Empirical Analysis of the Driving Factors of China’s ‘Land Finance’ Mechanism Using Soft Budget Constraint Theory and the PLS-SEM Model

Abstract

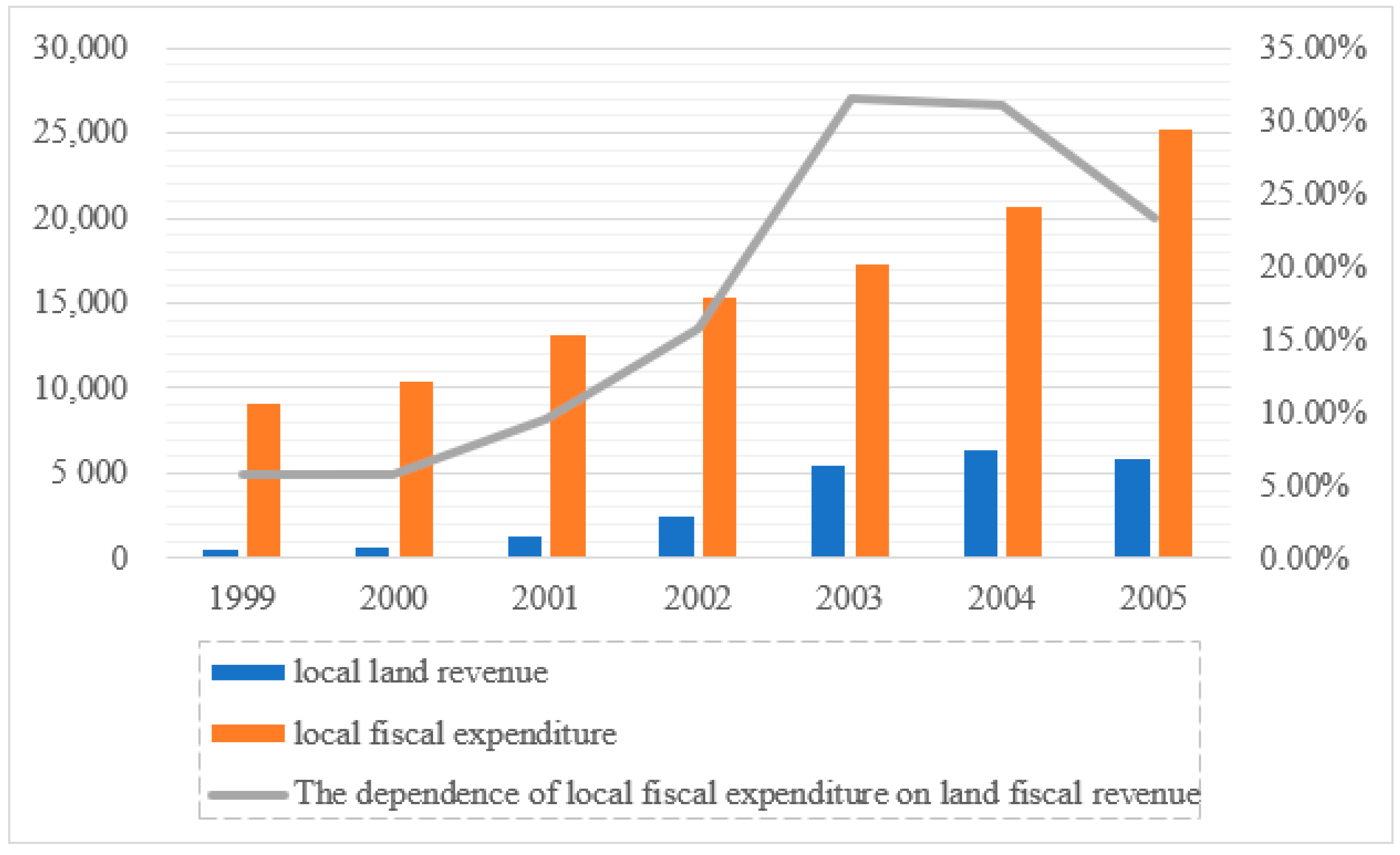

:1. Introduction

2. Literature Review

3. Theoretical Framework and Hypothesis Development

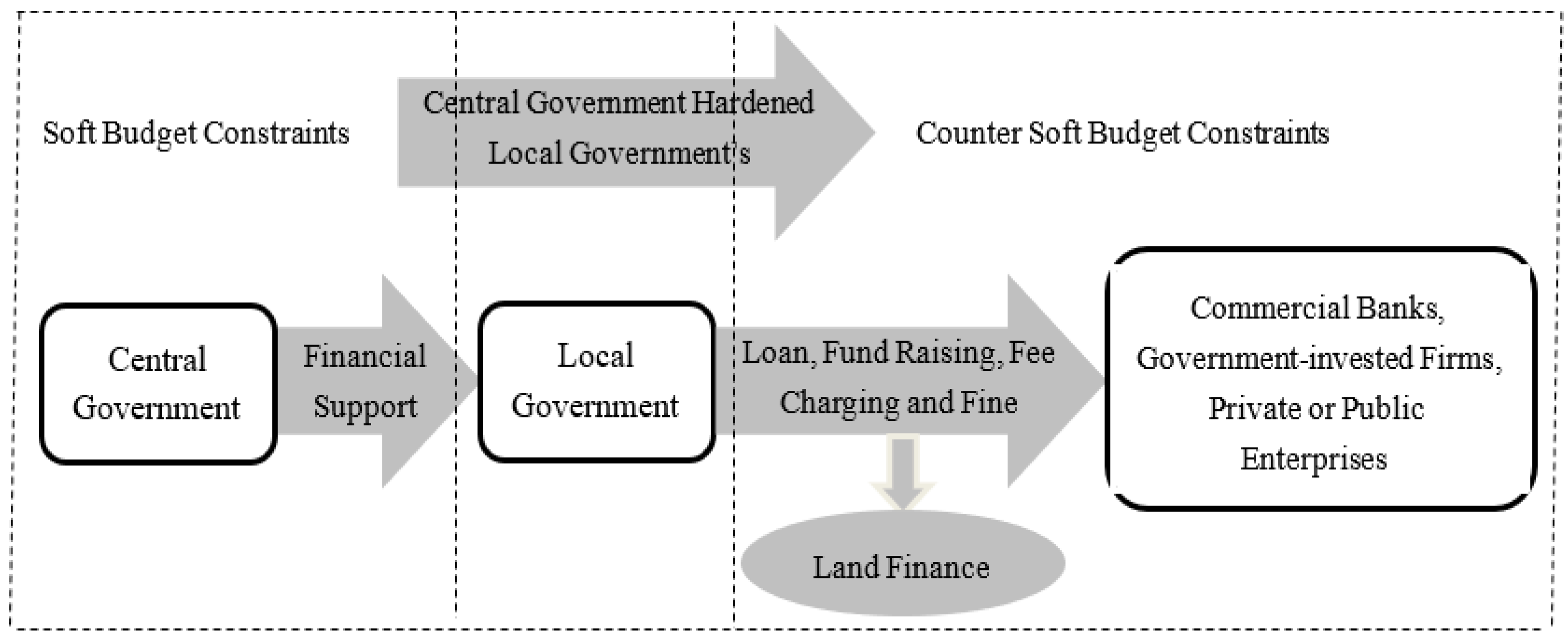

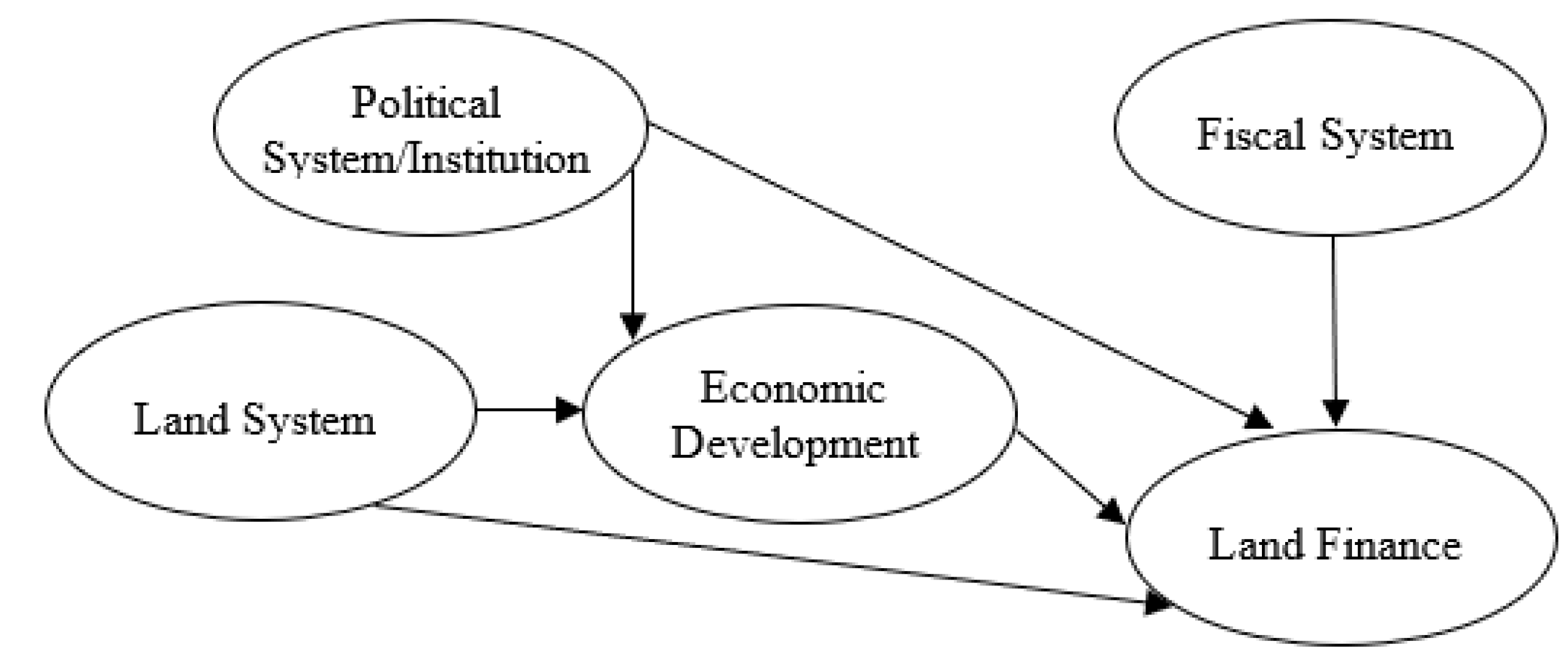

3.1. Theoretical Underpinnings

3.2. Hypotheses

3.3. Several Hypotheses on Land Financing are Proposed for Testing Based on SBC Theory

4. Data and Research Method

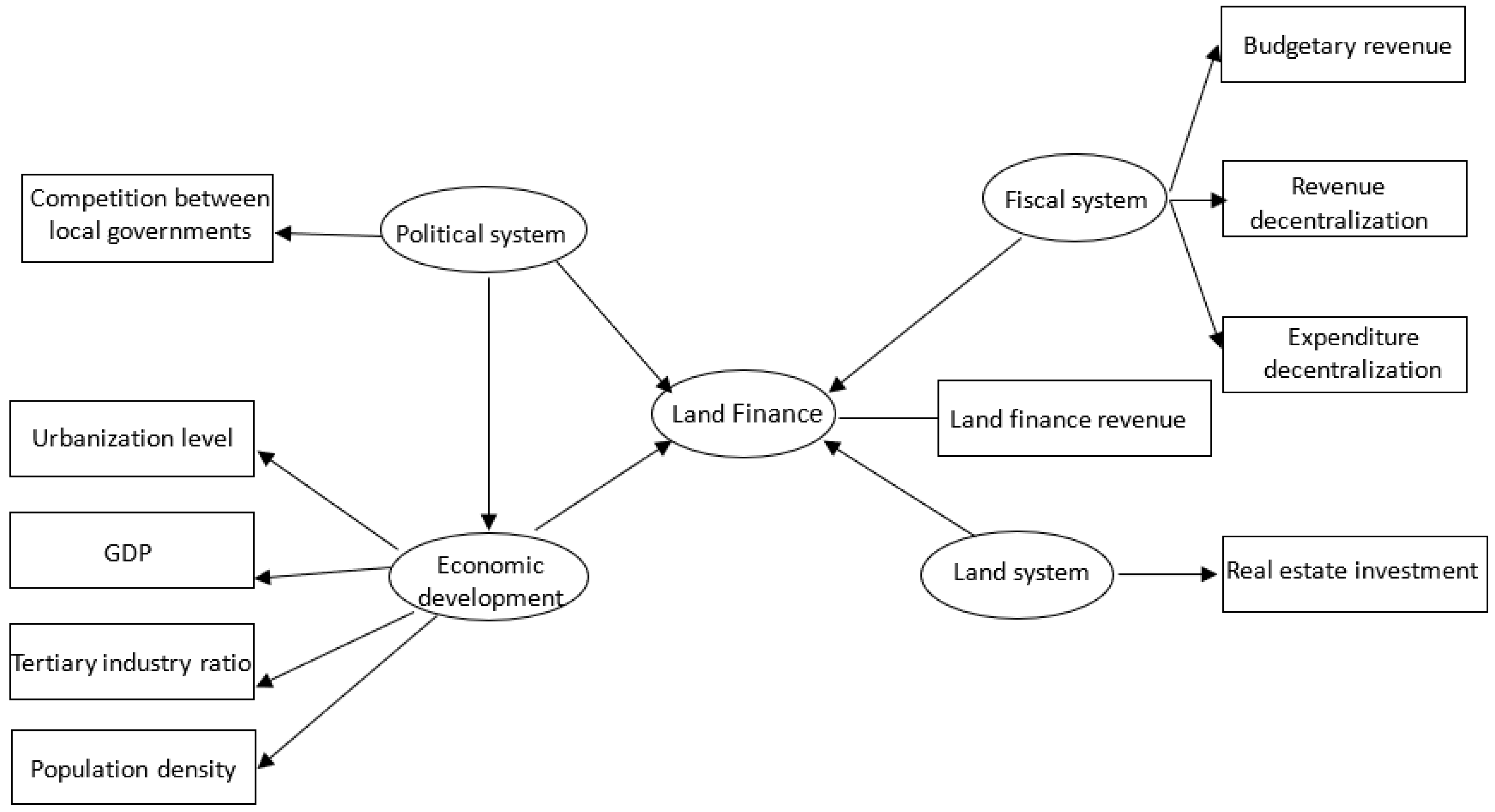

4.1. Indicator

4.1.1. Endogenous Indicators

4.1.2. Exogenous Indicators

4.2. Data Source

4.3. Research Method

5. Results and Discussion

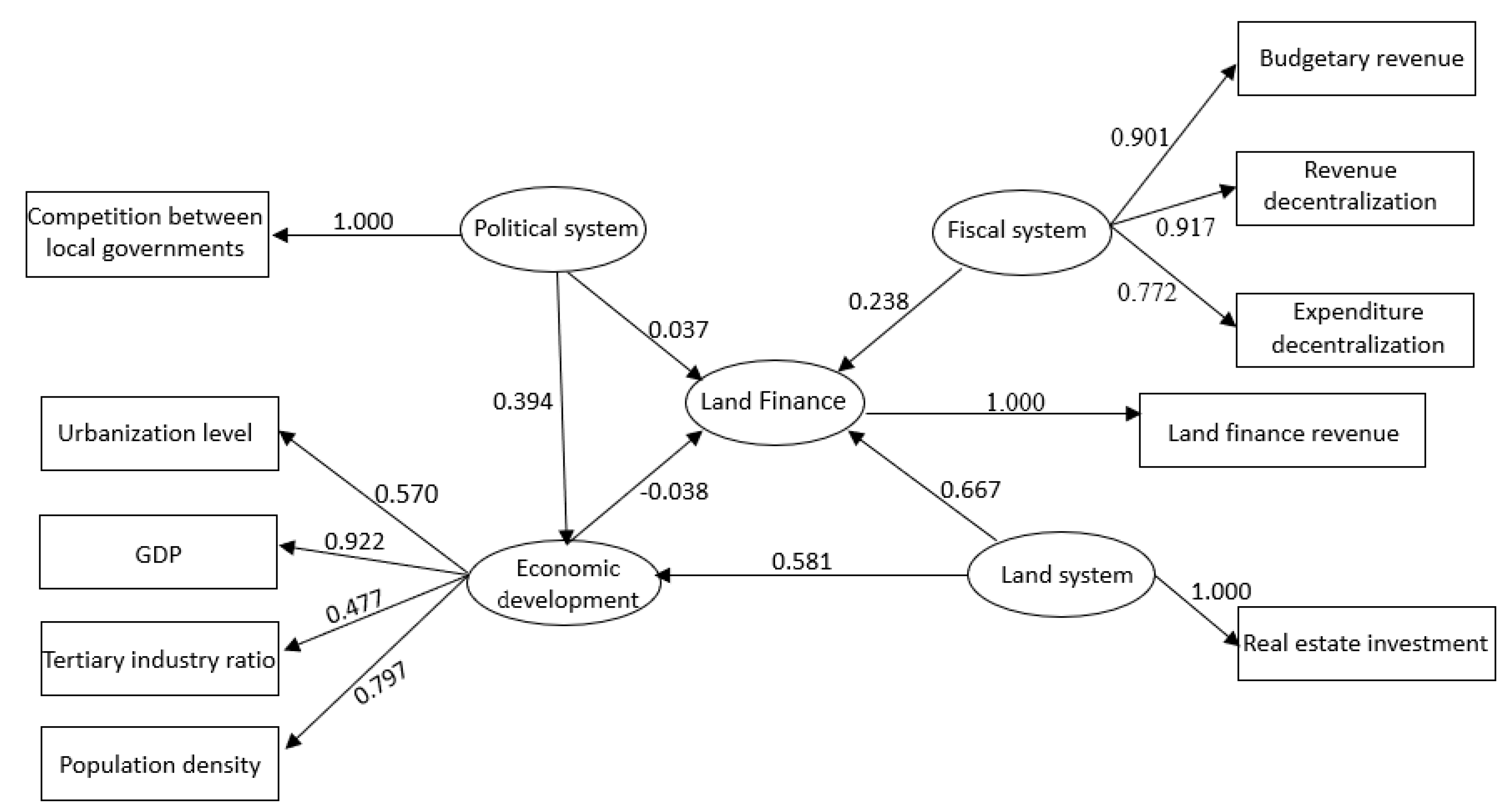

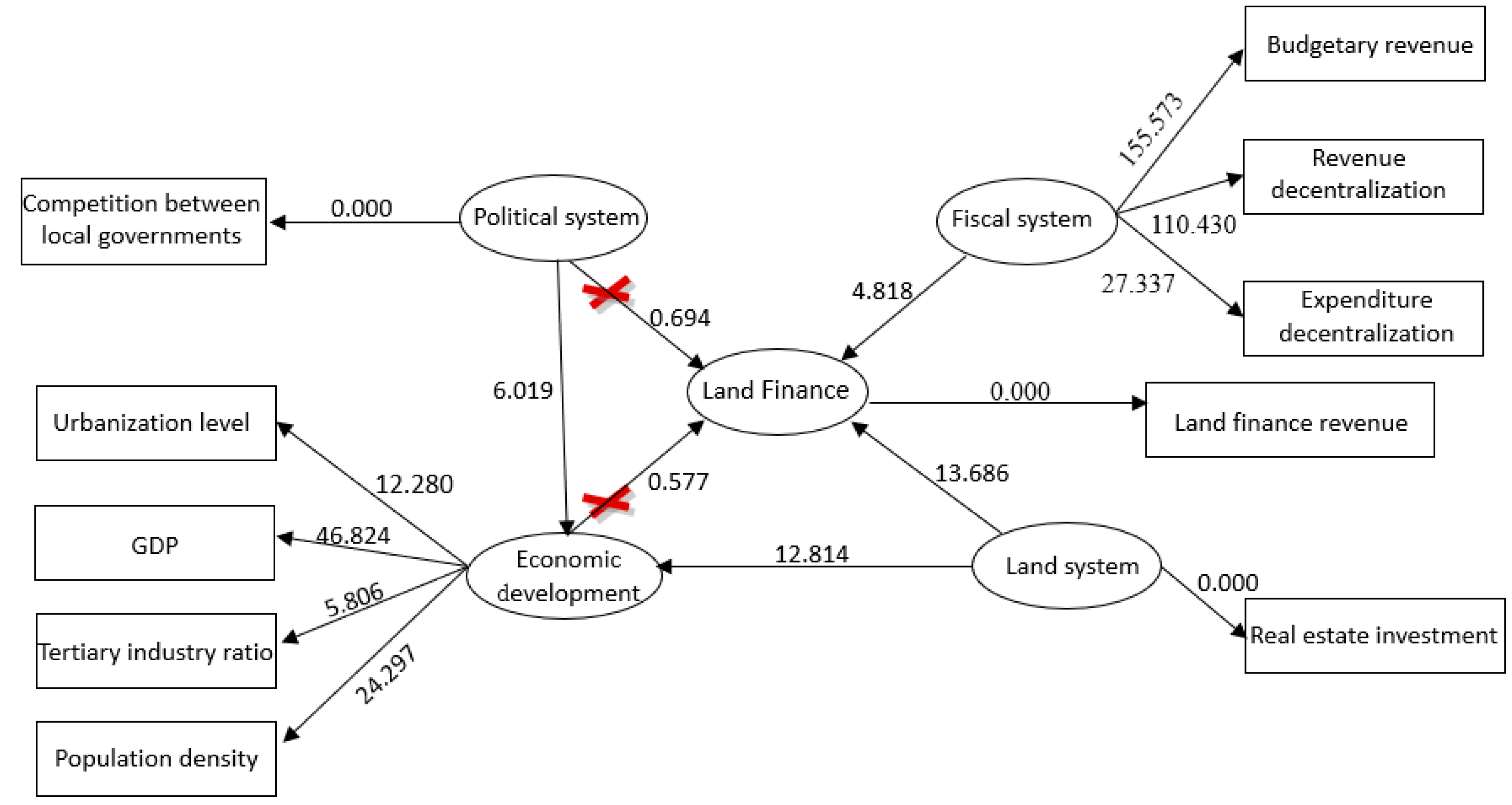

5.1. External Examination of the Model

5.2. Internal Examination of the Model

5.3. Results and Analysis

5.3.1. Economic Development Has an Insignificant Influence on Land Finance

5.3.2. The Fiscal System Has a Significant Positive Correlation with Land Finance

5.3.3. The Land System Correlates Positively and Significantly with Land Finance

5.3.4. The Land Systems Bears Significant Positive Correlation with Economic Development

5.3.5. The Political System Has an Insignificant Influence on Land Finance

5.3.6. The Political System Has a Significant Positive Impact on Economic Development

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Wu, Q.; Li, Y.; Yan, S. The incentives of China’s urban land finance. Land Use Policy 2015, 42, 432–442. [Google Scholar]

- Jia, K.; Su, J. The reform of the division of powers between central and local governments. Res. Financ. Econ. Issues 2016, 71–77. (In Chinese) [Google Scholar]

- Cai, M. Land for welfare in China. Land Use Policy 2016, 55, 1–12. [Google Scholar] [CrossRef] [Green Version]

- Wei, Y.; Lam, P.T.I.; Chiang, Y.H.; Leung, B.Y.P. The effects of monetary policy on real estate investment in China: A regional perspective. Int. J. Strateg. Prop. Manag. 2014, 18, 368–379. [Google Scholar] [CrossRef]

- Tsai, P.H. Fiscal incentives and political budget cycles in China. Int. Tax Public Financ. 2016, 23, 1–44. [Google Scholar] [CrossRef]

- Baskaran, T.; Feld, L.P.; Schnellenbach, J. Fiscal federalism, decentralization, and economic growth: A meta-analysis. Econ. Inq. 2016, 54, 103–133. [Google Scholar] [CrossRef]

- Wang, W.; Ye, F. The political economy of land finance in China. Public Budg. Financ. 2016, 36, 91–110. [Google Scholar] [CrossRef]

- Xin, B.; Yu, S. A probe into the correlation between land finance and local economic growth. Contemp. Finan. Econ. 2010, 43–47. (In Chinese) [Google Scholar]

- Zhou, X.; Yan, X. The correlation analysis between land finance and urban expansion in new institutional economics perspertive. Urban Studies 2010, 17, 159–162. (In Chinese) [Google Scholar]

- Guo, S.; Liu, L.; Zhao, Y. The business cycle implications of land financing in China. Econ. Model. 2015, 46, 225–237. [Google Scholar] [CrossRef]

- Zhang, W.; Xu, H. Effects of land urbanization and land finance on carbon emissions: A panel data analysis for Chinese provinces. Land Use Policy 2017, 63, 493–500. [Google Scholar] [CrossRef]

- Xu, J.; Yeh, A.; Wu, F. Land commodification: New land development and politics in China since the late 1990s. Int. J. Urban Reg. Res. 2010, 33, 890–913. [Google Scholar] [CrossRef]

- Liu, T.; Cao, G.; Yan, Y.; Wang, R.Y. Urban land marketization in china: central policy, local initiative, and market mechanism. Land Use Policy 2016, 57, 265–276. [Google Scholar] [CrossRef]

- Liu, Y.; Fan, P.; Yue, W.; Song, Y. Impacts of land finance on urban sprawl in China: The case of chongqing. Land Use Policy 2018, 72, 420–432. [Google Scholar] [CrossRef]

- Fu, Q. When fiscal recentralisation meets urban reforms: Prefectural land finance and its association with access to housing in urban China. Urban Stud. 2015, 52, 1791–1809. [Google Scholar] [CrossRef]

- Zheng, H.; Wang, X.; Cao, S. The land finance model jeopardizes China’s sustainable development. Habitat Int. 2014, 44, 130–136. [Google Scholar] [CrossRef]

- Chen, W.Y.; Hu, F.Z.Y. Producing nature for public: Land-based urbanization and provision of public green spaces in China. Appl. Geogr. 2015, 58, 32–40. [Google Scholar] [CrossRef]

- Pan, J.N.; Huang, J.T.; Chiang, T.F. Empirical study of the local government deficit, land finance and real estate markets in China. China Econ. Rev. 2015, 32, 57–67. [Google Scholar] [CrossRef]

- Ye, F.; Wang, W. Determinants of land finance in China: A study based on provincial-level panel data. Aust. J. Public Adm. 2013, 72, 293–303. [Google Scholar]

- Zhao, Y. Land finance in China: History, logic and choice. Urban Dev. Stud. 2014, 21, 1–13. (In Chinese) [Google Scholar]

- Guo, G. China’s local political budget cycles. Am. J. Political Sci. 2009, 53, 621–632. [Google Scholar] [CrossRef]

- Wang, Y.; Hui, C.M. Are local governments maximizing land revenue? evidence from China. China Econ. Rev. 2017, 43, 196–215. [Google Scholar] [CrossRef]

- Cao, G.; Feng, C.; Tao, R. Local “land finance” in China’s urban expansion: Challenges and solutions. China World Econ. 2010, 16, 19–30. [Google Scholar] [CrossRef]

- Tian, L. Land use dynamics driven by rural industrialization and land finance in the peri-urban areas of China: “The examples of jiangyin and shunde”. Land Use Policy 2015, 45, 117–127. [Google Scholar] [CrossRef]

- Shen, W.; Xiao, W.; Wang, X. Passenger satisfaction evaluation model for urban rail transit: A structural equation modeling based on partial least squares. Transp. Policy 2016, 46, 20–31. [Google Scholar] [CrossRef]

- Kornai, J. “hard” and “soft” budget constraint. Acta Oeconomica 1980, 25, 231–245. [Google Scholar]

- Zhou, X. Inverted soft budget constraint: Extra-budgetary resource seeking in local governments. Soc. Sci. China 2005, 36–47. (In Chinese) [Google Scholar]

- Kornai, J. The place of the soft budget constraint syndrome in economic theory. Soc. Sci. Electron. Publ. 1998, 26, 11–17. [Google Scholar] [CrossRef]

- Goldfeld, S.M.; Quandt, R.E. Budget constraints, bailouts, and the firm under central planning. J. Comp. Econ. 1988, 12, 502–520. [Google Scholar] [CrossRef]

- Maskin, E.; Xu, C. Soft budget constraint theories: From centralization to the market. Econ. Transit. 2010, 9, 1–27. [Google Scholar] [CrossRef]

- Qian, Y.; Roland, G. Federalism and the soft budget constraint. Am. Econ. Rev. 1998, 88, 1143–1162. [Google Scholar] [CrossRef]

- Moesen, W.; Cauwenberge, P.V. The status of the budget constraint, federalism and the relative size of government: A bureaucracy approach. Public Choice 2000, 104, 207–224. [Google Scholar] [CrossRef]

- Liu, Y.L. From predator to debtor the soft budget constraint and semi-planned administration in rural China. Mod. China Int. J. Hist. Soc. Sci. 2012, 38, 308–345. [Google Scholar]

- Tjerbo, T.; Hagen, T.P. Deficits, soft budget constraints and bailouts: Budgeting after the norwegian hospital reform. Scand. Political Stud. 2009, 32, 337–358. [Google Scholar] [CrossRef]

- Hu, F.Z.Y.; Qian, J. Land-based finance, fiscal autonomy and land supply for affordable housing in urban China: A prefecture-level analysis. Land Use Policy 2017, 69, 454–460. [Google Scholar] [CrossRef]

- Ye, L.; Wu, A.M. Urbanization, land development, and land financing: evidence from Chinese cites. J. Urban Aff. 2014, 36, 354–368. [Google Scholar]

- Huang, Z.; Wei, Y.D.; He, C.; Li, H. Urban land expansion under economic transition in China: A multi-level modeling analysis. Habitat Int. 2015, 47, 69–82. [Google Scholar] [CrossRef]

- Gong, L.; Xiao, J.; Zhang, Q. Promotion incentive: Corruption and its implications on local fiscal cycles in China. Procedia Eng. 2017, 198, 845–893. [Google Scholar] [CrossRef]

- Rochlitz, M.; Kulpina, V.; Remington, T.; Yakovlev, A. Performance incentives and economic growth: Regional officials in Russia and China. Eurasian Geogr. Econ. 2015, 56, 421–445. [Google Scholar] [CrossRef]

- Yang, Z. Tax reform, fiscal decentralization, and regional economic growth: New evidence from China. Econ. Model. 2016, 59, 520–552. [Google Scholar] [CrossRef]

- Qian, M.; Huang, Y. Political institutions, entrenchments, and the sustainability of economic development—A lesson from rural finance. China Econ. Rev. 2016, 40, 152–178. [Google Scholar] [CrossRef]

- Shatkin, G. The real estate turn in policy and planning: Land monetization and the political economy of peri-urbanization in Asia. Cities 2016, 53, 141–149. [Google Scholar] [CrossRef]

- Weingast, B.R. Second generation fiscal federalism: Political aspects of decentralization and economic development. World Dev. 2014, 53, 14–25. [Google Scholar] [CrossRef]

- Wei, Y.; Huang, C.; Lam, P.T.I.; Yuan, Z. Sustainable urban development: A review on urban carrying capacity assessment. Habitat Int. 2015, 46, 64–71. [Google Scholar] [CrossRef]

- Wu, Q.; Li, Y. Fiscal Decentralization, Competition and Local Land Revenue. Financ. Trade Econ. 2010, 51–59. (In Chinese) [Google Scholar]

- Wu, F. China’s recent urban development in the process of land and housing marketisation and economic globalization. Habitat Int. 2001, 25, 273–289. [Google Scholar] [CrossRef]

- Kung, J.; Chen, S. The tragedy of the nomenklatura career incentives and political radicalism during China’s great leap famine. Am. Political Sci. Rev. 2011, 105, 27–45. [Google Scholar] [CrossRef]

- Carvalho, D. The real effects of government-owned banks: Evidence from an emerging market. J. Financ. 2014, 69, 577–609. [Google Scholar] [CrossRef]

- Drazen, A.; Eslava, M. Electoral manipulation via voter-friendly spending: Theory and evidence. J. Dev. Econ. 2010, 92, 39–52. [Google Scholar] [CrossRef]

- Ye, L.; Wu, A.M. Urbanization, land development, and land financing: Evidence from Chinese cities. J. Urban Aff. 2014, 36, 354–368. [Google Scholar]

- Hair, J.F.; Sarstedt, M.; Ringle, C.M.; Mena, J.A. An assessment of the use of partial least squares structural equation modeling in marketing research. J. Acad. Mark. Sci. 2012, 40, 414–433. [Google Scholar] [CrossRef]

- Cassel, C.; Hackl, P.; Westlund, A.H. Robustness of partial least-squares method for estimating latent variable quality structures. J. Appl. Stat. 1999, 26, 435–446. [Google Scholar] [CrossRef]

- Chin, W.W.; Marcolin, B.L.; Newsted, P.R. A partial least squares latent variable modeling approach for measuring interaction effects: Results from a monte carlo simulation study and an electronic-mail emotion/adoption study. Inf. Syst. Res. 2003, 14, 189–217. [Google Scholar] [CrossRef]

- Aibinu, A.A.; Al-Lawati, A.M. Using pls-sem technique to model construction organizations’ willingness to participate in e-bidding. Autom. Constr. 2010, 19, 714–724. [Google Scholar] [CrossRef]

- Guan, J.; Ma, N. Structural equation model with pls path modeling for an integrated system of publicly funded basic research. Scientometrics 2009, 81, 683–698. [Google Scholar] [CrossRef]

- Astrachan, C.B.; Patel, V.K.; Wanzenried, G. A comparative study of cb-sem and pls-sem for theory development in family firm research. J. Fam. Bus. Strategy 2014, 5, 116–128. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using pls path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Chin, W.W. A comparison of approaches for the analysis of interaction effects between latent variables using partial least squares path modeling. Struct. Equ. Modeling A Multidiscip. J. 2010, 17, 82–109. [Google Scholar] [CrossRef]

- Li, X.; Lu, X. Analysis on the land finance and land conveyance in the context of economic growth. China Land Sciences 2012, 26, 42–47. (In Chinese) [Google Scholar]

- Yang, H.M. The effects of land market development on economic growth: An empirical analysis based on Chinese panel data, 1999–2005. Ecol. Econ. 2010, 6, 88–95. [Google Scholar]

- Blanchard, O.; Shleifer, A. Federalism with and without political centralization: China versus russia. Imf. Staff. Pap. 2001, 48, 171–179. [Google Scholar]

- Lin, J.Y.; Liu, Z. Fiscal decentralization and economic growth in China. Econ. Dev. Cult. Chang. 2000, 49, 1–21. [Google Scholar] [CrossRef]

- Li, H.; Zhou, L.A. Political turnover and economic performance: The incentive role of personnel control in China. J. Public Econ. 2003, 89, 1743–1762. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Countries | Periods | Methodologies | Causality Relationship |

|---|---|---|---|---|

| [23] | China | 1999–2005 | Panel data analysis | Land system correlates positively with land finance |

| [8] | China | 1999–2008 | Panel data analysis | |

| [35] | China | 2009–2013 | Spatial analysis | |

| [7] | China | 1999–2009 | Econometric models | |

| [8] | China | 1994–2007 | Panel data analysis | Land system correlates positively with economic development |

| [9] | China | 2013 | Econometric models | |

| [19] | China | 1999–2009 | Fixed effects models and random effects models | Economic development correlates positively with land finance |

| [13] | China | 1999–2010 | Panel data analysis | |

| [36] | China | 1999–2009 | Econometric models | |

| [37] | China | 2005–2008 | Local spatial statistic | |

| [1] | China | 1999–2008 | Econometric models | Political system correlates positively with land finance |

| [19] | China | 1999–2009 | Panel data analysis | |

| [7] | China | 1999–2009 | Econometric models | |

| [24] | China | 2001–2010 | Spatial analysis | |

| [38] | China | 1990–2006 | Econometric models | |

| [5] | China | 1980–2006 | Regression analysis | Political system correlates positively with economic development |

| [39] | Russia and China | 2000–2015 | Contrastive analysis | |

| [40] | China | 1990–2012 | Econometric models | |

| [41] | China | 1986–2002 | Fixed survey | |

| [42] | Asia | in the late 1980s | Contrastive analysis | |

| [24] | China | 2001–2010 | Spatial analysis | |

| [38] | China | 1990–2006 | Econometric models | |

| [1] | China | 1999–2008 | Econometric models | Fiscal system correlates positively with land finance |

| [19] | China | 1999–2009 | Panel data analysis | |

| [35] | China | 2009–2013 | Spatial analysis | |

| [7] | China | 1999–2009 | Econometric models | |

| [6] | China | 1982–1992 | Econometric models | |

| [43] | China | 2013 | Second Generation Fiscal Federalism theoretical model |

| Category | Indicators | Explanations | Ref. |

|---|---|---|---|

| Political system | Party secretaries’ tenure | Party secretaries’ accumulated time in office (in months by the end of that year) | [19,21,22] |

| Party secretaries’ distance to retirement age | Legal retirement age minus party secretaries’ age | [19,49] | |

| Competition amongst local governments | Use per capita foreign direct investment (FDI) to measure the degree of competition amongst local governments | [1,7,22] | |

| Fiscal system | Budgetary revenue | General budget revenues of local governments, State-controlled funds under budget management | [1,19,35] |

| Transfer dependency | Percentage of fiscal transfer from upper-level government in local budgetary expenditure | [7,19] | |

| Revenue decentralization | Budgetary revenue share of sub-provincial governments in a province (measured at the provincial level) | [1,7,35] | |

| Expenditure decentralization | Budgetary expenditure share of sub-provincial governments in a province (measured at the provincial level) | [35,19] | |

| Fiscal deficits | Gap between fiscal expenditure and fiscal revenue | [37,22] | |

| Land system | Real estate investment | Annual investment in land development projects | [35,19] |

| Land marketization level | Measures the weight of each transaction type by the relative land price and then calculates the degree of marketization of the land market (%, the higher the value, the higher the degree of marketization is) | [22,37,50] | |

| Cultivated land | Per capita cultivated land area | [35,19] | |

| Economic development | Urbanization level | Percentage of nonagricultural population in the total population | [1,13,35] |

| GDP | Measure of the economic development level | [19,22,37] | |

| Tertiary industry ratio | Percentage of tertiary industry output in GDP | [19] | |

| Secondary industry ratio | Percentage of secondary industry output in GDP | [13,19] | |

| Population density | Number of residential population per km2 of land area | [19,23,35] |

| Economic Development | Fiscal System | Land System | Political System | |

|---|---|---|---|---|

| Urbanization level | 0.559 | |||

| GDP | 0.921 | |||

| Tertiary industry ratio | 0.504 | |||

| Secondary industry ratio | −0.087 | |||

| Population density | 0.787 | |||

| Budgetary revenue | 0.901 | |||

| Transfer dependency | −0.418 | |||

| Revenue decentralization | 0.92 | |||

| Expenditure decentralization | 0.741 | |||

| Fiscal deficits | 0.001 | |||

| Per capita cultivated land area | 0.034 | |||

| Real estate investment | 0.989 | |||

| Land marketization level | −0.215 | |||

| Party secretaries’ tenure | 0.082 | |||

| Party secretaries’ distance to retirement age | −0.47 | |||

| Competition between local governments | 0.929 |

| Cronbach’s Alpha | rho_A | Composite Reliability (CR) | Average Variance Extracted (AVE) | |

|---|---|---|---|---|

| Economic development | 0.687 | 0.989 | 0.796 | 0.509 |

| Fiscal system | 0.839 | 0.913 | 0.899 | 0.75 |

| Land system | 1 | 1 | 1 | 1 |

| Land finance | 1 | 1 | 1 | 1 |

| Political system | 1 | 1 | 1 | 1 |

| Economic Development | Fiscal System | Land System | Land Finance | Political System | |

|---|---|---|---|---|---|

| Economic development | 0.914 | ||||

| Fiscal system | 0.824 | 0.866 | |||

| Land system | 0.69 | 0.75 | 1 | ||

| Land finance | 0.639 | 0.723 | 0.83 | 1 | |

| Political system | 0.554 | 0.418 | 0.276 | 0.3 | 1 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhu, X.; Wei, Y.; Lai, Y.; Li, Y.; Zhong, S.; Dai, C. Empirical Analysis of the Driving Factors of China’s ‘Land Finance’ Mechanism Using Soft Budget Constraint Theory and the PLS-SEM Model. Sustainability 2019, 11, 742. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030742

Zhu X, Wei Y, Lai Y, Li Y, Zhong S, Dai C. Empirical Analysis of the Driving Factors of China’s ‘Land Finance’ Mechanism Using Soft Budget Constraint Theory and the PLS-SEM Model. Sustainability. 2019; 11(3):742. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030742

Chicago/Turabian StyleZhu, Xinhua, Yigang Wei, Yani Lai, Yan Li, Sujuan Zhong, and Chun Dai. 2019. "Empirical Analysis of the Driving Factors of China’s ‘Land Finance’ Mechanism Using Soft Budget Constraint Theory and the PLS-SEM Model" Sustainability 11, no. 3: 742. https://0-doi-org.brum.beds.ac.uk/10.3390/su11030742