Corporate Ethical Responsibility in Management Research: Intellectual Bases, Focus, Salience, and Future

1

School of Management, Harbin Institute of Technology, Harbin 150001, China

2

School of Management, Guangzhou University, Guangzhou 510006, China

3

Business Division, Institute of Textiles and Clothing, Hong Kong Polytechnic University, Hong Kong, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(8), 2368; https://0-doi-org.brum.beds.ac.uk/10.3390/su11082368

Submission received: 22 March 2019

/

Revised: 14 April 2019

/

Accepted: 16 April 2019

/

Published: 20 April 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:This study provides an overview of corporate ethical responsibility (CER) studies and discusses potential future research directions. We use citations analysis in this study, because it is an efficient method for identifying and visualizing intellectual bases in a given field. Then, it presents a conceptual model that summarizes the key relationships within the CER literature by reviewing the source articles. Finally, this study synthesizes intellectual contributions to CER literature, highlights unresolved issues, and identifies areas for future research.

1. Introduction

Corporate social responsibilities (CSRs) are comprised of three areas of responsibility—economic, legal, and ethical [1]. Although many studies have been conducted on the economic and legal dimensions of CSRs, the ethical dimension has received relatively little attention among business and management disciplines. Corporate ethical responsibility (CER) is currently a challenging issue for businesses, because of the rising expectations related to operations and supply chain transparency. CER advocates that companies having strong self-restraint and altruistic duties that strengthen stakeholders’ rights and expand public policy. In contrast, both corporate economic and legal responsibilities are mandatory [2].

CER has played an increasingly critical role in regulating the market order in global economies. Many developing countries have achieved remarkable economic progress with market-oriented reforms. However, developing countries are sometimes characterized by moral degradation, exemplified by widespread counterfeit products and unsafe food sales, resource wasting, corruption, and fraudulent dealings [3,4]. Although the governments in developing countries are strengthening their policies and laws, their legal frameworks remain relatively weak compared with developed countries [5]. In most developing countries, a solid or effective legal framework regulating firms’ ethical behavior is absent. Therefore, the promotion of CER is essential in order to prohibit further ethical degradation in business practices in developing countries. In addition to the issues related to the effectiveness of their legal systems, developing countries’ national laws do not regulate corporate ethical behaviors beyond their national territory.

By the same token, international law imposes no direct legal obligation on corporate ethical decisions [6]. Therefore, the legal vacuum creates an “ethical free space” or a “responsibility free space” [7]. With the growing trend of globalization, ethical decisions in business practices often influence sustainable supply chain networks spanning multiple countries. Thus, CER is a critical emerging topic that requires further research, compared to the economic and legal aspects of CSR.

This study provides several contributions to CER literature. First, we identify the intellectual bases (i.e., research clusters) of CER. Second, we propose an integrative model of CER that includes key constructs, performance measurements, antecedents, moderators, mediators, and outcomes, based on comprehensive research. Third, we identify crucial research gaps for future studies, to advance our knowledge of CER and facilitate in the application of CER in business practices. The intellectual bases and conceptual model aim to offer assistance to researchers in this area, by the comprehensive overview. Furthermore, this research concludes the relationships between CER and performance by identifying the outcomes (financial and non-financial performance) of CER. The conclusions are useful for policymakers for designing policies to promote CER. Especially in the developing countries, business ethics are still being formed, and many firms lack CSR consciousness [8]. The conclusions have forward-looking and guiding significances. In addition, the study provides the research directions for the researchers on future CER research directions.

In the methodology section, the research methodology and data sources are explained in detail. Based on our co-citation cluster analysis, we visualize the intellectual network mapping of CER in the “Intellectual Bases of CER” section. In the “Focus and Salience on CER” section, we present key relationships in the conceptual CER model, including antecedents, definitions, measurements, moderations, mediations, and outcomes of CER. We synthesize the intellectual contributions of CER studies and highlight unresolved research gaps. Finally, we recommend future research directions for CER studies, based on the unresolved research questions. They include an improvement in the approach to measuring CER performance, the urgent need for studies about the mediators between CER and outcomes, and theoretical and empirical research on advancing CER research methodology.

2. Methodology

In this section, we explain the choices of journals and articles for sampling, and then introduce the review methodologies.

2.1. Selection of Management Journals

CSR is considered an applied management topic [9]. While CER is a major branch of CSR, we focus on mainstream management journals for this review. The focus on mainstream management ensure academic quality and rigor [10]. We include all of the journals from the University of Texas at Dallas Top 100 Business School Research Rankings; this list was is comprised of 24 journal outlets. To evaluate the research excellence of business schools, the Financial Times (FT) magazine ranks the top 45 business and management journals (FT 45). It is worth mentioning that the number of journals of FT 45 increased from 45 to 50 journals in 2017, however, during the data collection period from 1985 to 2015, we used the FT 45 journal list. In total, 23 journals are included in both journal lists. Therefore, the total number of journals included in our search is 46. They include the “Academy of Management Review”, “Academy of Management Journal”, “Mis Quarterly”, “Journal of Operations Management”, “Organization Science”, “Administrative Science Quarterly”, “Strategic Management Journal”, “Journal Of International Business Studies”, “Information Systems Research”, “Production and Operations Management”, “Manufacturing and Service Operations Management”, “Management Science”, “Operations Research”, “Journal on Computing”, “The Accounting Review” or “Journal of Accounting and Economics”, “Journal of Finance”, “Journal of Financial Economics”, “The Review of Financial Studies”, “Journal of Consumer Research”, “Journal of Marketing”, “Journal of Marketing Research”, “Marketing Science“, ”Academy of Management Perspectives”, “Accounting, Organizations, and Society”, “American Economic Review”, “California Management Review”, “Contemporary Accounting Research”, “Econometrica”, “Entrepreneurship Theory And Practice”, “Harvard Business Review”, “Human Resource Management”, “Journal of Accounting Research”, ”Journal of Applied Psychology”, “Journal of Business Ethics”, “Journal of Business Venturing”, “Journal of Financial and Quantitative Analysis”, “Journal of Financial Economics”, “Journal of Management Studies”, “Journal of Political Economy”, “Journal of the American Statistical Association”, “Organizational Behavior and Human Decision Processes”, ”Quarterly Journal of Economics”, “Rand Journal of Economics”, “Review of Accounting Studies”, and “Sloan Management Review”.

2.2. Selection of CER Articles

Previous literature that directly uses “corporate ethical responsibility” as the key word is limited. Several keywords can be used in the context of CER, such as the “ethical frame of CSR”, “ethics of CSR”, “ethics and CSR”, “CSR”, and “ethical citizenship”. Therefore, the keyword string includes “corporate ethical responsibility” or “corporate social responsibility” and “ethic*”. Based on the above keyword string, we collect 497 articles published from 1985 to 2015 from the selected 46 journals through the Web of Science.

2.3. Citation Analysis and Literature Review

To conduct an in-depth literature review with a high degree of objectivity, incorporating systematic research methods, such as a citation context analysis, is essential [10]. Citation analysis, based on the premise that authors cite documents, is an established method to demonstrate the impact of previous research on a study. The cited frequency of an article mainly depends on the article quality, research method, journal placement, and so on. [11]. Co-citation analysis, a branch of citation analysis, is a bibliometric technique that maps the intellectual structure of a research field [12]. Co-citation analysis methods include journal co-citation analysis, author co-citation analysis, and document co-citation analysis. Journal co-citation reveals the macrostructure of scholarly disciplines by analyzing journal titles from a macro-level, whereas author co-citation and document co-citation analysis reveal the “invisible college” of scientific research at a micro-level [13]. Document co-citation analysis reveals more specific patterns than author co-citation analysis, because the cited references in document co-citation analysis carry more specific information than the cited authors in author co-citation analysis. Therefore, this study explores the underlying intellectual structure of CER with document co-citation analysis. To illustrate the research status of the CER literature in detail, the content of each study must be reviewed. Thus, in addition to citation and co-citation analyses, we review the 497 source articles and discuss their findings in relation to CER. We then propose a conceptual model, including the antecedents, definitions, measurements, moderators, mediators, and outcomes in CER, based on the analysis of the key articles of the 497 source articles.

3. Intellectual Bases of CER

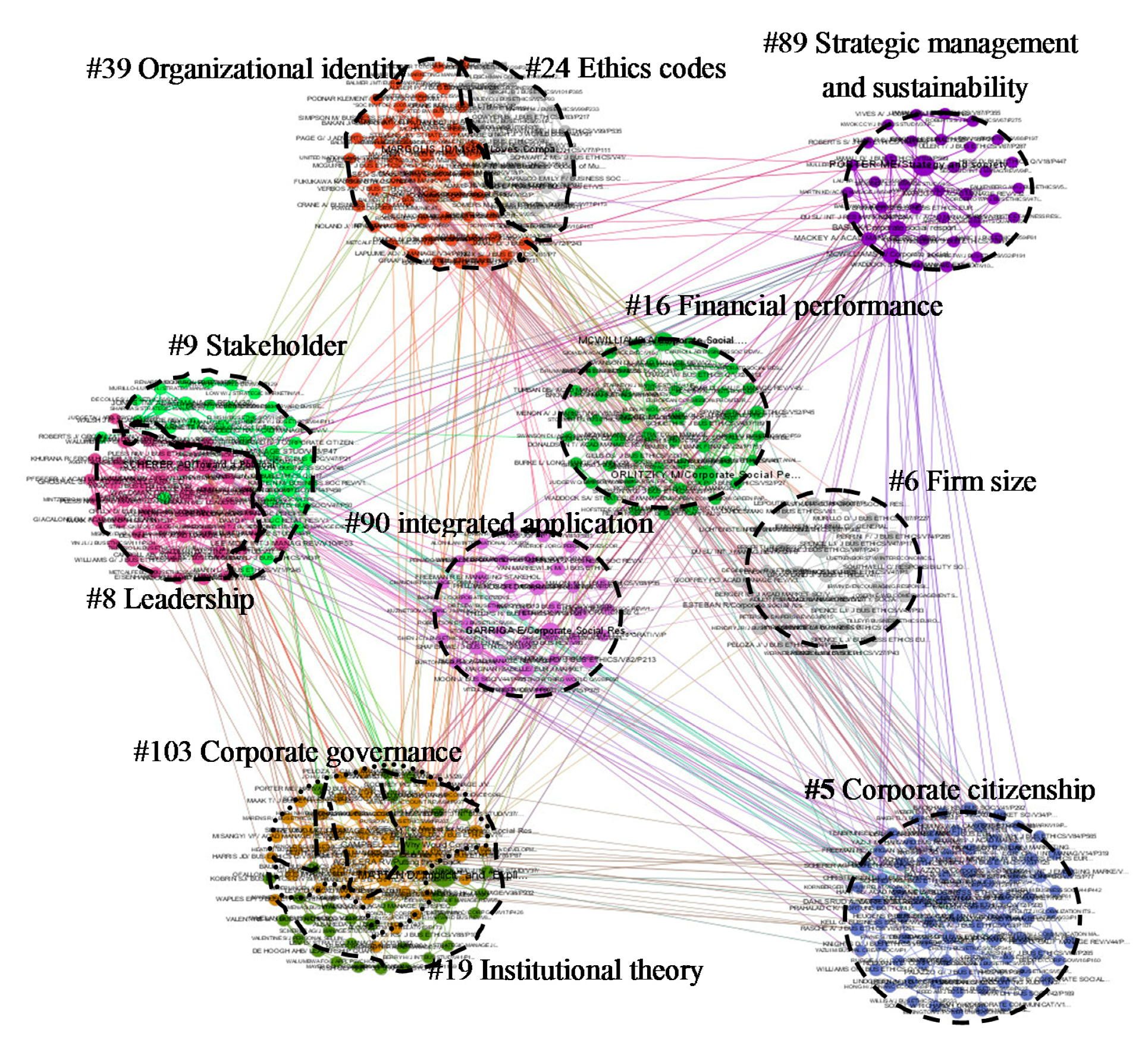

Document co-citation networks present connections among co-cited documents and provide the intellectual base of a given knowledge domain [13]. Our bibliometric analysis was based on the 664 publications cited at least two times in our sample. The core areas and strongest links of a specific research field can be demonstrated using social network techniques. Table 1 summarizes the clusters of the co-cited references with close to 30 or more documents. The “#” denotes for the ID for each cluster. Each ID number was generated randomly by the used tool (Gephi). As is shown in Appendix A, 104 clusters are generated, from “# = 0” to “# = 103”. “n” is the number of co-cited documents in each cluster. “n” also denotes the number of nodes in the corresponding cluster network, because one document is one node in document co-cited networks.

Figure 1 illustrates the salient network structure of co-cited references related to CER, on the basis of the co-cited clusters with nearly 30 or more documents. This network comprises 493 nodes and 1526 links. Each cited document is one node. The network diagram was generated using Gephi, and the diagram revealed the core areas of research interest. We identified the following eight intellectual bases by analyzing the co-citation clusters and reviewing the co-citation documents: (1) organization ethics (including #39 organizational identity and #24 ethics codes), (2) institutional theory for CER (including #19 institutional theory and #103 corporate governance), (3) stakeholder perspectives of CER (including #9 stakeholder and #8 leadership), (4) corporate citizenship (#5), (5) strategic management and sustainability (#89), (6) firm performance (#16), (7) firm size (#6), and (8) integrated application (#90) (Figure 1).

3.1. Organization Ethics

Two clusters were included in this intellectual base. Cluster #24 comprised articles with “corporate ethics”, “business code”, “codes of conduct”, “ethics standards”, “corporate culture”, “ethical culture”, and “climate” as keywords. Cluster #39 included articles with keywords such as “organizational theory”, “business ethics”, “organizational identity”, “ethical corporate identity”, and “ethical organizational identity”.

The infrastructure of organizational ethics is composed of the ethics culture, ethics climate, ethics codes, and ethics programs [14]. Researchers have noted the effect of the ethical culture, ethical climate, ethics codes, and ethics programs on organizational behavior. Carroll [15] proposed a framework for integrating ethical social responsibility into corporate culture. Ethical culture is a feature of the organization culture, and has a positive influence on employees’ ethical behavior [16]. By contrast, ethical climate refers to a shared perception of ethical criteria regarding, the criteria among organization members [17]. Ethical climate greatly influences non-code settings [18].

Ethics codes are a means for self-regulation and typically identify the organization’s conduct standards [14]. Kish-Gephart et al. [19] used a meta-analytical approach and concluded that ethics codes are negatively related to unethical behavior.

An ethics program refers to the formal or informal control system, which usually includes ethics training, a telephone hotline for consultation or reporting, investigation processes, and the assessment of ethical performance [20]. However, academic studies related to this field have remained scant [14].

Ethical identity is rooted in social cognitive theory and social identity theory [21]. Organizational ethical identity is a special form of social identity, constructed socially through the individual’s and group members’ thoughts, feelings, and behaviors, integrated into the organizational context [22]. Based on an analysis of power-related literature, DeCelles et al. [23] proposed that organizational ethical identity can protect against self-interested behavior.

3.2. Institutional Theory for CER

Two clusters were included in this intellectual base. The main keywords of cluster #19 were “CSR”, “institutional legitimacy”, “institutional theory”, “institutional infrastructure”, and “institution”. The main keywords of cluster #103 were “institutional theory” and “corporate governance”. Institutions play a crucial role in reaching an agreement on environmental protection. Husted and Allen [24] argued that institutional pressures, instead of strategic consideration, were guiding management decisions with respect to CSR in multinational firms. Matten and Moon [25] analyzed the globalized diffusion of explicit CSR practices from an institutional theory perspective, in which CSR helps to accumulate institutional legitimacy for the organization. However, in the institutional-level literature, little attention has been focused on the mediators or underlying mechanisms of the CSR-outcome relationship.

3.3. Stakeholder Perspectives of CER

Two clusters were present in this intellectual base. The keywords included in cluster #9 were “stakeholder influence capacity”, “stakeholder-related decisions”, and “stakeholder responsibility”, and those in cluster #8 were “leadership”, “socially responsible leader”, and “responsible leadership”. Freeman [28] argued that corporate executives should establish a fiduciary relationship with stakeholders. Clarkson [29] introduced stakeholder theory into the research of CSR. One of its core ideas is that enterprises must fulfill their responsibilities. Jones et al. [30] used convergent elements of major ethical theories to constitute a typology of corporate stakeholder cultures, and explained how these cultures lie on a continuum, ranging from individually self-regarding to fully other-regarding. By reviewing the classic literature, Jamali [31] concluded that stakeholder methodology has been integrated into the empirical studies related to CSR, and provides substantial benefits in approaches for deriving intuitive insights, particularly in the context of expanding on specific stakeholder issues.

Another major topic of stakeholder theory is the relationship between the firm (mainly represented by its leaders) and stakeholders. Therefore, leadership in CSR fields has become a pertinent topic in recent years. Waldman et al. [32] proposed that corporate leadership plays a key role implementing CSR initiatives. Treviño, den Nieuwenboer, and Kish-Gephart [14] argued that leadership also has a significant influence on subordinates’ notions and behaviors.

3.4. Corporate Citizenship

The keywords in cluster #5 included “citizenship” and “corporate citizenship”. Corporate citizenship is a type of citizenship that acknowledges that the corporation provides certain aspects of citizenship for other constituencies [33]. Corporate citizenship not only comprises traditional stakeholders, such as shareholders, employees, and customers, but includes broader stakeholders without a direct transacting relationship with the firm. For corporate citizenship, corporations assume functions that have been typically related to the government and welfare state. Furthermore, corporate citizenship also brings about the protection of social rights in the context where governmental regulations are not sufficient [34].

3.5. Strategic Management and Sustainability

Cluster #89 contained keywords such as “competitive advantage”, “strategic implication”, “corporate strategy”, “sustainable development”, and “sustainability”. Business strategies of CSR are based on the concept of sustainable development [35]. Companies operated by intellectual leaders engage in more strategic management of CSR than comparable firms [36]. Porter and Kramer [37] presented a model of the supply and demand for CSR investment, and concluded that CSR practices maximize the firm’s market value, although they cannot maximize the present profit. Based on organizational sensemaking, Basu and Palazzo [38] proposed a set of three-dimensional strategic management to guide CSR-related activities. The three dimensions include cognitive (what firms think), linguistic (what the firm says), and conative (how the firm tends to behave) considerations.

3.6. Financial Performance

The keywords in cluster #16 included “stakeholder theory”, “strategy”, “reputation”, “ethical investment”, “shareholder activism”, “marketing strategy”, and “corporate financial performance” (CFP). Margolis and Walsh [39] explored the reason the relationship between corporate social performance (CSP) and CFP has been the subject of (often) heated debate, and provided a comprehensive review, critique, and integration of the empirical literature. Through an empirical analysis, Simpson and Kohers [40] indicated a positive relationship between CSP and CFP in the banking industry. Orlitzky et al. [41] analyzed the relationship between CSP and CFP by using meta-analysis based on stakeholder theories and competitive advantage theory, and concluded that CSP reputation indices have a higher correlation with CFP than other indicators of CSP (for example, environmental responsibility).

3.7. Firm Size

The keywords in cluster #6 included “small- and medium-sized enterprises” (SMEs), “multistakeholder approach”, “organizational ethics”, and “social capital”. Firm size was considered as a key factor influencing specific choices in the CSR field. SMEs remain the dominant organizational form in all organization for economic co-operation and developing countries [42], and thus the CSR of SMEs contributes significantly to the CSR literature. Jenkins [43] admitted that stakeholder theory potentially provides a framework for SMEs’ CSR. Perrini et al. [44] conducted a comparison between large firms and SMEs on CSR strategies, and found that large corporations are more capable of identifying relevant stakeholders and meeting their demands using CSR strategies.

3.8. Integrative Application

Cluster #90’s keywords included “CSR”, “corporate citizenship”, “sustainable development”, “comprehensive”, “ethical responsibility”, “economic responsibility”, “corporate citizenship”, “synthesis”, “stakeholder theory”, “competitive advantage”, and “cross-cultural ethics”. Garriga and Mele [45] argued that each factor of CSR presents four dimensions (profit, social demands, political performance, and ethical value), and suggested the necessity for the development of a synthetic theory to integrate these four dimensions. Windsor [2] assessed three key research fields, namely economic responsibility, ethical responsibility, and corporate citizenship, and gauged the prospect of their theoretical synthesis. Jamali [31] tested related hypotheses that originated from the stakeholder literature of CSR based on institutional and stakeholder theory, and proposed that firms have a tendency toward homogenization.

4. Focus and Salience on CER

Citation and co-citation analyses provide the intellectual bases of CER and enable the visualization of the knowledge structure of the literature. However, understanding how these intellectual bases can be applied in various contexts requires a more comprehensive review of the sample articles. We reviewed the 497 source articles in relation to CER from 1985 to 2015. The collection method of the 497 source articles has been explained in the section “Selection of CER Articles”. We developed a conceptual model that integrates the key relationships, including antecedents, definitions, measurements, moderations, mediations, and outcomes of CER.

4.1. Antecedents

As is shown in Table 2, institutional factors are a key antecedent of CER. Campbell [46] argued that institutional factors (i.e., public and private regulation and non-governmental organizations) play key roles in monitoring and encouraging appropriate corporate behaviors. Husted and Allen [24] surveyed Mexican multinational enterprises (MNEs), and revealed that institutional pressures (instead of strategic planning) encouraged MNEs to promote CSR. Based on agency theory and stakeholder theory, Guay et al. [47] developed a framework to identify why non-governmental organizations (NGOs) are an essential factor for implementing ethical and social responsibility initiatives.

Competitive conditions also influence CER. Van de Ven and Jeurissen [48] examined the influences of competitive conditions on the decisions of CER strategies. They revealed that different levels of competition produced different levels of moral legitimacy in relation to a firm’s behavior. A firm must develop its own strategy of social responsibility and ethical considerations, in light of its competitive position.

Building corporate reputation is an essential initiative of CER. Roberts [49] proposed that the motivation to develop corporate reputation positively affects the implementation of ethical sourcing codes.

4.2. Definitions and Measurements of CER

Carroll [15] proposed that CER refers to the behaviors and activities that are expected by society and non-mandatory, but not necessarily codified into law. Windsor [2] concluded that ethical responsibilities, as an impartial moral reflection, are in between unarguably mandatory compliance (economic and legal) and arguably desirable philanthropy (voluntary). Overall, we believe that CER is a type of corporate responsibility that engages voluntary ethical activities more than legal requirements; it is composed of the following two dimensions: society and environment. Furthermore, proactive CSR may be synonymous with CER. Torugsa et al. [56] proposed that proactive CSR refers to a pattern of social responsibility adopted voluntarily, beyond complying with laws and regulations.

We identified inconsistent and varied methods of measuring CER. Cragg [57] proposed that human rights should be included in the category of ethical responsibility, but these rights have still not played a prominent role in ethical considerations. Thus, contemporary society should formulate positive human rights obligations for corporations [58]. Kaptein and Schwartz [59] argued that codes of ethics are the guides of corporate ethical responsibilities for organizational stakeholders. By exploring the codes of ethics of 157 listed companies, Stohl et al. [60] concluded that through global participation, cooperation, and agreement, the ethics codes have become the standard communication features of firms worldwide. Van de Ven [61] argued that trustworthiness and creditability are the key success factors of CER.

Many CER studies used surveys to measure these constructs in their research models. For instance, Lin et al. [62] measured CER using a five-point Likert scale in two dimensions, namely “fair treatment of business partners and co-workers” and “having a comprehensive code of conduct”. Jin et al. [63] surveyed CSR and ethics by differentiating between the five-point Likert scales in relation to top managers’ values; an organization adopting social responsibility beyond shareholder and organizational interests encourages employees to participate in community services.

In addition to the social aspects, the measurement of CER can also cover the environmental dimension. Korhonen [64] argued that environmental life cycle assessment, ecological footprints, and industrial ecology can be used to measure ethics in CSR. Torugsa, O’Donohue, and Hecker [56] proposed that 11 items in the environmental dimension of proactive CSR are commonly viewed as CER dimensions.

In the following, we identify the moderators, mediators, and outcomes, shown in Table 3.

4.3. Moderators

Moderators are variables that demonstrate the conditions under which CER leads to an outcome [65]. The correlation between CER and firm performance may depend on moderating factors, such as national or organizational cultural environment, market settings, and corporate characteristics. For example, Maignan and Ralston [66] investigated ethical codes of conduct, the management of environmental impacts, sponsorships, quality programs, and webpages of organizations in the United Kingdom, the United States, France, and the Netherlands. Zheng, Luo, and Wang [4] found that CER had a more important effect on both corporate legitimacy and competitive advantage in a morally degrading context. Compared with European corporations, U.S. corporations are more active in introducing CSR practices to express their own organizational culture and mentioning ethics codes. Torugsa, O’Donohue, and Hecker [56] revealed that the relationship between proactive environmental responsibility and CFP was positively moderated by the firm’s size and age.

4.4. Mediators

Mediators refer to variables that explain the mechanisms and underlying factors by which CER practices are related to an outcome [65]. Despite the fact that the significance of corporate ethics is continuously increasing, few studies have explored the intermediate mechanisms that analyze the influence of corporate ethics on firm performance (Chun et al.) [67]. Lin, Baruch, and Shih [62] surveyed members of 172 team-based companies, and concluded that team self-esteem mediated the influence of corporate ethical citizenship on team performance. Chun, Shin, Choi, and Kim [67] surveyed 3821 employees from 130 companies in Korea, and proposed that the collective organizational commitment and organizational interpersonal citizenship play major mediating roles between corporate ethics and CFP.

4.5. Outcomes

Success in business is measured almost exclusively by CFP. If CER behavior can promote positive CFP, it provides the impetus for many corporations to engage in CER [68]. Several researchers have explored the relationship between CER and CFP, as is shown in Table 3. For examples, Arjoon [69] proposed that firms pursuing ethically-driven strategies have a greater potential for profit than firms using only profit-driven strategies. Jin, Drozdenko, and DeLoughy [63] conducted a survey of 680 financial professionals and proposed that the perceived performance outcomes of financial corporations are correlated to ethical and social responsibility. Chakrabarty and Bass [70] analyzed whether CER practices can help mitigate microfinance portfolio risk in the microfinance industry. Recent studies have explored the relationships between CER and non-financial outcomes. Jin and Drozdenko [51] studied IT professionals in the United States, and found that socially responsible and ethical organizations can obtain positive non-financial outcomes, such as commitment, customer satisfaction, organizational effectiveness, and successful system implementations. Shum and Yam [53] indicated that CER had positive mediating effects on the relationship between economic responsibility and discretionary CSR. Based on an analysis of 300 Chinese firms, Zheng, Luo, and Wang [4] confirmed that combining CSR and business ethics positively promoted both corporate legitimacy and competitive advantage.

Several studies have focused on the outcomes of the microfoundations of CER. Foss [71] noted that microfoundations are the foundations of a field that depend on an individual’s actions and interactions, and microfoundations can be utilized with CER. For instance, Lin, Baruch, and Shih [62] revealed that ethical citizenship affects task performance through team self-esteem.

A summary of the conceptual and empirical research on CER is provided in Table 3.

5. Discussion and Conclusion

This study investigated CER using citations, co-citations, and source data from the selected 46 journals through the Web of Science between 1985 and 2015. Through co-citation analysis, we found the intellectual bases of the CER knowledge domains. The intellectual bases of CER are mainly composed of organization ethics, institutional theory, stakeholder theory, corporate citizenship, sustainability and strategic management, financial performance, firm size, and so on. It is worth mentioning that firm size has many different measuring methods, and different proxies capture different aspects of firm size [72]. For example, the total assets represent the firm’s total resources, the total sales mainly denote the product market and are not prospective, while market capitalization is more market-oriented and forward-looking. Therefore, using a different proxy of firm size may have a different relationship with CER.

Using 497 journal articles, we reviewed the CER literature for definitions, measurements, antecedents, moderations, mediations, and outcomes. Although there was some consensus on the definition of CER, methods for measuring CER need to be developed. Furthermore, the present constructs for measuring CER are mainly based on Likert scales and are composed of a subjective CSR index, which may have led to method bias in previous studies; additional theoretical and empirical studies are required to explore the motives underlying CER. Empirical evidence is required in order to illustrate the mechanism of how an ethical decision is made within an organization. From the microfoundation perspective, investigating how an individual’s value interacts with that of others is vital for constituting an organization’s culture and CER behavior. The data collection method in the existing literature was mainly cross-sectional, which means that the causality between the CER and performance remains unclear. Scholars have investigated moderators, including the culture’s environment, industry, and corporate characteristics. The CER outcome relationship is stronger when these factors exist together in context. A discussion of the mediators of the CER outcomes in the literature is virtually nonexistent. Mediators of the CER outcomes are the followers’ perceptions of team self-esteem, organizational commitment, and organizational interpersonal citizenship. In addition, we found that the organizations in developed countries are the major actors being studied in CER literature. Although there are many ethical issues in developing countries, the organizations and policies in developing countries received much less attention.

6. Further Research

We identify several areas of future research in CER. First, the approach to measuring CER performance must be improved. For instance, institutional- and organizational-level measurements use a quantitative approach, and individuals (or teams) can use a qualitative approach. Research on the microfoundations of CER can provide crucial insights that would improve the knowledge related to CER.

Second, our literature review indicates the urgent need for studies about the mediators between CER and its outcomes. This knowledge gap signifies the need to conduct research that can promote an understanding of the underlying mechanisms and processes of CER.

Third, future research should prove or develop organizational theories that advance CER studies. Individual behavior, psychology, and neurobiology may make critical contributions to the guiding mechanisms of CER. For example, a behavioral contagion may explain the formation and spread of CER practices. A behavioral contagion refers to when a recipient’s behavior changes to become more like that of another actor or initiator. Non-influential individuals are susceptible to being influenced by influential individuals. Influential individuals cluster in the network; therefore, along with their influential individuals, they may be instrumental in the spread of behaviors in the network.

Fourth, methodological approaches in CER studies should be advanced. Our review indicated the need for longitudinal studies. The causality between CER and outcomes can only be verified by longitudinal data. Furthermore, CER studies could employ a multi-level analysis (i.e., individual vs. firm level) research design. For example, an individual’s level of homogeneity could affect the likelihood of a firm making CER decisions.

Last but not least, corporate strategies for promoting and implementing CER practice should be developed in every firm in the future. Every firm could develop different measures to optimize the resources that promote CER. For example, executive compensation can be tied to CER-related milestones, because direct incentives for CSR is an effective tool to improve firm social performance [73]. Furthermore, firms need to cautiously design CER compensation contracts, because transparent CSR contracts and opaque CSR contracts may have different a influence on firm value [74].

Author Contributions

Y.J. and C.K.Y.L. conceived this research and wrote the manuscript. H.W. provided citation anlaysis. X.X. commented for the overall study, and provided valuable suggestion.

Funding

This research was funded by the National Social Science Fund of China (No. 18ZDA043). This research was also supported by the National Natural Science Foundation of China (NSFC) (grant No. 71671053, No. 71771067, and No. 71841024) and the National Key R&D Program of China (No. 2016YFC0701800 and No. 2016YFC0701808).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Appendix the whole documents co-cited analysis (DCA) clusters.

| # (ID) | n | % of the Network |

|---|---|---|

| 0 | 1 | 0.15 |

| 1 | 1 | 0.15 |

| 2 | 1 | 0.15 |

| 3 | 1 | 0.15 |

| 4 | 1 | 0.15 |

| 5 | 85 | 12.8 |

| 6 | 35 | 5.27 |

| 7 | 1 | 0.15 |

| 8 | 48 | 7.23 |

| 9 | 34 | 5.12 |

| 10 | 1 | 0.15 |

| 11 | 1 | 0.15 |

| 12 | 2 | 0.3 |

| 13 | 1 | 0.15 |

| 14 | 1 | 0.15 |

| 15 | 1 | 0.15 |

| 16 | 53 | 7.98 |

| 17 | 1 | 0.15 |

| 18 | 1 | 0.15 |

| 19 | 36 | 5.42 |

| 20 | 1 | 0.15 |

| 21 | 1 | 0.15 |

| 22 | 1 | 0.15 |

| 23 | 1 | 0.15 |

| 24 | 29 | 4.37 |

| 25 | 1 | 0.15 |

| 26 | 2 | 0.3 |

| 27 | 1 | 0.15 |

| 28 | 2 | 0.3 |

| 29 | 1 | 0.15 |

| 30 | 1 | 0.15 |

| 31 | 1 | 0.15 |

| 32 | 1 | 0.15 |

| 33 | 1 | 0.15 |

| 34 | 1 | 0.15 |

| 35 | 1 | 0.15 |

| 36 | 1 | 0.15 |

| 37 | 1 | 0.15 |

| 38 | 1 | 0.15 |

| 39 | 53 | 7.98 |

| 40 | 1 | 0.15 |

| 41 | 1 | 0.15 |

| 42 | 1 | 0.15 |

| 43 | 3 | 0.45 |

| 44 | 1 | 0.15 |

| 45 | 10 | 1.52 |

| 46 | 1 | 0.15 |

| 47 | 1 | 0.15 |

| 48 | 1 | 0.15 |

| 49 | 1 | 0.15 |

| 50 | 1 | 0.15 |

| 51 | 1 | 0.15 |

| 52 | 2 | 0.3 |

| 53 | 2 | 0.3 |

| 54 | 1 | 0.15 |

| 55 | 1 | 0.15 |

| 56 | 1 | 0.15 |

| 57 | 1 | 0.15 |

| 58 | 1 | 0.15 |

| 59 | 1 | 0.15 |

| 60 | 1 | 0.15 |

| 61 | 1 | 0.15 |

| 62 | 1 | 0.15 |

| 63 | 1 | 0.15 |

| 64 | 1 | 0.15 |

| 65 | 1 | 0.15 |

| 66 | 1 | 0.15 |

| 67 | 24 | 3.61 |

| 68 | 1 | 0.15 |

| 69 | 1 | 0.15 |

| 70 | 1 | 0.15 |

| 71 | 1 | 0.15 |

| 72 | 1 | 0.15 |

| 73 | 1 | 0.15 |

| 74 | 1 | 0.15 |

| 75 | 1 | 0.15 |

| 76 | 1 | 0.15 |

| 77 | 1 | 0.15 |

| 78 | 15 | 2.28 |

| 79 | 2 | 0.3 |

| 80 | 1 | 0.15 |

| 81 | 2 | 0.3 |

| 82 | 1 | 0.15 |

| 83 | 1 | 0.15 |

| 84 | 1 | 0.15 |

| 85 | 1 | 0.15 |

| 86 | 1 | 0.15 |

| 87 | 1 | 0.15 |

| 88 | 1 | 0.15 |

| 89 | 37 | 5.57 |

| 90 | 39 | 5.87 |

| 91 | 2 | 0.3 |

| 92 | 1 | 0.15 |

| 93 | 14 | 2.13 |

| 94 | 2 | 0.3 |

| 95 | 1 | 0.15 |

| 96 | 1 | 0.15 |

| 97 | 4 | 0.61 |

| 98 | 1 | 0.15 |

| 99 | 2 | 0.3 |

| 100 | 5 | 0.76 |

| 101 | 1 | 0.15 |

| 102 | 1 | 0.15 |

| 103 | 44 | 6.63 |

| 664 | 100 |

References

- Schwartz, M.S.; Carroll, A.B. Corporate social responsibility: A three-domain approach. Bus. Ethics Q. 2003, 13, 503–530. [Google Scholar] [CrossRef]

- Windsor, D. Corporate social responsibility: Three key approaches. J. Manag. Stud. 2006, 43, 93–114. [Google Scholar] [CrossRef]

- Vynoslavska, O.; McKinney, J.A.; Moore, C.W.; Longenecker, J.G. Transition ethics: A comparison of ukrainian and united states business professionals. J. Bus. Ethics 2005, 61, 283–299. [Google Scholar]

- Zheng, Q.Q.; Luo, Y.D.; Wang, S.L. Moral degradation, business ethics, and corporate social responsibility in a transitional economy. J. Bus. Ethics 2014, 120, 405–421. [Google Scholar] [CrossRef]

- Firth, M.; Wang, K.; Wong, S.M.L. Corporate transparency and the impact of investor sentiment on stock prices. Manag. Sci. 2015, 61, 1630–1647. [Google Scholar]

- Scherer, A.G.; Palazzo, G. The new political role of business in a globalized world: A review of a new perspective on csr and its implications for the firm, governance, and democracy. J. Manag. Stud. 2011, 48, 899–931. [Google Scholar] [CrossRef]

- Jamali, D.; Karam, C. Corporate social responsibility in developing countries as an emerging field of study. Int. J. Manag. Rev. 2018, 20, 32–61. [Google Scholar] [CrossRef]

- Du, X.Q. How the market values greenwashing? Evidence from china. J. Bus. Ethics 2015, 128, 547–574. [Google Scholar] [CrossRef]

- Lockett, A.; Moon, J.; Visser, W. Corporate social responsibility in management research: Focus, nature, salience and sources of influence. J. Manag. Stud. 2006, 43, 115–136. [Google Scholar] [CrossRef]

- Chen, C.M. Science mapping: A systematic review of the literature. J. Data Inf. Sci. 2017, 2, 1–40. [Google Scholar]

- Dang, C.Y.; Li, Z.C. Drivers of research impact: Evidence from the top three finance journals. Acco. Financ. 2018, 2, 1–54. [Google Scholar] [CrossRef]

- Ma, Z.Z.; Lee, Y.; Yu, K.H. Ten years of conflict management studies: Themes, concepts and relationships. Int. J. Confl. Manag. 2008, 19, 234–248. [Google Scholar] [CrossRef]

- Liu, Z.G.; Yin, Y.M.; Liu, W.D.; Dunford, M. Visualizing the intellectual structure and evolution of innovation systems research: A bibliometric analysis. Scientometrics 2015, 103, 135–158. [Google Scholar] [CrossRef]

- Treviño, L.K.; den Nieuwenboer, N.A.; Kish-Gephart, J.J. (un)ethical behavior in organizations. Annu. Rev. Psychol. 2014, 65, 635–660. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Treviño, L.K. A cultural perspective on changing and developing organizational ethics. Res. Organ. Chang. Dev. 1990, 4, 195–230. [Google Scholar]

- Victor, B.; Cullen, J.B. The organizational bases of ethical work climates. Admin. Sci. Q. 1988, 33, 101–125. [Google Scholar] [CrossRef]

- Treviño, L.K.; Weaver, G.R.; Reynolds, S.J. Behavioral ethics in organizations: A review. J. Manag. 2006, 32, 951–990. [Google Scholar] [CrossRef]

- Kish-Gephart, J.J.; Harrison, D.A.; Trevino, L.K. Bad apples, bad cases, and bad barrels: Meta-analytic evidence about sources of unethical decisions at work. J. Appl. Psychol. 2010, 95, 1–31. [Google Scholar] [CrossRef] [PubMed]

- Kaptein, M. Ethics programs and ethical culture: A next step in unraveling their multi-faceted relationship. J. Bus. Ethics 2009, 89, 261–281. [Google Scholar] [CrossRef]

- Ashforth, B.E.; Mael, F. Social identity theory and the organization. Acad. Manag. Rev. 1989, 14, 20–39. [Google Scholar] [CrossRef]

- Verbos, A.K.; Gerard, J.A.; Forshey, P.R.; Harding, C.S.; Miller, J.S. The positive ethical organization: Enacting a living code of ethics and ethical organizational identity. J. Bus. Ethics 2007, 76, 17–33. [Google Scholar] [CrossRef]

- DeCelles, K.A.; DeRue, D.S.; Margolis, J.D.; Ceranic, T.L. Does power corrupt or enable? When and why power facilitates self-interested behavior. J. Appl. Psychol. 2012, 97, 681–689. [Google Scholar] [CrossRef] [PubMed]

- Husted, B.W.; Allen, D.B. Corporate social responsibility in the multinational enterprise: Strategic and institutional approaches. J. Int. Bus. Stud. 2006, 37, 838–849. [Google Scholar] [CrossRef]

- Matten, D.; Moon, J. “Implicit” and “explicit” csr: A conceptual framework for a comparative understanding of corporate social responsibility. Acad. Manag. Rev. 2008, 33, 404–424. [Google Scholar] [CrossRef]

- Haxhi, I.; Aguilera, R.V. An institutional configurational approach to cross-national diversity in corporate governance. J. Manag. Stud. 2017, 54, 261–303. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate governance and firm value: The impact of corporate social responsibility. J. Bus. Ethics 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman Press: Boston, MA, USA, 1984. [Google Scholar]

- Clarkson, M.E. A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Jones, T.M.; Felps, W.; Bigley, G.A. Ethical theory and stakeholder-related decisions: The role of stakeholder culture. Acad. Manag. Rev. 2007, 32, 137–155. [Google Scholar] [CrossRef]

- Jamali, D. A stakeholder approach to corporate social responsibility: A fresh perspective into theory and practice. J. Bus. Ethics 2008, 82, 213–231. [Google Scholar] [CrossRef]

- Waldman, D.A.; Siegel, D.S.; Javidan, M. Components of ceo transformational leadership and corporate social responsibility. J. Manag. Stud. 2006, 43, 1703–1725. [Google Scholar] [CrossRef]

- Matten, D.; Crane, A. Corporate citizenship: Toward an extended theoretical conceptualization. Acad. Manag. Rev. 2005, 30, 166–179. [Google Scholar] [CrossRef]

- Hahn, R. The ethical rational of business for the poor—Integrating the concepts bottom of the pyramid, sustainable development, and corporate citizenship. J. Bus. Ethics 2009, 84, 313–324. [Google Scholar] [CrossRef]

- Gauthier, C. Measuring corporate social and environmental performance: The extended life-cycle assessment. J. Bus. Ethics 2005, 59, 199–206. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate social responsibility: Strategic implications. J. Manag. Stud. 2006, 43, 1–18. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The link between competitive advantage and corporate social responsibility—Response. Harv. Bus. Rev. 2007, 85, 136–137. [Google Scholar]

- Basu, K.; Palazzo, G. Corporate social responsibility: A process model of sensemaking. Acad. Manag. Rev. 2008, 33, 122–136. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. People and Profits?: The Search for a Link between a Company’s Social and Financial Performance; Psychology Press: London, UK, 2001. [Google Scholar]

- Simpson, W.G.; Kohers, T. The link between corporate social and financial performance: Evidence from the banking industry. J. Bus. Ethics 2002, 35, 97–109. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Spence, L.J.; Rutherfoord, R. Small business and empirical perspectives in business ethics: Editorial. J. Bus. Ethics 2003, 47, 1–5. [Google Scholar] [CrossRef]

- Jenkins, H. Small business champions for corporate social responsibility. J. Bus. Ethics 2006, 67, 241–256. [Google Scholar] [CrossRef]

- Perrini, F.; Russo, A.; Tencati, A. Csr strategies of smes and large firms. Evidence from italy. J. Bus. Ethics 2007, 74, 285–300. [Google Scholar] [CrossRef]

- Garriga, E.; Mele, D.N. Corporate social responsibility theories: Mapping the territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Guay, T.; Doh, J.P.; Sinclair, G. Non-governmental organizations, shareholder activism, and socially responsible investments: Ethical, strategic, and governance implications. J. Bus. Ethics 2004, 52, 125–139. [Google Scholar] [CrossRef]

- Van de Ven, B.; Jeurissen, R. Competing responsibly. Bus. Ethics Q. 2005, 15, 299–317. [Google Scholar] [CrossRef]

- Roberts, S. Supply chain specific? Understanding the patchy success of ethical sourcing initiatives. J. Bus. Ethics 2003, 44, 159–170. [Google Scholar] [CrossRef]

- Graafland, J.; van de Ven, B.; Stoffele, N. Strategies and instruments for organising csr by small and large businesses in the netherlands. J. Bus. Ethics 2003, 47, 45–60. [Google Scholar] [CrossRef]

- Jin, K.G.; Drozdenko, R.G. Relationships among perceived organizational core values, corporate social responsibility, ethics, and organizational performance outcomes: An empirical study of information technology professionals. J. Bus. Ethics 2010, 92, 341–359. [Google Scholar] [CrossRef]

- Romani, L.; Szkudlarek, B. The struggles of the interculturalists: Professional ethical identity and early stages of codes of ethics development. J. Bus. Ethics 2014, 119, 173–191. [Google Scholar] [CrossRef]

- Shum, P.K.; Yam, S.L. Ethics and law: Guiding the invisible hand to correct corporate social responsibility externalities. J. Bus. Ethics 2011, 98, 549–571. [Google Scholar] [CrossRef]

- Angelidis, J.; Ibrahim, N. An exploratory study of the impact of degree of religiousness upon an individual’s corporate social responsiveness orientation. J. Bus. Ethics 2004, 51, 119–128. [Google Scholar] [CrossRef]

- Christensen, L.J.; Mackey, A.; Whetten, D. Taking responsibility for corporate social responsibility: The role of leaders in creating, implementing, sustaining, or avoiding socially responsible firm behaviors. Acad. Manag. Perspect. 2014, 28, 164–178. [Google Scholar] [CrossRef]

- Torugsa, N.A.; O’Donohue, W.; Hecker, R. Proactive csr: An empirical analysis of the role of its economic, social and environmental dimensions on the association between capabilities and performance. J. Bus. Ethics 2013, 115, 383–402. [Google Scholar] [CrossRef]

- Cragg, W. Human rights and business ethics: Fashioning a new social contract. J. Bus. Ethics 2000, 27, 205–214. [Google Scholar] [CrossRef]

- Wettstein, F. Csr and the debate on business and human rights: Bridging the great divide. Bus. Ethics Q. 2012, 22, 739–770. [Google Scholar] [CrossRef]

- Kaptein, M.; Schwartz, M.S. The effectiveness of business codes: A critical examination of existing studies and the development of an integrated research model. J. Bus. Ethics 2008, 77, 111–127. [Google Scholar] [CrossRef]

- Stohl, C.; Stohl, M.; Popova, L. A new generation of corporate codes of ethics. J. Bus. Ethics 2009, 90, 607–622. [Google Scholar] [CrossRef]

- Van de Ven, B. An ethical framework for the marketing of corporate social responsibility. J. Bus. Ethics 2008, 82, 339–352. [Google Scholar] [CrossRef]

- Lin, C.P.; Baruch, Y.; Shih, W.C. Corporate social responsibility and team performance: The mediating role of team efficacy and team self-esteem. J. Bus. Ethics 2012, 108, 167–180. [Google Scholar] [CrossRef]

- Jin, K.G.; Drozdenko, R.; DeLoughy, S. The role of corporate value clusters in ethics, social responsibility, and performance: A study of financial professionals and implications for the financial meltdown. J. Bus. Ethics 2013, 112, 15–24. [Google Scholar] [CrossRef]

- Korhonen, J. On the ethics of corporate social responsibility - considering the paradigm of industrial metabolism. J. Bus. Ethics 2003, 48, 301–315. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility a review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar]

- Maignan, I.; Ralston, D.A. Corporate social responsibility in europe and the us: Insights from businesses’ self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Chun, J.S.; Shin, Y.; Choi, J.N.; Kim, M.S. How does corporate ethics contribute to firm financial performance?: The mediating role of collective organizational commitment and organizational citizenship behavior. J. Manag. 2013, 39, 853–877. [Google Scholar] [CrossRef]

- Joyner, B.E.; Payne, D. Evolution and implementation: A study of values, business ethics and corporate social responsibility. J. Bus. Ethics 2002, 41, 297–311. [Google Scholar] [CrossRef]

- Arjoon, S. Virtue theory as a dynamic theory of business. J. Bus. Ethics 2000, 28, 159–178. [Google Scholar] [CrossRef]

- Chakrabarty, S.; Bass, A.E. Comparing virtue, consequentialist, and deontological ethics-based corporate social responsibility: Mitigating microfinance risk in institutional voids. J. Bus. Ethics 2015, 126, 487–512. [Google Scholar] [CrossRef]

- Foss, N.J. Why micro-foundations for resource-based theory are needed and what they may look like. J. Manag. 2011, 37, 1413–1428. [Google Scholar] [CrossRef]

- Dang, C.Y.; Li, Z.C.; Yang, C. Measuring firm size in empirical corporate finance. J. Bank. Financ. 2018, 86, 159–176. [Google Scholar] [CrossRef]

- Hong, B.; Li, Z.C.; Minor, D. Corporate governance and executive compensation for corporate social responsibility. J. Bus. Ethics 2016, 136, 199–213. [Google Scholar] [CrossRef]

- Ikram, A.; Li, Z.F.; Minor, D. Csr-Contingent Executive Compensation Contracts. Available online: https://ssrn.com/abstract=3019985 (accessed on 18 June 2018).

Figure 1.

The intellectual bases of corporate ethical responsibility (CER).

Table 1.

The largest documents co-cited analysis (DCA) clusters.

| # | n | % of the Network | Accumulated % of the Network | Keywords |

|---|---|---|---|---|

| 5 | 85 | 12.8 | 12.8 | Citizenship and corporate citizenship |

| 16 | 53 | 7.98 | 20.78 | Stakeholder theory, strategy, reputation, ethical investment, shareholder activism, and marketing strategy and financial performance |

| 39 | 53 | 7.98 | 28.76 | Organizational theory, business ethics, organizational identity, ethical corporate identify, and ethical organizational identity |

| 8 | 48 | 7.23 | 35.99 | Leadership, socially responsible leader, and responsible leadership |

| 103 | 44 | 6.63 | 42.62 | Institutional theory and corporate governance |

| 90 | 39 | 5.87 | 48.49 | Corporate social responsibility, ethical responsibility, corporate citizenship, sustainable development, comprehensive, and so on |

| 89 | 37 | 5.57 | 54.06 | Competitive advantage, strategic implication, corporate strategy, and sustainable development and sustainability |

| 19 | 36 | 5.42 | 59.48 | Corporate social responsibility, institutional legitimacy, institutional theory, institutional infrastructure, and institution |

| 6 | 35 | 5.27 | 64.75 | Small- and medium-sized (SME), stakeholder theory, multi-stakeholder approach, organizational ethics, social capital, and small- and medium-sized enterprises |

| 9 | 34 | 5.12 | 69.87 | Stakeholder influence capacity, stakeholder-related decisions, and stakeholder responsibility |

| 24 | 29 | 4.37 | 74.25 | Corporate ethics, business code, codes of conduct, ethics standards corporate culture, and ethical culture and climate |

Table 2.

The antecedents of corporate ethical responsibility (CER). NGOs—non-governmental organizations.

Table 2.

The antecedents of corporate ethical responsibility (CER). NGOs—non-governmental organizations.

| Antecedents of CER | |

|---|---|

| Conceptual papers | |

| Institutional factors | |

| Institutional conditions (Campbell 2007) [1] | |

| NGOs (Guay, Doh et al. 2004) [2] | |

| Reputational concerns [3] | |

| Ethical identity (Romani and Szkudlarek 2014) [4] | |

| Leadership (Christensen, Mackey et al. 2014) [5] | |

| Empirical papers | |

| Institutional factors | |

| Internationally institutional pressures (Husted and Allen 2006) [6] | |

| Competitive conditions (van and Jeurissen, 2005) [7] | |

| The size of the business (Graafland et al. 2003) [8] | |

| Organizational values (Jin and Drozdenko 2010 and 2013) [9,10] | |

| Economical responsibility and legal responsibility (Shum and Yam 2011) [11] | |

| Religion and degree of religiousness (Ibrahim 2004) [12] |

Table 3.

Summary of conceptual and empirical research on CER.

| Moderators of CER-Outcomes | Mediators of CER-Outcomes | Outcomes of CER | |

|---|---|---|---|

| Conceptual papers | |||

| Financial performance Potential profit (Arjoon 2000) [13]; | |||

| Nonfinancial performance | |||

| Discretionary CSR (Shum and Yam 2011) [11] | |||

| Empirical papers | |||

| Socio-cultural and market settings | Organizational factors | Financial performance | |

| Businesses in the four countries had a different eagerness to convey socially responsible images (Maignan and Ralston 2002) [14] | Team self-esteem (Chun et al. 2013) [15] | Better market share and profitability (Jin and Drozdenko 2010 and 2013; Chun et al. 2013) [9,10,15] | |

| Moral degradation (Zheng et al. 2014) [16] | |||

| Corporate characteristics (industry and firm environment) | Organizational commitment and organizational interpersonal citizenship (Chun et al. 2013) [15] | Long-term financial success for SMEs (Torugsa, O’Donohue, and Hecker [56] | |

| Industry (Jin and Drozdenko 2010 and 2013) [9,10] | Mitigating microfinance portfolio risk (Chakrabarty and Bass 2015) [17] | ||

| Firm size and the duration of the firm’s experience (Torugsa, O’Donohue, and Hecker 2013) [18] | Nonfinancial performance | ||

| Commitment, customer satisfaction, and organizational effectiveness (Jin and Drozdenko 2010) [9] | |||

| Discretionary CSR (Shum and Yam 2011) [11] | |||

| Task performance (Lin et al. 2012) [19] Responsible leader (Stahl and De 2014) [20] | |||

| Corporate legitimacy and competitive advantage (Zheng et al. 2014) [16] |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Jiang, Y.; Xue, X.; Lo, C.K.Y.; Wu, H. Corporate Ethical Responsibility in Management Research: Intellectual Bases, Focus, Salience, and Future. Sustainability 2019, 11, 2368. https://0-doi-org.brum.beds.ac.uk/10.3390/su11082368

AMA Style

Jiang Y, Xue X, Lo CKY, Wu H. Corporate Ethical Responsibility in Management Research: Intellectual Bases, Focus, Salience, and Future. Sustainability. 2019; 11(8):2368. https://0-doi-org.brum.beds.ac.uk/10.3390/su11082368

Chicago/Turabian StyleJiang, Ying, Xiaolong Xue, Chris K. Y. Lo, and Hengqin Wu. 2019. "Corporate Ethical Responsibility in Management Research: Intellectual Bases, Focus, Salience, and Future" Sustainability 11, no. 8: 2368. https://0-doi-org.brum.beds.ac.uk/10.3390/su11082368

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.