Is Green Regulation Effective or a Failure: Comparative Analysis between Bangladesh Bank (BB) Green Guidelines and Global Reporting Initiative Guidelines

Abstract

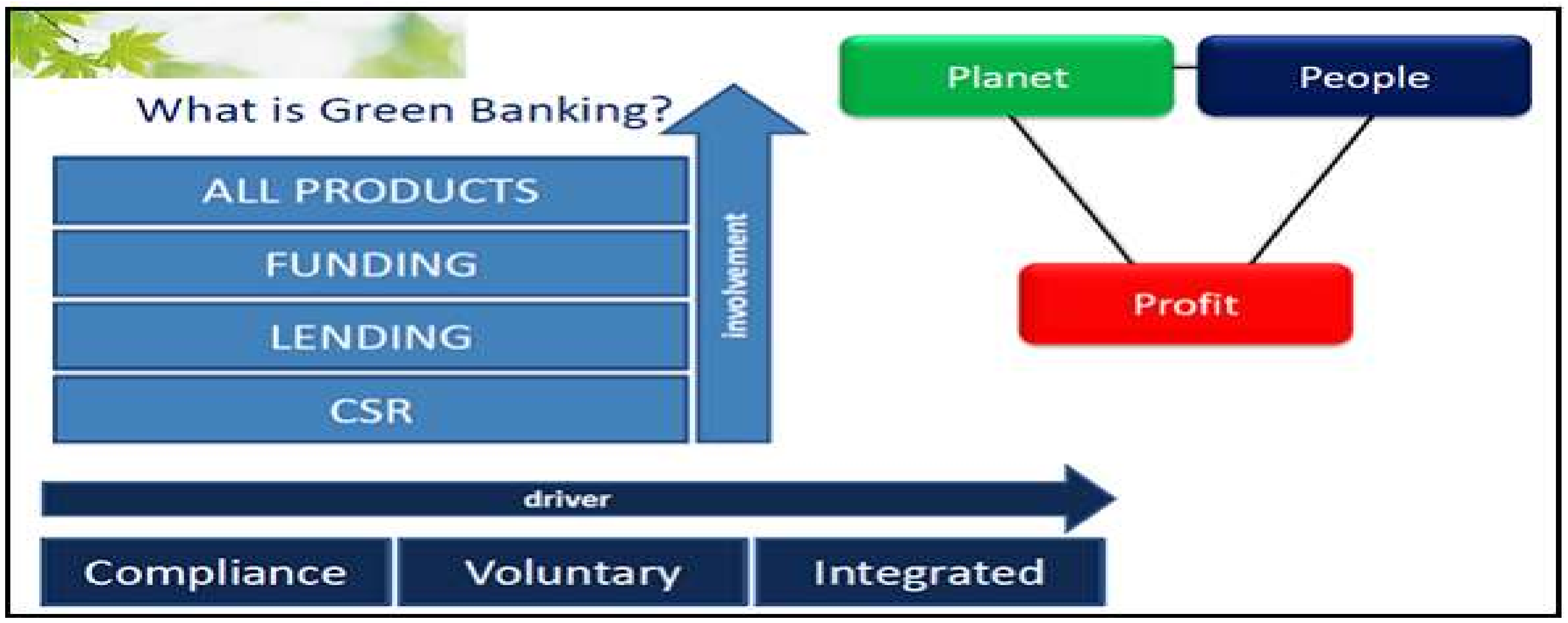

:1. Introduction

2. Theoretical Discussion

2.1. Institutional Theory

2.2. Stakeholder Theory

2.3. Legitimacy Theory

3. Literature Review

3.1. Developed Countries Green Regulation

3.2. Developing Countries’ Green Regulation

3.3. BB’s Green Regulation

3.4. GRI Regulation

4. Research Methodology

4.1. Sample Selection

4.2. Research Methods

5. Result and Discussion

5.1. Comparative Analysis between GRI and BB Guidelines

5.1.1. Similarities between GRI Guidelines and BB’s Green Guidelines

5.1.2. GRI Coding and Bank Reporting

5.2. Green Reporting Performance Based on BB Green Guidelines

5.2.1. Green Reporting of Banks

5.2.2. SWOT Analysis of BB Green Regulation

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

| GR Code and Content Name | Content Information |

|---|---|

| GR1-Green policy and strategy | Short-term and long-term policies for carbon emission and footprint, environmental protections, climate change, and global warning, climate adaptation and mitigation, energy efficiency, and renewable energy; sector specific environmental policies and strategic planning; establishing green banking unit, director level committee. |

| GR2-Environmental risk management | Assessing possible sources of risks before credit sanction; developing and updating credit risk methodology; auditing guidelines and reporting format considering environmental and climate risks; introducing environmental due diligence (EDD) checklist. |

| GR3-Green financing | Encouraging investing in renewable energy project, clean water project, waste water and management treatment plant, solid and hazardous disposal plant, and green and environmental innovation and technology. |

| GR4-Climate change risk fund | Climate change responsibility; formulation and utilization of climate change fund for flood, cyclone, and drought; ensure more financing in the climate vulnerable areas and sectors. |

| GR5-Green office management | Energy use, saving, and efficiency; electricity consumption and saving; gas and fuel consumption and saving; water consumption and saving; less consumption of paper; eco printing; using solar energy; green office guide; reduce business travel. |

| GR6-Green product and marketing | Online banking; mobile banking; SMS banking; Internet banking; video conferencing; virtual meeting; E-statement; online clearing house; online advertising; telemarketing; Email documentations. |

| GR7-Stakeholders training and awareness | Social, investors, and customers awareness of environmental, water, and air pollution; using renewable sources of energy; tree plantation; use energy efficient vehicles; regular training to the employees; introducing green day, green events. |

| GR8-Innovative green concept and technology | Technology transfer; investing green technology; resources mobilization by technology; electronic fund transfer; establishing ATM; research and development. |

| GR9-Green reporting | Quarterly, half yearly, and yearly green banking reporting; disclosing details of environmental initiatives and carbon footprint; providing sufficient information on climate risk fund utilization and green financing; using standalone sustainability reporting; updated website regarding green disclosures and annual report; real time information. |

| GR10-Internationalization of green reporting | Using globally recognized reporting standards; following GRI guidelines; green reporting assured by third party verification and introducing social and environmental auditing. |

| GR11-Reward and motivation | Ranking top ten green banks; risk rating facility; positive impact on CAMEL rating; opening new branches; CSR rating; tax benefit; gaining circulation of Green Bank logo. |

Appendix B

| AB Bank Ltd. (AB) Al-Arafah Islami Bank Ltd. (AAIBL) Bank Asia Ltd. (BAL) BRAC Bank Ltd. (BRAC) City Bank Ltd. (CBL) Dhaka Bank Ltd. (DBL) Dutch Bangla Bank Ltd. (DBBL) Eastern Bank Ltd. (EBL) EXIM Bank Ltd. (EXIM) First Security Islami Bank Ltd. (FSIBL) ICB Islami Bank Ltd. (ICB) IFIC Bank Ltd. (IFIC) Islami Bank Bangladesh Ltd. (IBBL) Jamuna Bank Ltd. (JBL) Mercantile Bank Ltd. (MBL) | Mutual Trust Bank Ltd. (MTB) National Bank Ltd. (NBL) National Credit and Commerce Bank Ltd. (NCC) One Bank Ltd. (OBL) Premier Bank Ltd. (PrBL) Prime Bank Ltd. (PBL) Pubali Bank Ltd. (PuBL) Rupali Bank Ltd. (RBL) Shahjalal Islami Bank Ltd. (ShIBL) Social Islami Bank Ltd. (SoIBL) South East Bank Ltd. (SEBL) Standard Bank Ltd. (SBL) Trust Bank Ltd. (TBL) United Commercial Bank Ltd. (UCB) Uttara Bank Ltd. (UBL) |

References

- UNFCCC. Available online: http://www4.unfccc.int/ndcregistry/PublishedDocuments/Bangladesh%20First/INDC_2015_of_Bangladesh.pdf/ (accessed on 25 October 2017).

- Masud, M.A.K.; Hossain, M.S. Green Banking and Reporting of Bangladeshi Commercial Banks: An Observation under Global Reporting Initiative (GRI). In Proceedings of the Global Conference on Business & Economics, Dhaka, Bangladesh, 21 May 2016. [Google Scholar]

- Schultze, W.; Trommer, R. The concept of environmental performance and its measurement in empirical studies. J. Manag. Control 2012, 22, 375–412. [Google Scholar] [CrossRef]

- Albertini, E. Does Environmental Management Improve Financial Performance? A Meta-Analytical Review. Org. Environ. 2013, 26, 431–457. [Google Scholar] [CrossRef]

- Esteban-Sanchez, P.; de la Cuesta-Gonzalez, M.; Paredes-Gazquez, J.D. Corporate social performance and its relation with corporate financial performance: International evidence in the banking industry. J. Clean. Prod. 2017, 162, 1102–1110. [Google Scholar] [CrossRef]

- Nurunnabi, M. Who cares about climate change reporting in developing countries? The market response to, and corporate accountability for, climate change in Bangladesh. Environ. Dev. Sustain. 2016, 18, 157–186. [Google Scholar] [CrossRef]

- Perrault, E.; Clark, C. Environmental Shareholder Activism: Considering Status and Reputation in Firm Responsiveness Organization. Org. Environ. 2016, 29, 194–211. [Google Scholar] [CrossRef]

- Masud, M.A.; Bae, S.; Kim, J. Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh. Sustainability 2017, 9, 1717. [Google Scholar] [CrossRef]

- Chen, L.; Tang, O.; Feldmann, A. Applying GRI reports for the investigation of environmental management practices and company performance in Sweden, China and India. J. Clean. Prod. 2015, 98, 36–46. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I.; Cortese, C. Corporate social responsibility reporting quality, board characteristics and corporate social reputation: Evidence from China. Pac. Account. Rev. 2015, 27, 95–118. [Google Scholar] [CrossRef]

- Sobhani, F.A.; Amran, A.; Zainuddin, Y. Sustainability disclosure in annual reports and websites: A study of the banking industry in Bangladesh. J. Clean. Prod. 2012, 23, 75–85. [Google Scholar] [CrossRef]

- Delgado-Márquez, B.L.; Pedauga, L.E.; Cordón-pozo, E. Industries Regulation and Firm Environmental Disclosure : A Stakeholders’ Perspective on the Importance of Legitimation and International Activities. Org. Environ. 2016, 1–19, in press. [Google Scholar] [CrossRef]

- Comyns, B. Determinants of GHG Reporting: An Analysis of Global Oil and Gas Companies. J. Bus. Ethics 2016, 136, 349–369. [Google Scholar] [CrossRef]

- Carrots and Sticks Global Trends in Sustainability Reporting Regulation and Policy. Available online: https://www.carrotsandsticks.net/wp-content/uploads/2016/05/Carrots-Sticks-2016.pdf/ (accessed on 10 June 2017).

- Wagner, R.; Seele, P. Uncommitted Deliberation? Discussing Regulatory Gaps by Comparing GRI 3.1 to GRI 4.0 in a Political CSR Perspective. J. Bus. Ethics 2017, 1–19. [Google Scholar] [CrossRef]

- Ortiz-de-Mandojana, N.; Aguilera-Caracuel, J.; Morales-Raya, M. Corporate Governance and Environmental Sustainability: The Moderating Role of the National Institutional Context. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 150–164. [Google Scholar] [CrossRef]

- Lopatta, K.; Jaeschke, R.; Canitz, F.; Kaspereit, T. International Evidence on the Relationship between Insider and Bank Ownership and CSR Performance. Corp. Gov. 2017, 25, 41–57. [Google Scholar] [CrossRef]

- Dam, L.; Scholtens, B. Ownership Concentration and CSR Policy of European Multinational Enterprises. J. Bus. Ethics 2013, 118, 117–126. [Google Scholar] [CrossRef]

- Mahfuzur Rahman, S.M.; Barua, S. The Design and Adoption of Green Banking Framework for Environment Protection: Lessons From Bangladesh. Aust. J. Sustain. Bus. Soc. 2016, 2, 1–19. [Google Scholar]

- Bose, S.; Khan, H.Z.; Rashid, A.; Islam, S. What drives green banking disclosure? An institutional and corporate governance perspective. Asia Pac. J. Manag. 2017, 1–27. [Google Scholar] [CrossRef]

- Hossain, M.; Bir, A.T.; Tarique, K.M.; Momen, A. Disclosure of Green Banking Issues in the Annual Reports: A Study on Bangladeshi Banks. Middle East J. Bus. 2016, 11, 19–30. [Google Scholar] [CrossRef]

- Uddin, S.; Siddiqui, J.; Islam, M.A. Corporate Social Responsibility Disclosures, Traditionalism and Politics: A Story from a Traditional Setting. J. Bus. Ethics 2016, 1–20. [Google Scholar] [CrossRef]

- Khan, A.; Muttakin, M.B.; Siddiqui, J. Corporate Governance and Corporate Social Responsibility Disclosures: Evidence from an Emerging Economy. J. Bus. Ethics 2013. [Google Scholar] [CrossRef]

- Masud, M.A.K.; Kabir, M.H. Corporate social responsibility evaluation by different levels of management of Islamic banks and traditional banks: Evidence from banking sector of Bangladesh. Probl. Perspect. Manag. 2016, 14, 194–202. [Google Scholar] [CrossRef]

- Willis, A. The Role of the Global Reporting Initiative’s Sustainability Reporting Guidelines in the SocialScreening of Investments. J. Bus. Ethics 2003, 43, 233–237. [Google Scholar] [CrossRef]

- Khan, H.; Azizul Islam, M.; Kayeser Fatima, J.; Ahmed, K. Corporate sustainability reporting of major commercial banks in line with GRI: Bangladesh evidence. Soc. Responsib. J. 2011, 7, 347–362. [Google Scholar] [CrossRef]

- Islam, M.N.; Chowdhury, M.A.F. Corporate sustainability reporting in the banking sector of Bangladesh: An appraisal of the G4 of the Global Reporting Initiative. Int. J. Green Econom. 2016, 10. [Google Scholar] [CrossRef]

- Bebbington, J.; Higgins, C.; Frame, B. Initiating sustainable development reporting: Evidence from New Zealand. Account. Audit. Account. J. 2009, 22, 588–625. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D.; Magnan, M. Intra-industry imitation in corporate environmental reporting: An international perspective. J. Account. Public Policy 2006, 25, 299–331. [Google Scholar] [CrossRef]

- Higgins, C.; Larrinaga, C. Sustainability reporting insights from institutional theory. In Sustainability Accounting and Accountability; Bebbington, J., Unerman, J., O’Dwyer, B., Eds.; Routledge: London, UK; New York, NY, USA, 2014. [Google Scholar]

- Azim, M.; Kluvers, R. Resisting Corruption in Grameen Bank. J. Bus. Ethics 2017. [Google Scholar] [CrossRef]

- Oliver, C. Strategic responses to institutional processes. Acad. Manag. Rev. 1991, 16, 145–179. [Google Scholar] [CrossRef]

- Scott, W.R. The adolescence of institutional theory. Adm. Sci. Q. 1987, 32, 493–511. [Google Scholar] [CrossRef]

- Dillard, J.F.; Rigsby, J.T.; Goodman, C. The making and remaking of organization context: Duality and the institutionalization process. Account. Audit. Account. J. 2004, 17, 506–542. [Google Scholar] [CrossRef]

- Berrone, P.; Fosfuri, A.; Gelabert, L.; Gomez-Mejia, L.R. Necessity as the mother of ‘green’ inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 2013, 34, 891–909. [Google Scholar] [CrossRef]

- Freeman, E.R. Strategic Management: A Stakholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Kiliç, M.; Kuzey, C.; Uyar, A. The impact of ownership and board structure on Corporate Social Responsibility (CSR) reporting in the Turkish banking industry. Corp. Gov. 2015, 15, 357–374. [Google Scholar] [CrossRef]

- Benlemlih, M.; Shaukat, A.; Qiu, Y.; Trojanowski, G. Environmental and Social Disclosures and Firm Risk. J. Bus. Ethics 2016, 1–14. [Google Scholar] [CrossRef]

- Gray, R.H.; Owen, D.; Adams, C. Accounting & Accountability: Changes and Challenges in Corporate Social and Environmental Reporting; Prentice Hall: Upper Saddle River, NJ, USA, 1996. [Google Scholar]

- Ntim, C.G.; Lindop, S.; Thomas, D.A. Corporate governance and risk reporting in South Africa: A study of corporate risk disclosures in the pre- and post-2007/2008 global financial crisis periods. Int. Rev. Financ. Anal. 2013, 30, 363–383. [Google Scholar] [CrossRef]

- Clarkson, P.; Li, Y.; Richardson, G.; Vasvari, F. Revisiting the Relation between Environmental Performance and Environmental Disclosure: An Empirical Analysis. Account. Org. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M. An examination of social and environmental reporting strategies. Account. Audit. Account. J. 2001, 14, 587–616. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Org. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Ullah, H.; Rahman, A. Corporate social responsibility reporting practices in banking companies in Bangladesh. J. Financ. Rep. Account. 2015, 13, 200–225. [Google Scholar] [CrossRef]

- Khan, H.; Halabi, A.K.; Samy, M. Corporate social responsibility (CSR) reporting: A study of selected banking companies in Bangladesh. Soc. Responsib. J. 2009, 5, 344–357. [Google Scholar] [CrossRef]

- Day, R.; Woodward, T. CSR reporting and the UK financial services sector. J. Appl. Account. Res. 2009, 10, 159–175. [Google Scholar] [CrossRef]

- Tsang, E. A Longitudinal Study of Corporate Social Reporting in Singapore: The Case of the Banking, Food and Beverages and Hotel Industries. Account. Audit. Account. J. 1998, 11, 624–635. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Feng, C.; Shi, B.; Kang, R. Does Environmental Policy Reduce Enterprise Innovation?—Evidence from China. Sustainability 2017, 9, 872. [Google Scholar] [CrossRef]

- Dissanayake, D.; Tilt, C.; Xydias-Lobo, M. Sustainability reporting by publicly listed companies in Sri Lanka. J. Clean. Prod. 2016, 129, 169–182. [Google Scholar] [CrossRef]

- Subramaniam, N.; Kansal, M.; Babu, S. Governance of Mandated Corporate Social Responsibility: Evidence from Indian Government-owned Firms. J. Bus. Ethics 2017, 143, 543–563. [Google Scholar] [CrossRef]

- Patel, T.; Rayner, S. A Transactional Culture Analysis of Corporate Sustainability Reporting Practices: Six Examples From India. Bus. Soc. 2012, 54, 283–321. [Google Scholar] [CrossRef]

- Mahmood, Z.; Kouser, R.; Ali, W.; Ahmad, Z.; Salman, T. Does Corporate Governance Affect Sustainability Disclosure? A Mixed Methods Study. Sustainability 2018, 10, 207. [Google Scholar] [CrossRef]

- Hossain, M.M.; Momin, M.; Rowe, A.; Quaddus, M. Corporate social and environmental reporting practices: A case of listed companies in Bangladesh. Sustain. Account. Manag. Policy J. 2017, 8. [Google Scholar] [CrossRef]

- Hoque, A.; Clarke, A.; Huang, L. Lack of Stakeholder Influence on Pollution Prevention: A Developing Country Perspective. Org. Environ. 2016. [Google Scholar] [CrossRef]

- Khan, H. The effect of corporate governance elements on corporate social responsibility (CSR) reporting. Int. J. Law Manag. 2010, 52, 82–109. [Google Scholar] [CrossRef]

- Boiral, O. Sustainability reports as simulacra? A counter-account of A and A+ GRI reports. Account. Audit. Account. J. 2013, 26, 1036–1071. [Google Scholar] [CrossRef]

- Milne, M.J.; Kearins, K.; Walton, S. Creating adventures in wonderland: The journey metaphor and environmental sustainability. Organization 2006, 13, 801–839. [Google Scholar] [CrossRef]

- GRI Database. Global Reporting Database. Available online: http://database.globalreporting.org/search/ (accessed on 28 October 2017).

- Baral, N.; Pokharel, M.P. How Sustainability Is Reflected in the S&P 500 Companies? Strategic Documents. Org. Environ. 2017, 30, 122–141. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef] [Green Version]

- Oh, W.Y.; Chang, Y.K.; Martynov, A. The Effect of Ownership Structure on Corporate Social Responsibility: Empirical Evidence from Korea. J. Bus. Ethics 2011, 104, 283–297. [Google Scholar] [CrossRef]

- Chang, Y.K.; Oh, W.-Y.; Park, J.H.; Jang, M.G. Exploring the Relationship Between Board Characteristics and CSR: Empirical Evidence from Korea. J. Bus. Ethics 2017, 140, 225–242. [Google Scholar] [CrossRef]

- IBBL. Annual Report of Islami Bank Bangladesh Bank 2013 to 2016. Available online: http://www.islamibankbd.com/annual_report.php (accessed on 20 November 2017).

- SoIBL. Annual Report of Social Islami Bank Bangladesh 2015 to 2016. Available online: https://www.siblbd.com/home/annual_reports (accessed on 20 November 2017).

- TBL. Annual Report of Trust Bank 2013. Available online: https://www.tblbd.com/corporate-information/reports-and-statements accesses on (accessed on 20 November 2017).

- UCB. Annual Report of United Commercil Bank 2015 to 2016. Available online: http://www.ucb.com.bd/index.php?page=know-ucb/investor-relations/annual-report (accessed on 20 November 2017).

- The Daily Star. Available online: http://www.thedailystar.net/business/101m-heist-bb-governor-ready-quit-791542 (accessed on 20 November 2017).

- Wikipedia. Available online: https://en.wikipedia.org/wiki/SWOT_analysis/ (accessed on 6 November 2017).

- CSR Report. Bangladesh Bank CSR Report 2013 to 2014. Available online: https://www.bb.org.bd/pub/publictn.php# (accessed on 20 November 2017).

- Bangladesh Bank. Annual Report 2016. Available online: https://www.bb.org.bd/pub/publictn.php# (accessed on 20 November 2017).

- Masud, M.A.K.; Hossain, M.S. Corporate Social Responsibility Reporting Practices in Bangladesh: A Study of Selected Private Commercial Banks. IOSR J. Bus. Manag. 2012, 6, 42–47. [Google Scholar] [CrossRef]

- Sayaduzzaman, M.; Masud, M.A.K. Corporate Social Responsibility Practices of Private Commercial Banks in Bangladesh: A Comparative Study. Cost Manag. 2012, 40, 34–39. [Google Scholar]

- The Daily Star. Available online: http://www.thedailystar.net/news-detail-268251 (accessed on 8 November 2017).

- The Daily Star. Available online: http://www.thedailystar.net/business/idb-dismayed-abrupt-changes-islami-bank-1355152 (accessed on 7 November 2017).

- Nikolaou, I.E. Environmental accounting as a tool of qualitative improvement of banks’ services: The case of Greece. Int. J. Financ. Serv. Manag. 2006, 2, 133–143. [Google Scholar] [CrossRef]

| GRI Guidelines | UNGC “Ten Principles” | OECD “Multinational Enterprise Guidelines” |

|---|---|---|

| Economic Aspect (EC1–EC9) | No specific principles | General policies |

| Environmental Aspect (EN1–EN34) | Principle 7, 8 and 9 | Environment |

| Social Aspect: Sub-category Labor Practice (LA1–LA14) Human Right (HR1–HR12) Society (SO1–SO11) Product Responsibility (PR1–PR9) | Principle 1, Principle 2, Principle 3, Principle 4, Principles 5, 6, and Principle 10 | Employment and industrial relation Combating bribery Consumer interests Competition |

| Comply with GRI (GRI Database) | Sourcing GRI (GRI Database) | Informal GRI (Annual Report) |

|---|---|---|

| BAL MTB PBL | EBL (Citing GRI) BRAC (Non-GRI) SEBL (Non-GRI) | IBBL SoIBL TBL UCB |

| Areas | Possible Explanation |

|---|---|

| Green Strategies (GS) | GS incorporate and enhance environmental attempt and policy. |

| Environmental Risk Management (ERM) | ERM is the key initiative of carbon emission and carbon footprint measurement. |

| Green Financing (GF) | GF is the key tool of motivating green environment and strategy. |

| Energy Efficiency (EE) | EE is the result of GS and GF. |

| Green Innovation (GI) | Innovation and technology is the power of GS. |

| Stakeholder Engagement (SE) | SE ensures the efficiency and effectiveness of GS, ERM, GF, EE, and GI. ES is the life-blood of the green movement. |

| GRI Code Number | GRI Code Name |

|---|---|

| EN3 | Energy (energy consumption within the organization) |

| EN6 | Energy (reduction of energy consumption) |

| EN15 | Emission (direct greenhouse gas emissions) |

| EN16 | Emission (energy indirect greenhouse gas emissions) |

| EN19 | Emission (reduction of greenhouse gas emissions) |

| EN27 | Products and services (extent of impact mitigation of environmental impacts of products and services) |

| EN29 | Compliance (monetary value of significant fines and total number of non-monetary sanctions for non-compliance with environmental laws and regulations) |

| EN31 | Expenditure and Investment (total environmental protection expenditures and investments) |

| Bank/GRS | GR1 | GR2 | GR3 | GR4 | GR5 | GR6 | GR7 | GR8 | GR9 | GR10 | GR11 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| All Banks | 120 | 119 | 114 | 101 | 119 | 120 | 116 | 117 | 119 | 11 | 120 |

| Percentage (%) | 100 | 99.17 | 95 | 84 | 99.17 | 100 | 96.67 | 97.50 | 99.17 | 9.17 | 100 |

| Strong Areas | Benefit Perceived | Weak Areas | Don’t Care |

|---|---|---|---|

| GR1-Green policy and strategy | Policy formulation; green banking unit. | GR10-Internationalization of green reporting | Non-GRI reporting; zero external assurance; zero environmental auditing. |

| GR6-Green product and marketing | Proper utilization of alternative technology; energy efficiency. | GR4-Climate change risk fund | Irresponsible risk fund formulation and utilization; information not available. |

| GR11-Reward and motivation | CSR expenditure increased; maximum tax benefit; new branches opening. | ||

| Green Reporting Score | GRS Percentage | Rank |

|---|---|---|

| 44 | 100 | 1 (2 banks) |

| 43 | 97.73 | 2 (1 bank) |

| 40 | 90.91 | 3 (22 banks) |

| 37 | 84.09 | 4 (1 banks) |

| 36 | 81.82 | 5 (2 banks) |

| 31 | 70.45 | 6 (1 banks) |

| 25 | 56.82 | 7 (1 bank) |

| Top Banks | Possible Perspectives | Poor Banks | Possible Perspectives |

|---|---|---|---|

| Bank Asia (BAL) Prime Bank (PBL) | Legitimate with society and stakeholders; institutional commitment. | Pubali Bank (PuBL) ICB Islami Bank (ICB) | Lack of commitment to the society and stakeholders; unaware of climate responses. |

| Year | TGRS | Mean | Median | Std. Dev. | Minimum | Maximum | Mode |

|---|---|---|---|---|---|---|---|

| 2013 | 292 | 26.545 | 29.000 | 8.574 | 2 | 30 | 29 |

| 2014 | 295 | 26.818 | 30.000 | 8.396 | 3 | 30 | 30 |

| 2015 | 294 | 26.727 | 30.000 | 8.369 | 3 | 30 | 30 |

| 2016 | 296 | 26.909 | 30.000 | 7.749 | 5 | 30 | 30 |

| Strengths First specific environmental regulation; Climate drivers (raising the issue of climate change, global warming, carbon emission, and carbon footprint); Climate financing;Climate change risk fund; In-house energy efficiency drives; Environmental due diligence checklist; Motivational. | Weaknesses Scatter guidelines rather than strategic; Unstructured and immature; Absence of reporting principles; Non-compliance regulation; Ignoring economic and social issues; Level of transparency; Qualitative rather than quantitative; Ignoring biodiversity issues; How to implement? |

| Opportunities Climate adaptation and mitigation; Awareness of the stakeholders; Business competitiveness; Triple bottom line concept; Promoting E-business (E-commerce, E-governance, E-marketing); Contribution in the global 2° temperature; Organized and regulated sector. | Threats Advertising and tax benefit; Political CSR; Powerful leaders’ project development; Family control management; Financial misconduct; Limited progress of GRI introduction; No external verification; Controlling and monitoring. |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Masud, M.A.K.; Hossain, M.S.; Kim, J.D. Is Green Regulation Effective or a Failure: Comparative Analysis between Bangladesh Bank (BB) Green Guidelines and Global Reporting Initiative Guidelines. Sustainability 2018, 10, 1267. https://0-doi-org.brum.beds.ac.uk/10.3390/su10041267

Masud MAK, Hossain MS, Kim JD. Is Green Regulation Effective or a Failure: Comparative Analysis between Bangladesh Bank (BB) Green Guidelines and Global Reporting Initiative Guidelines. Sustainability. 2018; 10(4):1267. https://0-doi-org.brum.beds.ac.uk/10.3390/su10041267

Chicago/Turabian StyleMasud, Md. Abdul Kaium, Mohammad Sharif Hossain, and Jong Dae Kim. 2018. "Is Green Regulation Effective or a Failure: Comparative Analysis between Bangladesh Bank (BB) Green Guidelines and Global Reporting Initiative Guidelines" Sustainability 10, no. 4: 1267. https://0-doi-org.brum.beds.ac.uk/10.3390/su10041267