Does the Role of Media and Founder’s Past Success Mitigate the Problem of Information Asymmetry? Evidence from a UK Crowdfunding Platform

,

,  and

and

Abstract

:1. Introduction

Does the level and type of used media and successful track record of previous projects influence the success/reward rate of crowdfunding campaigns?

2. Literature Review

2.1. Role of Information Asymmetry in Crowdfunding

2.2. Problems of Information Asymmetry in Crowdfunding

2.3. Possible Determinants of Information Asymmetry on Crowdfunding Platforms

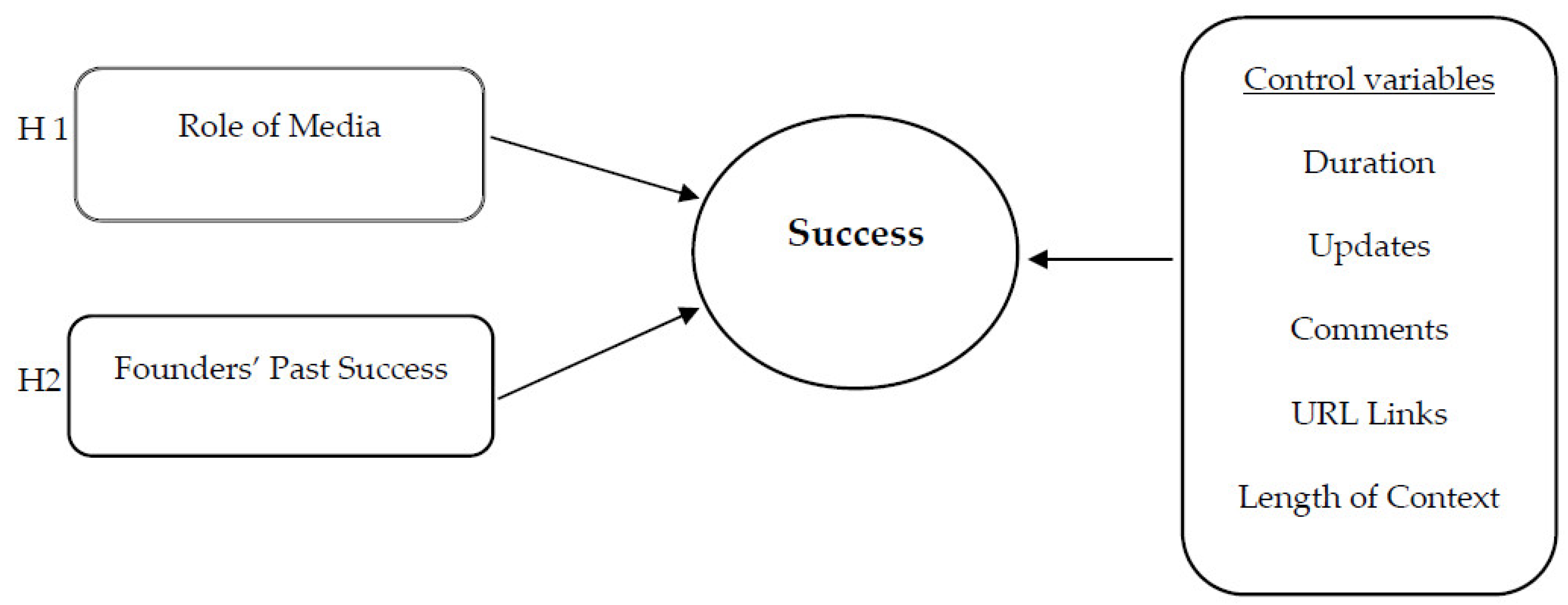

3. Research Hypotheses

3.1. Role of Media

3.2. Founder’s Past Experience

4. Data and Methods

4.1. Context Construction and Data Sample

4.2. Measures

4.2.1. Dependent Variables

4.2.2. Independent Variables

4.2.3. Control Variables

4.3. Methods

5. Empirical Results

5.1. Multicollinearity Analysis

5.2. Descriptive Statistics

5.3. Correlation Matrix

5.4. Multivariate Analysis

5.5. Discussion and Contributions

5.6. Robustness Tests

6. Conclusions Limitations, and Future Research

Author Contributions

Funding

Conflicts of Interest

References

- Amit, R.; Glosten, L.; Muller, E. Entrepreneurial Ability, Venture Investments, and Risk Sharing. Manag. Sci. 1990, 36, 1233–1246. [Google Scholar] [CrossRef]

- Evans, D.S.; Leighton, L.S. The Determinants of Changes in U.S. Self-Employment, 1968–1987. Small Bus. Econ. 1989, 1, 111–119. [Google Scholar] [CrossRef]

- Li, Y.; Chi, T. Venture Capitalists’ Decision to Withdraw: The Role of Portfolio Configuration from a Real Options Lens. Strateg. Manag. J. 2013, 34, 1351–1366. [Google Scholar] [CrossRef]

- Badulescu, D.; Simut, R.; Badulescu, A. Looking for Better Financing: A Quantitative Approach on Collateral Importance in SMEs Relationship Lending. In Proceedings of the 8th International Economic Conference on International Days of Statistics and Economics, Prague, Czech Republic, 11–13 September 2014; pp. 43–52. [Google Scholar]

- Bruton, G.; Khavul, S.; Siegel, D.; Wright, M. New Financial Alternatives in Seeding Entrepreneurship: Microfinance, Crowdfunding, and Peer-to-Peer Innovations. Entrep. Theory Pract. 2015, 39, 9–26. [Google Scholar] [CrossRef]

- Schwienbacher, A.; Larralde, B. Crowdfunding of Small Entrepreneurial Ventures. SSRN Electron. J. 2010. [Google Scholar] [CrossRef]

- Xu, L.; Wu, Q.; Du, P.; Qiao, X.; Tsai, S.B.; Li, D. Financing Target and Resale Pricing in Reward-Based Crowdfunding. Sustainability 2018, 10, 1. [Google Scholar] [CrossRef]

- Oba, B.; Atakan, S.; Kirezli, O. Value Creation in Crowdfunding Projects-Evidence from an Emerging Economy. J. Innov. Econ. 2018, 26, 37. [Google Scholar] [CrossRef]

- Belleflamme, P.; Lambert, T.; Schwienbacher, A. Crowdfunding: Tapping the Right Crowd. J. Bus. Ventur. 2014, 29, 585–609. [Google Scholar] [CrossRef]

- Kirmani, A.; Rao, A.R. No Pain, No Gain: A Critical Review of the Literature on Signaling Unobservable Product Quality. J. Mark. 2000, 64, 66–79. [Google Scholar] [CrossRef]

- Courtney, C.; Dutta, S.; Li, Y. Resolving Information Asymmetry: Signaling, Endorsement, and Crowdfunding Success. Entrep. Theory Pract. 2017, 41, 265–290. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Ley, A.; Weaven, S. Investigating the Agency Dynamics of Crowdfunding in Start-up Capital Financing. Acad. Entrep. J. 2011, 17, 85–111. [Google Scholar]

- Gulati, R.; Higgins, M.C. Which Ties Matter When? The Contingent Effects of Interorganizational Partnerships on IPO Success. Strateg. Manag. J. 2003, 24, 127–144. [Google Scholar] [CrossRef]

- Zuckerman, E.W. The Categorical Imperative: Illegitimacy Discount 1. Am. J. Sociol. 1999, 104, 1398–1438. [Google Scholar] [CrossRef]

- Hornuf, L.; Schwienbacher, A. Market Mechanisms and Funding Dynamics in Equity Crowdfunding. J. Corp. Financ. 2017, 50, 556–574. [Google Scholar] [CrossRef]

- Ahlers, G.K.C.; Cumming, D.; Günther, C.; Schweizer, D. Signaling in Equity Crowdfunding. Entrep. Theory Pract. 2015, 39, 955–980. [Google Scholar] [CrossRef] [Green Version]

- Vulkan, N.; Åstebro, T.; Sierra, M.F. Equity Crowdfunding: A New Phenomena. J. Bus. Ventur. Insights 2016, 5, 37–49. [Google Scholar] [CrossRef]

- Agrawal, A.; Catalini, C.; Goldfarb, A. The Geography of Crowdfunding. SSRN Electron. J. 2011. [Google Scholar] [CrossRef]

- Mollick, E. The Dynamics of Crowdfunding: An Exploratory Study. J. Bus. Ventur. 2014, 29, 1–16. [Google Scholar] [CrossRef]

- Turan, S.S. Financial Innovation—Crowdfunding: Friend or Foe? Procedia Soc. Behav. Sci. 2015, 195, 353–362. [Google Scholar] [CrossRef]

- Zott, C.; Huy, Q.N. How Entrepreneurs Use Symbolic Management to Acquire Resources. Adm. Sci. Q. 2007, 52, 70–105. [Google Scholar] [CrossRef]

- Bi, S.; Liu, Z.; Usman, K. The Influence of Online Information on Investing Decisions of Reward-Based Crowdfunding. J. Bus. Res. 2017, 71, 10–18. [Google Scholar] [CrossRef]

- Chen, X.-P.; Yao, X.; Kotha, S. Entrepreneur Passion and Preparedness in Business Plan Presentations: A Persuasion Analysis of Venture Capitalists’ Funding Decisions. Acad. Manag. J. 2009, 52, 199–214. [Google Scholar] [CrossRef]

- Ngoc, T.N. Crowdfunding in Vietnam: The Impact of Project and Founder Quality on Funding Success; University of Twente: Enschede, The Netherlands, 2017. [Google Scholar]

- Shane, S.; Cable, D. Network Ties, Reputation, and the Financing of New Ventures. Manag. Sci. 2002, 48, 364–381. [Google Scholar] [CrossRef] [Green Version]

- Stiglitz, J.E. The Contributions of the Economics of Information to Twentieth Century Economics. Q. J. Econ. 2000, 115, 1441–1478. [Google Scholar] [CrossRef]

- Gerber, E.M.; Hui, J.S.; Kuo, P.-Y. Crowdfunding: Why People Are Motivated to Post and Fund Projects on Crowdfunding Platforms. In Proceedings of the ACM Conference on Computer Supported Cooperative work, Seattle, WA, USA, 11–15 February 2012; pp. 1–10. [Google Scholar]

- Hornuf, L.; Schwienbacher, A. Funding Dynamics in Crowdinvesting. pp. 1–47. Available online: http://hdl.handle.net/10419/112969 (accessed on 25 October 2018).

- Moritz, A.; Block, J.; Lutz, E. Investor Communication in Equity-Based Crowdfunding: A Qualitative-Empirical Study. Qual. Res. Financ. Mark. 2015, 7, 309–342. [Google Scholar] [CrossRef]

- Burtch, G.; Ghose, A.; Wattal, S. The Hidden Cost of Accommodating Crowdfunder Privacy Preferences: A Randomized Field Experiment. Manag. Sci. 2015, 61, 949–962. [Google Scholar] [CrossRef] [Green Version]

- Gangi, F.; Daniele, L.M. Remarkable Funders: How Early-Late Backers and Mentors Affect Reward-Based Crowdfunding Campaigns. Int. Bus. Res. 2017, 10, 58. [Google Scholar] [CrossRef]

- Burtch, G.; Ghose, A.; Wattal, S. An Empirical Examination of the Antecedents and Consequences of Contribution Patterns in Crowd-Funded Markets. Inf. Syst. Res. 2013, 24, 499–519. [Google Scholar] [CrossRef]

- Agrawal, A.; Catalini, C.; Goldfarb, A. Are Syndicates the Killer App of Equity Crowdfunding? Calif. Manag. Rev. 2016, 58, 111–124. [Google Scholar] [CrossRef] [Green Version]

- Mavlanova, T.; Benbunan-Fich, R.; Koufaris, M. Signaling Theory and Information Asymmetry in Online Commerce. Inf. Manag. 2012, 49, 240–247. [Google Scholar] [CrossRef]

- Akerlof, G. The Market for “Lemons”: Quality Uncertainty and the Market Mechanism; Oxford University Press: Oxford, UK, 1970. [Google Scholar]

- Agrawal, A.; Catalini, C.; Goldfarb, A. Some Simple Economics of Crowdfunding; University of Chicago Press: Chicago, IL, USA, 2014; Volume 14. [Google Scholar] [CrossRef]

- Shun, Y.; Guodong, G.; Viswanathan, S. Strategic Behavior in Online Reputation Systems: Evidence from Revoking on Ebay1. MIS Q. 2014, 38, 1033–1056. [Google Scholar]

- Wessel, M.E. Crowdfunding: Platform Dynamics under Asymmetric Information. Ph.D. Thesis, Technischen Universität Darmstadt, Darmstadt, Germany, 2016. [Google Scholar]

- Tomboc, G.F.B. The Lemons Problem in Crowdfunding. Inf. Technol. Priv. Law 2013, 30, 253–279. [Google Scholar]

- Mollick, E.R. Delivery Rates on Kickstarter. SSRN Electron. J. 2015. [Google Scholar] [CrossRef] [Green Version]

- Wessel, M.; Thies, F.; Benlian, A. The Effects of Relinquishing Control in Platform Ecosystems: Implications from a Policy Change on Kickstarter; International Conference of Information Systems: Ft. Worth, TX, USA, 2015. [Google Scholar]

- Ghazawneh, A.; Henfridsson, O. Balancing Platform Control and External Contribution in Third-Party Development: The Boundary Resources Model. Inf. Syst. J. 2013, 23, 173–192. [Google Scholar] [CrossRef]

- Benlian, A.; Hilkert, D.; Hess, T. How Open Is This Platform? The Meaning and Measurement of Platform Openness from the Complementors’ Perspective. J. Inf. Technol. 2015, 30, 209–228. [Google Scholar] [CrossRef]

- Micheal, S. Job Market Signaling. Q. J. Econ. 1973, 87, 355–374. [Google Scholar] [CrossRef]

- Spence, M. Signaling in Retrospect and the Informational Structure of Markets. Am. Econ. Rev. 2002, 92, 434–459. [Google Scholar] [CrossRef]

- Stiglitz, J.E. The Theoy of Screening, Education, the Distribution of Income. Am. Econ. Rev. 1975, 65, 283–300. [Google Scholar] [CrossRef]

- Crosetto, P.; Regner, T. It’s Never Too Late: Funding Dynamics and Self Pledges in Reward-Based Crowdfunding. Res. Policy 2018, 47, 1463–1477. [Google Scholar] [CrossRef]

- Colombo, M.G.; Franzoni, C.; Rossi-Lamastra, C. Internal Social Capital and the Attraction of Early Contributions in Crowdfunding. Entrep. Theory Pract. 2014, 39, 75–100. [Google Scholar] [CrossRef]

- Polzin, F.; Toxopeus, H.; Stam, E. The Wisdom of the Crowd in Funding: Information Heterogeneity and Social Networks of Crowdfunders. Small Bus. Econ. 2018, 50, 251–273. [Google Scholar] [CrossRef]

- Hobbs, J.; Grigore, G.; Molesworth, M. Success in the Management of Crowdfunding Projects in the Creative Industries. Internet Res. 2016, 26, 146–166. [Google Scholar] [CrossRef]

- Beckman, C.M.; Burton, M.D.; O’Reilly, C. Early Teams: The Impact of Team Demography on VC Financing and Going Public. J. Bus. Ventur. 2007, 22, 147–173. [Google Scholar] [CrossRef]

- Gompers, P.; Kovner, A.; Lerner, J.; Scharfstein, D. Venture Capital Investment Cycles: The Impact of Public Markets. J. Financ. Econ. 2008, 87, 1–23. [Google Scholar] [CrossRef]

- Burton, M.D.; Sørensen, J.B.; Beckman, C.M. Coming from Good Stock: Career Histories and New Venture Formation. Res. Sociol. Organ. 2002, 19, 229–262. [Google Scholar]

- Hsu, D.H. Experienced Entrepreneurial Founders, Organizational Capital, and Venture Capital Funding. Res. Policy 2007, 36, 722–741. [Google Scholar] [CrossRef]

- Crowdfunder. Available online: https://www.crowdfunder.co.uk/about-us/ (accessed on 4 December 2017).

- Rutland, H. £50,000,000 Raised by the Crowd!Crowdfunder Stories. Available online: https://www.crowdfunder.co.uk/stories/50000000-raised-by-the-crowd/ (accessed on 13 April 2018).

- Crowdfunder. Crowdfunding-How to Guide; Crowdfunder: Newquay, UK, 2015; Available online: http://www.crowdfunder.co.uk/uploads/Content/cfuk_a4_crowdfunding_for_crowdfunders-vd-interactive.pdf (accessed on 14 April 2018).

- Dorfleitner, G.; Priberny, C.; Schuster, S.; Stoiber, J.; Weber, M.; de Castro, I.; Kammler, J. Description-Text Related Soft Information in Peer-to-Peer Lending—Evidence from Two Leading European Platforms. J. Bank. Financ. 2016, 64, 169–187. [Google Scholar] [CrossRef]

- Lukkarinen, A.; Teich, J.E.; Wallenius, H.; Wallenius, J. Success Drivers of Online Equity Crowdfunding Campaigns. Decis. Support Syst. 2016, 87, 26–38. [Google Scholar] [CrossRef]

- Parhankangas, A.; Renko, M. Linguistic Style and Crowdfunding Success among Social and Commercial Entrepreneurs. J. Bus. Ventur. 2017, 32, 215–236. [Google Scholar] [CrossRef]

- Lodhia, S. Web Based Social and Environmental Communication in the Australian Minerals Industry: An Application of Media Richness Framework. J. Clean. Prod. 2012, 25, 73–85. [Google Scholar] [CrossRef]

- Sun, P.C.; Cheng, H.K. The Design of Instructional Multimedia in E-Learning: A Media Richness Theory-Based Approach. Comput. Educ. 2007, 49, 662–676. [Google Scholar] [CrossRef]

- Rockmann, K.W.; Northcraft, G.B. To Be or Not to Be Trusted: The Influence of Media Richness on Defection and Deception. Organ. Behav. Hum. Decis. Process. 2008, 107, 106–122. [Google Scholar] [CrossRef]

- Anderson, J.C.; Hernandez, S.; Jessup, E.L.; North, E. Perceived Safe and Adequate Truck Parking: A Random Parameters Binary Logit Analysis of Truck Driver Opinions in the Pacific Northwest. Int. J. Transp. Sci. Technol. 2018, 7, 89–102. [Google Scholar] [CrossRef]

- Skirnevskiy, V.; Bendig, D.; Brettel, M. The Influence of Internal Social Capital on Serial Creators’ Success in Crowdfunding. Entrep. Theory Pract. 2017, 41, 209–236. [Google Scholar] [CrossRef]

- Josefy, M.; Dean, T.J.; Albert, L.S.; Fitza, M.A. The Role of Community in Crowdfunding Success: Evidence on Cultural Attributes in Funding Campaigns to “Save the Local Theater. ” Entrep. Theory Pract. 2017, 41, 161–182. [Google Scholar] [CrossRef]

- Smith, D.A.; Brame, R. Tobit Models in Social Science Research: Some Limitations and a More General Alternative. Sociol. Methods Res. 2003, 31, 364–388. [Google Scholar] [CrossRef]

- Giudici, G.; Guerini, M.; Rossi-Lamastra, C. Reward-Based Crowdfunding of Entrepreneurial Projects: The Effect of Local Altruism and Localized Social Capital on Proponents’ Success. Small Bus. Econ. 2018, 50, 307–324. [Google Scholar] [CrossRef]

- Lin, T.-C.; Pursiainen, V. Fund What You Trust? Social Capital and Moral Hazard in Crowdfunding. SSRN Electronic J. 2018. [Google Scholar] [CrossRef]

- Peter, K. A Guide to Econometrics; Blackwell Publishing: Oxford, UK, 2008; Volume 91. [Google Scholar]

- Fong, E.A.; Xing, X.; Orman, W.H.; Mackenzie, W.I. Consequences of Deviating from Predicted CEO Labor Market Compensation on Long-Term Firm Value. J. Bus. Res. 2015, 68, 299–305. [Google Scholar] [CrossRef]

- Henderson, A.D.; Fredrickson, J.W. Top Management Team Coordination Needs and Test of the Ceo Pay Gap: A Competitive Economic and Behavioral Views. Acad. Manag. J. 2001, 44, 96–117. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis; Pearson Education Limited: Harlow, UK, 2010. [Google Scholar]

- Liu, L.; Suh, A.; Wagner, C. Empathy or Perceived Credibility? An Empirical Study on Individual Donation Behavior in Charitable Crowdfunding. Internet Res. 2018, 28, 623–651. [Google Scholar] [CrossRef]

- Steigenberger, N.; Wilhelm, H. Extending Signaling Theory to Rhetorical Signals: Evidence from Crowdfunding. Organ. Sci. 2018, 29, 529–546. [Google Scholar] [CrossRef]

- Cholakova, M.; Clarysse, B. Does the Possibility to Make Equity Investments in Crowdfunding Projects Crowd Out Reward-Based Investments? Entrep. Theory Pract. 2015, 39, 145–172. [Google Scholar] [CrossRef]

- Mollick, E.; Nanda, R. Wisdom or Madness? Comparing Crowds with Expert Evaluation in Funding the Arts. Manag. Sci. 2015, 62, 1533–1553. [Google Scholar] [CrossRef]

- Boyce, M.S.; Vernier, P.R.; Nielsen, S.E.; Schmiegelow, F.K.A. Evaluating Resource Selection Functions. Ecol. Model. 2002, 157, 281–300. [Google Scholar] [CrossRef]

- Coffey, C.S.; Hebert, P.R.; Ritchie, M.D.; Krumholz, H.M.; Gaziano, J.M.; Ridker, P.M.; Brown, N.J.; Vaughan, D.E.; Moore, J.H. An Application of Conditional Logistic Regression and Multifactor Dimensionality Reduction for Detecting Gene-Gene Interactions on Risk of Myocardial Infarction: The Importance of Model Validation. BMC Bioinform. 2004, 5, 49. [Google Scholar] [CrossRef]

- Dreiseitl, S.; Ohno-Machado, L. Logistic Regression and Artificial Neural Network Classification Models: A Methodology Review. J. Biomed. Inform. 2002, 35, 352–359. [Google Scholar] [CrossRef]

- Steyerberg, E.W.; Harrell, F.E.; Borsboom, G.J.J.; Eijkemans, M.J.; Vergouwe, Y.; Habbema, J.D.F. Internal Validation of Predictive Models. J. Clin. Epidemiol. 2001, 54, 774–781. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Author of the Paper | Focus Area | Research Gap | Theoretical Stance | Paradigm/Method | Sample | Findings |

|---|---|---|---|---|---|---|

| Mollick [20] | Exploring the dynamics of crowdfunding and how it operates (drivers of success, the impact of geography, post-funding behaviors) | Using a large dataset, an attempt to avail an analytical understanding of the dynamics of crowdfunding. | The role of key quality signals. Impact of network size in providing connections and endorsing quality. The influence of geography on crowdfunding parameters. | Analyze the data through logistic regression and used STATA for distance information and the Cox model for delays in delivery. | A total of 48,526 projects for a time period of two years (2009 to 07/2012) have been extracted from the crowdfunding platform called Kickstarter across all categories. | Project quality (such as the presence of video, updates and spelling correctness) and personal networks (Facebook friends) are positively related to the success of fundraising. Both project type and funding success are influenced by geography. The majority of founders try to fulfill their promise to funders, but mostly not in a timely manner, with longer delays found in larger and overfunded projects |

| Courtney et al. [11] | Examines when signals and third-party endorsement, obtained from multiple sources that improve or diminish one another’s effect. | Signals through start-up actions and characteristics can mitigate information asymmetry concerns about project quality and founder credibility. | Signals originating from the start-up, endorsement originating from third parties, the interplay of signals and third-party endorsement. | Analyze the data through logistic regression, two-stage Heckman procedure, and first stage probit model. | A total of 170,248 projects from 4/2009 to 12/2015 were extracted from the crowdfunding platform called Kickstarter across all categories. | Both start-up originating signals and third-party endorsement mitigate information asymmetry concerns about project quality and founder credibility. |

| Crosetto and Regner [48] | Exploring the dynamics of funding and pledgers’ motivations. | An attempt to avail an analytical understanding about project-level and pledge-level variables in crowdfunding. | Crowdfunding and innovation, empirical studies on crowdfunding. | Normalized project time, descriptive statistics, linear regression, questionnaire, and interviews. | A total of 2254 projects extracted from German platform called Startnext from 10/2010 to 2/2014. | Majority of the projects that eventually succeed are not on a successful track at 75% of their funding period. And late successes are basically boosted by an information cascade during the final 25% of the funding duration. Results from interviews and questionnaires prove that project communication efforts play a role in making a project successful. |

| Colombo et al. [49] | Why early contributions are so necessary for crowdfunding success? What are the core factors that attract early contributions? | Investigating the relationship between early support (in forms of capital and backers) and final success. Furthermore, examining the role of social capital in crowdfunding via fascinating early contributions. | Uncertainties and information asymmetries at the initial stage of crowdfunding. The role of early contributions and internal social capital in attracting initial funding. | Analyze the data through the Probit and Tobit model. | Extracted a total of 669 projects in four categories, namely design, technology, film, and video and also video games from Kickstarter, covering the time period from 10/2012 to 01/2013. | Concluded that internal social capital is critical in raising funds and engaging funders in the initial phase of crowdfunding of a project. It is reported that there is a positive relationship between early contributions and probability of final success hence, they mediate the influence of internal social capital on project success. |

| Polzin et al. [50] | How does the type of information used by crowdfunders vary with the strength of their ties to the project? | Empirically tested the heterogeneity between in-crowd and out-crowd funders by analyzing large scale data through a survey among project funders. | Signaling in early-stage finance and information cascades, in-crowd information needs and out-crowd information need. | Descriptive Statistics, factor analysis and logistic regression. | A total of 283 observations assessed through 5-point Likert scale questionnaire. | Concluded that in-ward investors rely more on information about the project creator than out-crowd investors. Out-crowd investors do not give more importance to the information about the project itself than in-crowd investors. |

| Ahlers et al. [17] | How do venture quality (human, social, and intellectual capital) and uncertainty level (equity share, financial projections) impact crowdfunding success? | Empirically examine the impact of signals used by entrepreneurs to motivate investors, and to contribute an equity-based crowdfunding project. | Information asymmetries in crowdfunding. Signaling values of venture quality attributes and indicators of uncertainty that impact on the probability of success. | Analyze the data through Univariate analysis, binomial regression, Ordinary Least Square (OLS) regression, and exponential hazard models. | A total of 104 campaigns published on ASSOB from 10/2006 to 10/2011. | Regarding venture quality signals, human capital is positively related to funding success; whereas less evidence available in supporting the role of social capital and intellectual capital. Retaining equity and providing detailed financial forecasts can act as effective signals to decrease information asymmetry and therefore increase the likelihood of success. |

| Bi et al. [23] | What is the impact of online information on investing decisions in reward-based crowdfunding? | Introducing the elaboration likelihood model to crowdfunding literature and investigating which type of online information has a resilient impact on investment behavior. | Elaboration likelihood model: central route (project quality signals) and peripheral route (electronic word-of-mouth). Which route, and information can influence the decision to invest? | Hierarchical multiple regression for the full sample and for each project category. | A total of 999 projects extracted from a Chinese platform called zhongchou.com in the categories of Science & Technology, Art, Entertainment, and Agriculture. | Explanatory description of texts and higher video counts higher project quality signals; more “Like” and reviews suggest better electronic word-of-mouth. Generally, the effects of the central route and peripheral factors on investors’ funding decisions are almost equal. |

| Oba et al. [8] | If a project is successful, then it creates a value proposition and signals it effectively. | Analyze the platform reputation, reward attributed and characteristics of project owner. | Signaling theory and information asymmetry, ecosystem of crowdfunding in Turkey. | Descriptive statistics, univariate analysis (t-test), ANOVA, regression analysis. | A total of 354 campaigns extracted from three Turkish crowdfunding platforms e.g., Fongogo, Fonlabeni and crowdFON. | They concluded that platform reputation and entrepreneurial capacity of the project owner are strongly associated with success of the project. |

| Gangi and Daniele [32] | How early-late backers and mentors affect reward-based crowdfunding campaigns. | Resolving the information asymmetry barriers among insiders and outsiders in determining the campaign success. | Impact of early-late backers. Impact of project mentor. | Descriptive statistics and multivariate analysis. | A total of 578 campaigns extracted from two Italian platforms e.g., Produzioni dal basso and Eppala. | They concluded that both type of funders are remarkably important for the project success. |

| Variables | Mean | Min | Max | Standard Deviation |

|---|---|---|---|---|

| Fully funded | 0.32 | 0 | 1.00 | 0.46 |

| No. of backers | 33.40 | 0 | 4913.00 | 118.98 |

| Funding amount | £1782.24 | 1 | 367,200.00 | 8356.76 |

| Role of media | 0.84 | 0 | 3.00 | 1.07 |

| Founder’s past success | 0.25 | 0 | 1.96 | 0.18 |

| Duration (days) | 37.85 | 0 | 1000.00 | 19.20 |

| Length of the context | 2238.97 | 0 | 24,506.00 | 2116.32 |

| Updates | 0.89 | 0 | 41.00 | 2.44 |

| Comments | 0.26 | 0 | 2.50 | 0.39 |

| URL links | 0.15 | 0 | 1.86 | 0.27 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) |

|---|---|---|---|---|---|---|---|---|---|---|

| Fully Funded (1) | 1 | |||||||||

| No. of Backers (2) | 0.218 ** (0.000) | 1 | ||||||||

| Funding Amount (3) | 0.180 ** (0.000) | 0.572 ** (0.000) | 1 | |||||||

| Role of Media (4) | 0.174 ** (0.000) | 0.117 ** (0.000) | 0.146 ** (0.000) | 1 | ||||||

| Founder’s Past Success (5) | 0.112 ** (0.000) | 0.026 ** (0.001) | 0.013 (0.120) | 0.064 ** (0.000) | 1 | |||||

| Duration (6) | −0.152 ** (0.000) | −0.007 (0.422) | 0.021 * (0.010) | 0.087 ** (0.000) | −0.019 * (0.022) | 1 | ||||

| Updates (7) | 0.242 ** (0.000) | 0.313 ** (0.000) | 0.281 ** (0.000) | 0.238 ** (0.000) | 0.020 * (0.013) | 0.053 ** (0.000) | 1 | |||

| Comments (8) | 0.369 ** (0.000) | 0.379 ** (0.000) | 0.299 ** (0.000) | 0.184 ** (0.000) | 0.162 ** (0.000) | −0.057 ** (0.000) | 0.294 ** (0.000) | 1 | ||

| URL Links (9) | 0.174 ** (0.000) | 0.152 ** (0.000) | 0.158 ** (0.000) | 0.329 ** (0.000) | 0.062 ** (0.000) | 0.023 ** (0.004) | 0.217 ** (0.000) | 0.153 ** (0.000) | 1 | |

| Length of the Context (10) | 0.165 ** (0.000) | 0.202 ** (0.000) | 0.233 ** (0.000) | 0.399 ** (0.000) | 0.022 ** (0.008) | 0.088 ** (0.000) | 0.337 ** (0.000) | 0.245 ** (0.000) | 0.439 ** (0.000) | 1 |

| DV Method | I | II | III |

|---|---|---|---|

| Number of Backers | Funding Amount | Fully Funded | |

| Tobit | Tobit | Logistic reg. | |

| B(SE) | B(SE) | B(SE) | |

| Role of media | 0.076 *** (0.012) | 0.068 *** (0.011) | 0.129 *** (0.020) |

| Founders’ past success | 0.457 *** (0.064) | 0.282 *** (0.061) | 0.771 *** (0.109) |

| Duration | −1.101 *** (0.052) | −0.832 *** (0.049) | −1.854 *** (0.091) |

| Updates | 0.888 *** (0.045) | 0.891 *** (0.040) | 1.533 *** (0.076) |

| Comments | 0.983 *** (0.032) | 0.940 *** (0.028) | 1.637 *** (0.054) |

| URL Links | 0.393 *** (0.046) | 0.381 *** (0.042) | 0.602 *** (0.077) |

| Length of context | 0.060 (0.035) | 0.103 ** (0.034) | 0.123 * (0.061) |

| Constant | 0.358 * (0.126) | −0.259 * (0.121) | 0.562 ** (0.217) |

| Sigma | 0.404 *** | 1.172 *** | |

| Observations | 14,887 | 14,887 | 14,887 |

| Uncensored | 10,101 | 10,102 | |

| Left-censored | 4786 | 4785 | |

| Mean VIF | 1.891 | 3.358 | |

| Maximum VIF | 3.267 | 3.928 | |

| Likelihood Chi 2 | 9445 | 7,944 | |

| McFadden’s pseudo R2 | 0.170 | ||

| Nagelkerke pseudo R2 | 0.269 |

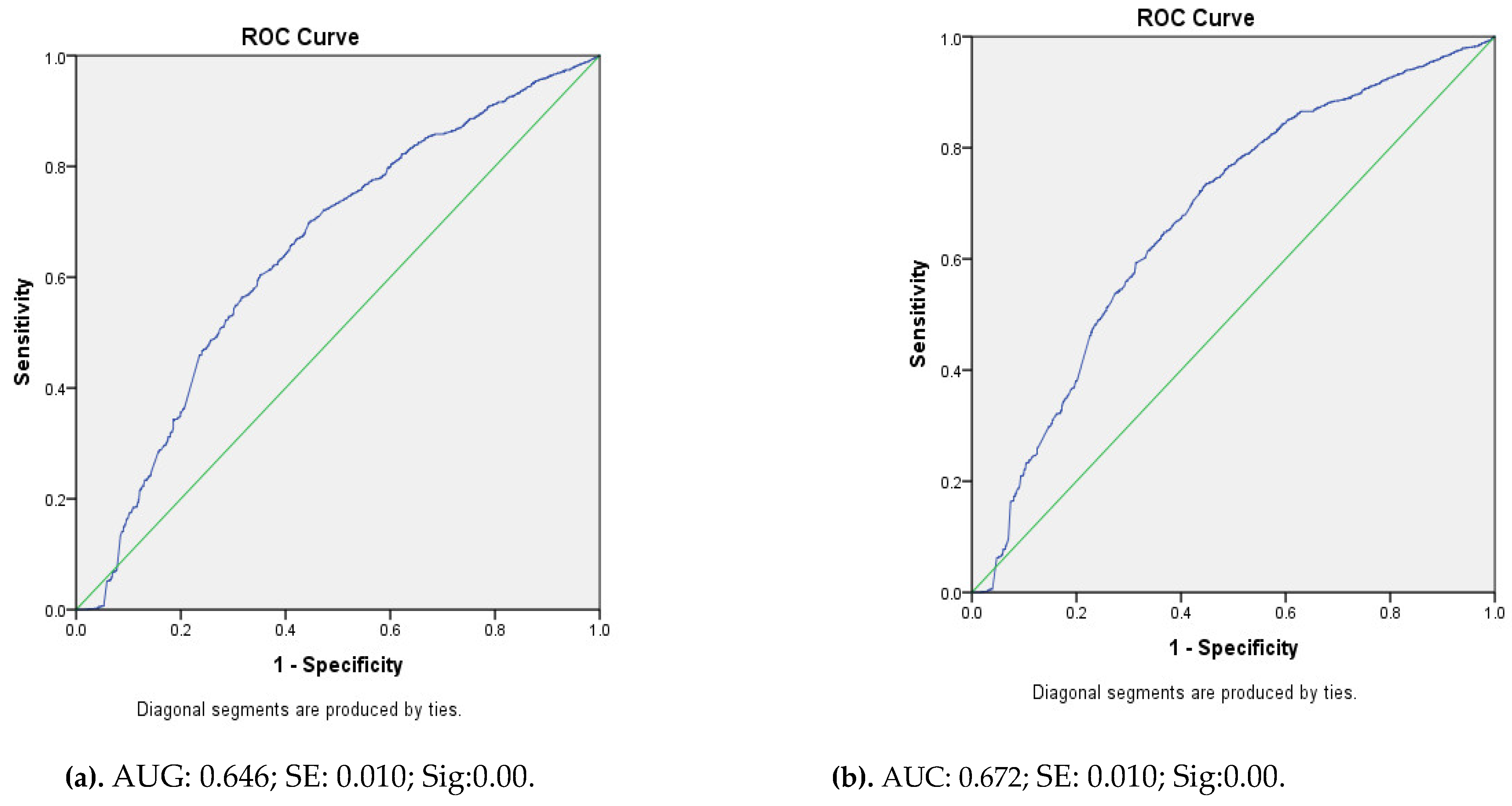

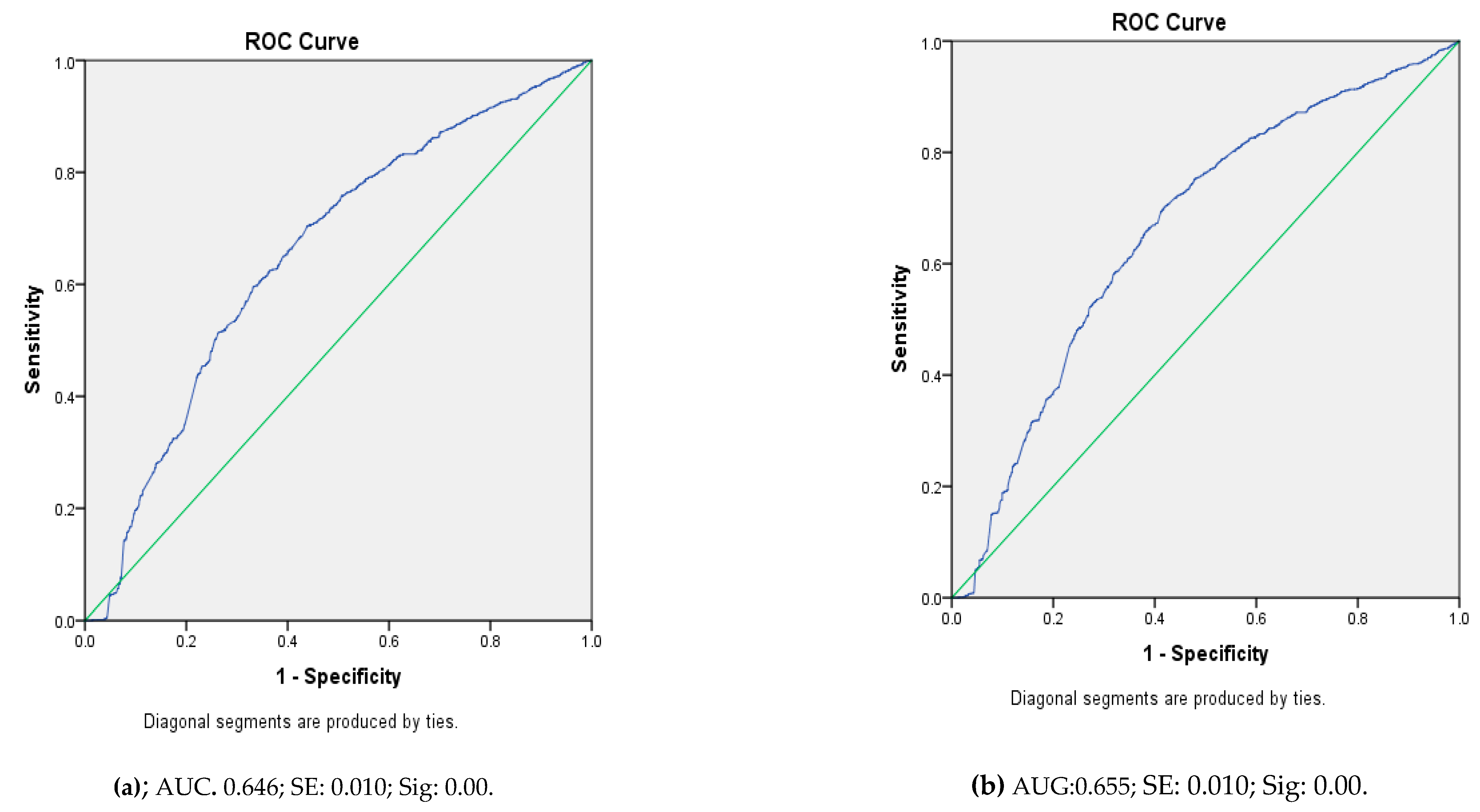

| Validation Dataset | ||||

|---|---|---|---|---|

| Subsample 1 | Subsample 2 | Subsample 3 | Subsample 4 | |

| AUC | 0.646 | 0.672 | 0.655 | 0.662 |

| SE a | 0.010 | 0.010 | 0.010 | 0.010 |

| Sig b | 0.00 | 0.00 | 0.00 | 0.00 |

| Bootstrap a | ||||||

|---|---|---|---|---|---|---|

| Sig. | 95% CI | |||||

| B | Bias | SE | (2-tailed) | Upper | Lower | |

| Media | 0.129 | 0.000 | 0.021 | 0.001 | 0.090 | 0.171 |

| Founders Past Success | 0.771 | 0.004 | 0.113 | 0.001 | 0.565 | 0.994 |

| Duration | −1.854 | −0.002 | 0.094 | 0.001 | −2.039 | −1.665 |

| Updates | 1.533 | 0.004 | 0.080 | 0.001 | 1.391 | 1.705 |

| Comments | 1.637 | 0.002 | 0.055 | 0.001 | 1.529 | 1.747 |

| URL Links | 0.602 | −0.001 | 0.080 | 0.001 | 0.451 | 0.768 |

| Length of Context | 0.123 | −0.001 | 0.061 | 0.041 | 0.008 | 0.244 |

| Constant | 0.562 | 0.002 | 0.221 | 0.015 | 0.112 | 0.978 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Usman, S.M.; Bukhari, F.A.S.; Usman, M.; Badulescu, D.; Sial, M.S. Does the Role of Media and Founder’s Past Success Mitigate the Problem of Information Asymmetry? Evidence from a UK Crowdfunding Platform. Sustainability 2019, 11, 692. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030692

Usman SM, Bukhari FAS, Usman M, Badulescu D, Sial MS. Does the Role of Media and Founder’s Past Success Mitigate the Problem of Information Asymmetry? Evidence from a UK Crowdfunding Platform. Sustainability. 2019; 11(3):692. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030692

Chicago/Turabian StyleUsman, Sardar Muhammad, Farasat Ali Shah Bukhari, Muhammad Usman, Daniel Badulescu, and Muhammad Safdar Sial. 2019. "Does the Role of Media and Founder’s Past Success Mitigate the Problem of Information Asymmetry? Evidence from a UK Crowdfunding Platform" Sustainability 11, no. 3: 692. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030692