Virtuality Changes Consumer Preference: The Effect of Transaction Virtuality as Psychological Distance on Consumer Purchase Behavior

School of Management Information Systems, Kookmin University, Seoul 02707, Korea

Sustainability 2019, 11(23), 6618; https://0-doi-org.brum.beds.ac.uk/10.3390/su11236618

Submission received: 31 October 2019

/

Revised: 14 November 2019

/

Accepted: 19 November 2019

/

Published: 22 November 2019

(This article belongs to the Special Issue Fintech and Logistics in the Fourth Industrial Revolution Era)

Abstract

:With the rapid development of information and communication technology, a variety of new industries and services are rapidly evolving based on the convergence between existing Information and Communication Technology (ICT) and heterogeneous industries. In the meantime, the FinTech market, created by the convergence of financial and ICT areas, is emerging and growing rapidly. The new market of virtual transaction based on digital money is growing faster than any other FinTech area. The purpose of this study is to determine whether the perceived difference in the virtuality of a consumer’s transaction affects the consumer’s purchasing behavior and how the behavior changes. Specifically, this study revealed that consumers’ perceived virtuality differs according to the type of transaction method. Consumers felt that the money was more virtual when they had digital (virtual) currency for a service than when they had cash. This virtuality of money controls the psychological distance of the consumer’s money, which is closer to cash than virtual currency. This difference in psychological distance affects consumers’ information processing, such that when psychological distances are far (vs. close), consumers prefer products that are described as abstract (vs. concrete), and have a more favorable attitude toward products with more variety.

1. Introduction

With the rapid development of Information and Communication Technology (ICT), a variety of new industries and services are rapidly evolving based on the convergence between existing ICT and heterogeneous industries, or between online and offline services. In the meantime, the FinTech market, created by the convergence of financial and ICT areas, is emerging and growing rapidly [1]. In particular, with the development of mobile technologies (i.e., smartphones and tablet PCs), the new market of virtual transactions, based on digital money, is growing faster than any other FinTech area, including mobile payment, digital wallet, virtual transfer, peer-to-peer financial platforms, and financial data analysis.

A new technology, digital money, has emerged as a medium of exchange/measure and store of value in electronic form [2]. As a purely digital form of currency, digital money exists as a means of payment with a cash equivalence. It is used for commercial transactions of goods and services in a highly connected world in which the globalization of trade is increasing and most of the population is becoming urbanized. Digital money has been facilitated by the use of technologies such as mobile phones, cloud computing, data analytics, encryption and storage, and near-field communication technology. The diffusion of these technologies is likely to accelerate the virtuality of transactions, and hence their scale and scope, lubricating frictions in the financial system to make the world go around more quickly and extensively [3,4].

Digital money dematerializes by moving everyday economic transactions—such as payments, transfers, and receipts—from the physical to the digital world. Although its progress will evolve as the technology and its social and economic influences interact, it is potentially transformational technology. Digital money makes transactions faster, cheaper and more widespread. It disintermediates, connecting people and money more closely [5].

According to this trend, Samsung and Apple, the dominant smartphone makers, have launched their own digital money using their smartphones [6]. Also, Alibaba, Amazon, and other online shopping service providers have utilized digital money that can be used without restrictions in their marketplace [7]. In other words, digital money is a new business opportunity for companies in various industries. For consumers, digital money offers the potential for easier and cheaper access to finance. However, it also carries risks for consumer security and privacy insofar as their wealth is digitally managed.

Would consumers’ use of digital money not only change these technical aspects but also their consumption patterns and behaviors? When credit cards were first introduced, several studies such as Hirschman [8] and Prelec and Loewenstein [9] showed that credit card use, and cash use differed in terms of consumer behavior. These studies revealed that credit card purchasing methods tend to exhibit (1) stronger purchasing tendencies and (2) more consumption than cash-based purchasing methods [8,9]. The cause of this phenomenon is explained through the concept of the pain of payment [9]. This concept refers to the feeling of loss that one feels after spending money. Since the pain of payment by credit card is much smaller than that of cash payment, consumers are more likely to spend more on their credit cards than when using cash. At the present time, after 30 years of credit card use, credit card use and cash use are very similar in many respects, with the exception of some consumers who only use credit cards (e.g., freshmen in university).

The use of digital money differs from credit cards in many ways [2,10]. Divided broadly, (1) all transactions and expenditures are made in a virtual environment, (2) balances of currency exist only in digital numbers, not as physical entities, and (3) payment is made using virtualization-based technologies such as barcode recognition or Near-Field Communication (NFC). When consumers perform these virtual transactions, is the consumer’s psychological and cognitive processing the same as when they use traditional cash or credit cards? If so, what mechanisms influence consumer behavior? This study begins with these key questions. In my knowledge, recent research on digital money has focused on (1) the definition of digital money [2,11], (2) the macroscopic perspective of digital money on the economy [10,12], and (3) the motive and individual perception for using digital money [13,14,15]. There is a lack of studies to show the psychological mechanism for digital money.

The purpose of this study is to determine whether the perceived difference in the virtuality of consumer transactions affects the consumer’s purchasing behavior and, if so, how the consumer’s behavior changes. Specifically, if the consumer feels a different level of virtuality for each transaction, it is plausible that this virtuality can affect the consumer’s information processing and change the consumer’s buying behavior. If consumers feel the level of virtuality is greater, and the transaction psychologically feels more distant from themselves. According to construal level theory [16,17,18], if an individual feels psychologically distant, he/she will process information at a higher construal level, meaning that he/she will prefer something more desirable when choosing a product and more diverse when constructing a product. On the other hand, if the psychological distance between oneself and a transaction is relatively short, one may think more concretely and prefer a more feasible option than what one desires, and a more familiar and harmonious composition than a new and diverse composition. This study examines and tests the proposed hypothesis through two experiments, and finally derives theoretical contribution points and practical implications from the perspectives of (1) companies managing digital money, (2) consumers who use digital money, and furthermore (3) central and local governments which need to derive a policy or overall structure for digital money.

This paper is organized as follows. After the introduction, we review the related research on virtual payment, construal level theory, and virtuality, deriving an interesting hypothesis with a persuasive logic. The two experiments that were conducted to test the hypothesis presented are described in turn, and the contributions of the study based on the results of the study are presented in the conclusion section.

2. Theoretical Background and Hypotheses

2.1. Virtual Transaction Based on Digital Money

Recently, with the rapid development of ICT technology, financial settlement services that were processed on a PC basis are now being processed in a mobile environment through smartphones. In addition, if financial services were mostly provided under the leadership of the traditional financial industry, a new financial services market provided by the non-financial ICT companies is growing. In other words, a new financial service, FinTech, is appearing. FinTech is a new convergent financial service that combines the words “finance” and “technology” [1].

FinTech is meant to include all of the technical processes that can create new software or improve the performance of financial services. FinTech is a general term for technologies that affect financial institutions’ overall operations, including financial decision making, risk management, portfolio restructuring, compliance work, performance management, system integration, online transfers, and payments. FinTech also includes mobile finance, easy payments, money transfer, asset management, and crowdfunding, using wireless Internet and telecommunications technology.

Among the FinTech services, digital money-based virtual transactions are attracting attention as a core industry due to the rapid increase in smartphone usage and the continuous development of information and communication technology. Digital Money initially meant ‘virtual money,’ which e-commerce and content providers had offered to their members in the form of mileages and issue as a kind of incentive to sustain customers [19]. In the past, digital money was limited to mileage points and promotional coupons, but in recent years, it has become possible to make virtual transactions—such as financial transactions and shopping as a currency—that are physically invisible but have the same effect as money in the digital world. [10]. With reference to the above previous research, this study defines digital money as ‘electronic payment means having the same (or similar) value as the currency we normally use.’

Digital money has made it possible for consumers to make simple payments and purchase goods and services using mobile devices that guarantee mobility in online and offline environments. The simple payment service through digital money refers to a service that enables payment through a simple authentication process, as opposed to existing payment methods that literally input credit card information or authenticate through authorized certificates. Simple payments services are emerging alongside the development of new technologies such as one-click payment, no Active X, and new authentication technology (e.g., password, pattern, fingerprint, etc.). The simple payment service market is currently forming a competitive structure with operators participating in the market in various industries and is categorized according to the characteristics of its providers [20]. The representatives include Apple Pay in the US, Alipay in China, and Kakao Pay in Korea, Amazon and Seoul City are even launching their own digital money.

Virtual transactions through digital money differ from traditional transactions. First, digital money is more virtual than traditional transactions because it pays for money without a physical entity. Second, the balance cannot be accessed directly after the payment—unlike with cash, which goes directly into the recipient’s wallet—digital money remains more virtual in the digital world. Finally, consumers use the latest technology in most of their processes, from paying to checking balances. Consumers perceive the transactions through digital money as a virtual experience by experiencing firsthand the many scenes that have appeared in movies in the past (e.g., payment through QR code or NFC contact). The virtuality of the consumer perceived through the above digital money can affect the purchasing behavior of the consumer. If I check how this virtuality affects consumers’ information processing, I can predict the changes in consumer behavior accordingly.

2.2. Virtuality as a Psychological Distance

Various research fields consider virtuality an important research topic and, in general, define it as a digital object or experience without physical existence [21]. Research on virtuality has been conducted in various fields such as Augmented Reality, Virtual Reality to Personal Online Community Activity, Avatar Activity, and Organizational Virtual Team Virtual Office. This study focuses on the virtuality of digital money and virtual transactions based on the emergence of FinTech.

In this study, I would like to argue that virtuality can be thought of as another form of psychological distance. For this purpose, let us first consider the construal level theory and the concept of psychological distance. The construal level theory is a comprehensive model of what kind of thinking is used, and under what conditions, among the various ways of thinking [17,18]. According to the construal level theory, an individual has a different level of interpretation of a particular object depending on the object of decision-making, the psychological distance to the environment, or the context, resulting in different ways of thinking and decision making. Individuals measure their psychological distance from a particular object or event based on their place or the current time. The further the future is from now, the farther away from the present place, the less familiar or stranger, the less likely that a particular event will occur—the greater the individual’s psychological distance. Depending on the psychological distance, the individual’s way of thinking will change. The greater the psychological distance is, the more likely people are to make a higher-level construal of things or events, the shorter the psychological distance is, the more likely they are to make lower-level construal.

Several studies of construal level theory have shown that if an individual has a high-level construal, he/she goes through an abstract thought process, and if an individual has a low-level construal, he/she goes through a specific thought process [16,17]. Focusing on important variables known to control psychological distance (e.g., temporal, spatial, social, and probable distance), many studies [22,23,24,25] explain how individuals behave in the real world depending on these variables and how companies can use these variables. The search for what controls psychological distance is a more fundamental, scalable, and valuable study.

This study argues that the perceived virtuality of an individual can act as a form of psychological distance. It is very interesting to consider how the virtual perception of the individual will affect his/her construal level. For the digital money that I focus on in this study, what does it mean for consumers to feel that digital money transactions are more virtual than traditional transactions? Individuals can feel free from physical reality through virtual transactions and feel a bit off from their recent restrictions. In a situation far from reality, an individual can be freed from various constraints that bind and define him/her in the real world, which makes it easier for him/her to pursue his/her values. After all, in situations where the individual feels highly virtual, individual decision-making will focus on the purpose itself rather than on the means necessary to achieve it. In addition, in evaluating a particular object or event under highly perceived virtuality, an individual will be more likely to put weight on desirability instead of feasibility—a problem that is primarily confined to the real world. In the case of highly perceived virtuality, it is freed from the realistic constraints of the individual, so it is more likely to be relatively free and less likely to consider the feasibility of the event.

2.3. Change of Purchase Behavior Depending on Payment Method

This study examines the change of purchase behavior depending on the payment method from two perspectives. The first is to determine what attributes consumers choose based on their virtuality in relation to the product’s choice.

Construal level theory argues that the construal level is determined by the psychological distance and that the appropriate type of information is also determined by the construal level [18]. Information types can be classified in various ways, but this study intends to classify them into two types: attribute-based information and benefit-based information. This is a type of framing in which the characteristics of a particular product or service are described as either “specific and relatively objective attributes or fact-based descriptions” or “interpretations once processed as abstract and subjective benefits” [26].

Attribute-based information is the information that emphasizes the unique features or functions of a product or service and can show the capabilities and means of the product concretely and objectively. On the other hand, benefit-based information can show the results, benefits, needs, and objectives of using these functions and features [26]. In other words, it can be interpreted as ‘means-purpose difference’ and ‘process-result difference’ to emphasize either attribute-oriented information or benefit-based information. In comparison, attribute-based information is to means as benefit-based information is to purpose [27]. In addition, attribute-based information is to process as benefit-based information is to result [28].

According to the study of the effects of information types using the construal level theory, individuals with higher construal levels are closer to “objective/result-oriented thinking that values the outcome of the event or the benefits of the object” and those with lower construal levels are closer to “process/means-oriented thinking to achieve a goal” [28]. In addition, abstractive thoughts at a higher construal level are more likely to be set based on the desirability of the results/ benefits of using the product or service. Conversely, the concrete idea of the lower construal level is more likely to be set based on the details of the product or service, the process of use, and the feasibility of the means [29]. The reasons for the preference for this type of information are as follows. Individuals with a higher construal level draw on the core of a given piece of information to visualize relatively neat and clear abstracts in their minds. On the other hand, individuals with a lower construal level break down the given information to the desired level to derive detailed elements and to envision specific and practical content in their minds. Given the same type of information as the thinking-style in mindset, it is easier and faster to accept, and this quick acceptance itself feels more persuasive as the metacognitive action.

As mentioned earlier, when a consumer purchases a product through a virtual transaction, the perceived virtuality felt by the consumer will be higher than that of a traditional transaction. At the point of decision-making, the greater the degree of virtuality perceived by an individual, the greater the psychological distance from the object he or she faces will be, because he/she feels that he/she is away from reality. That is, he/she has a higher construal level. In this case, if an individual is dealing with a product that emphasizes abstract benefits rather than a specific attribute, he/she thinks that he/she has received his/her own way of thinking and more appropriate information (i.e., metacognitive effect), and consequently has a more favorable attitude toward the product. On the other hand, in the case of the traditional transaction, when the degree of virtuality is low, the situation is not very different from the reality on which it is based, so individuals are more likely to have a lower construal level. In this case, if an individual is dealing with a product that emphasizes concrete attributes rather than abstract benefits, he/she thinks that he/she has received the same type of information as his/her own way of thinking (i.e., a metacognitive effect), and consequently has a more favorable attitude toward the product. Accordingly, I hypothesize the following.

Hypothesis 1.

When purchasing a product through a virtual transaction, the consumer’s attitude toward the product described as benefit-based information will be higher than the attitude toward the product described as attribute-based information.

Hypothesis 2.

When purchasing a product through a traditional transaction, the consumer’s attitude toward the product described as attribute-based information will be higher than the attitude toward the product described as benefit-based information.

Another important consumption pattern is variety-seeking. Variety-seeking is defined and handled from various points of view, from motivational parts such as a dynamic satiation model of variety-seeking behavior [30] and a balance model for variety-seeking [31], to behavioral parts such as a single choice on each purchase occasion in successive periods (i.e., sequential choices) [32,33,34,35] and multiple choices simultaneously on a single purchase occasion (i.e., simultaneous choices) [32,36]. This study deals with the variety-seeking behavior that entails a selection of multiple items from Simonson [32].

People seek variety because of their intrinsic desire for unfamiliar, new, or unique experiences. Faison [37] argued that variety-seeking is ultimately an internal drive—an inherent desire for making a change. Individuals are always ready to look for something new or different and to avoid the feeling of boredom or lack of stimulation [37,38]. This variety-seeking also carries risks. If an individual chooses something new rather than a familiar or well-known option, he/she may be disappointed or dissatisfied with the product and may hear others’ accusations or complaints. In other words, there is always a conflict between the desirability of pursuing newness and the feasibility of being safe and stable in variety-seeking behavior. This study believes that construal level theory can explain who prevails between these two conflicts.

When consumers have a higher construal level, consumers are likely to process information based on desirability rather than feasibility. In this case, consumers’ inherent desire for newness can be superior to the feasibility of reality, and thus there is a high possibility for variety-seeking behaviors to be motivated by desire. On the other hand, when consumers have a lower construal level, they will process information based on feasibility rather than desirability. Consumers will focus more on the risks than on the pursuit of newness, and they are more likely to be more stable. This is expected to lower the variety-seeking behavior as a result.

This study argues that the perceived virtuality of transactions affects the construal level and psychological distance to a target. As a result, in the case of virtual transactions, the psychological distance and construal level may increase, and consumers may be more inclined to pursue their inherent desire for newness. The thought of “taking something new with this opportunity” will be greater than the concern over the risks that come from new and unfamiliar choices, and products with multiple options will take preference. On the other hand, in the case of relatively traditional transactions, consumers’ psychological distance to a target is close and the thoughts about reality appear more frequently. In this case, consumers want their purchases to meet their past levels of satisfaction by making more stable purchases than new pursuits. Eventually, consumers will prefer products that consist of familiar and well-known options rather than a variety of options. Accordingly, I hypothesize the following.

Hypothesis 3.

When purchasing a product through a virtual transaction, the consumer’s attitude toward the product with more variety (new and challenging options) will be more positive than his/her attitude toward the product with less variety (familiar and well-known options).

Hypothesis 4.

When purchasing a product through a traditional transaction, the consumer’s attitude toward the product with less variety (familiar and well-known options) will be more positive than his/her attitude toward the product with more variety (new and challenging options).

3. Experiment 1: The Effect of Virtuality on Product Attitude Depending on Information Type

3.1. Research Method

3.1.1. Experiment Design and Participants

The purpose of experiment 1 was to find the effect of virtuality on Consumer information Processing and consequent purchase behaviors depending on the type of product information. Specifically, focusing on the virtuality of a transaction, I tried to show that consumers’ preferred form of information changes, ultimately affecting product purchases, according to the level of virtuality the consumer feels. To verify these relationships, a 2 × 2 factorial design was conducted for this experiment. The independent variables were: virtuality of payment method (virtual vs. real), and information type (benefit-based vs. attribute-based). Two hundred people participated voluntarily. Their average age was approximately 33.99 years, and 49% were male. A reward of $5 was given to all the participants who visited the experimental site. All of them already had online shopping experience with major Korean service providers such as Gmarket, 11st, and SSG. Participants were randomly assigned to each condition.

This study tests the proposed hypotheses using experiments. Pre-testing is necessary to create the stimulus of the experiment. Similar to other studies [26,39,40,41,42,43,44], a qualitative small interview was conducted on 10 college students. Through this investigation, the experiment subjects, the stimuli of the independent variables, and the suitability of the scenario could be determined. Several comments from the pilot test were used to correct the stimulus and correct the measurement items.

All participants visited a virtual shopping mall site referring to the Amazon site. Amazon is a very famous shopping platform across the world but has not yet provided major services in Korea. So, I benchmarked it to develop the virtual site. For the participants, the service was considered to be a new shopping platform, eliminating any prejudice about the past online shopping experience.

3.1.2. Experiment Variables and Measurements

(1) Virtuality of Transaction Type

In order to manipulate the level of virtuality perceived by an individual when making a purchase, the transaction type was divided into cash settlement and virtual currency settlement. In this experiment, the participants received a total of $100 in rewards for their initial membership with the online shopping platform. The types of transactions varied depending on whether the participants received this reward in cash or virtual currency. Through this manipulation, the study expected participants to use the same amount but different types of currency so that those who were given cryptocurrencies—as opposed to those who were given cash—would perceive the payment method to be more virtual and experience a greater psychological distance. To check the manipulation, this experiment borrowed and revised the virtuality measurement of a previous study [39,40]. The 7-point numeric scale measurements were as follows: the reward is (1) real–virtual, (2) tangible–intangible, (3) held in hand–not held in hand, and (4) analog–digital. To measure the psychological distance for the reward, the participants were asked to take four measurements on a 7-point numeric scale. The measurements were as follows: the reward is (1) psychologically close–psychologically far, (2) great in mind–small in mind, (3) concrete–abstract (4) close to my possessions–far from my possessions.

(2) Information Type

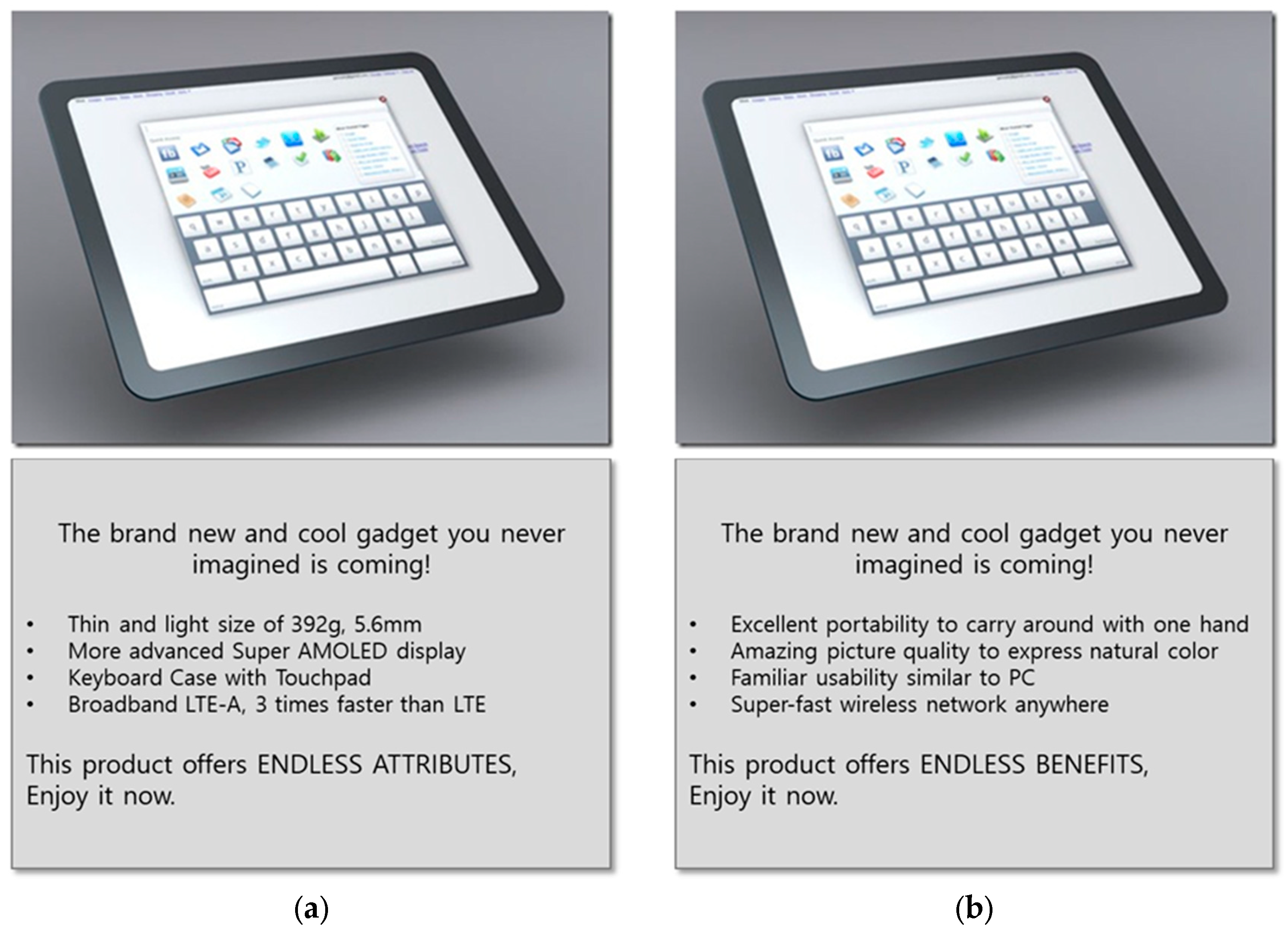

In this experiment, the selected target product was a tablet PC, this was chosen because Tablet PCs have a variety of attributes and benefits information and, relatively speaking, the participants were well-acquainted therewith. For this reason, it has been used as a target product of previous experiments in other studies [45]. In a preliminary survey involving ten college students, several opinions were collected about the attributes and benefits of tablet PCs. Based on these, attribute-oriented and benefit-oriented information were created and used as the stimuli of the main experiment (see Figure 1).

In order to check the manipulation of the product information type, two questions asking what the product advertisement emphasized were provided to the participants. The questions are as follows: “The product information emphasizes benefits (vs. attributes)” and “The information is abstract (vs. concrete).” The participants indicated their perceptions on a 7-point scale.

(3) Product Attitude

The measurements of attitudes toward the product were modified to suit this study, with reference to similar studies [26,39,40,41,42,43,44,46]. For the three commonly-measured questions, ‘good,’, ‘likable,’ and ‘favorable,’ the participants were asked to mark the score that most closely resembled their feelings on the 7-point scale. These values were averaged and used as the final dependent variable.

3.1.3. Experiment Procedure

The participants were first guided by the purpose of the survey and general precautions. Then, a hypothetical scenario for this experiment was introduced. The content of the scenario explained that a new shopping platform would soon begin offering services in Korea and that to attract initial customers, the company was offering a $100 reward to consumers participating in the panel. Depending on the transaction type, half of the participants received $100 in cash for the purpose of traditional transactions, while the other half earned $100 in Digital Pay for the purpose of virtual transactions.

After that, several products were introduced under the name “Editor’s Choice,” referring to products recommended by the shopping platform. Among the products introduced, the fifth was the experiment target product—a $100 mini-tablet. By clicking on the thumbnail image of this product, the product’s description could be seen, where different product introduction pages—depending on the conditions of the information type—could be found. After reading all the information about the product carefully, the participants filled out the questionnaire, answering questions related to product attitude, manipulation check, and general characteristics such as previous shopping experience, gender, and age, and finally ended the experiment with appreciations.

3.2. Research Results

3.2.1. Manipulation Checks

The participants’ four-item responses—designed for a manipulation check of their perception of the level of the virtuality of the transaction type—were averaged (Eigen Value = 3.45, Cronbach’s Alpha = 0.95). An ANOVA analysis indicated the presence of the main effect of virtuality (F (1,198) = 364.71, p < 0.001). The participants that were given virtual money (i.e., Digital Pay) perceived their reward to be more virtual (Mvirtual = 5.81) than the participants that were given real money (i.e., cash) (Mreal = 2.66).

Furthermore, the participants’ four-item responses—designed to place the reward at a psychological distance—were averaged (Eigen Value = 2.83, Cronbach’s Alpha = 0.86). An ANOVA analysis indicated the presence of the main effect of the psychological distance (F (1,198) = 362.95, p < 0.001). The participants that were given virtual money (i.e., Digital Pay) perceived their reward to be more distant (Mvirtual = 5.57) than the participants that were given real money (i.e., cash) (Mreal = 2.90).

A simple regression analysis was performed to verify the relationship between these two variables. The perceived virtuality according to the transaction type was set as an independent variable, and the psychological distance to the reward was set as a dependent variable. As a result, the perceived virtuality accounts for a large part of the psychological distance (r2 = 0.637, F (1,198) = 348.02, p < 0.001) and the standardized regression coefficient was 0.80 (p < 0.001). In other words, the two variables had a positive relationship.

Finally, two items of manipulation check on the type of product information were also identified through a one-way ANOVA analysis. Respondents perceived the content of advertisement differently when they read attribute-based information and benefit-based information, and the difference was significant (Eigen Value = 1.55, Cronbach’s Alpha = 0.70, Mattribute-based = 3.60 vs. Mbenefit-based = 4.17, F (1,198) = 7.88, p < 0.001). In sum, all manipulations were successful.

3.2.2. Hypothesis Testing

I conducted a two-way ANOVA analysis on product attitude in order to test hypotheses 1 & 2. The participants’ product attitude was measured as three items (Eigen Value = 2.75, Cronbach’s Alpha = 0.96), which were then averaged and used for the analysis. Table 1 shows the descriptive statistics of product attitude, and Table 2 shows the results of the ANOVA test.

The results of the ANOVA test showed that the gender and age of the participants had no effect on product attitudes. The two main effects of transaction and information types were not significant. Interestingly, the interaction effects of transaction and information types were significant.

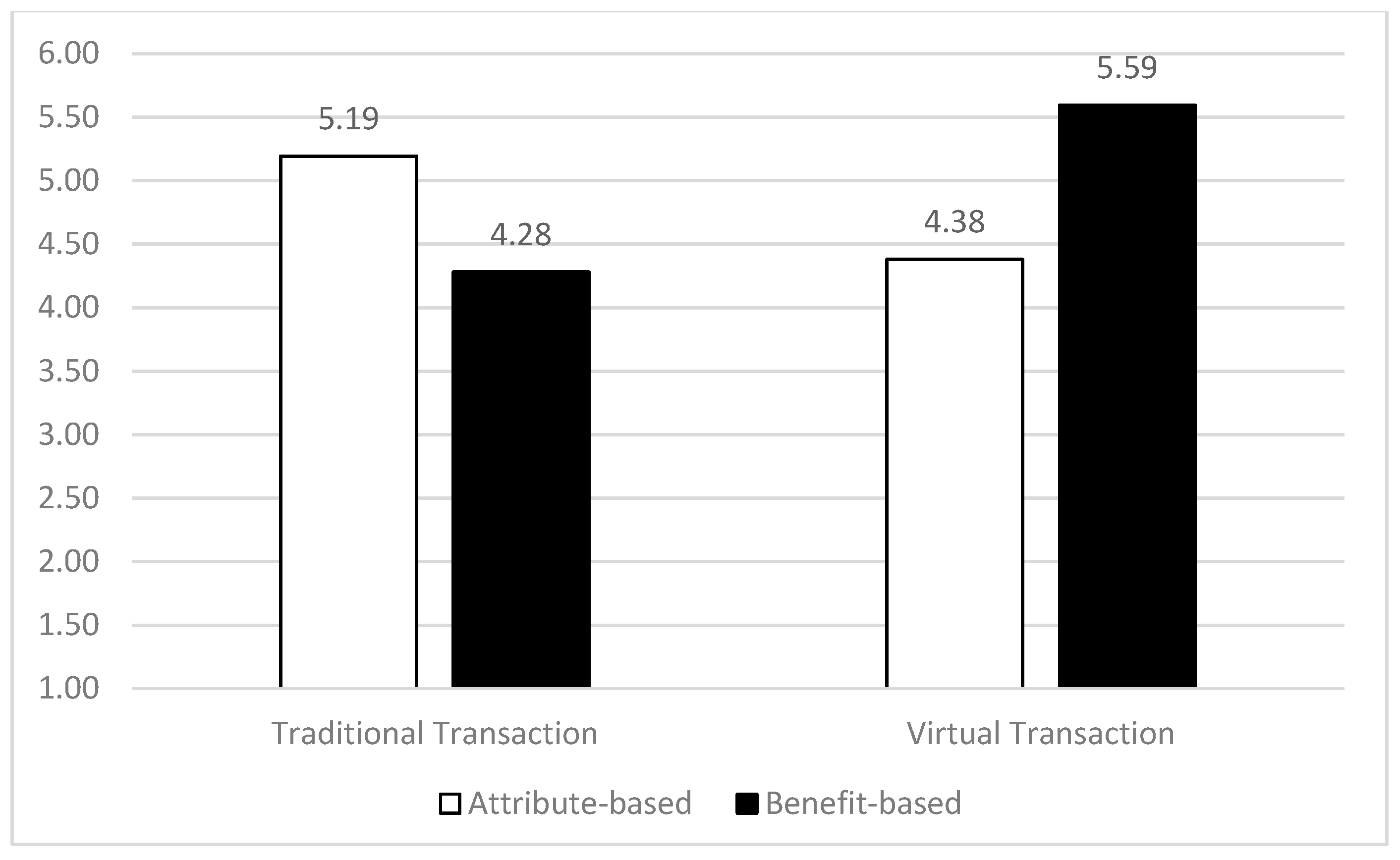

In order to examine the interaction effects of the transaction and information types on product attitude, I analyzed the effect of information type on product attitude according to the transaction type (see Figure 2). As expected, when the transaction type was traditional, the participants had a more favorable product attitude when an attribute-based information was provided than when a benefit-based information was provided (Mattribute-based = 5.19 vs. Mbenefit-based = 4.28, F (1,98) = 13.604, p < 0.001). On the other hand, when the transaction type was virtual, the participants had a more favorable product attitude when the benefit-oriented information was provided than when the attribute-based information was provided (Mattribute-based = 4.38 vs. Mbenefit-based = 5.59, F (1,98) = 22.512, p < 0.001). Therefore, both hypothesis 1 and hypothesis 2 were accepted.

4. Experiment 2: The Effect of Virtuality on Product Attitude Depending on Product Variety

4.1. Research Method

4.1.1. Experiment Design and Participants

The purpose of experiment 2 was to find the effect of virtuality on consumer information processing and the consequent buying behavior depending on product variety. As seen in experiment 1, the virtuality of the transaction type affected the psychological distance to money, which changes consumer purchasing behavior in terms of variety seeking. In order to test the above hypotheses, a 2 × 2 factorial design was conducted for this experiment. The independent variables were: virtuality of transaction type (virtual vs. traditional) and product variety (more variety vs. less variety). Two hundred people participated voluntarily. Their average age was approximately 34.06 years, and 46% were male. Similar to experiment 1, a reward of $5 was given to each of the participants. For this experiment, I reused the virtual shopping platform.

4.1.2. Experiment Variables and Measurements

(1) Virtuality of Payment Method

The virtuality of the transaction type was manipulated in a similar way to the first experiment. Different participants were used and were also given initial membership reward of $20. The rewards were given in cash to one group and Digital Pay to another group, depending on virtuality manipulation conditions. In order to check the difference of individual’s perception of virtuality depending on the transaction type, the four manipulation check items of experiment 1 were slightly modified to fit the experiment. In addition, four measurements of psychological distance from experiment 1 were used together to measure the psychological distance of the reward.

(2) Product Variety

The target product used as an experiment stimulus in this experiment was ice cream with various flavors. Ice cream brands like Baskin Robbins and Coldstone have a variety of flavors. The target product was “8 in 1 Variety Pack,” which offered eight ice cream cups in one set. Depending on the product variety condition, the eight ice cream cups had different ice cream flavors. All eight flavors were different (8 × 1 = 8) in the more variety condition. Participants in the less variety condition were given one set containing two cups of four popular flavors (4 × 2 = 8). The manipulation is equivalent to the total amount of ice cream, where the variety of flavors of ice cream varies depending on the conditions. To ensure that the manipulation was successful in terms of diversity, the following questions were asked: (1) “does the product provide a variety of flavors?”, (2) “does the product meet various needs?”, (3) “does the product seek a new taste?”, and (4) “does the product consist of various attributes?”

(3) Product Attitude

The attitude toward the product actually was the same as in Experiment 1, so it was slightly modified to fit this experiment with reference to the existing research [26,39,40,41,42,43,44,46]. I used the average of three, generally measured items from a seven-point scale—namely ‘good,’ ‘likable,’ and ‘favorable’—as the final dependent variable.

4.1.3. Experiment Procedure

First, the participants were guided about the purpose of the survey and general precautions. Then, a hypothetical scenario was introduced for this experiment. Like in experiment 1, the explained content of the scenario was that a famous global shopping platform would soon begin to offer services in Korea. The participants were told that the company was constructing an initial panel, which they were part of, and that they would receive a $20 reward for their participation. Depending on the condition of the transaction type, they received $20 in cash for the traditional condition and $20 in Digital Pay currency for the virtual condition.

Next, several products were introduced under the name “Editor’s Choice,” which referred to products recommended by the shopping platform. Among the recommended products, the target product of this study—a $20 ice cream set—was listed fifth. The participants clicked on the thumbnail image of the product to view the product’s detail page. This page displayed the different composition of the products depending on the condition of product variety. After carefully reading all of the information about the product, the participants filled out the questionnaire, responding to questions about product attitude, manipulation checks, and general characteristics, and ended the experiment with a thank you.

4.2. Research Results

4.2.1. Manipulation Checks

The participants’ four-item responses—designed for a manipulation check of their perception of the level of the virtuality of the payment method—were averaged (Eigen Value = 3.60, Cronbach’s Alpha = 0.96). An ANOVA analysis indicated the presence of the main effect of virtuality (F (1,198) = 187.56, p < 0.001). The participants that were given virtual money (i.e., Digital Pay) perceived their reward to be more virtual (Mvirtual = 4.75) than participants that were given real money (i.e., cash) (Mtraditional = 3.59).

Furthermore, the participants’ four-item responses—designed to place the reward at a psychological distance—were averaged (Eigen Value = 3.59, Cronbach’s Alpha = 0.96). An ANOVA analysis indicated that the presence of the main effect of psychological distance (F (1,198) = 176.82, p < 0.001). The participants that were given virtual money (i.e., Digital Pay) perceived their reward to be more distant (Mvirtual = 4.70) than participants that were given real money (i.e., cash) (Mtraditional = 3.56).

A simple regression analysis was conducted to verify the relationship between these two variables. The perceived virtuality, depending on the transaction type, was set as an independent variable, and the psychological distance to the reward was set as a dependent variable. The analysis showed that perceived virtuality accounts for much of the psychological distance (r2 = 0.573, F (1,198) = 266.20, p < 0.001), and the standardized regression coefficient was found to have a positive relationship of 0.76 (p < 0.001).

Finally, the manipulation check on the product variety was conducted through the F-test. The participants perceived the product variety differently depending on the level of product variety, and the difference was significant (Eigen Value = 3.54, Cronbach’s Alpha = 0.96, Mmore-variety = 4.79 vs. Mless-variety = 3.65, F (1,198) = 184.39, p < 0.001). In sum, all manipulations were successful.

4.2.2. Hypothesis Testing

I conducted a two-way ANOVA analysis on product attitude in order to test hypotheses 3 & 4. The product attitude was measured as three items (Eigen Value = 2.40, Cronbach’s Alpha = 0.87), which were averaged and used for the analysis. Table 3 shows the descriptive statistics of product attitude, and Table 4 shows the results of the ANOVA test.

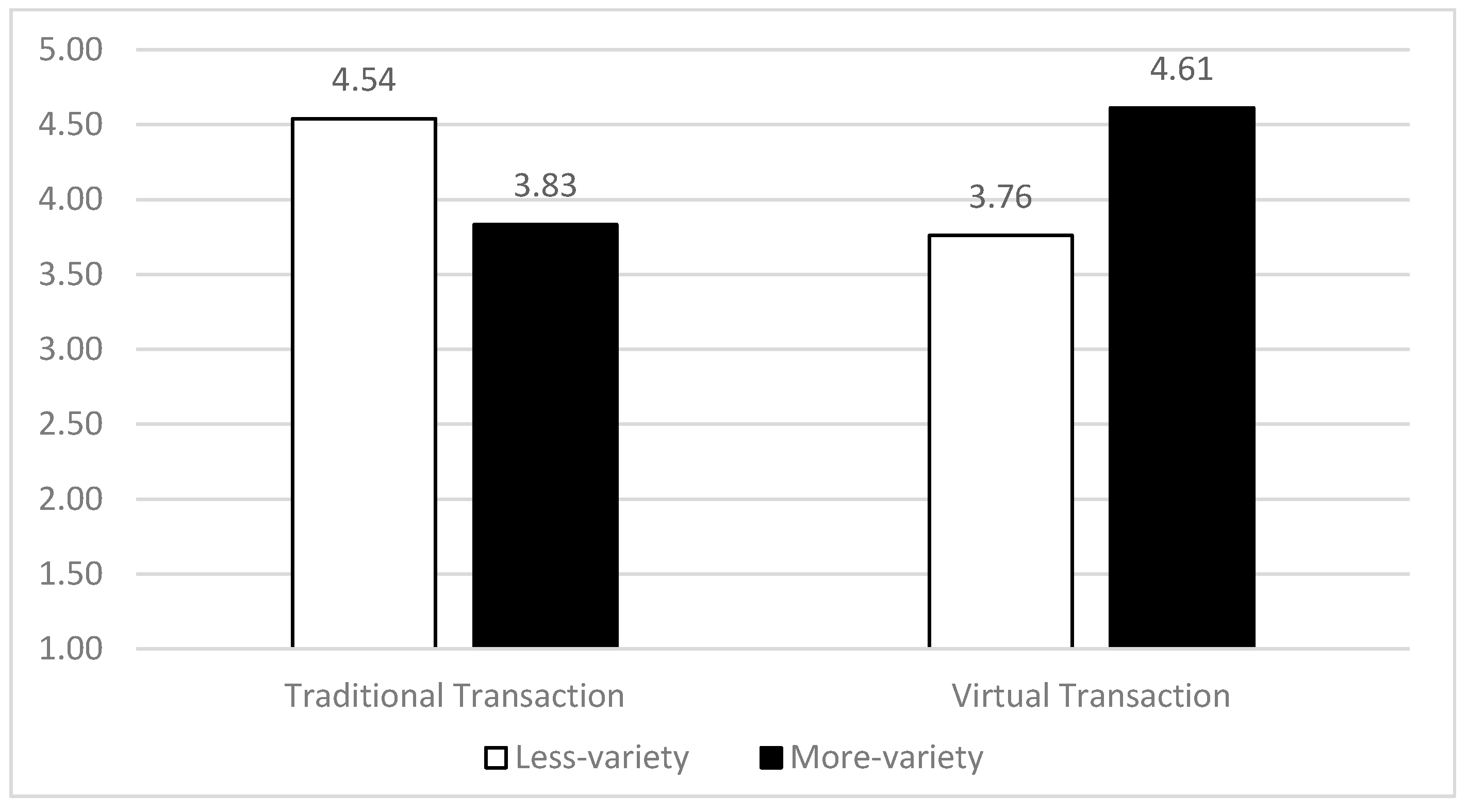

The results of the ANOVA test showed that the gender and age of the participants had no effect on product attitudes. The main effects of transaction type and product variety were not significant. Interestingly, only the interaction effects of transaction type and product variety were significant—a result in need of further analysis. The interaction effect can be seen in the graph below (see Figure 3). As expected, when the payment was made in cash, participants had a more favorable product attitude when the less-variety product was offered than when more-variety product was offered (Mless-variety = 4.54 vs. Mmore-variety = 3.83, F (1,98) = 13.49, p < 0.001). On the other hand, when the payment was made with digital money, the participants had a more favorable product attitude when the more-variety product was provided than when the less-variety product was provided. (Mless-variety = 3.76 vs. Mmore-variety = 4.61, F (1,98) = 18.271, p < 0.001). Therefore, both hypothesis 3 and hypothesis 4 were accepted.

5. Conclusions

In this study, I confirmed that the perceived virtuality of consumers changes the consumer’s consumption behavior. Specifically, this study revealed that consumers’ perceived virtuality differs according to the type of transaction method. Consumers perceived that the money was more virtual when they had digital (virtual) currency for a service than when they had cash. This virtuality of money controls the psychological distance of the consumer’s money, which is closer to cash and further from virtual currency. This difference in psychological distance affects consumers’ information processing, with the result that when psychological distances are far (vs. close), consumers prefer products that are described as abstract (vs. concrete), and a have more favorable attitude toward the more-variety (vs. less-variety) product.

This study has the following theoretical contributions. First, it showed the effect of virtuality as a psychological distance. Existing studies have mainly dealt with time, space, social distance, and probability of occurrence as psychological distance variables [16,17,18]. In addition, this study shows that virtuality can change psychological distance, showing that the construal level theory is extended by presenting virtuality as another psychological distance. The second contribution is that consumers feel different levels of virtuality depending on their transaction method. The existing research on payment methods [2,10,11,12,13,14,15] has been insufficient to suggest the psychological mechanisms of consumers. This study explains how the behavior pattern of consumers changes according to transaction type, based on the theoretical mechanism of construal level theory [16,17,18]. Lastly, this study constitutes a further step in the research field of the information type and product variety by using these as moderating variables for the effect of virtuality on consumer decision-making. There has been extensive research on information types [26,47], yet there no approach has been made from the perspective of individual virtual-feeling. In addition, the literature has not shown that the variety-seeking activity varies according to the construal level [32,35,36], furthermore it does not reveal how the variety-seeking strategy depends on the perceived virtuality. This study emphasizes the important role of virtuality in both information-type research and variety-seeking research.

The practical contributions of this study are identified for each subject. First, this study can guide the strategic directions on how to manage digital money for service providers who operate online shopping platforms. Consumers feel that digital money is psychologically distant from themselves, so they want to spend it on more abstract and desirable products. Therefore, in order to induce the purchase of consumers who are heavily charged with digital money, it is necessary to provide a recommendation list that can stand out in terms of desirability and diversity. On the other hand, consumers who use cash or credit cards to make purchases, rather than digital money, may feel their own means of payment psychologically close to themselves, so it is better to provide more specific and concrete information or recommend a feasible, familiar, and realistic product. Second, from the consumer’s point of view, the consumer should remember that he/she thinks about the same amount of money differently, depending on where it is stored. As the mental accounting theory suggests, consumers store the same money but in different psychological accounts, depending on the type of money. At this time, the more virtual accounts there are, the more likely the behavioral tendency of consumers depends on the psychological distance. Therefore, in order to make an effective purchase, it is necessary to carefully watch the change of one’s own purchase behavior. Finally, this study also gives important implications for central and local governments. Although not discussed in this study, cryptocurrencies like Bitcoin—which has recently emerged as an important issue—is one kind of virtual money for consumers. Unlike traditional stock or bond markets, consumers can have aggressive investment strategies and consumption behaviors that arise from their different ideas about highly virtualized currencies. By understanding the virtuality of currencies, a policy guide on how to manage newly released cryptocurrencies can be established.

Despite the above implications, this study has the following limitations. First, this study did not confirm the bidirectional relationship between virtuality and psychological distance, rather, it confirmed only one direction. In this study, the greater the virtuality an individual perceives, the greater the psychological distance they have in relation to it. However, it was not verified whether the psychological distance affects the level of perceived virtuality. If this is verified, the cyclical relationship between virtuality and psychological distance can be assessed. Second, this study considers only two specific variables and controls many variables. Consumers’ transaction type can affect many other variables besides the virtuality. This study focused only on the virtuality of transaction means, and future studies need to establish a more comprehensive research model in consideration of the convenience and technology of transaction means. Finally, this study deals only with cash and service pay, which is self-defined by the service provider. The expansion of the currency level—such as cryptocurrency, which has been recently growing—and the payment means, such as NFC and QR codes, are necessary for future research. In addition, this study does not consider individual risk-taking tendencies. However, those who are risk-averse inferred are likely to be prevention-focused in general [48,49,50] and feel psychologically close to most of the subjects, so they will have a cash-like outcome pattern when using digital money. Above all limitations can be a direction for future research.

Funding

This work was supported by LG Yonam Foundation (of Korea).

Acknowledgments

Do-Hyung Park thanks Yoonhee Hwang, Chaehee Park, and Chanhee Park for their insightful and helpful comments.

Conflicts of Interest

The author declares no conflicts of interest.

References

- Zhao, Q.; Tsai, P.-H.; Wang, J.-L. Improving financial service innovation strategies for enhancing china’s banking industry competitive advantage during the fintech revolution: A Hybrid MCDM model. Sustainability 2019, 11, 1419. [Google Scholar] [CrossRef]

- Dodgson, M.; Gann, D.; Wladawsky-Berger, I.; Sultan, N.; George, G. Managing digital money. Acad. Manag. J. 2015, 58, 325–333. [Google Scholar] [CrossRef]

- Brynjolfsson, E.; McAfee, A. The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies; WW Norton & Company: New York, NY, USA, 2014. [Google Scholar]

- Chuen, D.L.K. Handbook of Digital Currency: Bitcoin, Innovation, Financial Instruments, and Big Data; Academic Press: Cambridge, MA, USA, 2015. [Google Scholar]

- Kang, N.; Kim, J. An Empirical Analysis of Bitcoin Price Jump Risk. Sustainability 2019, 11, 2012. [Google Scholar] [CrossRef]

- Majumder, A.; Goswami, J.; Ghosh, S.; Shrivastawa, R.; Mohanty, S.P.; Bhattacharyya, B.K. Pay-Cloak: A Biometric Back Cover for Smartphones: Facilitating secure contactless payments and identity virtualization at low cost to end users. IEEE Consum. Electron. Mag. 2017, 6, 78–88. [Google Scholar] [CrossRef]

- Shin, Y.J.; Choi, Y. Feasibility of the Fintech Industry as an Innovation Platform for Sustainable Economic Growth in Korea. Sustainability 2019, 11, 5351. [Google Scholar] [CrossRef]

- Hirschman, E.C. Differences in consumer purchase behavior by credit card payment system. J. Consum. Res. 1979, 6, 58–66. [Google Scholar] [CrossRef]

- Prelec, D.; Loewenstein, G. The red and the black: Mental accounting of savings and debt. Mark. Sci. 1998, 17, 4–28. [Google Scholar] [CrossRef]

- Perry, M.; Ferreira, J. Moneywork: Practices of use and social interaction around digital and analog money. ACM Trans. Comput. Hum. Interact. 2018, 24, 41. [Google Scholar] [CrossRef]

- Sahoo, P.K. Bitcoin as digital money: Its growth and future sustainability. Theor. Appl. Econ. 2017, 24, 53–64. [Google Scholar]

- O’neill, J.; Dhareshwar, A.; Muralidhar, S.H. Working digital money into a cash economy: The collaborative work of loan payment. Comput. Support. Coop. Work 2017, 26, 733–768. [Google Scholar] [CrossRef]

- Rastogi, V.; Kushwaha, P. Success and failure of digital money and virtual money: Case of cryptocurrency-bitcoin. IME J. 2019, 13, 74–81. [Google Scholar]

- Ferreira, J.; Perry, M. From transactions to interactions: Social considerations for digital money. In Disrupting Finance; Springer: Berlin/Heidelberg, Germany, 2019; pp. 121–133. [Google Scholar]

- Biradar, S.L.; Balkrushna, H.R. Digital Money: An Analysis of Users’ Perception. Manag. Account. J. 2019, 54, 81–84. [Google Scholar]

- Liberman, N.; Sagristano, M.D.; Trope, Y. The effect of temporal distance on level of mental construal. J. Exp. Soc. Psychol. 2002, 38, 523–534. [Google Scholar] [CrossRef]

- Trope, Y.; Liberman, N. Temporal construal. Psychol. Rev. 2003, 110, 403. [Google Scholar] [CrossRef] [PubMed]

- Trope, Y.; Liberman, N. Construal-level theory of psychological distance. Psychol. Rev. 2010, 117, 440. [Google Scholar] [CrossRef] [PubMed]

- Dowling, G.R.; Uncles, M. Do customer loyalty programs really work? Sloan Manag. Rev. 1997, 38, 71–82. [Google Scholar]

- Choi, Y.; Sun, L. Reuse intention of third-party online payments: A focus on the sustainable factors of Alipay. Sustainability 2016, 8, 147. [Google Scholar] [CrossRef]

- Poster, M. What’s the Matter with the Internet? University of Minnesota Press: Minneapolis, MN, USA, 2001. [Google Scholar]

- Zhao, M.; Xie, J. Effects of social and temporal distance on consumers‘ responses to peer recommendations. J. Mark. Res. 2011, 48, 486–496. [Google Scholar] [CrossRef]

- White, K.; MacDonnell, R.; Dahl, D.W. It’s the mind-set that matters: The role of construal level and message framing in influencing consumer efficacy and conservation behaviors. J. Mark. Res. 2011, 48, 472–485. [Google Scholar] [CrossRef]

- Van Houwelingen, G.; Van Dijke, M.; De Cremer, D. Fairness enactment as response to higher level unfairness: The roles of self-construal and spatial distance. J. Manag. 2017, 43, 319–347. [Google Scholar] [CrossRef]

- Williams, L.E.; Stein, R.; Galguera, L. The distinct affective consequences of psychological distance and construal level. J. Consum. Res. 2013, 40, 1123–1138. [Google Scholar] [CrossRef]

- Park, D.-H.; Kim, S. The effects of consumer knowledge on message processing of electronic word-of-mouth via online consumer reviews. Electron. Commer. Res. Appl. 2008, 7, 399–410. [Google Scholar] [CrossRef]

- Peter, J.P.; Olson, J.C.; Grunert, K.G. Consumer Behaviour and Marketing Strategy; McGraw-Hill: London, UK, 1999. [Google Scholar]

- Hamilton, R.W.; Thompson, D.V. Is there a substitute for direct experience? Comparing consumers‘ preferences after direct and indirect product experiences. J. Consum. Res. 2007, 34, 546–555. [Google Scholar] [CrossRef]

- Thompson, D.V.; Hamilton, R.W.; Petrova, P.K. When mental simulation hinders behavior: The effects of process-oriented thinking on decision difficulty and performance. J. Consum. Res. 2009, 36, 562–574. [Google Scholar] [CrossRef]

- McAlister, L. A dynamic attribute satiation model of variety-seeking behavior. J. Consum. Res. 1982, 9, 141–150. [Google Scholar] [CrossRef]

- Farquhar, P.H.; Rao, V.R. A balance model for evaluating subsets of multiattributed items. Manag. Sci. 1976, 22, 528–539. [Google Scholar] [CrossRef]

- Simonson, I. The effect of purchase quantity and timing on variety-seeking behavior. J. Mark. Res. 1990, 27, 150–162. [Google Scholar] [CrossRef]

- Givon, M. Variety seeking through brand switching. Mark. Sci. 1984, 3, 1–22. [Google Scholar] [CrossRef]

- Lattin, J.M.; McAlister, L. Using a variety-seeking model to identify substitute and complementary relationships among competing products. J. Mark. Res. 1985, 22, 330–339. [Google Scholar] [CrossRef]

- Kahn, B.E.; Kalwani, M.U.; Morrison, D.G. Measuring variety-seeking and reinforcement behaviors using panel data. J. Mark. Res. 1986, 23, 89–100. [Google Scholar] [CrossRef]

- Ratner, R.K.; Kahn, B.E.; Kahneman, D. Choosing less-preferred experiences for the sake of variety. J. Consum. Res. 1999, 26, 1–15. [Google Scholar] [CrossRef]

- Faison, E.W. The neglected variety drive: A useful concept for consumer behavior. J. Consum. Res. 1977, 4, 172–175. [Google Scholar] [CrossRef]

- Venkatesan, M. Cognitive consistency and novelty seeking. In Consumer Behavior: Theoretical Sources; Prentice-Hall: Englewood Cliffs, NJ, USA, 1973; pp. 355–384. [Google Scholar]

- Park, D.-H. Virtuality as a Psychological Distance: The Strategy for Advertisement Message Appeal Depending on Virtuality. J. Inf. Technol. Appl. Manag. 2017, 24, 39–54. [Google Scholar]

- Park, D.-H. Virtuality as a Psychological Distance and Temporal Distance: Focusing on the Effect of Product Information Type on Product Attitude. Knowl. Manag. Res. 2017, 18, 163–178. [Google Scholar]

- Park, D.-H.; Lee, J.; Han, I. The effect of on-line consumer reviews on consumer purchasing intention: The moderating role of involvement. Int. J. Electron. Commer. 2007, 11, 125–148. [Google Scholar] [CrossRef]

- Park, D.-H.; Lee, J. eWOM overload and its effect on consumer behavioral intention depending on consumer involvement. Electron. Commer. Res. Appl. 2008, 7, 386–398. [Google Scholar] [CrossRef]

- Lee, J.; Park, D.-H.; Han, I. The effect of negative online consumer reviews on product attitude: An information processing view. Electron. Commer. Res. Appl. 2008, 7, 341–352. [Google Scholar] [CrossRef]

- Lee, J.; Park, D.-H.; Han, I. The different effects of online consumer reviews on consumers‘ purchase intentions depending on trust in online shopping malls: An advertising perspective. Internet Res. 2011, 21, 187–206. [Google Scholar] [CrossRef]

- Zhao, M.; Hoeffler, S.; Zauberman, G. Mental simulation and preference consistency over time: The role of process-versus outcome-focused thoughts. J. Mark. Res. 2007, 44, 379–388. [Google Scholar] [CrossRef]

- Park, S.B.; Park, D.H. The effect of low-versus high-variance in product reviews on product evaluation. Psychol. Mark. 2013, 30, 543–554. [Google Scholar] [CrossRef]

- Agrawal, N.; Wan, E.W. Regulating risk or risking regulation? Construal levels and depletion effects in the processing of health messages. J. Consum. Res. 2009, 36, 448–462. [Google Scholar] [CrossRef] [Green Version]

- Kim, K.-W.; Park, D.-H. Individual Thinking Style leads its Emotional Perception: Development of Web-style Design Evaluation Model and Recommendation Algorithm Depending on Consumer Regulatory Focus. J. Intell. Inf. Syst. 2018, 24, 171–196. [Google Scholar]

- Kim, K.-W.; Park, D.-H. Emoticon by Emotions: The Development of an Emoticon Recommendation System Based on Consumer Emotions. J. Intell. Inf. Syst. 2018, 24, 227–252. [Google Scholar]

- Kim, K.-W.; Park, D.-H. Design Evaluation Model Based on Consumer Values: Three-step Approach from Product Attributes, Perceived Attributes, to Consumer Values. J. Intell. Inf. Syst. 2017, 23, 57–76. [Google Scholar]

Figure 1.

Experiment Stimuli. (a) Stimulus for attribute-oriented information. (b) Stimulus for benefit-oriented information

Figure 1.

Experiment Stimuli. (a) Stimulus for attribute-oriented information. (b) Stimulus for benefit-oriented information

Figure 2.

Interaction Effect of Transaction Type × Information Type.

Figure 3.

Interaction Effect of Payment Method × Product Variety.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Descriptive statistics on the product attitude of experiment 1.

| Transaction Type | Information Type | Mean | Std. Deviation | N |

|---|---|---|---|---|

| Traditional | Attribute-based | 5.19 | 1.09 | 50 |

| Benefit-based | 4.28 | 1.37 | 50 | |

| Virtual | Attribute-based | 4.38 | 1.58 | 50 |

| Benefit-based | 5.59 | 0.87 | 50 |

Table 2.

ANOVA test on product attitude of experiment 1.

| Source | F-Value | Significance |

|---|---|---|

| Corrected Model | 8.238 | 0.000 |

| Intercept | 78.215 | 0.000 |

| Age | 1.943 | 0.165 |

| Gender | 0.810 | 0.369 |

| Transaction Type (Traditional vs. Virtual) | 1.839 | 0.177 |

| Information Type (Attribute-based vs. Benefit-based) | 0.697 | 0.405 |

| Transaction Type × Information Type | 35.317 | 0.000 |

Table 3.

Descriptive statistics on product attitude of experiment 2.

| Transaction Type | Product Variety | Mean | Std. Deviation | N |

|---|---|---|---|---|

| Traditional | Less Variety | 4.54 | 0.96 | 50 |

| More Variety | 3.83 | 0.96 | 50 | |

| Virtual | Less Variety | 3.76 | 0.99 | 50 |

| More Variety | 4.61 | 1.01 | 50 |

Table 4.

ANOVA test on product attitude of experiment 2.

| Source | F-Value | Significance |

|---|---|---|

| Corrected Model | 6.742 | 0.000 |

| Intercept | 122.340 | 0.000 |

| Age | 1.575 | 0.211 |

| Gender | 0.191 | 0.663 |

| Transaction Type (Traditional vs. Virtual) | 0.088 | 0.768 |

| Product Variety (Less-variety vs. More-variety) | 0.159 | 0.690 |

| Transaction Type × Product Variety | 32.002 | 0.000 |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Park, D.-H. Virtuality Changes Consumer Preference: The Effect of Transaction Virtuality as Psychological Distance on Consumer Purchase Behavior. Sustainability 2019, 11, 6618. https://0-doi-org.brum.beds.ac.uk/10.3390/su11236618

AMA Style

Park D-H. Virtuality Changes Consumer Preference: The Effect of Transaction Virtuality as Psychological Distance on Consumer Purchase Behavior. Sustainability. 2019; 11(23):6618. https://0-doi-org.brum.beds.ac.uk/10.3390/su11236618

Chicago/Turabian StylePark, Do-Hyung. 2019. "Virtuality Changes Consumer Preference: The Effect of Transaction Virtuality as Psychological Distance on Consumer Purchase Behavior" Sustainability 11, no. 23: 6618. https://0-doi-org.brum.beds.ac.uk/10.3390/su11236618

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.