4.2. The Main Composition of Carbon Emissions and Electricity Consumption

Chou’s study [

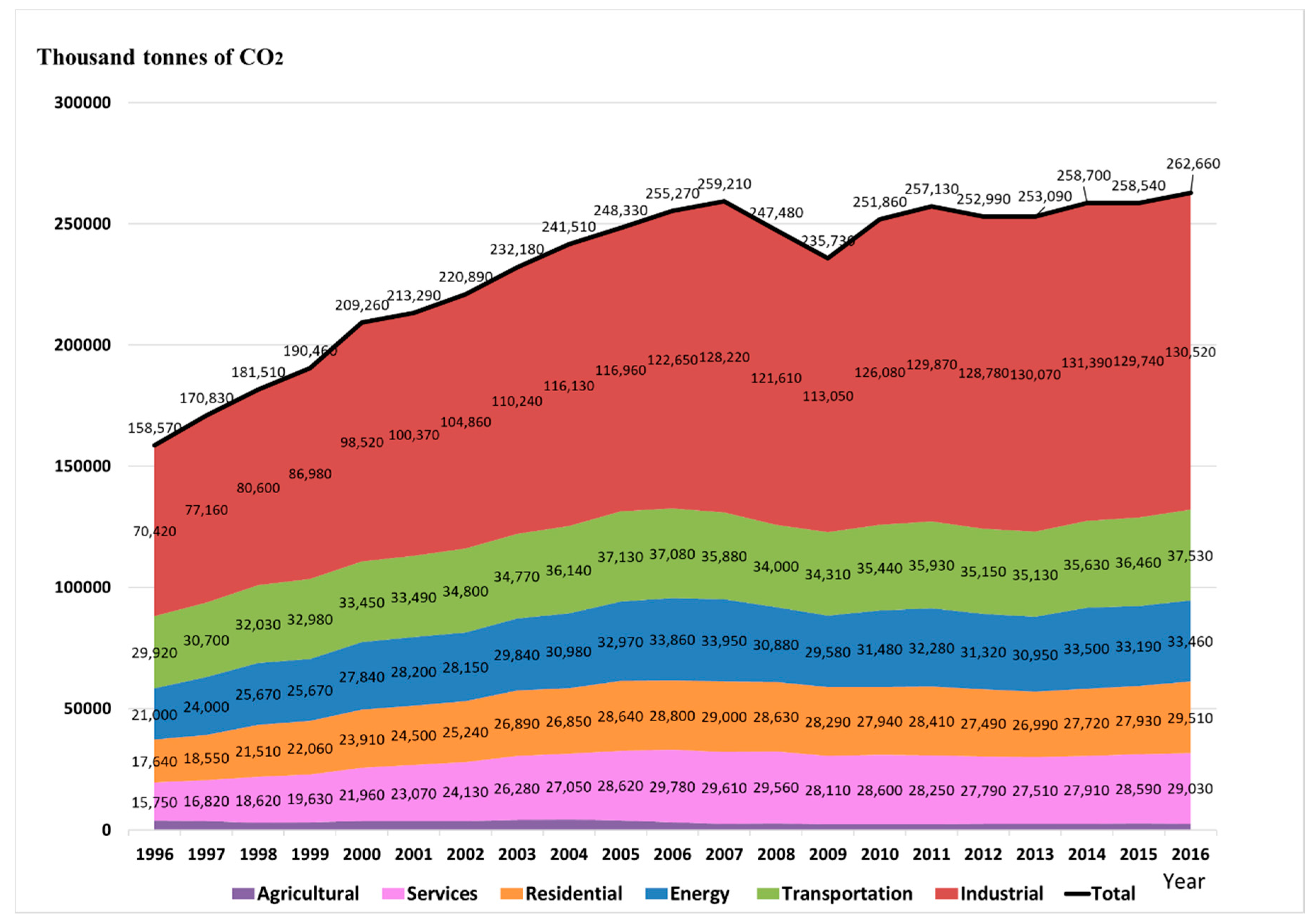

15] showed that in the past 20 years, Taiwan’s carbon emissions have grown by 111,860 kilotons, with the industrial sector accounting for 56.2% (62,940 kilotons) (

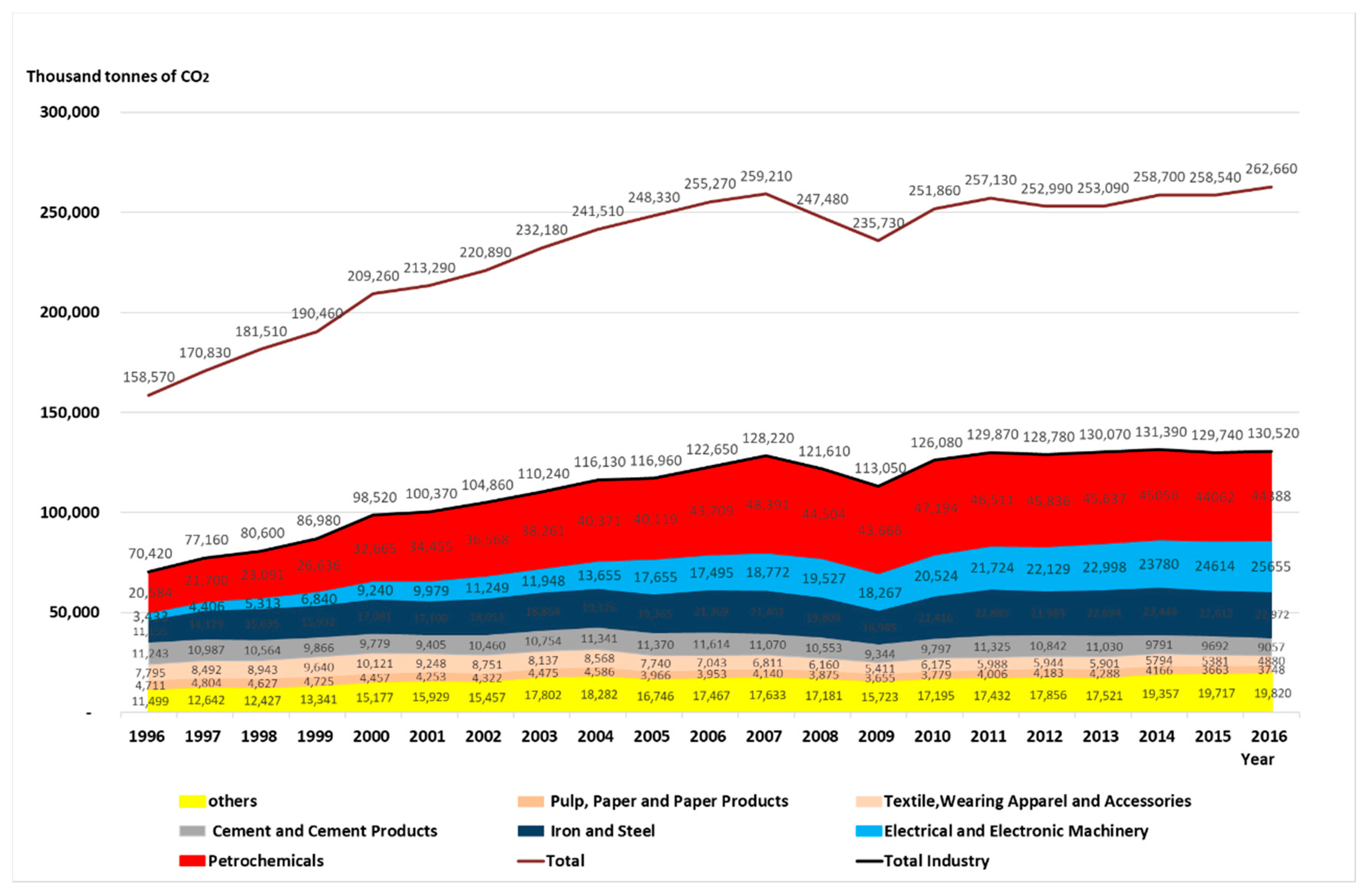

Figure 1). When looking at the industrial sector (

Figure 2), the petrochemical industry accounted for 22.3% (24,916 kilotons), and the electronics industry accounted for 20.3% (22,717 kilotons), of which the growth of the petrochemical and electronics industries accounted for 42.6% of the country’s emissions and 75.7% of industrial emissions. It can therefore be said that the petrochemical and electronics industries have been the main contributors toward carbon emissions in Taiwan. However, the nature of Taiwan’s petrochemical and electronics industries are very different. The contribution of the electronics industry to Taiwan’s GDP has been increasing year after year, while the energy intensity has been decreasing every year, which means that the GDP efficiency of the electronics industry is better than the petrochemical industry. Since the main carbon emissions and electricity consumption of the electronics industry come mainly from electricity consumption, improving Taiwan’s energy composition and increasing the efficiency of energy consumption would be able to effectively reduce the carbon emissions from the electronics industry. Comparatively, the petrochemical industry, by its very nature, produces high carbon emissions and is highly energy intensive. As Taiwan currently faces a situation of high carbon emissions and electricity consumption by the petrochemicals and electronics industries, which are conundrums intertwined with the transformation of energy, environment, and industry, while at the same time being confronted by the dual pressures of international low-carbon and domestic environmental movements, the only solution for Taiwan therefore seems to be to reduce carbon emissions, energy demand, and pollution, in order to remain competitive [

16]. Therefore, the key is in how to reform the structure of these energy-intensive industries to accommodate the high-value-added electronics industries.

Although Taiwan has introduced several successive policy programs to respond to international green conventions since 1998, it has continued to develop energy-intensive industries that produce high carbon emissions and use a high amount of energy [

15] In addition, most of the carbon emissions from the electronics industry come from electricity use, of which, process carbon emissions made up 20% of ICT carbon emissions in 2009, but has since been reduced to 14.5% in 2015, which shows that the process energy efficiency in the electronics industry has turned toward a developmental trend based on innovative design in order to increase additional value. Research showed that the main drivers behind Taiwan’s low carbon transition, which relied on the internalization of external costs, such as via using carbon tax, environmental impact assessment, alternative energy development, and the promotion of an industrial transition, has lacked success [

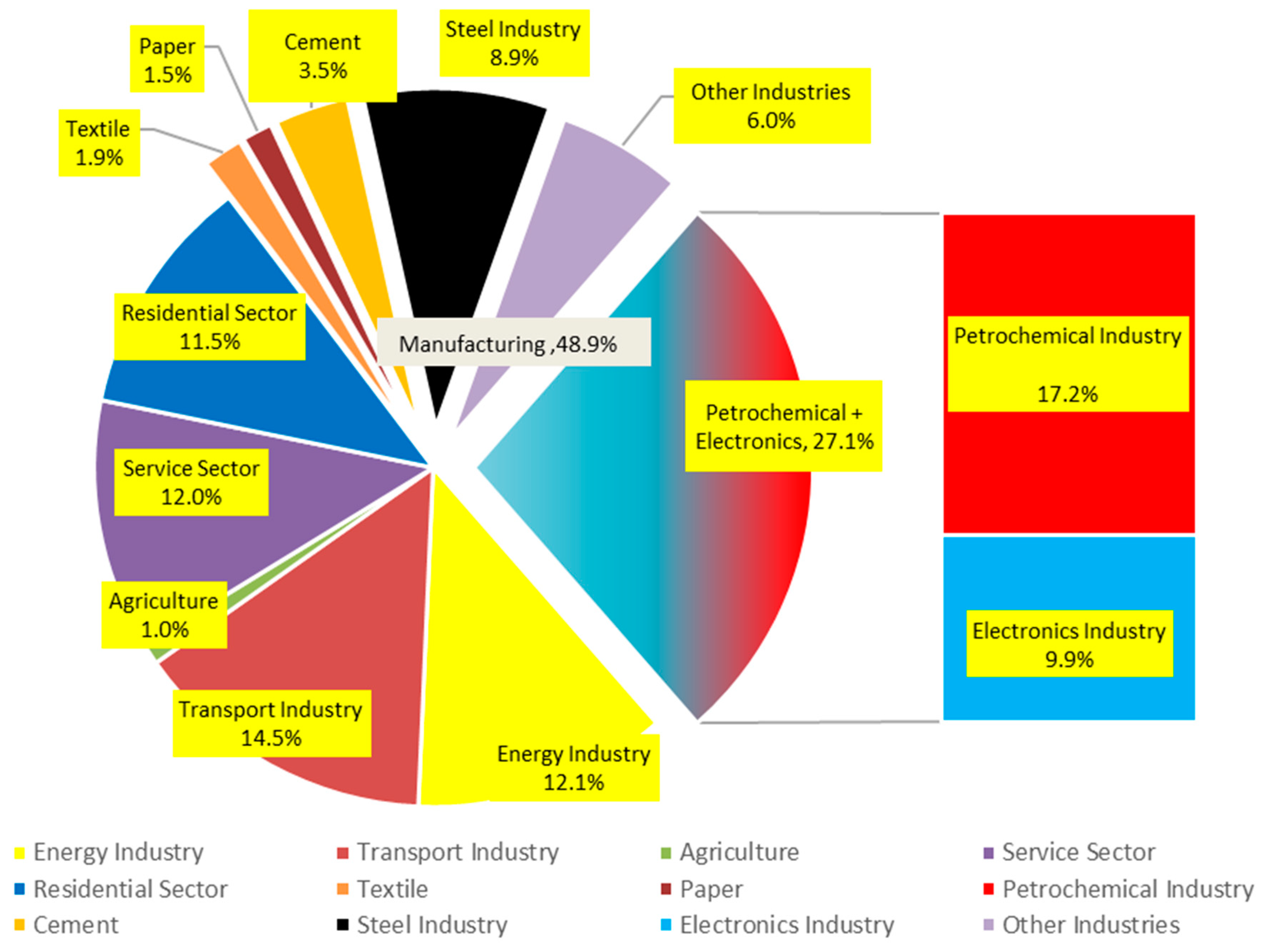

16]. As can be seen in

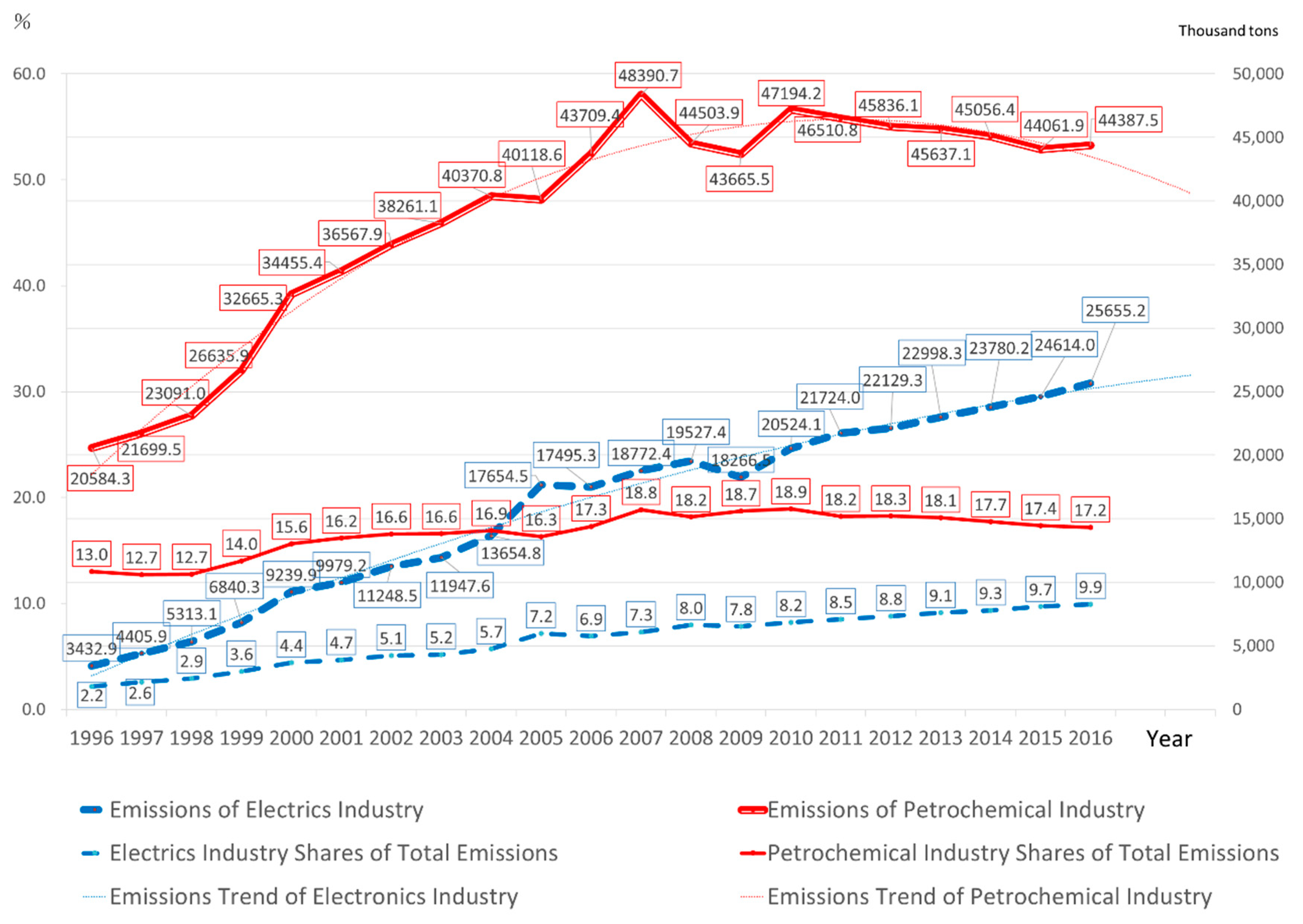

Figure 3, among Taiwan’s main carbon sources, industrial sources accounted for 48.9%, of which, more than half were from the petrochemical industry and electronics industry, which accounted for 27.1% of Taiwan’s carbon emissions in 2016, whereas other industries accounted for only 21.8%. In other words, more than a quarter of the carbon emissions in Taiwan are produced by the petrochemical industry and the electronics industry. The carbon emissions by the energy and transportation sectors accounted for another quarter (26.6%), and the residential, services, and agriculture sectors made up the remaining quarter.

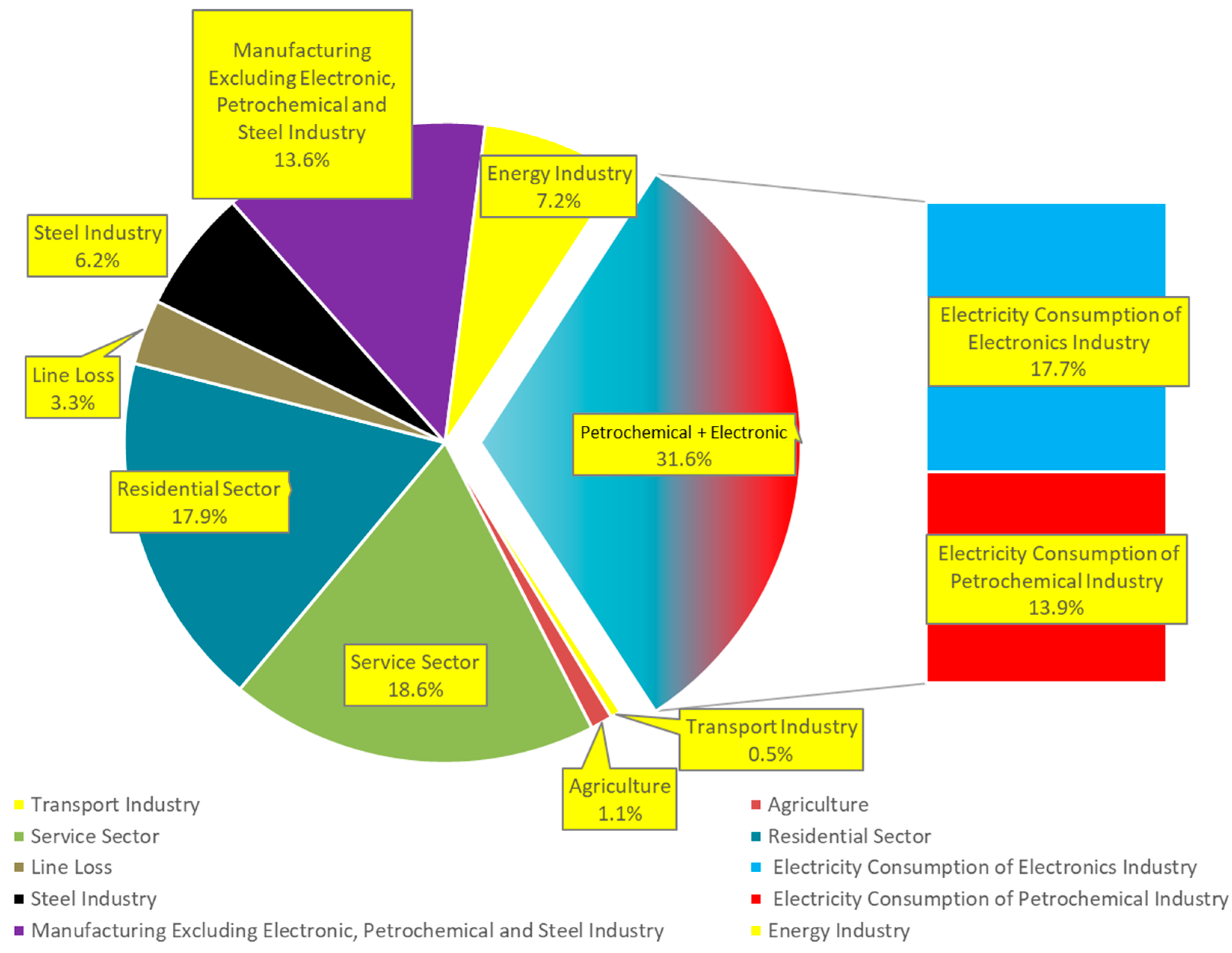

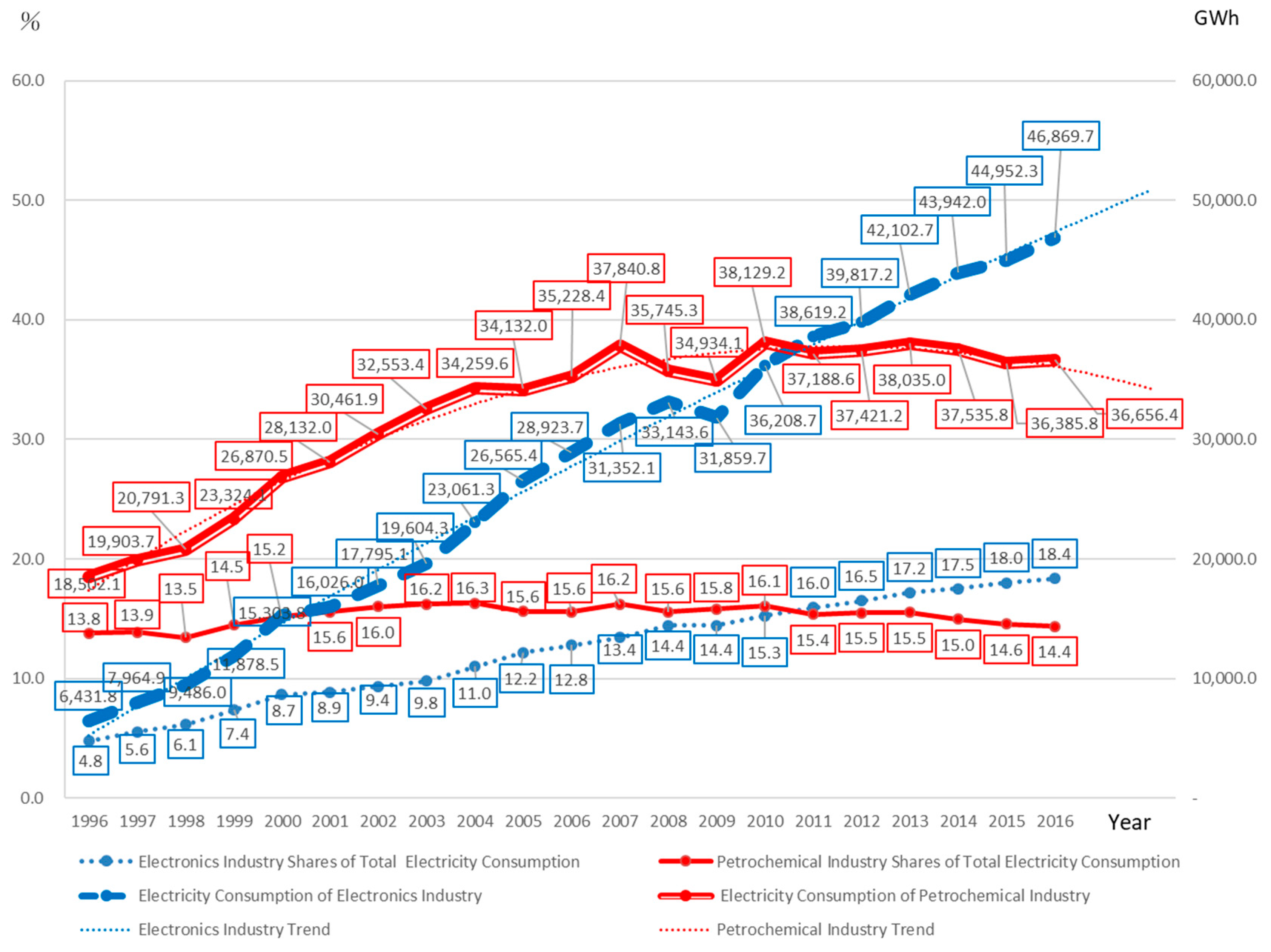

Figure 4 shows that the petrochemical and electronics industries made up the bulk of the total electricity consumption in Taiwan in 2016, with a consumption of 31.6%. The electricity consumption by the energy sector and by industries other than the petrochemicals industries made up 27.0%, which means that the energy consumption by the industrial and energy sectors comprised 58.6% of Taiwan’s electricity use and produced 62% of the carbon emissions. From the above analysis, it can be seen that for Taiwan to be able to effectively reduce carbon emissions and electricity consumption, whilst maintaining Taiwan’s international competitiveness, the key therefore lies in managing the high carbon emissions and high electricity consumption of the petrochemical and electronics industries. On the whole, the carbon emissions of 44,388 kilotons from the petrochemical industry is higher than the 25,655 kilotons from the electronics industry by about 1.7 times. In terms of electricity consumption, the electronics industry consumed 1.3 times that of the petrochemical industry.

Figure 5 and

Figure 6 show that over the past 20 years, the carbon emissions and electricity consumption of the chemical materials manufacturing (petrochemical and chemical materials manufacturing industries) and electronics (ICT) have been gradually increasing, though in recent years, chemical materials manufacturing has reached saturation. The current trend therefore suggests that carbon emissions and electricity consumption in the electronics industry will continue to rise [

17].

Based on available data, the TSMC is projected to consume about one-third of the total electricity consumption in Taiwan in the foreseeable future. Subsequently, along with a key process technology of the semiconductor industry, namely extreme ultraviolet lithography (EUV), electricity consumption will continue to increase. TSMC estimated that the electricity consumption of the 5-nm manufacturing process will be 1.48 times that of the current mainstream manufacturing process [

5] As TSMC had planned for mass production using the 5-nm manufacturing process in 2020, it would lead to a surge in electricity consumption, which would outpace the original electricity consumption plan. Thus, according to the policy, it would therefore be necessary to do an environmental impact assessment. Toward this end, the increase in projected power demand is extremely alarming, from the original plan of 1.52 GW to 2.22 GW, which is a substantial increase of 46%.

Under the latest national industrial development plan in Taiwan, the “five plus two industrial innovation plan,” the semiconductor industry lies at the foundation for the plan. For the five plus two industrial innovation plan, the Smart Machinery Industry Promotion Plan, the Asian Silicon Valley Development Plan, the Green Energy Technology plan, along with the biomedical, national defense, and new agriculture industries, as well as in the adoption of the circular economy, plus the two ICT-related investments under the Smart Machinery Industry Promotion Plan and the Asian Silicon Valley Development Plan, the government has invested 4 billion USD, with private investment amounting to about 1.7 billion USD. The electronics industry is also the basis from which new future applications, such as artificial intelligence and the internet of things, will develop from. Therefore, the future of the electronics industry will be the backbone of Taiwan’s economic development. However, for the electronics industry to continue to be developed in Taiwan, its electricity consumption will continue to grow, and in turn, lead to higher carbon emissions. The government therefore needs to think about how to sustain the development of the electronics industry whilst trying to meet the national carbon reduction targets within a limited energy supply and power generation capacity. As such, the biggest challenge that Taiwan is facing in its economic development is whether Taiwan’s energy transition can cope with the needs of its industrial development.

Since the contribution of the electronics industry to Taiwan’s economy is built on a high electricity consumption that leads to high carbon emissions and energy consumption, Taiwan’s economic policy therefore needs to weigh the trade-offs and consider how the electronics industry can continue to contribute greatly to the economy under the limited power generation and environmental capacity of Taiwan. The clue to this might lie in the incomplete industrial transformation that began in the 1980s, which would now need to be restarted. As a background, the industrial characteristics of the electronics industry and the chemical materials manufacturing industry (petrochemical industry) are different, and their contributions to Taiwan’s GDP are also vastly different. From

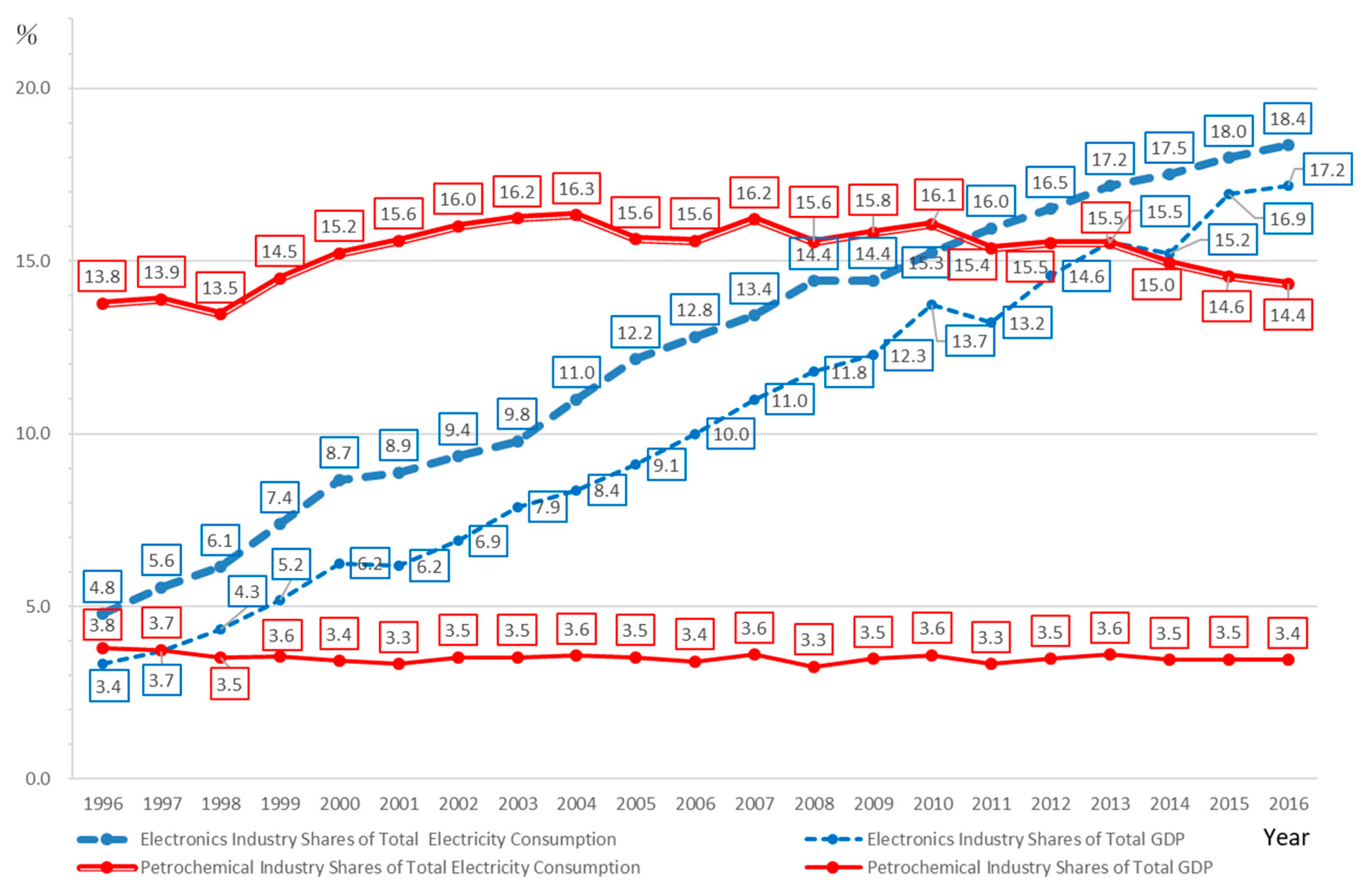

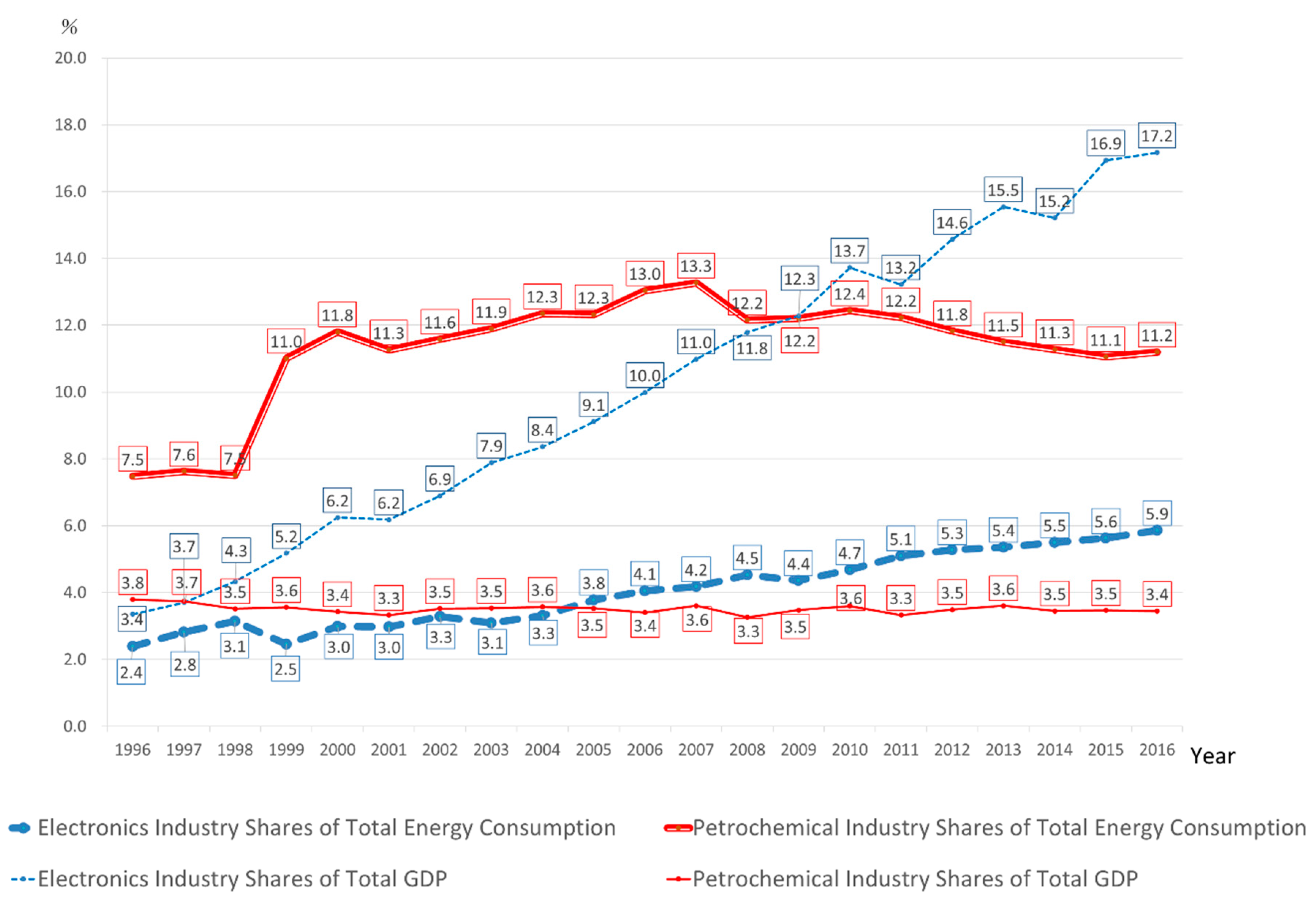

Figure 7, it can be seen that in the past 20 years, the electricity consumption and demand of the electronics industry has grown by 3.8 times and by 5.5 times as a percentage of GDP, and by 2016, reached 18.4% and 17.2%, respectively. The Formosa petrochemical corporation’s Sixth Naphtha Cracking Project in the petrochemical industry was successively completed during the first phase (1998–1999), second phase (2000), third phase (2003), and fourth phase (2007), and during this period of construction, it reached a peak in electricity consumption, at 16.3% in 2003 and 2007, but since then, this had fallen slightly to 14.4% by 2016. However, while the petrochemical industry dominated a high proportion of electricity consumption, its contribution to GDP was only 3.4%, having declined from 3.8% in 1996. Meanwhile, its electricity consumption in 2016 was high, at 14.4%. In comparison, electricity consumption in the electronics industry was high as well (18.5%), but the GDP contribution was able to reach 17.2% in 2016. Therefore, the high electricity consumption and power demand in the electronics industry brings about a higher contribution to the GDP, but the petrochemical industry is more energy intensive yet its contribution to the GDP is low.

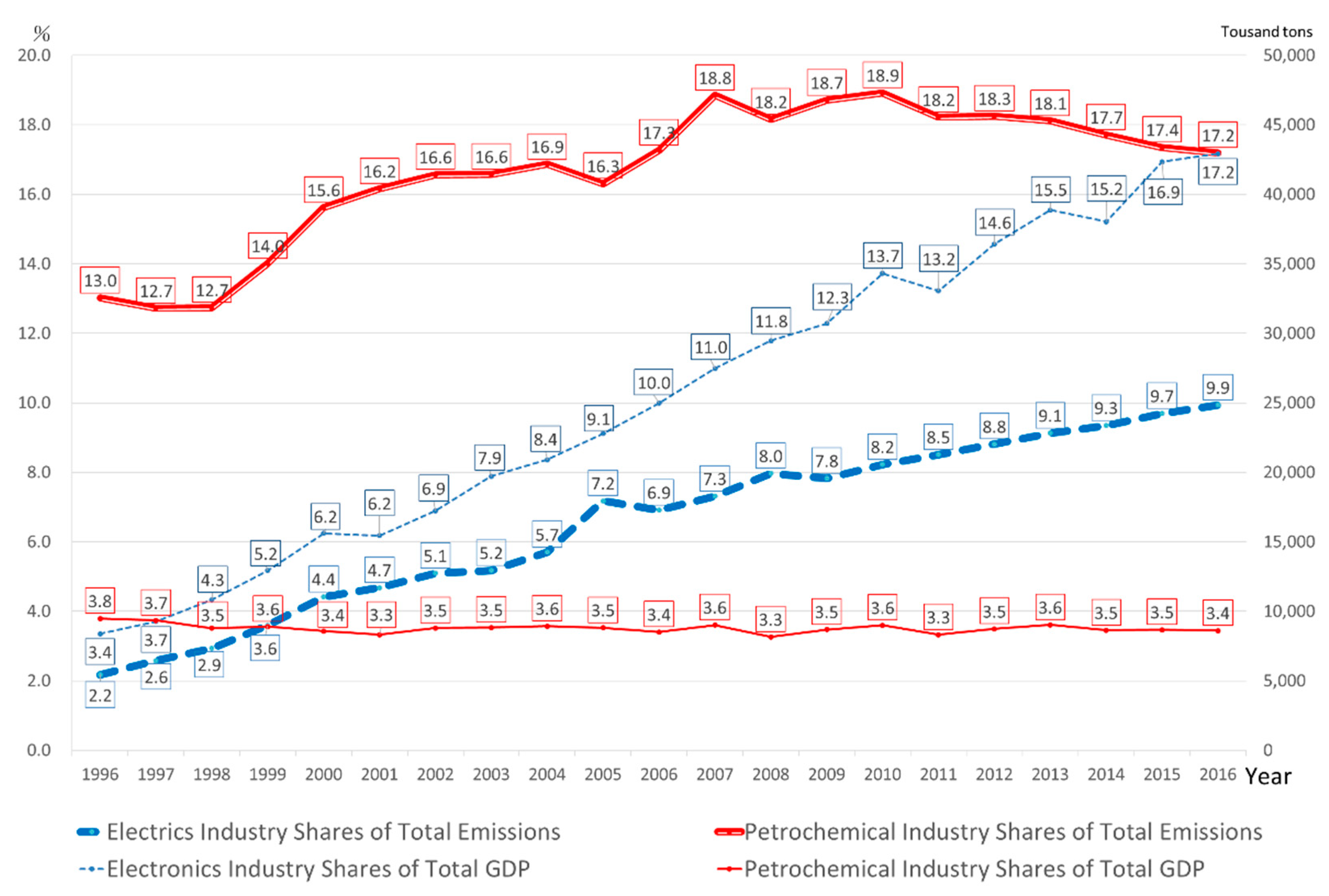

Next, we looked at the ratio of carbon emissions to GDP in

Figure 8. As the carbon emissions in the petrochemical industries is not only due to its electricity consumption, but also due to the process of fossil fuel burning, which also resulted in a large amount of carbon emissions, its carbon footprint as a proportion of the country’s carbon emissions is therefore higher than that for electricity consumption, reaching 17.2% of carbon emissions in the country, compared to 9.9% in the electronics industry. It is worth noting that the GDP growth rate of the electronics industry is faster than that of its carbon emissions, and the gap between the gradient of the lines is also increasing, which therefore demonstrates that the carbon emissions in the electronics industry is gradually decoupling from GDP.

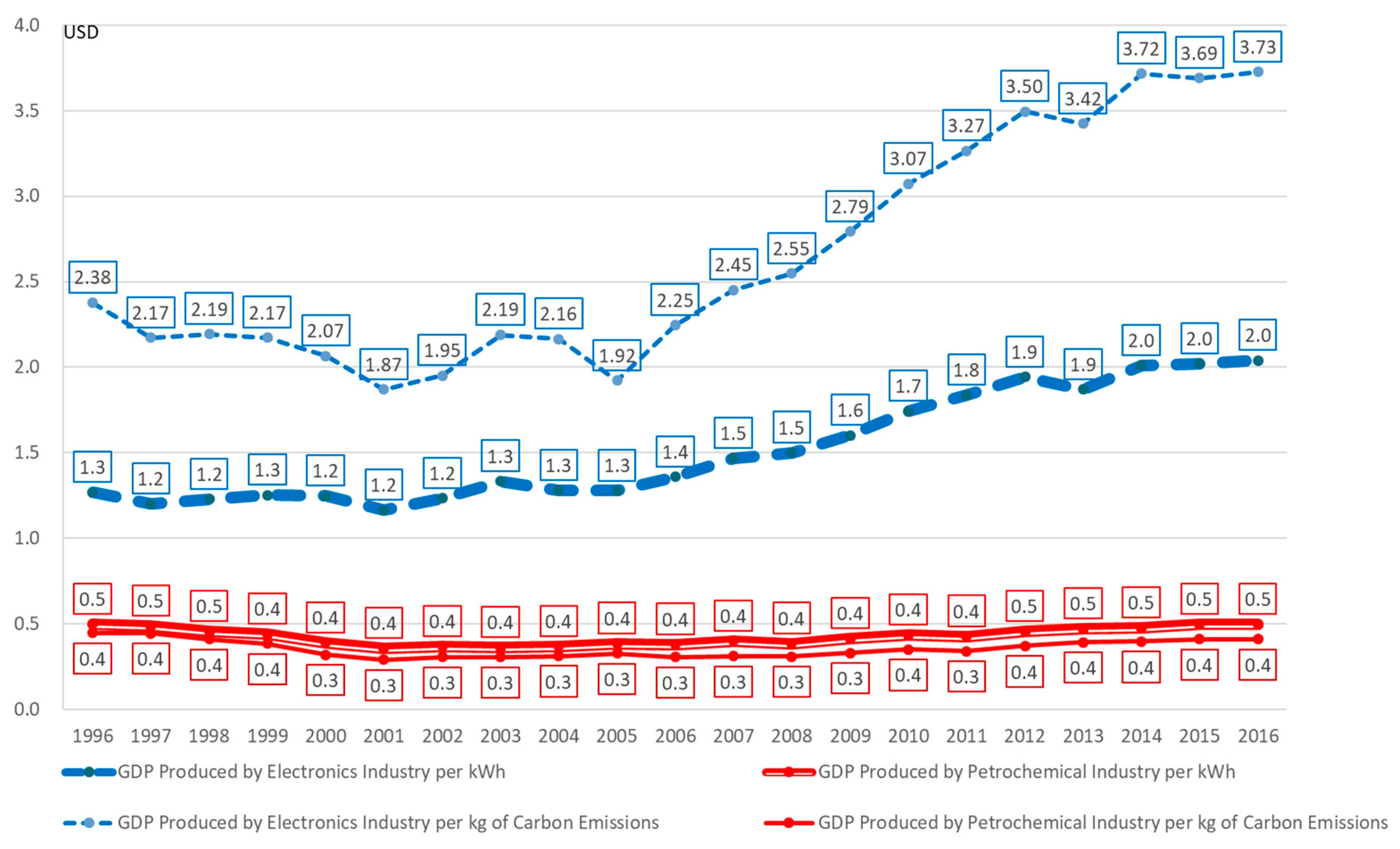

Figure 9 compares the GDP per kilogram of carbon emissions in the electronics and petrochemical industries with the GDP per kilowatt-hour, which clearly shows the GDP efficiency from carbon emissions and energy use. In 1996, the electronics industry produced 1.3 USD of GDP per kilowatt hour, and by 2016, it generated 3.73 USD per kilowatt-hour. The GDP efficiency from energy use therefore increased by 1.6 times in 20 years. The petrochemical industry produced only about 0.4 to 0.5 of GDP per kilowatt-hour from 1996 to 2016. Therefore, the GDP produced by the electronics industry with every kilowatt-hour of electricity was 4.1 times that of the petrochemical industry, and the GDP produced per kilogram of carbon emissions was 9.8 times that of the petrochemical industry.

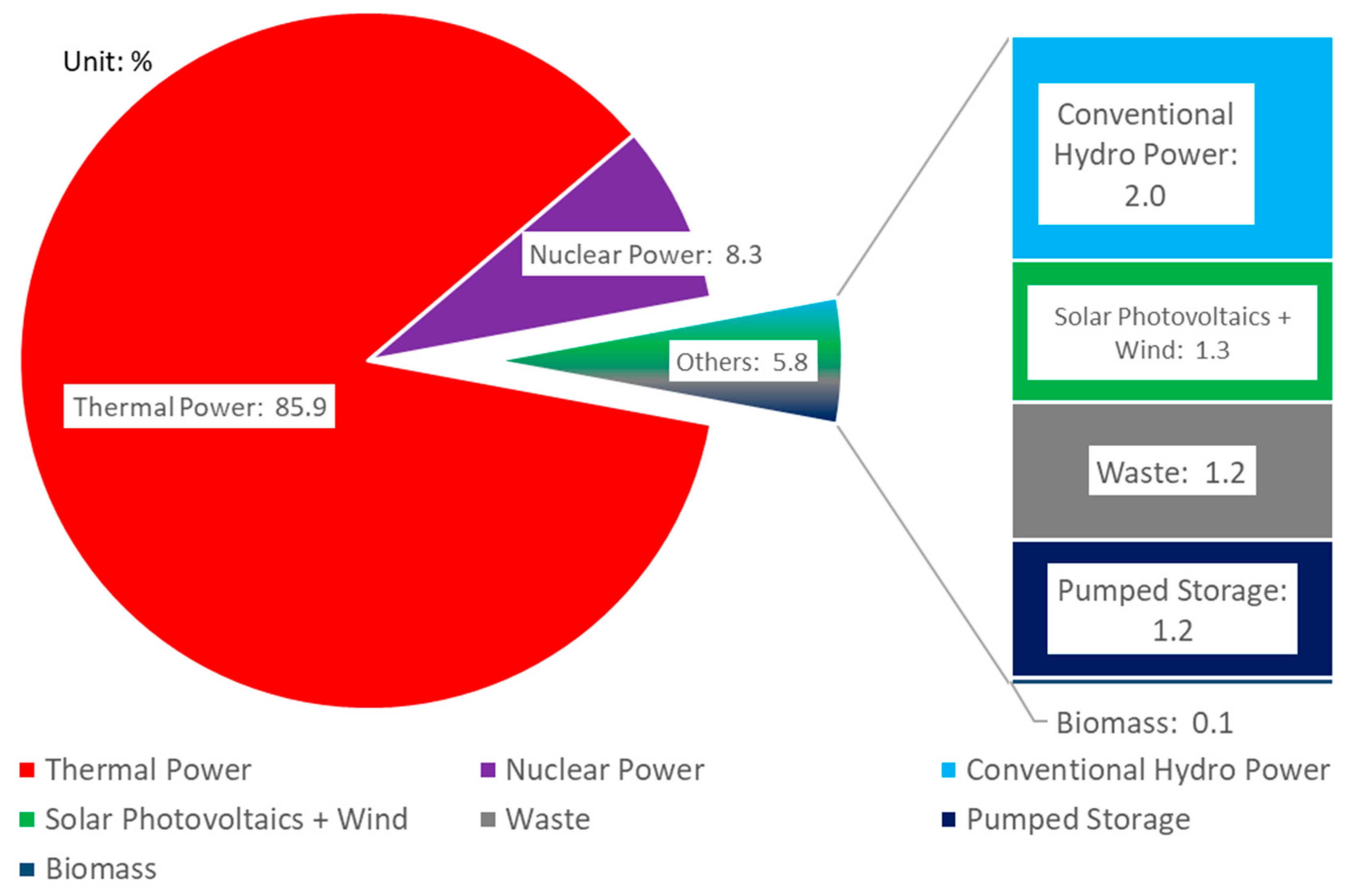

In addition, as can be seen from

Figure 10, the petrochemical industry itself consumes a lot of fossil fuels, resulting in the high carbon emissions. As seen from the perspective of electricity consumption (calculated as a barrel of oil equivalent), the difference between the electronics industry and the petrochemical industry becomes even more obvious. In 2016, the electricity consumption in the electronics industry accounted for 18.4% of the country’s consumption and 9.9% of carbon emissions, but energy consumption accounted for only 5.9% of the country’s consumption. For the petrochemical industry, electricity consumption comprised 14.4%, carbon emissions made up 17.2%, and energy consumption comprised 11.2%. In terms of the overall energy consumption, it can therefore be seen that the contributions of the electronics industry’s GDP had already decoupled from its energy consumption. This decoupling can be seen from the GDP per unit of energy use (change in the ratio between the two), which

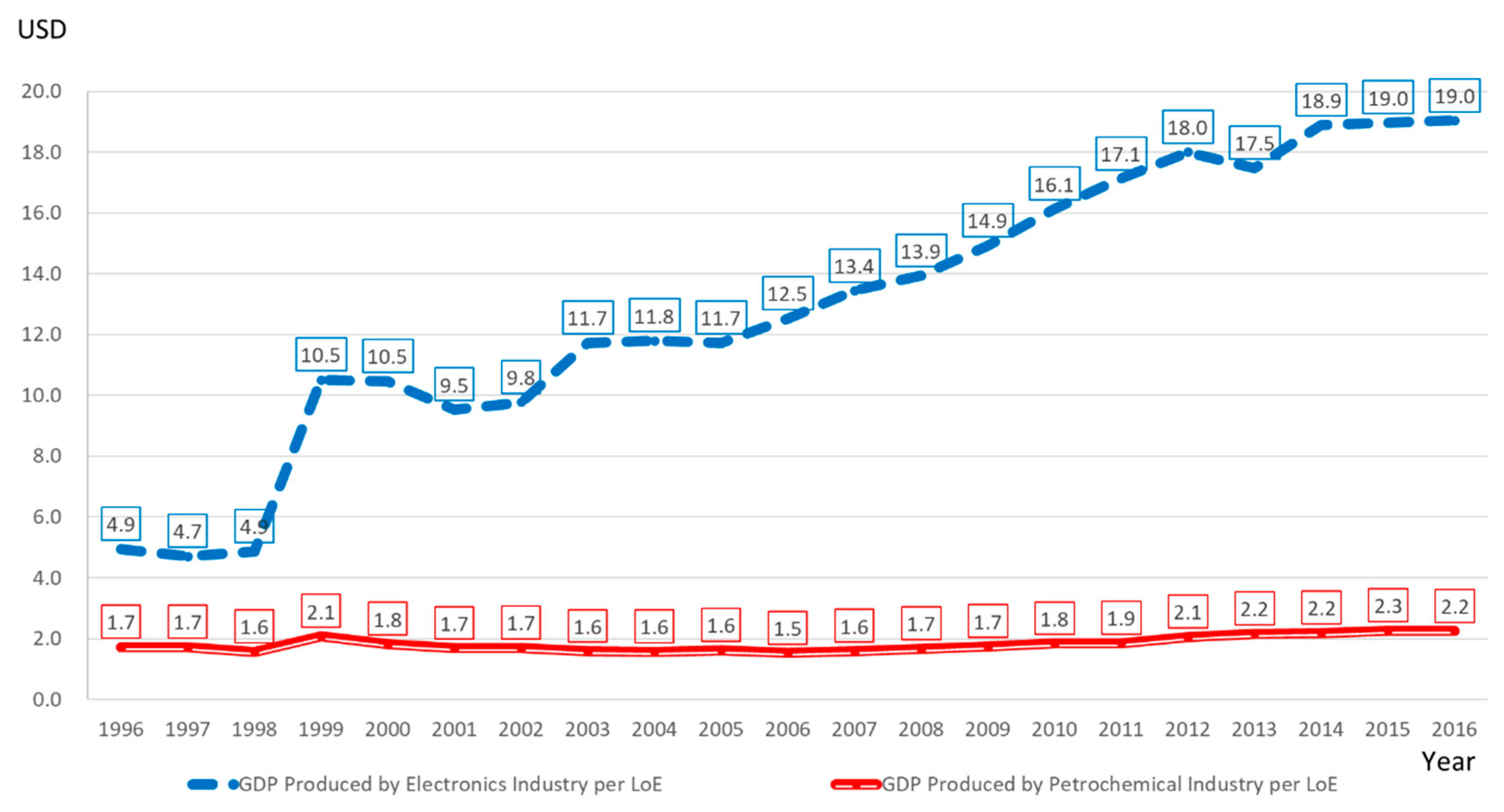

Figure 11 clearly shows: for every liter of oil equivalent energy use, the electronics industry produced a GDP of 19 USD, but this was only 2.2 USD for the petrochemical industry, with the difference being almost 8.4 times more.

As can be seen from the various data sets above, the two industries with the highest electricity consumption and carbon emissions in Taiwan are the electronics and petrochemical industries. In addition, the GDP per unit of carbon emissions and the GDP per unit of energy use (per liter oil equivalent, LoE) in the electronics industry is nearly 10 times higher than that of the petrochemical industry (see

Figure 9 and

Figure 11), while the GDP per unit of electricity used in the electronics industry was 4.1 times higher than the petrochemical industry (

Figure 9). It can thus be seen that as long as the electronics industry in Taiwan is able to find a solution to mediate its high electricity consumption, it will be able to grow under the limits of the energy and environmental constraints in Taiwan, and continue to significantly contribute to Taiwan’s GDP. In comparison, the innate processes of the petrochemical industry require high energy consumption but contributes less to the GDP. In addition to having to resolve the issue of electricity consumption and the innate characteristics of the industries that impact on electricity consumption, it would therefore also require an industrial transition to find a solution to the problem of high carbon emissions, and high electricity and energy consumption. In view of the fact that the energy supply is highly reliant on imports, and with so many industries that are dependent on energy as their raw material, they would therefore only be able to maintain their production profitability by relying on fossil fuel subsidies, which results in external costs being underestimated (unlevied carbon and energy taxes), and the environment being sacrificed.

4.3. Countermeasures: Reducing the Energy Consumption of the Petrochemical Industry to Maintain the Growing Electronics Industry

Although Taiwan was unsuccessful in weaning off its reliance on the heavy chemical industry during the industrial transformation in the 1990s, by 2016, Taiwan’s semiconductor exports had already accounted for 13.6% of global exports (ranking third in the world), and the semiconductor industry has thus gained more importance than the chemical industry in becoming the lifeblood of Taiwan’s economic development. The vertical integration of Taiwan’s semiconductor industry is highly flexible in the various processes of integrated circuit (IC) design, foundry production to package testing, and other fields. In 2016, the production value of Taiwan’s semiconductor industry reached 81 billion USD, and is expected to grow by 3.5% this year to reach 84 billion USD. Meanwhile, while Taiwan’s patent advantage lies in the integrated circuit technologies (ICT) industry, it is also mainly in the semiconductor industry and basic communication processing. Electronic information products have grown to produce the highest output value in Taiwan’s manufacturing industry. Taiwan’s ICT industry accounts for nearly 40% of Taiwan’s total exports and 20% of its GDP, of which 55% is exported to China (and Hong Kong).

TSMC has a current capital of 8.6 billion USD, which is the largest on Taiwan’s stock exchange, and its market value accounts for as much as 19.5% of the market. Based on the current development trend of Taiwan’s electronics industry, it is inevitable that the electronics industry will need to urgently address the issues of carbon emissions and power supply capacity in Taiwan [

17]. As the carbon emissions from the electronics industry comes mainly from electricity consumption, the key to the sustained development of the electronics industry therefore lies in the supply of electricity. Taking the Fourth Stage of the Central Taiwan Science Park as an example, AU Optronics’ power demand at the science park was 700 MW, and when including the upstream and downstream manufacturers located in the park, the power demand was 1.2 GW. In comparison, TSMC requires 1.1 GW of power load from the Taiwan’s power system every day, and accounts for 3% of the peak load in Taiwan (of about 36 GW). According to TSMC’s plans for new factories and other facilities, its power demand will increase by 1.1 GW over the next 10 years, and will account for 6% of the total power demand in Taiwan by then. Earlier this year, TSMC announced that it has planned for the mass production of chips based on its 5-nm process by 2020, which would increase its power demand by 720 MW [

3]. It was reported previously that the power demand of TSMC’s 3-nm chip factory was about 2.1 GW, and is currently at 1.25 GW, but this is still 1.7 times that of the 5-nm chip factory, and about three times the power generation capacity of Taichung’s power plants. It is estimated that TSMC’s overall power demand will also increase to 3 GW due to the 3-nm process, exceeding Taiwan’s overall power supply capacity by 10% [

5].

In terms of regional supply and demand, there is ample power supply in the central and southern regions. When not considering the power supply capacity of the first nuclear plant, the power supply capacity in the northern regions could be lower than the peak demand in the same regions (570 MW). Although the power supply capacity in the southern region is currently greater than the load demand, the remaining power was 1.68 GW in 2017, and as the plants are successively retired, it is estimated that TSMC’s current expansion will increase the power load in the south, which could greatly increase the strain on carbon emissions and power load in the southern regions [

17].

From the analysis above, it can be seen that the greatest strain on Taiwan’s electricity and carbon emissions comes from the electronics and petrochemical industries. In addition, the electronics industry also represents a significant contribution to Taiwan’s GDP and will continue to be the mainstay of Taiwan’s economic development, with the government and the private sector also focused on investments in the electronics industry. The high energy consumption and high carbon emissions in the petrochemical industry are also produced due to the innate processes of the petrochemical industry, which requires the burning of large quantities of fossil fuel, in addition to requiring high amounts of electricity. On the other hand, Taiwan’s economy has moved toward types of industries like electronics, where manufacturing is based on knowledge, innovation, and increasing added value. The IC manufacturing industry has also moved from assembly and original equipment manufacturer (OEM) production to projects based on IC design, precision technologies, and system integration (such as TSMC, Largan Precision, and HTC). This is also why the electronics industry is also not considered part of the energy-intensive industries, as the GDP produced per kilowatt-hour of electricity use is 4.4 times that of the petrochemical industry, and 12 times in terms of the GDP per kilogram of CO2 emissions, and 13 times in terms GDP per liter of oil equivalent production. Therefore, the key to whether the electronics industry can continue to achieve favorable development in Taiwan lies with an industrial transition, and whether the government is able to transit away from the petrochemical industry, otherwise the development of the ICT industry will be constrained. It is of course necessary to consider whether the affected groups and social support system can withstand the impact of the production reduction of the petrochemical industry or the transition away from it, which would require social impact assessments be conducted and adjustment measures designed for the most vulnerable groups. However, considering the current situation in Taiwan, the government is faced with the dilemma of how to proceed.

Research shows that Taiwan’s low-carbon and energy transition plans over the last 20 years have been mutually contradictory [

15]. From the perspective of the post-development theory, the economic orientation that Taiwan’s government has adopted has led to it lagging behind other industrialized countries, but this has come at the sacrifice of the environment and people’s health, and resulted in the economy being driven by energy-intensive industries. However, from the rapid economic growth of Taiwan in the 1970s to Taiwan’s GDP per capita breaking through

$US10,000 in 1992, Taiwan’s competitive edge no longer lies in low-cost labor, nor does it lie in a sacrificial system based on low production costs that plunders the environment and health of the people. Environmental awareness has been gradually improving and the country has turned its attention to environmental and labor rights and interests, while at the same time, petrochemical capital from the United States and Japan was also gradually being withdrawn from Taiwan. Therefore, since the “Economic Construction Plan” created in 1976, strategic industries have been supported with a policy direction, especially in the electronics industry, that was intended to replace the heavy and chemical industries [

19]. However, under the political influence of the private sector, which continued to engage in downstream petrochemical processing and raw material exports, this has resulted in the transition away from the heavy and chemical industries being only half-complete. In the 1980s, the electronics industry grew rapidly in the science parks and became an important bedrock for Taiwan’s economy. However, from when the fifth naphtha cracker plant commenced production in 1994 to the completion of the sixth naphtha cracker plant in 1998, the national policy continued to promote the petrochemical industry, which resulted in the existence of two high energy-using industries in Taiwan: the electronics and petrochemical industries. The policies at that time resulted in the petrochemical industry reducing the space for the electronics industry to compete in, thereby threatening Taiwan’s economic development. How these two industries should be transformed is not only a question for Taiwan’s energy transition and greenhouse gas reduction plans, but more importantly, is a key challenge for the future development of Taiwan.

Taiwan should therefore reduce the actual emissions and electricity consumption of the petrochemical industry, and not only in terms of its contribution rate to the GDP. The analysis in this section shows that the petrochemical industry has a large amount of direct emissions. According to the Ministry of Economic Affairs, the best available control technology (BACT) has been achieved for direct emissions from large facilities [

20]. However, industry representatives believe that the reduction target may hinder Taiwan’s industrial development and damage Taiwan’s international competitiveness. Therefore, the hands of the government are tied and it feels constrained in its ability to tackle the core of these problems. Relatively speaking, the carbon emissions of the electronics industry are mainly produced via the electricity generation of the energy sector. As such, the next section will focus on looking at how Taiwan’s energy composition can be improved to reduce carbon emissions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}