Does Corporate Social Responsibility Mediate the Relation between Boardroom Gender Diversity and Firm Performance of Chinese Listed Companies?

, ,

, ,

Abstract

:1. Introduction

2. Theory and Hypotheses Development

2.1. Boardroom Gender Diversity and Firm Performance

Theoretical Underpinnings for Superior Board Performance with Greater Female Representation

2.2. CSR and Firm Performance

2.3. Boardroom Gender Diversity and Firm Performance: The Mediation Role of CSR

3. Research Design

3.1. Sample

3.2. Measures

3.3. Models Estimation

4. Empirical Results

4.1. Descriptive Statistics

4.2. Correlation Matrix

4.3. Multivariate Analysis

4.4. Robustness Tests

4.4.1. Alternative Measure of Boardroom Gender Diversity

4.4.2. Problem of Endogeneity

5. Conclusions and Future Research

Author Contributions

Conflicts of Interest

References

- Parker, J. Integrating CSR with hospitality management programmes in higher education. Int. J. Green Econ. 2011, 5, 396–404. [Google Scholar] [CrossRef]

- Abeysuriya, K.; Mitchell, C.; White, S. Can corporate social responsibility resolve the sanitation question in developing Asian countries? Ecol. Econ. 2007, 62, 174–183. [Google Scholar] [CrossRef] [Green Version]

- Teck Hui, L. Combining faith and CSR: A paradigm of corporate sustainability. Int. J. Soc. Econ. 2008, 35, 449–465. [Google Scholar] [CrossRef]

- Ball, A.; Craig, R. Using neo-institutionalism to advance social and environmental accounting. Crit. Perspect. Account. 2010, 21, 283–293. [Google Scholar] [CrossRef]

- Newell, P. Citizenship, accountability and community: The limits of the CSR agenda. Int. Aff. 2005, 81, 541–557. [Google Scholar] [CrossRef]

- Golob, U.; Bartlett, J.L. Communicating about corporate social responsibility: A comparative study of CSR reporting in Australia and Slovenia. Public Relat. Rev. 2007, 33, 1–9. [Google Scholar] [CrossRef]

- Lafuente, A.; Viñuales, V.; Pueyo, R.; Llaría, J. Responsabilidad Social Corporativas Y Politicas Publicas; Fundacion Alternativas: Madrid, Spain, 2003. [Google Scholar]

- Bear, S.; Rahman, N.; Post, C. The impact of board diversity and gender composition on corporate social responsibility and firm reputation. J. Bus. Ethics 2010, 97, 207–221. [Google Scholar] [CrossRef]

- Rao, K.; Tilt, C. Board composition and corporate social responsibility: The role of diversity, gender, strategy and decision making. J. Bus. Ethics 2016, 138, 327–347. [Google Scholar] [CrossRef]

- Davis, K. The case for and against business assumption of social responsibilities. Acad. Manag. J. 1973, 16, 312–322. [Google Scholar]

- Chen, H.; Wang, X. Corporate social responsibility and corporate financial performance in China: An empirical research from Chinese firms. Corp. Gov. Int. J. Bus. Soc. 2011, 11, 361–370. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business Is to Increase Its Profits. New Cork Times Magazine, 13 September 1970. [Google Scholar]

- Tang, L.; Li, H. Corporate social responsibility communication of Chinese and global corporations in China. Public Relat. Rev. 2009, 35, 199–212. [Google Scholar] [CrossRef]

- Lin, C.-Y.; Ho, Y.-H. Determinants of green practice adoption for logistics companies in China. J. Bus. Ethics 2011, 98, 67–83. [Google Scholar] [CrossRef]

- Noronha, C.; Tou, S.; Cynthia, M.I.; Guan, J.J. Corporate social responsibility reporting in China: An overview and comparison with major trends. Corp. Soc. Resp. Environ. Manag. 2013, 20, 29–42. [Google Scholar] [CrossRef]

- Zhou, C. The future roles of STPs in green growth of China: Based on the public-university-industry triple helix for sustainable development. J. Knowl.-Based Innov. China 2011, 3, 216–229. [Google Scholar] [CrossRef]

- Cai, H.; Wang, X. The substitution effect of cigarette excise tax for tobacco leaf tax in China. China Agric. Econ. Rev. 2010, 2, 385–395. [Google Scholar] [CrossRef]

- Wu, Y. Chemical fertilizer use efficiency and its determinants in China’s farming sector: Implications for environmental protection. China Agric. Econ. Rev. 2011, 3, 117–130. [Google Scholar] [CrossRef]

- Tian, D.; Chao, C.-C. Strategies under pressure: USA-China copyright dispute. J. Sci. Technol. Policy China 2011, 2, 219–237. [Google Scholar] [CrossRef]

- Fang, X. Re-examining the reform of China’s science and technology system: A historical perspective. J. Sci. Technol. Policy China 2010, 1, 7–17. [Google Scholar] [CrossRef]

- Hongwei, W.; Ping, L. Empirical analysis of the sources of China’s economic growth in 1978–2008. J. Knowl.-Based Innov. China 2011, 3, 91–105. [Google Scholar] [CrossRef]

- Cheung, Y.-L.; Jiang, P.; Tan, W. A transparency disclosure index measuring disclosures: Chinese listed companies. J. Account. Public Policy 2010, 29, 259–280. [Google Scholar] [CrossRef]

- Wang, K.; Sewon, O.; Claiborne, M.C. Determinants and consequences of voluntary disclosure in an emerging market: Evidence from China. J. Int. Account. Audit. Tax. 2008, 17, 14–30. [Google Scholar] [CrossRef]

- Xiao, H.; Yuan, J. Ownership structure, board composition and corporate voluntary disclosure: Evidence from listed companies in China. Manag. Audit. J. 2007, 22, 604–619. [Google Scholar]

- Tang, Z.; Tang, J. Stakeholder–firm power difference, stakeholders’ CSR orientation, and SMEs’ environmental performance in China. J. Bus. Ventur. 2012, 27, 436–455. [Google Scholar] [CrossRef]

- Guo, J.; Sun, L.; Li, X. Corporate social responsibility assessment of Chinese corporations. Int. J. Bus. Manag. 2009, 4, 54. [Google Scholar] [CrossRef]

- Dutta, P.; Bose, S. Gender Diversity in the Boardroom and Financial Performance of Commercial Banks: Evidence from Bangladesh. Available online: https://core.ac.uk/download/pdf/12015783.pdf (accessed on 9 October 2018).

- Erhardt, N.L.; Werbel, J.D.; Shrader, C.B. Board of director diversity and firm financial performance. Corp. Gov. Int. Rev. 2003, 11, 102–111. [Google Scholar] [CrossRef]

- Dezsö, C.L.; Ross, D.G. Does female representation in top management improve firm performance? A panel data investigation. Strateg. Manag. J. 2012, 33, 1072–1089. [Google Scholar] [CrossRef] [Green Version]

- Smith, N.; Smith, V.; Verner, M. Do women in top management affect firm performance? A panel study of 2500 Danish firms. Int. J. Product. Perform. Manag. 2006, 55, 569–593. [Google Scholar] [CrossRef]

- Carter, D.A.; Simkins, B.J.; Simpson, W.G. Corporate governance, board diversity, and firm value. Financ. Rev. 2003, 38, 33–53. [Google Scholar] [CrossRef]

- Vinnicombe, S. Women on Corporate Boards of Directors: International Research and Practice; Edward Elgar Publishing: Cheltenham, UK, 2009. [Google Scholar]

- Clacher, I.; Hagendorff, J. Do announcements about corporate social responsibility create or destroy shareholder wealth? Evidence from the UK. J. Bus. Ethics 2012, 106, 253–266. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate governance and firm value: The impact of corporate social responsibility. J. Bus. Ethics 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. Extrinsic and intrinsic drivers of corporate social performance: Evidence from foreign and domestic firms in Mexico. J. Manag. Stud. 2010, 47, 1–26. [Google Scholar] [CrossRef]

- Qu, W.; Leung, P. Cultural impact on Chinese corporate disclosure—A corporate governance perspective. Manag. Audit. J. 2006, 21, 241–264. [Google Scholar] [CrossRef]

- Walls, J.L.; Berrone, P.; Phan, P.H. Corporate governance and environmental performance: Is there really a link? Strateg. Manag. J. 2012, 33, 885–913. [Google Scholar] [CrossRef]

- Hung, H. Directors’ roles in corporate social responsibility: A stakeholder perspective. J. Bus. Ethics 2011, 103, 385–402. [Google Scholar] [CrossRef]

- De Villiers, C.; Naiker, V.; Van Staden, C.J. The effect of board characteristics on firm environmental performance. J. Manag. 2011, 37, 1636–1663. [Google Scholar] [CrossRef]

- Sahin, K.; Basfirinci, C.S.; Ozsalih, A. The impact of board composition on corporate financial and social responsibility performance: Evidence from public-listed companies in Turkey. Afr. J. Bus. Manag. 2011, 5, 2959–2978. [Google Scholar]

- Arora, P.; Dharwadkar, R. Corporate governance and corporate social responsibility (CSR): The moderating roles of attainment discrepancy and organization slack. Corp. Gov. Int. Rev. 2011, 19, 136–152. [Google Scholar] [CrossRef]

- Francoeur, C.; Labelle, R.; Sinclair-Desgagné, B. Gender diversity in corporate governance and top management. J. Bus. Ethics 2008, 81, 83–95. [Google Scholar] [CrossRef]

- Virtanen, A. Women on the boards of listed companies: Evidence from Finland. J. Manag. Gov. 2012, 16, 571–593. [Google Scholar] [CrossRef]

- Pan, Y.; Sparks, J.R. Predictors, consequence, and measurement of ethical judgments: Review and meta-analysis. J. Bus. Res. 2012, 65, 84–91. [Google Scholar] [CrossRef]

- Bilimoria, D.; Wheeler, J.V. Women corporate directors: Current research and future directions. Women Manag. Curr. Res. Issues 2000, 2, 138–163. [Google Scholar]

- Eagly, A.H.; Johnson, B.T. Gender and leadership style: A meta-analysis. Psychol. Bull. 1990, 108, 233–256. [Google Scholar] [CrossRef]

- Ingley, C.; Van Der Walt, N. Do board processes influence director and board performance? Statutory and performance implications. Corp. Gov. Int. Rev. 2005, 13, 632–653. [Google Scholar] [CrossRef]

- Post, C.; Byron, K. Women on boards and firm financial performance: A meta-analysis. Acad. Manag. J. 2015, 58, 1546–1571. [Google Scholar] [CrossRef]

- Ferreira, D. Board diversity: Should we trust research to inform policy? Corp. Gov. Int. Rev. 2015, 23, 108–111. [Google Scholar] [CrossRef]

- Larcker, D.; Tayan, B. Corporate Governance Matters: A Closer Look at Organizational Choices and Their Consequences; Pearson Education: London, UK, 2015. [Google Scholar]

- Matsa, D.A.; Miller, A.R. A female style in corporate leadership? Evidence from quotas. Am. Econ. J. Appl. Econ. 2013, 5, 136–169. [Google Scholar] [CrossRef]

- Ahern, K.R.; Dittmar, A.K. The changing of the boards: The impact on firm valuation of mandated female board representation. Q. J. Econ. 2012, 127, 137–197. [Google Scholar] [CrossRef]

- Adams, R.B.; Ferreira, D. Women in the boardroom and their impact on governance and performance. J. Financ. Econ. 2009, 94, 291–309. [Google Scholar] [CrossRef]

- Jurkus, A.F.; Park, J.C.; Woodard, L.S. Women in top management and agency costs. J. Bus. Res. 2011, 64, 180–186. [Google Scholar] [CrossRef]

- Carter, D.A.; D’Souza, F.; Simkins, B.J.; Simpson, W.G. The gender and ethnic diversity of US boards and board committees and firm financial performance. Corp. Gov. Int. Rev. 2010, 18, 396–414. [Google Scholar] [CrossRef]

- Adler, R.D. Women in the executive suite correlate to high profits. Harv. Bus. Rev. 2001, 79, 30–32. [Google Scholar]

- Huang, S.K. The impact of CEO characteristics on corporate sustainable development. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 234–244. [Google Scholar]

- Harjoto, M.; Laksmana, I.; Lee, R. Board diversity and corporate social responsibility. J. Bus. Ethics 2015, 132, 641–660. [Google Scholar] [CrossRef]

- Gupta, P.P.; Lam, K.C.; Sami, H.; Zhou, H. Board Diversity and Its Long-Term Effect on Firm Financial and Non-Financial Performance. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2531212 (accessed on 9 October 2018).

- Terjesen, S.; Couto, E.B.; Francisco, P.M. Does the presence of independent and female directors impact firm performance? A multi-country study of board diversity. J. Manag. Gov. 2016, 20, 447–483. [Google Scholar] [CrossRef]

- Khan, W.A.; Vieito, J.P. CEO gender and firm performance. J. Econ. Bus. 2013, 67, 55–66. [Google Scholar]

- Eagly, A.H. Sex Differences in Social Behavior: A Social-Role Interpretation, Lawrance Erlbaum Associates; Lawrence Erlbaum: Hillsdale, NJ, USA, 1987. [Google Scholar]

- Rosener, J. America’s Competitive Secret: Utilizing Women as A Power Strategy; Oxford University Press: New York, NY, USA, 1995. [Google Scholar]

- Arfken, D.E.; Bellar, S.L.; Helms, M.M. The ultimate glass ceiling revisited: The presence of women on corporate boards. J. Bus. Ethics 2004, 50, 177–186. [Google Scholar] [CrossRef]

- Becker, G.S. Human Capital: A Theoretical and Empirical Analysis, with Special Reference to Education; National Bureau of Economic Research: New York, NY, USA, 1964. [Google Scholar]

- Singh, V.; Terjesen, S.; Vinnicombe, S. Newly appointed directors in the boardroom: How do women and men differ? Eur. Manag. J. 2008, 26, 48–58. [Google Scholar] [CrossRef] [Green Version]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does it Pay to be Good? A Meta-Analysis and Redirection of Research on the Relationship between Corporate Social Responsibility and Financial Performance; Working Paper; University of Michigan: Ann Arbor, MI, USA, 2007. [Google Scholar]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Tsoutsoura, M. Corporate Social Responsibility and Financial Performance. Available online: https://escholarship.org/uc/item/111799p2 (accessed on 9 October 2018).

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does it Pay to be Good … and Does it Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial Performance. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1866371 (accessed on 9 October 2018).

- Castelo Branco, M.; Lima Rodriques, L. Positioning stakeholder theory within the debate on corporate social responsibility. EJBO-Electron. J. Bus. Ethics Organ. Stud. 2007, 12, 5–15. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Brown, J.A.; Forster, W.R. CSR and stakeholder theory: A tale of Adam Smith. J. Bus. Ethics 2013, 112, 301–312. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Does it pay to be really good? Addressing the shape of the relationship between social and financial performance. Strateg. Manag. J. 2012, 33, 1304–1320. [Google Scholar] [CrossRef]

- Menguc, B.; Ozanne, L.K. Challenges of the “green imperative”: A natural resource-based approach to the environmental orientation–business performance relationship. J. Bus. Res. 2005, 58, 430–438. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 303–319. [Google Scholar] [CrossRef]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar]

- Julian, S.D.; Ofori-dankwa, J.C. Financial resource availability and corporate social responsibility expenditures in a sub-Saharan economy: The institutional difference hypothesis. Strateg. Manag. J. 2013, 34, 1314–1330. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef] [Green Version]

- Van Beurden, P.; Gössling, T. The worth of values—A literature review on the relation between corporate social and financial performance. J. Bus. Ethics 2008, 82, 407–424. [Google Scholar] [CrossRef]

- Zu, L.; Song, L. Determinants of managerial values on corporate social responsibility: Evidence from China. J. Bus. Ethics 2009, 88, 105–117. [Google Scholar] [CrossRef] [Green Version]

- Bebchuk, L.A.; Weisbach, M.S. The state of corporate governance research. Rev. Financ. Stud. 2010, 23, 939–961. [Google Scholar] [CrossRef]

- Chhaochharia, V.; Grinstein, Y. CEO compensation and board structure. J. Financ. 2009, 64, 231–261. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The business case for corporate social responsibility: A review of concepts, research and practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Kurucz, E.C.; Colbert, B.A.; Wheeler, D. The business case for corporate social responsibility. In The Oxford Handbook of Corporate Social Responsibility; Oxford University Press: Oxford, UK, 2008. [Google Scholar]

- Fassin, Y.; Van Rossem, A. Corporate governance in the debate on CSR and ethics: Sensemaking of social issues in management by authorities and CEOs. Corp. Gov. Int. Rev. 2009, 17, 573–593. [Google Scholar] [CrossRef]

- Blau, P.M. Inequality and Heterogeneity: A Primitive Theory of Social Structure; Free Press: New York, NY, USA, 1977; Volume 7. [Google Scholar]

- Campbell, K.; Mínguez-Vera, A. Gender diversity in the boardroom and firm financial performance. J. Bus. Ethics 2008, 83, 435–451. [Google Scholar] [CrossRef]

- Ahmed Haji, A. Corporate social responsibility disclosures over time: Evidence from Malaysia. Manag. Audit. J. 2013, 28, 647–676. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef] [Green Version]

- Abdullah, S.N.; Mohamed, N.R.; Mokhtar, M.Z. Board independence, ownership and CSR of Malaysian Large Firms. Corp. Ownersh. Control 2011, 8, 417–431. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Cochran, P.L.; Wood, R.A. Corporate social responsibility and financial performance. Acad. Manag. J. 1984, 27, 42–56. [Google Scholar]

- Tan, J.; Peng, M.W. Organizational slack and firm performance during economic transitions: Two studies from an emerging economy. Strateg. Manag. J. 2003, 24, 1249–1263. [Google Scholar] [CrossRef]

- Thompson, J. Organizations in Action; McGraw-Hill: New York, NY, USA, 1967. [Google Scholar]

- Grosvold, J.; Brammer, S.; Rayton, B. Board diversity in the United Kingdom and Norway: An exploratory analysis. Bus. Ethics Eur. Rev. 2007, 16, 344–357. [Google Scholar] [CrossRef]

- Hafsi, T.; Turgut, G. Boardroom diversity and its effect on social performance: Conceptualization and empirical evidence. J. Bus. Ethics 2013, 112, 463–479. [Google Scholar] [CrossRef]

- Bruynseels, L.; Cardinaels, E. The audit committee: Management watchdog or personal friend of the CEO? Account. Rev. 2013, 89, 113–145. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility: A review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Weber, M. The business case for corporate social responsibility: A company-level measurement approach for CSR. Eur. Manag. J. 2008, 26, 247–261. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef] [Green Version]

- Gjølberg, M. Measuring the immeasurable?: Constructing an index of CSR practices and CSR performance in 20 countries. Scand. J. Manag. 2009, 25, 10–22. [Google Scholar] [CrossRef]

{kind=link}

| CSR Reporting Items | Binary Scale | |

|---|---|---|

| 1 | Referring to GRI sustainability reporting guideline or not | 1,0 |

| 2 | Reporting protection of shareholder interests or not | 1,0 |

| 3 | Reporting protection of creditor interests or not | 1,0 |

| 4 | Reporting protection of employee interests or not | 1,0 |

| 4 | Reporting protection of supplier interests or not | 1,0 |

| 6 | Reporting protection of interests of clients and consumers or not | 1,0 |

| 7 | Reporting environment and sustainability or not | 1,0 |

| 8 | Reporting public relations and social and public welfare or not | 1,0 |

| 9 | Reporting social responsibility system construction and improvement or not | 1,0 |

| 10 | Reporting secure production or not | 1,0 |

| 11 | Reporting deficiencies of company or not | 1,0 |

| Variable Name | Abbreviation | Description |

|---|---|---|

| Boardroom gender diversity | BGD | Boardroom gender diversity is calculated by using the Blau index, which is measured as where Pi is the percent of male and female in the board and n is 2 representing number of categories (male and female). |

| Proportion of female director | PFD | Total number of female director divided by total number of director on the board. |

| Corporate social responsibility reporting index | CSRRI | A dichotomous procedure is adopted whereby a company is awarded 1 if an item is reported and 0 if it is not reported, and the total score of CSR reporting index has been computed based on the following formula |

| Tobin Q | TQ | (Total assets market capitalization—book value of equity—deferred tax liability)/total assets. |

| Independent director | ID | Number of independent directors divided by total directors, multiplied by 100. |

| CEO power | CEOP | A dummy variable equal to 1 if the CEO has the also chair role, otherwise 0. |

| Board member meeting frequency | BMMF | Number of board of directors’ meetings in a year. |

| Firm size | FS | Natural log of total assets. |

| Leverage | Lev | Total debt divided by total assets. |

| Big4 | Big4 | A dummy variable that is 1 if a listed firm is audited by one of the international Big 4 audit firms or their joint ventures in China and zero otherwise. |

| Board size | BS | Total number of directors on the board. |

| Board member average age | BMAA | The average age of board of directors. |

| State owned enterprise | SOE | A dummy variable equal to 1 if the firm is a state-owned enterprise, otherwise 0. |

| Firm age | FA | Number of year of listing. |

| Variable | Obs | Mean | Std. Dev |

|---|---|---|---|

| BGD(BI) | 4257 | 0.1844319 | 0.1590432 |

| CSR | 4257 | 0.7319474 | 0.1480728 |

| TQ | 4257 | 1.808066 | 2.078244 |

| ID | 4257 | 0.3699925 | 0.0662303 |

| CEOP | 4257 | 0.179704 | 0.3839858 |

| BMMF | 4257 | 9.966643 | 4.441063 |

| FS | 4257 | 23.07651 | 1.749106 |

| Lev | 4257 | 0.5098044 | 0.2168527 |

| Big4 | 4257 | 0.1654135 | 0.371597 |

| BS | 4257 | 9.545455 | 2.309339 |

| BMAA | 4257 | 51.27363 | 3.826847 |

| SOE | 4257 | 0.599859 | 0.4899843 |

| FA | 4257 | 11.58388 | 5.634835 |

| BGD | CSR | TQ | ID | CEOP | BMMF | FS | Lev | Big4 | BS | BMAA | SOE | FA | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BGD(BI) | 1.000 | ||||||||||||

| CSR | 0.070 *** | 1.000 | |||||||||||

| TQ | 0.077 ** | 0.026 * | 1.000 | ||||||||||

| ID | 0.027 * | 0.000 | 0.025 | 1.000 | |||||||||

| CEOP | 0.080 *** | 0.069 *** | 0.152 *** | 0.086 *** | 1.000 | ||||||||

| BMMF | 0.050 *** | 0.043 *** | −0.065 *** | 0.042 *** | −0.012 | 1.000 | |||||||

| FS | −0.073 *** | 0.221 *** | −0.441 *** | 0.054 ** | −0.132 *** | 0.170 ** | 1.000 | ||||||

| Lev | −0.064 *** | 0.131 ** | −0.502 *** | 0.017 | −0.125 *** | 0.192 *** | 0.595 ** | 1.000 | |||||

| Big4 | −0.074 *** | 0.140 *** | −0.170 *** | 0.053 *** | −0.079 *** | 0.061 *** | 0.546 ** | 0.227 *** | 1.000 | ||||

| BS | −0.029 ** | 0.110 *** | −0.216 *** | −0.246 *** | −0.141 *** | 0.023 | 0.445 ** | 0.257 *** | 0.264 *** | 1.000 | |||

| BMAA | 0.098 ** | −0.063 *** | −0.110 *** | 0.077 *** | −0.065 *** | −0.035 ** | 0.201 ** | 0.073 *** | 0.072 *** | 0.062 *** | 1.000 | ||

| SOE | −0.163 * | 0.077 *** | −0.222 *** | −0.029 *** | −0.230 ** | −0.072 ** | 0.291 *** | 0.212 *** | 0.167 *** | 0.193 *** | 0.153 *** | 1.000 | |

| FA | 0.033 * | 0.095 *** | −0.185 *** | −0.014 | −0.127 *** | 0.061 *** | 0.189 *** | 0.262 *** | 0.029 ** | 0.040 *** | 0.205 *** | 0.313 *** | 1.000 |

| Variables | Model 1 (TQ) | Model 2 (CSR) | Model 3 (TQ) | |||

|---|---|---|---|---|---|---|

| Coef. | p-Value | Coef. | p-Value | Coef. | p-Value | |

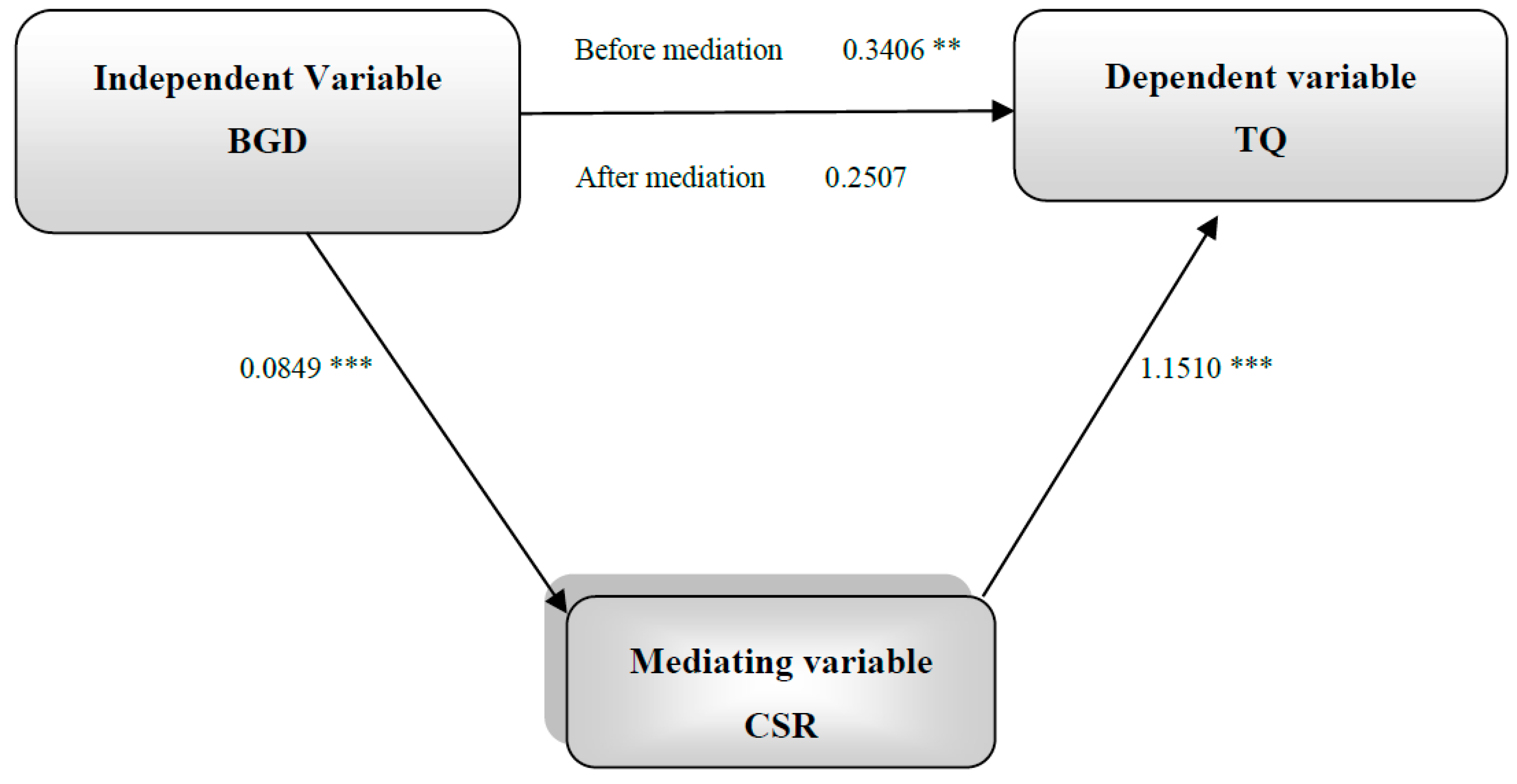

| BGD(BI) | 0.3406 ** | 0.041 | 0.0849 *** | 0.000 | 0.2507 | 0.151 |

| CSR | 1.1510 *** | 0.000 | ||||

| ID | 0.9556 ** | 0.030 | 0.0081 | 0.819 | 0.9628 ** | 0.028 |

| CEOP | 0.3279 *** | 0.000 | 0.0151 ** | 0.011 | 0.3465 *** | 0.000 |

| BMMF | 0.0151 ** | 0.016 | 0.0012 | 0.813 | 0.0151 ** | 0.016 |

| FS | −0.2668 *** | 0.000 | 0.0157 *** | 0.000 | −0.28481 *** | 0.000 |

| Lev | −3.399 *** | 0.000 | −0.0035 | 0.786 | −3.399 *** | 0.000 |

| Big4 | 0.2892 *** | 0.001 | 0.0147 ** | 0.040 | 0.2706 *** | 0.002 |

| BS | −0.0066 | 0.631 | 0.00076 | 0.499 | −0.0075 | 0.583 |

| BMAA | −0.0066 | 0.135 | 0.00073 | 0.225 | −0.0121 | 0.104 |

| SOE | −0.2413 *** | 0.000 | 0.0011 | 0.820 | −0.2418 *** | 0.000 |

| FA | −0.0091 * | 0.085 | 0.0012 *** | 0.005 | −0.0104 ** | 0.049 |

| Constant | 9.9181 *** | 0.000 | 0.8319 *** | 0.000 | 8.9619 *** | 0.000 |

| F | 160.53 | 25.71 | 151.50 | |||

| Adj-R2 | 29.67 | 6.00 | 30.27 | |||

| Variables | Model 1 (TQ) | Model 2 (CSR) | Model 3 (TQ) | |||

|---|---|---|---|---|---|---|

| Coef. | p-Value | Coef. | p-Value | Coef. | p-Value | |

| PFD | 0.4438 ** | 0.042 | 0.0935 *** | 0.000 | 0.3457 | 0.112 |

| CSR | 1.1517 *** | 0.000 | ||||

| ID | 0.9448 ** | 0.031 | 0.0108 | 0.760 | 0.9549 ** | 0.029 |

| CEOP | 0.3281 *** | 0.000 | 0.0149 ** | 0.012 | 0.3464 *** | 0.000 |

| BMMF | 0.01524 ** | 0.015 | 0.00015 | 0.770 | 0.0151 ** | 0.016 |

| FS | −0.2669 *** | 0.000 | 0.0157 *** | 0.000 | −0.2850 *** | 0.000 |

| Lev | −3.3998 *** | 0.000 | −0.0041 | 0.750 | −3.3992 *** | 0.000 |

| Big4 | 0.2881 *** | 0.001 | 0.0143 ** | 0.047 | 0.2700 *** | 0.002 |

| BS | −0.0055 | 0.687 | 0.0010 | 0.373 | −0.0067 | 0.625 |

| BMAA | −0.0109 | 0.143 | 0.00073 | 0.229 | −0.01190 | 0.111 |

| SOE | −0.2385 *** | 0.000 | 0.0010 | 0.838 | −0.2389 *** | 0.000 |

| FA | −0.0094 * | 0.076 | 0.0011 *** | 0.006 | −0.0107 ** | 0.044 |

| Constant | 9.9145 *** | 0.000 | 0.8358 *** | 0.000 | 8.9537 *** | 0.000 |

| F | 160.58 | 24.96 | 151.56 | |||

| Adj-R2 | 29.67 | 5.83 | 30.28 | |||

| Variables | Lag of Independent Variables | Two-Stage Least Square (2SLS) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Model 1 (TQ) | Model 2 (CSR) | Model 3 (TQ) | Model 4 (TQ) | Model 5 (CSR) | Model 6 (TQ) | |||||||

| Coef. | p-Value | Coef. | p-Value | Coef. | p-Value | Coef. | p-Value | Coef. | p-Value | Coef | p-Value | |

| BGD(BI) | 0.074 * | 0.066 | 0.070 *** | 0.000 | 0.0055 | 0.974 | 0.119 * | 0.066 | 0.112 *** | 0.000 | 0.008 | 0.974 |

| CSR | 1.173 *** | 0.000 | 1.173 *** | 0.000 | ||||||||

| ID | 0.947 ** | 0.031 | 0.012 | 0.728 | 0.958 ** | 0.029 | 0.952 ** | 0.030 | 0.006 | 0.864 | 0.957 ** | 0.028 |

| CEOP | 0.333 *** | 0.000 | 0.014 ** | 0.015 | 0.352 *** | 0.000 | 0.332 *** | 0.000 | 0.015 *** | 0.008 | 0.352 *** | 0.000 |

| BMMF | 0.015 * | 0.013 | −0.002 | 0.666 | 0.0154 ** | 0.013 | 0.015 ** | 0.013 | 0.008 | 0.869 | 0.015 ** | 0.013 |

| FS | −0.265 *** | 0.000 | −0.016 *** | 0.000 | −0.284 *** | 0.000 | −0.266 *** | 0.000 | 0.015 *** | 0.000 | −0.284 *** | 0.000 |

| Lev | −3.41 *** | 0.000 | 0.005 | 0.663 | −3.41 *** | 0.000 | −3.41 *** | 0.000 | −0.002 | 0.852 | −3.413 *** | 0.000 |

| Big4 | 0.282 *** | 0.001 | −0.014 ** | 0.051 | 0.264 *** | 0.003 | 0.283 *** | 0.001 | 0.015 ** | 0.035 | 0.264 ** | 0.003 |

| BS | −0.006 | 0.642 | −0.0006 | 0.566 | −0.007 | 0.600 | −0.006 | 0.644 | 0.0007 | 0.529 | −0.007 | 0.599 |

| BMAA | −0.012 | 0.103 | −0.0006 | 0.264 | −0.013 * | 0.078 | −0.012 | 0.110 | 0.0008 | 0.167 | −0.013 * | 0.080 |

| SOE | −0.256 *** | 0.000 | 0.0005 | 0.917 | −0.255 *** | 0.000 | −0.252 *** | 0.000 | 0.002 | 0.610 | −0.255 *** | 0.000 |

| FA | −0.008 | 0.123 | −0.001 *** | 0.002 | −0.009 * | 0.068 | −0.008 | 0.115 | 0.001 ** | 0.011 | −0.009 ** | 0.072 |

| Constant | 10.0 *** | 0.000 | 0.8358 *** | 0.000 | 9.02 *** | 0.000 | 9.98 *** | 0.000 | 0.822 *** | 0.000 | 9.026 *** | 0.000 |

| F | 159.97 | 24.51 | 151.16 | |||||||||

| WaldChi2 | 1765.66 | 270.83 | 1819.51 | |||||||||

| Adj-R2 | 29.60 | 5.73 | 30.23 | 29.82 | 6.13 | 30.43 | ||||||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sial, M.S.; Zheng, C.; Cherian, J.; Gulzar, M.A.; Thu, P.A.; Khan, T.; Khuong, N.V. Does Corporate Social Responsibility Mediate the Relation between Boardroom Gender Diversity and Firm Performance of Chinese Listed Companies? Sustainability 2018, 10, 3591. https://0-doi-org.brum.beds.ac.uk/10.3390/su10103591

Sial MS, Zheng C, Cherian J, Gulzar MA, Thu PA, Khan T, Khuong NV. Does Corporate Social Responsibility Mediate the Relation between Boardroom Gender Diversity and Firm Performance of Chinese Listed Companies? Sustainability. 2018; 10(10):3591. https://0-doi-org.brum.beds.ac.uk/10.3390/su10103591

Chicago/Turabian StyleSial, Muhammad Safdar, Chunmei Zheng, Jacob Cherian, M.A. Gulzar, Phung Anh Thu, Tehmina Khan, and Nguyen Vinh Khuong. 2018. "Does Corporate Social Responsibility Mediate the Relation between Boardroom Gender Diversity and Firm Performance of Chinese Listed Companies?" Sustainability 10, no. 10: 3591. https://0-doi-org.brum.beds.ac.uk/10.3390/su10103591