,

68,

69,

70,

71,

72] and social protection of the unemployed [

47,

55,

56,

57,

58,

60,

73].

Currently, in many countries, trends in increasing the number of people in need of social protection are growing. As a result, the question of the sustainability assessing of public social security systems is relevant. In general, the theoretical and methodological basis for assessing of the various economic systems’ stability is considered in many scientific works, in particular [

74,

75,

76,

77,

78,

79]. The authors pay special attention to the assessment of the economic stability of individual firms [

75,

76,

80] and the sustainability of economic development of states in terms of resource constraints [

11,

77,

78,

79,

81]. Regarding the sustainability of state social security systems, its evaluation is mainly viewed from the point of view of the deficit of state and municipal budgets, as well as state social insurance funds [

11,

12,

13,

62,

63,

78,

79]. At the same time, the authors identify a variety of factors that influence the formation of such a deficit, including the increase in the number of people who are provided with social security. However, the question of assessing the impact of economically labor-saving technological changes on the sustainability of state social security systems, at present, is not sufficiently researched in scientific literature. Taking into account that this issue is relevant, there is a need for more detailed consideration.

For this purpose, the following main tasks should be solved: to determine the criteria by which the state social security system can be considered as sustainable; to describe the mechanism of the impact of labor-saving technological changes on the sustainability of the state social security system; to substantiate the methodical principles of quantitative evaluation of this impact. In particular, it is important to test the hypothesis that the impact of labor-saving technological changes on the sustainability of the state social security system is always negative.

3. Methodology

3.1. General Approaches to Assessing the Sustainability of the State Social Security System

The assessment of the sustainability of the state social security system should be based on the same principles used in assessing the sustainability of any type of system [

11,

13]. First of all, it is necessary to identify the ability of the state social welfare system to adapt to the possible effects on it, of certain factors. Then, such a system can be considered stable if, as a result of adaptation to external influences, it can continue to function normally. Such an approach to assessing the sustainability of the state social security system makes it possible to establish its stability with respect to a certain level of external influence. At the same time, a situation is possible in which this system will be stable at a certain relatively small level of influence on it, however, at a stronger level of influence, the system will be unstable.

In general, the state social security system is characterized by three main groups of parameters: the amount of revenues from the funds from which public expenditure on social security is financed; number of persons—recipients of social assistance in terms of categories of such persons; social expenditure norms, which in most cases are set per person, depending on the category to which it belongs. Then, the state social security system can be considered stable in relation to the influence on it of a certain factor, if under such influence, this system will continue to pay social assistance in appropriate amounts to all categories of persons in accordance with the requirements established by legislative and regulatory acts.

From the point of view of ensuring the stability of the state social security system, the negative impact of factors that reduce the number of taxpayers and contributions to state social insurance is particularly negative [

9,

12,

79]. The situation is even more complicated if the former taxpayer and contributor becomes a social security recipient.

One of the possible ways of adapting the state social security system to the influence of a certain factor is redistribution of social expenditures coming from one or another monetary fund. Social payments to the population may be made at the expense of the funds of the state social insurance funds (in particular, the pension fund), as well as at the expense of state and municipal budgets. The influence of a certain factor on the state social security system can lead to a reduction in revenues to state social insurance funds, but to increase the revenues to state or municipal budgets. Then, due to redistribution of social expenditures between different funds, the level of social security may remain unchanged or even increase. An example of such a redistribution is the coverage of the state pension fund deficit at the expense of the state budget.

Another way of adapting the state social security system to the impact of a certain factor is to reduce administrative costs for the functioning of public institutions that organize such provisions.

If, due to the effect of a certain factor, the state social security system is not able to fully perform its functions, then it is necessary to look for additional reserves to increase the stability of this system. These reserves should be divided into internal and external ones. Internal reserves for improving the sustainability of the state social security system are in the middle of the country, and external reserves provide for assistance from other countries or from international financial institutions. In particular, the internal reserves of the sustainability of the state social security system may include changes in the structure of state and municipal budgets, in order to increase the share of social expenditures, as well as a certain increase in the rates of certain taxes and contributions to state social insurance.

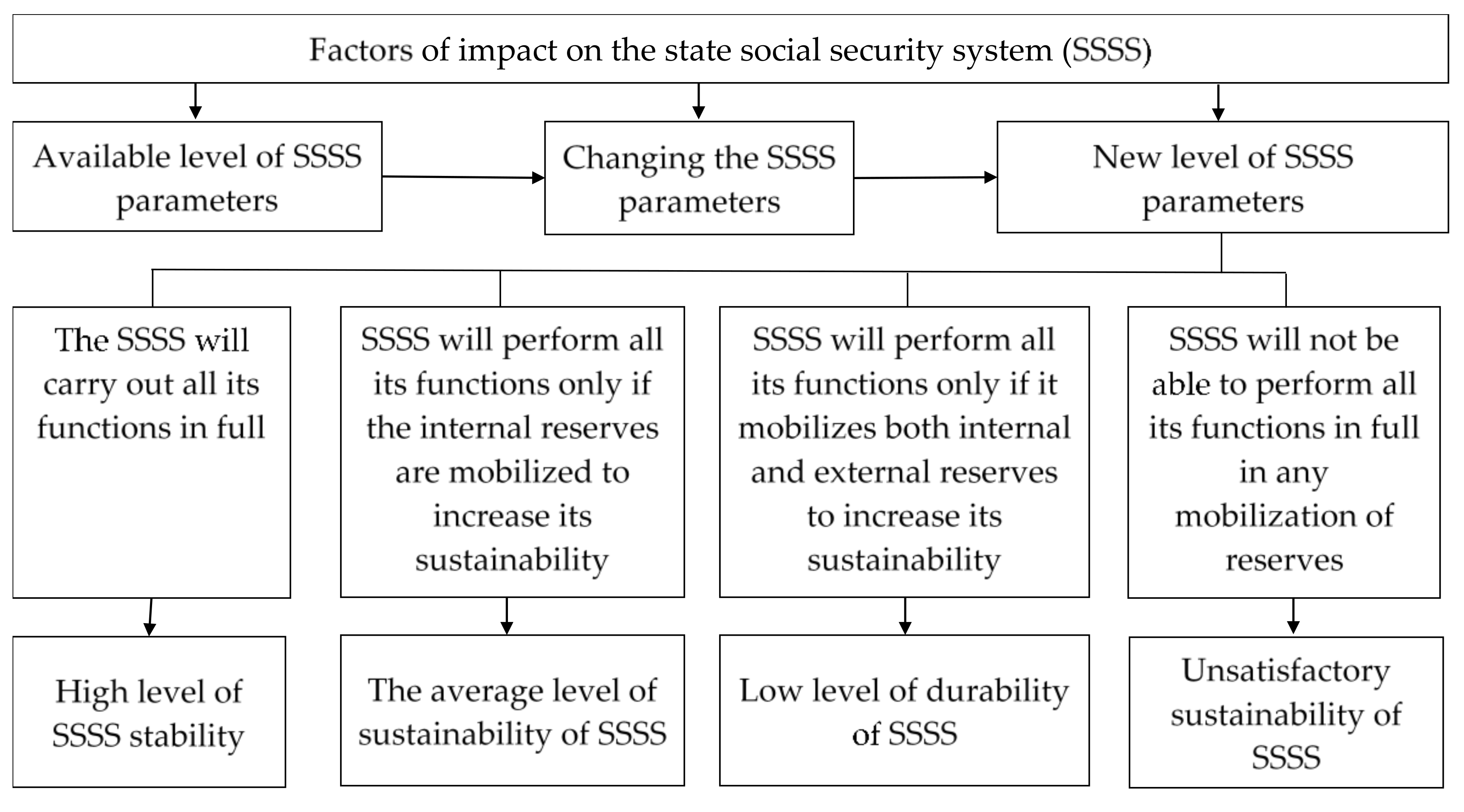

Taking into account the above, there is an opportunity to perform a qualitative gradation of the level of stability of the state social security system, as presented in

Figure 1.

As it follows from

Figure 1, it is appropriate to highlight the following levels of stability of the state social security system: high, medium, low, and unsatisfactory. At the same time, the unsatisfactory level of stability of the state social security system means that this system will not be able to function properly if it has some external influence. Under these circumstances, changes will be required in legislative and regulatory acts, in particular, in order to reduce the list of categories of people who can count on social security and reduce the standards of such provision.

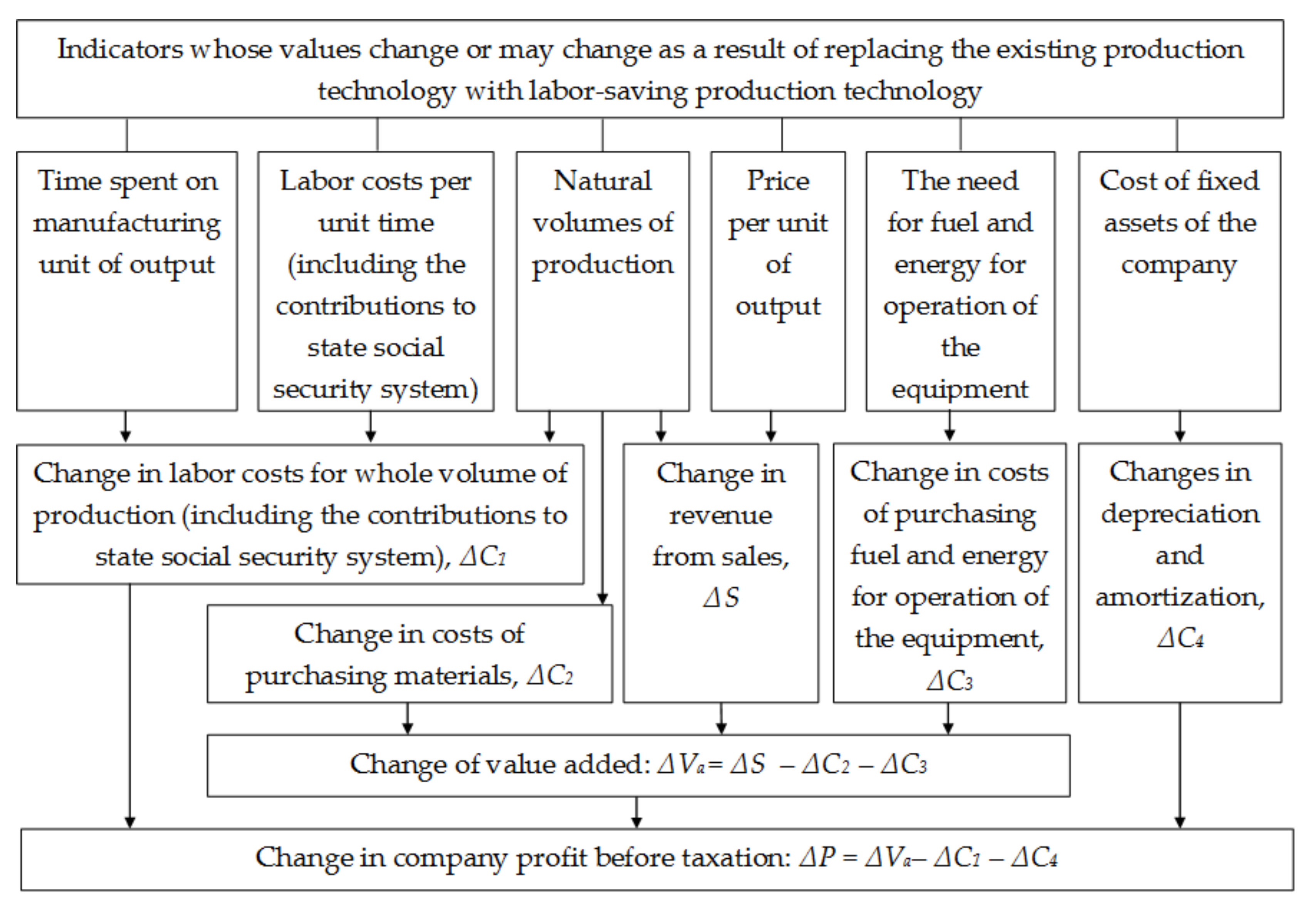

3.2. Modeling the Effect of Economically Efficient Technological Changes on the Company’s Income and Expenses

In order to assess the impact of economically efficient technological changes on the sustainability of the state social security system, it is first necessary to assess the impact of these changes on the amount of revenues in the budgets and state social insurance funds. In turn, the size of these revenues directly depends on the volumes and structure of income and expenditure of enterprises. Therefore, there is a need for modeling the impact of economically efficient technological changes on income and expenses of the firm.

It should be noted that in the future under technological saving, technological changes will be understood to be such changes in the technology of manufacturing certain products, which reduce the time expenditure for the production of a unit of this product. Consequently, a necessary sign of a work-saving technological change is to reduce the time spent on the production of a unit of product. However, it should be noted that the presence of this feature does not always mean that there have been some changes in the technology of manufacturing products. A possible situation in which there is a reduction of time expenditure is due to increased skill of workers.

In general, the task of modeling the impact of efficiently maintaining technological changes on the company’s income and expenses is rather complicated. This is due, first of all, to a significant number of such changes. The main types of economically efficient technological changes are presented in the

Table 1.

As follows from the presented grouping of types of economically efficient technological changes (

Table 1), such changes do not necessarily lead to a reduction in the number of employees of the firm. If the natural volumes of manufacturing of products after the transition to labor-saving technology will increase, then there is a situation in which the company will have an additional need for workers., This case will be discussed below in more detail.

It should also be noted that in the vast majority of cases, the implementation of labor-saving technologies requires some technical improvements [

16,

18,

29,

41,

42]. These improvements, in turn, require investments. In this case, it is expedient to highlight the following two cases:

- (1)

When the introduction of technical improvements does not require the decommissioning of certain equipment. In particular, this case may occur when the firm is modernizing its equipment. Under these conditions, the firm will be interested in the introduction of labor-saving technologies, if the increase in its profit as a result of such implementation will be higher than the minimum allowable for the owners of the company regarding the amount of profit. In turn, the minimum allowable value of profit will be determined as the result of the product of the amount of investment in modernizing the equipment at the minimum allowable return on investment;

- (2)

When the transition to labor-saving technology requires the replacement of the firm’s equipment on the new one. In this case, often there is a situation where the existing equipment did not complete its depreciation. Under these conditions, the firm will be interested in the introduction of low-cost technologies, if the increase in its profit will not only be higher than the minimum allowable value of profit, but also cover losses from incomplete depreciation of existing equipment.

With the introduction of labor-saving technologies in the enterprise, there can also be an increase in the amount of depreciation deductions and costs associated with the operation of equipment. In particular, the increase in the amount of depreciation can occur if the new equipment will cost more than the old one. With regard to the increase in equipment operating costs, such growth will occur, in particular, if new equipment will require more fuel and energy than the old one. It is also possible that the introduction of efficient technologies leads to an increase in the level of remuneration of workers, in particular, if the requirements for their qualification are increased.

When modeling the effect of efficiently maintaining technological changes on the company’s income and expenses, it is expedient to divide the company’s expenses into the following four groups: costs, the total value of which, calculated on the entire company’s output after the implementation of labor-saving technology, remains constant (this is, in particular, the overwhelming majority of fixed costs); expenditures, the value of which, per unit of output after implementation of labor-saving technology, remains constant (this, in particular, is due to the vast majority of costs coming from the purchase of materials); expenses, the total value of which, calculated on the entire volume of the company’s products after the introduction of labor-saving technology, may increase (this is, first of all, the cost of depreciation of equipment and the cost of fuel and energy for equipment operation); costs, the value of which per unit of production of the company after the introduction of labor-saving technology are changing (this is, first of all, the cost of labor remuneration).

Figure 2 represents a model of the impact of labor-saving technological changes on revenues and expenses of enterprise.

As it follows from

Figure 2, the change of company’s profit, related to replacing the existing production technology of certain products to labor-saving technology, largely depends on the change of revenues from the sale of these products. In general, in order to predict the change in sales revenue of the company, a detailed microeconomic analysis is required [

3,

5,

47,

77]. However, two cases can be identified in advance:

- (1)

When the firm does not occupy a significant market share of corresponding products. In this situation, the company can increase the volume of production and sales, but the products price will not change significantly. Consequently, in this case, the sales revenue will be directly proportional to the natural volume of production, and the company will be interested in maximizing this volume, taking into account the constraints of its available resources;

- (2)

When the company can cause the change (decrease) of the product price by increasing the volume of production and products sales. In this case, the optimal natural volume of production and product sales will exist for maximizing the company’s profits. At the same time, the transition to labor-saving production technologies should encourage the company to increase its production volumes. This is due to two main circumstances. First, usually the company can reduce the cost per unit of output (by reducing the labor cost per unit of output) due to the transition to labor-saving technologies. Secondly, during the transition to the labor-saving technology, only the part of fixed assets is replaced, and the rest of assets (including buildings) remain unchanged.

Consequently, the replacement of existing production technology with labor-saving technology will help to increase the natural volumes of production and product sales. Accordingly, as a result, not only the company’s profit will be increased, but the total amount of labor costs for its staff may be increased.

3.3. Development of Model for Assessing the Impact of Labor-Saving Technological Changes on the Sustainability of the State Social Security System

The assessment of the impact of labor-saving technological changes on the sustainability of the state social security system can occur at the level of the separate enterprise, at the industry level, or at the state level.

However, the results of such assessment at the industry or state level will be less accurate than the results of separate enterprise. This is can be explained by the fact that at the industry or state level it is not possible to determine, with high accuracy, the impact of labor-saving technological changes on the indicators of enterprise activity. Given these considerations, we will present a model for assessing the impact of labor-saving technological changes of a particular company on the sustainability of the state social security system.

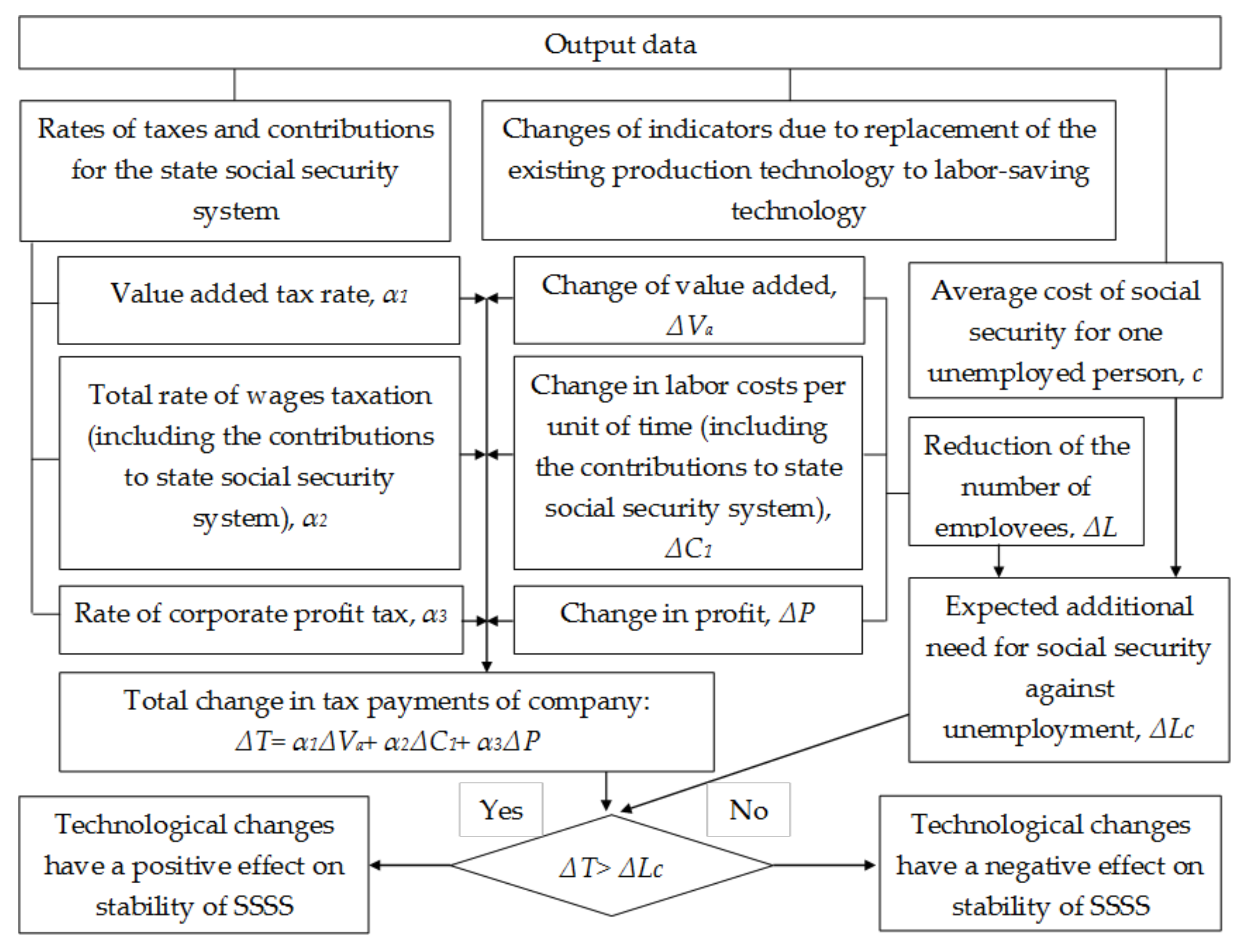

The basic idea of this model, the schematic representation of which is shown in

Figure 3, is to compare the growth of company tax payments (including the contributions to state social security system) with the expected additional necessity for social security for employees, which will be dismissed, due to the transition to the labor-saving production technology. It should be noted that the case of application of proportional tax scales is considered below.

In order to determine the expected additional necessity for social security, it is necessary to assess the significance of two indicators: the number of employees who will be dismissed, and the average cost of social security for one unemployed person. However, if the first indicator can be estimated accurately, the assessment of the value of the second indicator is faced with significant difficulties. This is due to the fact that it is necessary to take into account many different factors, not all of which can be accurately predicted, for calculation of the average cost of social security for one unemployed. In particular, these factors include share of dismissed employees, who will need to apply for unemployment benefits, in the total number of dismissed employees; time period during which the appeal for unemployment benefits will occur; duration of the unemployment benefit payment period; monthly amount of this unemployment benefits; duration and cost of retraining employees, which is financed from security payments, etc. Therefore, in order to assess the impact of labor-saving technological changes on the stability of the state social security system, it is appropriate to estimate the ratio of the growth of tax payments of the company to the number of its dismissed employees:

where

I—indicator of the assessment of the impact of labor-saving technological changes taking place in particular company on the stability of the state social security system; Δ

T—total growth of company tax payments (including the contributions to state social security system) as a result of the transition to the labor-saving production technology; Δ

L—the number of employees dismissed by this company as a result of the transition to labor-saving production technology.

If the value of the indicator (1) is negative in the situation when ΔL is bigger than 0, then, a priori, it can be argued that labor-saving technological changes of the particular company negatively affect the sustainability of the state social security system. If the value of the indicator (1) is positive, the larger it is, the more positive will be the effects on the SSSS.

The study of regularities of the impact of labor-saving technological changes on the stability of the state social security system requires the formalization of the indicators ΔT and ΔL, and their ratio. It is necessary to perform such formalization in the case of the following assumptions:

- (1)

that transition to labor-saving technology causes changes in different indicators of the company’s activity, such as norm of time consumption per production and the natural annual production volume;

- (2)

the price of production unit and amount of wages per unit of time remain unchanged;

- (3)

the annual value of depreciation and amortization and energy costs per production unit remain unchanged.

Under these assumptions, the annual growth of value added will be equal to the sum of value of annual growth of labor costs and annual growth of company profit. Accordingly, the aggregate growth of the company’s annual tax payments (including the contributions to state social security system) as a result of the transition to labor-saving production technology will be determined as follows:

or

where Δ

Va—growth of the annual value of the company’s added value;

α1—the value-added tax rate (in fractions of unit); Δ

C1—change in annual labor costs for all volume of production (including the contributions to state social security system);

α2—total rate of wages taxation (including the rates of contributions to state social security system) (in fractions of unit); Δ

P—growth of the annual value of profit before taxation of the company;

α3—corporate profit tax rate (in fractions of unit).

At the same time, the change in the annual labor costs for all volume of production as a result of the transition to the labor-saving production technology will be determined by formula:

where

S—labor costs per unit of time (including the contributions to state social security system);

N1,

N0—annual natural volumes of production, respectively, after and before the company’s transition to labor-saving technology;

n1,

n0—time spent on the production of unit of product, respectively, after and before the company’s transition to labor-saving technology.

The number of employees dismissed by the company as a result of its transition to labor-saving production technology, can be estimated using the following formula:

where

L0—the number of employees before the company’s transition to labor-saving production technology.

In view of Equation (4), the formula (3) takes the following form:

Substituting formula (5) and (6) into Equation (1) we obtain:

or

where

Va0 —annual value added before the company’s transition to labor-saving production technology;

β—growth rate of natural annual production volumes after the company’s transition to labor-saving production technology (

β = N1/N0).

It is necessary to note that formula (8) is the sum of two equations, each of which corresponds to a certain effect caused by the impact of labor-saving technological changes on the stability of the state social security system. The first effect is caused by growth of the natural volume of production. The second effect is due to the replacing the part of labor costs by the company’s profit. At the same time, the second effect can have a positive effect on the sustainability of the state social security system only if α3 > α2, i.e., if the level of profit taxation exceeds the level of taxation of wages.

These two effects can be related to the effects of the direct impact of labor-saving technological changes on the stability of the state social security system. The effects of the indirect impact of these changes should be highlighted. In particular, the additional tax revenues from firms that produce labor-saving equipment can cause these effects. In addition, if company with labor-saving technology increases its production output, the tax payments from enterprises, who deals with manufacturing materials necessary for the production of these products, may increase.

4. Empirical Analysis

4.1. Analysis of the Main Indicators of the Functioning of the State Social Security System of Ukraine

The state social security system of Ukraine operates thanks to the money accumulated in the state budget, municipal budgets, and three state social insurance funds: State Pension Fund, Social Insurance Fund of Ukraine (from which, in particular, the temporary-disability benefits are paid), and Social Insurance Fund for Unemployment [

82]. As it follows from the data presented in the

Table 2, the largest share of expenditures on state social security system in 2016 was taken by expenditures of Pension Fund—about 65%—while, for example, the share of expenditures of Social Insurance Fund for Unemployment was only 2.11%.

However, the state and municipal budgets finance not only the social security expenditures (in particular, the expenditures on utility services subsidies), but these budgets also provide the dotation to cover the deficit of state social insurance funds. As follows from the

Table 3, in 2016, more than half of State Pension Fund revenues was received through obtaining budget dotation.

Thus, the state social security system of Ukraine functions through redistribution of funds from budgets to the state social insurance funds. Due to this, a sufficient level of stability of social security system is maintained. At the same time, the main criterion of consideration of the state social security system of Ukraine as sustainable is that all social expenditures are made in full extent, and in accordance with terms established by the legislation.

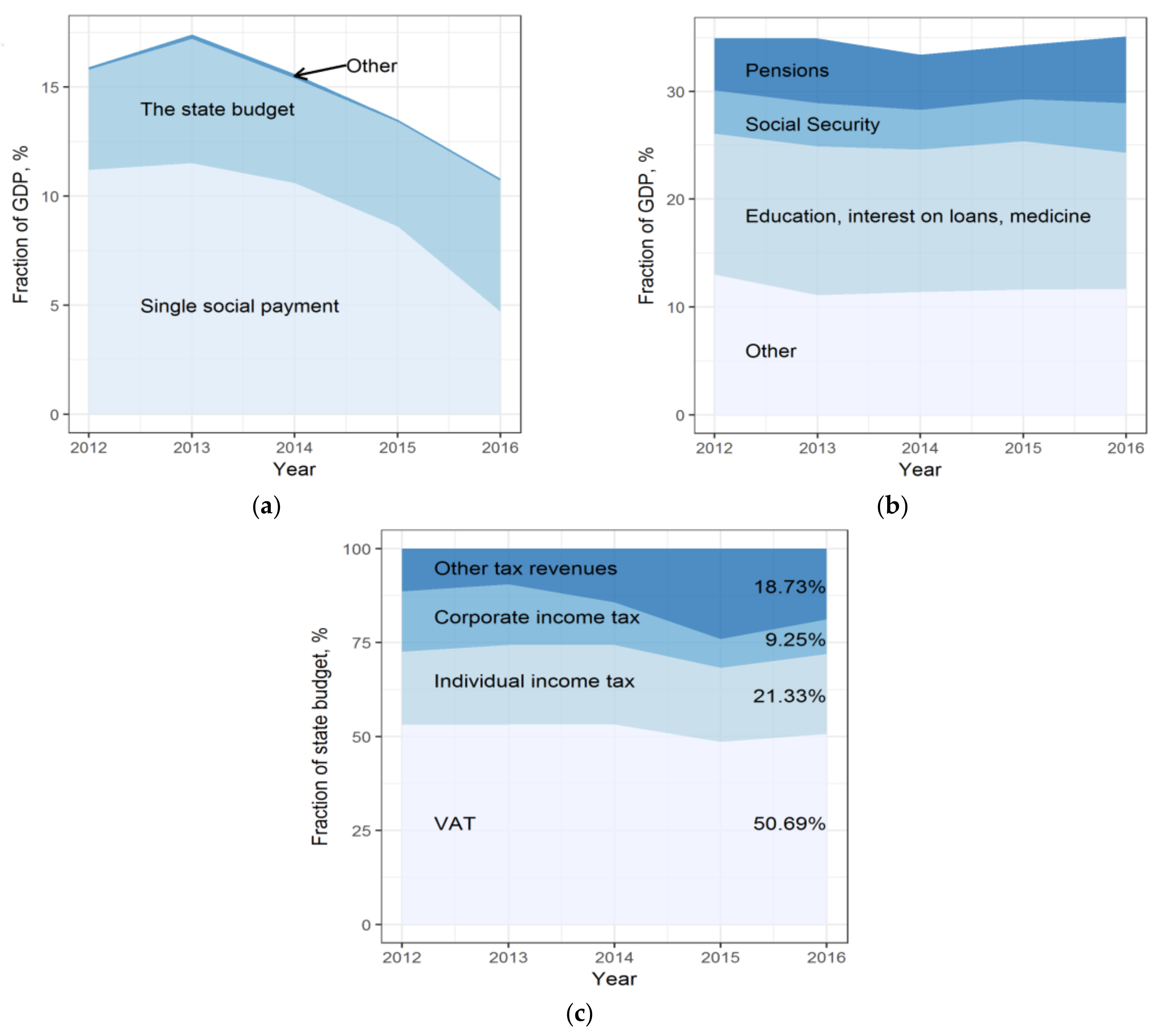

In order to analyze the dynamics of separate indicators of the functioning of state social security system during 2012–2016, it is possible to use the data presented in

Figure 4. In particular, as can be seen from

Figure 4a, during the investigated period, there was a decrease of share of State Pension Fund revenues in the gross domestic product of Ukraine. At the same time, this decrease was mainly due to the reduction of the share of insurance contributions in the structure of revenues of State Pension Fund. As it follows from

Figure 4b, the share of expenditures of the consolidated budget of Ukraine in the gross domestic product remained stable during the period of 2012–2016. The same situation applies to the structure of tax revenues in the consolidated budget of Ukraine. As can be seen from

Figure 4c, during the investigated period, about half of these revenues was provided by value-added tax, whereas the revenues from income tax for individuals and corporate profit tax represent about 20% and 10%, respectively, of the total tax revenues. Consequently, these three taxes form the basis of the tax system of Ukraine. It should be noted that the sustainability of the state social security system of Ukraine can be achieved mainly due to the small average size of social security provision per recipient. This statement illustrates the data presented in

Table 4.

As it follows from the

Table 4, the average size of pensions and unemployment benefits in Ukraine is low. At the same time, in 2014, there was a significant decrease in their dollar equivalent, which was conditioned by economic crisis in Ukraine during this period. It should also be noted that the relative level of public expenditures on social protection of the population in Ukraine is quite high. In particular, in 2015, the share of these expenditures in Ukraine’s gross domestic product exceeded 22%, while in the EU-28, for example, the average value of this indicator in 2015 was 20% (the highest was in Finland—25.6%) [

85]. However, the size of social expenditures per recipient in Ukraine is much lower than in any EU country. This is due to the low level of gross domestic product per capita in Ukraine (in 2015—about 2500 euros, while in the EU-28—28,900 euros).

4.2. Analysis of the Dynamics of Indicators Characterizing the Ukrainian Labor Market

Crisis phenomena that began in Ukraine since 2014 have had a negative impact on all areas of the economy and, in particular, on the labor market (

Table 5).

The employment situation in Ukraine since 2014 has deteriorated significantly. In particular, the unemployment rate increased from 7.7% in 2013 to 9.7% in 2014 (

Table 5). At the same time, in 2014, the load on 10 vacancies significantly increased from 73 to 111 people. Over the next two years, the unemployment rate stabilized in comparison with 2014. However, no significant improvement has taken place. It should also be mention the tendency towards reducing quantity of the economically active population of Ukraine during 2014–2016, which is due to, among other things, a significant outflow of Ukraine’s able-bodied population abroad. The process of labor emigration caused some decrease in the number of unemployed in 2015, compared to the previous year, however, in 2016, the number of unemployed increased again.

Thus, there is a clear tendency to increase the number of unemployed in Ukraine. The unemployment rate is rather high (almost 10%). It should also take into account hidden unemployment, which is not reflected in official statistics, and which, according to various estimates, may be approximately equal to registered unemployment.

4.3. Assessing the Impact of Changes in Labor Productivity on Costs and Benefits of Enterprises across the Different Economic Sectors of Ukraine

The stability of the state social security system of Ukraine at the macroeconomic level is determined, first of all, by the volume and dynamics of tax revenues in the state and municipal budgets in the form of three main taxes—value-added tax, income tax for individuals, and corporate tax. The size of these revenues is directly determined by the volume of relevant object of taxation (added value, employee wages, and company profits).

In the context of reseach of the impact of labor-saving technological changes on the sustainability of the state social security system of Ukraine, the study of establishing the relationship between the change in labor productivity and the change in value added, employee wages and company profits by industry is necessary. Output data needed to solve this problem is presented in

Table 6. At the same time, labor productivity, in this case, was defined as the ratio of sales revenues in a certain economic sector to the average number of employees in this economic sector.

Based on data of growth rates of indicators in 2016 compared to 2015 (

Table 6), we established a linear regression relationship between the change in the level of labor productivity in the economic sectors and the change in the added, labor costs, and profits of enterprises of Ukraine. In other words, we constructed three separate linear regressive dependencies, each of which was an independent variable of the growth rate of labor productivity, and the dependent variables were, respectively, the growth rate of value added, the growth rate of labor costs, and the growth rate of profits firms. The results of the regression analysis are presented in

Table 7.

According to the data of the

Table 7, there is a close relationship between the investigated indicators, which is sufficiently accurately approximated by linear regression model. This conclusion is confirmed by sufficiently high values of the coefficient of determanation

R2. In addition, the estimated values of the

F-criterion and

t-criterion indicate the statistical significance of all three regression equations.

The links between productivity growth and profit gains, as well as between productivity growth and value-added gains, are the most dense (for these dependencies, the magnitude of the coefficient R2 is the highest). This is especially true of the relationship between the growth in labor productivity and the increase in profits and value added. At the same time, the comparison of the coefficients of regression equations shows that the average percentage increase of labor productivity causes the higher percentages of profit growth than the growth of wage costs. This may be a sign of a labor-saving technological changes. Consequently, the growth of labor productivity in the Ukrainian economy is an important factor in increasing the tax base and, accordingly, the tax revenues in the budgets and state social insurance funds.

4.4. Assesment of the Impact of Labor-Saving Technological Changes in Ukrainian Industry Sectors on the Stability of its State Social Security System

At present, Ukraine does not belong to high-tech countries in most sectors of the economy. In particular, for most types of products manufactured by Ukrainian enterprises, there are inherent high costs of human resources. This naturally causes low productivity. However, a number of enterprises are already actively implementing mechanization and automation of production. In the future, this trend should be further strengthened as many Ukrainian enterprises are in urgent need of technology upgrades, replacing outdated fixed assets [

88].

It should be noted that the important indicator of the innovation potential of any country is the level of patent activity [

89,

90]. In Ukraine, this level is rather high: in the first quarter of 2016, 2140 patents were registered by the State Intellectual Property Service of Ukraine [

91].

However, at present, the level of innovation activity of industrial enterprises in Ukraine is not very high, and many innovations are not commercialized. Thus, in 2015, only 17.3% of Ukrainian industrial enterprises carried out innovative activities. In particular, 458 resource-saving technological processes were implemented during this year, which approximately corresponds to the number of such processes that were introduced by the industrial enterprises of Ukraine in previous years [

85].

In order to evaluate the impact of labor-saving technological changes on the sustainability of the state social security system in Ukraine, we selected 22 industrial enterprises, which implemented programs of mechanization and automation of production during 2015. The data characterizing the consequences of implementing these programs by industry sectors are presented in

Table 8.

The results of the assessment of the impact of labor-saving technological changes on the stability of the state social security system of Ukraine by industry sectors are given in

Table 9. It was taken into account that the tax rates in Ukraine, respectively, are the following: value-added tax—20%, income tax for individuals—18%, corporate tax for enterprises—18%, and the rate of the single social contribution to the state social insurance funds is 22% of the wage size. It should also be noted that the growth of the annual value of tax contributions in

Table 9 was determined by the Formula (2):

The indicator for assessing the impact of labor-saving technological changes on the stability of the state social security system was calculated by the Formula (1).

We note that the operation of division on the coefficient 1.22 in the Formula (9) is due to the fact that in

Table 8, the increase in annual labor costs is provided, including contributions to state social insurance. At the same time, these contributions are paid on salaries without taking into account the value of contributions to state social insurance. In addition, it should be noted that in Ukraine, contributions to state social insurance are paid only by employers.

For example, for the food industry, the results were obtained as follows: an increase in the annual value of tax payments: 23.761 × 0.2 + 1443 × (0.18 + 0.22)/1.22 + 17.987 × 0.18 = 8463 ths. UAH; including, as a result of growth of volumes of production: 52.875 × (1.1878 − 1) = 9930 ths. UAH; as a result of replacing part of the labor costs by the size of the profits firms: 8463 − 9930 = −1467 ths. UAH; indicator of the estimation of the impact of efficiently effective technological changes on the stability of the state social security system: 8463/187 = 45.26 ths. UAH per person.

As it follows from the data presented in the

Table 9, the value of the indicator of assessment of the impact of labor-saving technological changes on the stability of the state social security system in various industry sectors is significantly different. The highest value was noted in food-producing enterprises. For such enterprises, the value of this index divided by 12 months is higher than the average monthly unemployment benefit in 2016 (see

Table 4). Consequently, labor-saving technological changes in the investigated food-producing enterprises undoubtedly had a positive impact on the sustainability of the state social security system.

At the same time, at the instrument-producing enterprises, the indicator of the assessment of the impact of labor-saving technological changes on the stability of the state social security system has a negative significance. Consequently, the effect of labor-saving technological changes on this stability at instrument-producing enterprises was extremely negative. In all investigated industry sectors, there is a negative value of growth of the annual tax, caused by the replacement of part of the labor costs by the amount of profit. This is due to the fact that the level of tax burden on wages in Ukraine is much higher than the level of tax burden on enterprise profits.

5. Conclusions

5.1. Results of Empirical Analysis

Empirical analysis in this work was conducted on the example of Ukraine. The realized investigation of the state system of social security in Ukraine has shown that it functions through redistribution of funds from budgets to the state social insurance funds. Due to this, a sufficient level of stability of social security system is maintained. At the same time, the main criterion of consideration of the state social security system of Ukraine as sustainable is that all social expenditures are made in full extent, and in accordance with terms established by the legislation.

The analysis of certain indicators of the Ukrainian labor market has shown that the employment situation in Ukraine has deteriorated significantly since 2014. In particular, the unemployment rate increased from 7.7% in 2013 to 9.7% in 2014. At the same time, in 2014, the load on 10 vacancies significantly increased from 73 to 111 people. Over the next two years, the unemployment rate stabilized in comparison with 2014. However, no significant improvement has taken place.

In the context of the study of the impact of labor-saving technological changes on the sustainability of the state social security system, the correlation between the change in labor productivity and the change in value added, wages of employees, and profits of companies by economic sectors of Ukraine was established. The analysis showed that there is close relationship between the investigated parameters, which is sufficiently accurately approximated by linear regression model.

In order to evaluate the impact of labor-saving technological changes on the sustainability of the state social security system in Ukraine, in this work, there were selected 22 industrial enterprises, which implemented programs of mechanization and automation of production during 2015. The performed calculations showed that the value of the indicator of assessing the impact of labor-saving technological changes on the stability of the state social security system in various industry sectors is significantly different. The highest indicator of assessing the impact is in food-producing enterprises, and the lowest is in instrument-producing enterprises. At the same time, in all investigated industry sectors, there is a negative value of growth of the annual tax payments, caused by the replacement of part of the labor costs by the amount of profit.

5.2. The Main Theoretical Results of Research

The conducted research shows the relevance of assessing the impact of technological changes on the sustainability of the state social security system, as at present time, in many countries, there is a tendency to increase the number of people eligible for state social security. At the same time, among the factors that determine this increase, we should also call the technological unemployment.

In order to assess the impact of labor-saving technological changes on the sustainability of the state social security system, it is necessary to estimate the impact of these changes on the revenues of the budgets and state social insurance funds. In turn, the size of these revenues directly depends on the volumes and structure of incomes and expenses of enterprises. Therefore, there is necessity for modeling the impact of labor-saving technological changes on revenues and costs of the company. The conducted research shows that the measure of this impact for various objects of taxation is different: the labor-saving technologies usually contribute to firms’ profits increase, and they assist to value-added growth quite often. The growth of company’s total personnel costs as a result of implementation of labor-saving technological changes can happen only under conditions of sufficiently increased physical volumes of production.

During the research, two main effects were identified, which are caused by the impact of labor-saving technological changes on the sustainability of the state social security system. The first effect caused by growth of natural volumes of production. The second effect is due to the replacing the part of labor costs by the company’s profit. At the same time, the second effect can have a positive effect on the sustainability of the state social security system, only if the level of the company’s profit taxation exceeds the level of taxation of wages. Consequently, the state social security systems of those countries that fulfill this condition have a higher degree of sustainability.

These two effects can be related to the effects of the direct impact of labor-saving technological changes on the stability of the state social security system. The effects of the indirect impact of these changes should be highlighted. In particular, the additional tax revenues from firms that produce labor-saving equipment can cause these effects. In addition, if a company with labor-saving technology increases its production output, the tax payments from enterprises who deal with manufacturing materials necessary for the production of these products, may increase.

In this work, among other things, the authors developed a mathematical model for assessing the impact of labor-saving technological changes on the sustainability of the state social security system in the case where after these changes, the growth of the company’s physical volumes of production is increasing, and the price of products remains constant. The conducted study showed that with sufficient increase of the natural volume of production, the received additional tax revenues completely overwhelmed the additional costs of social security for dismissed workers. Thus, the hypothesis indicated in chapter 2 that labor-saving technological changes always have negative effects on the sustainability of the state social security system is not correct. However, if the volumes of production do not increase, and the level of taxation of labor costs exceeds the level of taxation of corporate profits, and the impact of labor-saving technological changes on the sustainability of the state social security system will be a priori negative.

5.3. Possibilities of Using the Obtained Results in Managerial Practice

Obtained results can be applied for substantiating the measures of the state social security policy. In particular, the model of assessing the impact of labor-saving technological changes on the sustainability of the state social security system can be used for this purpose. The main idea of this model is to compare the growth of company tax payments (including the contributions to state social security system) with the expected additional necessity for social security for employees who will be dismissed, due to the transition to the labor-saving production technology.

In order to assess the impact of labor-saving technological changes on the sustainability of the state social security system, it is advisable to use the indicator proposed in this work. This indicator is determined by dividing the total growth of tax payments of the company (including the contributions to state social security system) as a result of the transition to labor-saving production technology to the number of employees which the company must dismiss as a result of the transition to this production technology.

Based on the proposed indicator, it is expedient to create a mechanism for monitoring the impact of labor-saving technological changes on the level of sustainability of the state social security system. This monitoring should be carried out at the level of the individual company, and at the level of economic sector. At the same time, it is necessary to identify the reasons that determine the differences in the values of proposed indicators for various sectors of the economy. Such differentiation can be caused by different growth rates of production volume in various economic sectors. Then, it is important to identify the reasons that cause the differences in these rates of growth. These reasons may have objective character, for example, limited demand for products or limited volumes of resources for their production. However, some of the reasons of differences in the rates of output growth in various economic sectors can be subjected to managerial influence (for example, level of monopoly, difficulty of doing business, etc.).

At the same time, the state social security system can be considered as a system resistant to the influence on it of certain factors; if under its influence, this system will continue to give the social assistance payments in appropriate amounts to all categories of persons in accordance with the requirements established by legislative and regulatory acts. One of the most important ways of ensuring the sustainability of the state social security system is its adaptation to external influences by redistributing social expenditures between its funds, in particular, between the budget and state social insurance funds.

Ensuring the proper level of sustainability of the state social security system in conditions of labor-saving technological changes requires the state authorities to create enabling conditions for the growth of volumes of production and sales of products, that is, the increase of business activity of enterprises. It is also possible to highlight other measures that can be taken by public authorities. In particular, they can also include an increase of tax rates and an increase of public debt in order to finance the state social expenditures.

It should be taken into account that some of these measures can affect the pace of implementation of labor-saving technological changes in the future. In other words, not only technological changes can affect the sustainability of the state social security system. Some other measures for ensuring such resilience can affect the scale of the introduction of new technologies in the economy. In particular, an increase of corporate profit tax rate can reduce the attractiveness of investment and, therefore, inhibits the technological changes. On the other hand, an increase in the rates of state social security contributions for employers can lead to acceleration of implementation of their labor-saving technological changes, because the increase in the rates can provoke an increase of personnel costs.

5.4. Prospects for Further Research

Further research on te assessment of the impact of labor-saving technological changes on the sustainability of the state social security system require more detailed studies of the abovementioned effects, which are caused by indirect influence of these changes.

In addition, the study of the impact of technological changes on the sustainability of the state social security system may be interesting if the companies can influence the price of their products, increasing volume of production and sales of products. It is also worth considering the use of progressive tax scales and their impact.

The studies of long-term effects of implementation of labor-saving technologies are also important and necessary. In particular, these studies should take into account the tendency of reducing the share of the working population in the age structure of the population, which is inherent in many countries.

Finally, the mechanism of impact of tax rates changes on the pace of implementation of labor-saving technologies needs more detailed research.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}